gemstone and gold marketing forsmall scale mining in tanzania

TRANSCRIPT

•

•

International Business Initiatives

GEMSTONE AND GOLDMARKETING FOR SMALL SCALE

MINING IN TANZANIA

FINAL REPORT FOR PHASE IUSAID Equity and Growth through Economic Research

Trade Policy Studies

ECONOMIC AND SOCIAL RESEARCH FOUNDATION(ESRF)

TAN DISCOVERYand

INTERNATIONAL BUSINESS INITIATIVES(IBI)

April 14, 1998

1530 Key Blvd, suite 714Rosslyn, Va 22209

Tel. 703 525-2277 Fax 703 525-2211email: [email protected]

•

•

ii

ACKNOWLEDGMENTS

The team that conducted this study comprised Rogers Sezinga (TanDiscovery), Lucie ColvinPhillips (IBI), Haji Semboja and Godius Kahyarara (ESRF). The Policy Advisory Committee thatsupervised it comprised, in their individual capacities, the Commissioner of Mines Gray .Mwakalukwa, Director of the ESRF Professor Samuel Wangwe, Chairman of the Chamber of MinesSamuel Lwakatare, and several representatives of the government and academic community. Thestudy was funded by United States Agency for International Development (USAID) under theEquity and Growth through Economic Research Trade Policy cooperative agreement(EAGER/Trade), through subagreements by the primary recipient, Associates for InternationalResources and Development (AIRD), with IBI and ESRF. To the people in all of theseorganizations, and the friends, miners, brokers, dealers and Ministry of Energy and Mineralsrepresentatives who so graciously contributed their time and thoughts to this effort, we say aheartfelt thanks. They deserve most of the credit for the study, but none of the blame. The viewsrepresented here are those ofthe authors, not of the US or Tanzanian governments or any of theiragencies. Any errors or omissions are the responsibility of the authors.

iii

Table of Contents

Executive Summary '. . . . . . . . . . . . . . . . . . . . . . . . .. v

1. INlRODUCTION 11.1 Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 11.2 Government Objectives for the Sector . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 21.3 Purpose of this Study 31.4 Methodology . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 5

1.4.1 The consultative process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 51.4.2 Field interviews and data collection 51.4.3 Review of available literature 7

2. MARKETING FOR SMALL SCALE MINING IN TANZANIA. . . . . . . . . . . . . . . . . . . . . .. 112.1 Background of Mineral Marketing in Tanzania .. . . . . .. . . . . . . . . . . . . . . . . . . . . .. 112.2 Structure and Characteristics of the Market. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 12

2.2.1 Economic Geography of Mineral Markets . . . . . . . . . . . . . .. . . . . . . . . . .. 122.2.2 The Marketing Chain 12

2.3 Profiles of the Participants in the Minerals Markets ~ . . . . . . . . .. 152.3.1 Mine Workers 152.3.2 Claim holders 182.3.3 Brokers 202.3.4 Master Dealers 24

2.4 Factors influencing prices of gold and gemstones 26

3. SECONDARY ECONOMIC ACTIVITIES IN MINING COMMUNITIES 293.1 The Impact of Various Economic·Activities in Mining Areas 30

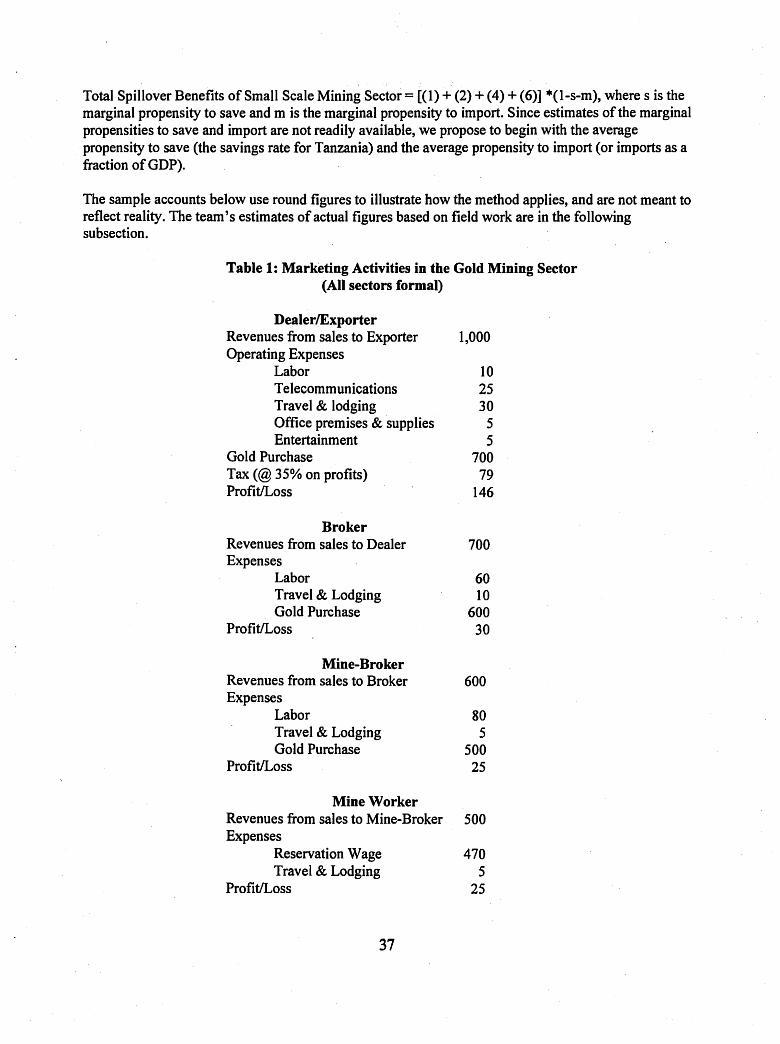

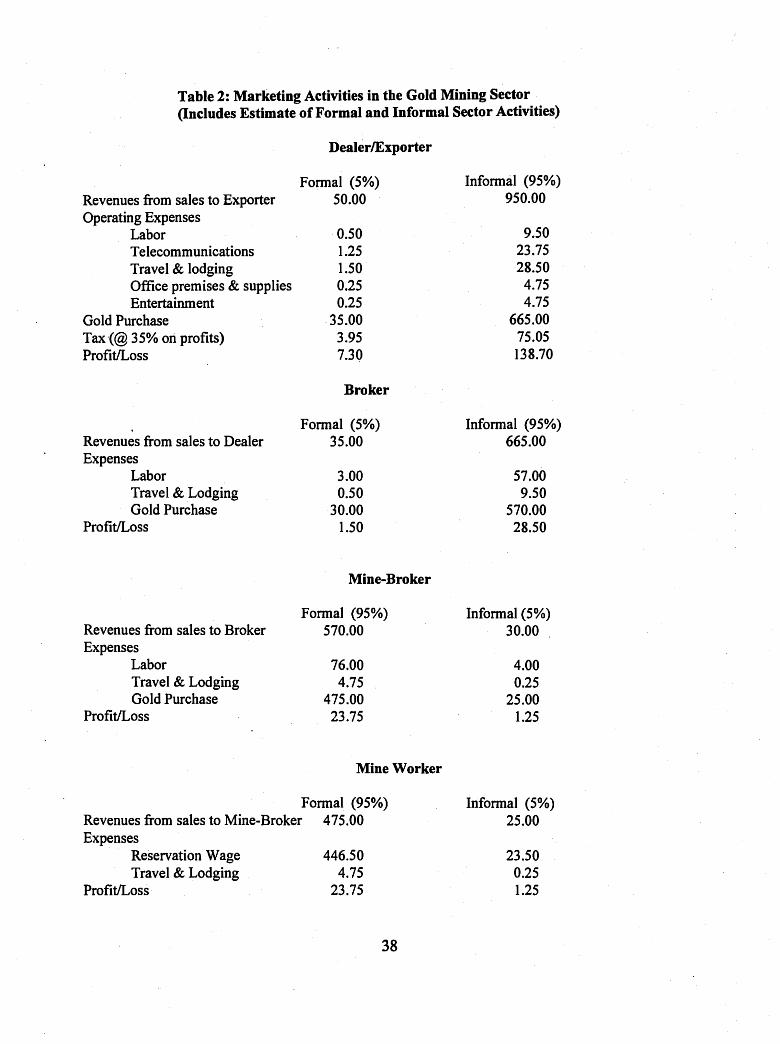

4. ECONOMIC EVALUAnON OF THE GEM AND GOLD TRADES. . . . . . . . . . . . . . . . . . .. 334.1 Economic Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 33

4.1.1 Methods Used 334.1.2. Results 394.2.3. Contribution to GDP from Mining Using the Income Method .. . . . . . . .. 48

4.3. Foreign Exchange and Minerals Marketing 494.3.1 Impact of Minerals Exports on FOREX Earnings 494.3.2 Impact of Exchange Controls and Currency Fluctuations on the Trade 49

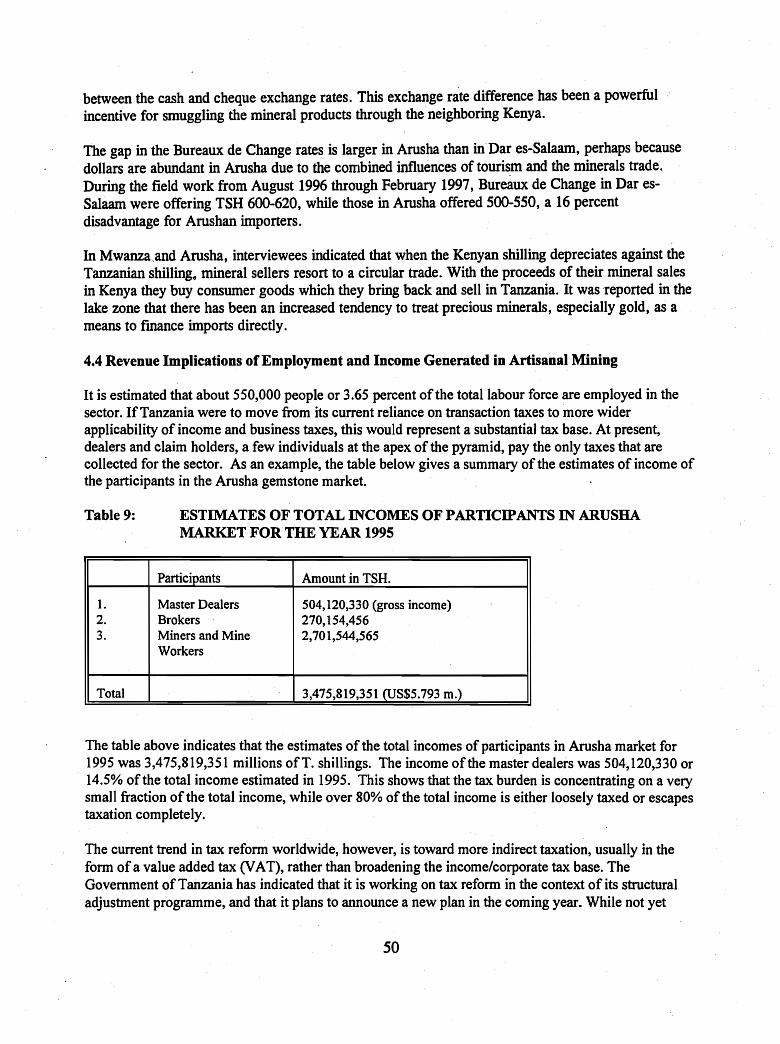

4.4 Revenue Implications of Employment and Income Generated in Artisanal Mining .. 504.5 Policies Favouring Value Added Activities 514.6 Negative Externalities from Artisanal Mining . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 53

