gbi asia-pacific launch presentation

TRANSCRIPT

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

GBI Asia-Pacific Launch Presentation

SEPTEMBER 2020

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Change and continuity

We normally start to think about what we’re going to cover in the GBI launch presentations at the start of the year, and this year was really no different. Though we envisaged focusing on an attitudinal segmentation for 2020, COVID-19 has inevitably become the main focus.

However, some things have not changed, including the reasons why this audience is so important and how we’re providing you with more insight, so you better understand how to reach, communicate and engage this audience.

2

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Who are the Global Business Influencers?

The GBI survey reaches senior business people in companies with 50+ employees. By definition the Global Business Influencers are a very niche group representing less than 1% of the population.

But as we’ll see, taking into account their influence, spending power and the corporate budgets they control, they are a disproportionately important audience for B2B marketers and represent the key to profitability for sectors such as: finance, luxury goods and cars, airlines, and hotels.

We speak to over 13,200 Global Business Influencers in 30 markets, across Africa, APAC, Europe, the Middle East and the US.

They’re a fascinating and valuable audience who we want to be able to help you to better understand.

3

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Giving you more insight

To bring you the most valuable insights, every year we make developments to the survey. For 2020, we’ve upped the bands in luxury to reach those high end purchasers of luxury watches, jewellery, arts and antiques, and consumer electronics.

4

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Giving you more insight

To help create more granular influencer targets, we’re asking the GBI whether they’ve spoken at an industry event or a conference, published a book or research paper, or have been interviewed in the press while representing their company.

5

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Giving you more insight

This year we’re also linking the main survey (run amongst 13,200 GBI’s) with the Barometer survey, which asks additional questions among 1,000 respondents.

6

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Giving you more insight

This will give you:

• Easier to access insights – more data, all in the same place.

• Richer insights – providing the potential to cross analyse data from the different surveys. For example, answering questions such as ‘how do a CEO’s business challenges differ to that of a CTO/CIO?’ and ‘what are the luxury purchase drivers for those intending to purchase a watch worth US$20,000 or more?’

7

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Giving you more insight

To help humanise the audience, we’ve re-visited all our attitudinal statements on the survey and created a segmentation.

We have attitudes set up around a variety of areas including: globalisation, travel, leadership, luxury, technology, social responsibility, wealth, environment and exploration.

8

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

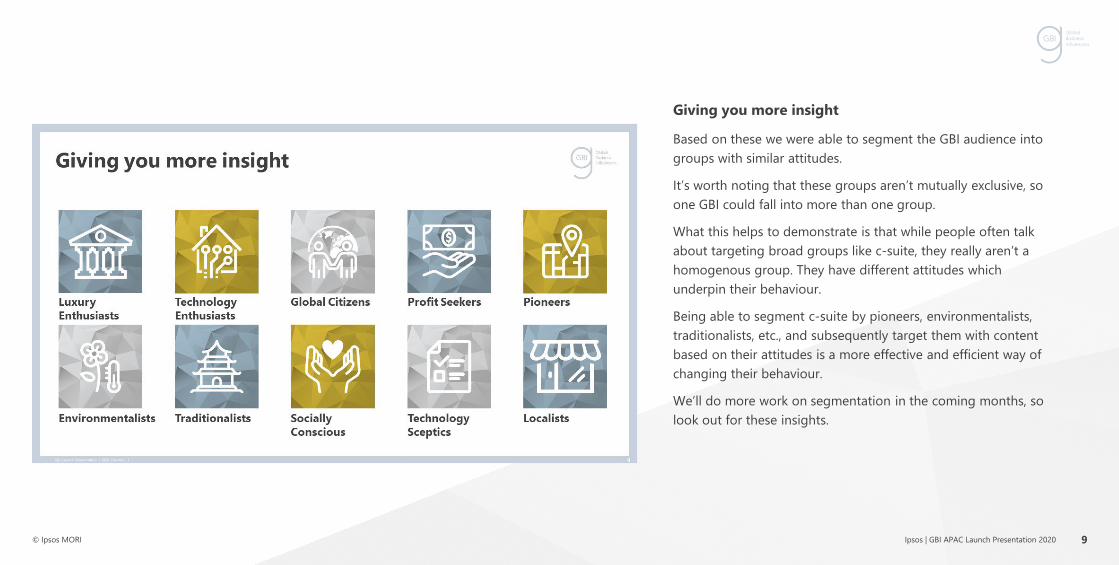

Giving you more insight

Based on these we were able to segment the GBI audience into groups with similar attitudes.

It’s worth noting that these groups aren’t mutually exclusive, so one GBI could fall into more than one group.

What this helps to demonstrate is that while people often talk about targeting broad groups like c-suite, they really aren’t a homogenous group. They have different attitudes which underpin their behaviour.

Being able to segment c-suite by pioneers, environmentalists, traditionalists, etc., and subsequently target them with content based on their attitudes is a more effective and efficient way of changing their behaviour.

We’ll do more work on segmentation in the coming months, so look out for these insights.

9

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

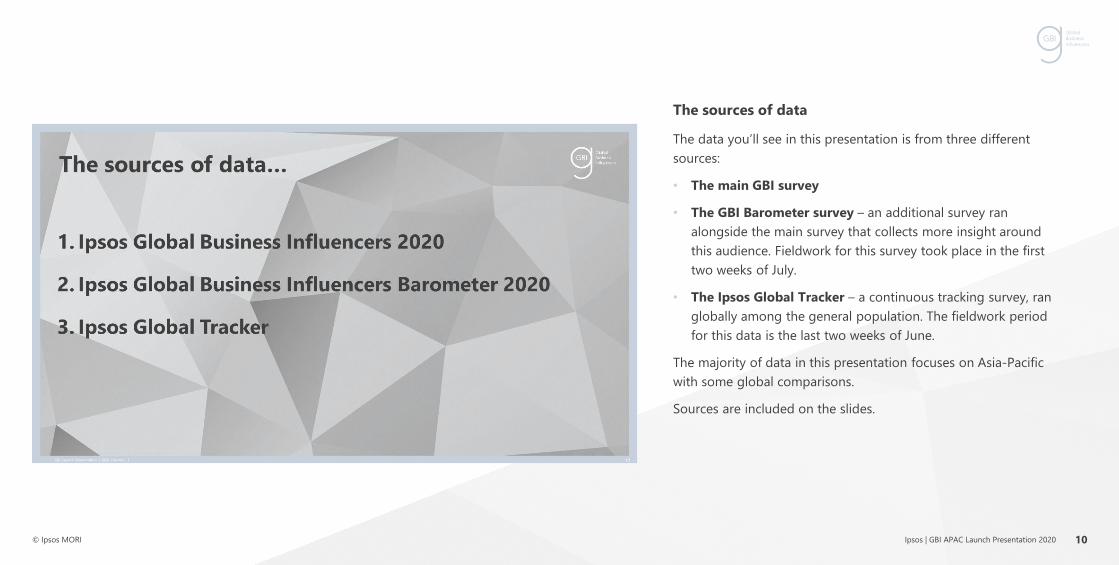

The sources of data

The data you’ll see in this presentation is from three different sources:

• The main GBI survey

• The GBI Barometer survey – an additional survey ran alongside the main survey that collects more insight around this audience. Fieldwork for this survey took place in the first two weeks of July.

• The Ipsos Global Tracker – a continuous tracking survey, ran globally among the general population. The fieldwork period for this data is the last two weeks of June.

The majority of data in this presentation focuses on Asia-Pacific with some global comparisons.

Sources are included on the slides.

