global ict department (gict) the world bank group best practices and lessons from internet...

TRANSCRIPT

GLOBAL ICT DEPARTMENT (GICT)

THE WORLD BANK GROUP

Best Practices and Lessons from Internet Infrastructure Development

Initiatives

Rob StephensWorld Bank Group

March 24, 2005

El Uso de Internet en las Americas17 de Junio, 2005

CIDE

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPContents

The World Bank Group and ICTs

Affordability and the access gap

Universal Access: the OBA & smart subsidy approach

Examples: Guatemala and Peru

Closing observations

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

The World Bank Group and ICTs

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPExamples of World Bank Group Work

Finance studies: WSIS/UN financing of ICTs studies and Regulatel universal access project

Development of national sector policy and implementation strategy – e-strategies, etc

Privatization of state-owned telecom operators

Encourage public private partnerships

Establishment of legal and regulatory framework and institutions

Capacity-building and finance spectrum management

Design and finance universal access programs

Foster and finance incubators

Invest in private sector companies

Development, Implementation and Financing of UA Schemes

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

No project yetTechnical AssistanceTA & Investment

GICT Rural Access Projects

Project under development

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPGICT Portfolio 2005

GICT’s Transactions Sub-SectorsGross Amount

(US$5.0 billion Approvals*)

GICT’s Transactions per RegionGross Amount

(US$5.0 billion Approvals*)

(*) % related to transaction volumes in US$

GICT Portfolio

Fixed Telephony27%

Mobile Telephony

51%

Other - Satellite, Radio, TV

2%

Cable & Broadband

14%Information Technology

6%

• Current portfolio totals US$1.07 billion - 7%of total IFC portfolio

• 140 investments in 52 countries

South Asia7%

World1%

Latin America & Caribbean

31%

Middle East and North Africa

11%

Southern Europe and Central Asia

16%

Sub-Saharan Africa10% East Asia and

Pacific13%

Central and Eastern Europe

11%

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

An overview of the rural access problem

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Health

Environmental and natural resouces management

Business Services

Education

PublicServices

Telecommunications Infrastructure

Financial Sector

Telecommunications are a key element of economic Telecommunications are a key element of economic and social development ...and social development ...

Less isolation in poor and rural areas

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Wireless/cellular explosion subscribers growing globally at 30-50% per year, in Africa this rate is of

150%

substantial penetrations are being achieved, already overcoming that of fixed lines worldwide

mobile phones are becoming a means of access for many:— pre-pay mass market— wireless payphones

Satellites fill in the gaps: offer cost-effective solution for remote locations, particularly if power

systems are already available

deployed in rural areas of Chile, Colombia, Guatemala, Peru, South Africa, and elsewhere

serve to demonstrate there is actual demand & viable markets

… … and they are becoming increasingly more and they are becoming increasingly more affordableaffordable

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Very rapid growth of ISPs, Internet hosts & users

Phoneshops:

basic public telephone

some are adding fax and PCs/e-mail

Telecenters:

basic public telephone & fax

e-mail, Internet, computers

training resources, skills transfer, community role

access to gov’t & commercial data, distance education, health & other info services

Telecenters sustainabilty (financial, social, cultural) challenge

Internet services are also slowly becoming essentialInternet services are also slowly becoming essential

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPHowever, great inequalities remainHowever, great inequalities remain

0

20

40

60

80

100

120

0 800 2000 4000 8500 15000 30000

Per-capita GDP (PPP)

Hou

seho

ld p

enet

ratio

n (p

er 1

00)

0

20

40

60

80

100

120

0 800 2000 4000 8500 15000 30000

Per-capita GDP (PPP)

Hou

seho

ld p

enet

ratio

n (p

er 1

00)

Country

Rural areas / Low-income users

Other urban areas / middle-income users

Capital / High-income users

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPThe digital divide is widest between urban and rural areasThe digital divide is widest between urban and rural areas

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPGiving rise to universal service & universal access Giving rise to universal service & universal access

policiespolicies

-

10

20

30

40

50

60

70

80

90

100

1 3 5 7 9 11 13 15 17 19 21Per-capita income (US$ 000's - illustrative only)

Line

s pe

r 10

0 h

ouse

hold

s

-

10

20

30

40

50

60

70

80

90

100

1 3 5 7 9 11 13 15 17 19 21Per-capita income (US$ 000's - illustrative only)

Line

s pe

r 10

0 h

ouse

hold

s

Universal

Access

Universal

Access

Universal ServiceUniversal Service

Primary focus: shared

access (payphones)

for rural areas

Primary focus: private lines

for low-income users

Developing countries focus limited resources primarily on universal access in rural areas/where the market failure is greatest. Urban areas – markets serve

