gartner on outsourcing, 2005 - ulisboa · 5.0 business process outsourcing.....17 5.1 issues,...

TRANSCRIPT

ResearchPublication Date: 14 December 2005 ID Number: G00131095

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved. Reproduction of this publication in any form without prior written permission is forbidden. The information contained herein has been obtained from sources believed to be reliable. Gartner disclaims all warranties as to the accuracy, completeness or adequacy of such information. Although Gartner's research may discuss legal issues related to the information technology business, Gartner does not provide legal advice or services and its research should not be construed or used as such. Gartner shall have no liability for errors, omissions or inadequacies in the information contained herein or for interpretations thereof. The opinions expressed herein are subject to change without notice.

Gartner on Outsourcing, 2005 Lorrie Scardino, Dane S. Anderson, Robert H. Brown, Claudio Da Rold, Cassio Dreyfuss, Frances Karamouzis, John-David Lovelock, William Maurer, Cynthia Moore, Allie Young

This research will help you understand what's going on in the outsourcing market today. It examines key issues, trends and events in outsourcing from 2005, and provides an outlook for 2006.

Publication Date: 14 December 2005/ID Number: G00131095 Page 2 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

TABLE OF CONTENTS

1.0 Introduction.................................................................................................................................. 4 2.0 Service Delivery Models .............................................................................................................. 4

2.1 Issues, Trends and Events ............................................................................................. 4 2.2 What We Saw in the Outsourcing Market in 2005 That Will Affect Service Delivery Models .................................................................................................................................. 5 2.3 What You Need to Know About Service Delivery Models.............................................. 6 2.4 What Gartner Expects to See for Service Delivery Models in 2006............................... 7

3.0 Infrastructure and Network Outsourcing...................................................................................... 9 3.1 Issues, Trends and Events ............................................................................................. 9 3.2 What We Saw in Infrastructure and Network Outsourcing in 2005................................ 9 3.3 IT Infrastructure Outsourcing Forecast Through 2009 ................................................. 10 3.4 What You Need to Know About Infrastructure and Network Outsourcing ................... 11 3.5 What Gartner Expects to See for Infrastructure and Network Outsourcing in 2006 .... 12

4.0 Application Outsourcing............................................................................................................. 13 4.1 Issues, Trends and Events ........................................................................................... 13 4.2 What We Saw in Application Outsourcing in 2005....................................................... 13 4.3 Application Outsourcing Forecast Through 2009......................................................... 15 4.4 What You Need to Know About Application Outsourcing ............................................ 15 4.5 What Gartner Expects to See in Application Outsourcing in 2006............................... 16

5.0 Business Process Outsourcing.................................................................................................. 17 5.1 Issues, Trends and Events .......................................................................................... 17 5.2 What We Saw in BPO in 2005 ..................................................................................... 18 5.3 BPO Forecast Through 2009 ....................................................................................... 19 5.4 What You Need to Know About BPO........................................................................... 19 5.5 What Gartner Expects to See in BPO in 2006 ............................................................. 20

6.0 Geographic Issues, Trends and Events in the Outsourcing Market.......................................... 21 6.1 What We Saw in the Global Outsourcing Market in 2005 ............................................ 21 6.2 IT Services Forecast by Geography Through 2009 ..................................................... 22 6.3 What You Need to Know About Regional and Geographic Issues That Affect the Worldwide Outsourcing Market .......................................................................................... 22

6.3.1 The Offshore Effect Goes Well Beyond India .............................................. 22 6.3.2 Turbulence in the European Market ............................................................. 23 6.3.3 Latin America Becomes a Burgeoning Nearshore and Offshore Destination23 6.3.4 Asia/Pacific Markets Are as Diverse as the Geography Is Expansive ......... 24

6.4 What Gartner Expects to See in the Global Outsourcing Market in 2006.................... 25 7.0 Outsourcing Practices by Vertical Industry................................................................................ 25

7.1 Vertical Industry Forecast Through 2009 ..................................................................... 25 8.0 Outsourcing Practices in the Utilities Industry ........................................................................... 29

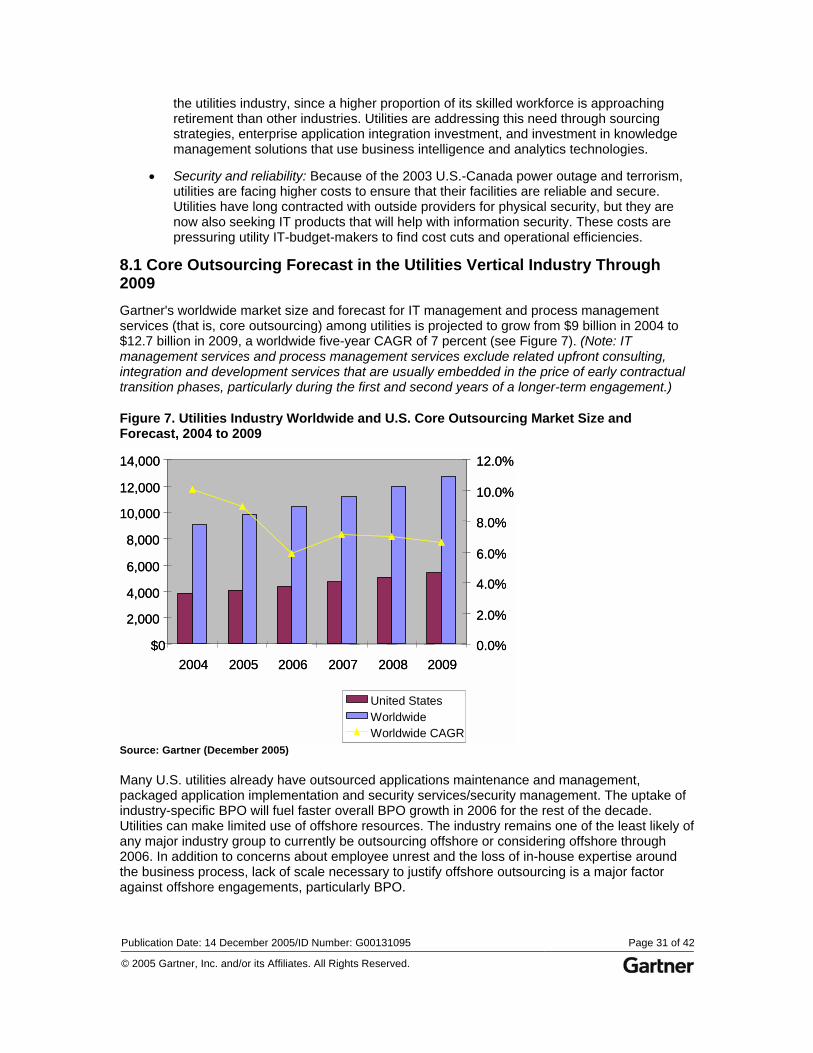

8.1 Core Outsourcing Forecast in the Utilities Vertical Industry Through 2009 ................. 31 8.2 What You Need to Know About Outsourcing in the Utilities Sector in 2006 ................ 32 8.3 What Gartner Expects to See in the Utilities Industry in 2006 ..................................... 33

9.0 Performance Management ........................................................................................................ 33 9.1 Issues, Trends and Events ........................................................................................... 33 9.2 Projected Adoption ....................................................................................................... 34 9.3 What You Need to Know About Performance Management........................................ 35 9.4 What Gartner Expects to See for Performance Management in 2006......................... 35

Publication Date: 14 December 2005/ID Number: G00131095 Page 3 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

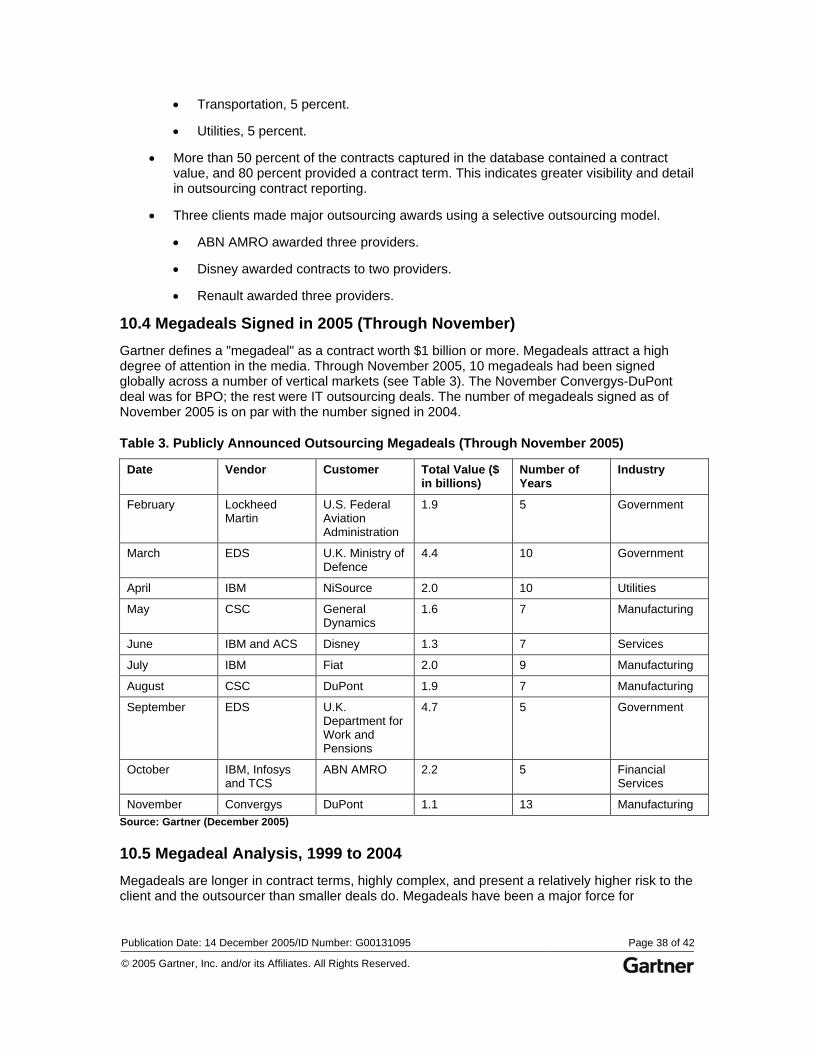

10.0 Outsourcing Contract Analysis ................................................................................................ 36 10.1 Introduction................................................................................................................. 36 10.2 Outsourcing Awareness and Contract Reporting....................................................... 37 10.3 Outsourcing Contracts Signed in 2005 (Through November) .................................... 37 10.4 Megadeals Signed in 2005 (Through November) ...................................................... 38 10.5 Megadeal Analysis, 1999 to 2004 .............................................................................. 38 10.6 Analysis of Outsourcing Contracts in Vertical Markets ............................................. 39 10.7 Uptake of Outsourcing in Geographies ...................................................................... 40 10.8 What You Need to Know About Outsourcing Contract Trends .................................. 40

LIST OF TABLES

Table 1. Worldwide BPO Market Size and Forecast, 2004 to 2009................................................ 19 Table 2. Five-Year Growth Rates for Discrete and Outsourced Services by Region, 2004 to 200922 Table 3. Publicly Announced Outsourcing Megadeals (Through November 2005) ........................ 38

LIST OF FIGURES

Figure 1. IT Infrastructure Outsourcing Forecast, 2004 to 2009 ..................................................... 11 Figure 2. Enterprise Application Outsourcing Forecast, 2004 to 2009............................................ 15 Figure 3. Worldwide Forecast for Core Outsourcing by Vertical Market, 2005 to 2009 (U.S. $Millions).......................................................................................................................................... 26 Figure 4. North America: Vertical-Industry Drivers.......................................................................... 27 Figure 5. Europe, the Middle East and Africa: Vertical-Industry Drivers ......................................... 28 Figure 6. Asia/Pacific: Vertical-Industry Drivers .............................................................................. 29 Figure 7. Utilities Industry Worldwide and U.S. Core Outsourcing Market Size and Forecast, 2004 to 2009............................................................................................................................................. 31

Publication Date: 14 December 2005/ID Number: G00131095 Page 4 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

STRATEGIC PLANNING ASSUMPTION(S)

• Through 2008, more than 50 percent of new outsourcing deals will include IT utility service components (0.7 probability).