10

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

COVID-19: A diverse challenge

The past few months have been dominated by COVID-19 and this has bought around a set of new and diverse challenges. It’s affected us all in different ways, and the full implications are yet to be realised (especially with second and third waves anticipated in some markets).

This presentation explores what the Global Business Influencers think about COVID-19, the challenges it’s created for them, and how they’ve adapted both in their business and personal lives. As the more you know about them, the more effectively you can communicate with this influential audience.

11

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

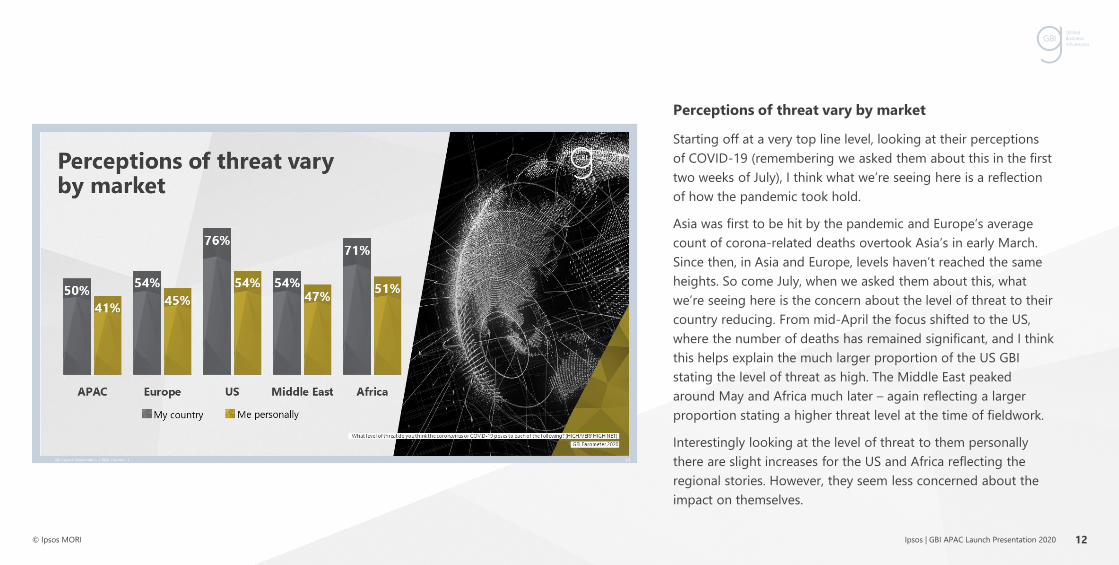

Perceptions of threat vary by market

Starting off at a very top line level, looking at their perceptions of COVID-19 (remembering we asked them about this in the first two weeks of July), I think what we’re seeing here is a reflection of how the pandemic took hold.

Asia was first to be hit by the pandemic and Europe’s average count of corona-related deaths overtook Asia’s in early March. Since then, in Asia and Europe, levels haven’t reached the same heights. So come July, when we asked them about this, what we’re seeing here is the concern about the level of threat to their country reducing. From mid-April the focus shifted to the US, where the number of deaths has remained significant, and I think this helps explain the much larger proportion of the US GBI stating the level of threat as high. The Middle East peaked around May and Africa much later – again reflecting a larger proportion stating a higher threat level at the time of fieldwork.

Interestingly looking at the level of threat to them personally there are slight increases for the US and Africa reflecting the regional stories. However, they seem less concerned about the impact on themselves.

12

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

GBI more concerned about personal threat

But, in comparison to the general population their views do differ. Though we might have expected the reverse given the GBI’s wealth, access to health services, ability to get away, etc., the GBI are more personally concerned about the threat than the general population.

Ultimately, we all have worries – we’re all human – and there has been plenty written about money not resolving all problems. The GBI are going to be more knowledgeable about the situation and the outlook for the future. So, concerns they have regarding the health risks of COVID-19 might be amplified and possibly they’re concerned about the impact on their personal wealth.

13

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

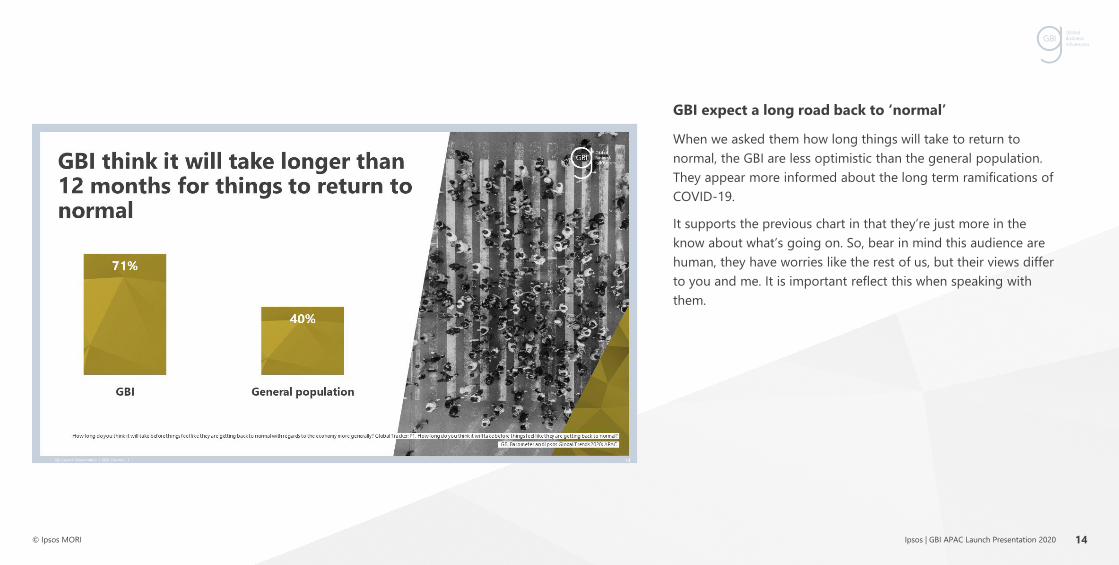

GBI expect a long road back to ‘normal’

When we asked them how long things will take to return to normal, the GBI are less optimistic than the general population. They appear more informed about the long term ramifications of COVID-19.

It supports the previous chart in that they’re just more in the know about what’s going on. So, bear in mind this audience are human, they have worries like the rest of us, but their views differ to you and me. It is important reflect this when speaking with them.

14

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

There is a long road ahead for the economy in Europe

Over the next 12 months, almost 60% say the economic condition of their country will not improve., which is similar to Europe.

Interestingly the US GBI are much more bullish, potentially reflecting the recent NASDAQ performance. In the US, 65% think things will improve over the next 12 months vs 39% in Asia. We need to take into account these differing regional views in global ad campaigns and bear in mind the stage in which countries are at in the COVID-19 pandemic.

