gasb 68 in 2006 the governmental accounting standards board (gasb) began a project to examine how...

TRANSCRIPT

GASB 68In 2006 the Governmental Accounting Standards Board (GASB) began a project to examine how Pension Plan liabilities and expense are determined and reported on the financial statements of governmental and quasi-governmental entities including Housing Authorities. An exposure draft was published in 2011 and the final standard - GASB 68 - in June 2012. It is effective for years beginning on or after June 15, 2014 (for PHA FYEs 6/30/2015, 9/30/2015, 12/31/2015 and 3/31/2016).

2

GASB 68 has a very significant impact on both the reporting of pension balances and activity, as well as related disclosures in the footnotes. If you would like a copy of GASB 68, it may be obtained (for free!) at the GASB website www.gasb.org (for a list of specific pronouncements you may see the link on their homepage for “standards and guidance” or you may go directly there from here):http://www.gasb.org/jsp/GASB/Page/GASBSectionPage&cid=1176160042391

This session will briefly summarize what GASB 68 means for PHAs and will help you to determine if and how this new standard will affect you.

3

ImpactsThe largest impacts of GASB 68 in the PHA-arena are for those agencies that have defined benefit plans. That is because, for the first time ever, PHAs will be required to report any unfunded pension liabilities on their balance. This is true even if you are in a state retirement plan. The annual pension expense will also be affected. GASB felt that this would provide more transparency regarding pension costs and that there would be no more “kicking the can down the road”. Defined contribution retirement plans will also be affected. So this has an impact on just about everybody. 4

5

6

GASB 68 Implementation Guide Note that GASB has published an

implementation guide for affected governmental entities including PHAs.

A full copy of the GASB 68 Implementation Guide may also be obtained from the GASB website for free, at www.gasb.org. Be advised that GASB 68 and the related Implementation Guide adds up to 500+ pages of reading material combined. This is complicated stuff!

7

GASB 68 revises the recognition,

measurement, and disclosure requirements for employers that provide retirement plans.

In the case of defined benefit pension plans, it will totally change the way net pension liabilities are reported, to include the entire pension liability minus the plan’s net position (assets minus liabilities in the plan).

More details to follow later in this session.

8

Pension Expense

It will also alter the way that changes in the net pension liabilities are reported. In many cases the change in the net pension liability will be recognized as an expense in the period the change occurred. In some cases it will be reported as a deferred inflow/outflow with the expense then recognized in future period(s).

9

Defined benefit plans provide retirement benefits based upon a set formula or schedule, that is not necessarily a function of how much has been contributed by the employer and/or employee. For example, let’s assume a given individual is eligible for a retirement benefit equal to 60% of his/her salary at retirement, based upon the years of service they have put in. The plan then collects from participating employers amounts needed to cover these benefits and of course the performance of investments in the plan also impacts the amount that needs to be contributed.

