global leadership india can do it telecom r.sai santosh

TRANSCRIPT

Global Leadership – India can do it.

Telecom

• Telecom – Historical Development & Industry Overview

• India’s connection to Global Telecom Leadership

• Mobile leading Telecom growth in India

• India Telecom poised for Global Leadership – Why India can do it

• Reliance’s contribution to Indian Telecom’s Global leadership

Index

Telecom – Historical Development & Industry Overview

• Telecom is considered a basic infrastructure industry, critical for and integral to a country’s growth

• Various studies by World Bank & LBS suggest that increase in Teledensity leads to rapid growth in country’s GDP

(US $1 investment in telecom leads to US$ 6 increase in GDP)

Telecom Industry Overview

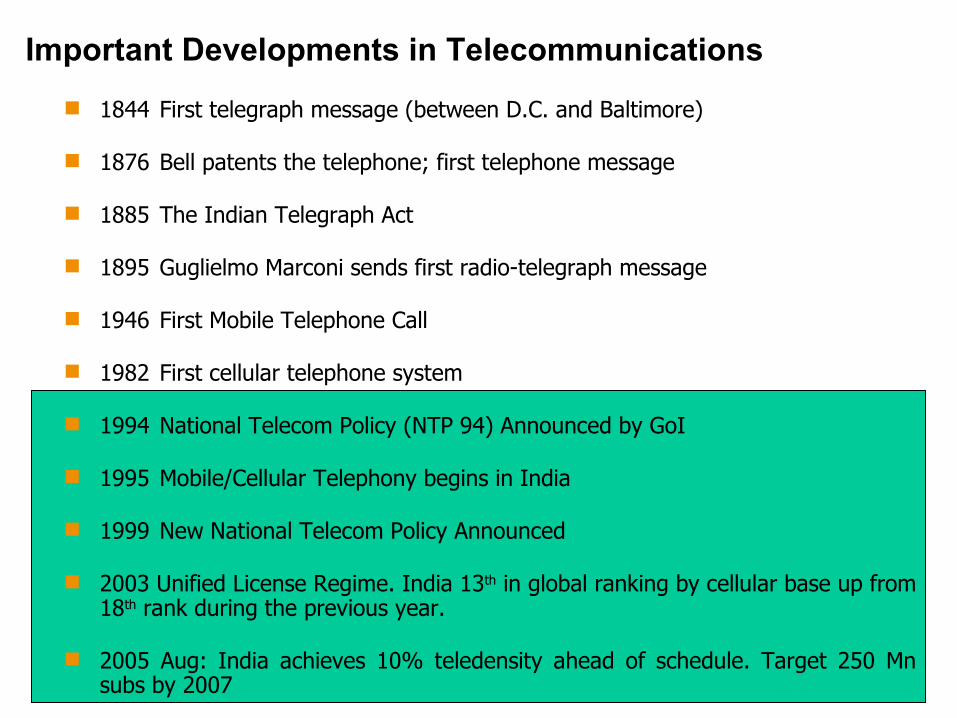

Important Developments in Telecommunications

1844 First telegraph message (between D.C. and Baltimore)

1876 Bell patents the telephone; first telephone message

1885 The Indian Telegraph Act

1895 Guglielmo Marconi sends first radio-telegraph message

1946 First Mobile Telephone Call

1982 First cellular telephone system

1994 National Telecom Policy (NTP 94) Announced by GoI

1995 Mobile/Cellular Telephony begins in India

1999 New National Telecom Policy Announced

2003 Unified License Regime. India 13th in global ranking by cellular base up from 18th rank during the previous year.

2005 Aug: India achieves 10% teledensity ahead of schedule. Target 250 Mn subs by 2007

India’s connection to Global Telecom Leadership

India’s connection to Global Telecom Leadership

JC Bose is credited with simultaneous invention of Telegraph, independent of Marconi of Italy

World’s 1st sea cable for telegraph messages was between India & England (Calcutta to London)

Among top-5 private Indian companies with over Rs. 1 Lakh Cr. Market Cap, two are telecom operators. Both are also among top-6 Asian Telecom operators

