gnss, earth observation and satellite telecommunication ... · pdf filegnss, earth observation...

TRANSCRIPT

GNSS, Earth Observation and Satellite Telecommunication

Applications and Markets

October 2009

Table of Contents

1. Global Navigation Satellite Systems (GNSS) .................................................................................... 4

1.1. Global navigation systems ....................................................................................................... 5

1.1.1. GPS ................................................................................................................................... 5

1.1.2. GLONASS .......................................................................................................................... 6

1.1.3. Galileo .............................................................................................................................. 6

2. GNSS Market ................................................................................................................................... 8

3. GPS Technology Market and Trends ............................................................................................. 10

3.1. GPS chipset miniaturization and falling prices ...................................................................... 10

3.2. GPS enabled handsets in navigation markets ....................................................................... 10

3.3. Auto, mobile and handheld segments important in navigation market ............................... 11

3.4. Handset market – location based services adoption, applications driving sales .................. 13

3.5. Growing demand for precision GNSS .................................................................................... 14

4. GNSS Services Markets and Market Trends .................................................................................. 15

4.1. Land Applications, location based services (LBS) .................................................................. 15

4.1.1. Navigation...................................................................................................................... 17

4.1.2. Tracking & fleet management services ......................................................................... 21

4.1.3. Traffic management & public transport ........................................................................ 26

4.1.4. Location-based social networks (LBSN) ......................................................................... 31

4.1.5. Location-based gaming.................................................................................................. 34

4.1.6. Law Enforcement ........................................................................................................... 35

4.2. Precision GNSS applications .................................................................................................. 36

4.2.1. Agriculture & Forestry ................................................................................................... 40

5. Remote Sensing and Earth Observation ........................................................................................ 46

5.1. Satellite imaging .................................................................................................................... 47

5.2. Earth Observation value chain .............................................................................................. 51

5.2.1. Data providers ............................................................................................................... 53

5.2.2. Value adding sector ....................................................................................................... 56

5.3. Earth observation applications .............................................................................................. 59

5.3.1. Agriculture ..................................................................................................................... 59

5.3.2. Earth observation applications in forestry and forest management ............................ 62

5.3.3. Energy Industry applications ......................................................................................... 63

5.3.4. Marine applications ....................................................................................................... 72

3

5.4. Providers of satellite imagery ................................................................................................ 75

6. Fixed Satellite Service (FSS) market............................................................................................... 84

6.1. Market size and segmentation .............................................................................................. 84

6.1.1. Applications ................................................................................................................... 85

6.1.2. Geographical segmentation .......................................................................................... 87

6.2. Perspectives and market trends ............................................................................................ 89

6.2.1. Technological segmentation for application segmentation .......................................... 89

6.2.2. Growing demand for video capacity ............................................................................. 89

7. Mobile Satellite Service (MSS) market .......................................................................................... 91

7.1. Market size and segmentation .............................................................................................. 91

7.1.1. Maritime market ........................................................................................................... 92

7.1.2. Land services market ..................................................................................................... 93

7.1.3. Aeronautical market ...................................................................................................... 95

7.2. Perspectives and market trends ............................................................................................ 95

7.2.1. Broadband adoption ...................................................................................................... 95

7.2.2. Handheld market ........................................................................................................... 97

7.2.3. In-flight communications............................................................................................... 98

7.2.4. Changes in the supply chain .......................................................................................... 98

7.2.5. Military demand .......................................................................................................... 100

7.3. MSS competitor overview ................................................................................................... 101

7.3.1. Barriers to entry in MSS sector .................................................................................... 101

7.3.2. Companies offering MSS ............................................................................................ 102

4

1. Global Navigation Satellite Systems (GNSS)

Satellite-based navigation is, together with telecommunications and Earth observation, one of the

three main legs of the so called space applications. Satellite-based navigation systems or Global

Navigation Satellite Systems (GNSS) are services which provide signals that can be used to accurately

locate the position of people and places, and to provide safe navigation information for moving

platforms such as ships, aircraft, and automobiles, anywhere on the surface of the Earth and out to

near space.

The infrastructure of a GNSS system can be basically divided into three so-called segments: the space

segment, the ground segment, and the user segment.

The space segment in composed of the satellites which transmit the navigation signal, also

called signal in space, used by the user receiver to calculate its position, time, and velocity.

The ground segment or ground control segment includes all the means used by the

owner or operator to keep the system working appropriately, tracking the satellite

constellation and transmitting the corrected orbital parameters. This includes a control

center or master station, and ground stations to control and monitor the satellite

constellation and provide the satellites and user with the information needed to generate an

adequate signal in space.

The user segment is composed of the user receivers which get the signals from the

satellite, perform the calculations using different algorithms, and provide the user with

the required service.

In addition to these three segments, another two components, which are not strictly part of the

GNSS, have to be taken into account, the launch segment and the external entities. The launch

segment includes all the means (basically launch services and early operations) in order to place the

satellites into their defined orbits from where they will provide the signals. The term external entities

refers in a broad sense to any entity that interacts with the GNSS system. Some examples include

entities providing time reference information (Coordinated Universal Time, UTC), and precise Earth-

based position reference (GTRF system), other GNSS systems, other systems providing regional

integrity information, the scientific community and so forth.

5

Augmentation systems can also be considered as part of the GNSS. Those are systems that use space

or ground-based infrastructure to enhance the navigation signals with greater performances or value

added services in a determined local or regional area. Depending on the infrastructure used for the

augmentation, the augmentation systems can be classified as ground-based (GBAS) or satellite-based

(SBAS). An example of SBAS is European Geostationary Navigation Overlay Service (EGNOS).

Consisting of three geostationary satellites and a network of ground-stations, EGNOS augments the

existing GNSS (GPS and GLONASS) systems.

Basically, navigation satellite systems implement a time-difference-of-arrival concept. This is done

using precise satellite position and on-board atomic clocks to generate navigation messages that are

continuously broadcast from each of the satellites in the GNSS constellation. These messages,

containing information about the position and clock of the satellite sending the message, can be

received and processed by users anywhere in the world (within the coverage of the system). The

receiver, upon reception of those messages, determines the distance between both, by measuring

the travel time of the signal. The user needs the information of at least three satellites in order to

determine its position with enough accuracy (ranging between centimeters and a few meters,

depending on different factors). The signal from a fourth satellite would provide the accurate (in the

order of nanoseconds) reference of time.

1.1. Global navigation systems

The GNSS of today consists of two satellite constellations, the US Global Positioning System (GPS)

and the Russian GLONASS. These are the only two satellite systems in orbit from which military and

civilian users can determine their positions free of any charges almost anywhere on Earth. Of these

two systems the GPS is fully operational today, offering worldwide service.

1.1.1. GPS

The concept of GPS started in the early 1970s as a way for the United States military to accurately

identify locations throughout the globe. Between 1978 and 1985, the US Department of Defense

launched the first generation of GPS satellites (Block I) exclusively for military use. However, in 1983

following the downing of Korean Airlines Flight 007 after it strayed over territory belonging to the

Soviet Union, President Ronald Reagan decided to permit civilian use of GPS technology once it

became operational. Launches of second generation GPS Block II satellites, which included a signal

for civilian use, began in 1989, and additional Block IIA GPS satellites were launched in the early

1990s to complete the GPS constellation. Air Force Space Command (AFSPC) declared full operational

capability on April 27, 1995.

The current GPS constellation consists of 32 satellites in nearly circular orbits, at an altitude of

approximately 20,200 kilometers above the earth (most recent launches took place in March 2009).

The satellites are arranged on 6 planes, each of them containing at least 4 slots where satellites can

be arranged equidistantly. The circulation time of the satellites is about 12 hours.

