gasb 61, the financial reporting entity purpose & … · 11/12/2012 2 gasb 61, the financial...

TRANSCRIPT

11/12/2012

1

GASB Statement No. 61, The Financial Reporting Entity: Omnibus An Amendment of GASB Statements No. 14 and No. 34Presented byAndrew Richards, CPA, PartnerChristopher Telli, CPA, Senior ManagerNovember 13, 2012

GASB 61, The Financial Reporting EntityPurpose & Objective

• Amends GASB Statement 14 & 34 to improve financial reporting for a governmental financial reporting entity

• Clarifies/Amendso Financial Accountability Concept

o “Misleading to Exclude” criteria

o Blending criteria

o Reporting of equity interest in legally separate organizations

4

11/12/2012

2

GASB 61, The Financial Reporting EntityPurpose & Objective

• Improves guidance relating to component units & equity interest transactions, making financial statements more relevant

• Allows users to better assess accountability of elected officials

• Improves focus of the financial reporting entity on the primary government & allows for better distinction of primary government (PG) & component unit (CU)

• Helps ensure PG doesn’t understate financial position for equity interests

5

• Provisions of this Statement are effective for financial statements for periods beginning after June 15, 2012

o Earlier application is encouraged

6

GASB 61, The Financial Reporting Entity Effective Date

11/12/2012

3

• Primary governments

• Stand-alone governments

• Separately issued financial statements of governmental components

• Nongovernmental component units when included in a governmental financial reporting entity

7

GASB 61, The Financial Reporting Entity Scope

• Component unit: Legally separate organizations for which elected officials of the primary government are financially accountable. In addition, a component unit can be another organization for which the nature and significance of its relationship with a primary government is such that exclusion would cause the reporting entity's financial statements to be misleading

⁰ Can be governmental organization, nonprofit of for-profit corporation

8

GASB 61, The Financial Reporting Entity Component Unit Definition

11/12/2012

4

• GASB 14 requires inclusion of a legally separate entity if it’s fiscally dependent on the primary government

o GASB 61 amends this to ALSO require a financial benefit or burden relationship, in addition to being fiscally dependent

o If the financial accountability concept is met, the organization should be reported as part of the primary government’s financial reporting entity

9

GASB 61, The Financial Reporting Entity Amended Inclusion Criteria

GASB 61, The Financial Reporting Entity Amended Inclusion Criteria

• Fiscally dependent: A government that cannot do one or more of the following without the substantive approval of another government: (a) determine and modify its budget, (b) levy taxes or set rates or charges, or (c) issue bonded debt

• A financial benefit or burden relationship exists if the primary government is

o Legally entitled to or can access the organization’s resources

o Legally obligated or has otherwise assumed the obligation to finance deficits of, or provide financial support to the organization

o Obligated in some manner for debt of the organization

10

11/12/2012

5

GASB 61, The Financial Reporting Entity Amended Inclusion Criteria

• The primary government is financially accountable if it appoints voting majority of the organization’s governing board &

1. It is able to impose its will on the organization, OR

2. There is potential for the organization to provide specific financial benefit to, or burden on, the primary government

11

• Primary government may be financially accountable for a fiscally dependent government even if that government has a:

1) Separately elected governing board (elected school board but fiscally dependent on local government)

2) Governing board appointed by a higher level of government (school board appointed by State officials but fiscally dependent on local government)

3) Jointly appointed board (board appointed jointly by several local governments but fiscally dependent on one)

12

GASB 61, The Financial Reporting Entity Amended Inclusion Criteria

11/12/2012

6

Question #1

It is possible for a component unit of a municipality to be which of the following a) another governmental organizationb) a for-profit corporationc) a not-for-profit corporationd) all of the abovee) Not sure

13

• Potential for dual inclusiono Organization could meet financial accountability criteria

for one primary government, but fiscally dependent on another

o Can only be component unit in one reporting entityo Requires careful judgment o Generally, fiscal dependency will govern, but not always

