geisinger health system - healthcare financial management ... · pdf file– manage:...

TRANSCRIPT

1

11Timothy Fitzgerald, CFA, FHFMA

Vice President, Treasury Management

2

Geisinger Health SystemAn Integrated Health Services Organization

Physicians & Providers

$1.1 Billion~1,300 Physicians

~800 Advanced Practitioners

~520 Fellows

~425 Med Students

~215 clinic sites

Healthcare Facilities

$3.1 Billion7 Acute Hospitals

8 Surgery Centers

2 Nursing Homes

Home Health & Hospice

Managed Care

$2.4 Billion~500,000 members

Diversified Products

Public/Private Exchanges

~56,000 contracted providers

Budget Year 2016 $ & Statistics

2

4

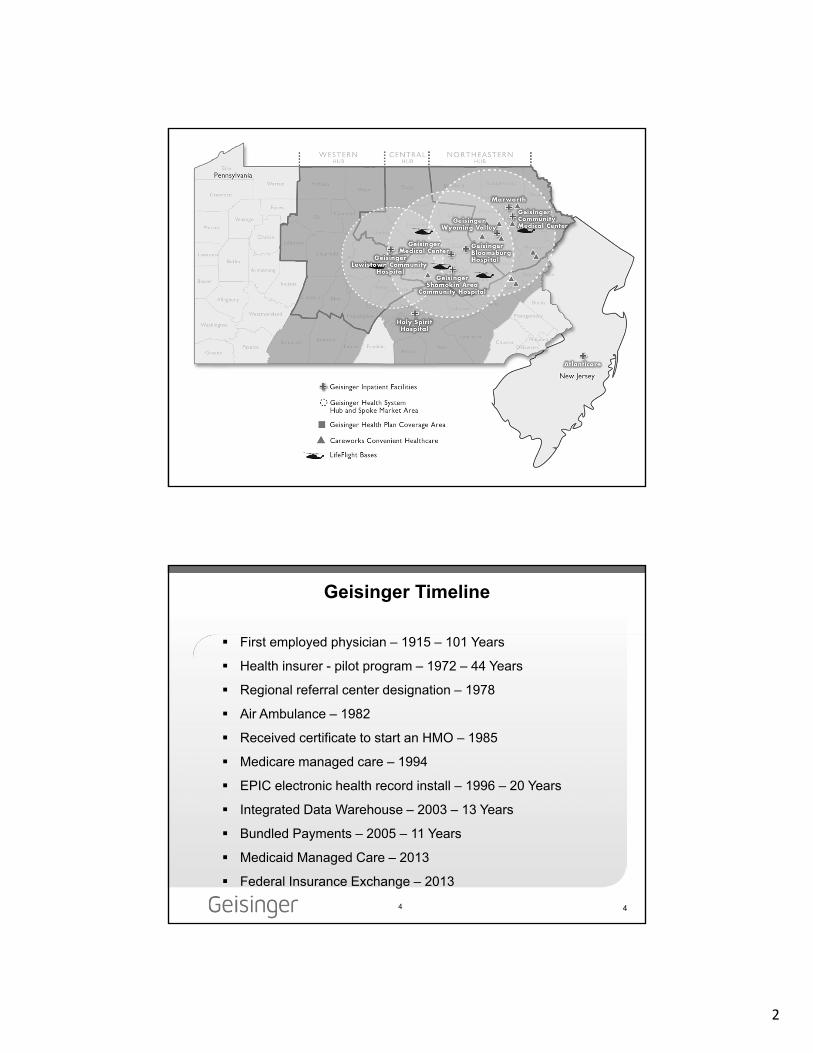

Geisinger Timeline

First employed physician – 1915 – 101 Years

Health insurer - pilot program – 1972 – 44 Years

Regional referral center designation – 1978

Air Ambulance – 1982

Received certificate to start an HMO – 1985

Medicare managed care – 1994

EPIC electronic health record install – 1996 – 20 Years

Integrated Data Warehouse – 2003 – 13 Years

Bundled Payments – 2005 – 11 Years

Medicaid Managed Care – 2013

Federal Insurance Exchange – 2013

4

3

5

StrategyA Proven Patient Experience

Clinic:

– Deliver complex care close to the patient – “Right Care”– Large multispecialty, ambulatory sites capture increasing

outpatient activity

Hospitals:

– Grow high-acuity service lines – stop outmigration– Distill lower acuity to outpatient facilities or local community

hospitals

Health Plan:

– Change health outcomes with innovative care management –ex./ ProvenHealth Navigator® (advanced medical home)

– Differentiated from traditional arbitrage model of insurance– Efficient underwriting and product diversification

