global and regional financial safety nets - institute for international

TRANSCRIPT

Global and Regional Financial Safety Nets: Lessons from Europe and Asia

Rhee, Sumulong and Vallée Asian Development Bank and Bruegel

11 October 2013

1

The views expressed in this document are those of the author and do not necessarily reflect the views and policies of the Asian Development Bank or its Board of Governors or the governments they represent.

Table of Contents • Rise of regional arrangements

– Two generations of Regional Financial Arrangements – The European and the Asian experiences – The new international and regional safety net

architecture • Cooperation challenges and policy prescriptions

– Strengthening existing global and regional arrangements

– Collaboration between the IMF and regional financial arrangements

– Cooperation with other stakeholders

2

Rise of regional arrangements

3

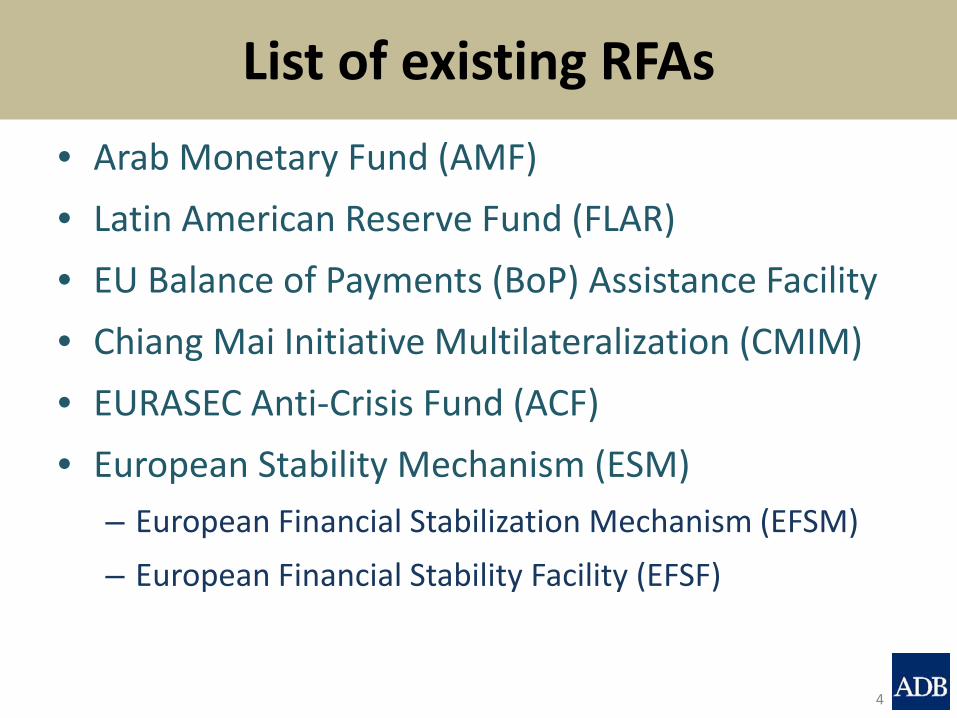

List of existing RFAs • Arab Monetary Fund (AMF) • Latin American Reserve Fund (FLAR) • EU Balance of Payments (BoP) Assistance Facility • Chiang Mai Initiative Multilateralization (CMIM) • EURASEC Anti-Crisis Fund (ACF) • European Stability Mechanism (ESM)

– European Financial Stabilization Mechanism (EFSM) – European Financial Stability Facility (EFSF)

