global outlook - institutional dialogue · global outlook paul domjan (ceo), 4cast-rge 18 october...

TRANSCRIPT

Global outlook

Paul Domjan (CEO), 4CAST-RGE18 October 2016

Source: Roubini Global Economics

Muddle-through “new abnormal”

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Base Case - 55% Upside Case - 5% Adverse Case - 40%

Modest Divergent, Muddle-Through New Abnormal

Growth Acceleration, Deleveraging Delayed (&

Unnecessary)

Negative Feedback Loop & Outflows

Scenario

• Output gaps closegradually.

• EMs grow below pre-crisis pace with slow reforms.

• Slow hikes in U.S. and most EMs., EZ continues to ease.

• Demography, poor reform pace stunt potentialgrowth globally.

• Political risks dampen investment

• Inflation modest.

• Above-potential growth in most DMs, spurred by pro-business and pro-labor policies, investment, productivity and wage growth reverse hysteresis.

• EM reforms support sustainable growth, including China.

• Inflation moderate as central banks exit ZIRP.

• Tighter financial conditions increase risk of slowdown/recession.

• European turmoil post-Brexit, and/or

• Sharp China slowdown, and/or

• EM outflows cause weakness, downgrades, selected defaults, capital controls.

• Deflation risks.

GDP 2016 (PPP)

3.2% 4.0% or higher 2% or lower

Source: Roubini Global Economics.

3

Likely expansionary fiscal measures and multiplier

roubini.com | [email protected] Tel: 212.645.0010 | [email protected] Tel: +44 (0) 20 7092 8850 | [email protected] Tel: +65 6434 8890

Red denotes a change from our original analysis in February 2016. Fiscal Multipliers are estimated by RGE using our global econometric model.

Will Won't Fiscal multiplier

Japan X 1.17

U.S. X 0.95

Spain X 0.76

Norway X 0.69

Canada X 0.6

Indonesia X 0.59

UK X 0.57

France X 0.56

Italy X 0.51

Germany X 0.44

Sweden X 0.41

Turkey X 0.41

Switzerland X 0.32

S. Korea X 0.32

China X 0.18

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

US Politics & Economics

5

The Senate is a near to a toss-up

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Source: FiveThirtyEight

6

Can he do that? Imagining a Trump presidency

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Trumps’ Promises

Can he do that?

Withdraw from NAFTA

Yes. Entering / exiting trade agreements are generally powers of the president

Change U.S. FX policy

Yes. FX policy is the responsibility of the executive branch, exercised through the Treasury Department. The president can order the Treasury to undertake FX intervention.

Take the U.S. into war

Yes, but only because Congress has granted that power to the president. Constitutionally, Congress has this power but historically have delegated to the president

“Tear up” the Iran nuclear deal?

Sort of. Trump could pull the U.S. out of the agreement, but could not require other parties to the deal to pull out. He could also reinstate U.S. sanctions.

Ban Muslim immigration

Sort of. Presidents may suspend entry of people/groups that “would be detrimental to the interests” of the US. However, a ban on Muslims would likely be challenged on a number of constitutional grounds (e.g. 1st amendment bans religious discrimination)

Source: Roubini Global Economics

7

Can he do that? Imagining a Trump presidency

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Trumps’ Promises

Can he do that?

Order a nuclear strike

Yes - The president has sole authority to order a nuclear strike.

Build a border wall

Maybe. If Congress authorizes the expense of a wall, Trump can build it. If Congress declines, Trump could use part of the security budget, but that might be challenged in the courts.

Force China to change trade / FX policies

No, but just as in the case of getting Mexico to pay for a border wall, Trump has suggested restrictions on trade as a tool to force China to act.

Overturn Dodd-Frank

No. However, the executive powers of the President include supervision of most federal regulatory agencies, which are charged with enforcing provisions of the Dodd-Frank Act.

Change fiscal policy

No, not in a direct way. Presidents propose budgets, but Congress writes the actual budget and passes it. The president can veto the budget and suggest changes, but it is still up to Congress to determine tax and spending levels.