10

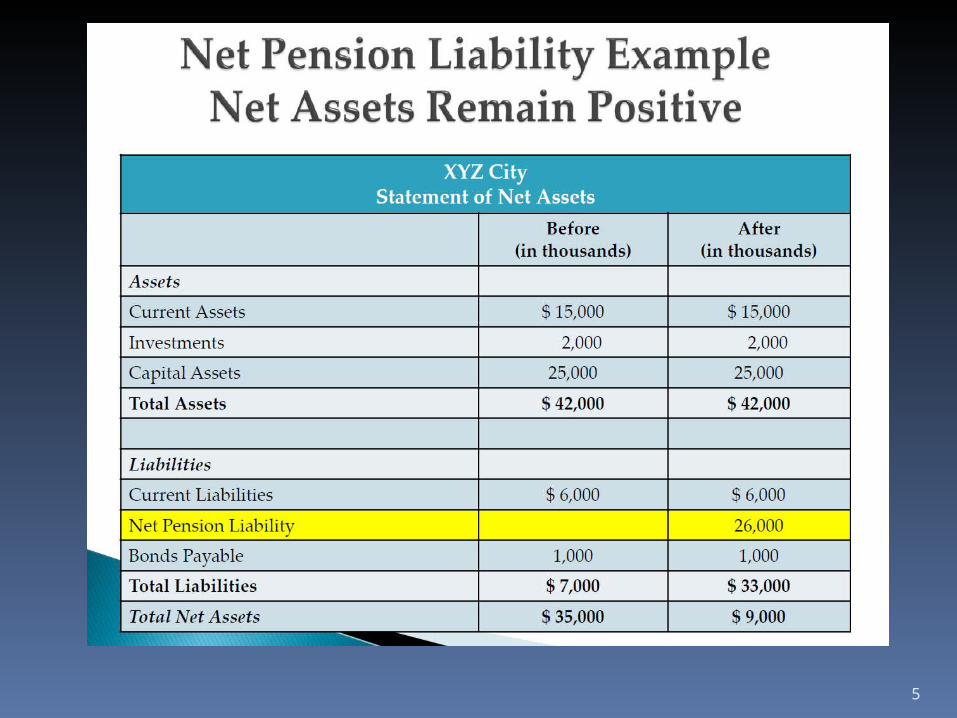

Unfunded Liability

Sometimes the contributions are not sufficient to fully fund all future benefits. In general the plan is then considered to be under-funded and in accordance with GASB 68 a liability will most likely need to be reported on the balance sheet of each participating employer, reflecting the unfunded portion of future benefit payments. This is the major purpose of GASB 68.

11

Defined contribution plans on the other hand provide retirement benefits that are based directly upon the amount contributed by employers / employees, plus any growth in the investments in the plan (investment income / capital gains). So what is contributed to the plan comes back out of the plan during retirement. It is not based upon a separate formula or schedule.

Given that defined contribution plans are easiest to explain, let’s start there.

12

Defined Contribution Plans

The GASB in its piece on defined contribution plans makes the distinction between defined benefit and defined contribution as follows: “Defined contribution pensions stipulate the contributions a government must make to an active employee’s account each year. A defined benefit pension plan, by contrast, specifies the benefits to be provided to the employees after the end of their employment.” (emphasis is mine) 13

Defined Contribution Retirement Plan Expense

The expense to be recognized when an employer such as a PHA has a defined contribution plan, is equal to the contributions required for that year in accordance with the plan, minus any amounts that were forfeited by employees (e.g. an employee terminates before becoming vested in the plan).

14

Defined Contribution Retirement Plan Liability Defined Contribution Plans often have

little or no pension liability associated with them. If the defined contribution pension expense exceeds the amount that was contributed, the difference will be reported as a liability. This typically occurs if there are contributions that are due for the fiscal year or other reporting period that were not remitted by the end of the fiscal year or other reporting period. (basically a year end payable due to timing difference).

15

Special Funding Situations If another entity is legally responsible for

some or all of the PHA’s defined contribution expense, and either (a) the amount the other entity is required to contribute is not based on events or circumstances unrelated to pensions, and/or (b) the contributing entity is the only entity legally required to contribute to the plan, then it is considered a “special funding situation”. What happens in this case is that the full pension expense is reported in the financial statements of the PHA and the third party non-PHA share is reported as revenue in the financial statements. 16

Defined Contribution Plan DisclosuresIn addition to the expense and possibly a liability as indicated above, the PHA’s financial statements must include footnote disclosures as follows:Description of the defined contribution pension plan and related benefits;The contribution rates for the PHA employer, for employees, and if applicable any third parties that are not the PHA or its employees;The amount of pension expense and;The amount of the employer’s outstanding liability if any. 17

The first step in implementing GASB 68 is determining plan type. There are generally three types of plans:1.Single employer plans – pretty self explanatory, these plans are dedicated to one employer. Not many PHAs, if any, will have a dedicated defined benefit plan just for them.2.Agent multi-employer plans – these are plans that cover more than one employer but track expense and liability data on each employer separately. Generally the assets of the plan are legally segregated by employer. 18

Three types of plans – continued3. Cost sharing multi-employer plans –

these plans do not segregate assets by employer, and the funds in the plan may therefore be used to pay benefits for any participating employer. Under GASB 68 cost sharing multi employer plans must calculate each employers “proportionate share” of the pension expense and pension liability. GASB dictates the options for plans to do so.

19

Pension Liabilities – 2 typesEmployers that provide defined benefit retirement plans may have to report liabilities from two possible sources: A liability due to the unfunded portion of future retirement benefits – a noncurrent liability (explained shortly).A separate liability, if applicable, for contributions payable at Fiscal Year End that have been assessed by the plan but not paid to the plan. This is a current liability, unless a portion of it is in a long-term installment agreement.

20

Unfunded Pension LiabilityThe Net Pension Liability is equal to:

The Total Pension Liability = TPL (equal to the net present value of

future benefit payments attributable to past periods of service)

minusThe Pension Plan’s Net Position (i.e.

the retirement plan’s assets, less plan liabilities)

EqualsThe Net Pension Liability = NPL 21

Additional Details As stated earlier this will typically be a

non-current liability. The calculation is based upon the

benefits earned, not the required funding due.

