globalization and its challenges - ucsc directory of ...hutch/econ143/fischerglobal.pdf ·...

TRANSCRIPT

RICHARD T ELY LECTURE

Globalization and Its Challenges

By STANLEY FISCHER

I stand here with deeply con icting emotionsI am honored to be delivering this prestigiouslecture I am profoundly sad that Rudi Dorn-busch who should have delivered the Ely Lec-ture died in July last year and that I am here inhis place So I would like to start by talkingabout Rudi

Rudi was born and grew up in Krefeld Ger-many He was an undergraduate at the Univer-sity of Geneva and completed his PhD at theUniversity of Chicago in 1971 which is wherewe met He was a student of Robert Mundelland both the subject matter (the development ofthe Mundell-Fleming model) and the eleganceand insights of his early work re ected Mun-dellrsquos in uence He taught at the University ofRochester and at the University of Chicago be-fore accepting an offer from MIT in 1975

In 1976 soon after coming to MIT Rudiwrote his most famous and in uential theoreti-cal article ldquoExpectations and Exchange RateDynamicsrdquo As Ken Rogoff (2002 p 1) said inhis celebratory lecture on the 25th anniversaryof its publication ldquoThe lsquoovershootingrsquo papermarks the birth of modern internationalmacroeconomicsrdquo

From the late 1970rsquos Rudi became increas-ingly interested in policy issues Within a de-cade he had become one of the outstanding

policy economists of our time In his policywork he displayed the same rare talent as he hadin his theoretical work of being able to extractthe essence of a complicated problem and ex-plain it in terms that made it seem simpleAmong his policy papers the most famous isthe 1994 Brookings paper with AlejandroWerner that predicted the Mexican peso crisisbut that is only one of many applied papers thatrepays rereading

As his policy interests grew Rudirsquos famespread He was an indefatigable global travelerspeaker and writer and a frequent columnist Inhis more popular articles in his columns and onthe podium his wit and the speed of his mindmade him an exciting and formidable presenceHe was one of the nest debaters and polemi-cists in the profession He was tough and did notshy away from stating his views often in waysthat re ected the advice of Keynes ldquoWordsought to be a little wild for they are the assaultof thoughts on the unthinkingrdquoAt various timeshe was persona non grata to the authorities in anumber of countries it did not help that moreoften than not he was right

Despite his public persona Rudi was anexcellent con dential policy adviser When Iwas at the IMF I often called him to discussa dif cult situation His advice was alwaysthoughtful typically nuanced and frequentlyprovided insights that no one else had seenmdashand he was willing to talk as long as it took

Rudi played a central role in the MIT Eco-nomics Department He was a spectacularlysuccessful teacher in the classroom in super-vising theses and through his textbooks But hedid not spoonfeed the students sometimes po-sitioning himself in front of an unfortunate stu-dent asking a series of questions until heextracted an answer Nonetheless he won manyprizes for teaching Every outstanding Ameri-can international macroeconomist who has been

Citigroup 399 Park Avenue New York NY 10022-4614 (e-mail scherscitigroupcom) This is a revisedversion of the Ely Lecture presented at the American Eco-nomic Association meetings in Washington DC on 3 January2003 The Ely Lecture was originally to have been presentedby Rudi Dornbusch who died on 25 July 2002 I am gratefulto Andrew Balls Olivier Blanchard Vittorio Corbo AngusDeaton Peter Diamond Jaewoo Lee Prachi Mishra ChiNguyen Maurice Obstfeld Ratna Sahay Lyn Squire LarrySummers and John Williamson and to my Citigroup col-leagues Lewis Alexander Eric Darwell and Dana Petersonfor their assistance and advice Views expressed are those ofthe author and not necessarily of Citigroup

1

to MIT among them Jeffrey Frankel PaulKrugman Maurice Obstfeld and Ken Rogoffwas a Rudi student And there are outstandingRudi students all over the globe many of themhere tonight many of them professional econ-omists some who became Rudirsquos co-author ona paper many who became policymakers In therichly deserved devotion of this legion of stu-dents to their teacher and friend lies the greatestcompliment to his teaching and mentoring

I had the good fortune and pleasure ofcollaborating with Rudi in the writing of twotextbooks and several articles Our textbookMacroeconomics which has sold well over amillion copies worldwide has given me asmuch satisfaction as anything else I have donein my professional life And I know Rudi feltthe same way

Rudi was a vital and positive personalitywho lit up any group in which he participatedHe was among the most talented of men andamong the warmest the most generous with histime and himself available for his students andhis friends whenever they needed him Whenthey called or visited Rudi would say ldquoTellme everythingrdquo and then give them his sympa-thy his understanding and his unsentimentaladvice

We will miss Rudi deeply including tonightfor his incisive mind the brilliance of his in-sights the exuberance of his writing and hischallenges to conventional thinkingmdashbut mostof all for his friendship and the pleasure of hiscompany

I The Globalization Debate

The debate over globalization is lively oftenpassionate and has sometimes been violent Atleast until recently it has been intensifying1

The debate is untidy and ill-de ned and onecould react by saying that it has no place in aprofessional setting like this one But we cannotafford to ignore it for the views and attitudesexpressed in it will inevitably affect public pol-icymdashand the issues are critically important forthe future economic growth and well-being ofall the people of the globe2

Here is the message Globalization theongoing process of greater interdependenceamong countries and their citizens is complexand multifaceted Many of the problems that thecritics of globalizationpoint to are real Some ofthem relate to economics Others relate to non-economic but no less important aspects of lifeAnd while some of the problems do stem fromthe process of global integration others do not

As far as economics is concerned the bigchallenge is poverty and the surest route tosustained poverty reduction is economic growthGrowth requires good economic policies Theevidence strongly supports the conclusion thatgrowth requires a policy framework that prom-inently includes an orientation toward integra-tion into the global economy This placesobligations on three groups those who are mostresponsible for the operation of the internationaleconomy primarily the governments of the de-veloped countries those who determine the in-tellectual climate which includes this audiencebut also government and nongovernment orga-nizations and individuals and the governmentsof the developing countries who bear the majorresponsibility for economic policy in theircountries

Let me start by discussing the historical back-ground the protagonists their views and the

1 During the 1970rsquos the word ldquoglobalizationrdquo was nevermentioned in the pages of The New York Times In the 1980rsquosthe word cropped up less than once a week in the rst halfof the 1990rsquos less than twice a week and in the latter halfof the decade no more than three times a week In 2000there were 514 stories in the paper that made reference toldquoglobalizationrdquo there were 364 stories in 2001 and 393references in 2002 Based on stories in The New York Timesthe idea of being ldquoanti-globalizationrdquo was not one thatexisted before about 1999 Turning from the newspaper tothe internet ldquoglobalizationrdquo brings up 16 million links

through the use of the Google search engine and typingin ldquoanti-globalizationrdquo brings up 80000 links Type inglobalization and inequality and there are almost 500000references 700000 references to globalization and environ-ment almost 200000 links to globalization and laborstandards 50000 references to globalization and multina-tionals and 70000 references to globalization and culturaldiversity A search of globalization and the IMF yields180000 suggestions

2 For a comprehensive review of the economic issuessee the extremely useful paper by Francois Bourguignon etal (2002) which covers many of the issues in this lecture(see also International Monetary Fund 1997 World Bank2002a)

2 AEA PAPERS AND PROCEEDINGS MAY 2003

issues Economic globalization the ongoingprocess of greater economic interdependenceamong countries is re ected in the increasingamount of cross-border trade in goods and ser-vices the increasing volume of international nancial ows and increasing ows of laborAs is well known to our profession economicglobalization thrived in the period before 1914but was set back by the two World Wars and theGreat Depression3 The international nancialorder that was established at the end of WorldWar II sought to restore the volume of worldtrade and by 1973 world trade as a percentageof world GDP was back to its 1913 level and ithas continued to grow almost every year since4

While the founders of the Bretton Woodssystem saw the restoration of trade in goods andservices as essential to the recovery of theglobal economy they did not have the samebenign view of capital ows Nonetheless cap-ital ows among the industrialized countries didrecover during the 1950rsquos and intensi ed in the1960rsquos Rapidly they became too powerful forthe pegged exchange-rate system to surviveand by 1973 as a result of the impossible trinity(of a pegged exchange rate capital mobilityand a monetary policy directed at domestic ob-jectives) the Bretton Woods adjustable-pegsystem had to give way to exible exchangerates among the major countries