5. OPPORTUNITIES AND CONSTRAINTS IN MINERALS MARKETING ..... . . . . . . . . .. 555.1 Opportunities. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 55

5.1.1 Balanced Development of Modern and Artisanal Mining 555.1.2 Competing with Kenya 575.1.3 Developing downstream value-added activities 58

5.2 Constraints and their policy implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .. 595.2.1 The fiscal regime 59

iv

5.2.1.1 High and unpredictable tax levels 595.2.1.2 Many different taxes, payable to different authorities. . . . . . . . . . . . . . .. 595.2.1.3. Fears of future taxation 605.2.1.4. Cumbersome and unclear tax payment procedures 605.2.1.5 An inequitable taxation system 60

5.3 Asymmetric information and the skills gap 60504 Bureaucracy and cumbersome procedures in the marketing of minerals 635.5 Lack ofenforcement of marketing regulations 0 635.6 Financial constraints o. 645.7 Lack ofIndependent Appraisals ofValue 645.8 Smuggling 0 ••••••••••••••••••••••••••••• 0 ••••• 0 •• 0 •••••• 0 ••••••••••• 0 65

5.8.1 Motives for Smuggling o ••••••••••••••• 0 •••• 0 .0 ••••••••••••••••• 655.8.2 Why Kenyan dealers offer a better market. 0 • 0 0 • 0 ••••••••••••••••••• 665.8.3 Nationality and smuggling 0 ••• 0 • 0 0 • • • • • • • • • • • • • • • • • •• 67

6.RECOMMENDAnONS FOR BEITER INTEGRATED MINERAL MARKETS. . . . . . . . .. 696.1 General Recommendations 0 ••••••••••••••••• 0 • • • • • •.• • • • • • • • • • • • • •• 696.2 Government Ministries 0 0 0 0 0 • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • • •• 716.3 Financial Services 0 • 0 •• 0 ••••••••• 0' •••••••••• 0. • • • • • • • • • • • • • • • • •• 746.4 Mineral Markets Promotion 0.0 •••••••••••••••••••••••••••••••••••••••••• 756.5 Improve Socioeconomic Situation in Mining Communities. . . . . . . . . . . . . . . . . . . .. 766.6 Balance the Interests and Activities of Fonnal and Artisanal Mining .. 0 •• 0 •••••• 0 76

ANNEX 1 .. 000 ••••••••••••••••• 0 ••••••••••••••••••••••••••••••••••• 0 0 ••••••••• 79ANNEX 2 0.0 •••••••••••••••••••••••••••••••••••••••••••••••••• 0 •• 0.0 ••••••• : •• 81ANNEX 3 .. 00 ••••••••••••••••••••••••••••••••••• 0 •••••••••••• 0 0 0 0 0 0 ••••••••••• 89ANNEX 4 0.0 •••••••••••••••••••••••••••••••••••••••••••••••••• 0.00 ••••••••••• 101ANNEX 5 0 •••••••••••••••••••••••••••••••••••••••• 0.00 ••••••••••• 113ANNEX 6 0 0 •••••••••••••••• 0 0 ••••••••••• 115BIBLIOGRAPHY 0 •• 0 0 • • • • • • • • • • • • • • • • • • • • • • • • • • • • •• 119

v

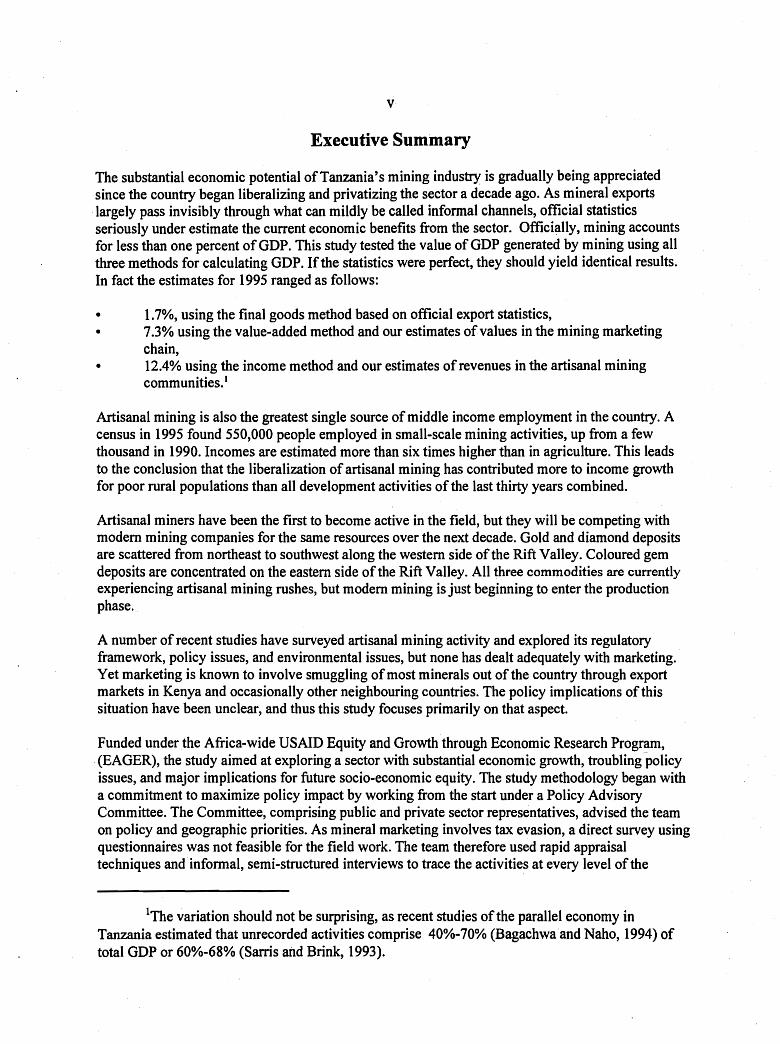

Executive Summary

The substantial economic potential of Tanzania's mining industry is gradually being appreciatedsince the country began liberalizing and privatizing the sector a decade ago. As mineral exportslargely pass invisibly through what can mildly be called informal channels, official statisticsseriously under estimate the current economic benefits from the sector. Officially, mining accountsfor less than one percent of GOP. This study tested the value of GOP generated by mining using allthree methods for calculating GOP. If the statistics were perfect, they should yield identical.results.In fact the estimates for 1995 ranged as follows:

• 1.70/0, using the final goods method based on official export statistics,• 7.30/0 using the value-added method and our estimates ofvalues in the mining marketing

chain,• 12.40/0 using the income method and our estimates of revenues in the artisanal mining

communities. 1

Artisanal mining is also the greatest single source of middle income employment in the country. Acensus in 1995 found 550,000 people employed in small-scale mining activities, up from a fewthousand in 1990. Incomes are estimated more than six times higher than in agriculture. This leadsto the conclusion that the liberalization of artisanal mining has contributed more to income growthfor poor rural populations than all development activities of the last thirty years combined.

Artisanal miners have been the first to become active in the field, but they will be competing withmodern mining companies for the same resources over the next decade. Gold and diamond depositsare scattered from northeast to southwest along the western side of the Rift Valley. Coloured gemdeposits are concentrated on the eastern side of the Rift Valley. All three commodities are currentlyexperiencing artisanal mining rushes, but modem mining is just beginning to enter the productionphase.

A number of recent studies have surveyed artisanal mining activity and explored its regulatoryframework, policy issues, and environmental issues, but none has dealt adequately with marketing.Yet marketing is known to involve smuggling ofmost minerals out of the country through exportmarkets in Kenya and occasionally other neighbouring countries. The policy implications of thissituation have been unclear, and thus this study focuses primarily on that aspect.