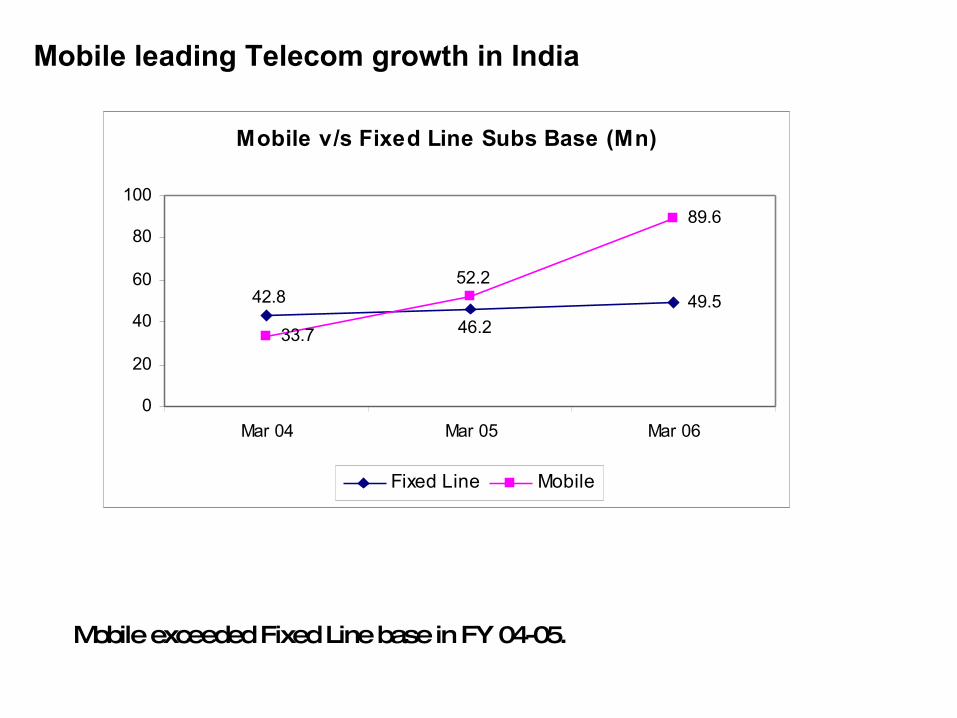

Mobile leading Telecom growth in India

Mobile leading Telecom growth in India

Mobile exceeded Fixed Line base in FY 04-05.

Mobile v/s Fixed Line Subs Base (Mn)

49.5

33.7

89.6

46.2

42.852.2

0

20

40

60

80

100

Mar 04 Mar 05 Mar 06

Fixed Line Mobile

India – The mobile juggernaut rolls

17.5 20 28

60

0.03 0.22 0.8 1.1 1.6 3.1 5.510.5

28

48

76

136

0

20

40

60

80

100

120

140

160

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Mill

ions

Net Ads Cum Subs

RCL – Soft launch on 28th Dec 02 and

Commercial launch on May 1 2003

•Indian Mobile growth on a J curve•Reliance’s entry stimulates mobile market growth.•Subscriber numbers grown over 12 times in last 4 years.