6

Transforming Healthcare with Technology

Fully-integrated Electronic Health Record

Patient Portal: ~270,000 users (37% of patients)– Patient self-service

– Home monitoring integrated with Medical Home

“Outreach Health IT” to Non-Geisinger Providers– 10,221 users in 865 non-Geisinger practices

– Remote support for regional ICUs (eICU®)

– Telestroke services to regional EDs (eHealth)

Regional Health-Information Exchange (KeyHIE)– 22 hospitals, 175 practices, 1.1M patients

“Most Wired” for 13 consecutive years

4

7

Genomics

Bio-bank - consented DNA samples 98,000 patients

Regeneron® partnership– World’s most comprehensive genotype-phenotype resource

– Goal: sequence 250,000 patients DNA (50,000 completed)

– Aid drug development and genomic medicine

– Sequenced at no cost to Geisinger

Data warehouse linked to EHR & health plan data

Stable market area population

MyCode® Community Health Initiative - health research

GenomeFIRST Medicine– Treatment and prevention before symptoms

– Physicians and counselors trained to act on results

8

Geisinger GenomeFIRST Genomic Medicine

27 common conditions found in GenomeFIRST

Example– Familial Hypercholesterolemia (FH) early-onset coronary artery

disease and stroke

– Affects > 1 million people and <1% realize it

– Prevalence: 1 in 175, much higher in hereditary family

– 20-fold increase in heart attack, 20% of those before age 45

Goals– Diagnose: 500 cases in MyCode participants/family (1-3 years)

– Manage: Aggressive cholesterol management (1-3 years)

– Population Health: Sustainable decrease in heart attacks in people under 60 in our service area (10-15 years)

5

9

ProvenCare® Acute Episodic Bundles

CAB and PCI

Bariatric Surgery

PerinatalSurgical Mgmt. of

Lung Cancer

Hip: Fragility Fracture or

Arthroplasty

Heart Failure

Lumbar Spine

• Clinical Best Practices

• Workflow Process Redesign

• Convener for CMMI Bundling Initiative (7 organizations)

• Corporate Destination Medicine Option

• Clinical Best Practices

• Workflow Process Redesign

• Convener for CMMI Bundling Initiative (7 organizations)

• Corporate Destination Medicine Option

COPDTotal Knee Arthroplasty

See Reference to New York Times Articles and other press coverage in Appendix, Exhibits A and D

10

Population HealthProvenHealth Navigator®

Health Affairs: 4/26/2015.

