gas flaring reduction: opec views opec secretariat

TRANSCRIPT

Gas Flaring Reduction: OPEC Views

OPEC Secretariat

Outline of presentation

• Energy demand growth forecasts and impact on associated gas volumes and flaring

• OPEC gas flaring history and progress and specific examples of gas flaring reduction in OPEC Member Countries

• Gas flaring reduction challenges

• Joint OPEC/ World Bank workshop on gas flaring and potential role of GGFR in facilitating financing and carbon credits

• Concluding remarks

World energy demand by fuel type(mtoe)

0

2000

4000

6000

8000

10000

12000

14000

16000

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

mto

e

Oil

Hydro/nuclear/renewables

Coal

Gas

History Projection Growth (% pa) Fuel shares (%) 2005-2025 2005 2010 2020 2025

Oil 1.6 39.7 39.5 39.2 38.9 Solids 1.2 26.7 26.2 25.0 24.3 Gas 2.6 23.7 24.7 27.0 28.3 Hyd/Nuc/Ren 0.9 9.9 9.6 8.9 8.5 Total 1.7 100.0 100.0 100.0 100.0

Oil supply outlook, mb/d (reference case)

2005 2010 2015 2020 2025

OECD 20.5 20.6 20.7 20.5 19.5

DCs, excl. OPEC 16.1 18.6 19.7 20.0 19.9

Transition economies 11.7 14.4 15.5 16.1 16.5

Total non-OPEC 50.1 55.8 58.3 59.4 58.9

OPEC (incl. NGLs) 33.1 34.9 39.7 46.2 54.3