According to sources, GPS cost between $10 and $11 billion to build between 1987 and 2002. Since

2000 additional $1.6 billion has already been spent on GPS modernization program IIIA without any

6

new generation satellites launched to date.1 It is claimed that GPS currently contributes $30 billion to

the U.S. economy annually.2

1.1.2. GLONASS

GLONASS (Global Navigation Satellite System) is the Russian equivalent of the U.S. Global Positioning

System, and is designed for both military and civilian use. Development on GLONASS began in 1976,

with a goal of global coverage by 1991. Beginning on 12 October 1982, numerous launches added

satellites to the system until the constellation was completed in 1995. Economic problems

suspended the project, and Russia committed to restore the system in 2001. Since 2007, Russian

military has provided open access to the civilian navigation signals of the GLONASS system, to

Russian and foreign consumers free of charge and without limitations.

As of June 2009, the GLONASS system comprises 20 satellites. A total of 17 satellites are operational

while three remain under maintenance. The system requires 18 satellites for continuous navigation

services covering the entire territory of the Russian Federation, and 24 satellites to provide services

worldwide. Two Proton-M launch vehicles are expected to lift off this year to put six more Glonass-M

satellites into orbit. GLONASS is expected to become fully operational with 24 satellites early in

2010.3

Several North American and European manufacturers offer combined GPS/GLONASS OEM products,

including NovAtel, Javad GNSS4, Trimble, Septentrio5, and Leica6.

The stable progress in rebuilding and modernizing GLONASS and the launch of single GLONASS/GPS

chips by Javad and other manufacturers have even sparked interest from large players in the mobile

phone industry. Nokia has been investigating the use of GLONASS for its handsets.7

1.1.3. Galileo

The Galileo Positioning System is a satellite navigation system, being built by the European Union

(EU) as an alternative to the US Global Positioning System (GPS) and the Russian GLONASS. Unlike

GPS and GLONASS, Galileo is a navigation infrastructure fully under civilian control.

The idea of a European geopositioning system similar to the GPS and Russia’s Global Navigation

GLONASS originated a decade ago, when teams of engineers from France, Germany, Italy, and the

United Kingdom developed a joint concept for an independent set of satellites that would provide

superior accuracy and not be vulnerable to military cutoff. In March 2002, the European Union (EU)

and the European Space Agency (ESA) agreed to proceed with the project, named Galileo, which they

visualized as a public-private partnership (PPP) that ultimately would pay for itself by providing

premium paid services with encoded signals.

1 http://www.telecommagazine.com/article.asp?HH_ID=AR_5309

2 http://www.washingtonpost.com/wp-dyn/content/article/2008/05/15/AR2008051504007.html

3 http://www.insidegnss.com/node/1389

4 http://www.javad.com/jns/index.html?/jns/technology/jns_digital_chip_specifications.html

5 http://www.septentrio.com/products_gps.htm

6 http://www.leica-geosystems.com/corporate/en/products/gps_systems/lgs_67536.htm

7 http://www.insidegnss.com/node/534

7

However, in early 2007 the consortium of eight leading aerospace and telecom companies, known as

the European Satellite Navigation Industries, formally abandoned the project. The consortium could

not reach agreement on issues such as the allocation of lucrative contracts, and the European Union

took control.

Lack of public funds then led to a period of great uncertainty for Galileo. Although the original aim

had been to have the system operational by 2008, by 2007 only one test satellite (GIOVE-A) was in

orbit and just four of the thirty in the projected constellation had been ordered. The EC proposed to

fully fund the project using public money, leaving private companies to run the system. The EC

funding was to come from its surplus agriculture and administration budgets for 2007 and 2008. The

project was finally approved by the 27 EU transport ministers in November 2007 in an amount of

€3.4 billion. Total estimated investment costs of the Galileo project are €5.4 billion.

In June 2009 ESA and commercial launch services provider Arianespace signed a contract for the

launch of the first four operational Galileo satellites. The deal calls for the Galileo satellites to be sent

into orbit in pairs using two Soyuz launch vehicles. The launches will be made from the Soyuz launch

facility currently under construction at the Guiana Space Center, in French Guiana. All four of the

satellites are supposed to be in orbit by the end of 2010.

Initial operational capability, with about eighteen satellites in orbit, is planned for 2012. Full

operational capability of the system with a network of 30 satellites is expected in 2013.

In July 2007 the EU and USA signed an interoperability agreement under which they approved design

for a common civil signal. Incorporation of the multiplexed binary offset carrier (MBOC) frequency

means future users will be able to obtain signals from either, GPS or Galileo, using a single handset.

Similarly, discussions are underway between the Russian Federal Space Agency and the EU to ensure

a degree of interoperability between GLONASS and Galileo.

It is anticipated that Galileo will benefit the European economy to the tune of about €60 billion

annually by 2030.

Figure 1 Galileo development timeline

8

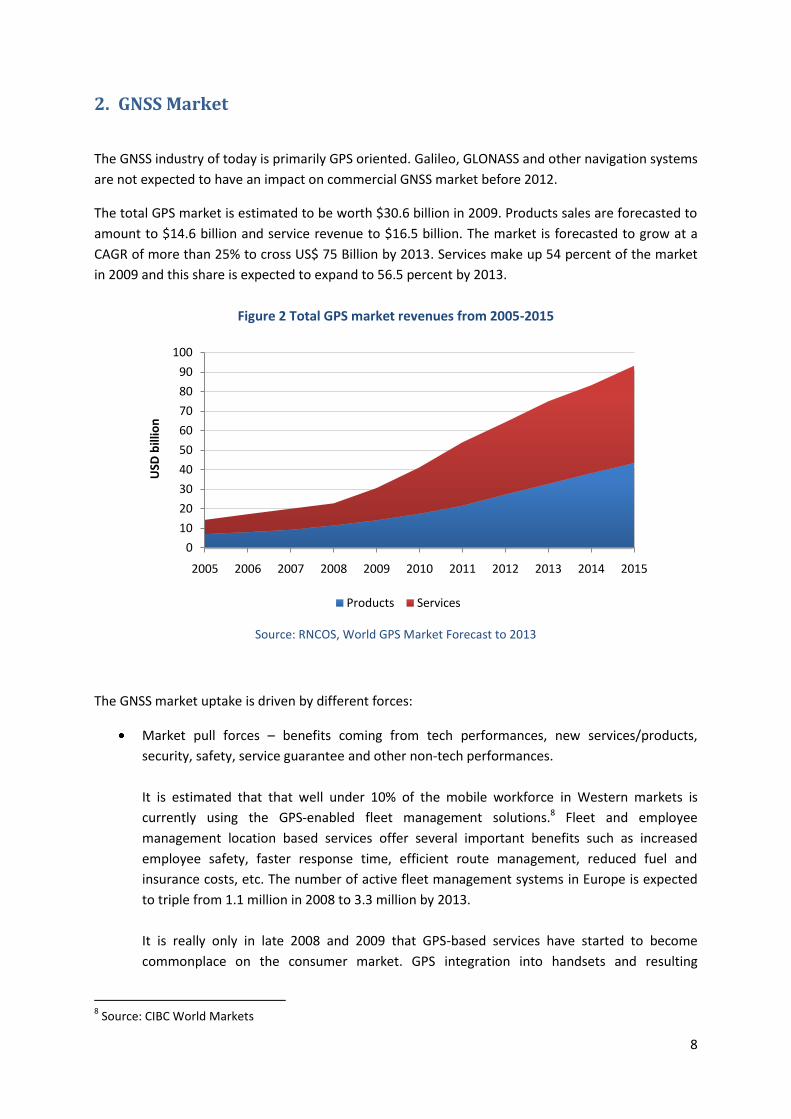

2. GNSS Market

The GNSS industry of today is primarily GPS oriented. Galileo, GLONASS and other navigation systems

are not expected to have an impact on commercial GNSS market before 2012.

The total GPS market is estimated to be worth $30.6 billion in 2009. Products sales are forecasted to

amount to $14.6 billion and service revenue to $16.5 billion. The market is forecasted to grow at a

CAGR of more than 25% to cross US$ 75 Billion by 2013. Services make up 54 percent of the market

in 2009 and this share is expected to expand to 56.5 percent by 2013.