14

GASB 61, The Financial Reporting Entity Amended Inclusion Criteria

11/12/2012

7

• Paragraphs 12, 20, 39 and 66 of Statement 14 allowed for legally separate entities to be included as component units, even if they do not meet criteria for inclusion, if exclusion would make the financial statements misleading or incomplete

• GASB 61 eliminates “incomplete” & amends GASB 14 to clarify the manner in which “misleading to exclude” provisions should be applied in making this determination

15

GASB 61, The Financial Reporting Entity “Misleading to Exclude” Criterion

• For organizations not meeting the financial accountability criteria

o Management may include if professional judgment determines exclusion is misleading

o Determinations based on nature & significance of organization’s relationship to primary government

o Should be applied for all separately issued financial statements

16

GASB 61, The Financial Reporting Entity “Misleading to Exclude” Criterion

11/12/2012

8

• GASB 61 further clarifies what types of relationships should be considered when determining if misleading to exclude

o Closely related or financially integrated Closely related: Focus on financial relationships

Financially integrated: Documented through policies, practices or organizational documents of either primary government or the organization being evaluated

17

GASB 61, The Financial Reporting Entity “Misleading to Exclude” Criterion

• Clarifies types of relationships that affect the determination of major component units

• Eliminates requirement to consider each component unit’s significance relative to other component units

• Requires consideration of nature and significance of relationship to primary government

o Services providedo Transactionso Significant burden or benefit relationship

18

GASB 61, The Financial Reporting Entity Major Component Unit Requirement

11/12/2012

9

• Presentation & reporting requirementso Major component unit reporting requires one of the

following Presenting each major component unit in a separate column in

the reporting entity’s statements of net assets & activities

Combining statements of major component units in reporting entity’s basic financial statements after the fund financial statements, or

Presenting condensed financial statements in notes

o Nonmajor component units should be aggregated in a single column

o Combining statements allowed but not required19

GASB 61, The Financial Reporting Entity Major Component Unit Requirement

Question #2

An organization is included with a primary government’s reporting entity if that organization is fiscally dependent ANDa) A potential financial benefit or burden relationship

existsb) The primary government appoints all of the board

membersc) The entity is not a component unit of another

governmentd) the entity has a derivative instrumente) Not sure

20

11/12/2012

10

• Amends paragraph 53 of Statement No. 14 to include additional provision when governing bodies are substantively the same

• Adds provision for component units whose total debt outstanding is expected to be repaid entirely or almost entirely with resources from primary government

21

GASB 61, The Financial Reporting Entity Blending Criteria

GASB 61, The Financial Reporting Entity Blending Criteria

• Substantively the sameo Sufficient representation of primary government’s entire

governing body on the component unit’s governing body so decisions of the primary government cannot be overridden by component units

o Happens when primary government’s board is essentially the same as component unit’s board

o Example: city redevelopment authority is comprised entirely, or almost entirely, of city council members

22

11/12/2012

11

• Blending method should be used when governing bodies substantively the same

&

o There is financial benefit or burden relationship

OR

o Management of the primary government has operational responsibility for component unit

23

GASB 61, The Financial Reporting Entity Blending Criteria

GASB 61, The Financial Reporting Entity Blending Criteria

• Operational responsibilityo Management in this context are people below the

governing board Responsible for day-to-day operation

o Achieved if management manages activities of the component unit in essentially the same manner in which it manages its own programs, departments or agencies

24

11/12/2012

12

• Blending method should also be used ifo Services provided by component unit are entirely, or almost

entirely, to primary government or exclusively, or almost exclusively, benefits primary government Similar to internal service funds

o Requirement still met if Services provided to others are insignificant to overall activities of

component unit Services are provided indirectly to primary government (i.e. to

employees)

25

GASB 61, The Financial Reporting Entity Blending Criteria

• Blending also required for component units whose total debt outstanding, including leases, is expected to be repaid entirely, or almost entirely, with resources of primary government

o New Requiremento Repayment generally occurs through continuing pledge &

appropriation by the primary government to component unit

26

GASB 61, The Financial Reporting Entity Blending Criteria

11/12/2012

13

• Reporting blended component unitso Statement clarifies that funds of a blended component

unit have the same financial reporting requirements as a fund of primary government Included as part of primary government’s other funds in fund

statements &/or combining statements

General fund of blended component unit is still reported as a special revenue fund