4

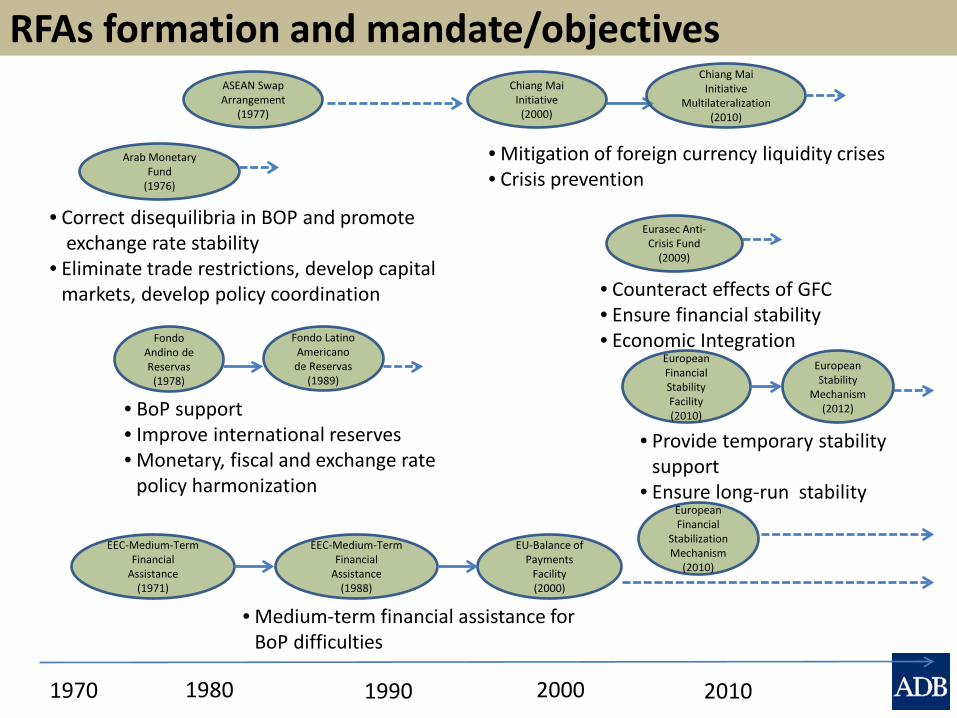

RFAs formation and mandate/objectives

Fondo Andino de Reservas

(1978)

Arab Monetary Fund

(1976)

1970 1980 1990 2000 2010

Chiang Mai Initiative

(2000)

Eurasec Anti-Crisis Fund

(2009)

European Financial Stability Facility (2010)

European Stability

Mechanism (2012) • BoP support

• Improve international reserves • Monetary, fiscal and exchange rate

policy harmonization

• Correct disequilibria in BOP and promote exchange rate stability

• Eliminate trade restrictions, develop capital markets, develop policy coordination

• Mitigation of foreign currency liquidity crises • Crisis prevention

• Counteract effects of GFC • Ensure financial stability • Economic Integration

• Provide temporary stability support

• Ensure long-run stability

EU-Balance of Payments

Facility (2000)

EEC-Medium-Term Financial

Assistance (1988)

• Medium-term financial assistance for BoP difficulties

Fondo Latino Americano

de Reservas (1989)

Chiang Mai Initiative

Multilateralization (2010)

EEC-Medium-Term Financial

Assistance (1971)

European Financial

StabilizationMechanism

(2010)

ASEAN Swap Arrangement

(1977)

First generation RFAs • Includes EEC-MTFA, AMF, FAR • Established not as a result of financial crisis, but in

anticipation of BoP instability • Started in the late 1970s with the demise and the

perceived travails of the international monetary system • Questions:

– Why didn’t the large Latin American countries join FAR/FLAR?

– Why did oil-exporting Middle East countries see the need for an RFA?

– Why were they, in particular, EEC-MTFA, created when IMF has programs to address BoP problems?