15

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

There is a long road ahead for their business

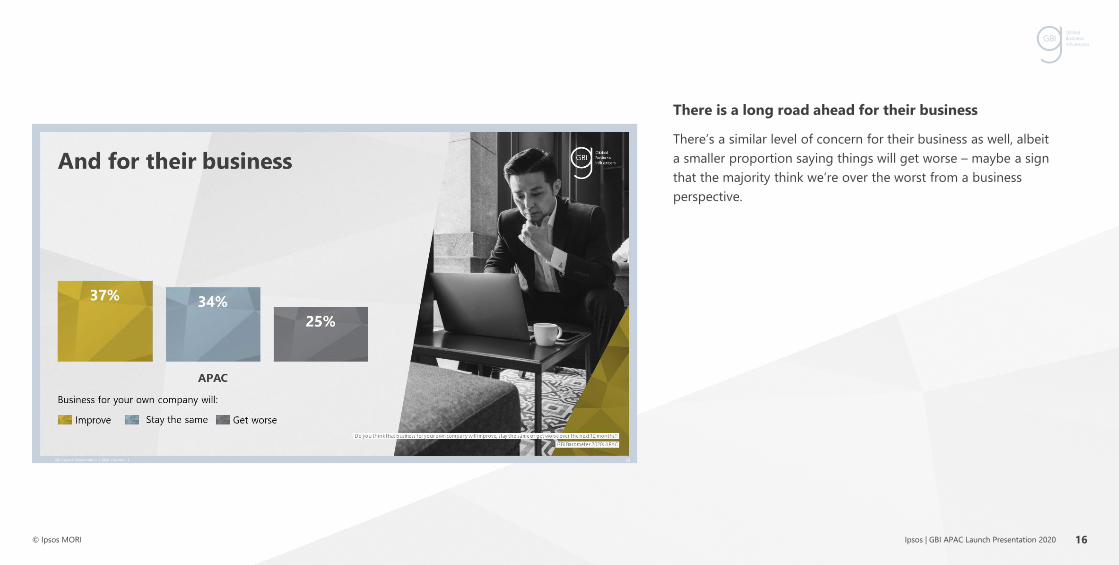

There’s a similar level of concern for their business as well, albeit a smaller proportion saying things will get worse – maybe a sign that the majority think we’re over the worst from a business perspective.

16

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

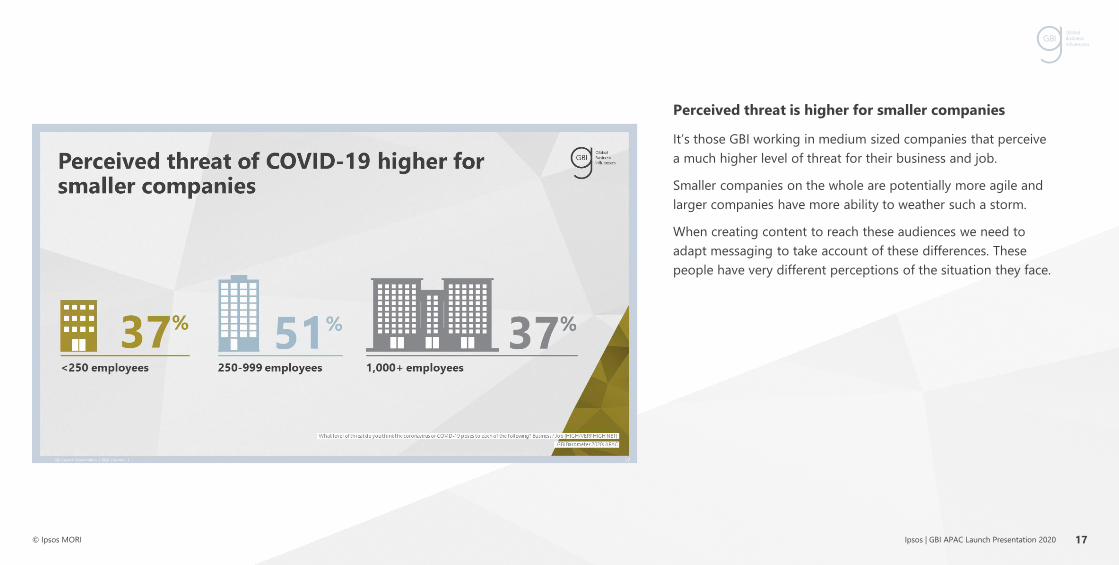

Perceived threat is higher for smaller companies

It’s those GBI working in medium sized companies that perceive a much higher level of threat for their business and job.

Smaller companies on the whole are potentially more agile and larger companies have more ability to weather such a storm.

When creating content to reach these audiences we need to adapt messaging to take account of these differences. These people have very different perceptions of the situation they face.

17

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

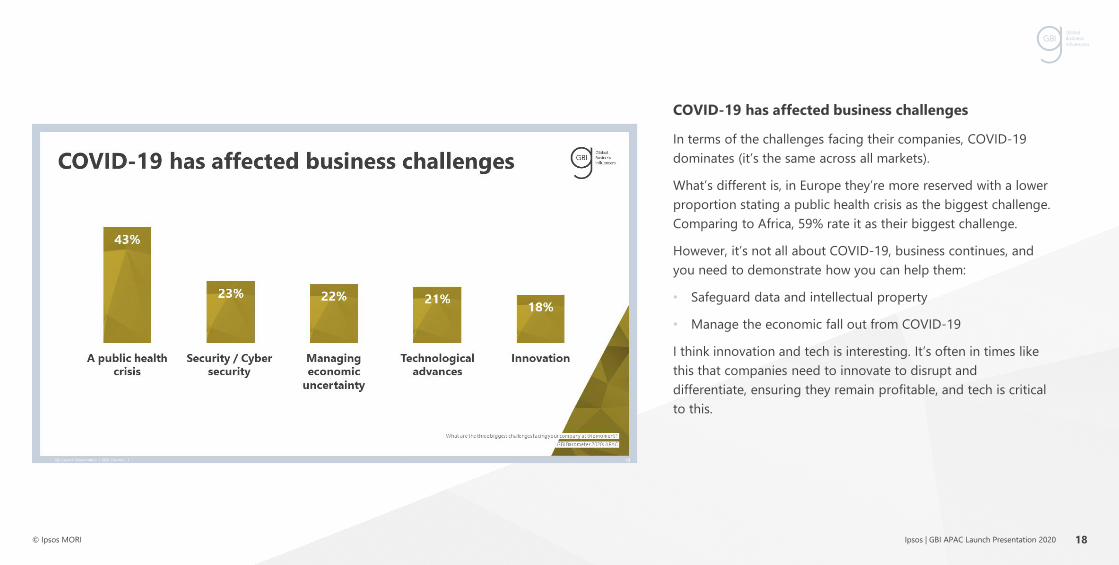

COVID-19 has affected business challenges

In terms of the challenges facing their companies, COVID-19 dominates (it’s the same across all markets).

What’s different is, in Europe they’re more reserved with a lower proportion stating a public health crisis as the biggest challenge. Comparing to Africa, 59% rate it as their biggest challenge.

However, it’s not all about COVID-19, business continues, and you need to demonstrate how you can help them:

• Safeguard data and intellectual property

• Manage the economic fall out from COVID-19

I think innovation and tech is interesting. It’s often in times like this that companies need to innovate to disrupt and differentiate, ensuring they remain profitable, and tech is critical to this.

18

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Looking forward five years, priorities change

Looking ahead five years, the challenges are very similar. What’s interesting, is while in the US and Europe a public health crisis has dropped in importance, it remains top in APAC. Albeit the proportion saying it will be the biggest challenge is a lot lower vs the 43% we saw on the previous chart. This is an indication of the long lasting effect of COVID-19 or the possibility of something similar.

So, we’re seeing priorities shift and with this budgets shift too.