Funded under the Africa-wide USAID Equity and Growth through Economic Research Program,.(EAGER), the study aimed at exploring a sector with substantial economic growth, troublingpolicyissues, and major implications for future socio-economic equity. The study methodology began witha commitment to maximize policy impact by working from the start under a Policy AdvisoryCommittee. The Committee, comprising public and private sector representatives, advised the teamon policy and geographic priorities. As mineral marketing involves tax evasion, a direct survey usingquestionnaires was not feasible for the field work. The team therefore used rapid appraisaltechniques and· informal, semi-structured interviews to trace the activities at every level of the

lThe variation should not be surprising, as recent studies of the parallel economy inTanzania estimated that unrecorded activities comprise 40%-70% (Bagachwaand Naho, 1994) oftotal GDP or 60%-68% (Sarris and Brink, 1993).

vi

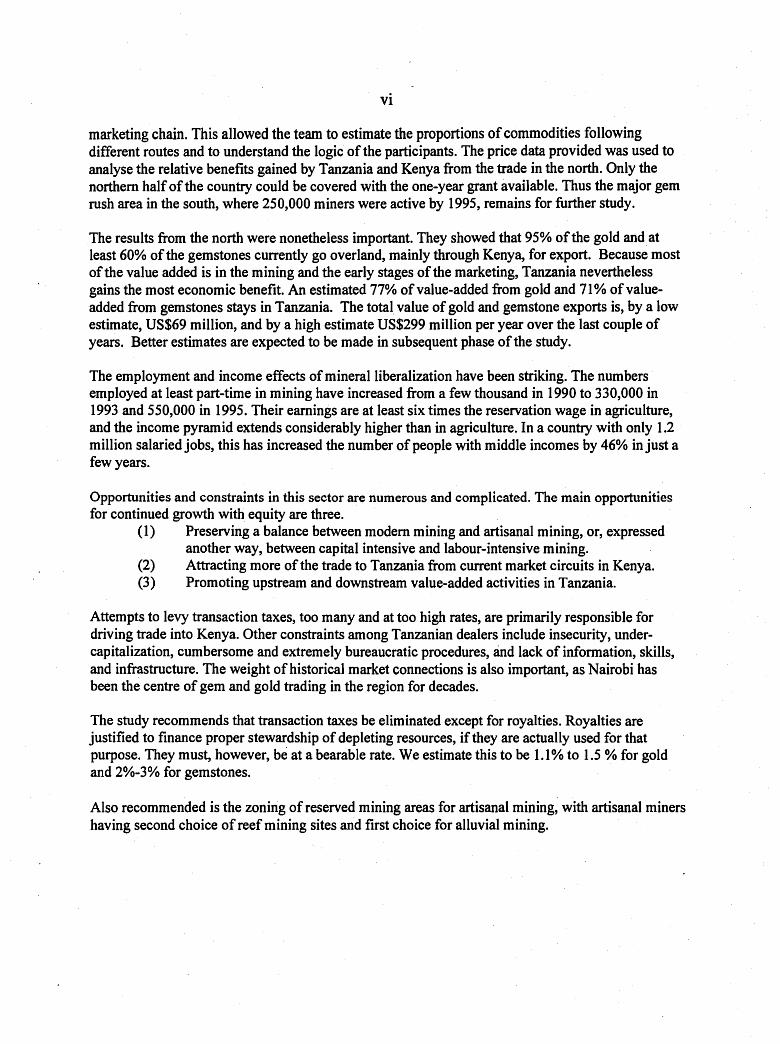

marketing chain. This allowed the team to estimate the proportions of commodities followingdifferent routes and to understand the logic of the participants. The price data provided was used toanalyse the relative benefits gained by Tanzania and Kenya from the trade in the north. Only thenorthern half ofthe country could be covered with the one-year grant available. Thus the major gemrush area in the south, where 250,000 miners were active by 1995, remains for further study.

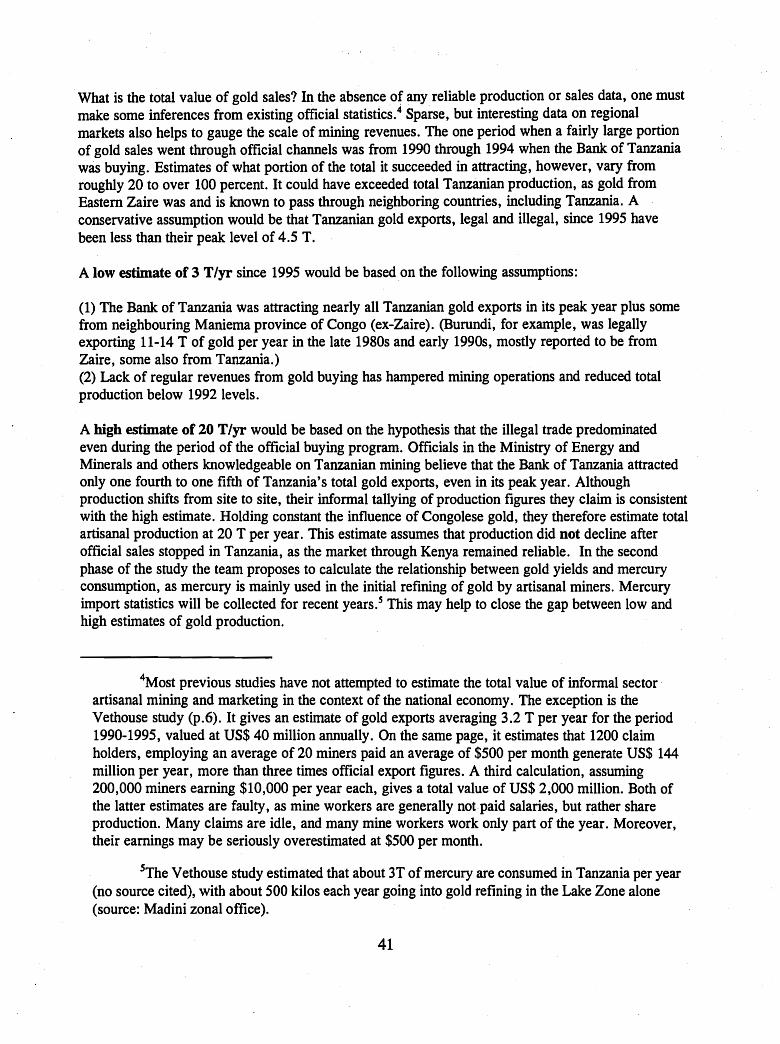

The results from the north were nonetheless important. They showed that 95% of the gold and atleast 60% of the gemstones currently go overland, mainly through Kenya, for export. Because mostof the value added is in the mining and the early stages ofthe marketing, Tanzania neverthelessgains the most economic benefit. An estimated 77% of value-added from gold and 71% ofvalueadded from gemstones stays in Tanzania. The total value of gold and gemstone exports is, by a lowestimate, US$69 million, and by a high estimate US$299 million per year over the last couple ofyears. Better estimates are expected to be made in subsequent phase of the study.

The employment and income effects of mineral liberalization have been striking. The numbersemployed at least part-time in mining have increased from a few thousand in 1990 to 330,000 in1993 and 550,000 in 1995. Their earnings are at least six times the reservation wage in agriculture,and the income pyramid extends considerably higher than in agriculture. In a country with only 1.2million salaried jobs, this has increased the number of people with middle incomes by 46% in just afew years.

Opportunities and constraints in this sector are numerous and complicated. The main opportunitiesfor continued growth with equity are three.

(l) Preserving a balance between modem mining and artisanal mining, or, expressedanother way, between capital intensive and labour-intensive mining.

(2) Attracting more of the trade to Tanzania from current market circuits in Kenya.(3) Promoting upstream and downstream value-added activities in Tanzania.

Attempts to levy transaction taxes, too many and at too high rates, are primarily responsible fordriving trade into Kenya. Other constraints among Tanzanian dealers include insecurity, undercapitalization, cumbersome and extremely bureaucratic procedures, and lack of information, skills,and infrastructure. The weight of historical market connections is also important, as Nairobi hasbeen the centre of gem and gold trading in the region for decades.

The study recommends that transaction taxes be eliminated except for royalties. Royalties arejustified to finance proper stewardship of depleting resources, if they are actually used for thatpurpose. They must, however, be at a bearable rate. We estimate this to be 1.1% to 1.5 % for goldand 2%-3% for gemstones.

Also recommended is the zoning of reserved mining areas for artisanal mining, with artisanal minershaving second choice of reef mining sites and first choice for alluvial mining.

1.1. Background

The substantial economic potential of Tanzania's mining industry is increasingly being appreciatedsince the country began liberalizing and privatizing the sector a decade ago. The comprehensiveeconomic reforms adopted in the mid 1980s have led to the liberalization ofthe mining sector,followed by a dramatic increase in private sector participation in mineral trade and production.According to the official statistics, it still contributes only about 1 percent ofthe GDP, and roughly20/0 of the total export earnings. These figures, however, seriously underestimate the value ofcurrentmining and related activities, as artisanal mining of gold, coloured gems and diamonds and therelated marketing mainly lies within the informal sector. Employment and income growth in themining sector are also on the rise and a census in 1995 found that 550,000 people were employed inthe sector (Tan Discovery, 1996). There are only 1.2 million total salaried jobs in Tanzania, whichmeans that the mining sector has added another 46% of middle income jobs to the total employment,mostly in the last five years. No other sector has made a similar contribution to social well-being andincome distribution. These jobs may be at risk, however, as more formal mining investments aredeveloping rapidly.

Official statistics also do not reflect the potential that Tanzania has in the mining sector, as reserveshave not been systematically evaluated. Recent studies show that the sector has an immediatepotential for rapid growth in the next few years (Intra governmental Export Strategy Task Force,1995).

1.1.1 Mineral Geology

Tanzania has a rich mineral resource base. Geological mapping, exploration and mining activitiesdating back to the early twentieth century culminated in the first comprehensive geological andminerals survey in 1958, which is still a classic (Harris, 1958). This was recently updated for thegovernment (Ministry of Energy and Minerals, ed. Brian Hester, .1992, 1995). Artisanal miners andmajor companies, however, are both interested in gold, diamond, and coloured gems. The gold anddiamond reserves have been well documented in UNDP-sponsored studies and studies sponsored byprivate mining companies. Commercially, viable deposits are scattered along the western side of theRift Valley, gold in the greenstone belts of the Archean craton and diamonds in the hundreds ofKimberlite pipes throughout the same geographic area.

Gold mining activity is concentrated in three major areas, but activity often shifts as old depositsbecome less profitable and new ones are found. The main gold areas include the following:

• the Lake Zone gold fields, south and east ofLake Victoria, up to the Kenya border. The mostactive sites are Geita, Bulyanhulu near Kahama, Irambe, Sekenke, Kilima Fedha, Serengeti,Nyambegena, Buzroba, Matinje, Musoma and Tarime (north Mara).the Lupa area in Chunya District of Mbeya Region near the Zambia border. The most activemining sites are Saza, Makongolosi, Ntumbi, Chunya, Lupa-Sira, Sengambi, Mabadaga andIyai.Mpanda, with six active mining areas: D-reef, Magamba, Kapanda, Kitisunga, Ibindi, andSikitiko.

1

new sites at Lukalasi in Mbinga district, Kitowero in Liwale district and Buma in Manyonidistrict.

The major diamond mining areas are in northern Tanzania, around Shinyanga, Mwananga, Mabukiand Mwanza. Williamson Diamond Mine is the only formal mining operation, but diamonds worth anestimated $13 million to $16 million per year (VethouseIUSAID, 1995) are produced by artisanalminers and exported, mostly through informal channels.