• By 2008, more than 70 percent of new application utility offerings will be targeted at business units or line managers, rather than IT organizations (0.7 probability).

• By 2015, 30 percent of all professional IT service jobs will be delivered from emerging markets rather than developed countries (0.8 probability).

ANALYSIS

1.0 Introduction In 2005, the political rhetoric about outsourcing and offshoring died down, and organizations focused on getting better results from outsourcing. Although many organizations still focused on costs, they looked beyond costs and tried to figure out how to get more business value from outsourcing.

The "Gartner on Outsourcing" report was created to provide an annual "state of the market" for organizations that are outsourcing or considering outsourcing. Being informed about what has been happening and what will likely happen next year enables you to make better outsourcing decisions.

This report covers a comprehensive range of topics:

• Service delivery model trends that affect the market and, hence, the options for organizations to consider

• Three primary service lines that are outsourced — infrastructure, applications and business processes

• Regional issues that affect outsourcing around the world

• Vertical-industry drivers that affect the use of outsourcing

• Performance management as it evolves from "reporting metrics" to "managing business outcomes"

• Contract activity for the year, highlighting trends and megadeals

In every edition of "Gartner on Outsourcing," we select one or more hot outsourcing areas for additional focus and deeper analysis. In this edition, we examine the utilities vertical industry (electric, natural gas and water services).

2.0 Service Delivery Models Analytical sources: Claudio Da Rold and Frances Karamouzis

2.1 Issues, Trends and Events Two big trends in outsourcing service delivery options are beginning to intersect: global delivery and IT services as a "utility."

Publication Date: 14 December 2005/ID Number: G00131095 Page 5 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Global delivery: The use of global IT labor, whether "nearshore" (in a neighboring country) or "offshore" (halfway around the world), is continuing at a rapid pace with vigorous competition. Global sourcing, however, is moving beyond the quick search for cheaper labor and on to more complex deals as organizations learn the benefits and limitations of global sourcing.

Organizations continue to pressure their relationships with service providers to get more value, which often means lowering costs and improving services. Service providers are pressured to get the most out of their delivery models, pass on their cost savings to clients and improve profitability. These pressures are forcing clients and service providers to seek new ways to deliver services with greater efficiency, effectiveness and, in some cases, to transform the way work gets done.

Utility: At the same time global delivery is integrating into organizational sourcing strategies and service provider delivery models, utility-style IT services are making a slow but steady entrance into service providers' portfolios. The "utility" delivers IT infrastructure, application and business process services from resource pools delivered by the provider, using leveraged, pre-configured solutions, rather than dedicated resources focused on operations that have been customized for a particular organization. Although infrastructure utility solutions are the most prevalent in the market today, the approach is evident across all layers.

• Infrastructure utility: The standardization and industrialization of IT infrastructure services will be a major force in IT services. Through 2008, more than 50 percent of new outsourcing deals will include IT utility service components (0.7 probability). The infrastructure utility is generating the most interest from buyers of services and the most investment from service providers. Offerings such as Electronic Data Systems' (EDS's) Agile Enterprise, HP's Adaptive Enterprise and IBM's On Demand are the most prominent examples.

• Applications utility: The evolution toward software-as-a-service is another significant change. More users are accepting "good enough" software. Application service providers (ASPs) are enjoying resurgence from earlier setbacks. Business units will also become increasingly involved in making application buying decisions. By 2008, more than 70 percent of new application utility offerings will be targeted at business units or line managers, rather than IT organizations (0.7 probability).

• Business process utility (BPU): The third layer of utility services represents a major evolution of business process outsourcing (BPO) services. BPU is a business process management service based on highly standardized processes and a unified, one-to-many technology platform.

2.2 What We Saw in the Outsourcing Market in 2005 That Will Affect Service Delivery Models

• Deal size, structure and complexity: Offshore pure play providers (mostly Indian providers) were invited to bid on a record number of deals that were more than $30 million, while traditional providers, such as IBM, publicly announced that their deal sizes were getting smaller. Deals in 2005 had more-complex terms and conditions, and penalties and incentives. More-complex sourcing strategies are developing in the maturing marketplace.

• Shared/captive centers: Captive centers became more attractive as organizations evaluated offshore outsourcing beyond the applications layer and could not find credible offerings from providers that had the necessary maturity, experience and scale to deliver the services. (Captive centers deliver low-cost labor to a company using the company's

Publication Date: 14 December 2005/ID Number: G00131095 Page 6 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

own employees and facilities.) At the same time that new shared/captive centers were created, some mature shared/captive centers were sold to investors or service providers (see "Gecis Improves Its Position in Finance and Accounting BPO").

• Nearshoring: Risk-adjusted cost comparisons, factoring in country and provider options, drove some organizations to pursue options closer to home. Organizations in the U.S. investigated Mexico and Canada, while organizations in Western Europe looked at Eastern European countries.

• India: Although India is still a formidable competitor and recognized leader, it is no longer the foregone conclusion for organizations investigating various global sourcing options. Many countries have invested heavily to attract work, and some focus on specific kinds of services, such as BPO in Eastern Europe. Organizations started to match each service they needed with the country and service provider best suited for the job.

• New service categories: Organizations examined BPO opportunities, domestic and offshore, at a frenetic pace. Early adopters of offshore applications outsourcing and BPO signed offshore infrastructure deals. This new form of service delivery for infrastructure will disrupt a mature, commoditized market (see "Positions 2005: Global Sourcing and the Impact of New Delivery Models on IT Services").

• Convergence/collision: Major shifts in the IT-intensive service provider landscape became more pronounced. New providers started to emerge. Telecommunications companies acquired IT service providers or evaluated new IT-service strategies, especially in Asia/Pacific and Europe. Other vertical businesses, such as financial services providers and media service providers, also entered the field as the line blurred between IT and business services, and as BPU ventures sponsored and co-owned by leading clients started to emerge (see "A Business Process Utility May Help the Recording Industry Deal With the Digital Revolution").

• Profits and growth: Established providers (such as HP, IBM and Siemens) began multiyear restructuring programs to focus more on profitability and growth as competition got tougher and margins shrank (see "IBM Applies On-Demand Concepts to Itself, Starting in Europe"). Offshore providers increasingly sought to better serve vertical industries and business processes by acquiring front-end capabilities or consulting firms.

2.3 What You Need to Know About Service Delivery Models The evolution of service delivery models — moving from fixed, custom environments, often in close proximity to the client, to global delivery and the adoption of more-standardized utilities — is not without challenges. Be aware of these challenges and make provisions for them in your sourcing strategies.

Global Delivery

• Gaps in virtual global teams: Business benefits will only come when delivery is seamless through virtual teams operating around the world. This is not yet a reality, and not all the tools, processes and organizational structures are fully developed. Communication gaps remain because of cultural differences, and execution gaps remain because of different security needs and regulations, and the immaturity of process standardization.

• Workforce discontinuities: The quality and capability of labor pools around the world will fluctuate as providers race to establish niches and dominance in specific capabilities. By

Publication Date: 14 December 2005/ID Number: G00131095 Page 7 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

2015, 30 percent of all professional IT services jobs will be delivered from emerging markets rather than developed countries (0.8 probability).

Infrastructure Utility

• Marketing hype: The hype about infrastructure that is agile, adaptive and available on demand has prevented prospective clients from understanding what is real and what is a marketing pitch. To counter this, Gartner has developed a formal definition of an infrastructure utility maturity model that describes the different stages of IT infrastructure utility offerings (see "Gartner Introduces the Infrastructure Utility Maturity Model" and "Gartner Updates its Definition of IT Infrastructure Utility").

• Pricing: Pricing can be very confusing. This confusion will persist until standards emerge. Traditional ways of pricing infrastructure services are inadequate for utility approaches to infrastructure services. The industry has no accepted pricing method for the variability it promises (see "IT Infrastructure Utility Needs New Pricing Models").

Application Utility

• Fragmentation: Application utility will not become a single market. It will fragment by vertical and business processes. Potentially, it will split into hundreds of different solutions and providers, organized around service value chains built by infrastructure utility providers or larger independent software vendors (ISVs).

• Mass-customization: Application on-demand suites require clients to evolve from their "customize-first" approach to the opposite, where "good enough, ready to use" suites are acceptable and customized jobs are done as a last resort, at least for nondifferentiated applications and processes.

Business Process Utility

• Standardization: Many organizations still need to recognize the value of standardization. They need to move from the concept of "customize first" to "good enough, customize as a last resort," at least for nondifferentiating processes.

• Lack of providers: Relatively few providers are experimenting with credible BPU services.

• Moving target: Because BPU deals are just emerging, it will take a while for the industry to develop best practices and reliable business models.

• Industry expertise: Performance in some early BPU deals was disappointing because specific vertical industry requirements had not been built into the utilities. Evaluate the vertical industry expertise of the provider and the utility solution.

2.4 What Gartner Expects to See for Service Delivery Models in 2006 Global Delivery

• The market will continue to grow significantly for globally delivered services. IT employment and salaries in higher-cost areas will continue to be challenged by competition from low-cost countries.

• Emerging areas, such as infrastructure and R&D, with be sources of healthy growth, given their current small base. The service provider landscape will continue to change as incumbent service providers are unable to navigate around smaller, aggressive newcomers, such as offshore pure plays. The smaller providers will gain market share

Publication Date: 14 December 2005/ID Number: G00131095 Page 8 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

and "mind share," and more of them will be viewed as credible competitors for larger deals.