19

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

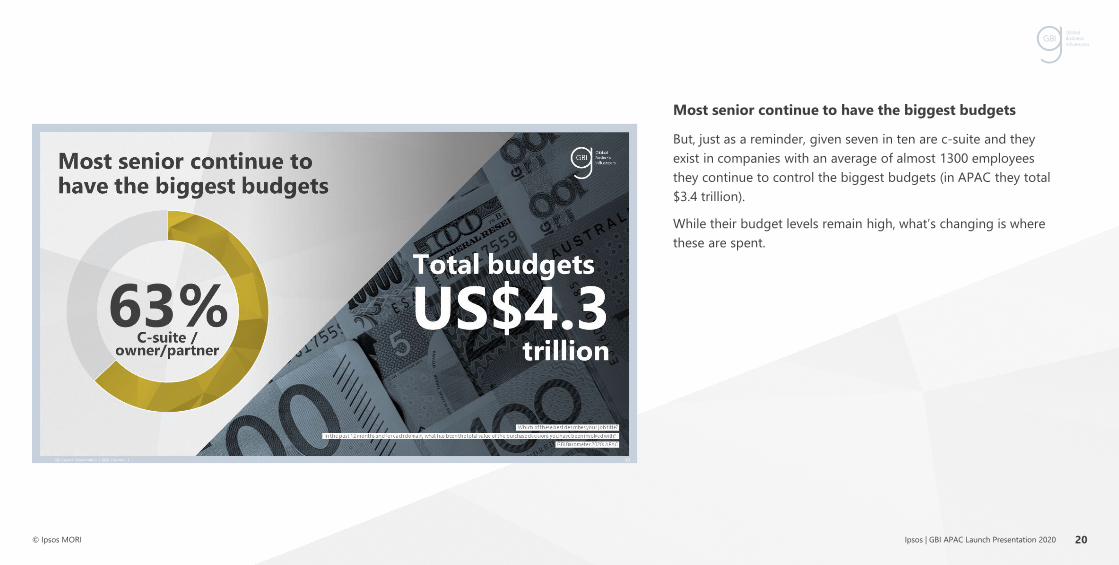

Most senior continue to have the biggest budgets

But, just as a reminder, given seven in ten are c-suite and they exist in companies with an average of almost 1300 employees they continue to control the biggest budgets (in APAC they total $3.4 trillion).

While their budget levels remain high, what’s changing is where these are spent.

20

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Budget priorities are shifting

Back in July we asked the GBI to look forward 12 months and indicate whether they thought their spending would be lower, the same or higher than pre COVID-19 in a variety of different B2B areas. I think what’s positive is that generally a larger proportion of the GBI, across all categories, think spending will be either the same or higher than pre-COVID. It’s when we start to look at the detail that we see differences in these levels.

For areas such as company events and travel, as we’d expect, we’re seeing a much more hesitant return to pre-COVID spending. Only around 55% say spend will be the same or higher. But, the proportion spending the same or higher elsewhere is much larger, mirroring the need to adapt.

Product development and R&D is at the heart of that and over athird are planning to spend more in this area than pre-COVID.

Investment in IT and tech helps facilitate this and of course other areas such as remote working solutions, where over four in ten are saying spending will increase.

21

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Businesses are adapting

When we asked them about different working scenario’s in 12 months time, companies really are shifting to remote working. They’re not just saying there will be more opportunities for flexible working, they’re taking action, there’s an increase in use of collaborative IT platforms.

However, perhaps concerningly, over six in ten are reducing office space.

22

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Adapting brings new challenges

Many GBI say remote working is going to make managing teams more difficult.

23

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Business values are therefore shifting

We talked last year about the importance of trust. It’s rated here as the most important value. Earlier we saw this focus on the need to adapt, COVID-19 is really testing how adaptable businesses, institutions, governments, and entire societies are. The fabric of trust provides the means by which co-ordination and co-operation can be achieved. Such co-operation can drive behaviours to bring an economy back up to speed.

It is essential your employees have to trust you and the measures you’re putting in place to keep them safe to allow them to work.

Maintaining team spirit is also important. Few people have a large house and garden in built up metropolitan areas and not seeing work colleagues adds to the challenge. We need strong leaders, like the GBI, to guide us through these difficult times.

COVID-19 means that priorities have shifted and while budgets remain high, where they are spent is changing. Additionally, business’ operations and values are adapting to COVID-19, it’s these values you need to think about leveraging in messaging.

24

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Impact of COVID-19 on personal lives

So, that’s it on the business side, lets now look at the impact of COVID-19 on the GBI’s personal lives.

25

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

High salaries

In the previous slides, we’ve already touched on how senior this audience are, and a bi-product of being in these senior positions is that they come with very big salaries.

26

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Pay-cuts and off-setting COVID-19 impact

It’s been very well documented over the past few months that many business executives have taken large pay-cuts to off-set the impact of COVID-19 and fund relief efforts in the battle against the virus.

27

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

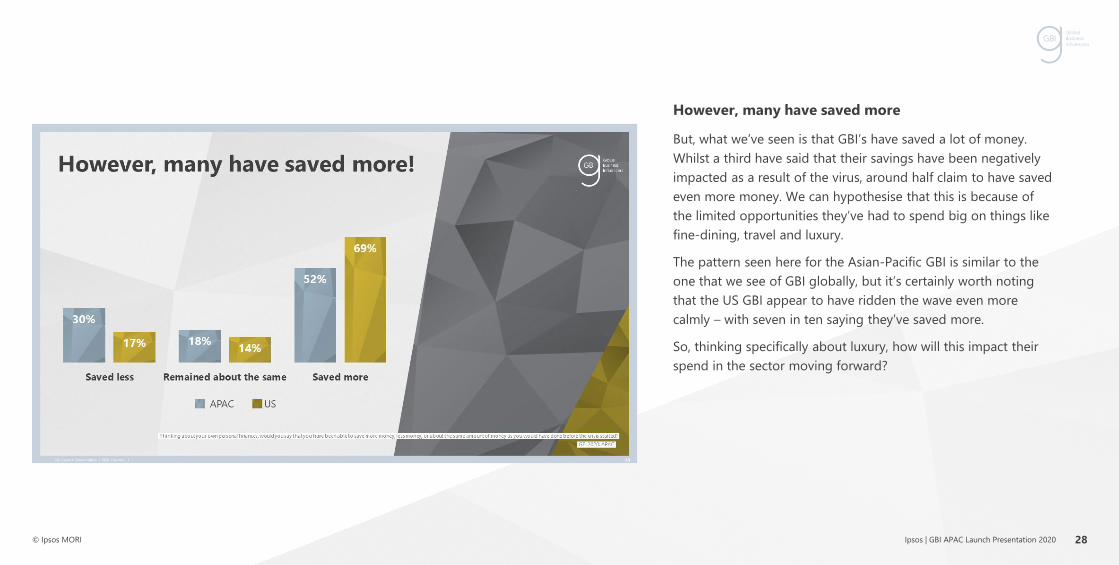

However, many have saved more

But, what we’ve seen is that GBI’s have saved a lot of money. Whilst a third have said that their savings have been negatively impacted as a result of the virus, around half claim to have saved even more money. We can hypothesise that this is because of the limited opportunities they’ve had to spend big on things like fine-dining, travel and luxury.

The pattern seen here for the Asian-Pacific GBI is similar to the one that we see of GBI globally, but it’s certainly worth noting that the US GBI appear to have ridden the wave even more calmly – with seven in ten saying they’ve saved more.

So, thinking specifically about luxury, how will this impact their spend in the sector moving forward?