Indian mobile market at an inflection point

India Telecom – Elements of Global Leadership & Why India can do it

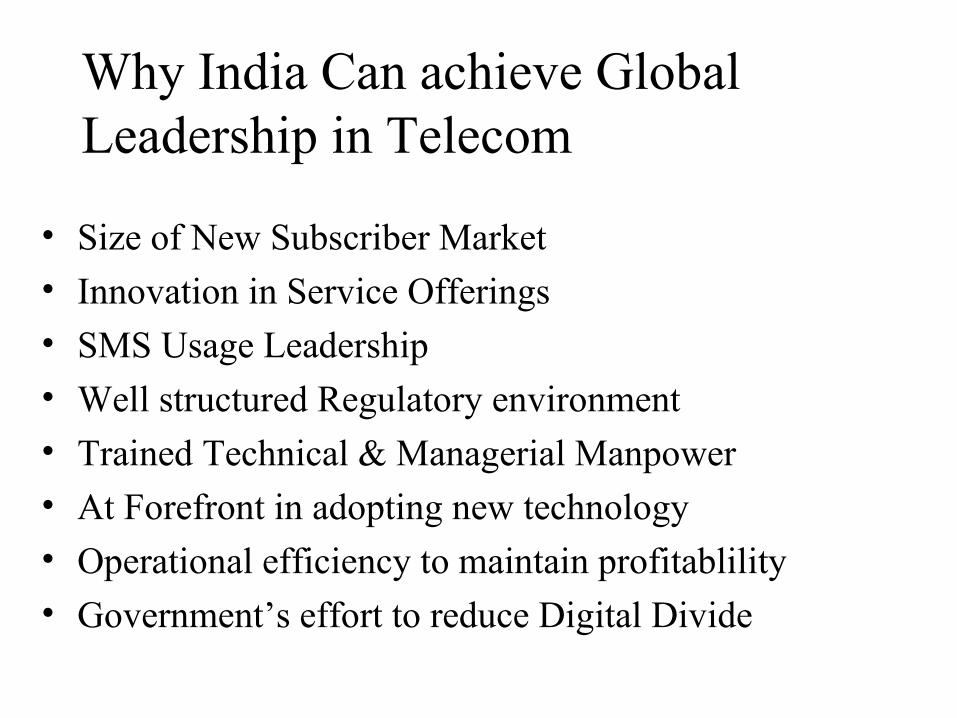

Why India Can achieve Global Leadership in Telecom

• Size of New Subscriber Market• Innovation in Service Offerings• SMS Usage Leadership• Well structured Regulatory environment• Trained Technical & Managerial Manpower• At Forefront in adopting new technology• Operational efficiency to maintain profitablility• Government’s effort to reduce Digital Divide

• Half a billion consuming class by 2007.

• A historical 5-6 year lag vs. China - Current base to grow to 250mn by 2008

• Expected to add 6-7 million subs per month consistently.

20%16%0.3%China

2.9%1.2%-India

20%19%1.6%World

200320021995

• An underserved market.

Current teledensity at only 18%

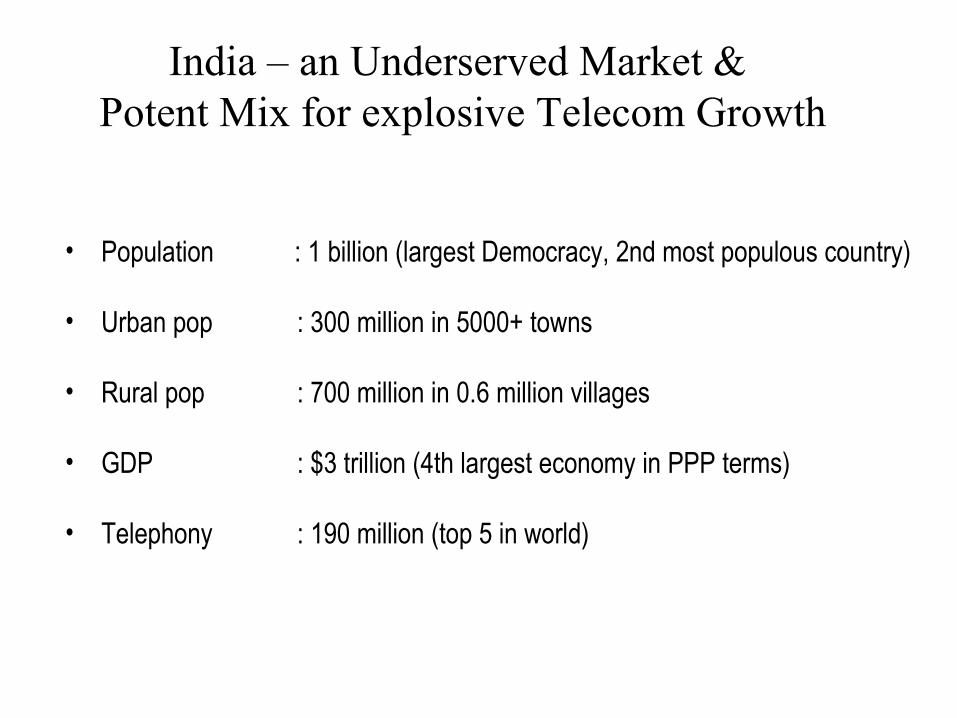

India – an Underserved Market & Potent Mix for explosive Telecom Growth

India – an Underserved Market & Potent Mix for explosive Telecom Growth

• Population : 1 billion (largest Democracy, 2nd most populous country)

• Urban pop : 300 million in 5000+ towns

• Rural pop : 700 million in 0.6 million villages

• GDP : $3 trillion (4th largest economy in PPP terms)

• Telephony : 190 million (top 5 in world)

