german real estate market in a good state - … · german real estate market in a good state real...

TRANSCRIPT

GERMAN REAL ESTATE MARKET IN A GOOD STATE

REAL ESTATE MARKET GERMANY 2013 | 2014

A RESEARCH PUBLICATION BY DG HYP OCTOBER 2013

1

Real Estate Market Germany 2013 | 2014

Table of Contents

Preface ___________________________________________________________________ 2

Summary _________________________________________________________________ 3

Economic Conditions in Germany ____________________________________________ 5

German Real Estate Market buoyant compared to the rest of Europe __________ 6

Retail Properties ___________________________________________________________ 10

Office Properties __________________________________________________________ 23

Residential Properties ______________________________________________________ 35

Overview of Forecasts _____________________________________________________ 39

Imprint ___________________________________________________________________ 40

Disclaimer _________________________________________________________________ 40

DG HYP Offices ____________________________________________________________ 41

2

Real Estate Market Germany 2013 | 2014

Preface

As a commercial real estate bank, we support our business divisions and risk manage-ment teams with their credit and lending decisions through regular analysis of the markets we actively cover. We publish the results of our analyses in commercial real estate market reports, targeting investors as well as our partners within the Coopera-tive Financial Services Network: these are German cooperative banks, with whom we jointly originate financings in the various regions.

The present report continues our series of studies concerning the German real estate market, published in the autumn of each year. This research study looks at market developments for retail, office and residential real estate during 2013, and provides an outlook for 2014.

Our analysis has shown that the German commercial real estate market in the prime locations of Hamburg, Berlin, Cologne, Dusseldorf, Frankfurt, Stuttgart and Munich is in a good state. Whilst the euro debt crisis and the recession in the euro zone have left their marks on the German economy as well, economic momentum has been driven especially by the domestic economy, helped by a benign labour market and rising personal incomes. On the real estate market, these favourable developments translate into rising rents for the three market segments we have analysed: retail, office and residential. Economic recovery is expected to continue during the second half of the year: hence, the chances are good that the positive trend on real estate markets is set to prevail.

In a European context, top locations in Germany have thus shown above-average per-formance. Thanks to unabated interest from domestic as well as international investors in German commercial real estate, Germany has seen a marked increase in its market share amongst the five major European real estate markets (Germany plus the United Kingdom, France, Italy and Spain). In fact, the share of Germany in aggregate invest-ments in these five countries (excluding residential portfolios) rose from around 20 per cent in 2009 to as much as 30 per cent last year.

The German real estate market report is of course also available in German. All pre-viously published DG HYP market reports can be downloaded from our website (on www.dghyp.de/en/unternehmen/market-research; contact us if you prefer a printed version.

Deutsche Genossenschafts-Hypothekenbank AG

October 2013

3

Real Estate Market Germany 2013 | 2014

SUMMARY

» The German commercial real estate market remains buoyant in the seven top locations reviewed - Berlin, Dusseldorf, Frankfurt, Hamburg, Cologne, Munich and Stuttgart. The euro debt crisis and the recession in the eurozone have also had a negative impact on the German economy. However, the robust labour market with almost 42 million people in employment is ensuring good demand for office space. Rising wages are supporting the retail sector and helping private households to pay increasing rents.

» The positive conditions are reflected in rising rents in the three market segments considered - retail, office and residential. The top German locations are thus outperforming by European standards, as evident from our comparison of important European real estate markets.

» The German economy has now emerged from the lean period at the end of 2012 / beginning of 2013, returning to positive growth again in the spring. The domestic economy in particular is recovering and is driving the economy for-ward. Despite the strained conditions affecting other countries, the economic recovery is likely to continue in the second half. Sentiment indicators for com-panies, such as the ifo business climate, have therefore shown positive read-ings in recent months. There is therefore a good chance that the positive sentiment will also continue in the real estate market.

RETAIL PROPERTIES

Change in rent in % y-o-y

Prime rents in EUR per sqm

2012 2013e 2014e 2012 2013e 2014e

Berlin 6.7 5.0 3.2 240 252 260

Cologne 4.4 2.1 2.1 235 240 245

Dusseldorf 1.4 4.5 4.3 220 230 240

Frankfurt 3.9 1.9 1.9 265 270 275

Hamburg 4.3 4.1 2.0 245 255 260

Munich 3.4 3.3 3.2 305 315 325

Stuttgart 0.0 3.6 3.0 225 233 240

Average for top locations 4.6 3.9 2.8 248 258 265

Source: BulwienGesa, Feri, DZ BANK Research forecast

» While retail sales are growing only slightly despite the positive economic condi-tions, central shopping areas in prime locations are enjoying a high level of popularity. This is being boosted by the purchasing power of tourists and busi-ness travellers. Retail space in the 1A sites of top locations therefore remains attractive to, and is generating strong demand from national and international chain stores as well as mono-label and flagship stores. However, the volume of space in these locations is severely limited.

» Prime rents in prime locations are therefore continuing to rise. Average rents of almost EUR 260 per sqm are being paid this year. The upward pace is however likely to weaken slightly as a result of the economic slowdown and the high level of rents.

4

Real Estate Market Germany 2013 | 2014

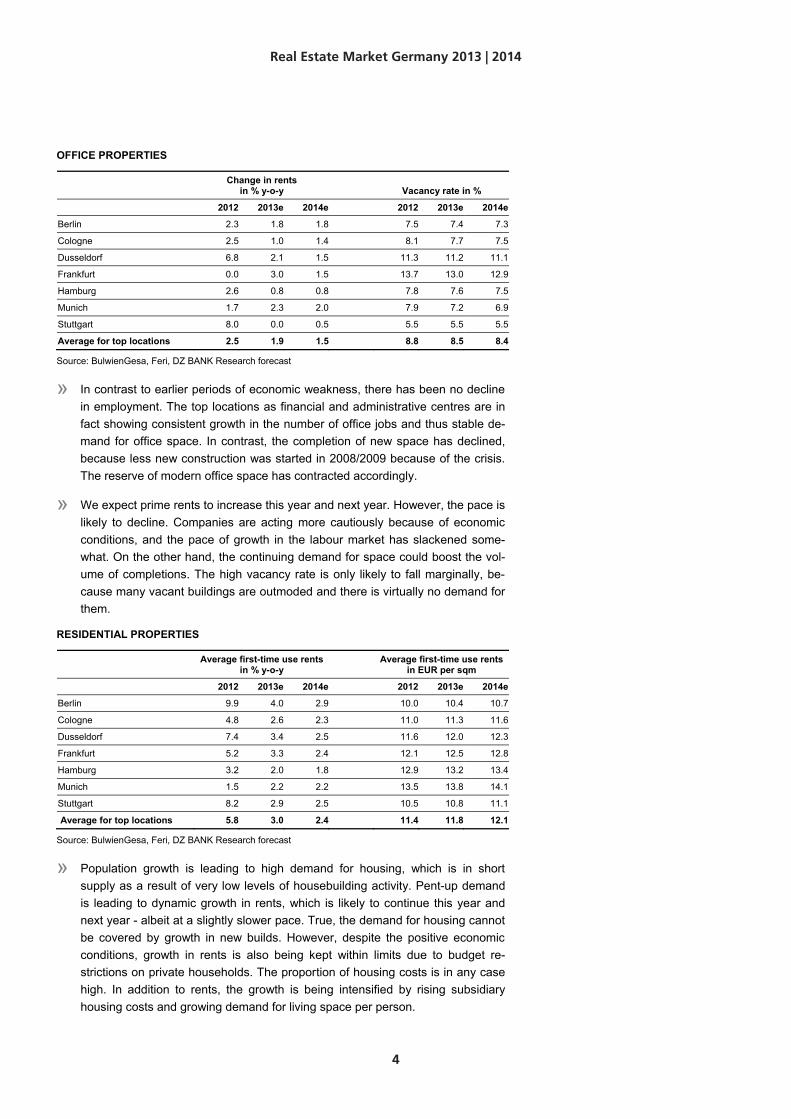

OFFICE PROPERTIES

Change in rents in % y-o-y Vacancy rate in %

2012 2013e 2014e 2012 2013e 2014e

Berlin 2.3 1.8 1.8 7.5 7.4 7.3

Cologne 2.5 1.0 1.4 8.1 7.7 7.5

Dusseldorf 6.8 2.1 1.5 11.3 11.2 11.1

Frankfurt 0.0 3.0 1.5 13.7 13.0 12.9

Hamburg 2.6 0.8 0.8 7.8 7.6 7.5

Munich 1.7 2.3 2.0 7.9 7.2 6.9

Stuttgart 8.0 0.0 0.5 5.5 5.5 5.5

Average for top locations 2.5 1.9 1.5 8.8 8.5 8.4

Source: BulwienGesa, Feri, DZ BANK Research forecast

» In contrast to earlier periods of economic weakness, there has been no decline in employment. The top locations as financial and administrative centres are in fact showing consistent growth in the number of office jobs and thus stable de-mand for office space. In contrast, the completion of new space has declined, because less new construction was started in 2008/2009 because of the crisis. The reserve of modern office space has contracted accordingly.

» We expect prime rents to increase this year and next year. However, the pace is likely to decline. Companies are acting more cautiously because of economic conditions, and the pace of growth in the labour market has slackened some-what. On the other hand, the continuing demand for space could boost the vol-ume of completions. The high vacancy rate is only likely to fall marginally, be-cause many vacant buildings are outmoded and there is virtually no demand for them.

RESIDENTIAL PROPERTIES

Average first-time use rents in % y-o-y

Average first-time use rents in EUR per sqm

2012 2013e 2014e 2012 2013e 2014e

Berlin 9.9 4.0 2.9 10.0 10.4 10.7

Cologne 4.8 2.6 2.3 11.0 11.3 11.6

Dusseldorf 7.4 3.4 2.5 11.6 12.0 12.3

Frankfurt 5.2 3.3 2.4 12.1 12.5 12.8

Hamburg 3.2 2.0 1.8 12.9 13.2 13.4

Munich 1.5 2.2 2.2 13.5 13.8 14.1

Stuttgart 8.2 2.9 2.5 10.5 10.8 11.1

Average for top locations 5.8 3.0 2.4 11.4 11.8 12.1

Source: BulwienGesa, Feri, DZ BANK Research forecast

» Population growth is leading to high demand for housing, which is in short supply as a result of very low levels of housebuilding activity. Pent-up demand is leading to dynamic growth in rents, which is likely to continue this year and next year - albeit at a slightly slower pace. True, the demand for housing cannot be covered by growth in new builds. However, despite the positive economic conditions, growth in rents is also being kept within limits due to budget re-strictions on private households. The proportion of housing costs is in any case high. In addition to rents, the growth is being intensified by rising subsidiary housing costs and growing demand for living space per person.

5

Real Estate Market Germany 2013 | 2014

ECONOMIC CONDITIONS IN GERMANY

ECONOMIC FORECAST GERMANY

in % y-o-y 2011 2012 2013e 2014e

GDP 3.3 0.7 0.6 2.0

Private consumption 2.4 0.7 0.9 1.4

Public consumption 1.1 1.0 0.8 1.0

Investment 6.9 -2.1 -1.4 4.5

Exports 8.0 3.3 1.4 7.8

Imports 7.4 1.4 2.1 8.4

Inflation rate (HVPI) 2.5 2.1 1.7 2.1

Unemployment rate (BA) 7.1 6.8 6.9 6.8

Budget balance in % of GDP -0.8 0.2 0.1 0.3

Source: DZ BANK Research

The German economy has now emerged from the lean period at the end of 2012 / beginning of 2013, returning to positive growth again in the spring. GDP increased by 0.7 per cent in the second quarter after stagnating at the beginning of 2013. The German economy in particular is recovering and is driving the economy forward. However, the external economic environment remains strained due to the ongoing negative effects of the eurozone crisis and the difficulties in some other regions of the world. The signs are that the recovery will continue in the second half. Sentiment indicators for economies, such as the ifo business climate, have shown a positive trend in recent months, and companies are more confident again about their business prospects. Private households are also showing optimism in surveys. The positive employment situation and income growth are providing stable conditions for private consumer spending. We expect macroeconomic growth of 0.6 per cent this year and, on average, stronger annual growth of two per cent in 2014. The unemployment rate - which has increased slightly this year - is likely to return to its 2012 level next year.

