german retail strategy and operations - rwe group · german retail strategy and operations ... ii...

TRANSCRIPT

German Retail Strategyand OperationsDr. Andreas RadmacherBoard Member, Portfolio and Sales ManagementRWE Energy AG

October 26, 2006

RWE Energy Capital Market Day 2006

2

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Today’s Topics

I Positioning of RWE Energy in the German energy marketafter the first phase of liberalisation

II RWE Energy's value-oriented retail strategy

III Efficiency enhancement as an additional value driver

3

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Re-organisation of RWE Energy was implemented to meet customers’ needs

I Positioning in the German energy market

2003/2004 2005/2006

Re-organisationof RWE Group

Further enhancingRWE Energy's capabilities

Integrated offer of electricity, gas and water supply through RWE Energy Group

Merging RWE Plus, RWE Net and RWE Solutions into RWE EnergyIntegration of RWEGas and Thyssengasinto RWE EnergyEstablishment of a regional, customer-oriented organisation

Establishing RWE Key Account GmbH for focusedmarket positioning for large and sophisticated industrial customers

RWE Energy-wide portfolio optimisation throughcentral retail portfolio management

Integration of gas portfolio management for Germanyand Czech Republic

4

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

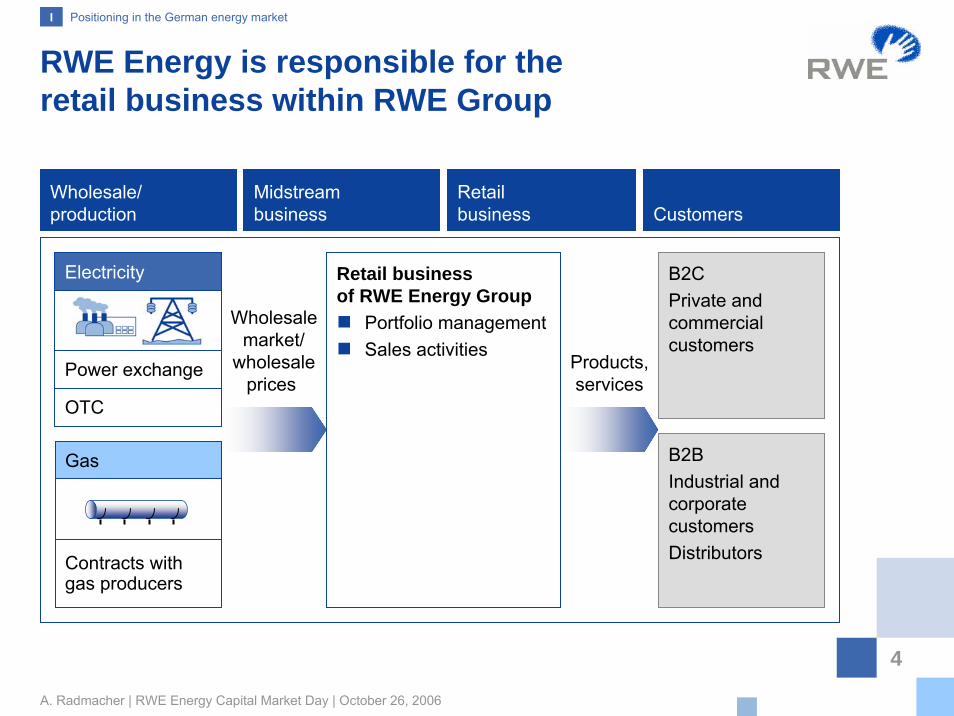

RWE Energy is responsible for the retail business within RWE Group

I Positioning in the German energy market

Wholesale/ production

Midstreambusiness

Retailbusiness Customers

Electricity

Power exchange

OTC

Gas

Contracts with gas producers

B2CPrivate andcommercial customers

B2BIndustrial and corporate customersDistributors

Retail businessof RWE Energy Group

Portfolio management Sales activities

Wholesalemarket/

wholesaleprices

Products,services

5

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

RWE Energy successfully defended its no. 1 position in the German electricity market