Determining the Total Pension Liability will typically require the services of an actuary.

If you are in a state or other multi-employer plan, chances are they will calculate this and provide it to you.

22

Applicable DatesThere are three different dates that may be used to measure the pension liability:An “actuarial valuation date” no more than 30 months plus 1 day prior to the Fiscal Year End of the employer (in this case GASB 68 requires “roll forward” procedures to be applied); A “measurement date” no earlier than the end of the prior fiscal year; orThe employers Fiscal Year End. The dates used for Total Pension Liability and the plan’s Net Position must, of course, correspond. Note that actuarial valuations must occur at least every two years. 23

Information to be Provided by a Multi Employer Plan If you are part of the state retirement

system or some other multi employer plan, whether it is an agent multi employer or a cost sharing plan, you should receive the following information within a reasonable timeframe that allows you to comply with GASB 68: Unfunded Pension Liability Current Year Pension Expense Deferred Outflow and Deferred Inflow Balances Information Needed For Disclosures

24

How Plans Will Calculate the Net Pension LiabilityCalculating the Net Pension Liability involves three steps: (1) first the plan will estimate what benefits will be paid out for current employees and retirees based upon current years of service and other factors affecting benefit amounts, (2) as shown on the earlier slide, this stream of estimated future benefit payments is then “discounted back” to determine the Net Present Value (NPV) – what this number represents is how much the plan would need to have “in the bank” so to speak, right now,

25

in order to satisfy all future benefit obligations, and(3) deduct the amount that the plan already has “in the bank” – actually the current Net Position of the retirement plan itself – its assets including cash, investments, receivables, etc, minus its liabilities.

When determining part 1 above, the estimate of what benefits will be paid out, the actuary employed by the plan will take into account current salaries, years of services, inflationary increases the plan is obligated to provide, etc. These are taken as they are based upon conditions at the date the liability is determined. 26

When determining the discounted Net Present Value of all future benefit payments for purposes of determining pension liability, there are two different discount rates that might be used by the plan:The realistic expected future return on retirement plan investments (e.g. 6-8%)Or, the rate for 20 year tax exempt municipal bonds AA Aa or higher (e.g 2-4%)

27

Discount Rates The realistic expected future return on

retirement plan investments 6-8% can be used for as long as the plan’s net assets are anticipated to be sufficient to pay benefits, as projected year by year into the future. This analysis takes into account contributions, investment earnings, retirement benefits, and administrative expenses.

The lower 2-4% rate -the 20 year tax exempt municipal bonds AA Aa or higher - is required for any years that the test above comes out negative - years in which a shortfall is anticipated.

28

Net Present Value

Imagine what a difference this can make in the calculation of Net Present Value – 2-4% versus 6-8%, in our example - considering the long term horizons involved.

29

The calculation of the Net Present Value

of future benefit payments is further complicated by the fact that the assessment of whether retirement plan net position is sufficient to cover anticipated benefits, is determined on a year by year basis (year 1, year 2, year 3, and so on). A projection is completed that can carry out many years, indicating each year with a discount rate of either (1) the rate of return on plan investments if the plan’s projected net position that year is enough to cover benefit payments (if there is NOT a shortfall), or (2) the 20 year muni bond rate it the plan’s projected net position that year is not enough to cover benefit payments. 30

This can result in the discount rate

varying by year, and GASB 68 requires that a single “blended” rate be calculated for all of the years used. The GASB 68 implementation guide provides an example of this calculation with numbers filled in. It is too complicated and voluminous to include in this seminar, considering that the plan will usually provide this information to the PHA. If you would like to see a detailed example, refer to the GASB 68 implementation guide, page 118 (gasb.org).

31

Accounting for Expense, Deferred Outflows and Deferred Inflows

An important part of understanding GASB 68 is recognizing how to account for the change in the Net Pension Liability (NPL) from one period to the next. The net change in the NPL from last Fiscal Year End to the current Fiscal Year End is, for the most part, current year pension expense. However, there are exceptions – items that are recognized as expense in future periods.

32

33

Certain changes in Net Pension Liability (NPL) will not immediately hit expense Changes in Actuarial Assumptions

(including Economic and Demographic items)

Differences between actual and assumed actuarial experience

Differences between projected earnings and actual earnings on investments

Changes in Proportionate Share Employer contributions made after

measurement date 34

35

Your Plan is to Report Deferred Outflows and Deferred Inflows This sounds really complicated but

the fact is unless you are in a single employer plan (very few PHAs if any are in that situation), the plan administrator should account for and report deferred outflows and inflows to you annually. I strongly recommend you ask that question asap.

