game changer a new kind of value chain for entertainment ... · a new kind of value chain for...

TRANSCRIPT

December 2013

Game changerA new kind of value chain for entertainment and media companies

2 Game Changer: A new kind of value chain

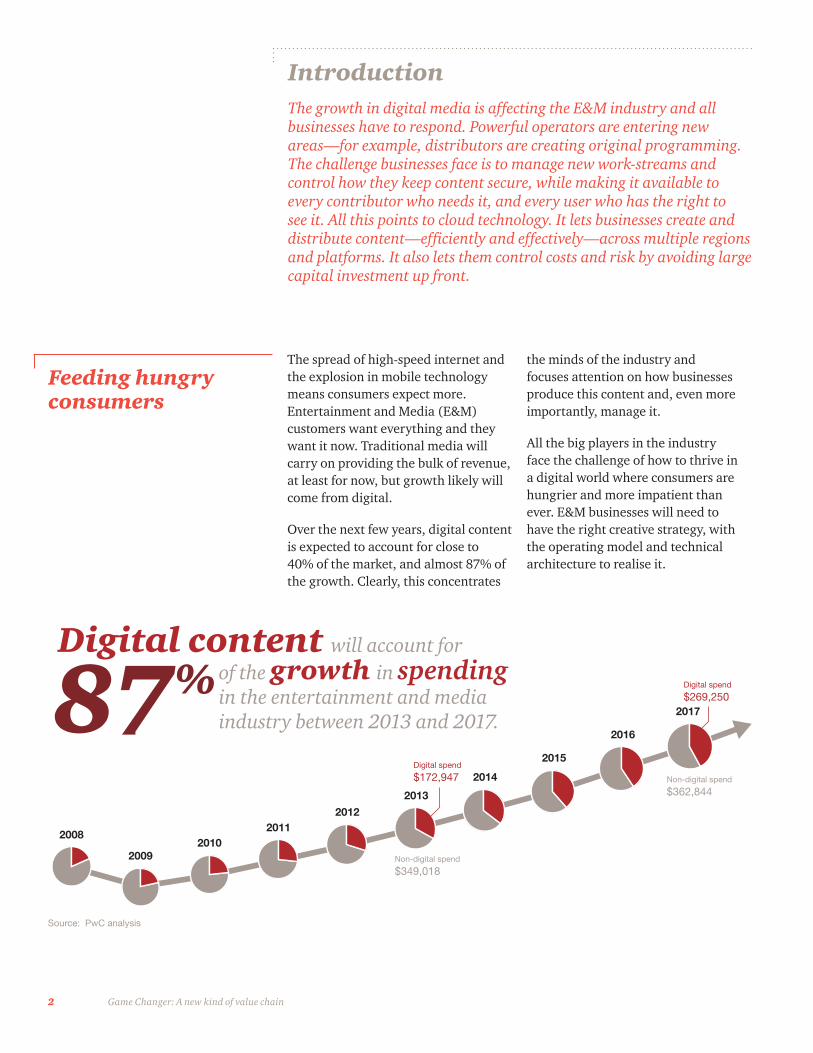

The spread of high-speed internet and the explosion in mobile technology means consumers expect more. Entertainment and Media (E&M) customers want everything and they want it now. Traditional media will carry on providing the bulk of revenue, at least for now, but growth likely will come from digital.

Over the next few years, digital content is expected to account for close to 40% of the market, and almost 87% of the growth. Clearly, this concentrates

the minds of the industry and focuses attention on how businesses produce this content and, even more importantly, manage it.

All the big players in the industry face the challenge of how to thrive in a digital world where consumers are hungrier and more impatient than ever. E&M businesses will need to have the right creative strategy, with the operating model and technical architecture to realise it.

Feeding hungry consumers

IntroductionThe growth in digital media is affecting the E&M industry and all businesses have to respond. Powerful operators are entering new areas—for example, distributors are creating original programming. The challenge businesses face is to manage new work-streams and control how they keep content secure, while making it available to every contributor who needs it, and every user who has the right to see it. All this points to cloud technology. It lets businesses create and distribute content—efficiently and effectively—across multiple regions and platforms. It also lets them control costs and risk by avoiding large capital investment up front.