I Positioning in the German energy market

Market shares4 Germany 2004

Electricity Gas

Industrial/corporate

B2C

~ 7%~ 20%

~ 16% ~ 8%

External sales1 RWE Energy Germany 2005

Revenues (€ m) 7,4212/3 4,8803

Volumes (TWh) 1132 166

322

51

30 28

44

94Distributors

Industrial/corporate

Private/commercialB2C

B2B

GasElectricity

Munich

Berlin

Stuttgart

Frankfurt

Leipzig

Hamburg

Hanover

Saarbrücken Ludwigshafen

Augsburg

Dresden

Chemnitz

HalleEssen

Gelsenkirchen Dortmund

Osnabrück

Bad Kreuznach

Koblenz

Northern region

RWEKey Account

RWE RR

Süwag

VSE

LEW

enviaM

RWE WWE

Eastern region

Southern region

Central region

Western region

South-western region

1 Not including direct retail revenues and volumes from other RWE counterparties (electr. approx. 19 TWh; gas approx. 23 TWh) 2 Not including EEG/KWKG-revenues and volumes (approx. 23 TWh), EEG/KWKG are German laws referring to renewables/CHPs3 Not including electricity tax, gas tax and external grid revenues4 Comprising fully consolidated participations

6

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

– Electricity Germany –

Volumes shifted away from retail with emerging wholesale market

1 1998: Comprising RWE (old) and VEW (Merger to RWE (new) in 2000)2 Total volume of 197 TWh excludes EEG-/KWKG-volumes of approximately 23 TWh, EEG/KWKG are German laws referring to renewables/CHPs

Development of sales structure

I Positioning in the German energy market

External sales External sales2

Declining share of direct retail

Retail100%

Retail64%

Wholesale36%

Pre-Market Opening (1998)

Competition(2005)

TotalGermany

RWEGroup1

520 TWh

197 TWh

453 TWh

167 TWh +18%

+15%

RWE kept up with growth of German electricity market

With liberalisation a liquid wholesale market developed, wholesale prices became transparent

Share of direct retail market decreased due to shift of volumes to wholesale

The challenge for RWE Energy is to retain retail customers with attractive services/products at positive profit margins

Emerging wholesale market

7

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2C electricity gross margin is a relevantvalue driver – but a cost driver as well

I Positioning in the German energy market

Before liberalisation (1998) Competition (2005)

1 Sales of other RWE counterparties 2 Not including EEG/KWKG-revenues and volumes (approx. 23 TWh), EEG/KWKG are German laws referring to renewables/CHPs3 1998: Comprising RWE (old) and VEW (Merger to RWE (new) in 2000)4 Gross margin: Revenues – (governmental charges + energy procurement + grid fees)

Electricity sales volumeRWE Group3 Germany

Electricity sales volumeRWE Group Germany

Electricity gross margin4

RWE Energy Germany

Industrial/corporate

72

B2C32

Distributors63

Others1 13

Distributors2

32

Wholesale71

Industrial/corporate

51

B2C 30

Industrial/corporate

33%

B2C60%

167 TWh

197 TWh 100%Approx. 165 customers

Approx.46,000 customers

Approx. 7.13 millioncustomers

Distributors 7%

8

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

RWE Energy will continue tofocus on value above volume

* Gross margin: Revenues – (governmental charges + energy procurement + grid fees)

RWE Energy successfully implementeda value-oriented retail strategy

I Positioning in the German energy market

– RWE Energy Electricity Germany –

Development of volume and gross margin*

2003 2004 2005 ...

Gross margin

Sales volume

Value-oriented retail strategy

Portfolio adjustment led to reduced volume, especially in B2B-segments

Value-orientation results in increasing total margin

100%

9

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Today’s Topics

I Positioning of RWE Energy in the German energy marketafter the first phase of liberalisation

II RWE Energy's value-oriented retail strategy

III Efficiency enhancement as an additional value driver

10

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Main challenges going forward: Electricity

Segments Market trends Critical success factors

General High prices, volatility and liquidity dominate the market

Apply value-oriented sales policy,especially in periods of high energy prices

Benefit from market opportunities

B2C Increasing competition and churn rates in Germany

Enhance customer retentionby service leadership

Achieve process excellence& improve cost-to-serve

B2B Customers purchase more professionally. Increasing market know-how and demand for structured products

Intensify knowledge about customers

Market tailor-made products, increase product innovation rate, and improve time-to-market

Bundle know-how and processes

II Value-oriented retail strategy

11

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Main challenges going forward: Gas

Segments Market trends Critical success factorsImport dependency increases, few players dominate the upstream business

Improve the position in the market

Increase portion of direct purchasefrom producers

LNG will play an important role Diversify purchase portfolio

Get access to projects & counterparties

Evolving of liquid hubs Centralise portfolio management

Get access to hubs & counterparties

B2C New market model in Germany sets the course for increasing competition and churn rates