Source: Roubini Global Economics

In the U.S., consumers are the whole story…

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

30%

31%

32%

33%

34%

35%

36%

66%

67%

68%

69%

70%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Consumers' share of GDP (left axis) Everything else (right axis)

Source: Roubini Global Economics, Haver

…but consumer spending has recently outpaced job gains

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

90

140

190

240

290

340

2012 2013 2014 2015 2016

Average Monthly Job Gain (Left Axis) Consumer Spending Growth (Right Axis)

This gap is a worry

Source: Roubini Global Economics, Haver

15%

20%

25%

30%

35%

1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Government Consumption % of GDP

Canada U.S. Germany UK

11

Government consumption expenditure on the rise

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Trudeau Government'sFiscal Stimulus So Far

Source: Roubini Global Economics, Haver

12

House prices have surged above trend

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

50

70

90

110

130

150

170

190

210

2000 2001 2002 2003 2004 2005 2007 2008 2009 2010 2011 2012 2014 2015 2016

Teranet Housing Price Index Trend

Source: Roubini Global Economics, Haver

14

Consumption still the main driver of Chinese growth

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

-2

0

2

4

6

8

10

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16

Contributions to change in real GDP (%, YTD, NSA)

Final Consumption Gross Fixed Capital Net Exports GDP growth y/y)

Source: Roubini Global Economics, Haver

15

CNY is now weakening against its basket

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

600

650

700

750

800

8500

20

40

60

80

100

120

140

Mar2013

Jun2013

Sep2013

Dec2013

Mar2014

Jun2014

Sep2014

Dec2014

Mar2015

Jun2015

Sep2015

Dec2015

Mar2016

Jun2016

CFETS (end 2014=100) RMB Exchange Rate: United States (Yuan/100 US$; right axis) CNY/EUR (right axis)

Source: Roubini Global Economics, Haver Analytics

16

Yuan depreciation no longer damaging financial markets?

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

2.5%

2.7%

2.9%

3.1%

3.3%

3.5%

3.7%

6.2

6.3

6.4

6.5

6.6

6.7

6.8

Jan-2015 Apr-2015 Jul-2015 Oct-2015 Jan-2016 Apr-2016 Jul-2016

CNY/USD (4-wk avg, left axis) Baa/Treasury Yield Spread (4-wk avg, right axis)

This decoupling of risk away

from CNY reflects reduced

concern about China’s near-

term macro performance

Source: Roubini Global Economics, Haver Analytics

So far not as bad as feared, but too early to tell

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

35

40

45

50

55

60

65

70

Feb-13 Aug-13 Feb-14 Aug-14 Feb-15 Aug-15 Feb-16 Aug-16

Purchasing Managers Index (>50 = expansion)

Manufacturing PMI Services PMI Construction PMI

Referendum

Source: Source: IHS Markit/CIPS

0

0.005

0.01

0.015

0.02

0.025

0.03

0.035

2013 2014 2015 2016 2017 2018 2019 2020

GDP Growth (% y/y)

RGE forecast (13 Jun 2016) RGE forecast (19 Sept 2016) Historic

Growth still likely to suffer, at least in the short term

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Pre-Brexit forecast

Post-Brexit forecast

Source: Roubini Global Economics,

UK now expected to loosen fiscal policy

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

-£50

£0

£50

£100

£150

£200

Full year PSNB (bns) March 2016 Budget 2016 Autumn Budget (expected)

But Public-Sector Net Borrowing (PSNB) should remain on a downward

(albeit flatter) trajectory

Fiscal policy options• Infrastructure spending• VAT & corporate tax cuts• Housing market reform

Source: Roubini Global Economics, OBR

Our 10-year Europe scenarios (introduced July 2015)

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

More integratedLess integrated

More flexible / diverse

Less flexible / diverse

Nation StatesDisunity & rigidities, nation states

regain sovereignty through EU exits, possibly in a disorderly

fashion.

‘Germanification’More integration but less flexibility.

Led by Germany, EU members forced into current account &

budget surpluses.

Transfer UnionEurope integrates & becomes more

flexible internally. Nation states lose significance in favour of cross-

border blocs.