• A majority of deals that are $50 million or more will have some globally sourced components. Global delivery may not be the thrust of the deal, but some portion of the deal must be optimized through global delivery options.

• Emerging outsourcing centers in Mexico, Brazil, Russia, China and Eastern Europe will attract more work, sometimes at India's expense.

• The minimum level of competitive parity will require some element of global delivery, especially in the applications space. Demands will increase for more-strategic and higher-value work premised on business outcomes as well as labor arbitrage.

• Remote management services, still a niche market, will generate more interest from prospective clients and providers.

Infrastructure Utility

• Outsourcing providers that also control hardware and software platforms will sell mixed forms of outsourcing and utility while investing R&D money in new utility offerings and solutions.

• Product-independent outsourcing providers will move to build stronger partnerships with hardware and software vendors.

• Niche providers will try to jump ahead of the competition with more-aggressive utility models and virtualization-based approaches.

• New pricing approaches, for example, based on virtual boxes, the number of CPUs allocated, and independent or benchmark-based units will start to emerge, as well as attempts to define entirely new units to emulate true utilities (similar to watts of energy). This pricing will be mixed into traditional outsourcing approaches, where pricing has been highly customized and baseline-driven.

Application Utility

• Because of fragmentation, no large application utility deals will emerge, but incremental growth will continue.

• This delivery model will grow at different speeds by location, vertical industry, process and application area. For ISVs and traditional service providers, the risk will be whether someone else has built a successful application utility in their area of strength.

• More users will accept shared, mass-customized, ready-to-use applications that are accessed on a usage basis for areas of noncore processes.

Business Process Utility

• BPU deals will slowly emerge, but it will take time to assess whether they are successful. BPU is far from a mainstream approach, nor will it become one in 2006.

• Industrywide efforts will begin in some vertical industries for process standardization. Competing organizations will explore joint ventures, standard processes that can be shared by many organizations and consortia with service providers.

Publication Date: 14 December 2005/ID Number: G00131095 Page 9 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

3.0 Infrastructure and Network Outsourcing Analytical sources: Dane Anderson, Adam Couture, Claudio Da Rold, Robert DeSouza, Richard Matlus and Gianluca Tramacere

3.1 Issues, Trends and Events Infrastructure outsourcing includes the outsourcing of data centers, desktop services and networks. These are among the most mature functions outsourced today. Infrastructure and network outsourcing will continue on a solid and sustained growth trajectory in 2006, although it will be less than the double-digit growth of the 1990s.

As this market continues to mature, four major factors will affect it:

• Profitability and growth: Profitability of deals for service providers has always been important, but it has become even more so as the IT services market becomes more visible to investors. Also, several high-profile, unprofitable deals have become visible in recent years, sending a wake-up call that profits are not a given in an industry that was generally able to count on good margins. At the same time, service providers have to post consistent revenue growth.

• Standardization and the utility movement: IT infrastructure outsourcing is moving away from the management of customized, dedicated systems toward delivery using mass-customized, standardized, automated and shared IT systems. The market is selectively investing in the development of utility solutions, and those that invest wisely will be the future leaders. Delivery of these standardized and shared services has migrated during the past few years from the straightforward, co-location services at Internet data centers to managed-hosting storage utilities, and remote monitoring and management services.

• Globalization: Service providers are showing more interest and investment in offering new offshore infrastructure services, such as remote monitoring, database administration and technical support. At this point, however, more exploration and capability build-out, rather than adoption, is occurring. Providers are more actively pursuing infrastructure globalization plans than clients are.

• Sourcing maturity of the client base: We have seen increased sophistication in sourcing strategy, governance and practices. This intensified focus demonstrates that organizations are applying lessons learned from prior outsourcing experiences, and have learned from the successes and failures of others. Additionally, organizations that are in second- and third-generation outsourcing relationships are making sophisticated demands on their service providers, reflecting the evolving "sourcing maturity" of many organizations.

3.2 What We Saw in Infrastructure and Network Outsourcing in 2005 Service provider restructuring: Many major service providers restructured their organizations and changed some leadership. This restructuring has become an ongoing evolution for providers. Although restructuring was sometimes in response to negative factors, such as declining profits, there were times when leadership and organizational changes were made proactively to improve sales, operations, quality and accountability. Such activity, however, can disrupt a provider's internal operations and inhibit marketplace presence while the changes are sorted out.

More service options: Service providers addressed client demands for more service options. They responded by bundling and unbundling services in the combinations their clients demanded.

Publication Date: 14 December 2005/ID Number: G00131095 Page 10 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Information Technology Infrastructure Library (ITIL) standardization: More organizations around the world demanded ITIL capabilities and frameworks from service providers. ITIL became a "must have" for providers, rather than the differentiator it was a few years ago.

New relationships: With the push for standardized offerings, methods and processes, outsourcing providers increasingly pressed original equipment manufacturers (OEMs) to provide infrastructure that is priced on a usage basis. From this, alliances formed and began to resonate with some clients.

Premium pricing: Outsourcing providers increasingly charged a premium to manage infrastructure outside of their designated standard architectures, pushing buyers to gradually move to standard, shared environments.

Global delivery: Major providers, such as EDS, CSC and Perot Systems, offered a larger scope of remote management services delivered via offshore resources, including data center monitoring, security monitoring and network monitoring.

Selective outsourcing: This gained popularity among large, global corporations. Two examples include Walt Disney's infrastructure deals with IBM and ACS, and Renault's selection of HP and CSC to provide infrastructure services (see "Renault's Outsourcing Deals Signal Change in European Market"). At the same time, organizations realized that some outsourced services needed to come back in-house, and other services that were retained needed to be outsourced. Organizations with outsourcing experience embraced a multisourcing strategy that considers internal and external sources working together, rather than a bidirectional "in vs. out" decision.

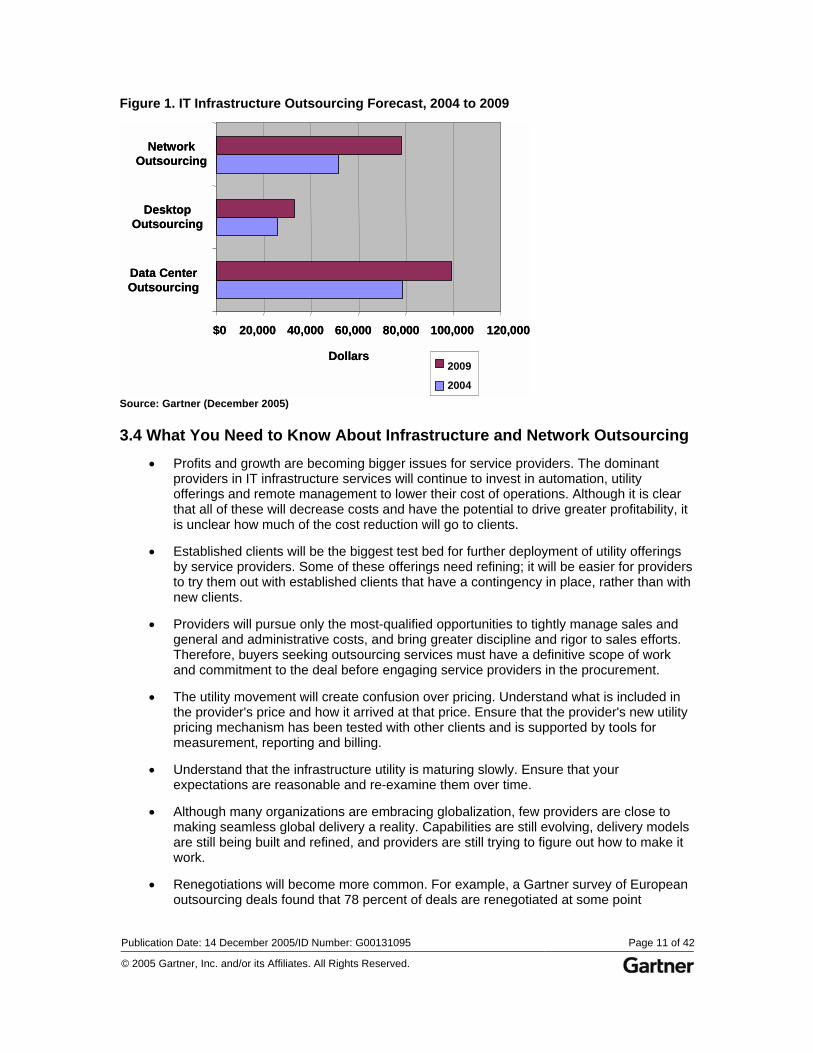

3.3 IT Infrastructure Outsourcing Forecast Through 2009 The IT outsourcing market is expected to grow at a 6.9 percent compound annual growth rate (CAGR) through 2009. The combined infrastructure outsourcing segments (data center, desktop and network outsourcing) equal more than 80 percent of total IT outsourcing spending (see Figure 1).

• Network outsourcing remains the fastest-growing segment, with an 8.5 percent CAGR between 2004 and 2009.

• Desktop outsourcing CAGR is forecast to grow at 5.1 percent between 2004 and 2009.

• Data center outsourcing CAGR is forecast to grow at 4.8 percent between 2004 and 2009.

Publication Date: 14 December 2005/ID Number: G00131095 Page 11 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Figure 1. IT Infrastructure Outsourcing Forecast, 2004 to 2009

$0 20,000 40,000 60,000 80,000 100,000 120,000

Data Center Outsourcing

Desktop Outsourcing

Network Outsourcing

2009

2004

Dollars

$0 20,000 40,000 60,000 80,000 100,000 120,000

Data Center Outsourcing

Desktop Outsourcing

Network Outsourcing

2009

2004

Dollars

Source: Gartner (December 2005)

3.4 What You Need to Know About Infrastructure and Network Outsourcing • Profits and growth are becoming bigger issues for service providers. The dominant

providers in IT infrastructure services will continue to invest in automation, utility offerings and remote management to lower their cost of operations. Although it is clear that all of these will decrease costs and have the potential to drive greater profitability, it is unclear how much of the cost reduction will go to clients.

• Established clients will be the biggest test bed for further deployment of utility offerings by service providers. Some of these offerings need refining; it will be easier for providers to try them out with established clients that have a contingency in place, rather than with new clients.

• Providers will pursue only the most-qualified opportunities to tightly manage sales and general and administrative costs, and bring greater discipline and rigor to sales efforts. Therefore, buyers seeking outsourcing services must have a definitive scope of work and commitment to the deal before engaging service providers in the procurement.

• The utility movement will create confusion over pricing. Understand what is included in the provider's price and how it arrived at that price. Ensure that the provider's new utility pricing mechanism has been tested with other clients and is supported by tools for measurement, reporting and billing.