28

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

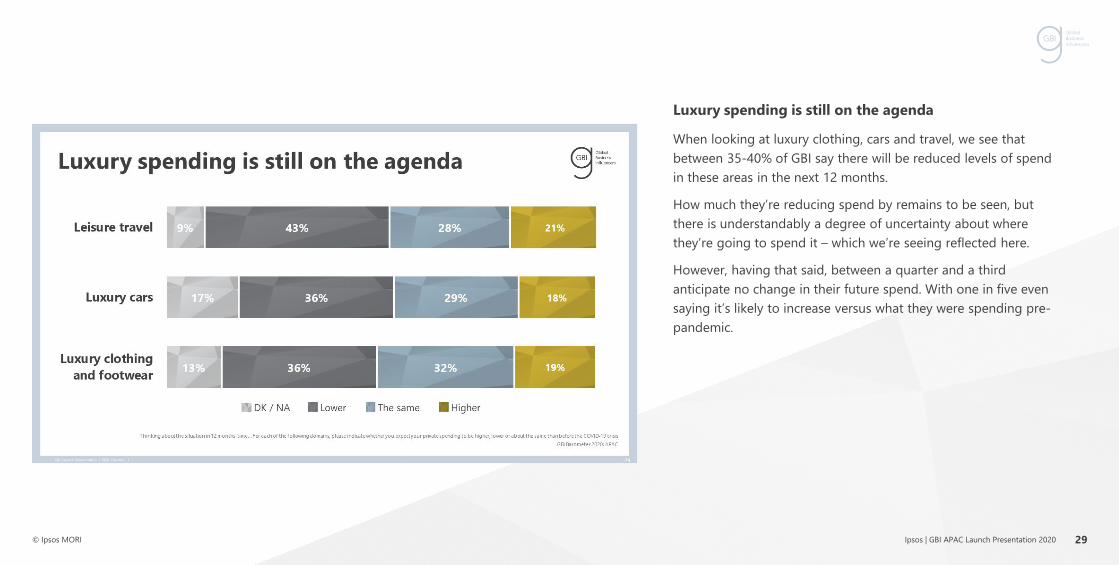

Luxury spending is still on the agenda

When looking at luxury clothing, cars and travel, we see that between 35-40% of GBI say there will be reduced levels of spend in these areas in the next 12 months.

How much they’re reducing spend by remains to be seen, but there is understandably a degree of uncertainty about where they’re going to spend it – which we’re seeing reflected here.

However, having that said, between a quarter and a third anticipate no change in their future spend. With one in five even saying it’s likely to increase versus what they were spending pre-pandemic.

29

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

GBI remain your best high end customers

The average intended spend across luxury areas remains high.

So, for GBI, although many things have changed since the pandemic began, they have managed to maintain their position as your key consumers when it comes to high-end luxury.

This really illustrates the importance of brand equity. Whilst spend levels have been affected, this audience are still the biggest spenders. Therefore, if you want to reach them and get a piece of the action, you need to continue to build your brand with them.

30

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Purchase channels continue to be varied

However, although they are the same valuable audience that they were this time last year, their spending behaviours may have adapted in that time as a result of the virus.

Among APAC GBI, in-store still ranks as the preferred option for luxury clothing and footwear purchases, but the gap between in-store and online looks like it’s starting to close.

31

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Personal experience

When looking at personal spend in luxury clothing, we know that ‘personal experience’ is a key driver, which explains why in-store purchases are still high.

But of course, websites/apps are continuing to evolve, and those luxury brands who enhance their digital engagement look set to reap the benefits among this audience.

32

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

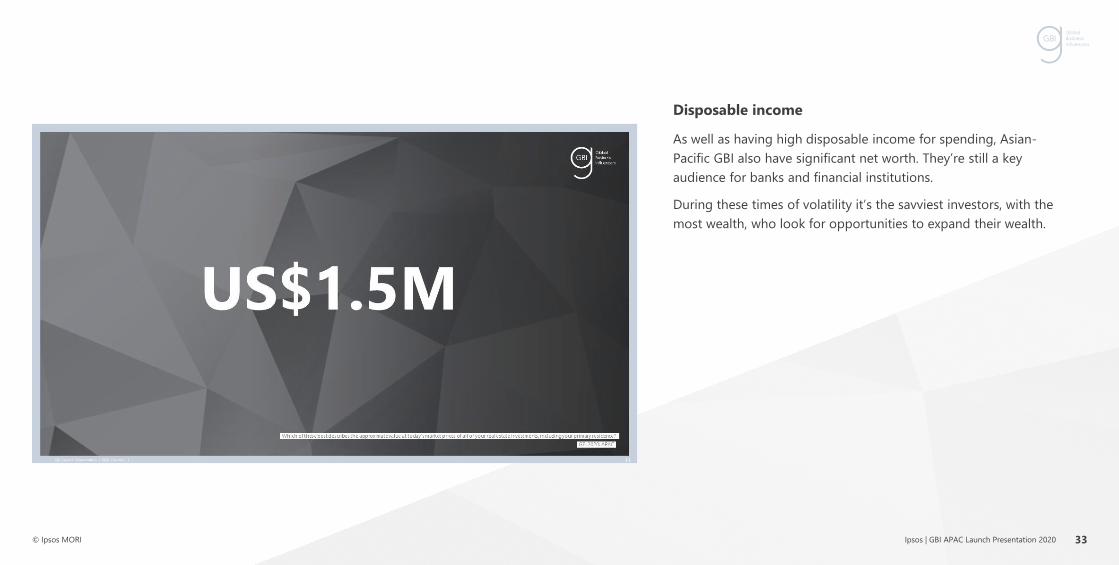

Disposable income

As well as having high disposable income for spending, Asian-Pacific GBI also have significant net worth. They’re still a key audience for banks and financial institutions.

During these times of volatility it’s the savviest investors, with the most wealth, who look for opportunities to expand their wealth.

33

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Personal financial activity

Reflecting this, they’re certainly doing a lot of activity.

During the pandemic, about half have been buying and selling stocks, re-evaluating their financial portfolios, and looking for opportunities to invest.