Indian Telecom – Net Adds Leader;Poised for phenomenal growth

43

85

145

207

279

335

388

0.03 0.22 0.8 1.1 1.6 3.1 5.5 10.528

4876

136

13.224

0

50

100

150

200

250

300

350

400

450

Yr 1 Yr 2 Yr 3 Yr 4 Yr 5 Yr 6 Yr 7 Yr 8 Yr 9 Yr 10 Yr 11 Yr 12 Yr 13 Yr 14 Yr 15 Yr 16 Yr 17 Yr 18

Mill

ions

China India

• India’s Historical 5-6 year lag to China• China, after peaking at 6 Mn, has come down to 5 Mn net adds pm• India has already overtaken China and reached nearly 7 Mn net adds pm• India destined to close the gap with China subs base

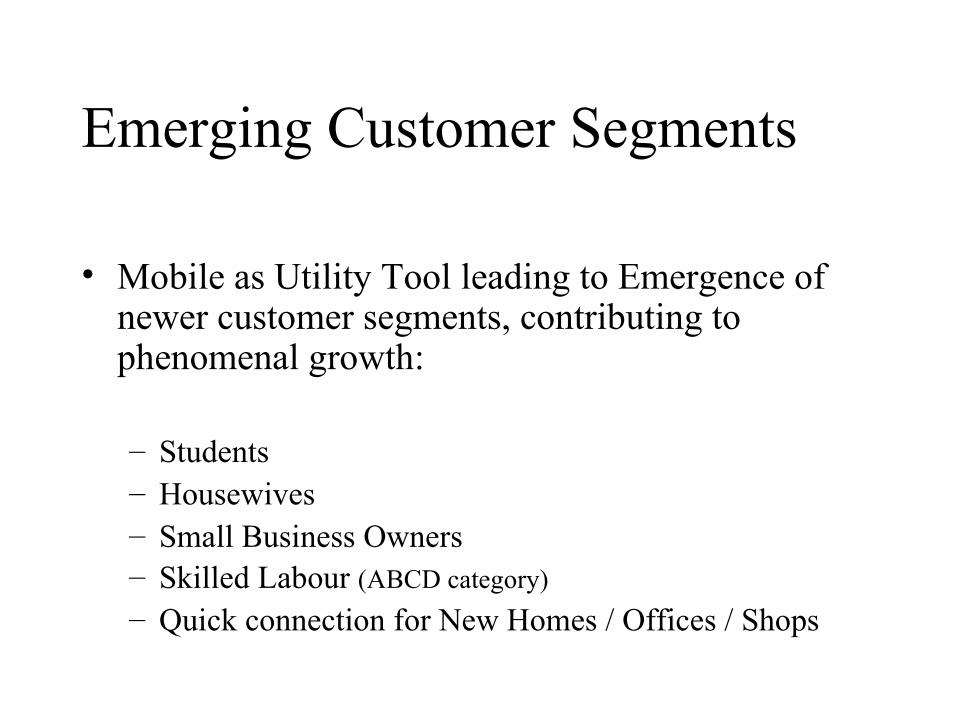

Emerging Customer Segments

• Mobile as Utility Tool leading to Emergence of newer customer segments, contributing to phenomenal growth:

– Students– Housewives– Small Business Owners– Skilled Labour (ABCD category)

