fy 2016 results - alpha bank · 9m 2013 resultsfy 2013 resultsfy 2016 results 4 i growth drivers...

TRANSCRIPT

F Y 2 0 1 6 R e s u l t s

March 30, 2017

9M 2013 Results FY 2013 Results 2 FY 2016 Results 2

This presentation contains forward-looking statements, which include comments with respect to our objectives and strategies, and the results of our operations and our business,

considering environment and risk conditions.

However, by their nature, these forward-looking statements involve numerous assumptions, uncertainties and opportunities, both general and specific. The risk exists that these

statements may not be fulfilled. We caution readers of this presentation not to place undue reliance on these forward-looking statements as a number of factors could cause future Group

results to differ materially from these targets.

Forward-looking statements may be influenced in particular by factors such as fluctuations in interest rates, exchange rates and stock indices, the effects of competition in the areas in

which we operate, and changes in economic, political, regulatory and technological conditions. We caution that the foregoing list is not exhaustive.

When relying on forward-looking statements to make decisions, investors should carefully consider the aforementioned factors as well as other uncertainties and events.

Pages

I. Macroeconomic Update 3

II. FY 16 Performance Highlights 7

III. FY 16 Performance 20

1. Balance Sheet 20

2. Pre Provision Income 22

3. Asset Quality 26

4. Liquidity 32

5. Capital 35

IV. Appendix 37

Table of Contents

3 FY 2016 Results 3

I. Macroeconomic Update

9M 2013 Results FY 2013 Results 4 FY 2016 Results 4

I

Growth Drivers from 2017 Onwards: Could They Shift to the Investment Side?

Macro Dynamics Remain Weak Reflecting the Lingering Uncertainty

Unemployment Declined with New Jobs in Tourism, Industry

and Public Administration

Business and Consumer Confidence: Two faces of Janus?

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

40

50

60

70

80

90

100

110

Business Confidence in Industry, lhs Business Confidence in Retail Trade, lhs Consumer Confidence Indicator, rhs

Source: ELSTAT, Alpha Bank calculations

Source: IOBE

15

17

19

21

23

25

27

29

-12

-10

-8

-6

-4

-2

0

2

4

2012 2013 2014 2015 2016 2017f 2018f

Public Consumption Net Exports

Private Consumption Investment (inc.inventories)

GDP, % yoy (E.C. forecasts) GDP (Alpha forecasts)

Unemployment Rate (%)

Resilience

Stagnation

Capital

Controls

Unemployment

Rate

pps

Source: ELSTAT, Alpha Bank calculations

-40

-20

0

20

40

60

80

100

120

140

-500.0

-400.0

-300.0

-200.0

-100.0

0.0

100.0

2010 2011 2012 2013 2014 2015 2016

Other Services

Public Adin. & Non-Business Sector*

Tourism

Trade

Construction

Industry

Agriculture

Part-time

Full- time

Bars: Contributions of New Jobs per Sector (yearly change in thousand employees, lhs)

Lines: Full-time and Part-time employment (Index 2010=100, rhs)

* Includes: Public Administration, Defence, Social Security, Education, Health, Arts

thous.

The Greek economy stalled in 2016 for a second consecutive year (2015: -0.2%,

2016: 0.0%), yet showing signs of resilience despite the imposition of capital

controls in July 2015

Private consumption growth was a solid 1.4% in 2016 despite the households’

tax burden, investment remain unchanged, while net exports subtracted 0.5

points from GDP

Our baseline scenario envisages an output expansion at a pace between 1.5%

and 1.7% in 2017. It necessitates an investment growth exceeding 10%, so that

net fixed capital formation, i.e. gross investment minus depreciation, to turn

positive again

New job contracts in private sector referring to part-time and temporary

employment account for 54.7% of total contracts, in 2016, outweighing full time

contracts that account for 45.3%

9M 2013 Results FY 2013 Results 5 FY 2016 Results 5

I

Drivers of the Over-Performance of Primary Surplus (State Budget) in 2016

Against the Target Set

Source: Min.Fin.

Fiscal Performance Better Than Targeted in 2016

Fiscal Discipline Is Getting More Intense . . .