6

11

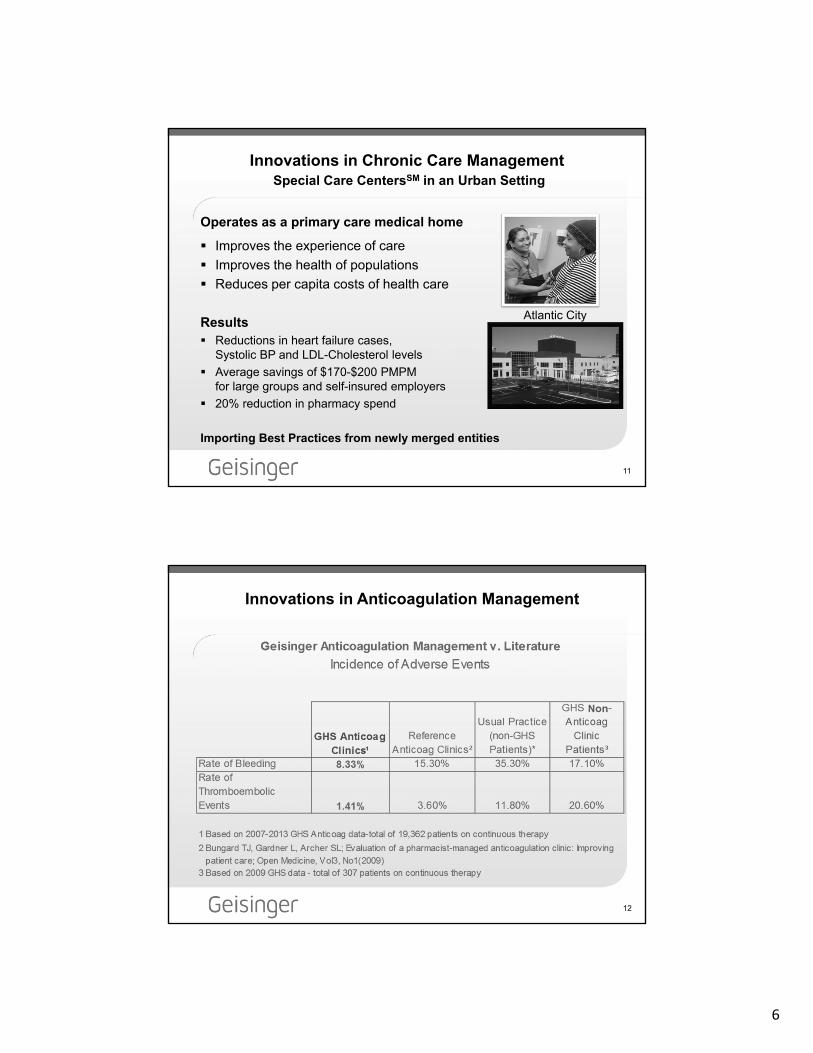

Innovations in Chronic Care ManagementSpecial Care CentersSM in an Urban Setting

Operates as a primary care medical home

Improves the experience of care

Improves the health of populations

Reduces per capita costs of health care

Results Reductions in heart failure cases,

Systolic BP and LDL-Cholesterol levels

Average savings of $170-$200 PMPMfor large groups and self-insured employers

20% reduction in pharmacy spend

Importing Best Practices from newly merged entities

Atlantic City

12

Innovations in Anticoagulation Management

7

13

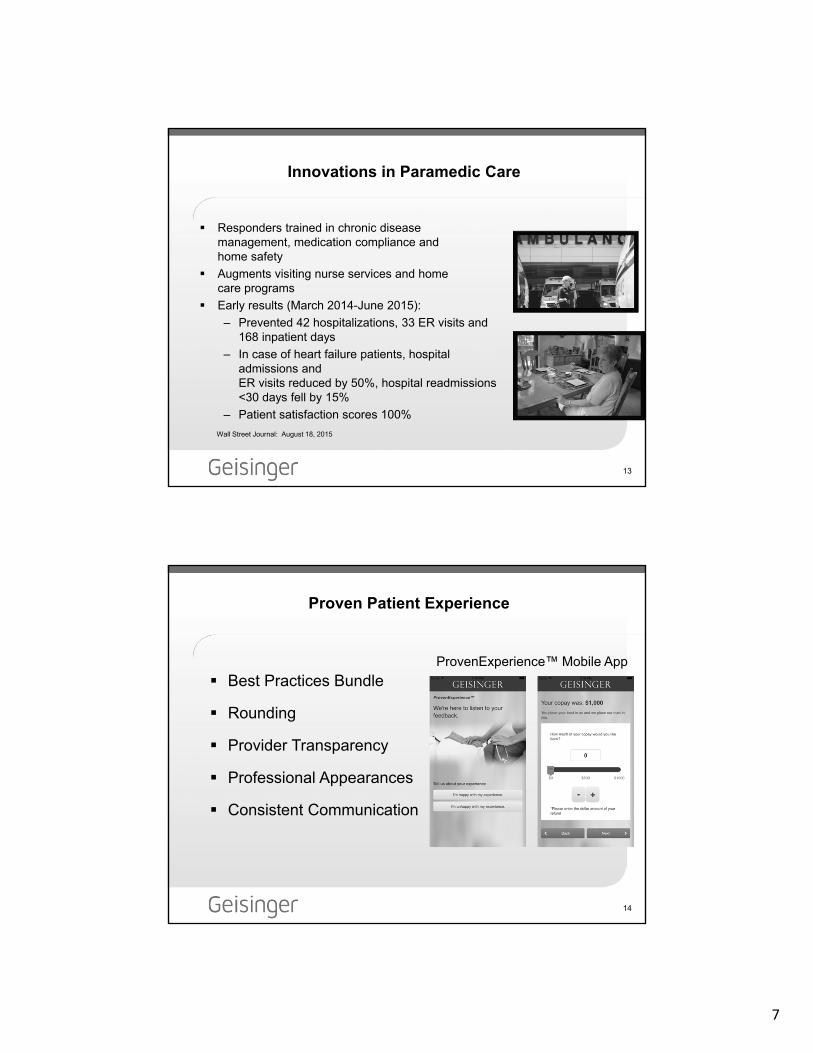

Innovations in Paramedic Care

Wall Street Journal: August 18, 2015

Responders trained in chronic diseasemanagement, medication compliance andhome safety

Augments visiting nurse services and home care programs

Early results (March 2014-June 2015):

– Prevented 42 hospitalizations, 33 ER visits and 168 inpatient days

– In case of heart failure patients, hospital admissions and ER visits reduced by 50%, hospital readmissions <30 days fell by 15%

– Patient satisfaction scores 100%

14

Proven Patient Experience

Best Practices Bundle

Rounding

Provider Transparency

Professional Appearances

Consistent Communication

ProvenExperience™ Mobile App

8

15

Patient Satisfaction Transparency

16

Mergers and Acquisitions Progress Report

Geisinger-Shamokin and Geisinger-Bloomsburg (2012)

