gasification for power, heat, fuels & chemicals strategic

TRANSCRIPT

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

©2018 Energy Technologies Institute LLP The information in this document is the property of Energy Technologies Institute LLP and may not be copied or communicated to a third party, or used for any purpose other than that for

which it is supplied without the express written consent of Energy Technologies Institute LLP.

This information is given in good faith based upon the latest information available to Energy Technologies Institute LLP, no warranty or representation is given concerning such information,

which must not be taken as establishing any contractual or other commitment binding upon Energy Technologies Institute LLP or any of its subsidiary or associated companies.

Gasification for power, heat, fuels & chemicals

Strategic insights for implementationDr Geraint Evans

Programme Manager – Bioenergy and CCS, ETI

SMi - 5th December 2018

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Agenda

• ETI

• Importance of bioenergy and value in the energy

system

• Why is gasification important?

• What is gasification?

– Value in the UK setting

• UK and beyond gasification landscape

• Lessons learned, future direction

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

What is the ETI?

2.

• The ETI is a public-private

partnership between global energy

and engineering companies and

the UK Government.

• Targeted development,

demonstration and de-risking of

new technologies for affordable

and secure energy

• Shared risk

ETI programme associate

ETI members

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

ETI Invests in projects at 3 levels

3.

9 Technology Programme areas

Delivering...

• New knowledge

• Technology development

• Technology demonstration

• Reduced risk

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

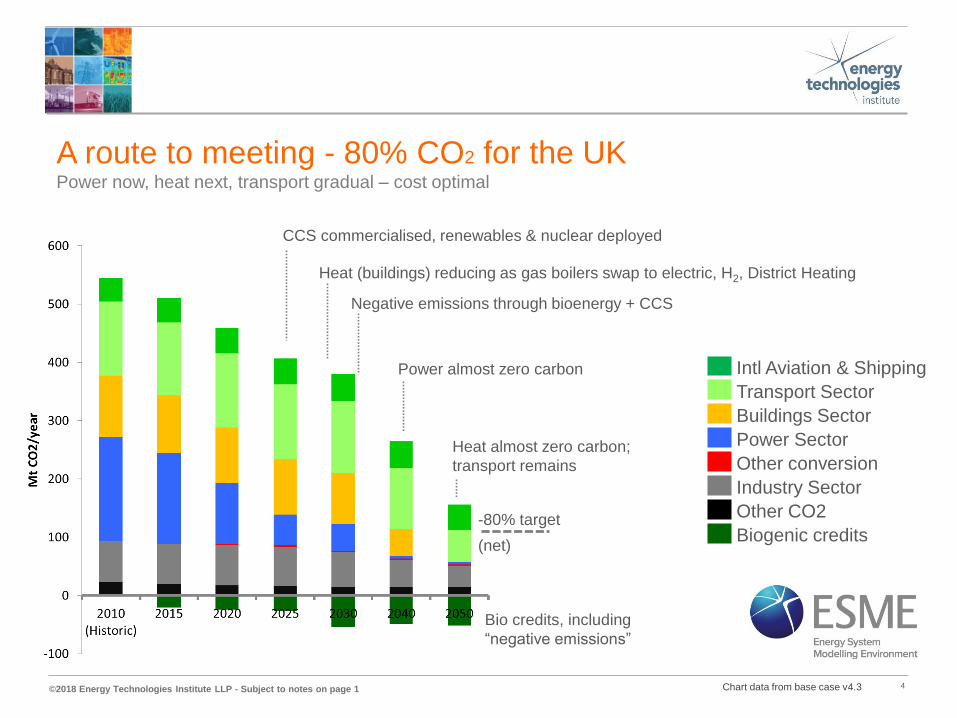

-80% target

(net)

A route to meeting - 80% CO2 for the UKPower now, heat next, transport gradual – cost optimal

Power almost zero carbon

Heat (buildings) reducing as gas boilers swap to electric, H2, District Heating

CCS commercialised, renewables & nuclear deployed

Negative emissions through bioenergy + CCS

Bio credits, including

“negative emissions”

Intl Aviation & Shipping

Transport Sector

Buildings Sector

Power Sector

Other conversion

Industry Sector

Other CO2

Biogenic credits

Chart data from base case v4.3 4

Heat almost zero carbon;

transport remains

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Why is ETI interested in gasification?