Figure 2 Total GPS market revenues from 2005-2015

Source: RNCOS, World GPS Market Forecast to 2013

The GNSS market uptake is driven by different forces:

Market pull forces – benefits coming from tech performances, new services/products,

security, safety, service guarantee and other non-tech performances.

It is estimated that that well under 10% of the mobile workforce in Western markets is

currently using the GPS-enabled fleet management solutions.8 Fleet and employee

management location based services offer several important benefits such as increased

employee safety, faster response time, efficient route management, reduced fuel and

insurance costs, etc. The number of active fleet management systems in Europe is expected

to triple from 1.1 million in 2008 to 3.3 million by 2013.

It is really only in late 2008 and 2009 that GPS-based services have started to become

commonplace on the consumer market. GPS integration into handsets and resulting

8 Source: CIBC World Markets

0

10

20

30

40

50

60

70

80

90

100

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

USD

bill

ion

Products Services

9

combination of location information with a data connection has great potential to

revolutionize the way people live and work. According to analysts location based advertising

would be predominantly used for monetizing location services and could generate $18 billion

in revenue by 2015 globally.9

Regulatory forces – directives, standards, certification, security;

Following the SOLAS regulation XI-2/6 adopted in December 2002 by the IMO (International

Maritime Organization) and effective over two stages (July 1, 2004 and July 1, 2006), all

vessels of more than 500 tons must be equipped with a SSAS (Ship Security Alert System).

SSAS is a GPS-based system that sends an alert from ship to shore in case of a piracy or

terrorist attack on-board a vessel.

44 US states out of 50 have regulations in place that require those criminals with a profile

that indicates a likelihood of them repeating their crimes to wear GPS tracking devices so

that authorities can monitor their movements. Florida’s experience shows offenders on GPS

tracking are less likely to get in trouble than those under traditional supervision. Nearly 6

percent of GPS-monitored offenders had committed new felonies or misdemeanors,

compared with 11 percent of those who were not electronically monitored.10 Similar tracking

systems are also being developed in Spain, Britain, France and Germany.

Social and scientific benefits forces – driven by non-commercial benefits related to

environment protection, civil protection, emergencies, scientific and research activities.

The European Union is promoting eCall technology to reduce the number of roadway

fatalities by minimizing the response time when an accident has occurred. eCall is a

combination of an In Vehicle System (NS), a device with a GSM cell phone and GPS location

capability, and a corresponding infrastructure of Public Safety Answering Points (PSAPs).

When the device detects an accident it automatically calls a PSAP, transmits the vehicle

location and other data. The European Commission has presented a policy document with a

strategy for introducing eCall in all new vehicles across Europe by 2014. This could create a

market for 200 million receivers assuming that this application will become mandatory across

the EU and so by 2022 most vehicles will have it installed (assuming an average vehicle life of

8 years in Europe).

The United States Enhanced 911 (E-911) emergency service takes advantage of GPS

positioning on GPS-enabled cell phones to zero in on a caller's location. By autumn 2012 all

wireless carriers in the US must comply with Federal Communications Commission’s (FCC)

strict location accuracy standards. As a result of this, In the US, nearly all new handsets are

GPS capable.

9 J.P. Morgan Europe Equity Research, Location, location, location: Analyzing Location Based Services

opportunities, June 2009 10

http://gpsmonitoring.com/blog/?p=349

10

3. GPS Technology Market and Trends

3.1. GPS chipset miniaturization and falling prices

The progress made in silicon technology allows for size reduction, power consumption reduction, and

integration of additional functionalities in the receivers.

Adoption rate for GPS technology has been hindered by cost, but falling chipset prices have increased

volume and market scope. Miniaturization and receiver advances are improving prices vs.

performance and favor its use in portable devices. This means that more phones and cars are

including GPS, and the technology is growing in consumer popularity. Average price of a GPS chipset

has fallen from $11 in 2003 to $3-$3.50 in the end of 2008. Application shipments for electronics

capable of GPS reached 291.3 million units in 2008. Growing at a compound annual growth rate of 27

percent, shipments could reach nearly 770 million units by 2012.

Figure 3 Average price of a GPS chipset and unit sales of GPS capable electronics

Source: SIRF estimates

3.2. GPS enabled handsets in navigation markets

Currently, the available navigation solutions on the consumer market can be divided into two broad

groups, integrated in-vehicle systems and handheld or portable systems.

In-vehicle systems can in turn be divided into OEM systems and aftermarket standard systems that

are integrated with car’s audio system. The handheld or portable systems can be divided into three

segments: dedicated navigation devices usually called personal navigation devices (PNDs), systems

based on smartphones and systems based on personal digital assistants (PDAs). Up until recent years

the consumer GPS device market has been driven mainly by the sales of dedicated personal

navigation devices (PNDs). These can either be in the format of a normal handheld computer with an

0

50

100

150

200

250

300

350

400

450

500

0

2

4

6

8

10

12

2003 2004 2005 2006 2007 2008 2009 2010

Sale

s o

f G

PS

en

able

d d

evi

ces

(mln

un

its)

Pri

ce o

f a

GP

S C

hip

set

($)

Price of a GPS chipset Sales of GPS capable electronics (million units)

Mass market adoption

11

integrated GPS receiver, or formats more suited for attaching on the dashboard of a car. Although

there is a trend of moving away from simple dedicated PND systems, these devices are still mainly

specialized for navigation purposes only. This has meant that contribution of GPS navigation systems

and products in the consumer space has been limited to mapping driving routes, tracking hikers and

marking coordinates.

Largest producers in the dedicated PND segment include US based Garmin, TomTom NV of

Amsterdam, Netherlands and Magellan. TomTom claimed it grew its PND market share in both North

America and Europe to 19 percent and 44 percent, respectively, up from 18 percent and 42 percent

during last year’s first quarter. Garmin’s market share stood at over 50% in North America. Garmin’s

global market share was 37% in 2008, TomTom held 24% of the total PND market worth about $9.44

billion according to financial reports of the largest producers.

PND market has seen incredible growth rates over the past couple of years (average global unit sales

growth of 60% over the period of 2005-2008). However the growth will probably start to slow

substantially as the market share of PNDs is expected to get disturbed by the availability of GPS-

enabled handsets or smartphones that will account for an estimated 87.8% share of the total GPS

market by the end of 2012. This trend towards GPS enabled handheld devices and navigation

software solutions accessed on smartphones is accompanied by a shift to a more service-oriented

business model in the GNSS marketplace.

This transition will not come overnight, but industry momentum is clearly shifting in this direction.

According to forecasts stand-alone PND unit sales will peak in 2009 and gradually decline with time.

Ultimately consumers will see less need to buy PNDs when their smartphones offer the same service,

even if the smartphone navigation experience is not quite as robust as that of the PND (e.g. smaller

screens on smartphones). PNDs will probably not go away entirely, but will increasingly be relegated

to a much smaller niche.

Changes in the portable GPS and personal navigation device (PND) markets are clearly illustrated by

Garmin’s and TomTom’s financial reports. In the second quarter of 2009 Garmin sales tumbled 27

percent to $669 million from $912 million during the same period a year ago. TomTom reported

revenue of $515.2 million, a decrease of 24 percent from $679 million during the same quarter last

year.

Largest PND market players are clearly looking to capitalize on this new trend. Garmin is set to enter

the smartphone market in Q3 2009 with a set of nüvifone branded handhelds. Garmin nüvifone G60

will be available beginning October 4 for AT&T customers in U.S. The Garmin hopes its phone will

create a growth area beyond its mainstay personal navigation devices segment, and possibly create a

niche of devices positioned as GPS-centric handsets.

3.3. Auto, mobile and handheld segments important in navigation market

While Garmin’s four product segments have remained the same over the years, the contribution

each makes to top and bottom line results have not. As customer demands have evolved, and as

Garmin has launched new products, its revenue and income mix has changed.