Source: Min.Fin.

. . . But Private Sector Arrears to the State Are Accumulating

% of GDP

-20

-15

-10

-5

0

5

2009 2010 2011 2012 2013 2014 2015 2016e 2017f 2018f

General Government Primary Balance

General Government Balance

General Government Primary BalanceTarget

40.0

95.3

30

40

50

60

70

80

90

100

2010 2013 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 2016

Private Arrears to the Public Sector Private Arrears, Quarterly +

in € bn

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

Personal Income Tax

Property Tax VAT Excise Tax on Fuel

Primary Expenditure

PIB* Expenditure

in € bn

Source: Min.Fin.

* Public Investment Budget

Fiscal outcome, in 2016, is better than targeted on the back of:

tax rate hikes applied upon an almost stable economic activity

government arrears’ clearance at low pace and

the extensive use of electronic transactions.

The most recent budget execution data point to a general government

primary surplus close to 2.0% of GDP for the full-year 2016, well in excess of

the respective program target set for 0.5% surplus

Primary surplus target in 2017 budget is well within reach, conditional on:

a rise in domestic economic activity as well as

the smooth implementation of the agreed structural measures aiming

to curb tax evasion and broaden the tax base

9M 2013 Results FY 2013 Results 6 FY 2016 Results 6

I

Source: ELSTAT

Inflation, Production and Competitiveness

Deflation Pressures Eased

Source: ELSTAT, EC Forecasts Winter 2017

Unit Labour Cost (ULC) and Price Competitiveness

-15

-10

-5

0

5

10

15

-6

-4

-2

0

2

4

6

HICP, lhs

Output Gap, rhs

ULC, rhs 80

85

90

95

100

105

110

115

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II III

2009 2010 2011 2012 2013 2014 2015 2016

REER* (ULC based) REER* (CPI based)

Competitiveness

recouped

• Tax hikes

• Risk premium

• Distortions in the

product markets

% %

%

Source: Eurostat

-10

-8

-6

-4

-2

0

2

4

Manufacturing Production (Index, 12-month mov. average % yoy)

Retail Trade (Index, 12-month mov. average % yoy)

Retail Trade excl. Fuel (Index, 12-month mov. average % yoy)

Hard Data: Industrial Production and Retail Sales (Turnover index at current prices)

* Real Effective Exchange Rate

Deflation pressures have eased in 2016 (HICP: 0%) as a result of the significant

increase of tax rates on consumption and the upward trend in energy prices in the

last two months of 2016

Internal devaluation in accordance with labour market flexibility resulted in

significant declines in unit labour cost

It is indicative that real effective exchange rate (REER) measured by unit labour

cost showed significant improvement

However, competitiveness measured by CPI improved only slightly, implying

rigidities in the product market that hamper price adjustments

7 FY 2016 Results 7

II. FY 16 Performance Highlights

9M 2013 Results FY 2013 Results 8 FY 2016 Results 8

Restoration in profitability in 2016 supports capital preservation ahead of further