• Understand that the infrastructure utility is maturing slowly. Ensure that your expectations are reasonable and re-examine them over time.

• Although many organizations are embracing globalization, few providers are close to making seamless global delivery a reality. Capabilities are still evolving, delivery models are still being built and refined, and providers are still trying to figure out how to make it work.

• Renegotiations will become more common. For example, a Gartner survey of European outsourcing deals found that 78 percent of deals are renegotiated at some point

Publication Date: 14 December 2005/ID Number: G00131095 Page 12 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

because of a lack of flexibility or innovation, a need to reduce or expand the scope of work, or the need to reduce costs. Renegotiations on a proactive basis, instead of in reaction to an event, will become more common.

3.5 What Gartner Expects to See for Infrastructure and Network Outsourcing in 2006

• Organizations already in outsourcing relationships should expect a steady stream of new options — with various costs and benefits — surrounding utility and automated service delivery.

• Selective outsourcing will continue to gain traction as the preferred sourcing model. Organizations will attempt to reduce risk by leveraging multiple providers in outsourcing engagements. Operating-level agreements will be required to manage service relationships among the team of providers.

• Organizations will pursue standardization and automation to optimize operations. Although many organizations could pursue these efforts on their own, many will pursue them via outsourcing relationships to reduce risk and exploit the market's capabilities.

• Service providers will continue to develop, refine, and promote standards and automation in conjunction with utility infrastructure offerings.

• Outsourcing providers, OEMs and ISVs will form new partnerships to mitigate the financial risks of providing IT asset-based services with usage-based pricing.

• Outsourcing providers and managed hosting companies will standardize on distinct tiers and classes of infrastructure. Clients will pay a premium to deviate from these defined tiers.

• Telecommunications providers will try to move up from network provision and managed hosting into more infrastructure delivery services.

• Growth for offshore infrastructure services will continue, but will be slower because of continued concerns over offshore providers' abilities to deliver secure, latency-free, high-quality infrastructure services, as well as the lack of robust, end-to-end infrastructure capabilities.

• The most significant global deals will come from pre-established service relationships, where trust and confidence provide the opportunity to try new delivery approaches.

• Nearshore deals will be more heavily investigated, including locations in Canada and Mexico for organizations in the U.S., and locations in Eastern Europe for organizations in Western Europe.

• Few (if any) new competitors will enter the market for infrastructure or network outsourcing, though some providers may merge and others will expand through acquisitions or partnerships.

• An increase in infrastructure contract renegotiations will lead to more deal terminations, but Gartner estimates that the number of terminations will remain below 5 percent of all deals.

Publication Date: 14 December 2005/ID Number: G00131095 Page 13 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

4.0 Application Outsourcing Analytical sources: Allie Young, Stacie Buttorff, Subhash Parameswaran, Lorrie Scardino and Gianluca Tramacere

4.1 Issues, Trends and Events Application outsourcing is a less-mature market than IT infrastructure outsourcing, but it continues to gain momentum. In 2005, cost continued to be a dominant driver for application outsourcing, and offshore delivery gained greater acceptance.

Gartner defines application outsourcing as a multiyear contract/relationship involving the purchase of ongoing application services from an external service provider (ESP), which supplies the people, processes, tools and methodologies for managing, enhancing, maintaining, and supporting custom and packaged software applications. Application outsourcing contracts can comprise a broad portfolio of services, such as application development, integration, deployment and support services, as well as consulting/advisory services. The foundation of application outsourcing, however, is a multiyear contract for ongoing application services. As such, discrete development projects or staff augmentation services are not considered to be application outsourcing.

In the mid-1990s, a flurry of large application outsourcing contracts in the U.S. led to an "all-or-nothing" approach to outsourcing legacy applications. Since then, more packaged applications have become available and, in 2005, legacy modernization became a more pressing business need. Although some large application outsourcing deals have been signed, the majority of them are accomplished in smaller, more-focused outsourcing arrangements. In part, this is explained by the past success of application services delivered by ESPs in project-based work. It also parallels the broader trend in the outsourcing market for greater control and focus via selective outsourcing.

Acceptance of Offshore/Global Delivery in Application Outsourcing

Several key forces have converged to support the acceptance of a global delivery model (GDM) for delivering application services:

• The demand for cost takeout in applications

• Requirements for greater flexibility in accessing application skills

• The overarching globalization of business

Today, most application outsourcing users have a bilateral view of global sourcing: on-site and offshore. Most often, "offshore" is equated with India. Gradually, organizations will evolve an integrated four-tier global model: on-site, onshore (domestic), offshore and nearshore.

To avoid the pitfalls of outsourcing offshore, include a formal review of delivery options for all of your sourcing decisions (see "Global Sourcing Demands New Strategies").

4.2 What We Saw in Application Outsourcing in 2005 • The desire to reduce costs continued to be a dominant driver for users seeking to

outsource applications.

• The application outsourcing market continued to mature (see "Hype Cycle for IT Services, 2005").

Publication Date: 14 December 2005/ID Number: G00131095 Page 14 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

• New providers took advantage of relatively low barriers to provide application outsourcing services. These providers offered varied and sometimes unique competencies, often based on their heritage in outsourcing.

• Offshore delivery gained widespread acceptance. Organizations that outsourced successfully were willing to outsource more. Even first-time outsourcers were keen to explore outsourcing their business applications.

• As users focused more on near-term goals to reduce costs, many overlooked long-term imperatives to achieve productivity gains in their application services work.

• As application services moved from project-based services to application outsourcing, pricing moved away from time-and-materials to fixed-cost based on service-level agreement (SLA) performance metrics.

• Many users still approached application outsourcing like a project, envisioning a certain number of full-time equivalents (FTEs) to manage their application work, many of whom are engaged via time-and-materials or staff augmentation contracts. Many users remained confused about the expectations and value of contracting for project work vs. outsourced relationships.

• The decision-making responsibility for sourcing issues shifted toward executives and board members.

• Application projects often were turned over to an offshore provider. Many of these deals evolved into long-term application outsourcing engagements for greater continuity, retained knowledge, SLA-based contracting and, thus, more value-based outcomes for clients.

• Gartner found that most application outsourcing contracts were valued at less than $10 million.

• Growing signs of dissatisfaction arose with some offshore services because of performance issues and rising attrition rates (primarily in India). Most application outsourcing users were committed to resolving these problems with their providers rather than terminating the relationships.

• Partnerships and joint ventures continued to form (for example, EDS established a partnership with Cognizant to support internal EDS legacy modernization initiatives and to supply Indian labor to EDS clients).

• Prominent outsourcing deals with large application outsourcing components were awarded by Renault and ABN AMRO. Although Renault awarded the application outsourcing work to a European company (Atos Origin), ABN AMRO awarded the application outsourcing work to two Indian service providers, Infosys and Tata Consultancy Services (TCS). The latter award validated a long-held Gartner view that the Indian companies would increasingly be viewed "on par" with traditional IT services providers, competing for the same clients and scopes of work (see "ABN AMRO's Megadeal Shows Multisourcing Is Taking Off").

• More country destinations emerged in enterprise sourcing strategies. Canada, Mexico and other Latin American countries were popular destinations with U.S. companies, while Eastern European locations emerged as options for Western European organizations.

Publication Date: 14 December 2005/ID Number: G00131095 Page 15 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

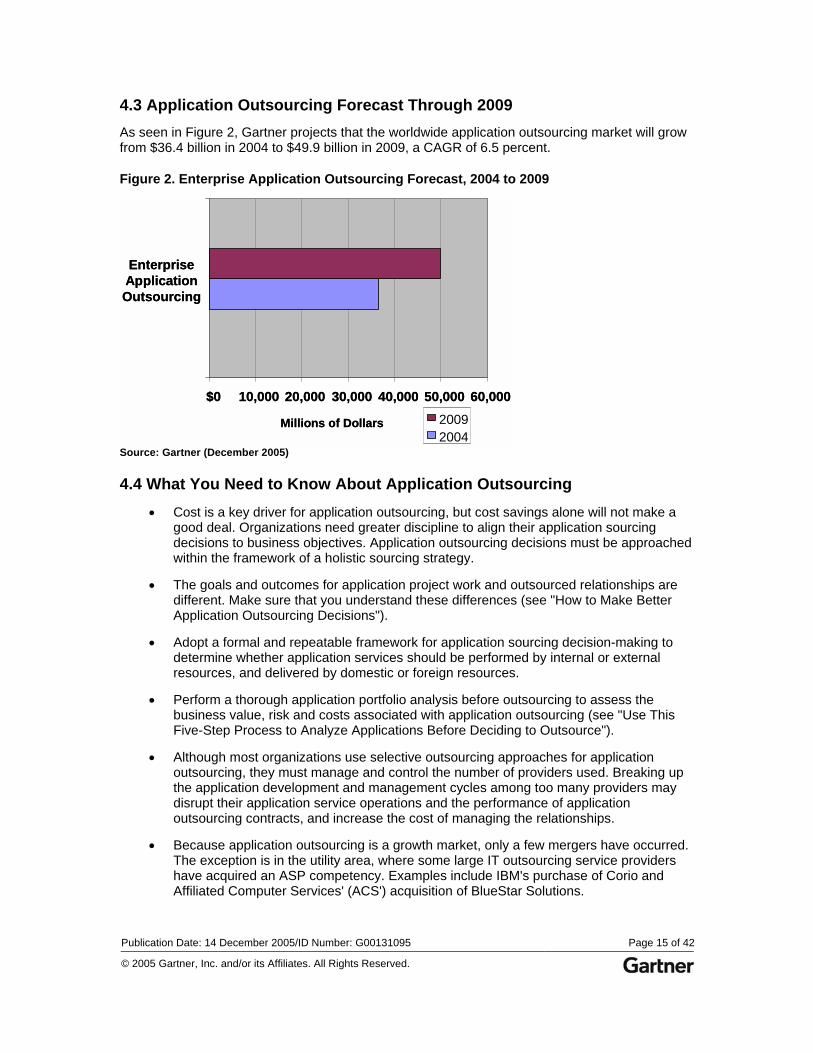

4.3 Application Outsourcing Forecast Through 2009 As seen in Figure 2, Gartner projects that the worldwide application outsourcing market will grow from $36.4 billion in 2004 to $49.9 billion in 2009, a CAGR of 6.5 percent.

Figure 2. Enterprise Application Outsourcing Forecast, 2004 to 2009

$0 10,000 20,000 30,000 40,000 50,000 60,000

Enterprise Application Outsourcing

20092004

Millions of Dollars

$0 10,000 20,000 30,000 40,000 50,000 60,000

Enterprise Application Outsourcing

20092004

Millions of Dollars

Source: Gartner (December 2005)

4.4 What You Need to Know About Application Outsourcing • Cost is a key driver for application outsourcing, but cost savings alone will not make a

good deal. Organizations need greater discipline to align their application sourcing decisions to business objectives. Application outsourcing decisions must be approached within the framework of a holistic sourcing strategy.