12

The auto/mobile segment has grown in importance for Garmin, contributing nearly 73% of

Garmin’s revenues in 2008 and about 58% of its income. However, gross margins in this

segment fell 5.5 percentage points from 2005 to 2008. That negative trend was offset by

increasing margins in the other three segments. Looking forward, the margins will certainly continue

to compress in the auto/mobile segment due to competition from the handset market, eventually

settling in the 32-35% range.

Segment Performance

FY2005 FY2008

Auto/ mobile

% of Revenue 39.2% 72.6%

Gross Margin 44.0% 38.5%

% of Income 33.7% 57.7%

Aviation % of Revenue 22.3% 9.3%

Gross Margin 66.2% 67.3%

% of Income 26.7% 15.2%

Marine % of Revenue 15.4% 5.9%

Gross Margin 51.2% 54.5%

% of Income 15.2% 8.4%

Fitness/ Outdoor

% of Revenue 23.1% 12.2%

Gross Margin 52.7% 57.7%

% of Income 24.4% 18.7%

13

3.4. Handset market – location based services adoption, applications

driving sales

Canaccord Adams handset survey (conducted February 2009). 40 respondents including carriers,

retailers, and partners like T-Mobile, Best Buy, Sprint and AT&T from the US, UK, Germany and

France.

What new services are customers asking for? GPS remains the most requested feature among buyers

at 18% (20% previously).11

2008 was the breakout year for GPS in mobile phones. In 2009 GPS will begin to penetrate into a

range of vertical markets, such as cameras, laptops, sporting equipment and first responder radios.

This will help to drive GPS chip shipment growth of over 25% year-on-year.

While global mobile handset shipments fell 13 percent year-over-year in the first quarter of 2009 –

the fastest fall rate in the industry’s history, GPS-enabled phones will climb to 300 million units for

the year, an increase of 25% over 2008. Strong performance will be driven by the ongoing demand

for feature-rich smartphones. Although slowing slightly in 2009, demand for smartphones, a group

that includes the Apple iPhone 3G, RIM’s BlackBerry devices, and Nokia N series phones among a

growing list, will increase at an average annual unit shipment rate of 19 percent through 2014.

During the period, GPS chipsets will continue to penetrate this segment; nine of every ten

smartphones will contain GPS chips in 2014, compared with one in three in 2008.

Handset vendors will increasingly leverage mobile applications to drive handset sales especially for

higher-end, higher-ASP (average selling price) and richer margin handsets. As handsets increasingly

serve more purpose than just voice and text communication, the ability to customize what the

handset can do for the user by the user will become important. Retention of customers is the other

big driver – a user is less likely to switch from an iPhone to a Nokia device after having customized

11

http://www.canaccordadams.com/NR/rdonlyres/C8F3D7AD-426B-42B5-BE8D-5FC3FB59233A/0/Feb2009HandsetSurvey.pdf

14

the handset with all his/her favorite applications and is very unlikely to forego any paid applications.

This is even more important today when replacement handsets account for 59% of total handset

sales (2008) up from 55% in 2007, and are expected to increase to 67% by 2010.

Differentiated service and software rather than only the hardware is already impacting market share

changes in the high-end space. Nokia has lost 10 percentage points (pp) of share in the converged

device space in 2008 vs. 2007 while Apple and RIM together have gained 11 pp. One of the attractive

features of using the iPhone, besides the capacitive touch screen, is a very large selection of

useful/entertaining applications that utilize handsets technological capabilities, including location

awareness.

Figure 4 Annual shipments of GPS-enabled handsets, million units, 2008-2014

3.5. Growing demand for precision GNSS

Precision GNSS equipment capable of accuracies of less than 10cm are used in a steadily growing

number of applications including land, marine and aerial surveying, structural monitoring of dams,

bridges and buildings, earthquake/tsunami warning systems, atmospheric and meteorological

research, space craft navigation and machine control systems for cargo handling, agricultural and

earth moving equipment.

Precision GNSS is rapidly developing from a niche technology for scientists and surveyors to an

essential productivity tool in globally important industrial sectors such as mining, agriculture and

construction. These milestones include the value of precision GNSS systems used for industrial

applications such as machine control in agriculture and civil engineering exceeding that of precision

GNSS for traditional uses such as surveying and science for the first time.

The precision agriculture segment has been performing well, showing double digit growth rate over

the past 5 years, and remains a leading driver for precision GNSS equipment market. Despite good

value proposition and healthy growth, the market remains well under penetrated. In North America,

less than 30% of farms greater than 200 hectares use guidance systems and less than 5% utilize auto-

steering devices.

15

Market for auto steering solutions harnessing precision GPS technology is large, with 3.5 million

tractors and combines in North America alone. OEMs are producing around another 100,000 new

tractors (40+HP) in the United States per year. About 20% of these are GPS equipped.12

In Europe over 150,000 new tractors are sold every year and only 8% of them are currently equipped

with GNSS-enabled receivers, a share that is forecast to rise to 13% in 2012. In addition about 4% of

the tractors being used have been retro-fitted with GNSS receivers.13

4. GNSS Services Markets and Market Trends

4.1. Land Applications, location based services (LBS)

By the beginning of 1990’s GPS receivers for land uses became affordable and commonplace. It

started with vehicle tracking and navigation and with handheld receivers used for hiking, data

collection, and general recreational pursuits. By 2003, the receiver box evolved into a chipset and

now even into a single chip; the prices dropped so dramatically that GPS capability could be

embedded into almost any other kind of electronic device.

The ease and low cost of adding GPS functionality opened up new possibilities and spurred many

companies to offer products and services that were heretofore either too expensive or too complex

for the average consumer.

Growth in new services was especially boosted by symbiotic relationship between GPS navigation

and different communication technologies. With the availability of the Internet, Wi-Fi, and satellite

and cellular links to communicate with GPS-equipped users, mobile location based applications

harnessing many different business models began to appear in the beginning of 2000s. In an

explosion of growth, the number of GNSS users on land has far outstripped all other users combined.

Essentially, every vehicle owner and every cell phone user has become a potential customer. This has

put the ultimate number of GNSS receivers that could be sold into the billions.

The concept of location-based services using mobile phones has been around since the late 1990s.

Its genesis was the Wireless Communications and Public Safety Act of 1999 (911 Act) by the United

States Federal Communication Commission (FCC), usually referred to as the E911 Mandate. The Act

mandated that beginning in 2001, American wireless operators offer some way of locating mobile

customers when they dial 911 (the national emergency number that connects callers to emergency

dispatch personnel) from their mobile phones. Even before the act was formalized, many in the

industry recognized that the same technology to be used for locating people in emergency situations

would also have commercial applications. In fact in the North American market, wireless carriers

have acted as the main channel for nascent consumer LBS sales, leveraging the location

infrastructure they had to create earlier this decade to address Federal E-911 mandates.

Location based services can be divided into consumer and corporate segments. Most commercial

location based applications have revolved around tracking and navigation services, to enable workers

12

Source: Fraser Mackenzie Equity Research 13

http://www.gsa.europa.eu/go/news/egnos-for-agriculture-providing-high-precision-at-a-low-cost

16

to more efficiently plan their routes and to support dispatch services. Asset tracking, too, is an

important LBS application. Although most of commercial services make use of specialized GPS

modules, there is a clear trend towards utilizing GPS equipped handsets for commercial applications

as well.

While consumer-based services have been slower to come to market, many operators throughout

the world now offer some LBS services. Community and entertainment services that are marketed

towards consumer market comprise location enabled chat and messaging applications, games,

friend-finder services and other services primarily designed for leisure or social contacts and

networking. Information services include local search services like “find the nearest” and other

applications that provide localized information based on the user’s position. Navigation services

incorporate all applications aimed at giving directions for drivers or pedestrians by displaying maps

and instructions on the handset display.