GDP GROWTH Y-O-Y IN PER CENT UNEMPLOYMENT RATE IN PER CENT

Source: DZ BANK Source: DZ BANK

-6

-4

-2

0

2

4

6

2002 2004 2006 2008 2010 2012 2014e

Germany

Eurozone5

6

7

8

9

10

11

12

13

2002 2004 2006 2008 2010 2012 2014e

Germany

Eurozone

German economy emerges from lean period

Indicators point to continuing recovery

6

GERMAN REAL ESTATE MARKET BUOYANT COMPARED TO THE REST OF EUROPE

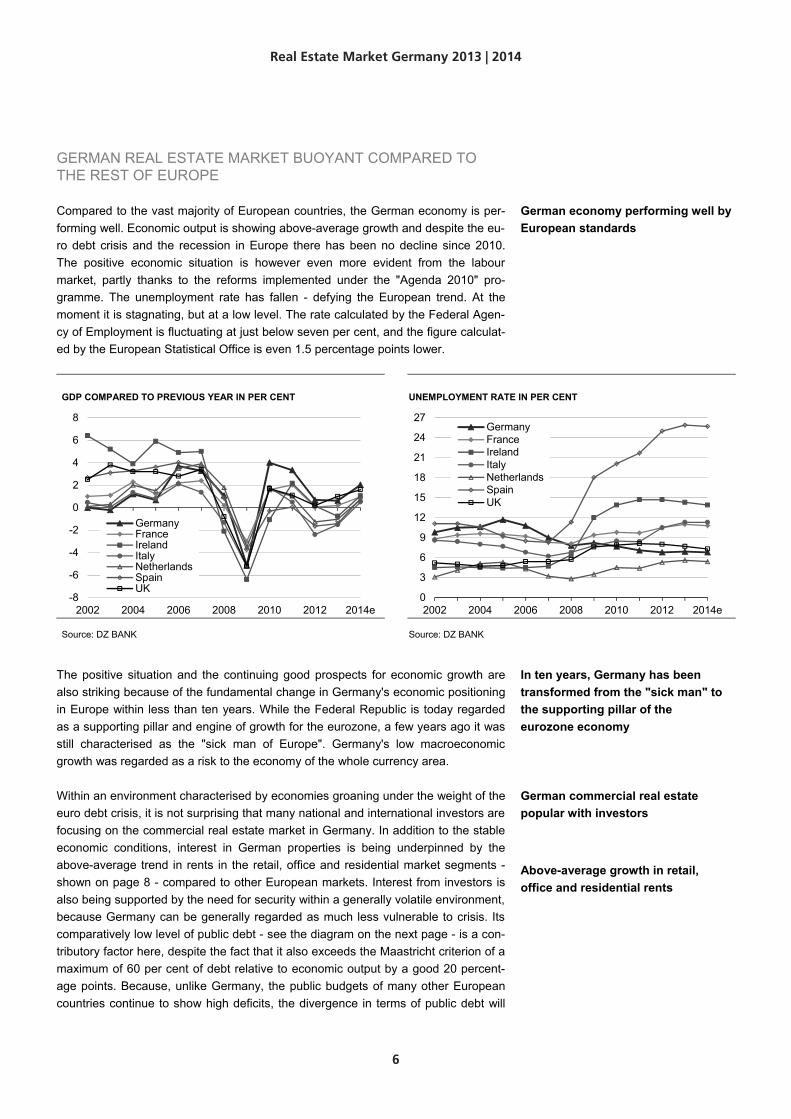

Compared to the vast majority of European countries, the German economy is per-forming well. Economic output is showing above-average growth and despite the eu-ro debt crisis and the recession in Europe there has been no decline since 2010. The positive economic situation is however even more evident from the labour market, partly thanks to the reforms implemented under the "Agenda 2010" pro-gramme. The unemployment rate has fallen - defying the European trend. At the moment it is stagnating, but at a low level. The rate calculated by the Federal Agen-cy of Employment is fluctuating at just below seven per cent, and the figure calculat-ed by the European Statistical Office is even 1.5 percentage points lower.

GDP COMPARED TO PREVIOUS YEAR IN PER CENT UNEMPLOYMENT RATE IN PER CENT

Source: DZ BANK Source: DZ BANK

The positive situation and the continuing good prospects for economic growth are also striking because of the fundamental change in Germany's economic positioning in Europe within less than ten years. While the Federal Republic is today regarded as a supporting pillar and engine of growth for the eurozone, a few years ago it was still characterised as the "sick man of Europe". Germany's low macroeconomic growth was regarded as a risk to the economy of the whole currency area.

Within an environment characterised by economies groaning under the weight of the euro debt crisis, it is not surprising that many national and international investors are focusing on the commercial real estate market in Germany. In addition to the stable economic conditions, interest in German properties is being underpinned by the above-average trend in rents in the retail, office and residential market segments - shown on page 8 - compared to other European markets. Interest from investors is also being supported by the need for security within a generally volatile environment, because Germany can be generally regarded as much less vulnerable to crisis. Its comparatively low level of public debt - see the diagram on the next page - is a con-tributory factor here, despite the fact that it also exceeds the Maastricht criterion of a maximum of 60 per cent of debt relative to economic output by a good 20 percent-age points. Because, unlike Germany, the public budgets of many other European countries continue to show high deficits, the divergence in terms of public debt will

-8

-6

-4

-2

0

2

4

6

8

2002 2004 2006 2008 2010 2012 2014e

GermanyFranceIrelandItalyNetherlandsSpainUK

0

3

6

9

12

15

18

21

24

27

2002 2004 2006 2008 2010 2012 2014e

GermanyFranceIrelandItalyNetherlandsSpainUK

German economy performing well by European standards

In ten years, Germany has been transformed from the "sick man" to the supporting pillar of the eurozone economy

German commercial real estate popular with investors

Above-average growth in retail, office and residential rents

Real Estate Market Germany 2013 | 2014

7

also continue to grow. There is therefore a good chance that Germany will remain one of the small group of countries awarded top ratings by the rating agencies Standard & Poor‘s, Moody’s and Fitch.

PUBLIC DEBT RELATIVE TO GDP IN PER CENT NEW DEBT RELATIVE TO GDP IN PER CENT

Source: DZ BANK Source: DZ BANK

Interest from investors in the German commercial real estate market is evident from the disproportionate growth in investment volume, which is shown in the diagrams on the next page. Housing portfolios are not included. The German proportion of in-vestment volume in the five countries - apart from Germany, these are France, the UK, Italy and Spain - has increased since 2009 from around 20 per cent to 30 per cent last year. This corresponds to a volume of around EUR 25bn. On the other hand, the figure has fallen in the periphery countries Italy and Spain. These two countries jointly do not even account for a proportion of five per cent. Although the volume relating to the UK - the largest commercial real estate market in Europe - has grown strongly, in relative terms the large British proportion has however de-clined slightly. France, the third largest European market for commercial real estate, performed well up to 2011. However, since last year, the weak economic situation and the backlog of reforms of the Socialist government led by President Hollande have had an impact. Consequently, investment volume in France declined in 2012, with the proportion relative to the market down again to just below 20 per cent.

Investment volume in the German commercial real estate sector is likely to exceed the previous year's level again this year, although no major surges are expected. Continuing strong demand from investors for lower-risk "core properties" accounts for only a small proportion of the market, and the number of transactions is therefore small. Although demand is picking up in the higher-risk "value added" and "opportun-istic" market segments as risk aversion eases, the limited amount of financing avail-able here is an obstacle to high volumes. In terms of types of property, in 2012, office space, which accounted for some 45 per cent of German investment volume, replaced retail space - which had been the frontrunner up to 2011.

60

70

80

90

100

110

120

130

140

DE FR IE IT NL ES UK

2011201220132014

Maastricht threshold: 60%

-15

-12

-9

-6

-3

0

3DE FR IE IT NL ES UK

2011201220132014 Maastricht threshold: -3%

Germany's market share has increased visibly

In 2012, investment in German commercial real estate reached EUR 25bn, and should increase slightly in 2013

Real Estate Market Germany 2013 | 2014

8

INVESTMENT IN COMMERCIAL PROPERTIES BY VOLUME AND … … AS A PROPORTION IN THE COUNTRIES REVIEWED

Source: BNPP Real Estate Source: BNPP Real Estate, own calculations

The shift in country weighting by investors within Europe due to varying economic trends has also been reflected in the rental yields on commercial properties. However, the range of about 100 basis points between the countries is fairly stable. In line with the varying tends in prices and rents, the sequence of the countries has however undergone a shift. Of the five countries already mentioned, Germany has shown the lowest level of average rental yield since 2009 due to the more moderate risk assessment for both retail and office property. Interestingly, the risk premium for Spanish commercial properties of a good 100 basis points is significantly lower than the yield divergence between German and Spanish sovereign bonds, which is currently about 250 basis points.

RETAIL: RENTAL YIELD FOR TOP LOCATIONS IN PER CENT OFFICE: RENTAL YIELD FOR TOP LOCATIONS IN PER CENT

Source: Feri Source: Feri

0

5

10

15

20

25

30

35

40

45

2009 2010 2011 2012

inve

stm

ent v

olum

e in

EU

R b

n

Germany

France

Italy

Spain

UK

0

10

20

30

40

50

60

2009 2010 2011 2012

shar

e in

%

Germany

France

Italy

Spain

UK

4,0

4,5

5,0

5,5

6,0

6,5

7,0

7,5

02 03 04 05 06 07 08 09 10 11 12 13e

GermanyFranceItalySpainUKaverage

4,0

4,5

5,0

5,5

6,0

6,5

7,0

7,5

02 03 04 05 06 07 08 09 10 11 12 13e

GermanyFranceItalySpainUKaverage

Retail and office: rental yield lowest for German properties

Real Estate Market Germany 2013 | 2014

9

Comparison of European retail, office and residential rents

RETAIL: PRIME RENTS AS INDEX (2002 = 100) AND … … COMPARED TO PREVIOUS YEAR IN PER CENT

Source: Feri, own calculations Source: Feri, own calculations

OFFICE: PRIME RENTS AS INDEX (2002 = 100) AND … … COMPARED TO PREVIOUS YEAR IN PER CENT

Source: Feri, own calculations Source: Feri, own calculations

RESIDENTIAL: PRIME RENTS AS INDEX (2002 = 100) AND … … COMPARED TO PREVIOUS YEAR IN PER CENT

Source: Feri, own calculations Source: Feri, own calculations

80

90

100

110

120

130

140

150

160

170

2002 2004 2006 2008 2010 2012

prim

e re

nt 2

002

= 10

0

DE Top-7

Amsterdam

Brussels

Dublin

London

Madrid

Paris

Rome

Vienna

-15

-10

-5

0

5

10

15

2008 2009 2010 2011 2012pr

ime

rent

YO

Y in

%

DE Top-7

Amsterdam

Brussels

Dublin

London

Madrid

Paris

Rome

Vienna

60

70

80

90

100

110

120

130

2002 2004 2006 2008 2010 2012

prim

e re

nt 2

002

= 10

0

DE Top-7

Amsterdam

Brussels

Dublin

London

Madrid

Paris

Rome

Vienna

-25

-20

-15

-10

-5

0

5

10

15

2008 2009 2010 2011 2012

prim

e re

nt Y

OY

in %

DE Top-7

Amsterdam

Brussels

Dublin

London

Madrid

Paris

Rome

Vienna

70

80

90

100

110

120

130

140

2002 2004 2006 2008 2010 2012

prim

e re

nt 2

002

= 10

0

DE Top-7

Amsterdam

Brussels

Dublin

London

Madrid

Paris

Rome

Vienna

-15

-10

-5

0

5

10

2008 2009 2010 2011 2012

prim

e re

nt Y

OY

in %

DE Top-7

Amsterdam

Brussels

Dublin

London

Madrid

Paris

Rome

Vienna

Real Estate Market Germany 2013 | 2014

10

RETAIL PROPERTIES

Conditions for the German retail sector are in fact good. Although macroeconomic growth is currently relatively low, this is having little impact on private households. In fact the opposite is the case: the economic slowdown is having virtually no impact on the robust labour market, and - in contrast to large parts of the eurozone - consum-ers are benefiting from distinctly low unemployment and growing wages. Against this background, there is a positive trend in the consumer climate despite the rampant euro debt crisis.