Customs UnionCountries regain some national

sovereignty in the context of the single market / free trade

agreements.

Source: Roubini Global Economics, Haver

Events over the last 12 months…

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Talk of debt relief for Greece

Catalan independence

Renzi’s reformsSlow progress on EZ

deposit insurance

Single EZ Treasury discussions

Turkey pact & post-coup crackdown

Portugal’s “Anti” government

Nearby wars

Brexit voteMore fiscal flexibility

Capital Markets Union progress

Flexibility in bank bail-in rules

Unorthodox ECB policy

Suspension of Schengen

No Spanish government

Bail-in dogma

Greek bailout conditions

Rise of populism

Migrant crisis

Increased terrorism

…have shifted the odds (in the “wrong” direction)

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Nation StatesDisunity & rigidities, nation states

regain sovereignty through EU exits, possibly in a disorderly

fashion.

‘Germanification’More integration but less flexibility.

Led by Germany, EU members forced into current account &

budget surpluses.

Transfer UnionEurope integrates & becomes more

flexible internally. Nation states lose significance in favour of cross-

border blocs.

Customs UnionCountries regain some national

sovereignty in the context of the single market / free trade

agreements.

15%

10%

45%

40%

20%

10%

--30%

30%

Source: Roubini Global Economics, Haver

The next 12 months contains numerous risk events

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Date Event

Oct 2 2016 Austria: Repeat of presidential elections

Oct 2 2016 Hungary: Referendum on refugee quotas

Nov 8 2016 U.S: Presidential election

Nov 20 2016 Italy: Constitutional referendum (could trigger general election)

Dec 2016 Spain: Possible elections if a govt can’t be formed

April/May 2017 France: Presidential election

June 2017 France: Parliamentary election

Sept 2017 Germany: Federal election

Source: Roubini Global Economics, Haver

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Equity Market Implications

27

Real GDP growth forecasts

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

RGE forecast

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2016 2017 2018 2019 2020 2021 2022 2023

RGDP y/y %

France Germany Great Britain (UK) Italy

Japan Spain Switzerland United States

28

FX forecasts (e.o.p)

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

0

20

40

60

80

100

120

140

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

EUR/GBP EUR/USD EUR/CHF GBP/USD USD/JPY (right axis)

RGE forecast

27 21

13 15 169 10

21

0

20

40

60

80

100Cyclically Adjusted Price to Earnings (Shiller PE)

Current CAPE

Equity valuations historically except in U.S., Switzerland

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Historic range

75th percentile

Median

25th percentile

Source: Research Affiliates, Roubini Global Economics

30

The long view: secular stagnation

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

10

100

1,000

10,000

100,000Dow

Dow

20 years

20 years

"only" 14 years (Dow) ...

WW1

Oil Shock 1

Credit Crunch 1

'42 ~ '65 Reflation epoch(19% annualised)

Stagnation Epoch

'82 ~ '98 Free-Market epoch(15% annualised)

4CAST-RGE contact details

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Editorial SuggestionsTo suggest new coverage, resources or content to RGE, email our research team at [email protected].

General InformationRGE welcomes your feedback. Please send us your comments or questions via email at [email protected].

Technical SupportFor technical support or questions about using our site, please contact [email protected].

AmericasSuite 2147

420 Lexington AvenueNew York, NY 10170

T: +1 212 897 6777F: +1 212 897 6776

EMEA (Head Office)8th Floor

52 Grosvenor GardensLondon, SW1W 0AU

T: +44 207.092.8850F: +44 [email protected]

Asia Pacific24 Raffles Place

21-04 Clifford CentreSingapore, 048621

T: +65 6236 1600F: +65 6236 [email protected]

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Back-up slides

U.S. jobs data weakens the case for a fed hike

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

1.6%

1.8%

2.0%

2.2%

2.4%

2.6%

2.8%

4.5%

5.0%

5.5%

6.0%

6.5%

7.0%

Unemployment rate (left axis) Average Hourly Earnings (right axis)

Stall in unemployment rate’s downward trend means a stall

in wage gains

Source: Roubini Global Economics, Haver

34

After a strong start to the year, credit growth easing

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

-10,000

0

10,000

20,000

30,000

40,000

50,000Three-month moving average (million CNY)