– Low cost delivery platforms aligned with GMC

Geisinger-Community Medical Center (2/2012)

– Major facility expansion, completed

– Physician integration

Geisinger-Lewistown Hospital (11/2013)

– Extensive administrative/clinical integration

Holy Spirit Health System (10/2014)

– Integration and population health planning underway

AtlantiCare Health System (10/2015)

– Debt restructured

9

17

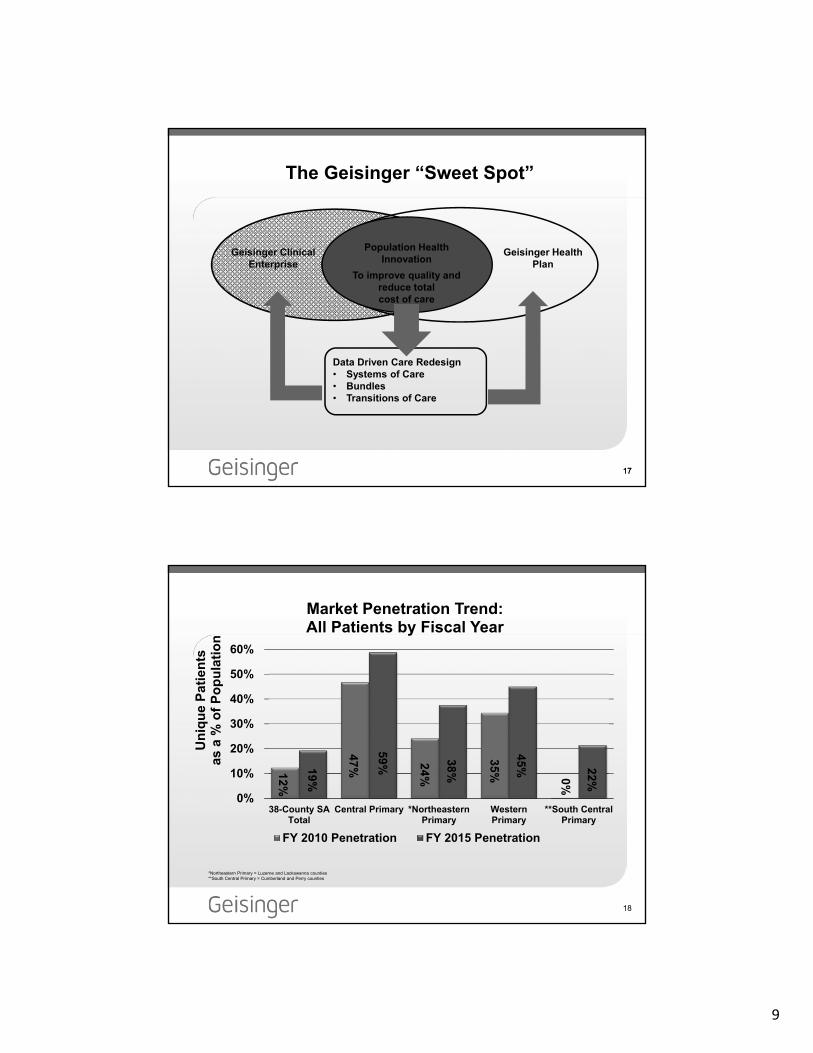

Geisinger Clinical Enterprise

Geisinger Health Plan

Data Driven Care Redesign• Systems of Care• Bundles• Transitions of Care

Population Health Innovation

To improve quality and reduce total cost of care

The Geisinger “Sweet Spot”

17

18

12%

47% 24%

35% 0%

19%

59% 38%

45% 22%

0%

10%

20%

30%

40%

50%

60%

38-County SATotal

Central Primary *NortheasternPrimary

WesternPrimary

**South CentralPrimary

Un

iqu

e P

atie

nts

as a

% o

f P

op

ula

tio

n

Market Penetration Trend:All Patients by Fiscal Year

FY 2010 Penetration FY 2015 Penetration

*Northeastern Primary = Luzerne and Lackawanna counties**South Central Primary = Cumberland and Perry counties