balance sheet restructuring; FY 16 Profit after Tax at €42mn II

Note: P&L numbers restated for the sale of Serbia

1 Includes €71.9mn related to the acquisition of Visa Europe from VISA Inc. in Q2 2016

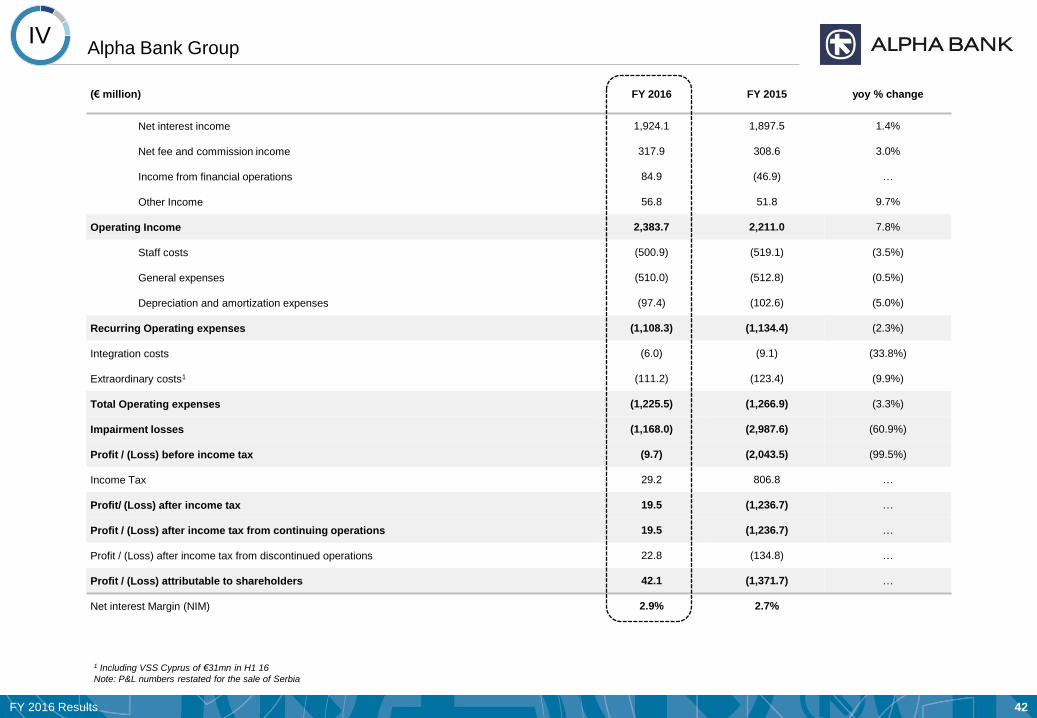

Profit & Loss (€ million) FY

2016

FY

2015

yoy %

change

Q4

2016

Q3

2016

qoq %

change

Net Interest Income (NII) 1,924 1,897 1.4% 490 481 1.8%

Fees and commissions Income 318 309 3.0% 81 81 0.1%

Trading & Other Income 1 142 5 … 31 25 …

Operating Income 2,384 2,211 7.8% 602 587 2.5%

Total Operating Expenses (1,226) (1,267) (3.3%) (356) (281) 26.3%

Recurring Operating Expenses (1,108) (1,134) (2.3%) (285) (281) 1.2%

Pre Provision Income (PPI) 1,158 944 22.7% 247 306 (19.3%)

Core Pre Provision Income 1,191 1,123 6.0% 302 297 1.5%

Impairment Losses (1,168) (2,988) (60.9%) (304) (258) 17.7%

Profit/ (Loss) before income tax

(PBT) (10) (2,043) … (57) 48 …

Income Tax 29 807 … 62 (8) …

Profit/ (Loss) after income tax from

Discontinued Operations 23 (135) … 15 1 …

Profit/ (Loss) after income tax 42 (1,372) … 20 41 (51.0%)