– Quick connection for New Homes / Offices / Shops

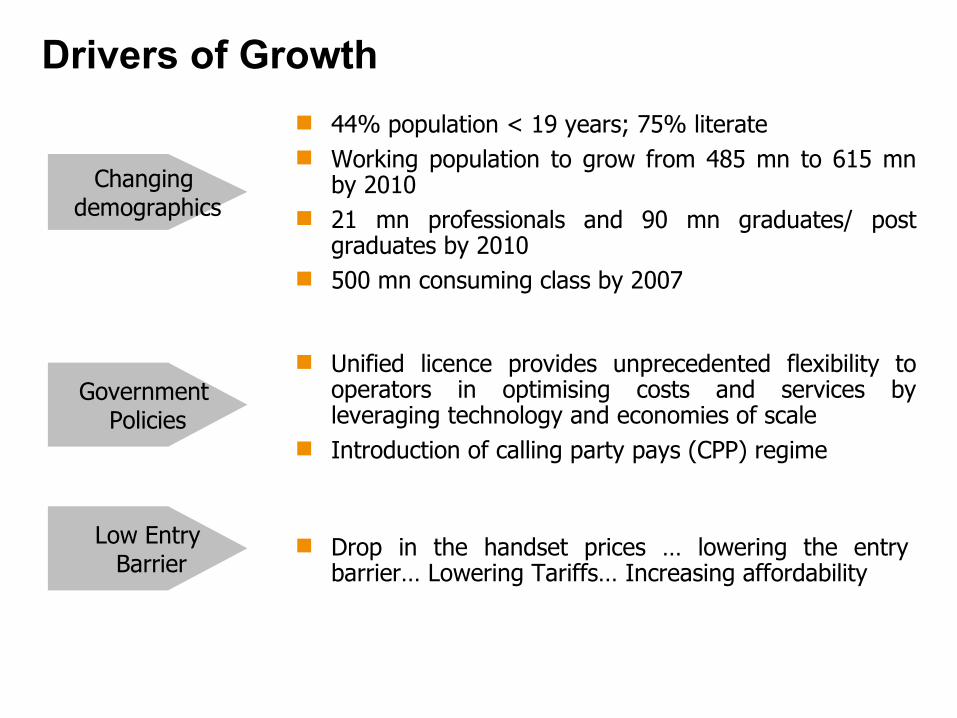

Drivers of Growth

Drop in the handset prices … lowering the entry barrier… Lowering Tariffs… Increasing affordability

Low Entry Barrier

Government Policies

Unified licence provides unprecedented flexibility to operators in optimising costs and services by leveraging technology and economies of scale

Introduction of calling party pays (CPP) regime

Changing demographics

44% population < 19 years; 75% literate Working population to grow from 485 mn to 615 mn

by 2010 21 mn professionals and 90 mn graduates/ post

graduates by 2010 500 mn consuming class by 2007

Innovation in Service Offerings

• 1st Prepaid in GSM & CDMA was launched in India along with simultaneous launch in one more country

• Innovative tariffs & service bundling – unparalleled in world

• Innovative Value Added Services & Useful Applications

LOW PER CAPITA INCOME & LIMITED CREDIT UNIVERSE LED TO SERVICE INNOVATIONS

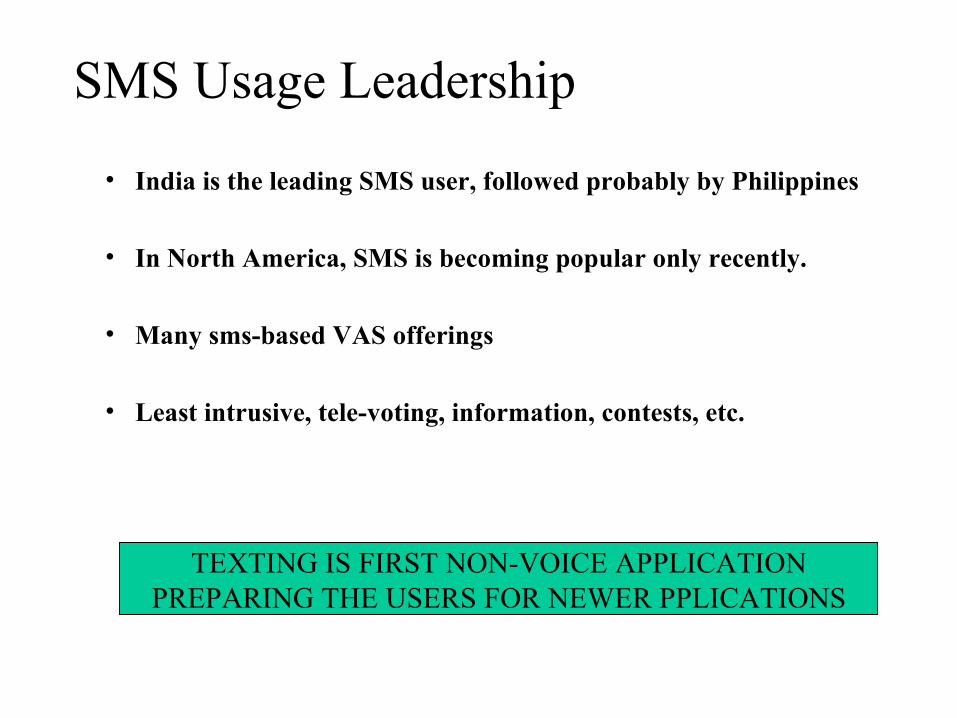

• India is the leading SMS user, followed probably by Philippines

• In North America, SMS is becoming popular only recently.