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Affordability and the access gapAffordability and the access gap

30000

1

1.5

2

2.5

3

3.5

4

0 5000 10000 15000 20000 25000

GDP per capita (US$)

Tel

eco

mm

un

icat

ion

s r

even

ue

as %

o

f G

DP

World

People spend about 2% on phone servicePeople spend about 2% on phone service

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

% GDPCountry

2.3 1.3Malaysia

Tanzania 1.92.1

1.6 1.3Botswana

1.2 1.5

Rural Areas

Perú

Source: A. Dymond, Intelecon

……including rural areas and poor customersincluding rural areas and poor customers

•Poor people in rural areas often have “high” willingness to pay for phone Poor people in rural areas often have “high” willingness to pay for phone service (different opportunity costs and income measurements)service (different opportunity costs and income measurements)

•Availability is a larger barrier than affordabilityAvailability is a larger barrier than affordability

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPAccess Divide: the two gaps

Current individual user access

Community access

Current expansion plans

Geographic Isolation

Po

vert

y

Market Efficiency Gap (MEG)

Commercially Feasible Market

Access Gap (MAP)

Rural Market Access Gap

Full Market Access Gap

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPHow to reduce the gaps?

Current individual user access

Community access

Current expansion plans

Geographic Isolation

Po

vert

y

Market Efficiency Gap (MEG) Market

Access Gap (MAP)

Remove Legal and Regulatory

Barriers

Develop Universal Access Programs Full Market Access Gap

Rural Market Access Gap

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Closing the access gap: output based Closing the access gap: output based aid (OBA) and the smart subsidyaid (OBA) and the smart subsidy

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPGovernment defines objectivesGovernment defines objectives

Provide 200 public telephones in a certain rural area, for a one-time subsidy and operate them for a ten year

period at specified minimum quality standards.

RURAL AREA

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPPrivate operators bid for subsidyPrivate operators bid for subsidy

$2 million

$1 million

$1.5 million$0.5 million

Concession is awarded to consortium requesting lowest subsidy.

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPSubsidy paid against investments

RURAL AREA

Output-Based Aid: Subsidy paid as investment targets are met.

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Project design aimed at commercial viability of concessions Max subsidy to make private NPV=0 Tariff structure and adjustments, interconnection charges allowed at expected traffic levels

Well-defined roll-out targets for operators E.g. Towns to be served/Services to be provided/ Quality indicators/ Contract length

No exclusivity rights or technology restrictions

Freedom to provide additional services

Key Features of OBA Projects in LAC

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPOutput-Based Aid (OBA)

Disbursement of public funding is tied to specified outputs or services delivered by private firms (or NGOs):

May complement or replace user-fees under structures where operator is responsible for financing and providing the service.

Public funding may be sourced from Bank loans, other kinds of donor assistance, or government’s own resources.

Potential benefits:

Better targeting of beneficiaries/outcomes

Better incentives for efficiency & innovation

Opportunities to leverage private financing.

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Problem

Universal services are socially desirable (social NPV>0) but not always commercially viable (private NPV<0)

Solution

Provide a one-time investment subsidy for private operators willing to provide the universal access service.

Bid the subsidy out competitively to ensure that costs are kept as low as possible. Paid over time as outputs are provided.

This effectively leverages maximum private investment in achieving universal service goals

OBA - Smart Subsidy Approach

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

The spread of the model

income level

level of interest

upper middle income

lower middle income

low income

water

transport

electricity

telecomChile

Guatemala

Nepal

(Paraguay)

Argentina

ChileBolivia

(Mexico) (Ecuador)

Cape Verde (Benin/Togo)

(Uganda) (Senegal)

Peru

Uganda (Nicaragua)

Colombia

South Africa Dom. Rep.

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPSome examples: designSome examples: design

Chile Colombia Peru Nepal

Year 19941995

1994 1999 19941998 20012003

Target Meet requests

Towns of 250+ Towns of 300+ Eastern Development Region

Funding Taxation USL+licenses 1% USL+fines IDA Credit

Revenues

US$6m pa. US$60m pa. US$12m pa. US$ 2m pa.