2017

2016

2015

2014

2013

20122011

20102009

2008

Digital content will account for of the growth in spending in the entertainment and media industry between 2013 and 2017.87%

Digital spend

$172,947

Non-digital spend

$349,018

Digital spend

$269,250

Non-digital spend

$362,844

Source: PwC analysis

3 Game Changer: A new kind of value chain

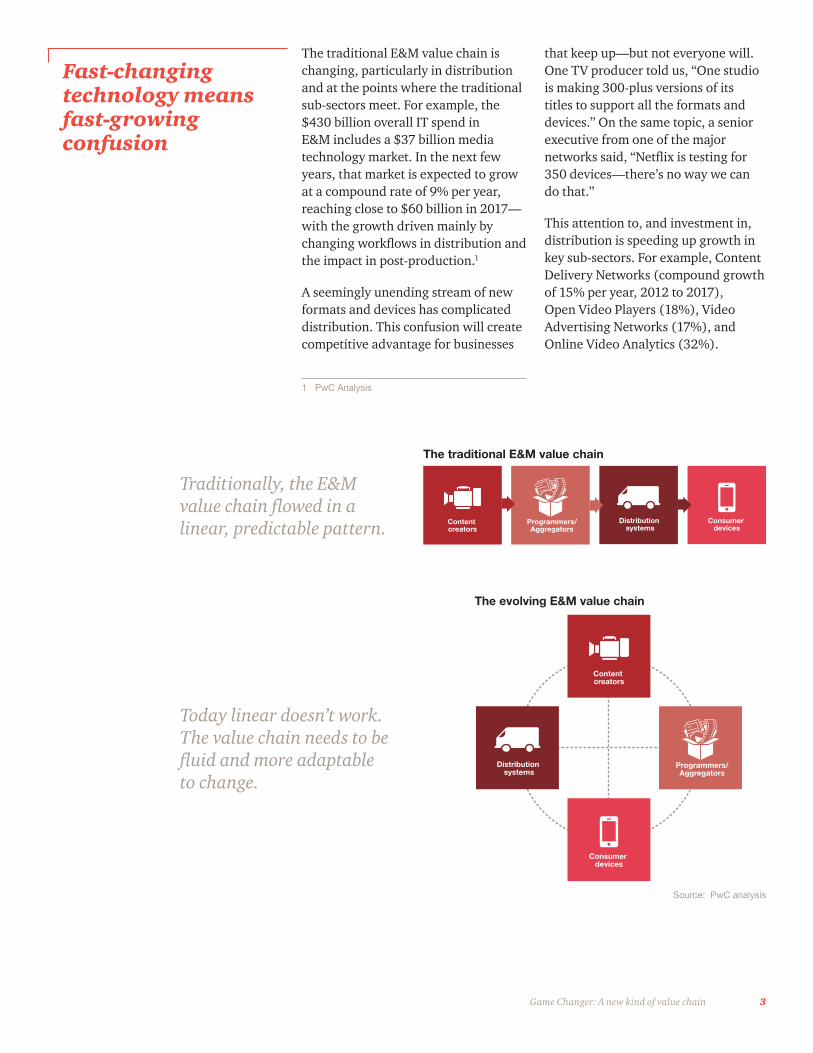

The traditional E&M value chain is changing, particularly in distribution and at the points where the traditional sub-sectors meet. For example, the $430 billion overall IT spend in E&M includes a $37 billion media technology market. In the next few years, that market is expected to grow at a compound rate of 9% per year, reaching close to $60 billion in 2017—with the growth driven mainly by changing workflows in distribution and the impact in post-production.1

A seemingly unending stream of new formats and devices has complicated distribution. This confusion will create competitive advantage for businesses

Fast-changing technology means fast-growing confusion

Consumer devices

Distribution systems

Programmers/Aggregators

Content creators

The traditional E&M value chain

The evolving E&M value chain

Source: PwC analysis

that keep up—but not everyone will. One TV producer told us, “One studio is making 300-plus versions of its titles to support all the formats and devices.” On the same topic, a senior executive from one of the major networks said, “Netflix is testing for 350 devices—there’s no way we can do that.”

This attention to, and investment in, distribution is speeding up growth in key sub-sectors. For example, Content Delivery Networks (compound growth of 15% per year, 2012 to 2017), Open Video Players (18%), Video Advertising Networks (17%), and Online Video Analytics (32%).

Consumer devices

Distribution systems

Programmers/Aggregators

Content creators

Traditionally, the E&M value chain flowed in a linear, predictable pattern.

Today linear doesn’t work. The value chain needs to be fluid and more adaptable to change.

1 PwC Analysis

4 Game Changer: A new kind of value chain

Clearly businesses are deciding what they can do and what they can’t. But the most successful ones will base these decisions not on what they’ve done in the past, but what will make strategic sense in the future.

Digital content is not bound by the constraints of traditional media. An individual content producer can take their product direct to the consumer, via iTunes, YouTube, or similar.