6

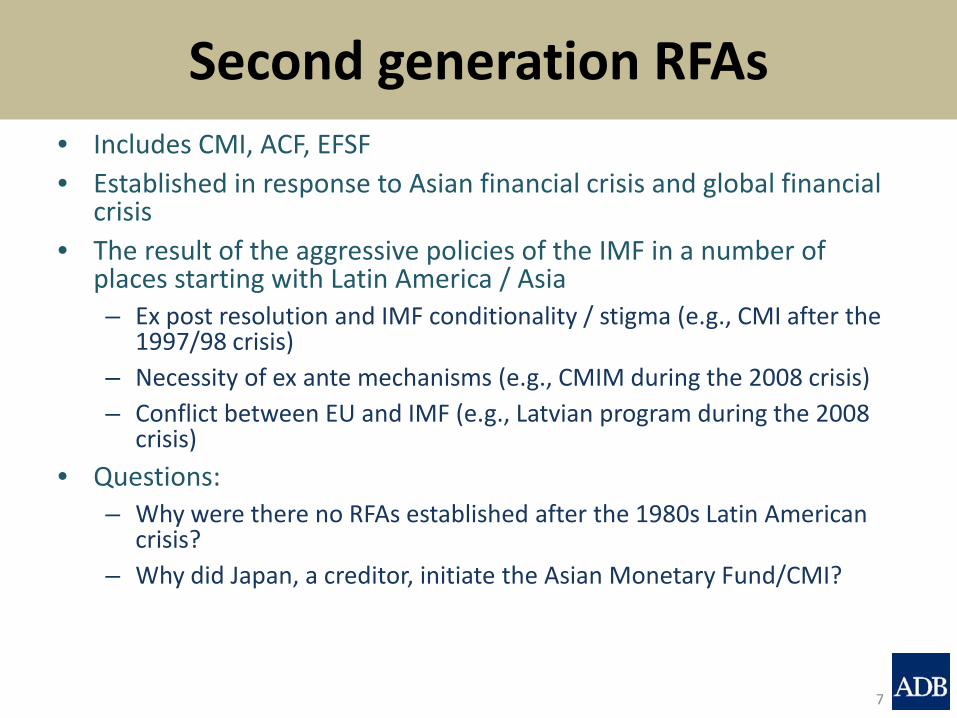

Second generation RFAs • Includes CMI, ACF, EFSF • Established in response to Asian financial crisis and global financial

crisis • The result of the aggressive policies of the IMF in a number of

places starting with Latin America / Asia – Ex post resolution and IMF conditionality / stigma (e.g., CMI after the

1997/98 crisis) – Necessity of ex ante mechanisms (e.g., CMIM during the 2008 crisis) – Conflict between EU and IMF (e.g., Latvian program during the 2008

crisis) • Questions:

– Why were there no RFAs established after the 1980s Latin American crisis?

– Why did Japan, a creditor, initiate the Asian Monetary Fund/CMI?

7

G20 and Global Safety Nets (GSNs)

• G20 Seoul Summit – Initial Korean proposal: Institutionalize bilateral

swaps (linkage between central banks and IMF) – Strengthening GSN vs Moral Hazard: * FCL, PCL, Multi-country FCL, etc.

• Cannes Summit – G20 principles for the IMF and Regional Financial

Arrangements

8

Existing RFAs: Characteristics

RFAs & No. of Members Legal basis Fund Size Paid-in Capital/ Pledge

W/ Option to Issue Bonds?

AMF 22 Agreement $2.7 Bn 600 Mn Arab Dinars Yes FLAR 7 Agreement $3.28 Bn $2.28 Bn Yes EU-BOP 27 Treaty €50 Bn €50 Bn Yes CMIM 13 Agreement $240 Bn Pledge No ACF 6 Treaty $8.513 Bn $8.513 Bn No ESM 17 Treaty €500 Bn €80 Bn Yes EFSM 27 Agreement €60 Bn Backed by EU Budget Yes EFSF 17 Agreement €440 Bn* Yes

* Combined lending ceiling of ESM & EFSF raised to €700 Bn in July 2013 with €80 Bn pledged by Member States and the balance to be raised from capital markets

9 Though a latecomer, ESM appears to be the strongest.

Existing RFAs: Instruments

• Loans, guarantees, swaps • Maturity varies from short term (e.g., 30 days)

to very long term (up to 20 years) • Interest rates are either fixed or floating based

on LIBOR • Ex ante vs. ex post mechanisms • Conditionality: not specified in detail yet

10

Existing RFAs: Instruments offered

11

RFA Instrument Duration Grace/ Rollover period

AMF Automatic loan Ordinary loan Extended loan Compensatory loan Structural Adj. facility Short-term liquidity

3 yrs 5 yrs 7 yrs 3 yrs 4 yrs

6 mos

3.5 yrs 3.5 yrs 1.5 yrs 2.0 yrs

renewable, 2x

FLAR BoP credit Foreign debt restructuring Liquidity credit Contingent credit Treasury credit

3 yrs 3 yrs 1 yrs

6 mos 30 days

1 yr 1 yr

renewable

EU BOP Loan/Credit line ~5 yrs on ave

CMIM Swap, Precautionary line Swap, Stability Facility

Both: 6 mos*; 1 yr**

Both: renewable up to 2 yrs*; 3 yrs**

Notes: * IMF-delinked; ** IMF-linked; STA- Subject to assessment of the designated decision-making group; SMSF – Secondary Market Support Facility; PCCL – Precautionary Conditioned Credit Line; ECCL – Enhanced Conditions Credit Line