Capital ows to developing countries grewmore slowly In the late 1970rsquos and early 1980rsquosthey consisted mainly of bank loans by the1990rsquos they took the form mainly of foreigndirect investment and purchases of marketablesecurities As the volume of international capi-tal ows to and from the emerging market coun-

tries (the more developed and larger developingcountries) increased the impossible trinity onceagain asserted itself and in a series of crisescountry after country was forced to give up itspegged exchange rate and allow the currency to oat

By now the gross volume of internationalcapital ows relative to global GDP far exceedsthe levels reached in the period just before1913 though net ows of foreign direct invest-ment have not yet attained the extraordinarylevels of the decade before World War I5

It is generally believed that with respect tomigration and labor ows the modern system isless globalized than it was a century ago6 In1911 nearly 15 percent of the United Statespopulation was foreign-born today that numberis probably a bit above 10 percent Emigrationrates from Europe especially Ireland and Italywere amazing 14 percent of the Irish popula-tion emigrated in the 1880rsquos and over 10 per-cent of the Italian population emigrated in the rst decade of the 20th century Jeffrey Wil-liamson (2002) attributes a signi cant part ofthe convergence of income levels in the Atlanticeconomy in the late 19th and early 20th centu-ries to mass migration7 Whether or not migra-tion and labor ows are greater now than they

3 Jeffrey Williamson (2002) classi es the period 1820ndash1914 as the rst great globalization era and the period sinceWorld War II as the second

4 Trade as a percentage of world GDP is estimated tohave risen from less than 5 percent in 1800 to a peak of justover 20 percent at the start of World War I and thencollapsed to 5 percent at the end of World War II Between1947 and the rst oil shock in 1973 world exports grew atan average annual rate of 88 percent per year Between1973 and 1990 they grew at an annual rate of 44 percentthe growth rate in the 1990rsquos was 7 percent As a result theworldrsquos markets for goods and services are more integratedthan ever before though the pattern is different with a risein intra-industry trade compared with the predominance ofinter-industry trade in the earlier period of globalization

5 Some suggest that capital markets remain less inte-grated today than in 1913 (eg Maurice Obstfeld and AlanTaylor 2003)

6 The note of caution is entered because it is not clearhow much labor ows between developing countries(SouthndashSouth labor ows) have changed These took placeon a large scale before 1913 but they are also very largetoday Timothy J Hatton and Williamson (2002 p 25)comment ldquoSouthndashSouth migration is not new It is justignored by economistsrdquo What is clear is that immigration ows to and from industrialized countries are lower nowthan in the decade before World War I (see Williamson2002) For example the annual immigration rate to theUnited States fell from about 116 per 1000 in 1910 to 04in 1940 and rose to 4 in the 1990rsquos The volume of remit-tances provides some evidence on labor-market integrationRemittances from overseas workers make labor services amajor export for many poor countries The volume of re-mittances increased from an annual average of $22 billion inthe 1970rsquos (measured in 1995 dollars) to $81 billion in the1990rsquos which is more than the annual volume of aid (Clau-dia Busch et al 2002)

7 In his work Jeffrey Williamson frequently uses theconvergence of prices rather than the volume of trade as anindicator of the extent of globalization

3VOL 93 NO 2 RICHARD T ELY LECTURE

were a century ago we are becoming moreglobalized in this regard too for migration rateshave been risingmdashand in a potentially impor-tant way for more migration than in the pastis from less-developed to more-developedcountries8

All this is at an abstract level In terms ofpeoplersquos daily lives globalization means thatthe residents of one country are more likely nowthan they were 50 years ago to consume theproducts of another country to invest in anothercountry to earn income from other countries totalk on the telephone to people in other coun-tries to visit other countries to know that theyare being affected by economic developmentsin other countries and to know about develop-ments in other countries

Globalization is much more than an eco-nomic phenomenon The technological andpolitical changes that drive the process ofeconomic globalization have massive noneco-nomic consequences9 In the words of AnthonyGiddens (2002 p 10) a leading sociologistldquoI would have no hesitation in saying thatglobalisation as we are experiencing it is inmany respects not only new but also revolu-tionary Globalisation is political technologi-cal and cultural as well as economicrdquo

The noneconomic aspects are at least as im-portant in shaping the international debate as arethe economic aspects Many of those who ob-ject to globalization resent the political and mil-itary dominance of the United States and theyresent also the in uence of foreign (predomi-nantly American) culture as they see it at theexpense of national and local cultures

The technological elements matter in practiceas well as in the debate For instance the eventsof 11 September 2001 could not have takenplace before the current global era The com-munications and transport systems that haveaccelerated the pace of globalization are also atthe disposal of terrorists money-launderers andinternational criminals On the positive side

improvements in communications and the spreadof information were critical to the collapse ofthe Iron Curtain People learned what was hap-pening in other countries and understood thatthey did not have to live the way they wereliving and the Iron Curtain fell

While we need to recognize the importanceand possibly the predominance of the noneco-nomic elements I shall focus on the economicdebate One set of views on economic global-ization is summed up by a characteristic passagefrom Rudi Dornbusch (2000 p 91)

On the verge of world de ation Japanbankrupt and Europe moving at near-stalling speed only the emerging marketsbattered and the United States beholding aglorious bubblemdashhow can this mark theend of a great century of prosperity Andyet this has been the best century evernever mind the great depression a mo-mentary setback from communism andsocialism and two great wars Mankindtoday is far and further ahead of where ithas ever been and there are the seeds ofinnovation from biology to the Internetfor better and richer lives even beyondour wildest dreams

This century and in particular the lastthree decades have witnessed just that asthe nation state has been dismantled infavor of a global economy state enter-prise and economic repression give wayto free enterprise and breathtaking inno-vation and greedy capitalism break downgovernment and corporate bureaucraciesAnyone who says impossible nds him-self interrupted by someone who just didit The process is far from complete in-novation and free enterprise spread themindset the success and the acceptanceof this model to the horror of status quopoliticians and the sheer exuberance of allthose who are willing to embrace a can-doattitude If this century taught anything itis surely this even daunting setbacks likedepression and war are only momentarytragediesmdashbuying opportunities if youlikemdashin a relentless advance of the stan-dard of living and the scope for enjoyingbetter lives One of the great economistsof this century Joseph SchumpetermdashAustrian nance minister of the 1920s

8 The fact that migration often has a brain-drain aspectraises important issues

9 The rapid increases in global integration in the secondhalf of the 19th century and early 20th century were drivenby the outbreak of peace in Europe and the invention of thetelegraph the steamship and the railroad

4 AEA PAPERS AND PROCEEDINGS MAY 2003

and Harvard professor at the endmdashwroteof creative destruction as the dramaticmechanism of economic progress Thatprocess is at work

A broad range of critics is arrayed on the otherside Among them are academics opinion lead-ers individuals and groups who see their inter-ests being affected by globalization politiciansNGOrsquos and demonstratorsmdashand these categoriesare not mutually exclusive10 To listen to thedebate in the terms each side paints the otherone might think that it is a discussion betweenDr Pangloss who believes that all is for thebest in the best of all possible worlds and thosewho believe that the world is going to hell in ahandbasket That is doubly misleading In the rstplace many of those who regard themselves aspro-globalization myself among them knowthat there is far too much misery in the worldthat there are many wrongs to be righted in theglobal economy and that it could be made tooperate much better And on the other sidemany (but not all) of the critics are not againstglobalization Rather from NGOrsquos demonstrat-ing for further debt relief and campaigning forgreater access of developing-country exports toindustrialized-countrymarkets to academic criticsquestioning current policy views many are seek-ing a better and fairer globalization

I will discuss ve of the key economic issuesin the debate11

(i) whether poverty and inequality are in-creasing or decreasing

(ii) whether integration into the global econ-omy is good for growth

(iii) whether the international nancial systemis too crisis prone and capital ows needto be banned or regulated

(iv) the unfairness of the global trading systemand the inadequacy of aid ows

(v) the role of the IMF

For want of time but also for lack of com-parative advantage I will not cover a host of

other economic issues that feature in the debateover globalization and its consequences amongthem whether globalization results in unfairlabor practices in developing countriesmdashan ar-gument which is not compelling whether glob-alization damages the environment whethermultinational corporations have become too pow-erful to the detriment of developing-country citi-zens and governments whether globalizationgives rise to tax competition that underminesthe capacity of governments to raise revenuesand thus to provide necessary services to theircitizens whether intellectual-property protec-tion is damaging the health of developing-country citizens and the roles of the WorldBank and the World Trade Organization Theseare important issues some of them critical andsome do not have simple answers But theseproblems are being seriously analyzed by econ-omists for instance by Bourguignon et al(2002) for the European Commission by theWorld Bank (2002a) and others12