Most of the large Hollywood studios are part of Ultraviolet, which lets consumers store content in the cloud and access it from different devices. Also, content aggregators like Google, Amazon, Netflix, and Microsoft are producing content themselves—the traditional domain of the studios and networks. Amazon recently announced streaming deals with CBS and PBS and is producing its own comedy series. Also, the

leading companies in online video—Google’s YouTube and Microsoft’s Xbox Studio—are moving towards a studio model where independents get equipment and support in return for distribution rights.

But the strength of these new entrants is not just about their capacity to create good content. For example, Google is investing more than $200m in original TV as a new way of driving its advertising business. And Netflix produced House of Cards, a high-quality drama that has attracted attention, and driven traffic and subscription customers to its parent site.

In these cases and others, the content is an asset in itself, but it also has a wider strategic value to the business. And this sort of innovation will only grow. Many of these new entrants are very large, and have the resources to experiment and disrupt.

Businesses are not just sticking with what they know best

driving digital growth

Content creators are increasingly building direct relationships with consumers

Content distributors are increasingly looking to create their own content

Advertisers are looking beyond the traditional agency model

5 Game Changer: A new kind of value chain

This growing complexity means that the traditional E&M value chain is not linear any more, but fluid and multi-directional. Not a chain at all, in fact, but something much more complex. Distribution can happen at any stage after pre-production starts and carry on right through work-in-progress.

As this becomes the new normal, businesses will need more flexibility and collaboration—to manage complex workflows and data being exchanged between everyone involved. This points to two big issues: how to manage the workflow, and how to store and share the assets at every stage of the process.

Workflows will increasingly focus on information and automation. Detailed analytics give businesses a clear picture of their consumers—based on the patterns of their life online. Also, as metadata identifies different versions of content, businesses will—in theory—be able to automatically

distribute different versions to different regions at different times. Of course, while the logic of this is simple, the logistics are highly complex.

Bringing analytics and metadata closer together will mean that specific, tailored content can be sent or offered to specific consumers. And that means new opportunities for advertisers, publishers, and subscription services.

But it’s not just about the consumers. It’s also vital to streamline the flow to, from, and among the creative team. This orchestration of creative resources presents a huge challenge, but also a huge opportunity for the businesses that get it right. They’ll be able to streamline a real-time creative process, operating at every stage of the production process, with collaborators spread across the world. This will help them manage workflow, and share resources—both in terms of content and production tools.

A new value chain means new opportunities

Pre-production Production

Post production

Media lifecyclemanagement

Multiplatformdistribution

Experienceintegration Consumption

Workflowplanning

Collaborationenablement

Richindexing

Metadataanalytics

Distributionorchestration

Customization/personalization

Measurementand interaction

Media asset flow

Information flow

Source: PwC analysis

6 Game Changer: A new kind of value chain

One way or another, everything we’ve described so far points in one very clear direction. Businesses need to store multiple copies of content at every stage of the value chain in a way that gives instant access to anyone and everyone who needs to work on it, or has the right to use it.

And that points in turn to cloud technology. And our research and interviews with industry leaders suggest six reasons why cloud services make sense for the E&M value chain:

1. Shifting from Capex to Opex—much lower up-front investment means less risk.

2. Flexibility—businesses only pay for what they use. Plus they can bring in new software fast and ramp up storage to support peak demand.

3. Lower costs—cheaper bandwidth and storage is making the cloud more affordable.

4. Full-time support—tools and software are supported and updated remotely.

5. Create and control content across all formats, for all devices.

6. Collaboration—the cloud is an ideal platform to collaborate efficiently across all content and all territories. It avoids duplication and creates consistency.

As the technology industry carries on accelerating, and faster internet serves faster machines, somehow consumers will stay ahead. And digital consumers, in particular, will always have the appetite for one more byte.

We believe that, in this market, businesses will thrive by using cloud technology that can flex and grow, controlled within workflows and strategy that can do just the same.

The answer is in the cloud

pwc.com/us/em

© 2013 PricewaterhouseCoopers LLP, a Delaware limited liability partnership. All rights reserved. PwC refers to the US member firm, and may sometimes refer to the PwC network. Each member firm is a separate legal entity. Please see www.pwc.com/structure for further details.

This content is for general information purposes only, and should not be used as a substitute for consultation with professional advisors. PwC US helps organizations and individuals create the value they’re looking for. We’re a member of the PwC network of firms in 157 countries with more than 184,000 people who are committed to delivering quality in assurance, tax and advisory services. Tell us what matters to you and find out more by visiting us at www.pwc.com/us.

CH14-0024

To have a deeper conversation about how this subject may affect your business, please contact:

Deborah Bothun [email protected]

Cindy [email protected](213) 217-3545

Matthew [email protected](213) 217-3326

Blake [email protected](408) 386-9140