Net Interest Margin (NIM) 2.9% 2.7% 3.0% 2.9%

Recurring Cost to Income ratio 48.2% 50.2% 48.6% 48.6%

Core PPI at € 1,191mn for the FY 16, up by 6% yoy, driven by an improved core

revenue performance and operating efficiencies. NIM improved by 20bps yoy to

2.9%

Recurring OPEX at €1,108 million, down by 2.3% yoy. Cost to income ratio at

48.2% for FY 16

Eurosystem funding further reduced to €18.3bn driven by deposits inflows,

EFSF bonds disposals and SME securitisation

NPLs at 38.1%. Cash coverage of 69%, supports implementation of NPE/NPL

reduction plan

LLPs at € 304mn in Q4, with Cost of Risk at 2.01% of gross loans

CET1 ratio increased to 17.1%. Tangible Equity at € 8.7bn. Tangible Book

Value per share at €5.66

Balance Sheet (€ billion) 31/12/2016 31/12/2015

Assets 64.9 69.3

Net Loans 44.4 46.2

Deposits 32.9 31.4

Eurosystem Funding 18.3 24.4

Tangible Equity (TE) 8.7 8.7

Common Equity Tier 1 ratio (CET1) 17.1% 16.6%

NPL ratio 38.1% 36.8%

Cash Coverage 69% 69%

Total Coverage 125% 126%

NPE ratio 53.7% 51.3%

Cash Coverage 49% 50%

Total Coverage 106% 108%

9M 2013 Results FY 2013 Results 9 FY 2016 Results 9

16.8% 6 bps 11 bps 5 bps 17.1% 20bps 17.3% 17.3% 17.0%

CET 1 Sep-16

Period Result

AFS Reserve

RWA impact / Other

CET 1 Dec-16

Sale of Serbia CET 1 Dec-16

Proforma

Total Capital Adequacy Ratio

Dec-16 Proforma

FL CET1 Dec-16

Proforma

CET1 ratio quarterly build up adjusted for the sale of Serbia

II Common Equity Tier I Ratio increased further to 17.3%, including the positive impact

from the sale of Serbia; Fully Loaded ratio at 17%

1 Proforma includes the positive impact from the sale of Serbia

CET1

capital 8,560 8,631

(€ million)

QoQ +50bps

1 1

FL CET 1 at 11.3% even if Tax Credit law 4340/2015 not implemented

17.0%

(6.8%)

+1.1% 11.3%

FL CET 1 Dec-16

Proforma

Tax Credit RWA relief FL CET 1 Dec-16

Proforma

High CET1 ratio at 17.1% at the end of 2016, up by 30bps qoq

CET 1 ratio at 17.3% and Fully Loaded CET 1 ratio at 17.0% adjusted for the impact from

the sale of Serbia

RWA over Total Assets at 78% based on the standardised method

1

Total SREP Capital

Requirement (TSCR)

for 2017 at 12.25%

1

Without implementation of

DTC law

1

9M 2013 Results FY 2013 Results 10 FY 2016 Results 10

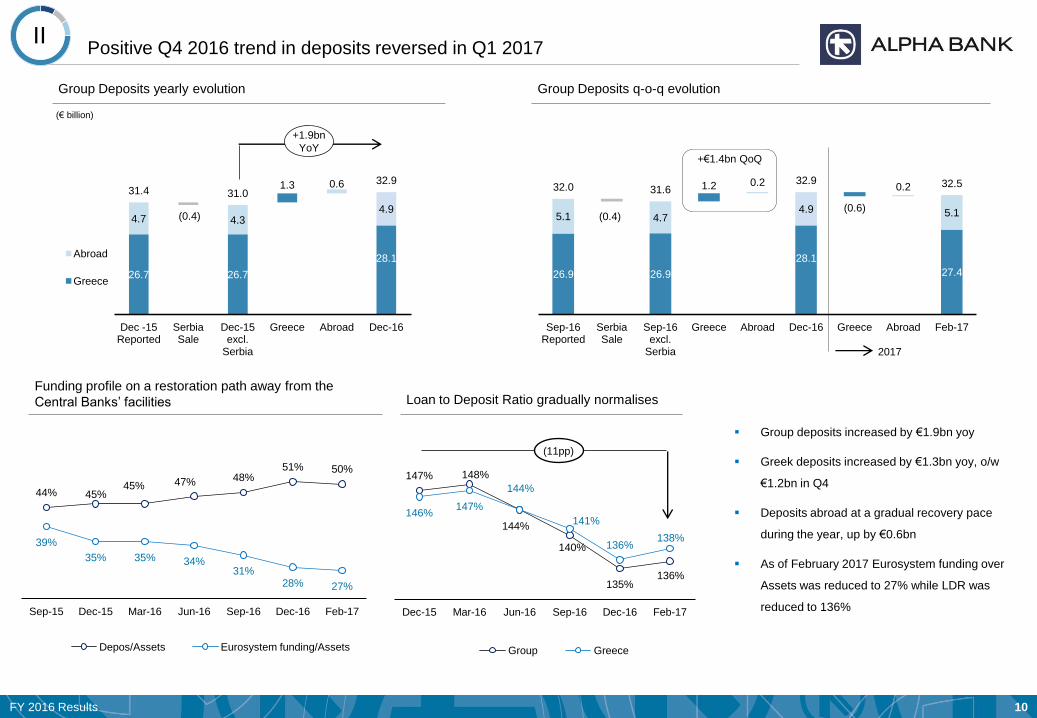

26.7 26.7

1.3

28.1

4.7 4.3

0.6

4.9 (0.4)

31.4 31.0

32.9

Dec -15 Reported

Serbia Sale

Dec-15 excl.