Commercially exploitable deposits ofcoloured gems tend to be found on the eastern side ofthe RiftValley. They also were originally discovered and exploited by individuals and small companies. Theyare now the subject of a mining rush comparable to that of Brazil in the 1980s. This geographicregion hosts two gemstones unique in the world, Tanzanite and green garnet (called Tsavorite inKenya, for the Tsavo area in which it was originally found). The only known deposit ofTanzanite inthe world lies near Merelani, in northern Tanzania between Arusha and Moshi. This is a brilliant butslightly brittle gemstone ranging in colour from pale violet to deep blue-violet. It was popularized byTiffany's in the late 1970s, and commanded a peak priceofUS$2500 per carat by 1983. Morerecently rare and precious Alexandrites, previously known only in Sri Lanka, have been found insouthern Tanzania near Tunduru. There are extensivedeposits of ruby (Morogoro and Umba River),sapphire, garnet, tourmaline (Umba River and Tunduru), emerald, chrysoberyl and other semiprecious gems (Tunduru).

1.2 Government Objectives for the Sector

The government has set the following objectives for the mining sector (Ministry of Energy andMinerals, 1997):

(1) to maximize fiscal and export earnings; and

(ii) to raise the contribution of the sector to total country GDP to at least 10% by the year2025.2

To attain these objectives, the government has recently commissioned a number of studies of themining sector, and sought support in the form ofa US$12 million five-year World Bank technicalassistance programme.

The government is also committed to make the mineral sector's development more regionally andglobally competitive and more efficient. It seeks to attract more of the production to formal exportchannels. This· is an attempt to make the sector more flexible and withstand both internal and externalchanges that might affect its progress.

It is envisaged that the mineral sector will substantially contribute towards income generation,employment creation, social and economic infrastructural development -- particularly for the rural

2This target is based on official statistics, which currently peg minerals exports at slightlyunder 2 percent ofGDP. The current study estimates that minerals exports actually comprise tenpercent or more ofGDP already, hidden by the fact that they do not go through official channels. Ahigher target·could therefore be set.

2

areas, and increase foreign exchange earnings and government revenue. In order to achieve themineral sector objectives, increased private sector participation in the mineral sector's developmentand reduction of the government's direct involvement in mineral production activities are beingemphasized. The government, however, shall continue to maintain the promotional and regulatoryrole in directing the activities of the mineral sector.

Factors that impede the effectiveness of the private sector in the country's mineral development, suchas the lack of stable fiscal and non-fiscal incentive packages, the institutional and legal framework,and the relevant financial and technological arrangements are being addressed. New mineral policyand mineral development strategies have been prepared and are being reviewed with a view to issuinga new Mining Code in 1997.

1.3. Purpose of this Study

This study is funded by USAID's Equity and Growth through Economic Research program, TradePolicy Component (EAGERffrade). This is an Africa-wide demand-driven policy researchprogramme, designed to fund studies that facilitate policy reforms aimed at accelerating growth whilepreserving socio-economic equity. This study, like others in the program, focuses on a sector withhigh potential growth that is currently inhibited by policy uncertainties during a transition from astatist to a market-oriented economy. It seeks to determine the policyframework most likely toenhance growth and socio-economic equity (in this case, mainly employment). At the same time, itrecognizes the need to maintain government revenues, so the fiscal implications of each policyrecommendation are analyzed. As policies must be politically feasible, this study has not beenconducted in isolation like many research projects. A Policy Advisory Comt:Jlittee comprising stakeholders from the public and private sectors has worked with the research team from the start. Theirinput and that of a larger body of stake-holders to be consulted through subsequent workshops will becritical in shaping the final recommendations of the study.

Specifically however, the study aims at exploring the nature and characteristics of the existingmineral market in Tanzania since it has been singled out as the main cause of poor performance ofthe mining sector. Back in the 1960s after the Arusha Declaration of 1967, the state nationalized mostmining. Private sector participation in minerals marketing was minimized and a parastatal monopolyfor mining and minerals marketing was created.

That monopoly was ended in 1987, but since then, the macroeconomic policy framework has beencited as a source of mineral marketing problems. Miners and dealers say that the fiscal regime,interest rate and exchange rate policies, unstable investment policies have hampered new investment.The artisanalnature of the mining activities has also been responsible for poor performance of themining sector in the country. Some artisanal claims and marketing operations are legal, but othersshade into parallel markets. Production and trade of minerals has been shrouded in secrecy, makingdetailed assessment of both performance and prospects exceedingly difficult. Miners do not readilyreveal the quantity they produce, and similarly mineral dealers are not prepared to give the actualfigures on what they export.

Since the end of the monopoly, some steps have been taken to create a legal private marketingsystem. For gem and diamond dealers, a partially viable legal framework is in place, but small-scalegold miners currently have no legal buyers for their ore. From 1990 to 1995, the Bank ofTanzania

3

and the state-owned National Commercial Bank operated a gold-buying scheme, but withdrewfrompurchasing gold after incurring substantial trading losses. There had been minor trading lossesthroughout, as bank personnel were not experienced in gold assaying and relied on assay results fromtheir buyers in London for final pricing. In the end a large shipment adulterated gold was bought,bankrupting the system and convincing the government to withdraw from state operated schemes.

Private gold dealers were allowed to register after this, but the conditions of registration haveincreasingly become less attractive. Those who registered the first year did not renew the secondyear. A new group registered, but they, too, did not renew the second year. Now (as ofJanuary 1997),there have been no legal gold exports for six months, although exports continue through parallelmarkets. Commercial banks, joint venture mining companies and licensed dealers are all interested increating buying programmes, but current fiscal practice makes it temporarily unfeasible. TheMinistry ofEnergy and Minerals is aware ofthe problem, and is seeking to establish a regulatoryframework that will provide for reliable buyers to be able to operate in Tanzania.

A substantial portion of the minerals produced in Tanzania is thus smuggled, mainly through Kenya,but also through Mozambique, Burundi, Rwanda, Uganda and other neighbouring countries. Theresult is that Tanzania's tax revenues from precious minerals are declining even as the miningactivity grows. There is also concern, noted by Export Strategy Task Force, that the foreign exchangethat is earned stays outside the formal banking system. The Task Force identified this as a majorissue to be studied. .

The Ministry ofEnergy, Minerals and Water has, with World Bank funding, funded a baseline studyto survey small-scale miners and their activities in all major mining areas in the country. The study,conducted by Tan Discovery, was presented and discussed at a workshop in Dodoma involvingrepresentatives of the Ministry, the Tanzania Chamber of Mines, as well as gem and gold dealers andminers.

The present study was c~>nceived and designed based on that workshop, where a consensus wasreached on what areas needed further research. The preliminary report provided little quantitativedata. In particular, there was no clear picture of gold and gem marketing systems. For the minerspresent at the workshop (as for dealers and government),·marketing was a top priority.

The government wanted a better understanding ofcurrent market operations in this sector. It isconcerned that the s~uggling currently going on in the mineral sector adversely affects. the overallcountry's economy especially with regard to the trade balance and the government budgetperformance. There was a large and visible channel through Kenya, but unofficial exports fromTanzania directly to Thailand and other Asian and Middle Eastern markets were also thought to besubstantial.

To create a competitive marketing system, Tanzania has to know how markets operate inneighbouring countries in comparison to the workings of its own markets. Tanzania has attempted tolevy royalties and export taxes on gold and gems, without realizing that neighbouring Kenya profitedfrom this by offering dealers tax free exports. Mozambique has recently entered the picture with verylow taxation on exported gems. Our hypothesis is that Tanzania has to compete for the trade, as itwill naturally seek the most advantageous market. With such easily concealed merchandise and vastopen borders, it is not cost-effective to suppress smuggling by force of law.

4

1.4 Methodology

1.4.1 The consultative process

An integral part of the study approach has been to work in consultation with a Policy AdvisoryCommittee comprising relevant policy makers from both the public and private sectors. The researchteam was mobilized at ESRF in August 1996 and a policy-makers' Advisory Committee wasimmediately constituted to guide the study. It comprises individuals who work in the Ministry ofEnergy and Minerals, the Tanzania Revenue Authority; the Tanzania Chamber of Mines; theTanzania Mineral Dealers' Association (TAMIDA) and the Federation of Miners Associations ofTanzania (FEMATA), all ofwhom serve in their individual, not official, capacities on the PolicyAdvisory Committee. It met in August 1996 to inaugurate the study and advise on the first field worktrip, which took place in the northern zone in August and September 1996. It met again in January1997 before the second field work trip, to the Lake Zone gold producing area, and met a third time inconnection with the EAGER workshop held in Dar es Salaam in August 1997.

1.4.2 Field interviews and data collection

The team used rapid rural appraisal methods to interview participants at every level of the marketingchain. The country was divided into four interior zones that include the main gold, diamond andcolored gem producing areas. Dar es-Salaam and Zanzibar constitute a fifth zone, important for theirrole in marketing, not for mining itself. The first two zones were canvassed in August and November1996. The remaining zones we hope to cover in a second phase of the research.

Key informant interviews were held with mining and other local officials throughout the zonescovered, and at the national level. We interviewed and collected data from officials in the Ministry ofEnergy and Minerals, the World Bank Minerals Sector Project, and the Tanzania Revenue Authority.We spoke with five representatives of international mining companies interested in Tanzania. At thelocal level we interviewed leaders of the mining community, mining associations, minerals zonalofficers, police, migration officers, and leaders of national professional associations involved inmining and marketing. Semi-structured interviews were conducted with miners and traders at alllevels of the chain, extensively in Tanzania and more lightly in Kenya. This proved the most usefulform of information collection, as participants nearly always refused to answer formal questionnaireson their marketing practices. The team agreed upon a set of topics to be covered with each type ofactor in the chain, and held semi-structured individual and small-group interviews, following aspecific set of topics, b~t without a formal questionnaire. In most cases the team took notes duringthe interviews. Whenever the team believed that this made the interviewees less forthcoming, notetaking was deferred. During evening feedback sessions the team compared notes and highlighted thekey ideas coming from each interviewee. Focus groups were held when possible, for example withthe mine claim-holders of Tanga Region and with the brokers ofArusha Region.This allowed us toestimate the proportions of commodities following different routes and to understand the logic of theparticipants. The price data provided was used to analyse relative benefits to Tanzania and Kenyafrom the trade.

