gold sheets - reutersshare.thomsonreuters.com/loanpricing/gold_sheets_aug_01_2011.pdf · gold...

TRANSCRIPT

Recent trends dominate despite

debt ceiling concerns

364-day

AA 3.5 2.5 5.0 20.3 5,000.0

A 9.83 7.00 12.50 50.50 2,094.00

BBB 21.7 10.0 30.0 166.7 558.3

Multi-year

AA 11.17 6.00 15.00 79.95 750

A+ NA NA NA NA NA

A 10.00 7.00 15.00 70.24 1,337.50

A- 18.33 15.00 25.00 141.67 1,166.67

BBB+ 17.50 15.00 20.00 140.00 1,550.00

BBB 21.25 15.00 30.00 135.63 1,162.50

BBB- 31.25 25.00 35.00 193.75 1,218.75

were light, with many investors looking to

remain invested but careful about picking

their spots. The result was a continued

buyers’ strike, causing the market to leak

slightly lower.

Volumes in the middle market loan space

were somewhat light but the same space

was insulated to a great extent from the

volatility in the broader market.

And the investment grade sector kept right

on ticking as banks continue to market large

bridge facilities at relatively thin spreads.

Leveraged

It was a tale of two markets in the pri-

mary leveraged loan market last week as

investors lapped up strong credits amid a

slowing pipeline.

With the drama unfolding in Washington

on the debt ceiling issue, the loan market

(LOAN MARKET cont’d on p. 2)

Thomson Reuters LPC uses the 3-5 latest transactions in each

ratings category. The credits represent syndications that were not

substantially under- or over-subscribed. Agent and syndications

fees are not included. Leveraged BSL Grid available at www.

loanconnector.com

BSL GRID Avg. Min. Max. Avg. Fully Avg.Applic. Undrawn Undrawn Undrawn Drawn FacRating (LIB spread Size + Ann ($Mils.) + Usage)

Due to the lack of adequate deal fl ow, the multi-year revolver of some rating categories will not be posted until such time when there are suffi cient deals to report.

Despite some growing nerves going

into the end of the week as the impasse

over the debt ceiling continued, the re-

sponse in the loan market was muted.

Throughout the week, the institutional

loan market showed continued strength

as most issuers were able to cut the

spreads on their loans during syndica-

tion. And while accounts were said to

be doing some lightening up throughout

the course of the week, sellside pres-

sure in the secondary market remained

relatively light.

If anything could be said of last week’s

events, it was that the recent trends that

have come to dominate the loan market

recently continued to dominate.

Investors favored better-quality names,

piling into loans with good ratings and

decent coupons while leaving lower-quality

names to go begging. Trading volumes

Copyright notice: Any copying, redistribution (including electronic forwarding) or republication of Thomson Reuters LPC publications, or their content is strictly prohibited. Copyright © 2011

GOLD SHEETS....................................................................Vol XXV, No. 29 A Thomson Reuters LPC Publication August 1, 2011

5 THINGS TO KNOW

• Immucor is preparing to launch a $700M credit

facility Tuesday via JP Morgan and Citigroup

to back its $1.97B buyout by TPG Capital.

• The CLO market has shown a remarkable

comeback in 2011. CLO issuance year to date

is $7.6B, with another $2B in the pipeline.

• Price levels in the syndicated loan market remain

weak as markets grapple with an uncertain

macroeconomic picture. Since April, average

prices for riskier second-lien multi-quoted

credits are down over 2.7 points to the 87

context.

• Non-sponsored middle market issuance topped

$29B in 2Q11 pushing the total for the fi rst half

to $49.5B, not far behind 1H07’s $56B.

WHAT TO WATCH

DDetailed. Accurate. Transparent.

LPC COLLATERALTHE FIRST STEP INCLO ANALYSIS

LPC COLLATERAL provides

a competitive edge to

CLO investors, managers

and traders.

For more information e-mail

[email protected] or visit

www.loanpricing.com

1 Despite the uptick in volatility seen in the

broader markets, the U.S. leveraged loan

market witnessed continued strength in

the form of a handful of downward price

fl exes. p. 17

2Thomson Reuters LPC’s Loan Market

Scoreboard provides a snapshot of key

statistics in the leveraged loan and high

yield bond markets. p. 3

3 U.S. independent power producer

Dynegy Inc, after failing to fi ll the book

on its $1.7B refi nancing deal by the July

22 commitment deadline, last week

raised pricing and revised tranching to

better match investor demand. p. 18

4 Deutsche Bank is in the market with a

$1.88B refi nancing for Silgan Holdings.

The facility comprises an $800M million,

fi ve-year revolver and multi-tranched

TLA. p. 18

5As the August 2 deadline for raising

the U.S. debt ceiling looms, market

participants wonder what the ultimate

impact of a downgrade could have in the

investment grade market. p. 19

GOLD SHEETS –August 1, 2011 2

INSIDE

Copyright notice: Any copying, redistribution

(including electronic forwarding) or republication of

Thomson Reuters LPC publications, or their content is strictly prohibited.

Copyright © 2011

LOAN MARKET SCORECARD ........................................ 3ANALYTIC SNAPSHOT ................................................... 5LCDS, IGR MARKET BASED PRICING ............................7RELATIVE VALUE ANALYSIS .......................................... 8FORWARD CALENDAR .................................................. 9LEAGUE TABLE ..............................................................10DEALS..........................................................................11-16THE WEEK IN NEWS ................................................ 17-24ASIA NEWS ....................................................................20EUROPE NEWS ..............................................................21

LT Sec’ Bond

Borrower Rating Loan LCDS Swap CDS

Aramark Corp B+ 241 274 523 395

Biomet Inc B+ 323 262 563 339

Burlington Coat Factory

Warehouse Corp B- 471 316 778 663

Cablevision Systems Corp BB 177 156 312 332

Hertz Corporation B+ 277 182 495 358

Huntsman International LLC B+ 244 205 395 354

Mediacom LLC BB- 297 427 575 627

Michaels Stores Inc B- 456 289 759 533

SuperValu Inc B+ 154 201 538 668

TRW Automotive Inc BB+ 111 197 257 220

Source: Source: Thomson Reuters Eikon

See www.loanconnector.com. for more names and methodology.

CROSS MARKET COMPS GRID

LOAN MARKET REVIEW

Fig. 1: Downward and upward price fl exes balance out in July

So

urc

e: T

ho

mso

n R

eu

ters

LP

C

H

HH

H

H

H

H

H

H

H

H

H

H

H HHHH

H

H

H

B

BB

B

B

B

B

B

B

B

B

B

B

B

B

B

B

B

B

B

B

Ashl

and

Evan

s An

alyt

ical

Tere

x

Qua

d/G

raph

ics

Acad

emy

Spor

ts

SunC

oke

Auto

parts

Auto

parts

(2n

d lie

n)

US

Secu

rity

Asso

c.

Cap

suge

l

Prim

edia

DEI

Hol

ding

s

SMAR

T M

odul

ar

INC

Res

earc

h

inVe

ntiv

Hea

lth

Cro

wn

Med

ia

Nor

it H

oldi

ngs

SRA

Inte

rnat

iona

l

Cum

ulus

(2nd

lien

)

Nan

a

Dyn

egy

Gas

Co

0%

2%

4%

6%

8%

10%

12%

H Final

B Original

Down UP

Yiel

d (3

−yea

r)

was largely immune to concerns about

sovereign default or a downgrade. Many

loan market investors noted that the

macroeconomic concerns engulfi ng the

U.S. are a much bigger issue for equity

investors than they are for loan or bond

market participants.

“Loan issuers don’t need a signifi cant

growth of GDP. They need an absence of

a recession,” said one investor from a large

buyside shop.

Many loan investors echoed that senti-

ment, noting that new money deals were

seeing signifi cant commitments, while

opportunistic refi nancing or dividend loans

were undergoing price tweaks. Investors

heaped praised on the continued supply

of high quality names such as Capsugel

and Autoparts Holdings.

In a clear sign of bifurcation in the market,

many refi nancing deals struggled to get

done as launched, with the most prominent

tweaks faced by Dynegy. The issuer moved

funds from its GasCo loan to the CoalCo

tranche and bumped up pricing by 125bp

on the GasCo piece.

Meanwhile, even though the number of

issuers undergoing upward and downward

price fl exes was more or less the same

in July, acquisition and LBO deals were

favored for downward price revisions (Fig.

1). Investors remain hungry for new money

deals and have been booking assets such

as Academy Sports’ $840 million covenant-

lite term loan, in spite of the deal being

highly levered. Other issuers that were

able to fl ex down were OM Group and U.S.

Security Associates.

And, despite investors’ “fl ight to quality,”

sponsors and issuers are still confi dent of

an open debt capital market, with recent

announcements for deals such as Kinetic

Concepts’ LBO loan providing comfort that

private equity fi rms are incentivized to put

money to work even amid an uncertain

economic picture.

Middle Market

A pair of buyout loans, a dividend deal

and a refi nancing hit the middle market last

week, and a handful of lenders announced

new hires.

CHI Overheard Doors launched a $203.5

million bank loan backing its sale to Fried-

man, Fleischer & Lowe from JLL Partners.

The deal is led by GE Capital and Wells

Fargo. The $127.5 million, six-year fi rst-lien

term loan is talked at LIB+525 with a 1.5

percent Libor fl oor and a 99 OID. The $51

million, 6.5-year second-lien term loan is

talked at LIB+925 with a 1.5 percent Libor

fl oor and a 98 OID. A $25 million, fi ve-year

revolver fi lls out the credit.

On Wednesday, Credit Suisse launched a

$215 million loan backing New Mountain

Capital’s acquisition of a majority stake in

SNL Financial. The deal includes a $30 mil-

lion revolver and a $175 million covenant-lite

term loan. Price talk on the loan is LIB+600

with a 1.25 percent fl oor and a 99 OID.

The loan also has 101 soft call protection

for one year.

On Thursday, Jefferies launched a $160

million refi nancing loan for Steak ‘N Shake.

The facility includes a $20 million, three-

year revolver and a $140 million, four-year

term loan. Pro forma leverage is being

marketed at 3.2 times. Proceeds from the

new facility will refi nance existing debt

and fund the return of capital to its parent

Biglari Holdings.

And MSC Software Corp set price talk on

its $215 million fi rst-year term loan. The loan

is talked at LIB+500 with a 1.5 percent Libor

fl oor. The OID is to be determined. However,

lenders will enjoy a 101 soft call for one

year. Proceeds from the Bank of America

Merrill Lynch-led loan will fund a dividend

to sponsors Symphony Technology Group

and Elliott Management Corp.

Elsewhere, FirstMerit Bank, Monroe

Capital, NewStar Financial each announced

new hires as they expand their respective

platforms.

Secondary

High beta fl ow names declined toward

the end of last week as the deadline for an

agreement to raise the debt ceiling drew

— cont’d from p. 1

GOLD SHEETS – AUGUST 1, 2011 3

(LOAN MARKET cont’d on page 4)

LOAN MARKET REVIEW

Fig. 2: Average bid in SMi100 declines amid thin volumes

So

urc

e:

LS

TA

/T

ho

mso

n R

eu

ters

LP

C M

TM

Pri

cin

g

6/23/2010 8/27/2010 11/1/2010 1/6/2011 3/14/2011 5/17/2011 7/21/201192

93

94

95

96

97

98

Avg.

bid

(%of

par

)

close and uncertainty began to weigh.