Adapt to customer needs

Prepare for more intensive competition

General

B2B Customers purchase more professionally. Competition increases,especially in the distributor segment

Intensify knowledge about customers and market products according to customer needs

II Value-oriented retail strategy

12

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Market environment for B2C in Germany differs from UK with developed competition

II

"Acquisition market" with high competition and switchingCompetition defines achievable retail marginsFocus on both– New customer acquisition– Customer retentionPlayers act nation-wideIn line with competitive gas market

Market environment B2C

Source customer switching and price: VDEW, Eurostat, Ofgem (2005)

So far "consolidation market" with limited churn rate and small retail margins – not attractive for new entrantsSo far focus on retaining customers, acquisition by focused market playersMany players act regional, some nation-wideCompetition in gas is expected to develop

Customer switchingsince 1999 (electricity)

Customer switchingsince 1999 (electricity)

UK

Ger

man

y

51%

5%

Neverswitched

Vendorswitchedat least once

Neverswitched

Vendorswitchedat least once

Value-oriented retail strategy

13

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

End of ex-ante price approval for B2C electricity may result in higher competition

In line with UK, the Netherlands, Austria, and the Scandinavian countriesGermany will also foster competition in the B2C market by abolishing ex-ante price approval as of July 2007

In markets with ex-ante price approval the sales gross margin is limitedby the difference between approved end-customer prices and initial costs (e.g. Germany: sales gross margin1 B2C 30 €/cust. p.a.2)

Market forces will decide the margin level in a de-regulated German electricity market. As a study shows, a pre-requisite for more intensive competition is a sales gross margin B2C of more than 60 €/cust. p.a.2

Experience from de-regulated markets abroad also shows that sales gross margins increase with the end of ex-ante price approval (e.g. UK: 100 €/cust. p.a.3, Sweden: 116 €/cust. p.a.4) and thus retail business becomes more attractive with more competitive activitiesby incumbents and new players

To retain customers and margins in such a competitive environment attractive products and high service quality are critical success factors

II Value-oriented retail strategy

1 Gross margin: Revenues – (governmental charges + energy procurement + grid fees)2 Source: Expertise of the University of Mannheim (Dec. 2005)3 Source: Eurostat, Ofgem (2005)4 Source: Eurostat, Nord Pool, Swedish Energy Agency (2005)

14

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

With higher competition incumbentsare expected to lose B2C market share

1 Example of incumbents in UK and NL 2 1999 – 2002: price-caps for ex-Public Electricity Suppliers in core region

Few customers actively hunt for price and switch supplierSome more customers might be motivated to switch, if – Actively approached

by competitors– Dissatisfied with current

supplierThe majority will stay with their vendor, if he invests in– Sufficient customer

satisfaction– Active customer retention

Different customer types Experience from other countries

Outside core region:(in equivalents to market share in core region)

ExampleUK1

ExampleNL1

15%

5%

II

In core region:(market share)

Prices de-regulated

ExampleUK1

ExampleNL1

Since 20022

Since 2004

100%

85%

60% With increased competition after price de-regulation from July 2007German incumbents may lose some market share

Value-oriented retail strategy

15

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2C customers in Germany: Cost savings are important for return, but there are more levers

II

* Gross margin: Revenues – (governmental charges + energy procurement + grid fees)

Source: VDEW, VDN, RWE Energy (2005)

Price components private customers 2005(3,500 kWh/a, approx. 19.46 ct/kWh)

Cost of sales have a minor impact on market success (example Germany)

Sensitivity for 1% change of driver

Effective lever for margins (example Germany)

39%

35%

4%

22%

Sales

Electricityprocurement

Govern-ment

Regulated grid

Changeprice

Change no.of customers

Changecost of sales

Driver Effect on gross margin*

Value-oriented retail strategy

16

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2C customer needs:Different customer groups have specific needs

Product Portfolio

Purely online product

Non-flexible payment policy

Long period tie-in

Light productNo frills

Short payment periods

Non-flexible payment policy

Basic tariffFixed price

Services, customer card, etc.

Individual communication

Non-flexible payment policy

Basic productFixed price

Services, customer card, etc.

Target-group specific services

More flexible payment policy

etc.