• Two key insights from BVCM modelling

• The sector will need a combination of

feedstocks

• Gasification

• key bioenergy enabler

• resilient

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Biomass – many types & sources available

• Wastes including waste wood

• Forest derived – long rotation forestry (LRF)

• Energy crops

• Agricultural residues such as straw

• Sugars, oils, starches

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

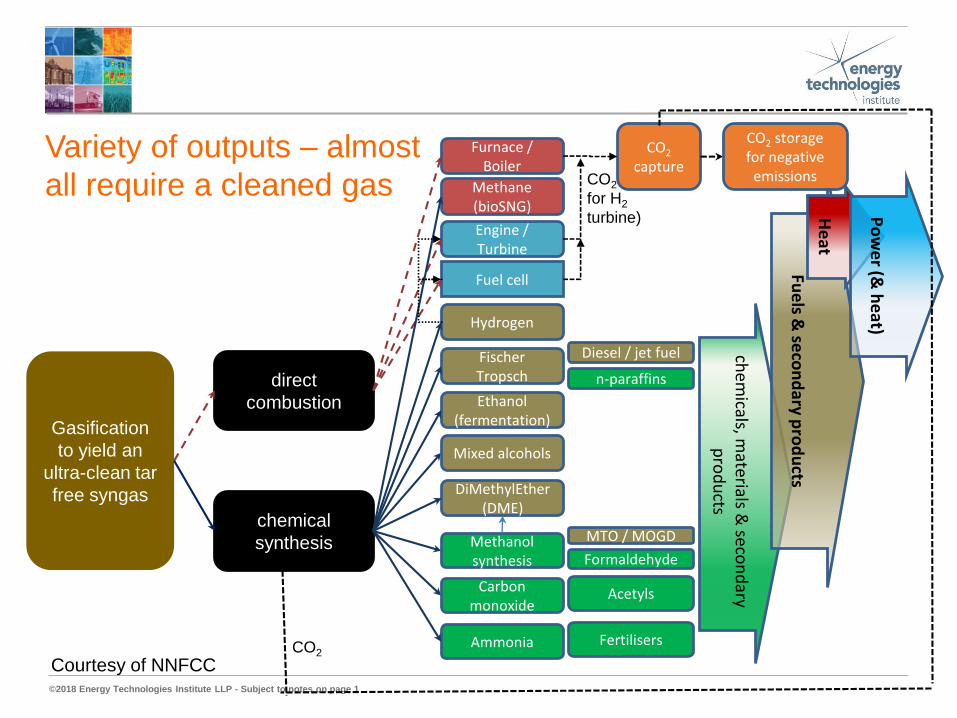

Variety of outputs – almost

all require a cleaned gas CO2 (n/a

for H2

turbine)

CO2

chem

icals, materials &

secon

dary

pro

du

cts

Methane (bioSNG)

Ethanol (fermentation)

Furnace / Boiler

Fuel cell

Fischer Tropsch

Hydrogen

Engine / Turbine

direct

combustion

chemical

synthesis

Gasification

to yield an

ultra-clean tar

free syngas

Methanol synthesis

Carbon monoxide

Mixed alcohols

Ammonia

DiMethylEther (DME)

Diesel / jet fuel

n-paraffins

Fertilisers

Acetyls

MTO / MOGD

Formaldehyde

Fue

ls & se

con

dary p

rod

ucts

He

at

Po

we

r (& h

eat)

