glaxo smithkline consumer healthcare ltd analyst …...quarter highlights impressive sales growth at...

TRANSCRIPT

Glaxo SmithKline Consumer Healthcare Ltd Analyst Presentation

Q 2 2011 Update

3rd August 2011

AGENDA

Quarter highlights

Financial Performance

Working Capital

Market Performance

Quarter Highlights

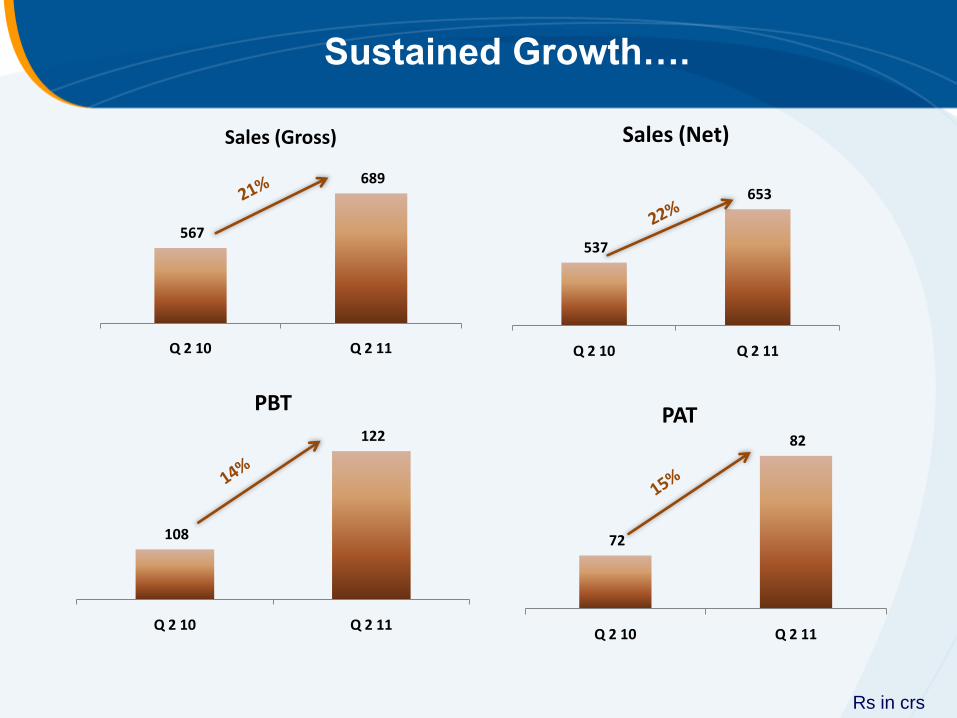

Impressive Sales Growth at 22% • Driven by strong volume growth of 16%• Best in the FMCG sector in volume