One question before turning to the evidenceAlmost everyone recognizes that the worldcould be a better place and that there is muchwork to be done to improve it Why then is somuch of the debate about whether the world isgetting better or worse rather than about whatcan be done to make it a better place It isbecause the debate is ultimately about policiesThe implicit premise is that if the world is goingto hell then the policies that have been followedfor the past 50 years are likely to be wrong Andif the world has been getting better then thepolicies are more likely to be right13 It is aseparate question whether it is globalization thatis responsible for what has happened

The policies in dispute are generally thosethat have been recommended by the international nancial institutions and most industrialized-country governments14 At the broadest level

10 For a discussion of the anti-globalization groups andtheir concerns see Kimberly Ann Elliott et al (2003)

11 See the discussion of the 12 charges against global-ization in the nal chapter of Bourguignon et al (2002)

12 For references to the literature see Bourguignon et al(2002) on the trade-related issues see also Jagdish Bhag-wati (2000)

13 While persuasive the implicit proposition is notlogically compelling for policies could be wrong even ifthe world is improving and right even if the world isdeteriorating

14 In that regard the present discussion is merely thelatest manifestation of a long-running economic policy

5VOL 93 NO 2 RICHARD T ELY LECTURE

the policy consensus consists of four elementspolicies to ensure macroeconomic stabilitymarket-oriented microeconomic policies inte-gration into the global economy particularly onthe trade side and a positive role for govern-ment in establishing monitoring and develop-ing the institutional framework of the economyproviding public goods including especially so-cial expenditures and conducting stabilizationpolicies

Beyond these broad headings detailed policyrecommendations have been spelled out inmany World Bank and IMF publications forinstance the World Development Reports of theWorld Bank15 One formulation that has re-ceived much attention and a large share of cal-umny is the so-called Washington consensus setout by John Williamson (1990)16 The ten ele-ments of the 1990 consensus were (i) scaldiscipline (ii) public-expenditure priorities ineducation and health (iii) tax reform (the taxbase should be broad and marginal tax ratesshould be moderate) (iv) positive but moder-ate market-determined interest rates (v) a com-petitive exchange rate as the ldquo rst essentialelement of an lsquooutward-orientedrsquo economic pol-icyrdquo (p 14) (vi) import liberalization (vii)openness to foreign direct investment (but ldquolib-eralization of foreign nancial ows is not re-garded as a high priorityrdquo [p 15]) (viii)privatization (based on ldquothe belief that privateindustry is managed more ef ciently than stateenterprisesrdquo [p 16]) (ix) deregulation and (x)protection of property rights

The Washington consensus is a brand namethat has been so abused as probably to haveoutlived its usefulness While no short descrip-tion of the economic policy choices that face acountry and of the principles that it should followcan be adequate to the complexities of the real-

world situation confronting policymakers I stillregard these ten elements as a useful shorthanddescription of a major part of a desirable basicpolicy orientation17 And for that reason I shall atleast for a while continue to use the term ldquoWash-ington consensusrdquo

II The Evidence on Povertyand Global Inequality

A Poverty

For some time it was accepted that the pro-portion of people living in poverty in the worldhas been declining but their absolute numberhas been increasing This refers to the WorldBankrsquos measure of absolute poverty de ned asliving on a real income of less than one dollara day18 There is no consistent fully reliable setof data re ecting longer-term developments inpoverty19 A useful estimate of post-World WarII developments is shown in Figure 1 the globalpoverty rate is estimated to have declined im-pressively from about 55 percent in 1950 to237 percent in 199220 It has continued fallingsince

The data most often used in discussing recentpoverty developments come from the WorldBank and are based on national estimates ofpoverty rates These estimates are likely to besubject to signi cant error as the recent debateover the Indian poverty data illustrates Indiangrowth in the 1990rsquos averaged nearly 6 percentmore than 3 percent per capita Aggregate con-sumption in the national income accounts roseby 32 percent per capita But household surveydata on which Indiarsquos poverty estimates are

debate that has at times pitted protectionists against free-traders and those who believe in a greater role for the stateagainst those who believe more in markets

15 See David Lindauer and Lant Pritchett (2002) for anaccount of changing views of development policy duringthe post-World War II period

16 These were not necessarily John Williamsonrsquos viewsbut rather his attempt to capture the consensus of the timeIn the article he expands on the range of views (includinghis own which generally include several quali cations)under each heading

17 I was one of the discussants of the Williamson (1990)paper at the time (my comments are on pp 25ndash28) andmentioned among the missing elements the responsibility ofthe government to create an enabling environment for eco-nomic activity the need for directed anti-poverty policiesand environmental concerns

18 Strictly speaking the $1 per day gure corresponds toa Penn World Tables Purchasing Power Parity income ofabout $108 in 1993 prices (Shaohua Chen and MartinRavallion 2001)

19 I am particularly grateful to Angus Deaton for guidingme through the debate on the poverty data He bears noresponsibility for the views set out in this section

20 These data are from Bourguinon and Christian Mor-risson (2002)

6 AEA PAPERS AND PROCEEDINGS MAY 2003

based showed very little increase in per capitaconsumption21

Based on the sample surveys poverty de-clined relatively little in India in the 1990rsquosBased on the national income accounts itshould have declined signi cantly One way ofcombining the data chosen by Surjit Bhalla(2002) is to assume that the distribution ofconsumption in the sample surveys is correctbut to adjust the mean increase in consumptionin the sample surveys to equal that in the na-tional income accounts This produces spectac-ular declines in poverty in India during the1990rsquos

The of cial data also show signi cant butsmaller declines in the Indian poverty ratefrom about 40 percent in 1987ndash1988 to 26 per-cent in 1999ndash2000 In checking these dataDeaton (2002a) reports ldquoMuch to my surprisemost of the of cially claimed reduction in pov-erty appears to be realrdquo22

Applying the Bhalla procedure to all coun-tries also produces rapid declines in global pov-erty23 More cautiously recent World Bank datashow the global poverty rate declining sharplyfrom 296 percent in 1990 to 232 percent in1999 (Table 1)24 According to these estimates(and they are only estimates) the absolute num-ber of the poor declined by 123 million peopleor 10 percent during this period The number ofpoor in China alone fell by 150 million Table1 shows that the major decline in the globalpoverty rate is accounted for by Asia with theabsolute number of poor in sub-Saharan Africa

21 Angus Deaton (2002a) provides a brief description ofthe problem

22 Deaton whose work is regarded as authoritative es-timates the poverty rate for 2000 to be 28 percent he ndsthat the poverty rate in India declined fairly steadily over thepast 20ndash30 years with no evidence of a pickup followingthe reforms in 1991 But he notes (Deaton 2002a) that

neither is there any evidence that the pro-market reforms ledto increases in poverty or slowed poverty reduction

23 Bhallarsquos (2002) estimates are that poverty was 30percent in 1987 and only 13 percent in 2000 This wouldimply that the last decade of the last century was the mostsuccessful in all of history in reducing poverty XavierSala-i-Martin (2002b) shows even larger declines in globalpoverty counts over the period 1970ndash1998 using a similarmethodology He estimates the $1 per day poverty rate to beonly 5 percent in 1998

24 Surprisingly the heading on a table very similar toTable 1 (table 12 p 18) in the United Nations Develop-ment Programrsquos (2002) Human Development Report isldquoWorldwide the number of people living on less than $1 aday barely changed in the 1990srdquo The table shows that eventhe absolute number of those living on less than $1 a daydeclined by 10 percent in the 1990rsquos

FIGURE 1 GLOBAL POVERTY RATES PERCENTAGE OF PEOPLE LIVING ON LESS THAN $1 PER DAY

Source Bourguignon and Morrisson (2002)

7VOL 93 NO 2 RICHARD T ELY LECTURE

(and also in the transition economies) risingsigni cantly

Between them China and India account for38 percent of the worldrsquos population In 1990they accounted for 60 percent of the worldrsquospoor It is therefore hardly surprising that theglobal poverty rate fell sharply in a decade inwhich China grew at more than 9 percent andIndia at 6 percent It may be argued that whathappened in China and India is atypical That istrue if the unit is the country but not if the unitis the individual25 Further there can be littledoubt that in both India and China the growthpolicy during the period was pro-globalizationpro-entry into the global economy Of coursenot every detail of policy in either country fol-lowed the Washington consensus but bothcountries grew faster after opening up26