CO2

capture

CO2 storage for negative

emissions

Courtesy of NNFCC

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

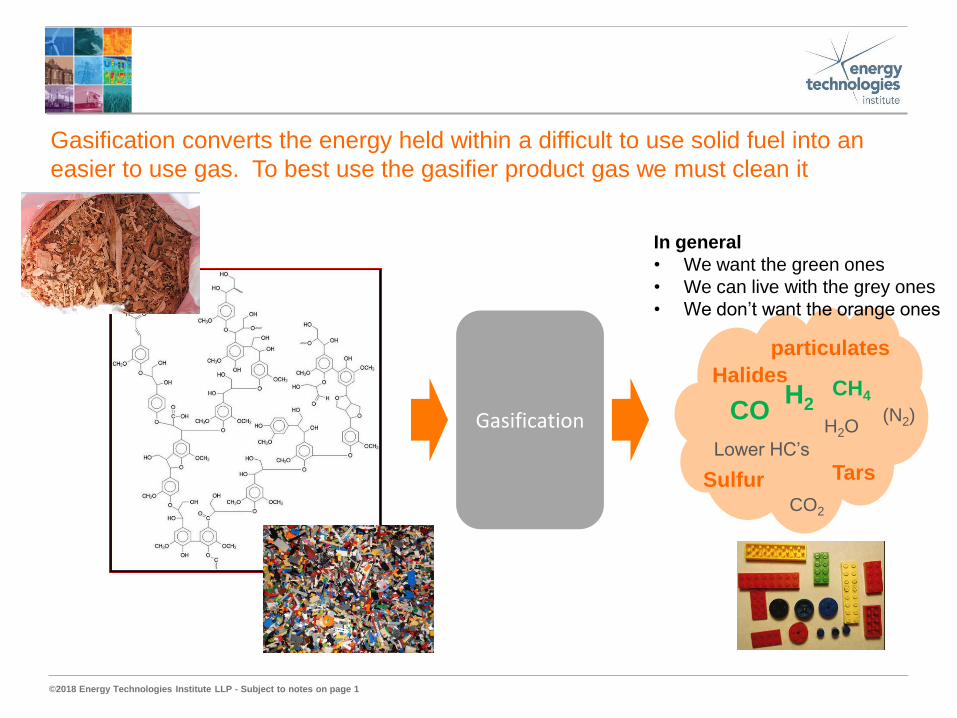

Gasification converts the energy held within a difficult to use solid fuel into an

easier to use gas. To best use the gasifier product gas we must clean it

Gasification CO

CO2

H2CH4

H2O

Lower HC’s

Tars

particulates

Sulfur

Halides

(N2)

In general

• We want the green ones

• We can live with the grey ones

• We don’t want the orange ones

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

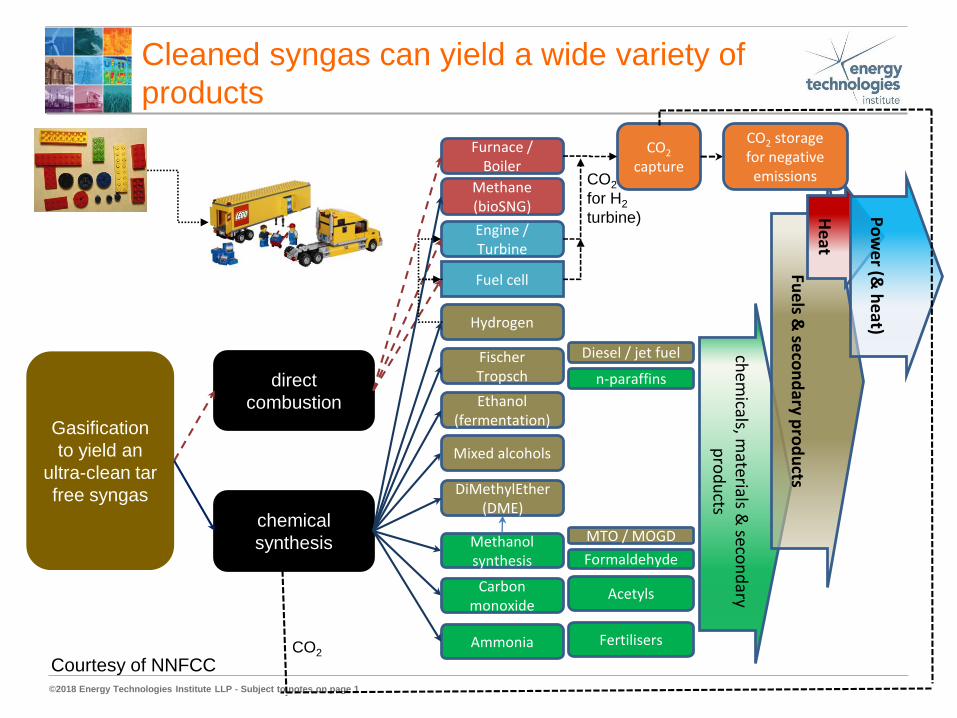

Cleaned syngas can yield a wide variety of

products

CO2 (n/a

for H2

turbine)

CO2

chem

icals, materials &

secon

dary

pro

du

cts

Methane (bioSNG)

Ethanol (fermentation)

Furnace / Boiler

Fuel cell

Fischer Tropsch

Hydrogen

Engine / Turbine

direct

combustion

chemical

synthesis

Gasification

to yield an

ultra-clean tar

free syngas

Methanol synthesis

Carbon monoxide

Mixed alcohols

Ammonia

DiMethylEther (DME)

Diesel / jet fuel

n-paraffins

Fertilisers

Acetyls

MTO / MOGD

Formaldehyde

Fue

ls & se

con

dary p

rod

ucts

He

at

Po

we

r (& h

eat)