• The goals and outcomes for application project work and outsourced relationships are different. Make sure that you understand these differences (see "How to Make Better Application Outsourcing Decisions").

• Adopt a formal and repeatable framework for application sourcing decision-making to determine whether application services should be performed by internal or external resources, and delivered by domestic or foreign resources.

• Perform a thorough application portfolio analysis before outsourcing to assess the business value, risk and costs associated with application outsourcing (see "Use This Five-Step Process to Analyze Applications Before Deciding to Outsource").

• Although most organizations use selective outsourcing approaches for application outsourcing, they must manage and control the number of providers used. Breaking up the application development and management cycles among too many providers may disrupt their application service operations and the performance of application outsourcing contracts, and increase the cost of managing the relationships.

• Because application outsourcing is a growth market, only a few mergers have occurred. The exception is in the utility area, where some large IT outsourcing service providers have acquired an ASP competency. Examples include IBM's purchase of Corio and Affiliated Computer Services' (ACS') acquisition of BlueStar Solutions.

Publication Date: 14 December 2005/ID Number: G00131095 Page 16 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

• Offshore work is intrinsic to the application outsourcing value proposition, and service providers' offerings are more often evaluated based on the availability of offshore options, proven processes to deliver quality outcomes and how access to critical application skill sets is achieved through global delivery.

• Globalization is also driving the uptake of application outsourcing. Many organizations are being drawn into international markets and they must support broader client bases. Offshore application outsourcing services have become one way to address the new complexities of remote offices.

• Indian providers have been amenable to the shift to SLA-based pricing, especially for ERP work, because their process maturity enables them to deliver at higher levels and preserve margins. Some consultants or integrators and outsourcing providers still have a strong preference for lower-risk, fixed-price (based on a number of FTEs) and time-and-materials pricing for application outsourcing.

• The shift to SLA-based pricing shows that the value proposition for application outsourcing is becoming more complex. Organizations are raising the bar on expected application outsourcing results. Price dominates, but processes, people, and quality are scrutinized and factored into decisions.

4.5 What Gartner Expects to See in Application Outsourcing in 2006 • The importance of vertical expertise in the ESP selection process will increase as

organizations seek application outsourcing providers that address their business requirements and bring proven experience.

• Large application outsourcing deals will be the exception; the majority of application outsourcing deals will be small or midsize, and selective outsourcing will be the norm. Deal size will slowly increase, however, and more application outsourcing contracts worth between $30 million and $100 million will be signed in 2006 than in past years.

• The extreme focus on savings will moderate as more-experienced buyers of application outsourcing become concerned with quality, attrition rates, expertise and cultural compatibility.

• More organizations will evaluate outsourcing their ERP environments.

• Indian providers of application services will gain greater visibility on shortlists for application outsourcing contracts. Their process expertise in global delivery will be a critical differentiator.

• ASP outsourcing options will steadily increase, focusing on specific processes or vertical market needs.

• The application outsourcing competitive landscape will become increasingly crowded, and service providers will strive to differentiate (see "User Guide for Making Application Outsourcing Provider Choices").

• Most users will continue to pursue selective outsourcing for their application contracts. However, because the application layer is closely linked to IT infrastructure and business processes, some users will take an end-to-end approach to outsourcing to force more provider accountability. Some providers will seek to leverage their full-service capabilities to win these deals. Others will use partners to support the various layers.

Publication Date: 14 December 2005/ID Number: G00131095 Page 17 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

• Infrastructure outsourcing contracts will be leveraged to up-sell into application outsourcing, and BPO contracts will be subsumed into application outsourcing work. Applications will increasingly be seen as the pivotal layer because of their linkage to infrastructure and business processes. Also, buying decisions will more often be driven by business units because of the linkage to business processes.

• Application outsourcing providers will pursue targeted acquisitions to expand their vertical competencies or their service capabilities, such as consulting or infrastructure skills. As the application outsourcing market matures in future years, more consolidation will occur.

5.0 Business Process Outsourcing Analytical sources: Robert Brown, Sujay Chohan, Robert DeSouza, Lisa Stone and Cathy Tornbohm

5.1 Issues, Trends and Events BPO is one of the fastest-growing segments of the IT services market. Gartner defines BPO as "the delegation of one or more IT-intensive business processes to an external provider that, in turn, owns, administers and manages the selected processes based on defined and measurable performance metrics."

Although BPO growth has been impressive, the market is far from homogeneous. BPO is best described as the sum of many markets. Its four major components worldwide are:

• Human resources (HR)

• Finance and accounting (F&A)

• Sales, marketing and customer care

• Supply chain management

In addition to this horizontal focus, more providers and buyers are increasing their focus on vertical-industry-specific BPO, such as mortgage processing in banks, patient records management in healthcare and claims processing in insurance. Although these vertical offerings have been around for years, more users are looking to outsource industry-specific tasks that were once considered "core" and, therefore, unsuitable for BPO (such as supply chain for retail). More providers are trying to replicate successful BPO offerings from one industry to another, with minimal alteration and maximum reuse of tools, methodologies and workflows.

Despite strong growth in recent years, the 2005 BPO market is still maturing (see "Hype Cycle for IT Services, 2005") and continues to attract more providers. The market and competitive landscape have coalesced around four general approaches:

• Discrete process BPO: The outsourcing of single subprocesses, such as benefits, as opposed to the entire HR function. These contracts make up the bulk of the market today.

• Comprehensive BPO: Contracts characterized by support for multiple business processes within a single process domain, such as payroll, benefits administration, and education and training within HR, or accounts payable, accounts receivable and tax management within F&A.

Publication Date: 14 December 2005/ID Number: G00131095 Page 18 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

• Multidomain BPO: Contracts that support a mix of functions across multiple process domains, such as pieces of HR, F&A, procurement and customer service. These contracts are uncommon.

• Business process utility: An externally provisioned business process management service based on standardized processes and a unified, one-to-many technology platform. The service provider manages and executes the business processes and the direct business process inputs. The service provider or client can execute the outputs. Contracts typically feature per-transaction fees with monthly minimums. The market for BPU comprised less than 5 percent of BPO deals in 2005.

Organizations are challenged with coordinating piecemeal outsourced processes, even if they have mastered strategic sourcing tenets. Because BPO clients are growing weary of coordinating the work of several providers, organizations will favor providers that can deliver integrated solutions. These integrated providers will possess end-to-end capabilities, derived through acquisition, or vertical or horizontal industry alliances. The adoption of comprehensive or multidomain BPO will become more prevalent, although organizations will evolve into such relationships incrementally, not through an initial contract.

Automation in BPO could have a greater effect than the use of offshore resources via a GDM. BPO traditionally has included people, processes and technology. Automation, however, will strip away the "people" element of BPO. Organizations will evaluate providers based on their ability to scale and deliver against organizational requirements, as opposed to taking over human and technology assets.

As the BPO market continues to mature, business process and IT-enabled automation are converging. Transaction processing services have long been a cornerstone of the BPO market. Some lower-end transaction processing services have become commodity offerings, and providers are looking to incorporate them into higher value-added BPO. A good example of this trend is the shift from commodity, paper-based check processing to automated payment processing services.

5.2 What We Saw in BPO in 2005 • Offshore BPO delivery increased. Providers showed particular interest in increasing the

range of offshore transaction-processing services to offset the current dominance of contact center services, bringing balance to their service mixes.

• Staff turnover increased at offshore call centers, resulting in higher costs to BPO customers.

• Demand for offshore services outstripped what the largest BPO providers could supply. Top providers were stretched thin and grew fast.

• The top end of the BPO market continued to consolidate. The larger providers, to add breadth and depth to their offerings, acquired midsize and niche BPO providers. Significant acquisitions included IBM's acquisition of Equitant, Gecis's purchase of Creditek and ACS's acquisition of Mellon Financial's HR operations.

• Although the larger providers got bigger by acquiring domain expertise, small niche providers continued to appear in North America. The BPO competitive landscape had 33 percent more providers in 2005 than in 2004.

Publication Date: 14 December 2005/ID Number: G00131095 Page 19 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

• More countries offered delivery options for BPO. China rose as a delivery location for Japan and Asia/Pacific, and Eastern Europe continued as the offshore destination of choice for continental Western European operations.

• Two large HR BPO deals were signed in 2005: one with Whirlpool and the other with DuPont. Convergys won both contracts. Although the Whirlpool announcement did not include a total contract value (and therefore cannot be counted as a megadeal), it is a 10-year deal with a scope of service that covers all of Whirlpool's employees and retirees. The DuPont deal is valued at $1.1 billion over 13 years. These large deals signal growing client acceptance of BPO (see "Convergys Boosts BPO Status With DuPont Human Resources Deal").

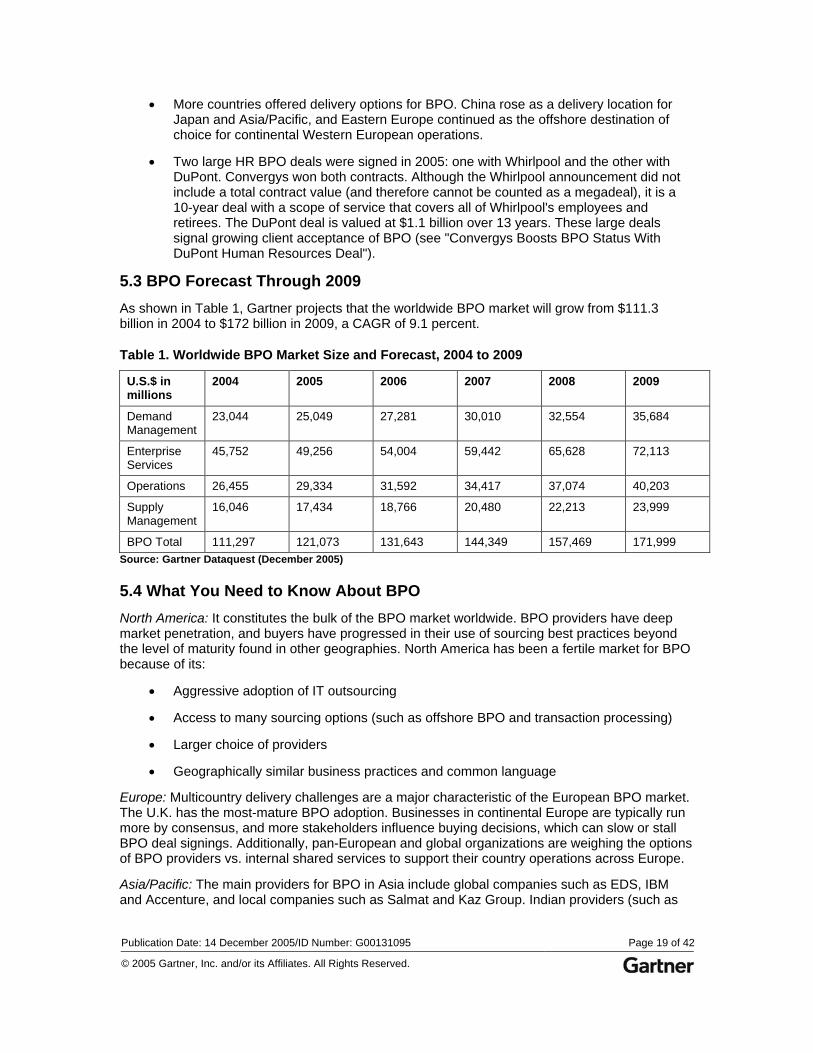

5.3 BPO Forecast Through 2009 As shown in Table 1, Gartner projects that the worldwide BPO market will grow from $111.3 billion in 2004 to $172 billion in 2009, a CAGR of 9.1 percent.