LABOUR MARKET CREATES GOOD CONDITIONS FOR RETAIL CONSUMER CONFIDENCE AT A RELATIVELY HIGH LEVEL

Source: Feri Source: GfK

However, these generally favourable conditions for consumption are having virtually no impact on the German retail sector. Almost all of the growth in retail sales currently evident is being offset by price increases. Growth is reported only in e-commerce, and high-street retail sales are therefore falling in real terms.

GROWTH IN THE RETAIL SECTOR ONLY IN E-COMMERCE … … AND RETAIL SPACE

Source: HDE excl. vehicles, fuel, pharmacies Source: HDE, own calculations, sales adjusted for e-commerce

0,0

1,0

2,0

3,0

4,0

5,0

6,0

7,0

6,0

7,0

8,0

9,0

10,0

11,0

12,0

13,0

14,0

1998 2001 2004 2007 2010 2013

hourly wages YOY in % (rhs)unemployment rate in % (lhs)

-4

0

4

8

12

16

20

2001 2003 2005 2007 2009 2011 2013

GfK consumer climate Germany

0

10

20

30

40

50

0

100

200

300

400

500

00 01 02 03 04 05 06 07 08 09 10 11 12 13e

e-co

mm

erce

sal

es in

EU

R b

n

reta

il sa

les

in E

UR

bn

retail sales (lhs)e-commerce sales (rhs)

3.000

3.200

3.400

3.600

3.800

4.000

105

110

115

120

125

130

00 01 02 03 04 05 06 07 08 09 10 11 12

reta

il sa

les

per s

qm in

EU

R

in m

illio

n sq

m

retail space (lhs)retail sales per sqm (rhs)

Despite economic slowdown, conditions for German retail sector are good …

… but little benefit for retail sales

Real Estate Market Germany 2013 | 2014

11

The downward trend in shop sales is in contrast with the almost continuous growth in retail space. Average sales in EUR per sqm of retail space - sales productivity - has consequently fallen nominally by about 13 per cent since 2000. Adjusted for in-flation, the decline in sales per sqm of retail space is almost 30 per cent. This trend shows that conditions for retail property are fairly weak based on the German retail sector as a whole due to the contracting scope for rent payments.

However, this trend does not relate to the whole retail sector. There is a completely different picture in the 1A sites of top locations. Since the end of the 1990s, prime rents in city centre shopping malls and attractive shopping centres in the seven cities have increased sharply. Nor is there any sign of this trend ending. Demand for at-tractive retail space - particularly from national and international store chains - exceeds the limited supply of available space here. Existing tenants will often only give up their retail space in return for corresponding "key money" payments. New space is often fully pre-let well before the new retail properties have been completed - even in large city centre shopping centres, such as the new "Skyline Plaza" centre which opened in Frankfurt at the end of August.

In contrast, the trend in rents in 1A locations in other large German cities is weaker. Here, rents are currently only slightly higher than those paid at the beginning of the 1990s. In contrast, rents in top locations have increased by around 50 per cent in the same period. However, secondary locations in city centres are not benefiting from the growth in prime rents. Here the rent level is stable in both top locations and also in regional centres. Store chains are showing virtually no inclination to move to sec-ondary locations - in response to high rents for 1A retail space or a lack of supply.

PRIME RENTS INCREASING MAINLY IN TOP LOCATIONS VIRTUALLY NO BENEFIT FOR SECONDARY LOCATIONS

Source: BulwienGesa, own calculations, DZ BANK Research forecast Source: BulwienGesa, own calculations, DZ BANK Research forecast

The positive trend in 1A city centre locations is based on various factors which have enhanced the potential of this retail space in recent years. These include a change in the way in which many customers shop, for example, on the one hand ordering goods via e-commerce, but on the other hand still wanting to go on a shopping trip since this enables them to "experience" products directly and obviously offers a posi-tive leisure experience. City centres are meeting this demand by providing attractive pedestrian zones and chic city-centre shopping centres with a broad range of chain

80

100

120

140

160

180

200

220

240

260

280

92 94 96 98 00 02 04 06 08 10 12 14e

prim

e re

nt in

EU

R p

er s

qm

Top-7 Regional-12

5

10

15

20

25

30

35

92 94 96 98 00 02 04 06 08 10 12 14e

rent

sec

onda

ry lo

catio

nin

EU

R p

er s

qm

Top-7 Regional-12

Expansion of retail space on the back of falling retail sales leads to a decline in sales productivity

1A sites in prime locations remain positive

Retail rents in top locations increasing faster than in regional centres

1A sites in prime locations benefit from shopping behaviour

Real Estate Market Germany 2013 | 2014

12

stores, mono-label and flagship stores. Leisure activities are enhanced, for example, by restaurants, fitness and wellness facilities and cinemas. Chain stores and manu-facturers are responding to the "hybrid" shopping behaviour with a multi-channel strategy consisting of a parallel focus on online sales and actually visiting 1A loca-tions ("clicks and bricks"). This applies particularly to the top locations which are pre-ferred by chain stores and branded goods suppliers because of their potential. This ensures a broader than average range of products, which in turn attracts customers.

Customer potential in the top locations has also increased steadily in recent years due to the growing number of residents (see page 36). An increase in the number of visits by affluent foreign tourists and business travellers is also generating further demand. Not without reason has the abovementioned Skyline Plaza been built in direct proximity to the Frankfurt Trade Fair.

The abovementioned developments seem to be having a similar impact in the seven top locations - as suggested at least by the trend in rents. The range of the increase in prime rents is therefore relatively small. The much weaker growth in Stuttgart is likely to be connected with the disproportionately negative impact of the economic crisis of 2008 and 2009 on the city where there is a heavy emphasis on industry. With the exception of Munich, the rent level also fluctuates only slightly around the average prime rent of currently approx. EUR 250 per sqm. The capital of Bavaria provides evidence of the excellent prospects for the retail sector with prime rents now in excess of EUR 300 per sqm.

MUNICH STILL THE CLEAR LEADER IN RETAIL TERMS RELATIVELY SMALL DIFFERENCES IN RENT TRENDS SINCE 2007

Source: BulwienGesa, own calculations, DZ BANK Research forecast Source: BulwienGesa, own calculations

Total retail space in the seven top locations varies between 1m sqm in Stuttgart and about 6m sqm in Berlin. Although total retail space is heavily dependent on the population of the city, there are nevertheless major differences on a per capita basis. The range extends from just under 1.4 sqm in Cologne to just over two sqm in Dusseldorf and Frankfurt. As we have already described above, per capita retail space has also increased significantly in the top locations in recent years. The differences in per capita retail space have increased considerably since 2002. However, this does not apply to Cologne - where relative retail space has remained virtually unchanged.

120140160180200220240260280300320340

92 94 96 98 00 02 04 06 08 10 12 14e

EU

R p

er s

qm

B

D

F

HH

K

M

S

Top-77,1

14,615,8

17,1 17,2 17,319,5

23,3

S K D B Top-7 M HH F

prime rent growth 2007-2012 in %

Purchasing power increases due to population growth and visitors

Trend in retail rents very similar in individual top locations

Per capita retail space in top locations has increased visibly in the last ten years

K = Cologne

Real Estate Market Germany 2013 | 2014

13

RETAIL: TOTAL RETAIL SPACE … … AND PER CAPITA IN SQM

Source: Feri, Comfort K = Cologne Source: Feri, own calculations K = Cologne

The range of the proportions of retail space close to city centres is even wider than for relative retail space and varies from about ten to 40 per cent. A high proportion indicates that city centre retail has a relatively high level of attractiveness in the respective location. However, this also reflects the extent to which large shopping centres have been constructed perhiperal to the city centre area.

Apart from Cologne, where retail space has not even grown by ten per cent, retail space has increased by 30 to just over 40 per cent in the last ten years depending on the top location. As a result of this strong growth in retail space, Cologne is the only city where retail sales have grown more strongly than retail space. While the divergence in Hamburg and Munich is still relatively small, sales growth in Dussel-dorf is lagging well behind the level of growth in retail space. However, the figures relate to the retail sector as a whole, and only limited conclusions can therefore be drawn concerning the situation in city areas. This also applies to the sales productivi-ty figures shown below on the right, which are comparatively low in Dusseldorf and Stuttgart. Nevertheless, it indicates a connection with prime rents which are lowest in Dusseldorf and Stuttgart. This does not however apply to Berlin. Here sales produc-tivity is still much lower, while prime rents are higher than in Dusseldorf and Stuttgart. Given the particularly small proportion of retail activity close to the city cen-tre in Berlin, it is nevertheless likely that the situation in the central area, and particu-larly in 1A locations, is in no way fully reflected in the average sales productivity figures for the location as a whole.

0

5

10

15

20

25

30

35

40

0

1

2

3

4

5

6

7

8

B HH M F K D S Top-7sh

are

in %

reta

il sp

ace

in s

qm m

retail space in sqm m (lhs) share of city center (rhs)

1,0

1,2

1,4

1,6

1,8

2,0

2,2

K M S HH B D F Top-7

reta

il sp

ace

per c

apita

in s

qm

2012 2002

Proportion of retail space close to city centres now between 10 and 40 per cent

Retail space has grown by up to 40 per cent in ten years

Real Estate Market Germany 2013 | 2014

14

GROWTH IN RETAIL RETAIL SPACE IN TOP LOCATIONS DECLINE IN SALES PRODUCTIVITY HAS EASED

Source: Feri, own calculations K = Cologne Source: Feri, own calculations *) in prices from 2000 K = Cologne

As expected, the figures for purchasing power and centrality for the top locations show above-average levels. Only in Berlin is purchasing power below the average level for Germany. This reflects the still low economic power of the German capital. In contrast, purchasing power in Munich is well above average, underlining the city's above-average attractions as a retail location. In terms of centrality, Dusseldorf, Co-logne and Stuttgart show particularly high levels.