CO2

capture

CO2 storage for negative

emissions

Courtesy of NNFCC

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

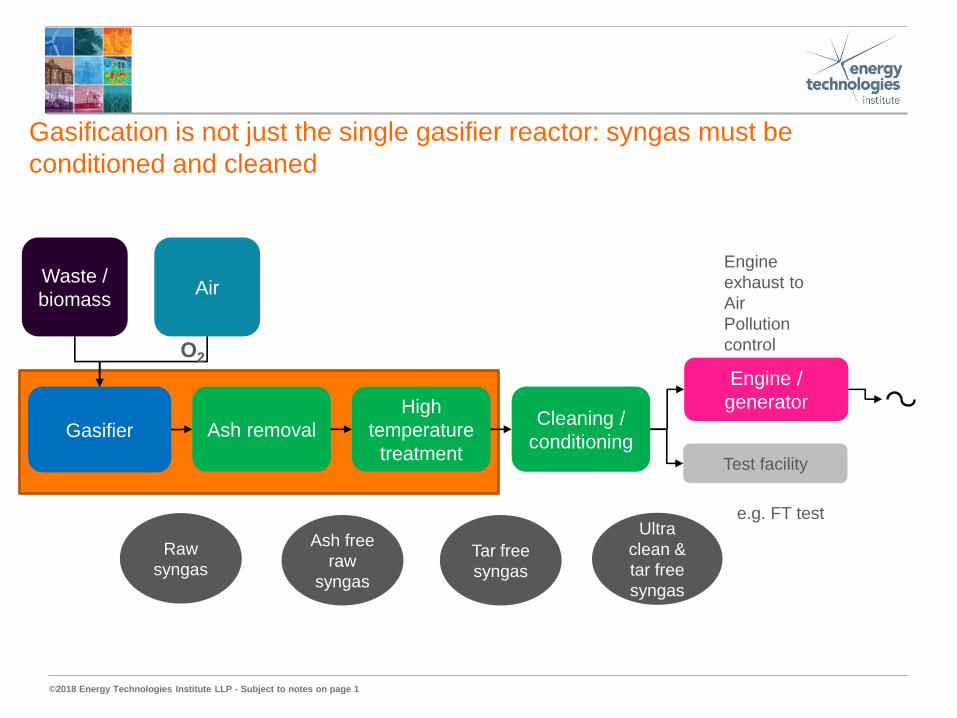

Gasification is not just the single gasifier reactor: syngas must be

conditioned and cleaned

AirWaste /

biomass

Gasifier

O2

Cleaning /

conditioning

Raw

syngas

Ultra

clean &

tar free

syngas

Engine /

generator

Test facility

Engine

exhaust to

Air

Pollution

control

High

temperature

treatment

Ash free

raw

syngas

Ash removal

Tar free

syngas

e.g. FT test

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

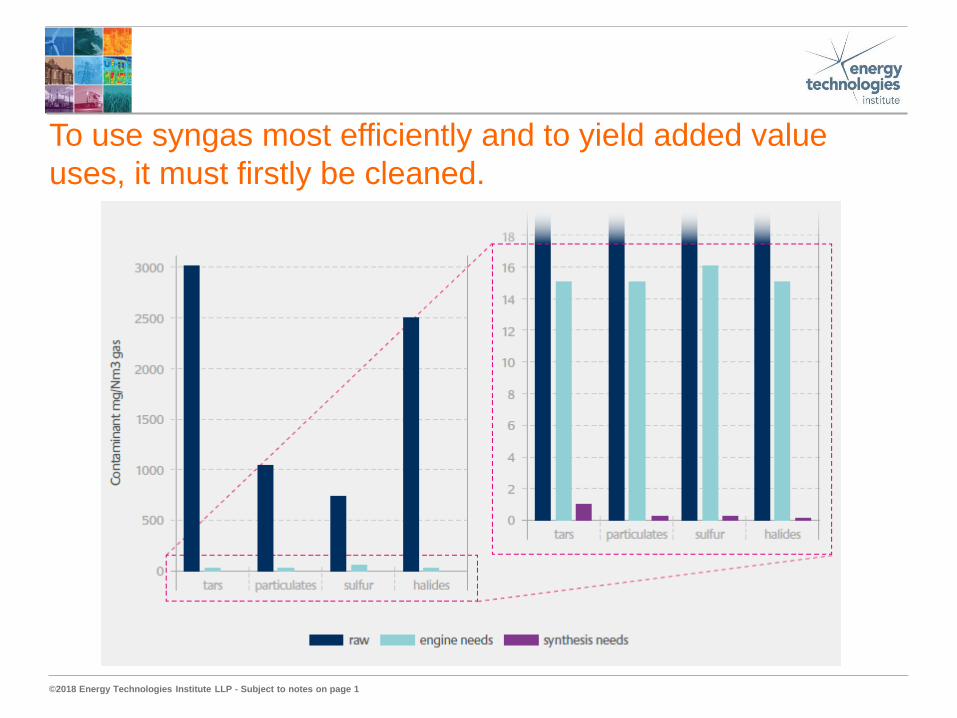

To use syngas most efficiently and to yield added value

uses, it must firstly be cleaned.