36

Agent vs Cost Sharing I do recommend that you determine as

soon as possible if you are participating in a “cost sharing” plan. In that case the plan will need to calculate each of these elements (NPL, Expense, Deferred Outflow, Deferred Inflow) and then report to you your allocable share of each. This is because you would not have the data to do so.

Probably most Agent plans will also do this, but it is possible (though unlikely) that they could just provide the needed data to you and drop it in your lap, since Agent plans track everything separately by employer. 37

Employer Contributions

Any contributions made during the current fiscal year are to be treated as a reduction of the Net Pension Liability (NPL). What this means in reality of course is that when the NPL is updated these contributions will become part of the pension expense. So it makes little difference whether the contributions are coded as a debit to the liability or a debit to expense as far as I can tell.

38

Employer Contributions A similar situation exists with bad debt

write-offs. Technically under GAAP accounting bad debts are written off to the Allowance for Doubtful Accounts, and then when the Allowance is updated periodically the write-offs flow through to expense. Many PHAs take the write-offs directly to expense – and essentially end up at the same place (that is, with the same amount of expense either way). To me, the same applies to employer retirement contributions, so I don’t understand why GASB requires this.

39

Pension Contributions made after the measurement date In a defined benefit pension plan, if

there are employer contributions that are made after the measurement date for the Net Pension Liability (NPL), these are shown as a deferred outflow, and not as expense nor a reduction to the NPL. These contributions will reduce the NPL in the following fiscal year.

Most PHAs will have this situation, unless your year end is the same as the plan year end.

40

Recording retirement contributions made after measurement dateThis fiscal year end:

Dr Deferred Outflow of Resources – Pension PlansCr Cash To record pension contributions made after the measurement date

Next fiscal year:Dr Net Pension Liability (or expense is ok)Cr Deferred Outflow of Resources – Pension Plans To reclassify pension contributions made in previous fiscal year after measurement date, from deferred outflow to reduce net pension liability

41

Accounting Issues

At the end of fiscal year 6/30/2015, 9/30/2015, 12/31/2015 or 3/31/2016, the Housing Authority will need to make an entry to book the Net Pension Liability (NPL), current year expense, deferred outflows of resources, deferred inflows of resources, and other items. Note that the net amount of the pension liability balance at the beginning of this first implementation/transition year will not be charged to expense, but will be a charge to beginning net position (equity), like a prior period adjustment. 42

Prior Period Adjustment

Therefore the initial entry will be as follows for the NPL beginning balance as of July 1, 2014, October 1, 2014, January 1 2015, or April 1, 2015:Dr Net Position (i.e. Equity)Cr Net Pension LiabilityTo record beginning balance of NPL

What about allocating this liability between programs?

43

Allocation of NPL

GASB has given no guidance regarding allocation of the Net Pension Liability between programs, as far as I can tell

HUD has give no guidance regarding allocation of the Net Pension Liability between programs

In fact, an online search has yielded no results on this, everybody seems to be ignoring it or maybe just “stymied”!

44

Allocation of NPL (cont’d) So what is the “correct” way to allocate

the Net Pension Liability / NPL? It seems like this would involve:

Step 1 Determining for each current worker and retiree every program that they have worked in, and how much the liability increased during the time they worked for that program, or at least the amount of salary each was paid in that timeframe

Step 2 (good luck with that)

45

Allocation of NPL (cont’d) I suppose a more realistic alternative

would be to just allocate the liability based upon current labor cost in each program – this is not 100% correct, but what else can we do?

Other Ideas?

46

COCC and Legacy Liabilities What we will give up with this

simplified method of allocation (for those PHAs that have COCCs) is the opportunity to fund the NPL as of the date you entered Asset Management with AMP, HCV, and other funds.

In other words HUD per the PIH 2007-9 supplement allowed COCC legacy liabilities to be funded from federal programs.

Can you determine what your NPL was in 2008 when you converted?

47

Year End Accounting

At some point you will receive a reconciliation or statement for the retirement plan (PERS, or equivalent).

Hopefully, the statement will reflect the unfunded pension liability (i.e. the NPL), the amount of deferred outflows, the amount of deferred inflows, and the pension expense.