27

GASB 61, The Financial Reporting Entity Blending Criteria – Reporting

Question #3

Major component units should be determined based on: a) The component unit's significance to other

component unitsb) The component unit's total assetsc) The component unit's total net assetsd) The component unit's significance to the primary

governmente) Not sure

28

11/12/2012

14

GASB 61, The Financial Reporting Entity Blending Criteria – Reporting• Business-type activities

o Business-type activity (BTA) that reports in a single column may blend component unit into single column Present condensed combining information in notes Condensed information should include (minimum)

Condensed statement of net assets Condensed statement of revenues, expenditures & changes in net assets Condensed statement of cash flows

o May also show blended component unit in separate column & combining primary government total column

o Multi-column BTA may add additional columns as if fund of primary government

29

• The Statement clarifies reporting of equity interests in legally separate organizations

o Primary government should report an asset for its equity interest in a discretely presented component unit If government’s intent is to directly enhance its ability to

provide governmental services, it should be discretely presented as a component unit

If government’s intent is to obtain income or profit, it should report equity as investment

o Minority interest in joint ventures are shown in net assets as “restricted, nonexpendable”

30

GASB 61, The Financial Reporting Entity Reporting Equity Interests in Component Unit

11/12/2012

15

• Clarifies that governments should disclose the rationale for including each component unit & manner in which it is included

• Additionally, notes should includeo Brief description of the component unit and its

relationship to primary governmento If component unit is discretely presented, blended or

included in the fiduciary fund financial statementso How separate financial statements for component

units may be obtained

31

GASB 61, The Financial Reporting Entity Amendments to Note Disclosures

GASB 61, The Financial Reporting Entity Amendments to Note Disclosures

• Notes essential to fair presentation in reporting entity’s basis financial statements include

o Governmental & business-type activities, major funds, nonmajor funds, including blended component units

o Major discretely presented component units (DPCU)

• Selected DPCU disclosures throughout noteso Use professional judgmento Determined on component unit by component unit basis

32

11/12/2012

16

GASB 61, The Financial Reporting Entity Impact

• Expected some component units may no longer meet inclusion criteria under new Standard

• Not expecting the reverse

• All component units will need reevaluation by primary government

• Blending must be reevaluated under new criteria o If no longer meets requirements to blend, then discretely

presented (de-blended)

• Change in reporting entity will result in restatement 33

Question #4

The blending criteria of GASB 61 is met if the governing bodies are substantively the same anda) A financial benefit or burden relationship existsb) The entities are financially integratedc) The financial statements are not otherwise

incompleted) It's based solely on professional judgmente) Not sure

34

11/12/2012

17

35

GASB 61, The Financial Reporting Entity Transition• In first period applied, treated as adjustment of prior

periods & restatement of all prior periods

• If restatement is not practical, cumulative effect should be reported as a restatement of beginning net assets (or fund equity or fund balance, as appropriate) for earliest period restated

• Financial statements should disclose nature of restatement & its effect

Component Unit Evaluation Flowchart

36

11/12/2012

18

GASB 61, The Financial Reporting Entity

Examples

All examples taken from GASB 2011-12 Comprehensive Implementation Guide

37

GASB 61, The Financial Reporting EntityExamples – Case 6

Case 6 – Board of Education with Appointed MembersFacts: Local boards of education are created as bodies corporate. The county board of commissioners appoints members of the board of education for municipalities located within the county, but may remove members only for cause. The local boards of education select their own management and control their own day-to-day operations.

State law gives the state legislature the responsibility for providing a uniform system of free public schools. Accordingly, the state grants the county the following budgetary authority:Local school boards submit their entire budget to the county commissioners.The county commissioners make appropriations to the local boards of education for that portion of the budget that is to be funded by the county.

The county commissioners approve the local school boards' budgets, which are then adopted by the local school boards.If the county board allocates funds specifically to certain purposes or functions, the local boards of education are permitted to change the appropriation for the intended program or purpose within certain limits.Changes in the school budget resolution, whether increases or decreases to projects in (1) acquisition of land or (2) building acquisition and construction, require county commissioner approval.