MUNICH HAS BY FAR THE HIGHEST PURCHASING POWER , … STUTTGART TOP OF THE LEAGUE IN TERMS OF CENTRALITY

Source: Comfort, own calculations K = Cologne Source: Comfort, own calculations K = Cologne

05

101520253035404550

K S M HH B F D Top-7

grow

th fr

om 2

002

to 2

012

in %

growth of retail space growth of retail sales

2.000

2.500

3.000

3.500

4.000

4.500

5.000

5.500

6.000

6.500

92 94 96 98 00 02 04 06 08 10 12

EU

R p

er s

qm *)

B DF HHK MS Top-7

90

95

100

105

110

115

120

125

130

B HH K S F D M Top-7

purc

hasi

ng p

ower

inde

x

German average

90

95

100

105

110

115

120

125

130

B F HH M D K S Top-7

cent

ralit

y in

dex German average

Retail figures for top locations mainly positive

Real Estate Market Germany 2013 | 2014

15

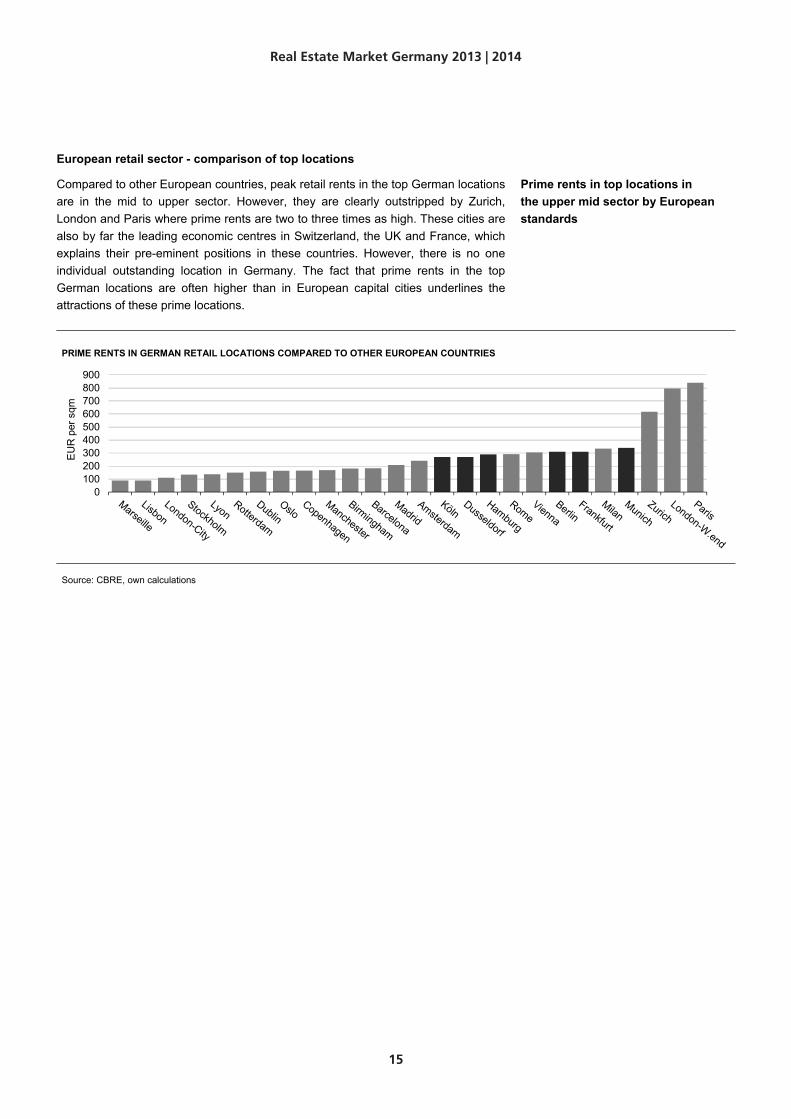

European retail sector - comparison of top locations

Compared to other European countries, peak retail rents in the top German locations are in the mid to upper sector. However, they are clearly outstripped by Zurich, London and Paris where prime rents are two to three times as high. These cities are also by far the leading economic centres in Switzerland, the UK and France, which explains their pre-eminent positions in these countries. However, there is no one individual outstanding location in Germany. The fact that prime rents in the top German locations are often higher than in European capital cities underlines the attractions of these prime locations.

PRIME RENTS IN GERMAN RETAIL LOCATIONS COMPARED TO OTHER EUROPEAN COUNTRIES

Source: CBRE, own calculations

0100200300400500600700800900

EU

R p

er s

qm

Prime rents in top locations in the upper mid sector by European standards

Real Estate Market Germany 2013 | 2014

16

Berlin: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

With retail space of 6m sqm, Berlin is the leader in Germany; however, based on a population of 3.5m people, retail sales are low. Per sqm, the city achieves only 70 per cent of the average figure for top locations, probably attributable mainly to low incomes and high unemployment. However, this weakness of the location does not have a negative impact on top retail locations, which are performing very well. De-mand far exceeds the supply of retail space, thus ensuring steady growth in prime rents, which are likely to top the level of EUR 250 per sqm this year. Retail activity in Berlin benefits more strongly than other top locations from its function as a test market for Germany. In addition to the size of the market, the location also benefits from a positive economic trend which has been ongoing for some time, and from the high and growing number of tourists, whose purchases account for a good quarter of retail sales in Berlin. The micro locations around Hackescher Markt and Alexanderplatz are also showing dynamic growth. The upgrading of Ku'damm, for example with Haus Cumberland, is also positive. Demand for retail space in top locations is likely to continue, and prime rents will therefore increase further. RETAIL PROPERTIES IN BERLIN

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,191 1,200 1,211 1,227

Per capita disp. income in % y-o-y 0.6 0.7 0.9 1.3

Unemployment rate (BA) in % 13.3 12.3 12.6 12.3

Retail sales in % y-o-y 1.2 1.9 2.1 2.6

Supply

Retail space in m sqm 5.9 6.0 6.1 6.3

Retail space in % y-o-y 0.4 1.6 2.8 2.4

Retail rents

Prime / secondary locations in EUR/sqm 225 / 14.0 240 / 14.0 252 / 14.0 260 / 14.0

Prime / secondary locations in % y-o-y 4.7 / 0.0 6.7 / 0.0 5.0 / 0.0 3.2 / 0.0

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast 12 regional centres: Augsburg, Bre-men, Darmstadt, Dresden, Essen, Hannover, Karlsruhe, Leipzig, Mainz, Mannheim, Münster, Nuremberg

50

100

150

200

250

300

350

2004 2006 2008 2010 2012 2014e

Berlin Top-7 Regional-121,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Berlin Top-7 Regional-12

Largest German retail location with relatively low purchasing power

Tourists an important demand group in Berlin

Real Estate Market Germany 2013 | 2014

17

Cologne: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

The fourth largest German city is one of the most popular shopping destinations. Co-logne has two of the top 5 most frequented shopping streets in Germany with Schildergasse and Hohe Straße. In contrast to Dusseldorf, some 40 kilometres away, where the emphasis is on luxury brands, the city centre of Cologne is geared much more to "mainstream" consumption. There are shops with expensive products, but these are not grouped in one area. Interest is therefore focused mainly on the retail space of national and international chains and mono-label stores. It is striking that the growth of around seven per cent in retail space in the last ten years has been much slower than the average rate of increase of 30 per cent reported for top locations. Amongst the top locations, Cologne therefore has the lowest per capita retail space of less than 1.4 sqm. The proportion of retail space in the city centre is also below-average at 19 per cent. Since, apart from the revitalisation of the Neumarkt-Galerie, no major projects are planned, there is no sign of any visible expansion of the retail space on offer close to the city centre. Consequently, demand from potential tenants can still not be met. This year and next year we expect prime rents to increase by just under two per cent respectively.

RETAIL PROPERTIES IN COLOGNE

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,529 1,552 1,566 1,584

Per capita disp. income in % y-o-y 1.3 1.5 0.9 1.1

Unemployment rate (BA) in % 9.6 9.5 9.8 9.5

Retail sales in % y-o-y 1.7 2.8 2.2 2.5

Supply

Retail space in m sqm 1.4 1.4 1.4 1.4

Retail space in % y-o-y 0.0 0.1 0.3 0.4

Retail rents

Prime / secondary locations in EUR/sqm 225 / 12.0 235 / 12.0 240 / 12.0 245 / 12.0

Prime / secondary locations in % y-o-y 2.3 / 0.0 4.4 / 0.0 2.1 / 0.0 2.1 / 0.0

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast

50

100

150

200

250

300

350

2004 2006 2008 2010 2012 2014e

Cologne Top-7 Regional-121,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Cologne Top-7 Regional-12

Top location with the lowest volume of per capita retail space

Supply shortage leads to increase in prime rents

Real Estate Market Germany 2013 | 2014

18

Dusseldorf: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

Dusseldorf, with its high purchasing power, is heavily in demand as a retail location. The "Kö" with its many luxury shops is one of the particularly attractive locations. High demand for retail space has long exceeded supply. Consequently, although prime rents are rising steadily, the level is slightly below average for the seven top locations. In 2012, growth of just over one per cent in rents was also low - on aver-age, rents in top locations have increased at three times this rate. However, this is likely to be attributable less to slackening demand than to the extensive construction activity in the centre of Dusseldorf. This includes the U-Bahn connection for the shopping district of Schadowstraße and the demolition of the "Tausendfüßler" viaduct completed in April 2013. In the medium term this will further increase the attractions of Dusseldorf as a retail location. Overall, we expect visible growth in prime rents both this year and next year. Following a fire at the "Kö-Bogen" property in Dusseldorf at the end of September, completion of the project's first construction phase – originally planned for October 2013 – is likely to be postponed. Given that the retail floor space of 19,000 square metres has already been fully let (with Breuninger, an upmarket German retailer, accounting for three-quarters of it), any such postponement will not make any difference to the supply situation of available space. RETAIL PROPERTIES IN DUSSELDORF

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,710 1,740 1,767 1,792

Per capita disp. income in % y-o-y 1.6 1.7 1.5 1.4

Unemployment rate (BA) in % 9.0 8.9 9.2 8.9

Retail sales in % y-o-y 2.2 3.1 3.4 3.1

Supply

Retail space in m sqm 1.2 1.2 1.2 1.3

Retail space in % y-o-y 7.4 1.8 2.5 1.3

Retail rents

Prime / secondary locations in EUR/sqm 217 / 13.5 220 / 13.5 230 / 13.5 240 / 13.5

Prime / secondary locations in % y-o-y 4.3 / 0.0 1.4 / 0.0 4.5 / 0.0 4.3 / 0.0

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast

Attractive shopping location with consistently high demand for retail space

1,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Dusseldorf Top-7 Regional-12

50

100

150

200

250

300

350

2004 2006 2008 2010 2012 2014e

Dusseldorf Top-7 Regional-12

Real Estate Market Germany 2013 | 2014

19

Frankfurt: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

The retail sector in Frankfurt is also characterised by a high demand overhang. This is evident from the fact that the "Skyline Plaza" was almost totally pre-let many months before it opened. The new shopping centre near the Trade Fair, which has 170 shops and around 38,000 sqm of retail space, opened its doors at the end of August. This further, significant expansion of retail space is likely to result in a slight weakening of the recent sharp increase in the growth in prime rents. The construc-tion work on the Zeil shopping street and on Goethestraße are also likely to have a dampening effect. The planned opening in October 2013 of "One GoethePlaza" is intended to slightly extend the Frankfurt luxury retail area, although the growth in re-tail space will be modest at 4,500 sqm. However, per capita retail space in Frankfurt is already well above-average at 2.2 sqm. The average for top locations is around 1.7 sqm. This also has to be seen relative to the high level of purchasing power - of the residents of Frankfurt themselves, many business travellers and tourists as well as customers from the surrounding area with its good transport links, for example in the Main-Taunus and Hochtaunus regions. Overall, we expect prime rents to grow by about two per cent respectively in 2013 and 2014, partly because if demand is sustained, virtually no new retail space will be created.

RETAILL PROPERTIES IN FRANKFURT

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,397 1,417 1,439 1,464

Per capita disp. income in % y-o-y 1.4 1.4 1.6 1.7

Unemployment rate (BA) in % 7.5 7.4 7.6 7.4

Retail sales in % y-o-y 2.3 3.1 1.6 2.2

Supply

Retail space in m sqm 1.4 1.4 1.5 1.5

Retail space in % y-o-y 0.4 1.2 3.0 1.5

Retail rents

Prime / secondary locations in EUR/sqm 255 / 18.0 265 / 18.0 270 / 18.0 275 / 18.1

Prime / secondary locations in % y-o-y 4.1 / 0.0 3.9 / 0.0 1.9 / 0.0 1.9 / 0.3

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast

50

100

150

200

250

300

350

2004 2006 2008 2010 2012 2014e

Frankfurt Top-7 Regional-121,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Frankfurt Top-7 Regional-12

The "Skyline Plaza" was fully pre-let before it opened

Prime rents likely to increase by around 2 per cent respectively in 2013 and 2014

Real Estate Market Germany 2013 | 2014

20

Hamburg: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

The second largest German city with a population of 1.8m is the pre-eminent shop-ping destination in North Germany. In terms of its catchment area, the customer potential is almost doubling. Demographic growth, an affluent population, and not least the large number of tourists and business travellers, support the purchasing power of the Hamburg retail sector. The broad supply structure is favourable, extending from classic consumer locations such as Spitalerstraße to the distinctly luxury locations such as Neuer Wall. The small proportion of retail space in the city centre - less than 20 per cent - is not optimal. Also, in recent years, virtually no new retail space has been created in top locations. The "Europa Passage" was also opened in 2006. Against this background, there is a broad view that a city centre concept should lead to significant growth in retail space to ensure that retail activity keeps pace with other major European cities. The need to expand retail space is ultimately evident from the high demand from chain stores for retail space for mono/multi-label and also flagship stores. Buoyant demand and a supply shortage will ensure that prime rents increase both this year and next year. Levels are roughly average for top locations. The positive general figures therefore tend to support above-average growth in future.