10

19

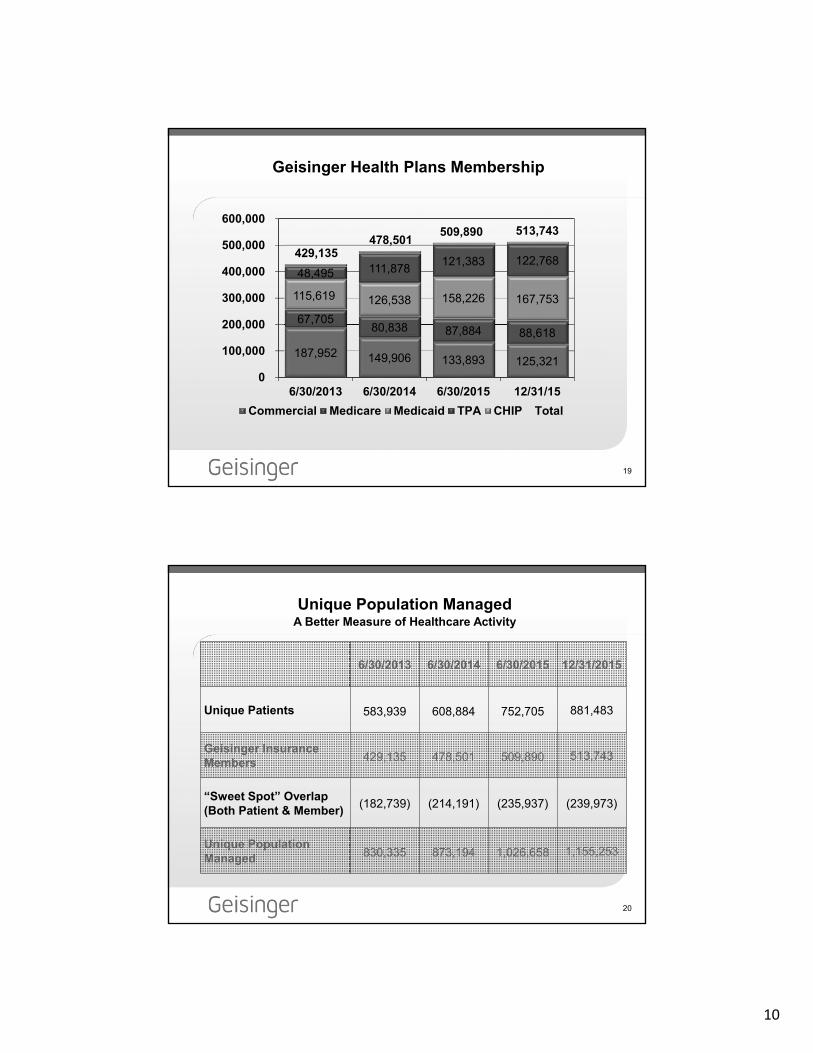

187,952 149,906 133,893 125,321

67,70580,838 87,884 88,618

126,538 158,226 167,753

48,495 111,878121,383 122,768

429,135478,501

509,890 513,743

0

100,000

200,000

300,000

400,000

500,000

600,000

6/30/2013 6/30/2014 6/30/2015 12/31/15

Commercial Medicare Medicaid TPA CHIP Total

Geisinger Health Plans Membership

115,619

20

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Unique Patients 583,939 608,884 752,705 881,483

Geisinger Insurance Members 429,135 478,501 509,890 513,743

“Sweet Spot” Overlap(Both Patient & Member)

(182,739) (214,191) (235,937) (239,973)