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

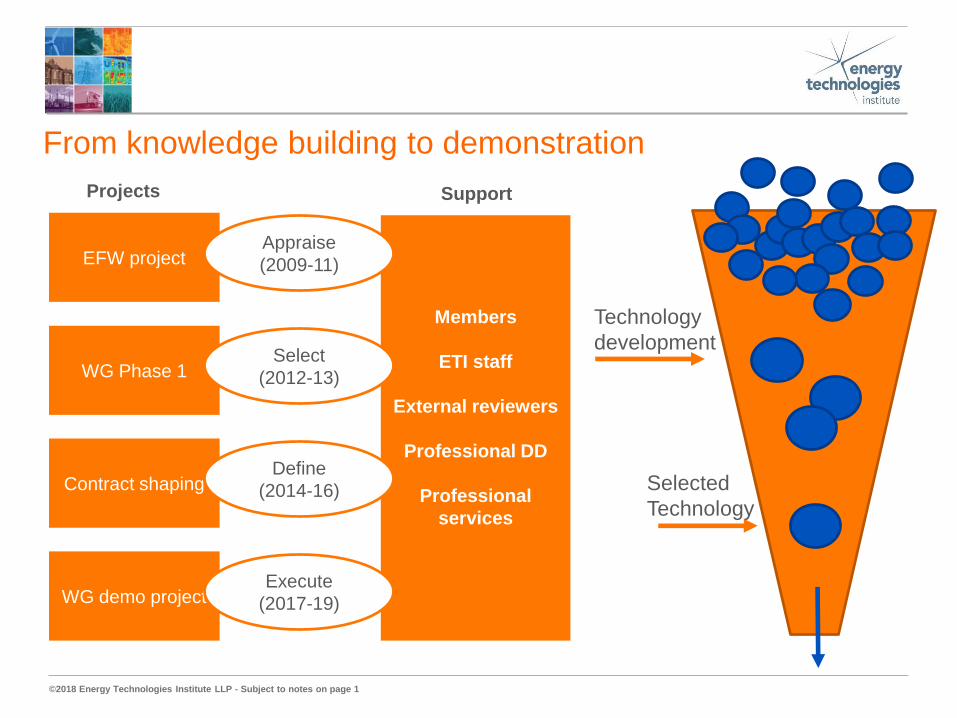

From knowledge building to demonstration

Members

ETI staff

External reviewers

Professional DD

Professional

services

Projects Support

EFW projectAppraise

(2009-11)

WG Phase 1Select

(2012-13)

Contract shapingDefine

(2014-16)

WG demo projectExecute

(2017-19)

Technology

development

Selected

Technology

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Loughborough

50 miles

ETI’s 1.5 MWe waste gasification project, Wednesbury

15.

©2018 Energy Technologies Institute LLP - Subject to notes on page 1 11.