RETAIL PROPERTIES IN HAMBURG

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,837 1,863 1,897 1,930

Per capita disp. income in % y-o-y 1.2 1.4 1.8 1.7

Unemployment rate (BA) in % 7.8 7.5 7.7 7.5

Retail sales in % y-o-y 1.4 2.0 2.3 2.9

Supply

Retail space in m sqm 2.9 2.9 3.0 3.0

Retail space in % y-o-y 2.1 1.4 1.9 1.7

Retail rents

Prime / secondary locations in EUR/sqm 235 / 40.0 245 / 40.0 255 / 40.0 260 / 40.0

Prime / secondary locations in % y-o-y 4.4 / 0.0 4.3 / 0.0 4.1 / 0.0 2.0 / 0.0

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast

50

100

150

200

250

300

2004 2006 2008 2010 2012 2014e

Hamburg Top-7 Regional-121,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Hamburg Top-7 Regional-12

Hamburg the pre-eminent shopping destination in North Germany

Prime rents likely to increase again this year and next year

Real Estate Market Germany 2013 | 2014

21

Munich: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

Munich occupies a leading role amongst the retail locations. A prime rent of EUR 300 per sqm was exceeded here for the first time last year. The preconditions for fur-ther positive market growth are also good. The favourable conditions are benefiting from low unemployment, high incomes and strong purchasing power in the sur-rounding area. The purchasing power figure of 130 is the highest amongst the top locations. Strong population growth is also a positive factor. Further demand is being generated by the large number of tourists and business travellers. Munich is particu-larly attractive in the retail and luxury segments in Germany because of its size and significance as a retail destination. It also stands apart positively from other locations which offer the almost ubiquitous selection of chains and brand shops by virtue of its range of attractive local stores. The number of shopping centres is also relatively small even after the opening of the Pasing Arcaden in 2011. Recent new retail space, for example in Hofstatt or Palais am Dom, was pre-let long before it opened. At the moment no major projects are being planned, and market conditions are therefore unlikely to ease. We therefore expect the upward trend in prime rents to continue in 2013 and 2014, as in recent years, increasing by around three per cent annually. RETAIL PROPERTIES IN MUNICH

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,779 1,803 1,825 1,850

Per capita disp. income in % y-o-y 1.3 1.3 1.2 1.4

Unemployment rate (BA) in % 5.1 5.0 5.2 5.0

Retail sales in % y-o-y 2.5 2.6 1.5 2.4

Supply

Retail space in m sqm 1.9 2.0 2.0 2.1

Retail space in % y-o-y 1.4 3.4 2.2 2.2

Retail rents

Prime / secondary locations in EUR/sqm 295 / 35.0 305 / 35.0 315 / 35.0 325 / 35.0

Prime / secondary locations in % y-o-y 3.5 / 0.0 3.4 / 0.0 3.3 / 0.0 3.2 / 0.0

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast

50

100

150

200

250

300

350

2004 2006 2008 2010 2012 2014e

Munich Top-7 Regional-121,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Munich Top-7 Regional-12

Prime rent breaks through 2012 level of EUR 300 per sqm

Prime rents in Munich likely to continue to rise despite high level

Real Estate Market Germany 2013 | 2014

22

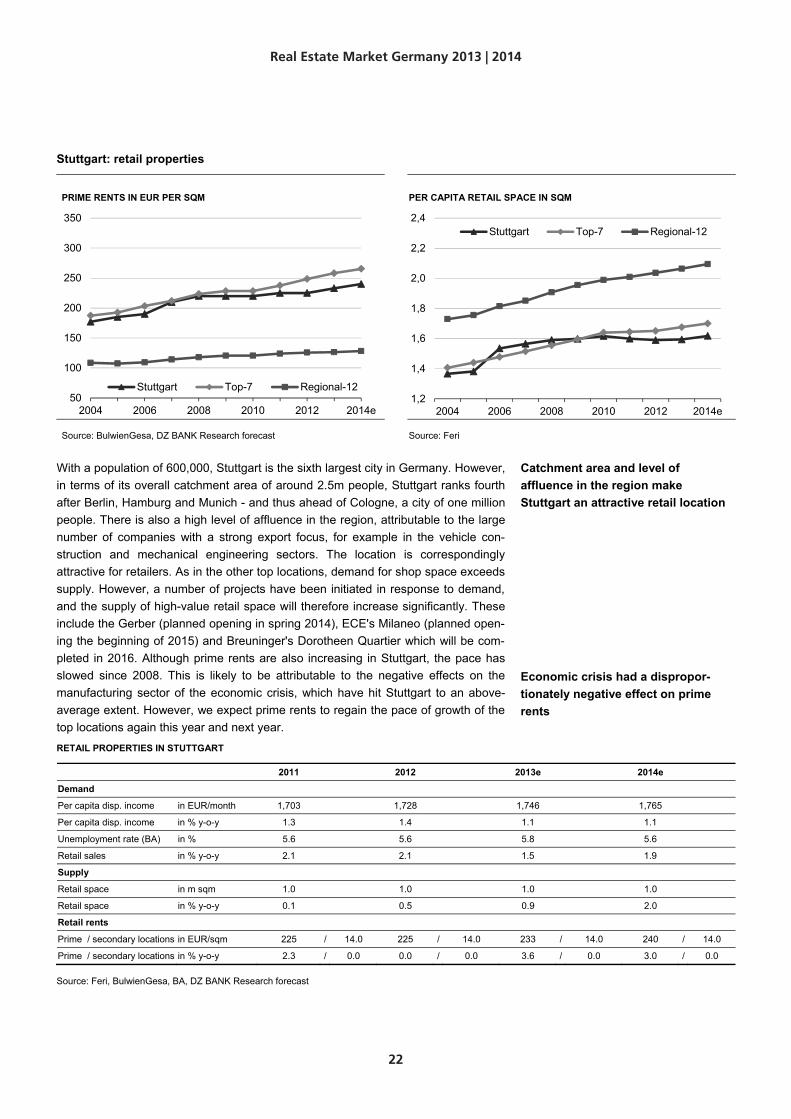

Stuttgart: retail properties

PRIME RENTS IN EUR PER SQM PER CAPITA RETAIL SPACE IN SQM

Source: BulwienGesa, DZ BANK Research forecast Source: Feri

With a population of 600,000, Stuttgart is the sixth largest city in Germany. However, in terms of its overall catchment area of around 2.5m people, Stuttgart ranks fourth after Berlin, Hamburg and Munich - and thus ahead of Cologne, a city of one million people. There is also a high level of affluence in the region, attributable to the large number of companies with a strong export focus, for example in the vehicle con-struction and mechanical engineering sectors. The location is correspondingly attractive for retailers. As in the other top locations, demand for shop space exceeds supply. However, a number of projects have been initiated in response to demand, and the supply of high-value retail space will therefore increase significantly. These include the Gerber (planned opening in spring 2014), ECE's Milaneo (planned open-ing the beginning of 2015) and Breuninger's Dorotheen Quartier which will be com-pleted in 2016. Although prime rents are also increasing in Stuttgart, the pace has slowed since 2008. This is likely to be attributable to the negative effects on the manufacturing sector of the economic crisis, which have hit Stuttgart to an above-average extent. However, we expect prime rents to regain the pace of growth of the top locations again this year and next year.

RETAIL PROPERTIES IN STUTTGART

2011 2012 2013e 2014e

Demand

Per capita disp. income in EUR/month 1,703 1,728 1,746 1,765

Per capita disp. income in % y-o-y 1.3 1.4 1.1 1.1

Unemployment rate (BA) in % 5.6 5.6 5.8 5.6

Retail sales in % y-o-y 2.1 2.1 1.5 1.9

Supply

Retail space in m sqm 1.0 1.0 1.0 1.0

Retail space in % y-o-y 0.1 0.5 0.9 2.0

Retail rents

Prime / secondary locations in EUR/sqm 225 / 14.0 225 / 14.0 233 / 14.0 240 / 14.0

Prime / secondary locations in % y-o-y 2.3 / 0.0 0.0 / 0.0 3.6 / 0.0 3.0 / 0.0

Source: Feri, BulwienGesa, BA, DZ BANK Research forecast

50

100

150

200

250

300

350

2004 2006 2008 2010 2012 2014e

Stuttgart Top-7 Regional-121,2

1,4

1,6

1,8

2,0

2,2

2,4

2004 2006 2008 2010 2012 2014e

Stuttgart Top-7 Regional-12

Catchment area and level of affluence in the region make Stuttgart an attractive retail location

Economic crisis had a dispropor-tionately negative effect on prime rents

Real Estate Market Germany 2013 | 2014

23

OFFICE PROPERTIES

Demand for office properties has benefited for some years from the robust state of the labour market. The number of people in work has thus increased to almost 42m, and the number of office workers topped ten million last year. The total number of people employed has therefore increased by around 2.5m within a decade, and the number of office workers has grown by more than 500,000. The marked economic slowdown last year has hampered this trend considerably; however, in contrast to the weak macroeconomic trend in the first half of the last decade, the number of jobs has not fallen and unemployment has not increased.

ECONOMY PICKING UP AGAIN SINCE SECOND QUARTER MORE THAN 10M PEOPLE EMPLOYED IN OFFICES

Source: Feri Source: Feri

The deep recession in the eurozone is over. The negative effects on the German economy are also therefore easing. Economic output thus increased again year-on-year in the second quarter after declining in the first three months of this year. Based on our forecast, the recovery will gain further momentum in future quarters. The risk of the euro debt crisis having a more severe impact on the labour market should therefore have been averted.

While the labour market has proved very robust during the financial market and euro debt crises, the number of planned new office building projects has declined, and growth in office space has flattened. The trend evident for some time in the office markets is thus continuing: since 2006, average growth of less than one per cent per annum in office space in the top locations has been lagging behind the strong growth of double this level in office employment. The situation in the office markets has therefore reversed: previously - from 1993 to 2005 - a high volume of new office space was built, although office employment was largely stagnating. True, large numbers of people were hired as a result of the dot-com boom, however about half of the jobs were then lost again when the share bubble burst and in the aftermath of "9/11". However, new office projects were driven even more strongly by the euphoria surrounding German reunification in the 1990s than by by "Internet hype".

-8,0

-6,0

-4,0

-2,0

0,0

2,0

4,0

6,0

1996 2000 2004 2008 2012

GDP YOY in %8,7

9,0

9,3

9,6

9,9

10,2

95

100

105

110

115

120

1996 2000 2004 2008 2012

empl

oyee

s in

mill

ion

empl

oym

ent 1

996

= 10

0

office workers in million (rhs)total employment index, (lhs)office workers index (lhs)

Robust labour market supports demand for office space

Risk of a stronger negative impact on the German labour market due to euro debt crisis seems to have been averted

Office space has grown more slowly than no. of office jobs since 2006

Real Estate Market Germany 2013 | 2014

24

THANKS TO THE POSITIVE TREND IN THE LABOUR MARKET … … OFFICE EMPLOYMENT IS GROWING FASTER THAN OFFICE SPACE

Source: Feri, own calculations, DZ BANK Research forecast Source: Feri, own calculations, DZ BANK Research forecast

In summary, trends in both the more distant and recent past are resulting in currently buoyant demand on the back of a generally fairly high supply of space. However, demand is focused mainly on modern, attractive and conveniently situated office space, as clearly reflected in the growth in prime rents. Modern office space is now in fairly short supply in most locations. In contrast, the existing supply of office space in the various locations consists mainly of older, outdated properties or is less con-veniently located. This explains the decline in the vacancy rate, although it is still at a relatively high level. One positive factor here is that the proportion of unoccupied of-fice space fell again last year to less than nine per cent for the first time since 2003.

