global energy demand outlook in the light of higher prices: update

TRANSCRIPT

EURO PEA N FUEL PRI CE CO N FEREN CE12

Global Energy Demand Outlook in the Light of Higher Prices: Update on the Implications of Recent

HurricanesKevin Lindemer

Executive Managing Director of EnergyGlobal Insight

Copyright © 2005 Global Insight, Inc. 2

Lessons from the Hurricanes and High Prices

• Increasingly, markets are event driven• The global economy seems to be much less

sensitive to oil price than previously thought• Demand side response has been relatively

weak and of short duration – so far.• Capacity limits in the U.S. and global oil

system were exposedOPEC capacity and global capacity to produce light/sweet crude oilGlobal heavy/sour refining capabilityUS natural gas supply capability

Copyright © 2005 Global Insight, Inc. 3

Demand Impact from High Oil/Energy Prices

• Demand appears to be less elastic than years past due to relative growth in transportation

• Price effect is smaller due to significant decline in fuel substitution capability

• Income effect is smaller due to continued decline in oil/gdp in nearly all countries.

Incremental oil demand/gdp nearly half the level of 10 years ago

• For many OECD consumers, the price of crude oil is a small fraction of their fuels costs

• In some major emerging markets, energy prices are subsidized and consumers do not ‘see’ higher prices

• Oil’s share of total energy continues to fall

Copyright © 2005 Global Insight, Inc. 4

Why Near-Record High Energy Prices Are Not a Problem…and Even Higher May Not Be

• Current high prices are – still – largely demand driven

• Petro dollars are being recycled more quickly through investments and financial flows

• There is an absence of inflationary pressures thanks to increased global and domestic competition

• As a result of prudent monetary policies, inflation expectations are relatively stable

Copyright © 2005 Global Insight, Inc. 5

Demand Growth: N. America and Asia dominate

0

20

40

60

80

100

120

1990 1995 2000 2005 2010 2015 2020

mill

ion

b/d

N America C/S America Europe Asia Pacific Middle East Africa FSU

Copyright © 2005 Global Insight, Inc. 6

How Far Can You Drive on $20 of Gas?

127 213 342 385771

4,627

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Germany India USA China SaudiArabia

Venezuela

Source: Foreign Affairs

Mile

s

Copyright © 2005 Global Insight, Inc. 7

US Fuel Cost per Mile Driven

0.0

5.0

10.0

15.0

20.0

25.0

1973 1977 1981 1985 1989 1993 1997 2001 2005

2004

cen

ts p

er m

ile

Cars SUVs

Copyright © 2005 Global Insight, Inc. 8

US Gasoline Demand: Bouncing Back

7,000

7,500

8,000

8,500

9,000

9,500

10,000

J F M A M J J A S O N D

Thou

sand

s of

bpd

2003 2004 2005

Copyright © 2005 Global Insight, Inc. 9

Energy Demand/GDP

100

150

200

250

300

350

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

MTO

E/B

illio

n$

US EU China India Japan

Copyright © 2005 Global Insight, Inc. 10

Oil Share of World Energy Index 1990 = 100

707580859095

100105110115120

1990 1992 1994 1996 1998 2000 2002 2004Source: BP Statistical Review

North America S.& C. America EU and Eurasia Mid EastAfrica Asia Pacific World

Copyright © 2005 Global Insight, Inc. 11

Incremental Oil Demand/GDP PPP

(0.060)

(0.040)

(0.020)

-

0.020

0.040

0.060

0.080

0.100

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005estTO

E/$1

000

GD

P PP

P

US EU China Linear (US) Linear (EU)

Copyright © 2005 Global Insight, Inc. 12

Global Transport Share of Oil Demand

30.0%

35.0%

40.0%

45.0%

50.0%

55.0%

1971 1976 1981 1986 1991 1996 2001

Copyright © 2005 Global Insight, Inc. 13

How High Can Price Go Before There is a GDP Impact?