Friday morning, a handful of fl ow names

opened down 25bp to 50bp as the impasse

continued. Meanwhile, new issues contin-

ued to hold up as better credits remained

in favor.

The average bid in the overall market

ended Thursday at 96.21, down from 96.25

the week before, according to LSTA/Thom-

son Reuters LPC MTM Pricing (Fig. 2). The

average bid in the SMi100 (the 100 most

widely held loans) ended Thursday at 96.95,

down from 96.99 the week before.

Chrysler’s TLB was trading 97-97.5 Friday

morning, down from 97.5-98 at the begin-

ning of the week. Harrah’s Entertainment’s

loan was trading 90-90.5 Friday morning,

down 25bp from the day before and a point

on the week.

Meanwhile, newer loans were holding

up better. Ashland’s TLB was ticked down

12.5bp Friday morning to 100.125-100.375

after holding at 100.25 throughout the

week.

OM Group’s new $350 million U.S. TLB

was 99.875-100.125 Friday morning after

breaking in that same context the day

before.

Reynolds Group’s new $2 billion term

loan was off slightly at 99-99.375 Friday

morning after breaking for trading in the

99.25-99.75 range Wednesday.

Academy Sports new $840 million term

loan was down about 50bp from its break

price earlier in the week at 99.5-100 Friday

morning.

Meanwhile, Capsugel’s new loan broke for

trading Wednesday afternoon in the 100.25-

100.75 range. Terex Corp’s new $460 million

term loan was trading 100.25-100.5 after

also breaking for trading Wednesday.

And bids for a $22 million cash loan BWIC

were due Thursday. The portfolio consists

of 21 tranches of mostly off-the run names.

Investment Grade

Despite growing concerns about the U.S.

debt ceiling, the investment grade loan

market continued to see a growing pipeline

for bridge loans backing M&A transactions.

In recent weeks, knowledge of at least four

potential bridge loans backing the acqui-

sitions of Medco Health Solutions, Nalco,

Temple-Inland and Southern Union have

been announced in the U.S. investment

grade loan market. And more are expected

to follow, according to bankers (see pg. X).

Express Scripts is currently in the market

with a $14 billion bridge loan via Credit

Suisse and Citigroup. Joining the bridge is a

$5.5 billion pro rata tranche that is expected

to subsequently become its permanent

fi nancing to back its merger with Medco

Health. The issuer is offering upfront fees

of roughly 40bp on its $14 billion bridge

loan and around 50bp on the $5.5 pro rata

tranches for commitments of $1 billion.

The company is currently in discussion

with the fi rst-tier of banks and is asking

for tickets of $1 billion, with $700 million

LOAN MARKET SCORECARD

For the week endedLEVERAGED PIPELINE ($Bils.) 2011 High 2011 Low 7/14/11 7/21/11 7/28/11

Leveraged pipeline $63.00 $16.00 $42.80 $50.30 $40.46 Instituitonal pipeline $45.00 $8.80 $25.62 $26.55 $18.55 Institutional new deals this week $9.75 $1.49 $1.68 Institutional closed deals this week $4.69 $0.47 $9.49

3Q11 To Date

YIELDS (LEVERAGED) 1Q11 2Q11 7/14/2011 7/21/11 7/28/11

Avg. Spread (bps) 409 436 516 516 509 Avg. Libor fl oor (%) 1.34% 1.33% 1.36% 1.37% 1.36%Avg. OID 99.34 99.13 98.61 98.61 98.63Avg. Yield (3yr term to repay) 5.67% 6.01% 7.04% 7.05% 6.97%

For the quarter ended For the week ended

FUND FLOWS 1Q11 2Q11 7/13/2011 7/20/11 7/27/11

(Lipper FMI)($Mils.) Bank loans +14,655 +9,311 +209 +2.4 +42.9HY bonds +6,398 -4,378 +1,301 +287.3 +303.8

SECONDARY 3/31/2011 6/30/2011 7/14/2011 7/21/11 7/28/11

Average Bid Levels SMi100 97.39 96.91 96.97 96.99 96.95Overall Market 96.42 96.48 96.45 96.25 96.21Euro Lev 40 97.04 96.04 95.55 95.21 94.94Middle Market 94.9 95.63 95.53 95.53 95.50Second Lien 89.09 87.52 87.04 86.89 87.48Covenant Lite 95.61 96.05 96.03 96.08 96.24LBOs 95.64 94.97 94.96 94.50 94.45Ba1/Ba2 98.4 97.93 97.96 97.97 97.96Ba3 98.67 98.5 98.48 98.41 98.38B1 98.65 98.73 98.82 98.86 98.50B2/B3 96.39 95.71 95.46 95.29 95.06 Source: Thomson Reuters LPC, Lipper FMI, LSTA/LPC MTM pricing

GOLD SHEETS –August 1, 2011 4

LOAN MARKET REVIEW

Fig. 3: Final week in July a big one for HY bonds

So

urc

e: T

ho

mso

n R

eu

ters

Wk

1/10

Wk

1/17

Wk

1/24

Wk

1/31

Wk

2/7

Wk

2/14

Wk

2/21

Wk

2/28

Wk

3/7

Wk

3/14

Wk

3/21

Wk

3/28

Wk

4/4

Wk

4/11

Wk

4/18

Wk

4/25

Wk

5/2

Wk

5/9

Wk

5/16

Wk

5/23

Wk

5/30

Wk

6/6

Wk

6/13

Wk

6/20

Wk

6/27

Wk

7/5

Wk

7/11

Wk

7/18

Wk

7/25

$0

$2

$4

$6

$8

$10

$12

$14

$16

Wee

kly

bond

vol

ume

($B

ils.)

allocated to the bridge loan and $300

million for the pro rata tranches. The pro

rata tranches constitute the loan portion of

the permanent fi nancing that, along with

a bond issuance, is expected to replace

the bridge. It includes a $4 billion funded

fi ve-year term loan A and a $1.5 billion fi ve-

year revolving credit. The fi rst-tier banks

are Bank of America Merrill Lynch, Bank of

Tokyo Mitsubishi, Credit Agricole, Deutsche

Bank, Mizuho, Morgan Stanley, Sumitomo

Mitsui, SunTrust, RBS and Wells Fargo,

sources said. Credit Suisse and Citigroup

are leading the fi nancing.

At current ratings of Baa3/BBB+, the

Express Scripts bridge pays LIB+175. Pric-

ing on the term loan A is also expected to

open at LIB+175.

Bankers are also waiting for International

Paper (IP)’s $1 billion 364-day bridge. And

Deutsche Bank is in the market with a $1.88

billion refi nancing for Silgan Holdings. The

facility comprises a $800 million fi ve-year

revolver and multi-tranched term loan A.

Bonds

Although last week began with a small

high yield pipeline, July will not end as the

lowest month of issuance since June 2010.

The week of July 25 will wind up pricing the

largest amount of weekly volume in the U.S.

high yield corporate bond market since May

16 (Fig. 3). In fact, last week’s volume of

$10.51 billion is almost twice as large as all

the other weeks in July combined.

Despite the continued uncertainty sur-

rounding the U.S. debt talks and fear of a

potential downgrade as Republicans and

Democrats refuse to compromise on a

budget plan, issuers are rushing into the

market ahead of the debt deadline. It is

important to note that the better quality,

well liked and well known high yield credits

were driving volume last week.

Double-B rated credits accounted for 60

percent of issuance last week. Tuesday was

by far the biggest volume day of the week

and year at $7.88 billion as a result of the

Reynolds Group and HCA bringing their

large two-part deals to market.

The Reynolds Group was the largest

deal to enter the high yield market since

Arch Coal priced its $2 billion offering in

early June. The deal performed well in the

secondary market, initially climbing over

2 points. Later Tuesday, infl uenced by the

Reynolds Group’s success, HCA pulled the

trigger and priced a quick print, $5 billion

dollar deal that was upsized from an origi-

nally planned $1 billion.

The book for the HCA deal was overheard

at around $10 billion, thus justifying the sub-

stantial upsize. HCA’s deal comes in as the

sixth-largest high yield deal on record and

made up nearly half of last week’s volume.

(Caleb Frazier, Leela Parker, Smita Madhur and Michael Langellotti contributed to this report.)

— cont’d from p. 3

RIGHT NOW THOUSANDSOF SYNDICATED LOANMARKET PROFESSIONALSARE READING THIS ISSUEOF GOLD SHEETS.

IS THERE SOMETHINGYOU’D LIKE TO TELLTHEM?

Now companies like yours can

connect with top-level decision

makers in the syndicated loan

market – by advertising in

Gold Sheets.

The audience you need to reach

reaches for Gold Sheets every

week for unique syndicated

loan market news and

comprehensive analysis. Act

now to get your message in

front of them.

For advertising specifications

and rates please visit

loanpricing.com/advertise.html

or

e-mail [email protected].

GOLD SHEETS – AUGUST 1, 2011 5

ANALYTIC SNAPSHOT

High yield bond volume slows in July

So

urc

e: T

ho

mso

n R

eu

ters

Jan−

10

Feb−

10

Mar

−10

Apr

−10

May

−10

Jun−

10

Jul−

10

Aug

−10

Sep

−10

Oct

−10

Nov

−10

Dec

−10

Jan−

11

Feb−

11

Mar

−11

Apr

−11

May

−11

Jun−

11

Jul−

11

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

VolumePipeline

Mon

thly

bon

d vo

lum

e($

Bils

.)

Middle market non-sponsored

tenors almost back to pre-crisis levels

So

urc

e:

Th

om

son

Re

ute

rs L

PC

2003 2004 2005 2006 2007 2008 2009 1Q10 2Q10 3Q10 4Q10 1Q11 2Q1120

25

30

35

40

45

50

55

60

Large MM

Trad. MM

Teno

r (m

onth

s)

AAA spreads for new issue CLOs

stablilize in 120-130bp area

So

urc

e: T

ho

mso

n R

eu

ters

LP

C

0.0x

3.0x

6.0x

9.0x

12.0x

15.0x

100

110

120

130

140

150

160

170

Fra

ser S

ulliva

n

Are

s M

gm

t

Oak H

ill Ad

v.