EXPANSION OF SPACE LEADS TO HIGH VACANCY RATE GOOD EMPLOYMENT LEVEL ENSURES GROWTH IN PRIME RENTS

Source: Feri, own calculations, DZ BANK Research forecast Source: BulwienGesa, own calculations, DZ BANK Research forecast

The varying ratios of supply and demand in the different segments of the office mar-ket also reflect the trend in rents. Average rents for non-central locations in 2011 and 2012 together thus increased by three per cent, while prime rents in the office sector grew at twice this rate. As a result of the growth in rents in recent years, prime rents are now once again at least in line with the average levels over the last 20 years. Rents for secondary locations are still about five per cent below the average for this

1,60

1,75

1,90

2,05

2,20

2,35

55

60

65

70

75

80

92 94 96 98 00 02 04 06 08 10 12 14eof

fice

wor

kers

in m

illio

n

offic

e sp

ace

in s

qm m

office space (lhs)office workers (rhs) -3,0

-2,0

-1,0

0,0

1,0

2,0

3,0

4,0

5,0

92 94 96 98 00 02 04 06 08 10 12 14e

YO

Y in

%

office spaceoffice workers

0

2

4

6

8

10

12

30

32

34

36

38

40

42

92 94 96 98 00 02 04 06 08 10 12

vaca

ncy

rate

in %

spac

e pe

r offi

ce w

orke

r in

sqm

space per office worker (lhs)vacancy rate (rhs)

0

2

4

6

8

10

12

30

32

34

36

38

40

42

92 94 96 98 00 02 04 06 08 10 12

vaca

ncy

rate

in %

spac

e pe

r offi

ce w

orke

r in

sqm

space per office worker (lhs)vacancy rate (rhs)

Vacancy rate down, but still high

Prime rents increased sharply in 2011 and 2012

Real Estate Market Germany 2013 | 2014

25

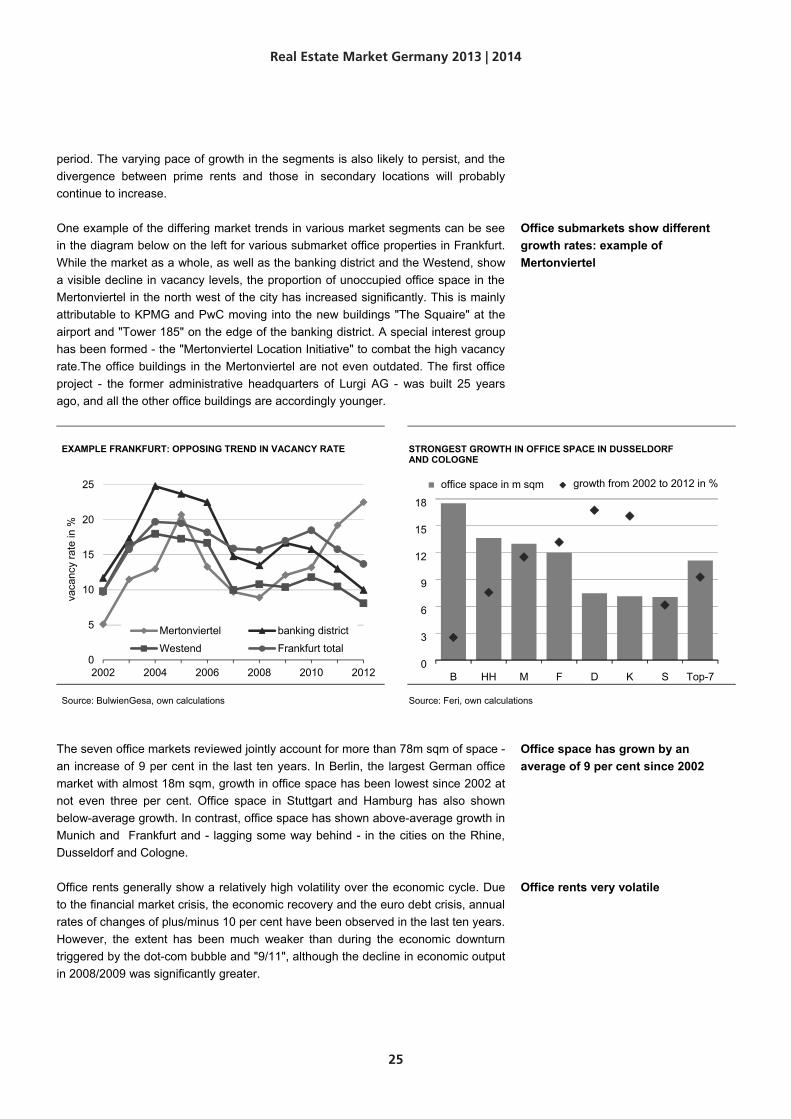

period. The varying pace of growth in the segments is also likely to persist, and the divergence between prime rents and those in secondary locations will probably continue to increase.

One example of the differing market trends in various market segments can be see in the diagram below on the left for various submarket office properties in Frankfurt. While the market as a whole, as well as the banking district and the Westend, show a visible decline in vacancy levels, the proportion of unoccupied office space in the Mertonviertel in the north west of the city has increased significantly. This is mainly attributable to KPMG and PwC moving into the new buildings "The Squaire" at the airport and "Tower 185" on the edge of the banking district. A special interest group has been formed - the "Mertonviertel Location Initiative" to combat the high vacancy rate.The office buildings in the Mertonviertel are not even outdated. The first office project - the former administrative headquarters of Lurgi AG - was built 25 years ago, and all the other office buildings are accordingly younger.

EXAMPLE FRANKFURT: OPPOSING TREND IN VACANCY RATE STRONGEST GROWTH IN OFFICE SPACE IN DUSSELDORF AND COLOGNE

Source: BulwienGesa, own calculations Source: Feri, own calculations

The seven office markets reviewed jointly account for more than 78m sqm of space - an increase of 9 per cent in the last ten years. In Berlin, the largest German office market with almost 18m sqm, growth in office space has been lowest since 2002 at not even three per cent. Office space in Stuttgart and Hamburg has also shown below-average growth. In contrast, office space has shown above-average growth in Munich and Frankfurt and - lagging some way behind - in the cities on the Rhine, Dusseldorf and Cologne.

Office rents generally show a relatively high volatility over the economic cycle. Due to the financial market crisis, the economic recovery and the euro debt crisis, annual rates of changes of plus/minus 10 per cent have been observed in the last ten years. However, the extent has been much weaker than during the economic downturn triggered by the dot-com bubble and "9/11", although the decline in economic output in 2008/2009 was significantly greater.

0

5

10

15

20

25

2002 2004 2006 2008 2010 2012

vaca

ncy

rate

in %

Mertonviertel banking district

Westend Frankfurt total

Office submarkets show different growth rates: example of Mertonviertel

Office space has grown by an average of 9 per cent since 2002

Office rents very volatile

0

3

6

9

12

15

18

B HH M F D K S Top-7

office space in m sqm growth from 2002 to 2012 in %

Real Estate Market Germany 2013 | 2014

26

PRIME RENTS FOR OFFICE SPACE IN EUR PER SQM … … AND IN PER CENT Y-O-Y

Source: BulwienGesa, own calculations, DZ BANK Research forecast K = Cologne

Source: BulwienGesa, own calculations, DZ BANK Research forecast K = Cologne

Stuttgart has the lowest vacancy rate of just under 6 per cent. It is followed by Berlin, Hamburg, Munich and Cologne, whose vacancy rates are about 8 per cent. The figures for Dusseldorf and Frankfurt are well above the average of 8 per cent at respectively 11 per cent and almost 14 per cent. Compared to the low level at the beginning of the 1990s, the vacancy rate in all locations has increased substantially, on average by around 6 percentage points.

VACANCY RATE DECLINING, BUT STILL VERY HIGH IT HAS INCREASED BY 4 TO 8 PERCENTAGE POINTS IN 10 YEARS

Source: Feri, own calculations K = Cologne Source: Feri, own calculations K = Cologne

10

15

20

25

30

35

40

45

50

92 94 96 98 00 02 04 06 08 10 12 14e

EU

R p

er s

qm

BDFHHKMSTop-7

-10-8-6-4-202468

10

04 05 06 07 08 09 10 11 12 13e 14e

YO

Y in

%

B D F HHK M S Top-7

0

2

4

6

8

10

12

14

16

S B HH M K D F Top-7

vaca

ncy

rate

in %

1992 1997 2001 2005 2010 2012

0

1

2

3

4

5

6

7

8

9

S B HH M K D F Top-7

chan

ge fr

om 2

002

to 2

012

in

perc

enta

ge p

oint

s

Stuttgart has the lowest, and Frankfurt the highest vacancy rate

Real Estate Market Germany 2013 | 2014

27

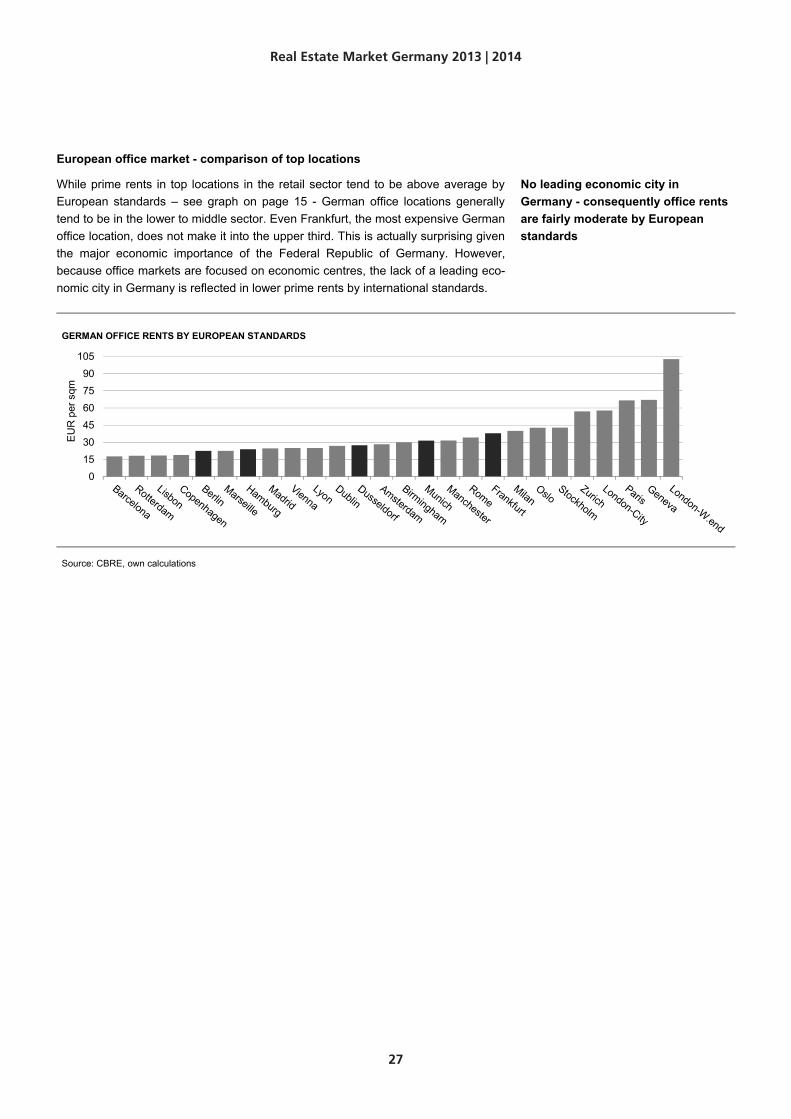

European office market - comparison of top locations

While prime rents in top locations in the retail sector tend to be above average by European standards – see graph on page 15 - German office locations generally tend to be in the lower to middle sector. Even Frankfurt, the most expensive German office location, does not make it into the upper third. This is actually surprising given the major economic importance of the Federal Republic of Germany. However, because office markets are focused on economic centres, the lack of a leading eco-nomic city in Germany is reflected in lower prime rents by international standards.