38

11/12/2012

19

GASB 61, The Financial Reporting EntityExamples – Case 6 (cont.)Case 6 – Board of Education with Appointed Members (cont.)

The county may allocate part or all of each appropriation by purpose, function or project.

The authority of the county is limited by a statutory requirement that the county provide adequate school facilities. However, the county has no authority over the administration of the construction. A local board of education has legal recourse if it feels that the county is not providing adequate facilities or is not fulfilling its statutory funding responsibilities. A clerk of court or a judge can order a county to increase its financial support of a local board of education.

Conclusion: The local board of education would be discretely presented as a component unit of the county. The county board of commissioners appoints the members of each local board of education and is able to impose its will through its budgetary authority, which grants the county approval authority over the entire budget and thus is not merely a compliance approval required as a condition to receive financial aid. In addition, the county commissioners have approval authority over the capital acquisitions of the local board of education.

39

GASB 61, The Financial Reporting EntityExamples – Case 6aCase 6a – Board of Education with Elected Members

Facts: Consider the same facts as in Case 6, except that the members of the local board of education are separately elected.

Conclusion: If the members of the local board of education are separately elected, the board of education would be evaluated as a component unit of the counties county based on the fiscal dependency criteria, which include the financial benefit or burden criteria. The board of education is fiscally dependent on the county based on the county’s budgetary approval authority. In addition, the local board of education imposes a financial burden because the county provides resources for its operations.The board should be reported as a discretely presented component unit.