KK

R

CS

AM

Bla

ckR

ock

Sym

ph

ony

ING

LC

MA

po

llo

GS

O B

lacksto

ne

Carly

le

Babso

nP

ineB

ridge

Blu

eM

oun

tain

CIF

C D

eerfie

ldIn

vesco

Pru

den

tial

Octa

gon C

redit

Ivy H

ill (MM

)

Levera

ge

AA

A S

pre

ad (

bps)

Debt to Equity AAA spread

Riskier loans show biggest pullback given

macro concerns

So

urc

e:

LS

TA

/T

ho

mso

n R

eu

ters

LP

C M

TM

Pri

cin

g

1/3/2011 2/10/2011 3/22/2011 5/2/2011 6/10/2011 7/21/201182

83

84

85

86

87

88

89

90

2nd

lien

aver

age

bids

(% o

f par

)

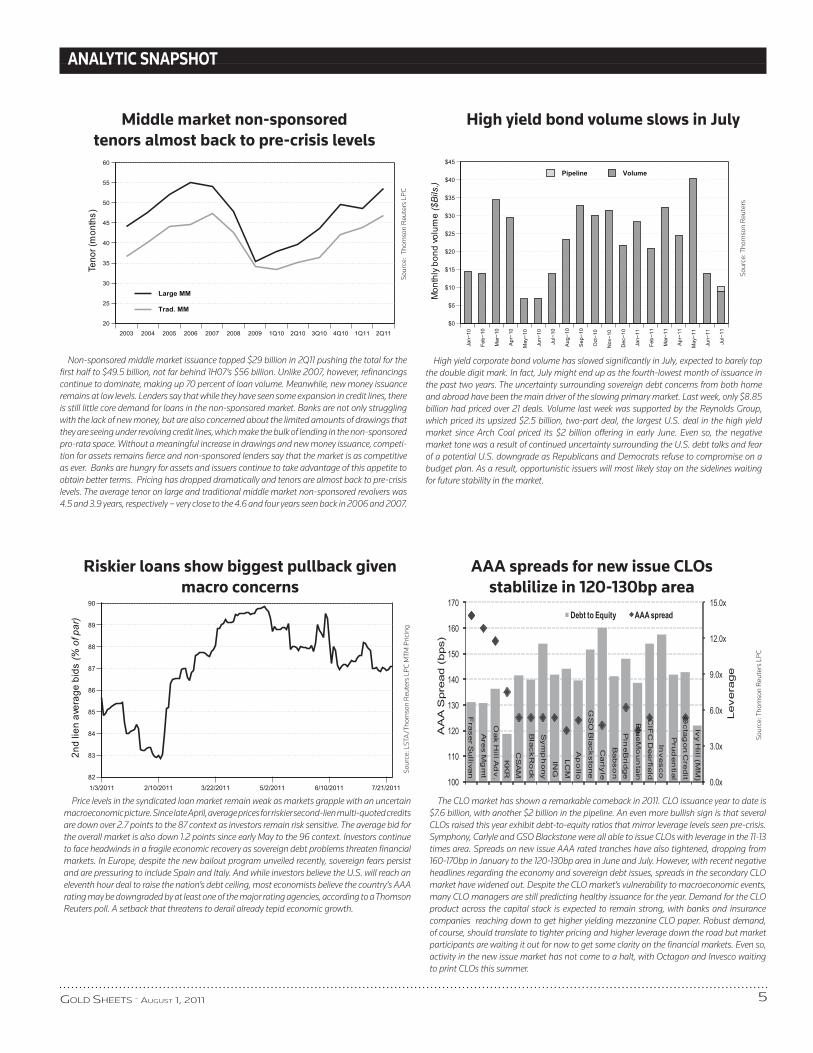

Non-sponsored middle market issuance topped $29 billion in 2Q11 pushing the total for the fi rst half to $49.5 billion, not far behind 1H07’s $56 billion. Unlike 2007, however, refi nancings continue to dominate, making up 70 percent of loan volume. Meanwhile, new money issuance remains at low levels. Lenders say that while they have seen some expansion in credit lines, there is still little core demand for loans in the non-sponsored market. Banks are not only struggling with the lack of new money, but are also concerned about the limited amounts of drawings that they are seeing under revolving credit lines, which make the bulk of lending in the non-sponsored pro-rata space. Without a meaningful increase in drawings and new money issuance, competi-tion for assets remains fi erce and non-sponsored lenders say that the market is as competitive as ever. Banks are hungry for assets and issuers continue to take advantage of this appetite to obtain better terms. Pricing has dropped dramatically and tenors are almost back to pre-crisis levels. The average tenor on large and traditional middle market non-sponsored revolvers was 4.5 and 3.9 years, respectively – very close to the 4.6 and four years seen back in 2006 and 2007.

High yield corporate bond volume has slowed signifi cantly in July, expected to barely top the double digit mark. In fact, July might end up as the fourth-lowest month of issuance in the past two years. The uncertainty surrounding sovereign debt concerns from both home and abroad have been the main driver of the slowing primary market. Last week, only $8.85 billion had priced over 21 deals. Volume last week was supported by the Reynolds Group, which priced its upsized $2.5 billion, two-part deal, the largest U.S. deal in the high yield market since Arch Coal priced its $2 billion offering in early June. Even so, the negative market tone was a result of continued uncertainty surrounding the U.S. debt talks and fear of a potential U.S. downgrade as Republicans and Democrats refuse to compromise on a budget plan. As a result, opportunistic issuers will most likely stay on the sidelines waiting for future stability in the market.

Price levels in the syndicated loan market remain weak as markets grapple with an uncertain macroeconomic picture. Since late April, average prices for riskier second-lien multi-quoted credits are down over 2.7 points to the 87 context as investors remain risk sensitive. The average bid for the overall market is also down 1.2 points since early May to the 96 context. Investors continue to face headwinds in a fragile economic recovery as sovereign debt problems threaten fi nancial markets. In Europe, despite the new bailout program unveiled recently, sovereign fears persist and are pressuring to include Spain and Italy. And while investors believe the U.S. will reach an eleventh hour deal to raise the nation’s debt ceiling, most economists believe the country’s AAA rating may be downgraded by at least one of the major rating agencies, according to a Thomson Reuters poll. A setback that threatens to derail already tepid economic growth.

The CLO market has shown a remarkable comeback in 2011. CLO issuance year to date is $7.6 billion, with another $2 billion in the pipeline. An even more bullish sign is that several CLOs raised this year exhibit debt-to-equity ratios that mirror leverage levels seen pre-crisis. Symphony, Carlyle and GSO Blackstone were all able to issue CLOs with leverage in the 11-13 times area. Spreads on new issue AAA rated tranches have also tightened, dropping from 160-170bp in January to the 120-130bp area in June and July. However, with recent negative headlines regarding the economy and sovereign debt issues, spreads in the secondary CLO market have widened out. Despite the CLO market’s vulnerability to macroeconomic events, many CLO managers are still predicting healthy issuance for the year. Demand for the CLO product across the capital stack is expected to remain strong, with banks and insurance companies reaching down to get higher yielding mezzanine CLO paper. Robust demand, of course, should translate to tighter pricing and higher leverage down the road but market participants are waiting it out for now to get some clarity on the fi nancial markets. Even so, activity in the new issue market has not come to a halt, with Octagon and Invesco waiting to print CLOs this summer.

GOLD SHEETS –August 1, 2011 6

THE WEEK’S BIGGEST WINNERS

Biggest Winners among widely quoted syndicated loans in secondary trading. All loans contain at least three bids.

Source: LSTA/LPC Mark-To-Market Pricing

Note: These are the averages of indicative bid prices provided by bank loan traders and expressed as a percentage of the par, or face, value. Coupon, or interest rate, is in

1/100s of a percentage point over Libor, the benchmark London Interbank Offered Rate. All ratings are for specifi c loans and not for the company itself except as noted

with an (a). These prices do not represent actual trades nor are they offers to trade; rather they are estimated values provided by dealers.

THE WEEK’S BIGGEST LOSERSBiggest Losers among widely quoted syndicated loans in secondary trading. All loans contain at least three bids.

Source: LSTA/LPC Mark-To-Market Pricing

Note: These are the averages of indicative bid prices provided by bank loan traders and expressed as a percentage of the par, or face, value. Coupon, or interest rate, is in

1/100s of a percentage point over Libor, the benchmark London Interbank Offered Rate. All ratings are for specifi c loans and not for the company itself except as noted

with an (a). These prices do not represent actual trades nor are they offers to trade; rather they are estimated values provided by dealers.

Pricing as of Friday, July 29

SECONDARY NEWS

Pricing as of Friday, July 29

Average WeeklyNon Institutional Par Losers Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)CCS Income Trust RC B2/B L+300 11/5/2013 90.75 -0.75Astoria Generating LC WR/NR L+225 2/1/2011 96.25 -0.63Aramark Corp LC Ba3/BB L+325 7/1/2016 99.00 -0.50Las Vegas Sands Delay Draw TL N.R.*/BB L+275 11/23/2016 96.43 -0.45Hub International LTD Delay Draw TL B2/B L+250 6/13/2014 97.25 -0.37

Average WeeklyInstitutional Par Losers Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Astoria Generating 2nd Lien TL N.R.*/CCC- L+375 8/1/2013 92.08 -3.67Telepizza SA TLB N.R.*/N.R.* E+225 12/11/2014 90.25 -2.36PHS Group Plc TLB N.R.*/N.R.* L+250 11/27/2015 91.65 -1.55Flint Group (Aster) TLB N.R.*/N.R.* E+225 12/31/2016 95.60 -0.90Gentiva Health Services Inc TLB Ba2/BB- L+350 8/17/2016 98.38 -0.78

Average WeeklyNon Institutional Distressed Losers Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Coach America Delay Draw TL N.R.*/N.R.* NA NA 79.00 -1.00Clear Channel Communications RC Caa1/CCC+ L+340 7/30/2014 87.56 -0.35ProSiebenSat 1 Media AG RC (EURO) N.R.*/N.R.* E+200 6/28/2015 86.67 -0.33Realogy Corp RC B1/B- L+425 4/10/2016 86.75 -0.25Central Parking Corp LC Ba3/CCC L+250 3/29/2014 85.00 -0.17

Average WeeklyInstitutional Distressed Losers Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Yell Group Plc (TPI) TLA N.R.*/N.R.* L+350 4/1/2014 35.50 -2.38Panrico SA TL (Euro) N.R.*/N.R.* E+453 NA 23.17 -2.08Viridian Group Plc TL N.R.*/N.R.* L+375 4/20/2013 84.17 -1.75Viridian Group Plc TL N.R.*/N.R.* L+375 4/20/2013 84.17 -1.75Yellow Brick Road TL (Euro) N.R.*/N.R.* NA NA 34.00 -1.67TXU Corp TLB B2/CCC L+450 10/10/2017 74.88 -1.67

**Par = Average Bid≥ 90 ***Distressed = Average Bid < 90 *Not rated

Average WeeklyNon Institutional Par Winners Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Realogy Corp Delay Draw TL B1/B- L+225 9/30/2013 94.25 +1.46Las Vegas Sands RC WR/BB L+150 5/1/2012 96.58 +0.58Travelport Inc Delay Draw TL Ba3/B L+225 5/23/2014 96.07 +0.45Flextronics International Ltd Delay Draw TL N.R.*/N.R.* L+225 10/1/2014 98.83 +0.38Flextronics International Ltd Delay Draw TL N.R.*/N.R.* L+225 10/1/2014 98.83 +0.38