Although the LBS services for the consumer market have been around for several years, applications

are now poised for strong growth due to several key drivers. One of the major drivers for location

based services all over the world includes the need on the part of mobile carriers to drive non-voice

revenue in the face of falling voice ARPU (average revenue per user). GPS-based LBS services are

seen as perfect opportunity for generating more mobile internet traffic and creating value-added

non-voice services which would increase subscriber ARPU.

Another important impetus for LBS services has been the growing popularity of GPS-equipped

smartphones and even more importantly the rise of several viable device “ecosystems” which have

become essential outlets for third-party companies and software developers. Significant software

markets have recently developed or are developing for Apple iPhone, Google Android, RIM

Blackberry, Nokia S60 and Palm Pre devices. Especially the Apple’s highly successful launch of its

iPhone in 2007 and associated App Store in 2008 has led other handset vendors and mobile

operators to introduce similar services, which is expected to bring about significant uptake of mobile

applications, including location-enhanced applications, among mainstream mobile users.

There are now (as of autumn 2009) over 2,500 location-based applications available in the iPhone

App Store and close to 400 location-aware applications available in the Android Marketplace. The

most popular type of location software in both stores is Travel, followed by Social Networking. The

Blackberry App World that serves RIM Blackberry devices has 57 location-aware applications.

ThemostpopularcategoriesarecurrentlyTravelandProductivity & Utilities.

The number of European users of mobile location-based services is expected to grow from 20 million

users in 2008 at a compound annual growth rate (CAGR) of nearly 37 percent to reach 130 million

users in 2014. Local search, navigation services and social networking are believed to become the top

applications in terms of number of users. Worldwide, the user base of LBS services will be growing to

486 million by 2012, up from 18.9 million in 2007 and 63 million in 2008.

17

Figure 5 European users of mobile location-based services, 2007-2014

Source: Berg Insight, Mobile Location Based Services 2009

The key enablers for LBS are rapidly falling into place. On-device application stores allow easier

access to mobile services for a broader audience at the same time as flat-rate data plans make

pricing more transparent. In conjunction with more operators opening their location platforms to

third parties, location aggregators have started to provide common application programming

interfaces (APIs) for accessing location data from multiple operators. This together with ever growing

GPS handset sales will allow more application developers to create location-enabled mobile

applications. It is estimated that 20 percent of mobile handsets shipped in 2009 will feature GPS and

that the installed base in Europe will surpass 50 percent of total handsets already in 2013.

With the exception of search and information as well as social networking services that are likely to

become predominantly ad-funded, many other service categories, notably tracking and most

navigation services can be expected to remain premium services. However, besides monthly

subscriptions and per-use fees, service providers increasingly offer one-time fees, service bundles or

device bundles to match consumer expectations.

4.1.1. Navigation

The first personal navigation systems were introduced in the 1980s for use in cars. These were based

on compass and gyroscopes since GPS was not available for civilian use at the time. At the beginning

of the 1990s, the first GPS based vehicle navigation systems became available. The rapid

advancements in micro electronics have since enabled new applications for personal navigation

systems, such as handheld devices with integrated maps.

Modern specialized consumer GPS receivers come in form of Portable Navigation Devices (PND)

which combine positioning capability and navigation functions. Personal Navigation Devices (PNDs),

i.e. transferable devices with integrated GPS receivers and digital maps, have in recent years gained

large scale mass-market acceptance. In Europe, PND shipments grew to 18.1 million units in 2008,

up from 16.5 million units in 2007. In North America, very strong sales resulted in remarkable growth

0

20

40

60

80

100

120

140

2007 2008 2009 2010 2011 2012 2013 2014

Mill

ion

use

rs

18

in 2008 – in total about 18 million units shipped, compared to 11 million in 2007. Booming personal

navigation device market is expected to grind to a halt in 2009 with little or no growth expected in

most regions – global unit sales are estimated to come in at 39 million units. This means that year-

on-year growth will be slowest in five years.

The personal navigation value chain comprises three principal categories of players. These are map

data providers, navigation solution providers and device manufacturers. In many cases, dynamic

content providers and mobile operators are also involved. Digital map data for the personal

navigation market are today available from two dominant players. Navigation software is available

from numerous providers developing products for several hardware platforms.

PND manufacturers

While there are over 100 PND brands on the market in Europe and North America, personal

navigation device market is ruled by two manufacturers – Garmin and TomTom, who together share

61% of the PND market worth about $9.44 billion in 2008 according to financial reports of the largest

producers. The business models of major navigation device producers are based on designing,

manufacturing and marketing GPS enabled navigation, communication and information devices.

This transition from PNDs to smartphone navigation will not be easy for Garmin and TomTom as their

core revenue base will likely shrink, but this process will take some time. TomTom likely has more

financial strength to weather this transition. At heart, TomTom has a core competency in marketing

and design, and their software offerings stand to do well as a featured application in smartphones.

TomTom also outsources its PND manufacturing, a model which should allow for them to scale down

in a declining PND market.

By contrast, Garmin’s core competency rests in hardware manufacturing an area which will be hit

hardest with the shift to smartphone and software offerings. Garmin’s answer to the smartphone

threat has been to jointly develop their own smartphone with original design manufacturer (ODM)

Asus. Garmin Asus nüvifone is unlikely to meaningfully alter the company’s trajectory. The device is

late to market and shows no signing of generating significant volume any time soon. Moreover, in

this field Garmin is competing against several far larger vendors. Success in the smartphone industry

is dependent on operating system platforms and developer interest. Garmin’s OS strategy appears to

be fragmenting, with pledged support to their own proprietary OS, Microsoft’s Windows Mobile and

potentially Google’s Android. This trend will leave Garmin exposed to many forces beyond their

control.

Map providers

Two companies – Netherlands-based Tele Atlas NV owned by TomTom NV and the Chicago-based

Navteq Corporation owned by Nokia, are responsible for supplying data to all major digital mapping

and navigation services in the world.

Nokia Corp. struck a deal to buy Navteq in October 2007 for $8.1 billion, with plans ultimately to use

maps as a cornerstone for selling ads tied to a cellphone user's location. A month later portable GPS

device-maker TomTom beat out rival Garmin in a bidding war for Tele Atlas, with a $4.2 billion offer.

Neither bid could be justified by the financial performance of the companies – Navteq was modestly

19

profitable while Tele Atlas was losing money – but according to analysts buyers were willing to pay a

"strategic premium" because of the value of mapping data to all players in the GPS industry.

Nokia’s acquisition of Navteq shows how serious handset manufacturers are about entering the PND

market and how the development of mobile location-based services can turn many handsets into

cost effective alternatives to in-vehicle navigation systems and personal navigation devices. As of

June 2009 most Nokia smartphones already are location-enabled, and free access to Navteq’s map

database has allowed Nokia to effectively contend with the likes of Garmin and TomTom.

All Nokia location-enabled are currently supplied with pre-installed version of Nokia Maps service,

that offers most if not all the functions that are included in majority of the modern specialized PND

devices and additional functions that are enabled by mobile internet connections. Maps service

includes travel guides, real-time updated maps, points of interests, and traffic information, plus the

expected turn by turn navigation, and more. Nokia Maps is currently the only service of its kind, but

nevertheless could seriously hurt the position of PND manufacturers as Nokia shipped 60.9 million

smartphones in 2008 for a total market share of 43.7 percent. Full Nokia Maps service license,

covering all regions of the world, currently costs €129.99 for one year. Walking licenses for one

country maps data start from €4.99 for one month of service.

Smartphone platforms

Navigation software is today available on most large smartphone platforms. Apple has preinstalled a

Google Maps application on their popular iPhone handset. Google Maps is also available on all

Google Android smartphones. Google Maps on mobile platforms offers most of the functionalities

that are available with Nokia Maps and is free to use. The main difference lies in the fact that unlike

Nokia Maps, Google Maps does not allow users to download maps into their handsets, so it requires

a data connection of some kind to function.