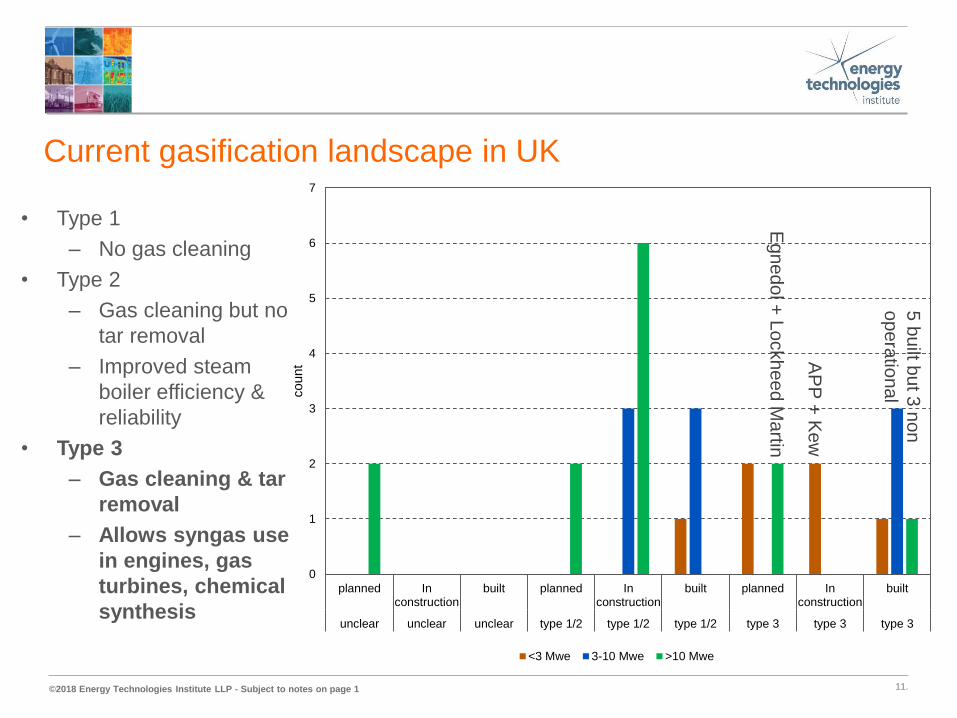

Current gasification landscape in UK

0

1

2

3

4

5

6

7

planned Inconstruction

built planned Inconstruction

built planned Inconstruction

built

unclear unclear unclear type 1/2 type 1/2 type 1/2 type 3 type 3 type 3

count

<3 Mwe 3-10 Mwe >10 Mwe

5b

uilt b

ut 3

no

n

op

era

tiona

l

AP

P +

Ke

w

Egnedol +

Lockheed M

artin

• Type 1

– No gas cleaning

• Type 2

– Gas cleaning but no

tar removal

– Improved steam

boiler efficiency &

reliability

• Type 3

– Gas cleaning & tar

removal

– Allows syngas use

in engines, gas

turbines, chemical

synthesis

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Current gasification landscape - Types 1 and 2

• Type 1 projects – more “bankable” than Type 3

– As of 2015:

• 3 operational in 2015 are not now;

• 2 decommissioned;

• >50 in planning process;

• 5 in construction – 2 or 3 now operational?

– 2018 examples

• Birmingham Biopower (updraft)

• Hull EnergyWorks (FB)

• No Type 2 projects in UK – lack of DH network infrastructure plus policy allows,

& therefore drives investment into Type 1

– Mainly in Scandinavia

– High energy efficiency – around 80% because of waste heat use.

• Lahti (hot gas cleaning before combustion in gas boiler) (FB)

• Vaskiluoto (co-fires cleaned gas in coal fired power station) (FB)

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Current gasification landscape – Type 3

• Increasing focus on Type 3 which promise to be able to deliver the gasification opportunity

– Excluding sub 1 MWe projects, some notable “misfortunes”

• Arbre, Teessidex2, Plymouth (and abroad, e.g. Choren in Germany, Gobigas in Sweden)

– Built:

• Refgas now built in Swindon (downdraft); Syngas Products

– In construction:

• Kew (FB) and APP (FB) in construction – commissioning 2018

– Planned:

• F4C gasification based projects (Johnson Matthey, Kew Technology, Progressive Energy,

Standard Gas, Velocys).

– Abroad

• BioTfuel (France) – in commissioning; for FT fuels (FB)

• Enerkem/AkzoNobel, Rotterdam for chemicals (FB) – 2021 plan

• Fulcrum Bioenergy (USA) – fuels (FB with external heating) – in construction

• Gussing, Austira - CHP plus demonstrations of H2, FT (indirect FB)

• KIT (Austria) – large scale research for methanol (FB) – aka Bioliq

• Skive, Denmark – CHP via engines (FB)

• SynTech/Royal Dahlman, India (indirect FB)

– Sub 1 MWe

• Numbers of kW scale downdraft gasifiers operating in UK

Useful (if incomplete wrt

UK projects) 2016

summary available from

IEA task 33

http://task33.ieabioener

gy.com/download.php?fi

le=files/file/2016/Status

%20report-corr_.pdf

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Findings from ETI gasification programme

• Gasification offers a number of benefits in the UK setting

– Flexible in feedstock and outputs - resilience

– Comparable/better efficiencies compared with other

technologies, especially at smaller scales

• Gasification of wastes and use of syngas in an engine is

technically feasible

– ETI’s targets are achievable

• Potential to be cost competitive with other sources of renewable

power

– scope to reduce costs as experience is gained (especially

procurement costs).

17.