GERMAN OFFICE RENTS BY EUROPEAN STANDARDS

Source: CBRE, own calculations

0153045607590

105

EU

R p

er s

qm

No leading economic city in Germany - consequently office rents are fairly moderate by European standards

Real Estate Market Germany 2013 | 2014

28

Berlin: office properties

PRIME RENTS IN % Y-O-Y VACANCY RATES IN %

Source: BulwienGesa, DZ BANK Research forecast Source: Feri, DZ BANK Research forecast

The office market is benefiting from the positive economic trend in Berlin. The fun-damental situation is also contributing: for example, the fashion mail order company Zalando has grown successfully. However, established companies are also showing interest in setting up or extending offices in Berlin. Demand is mainly for smaller of-fice space. Large-scale rentals are mainly for public sector administration. The larg-est rental of 25,000 sqm in the first half of 2013 was by Deutsche Rentenversicherung. Overall, space take-up of around 225,000 sqm during this peri-od was down by almost 20 per cent on the same period in the previous year. The main reason for this is the meagre supply of large, modern office space. The second half could however be more successful in terms of revenue as a result of requests for larger scale office space. In 2013 and 2014, the volume of completions increased sharply. Construction projects amounting to a total of 385,000 sqm will probably then be completed, some 70 per cent more than in the two previous years. However, the greater proportion is already let, and virtually no space will therefore come onto the free market. The vacancy rate is likely to fall slightly this year and next year. Prime rents should increase slightly.

OFFICE PROPERTIES IN BERLIN

2011 2012 2013e 2014e

Demand

GDP in % y-o-y 1.1 2.0 1.5 2.3

Per capita GDP in EUR tsd. 23.7 23.9 24.1 24.5

Per capita GDP in % y-o-y 0.2 0.8 0.8 1.9

Office employees in % y-o-y 2.6 2.7 1.4 1.5

Supply

Office space in m sqm 17.5 17.5 17.6 17.7

Office space in % y-o-y 0.5 0.2 0.3 0.5

Vacancy rate in % 8.0 7.5 7.4 7.3

Office rents

Prime / secondary locations in EUR/sqm 21.5 / 6.5 22.0 / 6.7 22.4 / 6.7 22.8 / 6.8

Prime / secondary locations in % y-o-y 4.9 / 0.0 2.3 / 3.1 1.8 / 0.6 1.8 / 0.9

Source: Feri, BulwienGesa, DZ BANK Research forecast

-12

-8

-4

0

4

8

2004 2006 2008 2010 2012 2014e

Berlin Top-7 Regional-125

6

7

8

9

10

11

2004 2006 2008 2010 2012 2014e

Berlin Top-7 Regional-12

Positive economic trend in Berlin

However, prime rents likely to increase only slightly

Real Estate Market Germany 2013 | 2014

29

Cologne: office properties

PRIME RENTS IN % Y-O-Y VACANCY RATES IN %

Source: BulwienGesa, DZ BANK Research forecast Source: Feri, DZ BANK Research forecast

Relative to its population of 1m, the office market in the fourth largest German city is fairly small at just over 7m sqm. However, in terms of space take-up, Cologne lies in only sixth position. The market trend is nevertheless positive, with space take-up of 133,000 sqm in the first half of 2013 up by about 5 per cent on the same period last year. This includes two completions of more than 10,000 sqm for tenants Cologne Trade Fair and the Student Services Center. Given the growth in the number of of-fice workers, demand for space is positive. The vacancy rate has fallen steadily from its 2006 level of not quite 10 per cent and is likely to be below 8 per cent this year. This trend is also connected with the low volume of new office space. In 2012, around 30,000 sqm of completed new build office space was only a quarter of the ten-year average level. This year and next year the total volume will probably reach 100,000 sqm, some 40 per cent of the long-term average. The vacancy rate is also likely to fall slightly next year based on the below-average expansion of office space. Prime rents could increase further slightly this year and next year. OFFICE PROPERTIES IN COLOGNE

2011 2012 2013e 2014e

Demand

GDP in % y-o-y 1.8 1.9 0.7 2.2

Per capita GDP in EUR tsd. 39.8 40.2 40.2 40.9

Per capita GDP in % y-o-y 0.9 0.8 0.0 1.7

Office employees in % y-o-y 2.7 1.3 1.1 1.7

Supply

Office space in m sqm 7.1 7.1 7.2 7.3

Office space in % y-o-y 0.7 0.7 1.3 0.9

Vacancy rate in % 8.6 8.1 7.7 7.5

Office rents

Prime / secondary locations in EUR/sqm 20.0 / 8.0 20.5 / 8.0 20.7 / 8.1 21.0 / 8.1

Prime / secondary locations in % y-o-y 0.0 / 0.0 2.5 / 0.0 1.0 / 0.6 1.4 / 0.6

Source: Feri, BulwienGesa, DZ BANK Research forecast

-12

-8

-4

0

4

8

2004 2006 2008 2010 2012 2014e

Cologne Top-7 Regional-125

6

7

8

9

10

11

2004 2006 2008 2010 2012 2014e

Cologne Top-7 Regional-12

City of a million people has relatively small office market

Prime rents likely to rise slightly in 2013 and 2014, vacancy rate could fall slightly

Real Estate Market Germany 2013 | 2014

30

Dusseldorf: office properties

PRIME RENTS IN % Y-O-Y VACANCY RATES IN %

Source: BulwienGesa, DZ BANK Research forecast Source: Feri, DZ BANK Research forecast

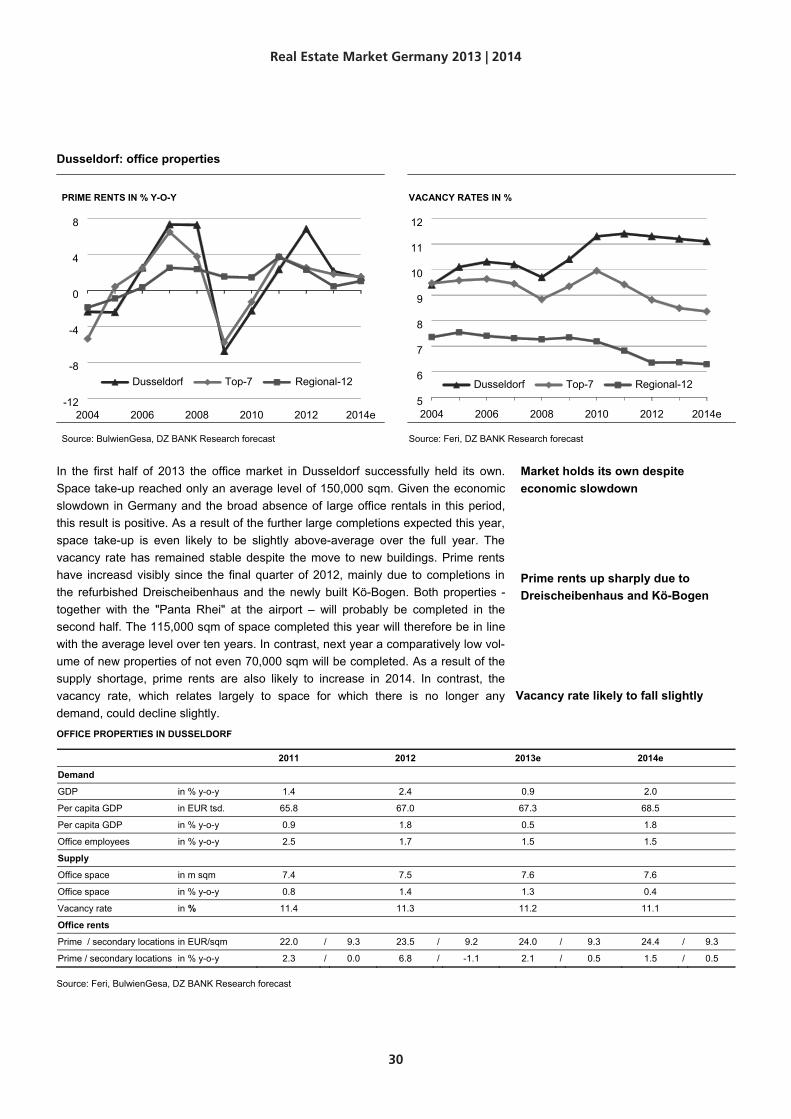

In the first half of 2013 the office market in Dusseldorf successfully held its own. Space take-up reached only an average level of 150,000 sqm. Given the economic slowdown in Germany and the broad absence of large office rentals in this period, this result is positive. As a result of the further large completions expected this year, space take-up is even likely to be slightly above-average over the full year. The vacancy rate has remained stable despite the move to new buildings. Prime rents have increasd visibly since the final quarter of 2012, mainly due to completions in the refurbished Dreischeibenhaus and the newly built Kö-Bogen. Both properties - together with the "Panta Rhei" at the airport – will probably be completed in the second half. The 115,000 sqm of space completed this year will therefore be in line with the average level over ten years. In contrast, next year a comparatively low vol-ume of new properties of not even 70,000 sqm will be completed. As a result of the supply shortage, prime rents are also likely to increase in 2014. In contrast, the vacancy rate, which relates largely to space for which there is no longer any demand, could decline slightly. OFFICE PROPERTIES IN DUSSELDORF

2011 2012 2013e 2014e

Demand

GDP in % y-o-y 1.4 2.4 0.9 2.0

Per capita GDP in EUR tsd. 65.8 67.0 67.3 68.5

Per capita GDP in % y-o-y 0.9 1.8 0.5 1.8

Office employees in % y-o-y 2.5 1.7 1.5 1.5

Supply

Office space in m sqm 7.4 7.5 7.6 7.6

Office space in % y-o-y 0.8 1.4 1.3 0.4

Vacancy rate in % 11.4 11.3 11.2 11.1

Office rents

Prime / secondary locations in EUR/sqm 22.0 / 9.3 23.5 / 9.2 24.0 / 9.3 24.4 / 9.3

Prime / secondary locations in % y-o-y 2.3 / 0.0 6.8 / -1.1 2.1 / 0.5 1.5 / 0.5

Source: Feri, BulwienGesa, DZ BANK Research forecast

Market holds its own despite economic slowdown

Prime rents up sharply due to Dreischeibenhaus and Kö-Bogen

Vacancy rate likely to fall slightly

5

6

7

8

9

10

11

12

2004 2006 2008 2010 2012 2014e

Dusseldorf Top-7 Regional-12

-12

-8

-4

0

4

8

2004 2006 2008 2010 2012 2014e

Dusseldorf Top-7 Regional-12

Real Estate Market Germany 2013 | 2014

31

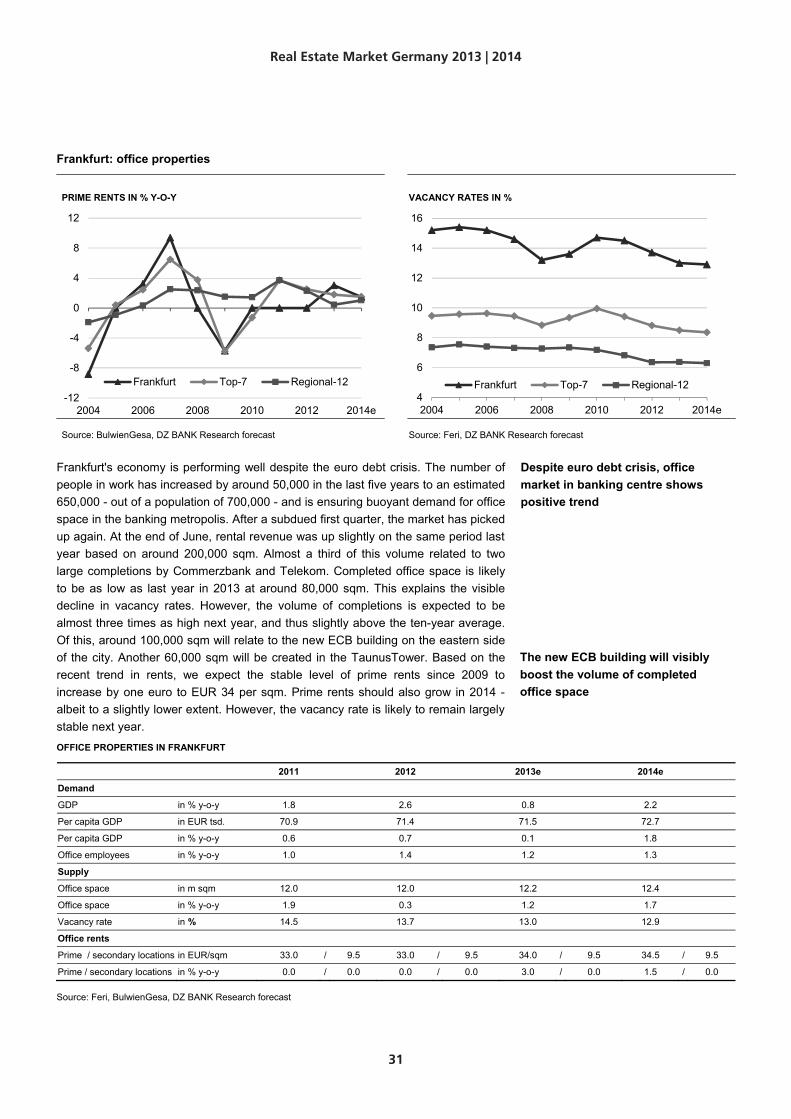

Frankfurt: office properties

PRIME RENTS IN % Y-O-Y VACANCY RATES IN %

Source: BulwienGesa, DZ BANK Research forecast Source: Feri, DZ BANK Research forecast