Duration 10 years 10 years 20 years 10 years

Payment Immediate Installments (18 months)

Installments (18 months)

Installments (2 years)

Price regulation

Yes+rural interconnect

Yes Yes No

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPSome examples: outcomesSome examples: outcomes

Chile Colombia Peru Nepal

Projects 200 6 7 1

Bidders - 2 to 7 2 to 5 3

Subsidy per town

$3,600 $4,600 $9,500 $9,365

Towns served

6,059 7,415 4,420 1,064

Population served

2.2m 3.7m 1.6m 4m

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPFinancing optionsFinancing options

Universal access funds, financed by: government budget operator revenue contributions (typically 1-2%) cellular, basic service or radio frequency license fees interconnect levies and ‘virtual fund’ transfers

Low interest operator loans national sources (e.g. USA’s REA loans) aid agency sources (not a good record)

Micro loans for phoneshops or other retailers e.g. Grameen Bank ‘phone ladies’ part financing by telecom operators

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Applying the access gap and OBA Applying the access gap and OBA model: Guatemala and Perumodel: Guatemala and Peru

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Guatemala – Liberalization achievements

LÍNEAS DE TELEFONÍA FIJA

286,4342,0

429,7517,0

610,7676,6

756,1846,0

944,1

1 132,2

2,9 3,1

4,14,8

5,55,9

6,57,1

7,9

8,9

0

200

400

600

800

1000

1200

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

mile

s d

e lín

eas

0

1

2

3

4

5

6

7

8

9

10

Tel

eden

sid

ad

líneas densidad Fuente. Paul Budde Inc., SIT

LÍNEAS DE TELEFONÍA MÓVIL

43,0 64,0 112,0320,0

660,5

1 009,2

1 386,0

1 875,1

3 168,3

0,4 0,6 1,03,0

5,8

8,6

13,5

24,9

12,0

0

500

1000

1500

2000

2500

3000

3500

1996 1997 1998 1999 2000 2001 2002 2003 2004

mile

s d

e lín

eas

0,0

5,0

10,0

15,0

20,0

25,0

30,0

Tel

eden

sid

ad

líneas densidad Fuente. Paul Budde Inc., SIT

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

DENSIDAD FIJA POR DEPARTAMENTOS, 2003

25,03

7,26 6,76 6,485,55 5,00 4,31

3,50 3,49 3,21 3,20 2,90 2,43 2,07 2,05 2,02 1,94 1,91 1,74 1,68 1,50 1,23

GUA SAC ZAC QUE ESC IZA CHQ RET CHM SUC PET EPR JAL JUT SNM STR HUE SOL TOT BVP AVP QUI

Promedio nacional: 7,87

Fuente: SIT, INE

… there is a pending agenda – access gap: example -- Guatemala

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPGuatemala: Identifying the Gaps

• Four areas were selected that had a high concentration of areas in clusters 4 & 5

• This led to selecting four departments: Petén, Huehuetenango, Alta Verapaz y Quiche.

• A field survey was carried out in these four departments

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Results of Gap Assessment in Guatemala

Las Brechas de Eficiencia de Mercado se calculan quitando a la población urbana y rural no pobre la densidad total fija y móvil.La Brecha de Acceso Real es la población rural pobre y pobre extrema que requiere de subsidio para poder accesar al servicio (y cuyo gasto en comunicación sí cubre el costo de O&M de TTPP).

BRECHAS DE ACCESO, EN NÚMERO DE HOGARES

Región Brecha de Eficiencia de Mercado Brecha de AccesoUrbano Rural Total (sólo rural)

Metropolitana 0 21,400 21,400 21,339Norte 0 10,653 10,653 66,791Nororiental 14,390 21,819 36,209 44,515Suroriental 16,700 21,841 38,541 73,034Central 19,821 0 19,821 79,817Suroccidental 0 79,697 79,697 150,815Noroccidental 4,541 23,544 28,085 116,415Petén 0 15,534 15,534 17,868TOTAL 55,451 194,488 249,939 570,595TOTAL población 349,343 1,225,274 1,574,617 3,594,749

Backbone Gap: 288 out of 331 Municipalies do not have backone access

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Estimated Costs of Bridging the Rural Access Gap in Guatemala

(En US Dólares)

Fase I: Piloto Fase II Fase III TotalTeléfonos Públicos Comunitarios 1,577 2,009 1,648 5,234 Teléfonos privados 6,315 6,639 5,331 18,285 POPs de Acceso a Internet 79 129 80 288 Población beneficiada 1,194,823 1,276,649 1,020,419 3,491,891 Monto de subsidio 6,960,319 8,996,392 7,813,710 23,770,421 Monto de Inversión 6,540,390 7,698,739 6,203,222 20,442,351

INDICADORES RESUMEN DE LOS PROYECTOS

Estimated not Actual/Unofficial

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

1% tax on operators could finance programs to fully address the rural access gap in Guatemala