34

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

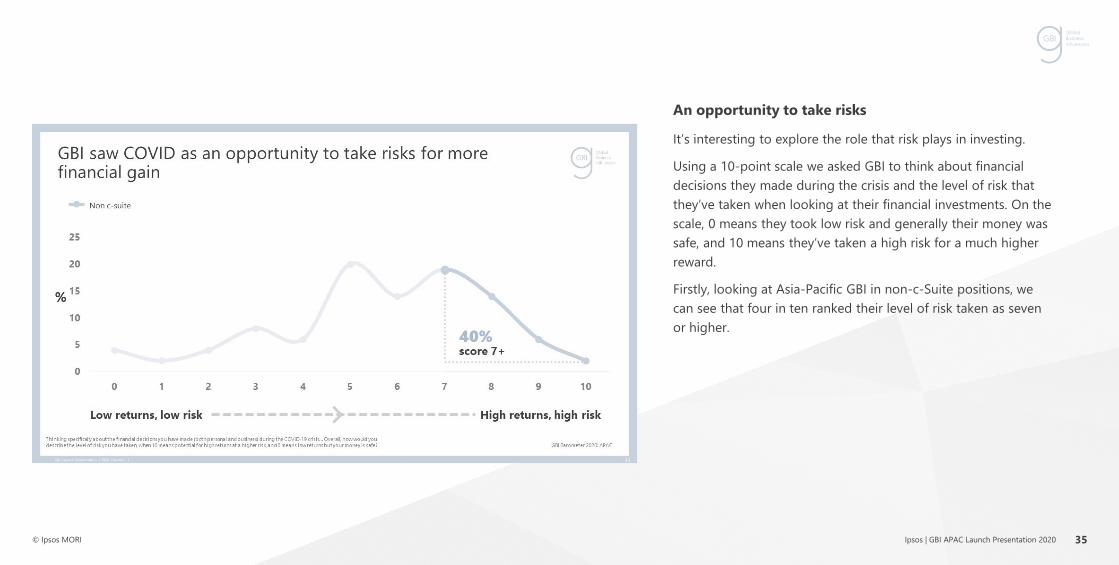

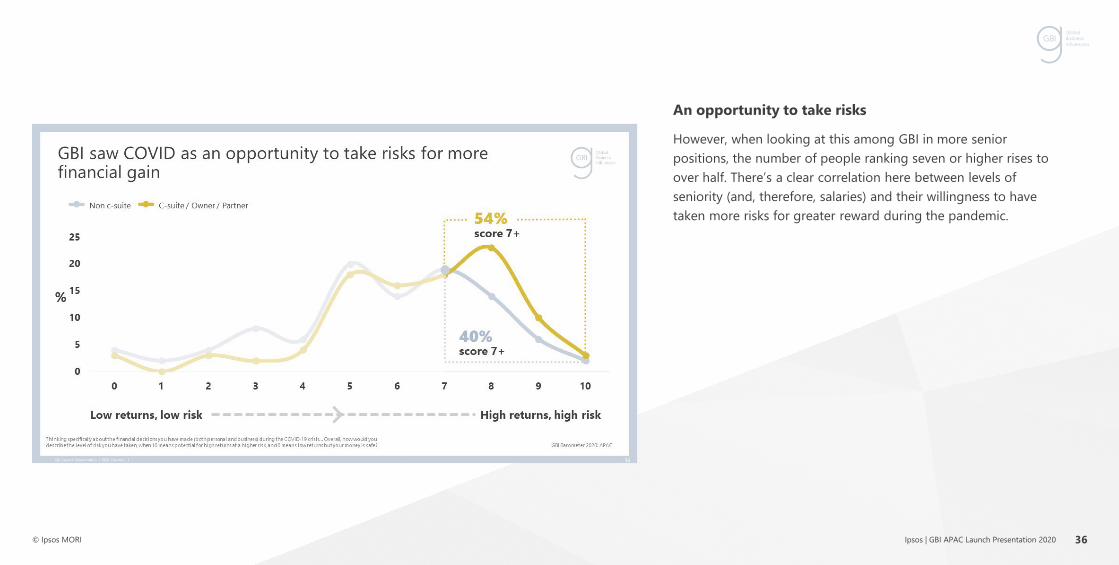

An opportunity to take risks

It’s interesting to explore the role that risk plays in investing.

Using a 10-point scale we asked GBI to think about financial decisions they made during the crisis and the level of risk that they’ve taken when looking at their financial investments. On the scale, 0 means they took low risk and generally their money was safe, and 10 means they’ve taken a high risk for a much higher reward.

Firstly, looking at Asia-Pacific GBI in non-c-Suite positions, we can see that four in ten ranked their level of risk taken as seven or higher.

35

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

An opportunity to take risks

However, when looking at this among GBI in more senior positions, the number of people ranking seven or higher rises to over half. There’s a clear correlation here between levels of seniority (and, therefore, salaries) and their willingness to have taken more risks for greater reward during the pandemic.

36

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

An opportunity to take risks

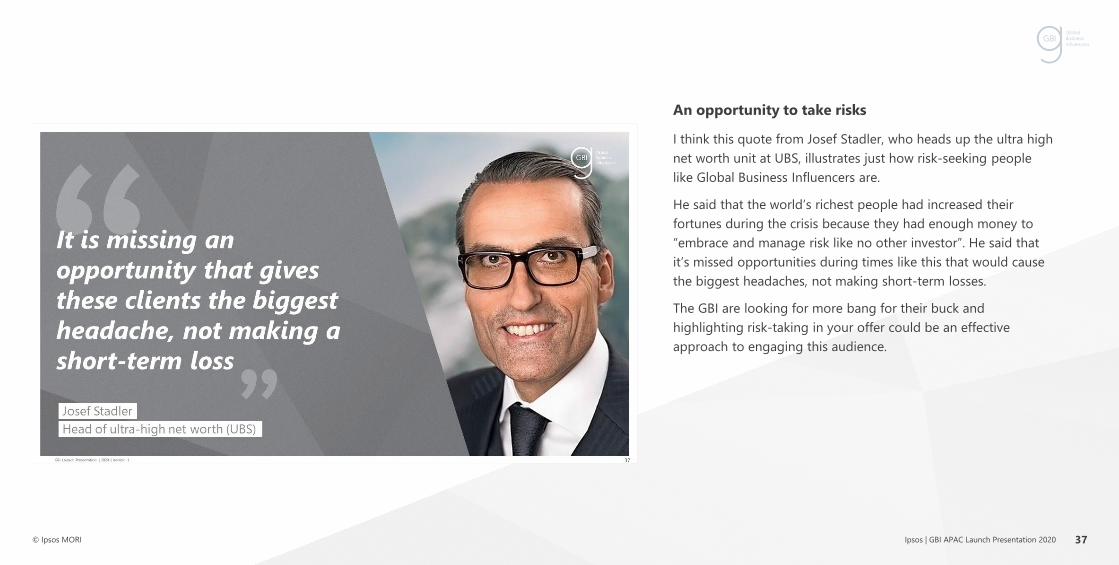

I think this quote from Josef Stadler, who heads up the ultra high net worth unit at UBS, illustrates just how risk-seeking people like Global Business Influencers are.

He said that the world’s richest people had increased their fortunes during the crisis because they had enough money to “embrace and manage risk like no other investor”. He said that it’s missed opportunities during times like this that would cause the biggest headaches, not making short-term losses.

The GBI are looking for more bang for their buck and highlighting risk-taking in your offer could be an effective approach to engaging this audience.

37

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Environmental, Social and Governance (ESG)

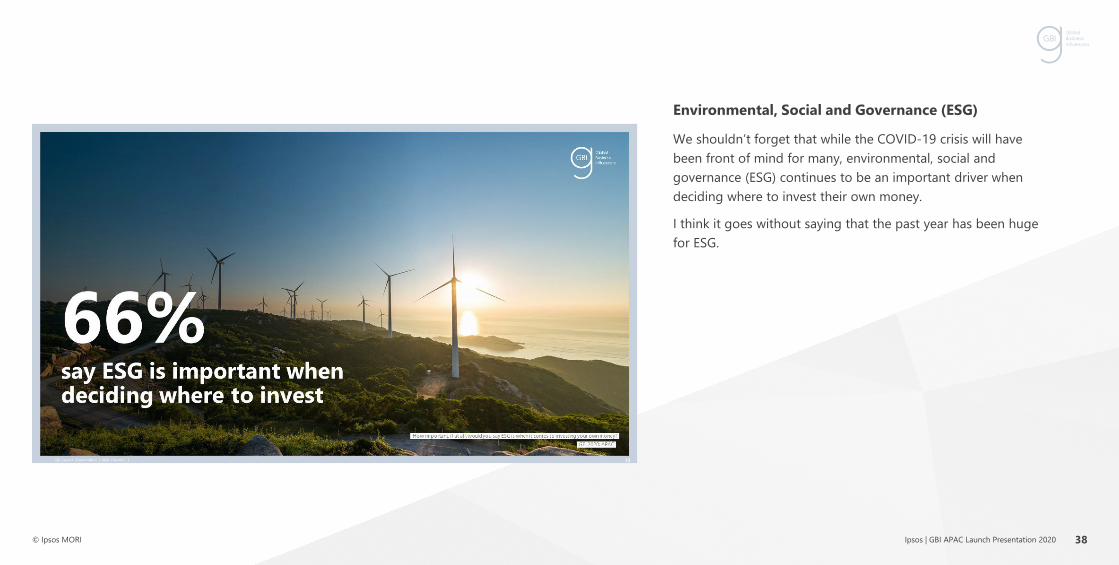

We shouldn’t forget that while the COVID-19 crisis will have been front of mind for many, environmental, social and governance (ESG) continues to be an important driver when deciding where to invest their own money.