Table 1. Worldwide BPO Market Size and Forecast, 2004 to 2009

U.S.$ in millions

2004 2005 2006 2007 2008 2009

Demand Management

23,044 25,049 27,281 30,010 32,554 35,684

Enterprise Services

45,752 49,256 54,004 59,442 65,628 72,113

Operations 26,455 29,334 31,592 34,417 37,074 40,203

Supply Management

16,046 17,434 18,766 20,480 22,213 23,999

BPO Total 111,297 121,073 131,643 144,349 157,469 171,999 Source: Gartner Dataquest (December 2005)

5.4 What You Need to Know About BPO North America: It constitutes the bulk of the BPO market worldwide. BPO providers have deep market penetration, and buyers have progressed in their use of sourcing best practices beyond the level of maturity found in other geographies. North America has been a fertile market for BPO because of its:

• Aggressive adoption of IT outsourcing

• Access to many sourcing options (such as offshore BPO and transaction processing)

• Larger choice of providers

• Geographically similar business practices and common language

Europe: Multicountry delivery challenges are a major characteristic of the European BPO market. The U.K. has the most-mature BPO adoption. Businesses in continental Europe are typically run more by consensus, and more stakeholders influence buying decisions, which can slow or stall BPO deal signings. Additionally, pan-European and global organizations are weighing the options of BPO providers vs. internal shared services to support their country operations across Europe.

Asia/Pacific: The main providers for BPO in Asia include global companies such as EDS, IBM and Accenture, and local companies such as Salmat and Kaz Group. Indian providers (such as

Publication Date: 14 December 2005/ID Number: G00131095 Page 20 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

TCS, Infosys/Progeon, HCL Technologies and Wipro Spectramind Services) have raised their profiles through offshore BPO services and are now competing globally against the larger U.S.-based BPO providers. These providers do not, however, generally have penetration among organizations in the Asia/Pacific region.

Knowledge process outsourcing: More Indian providers are promoting the idea of knowledge process outsourcing to describe higher complexity processes, such as analytics and R&D. Gartner estimates that such work comprises less than 5 percent of the offshore BPO market, and believes that the term is unnecessary in an already fragmented and complex BPO market.

Vertical-specific BPO growth: BPO focused at specific vertical operations is growing. The financial services industry remains the foremost adopter of BPO services, while government and education in North America will have the fastest growth rates for the adoption of vertical operations BPO.

Consolidation: As the market matures, consolidation will continue. Providers could shift market focus, jeopardizing service delivery. Organizations usually will not be significantly affected if their contracts stipulate contingencies for service continuity. Exit management will become a more important part of contract terms and conditions.

ERP: End-of-life for software contracts has become a significant impetus for BPO. Many users adopted ERP packages in 1999 as part of their year 2000 remediation strategies. As those packages age, BPO has become an alternative to upgrades. In some cases, often among small and midsize businesses, users will outsource their processes to a BPO provider, yet retain the software license to fully depreciate the software asset on their balance sheets.

Sourcing model preferences: BPO adopters are less likely to pursue selective outsourcing than their IT outsourcing counterparts. Many users look for BPO providers that can add subprocesses incrementally to the contract as their needs change over time. Many have also tried to master multiple supplier relationships for various processes (such as selecting a payroll specialist and a different benefits specialist), only to have trouble coordinating competitive suppliers.

5.5 What Gartner Expects to See in BPO in 2006 • The number of providers in the BPO market is unsustainable at all levels. At least one of

the major BPO providers will exit the market or be acquired. Overall market consolidation will primarily be seen through mergers and acquisitions.

• The leading providers for the larger, more-complex, multidomain BPO deals will include providers such as Accenture, ACS, Capgemini, CGI Group, CSC, EDS and IBM.

• Megadeals will continue to be the exception rather than the rule. Large BPO deals are complex and require investment, and few providers can handle the complexity and make the required level of investment. Most BPO activity will continue around smaller, more-focused deals, primarily in the back office and horizontal functions within HR and F&A domains.

• Few BPO providers can successfully demonstrate true multicountry BPO capabilities for multiple processes. Internal shared service centers that span several countries will be bought by established BPO providers or spun off into commercial operations. Gartner expects this activity to increase through 2007 as demand rises for multicountry and multiprocess jobs.

• Clarifications around BPO and compliance with the Sarbanes-Oxley Act of 2002 will not lead to an outright spike in demand for BPO. Rather, growth will accelerate as best practices and standards emerge, and as the issues of Sarbanes-Oxley-era BPO

Publication Date: 14 December 2005/ID Number: G00131095 Page 21 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

(especially in F&A) become more straightforward. Successful BPO providers will not lead with compliance; rather, they will incorporate compliance into a broader focus on process enhancement and best-in-class performance tied to business-based metrics.

• Web services and service-oriented architecture (SOA) technologies will increasingly influence BPO. Primarily, providers will look to SOA tools as a way to deliver efficient processes to their clients. In the longer term, such technologies may actually render BPO services unnecessary for more-astute organizations.

• Automated BPU services will continue to emerge, albeit slowly, as on-demand alternatives to traditional, multiyear BPO deals.

6.0 Geographic Issues, Trends and Events in the Outsourcing Market Analytical sources: Cassio Dreyfuss, Michele Caminos, Nicole France, Jim Longwood and Lorrie Scardino

Outsourcing is happening globally, but the portfolio of services and service maturity varies according to characteristics in each geographical area, including the economy and the maturity level of IT adoption and standardization. These two variables will ultimately drive outsourcing uptake in each country and in different areas inside a country.

Globalization pressures, however, are progressively making local variables less important. Multinational companies are pressing for global adoption of outsourcing solutions without appropriately considering local business practices or IT maturity levels. Conversely, multinational service providers are evolving toward a GDM, effectively learning how to manage and deploy resources worldwide.

As a result, a tiered market is emerging, in which multinational clients work with multinational service providers; and smaller, local businesses, which are often shunned by large service providers, engage with smaller, local service providers. This scenario creates an interesting gap, characterized by local or very specific needs of multinational clients that cannot be easily met by multinational service providers (because they don't have the required local knowledge or capability, or because they don't have the flexibility to comply with specific demands).

These factors have basically created two outsourcing approaches. In the most mature IT markets, outsourcing is becoming another tool in the IT toolbox as part of an overall business strategy, although not without challenges in more-advanced areas, such as utility computing. In less-mature IT markets, outsourcing is still a work in progress, and multinational and local or regional providers are still trying, testing and refining their business models.

6.1 What We Saw in the Global Outsourcing Market in 2005 Thinking globally and acting locally: Multinational service providers struggled to shift resources around the world to connect with local clients while maintaining high service levels. Local service providers that excel at navigating the culture and red tape of their home countries had trouble scaling up to a global perspective.

Leveraging scale for buying power: Multinational organizations leveraged their global scale and negotiated service contracts with global service providers, including their different geographic locations under a master agreement. They often modeled the service they expected to buy and deployed globally, overlooking different local practices (to the chagrin of local businesses and IT middle managers that had to make it work).

Publication Date: 14 December 2005/ID Number: G00131095 Page 22 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Leveraging scale for selling power: Multinational service providers moved to develop GDMs, striving to standardize service, while concurrently heralding the upcoming "utility" generation of products.

The immature side of global delivery: Organizations struggled with global processes, and the IT services market continued to invest in global consistency and process quality. Global delivery is still a big challenge on both sides.

Big break for small providers: In 2004, small providers were still complaining that they could not compete head-to-head with big providers for multinational clients. In 2005, the small providers adopted distinct strategies — not "scaled down" versions of multinational strategies. They moved away from the standard portfolios offered by multinationals. They leveraged characteristics (such as increased personal attention and relationships) that are beyond the practical reach of multinational service providers. As a result, multinational clients increasingly retained local service providers to cater to specific local needs.

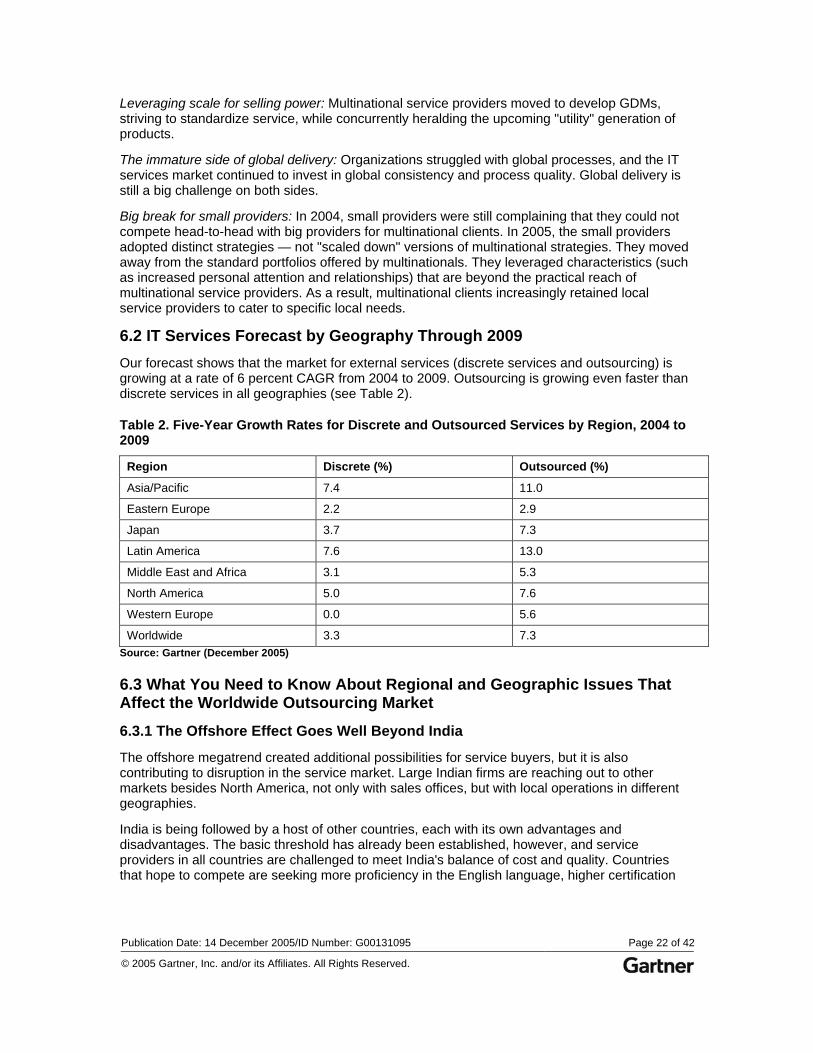

6.2 IT Services Forecast by Geography Through 2009 Our forecast shows that the market for external services (discrete services and outsourcing) is growing at a rate of 6 percent CAGR from 2004 to 2009. Outsourcing is growing even faster than discrete services in all geographies (see Table 2).