Unique Population Managed 830,335 873,194 1,026,658 1,155,253

Unique Population ManagedA Better Measure of Healthcare Activity

11

21

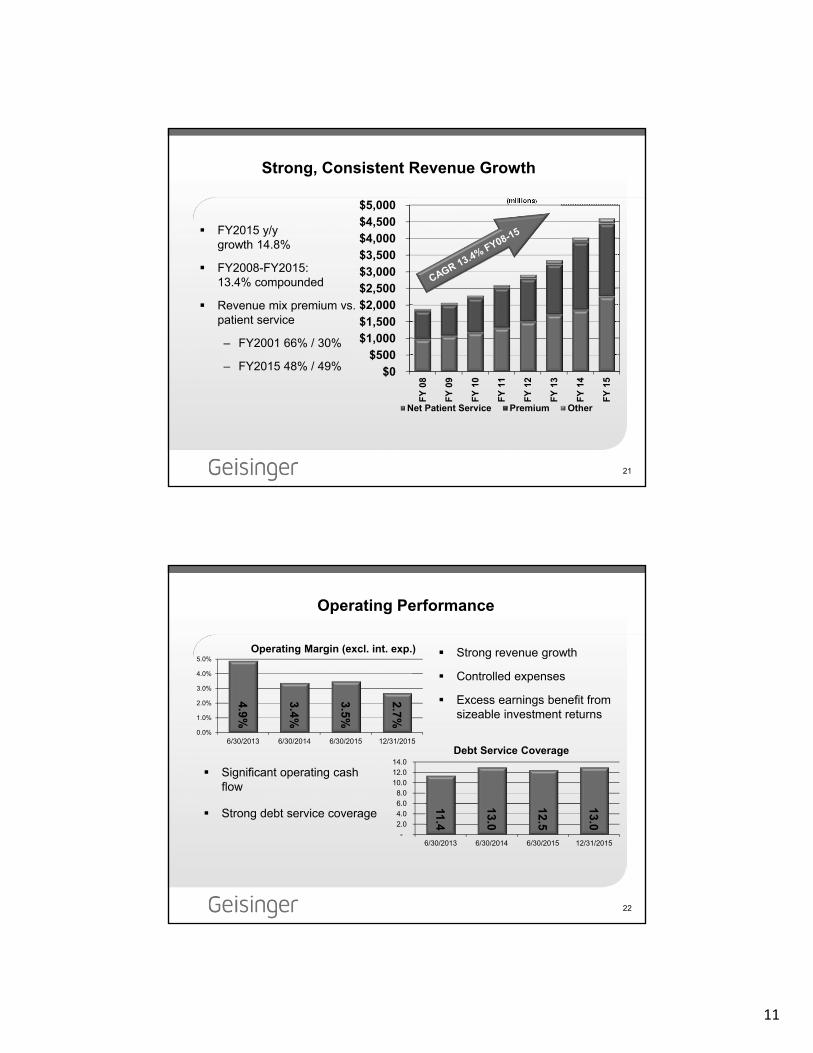

Strong, Consistent Revenue Growth

FY2015 y/y growth 14.8%

FY2008-FY2015: 13.4% compounded

Revenue mix premium vs. patient service

– FY2001 66% / 30%

– FY2015 48% / 49% $0$500

$1,000$1,500$2,000$2,500$3,000$3,500$4,000$4,500$5,000

FY

08

FY

09

FY

10

FY

11

FY

12

FY

13

FY

14

FY

15

Net Patient Service Premium Other

(millions)

22

Operating Performance

Significant operating cash flow

Strong debt service coverage

4.9%

3.4%

3.5%

2.7%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Operating Margin (excl. int. exp.)