Beyond the data on per capita income mostsocial indicators have also shown considerableimprovement in the postwar period and morerecently As Figure 2 (taken from the UnitedNations Development Programrsquos [2002] HumanDevelopment Report) shows adult literacy has

risen in all regions in the last 25 years andinfant mortality has declined signi cantly Lifeexpectancy has risen in most regions Howeverunder the impact of the HIVAIDS pandemicit has begun to decline in sub-Saharan Africawith particularly large and tragic impact inBotswana Zimbabwe South Africa andKenya27

The Human Development Report presents aHuman Development Index (HDI) which isbased on three equally weighted factors lifeexpectancy education and (the logarithm of) apurchasing-power-parity estimate of per capitaGDP28 Figure 3 shows changes in the HDI overthe past 20 years Note in particular that theHDI is inherently an index of relative perfor-mance so that the improvements in all regionsrepresent a convergence of this more generalmeasure of economic and social progress acrossregions

In addition as the 2002 Human DevelopmentReport shows democracy has been spreadingincluding in the developing world By one clas-

25 The sharp differences in poverty rates among Indianstates and among Chinese provinces should also containpolicy-relevant information

26 However Deaton (2002b) nds no acceleration in therate of poverty reduction following Indiarsquos policy reforms in1991

27 Life expectancy is estimated by applying current age-speci c mortality rates it thus is not the life expectancy ofan individual born today for which it would be necessary toforecast mortality

28 All measures are taken relative to the highest levelattained within the sample so the index is bounded aboveby 1

TABLE 1mdashREGIONAL BREAKDOWN OF POVERTY IN DEVELOPING COUNTRIES

Region

Number of people living onless than $1 per day

(millions)

$1 per dayheadcount index

(percent)

1987 1990 1999 1987 1990 1999

East Asia and Paci c 418 486 279 266 305 156excluding China 114 110 57 239 242 106

Europe and CentralAsia

1 6 24 02 14 51

Latin American andthe Caribbean

64 48 57 153 110 111

Middle East andNorth Africa

9 5 6 43 21 22

South Asia 474 506 488 449 450 366Sub-Saharan Africa 217 241 315 466 474 490

Total 1183 1292 1169 283 296 232Excluding China 880 917 945 285 285 250

Source World Bank staff estimates (Global Economic Prospects 2003)

8 AEA PAPERS AND PROCEEDINGS MAY 2003

si cation the number of authoritarian regimesdeclined from 67 to 26 between 1985 and 2000(hardly surprising given the transition in theformer Soviet bloc and the changes in LatinAmerica) while the number of nations catego-rized as ldquomost democraticrdquo rose from 44 to 82(United Nations Development Program 2002[ g 11])

Thus there is considerable evidence that onaverage conditions have been improving in thedeveloping countries That is to say the world isnot going to hell in a handbasket But that isemphatically not to say that everyone in thedeveloping countries is doing better In partic-ular conditions in most of sub-Saharan Africawhere per capita growth has been negative innearly half the countries in the last quarter cen-tury have been deteriorating and Latin Amer-ica has not done well in the last decade

The discussion of trends in global poverty isa signi cant part of the globalization debateBut it does not directly address the globalizationissue of whether whatever has been happeningis caused by increasing integration into the globaleconomy That question will be addressed when Idiscuss the impact of openness on growth

B Inequality

While a global Rawlsian perspective wouldlead to a focus on poverty reduction we need tofocus also on inequality not only because formany great inequality is undesirable per se butalso because growing inequality may have pow-erful political consequences For instance in the rst era of globalization changes in the incomedistribution that affected real wages and thereturns to land and capital led to pressure to

FIGURE 2 ALTERNATIVE INDICATORS OF HUMAN DEVELOPMENT

Notes Regions are abbreviated as follows LHD low human development SSA sub-Saharan Africa AS Arab states SAsouth Asia EA east Asia and the Paci c LA Latin America and the Caribbean CEE central and eastern Europe and CISOECD high-income OECDSource United Nations Development Programrsquos (2002) Human Development Report

9VOL 93 NO 2 RICHARD T ELY LECTURE

limit economic integration (Jeffrey Williamson2002) That could happen again as globaliza-tion creates losers as well as winners in the shortrun29

Inequality among national average incomesappears to have been increasing for at least 400years since before the rapid increases in eco-nomic integration that took place in the 19thcentury (Jeffrey Williamson 2002) Howeverthis long-term rise in inequality among nationalaverage incomes seems to have slowed duringthe past 20 years (see Bourguignon and Morris-son 2002 Sala-i-Martin 2002a b)

The convergence debate in macroeconomicswas based on purchasing-power-parity esti-mates of national average incomes As is wellknown and as Figure 4 illustrates the raw dataon country average incomes show divergencenot convergence The early results for instancethose of Robert J Barro (1997) supported con-ditional convergence Provided the conditioningvariables do not change in an offsetting direc-tion conditional convergence implies that the

inequality among country average incomeswould eventually declinemdashbut that could take avery long time The weight of the evidenceappears now to have moved away from theinitial conclusion of conditional convergencetoward the twin-peaks view that there is a con-vergence club among the high-income OECDcountries while lower-income countries areconverging to a lower income level (Danny TQuah 1996)

Developments in inequality within countriesmay be politically more important than changesin inequality among countries There was a risein inequality in the United States and the UnitedKingdom from the start of the 1980rsquos until wellinto the last decade Inequality during that pe-riod did not increase markedly in continentalEurope probably due to labor-market regula-tions social welfare programs and tax sys-tems30 Reviewing the literature Lawrence FKatz and David H Autor (1999) concluded thattrade explains at most 20 percent of the rise ininequality in the United States and that skill-biased technological change explains 80 percentof the rise31 There are also instances of increas-ing inequality within some poor countries in-cluding China and India even though incomeshave increased at both the top and the bottom ofthe scale In the transition economies of theformer Soviet bloc inequality increased sharplyin the 1990rsquos

Beyond the inequalities among national av-erage incomes and within countries stands theconcept of the distribution of global incomeamong all the worldrsquos people of which thereare now several estimates (eg Bhalla 2002Bourguignon and Morrisson 2002 Milanovic2002a Sala-i-Martin 2002) These are all basedon data on the distribution of income withinnations and some method (typically using pur-chasing power estimates) for comparing incomelevels across countries Figure 5 shows whysuch an estimate might nd inequality declining

29 See Branko Milanovic (2002b) for a forceful state-ment of the view that current trends are likely to produce abacklash unless globalization as we know it is tamed

30 They may well instead have produced higherunemployment

31 Kenneth Scheve and Matthew Slaughter (2001) em-phasize what they call the ldquoskills-preferences cleavagerdquo onglobalization among the American public in which viewson globalization are signi cantly affected by the skill levelof poll respondents

FIGURE 3 RECENT TRENDS IN THE HUMAN DEVELOPMENT

INDEX (HDI) SHOWING GLOBAL DISPARITIES

Notes Regions are abbreviated as follows SA South AsiaSSA sub-Saharan Africa AS Arab States DC all devel-oping countries EA east Asia and the Paci c LA LatinAmerica and the Caribbean CEE central and eastern Eu-rope and CIS OECD high-income OECDSource United Nations Development Programrsquos HumanDevelopment Report of ce calculations based on indicatortable 2

10 AEA PAPERS AND PROCEEDINGS MAY 2003

among nations it is the graphic representationof a population-weighted convergence diagramin which the dominance of China and Indiadrives the relationship Bourguignon and Mor-risson (2002) conclude that the inequality ofglobal income worsened from the start of the19th century until the end of World War II ldquoandafter that seems to have stabilized or to havegrown more slowlyrdquo32

Where does that leave us on both poverty andthe global distribution of income Poverty rateshave been declining especially in Asia So verylikely has the absolute number of those living atbelow one dollar a day Increasingly globalpoverty is being concentrated in Africa At thesame time poverty rates have not declinedmuch in Latin America in recent decades Tak-ing account of other social indicators as re-

ected in the HDI presents a more encouragingpicture of the changing fortunes of the poorestbut the HIV-AIDS epidemic is taking a sad tollon longevity in Africa