Average WeeklyInstitutional Par Winners Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Wind Telecomunicazione Spa TLA2 N.R.*/N.R.* E+400 11/2/2016 94.42 +1.54Wind Telecomunicazione Spa TLA2 N.R.*/N.R.* E+400 11/2/2016 94.42 +1.54Realogy Corp TLB B1/B- L+300 9/30/2013 94.25 +1.46Lender Processing Services Inc TLB Baa3/BBB L+250 6/16/2014 99.00 +1.33Abbot Group TLB N.R.*/CCC L+350 4/27/2016 91.17 +1.04

Average WeeklyNon Institutional Distressed Winners Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Tribune Co Incremental TL WR/NR L+250 4/19/2014 66.96 +0.92Lee Enterprises RC N.R.*/N.R.* L+150 1/31/2012 82.88 +0.88Capmark Financial Group Inc RC N.R.*/N.R.* L+67.5 3/23/2011 59.50 +0.80TXU Corp RC N.R.*/N.R.* L+350 10/10/2013 89.00 +0.67Capmark Financial Group Inc RC N.R.*/N.R.* L+67.5 3/23/2011 58.15 +0.56

Average WeeklyInstitutional Distressed Winners Loan rating bid changeName Tranche Moody’s/S&P Coupon Maturity (pct. pts.) (pct. pts.)Tribune Co TLB WR/NR L+300 5/17/2014 69.02 +1.11Culligan International TLB Caa2/CCC+ L+225 10/16/2012 75.75 +0.63Capmark Financial Group Inc TL N.R.*/N.R.* L+67.5 3/23/2011 58.32 +0.54American Gaming Systems TLB Caa2/B- L+300 5/1/2013 82.67 +0.50Capmark Financial Group Inc TL N.R.*/N.R.* L+67.5 3/23/2011 57.61 +0.46

**Par = Average Bid ≥ 90 ***Distressed = Average Bid < 90 *Not rated

GOLD SHEETS – AUGUST 1, 2011 7

BIGGEST WEEKLY LCDS MOVERS: LCDX16 NAMES As of Thursday, July 28

5 yr LCDS change Loan Spread* Loan Spread Basis

Name LCDS (LIB+) Change Basis Change

Reynolds Group Holdings Ltd 474 82 340 -1 134 82

Sabre Holdings Corporation 298 68 495 5 -196 63

Las Vegas Sands LLC 283 -61 259 4 23 -65

Toys ‘R’ Us Inc 308 54 448 2 -141 52

Dex Media West LLC 1,443 45 988 34 455 11

Univar Inc. 358 33 351 3 8 30

J. Crew Group, Inc. 465 25 452 6 14 19

Travelport LLC 330 23 346 -8 -16 32

Berry Plastics Corporation 292 19 348 1 -55 19

United AirLines Inc 465 18 315 -4 150 21

Avaya Inc. 624 17 368 5 256 11

Carestream Health, Inc. 499 17 529 11 -30 5

Laureate Education, Inc. 608 15 420 10 188 5

Wynn Las Vegas LLC 411 15 305 1 106 14

Allison Transmission 504 15 325 6 179 9

WEEKLY LCDS INDUSTRY SNAPSHOT: LCDX16 NAMES Avg. 5 yr LCDS Avg. Loan* Loan Spread Avg. Basis Industry LCDS Change Spread (LIB+) Change Basis Change Count

Automobiles & Components 213 2 244 2 -31 1 4

Capital Goods 548 5 554 3 -6 2 3

Commercial Services & Supplies 585 11 474 7 110 4 7

Consumer Services 333 -5 338 2 -5 -7 7

Food & Staples Retailing 275 4 246 2 29 2 3

Food, Beverage & Tobacco 299 -1 242 1 57 -2 4

Health Care Equipment & Services 261 3 327 3 -66 0 8

Materials 249 12 247 1 2 12 11

Media 501 2 556 5 -56 -3 10

Pharmaceuticals, Biotechnology & Life Sciences 248 -3 306 1 -58 -4 1

Real Estate 516 5 324 -3 192 8 3

Retailing 374 16 466 3 -92 13 5

Semiconductors & Semiconductor Equipment 427 0 175 0 252 0 1

Software & Services 335 8 389 0 -54 8 3

Technology Hardware & Equipment 434 8 285 3 149 4 3

Transportation 404 16 386 2 18 14 6

Utilities 417 2 231 1 186 1 3

*Assuming a rolling four-year term to maturity.For more information, write to [email protected] or contact your Reuters representative.

MARKET BASED PRICING SNAPSHOT

(Investment grade revolvers where drawn spread is tied to CDS/CDX)

CDS MARKET

Source: Thomson Reuters Eikon

Prior Prior

CDS/CDX CDS/CDX Deal Deal

Borrower name S&P Moody’s Drawn spread is tied to: Floor Cap (7/29/11) (near close) Deal Close Undrawn (Undrawn) (Drawn)

HJ Heinz Co BBB Baa2 One year CDS NA NA 19.91 14.2 6/30/2011 50 37.5 MBP

Air Products & Chemicals Inc A A2 Four year CDS 35 100 49.81 47.3 6/30/2011 NA 37.5 225

Altria Group Inc BBB Baa1 Details undisclosed NA NA NA NA 6/30/2011 37.5 15 MBP

Altria Group Inc BBB Baa1 Details undisclosed NA NA NA NA 6/30/2011 50 15 MBP

Paccar Inc A+ A1 50% of CDX 65 No cap 95.84 98.5 6/23/2011 4 NA MBP

Paccar Inc A+ A1 50% of CDX 65 No cap 95.84 98.5 6/23/2011 10 NA MBP

Baxter International Inc A+ A3 Co’s CDS (details undisclosed) 25 100 NA NA 6/17/2011 8 10 45

PepsiCo Inc A- A1 Details undisclosed NA NA NA NA 6/14/2011 2.5 4 MBP

PepsiCo Inc A- A1 Details undisclosed NA NA NA NA 6/14/2011 5 4 MBP

Illinois Tool Works Inc A+ A1 Details undisclosed NA NA NA NA 6/10/2011 10 10 MBP

Illinois Tool Works Inc A+ A1 Details undisclosed NA NA NA NA 6/10/2011 12.5 12.5 MBP

Novartis AG AA- Aa2 One year CDS 10 75 10.22 9.2 6/10/2011 5 5 MBP

Wal-Mart Stores Inc AA Aa2 One year CDS 10 75 13.86 13.9 6/9/2011 1.5 2.5 MBP

Wal-Mart Stores Inc AA Aa2 One year CDS 10 75 13.86 13.9 6/9/2011 NA 10 MBP

Wal-Mart Stores Inc AA Aa2 One year CDS 10 75 13.86 13.9 6/9/2011 4 10 MBP

Charles Schwab Corp A A2 Details undisclosed NA NA NA NA 6/8/2011 15 15 MBP

Automatic Data Processing NR NR Details undisclosed NA NA NA NA 6/7/2011 1.75 5 MBP

Automatic Data Processing NR NR Details undisclosed NA NA NA NA 6/7/2011 4 8 MBP

* Note: data shown in basis points

Source: Thomson Reuters LPC, Markit on Source: Thomson Reuters Eikon

GOLD SHEETS –August 1, 2011 8

Disc./L

IB−eq

uiv. s

pread

(bps)

0

200

400

600

800

1,000Loans Bonds

RELATIVE VALUE OF LEVERAGED LOANS VS. HIGH YIELD BONDS

Spread/ Discounted

Bank loan rating/ Coupon LIB-equiv.

Borrower Bond rating Tranche Maturity (bps/%) Spread (bps)

Avaya Inc B+ TLb Oct-14 275 382 CCC+/Caa2 Sr. Unsec. Nov-15 9.75% 767BE Aerospace Inc BBB-/Ba1 TLb Jul-14 275 262 BB+/Ba3 Sr. Unsec. Jul-18 8.5% 417Casella Waste Systems Inc BB/Ba2 TLb Apr-14 500 500 B-/Caa1 Sr. Sub. Feb-19 9.75% 714Cenveo Inc BB/Ba2 TLb Dec-16 475.0 463 B-/Caa1 Sr. Notes Aug-16 10.5% 881Charter Communications BB+/ Ba2 TLb Mar-14 225 230 /B1 Sr. Unsec. Sep-14 10.875% 619Compucom Systems Inc BB/Ba2 TLb Jul-14 300 425 B/B3 Sr. Sub. Oct-15 12.5% 936Constellation Brands BB/Ba3 TLb Jun-15 275 269 B+/B2 Sr. Sub. May-17 7.25% 319DineEquity Inc CCC+/B2 TLb Sep-17 450 450 CCC+/B3 Sr. Notes Oct-18 9.5% 528Emergency Medical Services B+/B1 TLB May-18 375 384 Caa1 Sr. Notes Jun-19 8.13% 539First Data Corp B+/B1 TLb Sep-14 275 504 CCC+/Caa2 Sr. Unsec. Sep-15 9.875% 798Graham Packaging B+ / B1 TLc Apr-14 425 421 CCC+/Caa1 Sr. Sub. Oct-14 9.875% 799Huntsman International LLC B+/Ba2 TLb Mar-17 250 308 B-/B3 Sr. Sub. Mar-20 8.625 391Isle of Capri Casinos BB-/Ba3 TLb Mar-16 350 339 B-/B3 Sr. Notes Mar-19 7.75% 468Laureate Education B/B1 TLb Aug-14 325 455 CCC+/Caa1 Sr. Sub. Aug-17 11.75% 773Lender Processing Services BBB/Baa3 TLb Jul-14 250 340 BB+/Ba2 Sr. Unsec. Jul-16 8.125% 610 Average of term loans 334 383Average of high yield bonds 9% 649

So

urc

e:

LS

TA

/LP

C M

ark

-to

-Ma

rke

t P

rici

ng

,Th

om

son

Re

ute

rs L

PC

The yield differential between loans and bonds for the 30 liquid names included in the LPC Relative Value composite tightened by 24bp last week. The average loan

yield increased to LIB+383 while the average bond swap spread decreased to LIB+649, creating a differential of 265bp. In contrast, the LTM bond-loan differential

averaged 259bp.

The chart compares institutional term loans with high yield bonds of several issuers on a Libor-equivalent basis. Loan spreads are determined by their coupon

and secondary market price, and are calculated through a discounted cash fl ow model. Bond Libor-equivalent spreads are determined by taking the yield to worst,

subtracting a comparable Treasury yield and swapping the result to a fl oating-rate equivalent.

The borrowers used in this analysis have loans that are widely held in institutional portfolios. In addition, the sample is weighted to refl ect the overall market share

of each industry. Fifteen of the borrowers are shown below. Averages apply to all 30 issuers that make up the LPC Relative Value composite. See LoanConnector

Relative Value page for a list of all 30 issuers.