Existing RFAs: Instruments & Terms

12

RFA Instruments & Terms Duration Grace/ Rollover period

ACF Stabilization credit (low inc) Sovereign loans (middle inc)

20 yrs 10 yrs

5 yrs 5 yrs

ESM Loan Credit line (PCCL & ECCL) SMSF

STA 1 yr STA

STA Renewable, 2x (6 mos ea)

STA

EFSM Loan/Credit line STA STA

EFSF Loan Credit line (PCCL & ECCL) SMSF

STA 1 yr

STA

STA Renewable, 2x (6 mos ea)

STA

Notes: * IMF-delinked; ** IMF-linked; STA- Subject to assessment of the designated decision-making group; SMSF – Secondary Market Support Facility; PCCL – Precautionary Conditioned Credit Line; ECCL – Enhanced Conditions Credit Line

Existing RFAs: Link to IMF Programs

13

RFA Link to IMF Programs

AMF Ordinary loans usually accompanied by an IMF program (other assistance not necessarily linked)

FLAR None but complements assistance provided by other IFIs including IMF

EU-BOP Not formally but organized jointly in recent cases; members are obliged to consult EU before approaching IMF

CMIM Beyond 30% of country’s allotment, disbursements must be linked to an IMF program; the de-linked portion to be increased to 40%

ACF Guided by IMF recommendations on loan concessionality when lending to low-income countries

ESM MoU between EC, ECB, IMF (where applicable), and beneficiary

EFSM Not legally but ECOFIN Council has explicitly stated that activation would only be in the context of a joint EU/IMF program

EFSF Framework agreement provides that support be provided in conjunction with the Fund and subject to conditionality in an MoU negotiated in liaison with the IMF and ECB

Except for CMIM and European RFAs, IMF involvement is optional.

Existing RFAs: Surveillance

14

RFA Surveillance

AMF No surveillance but with periodic consultations with members on their economic conditions

FLAR Macroeconomic Surveillance Program introduced in July 2011 and in the process of being fully implemented to include financial and banking stability to follow-up and advise member countries

EU-BOP ECOFIN and program partners including IMF shall verify compliance with the economic conditions of the MOU between the Commission and the member State prior to release of funds

CMIM Regional macroeconomic surveillance through AMRO

ACF Yes, through EDB, the manager of ACF

ESM Complements the new framework for reinforced economic surveillance in the EU, which includes a stronger a focus on debt sustainability and more effective enforcement measures, focuses on prevention and will substantially reduce the probability of a crisis emerging in the future

Existing RFAs: cases of disbursement?

RFA Fund utilization AMF Structural loans to Jordan, Morocco, Mauritania FLAR Financial credit to Bolivia, Colombia, Costa Rica,

Ecuador, Peru, Uruguay, Venezuela EU-BOP BOP assistance for Hungary, Latvia, and Romania CMIM Remains untapped since inception ACF Financial credit to Belarus and Tajikistan ESM/EFSF ESM to be used in Cyprus for first time. EFSF for

programmes in Greece, Ireland, Portugal and Spain. Hungary, Latvia, Romania with BoP assistance facility

15

Cooperation challenges and policy prescriptions

16

Why do we need RFAs? • Pros

– Better information on local conditions – Impose less stringent conditionality – May be able to immediately address local shocks

• Cons – More lenient on neighbors – Limited resource pool – Cannot address regionwide / global shocks – Lack of ample surveillance capacity

17

Strengthening Existing GSNs and RSNs • Bilateral Swaps & IMF Facilities: substitute or

complements? • Resources & linkages with central banks & central

bank’s unwillingness • Is stigma effects unique to IMF? How to reduce

stigma effects in RFAs? – Multi-country offer – Prequalification? – Build reputation by positive cases