Comfort products

II Value-oriented retail strategy

Customer Service Needs

17

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2C strategy:Customer retention and selective acquisition

Be the supplier of choice – retain and satisfy our customers

Satisfy customers in developing market with flawless, excellent service and customer care

Expand investment in customer retention to prepare for upcoming competition –prepare today for tomorrow's success

– Differentiated products and value-added services for different customer groups

– Trust and popularity for RWE/regional brands

– Established customer retention tools (loyalty cards, customer magazine, communication, events)

Ele

ctric

ityG

as/H

eatin

g Market cross-commodity heating services (gas, heat pump, etc.)

Tap potential from dual fuel

Develop the market on the basis of customer value: retain existing customers, acquire new ones

II Value-oriented retail strategy

18

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Also sold indepen-dently of energy supply

B2C: Examples for customer retention instruments

II

* www.klima-sucht-schutz.de (oil: 5400 kg CO2/a, heat pump: 3500 kg CO2/a; full costs oil: 2700 €/a, heat pump: 1900 €/a)

Advantages for customers through service partnersBrand/value perception reinforcedSwitching less likely

Extra services: customer cards

Heat pump with ecological advantage– Saves 2 t CO2 p.a. compared to oil – Cost advantage of € 12,000 in 15 years*RWE Energy supports installation through its market partners (marketing, subsidies)Growing market in Germany– 100,000 units sales potential in the

next 3 years– Of which a market share of 25% is achievableRWE Energy achieves long-term customer retention and increase of market share in heating – especially compared to oil

Heat pump

Credit card function

Additional options

Value-oriented retail strategy

19

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Customers are acquired via perceivable price differenceRegionally different levels of prices and margins require regional offers

B2C electricity: Customer acquisition only by regionally competitive prices

Average gross margin*

Regional incumbents define required price offer

* Gross margin: Revenues – (governmental charges + energy procurement + grid fees)

For the time being, little interestof customers in switching

Only offers in selected regions are feasible– Prices as low as necessary– Focus on high-margin regions

allows profits

Competitive prices and differentiated offers require lean and flexible business models for acquisition

Standard nation-wide pricing and market approach are not promising

Incumbent Competitor

Requiredprice difference

II Value-oriented retail strategy

20

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2C gas: Customer acquisition activities will be pursued as market develops

Politicians ask for competition

Pressure on grid charges

Roadmap for implementation of switching processes

Competition in gas is expected to develop

Present market framework offers hardly any market potential for growth

– Significant handling costs do not allow profits

– Switching processes have to be implemented in industry-wide approach

RWE Energy is actively preparing for future competition

– Development of products and marketing strategies

– Implementation of billing/switching processes

As soon as value-oriented growth is possible in the market, RWE Energy will actively enter into developing competition

II Value-oriented retail strategy

21

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2B: Customers’ energy market know-howdrives requirements

Corporate customersDemand full-energy supply

Relationship-oriented customers

Corporate customersand distributorsIncreasing interestin market pricedevelopmentNo structuring competency

Market-oriented customers

Sophisticated key accounts

Wholesale players

A B C D

Industrial customersand distributorsAdvanced energysector know-howIndividual products

Industrial customersand distributorsActive players in the wholesale marketStandard wholesale products

Cha

ract

eris

tics/

Req

uire

men

tsVo

l.

II

Approx. ≤ 2 GWh/a

Mar

ket

Tren

d

Approx. ≥ 2 GWh/a Approx. ≥ 20 GWh/a >> 20 GWh/a

Share of totalcustomers declining

Share of total customers rising

Share of total customers rising

Share of total customers stable

Value-oriented retail strategy

22

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2B strategy:Differentiated approach for customer types

Carefully push full-energy supply

Relationship-oriented customers

Selectively market standardised structured products

Market-oriented customers

Bring innovative products quickly and efficientlyto the customers

Sophisticatedkey accounts

Wholesaleplayers

A B C D

Offer standardised products to satisfied customers – at low cost-to-serve

Selectively market individual structured products

Handle standar-dised wholesale products efficiently

Market additional energy-related services

Ele

ctric

ityG

as

Market standardised products to existingand to new customers as market develops

Market innovative products and portfolio services to existing and to new customersas markets and customers develop

Develop the market on the basis of customer value: retain existing customers, acquire new ones

II Value-oriented retail strategy

23

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2B: Standardised structured productsfor market-oriented corporate customers