• The sample interviewed

The sampling pattern involved both geographic and socio professional stratification. In the two initialfield trips, the team interviewed over 300 people in two ofthe five zones into which we divided the

.5

country, including 20 master dealers, 123 mine owners, 50 brokers and 64 officials and miningcommunity leaders. Wholesale dealers, goldsmiths and jewelers in Dares Salaam were alsointerviewed, as were, for comparative purposes, dealers and officials in Kenya and Ghana.

In Tanga Region, all leaders of the Regional Miners Association (REMA) were interviewed. In theUmba River area, in addition to brokers of various types, six mining village leaders wereinterviewed. In Arusha, the major gem marketing town, we covered all types of participants in themineral market. We interviewed the top six dealers, who together dominate the market, and otherlicensed dealers for a total of 18 of the 62 master dealers in Arusha. Leaders ofTanzania MineralDealers Association were interviewed, the chairman and other members. In addition, all leaders ofRegional Mines Association in Arusha were interviewed, and 40 out ofthe 3,000 brokers active inArusha. Out of several operators in the area, fifteen medium scale traders and operators in othereconomic activities than mining were interviewed. The zonal mines officer ofArusha, ArushaRegional Police commander and officers ofTanzania Revenue Authority. Officers ofthe formerTanzania Gemstones Industries (TGI) in Moshi were interviewed. In Dodoma several claim holdersand mine workers in gold mines at Nzunguni were interviewed, as were several mineral claimholders, brokers, master dealers operators in mineral marketing. In Shinyanga we interviewed twomajor diamond dealers, and a regional mines officer.

Generally, the topics covered included m'arketingproblems, followed by a history ofthe participants'role in the market. This included:

~ the prices they paid and received at each point for each type and quality of goods;~ their estimate of how many goods were going to which markets from their operating base;~ the estimate of their price margins from one point to another, ofmonthly income or income

from each buying trip, and their operating costs;~ how the person got started in the mining sector, how much initial capital they had and from

where, how they built their capital, what risks and losses they had experienced, andwhether/where they had invested any gains;

~ their proposals for improving minerals marketing;~ relationships with relevant government departments.

The team also interviewed persons involved in auxiliary activities, such as retail shops, restaurants,bars, hotels, transport and other services, to determine the variety ofactivities that existed and insome case to study the monthly net incomes. It was not possible to conduct a proper quantitativesurvey, nor to create account balance sheets.·We therefore present this information in case-studyformat and do not attempt to quantify its global economic impact.

Since mining activities are spread throughout the interior zones ofthe country, a problem ofgeographic coverage presented itself from the start. Time and funding were important limitations.Time considerations included the fact that the government is considering a new Mining Law in 1997,the first major revision since 1979, and the input from this study would be most useful the faster itwas available. Another factor was the one-year time limit and modest funding cap on USAIDEAGER/Trade research grants, which obliged the team to produce a report based on the first twozones rather than completing the field work before drafting a report. The Policy Advisory Committeerecommended that the study team begin with the most important mining areas, but try to cover all ofthe major producing and marketing sites. The country was divided into five zones, to be covered insuccessive fieldwork trips:

6

(I) the northern zone, including the getri-bearingand trading areas ofTanga, UmbaRiver, Korogwe, Kilimanjaro, Moshi, Merelani and Arusha;

(ii) the lake zone, including the gold, diamond and gem mining areas of Mwanza,Tarime, Singida and Shinyanga;

(iii) the central zone, including Morogoro, Songea, Mpanda, Kigoma and Chunya;

(iv) the southern zone, including Tunduru and the surrounding Ruvumu River gem rusharea, plus the market towns of Mbeya and Mtwara; and

(v) Dar es-Salaam and Zanzibar Island.

Only the first two zones could be covered with the funds available for the first phase ofthe project.A second phase EAGERffrade grant will be proposed to enable the fieldwork to extend to theremaining three zones, to allow the economic analysis to explore fiscal and foreign-exchangeimplications of the trade and to fund workshops on the results.

Three sets of economic analyses were conducted during the study, as described in Chapter 4 anddetailed in Annex 3. The first analyses the impact of the mineral trade on the actual macro-economicsituation ofTanzania, including the impact of the liberalization of minerals trading on employment,income distribution and economic growth (GDP). It also examines the effects of smuggling on GDPand foreign exchange. Two main macro economic calculations are undertaken. First is the impact ofundeclared mineral exports on under valuation ofthe GDP, and on the undervaluation ofthe portionof GDP generated by mining. As precious minerals are almost entirely exported, the balance of tradeindicated in the official statistics is also substantially understated, as most of these exports areundeclared. It is known in mineral trade circles that these exports generate foreign exchange used tofinance imports. This helps to explain how Tanzania has managed to record an increasingly largenegative trade balance for many years, without a corresponding devaluation of its currency (whichfloats freely). Consumption of imports is clearly higher than official exports could finance.

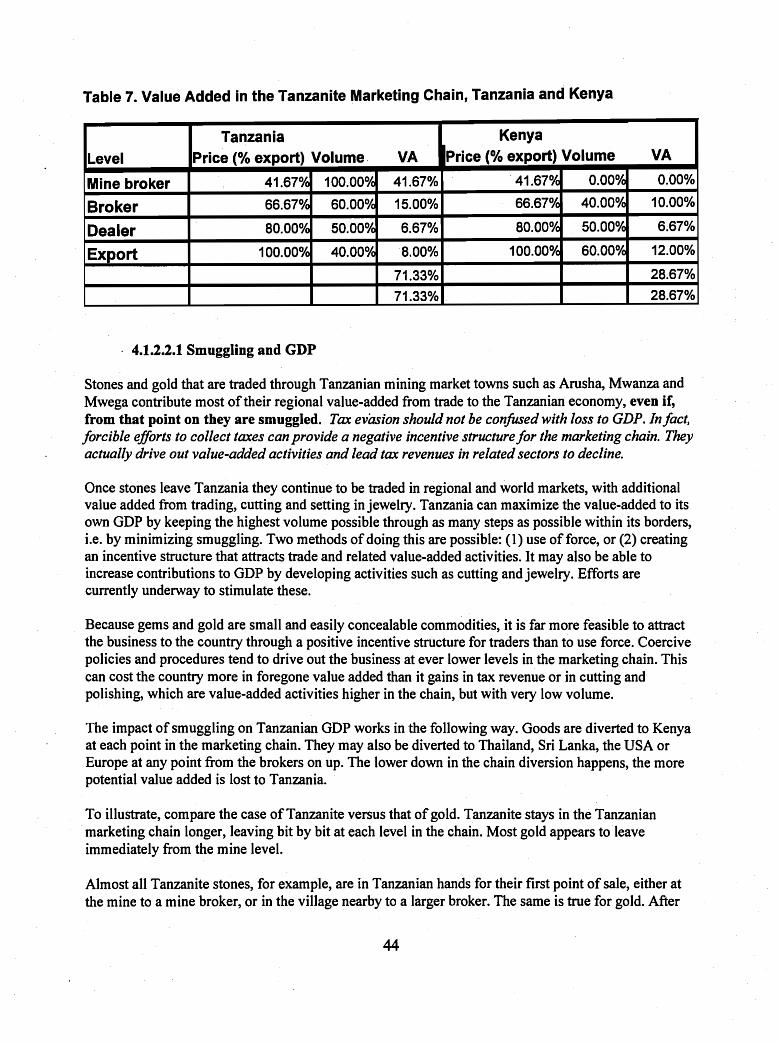

The second calculates the value-added from trade at each step in the marketing chain. This allowedus to estimate the distribution of economic benefits from northern Tanzanian mining between Kenyaand Tanzania. Our results showed that an estimated 95% ofgold and 60% of gems are smuggled outthrough Kenya. Most policy-makers in Tanzania tend to assume that an equivalent.portion ofeconomic benefit is lost to the Tanzanian economy. This turns out not to be true. When the reservevalue of minerals and the value-added from mining and the portion of the trade that takes place inTanzania are cumulated, the great majority of the economic benefit rebounds to the Tanzanianeconomy.

Finally, to analyse the competitiveness of Tanzania's business climate, a microeconomic model wasbuilt of the costs of doing business as a gem dealer. It shows how the tax structure and relative costsof capital favour the growth of business in Kenya rather than in Tanzania.

1.4.3. Review of available literature

A review ofthe literature conducted in the course ofthe study found that Tanzania's artisanal andsmall-scale mining sector is relatively well documented, but there is a dearth of comparative studies

7

on artisanal mining elsewhere in the world. Even in Brazil, Thailand and Ghana where such mining isthriving, there are only minor references in mining journals.

The US Bureau of Mines published two studies that allow Tanzania's new minerals industry to be putin perspective: Mineral Industries ofAfrica: 1993 International Review and World Gold: A MineralsAvailability Appraisal. (1994) The World Resources database maintained by World ResourcesInstitute is also a reference.

Previous literature on artisanal mining in Tanzania includes a series ofworldwide studies andworkshops fmanced by the World Bank, as well as surveys designed to attract mineral investment toTanzania. Background geological mapping and information is the third type of literature, mentionedabove in the introduction. In addition to the Harris·and Hester geological surveys, work by Kimambo(1984) gives a brief description of Tanzania mineral potential and various mining developmentactivities from the late 1950s to the mid 1970s. Another study reviewing mining operations andsocio-economic aspects from the late 1930s to early 1990s was done by Chachage (1994). Itexamined the mining industry and accumulation in Tanzania, and a critique ofthe relationshipbetween artisanal miners and formal mining companies.

There has been new interest in the mineral sector with the introduction of major changes in thesocioeconomic policies of the country in the mid eighties. Several studies have reviewed thecountry's mineral resources and made recommendations to improve the sector's performance. Astudy was commissioned by the Ministry of Energy and Minerals in 1994 as preparatory work for theMineral Sector Development Project funded by the World Bank.(Engineering Associates and TanDiscovery, 1994). The study examined at length the problems facing mineral sector development inTanzania. It signalled small-scale mining, training, environmental issues as areas needing furtherstudy.

Another group of studies aimed to attract and guide large scale mining investors. Examples of theseare: "Opportunities for Mineral Resource Development" (Hester, 1991 and 1996), and "The MineralSector in Tanzania" (Vethouse, 1996). These studies both provide summaries of the rich mineralresource base ofTanzania as well as the licensing procedures, the existing fiscal regime and otherinvestment incentives. Hester's work provides,details of specific mineral potential areas andgovernment efforts to support mining investors. The Vethouse Associates study, funded by USAID,provides an independent assessment ofthose efforts and makes recommendations to improve theexisting legal and regulatory framework.

