gold, monetary policy and inflation fina 425 assist. prof. dr. korhan gokmenoglu submitted by: emil...

TRANSCRIPT

Gold, Monetary Policy and Inflation

FINA 425

Assist. Prof. Dr. Korhan Gokmenoglu

Submitted by: Emil Seyidov 117465

Shahmar Aghalarov 117178

CONTENTS

Money and Prices The Gold Standard The Fall of the Gold Standard Stocks as Hedges against Inflation Why Stocks Fail as a short term Inflation

Hedge?

Money and Prices

Inflation is a rise in the general level of the prices related to an increase in the volume of money, which results in the loss of value of a currency.

One variable is important in determining the price level: the amount of money in circulation.

No sustained inflation is possible without continuous money creation, and every hyperinflation in history has been associated with an explosion of the money supply.

Money and Price Indexes in the United States, 1830 through December 2006

What has changed over the past half century that makes inflation the rule rather than the exception?

The answer is simple: control of the money supply has shifted from gold to the government.

With this shift, a whole new system has come into being that connects money, government deficits, and inflation.

U.S. and U.K. Price Indexes, 1800 through December 2006 (1800 = $1)

The Gold Standard

Governments were obligated to exchange dollars for a fixed amount of gold.

Since the total quantity of gold in the world was fixed, prices of goods generally remained relatively constant.

That is why the world experienced no overall inflation during the nineteenth and early twentieth centuries.

By equating the money in circulation to the quantity of gold available, the government essentially gave up control over monetary conditions.

The Fall of The Gold Standard

In the wake of the stock crash of 1929, the news that a few banks were having problems meeting withdrawals started a panic.

The Federal Reserve failed to prevent this crisis.

In addition, the depositors too were creating pressure on the government’s gold reserves.

The Fall of The Gold Standard

To prevent a steep loss of gold, Great Britain took the first step and abandoned the gold standard on September 20, 1931, suspending the payment of gold for sterling.

Eighteen months later, the United States also suspended the gold standard as the depression and financial crisis worsened.

The Fall of The Gold Standard

Stocks soared over 9 percent on April 19 and almost 6 percent the next day.

Investors felt the government could now provide the extra liquidity needed to stabilize commodity prices and stimulate the economy, which they regarded as a boon for stocks.

Bonds, however, fell, as investors feared the inflationary consequences of leaving the gold standard.

POSTDEVALUATION MONETARY POLICY

As part of the Bretton Woods, the U.S. government promised to exchange all dollars for gold at the fixed rate of $35 per ounce as long as countries fixed their currency to the dollar.

In 1968, the Congress ended the obsolete gold-backing requirement for dollar.

On August 15, 1971, President Nixon announced the “New Economic Policy”

The stock market responded enthusiastically by jumping almost 4 percent on record volume.

POSTGOLD MONETARY POLICY

The surge of inflation in 1979 urged the Federal Reserve to change its policy and seriously control inflation.

On October 6, 1979, Paul Volcker announced that no longer would the Federal Reserve set interest rates to guide policy, instead would exercise control over money supply.

Stocks fall almost 8 percent on record volume in 2 days following the announcement.

The tight monetary policy of the Volcker years eventually broke the inflationary cycle.

Restricting money growth proved to be the only real answer to controlling inflation.

THE FEDERAL RESERVE AND MONEY CREATIONWhen the Fed wants to increase the money

supply, it buys a government bond in the open market.

If the Federal Reserve wants to reduce the money supply, it sells government bonds from its portfolio.

The buying and selling of government bonds are called open market operations.

HOW THE FED’S ACTIONS AFFECT INTEREST RATES

An active market for reserves among banks is called the federal funds market, and the interest rate at which these funds are borrowed and lent, the federal funds rate.

The fed funds market is a private lending market among banks where rates are dictated by supply and demand.

If the Fed buys securities, the interest rate on federal funds goes down because banks then have ample reserves to lend.