RMB Bank Loans FX Bank Loans Corporate Bonds

Source: Roubini Global Economics, Haver Analytics

Fiscal space does exist in the Eurozone to help cushion risk

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Four components of ‘Fiscal Space’ France Germany Italy Spain

Primary Balance >

Debt stabilizing primary balance

2016

2017

2018

Real Growth > Real Interest Rate

2016

2017

2018

Contingent Liabilities (Structural) NPV (2015-50)

Contingent Liabilities (Banking Sector)

FISCAL SPACE

Source: Roubini Global Economics

Have space

Limited space

Low/No space

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2013-Q1

2013-Q3

2014-Q1

2014-Q3

2015-Q1

2015-Q3

2016-Q1

2016-Q3

2017-Q1

2017-Q3

2018-Q1

2018-Q3

2019-Q1

2019-Q3

GDP Growth (%)

Q/Q (RHS) Q/Q BoE Forecast AUG 2016 (RHS)

Y/Y Y/Y BoE Forecast AUG 2016

UK recession risk highest around turn of the year

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Source: BoE, 4CAST-RGE

Sentiment / confidence more important than institutional

arrangements in the short term

Unemployment falling where reforms implemented

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777 37

Source: Roubini Global Economics, Statistical Office of the European Communities

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Jan-2000 Dec-2001 Nov-2003 Oct-2005 Sep-2007 Aug-2009 Jul-2011 Jun-2013 May-2015

Harmonized unemployment rate (SA, %)

EZ France Germany Italy Spain UK

France is the exception

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777 38

Source: Roubini Global Economics, Statistical Office of the European Communities

0.0

5.0

10.0

15.0

20.0

25.0

30.0

Mar-2000 Jan-2002 Nov-2003 Sep-2005 Jul-2007 May-2009 Mar-2011 Jan-2013 Nov-2014

Metropolitan France: unemployment rate (%) by age group

Total 15-24 25-49 50+

Will it be enough to produce a Le Pen Presidency?

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777 39

Source: Roubini Global Economics, TNS Sofre, BVA, Odoxa - latest available polls (April – September 2016)

Polls suggest Marine Le Pen will (easily) make

it to the 2nd round…

11%

12%

15%

25%

29%

François Hollande

Jean-Luc Mélenchon

Emmanuel Macron

Alain Juppé*

Marine Le Pen

…but (so far) head-to-heads suggest she

would struggle to win

Hollande47%

Sarkozy58%

Macron61%

Juppe68%

Le Pen53%

Le Pen42%

Le Pen39%

Le Pen32%

…unless she’s running against the

sitting President!