Operator-branded white label navigation solutions are also supplied by major cellular carriers.

Largest mobile carrier in US, Verizon Wireless offers VZ Navigator GPS navigation software that is

compatible with most of its GPS handsets. The service costs $2.99 per day or $9.99 per month. VZ

Navigator will not incur data transfer charges, to download updates to the software, maps updates,

routes or re-routes. The software is based on Networks In Motion, Inc. mobile platform.

UK’s leading mobile network operator Vodafone is offering Vodafone Find & Go Sat Nav service in

Britain. The service, launched in February 2008, provides users with both in-car and pedestrian

navigation. It features 3D maps, live map updating, live traffic alerts and points-of-interest data. The

subscription to the service costs GBP 5 per month. When using the service data charges apply.

Service is based on Telmap Ltd. Navigator application.

20

Figure 6 Evolution of portable navigation devices

Perspectives for PND market

Map data is currently 75 percent of the cost of a specialized PND device. As portable navigation

system revenues and prices have been in freefall for the past 12 months, whereas map data prices

have stayed constant, the profit margins on PND manufacturers have fallen considerably. Shrinking

profits, low-cost competitors, and especially the rise of the smartphones have forced PND producers

to re-think their entire business models.

PND vendors are increasingly looking at service revenues as device revenue growth slows. In Europe,

total device revenues peaked in 2007 and revenues in North America peaked in 2008. In order to

make navigation services useful in everyday situations for more people, introducing wireless

connectivity to PNDs can enable integration of online services such as local search, enhanced traffic

information and automatic map updates. Many in the PND industry at the same time remain

skeptical about the potential of connected PNDs to become strong enough to salvage the market.

According to these arguments consumers want more than the standard PND, but they are not willing

to pay a whole lot of money for it. This opens up further opportunities for the handheld market as

GPS related components represent a marginal part of the overall cost of the smartphone.

Vendors are also adding new features and refining the user interface to facilitate command and

control, as well as improve the information presentation. New models will, for instance, gradually

introduce automatic speech recognition technology, 3D map features and photo-realistic textures.

21

New features and services will likely be crucial for convincing existing customers to upgrade their

existing devices to more advanced models.

4.1.2. Tracking & fleet management services

There are several types of tracking services for both consumer and corporate customers. A basic

distinction can be made between asset and people tracking services. People tracking services can be

used to locate elderly and children, or be used as portable alarms. Asset tracking services are used to

locate objects such as cars, courier shipments and similar. In contrast to people tracking services

privacy issues are less of a concern for asset tracking services. For corporate clients there are also

fleet management services and workforce management services available. These services are mainly

marketed as productivity enhancement services. Most tracking services need indoor coverage to be

useful, but the position accuracy needed varies depending on the specific application.

Tracking services are most widely used by corporate customers. Corporate market also generates the

majority of revenues for tracking services segment of the GNSS market. An increasing number of

businesses are deploying location-enhanced applications for asset tracking, fleet management and

workforce automation. There is also a market for tracking services among consumers, even though

this segment will be of relatively smaller value.

According to research firm Gartner, European corporate tracking services market, including fleet

management, was worth around €170 million and is estimated to reach €323 million in 2010. The

automotive telematics market (corresponding today mainly to a security devices for tracking stolen

vehicles) is a market in full expansion. It represented around €75 million in 2006 and is estimated by

Gartner to reach €105 million in 2010.

The European consumer tracking market, including asset tracking and services for tracking elderly

and children, is expected to be worth €18 million in 2009 and reach €40 million by 2010.

Asset and personnel tracking

Due to their activities, many companies have a large number of valuable assets in faraway places.

Keeping track of assets such as trailers or construction equipment is intricate, but using an asset

management system can optimize operations and minimize theft and misuse. There are numerous

systems available to monitor asset location based on GPS or mobile network location. Vehicle-

tracking solution companies are introducing new products that provide multiple functions including

location, security etc. Another popular function is geo-fencing where the system has defined a virtual

area where an asset should be located and triggers an alarm if the asset leaves that area. Companies

are implementing some or all of the above solutions, which all have one thing in common – they all

need wide area mobile connectivity to link the information generated by these devices to head

office. Indoor coverage is also useful. Tracking services are also marketed towards consumers, for

instance for tracking of stolen vehicles.

Many companies, such as security companies and other companies with many field workers, can

benefit from a work force management system. Systems integrated into handhelds typically enable

workers to send messages, status updates and positions to the company enterprise system. The

workforce manager can send back messages, view workers on a map, as well as give routes to new

sites. Security functions such as alarms are also part of the service.

22

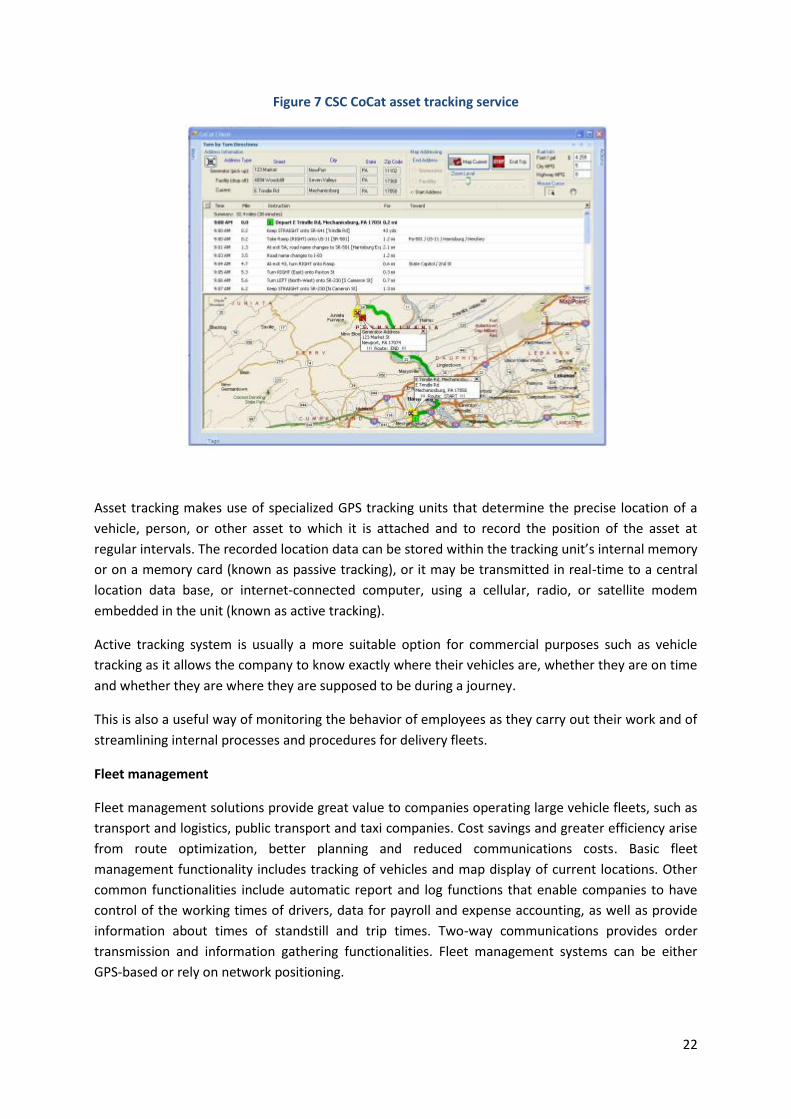

Figure 7 CSC CoCat asset tracking service

Asset tracking makes use of specialized GPS tracking units that determine the precise location of a

vehicle, person, or other asset to which it is attached and to record the position of the asset at

regular intervals. The recorded location data can be stored within the tracking unit’s internal memory

or on a memory card (known as passive tracking), or it may be transmitted in real-time to a central

location data base, or internet-connected computer, using a cellular, radio, or satellite modem

embedded in the unit (known as active tracking).