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

Learning from others

• Careful and considered approach to scale up is needed

• Convening capital for future demo projects & delivering

acceptable returns is hugely challenging

• Fully funded doesn’t mean “fully funded”

• Costs are uncertain – scope changes as move from FEED to

Detailed Design

• Feedstock understanding and handling is a key challenge

• Reliability, in first year, can be poor

• Use of revenue type subsidies (RO, RTFO etc.) is challenging

– Delays

– First year reliability

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

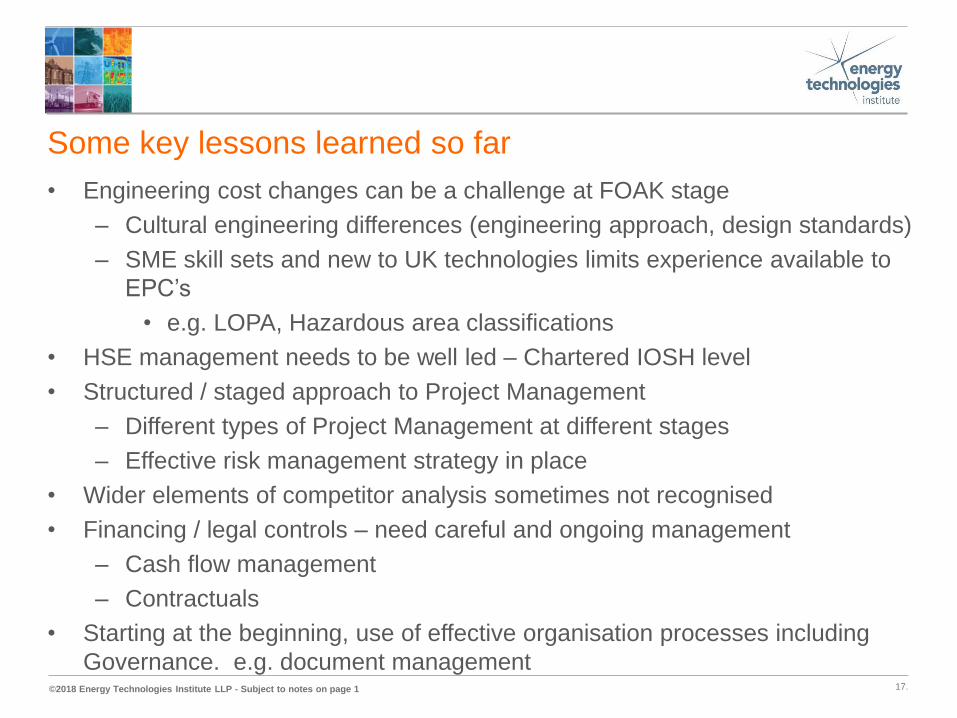

Some key lessons learned so far

• Engineering cost changes can be a challenge at FOAK stage

– Cultural engineering differences (engineering approach, design standards)

– SME skill sets and new to UK technologies limits experience available to

EPC’s

• e.g. LOPA, Hazardous area classifications

• HSE management needs to be well led – Chartered IOSH level

• Structured / staged approach to Project Management

– Different types of Project Management at different stages

– Effective risk management strategy in place

• Wider elements of competitor analysis sometimes not recognised

• Financing / legal controls – need careful and ongoing management

– Cash flow management

– Contractuals

• Starting at the beginning, use of effective organisation processes including

Governance. e.g. document management17.