*Le Pen still comes first with Sarkozy instead

of Juppe as the Republicain candidate

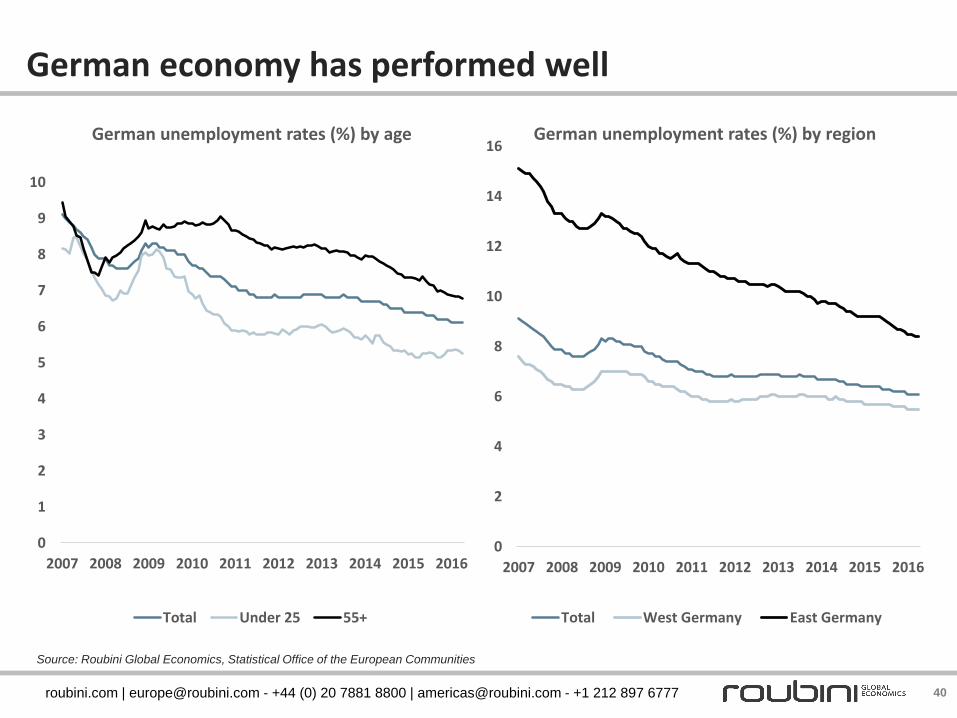

German economy has performed well

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777 40

Source: Roubini Global Economics, Statistical Office of the European Communities

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

German unemployment rates (%) by age

Total Under 25 55+

0

2

4

6

8

10

12

14

16

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

German unemployment rates (%) by region

Total West Germany East Germany

Germany - Putting AFD support into perspective

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777 41

Source: Roubini Global Economics, Statistical Office of the European Communities

0

5

10

15

20

25

30

35

40

45

50

Oct 2013 Jan 2014 Apr 2014 Jul 2014 Oct 2014 Jan 2015 Apr 2015 Jul 2015 Oct 2015 Jan 2016 Apr 2016 Jul 2016

Opinion polls since 2013 Federal election (6-poll rolling average, %)

CDU/CSU Social Democratic Party The Left

Green Party Free Democratic Party Alternative for Germany

Despite a drop in support

the two main parties are still

dominant nationally

Germany - Putting AFD support into perspective

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777 42

Source: Roubini Global Economics, INSA/YouGov

While the AFD (currently) appears to have

little chance of being part of the next

government.

CDU/CSU

CDU/CSU

SDP

SDP

Left

Left

Green

Green

FDP

FDP

AFD

AFD

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Election 2013

Poll 5 Sept 2016

Renzi attempting to increase Executive stability

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

New Electoral Law for the Chamber of Deputies (lower house)

Constitutional Referendum to Reform the Senate (upper house)

Introduces proportional representation through a list system in 100 constituencies.

Reduces size & limits the Senate’s legislative power (currently has equal power as the lower house).

The list with the most support nationally (provided it is above 40%) receives 340/630 seats (54%), ensuring a majority.

Members no longer elected; to be selected by regions from councilors & local mayors.

If no list achieves 40%, there will be a run-off between the two most popular lists.

The Senate will no longer have the ability to pass votes of (no) confidence in the government.

If the Senate reforms are not approved, the new electoral law will be repealed.

Step 1: Passed in 2015 Step 2: Oct/Nov 2016

For example, Italy’s constitutional referendum…

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Renzi loses & resigns

A caretaker / technocratic government passes budget & calls elections (under the old

rules)

Renzi loses & remains

But lacks credibility & is ineffective. Would probably

be forced to call early elections (under the old rules)

Renzi wins

Calls elections under new electoral rules (probably H1

2017) to try & secure his mandate for reform

Regardless of the referendum outcome, Italy will hold elections at some point in the next 20 months, potentially as early as Q1 2017…

…and subsequent elections

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

1. Partito Democratico (PD) + allies win

Continue with reform plan (pace depends on margin of victory and which electoral rules)

3. Five Star Movement win and don’t moderate

Pursue radical objectives of their movement including a potential EUR referendum

2. Five Star Movement win but moderate

Implement some minor reforms (e.g. basic income) but avoid any major upheavals

Increases odds EU survives

Increases odds of EU break-up

‘German-ification’

Transfer Union

Customs Union

Nation States

EZ rigidity – Government budget balances

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Source: Roubini Global Economics, Haver

-10.0

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Primary surplus (ex interest) as % of potential GDP