From the mid-1980s to the present time, the activities of artisanal and small-scale miners haveincreased considerably from few thousand miners to a community of more than 550,000 people.This development was followed by a number of studies addressing various sub-sectoral issues. In1994, UNDP financed studies of "Small-Scale Mining in Tanzania," the first part involved aTechnical Assessment (Hollaway 1994) and the other part concentrated on the InstitutionalFramework (Lwakatare, 1994). There was another UNDP study, "Export Development andPromotion of Mineral Resources" (Twum & Kanza, 1992) which reviewed existing data on thecountry mineral resources and made some practical recommendations on the problems facing themineral markets.

8

Comparative information has come largely through'WorldB~k efforts, as academic and technicalmining literature is remarkably silent on artisanal mining. In April, 1994, the World Bank organizeda Round Tab.1~ in Washington on Artisanal and Small Scale Mining with the aim of formulating aglobal "Comprehensive Strategy Towards Artisanal Mining."(World Bank, 1995,1996) Severalpapers where presented including a study on "Artisanal Mining in Tanzania" (Tan Discovery 1994)which mainly covered the organizational and socio-economic aspects. The round table deliberationsalso included the "Harare Guidelines for the Development of Small-Scale Mining," (UNDP 1992)and the past experiences in addressing the issues of the sub-sector. Roundtable speakers noted thatseveral million people worldwide earn a living from artisanal mining. They produce an estimated 20percent of the gold, 40 percent of the diamonds and nearly all of the gemstones mined in Africa. Thephenomenon is also widespread in Latin America, although Brazil's famous small miners aregradually being squeezed out by international mining companies. They produce 50 percent ofBrazilian gold today, against 70 percent some years ago.

In connection with the launch of its World Bank-funded mining sector reform, recently Tanzania'sMinistry of Energy and Minerals commissioned a detailed study of the small-scale sub-sector inTanzania. "The Baseline Survey and Development Strategy for artisanal and small scale miningprogramme" (Tan Discovery 1996) provides basic data and strategies on institutional, organizational,mining and processing, marketing, environmental and socio-economic aspects. The study did notcover some important issues on mineral markets which could help to influence policy changes inlegal and fiscal regimes to improve mineral markets.

None of these studies directly addressed marketing operations and related policy issues. This is thereason for the focus of the current study.

9

2.1 Background of Mineral Marketing in Tanzania

Mineral marketing processes and structures can be traced back to the colonial era. In the 1930s, agold rush in the Lupa area stimulated minerals exploration in many areas. Small reef miners withsome capital and equipment obtained from other economic sectors emerged and joined in theproduction and marketing ofgold.

Africans pressured the colonial government to grant them licenses because they were victims of lowwages and poor conditions. They had experience working in mines which at that time were under thesettlers and other European miners. A product sharing scheme allowed retired European civilservants, known as "verandah prospectors," to exploit artisanal mines in the late 1930s, contributingto the development of loose mineral marketing. The official market dominated mineral tradingalthough there were some reported cases of smuggling. By the end of the colonial period mineralproducts were contributing over 10% to the total export earnings.

After independence, the government continued to issue prospecting licenses on individual bases, butencouraged small operators to form mining cooperatives. Some of these cooperatives, such as LupaGold Diggers Association, which was formed in 1963, played a key role in both the mining andmarketing of gold from small scale miners. Later on, however, many mining properties were takenover by Greek nationals who also dominated the sisal industry.

Mineral trading was regulated by a 1965 mineral trading ordinance and a gold ordinance.Commercial banks supported mineral trading through the provision of credit facilities and mineralcustody service. Smuggling was minimal and most of the exports were handled by the few wellestablished companies. The main ones were Umba Ventures for Mining and Export of ColouredStones and Williamson Diamond Mines.

After the Arusha Declaration in 1967, most of the mining companies were nationalized. Thegovernment formed Tanzania Gemstone Industries Company (TGI) in 1972, with a monopoly inmining purchasing, producing and exporting coloured gemstones. In 1973, the government formedthe State Mining Corporation (STAMICO) which had the responsibility of overseeing thedevelopment of the mining sector, including new exploration and the operation of nationalizedmines.

STAMICO also became the parent company of TGI. From 1970 to the mid-1980s, the mineralexport performance was most unsatisfactory, as there was a drastic fall in gold exports and a gradualdecline in diamond exports. The exportation of gold, for example, dropped from 500 kg in 1969 to 20kg in 1971.

The comprehensive economic reforms introduced as part of economic recovery programmes ofthemid-1980s led to liberalization of the minerals markets through the issuing of mineral dealerslicenses to private operators in 1987. Soon after, mineral exports started to increase. The Bank ofTanzania established a gold buying system through the National Commercial Bank in 1990. Officialexports of gold accelerated to a peak ofUS$40,380,000 in 1992, from to US$I,152,057 in 1989. The

11

buying system was bankrupted by a scam in 1994 however, and subsequently discontinued. Since .1995, there has been inadequate provision for the legal purchase of gold in the country, and mostproduction has been marketed through the informal channels in Kenya.

By 1994 the currency was allowed to float freely and importers were allowed to use their ownsources of foreign exchange. Minerals markets began to flourish in Tanzania, and the influx ofcapital spurred new exploration. Plots in the Merelani Tanzanite mines were allocated to smallminers in two phases in 1995 and 1996, creating a surge in production there. Simultaneously. in thefar south, the Ruvuma River valley, which forms the border with Mozambique, was found to beextraordinarily rich in coloured and precious gemstones of many varieties. This set off a mine rushthat has brought over 250,000 people into that isolated enclave, and created a regular/traffic ofchartered flights, ocean freighter service and overland trips.

2.2 Structure and Characteristics of the Market

2.2.1 Economic Geography of Mineral Markets

The surveys found four levels in most of the minerals markets, namely the mining area, the primarymarket, the secondary market and the export market. Each of these has its own features. Buyers atone level of the market are sellers at the next level. Price margins between one level and the next canbe substantial, particularly when the volume of goods handled is low. The four levels are almostidentical for coloured stones and gold but the diamond market skips the primary market and in mostcases its secondary market is the export market. The more valuable the goods sold, the more likelysellers are to try to skip one or more links in the normal marketing chain and keep the mark upthemselves.

2.2.2 The Marketing Chain

• Market level one: The mining area

The first sale of raw gems or gold ore often takes place immediately at the mining sites. At thismarket stage, mine workers and small brokers are the main participants. The organization of artisanalmining favours this arrangement. Tanzanian mine workers refuse to work on salary, preferring theprevailing system of production sharing between worker and the mine claim holder and/or pit owner.Mine workers can market their official shares openly in nearby mining towns, but they'often secretvaluable finds and market these stolen goods to mine brokers directly at the mine.

• Market level two: The primary market

In mining villages a short distance from the mines one finds primary markets where·production entersquasi legal channels. Sales are legal, but, for reasons explained further on, most of the brokers at thislevel are not licensed. The degree of market activity in mining villages depends mainly on thequantity and quality of the recovered minerals. The main participants in this marketlevel are brokers'and small brokers. The latter frequently shuttle between the mining sites and the primary market.

On local market days mine workers are also active, selling small parcels of good quality stones.Master dealers and large scale brokers from major towns and even outside the country frequentlyvisit mining villages. The government banned foreigners from mining areas in 1996, but the

12

exclusion is difficult to enforce. Sometimes, participants in other economic activities living in themining villages and towns, such as retail shop keepers, barbers, owners of guest houses, bars, andothers also sometimes participate in this market stage. The market size varies considerablydepending on the type of mineral production and the level of international demand. When productionis high and dealers have received international orders, market volume swells quickly. In typicalmining villages there can be 3 to 5 long-distance brokers and several small mine brokers. In areaswhere production is small and uncertain, there are few visible signs of the trade. This was notedduring the survey at Mabuki diamond mining village, where currently brokers do not staypermanently in the village as they used to do. Trade is still taking place, but only through occasionalvisits by brokers. On the other hand, in thriving mining towns such as Merelani there were anestimated 3000 small brokers and 50 long-distance brokers.

• ~arketlevelthree: regionalmmarkettolVDs

Regional market towns are where most mineral dealers have established permanent offices. The mainmarket for both gems and gold throughout the region is Nairobi, but several Tanzanian towns aretrying to compete and other regional towns also have a role. The centre for the Tanzanian gem tradeis Arusha, although Mtwara in the south and Dar es Salaam also serve as regional gem markets.Mwanza, and Tarime are major gold markets, and Shinyanga dominates the diamond trade. Dar esSalaam also handles some ofthe gold trade, although most of it continues to Zanzibar for export.

In such markets, the existing infrastructure and facilities allow for easy export and access to foreignbuyers. These market towns need to have good road access, airports and telecommunications, whichare essential for dealers to communicate with their international buyers. The major participants inthese markets are master dealers, brokers, organized small-scale miners. Some illegal mineral tradersthat one could qualify as full time smugglers are based here. Legitimate dealers and brokers, thosewho usually try to abide by the law, also export through Kenya on some occasions, as it is sometimesthe only way to do business. There is some specialization in the coloured gem market, particulardealers who buy mainly one type of stone. Most dealers, however, put out buy orders whenever theyhave an international buyer for a particular type of stone.

Arusha market is the major gem centre in the country handling high quality goods suitable forfaceting. Products traded include Tanzanite from nearby Merelani, tourmaline from Tanga andArusha, green garnet from Arusha and Kilimanjaro and rhodolite from Tanga, Morogoro and Arusha.

Dar es Salaam is also a secondary market of minerals in the country. This market handles the largestvariety ofproducts, minerals of various types and qualities from different mining areas of thecountry. Some of the major mineral types traded in the market are:• ruby and sapphire from Morogoro, Tanga and the southern regions;• alexandrite and chrysobel of all sizes and grades from Mtwara, Ruvuma, and Lindi;• red gamet, rhodolites, tourmaline, amethyst, emerald and aquamarine;• gold and diamonds, mainly from the central and southern zones.