11.4

13.0

12.5

13.0

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Debt Service Coverage

Strong revenue growth

Controlled expenses

Excess earnings benefit from sizeable investment returns

12

23

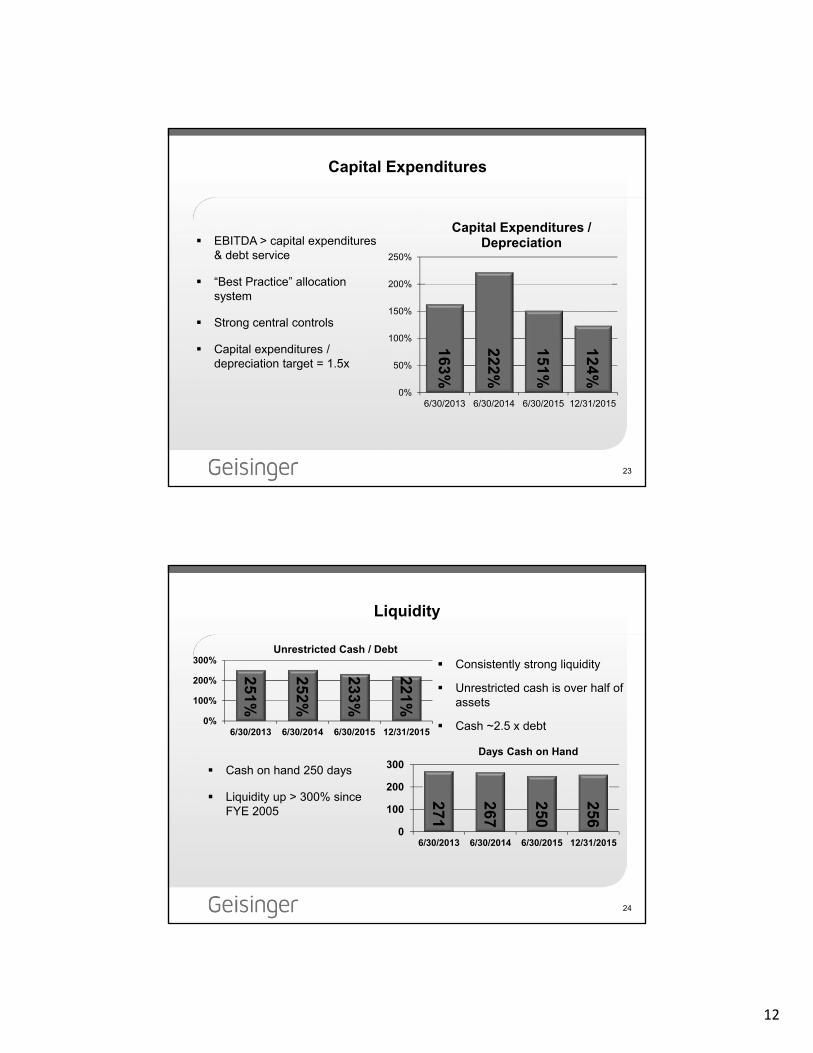

Capital Expenditures

EBITDA > capital expenditures & debt service

“Best Practice” allocation system

Strong central controls

Capital expenditures / depreciation target = 1.5x

163%

222%

151%

124%

0%

50%

100%

150%

200%

250%

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Capital Expenditures / Depreciation

24

Liquidity

Cash on hand 250 days

Liquidity up > 300% since FYE 2005

251%

252%

233%

221%

0%

100%

200%

300%

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Unrestricted Cash / Debt

271

267

250

256

0

100

200

300

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Days Cash on Hand

Consistently strong liquidity

Unrestricted cash is over half of assets

Cash ~2.5 x debt

13

25

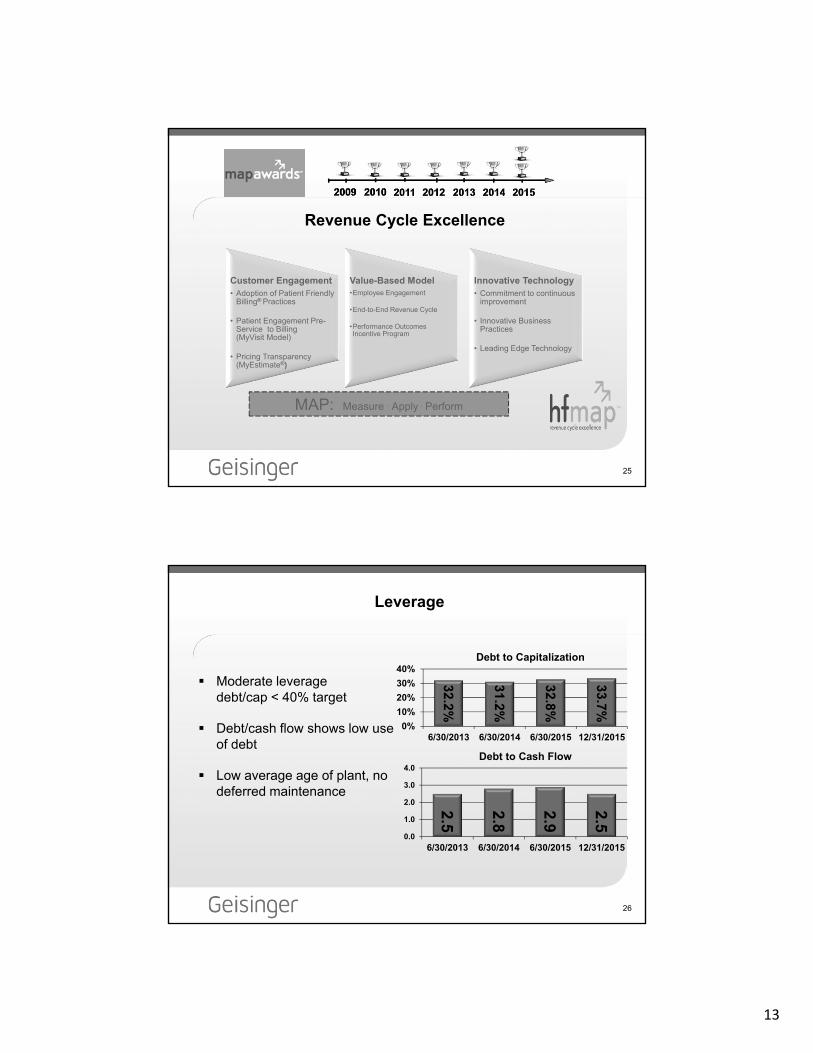

Revenue Cycle Excellence

Customer Engagement• Adoption of Patient Friendly

Billing® Practices

• Patient Engagement Pre-Service to Billing (MyVisit Model)

• Pricing Transparency (MyEstimate®)