Income-distribution developments are moremixed There has been a growing divergenceamong national average incomes Inequality hasrisen within many countries but it is likely thatinequality among the worldrsquos citizens declinedduring the last decades of the 20th centuryHowever we should not take too much comfortfrom that for as Sala-i-Martin (2002a) pointsout ldquoUnless Africa starts growing in the nearfuture income inequalities will start risingagainrdquo

III The Policy Issues

A Trade and Growth

Trade policy has long been central to eco-nomic policy choices In the early post-WorldWar II period the theory of import-substitutingindustrialization (ISI) dominated among devel-oping countries and its implementation forsome time seemed to produce positive resultsThen as time went by it was observed both thatcountries that had pursued export promotion

32 However Milanovic (2002a) nds that global incomeinequality increased between 1988 and 1993 in part be-cause of growing gaps between rural and urban incomes inChina By contrast Bhalla (2002) shows world inequality in2002 at its lowest level in the post-World War II period aresult of the much greater reductions in global poverty in the1990rsquos that his methodology produces Similarly Sala-i-Martin (2002a) nds massive decreases in global inequalityat the individual level between 1980 and 1998

FIGURE 4 AVERAGE ANNUAL GROWTH (1980ndash2000) ON INITIAL LEVEL

OF REAL GDP PER CAPITA

Note The data are values for real GDP in US dollars per equivalent adultSource Penn World Tables version 61 (available online httppwteconupennedu )

11VOL 93 NO 2 RICHARD T ELY LECTURE

strategies were more successful than those thathad focused on keeping imports out and that thereturns to ISI seemed to be diminishing

Early case studies of trade liberalization wereconducted in the 1970rsquos and 1980rsquos under theauspices of the OECD the National Bureau ofEconomic Research (NBER) and later theWorld Bank33 These by and large supported thecase for export promotion policies that is forintegration into the global economy Subse-quently a host of cross-sectional regressionstudies were undertaken34 most of them show-ing that greater openness is associated either withhigher levels of income or more rapid growth35

The study by Jeffrey Sachs and Andrew Warner

(1995) which concludes that ceteris paribusopen countries grow 2 percent per annum morerapidly than closed countries has received par-ticular attention A closely related literature ex-amines the mechanisms through which opennesscontributes to growth particularly through itsimpact on productivitywhere the availability ofimported inputs plays a role36

The regression studies have been comprehen-sively reexamined and criticized by FranciscoRodriguez and Dani Rodrik (2001) who arguethat the results are not robust the measures ofopenness used in the studies neither clearly ex-ogenous nor consistent across studies and theeconometrics awed37 Nonetheless the casestudies that show trade liberalization as an es-sential element in policy reforms that led togrowth the bulk of the empirical evidence andthe fact that the most spectacular growth storiesall involve rapid increases in both exports andimports (frequently after speci c policy deci-

33 The NBER studies are summarized in Bhagwati(1978) and Anne Krueger (1978) the World Bank studiesare summarized in Michael Michaely et al (1991)

34 T N Srinivasan and Bhagwati (1999) criticize theregression approach in arguing for the superiority of thecase-study method I have used both methods on differentoccasions and regard each as having important weaknesses(see also Krueger 1983)

35 Examples include David Dollar (1992) Dan Ben-David (1993) Jeffrey Sachs and Andrew Warner (1995)Sebastian Edwards (1998) Jeffrey Frankel and David Ro-mer (1999) and Dollar and Aart Kraay (2001a b) RobertE Hall and Charles Jones (1999) include both openness (theSachs-Warner index) and a measure of good governancewhich is highly correlated with the openness indicator

36 The literature on openness and growth is well sum-marized by Bourguignon et al (2002 pp 37ndash39) and byAndrew Berg and Krueger (2003)

37 Warnerrsquos (2001) draft response to the Rodriguez-Rodrik critique strongly disputes several of these criticismsincluding the suggestion that the black-market premium isnot a useful indicator of trade distortions and reaf rms theSachs-Warner conclusions

FIGURE 5 AVERAGE ANNUAL GROWTH (1980ndash2000) ON INITIAL LEVEL OF REAL GDP PER

CAPITA (AS IN FIG 4 BUT WITH AREA PROPORTIONAL TO POPULATION IN 1980)

Note The data are values for real GDP in US dollars per equivalent adultSource Penn World Tables version 61 (available online httppwteconupennedu )

12 AEA PAPERS AND PROCEEDINGS MAY 2003

sions have been made to open up) should per-suade us that openness to the global economyis a necessary though not suf cient conditionfor sustained growth38 To quote Dani Rodrik(2001 p 23) ldquoNo country has developed suc-cessfully by turning its back on internationaltrade and long-term capital owsrdquo

To say that is not to say that immediate fulltrade liberalization is necessarily the best policyfor a country nor that opening to trade is suf- cient for growth nor that the accompanyingpolicy framework is irrelevant39 Indeed theaccompanying framework is essential It is to sayhowever that countries that want to grow shouldas a key part of their policy framework orientthemselves toward integration into the globaltrading system to take advantage of the avail-ability both of much larger global than domes-tic markets and of more sophisticated capital-intermediate- and consumer-good imports40

B Growth Poverty and Inequality

Here I can be brief Logic dictates that thereis no way of lifting the populations of poorcountries out of poverty (say on the scale thathas been achieved in East Asia) without sus-tained growth Globally the decline in poverty

has been fastest where economic growth hasbeen fastest (in developing Asia) and slowestwhere growth performance has been worst (inAfrica)

Nor despite the early results of SimonKuznets does there appear to be any inevitableassociation between growth and inequalityrather it depends on the details of the policiesincluding distributional policies that accompanythe growth strategy41 In two related studiesDollar and Kraay (2001a b) conclude based ondata from 92 countries that on average theincome of the lowest fth of the income distri-bution rises one-for-one with aggregate incomeand that this same relationship holds for growththat is induced by trade liberalization

To say that on average growth or opening totrade does not adversely affect the incomesof the poor is not to say that the impact ofpolicy changes on income distribution shouldbe ignored when any particular policy change isbeing considered The opening of trade is de-signed to affect domestic relative prices andmost likely will affect the distribution of incomein each case42 If these effects are judged to beadverse transitional compensatory measuresand gradual liberalization may help mitigatethem (see Scheve and Slaughter 2001 pp 94ndash96) It is also the case that a small economytends to be more vulnerable to uctuations inthe terms of trade when it is open than when itis closed and that the poor may be the mostvulnerable in this regard43

C Capital-Account Liberalization

There is far more controversy about capital-account liberalization as part of a growthstrategy than there is about current-account lib-eralization That is not surprising for as the

38 Rodrik (2001 p 23) does not disagree with this con-clusion emphasizing rather the speed of adjustment and theneed for accompanying policies ldquoThe trick in the successfulcases has been to combine the opportunities offered byworld markets with a domestic investment and institution-building strategy to stimulate the animal spirits of domesticentrepreneurs Almost all of the outstanding casesmdashEastAsia China India since the early 1980smdashinvolve partialand gradual opening up to imports and foreign investmentrdquo

39 Berg and Krueger (2003 p 39) state ldquoOpenness hasimportant positive spillovers on other aspects of reform sothe correlation of trade with other pro-reform policiesspeaks to the advantages of making openness a primary partof the reform packagerdquo This relates to an emerging litera-ture (eg Dollar and Kraay 2002 William Easterly andRoss Levine 2002) that argues either that the growth effectsof openness and the institutional structure of the economyare dif cult to distinguish or that institutions are moreimportant I nd the Berg-Krueger argument on this pointpersuasive

40 Nancy Birdsall (2002) argues that openness does notwork well for the poorest countries because of their greaterdependence on primary exports and because of their greatervulnerability to external shocks It is nonetheless dif cult tosee how a small economy could hope to reach a high levelof income without integrating into the global economy

41 Barro (1999) states that the Kuznets curve doesemerge as a clear empirical regularity but does not explainmost of the variations of inequality across countries or overtime

42 Mattias Lundberg and Lyn Squire (1999) nd that growthis more sensitive than inequality to policy interventions

43 There is no general prescription for what these policiesshould be they need to be designed taking the circum-stances of the country into account for instance in theIndonesian crisis of 1997ndash1998 subsidizing the price of ricewas a key pro-poor policy

13VOL 93 NO 2 RICHARD T ELY LECTURE

Asian crisis drove home a country with an opencapital account is more vulnerable to externalshocks than one that is closed to external capital ows