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

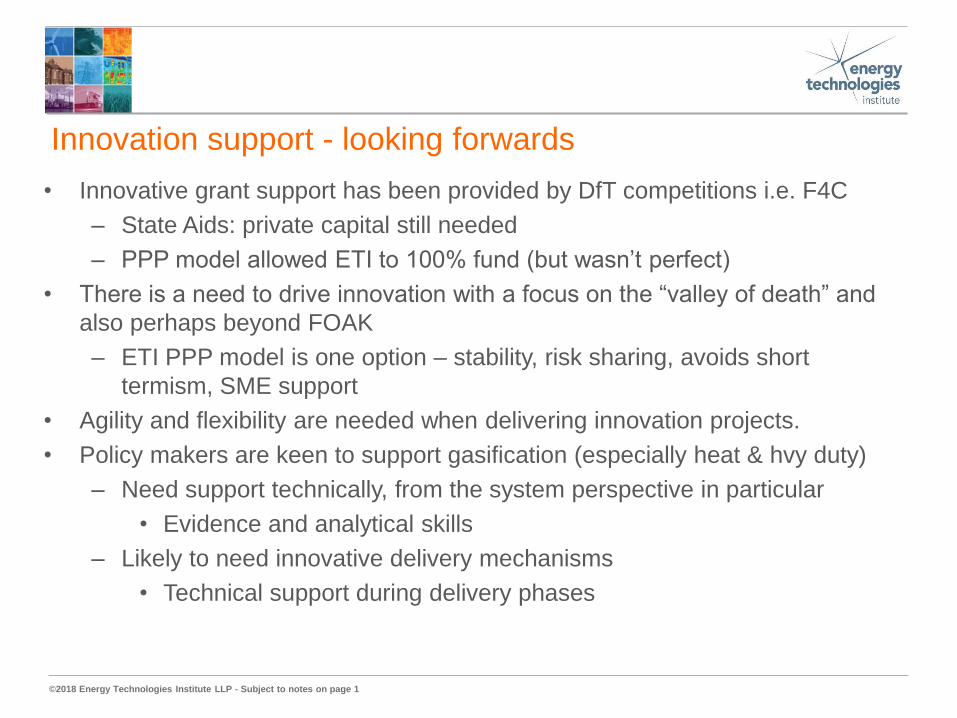

Innovation support - looking forwards

• Innovative grant support has been provided by DfT competitions i.e. F4C

– State Aids: private capital still needed

– PPP model allowed ETI to 100% fund (but wasn’t perfect)

• There is a need to drive innovation with a focus on the “valley of death” and

also perhaps beyond FOAK

– ETI PPP model is one option – stability, risk sharing, avoids short

termism, SME support

• Agility and flexibility are needed when delivering innovation projects.

• Policy makers are keen to support gasification (especially heat & hvy duty)

– Need support technically, from the system perspective in particular

• Evidence and analytical skills

– Likely to need innovative delivery mechanisms

• Technical support during delivery phases

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

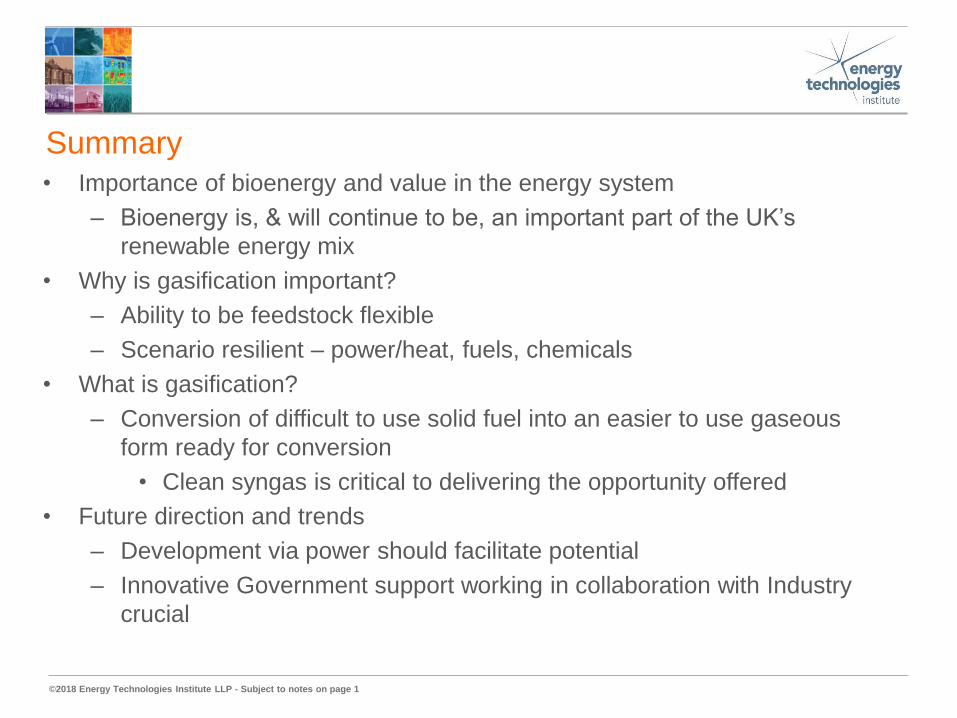

Summary

• Importance of bioenergy and value in the energy system

– Bioenergy is, & will continue to be, an important part of the UK’s

renewable energy mix

• Why is gasification important?

– Ability to be feedstock flexible

– Scenario resilient – power/heat, fuels, chemicals

• What is gasification?

– Conversion of difficult to use solid fuel into an easier to use gaseous

form ready for conversion

• Clean syngas is critical to delivering the opportunity offered

• Future direction and trends

– Development via power should facilitate potential

– Innovative Government support working in collaboration with Industry

crucial

©2018 Energy Technologies Institute LLP - Subject to notes on page 1

For more information

about the ETI visit

www.eti.co.uk

For the latest ETI news

and announcements

email [email protected]

The ETI can also be

followed on Twitter

@the_ETI

Registered Office

Energy Technologies Institute

Charnwood Building

Holywell Park

Loughborough

LE11 3AQ

For all general enquiries

telephone the ETI on

01509 202020