Value-Based Model•Employee Engagement

•End-to-End Revenue Cycle

•Performance Outcomes Incentive Program

Innovative Technology• Commitment to continuous

improvement

• Innovative Business Practices

• Leading Edge Technology

MAP: Measure . Apply . Perform

26

Leverage

Moderate leverage debt/cap < 40% target

Debt/cash flow shows low use of debt

Low average age of plant, no deferred maintenance

32.2%

31.2%

32.8%

33.7%

0%

10%

20%

30%

40%

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Debt to Capitalization

2.5

2.8

2.9

2.5

0.0

1.0

2.0

3.0

4.0

6/30/2013 6/30/2014 6/30/2015 12/31/2015

Debt to Cash Flow

14

27

AtlantiCare Debt Restructuring

Purpose: Conform terms with all other Geisinger debt

Refinanced: $224 million, ARMC tax-exempt bonds– ARMC Series 2007 Bonds defeased to 7/2017 call date

– ARMC Series 2012A, 2012B & 2014 Bond refinanced

Funded by $339 million, Geisinger Series 2015 Bonds– No new proceeds

– Refinanced all ARMC Bonds

– Refinanced $115 million, Geisinger Series 2009 B & C Bonds

– All under Geisinger Master Trust Indenture

Other AtlantiCare debt of $29 million restructured or repaid

28

Debt Mixas of 12/31/2015

$ in 000s

40.4%

47.4%

12.2%

Variable / Fixed Debt Mix

Effective Variable Natural Fixed

Synthetic Fixed

$342,300 , 23.7%$1,099,165 ,

76.3%

Committed Debt v Puttable$000’s

Puttable Committed

Liquid investments to puttable debt = 10.4x

15

29

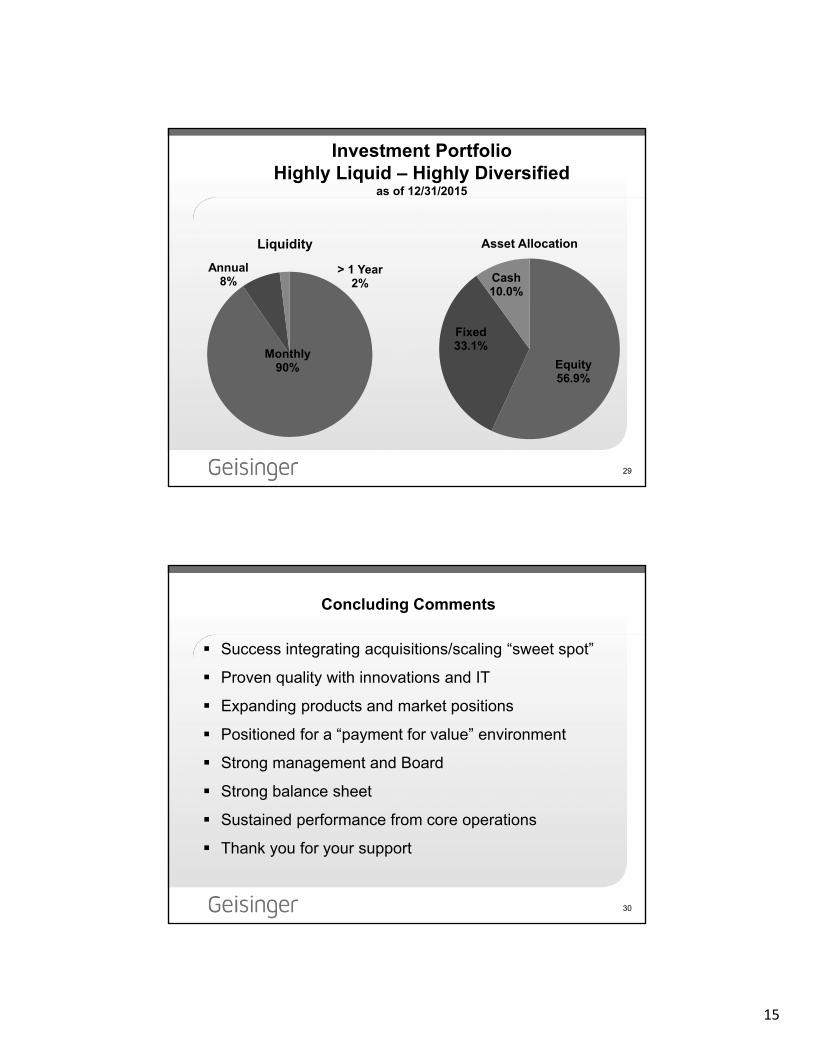

Investment PortfolioHighly Liquid – Highly Diversified

as of 12/31/2015

Monthly90%

Annual8%

> 1 Year2%

Liquidity

Equity56.9%

Fixed33.1%

Cash10.0%

Asset Allocation

30

Concluding Comments

Success integrating acquisitions/scaling “sweet spot”

Proven quality with innovations and IT

Expanding products and market positions

Positioned for a “payment for value” environment

Strong management and Board

Strong balance sheet

Sustained performance from core operations

Thank you for your support