So

urc

e: T

ho

mso

n R

eu

ters

LP

C

High yield spreads: loans vs. bonds(Disc. LIB-equivalent spread)

Em

erg

en

cy

Me

dic

al

Gra

ha

m P

ac

ka

gin

g

Isle

of

Ca

pri

Ca

sin

os

Hu

nts

ma

n I

nte

rna

tio

na

l L

LC

Ch

art

er

Co

mm

un

ica

tio

ns

Av

ay

a I

nc

Fir

st D

ata

Co

rp

BE

Ae

rosp

ac

e I

nc

Co

mp

uc

om

Sy

ste

ms

Inc

Ce

nv

eo

In

c

Co

nst

ell

ati

on

Bra

nd

s

La

ure

ate

Ed

uc

ati

on

Din

eE

qu

ity

In

c

Le

nd

er

Pro

ce

ssin

g S

erv

ice

s

Ca

sell

a W

ast

e S

yst

em

s In

c

RELATIVE VALUE MARKET

GOLD SHEETS – AUGUST 1, 2011 9

Amneal Pharmaceuticals Healthcare GE Capital/RBS Citizens 7/20 RFI 250 NA 5 325 NA

ArchBrook Laguna Holdings LLC Retail GE NA DIP 50 NA NA 375 NA

Ardent Health Services Healthcare BAML 7/14 ACQ 200 NA NA 500 NA

Aventine Renewable Energy Utilities Wells Fargo 7/21 GCP 50 NA 4 300-350 NA

BJ’s Wholesale Club Inc Retail DB/Citi/Barclays/Jefferies/GE/WF NA LBO 2575 NA NA NA NA

Blackboard Inc Technology BAML/DB/MS NA LBO 1150 NA NA NA NA

Bojangles Restaurants Eats Jefferies 7/26 LBO 215 NA 5 NA NA

California Pizza Kitchen Inc Eats Jefferies/GE Capital NA LBO 365 NA NA NA NA

Carrols LLC Eats NA NA GCP 85 NA NA NA NA

Chefs’ Warehouse Restaurants JPM/GE Capital NA RFI 80 NA NA 250 NA

CHI Overhead Doors GenManuf GE Capital/Wells Fargo 7/27 LBO 204 NA 5 NA NA

CKX Media NA NA LBO 595 NA NA NA

Clement Pappas FoodBeverage Jefferies/BMO 7/20 ACQ 280 NA NA NA NA

Diamond Foods Inc FoodBeverage BAML June ACQ 1000 NA 5 250 NA

Duckwall-ALCO Stores Retail Wells Fargo Capital Finance 7/21 RFI 120 NA 5 200 NA

Dynamics Research Corp Technology BAML/SunTrust Bank/PNC Bank NA ACQ 130 NA 5 400 50

Dynegy Inc Utilities Credit Suisse/Goldman Sachs/Barclays 7/11 ACQ 1700 NA 5 775 NA

EchoStar Corp Technology Deutsche Bank NA ACQ NA NA NA NA NA

Energy Transfer Equity LP OilGas Credit Suisse NA ACQ 3700 NA 364 NA NA

Fogo De Chao Eats JPM 7/26 GCP 205 NA 5 NA NA

General Cable Corp Cable JPM NA RFI 400 NA 5 150-200 NA

Go Daddy Technology BC/DB/RBC/KKR NA LBO NA NA NA NA NA

Henniges Automotive Automotive Credit Suisse/Macquarie/PNC 7/14 ACQ 155 NA 5 600 NA

Hertz Global Holdings Inc Automotive NA NA ACQ 650 NA NA NA NA

Immucor Inc Healthcare Citi/JPM NA LBO 1100 NA 5 NA NA

Insight Global Inc BusServices BNP Paribas 7/18 RFI 157 157 NA 500 NA

Insight Pharmaceuticals Healthcare GE Capital/RBC/SunTrust 7/21 ACQ 420 NA NA 500 NA

Ipreo Holdings BusServices RBC 7/7 LBO 170 115 NA NA NA

Kinetic Concepts Inc Healthcare BAML/CS/MS NA LBO 4950 NA NA NA NA

La Paloma Generating Utilities BAML 7/21 RFI 424 NA 5 NA NA

Lender Processing Services Technology JPM 7/28 RFI 1300 550 5 NA NA

Level 3 Communications Media BAML/Citi NA ACQ 1750 NA 7 425 NA

Lion Copolymer GenManuf HSBC/Wells Fargo 7/14 DivRecap 400 350 5 500 NA

Los Angeles Dodgers Holding Co Leisure JPM NA DIP 150 NA 1 700 NA

Masergy Communications Inc Telecom GE Capital 6/29 LBO 110 NA NA 450 NA

MCCI Medical Group Healthcare GE Capital/SunTrust 7/7 DivRecap 155 NA 5 500 NA

Meritas LLC BusServices Credit Suisse 7/6 RFI 200 NA NA 600 NA

Metropolitan Health Healthcare GE Capital 8/3 ACQ 355 NA 5 NA NA

Microsemi Corp Technology Morgan Stanley NA ACQ 425 NA NA NA NA

Nana Development Corp BusServices GoldmanSachs 6/7 RFI 435 NA 5 NA NA

Ocwen Financial Financials Barclays 7/19 ACQ 575 575 NA 575 NA

OM Group BusServices BAML/PNC/BNP 7/7 ACQ 900 600 NA 375 NA

OpenText Corp Technology Ba2/BB+ Barclays/RBC NA RFI 600 NA NA NA NA

Phillips Plastics Corp GenManuf GE Capital/BNP Paribas 7/20 ACQ 245 NA NA 500 NA

Pike Electric Corp Utilities Regions Bank 7/13 RFI 200 NA NA 250 NA

Pringles ConsProducts BAML NA RFI 1050 675 5 NA NA

Rock Ohio Caesars Gaming Credit Suisse/Deutsche Bank/Citadel 7/27 GCP 275 NA 5 NA NA

Royalty Pharma Healthcare BAML/GS/Citi 7/14 DivRecap 3600 NA 5.25 275 NA

Sealed Air Corp ConsProducts Citi 7/25 ACQ 4420 1300 5 250 NA

Smart Modular Technologies Technology B+/B2 JPM/UBS 6/23 LBO 350 NA 5 NA NA

SNL Financial Financials Credit Suisse 7/27 LBO 205 NA NA NA NA

Solera Holdings BusServices Goldman/BAML NA ACQ 350 NA NA NA NA

Stackpole International Automotive B2/B+ RBC 7/12 LBO 165 NA 5 475-500 NA

Steak ‘N Shake Restaurants Jefferies 7/28 RFI 160 NA 3 NA NA

U.S. Coal Corporation Mining Credit Suisse 7/18 NA 105 NA 6 600 NA

Water Pik Inc ConsProducts GE Capital 7/19 DivRecap 197 NA NA 500-525 NA

YRC Worldwide Shipping JPM NA RFI 400 NA NA 700 NA

Total TLs

TOTAL LEVERAGED $40,457,000,000 $4,322

NON-LEVERAGED

3M Co ConsProducts AA- JPM June RFI 1500 NA 5 NA NA

Airgas Inc OilGas BAML/Wells Fargo 6/23 RFI 750 NA 5 125 20

Banco Itau Financials BNP/HSBC/Mizuho 6/30 RFI 500 NA 3 120 NA

Bank of America Leasing Financials BAML March NA 90 NA 8 250 NA

BP Wind Energy Utilities A2/A NA July GCP 385 NA NA NA NA

Dentsply International Healthcare Morgan Stanley June ACQ 1750 NA 5 NA NA

Express Scripts Healthcare Baa3/BBB+ Credit Suisse/Citi July ACQ 14000 NA NA 175 NA

Georgia-Pacifi c LLC Paper NA 7/27 RFI 3000 NA NA NA NA

International Paper Paper UBS July ACQ 2200 NA NA NA NA

Jefferies Group Inc Financials BBB JPM/Natixis 5/26 ACQ 1000 NA 3 175 NA

Joy Global Inc Mining JPM/GS/BAML July ACQ 1500 NA 1 NA NA

Lonza Group Healthcare JPM 7/21 ACQ 2250 600 5 NA NA

NCR Corp BusServices JPM/RBC/BAML/MS July ACQ 1400 700 NA 125-150 NA

Praxair Inc OilGas BAML/Citi/HSBC July RFI 1750 NA 5 NA NA

Trafi gura AG OilGas BNP Paribas 6/24 GCP 1100 NA 1 115 35

Walgreens Co Retail BAML/Wells Fargo 6/23 RFI 500 NA 4 NA NA

TOTAL NON-LEVERAGED $33,675,000,000

TOTAL IN PIPELINE $74,132,000,000

Pro

Ann./ Forma

Lead Launch Resp. Deal TLs Tenor LIBOR Com. Tot./

Borrower Industry Rating Banks Date Date Purp. Amt. (B, C, D) in Yrs. Spread Fee Sr. Lev.

($Mils.) ($Mils.) (bps) (bps)

Deals in market as of July 28, 2011Added last week: $21.22 billion Bold = New from July 21

— compiled by Jon Methven

Tenor and pricing for pro rata tranches only. See LoanConnector for further deal information and additional forward calendars,

SYNDICATED LOAN FORWARD CALENDAR

GOLD SHEETS –August 1, 2011 10

Thomson Reuters LPC compiles league tables in four ways to catalogue different aspects of syndications volume:

Full-Credit

Full-credit leagues award full credit of a transaction to each agent/co-agent in the lending group.

Number of Deals

Number of deals leagues rank bank holding companies by the number of transactions led or co-led.

Agent-Only

Agent-only leagues award full credit to each lender with an admin., syn. or doc. agent title, up to fi ve banks. For deals $10 billion or more,

full credit awarded to up to fi ve lenders, provided they meet certain criteria.

Bookrunner

This table awards credit to bank(s) with a Bookrunner or Lead Arranger title on the loan documentation.

U.S. League Table Parameters

• Loans must be to U.S. borrowers (Thomson Reuters LPC’s Global League Tables rank worldwide lending).

• Commercial & industrial loans only (real estate and private placements are excluded).

• Loans greater than $10 billion and with more than fi ve agents receive weighted pro rata credit for Agent-only league tables.

For more information concerning league tables contact at (646) 223-6890.

THOMSON REUTERS LPC’S LEAGUE TABLES

Thomson Reuters LPC

GOLD SHEETS

Loans Editor

Tessa Walsh

Managing Editor

Jon Methven

Directors of Analytics

Ioana Barza

Maria C. Dikeos

Colm Doherty

New York Bureau Chief

Caleb Frazier

London Bureau Chief

Christopher Mangham

Hong Kong Bureau Chief

Jacqueline Poh

Australia Editor

Sharon Klyne

Senior Correspondents

Smita Madhur (New York)

Michelle Sierra (New York)

Foster Wong (Hong Kong)

Correspondents

Maggie Chen (Hong Kong)

Leela Parker (New York)

Alasdair Reilly (London)

Wakako Sato (Tokyo)

Clinton Townsend (New York)

Sandra Tsui (Hong Kong)

Production Manager

Michael Green

For subscription information call:Direct Marketing

(646) 223-6890

Gold Sheets is published 50 times a year by Thomson Reuters LPC,

3 Times Square, New York, NY 10036. If you notice incompleteness

or inaccuracies in Gold Sheets please contact Jon Methven at (646)

223-6840 or [email protected]. Gold Sheets is

available real-time via the world wide web on LoanConnector.

The content in this publication, including news, quotes, data and other

information, is provided by Reuters LPC and its third party content

providers for your personal information only, and is not intended for

trading purposes. Content in this publication is not appropriate for the

purposes of making a decision to carry out a transaction or trade. Nor

does it provide any form of advice (investment, tax, legal) amounting to

investment advice, or make any recommendations regarding particular

fi nancial instruments, investments or products.