II

Product example: Süwag Electricity Fund

Portfolio managementservices even for customerswith smaller energy volumes

Spreading the procurementrisk over time

Time-optimised procurement

Differentiation vis-à-vis customers

Volume,customer 1

Volume,customer 2

Volume,customer 3

Electricityfund

Furthercustomers

Several customers with individual contracts integrated in the electricity fundJoint manage-ment of the portfolio by Süwag

Energy volume split into tranchesIndividual tranches bought at different times by Süwag portfolio management Buying

tranches

Value-oriented retail strategy

24

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

B2B: Individual structured products for sophisticated industrial key accounts (1)

II

RWE Key Account Portfolio ManagementPortfolio monitoring and management is customers’daily business. Risk management gains importanceRWE Key Account supports their customers in developing, performing and monitoring individualrisk strategies

Product example

Customers are enabled to optimise their portfolio very flexibly– Products– Timeframe– Counterparties

"VIEW" as a professional internet tool to support portfolio management– Real-time portfolio analysis– Tracking of market

development– Support transaction and

risk management process

Customers' advantages

Value-oriented retail strategy

25

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

RWE Key Account Secure Catcher

Priceadjustment

Deliverystart

B2B: Individual structured products for sophisticated industrial key accounts (2)

II

RWE Key Account Power Casher

Product example Product example

RWE Key Account GmbH (KAG) buys from customers the right to use their assets flexibly –within defined limits Customers guarantee minimum availabilityKAG pays a fixed service premium for the assets to be kept availableWhen the assets are used, KAG pays an additional charge KAG organises market access processes for the customer

"Secure Catcher" allows customers to make a one-time adjustment to their contract prices and thus the opportunity to take advantage of declining market prices An option premium is charged for the possibility to adjust the contract

Market price in linewith OTC forwards

Price in line with"Secure Catcher"

(€/m)

Value-oriented retail strategy

26

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Operating distribution system in line with EU unbundlingGrid development planningBudget planning / targets to operator

Distribution System Operator (DSO)

B2B: Energy supply and service offers for distributors are coordinated by regional KAM

II

Supplying electricity and gasPortfolio management electricity and gas

Sales unit of Regional Energy Company (REC) / Key Account Manager (KAM)

Comprehensive service offeringInformation platform (extranet) Offer of consulting services, tools

Network Partners Club (NPC)

Billing and balancingCustomer support

Customer ServiceCompany (CSC)

Operating grids and assets Metering data managementMedium voltage plants, inspection, maintenance, analysis of insulating oil

Grid Service Company (GSC)

Value chain distributor

… Grid Billing RPM Sales

REC

DSO GSC CSC Sales ...

Key Account Manager (KAM)

Value-oriented retail strategy

27

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Today’s Topics

I Positioning of RWE Energy in the German energy marketafter the first phase of liberalisation

II RWE Energy's value-oriented retail strategy

III Efficiency enhancement as an additional value driver

28

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Central retail management of RWE Energy AG acts as a platform for best practice transfer

III Efficiency enhancement as an additional value driver

Create transparency and understanding as a starting point, e.g.

Definition of KPIs (revenues, costs and margin)Benchmarking between RECs

Product: electricity fund at SÜWAG applicable to other RECs

Reduction of cost-to-serve by harmonisation of IT-structure across RECsFurther stimuli by tracking of KPIsand process performance –internal competition

Identify best-practiceprocesses/products, e.g.

Roll-out best practice approach throughout the group, e.g.

Customer segmentationDifferentiated products and value-added servicesCustomer retention tools

Achieve efficiency gainsand set stimuli for further improvements, e.g.

29

A. Radmacher | RWE Energy Capital Market Day | October 26, 2006

Efficiency: Reducing cost-to-serve –example of optimising IT

1 Cost-to-serve B2C: Front & back office customer care and billing activities2 Gross margin: Revenues – (governmental charges + energy procurement + grid fees)

Reduction ofcost-to-serve

Market-driven harmonisation of the group-wide IT-requirements and IT-operations Realisation of synergies through group-wide best practice transferRoll-out of IT-approach to other cost drivers

III Efficiency enhancement as an additional value driver

Cost-to-serve1 B2CReducing IT-costs despite increasing requirements

Cost driverscost-to-serve

Gross margin2

Profit

Sales costs

– Cost-to-serve

– Marketing

– Acquisition

– Bad debt losses

– Other sales costs

Per-sonnel

Other

IT

Increasing requirements

Unbundling

Complex products

Customer interfaces

...

90%

100%

2005 2007 2009

ReducingIT-costs