I think it goes without saying that the past year has been huge for ESG.

38

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Environmental, Social and Governance (ESG)

We’ve seen issues around gender inequality, the rise of Greta Thunberg and of course, the Global Climate Strikes.

39

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Environmental, Social and Governance (ESG)

So, taking a business focus again, for GBI, ESG is incredibly important in deciding who they do business with.

You need to be demonstrating that:

• You have ESG-friendly products

• That your company is ethically and socially responsible

• You shout about the work you’re doing in this space in any marketing/comms.

40

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Environmental, Social and Governance (ESG)

Personally, GBI believe ESG has a number of benefits including building their company’s reputation and mitigating risk among investors.

41

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Environmental, Social and Governance (ESG)

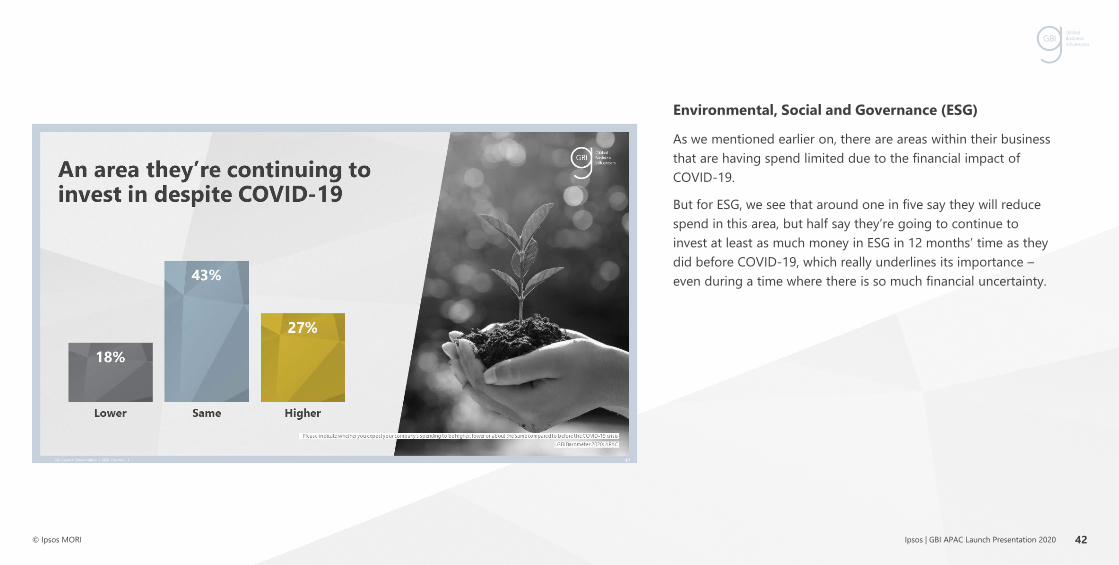

As we mentioned earlier on, there are areas within their business that are having spend limited due to the financial impact of COVID-19.

But for ESG, we see that around one in five say they will reduce spend in this area, but half say they’re going to continue to invest at least as much money in ESG in 12 months’ time as they did before COVID-19, which really underlines its importance –even during a time where there is so much financial uncertainty.

42

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

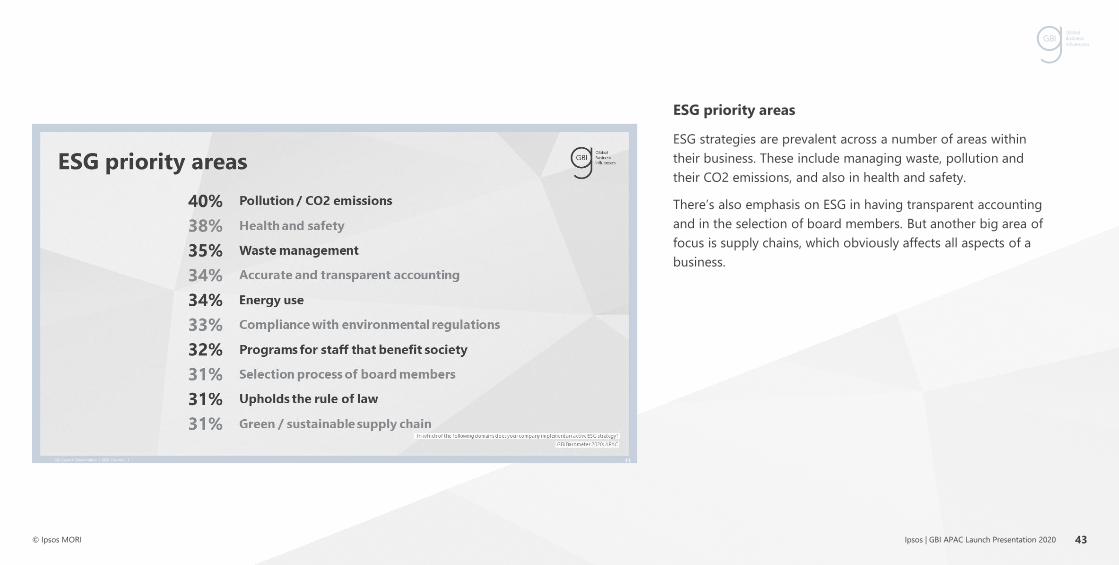

ESG priority areas

ESG strategies are prevalent across a number of areas within their business. These include managing waste, pollution and their CO2 emissions, and also in health and safety.

There’s also emphasis on ESG in having transparent accounting and in the selection of board members. But another big area of focus is supply chains, which obviously affects all aspects of a business.

43

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Transparent supply chains

Samsung recently claimed first spot in Gartner’s Top 25 Supply Chain award in Asia-Pacific. The win also saw them move up five places to 8th place in the global rankings. They were commended for having an advanced and highly integrated supply chain which spans across product, process and people.

This really proves the importance of having a transparent supply chain and it really helps us to understand why GBI are putting lots of focus on this in the future.

44

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Green supply chains

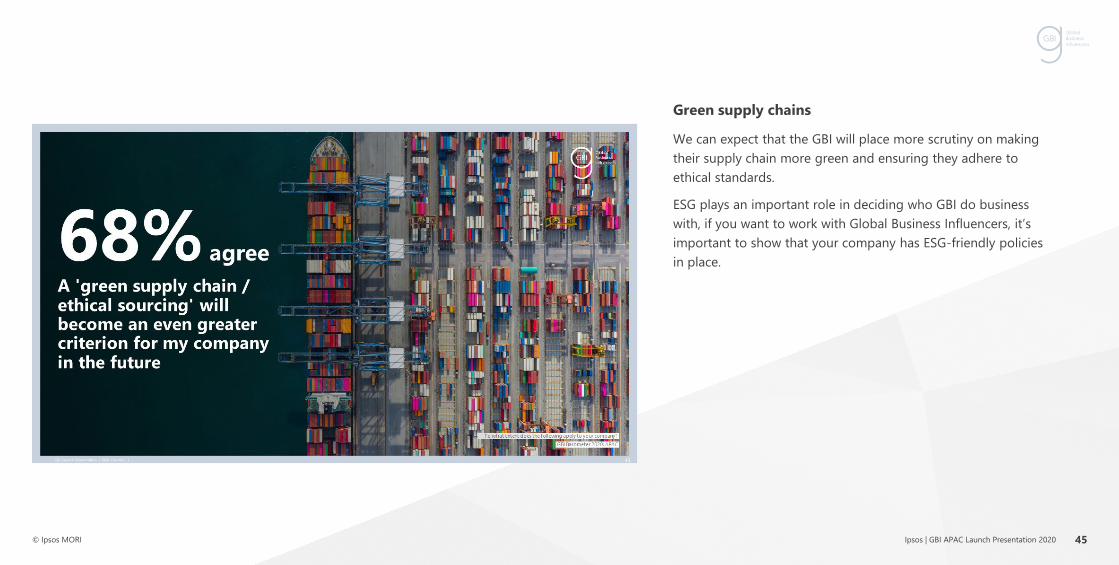

We can expect that the GBI will place more scrutiny on making their supply chain more green and ensuring they adhere to ethical standards.