Tanga was once the major gemstone centre, particularly in the early 1970s. Now the market is lessactive. It has two master dealers, neither ofwhich is very active, and a number of informal brokers.Tanga now serves as a transit point for materials from other parts of the country that are smuggledinto Kenya. Most of the minerals traded in Tanga originate from Umba valley mining area which is

13

situated in the same region. The important minerals traded in this market are sapphire, ruby and alltypes ofgarnet and tourmaline. During the survey, it was also observed that most ofthe me?iumgrade ruby from Morogoro is either marketed here or smuggled via Tanga to Kenya. SapphIre boughtin Tanga is later marketed in Dar es Salaam before it is exported, while tourmaline and garnet aremarketed through Arusha for export. The interviews conducted during the survey revealed that somegold from Singida and Dodoma is marketed in Tanga.

Mwanza is the major secondary market for minerals from the central and lake zone mining areas.Gold is the main commodity traded there. It is collected from the Regions of Singida, Shinyanga,Dodoma, Tabora, Mwanzaand Kagera. Participants estimated that 9S% of the gold is traded on theparallel market in Mwanza and later smuggled to neighbouring countries. It is sold in Nairobi,Mombasa, Nakuru, and Isibani, all Kenyan towns. Another route for gold from Mwanza is throughDar es Salaam and then Zanzibar. Soine diamonds from Mwabuki are sold in the Mwanza market andforeign diamond buyers occasionally visit the market.

Shinyanga town is famous in East Africa for t~e informal trading ofgem diamonds. Most ofthediamonds traded in this market are obtained from Maganzo mining village, including stolen materialsfrom the Mwadui diamond mine, Nyanghwale in Kahama and Mabuki in Kwimba. With theexception ofofficials sales from Mwadui Williamson Diamond Mine, most ofthe goods are fromartisanal miners and are marketed through informal channels. Field work interviews indicated thatforeign buyers obtain diamonds straight from local traders in and around Shinyanga town. Goodsfrom Shinyanga are then transported through Dar es Salaam or Mwanza and smuggled out.

Nairobi has been the main regional market for gems and gold since Tanzania attempted to nationalizemining in the 1960s. Its markets grew rapidly as mining activity increased in all countries in theregion in the 1980s an~ 1990s. Foreign buyers like it because air access is easy, dealers stock alltypes of products in good quantities, comfortable accommodations are available at reasonable prices,and their business can be done in relative security. Local sellers cited similar factors for taking theirproduce there. Prices are sometimes, but not always better. Even when they are not better, there is theadvantage that dealers will buy quickly all types and qualities of goods, so a broker can be in and outin a single day. Northern Tanzanian mining areas are geographically closer to Nairobi than to Dar esSalaam, and the road networks are considerably better. Security is reportedly a little better than inTanzania, although it is clearly better for Kenyan brokers than for Tanzanians.

Nairobi alone was estimated by one of its dealers to have about 300 active dealers. A significantnumber of them are well organized, well capitalized and have family ties in the business that spangenerations and continents. This gives them an advantage in market knowledge and contacts,something that many Tanzanian dealers lack. Some S4 major gem dealers are listed in the Nairobitelephone directory, together with eight minerals dealers. Many have multiple lines, reflecting thefact that international gem dealing requires intensive telecommunications. The Kenyan mineraldealers association had some 8S members before it became inactive a few years back. Some of themajor dealers interviewed in this study were not listed in the telephone directory, nor did theyparticipate in the dealers' association, which rends more credible the verbal estimate of300 activedealers.

In addition to a portion ofTanzania's precious minerals, Nairobi markets handle. some artisanaldiamonds and gold from Eastern Zaire, sapphires from Rwanda and smaller quantities ofgems andgold from throughout the Rift Valley area. This area, extending from Tanzania to southern Ethiopia

14

increasingly constitutes a regional market. Dealers throughout the region compete to buy theproduction, which flows wherever the trade is well organized and relatively secure. Kenya has somegem and gold mining of its own, but its main advantage has come through creating a free market forregional production. Imports are welcomed and pass untaxed, although not always without .harassment from officials. Export formalities in Nairobi are well organized, and, for establisheddealers, done on secure premises. Some Tanzanian production also goes through Mombasa, Kenya'smain coastal port.

• Market level four: Export markets

The export market is the final stage ofthe four market levels and normally it depends on the locationof transactions as well as the destinations ofthe purchased minerals. The export market can appearin several forms. The market can appear when a foreign buyer is purchasing from a dealer or duringgemstone show. Destinations of most of the mineral products has been to the processing centres,mainly in Asia, or directly to the major end users in USA, Japan and Europe.

Tanzania is presently a major new actor in international coloured gem markets, and a very small actorin world diamond and gold markets. Tanzania's garnets, sapphires, rubies, emeralds, tourmalinesmostly go to Thailand, Sri Lanka or mainland China for heat treatment and cutting. There, rubiesfrom Burma and Thailand, sapphires from Sri Lanka, Thailand and Australia, and emerald fromBrazil, Colombia, Zambia, Madagascar are co-mingled. While it is technically possible to determinethe mine origin of such stones, in practice they may be listed as being of Thai-origin in USA,Japanese, Singaporean, Hong Kong, or European jewelry markets. Lower quality market cutting atthe mass production level is increasingly being transferred from Thailand to mainland China, wherelabour costs are lower. Cutting operations also exist in India, mainly for emeralds and diamonds; inBelgium and Israel for diamonds; and on a smaller scale, in all developed countries.

Japan and Europe are the leading retail markets for top quality precious stones, including diamonds,Alexandrites and best grade Tanzanites. The US, however, is the largest market overall as massproduction and mass marketing technologies have been combined to create fine jewelry that lieswithin the reach of middle and lower-income households.

2.3 Profiles of the Participants in the Minerals Markets

The main participants in the market are mine workers, miners, brokers, informal mineral traders andmaster dealers. While the patterns described above represent typical market operations, participantsat any of the levels can and do come together and trade. Small brokers can playa role at any level. Inaddition to buying directly at the mines, there is a variety of small broker in most markets whoaccompanies the seller, helps him value his goods, and find a buyer. The roles and viewpoints of eachtype of participant in the market are described below.

2.3.1. Mine Workers

• Classification and profile

Mine workers are mainly young men from rural areas, although there are also older men, men fromurban areas and some women engaged in the actual digging. Some operate seasonally, returning totheir farms to sow and harvest their crops. Others work with targets, having in mind to get a certain

15

amount of income for a dowry or to go into business. Increasingly, however, mining is a year-roundactivity and one with an attractive career path. Successful mine workers become brokers, then dealersor mine claim holders. The may go into business in a mining related trade or service, while keeping ahand in mining. Pit and shaft mining is dirty, dangerous work. Most of the workers encountered insuch sites were men 18 to 30 years old. In alluvial mining, however, where the work is lessdangerous, one finds some women and older men participating in mining activities.

The reservation wage of these mine workers is difficult to calculate, as one would have to calculate ashadow wage based on the opportunity cost of their time and the shared costs of food a lodgingprovided by mine owners and/or more successful coworkers during the unproductive times.According to workers' testimony, however, the mine worker's position is a coveted one that a youngman must work his way into. He will work at manual labour jobs in the mining community longenough to build the savings and friendships necessary to join a mine workers' group.

We therefore took the daily wage ofa manual labourer in a mining area as a shadow reservationwage. This was found to average 2000 to 3000 TSH per day.

Mining operations ignore the existing legal framework in matters pertaining to issues like earningsand working conditions, as is the case for artisanal mining throughout the world. The rate ofaccidents at work is alarming. In Merelani informants claimed that an average ofone mine workerdies every week because of unsafe working conditions. Pit owners cannot properly superviseoperations in shaft mines because it is not safe for them to go down themselves. The pit ownersinterviewed at Merelani for example admitted that they cannot control the number ofworkers whooperate in their pits. They indicated that initially, before a pit starts to supply minerals, about 50workers ~an be operating but as soon as it starts producing, the number ofworkers in one pit caneven reach 150.

• The role of mine workers in the gemstone and gold market

Mine workers are among the main participants in the mineral market and are very active at the firststage ofthe market, as sellers at the mine sites or nearby villages. They are the primary source ofillegally traded minerals. They have an interest in getting the materials that they steal, above andbeyond their agreed shares, out of the area as quickly and quietly as possible. Mine workers were alsofound illegally mining claims which owners have left unattended for a long time. This was mainlyobserved in the Umba Valley, a sapphire mining area; Maganzo, a diamond mining area; and Sekenkeand Matinje, gold mining areas.

Sometimes mine workers are forced to sell their legitimate product to the nearest broker because theyare in need of immediate cash, for buying items like soaps, food and others. Most of the brokers arenot licensed. Many are Kenyans and could not get a license. Others, Tanzanian citizens, find thelicensing procedures too cumbersome and of little practical use. At Merelani, for example,researchers witnessed hundreds of brokers, many clearly from neighbouring Kenya, are activelybuying minerals from mine workers and taking them overland to Nairobi.

16

• Market power and size

While gold markets in Tanzania are fairly stable, gem markets are quite volatile. The value of roughgems varies so widely that few participants in the market can have a clear idea of the internationalprice a piece would bring. For all but the top gem quality material, demand for particular types ofgems within Tanzania depends on periodic orders that the major dealers receive from theirinternational buyers. Thus domestic demand is sporadic and only loosely related to internationaldemand. Therefore, while the workings of supply and demand for commodities are understood in .gold markets, participants think of gem markets in terms ofvariations in their personal bargainingpower. Bargaining is involved in all sales, and is sometimes quite lengthy process. The market sizeand power of mine workers is influenced by both the type and quality of the recovered minerals, theflow of information, and the number of buyers and sellers in the mining area. In areas where there isa free flow of market information and where buyers are many, mine workers possess market powerand also have a wide market for their products. In the Umba river mining area, for example, it wasobserved that buyers in the mining area are generally few and for certain types of minerals themarket is very thin. Hence some of the miners, through middlemen or themselves, are forced to crossthe border and look for markets outside the country. Mine workers in Umba valley mining area thinkof themselves as operating in a buyers' market with little market power.

This however, was not found to be the case in the Merelani mining area. There are thousands of bothlegal and illegal buyers at Merelani mining area. Even international buyers have ready access to thismining area and go there to buy stones. Unlike the Umba valley mining area, at Merelani there areseveral infonnal marketing centres within the mining area where both small and large brokers makedirect contact with the mine workers. These are known as 'Vijiweni,' which in Kiswahili designates astreet comer meeting place. The market volume is substantial here, driven by a surge in supply.Prices are declining rapidly, which confuses many in the mining business. For most stones a surge insupply would be a bonanza, as international demand and therefore prices are little influenced by localproduction in Tanzania. For Tanzanite, however, this is the only source and the surge in productioncaused international prices to collapse. Therefore, despite the presence of many buyers, workers inMerelani are not experiencing what they would call a sellers' market. In contrast, the sudden goldproduction in Nyangotho village in Tarime has shifted the broker's market power to the mineworkers, giving them a sense of market power.