• Increasing Paid-in capital in RFAs • Securing human capital for surveillance

18

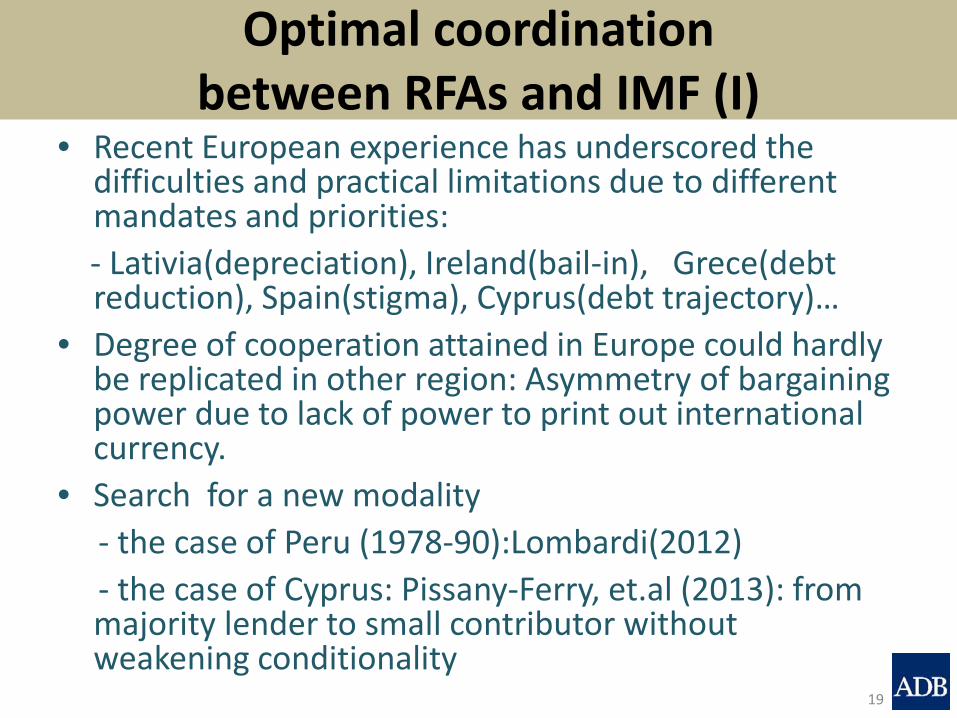

Optimal coordination between RFAs and IMF (I)

• Recent European experience has underscored the difficulties and practical limitations due to different mandates and priorities:

- Lativia(depreciation), Ireland(bail-in), Grece(debt reduction), Spain(stigma), Cyprus(debt trajectory)…

• Degree of cooperation attained in Europe could hardly be replicated in other region: Asymmetry of bargaining power due to lack of power to print out international currency.

• Search for a new modality - the case of Peru (1978-90):Lombardi(2012) - the case of Cyprus: Pissany-Ferry, et.al (2013): from

majority lender to small contributor without weakening conditionality

19

Optimal coordination between RFAs and IMF (II)

• Which conditionality to follow? - Ownership of reform can be enhanced by RFAs but can

RFAs impose conditionality? (legal issues) - Linkages with IMF: Governance issues • Decentralized and Complementary Surveillance - Track record of regional surveillance & capacity constraint - cross-regional linkages and spillovers can only be

internalized by IMF • Multi-layered and Multistakeholder lending - lend to countries or RFAs: joint lending system vs

reinsurance/guarantee system - legal issues

20

Optimal coordination within RFAs

• What are the possible forms of cooperation? – Information sharing – Capacity building – Risk sharing?

21

Optimal coordination between RFAs and RDBs

• What should be the role of regional development banks with the global/regional of safety nets? – Guarantors/ loans –ADB in 1997 and 2008 – Providers of advice – Providers of moral suasion / coordination Example is the Vienna initiative where EBRD/EIB

initiated agreement among private banks not to withdraw funds from eastern Europe in 2009

• Should other RFAs establish their version of Eurasian Development Bank to manage their funds?

22

Optimal coordination between RFAs and CBs

• What should be the role of central banks in the global system of safety nets?

• IMF coordinates swap arrangement with major central banks (Truman(2010, 2011), Korean G20)

• Linkages with through BIS? • IMF coordinating SDR allocation & swap

arrangements?

23

Thank you

Economics and Research Department

Asian Development Bank 6 ADB Avenue, Mandaluyong City

1550 Philippines www.adb.org

24