World 83.2 90.7 98.0 105.6 113.1

Evolution of gas flaring

0

50

100

150

200

250

Flar

ed G

as -

BC

M p

er Y

ear

OPEC Flared

Non-OPEC Flared

Global Gas Flared

Source: OPEC

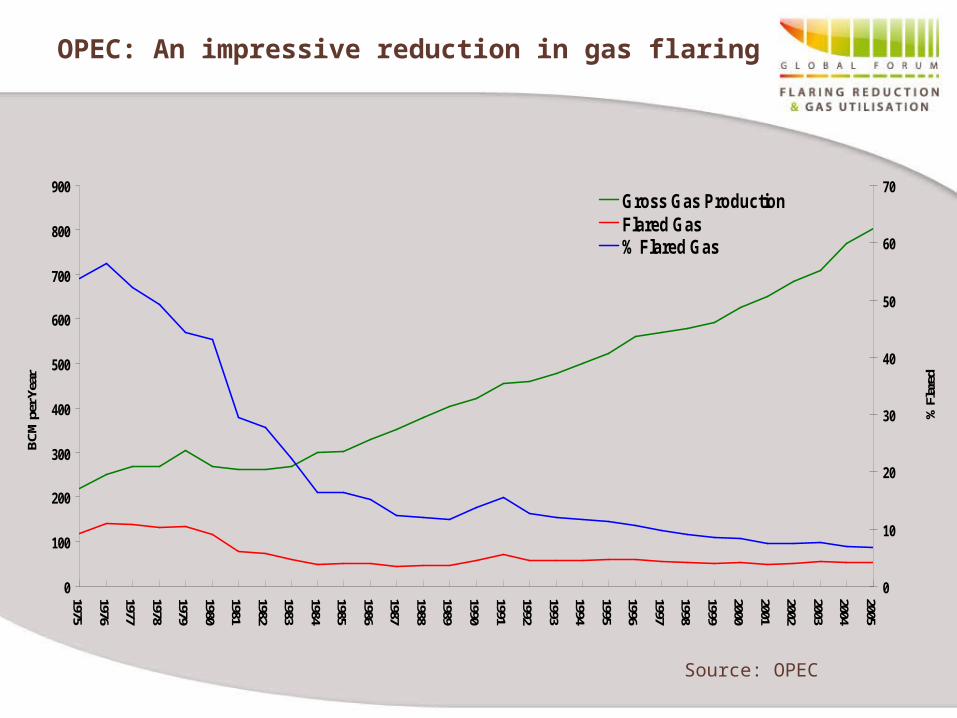

OPEC: An impressive reduction in gas flaring

Source: OPEC

BC

M p

er Y

ear

0

100

200

300

400

500

600

700

800

900

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

% F

lare

d

0

10

20

30

40

50

60

70Gross Gas ProductionFlared Gas% Flared Gas

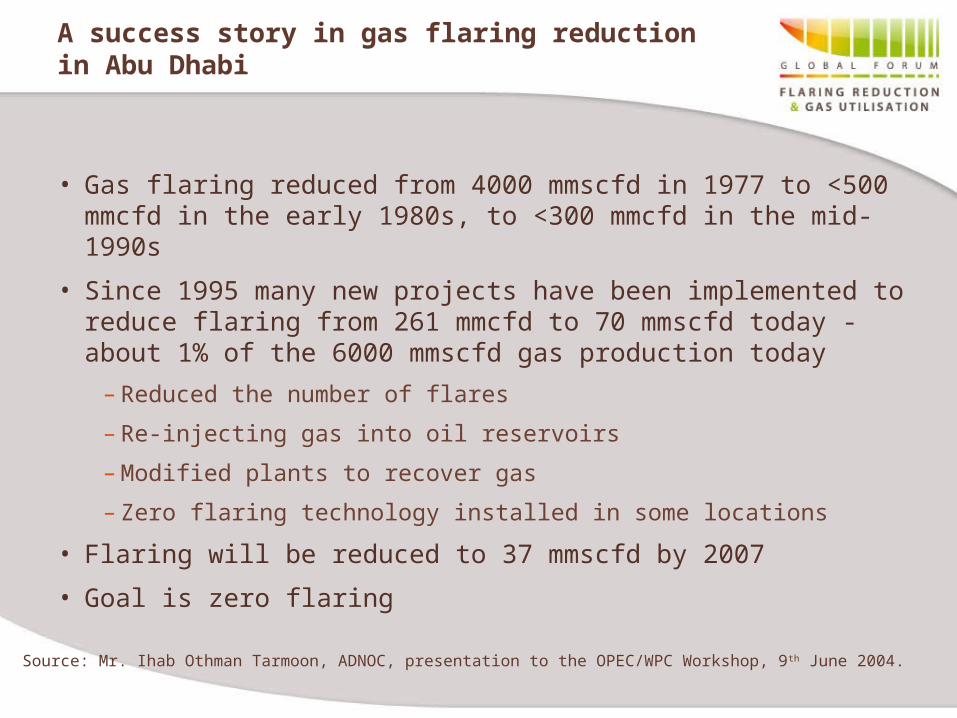

A success story in gas flaring reduction in Abu Dhabi

• Gas flaring reduced from 4000 mmscfd in 1977 to <500 mmcfd in the early 1980s, to <300 mmcfd in the mid-1990s

• Since 1995 many new projects have been implemented to reduce flaring from 261 mmcfd to 70 mmscfd today - about 1% of the 6000 mmscfd gas production today

– Reduced the number of flares

– Re-injecting gas into oil reservoirs

– Modified plants to recover gas

– Zero flaring technology installed in some locations

• Flaring will be reduced to 37 mmscfd by 2007

• Goal is zero flaring

Source: Mr. Ihab Othman Tarmoon, ADNOC, presentation to the OPEC/WPC Workshop, 9 th June 2004.