Frankfurt's economy is performing well despite the euro debt crisis. The number of people in work has increased by around 50,000 in the last five years to an estimated 650,000 - out of a population of 700,000 - and is ensuring buoyant demand for office space in the banking metropolis. After a subdued first quarter, the market has picked up again. At the end of June, rental revenue was up slightly on the same period last year based on around 200,000 sqm. Almost a third of this volume related to two large completions by Commerzbank and Telekom. Completed office space is likely to be as low as last year in 2013 at around 80,000 sqm. This explains the visible decline in vacancy rates. However, the volume of completions is expected to be almost three times as high next year, and thus slightly above the ten-year average. Of this, around 100,000 sqm will relate to the new ECB building on the eastern side of the city. Another 60,000 sqm will be created in the TaunusTower. Based on the recent trend in rents, we expect the stable level of prime rents since 2009 to increase by one euro to EUR 34 per sqm. Prime rents should also grow in 2014 - albeit to a slightly lower extent. However, the vacancy rate is likely to remain largely stable next year.

OFFICE PROPERTIES IN FRANKFURT

2011 2012 2013e 2014e

Demand

GDP in % y-o-y 1.8 2.6 0.8 2.2

Per capita GDP in EUR tsd. 70.9 71.4 71.5 72.7

Per capita GDP in % y-o-y 0.6 0.7 0.1 1.8

Office employees in % y-o-y 1.0 1.4 1.2 1.3

Supply

Office space in m sqm 12.0 12.0 12.2 12.4

Office space in % y-o-y 1.9 0.3 1.2 1.7

Vacancy rate in % 14.5 13.7 13.0 12.9

Office rents

Prime / secondary locations in EUR/sqm 33.0 / 9.5 33.0 / 9.5 34.0 / 9.5 34.5 / 9.5

Prime / secondary locations in % y-o-y 0.0 / 0.0 0.0 / 0.0 3.0 / 0.0 1.5 / 0.0

Source: Feri, BulwienGesa, DZ BANK Research forecast

-12

-8

-4

0

4

8

12

2004 2006 2008 2010 2012 2014e

Frankfurt Top-7 Regional-124

6

8

10

12

14

16

2004 2006 2008 2010 2012 2014e

Frankfurt Top-7 Regional-12

Despite euro debt crisis, office market in banking centre shows positive trend

The new ECB building will visibly boost the volume of completed office space

Real Estate Market Germany 2013 | 2014

32

Hamburg: office properties

PRIME RENTS IN % Y-O-Y VACANCY RATES IN %

Source: BulwienGesa, DZ BANK Research forecast Source: Feri, DZ BANK Research forecast

Transhipment volume in the second largest European sea port declined slightly by 1 per cent last year. However, like the economic slowdown in Germany, this did not have a negative impact on the office market. As a result of the steady increase in the number of office jobs, demand for office space remains positive. Space take-up of almost 220,000 sqm in the first half of this year was thus up slightly on the same period last year. The largest single completion here was 14,000 sqm for Philips. However, most of the demand in Hamburg is focused on medium-sized office space of very good quality and in good locations. In line with the broad-based economy of Hamburg, there is a balanced sector mix for office space. The volume of comple-tions reached about 85 per cent of the ten-year average of around 200,000 sqm in 2012. This year the volume is likely to fall to around 70 per cent of the long-term average. However, the figure will probably increase again to 185,000 sqm in 2014. After a sharp decline in the vacancy rate in the last two years to just under eight per cent, we expect the vacancy level to at best fall slightly this year and next year. Accordingly, prime rents are likely to increase marginally.

OFFICE PROPERTIES IN HAMBURG

2011 2012 2013e 2014e

Demand

GDP in % y-o-y 2.4 1.5 0.9 2.2

Per capita GDP in EUR tsd. 44.8 45.2 45.3 46.1

Per capita GDP in % y-o-y 1.7 0.7 0.4 1.8

Office employees in % y-o-y 1.9 1.8 2.1 1.6

Supply

Office space in m sqm 13.5 13.6 13.8 13.9

Office space in % y-o-y 1.0 1.2 0.9 1.2

Vacancy rate in % 8.5 7.8 7.6 7.5

Office rents

Prime / secondary locations in EUR/sqm 23.5 / 8.2 24.1 / 9.0 24.3 / 9.0 24.5 / 9.0

Prime / secondary locations in % y-o-y 4.4 / 2.5 2.6 / 9.8 0.8 / 0.0 0.8 / 0.0

Source: Feri, BulwienGesa, DZ BANK Research forecast

-8

-4

0

4

8

2004 2006 2008 2010 2012 2014e

HamburgTop-7Regional-12

5

6

7

8

9

10

11

2004 2006 2008 2010 2012 2014e

Hamburg Top-7 Regional-12

Broad-based economy of Hamburg ensures stable trend in office market

Real Estate Market Germany 2013 | 2014

33

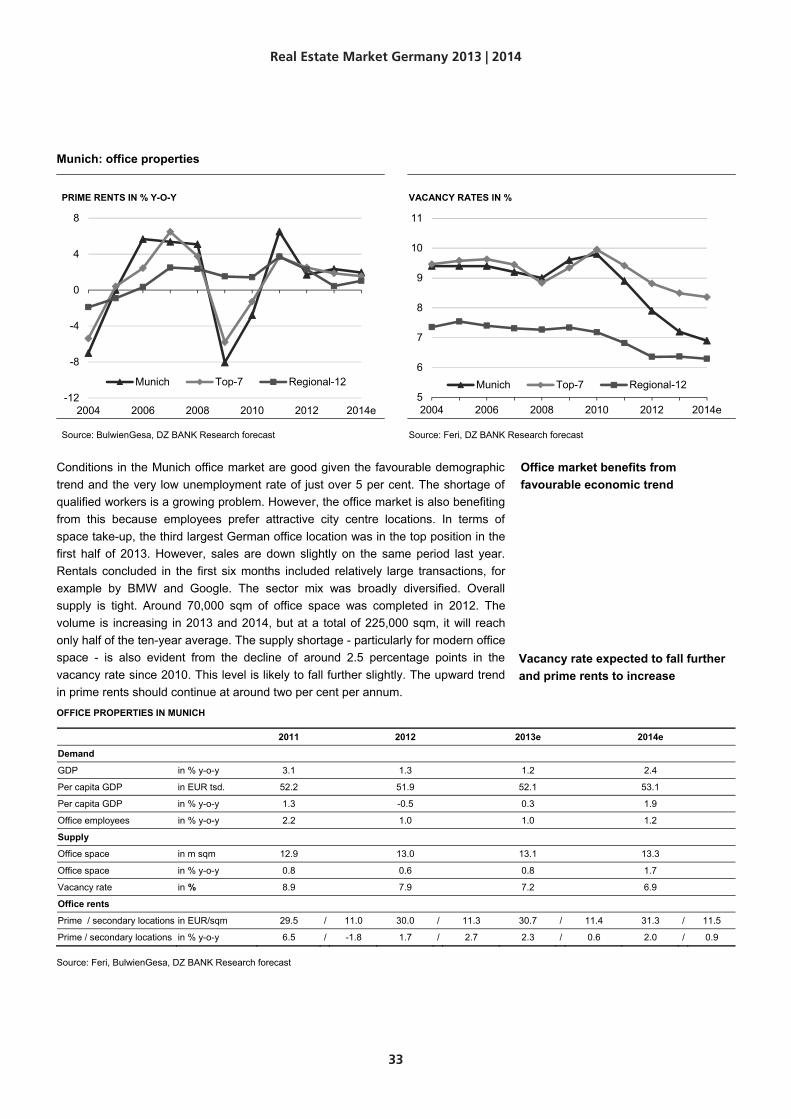

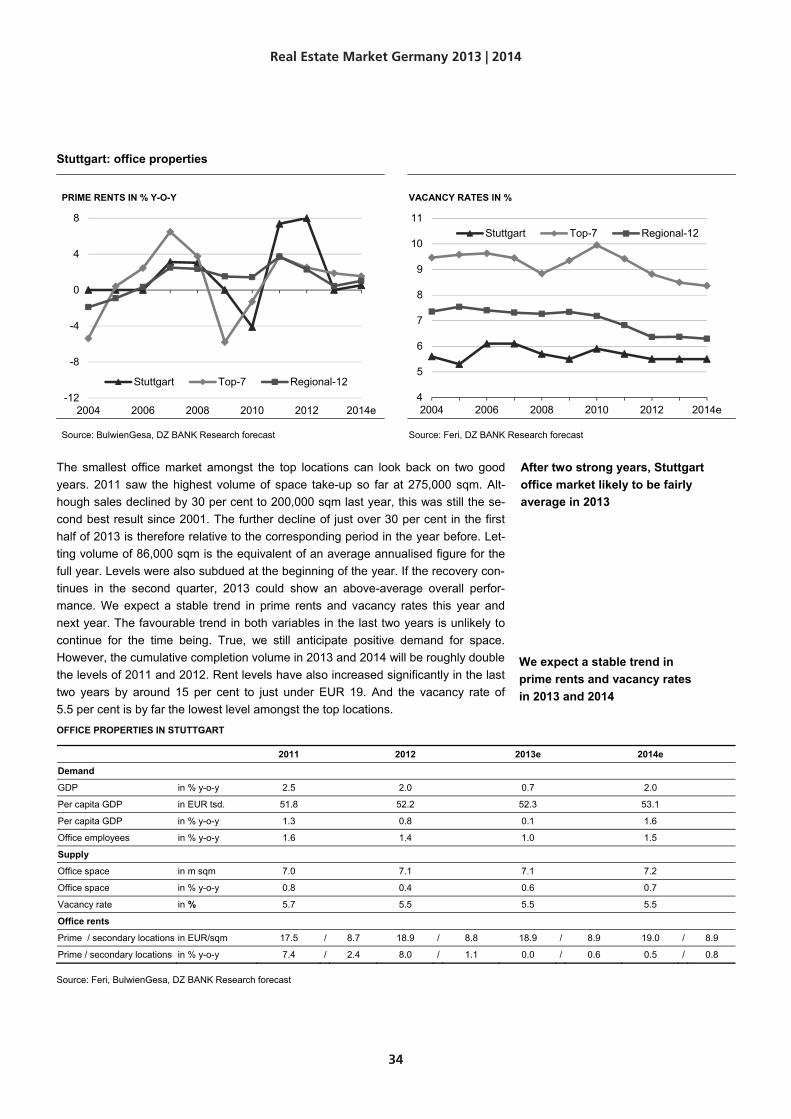

Munich: office properties

PRIME RENTS IN % Y-O-Y VACANCY RATES IN %

Source: BulwienGesa, DZ BANK Research forecast Source: Feri, DZ BANK Research forecast