Neither Thomson Reuters LPC nor its third party content providers

shall be liable for any errors, inaccuracies or delays in content, or for

any actions taken in reliance thereon. Thomson Reuters LPC expressly

disclaims all warranties, expressed or implied, as to the accuracy of

any of the content provided, or as to the fi tness of the information

for any purpose.

Ann = Annual

AIS* = All-in Spread (Drawn/Undrawn)

Cancel = Cancellation

CAN$ = Canadian Dollars

CBO = Competitive Bid Option

COF = Cost of Funds

Commit. = Commitment

CP = Commercial Paper

DIP = Debtor-in-Possession

DM = Deutschemarks

FF = Federal Funds

Ffr = French Francs

FQ = Fiscal Quarter

FY = Fiscal Year

GBR = Gold Base Rate

Guid.= Guidance Line (Uncommitted)

HK$ = Hong Kong Dollars

HLT = Highly Leveraged Transaction

is = Implied Senior

LIB = LIBOR (London

Interbank Offered Rate)

Lt = Lire

MMR = Money Market Rate

NA = Not Available/Not Applicable

P = Prime

PIK = Pay in Kind

SBLC = Standby Letter of Credit

Sfr= Swiss Francs

si = Senior Implied

TreasSpr = Treasury

TrLC = Trade Letter of Credit

Upfr. = Upfront

Util. Fee = Utilization Fee

Types of Loans

BL = Bridge Loan

LC = Letter of Credit

RC = Revolving Credit

TL = Term Loan

PARTIAL = No Pricing Info

Abbreviations

LEAGUE TABLE

2011 YTD U.S. New Money Bookrunner Volume

Bookrunner # of Market

Rank Bank Holding Company Volume Deals Share

1 Bank of America Merrill Lynch $51,021,082,391 240 22%

2 JP Morgan 37,727,848,041 154 16

3 Barclays Bank Plc 19,196,480,666 54 8

4 Morgan Stanley 17,653,750,000 32 7

5 Citi 16,598,608,247 50 7

6 Wells Fargo & Co 13,319,073,721 119 6

7 Credit Suisse 13,290,232,418 52 6

8 PNC Bank 5,620,669,428 50 2

9 General Electric Capital Corp 5,551,512,500 68 2

10 SunTrust Bank 4,965,225,000 50 2

11 Goldman Sachs & Co 4,853,665,000 20 2

12 Deutsche Bank 3,922,787,302 30 2

13 BNP Paribas SA 3,894,650,000 27 2

14 RBC Capital Markets 3,624,990,200 24 2

15 RBS 3,486,242,872 30 1

16 BMO Capital Markets 3,425,145,000 40 1

17 U.S. Bancorp 2,848,195,000 41 1

18 Mitsubishi UFJ Financial Group 2,788,397,250 17 1

19 Jefferies Finance LLC 2,254,500,000 13 1

20 UBS AG 2,245,300,000 14 1

21 KeyBank 1,951,375,000 24 1

22 Scotia Capital 1,866,460,000 14 1

23 Rabobank 1,705,200,000 12 1

24 Credit Agricole Corporate and Investment Bank S.A. 1,667,500,000 9 1

25 Societe Generale 943,960,000 10 1

Source: Thomson Reuters LPC

GOLD SHEETS – AUGUST 1, 2011 11* - ALL- IN SPREAD, DRAWN / UNDRAWN

BORROWER RATINGS AMOUNT TYPE MATUR. ACT./EXP. SPREADS FEES AIS* PURPOSE

INVESTMENT GRADE DEALS

EXPRESS SCRIPTS INC BBB+/Baa3 (Sr.) $5.5B Corp. purposes

St. Louis, MO (PACKAGE)

$45B

SIC 5912, 8011, 6719

(Drug stores and

proprietary stores)

PARTIAL

REFI CREDIT

LEAD LENDERS: Citigroup - Arranger/Lead Arranger, Credit Suisse AG - Arranger/Lead Arranger

COMMENTS: Credit will replace the company’s $14B bridge loan which backs the takeover of Metro Health Solutions. Co. is asking for $1B tickets with

$700M allocated to the BL and $300M to this agreement. Assignments: Pro Rata = y.

$1.5B RC 60 08/05/2011 NA/NA Corp. purposes

(Part 1/2) 08/05/2016

$4B TL A 60 08/05/2011 LIB+175 175.0/NA Corp. purposes

(Part 2/2) 08/05/2016

FEDEX CORP BBB/Baa2 (Sr.) $1B RC 60 04/26/2011 P+25 Com 25 125.0/25.0 Corp. purposes

Memphis, TN A-2/P-2 (CP) (Unsec’d) 04/26/2016 LIB+125 CP backup

$39B Capital expend.

SIC 4513, 4215

(Air courier

services)

REFI CREDIT GUARANTOR(S): Credit is guaranteed by certain of co.’s subsidiaries.

LEAD LENDERS: JPMorgan Chase Bank (8.5%) - Admin. Agent/Lead Arranger, BNP Paribas SA (4.5%) - Documentation Agent, SunTrust Bank (4.5%)

- Documentation Agent, Citibank (8.5%) - Syndications Agent/Lead Arranger

OTHERS IN DEAL: BOA (6.5%), Bank of Nova Scotia (6.5%), Goldman Sachs Bank USA (6.5%), Morgan Stanley Bank (4.5%), Deutsche Bank (4%), RegBk

(4%), Mizuho Corporate Bank USA (3.5%), Wells Fargo Bank (3.5%), BONYM (2.5%), Bank of Tokyo-Mitsubishi (2.5%), Commerzbank AG (2.5%), Fifth

Third Bank (2.5%), HSBCBankUSA (2.5%), Ind Comm Bk of China (2.5%), Keybank N.A. (2.5%), PNC Bank NA (2.5%), SMBC (2.5%), US Bank (2.5%),

ComericaBk (2%), First Tennessee Bank NA (2%), KBC (2%), Standard Chartered Bank (2%), State Street Bank (2%)

COMMENTS: Credit refi nances co.’s previous $1B credit agreement dated 07/22/09. JP Morgan Securities LLC and Citigroup Global Markets Inc. acted

as joint lead arrangers and joint bookrunners. Law Firm: Simpson Thacher & Bartlett LLP (for lender). Pricing: (See grid). Default rate = +200 bps.

Prime fl oor = one month LIBOR plus 100 bps. No LIBOR fl oor. Financial Covenant(s): Max. leverage ratio of 0.7:1. Prepayments: Amount Reduction

= 100%. Guarantor Release = 100%. Margin Reduction = 100%. Tenor Extension = 100%. Dividends are not materially restricted. Required Lenders =

51%. Term Changes = 100%. Assignments: Company consent required, Agent consent required. Assign. min. = $5M. Assign. fee = $4,000. Pro Rata

= y. Min. hold = $5M.

Level Sr Rating P+ LIB+ Com

1 > or =A- 0 87.5 17.5

2 > or =BBB+ 0 100 22.5

3 > or =BBB 25 125 25

4 > or =BBB- 50 150 32.5

5 <BBB- 100 200 37.5

Pricing is as indicated initially, tied to co.’s senior unsecured LTD ratings by S&P and Moody’s thereafter. If split rated, higher rating applies. If split rated

by more than one level, level below higher rating applies.

NATIONWIDE HEALTH BBB-/Baa2 (Sr.) $800M TL 12 06/03/2011 P+50 Com 10 150.0/10.0 Corp. purposes

PROPERTIES INC (Unsec’d) 06/01/2012 LIB+150

Newport Beach, CA

$439.3M

SIC 6798

(Real estate

investment trusts)

REFI CREDIT

LEAD LENDERS: JPM Co - Admin. Agent/Lead Arranger, Credit Agricole SA - Arranger/Lead Arranger, Keybank NA - Arranger/Lead Arranger, Wells

Fargo & Co - Arranger/Lead Arranger

COMMENTS: Credit replaces co.’s previous $700M RC dated 10/20/05. Credit Agricole Corporate & Investment Bank, Keybank NA, Wells Fargo Securi-

ties LLC and JP Morgan Securities LLC acted as joint bookrunners and joint lead arrangers. Law Firms: Sherry Meyerhoff Hanson & Crance LLP and

Skadden Arps Slate Meagher & Flom LLP (for borrower). Pricing: Default rate = Applic. P+200 bps. Prime fl oor = one month LIBOR plus 100 bps.

No LIBOR fl oor. Financial Covenant(s): Min. fi xed charge coverage ratio of 1.75:1; max. leverage ratio of 0.6:1. Min. net asset value of 85% of net asset

value as of closing. Max. secured debt ratio = 0.3:1. Max. unencumbered asset value ratio = 0.6:1. Indicated fi nancial covenant ratios required any

time acquisitions and dispositions by borrower are >$100M in any FQ. Indicated leverage ratio and unencumbered asset value ratio may be > 0.6:1 but

<= 0.65:1 for up to two consecutive FQs. Repayments: $800M install. on 06/01/2012. Prepayments: Debt Iss. Sweep = 100%. Equity Iss. Sweep =

100%. Amount Reduction = 100%. Margin Reduction = 100%. Tenor Extension = 100%. Dividends are not materially restricted. Required Lenders =

51%. Term Changes = 100%. Assignments: Company consent required, Agent consent required. Assign. min. = $5M. Assign. fee = $3,500. Pro Rata

= n. Elig. Assignees = commercial banks with total assets >$1B and combined capital and surplus >= $250M; life insurance cos. with admitted assets

>=$1B; nationally or internationally recognized investment banking cos. or other fi nancial institutions. Avg. life = 1 yrs.

GOLD SHEETS –August 1, 2011 12

PRAXAIR INC A/A2 (Sr.) $1.75B RC 60 07/28/2011 Com 8 NA/8.0 Corp. purposes

Danbury, CT A-1/P-1 (CP) 07/28/2016

$10.1B

SIC 2813, 3479, 3569

(Industrial gases)

PARTIAL

REFI CREDIT

LEAD LENDERS: Bank of America Merrill Lynch (9.14%) - Admin. Agent/Lead Arranger, Citibank (9.14%) - Syndications Agent/Lead Arranger, HSBC

(9.14%) - Syndications Agent/Lead Arranger

OTHERS IN DEAL: Bank of Tokyo-Mitsubishi (7.43%), Deutsche Bank (7.43%), RBS (7.43%), Wells Fargo Bank (7.43%), Credit Suisse (5.71%), JP Morgan

Chase (5.71%), Sovereign Bank (5.71%), BBVA (4.29%), Societe Generale (4.29%), SMBC (4.29%), BONYM (2.86%), Bank of Nova Scotia (2.86%), US

Bank (2.86%), China Merchants Bank (1.43%), Intesa Sanpaolo (1.43%), NorthernTr (1.43%)

COMMENTS: Credit refi nances existing debt. Pricing: (See grid). Assignments: Pro Rata = y.