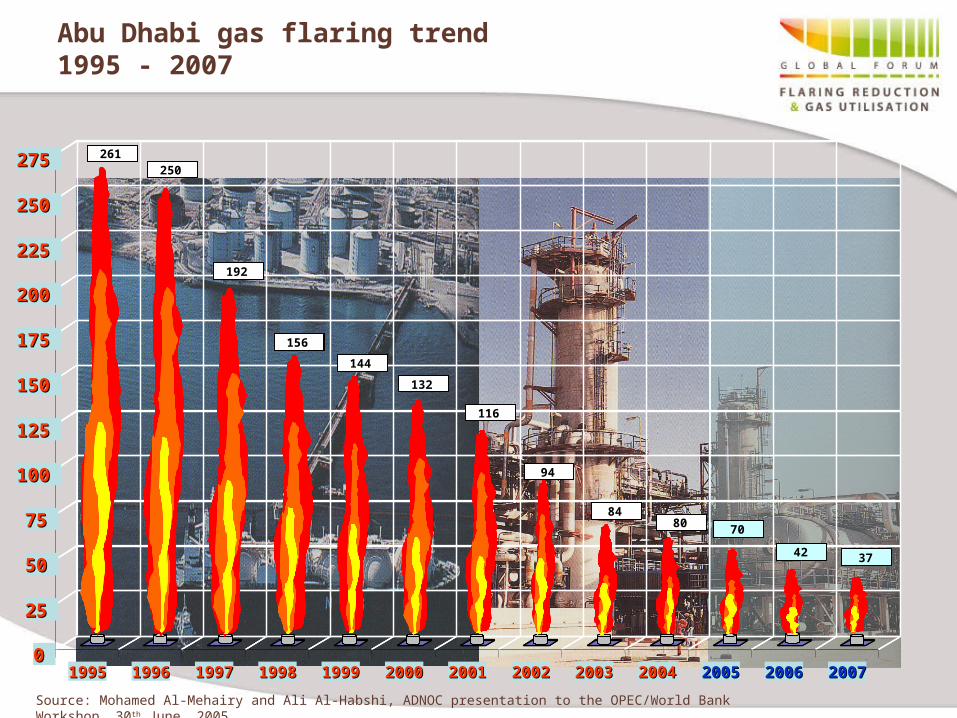

Abu Dhabi gas flaring trend 1995 - 2007

Source: Mohamed Al-Mehairy and Ali Al-Habshi, ADNOC presentation to the OPEC/World Bank Workshop, 30th June, 2005

0

25

50

75

100

125

150

175

200

225

250

275

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

261250

192

156

94

144

132

116

7461 53

38 35

0

25

50

75

100

125

150

175

0 0

25 25

50 50

75 75

100 100

125 125

150 150

175 175

200 200

225 225

250 250

275 275

19951995 19961996 19971997 19981998 19991999 20002000 20012001 20022002 20032003 20042004 20052005 20062006 20072007

261250

192

156

94

144

132

116

8480 70

42 37

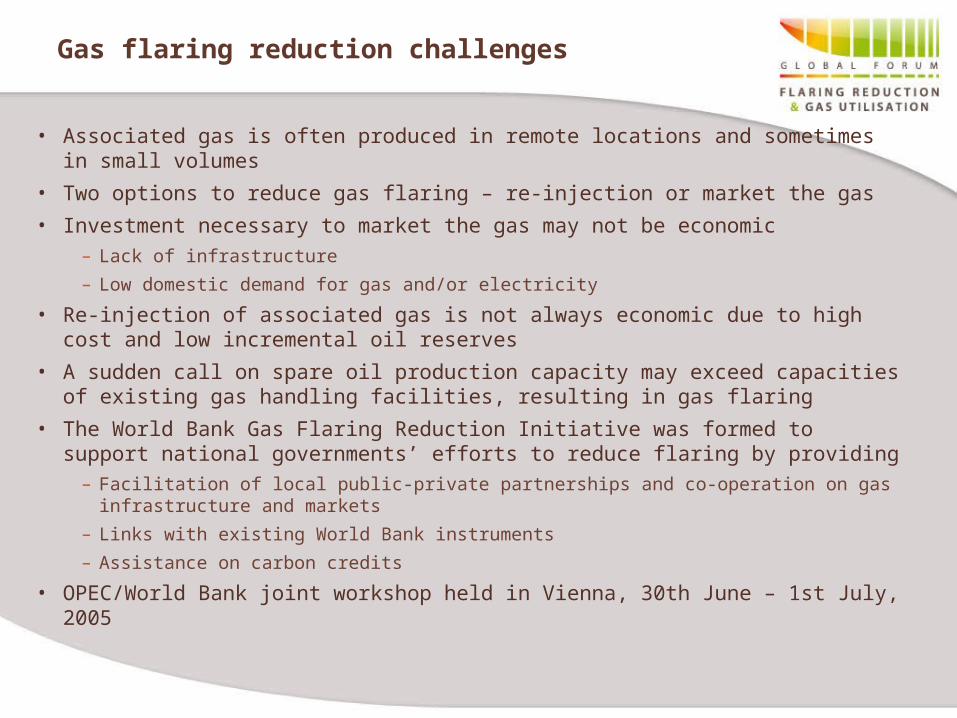

Gas flaring reduction challenges

• Associated gas is often produced in remote locations and sometimes in small volumes

• Two options to reduce gas flaring – re-injection or market the gas

• Investment necessary to market the gas may not be economic– Lack of infrastructure

– Low domestic demand for gas and/or electricity

• Re-injection of associated gas is not always economic due to high cost and low incremental oil reserves

• A sudden call on spare oil production capacity may exceed capacities of existing gas handling facilities, resulting in gas flaring

• The World Bank Gas Flaring Reduction Initiative was formed to support national governments’ efforts to reduce flaring by providing