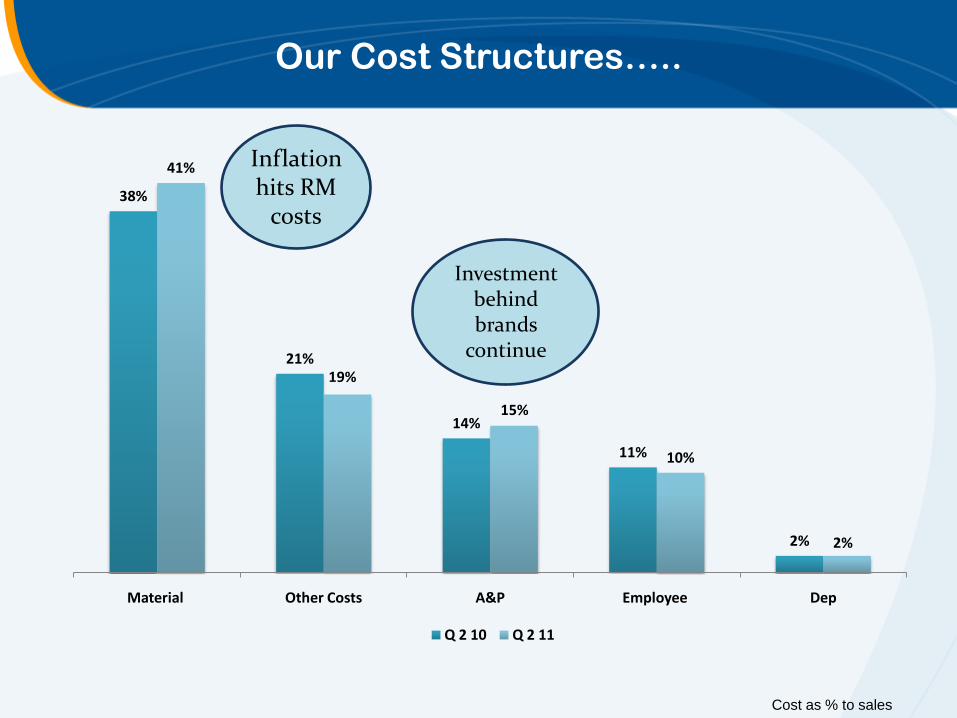

Investments behind brands continue ; A&P growing at 33%

Cost of goods sold higher by 300 bps • High Input costs • Planned lower production• Emphasis on Cost reduction initiatives

Operating profits grew by 13% ; PBT margins slightly higher at 14% leveraging treasury initiatives

PAT at Rs 83 crs grew by 15% Q on Q

Sustained Growth….

Rs in crs

567

689

Q 2 10 Q 2 11

Sales (Gross)

537

653

Q 2 10 Q 2 11

Sales (Net)