Recaudación Saldo netoFase I Fase II Fase III Total Estimada 1/ anual

Año 0 2,538,724 2,538,724 1,000,000 (1,538,724) Año 1 2/ 2,538,724 3,276,670 5,815,394 4,670,000 (1,145,394) Año 2 846,241 3,276,670 2,896,670 7,019,581 4,903,500 (2,116,081) Año 3 846,241 1,092,223 2,896,670 4,835,134 5,148,675 313,541 Año 4 846,241 1,092,223 965,557 2,904,021 5,406,109 2,502,088 Año 5 846,241 1,092,223 965,557 2,904,021 5,676,414 2,772,393 Año 6 1,092,223 965,557 2,057,780 5,960,235 3,902,455 Año 7 965,557 965,557 6,258,247 5,292,690 1/ Asume una disponibilidad para año 0 de US$ 1 millón en Fondetel.2/ Asume una contribución de 1% de los ingresos brutos del sector.

Desembolsos Ingresos

DESEMBOLSOS E INGRESOS REQUERIDOS POR ESTRATEGIA(US Dólares)

Esquema de desembolsos es: 30% como adelanto ante entrega de cronograma detallado de instalaciones, 30% contra entrega de sistema y 4 pagos anuales de 10%.

Estimated, Not Actual/Unofficial

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Gigantesco progreso en la obtención de Accesso Universal

Efecto de reducción de distancia ha sido dramático, pero las variantes entre regiones puede ser grande (debido a la altura, terreno e inclinación)

FITEL I FITEL II FITEL III FITEL IV Total/Avg

Approx. # of Sites 213 2,170 2,520 1,614 6,517

Population (m) 0.14 1.6 2.1 2.9 6.74

Subsidy (US$M) 5.1 12.1 30.7 11.4 59.3

Population / site 689 758 827 1,822 1,024

Subsidy / site US$ 23,937 5,575 12,163 7,061 8,266

Subsidy / pop US$ 34.74 7.36 14.71 3.88 8.65

Avg. Distance (prior) 90km 54km 24km NA 56km

Avg. Distance (post) 5km 8km 4km NA 5.7km

FITEL Program Summary Statistics

Impacto de FITEL (1)

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

•FITEL ha reducido la distancia de 5.7 km en promedio, esto es notable en un país con un terreno tan desafiante como Perú

•El impacto de teléfonos FITEL es numeroso, incluyendo un cuidadoso uso de dinero en algunos pueblos donde anteriormente usaban el trueque

Impacto de FITEL (2)

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

•Análisis de costo-beneficio de 1.64 y excedente por consumidor de 13 Soles por mes indica beneficios tangibles significativos

•Beneficios menos tangibles incluyen la mejora del contacto familiar, mejor salud y seguridad (llamadas de emergencia), integración de economías regionales y menor aislamiento

Impacto de FITEL (3)

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

• 70% de encuestados fueron conscientes de los teléfonos públicos en sus comunidades, sólo ~50% lo ha usado en el año pasado (MINAG análisis de encuesta)

• Promedio de gasto en telecomunicaciones es alrededor de 8 Soles por mes por usuario – US$ 2.3 – cerca de las salientes ARPU de muchos usarios de prepago en la ciudad

• Esto es equivalente al ~1.4 % de los ingresos familiares

• Modelo típico de uso ligeramente mayor a 3 llamadas por mes/usuario, 10 minutos por mes en promedio (Suministro-figuras afectadas)

• Más de 3.3 millones de llamadas por mes en teléfonos rurales GTH, 1.9 millón recibidas (58%) y1.4 millón salientes (42%)

Impacto de FITEL (4)

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

•FITEL alcanzó similar (ligeramente menor) subsidio por figuras prepagadas como FDT de Chile, entre US$ 5,600 y 12,000

•FITEL ha usado pilotos y circulado ofertas iniciales como experiencia de aprendizaje, y continua mejorando su programa, diseñando ofertas y marcos regulatorios.

• Tarifas de interconexion asimetricas para operadores rurales

•FITEL ha logrado mantener los costos administrativos de gestión del fondo en un nivel bajo (debajo del 2% del financiamiento) , aparece estable alrededor del 1%

Impacto de FITEL (5)

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUPComponents of Access Strategy

3. Telefonos Comunitarios/VSAT:Mejorar, mover, fomento uso para otros servicios

4. Telefonia Celular:

Estimular expansion celular

5. Banda Ancha Nacional:

Diagnostico y opciones.