• Global Insight sensitivity analysis of an oil price ‘shock’ on the global economy

• WTI price over $100 for two months and over $70 for six months and over $50 for an additional year.

• Slight negative impact on global GDP in the first year, no impact in the second and positive impacts in the following years.

• Price impact shaves 0.3 – 0.4 percent off growth for China and India in year 1 and 2.

• What price is too high?

Copyright © 2005 Global Insight, Inc. 14

WTI Crude Oil Price Cases

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

$100.00

$110.00

$120.00

Oct-05 Jan-06 Apr-06 Jul-06 Oct-06

Dol

lars

per

Bar

rel

Base Case Oil 'Shock'

Copyright © 2005 Global Insight, Inc. 15

Impact of $100 Oil Shock on World Growth

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Global Insight Scenario Model

Perc

ent C

hang

e in

Rea

l GD

P

Base Case Oil Shock

Copyright © 2005 Global Insight, Inc. 16

$100 Oil Impact on China’s GDP Growth

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Source: Global Insight Scenario Model

Perc

ent C

hang

e in

Rea

l GD

P G

row

th

Base Case Oil Shock

Copyright © 2005 Global Insight, Inc. 17

If demand is less responsive, what will or should be the future price?

• Historically, the oil market has nearly always had a governor to regulate surplus capacity and keep prices stable

• Are we entering an era where a demand regulator is needed to stabilize prices? Can it be done?

• If demand is much less responsive to price than in the past, why should OPEC ‘settle’ for only $45/bbl oil rent?

Historically, OPEC attempted to hold prices at a level that did not impact demand

Copyright © 2005 Global Insight, Inc. 18

OPEC Price Floors: Past, Present and Future?

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

1980 1985 1990 1995 2000 2005 2010

2004 $ Nominal $

……but why not target here?but why not target here?

‘‘NewNew’’ OPEC Reference Price?OPEC Reference Price?

‘‘OldOld’’ OPEC Reference PricesOPEC Reference Prices

……or target here?or target here?

Copyright © 2005 Global Insight, Inc. 19

If the future is higher prices, what are the implications?

• Faster growth rate for alternative and renewable fuels

• Unconventional oil production accelerates• Since demand is relatively inelastic, what

price will trigger a demand side response to reduce demand? Or,

• Will demand need to be ‘regulated’? Or, • Will consuming countries regulate price?• Policies that are sensitive to energy costs

may need to be reconsidered

Copyright © 2005 Global Insight, Inc. 20

Energy Supply Impacts from the Hurricanes is Diminishing, Gas May Still be an Issue

• Oil production lost is coming back at a relatively optimistic case.

Less than 0.1 mbd out by year endReplaced by imported crude oil

• Natural gas production returning at a steady pace.Small volumes out by year endReplaced by demand destruction

• Refineries will be back to nearly full production by year end

Small amount out will be replaced by higher output from other refineries and higher imports

Copyright © 2005 Global Insight, Inc. 21

Hurricane Related Oil Production OffLine

0

500

1000

1500

2000

2500

Sep-05 Oct-05 Nov-05 Dec-05 Jan-06 Feb-06

Shut

-in O

il Pr

oduc

tion

(MB

OPD

)

Oil Shut-in Pos. Oil Shut-in Neg. Oil Shut-in Actuals

Copyright © 2005 Global Insight, Inc. 22

Hurricane Related Gas Production Off-Line

0

2000

4000

6000

8000

10000

12000

14000

Sep-05 Oct-05 Nov-05 Dec-05 Jan-06 Feb-06

Shut

-in G

as P

rodu

ctio

n (M

MC

FD)