72

82

Q 2 10 Q 2 11

PAT

108

122

Q 2 10 Q 2 11

PBT

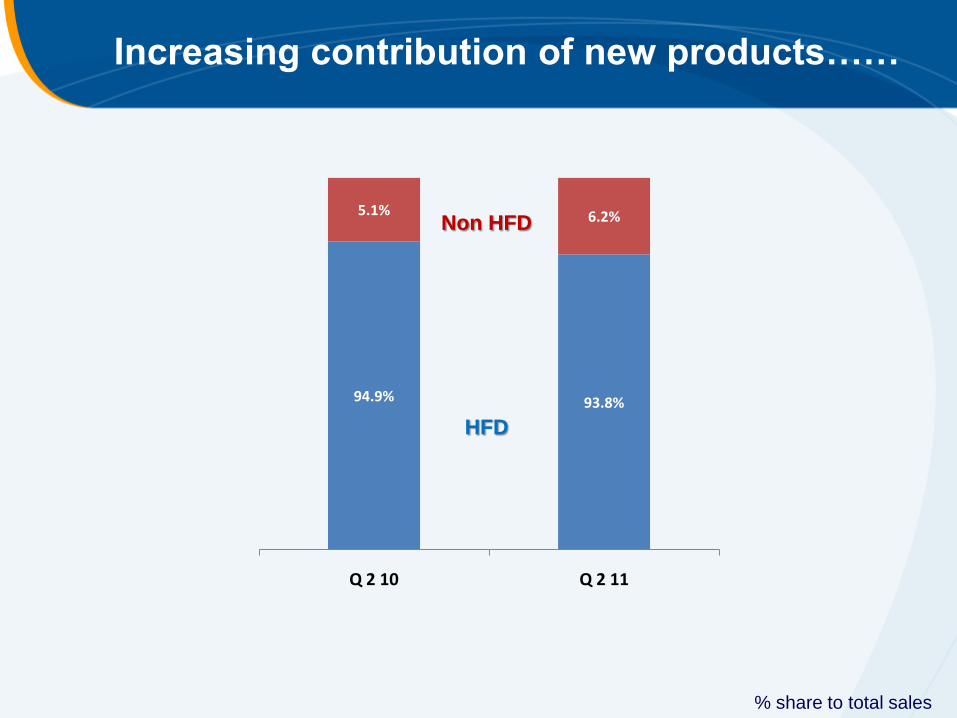

94.9% 93.8%

5.1% 6.2%

Q 2 10 Q 2 11

Increasing contribution of new products……

% share to total sales

Non HFD

HFD

Regional Split

% share to total sales

89%

11%

Domestic Exports

6%

34%

44%

4% 11%

North East South West Exports

% Increase in regions

Region % Inc

North 31%

South 16%

East 20%

West 16%

Exports 57%

5.9%15.5 %

Q on Q sales growth

Price

VolumeOverall Growth

21.4%

Other Income growing fast….

Rs in crs

13.8

8.9

4.5

18.0

14.0

4.0

Business Auxillary Comm Interest Income Others

Q 2 2010 Q 2 2011

Inflationary trend in input costs

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q 1 2011 Q 2 2011

Wheat Floursoftening a bit

18

19

20

21

22

23

24

25

Q1 2010 Q2 2010 Q3 2010 Q4 2010 Q 1 2011 Q 2 2011

Malted Barleyhigh inflation continues

16%

120 125 130 135 140 145 150 155 160 165 170 175

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q 1 2011

Q 2 2011

SMP16%

-

5

10

15

20

25

30

35

40

45

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q 1 2011

Q 2 2011

Sugarstill on the higher side20% at all time high levels

6%

Represents Q on Q inflation

Our Cost Structures…..

Cost as % to sales

38%

21%

14%

11%

2%

41%

19%

15%

10%

2%

Material Other Costs A&P Employee Dep

Q 2 10 Q 2 11

Inflation hits RM

costs

Investmentbehind brands

continue

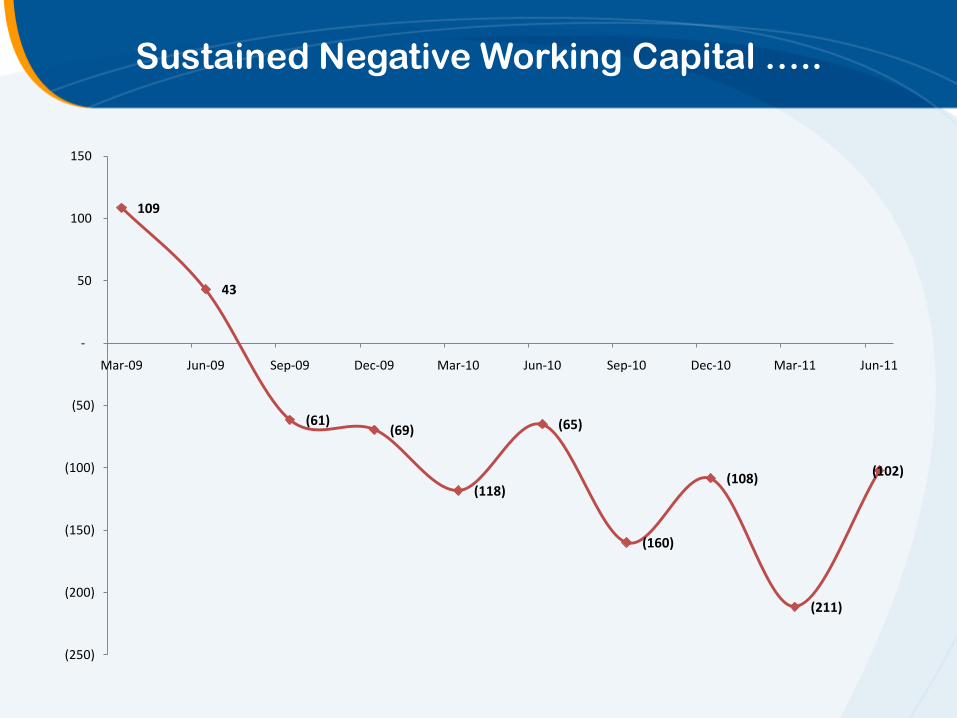

Sustained Negative Working Capital …..