Level Sr Rating Com

1 > or =AA- 5

2 > or =A+ 6

3 > or =A 8

4 > or =A- 10

5 > or =BBB+ 15

6 <BBB+ 17.5

Pricing is tied to company’s CDS, with initial fl oor of 25bp and a cap of 125bp. Level 1 a fl oor of 20bp and a cap of 100bp applies; for Level 2 a fl oor of

22.5bp and a cap of 112.5bp applies; for Level 3 a fl oor of 25bp and a cap of 125bp applies; for Level 4 a fl oor of 50bp and a cap of 137.5bp applies; for

Level 5 a fl oor of 75bp and a cap of 162.5bp applies; and for Level 6 a fl oor of 100bp and a cap of 187.5bp applies.

SOUTHWEST BBB-/Baa3 (Sr.) $800M RC 60 04/28/2011 P+125 Com 37.5 225.0/37.5 Corp. purposes

AIRLINES CO (Unsec’d) 04/28/2016 LIB+225 SBLC 225 Capital expend.

Dallas, TX

$12.1B

SIC 4512

(Air transportation,

scheduled)

REFI CREDIT

LEAD LENDERS: JP Morgan (15%) - Admin. Agent/Lead Arranger, Citibank (15%) - Syndications Agent/Lead Arranger, Barclays Capital Group (10.63%)

- Co-agent, Deutsche Bank AG (10.63%) - Co-agent, Goldman Sachs & Co (10.63%) - Co-agent, Morgan Stanley (10.63%) - Co-agent

OTHERS IN DEAL: BNP Paribas (6.88%), Comerica Bank NA (6.88%), Societe Generale (6.88%), WellsFar&Co (6.88%)

COMMENTS: Credit refi nances co.’s previous credit agreement dated 09/29/09. JP Morgan Securities LLC and Citigroup Global Markets Inc. acted as

co-lead arrangers and joint bookrunners. Law Firm: Simpson Thacher & Bartlett LLP (for lender). Pricing: (See grid). Default rate = +200 bps. Prime

fl oor = one month LIBOR plus 100 bps. No LIBOR fl oor. Option(s): $250M LC. Financial Covenant(s): Min. interest coverage ratio of 1.25:1. Indicated min.

interest coverage ratio may be reduced to 0.8:1 for two consecutive FQs, but co. must pay a quarterly fee of 25 bps to each bank for reduction. Prepay-

ments: Amount Reduction = 100%. Margin Reduction = 100%. Tenor Extension = 100%. Dividends are not materially restricted. Required Lenders =

51%. Term Changes = 100%. Assignments: Company consent required, Agent consent required. Assign. min. = $5M. Assign. fee = $3,500. Pro Rata

= y. Elig. Assignees: commercial banks with total assets >$1B.

Level Sr Rating P+ LIB+ Com SBLC

1 > or =A 0 100 12.5 100

2 > or =A- 12.5 112.5 15 112.5

3 > or =BBB+ 25 125 17.5 125

4 > or =BBB 50 150 25 150

5 > or =BBB- 75 175 32.5 175

6 <BBB- 125 225 37.5 225

Pricing is as indicated initially, tied to co.’s senior unsecured LTD ratings by S&P and Moody’s thereafter. SBLC fee = LIBOR margin plus co. also pays an

undisclosed issuance fee. If split rated, higher rating applies. If Split Rated by more than one level, level below higher rating applies.

* - ALL- IN SPREAD, DRAWN / UNDRAWN

BORROWER RATINGS AMOUNT TYPE MATUR. ACT./EXP. SPREADS FEES AIS* PURPOSE

INVESTMENT GRADE DEALS cont’d

GOLD SHEETS – AUGUST 1, 2011 13* - ALL- IN SPREAD, DRAWN / UNDRAWN

(Deal cont’d on next page)

BORROWER RATINGS AMOUNT TYPE MATUR. ACT./EXP. SPREADS FEES AIS* PURPOSE

M&A DEALS cont’d

BOJANGLES $215M LBO

RESTAURANTS INC (PACKAGE)

Charlotte, NC

SIC 5812

(Eating places)

PARTIAL

SPONSOR(S): Advent International Corp.

LEAD LENDERS: Jefferies Finance LLC - Arranger/Lead Arranger

COMMENTS: Credit backs the company’s buyout by Advent International. Credit comes with a roughly 45% equity check, which would value the deal at

approximately $390M. Jefferies is leading the deal. Assignments: Pro Rata = n.

$25M RC 60 08/05/2011 NA/NA LBO

(Part 1/2) 08/05/2016

$190M TL 72 08/05/2011 LIB+625 Upfr 100 625.0/NA LBO

(Part 2/2) 08/05/2017

COMMENTS: Pricing: Libor fl oor = 1.25%. OID = 99.

EXPRESS SCRIPTS INC BBB+/Baa3 (Sr.) $14B BL 12 08/05/2011 LIB+175 175.0/NA Takeover

St. Louis, MO 08/04/2012

$45B

SIC 5912, 8011, 6719

(Drug stores and

proprietary stores)

LEAD LENDERS: Credit Suisse AG - Admin. Agent/Lead Arranger, Citibank - Syndications Agent/Lead Arranger, Bank of America Merrill Lynch - Co-

arranger, Bank of Tokyo-Mitsubishi Group - Co-arranger, Credit Agricole SA - Co-arranger, Deutsche Bank AG - Co-arranger, Mizuho Bank - Co-arranger,

Morgan Stanley - Co-arranger, Royal Bank of Scotland Plc [US] - Co-arranger, Sumitomo Mitsui Banking Corp - Co-arranger, SunTrust Bank - Co-arranger,

Wells Fargo Bank - Co-arranger

COMMENTS: Credit fi nances the company’s $29.1B takeover of Medco Health Solutions,for $71.36 per share. The facility will be replaced by a permanent

bond and loan fi nancing consisting of a $1.5B RC and $4B TLA in August. Co. is asking for $1B tickets with $700M allocated to this facility and $300M

allocated to the $5.5B pro-rata agreement. Assignments: Pro Rata = y.

PROLOGIS INC BBB-/Baa2 (Sr.) $1.778B Acquis. line

Denver, CO (PACKAGE)

$909M

SIC 6798, 6531, 6512

(Real estate

investment trusts)

REFI CREDIT ADDITIONAL BORROWER(S): Credit is arranged for Prologis LP and certain affi liate borrowers.

COMMENTS: Credit is arranged to fi nance the merger between ProLogis and AMB Property Corp. Credit refi nances existing credit agreements dated

07/16/07 between AMB Property LP and Bank of America, an agreement dated 11/10/10 between AMP Property LP and JP Morgan Chase Bank NA,

and an agreement dated 10/06/05 between Old Prologis and Bank of America. Credit may be increased up to $2.75B (or its equivalent) and may be

extended for one additional year. Merrill Lynch Pierce Fenner & Smith Inc., JP Morgan Securities LLC, RBS Securities Inc. and Sumitomo Mitsui Bank-

ing Corp. acted as global lead arrangers and global bookrunners. Law Firms: Mayer Brown LLP, Weidema van Tol, Anderson Mori & Tomotsune and

Morrison & Foerster LLP (for borrower). Haynes & Boone (for lender). Pricing: (See grid). Default rate = +200 bps. Prime fl oor = one month LIBOR.

No LIBOR fl oor. Financial Covenant(s): Min. fi xed charge coverage ratio of 1.5:1; min. debt service coverage ratio of 1.5:1; max. loan to value ratio of 0.6:1.

Tangible Net Worth = $10B. Indicated loan to value ratio may be >0.6:1 but <=0.65:1 after any material acquisition. Prepayments: Amount Reduction

= 100%. Guarantor Release = 100%. Margin Reduction = 100%. Tenor Extension = 100%. Dividends are materially restricted. Required Lenders = 51%.

Term Changes = 100%. Assignments: Company consent required, Agent consent required. Assign. min. = $5M. Assign. fee = $3,500. Pro Rata = y.

Revolver/Line >= 1 Yr. EUR 480 M: Assign. min. = EUR 5 M Assign. Fee = EUR -,999,999. Assig. fee = US$3,500.Revolver/Line >= 1 Yr. JPY 22896 M :

Assign. min. = JPY 5 M Assign. Fee = JPY -,999,999. Assig. fee = US$3,500.

BBB-/Baa2 $702.432M RC 48 06/03/2011 P+40 Ann 30 170.0/30.0 Acquis. line

(At Close Sr.) (Part 1/3) 06/03/2015 LIB+140 SBLC 152.5

(Unsec’d) ExtenFee 20

GUARANTOR(S): ProLogis Inc. Credit is also guaranteed by Prologis LP.

GOLD SHEETS –August 1, 2011 14

LEAD LENDERS: Bank of America Merrill Lynch (10%) - Admin. Agent/Lead Arranger, JP Morgan (10%) - Syndications Agent/Lead Arranger, Royal Bank

of Scotland Plc [RBS] (10%) - Syndications Agent/Lead Arranger, Sumitomo Mitsui Banking Corp (6.63%) - Syndications Agent

OTHERS IN DEAL: Goldman Sachs & Co. (8.84%), RBC (8.84%), Wells Fargo Bank (8.84%), Citicorp NA (6.63%), Deutsche Bank (6.63%), MorganStnlyS-

rFund (6.63%), HSBC (3.68%), Calyon Corporate & Invest (2.95%), Credit Suisse (2.95%), ING Bank (2.95%), Scotiabank Europe Plc (2.95%), CompassBk

(1.47%), NorthernTr, PNCBk

COMMENTS: Facility labelled as euro tranche. Facility is also available in US dollars, pounds sterling and yen. Option(s): $73.2M LC and $146.3M swingline.

Level Sr Rating P+ LIB+ Ann SBLC

1 > or =A- 17.5 117.5 22.5 130

2 > or =BBB+ 25 125 25 137.5

3 > or =BBB 40 140 30 1152.5

4 > or =BBB- 65 165 35 177.5

5 <BBB- 105 205 45 217.5

Pricing is as indicated initially thru 10/03/11, tied to co.’s senior unsecured LTD ratings by S&P, Moody’s and Fitch thereafter. If rated by all three agencies,

higher of S&P and Moody’s applies. If rated by only two agencies, higher rating applies. SBLC fee includes a 12.5 bps issuance fee.

BBB-/Baa2 $285.273M RC 48 06/03/2011 P+40 Ann 30 170.0/30.0 Acquis. line

(At Close Sr.) (Part 2/3) 06/03/2015 LIB+140 SBLC 152.5

(Unsec’d) ExtenFee 20

GUARANTOR(S): ProLogis Inc. Credit is also guaranteed by Prologis LP.

LEAD LENDERS: Bank of America Merrill Lynch (14.38%) - Admin. Agent/Lead Arranger, JP Morgan (14.38%) - Syndications Agent/Lead Arranger, Royal

Bank of Scotland Plc [RBS] (14.38%) - Syndications Agent/Lead Arranger, Sumitomo Mitsui Banking Corp (10.66%) - Syndications Agent/Lead Arranger

OTHERS IN DEAL: Citibank Japan Ltd (10.66%), Deutsche Bank (10.66%), Morgan Stanley MUFG Loan (10.66%), Bank of Nova Scotia (3.55%), Calyon

Corporate & Invest (3.55%), Credit Suisse (3.55%), ING Bank (3.55%), Goldman Sachs & Co., HSBC, NorthernTr, PNCBk

COMMENTS: Facility labelled as yen tranche. Facility is also available in US dollars, Euros and pounds sterling. Option(s): $26.8M LC.