In considering capital-account liberalizationI assume that countries will and should at somestage in the course of their development want toliberalize the capital account and integrate intoglobal capital markets This view is based inpart on the fact that the most advanced econo-mies all have open capital accounts it is alsobased on the conclusion that the potential ben-e ts of well-phased and well-sequenced inte-gration into the global capital markets (and thisincludes the bene ts obtained by allowing for-eign competition in the nancial sector) out-weigh the costs4445

With regard to empirical evidence on thebene ts of capital-account liberalization Ibelieve we are roughly now where we werein the 1980rsquos on current-account liberaliza-tionmdashthat some evidence is coming in butthat it is at this stage weak and disputed46 Thedirection of causation is particularly problem-

atic in this case for as Hali Edison et al (2002b)note successful economies are generally openeconomies

The relationship between capital-account lib-eralization and growth is likely to be inherentlyweaker than that between current account liber-alization and growth since it is more dependenton the sequencing of reforms and the presenceof preconditions (eg a strong macroeconomicframework) than is the current-account liberal-ization relationship An interesting nding inthis regard is that of Carlos Arteta et al (2001)who conclude that capital-account openness hasa positive impact on growth contingent on theabsence of a large black-market premiummdashwhich is a good idicator of the absence of mac-roeconomic imbalances

At present most developing countries main-tain capital controls Experience suggests theyshould only be removed gradually at a timewhen the exchange rate is not under pressure47

and as the necessary infrastructure (in the formof strong domestic nancial institutions asound macroeconomic framework a market-based monetary policy the underpinnings of aneffective foreign-exchange market and the in-formation base necessary for the markets tooperate ef ciently) is put in place48 For mostcountries it would be desirable to begin allow-ing some exibility of exchange rates as thecontrols are eased unless the country intends tomove to a hard pegmdashand after Argentina thatdoes not look advisable unless there is a clearlyde ned terminal condition49 Prudential controls

44 The argument is developed at greater length in Fischer(1998) The point has been much disputed including byBhagwati (1998)

45 It is also based on the views that in practice capitalcontrols are often discriminatory a standing invitation tocorruption and grow progressively less effective over time

46 Rodrik (1998) presents a critical view of capital-account liberalization A set of papers presented at a May2002 World Bank conference ldquoFinancial GlobalizationA Blessing or a Curserdquo (available online httpwwwworldbankorgresearchconferences nancial_globalizationhtm ) on balance pointed to small positive impacts of nan-cial liberalization on growth (see eg Geert Bekaert et al(2002) Anusha Chari and Peter B Henry (2002) ArturoGalindo et al (2002) Pierre Gourinchas and Olivier Jeanne(2002) and Carmen Reinhart and Ioannis Tokatlidis (2002)Hali Edison et al (2002a) review the literature on therelationship between growth and capital-account liberaliza-tion They nd that capital-account liberalization spursgrowth signi cantly in a middle-income range of countriesbut not for rich or poor countries However in a study of 57countries using a wide array of measures of international nancial integration and an assortment of statistical meth-ods Edison et al (2002b) are unable to establish a relation-ship between greater international nancial integration andfaster economic growth They do identify indirect effectsby nding a signi cant impact from capital-account liber-alization on investment and nancial development thesetwo channels are estimated to increase growth by 05 per-cent per year or more

47 The removal of controls on out ows sometimes re-sults in a capital in ow a result of foreigners or domesticresidents bringing capital into the country in light of thegreater assurance it can be removed when desired

48 Some countries have attempted to impose controls onout ows once a foreign-exchange crisis is already underway This use of controls has generally been ineffective (seeAkira Ariyoshi et al 2000 pp 18ndash29 Edwards 1999 pp68ndash71) It has also to be considered that the imposition ofcontrols for this purpose in a crisis is likely to have alonger-term effect on the countryrsquos access to internationalcapital For the record I should note here that there is verylittle information about such use of controls in the Malay-sian case of 1998 for the controls were imposed whenexchange rates in the region were at their most depreciatedand as capital ows in all the crisis countries were reversing

49 For instance that the country plans to join the Euro-pean Monetary Union and give up its currency

14 AEA PAPERS AND PROCEEDINGS MAY 2003

that have a similar effect to some capital con-trols for instance limits on the open foreign-exchange positions that domestic institutionscan take should also be put in place as directcontrols are removed50

Any country using capital controls builds upan information system on capital ows It maybe useful to maintain an information base forsome time even after the removal of controls asin the Brazilian case for such information canbe useful in managing a crisis

Several countries among them Singaporethe three Asian crisis countries and Malaysiahave taken steps to limit the offshore use oftheir currencies In principle this makes it pos-sible to break the link between onshore andoffshore interest rates particularly by restrict-ing the convertibility of the currency for non-residentsmdashwho need access to the domesticbanking system to complete their transactions(see Shogo Ishii et al 2001)51 Ishii et al(2001) conclude that such restrictions have beenmore successful the more comprehensive theyhave been and that they could provide the au-thorities with a breathing space in which toimplement policy changes52 But as with othercapital controls their effectiveness tends toerode over time Further the longer the mea-sures are implemented and the stronger theyare the higher the associated costs in terms ofthe ef ciency of the nancial system are likelyto be

Excessive indebtedness of domestic nan-cial and non nancial institutions arises notfrom capital out ows but from in ows es-pecially short-term in ows Market-basedcapital-in ow controls Chilean style couldbe helpful for a country seeking to avoid thedif culties posed for domestic policy by cap-ital in ows This typically occurs when a

country is trying to reduce in ation using anexchange-rate anchor and for anti-in ationarypurposes needs interest rates higher thanthose implied by the sum of the foreign inter-est rate and the expected rate of currencydepreciation A tax on capital in ows canhelp maintain a wedge between the two inter-est rates In addition by taxing short-termcapital in ows more than longer-term in- ows capital-in ow controls can also in prin-ciple in uence the composition of in ows

Evidence from the Chilean experienceimplies that controls were for some timesuccessful in allowing some monetary-policyindependence and also in shifting thecomposition of capital in ows toward thelong end Empirical evidence presented byJose De Gregorio et al (2000) suggeststhat the Chilean controls lost their effective-ness after 1998 They have recently beenremoved

Thus controls can be used to help limit cap-ital out ows and maintain a pegged exchangerate given domestic policies consistent withmaintenance of the exchange rate Howeversuch controls tend to lose their effectiveness andef ciency over time Capital-in ow controlsmay for a time be useful in enabling a countryto run an independentmonetary policy when theexchange rate is softly pegged and may in u-ence the composition of capital in ows buttheir long-term effectiveness to those ends isdoubtful

D Instability in the Global Financial System

The series of emerging-market nancial cri-ses from Mexico in 1994 to Asia to RussiaBrazil Turkey Argentina and Brazil again hasbeen at the center of the globalization debateThe crises hit some countries that had at timesbeen described as model reformers and others(in Asia) that had been growing very fast Thecrises took a heavy toll on almost all of thecrisis countries as well as on other countriesaffected by the contagion53 Figure 6 shows thebehavior of output in the crises

50 Morris Goldstein (2002) recommends a ldquomanaged oating plusrdquo regime where the plus consists of measures todiscourage currency mismatching by domestic institutions

51 This paper describes three different mechanisms thatare used to limit offshore currency trading

52 Singapore has been gradually dismantling these con-trols Jaewoo Lee (2001) concludes that the Singapore con-trols were successful in large part because the underlyingmacroeconomic imbalances were very small and thereforedid not provide signi cant incentives to circumvent thecontrols 53 In this section I draw heavily on Fischer (2001 2002)

15VOL 93 NO 2 RICHARD T ELY LECTURE

The proximate cause of most of the criseswas the reversal of large-scale short-term capi-tal ows In every case except Brazil in 2001ndash2002 the crisis affected a country with a moreor less formally pegged exchange rate whichgave way usually at the beginning of the crisisIn every case except in Brazil the crisis hit acountry with a weak nancial systemmdashthoughthe Russian nancial system was very small atthe time of the crisis and the Argentinian bank-ing system had been strong a year before thecrisis but was severely weakened by measuresimposed on it in attempts to preserve the cur-rency peg

Capital- ow volatility during the crises wasmassive For the extreme cases between 1996and 1998 private capital in ows to Indonesiadeclined by 165 percent of GDP while theturnaround for Turkey between 2000 and 2001was 136 percent of GDP Among the crisiscountries shown in Figure 6 the smallest rever-sal in private capital ows was in Brazil wherethe decline was by 31 percent of GDP between2001 and 2002 This helps explain why Brazil is

the only country that kept growing through itsexternal crises

Although hedge funds received a large shareof the blame for the reversals and were proba-bly predominant in determining the timing ofsome of the crises54 the reversals were moregeneral and not con ned to short-term fundingNeither were they con ned to the actions offoreigners not surprisingly in most of the cri-ses domestic residents and corporations playeda prominent part in the capital- ow reversals