2. Internet y Telecentros:

Mas pilotos y estrategia para asegurar uso productivo

1. Liderazco, dialogo y coordinacion:

Consensuar una estrategia nacional de e-desarollo

GLOBAL ICT DEPARTMENT

THE WORLD BANK GROUP

Priority is universal access not universal service

Voice is the “killer ICT application” demanded by poor cellphone is the world’s most important 2-way ICT commodity

Privatization, Liberalization and Universal Access reforms at the same time: Chile, Peru, Guatemala, Colombia, Brazil

Private sector has lead role to invest in sector. Government roll is to stimulate private investment in less attractive areas.

Slow roll-out of some universal access programs

Rural build-out requirements imposed on privatized firms

Benefit: Service quickly provided to unserved communities

Policy Cost: Exclusivity periods and weaker regulation of incumbent

Universal access fund and agency established

Financing options: (1) government budget --Chile), (2) 1%-2% tax on telecom sector -- Peru, Colombia, Brazil), (2) Other sources – Guatemala.

Options: (1) part of regulator – Peru, Chile, (2) part of Ministry; (3) “independent”

Targeting of funds – Identify access gaps

Allocation of funds -- Output Based Aid (OBA) model/tenders

Universal programs evolve over time

Trends: From large national projects to smaller projects, from supply/infrastructure focus to projects that combine supply/infrastructure with demand generation and productive use.

Recap of LAC experiences

GLOBAL ICT DEPARTMENT

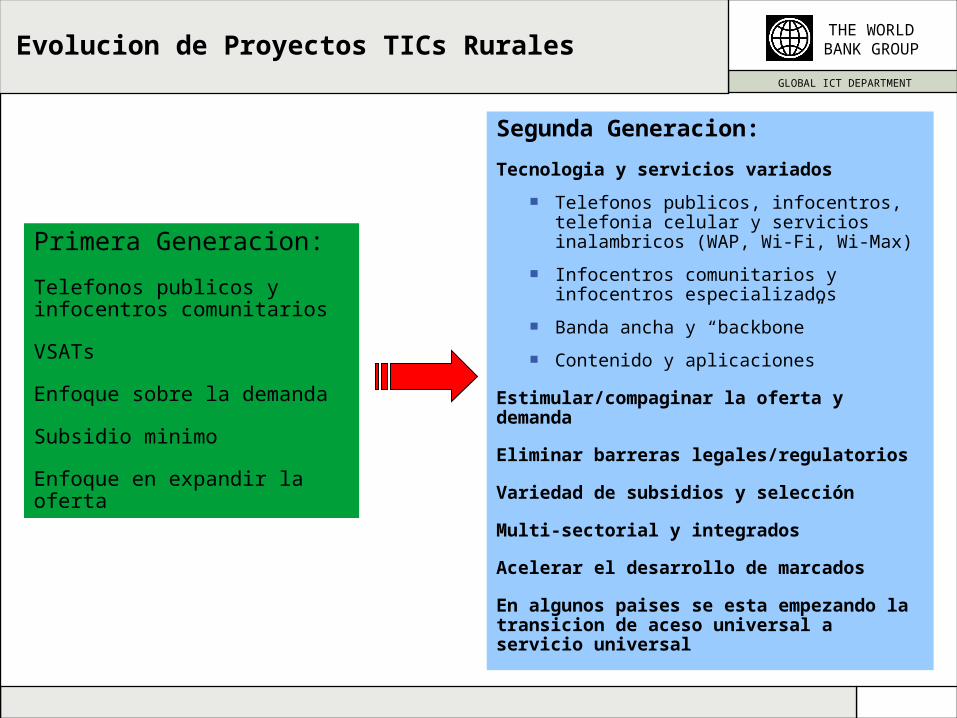

THE WORLD BANK GROUPEvolucion de Proyectos TICs Rurales

Primera Generacion:

Telefonos publicos y infocentros comunitarios

VSATs

Enfoque sobre la demanda

Subsidio minimo

Enfoque en expandir la oferta

Segunda Generacion:

Tecnologia y servicios variados

Telefonos publicos, infocentros, telefonia celular y servicios inalambricos (WAP, Wi-Fi, Wi-Max)

Infocentros comunitarios y infocentros especializados

Banda ancha y “backbone”

Contenido y aplicaciones

Estimular/compaginar la oferta y demanda

Eliminar barreras legales/regulatorios

Variedad de subsidios y selección

Multi-sectorial y integrados

Acelerar el desarrollo de marcados

En algunos paises se esta empezando la transicion de aceso universal a servicio universal