109

43

(61)(69)

(118)

(65)

(160)

(108)

(211)

(102)

(250)

(200)

(150)

(100)

(50)

-

50

100

150

Mar-09 Jun-09 Sep-09 Dec-09 Mar-10 Jun-10 Sep-10 Dec-10 Mar-11 Jun-11

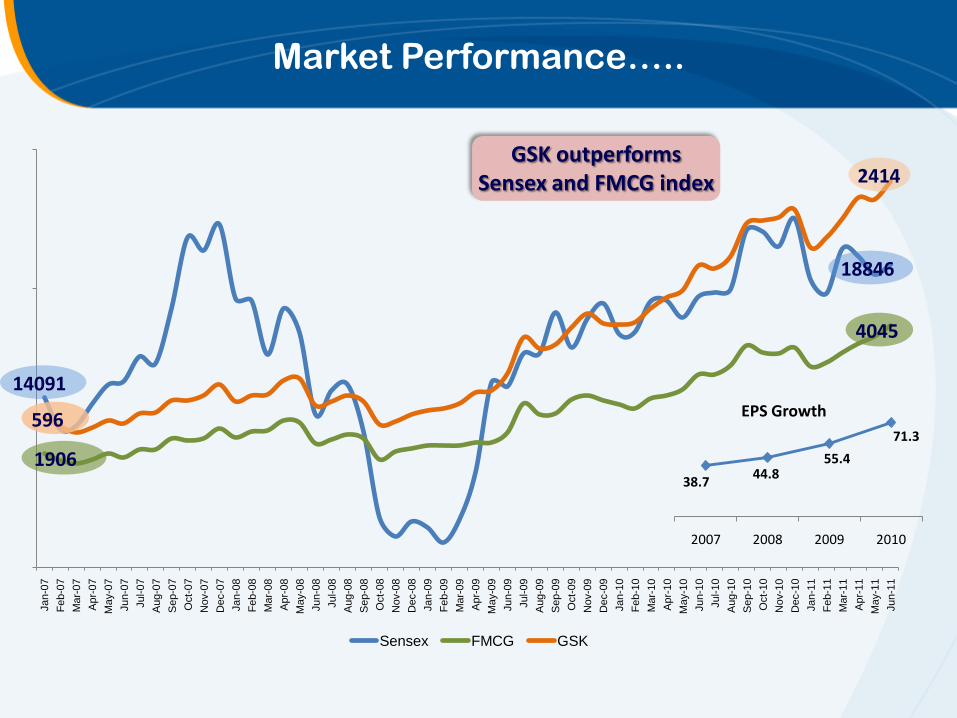

Market Performance…..Jan-0

7

Fe

b-0

7

Mar-

07

Apr-

07

May-0

7

Jun-0

7

Jul-07

Aug-0

7

Sep-0

7

Oct-

07

Nov-0

7

Dec-0

7

Jan-0

8

Fe

b-0

8

Mar-

08

Apr-

08

May-0

8

Jun-0

8

Jul-08

Aug-0

8

Sep-0

8

Oct-

08

Nov-0

8

Dec-0

8

Jan-0

9

Fe

b-0

9

Mar-

09

Apr-

09

May-0

9

Jun-0

9

Jul-09

Aug-0

9

Sep-0

9

Oct-

09

Nov-0

9

Dec-0

9

Jan-1

0

Fe

b-1

0

Mar-

10

Apr-

10

May-1

0

Jun-1

0

Jul-10

Aug-1

0

Sep-1

0

Oct-

10

Nov-1

0

Dec-1

0

Jan-1

1

Fe

b-1

1

Mar-

11

Apr-

11

May-1

1

Jun-1

1

Sensex FMCG GSK

18846

4045

2414

1906

596

GSK outperforms Sensex and FMCG index

14091

38.7 44.8

55.4

71.3

2007 2008 2009 2010

EPS Growth

Thank you