ESG plays an important role in deciding who GBI do business with, if you want to work with Global Business Influencers, it’s important to show that your company has ESG-friendly policies in place.

45

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Media

In this last section, we’ll talk you through GBI’s media consumption, how it’s changed since COVID-19 and how they think their behaviours will change in the future.

46

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

More frequent consumption across all platforms

You may remember seeing this chart at our launch event last year, Global Business Influencers continue to consume a massive amount of content from a variety of sources.

Looking here at yesterday reach (media accessed in the past day), digital consumption is unsurprisingly very high, but print and TV continues to be a very popular means of accessing content. There has been very little variance in this data even as far back as 2016.

Following on from conversations we had with lots of our subscribers, one theme that we saw popping up time and time again was a demand for insights around podcasts. This slide looked at consumption at a device level, but we also added a battery of questions this year that focussed on podcasts.

47

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Podcasts

Two-thirds of the Asian-Pacific GBI listen to podcasts at least weekly, which is about the same as GBI globally. This obviously represents a very sizeable audience.

48

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

Podcasts

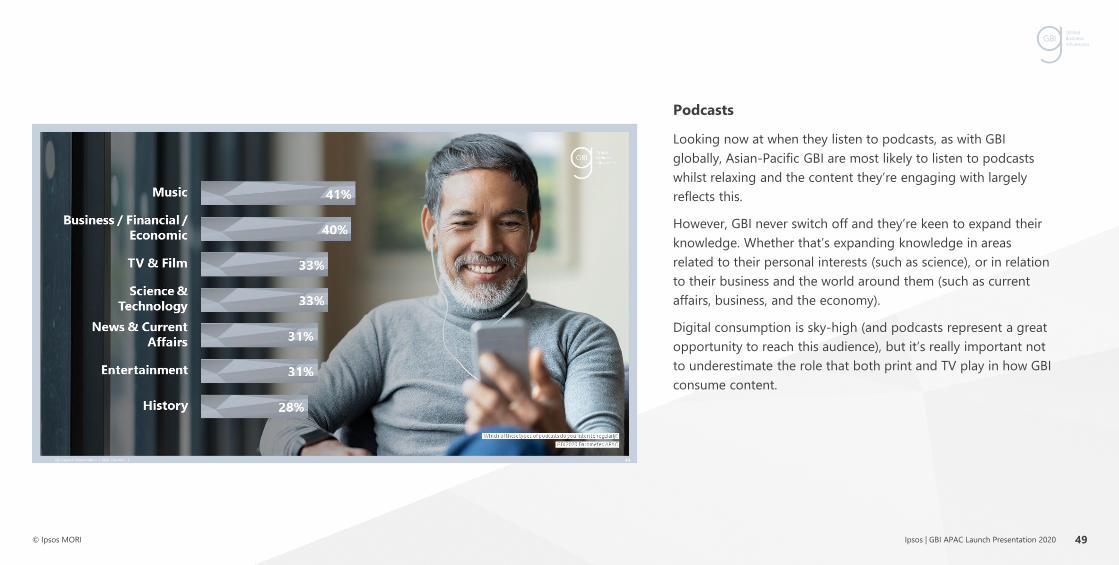

Looking now at when they listen to podcasts, as with GBI globally, Asian-Pacific GBI are most likely to listen to podcasts whilst relaxing and the content they’re engaging with largely reflects this.

However, GBI never switch off and they’re keen to expand their knowledge. Whether that’s expanding knowledge in areas related to their personal interests (such as science), or in relation to their business and the world around them (such as current affairs, business, and the economy).

Digital consumption is sky-high (and podcasts represent a great opportunity to reach this audience), but it’s really important not to underestimate the role that both print and TV play in how GBI consume content.

49

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

3 key takeaways

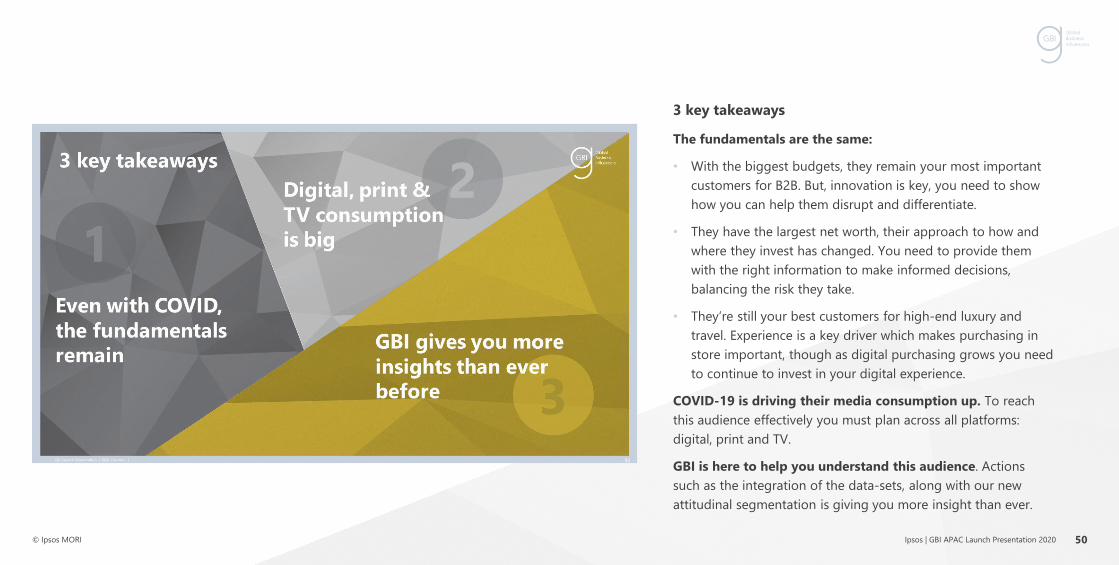

The fundamentals are the same:

• With the biggest budgets, they remain your most important customers for B2B. But, innovation is key, you need to show how you can help them disrupt and differentiate.

• They have the largest net worth, their approach to how and where they invest has changed. You need to provide them with the right information to make informed decisions, balancing the risk they take.

• They’re still your best customers for high-end luxury and travel. Experience is a key driver which makes purchasing in store important, though as digital purchasing grows you need to continue to invest in your digital experience.

COVID-19 is driving their media consumption up. To reach this audience effectively you must plan across all platforms: digital, print and TV.

GBI is here to help you understand this audience. Actions such as the integration of the data-sets, along with our new attitudinal segmentation is giving you more insight than ever.

50

Ipsos | GBI APAC Launch Presentation 2020© Ipsos MORI

James TorrSenior Director+44 (0)20 8861 [email protected]

Reece CarpenterResearch Manager+44 (0)20 8861 [email protected]