If the Fed sells securities, the federal funds rate goes

up because banks scramble for the remaining supply.

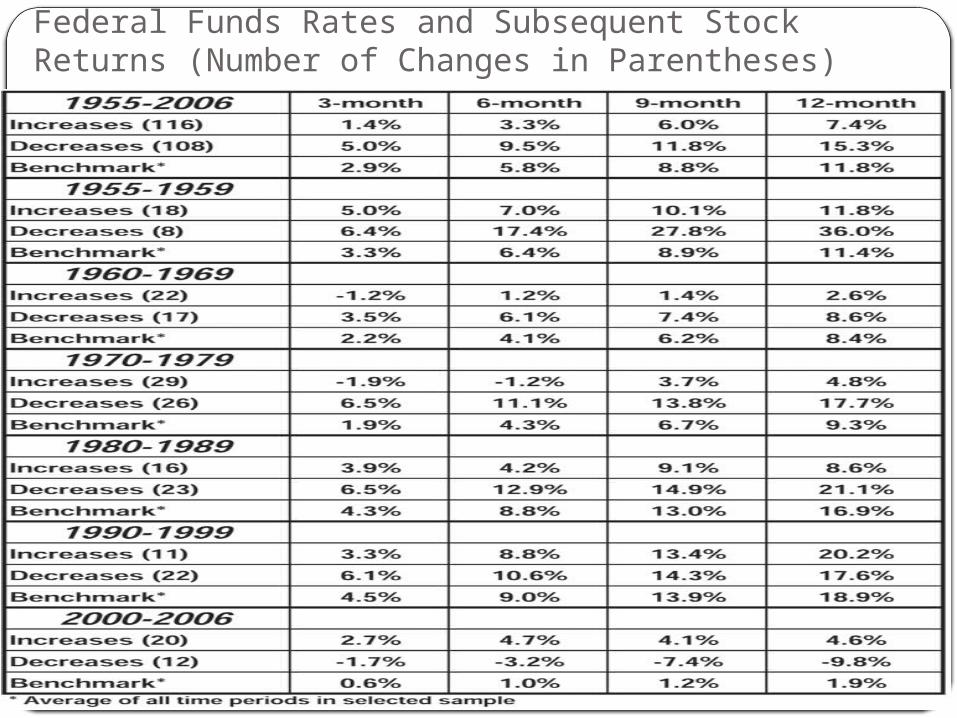

Federal Funds Rates and Subsequent Stock Returns (Number of Changes in Parentheses)

STOCKS AS HEDGES AGAINST INFLATION

In contrast to the returns of fixed-income assets over long periods of time, the returns on stocks over the same time periods have kept pace with inflation.

Since stocks are claims on the earnings of real assets, it is reasonable to expect that their long-term returns will not be influenced by inflation.

The ability of an asset such as stocks to maintain its purchasing power during periods of inflation makes equities an inflation hedge.

WHY STOCKS FAIL AS A SHORT-TERM INFLATION HEDGE

If stocks represent real assets, why do they fail as a short-term inflation hedge?

Inflation increases interest rates on bonds, and higher interest rates on bonds depress stock prices.

But higher expected inflation also raises the expected future cash flows available to stockholders.

In theory the returns from stocks will keep up with rising prices and stocks will be a complete inflation hedge.

WHY STOCKS FAIL AS A SHORT-TERM INFLATION HEDGE

Non-neutral Inflation: Supply-Side Effects

Taxes on Corporate Earnings

Inflationary Biases in Interest Costs

Capital Gains Taxes

CONCLUSION

Replacing gold standard with fiat was the start of new issues in finance : deflation and inflation.

Stock succeed as an inflation hedge in the long run, but not in the short run.

Inflation, although kinder to stocks than bonds, is still not good for equity holders.

But if inflation again rears its head, investors will do much better in stocks than in bonds.

“If you aren’t willing to own a stock

for ten years, don’t even think about

owning it for ten minutes”

Warren Buffett