What can be done to reduce the volatility ofcapital ows to emerging-market countriesThe rst response would be for countries to shutthemselves off from international capital owsIt bears emphasis that despite the crises andthe arguments of many critics of globalizationalmost no country has taken this route the

54 Following the Asian crisis an IMF study concludedthat a wide range of nancial institutions including bankshad engaged in the same behavior as the hedge funds (seeBarry Eichengreen and Don Mathieson 1998)

FIGURE 6 REAL GDP GROWTH

Source International Monetary Fund (World Economic Outlook)

16 AEA PAPERS AND PROCEEDINGS MAY 2003

revealed preference of the emerging-marketcountries is to stay involved with the interna-tional nancial system55

However as previously noted some coun-tries have taken measures to limit the offshoreuse of their currencies thus securing moremonetary-policy exibility In addition I shouldnote that capital- ow reversals would not havebeen so large had the in ows been smallerto begin with The introduction of a exibleexchange-rate system has generally sharply re-duced short-term capital in ows and is thus amajor part of the solution to the problem ofexcessive capital- ow volatility For transi-tional periods the use of Chilean-style capital-in ow controls and more detailed reportingrequirements can also help moderate in ows

The question also arises of whether policymeasures to mitigate the volatility of capital ows to emerging-market countries can betaken by the authorities in the major capitalmarkets from which the funds ow Manyincluding the authorities in some Asian coun-tries have argued for more transparency bythe hedge funds and other market partici-pants56 However it has not been possible toreach a consensus on greater disclosure ofposition-taking by nancial institutions par-ticipating in emerging markets Although it isdoubtful that a different consensus willemerge any time soon this issue should re-main on the agendamdashand in the meantime itremains open to emerging-market authoritiesto build better information systems about cap-ital ows in their countries

Also prominent on the agenda is private-sector involvement in the resolution of crisesLet me brie y take up two issues the extent towhich the of cial sector should seek to coordi-nate the actions of the private sector when acrisis appears imminent and the recent IMFproposal for a sovereign debt-restructuringmechanism57

During the 1980rsquos Latin American debt cri-sis the Federal Reserve System and the IMFworked closely with the principal creditors thebanks and the debtor countries to put together nancing packages As the 1990rsquos crises un-folded there were many who argued that theauthorities should act similarly and seek to co-ordinate the creditors In effect the argument isthat there is a bad equilibrium in which all thelenders seek to withdraw funds and only worsenthe crisis in doing so and a good equilibrium inwhich the creditors stay in and thereby helpmitigate the crisis In such situations in coor-dinating the creditors the authorities can be seenas resolving a collective-action problem that thecreditors acting individually cannot solve

This approach was successful in the SouthKorean crisis at the end of 1997 and in early1998 Nonetheless great care needs to be takenin seeking to coordinate the creditors It wouldbe destabilizing if the creditors were coordi-nated in every crisis for they would have agreater incentive to rush for the exits at the merehint of a crisis58 In addition it is much moredif cult for the authorities to justify coordinat-ing the creditors when there is a signi cant riskthat those who have been persuaded to stayin will nonetheless suffer losses That is whyindustrial-country regulators have been lessenthusiastic about creditor coordination in re-cent years than they were in the 1980s there isa con ict between their regulatory role and theirpressuring the banks to maintain portfolio posi-tions against their will

The recent experience suggests a differenti-ated approach to creditor coordination Some-times a formal approach may be necessary as inKorea at Christmas in 1997 at other times as inthe case of Brazil in March 1999 when thecommercial banks voluntarily agreed to main-tain their lines of credit less formal discussionscould serve better when nancing needs aresmall or when an IMF package seems adequate

55 Even Malaysia which imposed capital controls in1998 removed most of them within 1ndash2 years

56 For more detailed proposals see Wendy Dobson andGary Hufbauer (2001)

57 For a more comprehensive analysis see Fischer(2002)

58 This possibility was very much in the minds of thosecontemplating coordinated action during the crises of the1990rsquos we believed that the more often we sought tocoordinate the creditors the more likely it was that the crisiswould spread even further than it did and that in the limitthe entire system could seize up and we would have beenback in the 1930rsquos

17VOL 93 NO 2 RICHARD T ELY LECTURE

to reverse out ows there may be no need toapproach the creditors and in extreme and in-frequent cases an involuntary restructuring ofthe debt may be necessary

It is striking that when governments face thedecision on whether to seek to impose a stand-still andor restructure their debts in a nonvol-untary way they are generally willing to govery far to avoid a default Why The reasonsare (i) that a debt restructuring will almostcertainly involve a restructuring of the domestic nancial system where nancial institutions(including banks and pension funds) hold gov-ernment bonds as important parts of theirportfolios (ii) that there may be serious inter-ruptions to the payments mechanism and totrade credit59 and (iii) that it is impossible toknow when domestic and foreign con dence inthe governmentrsquos ability to meet its promiseswill be restored and for how long the countrywill be punished by the markets for havingdefaulted Rightly or wrongly probably rightlydebtor governments see the costs of a debt de-fault as extremely largemdashand much larger thanthe critics of IMF loans typically imply60

A key problem is that we have no acceptedframework in which a country in extremis canimpose a payments suspension or standstillpending agreement with its creditors to supportthe restoration of viabilitymdashwhich takes us toAnne Kruegerrsquos proposal for a Sovereign DebtRestructuring Mechanism (SDRM) a legalmechanism to approve payments standstills bysovereign nations and for the restructuring andif necessary writing down of sovereign debts61

The costs of resorting to such measures haveto be high if the international nancial system isto work well If creditors believe that emerging-

market debtors will too easily use legal provi-sions to restructure debts spreads will rise andcapital ows to those countries will declineThat is why policymakers from emerging-market countries generally oppose proposalsto make it easier for them to restructure theirpayments be it through collective-actionclauses or the creation of a sovereign bank-ruptcy procedure

Based on their behavior during the last de-cade I believe it unlikely that emerging-marketeconomic of cials will be encouraged to defaultby the presence of an SDRM though some ofthem fear that it would change the balance offorces within the country encouraging populistforces that often favor repudiating debtsRather an SDRM would be more likely toaffect the behavior of the IMF and the of cialsector which could become too quick to urgerestructurings as an alternative to IMF lendingThere is a balance to be struck and it is impor-tant for the effective operation of the interna-tional system that the IMF not step back fromproviding nancing to countries facing a liquid-ity crisis

The SDRM proposal has already achievedsuccess in leading the private sector to sup-port the inclusion of collective active clauses(CACrsquos) in bond contracts It is certainly desir-able that the IMF continue its important workon the mechanism But we should recognizethat at best it will take years to change the legalframework and that it is quite possible that itwill not in the end be possible to persuade theUS Congress on this issue In any case Ibelieve the Executive Board of the IMF shouldcontinue seeking to spell out more precisely aset of procedures for how it will act in the eventit concludes that a country has an unsustainablelevel of debt This would help formalize theapproach that has already been developed on anad hoc basis in response to some of the recentcrises At the very least it would provide moreclarity on the question for debtors and creditorsalike which would be a good in itself

Let me turn next to what the emerging-market countries can do to reduce their vulner-ability The crises of the last decade can be seenas the manifestation of the impossible trinity inthe emerging markets 25 years after the BrettonWoods system succumbed to the same forces

59 The experience of Argentina so far in its current crisissuggests that creditor legal action following a default maybe less disruptive than many including me had anticipated

60 It is the judgment of how far to go to help a countrythat seeks to avoid a default and of what probability ofsuccess to require that lies behind the controversies overrecent IMF support for Turkey its decision to supportArgentina in August 2001 and not to provide further sup-port in December 2001

61 National bankruptcy laws should apply to private-sector debtors who cannot make payments if debtors canpay in local currency the stay could permit a delay inconverting these payments into foreign currency

18 AEA PAPERS AND PROCEEDINGS MAY 2003

The adoption of exible exchange-rate systemsby most emerging-market countries is by farthe most important emerging-market crisis-prevention measure taken in response62 Inchoosing a new nominal anchor to replace theexchange rate most countries have (wisely Ibelieve) opted for in ation-targeting