Active tracking system is usually a more suitable option for commercial purposes such as vehicle

tracking as it allows the company to know exactly where their vehicles are, whether they are on time

and whether they are where they are supposed to be during a journey.

This is also a useful way of monitoring the behavior of employees as they carry out their work and of

streamlining internal processes and procedures for delivery fleets.

Fleet management

Fleet management solutions provide great value to companies operating large vehicle fleets, such as

transport and logistics, public transport and taxi companies. Cost savings and greater efficiency arise

from route optimization, better planning and reduced communications costs. Basic fleet

management functionality includes tracking of vehicles and map display of current locations. Other

common functionalities include automatic report and log functions that enable companies to have

control of the working times of drivers, data for payroll and expense accounting, as well as provide

information about times of standstill and trip times. Two-way communications provides order

transmission and information gathering functionalities. Fleet management systems can be either

GPS-based or rely on network positioning.

23

Stronger focus on cost efficiency is the main driver of fleet management market. It is expected that

penetration rate for fleet management in Europe will continue to increase in 2009 and 2010. The

number of fleet management systems in active use is forecasted to grow at a compound annual

growth rate of 20.5 percent from 1.1 million units at the end of 2008 to 3.3 million by 2013. The

penetration rate in the total population of non-privately owned commercial vehicles is estimated to

increase from 3.1 percent in 2008 to 9.3 percent in 2013. In the US currently nearly 1.9 million GPS

devices are used to monitor fleet vehicles, trailers, construction equipment and mobile workers.

Figure 8 Installed base of fleet management units (EU27+2, 2007–2013)

Source: Berg Insight

A diversity of international aftermarket solution providers compete for the top positions on the

European market. These include specialists such as Cybit, Minorplanet, Navman Wireless and

Trafficmaster from the UK, Masternaut from France, Digicore and MiX Telematics from South Africa

and Punch Telematics and Transics from Belgium, as well as the large corporations GE and

Qualcomm. The navigation vendors TomTom and Garmin are also active on the market, employing

strikingly different strategies. Trimble is a new entrant on the European fleet management market

but has a leading position in North America following the acquisition of @Road in 2007. Masternaut

is ranked as the largest player overall in terms of installed base with 100,000 units deployed, mainly

in France and the UK, while Transics is ranked as number one in the heavy trucks segment with about

55,000 units installed. All major truck manufacturers on the European market offer OEM telematics

solutions as a part of their product portfolio. Mercedes-Benz, Volvo and Scania launched their first

products in the 1990s and followed by MAN in 2000, Renault Trucks in 2004, DAF Trucks in 2006 and

IVECO in 2008.

24

Companies offering tracking and fleet management services

Masternaut

http://www.masternaut.co.uk/

Masternaut, founded in 1997, is the European leader in fleet management and asset tracking with

more than 100,000 equipped vehicles for 5,000 clients all over Europe. The company, which is based

in France and has a most significant presence in France and UK, has experienced rapid growth in

business and recorded a turnover of more than 31 million euros in 2007, rising to over 40 million in

2008. In March 2009 Masternaut was acquired by Hub télécom, the specialized telecom division of

Europe’s second largest airport group Aéroports de Paris. In the UK, Masternaut solutions are sold

through an independent business partner: Masternaut Three X.

Masternaut offers large range of vehicle and asset tracking services, mobile workforce applications,

and a range of back office, business intelligence and business management applications.

Vehicle and asset tracking services provides extensive visibility of vehicles including engine on/off

times, vehicle location, journey start times, speed, journey duration and journey end times as well as

idling. Alerts can be established to draw attention to specific circumstances associated with tracked

assets. These customizable alerts include out-of-hours vehicle usage, excessive speeding, vehicles

travelling outside pre-defined areas or late departures from appointments.

Mobile workforce services include a set of solutions that give real-time visibility of workforce. Mobile

workforce services also include satellite navigation application that comes integrated into central

tracking solution. A separate lone worker communication wearable device and service “Lokate” is

offered. It gives insight into location and historical movements of lone workers, allows sending alerts,

SMS messages and making telephone calls.

All Masternaut’s tracking solutions are fully-managed and operate through dedicated web-portals so

there is no investment in hardware needed or software installation required for clients and regular

automatic updates are included in the service. Geographic and location-based information for all

services is visualized using Microsoft’s Bing Maps for Enterprise platform.

Masternaut vehicle and asset tracking and mobile workforce services are priced by user. Prices range

from €25-€135 per vehicle or user per month. Lokate GPS watch costs £295.00 (€355) plus £14.95

(€18) per month subscription fee.

Cybit

http://www.cybit.co.uk/

Cybit is one of Europe’s leading providers of real time GPS vehicle tracking, fleet management tools

and mobile workforce tracking systems. Company currently provides tracking for 46,000 vehicles in

2,000 fleets. In 2008 company revenues were up 48% from £13.3 million (€16 million) in 2007 to

£19.7 million (€23.6 million).

Cybit Fleetstar range of services is divided into three groups – Field Service Management, Transport

& Logistics, and Public Sector & Utilities. Field Service Management services provide tools for

25

managing a mobile service workforce by providing access to real-time information about employee

locations and activities. Transport & Logistics services provide advanced fleet tracking and reporting

solution, with additional modules enabling advanced and user driven reporting, automatic links to

power take off, integrated satellite navigation and duty of care and data analyzer modules. Public

Sector & Utilities services are specifically designed to provide organizations delivering service into the

public arena with visibility of their mobile operations and vehicle fleet.

Fleetstar is a modular system that enables functionality to be added as and when usage develops or

your circumstances change. These enhanced options are available as a system upgrade on the

existing Fleetstar platform. No additional hardware or installation is required and modules are fully

configurable to individual business requirements. All Cybit services are fully-managed and accessed

through an internet-based platform.

Cybit Fleetstar tracking services are priced from £1.20 (€1.44) per vehicle per day.

Computer Sciences Corporation, CSC

http://www.csc.com/government/offerings/11054/20217-omnilocation

Computer Sciences Corporation (CSC) is one of the leading providers of management consulting and

IT services. The company is one of the leading outsourcing solutions providers in the world. It has a

strong position in providing IT services to government customers and is a top 10 federal contractor in

the United States. The company primarily operates in the US and Europe. Other international

operations of the company are in Australia, Asia and Canada. The company is headquartered in Falls

Church, Virginia and employs 89,000 people. The company recorded revenues of $16,739.9 million

during the financial year ended March 2009 (FY2008), an increase of 1.5% over 2008.

CSC’s wide range of services includes OmniLocation suite which is a set of safety location systems for

tracking people, vehicles, materials and assets. OmniLocation integrates location-based systems

data, such as GPS and RFID, with static and dynamic information about people, equipment, vehicles,

assets and infrastructure. Organizations can monitor the real-time location and status of assets in

motion or at rest through a single, interactive, real-world Web interface using Google Earth products

and Web 2.0 methods. In addition, the interface can integrate multiple location and mobile asset

tracking systems, including inventory management, vehicle tracking, access control, and status and

maintenance schedules of infrastructure.

The OmniLocation suite, launched in June 2008, includes three offerings that address a range of

location requirements: LOFT (Location Object Field Tracking), LISA (Location Intelligent Safety

Application) and CoCAT (Chain of Custody Asset Tracking).

OmniLocation’s LOFT solution is designed to help organizations visualize, protect and account for

mobile assets including lone workers (e.g., pipeline inspectors) and vehicles in the field. LOFT has

been used in 2007 and 2008 Tour of California and Tour de France professional cycling races, giving

cycling fans a “bird’s-eye view” of the race by tracking riders online during the race.

LISA enables organizations to visualize people, vehicles and assets that are moving or dispersed

throughout a facility. The solution integrates indoor (RFID) and outdoor (GPS) location information

data, object attributes, communications, and context and association information to track, map and

26

model enterprise operations in real-time. LISA combines situation awareness with location

information to help improve safety and security, prevent accidents and can be used to account for

personnel in an emergency.