Gas Shut-in Pos. Gas Shut-in Neg. Gas Shut-in Actuals

Copyright © 2005 Global Insight, Inc. 23

Refinery Capacity Offline from Rita and Katrina

-

1,000

2,000

3,000

4,000

5,000

6,000

9/24 10/8 10/22 11/5 11/19 12/3 12/17 12/31

Thou

sand

s of

bpd

Copyright © 2005 Global Insight, Inc. 24

Global Per Capita Oil and Energy Demand

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

1.600

1.800

1965 1970 1975 1980 1985 1990 1995 2000

Tonn

es p

er P

erso

n

Oil Energy

Copyright © 2005 Global Insight, Inc. 25

Global Oil Demand: What Could Have Been

0

20,000

40,000

60,000

80,000

100,000

120,000

1965 1970 1975 1980 1985 1990 1995 2000

Thou

sand

of b

pd

Copyright © 2005 Global Insight, Inc. 26

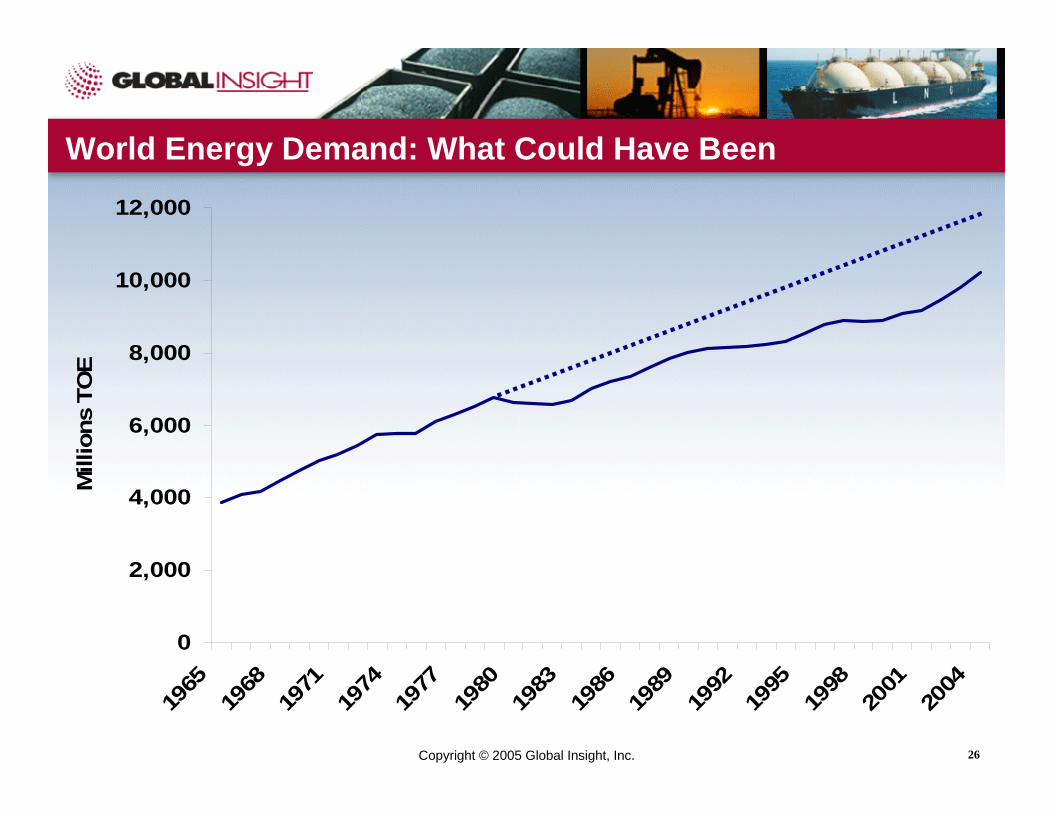

World Energy Demand: What Could Have Been

0

2,000

4,000

6,000

8,000

10,000

12,000

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

Mill

ions

TO

E

Copyright © 2005 Global Insight, Inc. 27

Thank you!

NameTitle

E-mail: [email protected]

EURO PEA N FUEL PRI CE CO N FEREN CE12

Thank You

Kevin LindemerExecutive Managing Director of Energy

E-mail: [email protected]