Level Sr Rating P+ LIB+ Ann SBLC

1 > or =A- 17.5 117.5 22.5 130

2 > or =BBB+ 25 125 25 137.5

3 > or =BBB 40 140 30 152.5

4 > or =BBB- 65 165 35 177.5

5 <BBB- 105 205 45 217.5

Pricing is as indicated initially thru 10/03/11, tied to co.’s senior unsecured LTD ratings by S&P, Moody’s and Fitch thereafter. If rated by all three agencies,

higher of S&P and Moody’s applies. If rated by only two agencies, higher rating applies. SBLC fee includes a 12.5 bps issuance fee.

BBB-/Baa2 $790M RC 48 06/03/2011 P+40 Ann 30 170.0/30.0 Acquis. line

(At Close Sr.) (Part 3/3) 06/03/2015 LIB+140 SBLC 152.5

(Unsec’d) ExtenFee 20

GUARANTOR(S): ProLogis Inc. Credit is also guaranteed by Prologis LP.

LEAD LENDERS: Bank of America Merrill Lynch (5.49%) - Admin. Agent/Lead Arranger, Sumitomo Mitsui Banking Corp (6.33%) - Syndications Agent,

JP Morgan (5.49%) - Syndications Agent/Lead Arranger, Royal Bank of Scotland Plc [RBS] (5.49%) - Syndications Agent/Lead Arranger

OTHERS IN DEAL: Goldman Sachs & Co. (8.23%), RBC (8.23%), Wells Fargo Bank (8.23%), Citicorp NA (6.33%), Deutsche Bank (6.33%), US Bank (6.33%),

Union Bank NA (6.33%), Morgan Stanley Bank (4.43%), HSBC (3.16%), PNCBk (3.16%), Bank of Nova Scotia (2.53%), Calyon Corporate & Invest (2.53%),

Credit Suisse (2.53%), ING Bank (2.53%), NorthernTr (2.53%), CompassBk (1.9%), MorganStnlySrFund (1.9%)

COMMENTS: Facility labelled as US tranche. Facility is also available in Euros, pounds sterling, yen and Canadian dollars. Option(s): $150M LC and

$100M swingline.

Level Sr Rating P+ LIB+ Ann SBLC

1 > or =A- 17.5 117.5 22.5 130

2 > or =BBB+ 25 125 25 137.5

3 > or =BBB 40 140 30 152.5

4 > or =BBB- 65 165 35 177.5

5 <BBB- 105 205 45 217.5

Pricing is as indicated initially thru 10/03/11, tied to co.’s senior unsecured LTD ratings by S&P, Moody’s and Fitch thereafter. If rated by all three agencies,

higher of S&P and Moody’s applies. If rated by only two agencies, higher rating applies. SBLC fee includes a 12.5 bps issuance fee.

* - ALL- IN SPREAD, DRAWN / UNDRAWN

BORROWER RATINGS AMOUNT TYPE MATUR. ACT./EXP. SPREADS FEES AIS* PURPOSE

M&A DEALS cont’d

PROLOGIS INC

CONT’D

GOLD SHEETS – AUGUST 1, 2011 15

ASSOCIATED ESTATES $125M TL 60 06/03/2011 P+80 Cancel 50 180.0/NA Corp. purposes

REALTY CORP (Unsec’d) 06/02/2016 LIB+180

Richmond Heights, OH

$153.7M

SIC 6798, 6513, 6531

(Real estate

investment trusts)

REFI CREDIT GUARANTOR(S): Co.’s subsidiaries acted as guarantors.

LEAD LENDERS: PNC Bank (24%) - Admin. Agent/Lead Arranger, US Bank NA (20%) - Documentation Agent, Wells Fargo & Co (24%) - Syndications Agent

OTHERS IN DEAL: RBS Citizens (11%), RaymndJamesCorp (11%), Citicorp (10%)

COMMENTS: Credit refi nances co.’s previous RC dated 10/18/10. PNC Capital Markets LLC acted as lead arranger. Law Firms: Greenberg Traurig LLP

(for borrower). SNR Denton (for lender). Pricing: (See grid). Default rate = +400 bps. Prime fl oor = one month LIBOR plus 100 bps. No LIBOR fl oor.

Indicated cancellation fee applies thru year one. Financial Covenant(s): Min. fi xed charge coverage ratio of 1.5:1; max. loan to value ratio of 0.6:1. Max.

consolidated unsecured debt to unencumbered real property value ratio = 0.6:1. Min. unencumbered real property adjusted NOI to consolidated interest

expense on consolidated unsecured debt ratio = 2:1. Min. % of total residential units in the qualifying unencumbered projects that are physically occupied

by tenants = 85%. Min. consolidated tangible net worth = $500M plus 85% of proceeds from any equity issuances. Prepayments: Amount Reduction

= 100%. Margin Reduction = 100%. Tenor Extension = 100%. Dividends are materially restricted. Required Lenders = 66.67%. Term Changes = 100%.

Assignments: Company consent required, Agent consent required. Assign. min. = $5M. Assign. fee = $3,500. Pro Rata = n.

Level Loa/Value P+ LIB+

1 >0.55 < or =0.6 155 255

2 >0.5 < or =0.55 130 230

3 >0.45 < or =0.5 105 205

4 < or =0.45 80 180

Pricing is as indicated initially thru 06/30/11, tied to co.’s consolidated outstanding debt to total asset value ratio thereafter.

DRESSER-RAND BB+/Ba1 (Sr.) $1B Corp. purposes

Houston, TX B+/B1 (Sub.) (PACKAGE)

$2B

SIC 3511

(Turbines and

turbine generator

sets)

REFI CREDIT ADDITIONAL BORROWER(S): D-R Holdings (France) SAS.

COMMENTS: Credit refi nances co.’s previous credit agreement dated 08/30/07. Indicated maturity may be extended to 03/15/16, if by 05/01/14, the

domestic borrower’s 2014 senior subordinated notes have (i) had their maturity extended to a date >= 6 months after 03/15/16, (ii) been repaid in cash in

full or (iii) been refi nanced by new unsecured senior or senior subordinated notes having maturity >= 6 months after 03/15/16. Credit may be increased

up to $1.15B. Credit comes in conjunction with $375M 144A senior subordinated notes due 05/01/21 at 6.5%. JP Morgan Securities LLC acted as sole lead

arranger and sole book manager. Law Firms: Gibson Dunn & Crutcher LLP and Shearman & Sterling LLP (for borrower). Vinson & Elkins LLP (for lender).

Pricing: (See grid). Default Rate = +200 bps. Prime fl oor = one month LIBOR plus 100 bps. No LIBOR fl oor. Financial Covenant(s): Min. interest cover-

age ratio of 3:1; max. debt to EBITDA ratio of 3.75:1. Max. Capex (initial) = $110M. Max. Capex (fi nal) = $150M. Capex carryover = 100%. Debt to EBITDA =

consolidated debt to consolidated EBITDA. Prepayments: Assets Sales Sweep = 100%. Indicated asset sales sweep not required if proceeds <= $5M or

if proceeds are reinvested within one year. Indicated prepayments apply to TL facilities. Amount Reduction = 100%. Guarantor Release = 100%. Margin

Reduction = 100%. Tenor Extension = 100%. Dividends are materially restricted. Required Lenders = 51%. Term Changes = 100%. Collateral Release

= 100%. Assignments: Company consent required, Agent consent required. Assign. min. = $5M. Assign. fee = $3,500. Pro Rata = n. Min. hold = $5M.

BB+/Ba1 $600M RC 38 03/15/2011 P+100 Upfr 87.5 200.0/37.5 Corp. purposes

(At Close Sr.) (Part 1/3) 05/01/2014 LIB+200 Com 37.5

B+/B1 (Sec’d) SBLC 212.5

(At Close Sub.)

B1 (At Close CP)

LEAD LENDERS: JP Morgan (9%) - Admin. Agent/Lead Arranger, Bank of America (8.5%) - Co-agent, Commerzbank AG (8.5%) - Co-agent, DnB NOR

Bank ASA (8.5%) - Co-agent, Sovereign Bank (8.5%) - Co-agent, Wells Fargo & Co (8.5%) - Co-agent

OTHERS IN DEAL: BBVA Compass (6.5%), Bank of Tokyo-Mitsubishi (6.5%), Citigroup (6.5%), HSBCBankUSA (6.5%), Sumitomo Mitsui Banking C (6.5%),

Barclays Bank Plc (4%), US Bank (4%), BB&T Cap (2%), ComericaBk (2%), Morgan Stanley (2%), NorthernTr (2%)

COMMENTS: Facility is also available in Euros and pounds sterling. Option(s): $600M LC and $30M swingline. LC can be Financial or Performance LC.

LC is also available in alternate currency. Euro sublimit = $350M. Pounds sterling sublimit = $75M. Collateral: Unknown.

Level Debt/CF P+ LIB+ Com SBLC

1 > or =3 175 275 50 287.5

2 > or =2.25 <3 150 250 50 262.5

3 > or =1.5 <2.25 125 225 37.5 237.5

4 <1.5 100 200 37.5 212.5

Pricing is as indicated initially, tied to co.’s consolidated debt to consolidated EBITDA ratio thereafter. Indicated SBLC fee applies for Financial LC. Co.

pays Performance LC as follows: 177.5 bps for Level 1, 162.5 bps for Level 2, 147.5 bps for Level 3 and 132.5 bps for Level 4. Financial and Performance

LC fee includes a 12.5 bps issuance fee.

* - ALL- IN SPREAD, DRAWN / UNDRAWN

(Deal cont’d on next page)

BORROWER RATINGS AMOUNT TYPE MATUR. ACT./EXP. SPREADS FEES AIS* PURPOSE

LEVERAGED DEALS cont’d

Non-M&A loans with LIBOR spreads ≥ 275 bps.

GOLD SHEETS –August 1, 2011 16

BB+/Ba1 $240M Del. Draw 38 03/15/2011 P+100 Upfr 87.5 200.0/37.5 Corp. purposes

(At Close Sr.) (Part 2/3) 05/01/2014 LIB+200 Com 37.5

B+/B1 (Sec’d)

(At Close Sub.)

B1 (At Close CP)

LEAD LENDERS: JP Morgan (9%) - Admin. Agent/Lead Arranger, Bank of America (8.5%) - Co-agent, Commerzbank AG (8.5%) - Co-agent, DnB NOR

Bank ASA (8.5%) - Co-agent, Sovereign Bank (8.5%) - Co-agent, Wells Fargo & Co (8.5%) - Co-agent

OTHERS IN DEAL: BBVA Compass (6.5%), Bank of Tokyo-Mitsubishi (6.5%), Citigroup (6.5%), HSBCBankUSA (6.5%), Sumitomo Mitsui Banking C (6.5%),