• Many sms-based VAS offerings

• Least intrusive, tele-voting, information, contests, etc.

SMS Usage Leadership

TEXTING IS FIRST NON-VOICE APPLICATIONPREPARING THE USERS FOR NEWER PPLICATIONS

• India has one of the best structured Regulatory Environment – DoT, TRAI, TDSAT

• India has moved from over-regulated to light-touch environment

• Smooth migration from 2 operator to 4 operator to 6 operator scenario is Exemplary.

Well structured Regulatory environment

• India quickly adopted CDMA – 1X directly in 2003, while many countries moved up gradually from lower versions .

• Earlier, India commenced cellular services with GSM Digital Service whereas other countries began with Analog Technologies

At Forefront in adopting new technology

LATEST TECHNOLOGY ADOPTION HELPED AND CREATEDA LARGE TECHNICAL MANPOWER BASE – ENVY OF WORLD

• Substantial talent pool of Technical & Managerial manpower.

• Sales / Marketing Professionals needed to be innovative for economy – conscious segments.

• Above two, created a cohesive & integrated Indian Telecom Management Philosophy.

• Notwithstanding equity-structure, Indian Telcos run by Indians

• By contrast, Indians are running 2 top global Telecom companies – Vodafone (UK); Orange (France)

Technical & Managerial Knowhow – Uniquely Indian

THE BOTTOM OF PYRAMID – UNIQUE STRENGTH

• Inspite of running at lowest tarrifs per minute, Indian telecom cos continue to run profitable operations with increasing EBITDA margins

• Using scale benefits to achieve cost & operational efficiency for higher profitability

• Indian cost-structures & ingenuity has led to best-in-world efficiencies

Operational efficiency to maintain profitablility

INDIAN BUSINESS MODEL IS ADAPTABLE IN MOST COUNTRIES

• Govt. of India &Regulatory bodies are making efforts that Telephony does not remain an urban phenomenon

• USO Scheme for offering Rural telephony, has helped to increase roll-out of rural telephony services by operators

• Reliancce has simultaneously focussed on both Voice & Data services in rural/ semi-urban areas

• Usage of modern communication by fisher-folk, farmers & small traders is catching up

Rural Communications

NATION IS COMMITTED TO ELIMINATE DIGITAL DIVIDE

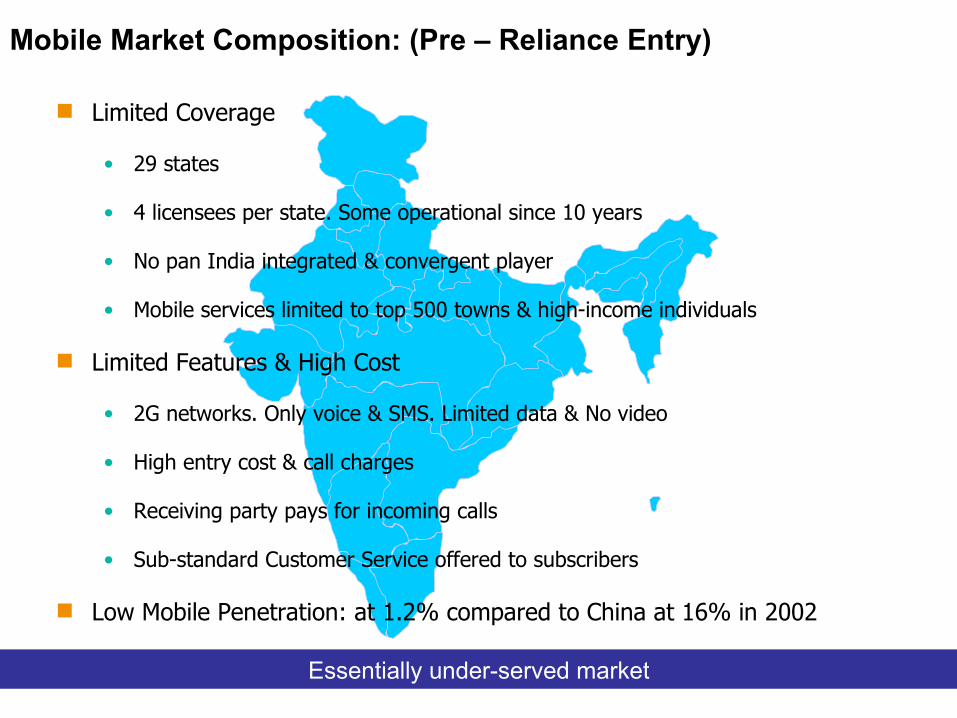

Individual Companies Can Catalyse Sectoral Growth – Reliance Story

Mobile Market Composition: (Pre – Reliance Entry)