However exchange-rate exibility is not suf- cient to prevent crises for a country maynonetheless get into trouble because of marketdoubts about its ability to service its debt Thisis the main cause of the 2002 crisis in BrazilEven with a exible exchange rate excessiveindebtedness of either the public or the privatesector and weaknesses in the nancial sectormake a country more vulnerable to both internaland external shocks

Hence countries wishing to operate in theinternational capital markets need both tostrengthen their nancial systems and to ensurethat their scal policies are sustainable Fiscalsustainability requires not only that the debt toGDP ratio will stabilize if things go well butalso that the debt will be sustainable (possiblywith the assistance of policy adjustments andthe IMF) if the economy is hit by shocksFiscal-sustainability criteria for emerging-marketcountries have not yet been de ned However itis likely that the Maastricht 60-percent debt-to-GDP threshold ratio is too high for countriessubject to much larger interest-rate and otherexternal shocks than are the industrializedcountries63

In criticizing IMF-supported programs it isoften remarked that industrialized countries cancut interest rates and run expansionary scal

policies when in recession but that the IMF doesnot recommend a similar course for emerging-market countries in crisis If a country in crisishas a strong scal position and has no problemborrowing then it can indeed run a more ex-pansionary scal policy64 But many emerging-market countries that enter IMF programs are ina debt crisis in which they cannot borrow fromthe market and high interest rates are addingto adverse debt dynamics The country cannotincrease market borrowing in these circum-stances65 and the international nancial institu-tions (IFIrsquos) do not usually have enoughresources to more than offset the contractionsimposed by the markets Thus scal policy hasto be tightened if the country is to avoid adefaultmdashas virtually every country in crisis des-perately wants to do

As to monetary policy if the country has fewdebts denominated in foreign currency and in- ation is low then it can cut interest rates andallow the currency to depreciate If however itscurrency is plunging then a rise in interest ratesis more likely than an interest-rate cut to slow orstop the collapse66

As already discussed in adapting themselvesto living in the international nancial systemcountries need also to be cautious about whenand how they liberalize capital-account transac-tions Other measures include greater transpar-ency about both data and the intentions of thegovernment and the adoption of international

62 By a exible exchange-rate system I do not mean apurely oating rate but rather a system in which the au-thorities may intervene to affect the rate but are not per-ceived as trying to defend a particular rate or narrow rangeof rates

63 Several economists have pointed to what they call theoriginal sin of emerging-market borrowers that they areunable to borrow internationally in their own currencies AsEichengreen and Ricardo Hausmann (2002) explain hadBrazil been borrowing in its own currency investor uncer-tainty that caused the real to plummet would mainly haveled to more competitive Brazilian exports rather than alarge increase in debt-servicing costs I see no simple solu-tion to the original-sin problem beyond establishing arecord that encourages creditors to accept the risks of lend-ing in emerging-market currencies

64 As noted in Jack Boorman et al (2000) the initialprograms supported by the IMF in Asia where governmentindebtedness was generally low tightened scal policyexcessively though policy was relaxed within a shorttime Policy was tightened because it was believed thiswould strengthen market con dence and would serve as adown-payment on the expected costs of nancial-sectorrestructuring

65 Mindful of the dif culties caused by tightening scalpolicy in a recession the IMF in late 2000 agreed withArgentina on a small scal expansion as a contribution torecovery Political economy is complicated we were told bysome Argentines at the time that this was a mistake notbecause Keynes was wrong but because the governmentwould use the extra room given by the IMF support toincrease the de cit by more than the agreed amount Theyturned out to be right

66 However at some point further increases in the in-terest rate become counterproductive because they makedebt dynamics worse and weaken the nancial conditions ofboth nancial and non nancial corporations

19VOL 93 NO 2 RICHARD T ELY LECTURE

codes and standards with regard to the nancialsystem scal- and monetary-policy transpar-ency accounting standards corporate gover-nance and so forth

E The International Trading System

Reductions in tariffs and the growth in tradein the past half century have been greater amongthe OECD countries than between industrial-ized and developing countries In particular asis well known agricultural protection in theEuropean Union the United States and Japandiscriminates against those goods in whichmany developing countries are relatively mostef cient and limitations on textiles exports(which are due to be removed in 2005) have asimilar effect Figure 7 illustrates this trade pro-tection of manufacturing and agriculture inhigh-income countries

The international trading system is biasedagainst developing countries In the wake ofSeptember 11 the Doha Round of trade nego-tiations was inaugurated and named ldquothe devel-opment roundrdquo It remains to be seen whetheragricultural subsidization and protection in theindustrialized countries will be lifted andwhether antidumping regulations and other non-tariff barriers will be eased To be sure reduc-ing agricultural protection is politically dif cultin the industrialized countries but absent such

changes the world trading system will remainunfairly tilted against the developing countries

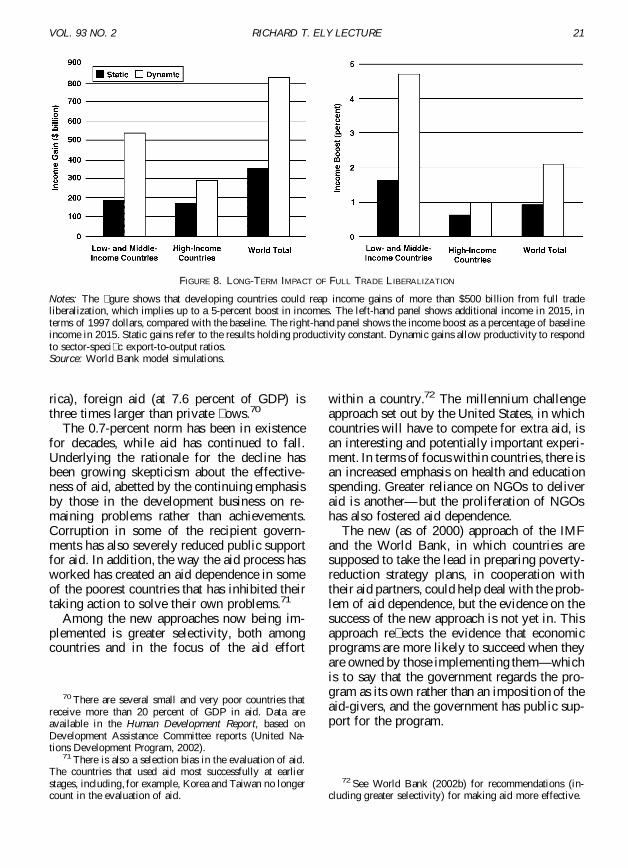

Figure 8 shows the results of a World Bankmodel simulation which examines the long-term impact of full trade liberalization67 Thedynamic gains calculation assumes that open-ness affects productivity With or without thiseffect the gains are impressive and are greaterrelatively and even absolutely for the develop-ing countries than for the industrialized coun-tries Nearly half the bene ts for the developingcountries come from the liberalization of agri-cultural trade

One other result bears emphasis A consistent nding of such studies is that at least half thegains for the developing countries derive fromgreater intra-developing-country trade that isSouthndashSouth trade In other words the devel-oping countries would bene t not only from theindustrialized countries opening up to their ex-ports but also from opening up their markets toeach other

Of the many measures that could be takento make the international system work betterand more fairly removing the bias againstdeveloping-country exports and further SouthndashSouth trade liberalization would be among themost effective

F Aid

Over the period 1990ndash2000 the percentageof their GDP given as aid by industrializedcountry governments fell from 033 percent to022 percent68 The total amount of aid is about$60 billion and donor governments are com-mitted to seeking to raise aidrsquos share of theirGDP by 2015 The share of 07 percent is anorm but only Scandinavian countries and theNetherlands come close to meeting this ratio(and they all exceed it)69 For the developingcountries as a whole net private capital owsfar exceed aid But for the group of the 44least-developed countries (32 of them in Af-

67 These results are presented in Global Economic Pros-pects 2003 (Ch 6)

68 Net grants by NGOs added another 003 percent ofdonor GDP to the total in each year

69 In 2002 Luxembourg gave 071 percent of its GDP inaid

FIGURE 7 TRADE PROTECTION IN INDUSTRIAL COUNTRIES

Note The gure shows tariffs on merchandise imported byhigh-income countries (as percentages) in 1995Source Global Economic Prospects 2003 (Ch 6)

20 AEA PAPERS AND PROCEEDINGS MAY 2003

rica) foreign aid (at 76 percent of GDP) isthree times larger than private ows70