– Facilitation of local public-private partnerships and co-operation on gas infrastructure and markets

– Links with existing World Bank instruments

– Assistance on carbon credits

• OPEC/World Bank joint workshop held in Vienna, 30th June – 1st July, 2005

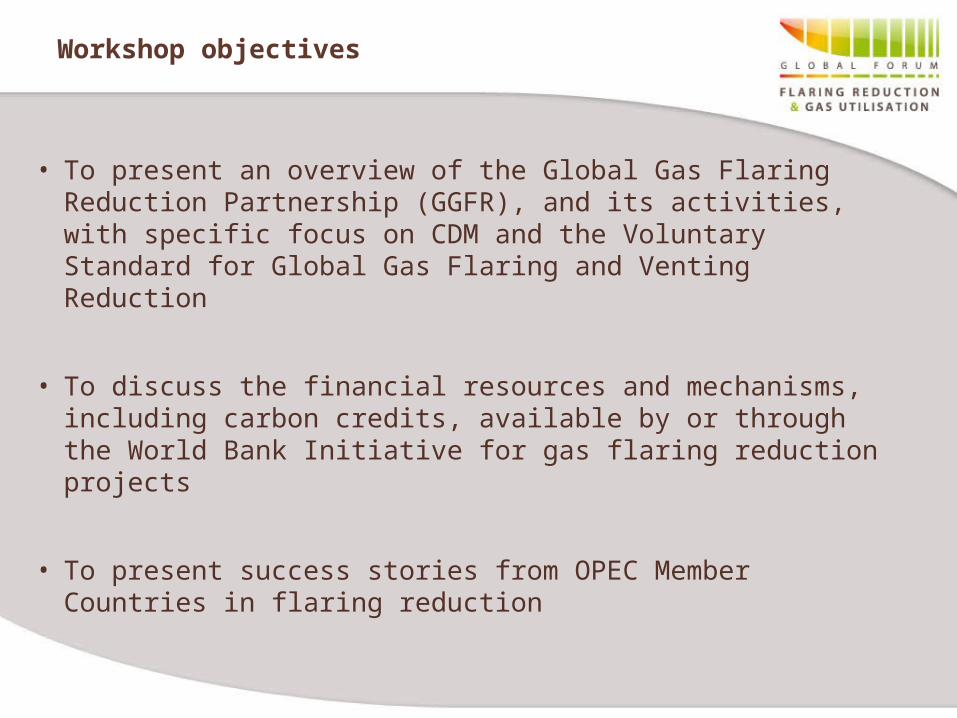

Workshop objectives

• To present an overview of the Global Gas Flaring Reduction Partnership (GGFR), and its activities, with specific focus on CDM and the Voluntary Standard for Global Gas Flaring and Venting Reduction

• To discuss the financial resources and mechanisms, including carbon credits, available by or through the World Bank Initiative for gas flaring reduction projects