Limited Coverage

• 29 states

• 4 licensees per state. Some operational since 10 years

• No pan India integrated & convergent player

• Mobile services limited to top 500 towns & high-income individuals

Limited Features & High Cost

• 2G networks. Only voice & SMS. Limited data & No video

• High entry cost & call charges

• Receiving party pays for incoming calls

• Sub-standard Customer Service offered to subscribers

Low Mobile Penetration: at 1.2% compared to China at 16% in 2002

Essentially under-served market

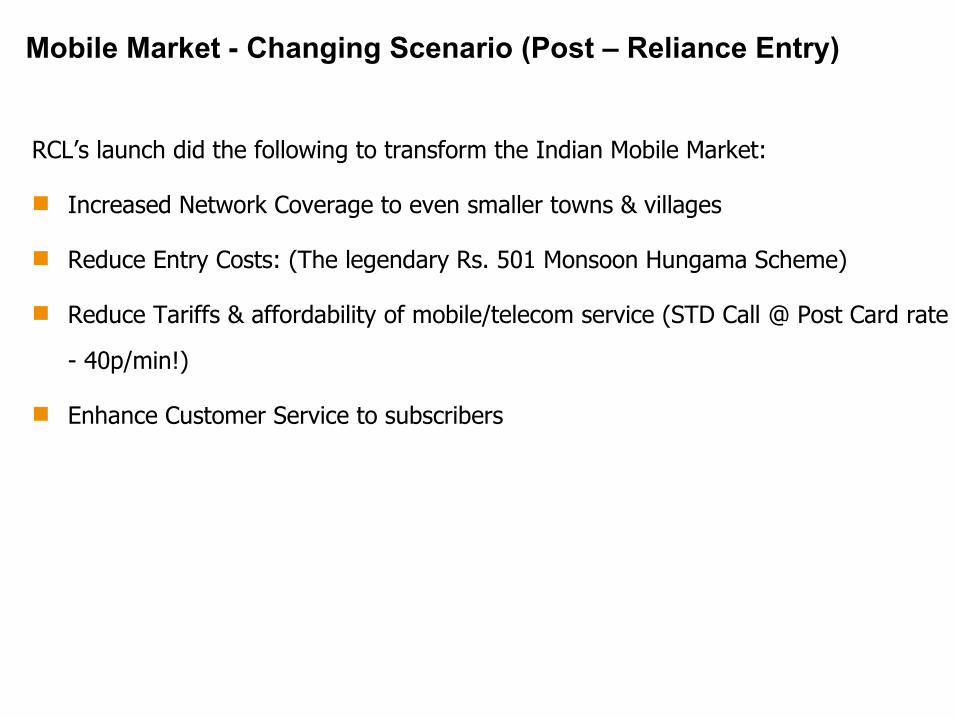

Mobile Market - Changing Scenario (Post – Reliance Entry)

RCL’s launch did the following to transform the Indian Mobile Market:

Increased Network Coverage to even smaller towns & villages

Reduce Entry Costs: (The legendary Rs. 501 Monsoon Hungama Scheme)

Reduce Tariffs & affordability of mobile/telecom service (STD Call @ Post Card rate

- 40p/min!)

Enhance Customer Service to subscribers

Taking mobility to the masses

FreeFreeRs 750/ monthRs 16.8/ minMin cost of Data services like news,

games on mobile etc

Rs 1500Rs 501* /

Rs 5000> Rs 5000> Rs 20,000Entry cost for going mobile

50p/msg

Rs 3/ min

Rs 0.40/min

Rs18/min

2003

Rs 6/minRs. 24 / minRs. 60 / minILD

Rs. 4/ msg

Rs. 30 / min

1995

1 p/ msgRs. 2 / msgSMS cost

Re 1/min

Rs. 0.40/ minRs. 9.60 / min

STD rates

( Mumbai – Delhi Call Cost)

20062002Parameter

* Balance over 36 months

Reliance led a dramatic drop in tariffs making mobile phones an affordable mass product.

INDIA HAS DONE IT.

IN TELECOM.

CAN DO EVERYWHERE!