• Mine workers' preparation for the market

Given the volatility of gem markets, participants try to adopt strategies to ensure better operation inthe market. At every level participants seek knowledge about how to value stones, and a financialcushion sufficient to let them offer their stones to several buyers. This usually requires either time ortravel. Mine workers lack market knowledge and equipment required to check the quality, weight andother chara~teristics and to assess the value of the stone. Moreover, they are usually short of cashand sometimes in debt. To a large extent, they depend on the service of the middlemen-provided byother participants in the market as elaborated in other parts of this section.

Ignorance of value assessment techniques is not a problem confined to mine workers. Theysometimes try to gain an advantage by playing on the ignorance of buyers. Neophyte buyers may begiven less time to observe the stone and duped by quality and value claims. During the survey, it wasnoted that the majority of inexperienced diamond buyers in Maganzo and Mabuki have been the

17

victims of such practice. The other strategy is to clean or oil their stones using various methods so asto improve the appearance of quality.

• Mine workers' concerns

The mine workers are not satisfied by current market arrangements. They feel that markets arelocated too far away. The fact that they cannot travel forces them to trade in the mining area marketwhich offers them less profit. Some ofthe mine workers interviewed suggested that secondarymarkets must have networks near the mining areas, either by sending their agents or opening offices,so as to reduce the number of stages and corresponding middlemen through which mineral materialspass. These mine workers however recognize the role played by the brokers and small brokers,especially in the buyers' market like Umba Valley and Mabuki.

2.3.2 Claim holders

• Classification and profIle

Claim holders are the other group of sellers at the first level of the marketing chain. Most claimholders are mature men with some capital and some standing in the community. A few earned theircapital and gained experience through mining, but many come from other sectors. A few arewomen or young men. How actively involved they are in the operation of their mines variesgreatly. Some claim holders are actively involved in the mining and marketing of their mineralswhile others sublet their titles to pit owners and financiers, who oversee the mining and marketingof the minerals produced and give commission to claim owners. It has been observed that instead ofpaying salaries to their workers, claim holders share what is produced with their workers at the endof production in such a way that they retain between 30% and 40% of the official production.

Claim holders would like to formalize their operations. Many said that the first thing they would doif they could afford it is put the workers on a salaried basis and increase security. A few claimholders with substantial working capital have been able to establish larger operations that use somemodern equipment and mining methods. In international mining parlance these would be classifiedas small-scale mining, while the hand operated mining that is more widespread is classed asartisanal.

The general pattern of mines visited on the field trips involved the use of simple tools, andsometimes primitive techniques of mining. With shovels, picks and explosives miners dig in alldirections, following hunches, indicative related mineral occurrences and actual veins. Often theresulting pits and shafts are unsafe. Multiple pits throughout an area scar the natural landscape andmercury used to refme gold compounds the environmental damage. This has especially beenobserved at Merelani and at the Maganzo and Mabuki diamond mining areas, and Misigiri andNzuguni gold mining areas.

Only a few medium-sized formal mines are operating in Tanzania. All are under foreignmanagement, although some are joint ventures with Tanzanian partners. Samax is mining graphitein Merelani, and presumably the Tanzanite that lies embedded in it, although its gem production is

18

not known. Williamson Diamond Mine has returned to production as an Anglo Am.ericansubsidiary. A few joint ventures in coloured gems also exist.

• The role of claim holders in the marketing of mineral products

Claim holders play an important role in the mineral market. They are the main sellers to masterdealers. Some miners are also master dealers so they export their products directly without passingthrough brokers. These are the major suppliers to the official market. This, however, does not meanthat all that is possessed by the miners is sold in the official market. The marketing route issometimes determined by those who support their production. Claim holders who receive substantialfinancial assistance either from local master dealers or Kenyan or other foreign dealers are expectedto sell their products to those who contribute in one way or another during production. This is themain· reason that miners may sell outside the official market. When the claim holders receivefmancial assistance from smugglers or master dealers located outside the country, they are generallyobliged to sell to the unofficial market.

In terms of market information, it was observed that these participants at least possess relevantinformation on the market situation, unlike the mine workers. Market information is a valuable assetwhich is normally exchanged at cost. Some miners assist their workers by providing them withinformation or a market for their stones. How closely mine owners are able to supervise their minesaffects how much of the production they actually see and market. When they are lax and have notrustworthy supervisor in the mine itself, only a small amount of their real production remains forthe official market.

• Preparation for the market

Claim holders' access to market information and ability to market their produce effectively varieswidely. Miners need to cobble, clean and sort their stones by size, shape and quality. In the case ofgold, they purify the ore to accepted market standards. The small-scale gem claim holders generallysell to local dealers, so their information needs and preparation of stones for market are limited. Thefew who are themselves dealers have to meet much stricter standards of sorting for the exportmarket. Organized claim holders have facilities necessary for preparing their mineral products formarketing. Gold miners use mercury retorts, and gem miners gemological testing kits, and weighingtools.

• Claim holders' costs

The cost of claim holders can be divided into marketing and production costs. Marketing costs differamong the claim holders depending on how they handle their marketing. Claim holders who sellthrough brokers pay them a commission, normally 10 percent of the sale price. Those who do theirown marketing have the same costs as brokers, mainly transportation and the opportunity cost oftheir own time. Those who commute between mining areas and market towns in any case, oftenmaintain a home with telephone and/or office facilities in town for their mining or other businesses.They probably do better by doing their own marketing, but no one keeps adequate accounts todetermine this. It may be mainly a psychological effect, as the unpredictable nature of preciousminerals sales creates mistrust and a strong incentive to retain personal control.

19

Apart from the marketing costs, claim holders also face production costs. This again differs amongthe claim holders depending on the type of mining operation. Small-scale miners in alluvial areasincur less costs than pit and shaft mining operations. Their main costs are labor, transportation andtheir own accommodations in mining areas, often a guest house. Again accounting systems arevirtually unknown, so hard figures could be gleaned only through long, intensive survey research.The only figure commonly known is the amount of start-up capital one'needs to go into a particularline of work in mining. For alluvial mine claim holders, start-up capital was estimated at aboutTSH.5oo,OOO. Small scale claim holders with semi-mechanized operations mining undergroundneed substantially more. At Merelani, it was possible to get some estimates on the production costs.According to the interviews there it was noted that where the Tanzanite occurs fairly close to thesurface, one could start production with a minimum of TSHIO million. In areas such as the recentlyopened block B where production requires a shaft mining down to about 200 m, between TSH50100 million are required. These costs of production have implications in the marketing process.When such costs are high, they affect both the volume and price of the production. The aircompressors and excavation equipment required are imported from abroad. Claim holders complainthat no local dealer provides them, and no credit is available for their purchase. All infonnantsagreed that it would be better to have shops selling mining equipment locally.

• Claim holders' concerns

High operating costs for mining, lack ofa reliable market, and unpredictable prices are among thepriority concerns of claim holders. Others are a lack of financial support from formal sources and aninappropriate tax regime, which they regard as offering little incentives for them to expand theproduction and marketing oftheir minerals.

2.3.3 Brokers

• Classification and profile

Many types of brokers participate in the minerals markets. Those who buy in mining areasor villagesand sell in secondary market towns are considered dealers by the law. Sometimes they are using theirown capital, but often they are collection agents for master dealers based in town, buying with thedealer's capital or not paying the seller until the stone is sold. They are granted a different type oflicense from master dealers, who are authorized to export. It is customary, however, to refer to them asbrokers, and in fact the roles of one type of broker or dealer may vary from one transaction to another.

The other main type of small brokers are really commission agents, guiding sellers to buyers inexchange for a 10 percent commission from the seller. Sometimes they collect another 5-10% from thedealer, if they come by after the sale and the dealer agrees that it was a good deal. These brokers maytransport the goods for the seller, but they do not actually buy the stones as they have insufficientcapital. Such commission.agent brokers operate both in the mining areas and in the secondary markettowns. None are licensed, as this type of work is not recognized by the law. The fact that the practiceis so widespread, however, is evidence that their services are badly needed.

Licensing is very limited among dealers and brokers not involved in overseas exports, in part becausecurrent regulations were designed without taking into account·how they operate. In Arusha alone,

20

active brokers are estimated between 3,000 to 4,000, ofwhich only 100 are licensed. The Governmentso far has not put into place regulations to formalize the activities of gold brokers.

Brokers can also be classified on the basis of nationality, i.e., Tanzanian and non-Tanzanian brokers.It was found during the interviews that there are many foreigners who are active in the mineral market,mainly acting as brokers. Most of these are acting for dealers who are based in their country oforigin.Most of them are Kenyans. At Merelani, it is estimated thatover 500 Kenyan brokers are based there.They can pass themselves off as Tanzanians, as they come from ethnic groups living on both sides ofthe border, namely Masai, Luo, Kamba, Taiga, and Kurya. Sometimes are known personally to befrom Kenyan villages, others can be recognized by their accent. Since English is the national languagein Kenya and is used in the schools, whereas in Tanzania Kiswahili plays that role, Kenyans aresometimes informally recognized by the fact that their English is better.

It is also possible to categorize brokers in terms of the size of their working capital as large, medium,and small.

(i) Small-scale brokers

These are small traders operating within the mining areas and mostly serving the middleman's roleof linking various participants in the market. Sometimes they are hired by medium scale brokersfrom urban centres to act as informers or/and security personnel. Most of these have workingcapital ranging between TSH.I0,000 and TSH. 50,000. There were about 3,000 total villagebrokers at Merelani trading markets. About 500 of these were foreigners, passing as Tanzanians,mostly Masai and Luo. The other important centre at which these small scale brokers are found is intown especially in areas where master dealers are found. In Arusha for example such brokers gatherat the OTTU building, where many miners and dealers have offices.

There are fewer small brokers in gold compared to gemstones. In most of the gold mining areasvisited, the number of small brokers ranged between 10-35 depending on the intensity of miningproduction. They work mainly as collection agents, buying for dealers.