• To present success stories from OPEC Member Countries in flaring reduction

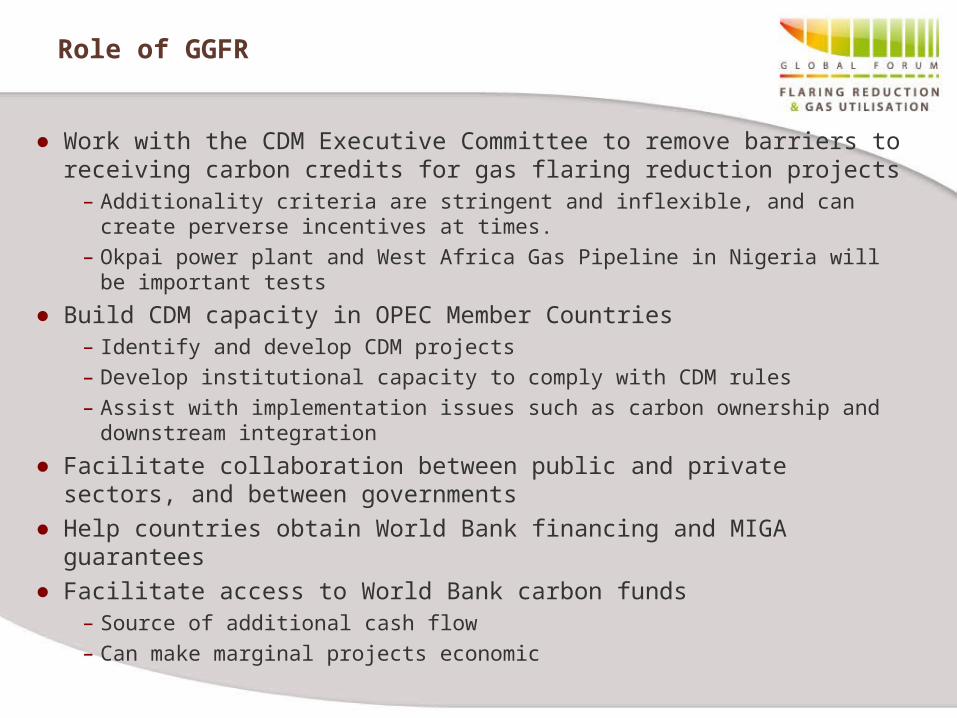

Role of GGFR

● Work with the CDM Executive Committee to remove barriers to receiving carbon credits for gas flaring reduction projects

– Additionality criteria are stringent and inflexible, and can create perverse incentives at times.

– Okpai power plant and West Africa Gas Pipeline in Nigeria will be important tests

● Build CDM capacity in OPEC Member Countries– Identify and develop CDM projects– Develop institutional capacity to comply with CDM rules– Assist with implementation issues such as carbon ownership and

downstream integration

● Facilitate collaboration between public and private sectors, and between governments

● Help countries obtain World Bank financing and MIGA guarantees● Facilitate access to World Bank carbon funds

– Source of additional cash flow– Can make marginal projects economic

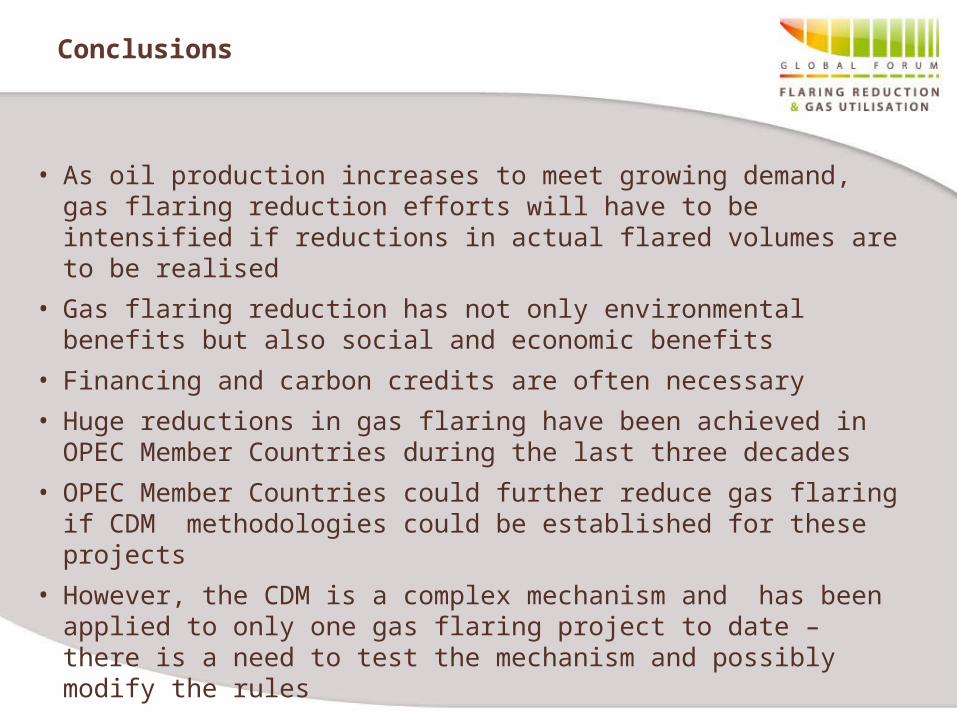

Conclusions

• As oil production increases to meet growing demand, gas flaring reduction efforts will have to be intensified if reductions in actual flared volumes are to be realised

• Gas flaring reduction has not only environmental benefits but also social and economic benefits

• Financing and carbon credits are often necessary

• Huge reductions in gas flaring have been achieved in OPEC Member Countries during the last three decades

• OPEC Member Countries could further reduce gas flaring if CDM methodologies could be established for these projects

• However, the CDM is a complex mechanism and has been applied to only one gas flaring project to date – there is a need to test the mechanism and possibly modify the rules

Thank You