This information will likely be as of the plan’s fiscal year end, but could be as of your fiscal year end. Remember the allowable measurement dates.

48

Year End EntryEach of the following entries would be made to update to the current balance as of the required measurement date per the plan statement:Dr Deferred Outflows of ResourcesCr Deferred Inflows of ResourcesCr Net Pension LiabilityDr/Cr Pension Expense for the net result of the above three itemsCould also include: administrative expense if not already recorded

49

Reporting of these balancesITEM CATEGORY

Net Pension Liability – Beginning Balance

Net Pension Liability – Ending Balance

Pension Expense Deferred Outflows Deferred Inflows

Prior Period Adjustment, is not recorded as expense

Long Term Liability, unless there is a payable at FYE

Income Statement Bal Sheet below Assets Bal Sheet below Liabilities

50

Special Funding SituationsIf another entity is legally responsible for some or all of the PHA’s defined benefit expense, and (a) the amount the other entity is required to contribute is not based on events or circumstances unrelated to pensions, and/or (b) the contributing entity is the only entity legally required to contribute to the plan, then it is considered a “special funding situation”.

51

Reporting Examples

52

Reporting Examples

53

Reporting Examples

54

Special Funding (Continued)Mentioned under the section for defined contribution plans and it also applies to defined benefit plans. In the PHA world this could occur if the employees are under the City or County plan and the City or County covers the cost. What happens in this case is that the full pension expense is reported in the financial statements of the PHA (the contribution from the PHA as well as the third party, such as the City or County). Then the third party, non-PHA share, is reported as revenue in the financial statements reflecting their contribution.

55

Note Disclosures and Required Supplementary Information (RSI) The Notes and RSI required by GASB

68 are BRUTAL. The remainder of this session will be

dedicated to providing a list of mandatory disclosures and required supplementary information.

56

Note disclosures Descriptive information on the plan,

including: Type of plan and the administrator Benefit terms including types of

benefits, key elements of the benefit formula, classes of employees covered, etc

Basis and authority for contributions, rates, and contributions in the reporting period

Availability of plan report57

Significant assumptions related to the

Total Pension Liability (TPL) Inflation, salary changes,

postemployment benefit changes, mortality assumptions, experience studies

Information concerning the discount rate – the rate, assumptions used, how the rate was determined for anticipated return on plan investments, how the rate was determined for the 20yr muni bond, which periods each was applied to, and other related information

58

Information regarding the pension plan’s fiduciary net position or reference to the plan report

The measurement date The actuarial valuation date Changes in: assumptions, other

inputs, benefit terms Changes subsequent to

measurement date Pension expense in current reporting

period

59

Deferred outflows and inflows of resources Balances by source Net Impact on pension expense in

each of the next 5 years Amount that will be a reduction of

the Net Pension Liability

60

For single plans and agent multi-

employer plans: Number of employees covered,

active and inactive Allocated insurance contracts Schedule of changes in Net Pension

Liability by source for the reporting period including service cost, interest, benefit changes, contributions by source, plan investment income, etc

All data concerning special funding situation if applicable

61

For cost sharing multi-employer plans: Employers allocated proportion,

basis for the allocation, and the change in the allocation

Employers proportionate share of NPL

Data concerning special funding situation if applicable

Third party proportionate share Employer’s proportionate share

62

Required Supplementary Information - Agent Plans 10 year schedules for the following:

Changes in Net Pension Liability (NPL) by source

Total Pension Liability (TPL), Pension Plan’s Net Position, Net Pension Liability (NPL), Pension Plan’s Net Position expressed as percentage of TPL, covered employee payroll, NPL as percentage of covered employee payroll (this information may be presented with first item, changes in Net Pension Liability by source

63

Actuarially determined employer

contribution (ADEC), contributions in relation to ADEC, difference, covered employee payroll, contributions as percentage of covered employee payroll

If there is no ADEC, then the statutory or contractual contribution requirements

Notes to RSI with methods and assumptions for ADEC and significant changes

64

Additional Required Supplementary Information for Cost Sharing Plans 10 year schedules for the following:

Employer’s proportionate share of NPL expressed as a percentage, the proportionate share of NPL expressed as an amount, covered employee payroll, proportionate share as a percentage of covered-employee payroll, pension plan’s net position as a percentage of TPL

65

If there is a special funding situation, then also the third party’s proportionate share and employers proportionate share

If there are statutory and/or contractual contribution requirements, the required contributions, contributions in relation to those required, difference, covered employee payroll, and contributions as a percentage of covered employee payroll

66