Figure 9 CSC Omnilocation iPhone client for tracking Tour de France riders

CoCAT provides companies with reliable accountability and a visible chain of custody during the

transportation of high value, hazardous or dangerous materials to help eliminate fraud and comply

with materials handling legislation. The solution combines fleet, asset and identity management, and

biometrics with location tracking information (GPS and RFID) to verify and monitor truck, trailer,

driver-custodian, shipper and receiver authentication.

4.1.3. Traffic management & public transport

Nowadays, sensors installed at selected traffic intersections are the main means of determining the

current traffic situation in real time in a large conurbation. The quality of the data depends mainly on

the number and spread of the systems installed.

In US the largest commercial traffic analysis network is operated by Navteq with over 4,000 lane

kilometers of sensors. In total the United States highway network consists of 6.4 million kilometers of

roads and streets. All commercial and federally managed sensor systems combined currently cover

less than 0.2% of the total US highway network. As a rule, the available investment budget limits the

quantity of sensors. Expensive cost of the sensing networks means that traffic information is usually

only available for busy highways in large metropolitan areas, but it's missing on arterial roads feeding

into these highways or on rural secondary roads. Thus the quality of the traffic information is

adversely affected by the small number of deployed monitoring sensors.

On the other hand, due to the recent advance in embedded techniques and wireless networks,

mobile devices with powerful computation, comparatively large storage, localization and wireless

27

communication capabilities are becoming increasingly popular. Alone in 78.0 million GPS-enabled

handsets were sold globally and shipments are forecasted to reach 770 million units in 2014.

In by utilizing GPS techniques, these powerful mobile devices can easily obtain the GPS information

in which the location of users and the speed are now available for navigation services or location-

based services. Data collected from mobile GPS devices provides access to real-time information on

traffic flows, crashes and travel time to help drivers anticipate delays. This traffic information

represents substantial value to the US economy as each year congestion costs $78 billion in delays

and wasted fuel, according to a report from the Texas Transportation Institute, a research arm of

Texas A&M University.

The use of GPS technology in public transportation such as buses and taxis is also increasing rapidly.

By equipping public transport vehicles with GPS transmitters, their location and speed can be

constantly tracked and this information turn is used to display estimated time of arrivals at street-

side bus stops. Tracking taxi cabs with GPS can yield significant cost savings and customer

satisfaction. When a call for a cab comes in the dispatcher can use a GPS tracking system to locate

the cab nearest to the pick-up. This saves not only vehicle miles but the customer also gets picked up

faster and to his destination happier.

Electronic satellite-based toll collection technology has advanced to the forefront of the discussion

on highway finance as policy makers seek a stable revenue source for funding maintenance and

construction of the highways. Construction costs have escalated and the demand for safe and

efficient highways has steadily increased all over the world. Highway capacity has increased

insignificantly over past decades while at the same time vehicle miles traveled have increased

dramatically. Increasing cost coupled with decreased revenue per mile driven has caused policy

makers to move towards mileage based user fees, which are seen as an effective way for generating

additional funds for transport infrastructure.

A GPS based tolling system relies on digital maps rather that overhead gantries or embedded loops

to determine a vehicles’ location and miles traveled for the purpose of assessing a charge. There is no

infrastructure on the ground other than what is used for enforcement; the basemaps and GIS

systems serve as virtual cordons where fees are assessed. Therefore, systems must be thoughtfully

developed and extensively tested to ensure their reliability and accuracy.

Siemens and China Mobile

In August 2008, Siemens and telecom provider China Mobile launched a pilot project in the Chinese

city of Guangzhou that utilizes positional data of taxis transmitted via GPS to obtain information on

the current traffic situation.

In many Chinese cities taxi fleets are equipped with satellite-based on-board units. The original aim

of this measure was to increase the safety of taxi drivers. The system signals the position of each taxi

to a central coordinating and monitoring office. The taxi can be located at any time thanks to the

positional data obtained via GPS.

During the project positional data of the more than 17,000 taxis are recorded every 20 seconds and

processed. The time, current position of the taxi, its direction of travel and its current speed are

recorded. Given that the taxis in the city are included in the normal flow of traffic on the main roads

28

– there are no separate lanes such as bus lanes – this pool of data constitutes a comprehensive

platform of information on the current traffic situation.

The data are then made available to telecom provider China Mobile who offers them to other road

users via general-access information sources such as cell phones, the web or via a hotline. The

information is also available on PDAs or PNDs (Personal Navigation Devices). This business model is

not only of interest to China, but could be implemented in all cities currently planning similar

projects.

Dash Navigation, Inc.

http://www.dash.net/

California, US based Dash Navigation was the first company to introduce internet-connected

personal navigation device to the marketplace in 2008. Dash approached traffic information

reporting in a new way - by collecting information from other people driving real commute routes,

during real commute times.

The Dash Express unit is a PND unit that can communicate back to the Internet using cellular data

networks or Wi-Fi (it contains three chips: GPS,Wi-Fi, and GPRS). Through its cellular and Wi-Fi

modems, the Dash Express delivers real-time traffic reports and monitors each of its user's road-

speed data as they travel. It reports the road-speed information to other Dash users within minutes,

creating local traffic reports, and thus providing the most up-to-date traffic information available.

Dash also added the more commonly available alerts from road sensors and other reporting sources

to supplement their network.

The quality of the traffic predictions made by Dash is directly correlated with the amount of users

providing input to the system – the more people who have the devices in a given area, the more

accurate the information.

Unfortunately, Dash couldn’t build a large user base and in June 2009 company was acquired by

Research In Motion (RIM), the Canadian maker of BlackBerry smartphones. Financial terms of the

deal were not disclosed. Dash had raised a total of $71 million in venture capital funding.

It is expected that RIM, who controls 17.4% of the global smartphone market, will use Dash’s

technology to upgrade the GPS capabilities in their upcoming devices in some capacity. Potentially,

with Dash’ technology RIM could turn its Blackberry users (28.5 million as of June 2009) into the

largest GPS network of traffic sensors not only in the US, but worldwide. This could open up totally

new possibilities for commercial traffic management applications.

Nokia and Navteq

Nokia and Navteq in conjunction with the University of California at Berkeley are currently running a

project called Mobile Millennium in the San Francisco Bay Area that uses GPS-enabled cell phones as

traffic monitors or "probes" to collect real-time traffic data14.

14

http://traffic.berkeley.edu/

29

To participate in the project volunteers with phones running on T-Mobile or AT&T's services can

register their phones and download the appropriate software through the project web site. Nokia

does not need to be the manufacturer of the hardware, but the phone needs GPS and has to be able

to run Java applications, like RIM Blackberry smartphones and Apple iPhones.

In brief, project uses anonymous speed and position information gathered by GPS-equipped cell

phones, fuses it with data from static traffic sensors, and broadcast traffic information back to the

phones.

As users drive with their phones in the car, they cross the virtual trip lines placed every quarter mile

on the Navteq maps on the program. As this happens, phone knows to send its coordinates and

traveling speed back to the engineers at UC Berkeley, who have created the algorithms to process

the data. Data is gathered only from locations that are statistically significant for traffic information.

This careful targeting minimizes bandwidth usage by collecting only traffic-relevant data, and equally

important, is privacy aware. The ultimate aim of the project is to provide drivers with current traffic

information where and when they can use it to make informed travel decisions that keep traffic

flowing.

Similarly to Dash Navigation traffic information system, the program will only work where there's a

large enough sample size to analyze. According to researchers in Nokia Research Center in Palo Alto,

Calif., the application works efficiently with only 2 percent of the drivers on the road using it.

Currently about 10,000 volunteers have joined the program.

Nokia expects a commercial offering to be available within the next two years. It's not clear yet if

Nokia will make the application available to phones other than ones made by Nokia. It's likely that

the application could be made available as part of a service offered through a wireless operator. This