Table 2. Five-Year Growth Rates for Discrete and Outsourced Services by Region, 2004 to 2009

Region Discrete (%) Outsourced (%)

Asia/Pacific 7.4 11.0

Eastern Europe 2.2 2.9

Japan 3.7 7.3

Latin America 7.6 13.0

Middle East and Africa 3.1 5.3

North America 5.0 7.6

Western Europe 0.0 5.6

Worldwide 3.3 7.3 Source: Gartner (December 2005)

6.3 What You Need to Know About Regional and Geographic Issues That Affect the Worldwide Outsourcing Market

6.3.1 The Offshore Effect Goes Well Beyond India

The offshore megatrend created additional possibilities for service buyers, but it is also contributing to disruption in the service market. Large Indian firms are reaching out to other markets besides North America, not only with sales offices, but with local operations in different geographies.

India is being followed by a host of other countries, each with its own advantages and disadvantages. The basic threshold has already been established, however, and service providers in all countries are challenged to meet India's balance of cost and quality. Countries that hope to compete are seeking more proficiency in the English language, higher certification

Publication Date: 14 December 2005/ID Number: G00131095 Page 23 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

levels in the Software Engineering Institute's Capability Maturity Model, ITIL and other standards, and service export tax breaks.

6.3.2 Turbulence in the European Market

In tough economic times, the use of outsourcing increases, primarily to reduce costs. Europe's economy is generally static or in decline, and organizations are increasing the use of outsourcing. Additionally, European organizations had been slow to adopt global delivery. Now, with the urgent need to reduce costs, they are more accepting of offshore and nearshore sourcing. At the same time, organizations are looking at outsourcing as a way to invigorate innovation, especially those that have been unable to execute strategic plans for innovation because of their limited ability to make the required investments in innovation. Consequently, organizations have expectations of cost reduction and business value from outsourcing — an expectation that is a challenge for the outsourcing market.

The market is fragmented on the supply side. Many regional providers serve clients in this region, and multinational and global providers target pan-European clients or European clients with worldwide operations. The competition is fierce, with smaller regional providers often competing head-to-head with global or multinational providers. Also, Europe has a high number of small and midsize businesses that global and multinational providers are challenged to serve.

Outsourcing providers in the European market are struggling to reduce operations costs to pass the savings on to their clients. Providers' profit margins are also declining, chiefly because of the high cost of doing business on a country-by-country basis. The market finds itself with complex operating models that were built up and maintained to address country-specific needs, and these operating models are a drain on profits. Most providers in Europe have been slow to see and act on the changes under way on the demand side.

The larger providers in Europe — Capgemini, EDS, IBM, Siemens, T-Systems International — are engaged in enterprisewide, multiyear restructuring programs, with a special emphasis on Europe. As part of this evolution, most service providers are reducing the number of employees in Western Europe and increasing their delivery capabilities nearshore (in Eastern Europe and Mediterranean Africa) or offshore (in India and Latin America; see "Outsourcing Can Act as a Driver or Ballast for IT Services Growth").

The focus of Indian providers on the European market forges on, as confirmed by the increasing acceptance of global delivery in continental Europe and the growth rate of offshore providers in Europe. One of the biggest confirmations of the Indian providers' traction in the European market was the deal between the Pearl Group and TCS involving the acquisition of approximately 1,000 Pearl staff by TCS (see "TCS Gains U.K. Service Capabilities With Pearl BPO Venture").

6.3.3 Latin America Becomes a Burgeoning Nearshore and Offshore Destination

Although countries in Latin America share a common origin, their economic, political and social conditions vary. Mexico and Brazil lead Latin America's IT market, and most service providers will choose these countries to anchor their Latin American efforts and find local partners.

In an outbound move, Mexican and Brazilian service providers are targeting North America, with whom they share a similar Western culture and compatible time zones. Two such examples are CPM, a company from Brazil, and Softek, a Mexican company. CPM initially provided services to General Electric's (GE's) Brazilian operations and was later retained in a nearshore and offshore capacity by GE to do work for its Mexican, U.S. and Spanish operations. Softek acquired GE's development centers in Mexico and extended its relationship with GE from Mexico to the U.S.

Indian providers still have an edge in lower costs and higher certification levels, so Latin American service providers are trying to differentiate their service portfolios and go-to-market

Publication Date: 14 December 2005/ID Number: G00131095 Page 24 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

strategies, leveraging specific Latin American characteristics (for example, the work style and culture in the region establishes easy and intense relationships with clients, exhibits great empathy with them, and is creative and operates with agility and flexibility). Armed with those strategies, they are now moving abroad with some interesting results.

To support their global diversification efforts, Indian companies are developing operations in Latin America, where they are blending a large number of local resources with Indian experts and their own methodologies. A notable example is TCS, which is using Brazilian resources for its part of the ABN AMRO deal. Other Indian companies are prospecting the region, selecting from between Mexico and Brazil to host their operations.

Two main hurdles still hamper global companies' IT development in Latin American countries:

• Laws and regulations tend to overprotect employees and are not suited to a dynamic service economy.

• Education, on average, is deficient.

6.3.4 Asia/Pacific Markets Are as Diverse as the Geography Is Expansive

The uptake of technology and services in Asia/Pacific differs significantly around the region. Culture, politics and local business practices often dictate IT services decisions, superseding the more technically focused evaluations used in the West. Mature markets are racking up single-digit growth rates for outsourcing, while developing markets are seeing much greater growth.

Offshore service provisioning across the region is less prevalent than in the U.S. or Western Europe. Labor arbitrage internally to the region is less attractive than between Asia/Pacific and other regions.

Mature Markets

• In Australia and New Zealand, IT outsourcing has been a common business practice for many years, and multisourcing discussions are advancing.

• In Hong Kong, financial institutions are advanced in their outsourcing practices, and the government is moving from out-tasking to outsourcing.

• In Singapore, growth in IT outsourcing looks quite strong, mirroring the tightly knit, healthy economy.

Developing Markets

• All eyes are on China, with its large population and fast uptake in technology and related services. The value of outsourcing is lower for the domestic market because of organizations' large, internal IT departments, low labor costs and strong skills coming out of the universities. Most Chinese service providers do not have outsourcing capabilities, methodologies or processes in place.

• South Korea is the second-largest market for outsourcing, with double-digit growth rates. This market is a captive market with the "chaebol" structure, where large conglomerates spinoff an IT services company, which then supports the other companies within the conglomerate with tight bonds in an almost captive market. The chaebols do not have mature service processes to handle sophisticated SLAs. The Korean transportation and financial industries are most open to the use of ESPs.

Publication Date: 14 December 2005/ID Number: G00131095 Page 25 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

6.4 What Gartner Expects to See in the Global Outsourcing Market in 2006 • Increasingly complex sourcing management: As technology becomes more complex,

the business environment more uncertain and services more globally diverse, outsourcing choices must become increasingly granular. Organizations will have to manage a dynamic and complex combination of internal and external resources from various geographies. This strategic approach will be evident first among global and mature companies.

• Critical local vs. global choices: As global providers enter new territories, and as local providers become mature and competitive, global vs. local choices will become critical. Buyers must be sure to include different local and global delivery models in their sourcing strategies and provider selection processes.

• Instability in the European IT services market: Outsourcing clients in Europe should expect high turbulence in the European market in 2006. There will be a continuous decline of the "national champions" in the European market (that is, providers that are strong in a single country, but not developed enough within the region or a number of countries). Sourcing best practices — especially around sourcing strategy, relationship management, risk management and exit management — should be considered mandatory.

• The role of China: China will remain a wild card in 2006. As a result of educational policies, it has the biggest pipeline of resources in the world (although currently not at the top position for service quality). However, its growing economy may employ those resources in internal IT organizations. Most likely, multinationals will partner with Chinese service providers — multinationals have the skills and Chinese service providers have the local relationships.