Serbia

Greece Abroad Dec-16

Abroad

Greece

Positive Q4 2016 trend in deposits reversed in Q1 2017 II

44% 45% 45% 47% 48%

51% 50%

39%

35% 35% 34% 31%

28% 27%

Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Feb-17

Depos/Assets Eurosystem funding/Assets

Group deposits increased by €1.9bn yoy

Greek deposits increased by €1.3bn yoy, o/w

€1.2bn in Q4

Deposits abroad at a gradual recovery pace

during the year, up by €0.6bn

As of February 2017 Eurosystem funding over

Assets was reduced to 27% while LDR was

reduced to 136%

Funding profile on a restoration path away from the

Central Banks’ facilities

Group Deposits yearly evolution

Loan to Deposit Ratio gradually normalises

(€ billion)

147% 148%

144%

140%

135% 136%

146% 147%

144%

141%

136% 138%

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Feb-17

Group Greece

(11pp)

+1.9bn

YoY

26.9 26.9

1.2

28.1

(0.6)

27.4

5.1 (0.4) 4.7

0.2

4.9

0.2

5.1

32.0 31.6 32.9 32.5

Sep-16 Reported

Serbia Sale

Sep-16 excl.

Serbia

Greece Abroad Dec-16 Greece Abroad Feb-17

+€1.4bn QoQ

2017

Group Deposits q-o-q evolution

9M 2013 Results FY 2013 Results 11 FY 2016 Results 11

4.8 5.2 4.8

(1.9)

(2.2) (0.3) (1.4)

(0.3) (0.5) 19.6

13.2 13.0

24.4

18.3 17.8

Dec-15 Deposits Inflows

Securities Disposal

Securitisation SME

Other B/S items

Interbank Repo

Dec-16 Feb-17

ECB ELA

Eurosystem reliance down by c.€6bn or -25% YoY;

Repo activity resumed since year end 2016 II

Eurosystem funding YoY reduction

(€ billion)

9.2

1.0 0.3

0.7 0.2

Dec-15 Dec-16 Feb-17 adjusted

Nominal Value Cash Value

(€ billion)

Pillar II reduced significantly, minimal balance

outstanding

o/w -€1.0bn Loans Deleveraging

1

o/w 2.2

EFSF

bonds

1 Adjusted for partial repayment of €700mn nominal value of Pillar II bonds on 14th of March 2017

o/w €1.6bn EFSF sale

0.3

0.6

1.2

Dec-15 Dec-16 Feb-17

Repos transactions up by €0.9bn since Dec. ‘15

€0.6bn

€0.3bn

(€ billion) -€8.9bn

o/w +€0.6bn Repos

-€6.1bn Eurosystem reliance at €18.3bn at the end of 2016,

mainly benefited by inflow of deposits, securities and B/S

deleveraging

Eurosystem funding reduced further in Feb. 2017 to

€17.8bn mainly due to repo transactions

Pillar 2 bonds reduced to €0.3bn to be fully repaid in the

coming months

Interbank repos increased to €1.2bn as of Feb. 2017,

gradually diversifying the Bank’s funding profile

TLTRO II as of end March at €3.1bn

Replacement of ELA funding, apart from banking book

evolution, will be driven by certain refinancing initiatives

with the restoration of market conditions

Covered bonds

Securitisations

Interbank repo

Senior bond issuance

9M 2013 Results FY 2013 Results 12 FY 2016 Results 12

Core PPI FY 16 at €1.2bn

Solid core PPI performance despite B/S deleveraging by €4.4bn II

2.3

(1.1)

1.2 €1.2bn

Core Operating Income

FY 16

Recurring Expenses

FY 16

Core PPI FY 16

2016 Target

1 Restated figures backward due to discontinued operations in Serbia

479 476 477

481

490

2.76% 2.77%

2.81%

2.88%

2.99%

465

475

485

495

505

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

NII NIM

(€ billion)