EA 19 France Germany Italy Spain

47

Housing stock tends and prices tend to move in sync

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Teranet Housing Price Index Y/Y % Housing Stock Y/Y %

Source: Roubini Global Economics, Haver

60

80

100

120

140

160

180

2010 2011 2012 2013 2014 2015 2016

Eurozone CAPE (Jan 2010 = 100, 4m rolling average)

Healthcare

Consumer discretionary

Financials

Industrials

Telecoms

Energy

Utilities

Materials

Eurozone sectoral CAPE – Flat or rolling over

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Source: Barclays, Roubini Global Economics

60

80

100

120

140

160

180

2010 2011 2012 2013 2014 2015 2016

Eurozone CAPE (Jan 2010 = 100, 4m rolling average)

Information technology

Consumer staple

Eurozone sectoral CAPE – Expanding

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Source: Barclays, Roubini Global Economics

50

Sequential trend easing in H2 2016

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

0

5

10

15

20

25

-25

-20

-15

-10

-5

0

5

10

15

20

25

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Retail sales (QSAA, left axis) Retail sales (y/y, right axis)

Source: Roubini Global Economics, Haver

51

Chinese liquidity surge has breathed life into property

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

-30

-20

-10

0

10

20

30

40

50

60

70

80

Nov-11 Apr-12 Sep-12 Feb-13 Jul-13 Dec-13 May-14 Oct-14 Mar-15 Aug-15 Jan-16 Jun-16

Three-month moving average (%, y/y)

Volume of Property Sold Value of buildings sold

Investment in residential construction Prices

Source: Roubini Global Economics, Haver Analytics

Request More Information

and

Disclaimer/Terms & Conditions

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Terms & Conditions / Certification / Disclaimer

roubini.com | [email protected] - +44 (0) 20 7881 8800 | [email protected] - +1 212 897 6777

Terms and Conditions

• RGE analysis is the property of 4CAST-RGE LIMITED (company number: 10179978) for the internal use of RGE clients. Any redistribution, including summarizations or synopses, is expressly prohibited without prior agreement from RGE. All rights reserved, 4CAST-RGE LIMITED. For questions about reprints or permission to excerpt or redistribute RGE content, clients should contact their RGE account representative.http://www.roubini.com/tos

Analyst Certification

• I Paul Domjan certify that the views expressed herein are mine and are clear, fair and not misleading at the time of publication. They have not been influenced by any relationship, either a personal relationship of mine or a relationship of the firm, to any entity described or referred to herein nor to any client of RGE nor has any inducement been received in relation to those views.

• I further certify that in the preparation and publication of this report I have at all times followed all relevant RGE compliance protocols including those reasonably seeking to prevent the receipt or misuse of material non-public information.

Disclaimer

• 4CAST-RGE LIMITED and all of its affiliates (hereafter, RGE) do not conduct “investment research” as defined in the FCA Conduct of Business Sourcebook (COBS) section 12 nor do they provide “advice about securities” as defined in the Regulation of Investment Advisors by the U.S. SEC.RGE is not regulated by the SEC or by the FCA or by any other regulatory body.

• This research report has not been prepared in accordance with legal requirements designed to promote the independence of investment research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Nonetheless, RGE has an internal policy that prohibits “front-running” and that is designed to minimize the risk of receiving or misusing confidential or potentially material non-public information.

• The views and conclusions expressed here may be changed without notice. RGE, its partners and employees make no representation about the completeness or accuracy of the data, calculations, information or opinions contained in this report. This report may not be copied, redistributed or reproduced in part or whole without RGE’s express permission.

• Information contained in this report or relied upon in its construction may previously have been disclosed under a consulting agreement with one or more clients. The prices of securities referred to in the report may rise or fall and past performance and forecasts should not be treated as a reliable indicator of future performance or results. This report is not directed to you if RGE is barred from doing so in your jurisdiction. Nor is it an offer or solicitation to buy or sell securities or to enter into any investment transaction or use any investment service.

© 4CAST-RGE LIMITED (company number: 10179978) 2016

No reproducing or redistribution without written consent.