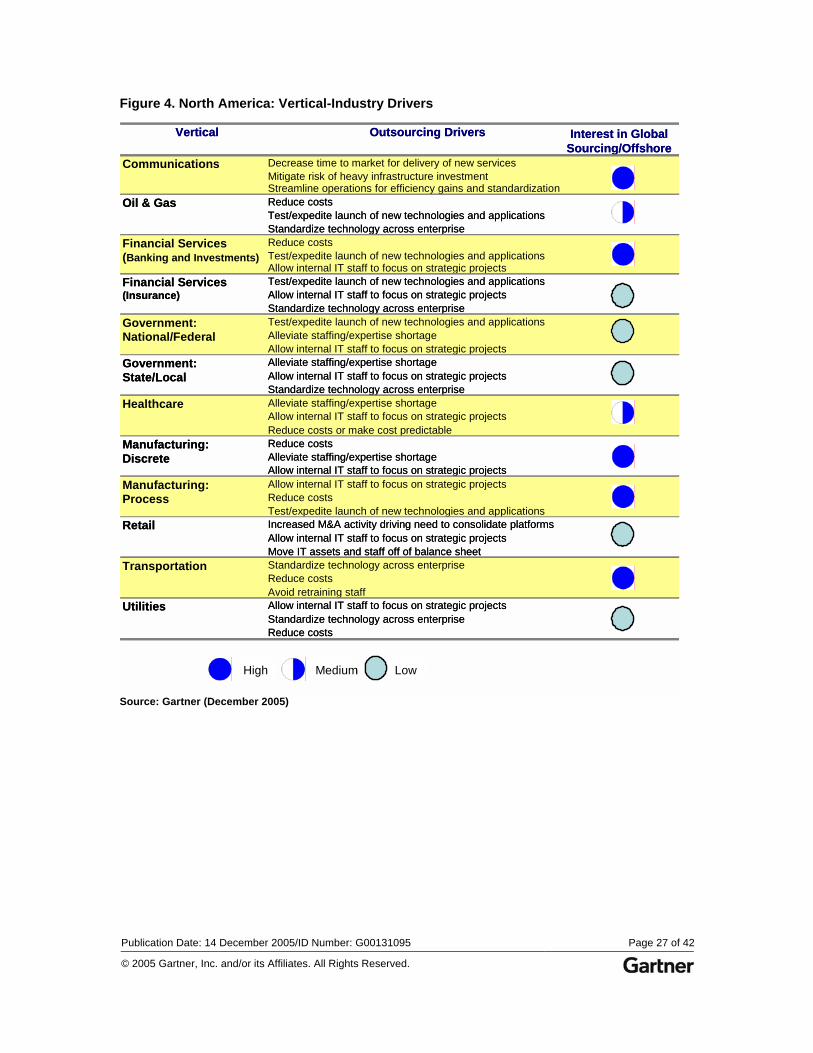

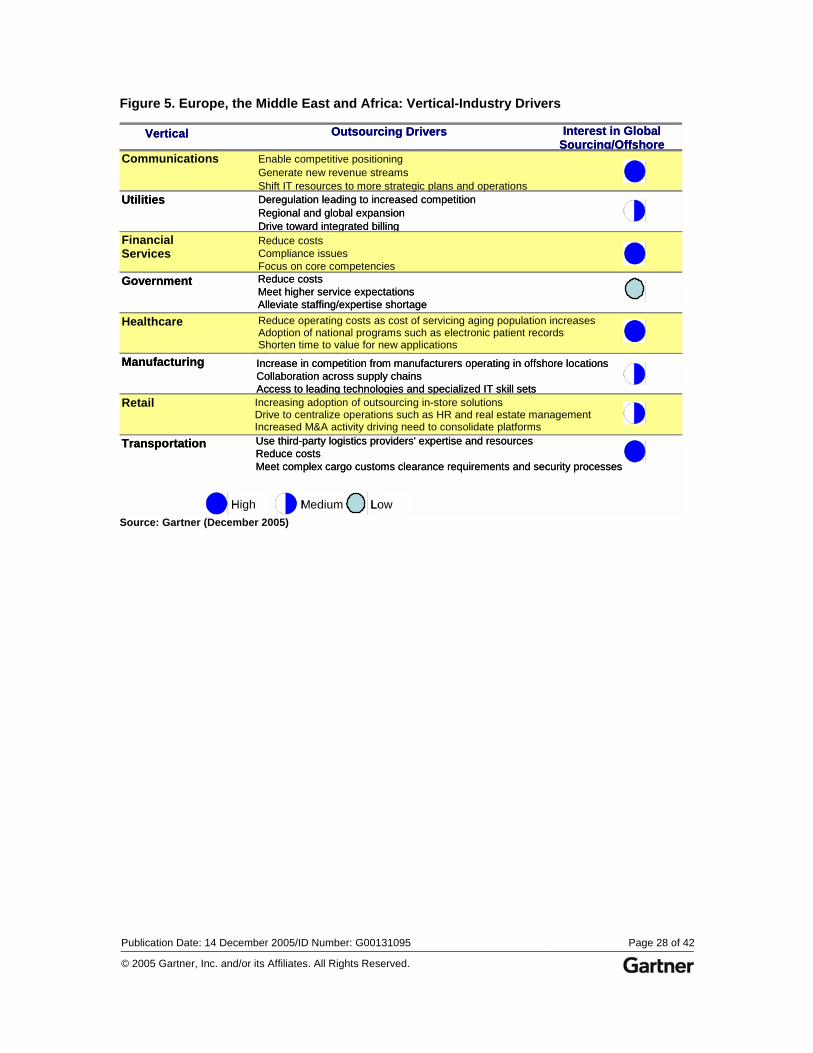

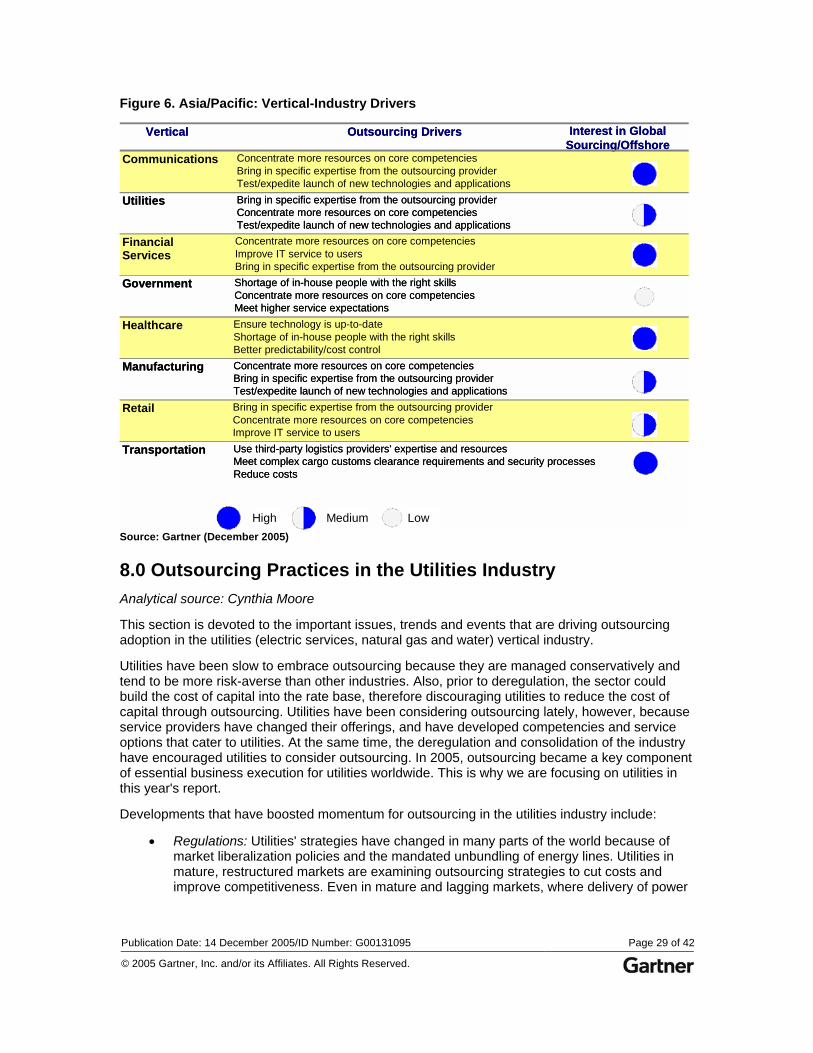

7.0 Outsourcing Practices by Vertical Industry Analytical sources: John Lovelock, Susan Cournoyer, Geraldine Cruz, Robert Goodwin, Venecia Liu, Cynthia Moore, Peter Redshaw, Emma Rose, Jeff Roster and Rishi Sood

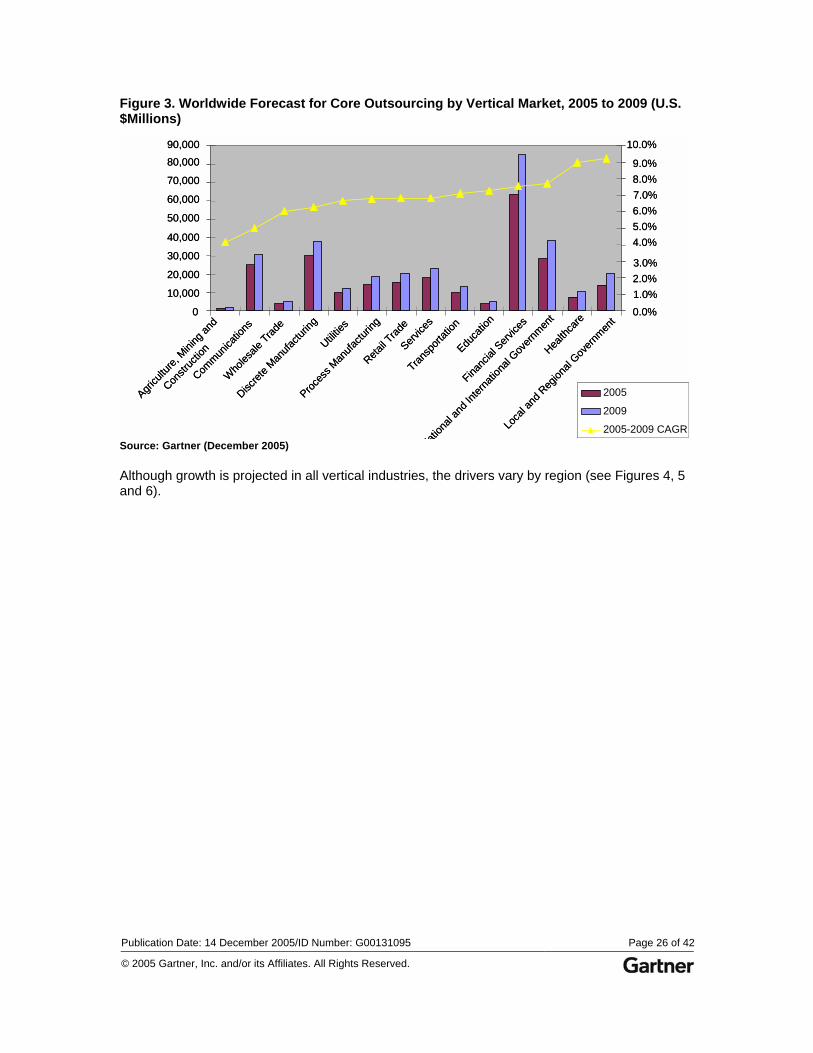

Financial services, government and manufacturing industries still constitute the largest core outsourcing markets globally, and continue to expand the range of services outsourced. (Gartner Dataquest defines core outsourcing as "the sum of IT management services and process management services.")

The utility and retail markets, traditionally reluctant to outsource, are increasingly embracing outsourcing. In 2005, two prominent deals were struck in these sectors: a $2 billion contract between the U.S. utility NiSource and IBM Global Services, and a $500 million contract between Dutch grocer Royal Ahold and EDS. Also, in 2005, two prominent contracts in the retail vertical industry were reversed: one between the U.S. retailer Sears, Roebuck and CSC, and one between the U.K. grocer Sainsbury and Accenture.

7.1 Vertical Industry Forecast Through 2009 Although the financial services, government and manufacturing industries will continue to dominate outsourcing spending through 2009, Gartner projects growth in every vertical industry (see Figure 3).

Publication Date: 14 December 2005/ID Number: G00131095 Page 26 of 42

© 2005 Gartner, Inc. and/or its Affiliates. All Rights Reserved.

Figure 3. Worldwide Forecast for Core Outsourcing by Vertical Market, 2005 to 2009 (U.S. $Millions)

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,00090,000