40

11/12/2012

20

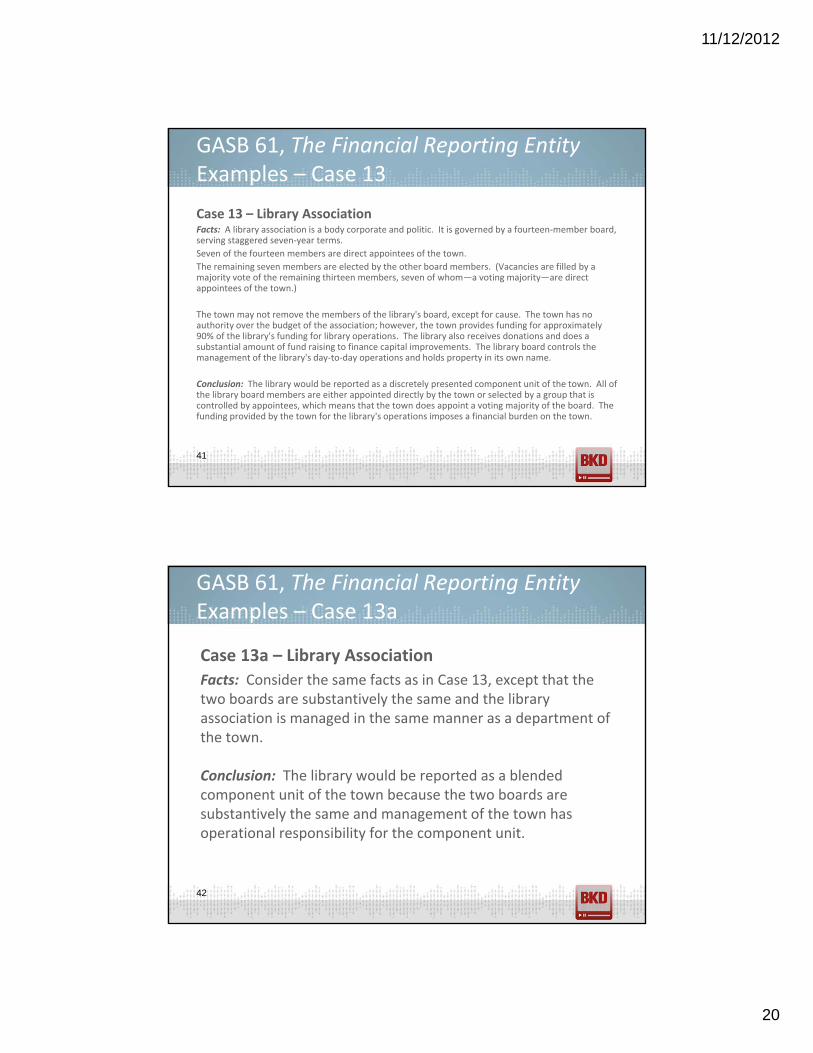

GASB 61, The Financial Reporting Entity Examples – Case 13Case 13 – Library AssociationFacts: A library association is a body corporate and politic. It is governed by a fourteen-member board, serving staggered seven-year terms.Seven of the fourteen members are direct appointees of the town.The remaining seven members are elected by the other board members. (Vacancies are filled by a majority vote of the remaining thirteen members, seven of whom—a voting majority—are direct appointees of the town.)

The town may not remove the members of the library's board, except for cause. The town has no authority over the budget of the association; however, the town provides funding for approximately 90% of the library's funding for library operations. The library also receives donations and does a substantial amount of fund raising to finance capital improvements. The library board controls the management of the library's day-to-day operations and holds property in its own name.

Conclusion: The library would be reported as a discretely presented component unit of the town. All of the library board members are either appointed directly by the town or selected by a group that is controlled by appointees, which means that the town does appoint a voting majority of the board. The funding provided by the town for the library's operations imposes a financial burden on the town.

41

GASB 61, The Financial Reporting EntityExamples – Case 13a

Case 13a – Library AssociationFacts: Consider the same facts as in Case 13, except that the two boards are substantively the same and the library association is managed in the same manner as a department of the town.

Conclusion: The library would be reported as a blended component unit of the town because the two boards are substantively the same and management of the town has operational responsibility for the component unit.

42

11/12/2012

21

GASB 61, The Financial Reporting EntityExamples – Case 21

Case 21 – Art FoundationFacts: The Carol Sauer Art Foundation was established as a legally separate, tax-exempt organization to support fine arts in the greater Anytown metro area. The foundation has a history of providing substantial financial support to several different entities each year including XYZ Art Museum, Anytown’s public museum; community theatre groups; and other organizations with objectives consistent with the foundation’s charter. Occasionally, donations received by the foundation are restricted for the benefit of specific organizations, but generally, restricted donations are distributed currently, rather than held. An accumulation of restricted resources would not be significant to any of the designated beneficiaries. The support given to XYZ Art Museum during the current year was significant to the museum. However, depending on the ongoing needs of other qualifying organizations and the foundation’s resources available for distribution, this level of support to the museum has varied considerably over the years.

Conclusion: The Carol Sauer Art Foundation is not required to be reported as a component unit of XYZ Art Museum because at least one of the three criteria is not satisfied. The “direct benefit” criterion is not met because the foundation supports several other organizations, and the resources it receives and holds are not entirely or almost entirely restricted for the benefit of XYZ Art Museum. Because the first criterion is not met, neither the “entitlement/ability to access” criterion nor the “significance” criterion needs to be considered. However, the “incomplete or misleading to exclude” concept in paragraph 41 of Statement 14, as amended, should be considered.

43

Andrew Richards, CPA | Partner | 501.372.1040 | [email protected]

Christopher Telli, CPA | Senior Manager | 719.471.4290 | [email protected]

11/12/2012

22

4545

Continuing Professional Education (CPE) Credits

BKD, LLP is registered with the National Association of State Boards of Accountancy (NASBA) as a sponsor of continuing professional education on the National Registry of CPE Sponsors. State boards of accountancy have final authority on the acceptance of individual courses for CPE credit. Complaints regarding registered sponsors may be submitted to the National Registry of CPE Sponsors through its website: www.learningmarket.org.

The information in BKD webinars is presented by BKD professionals, but applying specific information to your

situation requires careful consideration of facts & circumstances. Consult your BKD advisor before acting

on any matters covered in these webinars.

4646

CPE Credit

• Up to 1 CPE credit will be awarded upon verification of participant attendance; however, credits may vary depending on state guidelines

• For questions, complaints or comments regarding CPE credit, please email the BKD Learning & Development Department at [email protected]