Net Interest Margin (NIM) remains strong

1 1

Core PPI1 improved driven by increased NII in Q4

306 9 297 9 0

(4)

302 16

(71)

247

Q3 16 Reported

PPI

Trading and one-off costs

Q3 16 Core PPI

Δ NII Δ Fees Δ OPEX & other income

Q4 16 Core PPI

Trading Οne-off costs

Q4 16 Reported

PPI

(€ million)

€ 54mn impairment of assets

€ 4mn integration costs

€ 13mn other

(1.8) (2.2) (0.4 )

69.3

64.9

Dec-15 Net loans Securities Other Dec-16

Balance sheet deleveraging

(€ billion)

-€4.4bn

(€ million)

9M 2013 Results FY 2013 Results 13 FY 2016 Results 13

(6)

0

11 4 481

490

Q3 16 (restated)

Loans Deposits Funding Bonds & other

Q4 16

NII improvement mainly driven by the decrease in cost of funding II

NII qoq on the back of lower funding cost

(€ million)

Decreasing funding cost both in Eurosystem and time deposits

1.07%

0.93% 0.82% 0.81%

0.75% 0.68%

1.67% 1.59%

1.48%

1.29% 1.21%

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16 Feb-17

New time depos rates Funding cost incl. Pillar II fees

NII yoy

(€ million)

(264) (200)

(385) (307)

(148)

63 78 34

2,228 2,080

318 352

1,897 1,925

FY 15 Loans Deposits Funding Bonds & Others

FY 16

Bonds & Other

Loans

Funding

Depos

o/w €46mn related to Pillar II

and €32mn from ELA-ECB

Basic Balance Sheet Funding sources

56% 63%

35% 25%

8.5% 10%

0.5% 2%

Dec -15 Dec-16

Repos

ECB Funding

ELA Funding

Deposits

+7%

-10%

9M 2013 Results FY 2013 Results 14 FY 2016 Results 14

Fee generation supported by improved performance of our card business II

Income from Cards and Acquiring

Fee & Commission Income up by 3% yoy mainly on the back of

increased card usage

Debit card turnover more than doubled in FY 16 vs. a year ago

Alpha Bank sole Issuer in Greece of Amex & Diners Cards

Alpha is the only Bank accepting cards from all the major Payment

Schemes (Visa, MasterCard, Amex, Diners, China Union Pay)

Upon normalisation of the economic conditions, fee generation from

Loans and Asset Management to further contribute to the Net Fees

& Commission Income

57

64

FY 15 FY 16

12%

(€ million)

Credit and Debit Cards Turnover and Merchant Sales

%

Total

1.8 2.2

1.2

2.5 3.1

4.6

FY 15 FY 16

Credit Debit

40%

60%

Turnover

53%

47%

2x

49%

2.7

4.2

1.6

1.8 4.3

6.1

FY 15 FY 16

Greek cards International cards

37%

63%

30%

70%

(€ billion)

58%

15%

42%

Merchant Acquiring Sales

Net Fees & Commission Income

(€ million)

262.0 275.3

40.1 34.8

6.5 7.8

308.6 317.9

FY 15 FY 16

Investment Banking & Brokerage

Asset Gathering

Commercial Banking

3%

5%

9M 2013 Results FY 2013 Results 15 FY 2016 Results 15

-3.5%

-0.5%

-5.0%

519 501

513 510

103 97

1,134 1,108

Dec -15 Dec-16

Depreciation & Amortization

G&As

Staff costs

1,150 1,120 1,108

(30)

FY 16 Target

Serbia Discontinued operations

FY 16 Target adj. for

Serbia sale

FY 16 Actual adj. for

Serbia sale

OPEX beat target set for FY 16 on the back of the ongoing platform rationalisation II

Recurring Operating Expenses

Employees

(€ million)

(249) (921) (24) (323) (476)

13,856

11,863

Dec-15 Cyprus VSS

Serbia Sale

Abroad Hilton Greece Dec-16

Branches

(76)

(7)

(93)

897

721

Dec-15 Serbia Sale

Abroad Greece Dec-16

Recurring Operating Expenses decreased by 2.3% yoy

(€ million)

-€26mn

-2.3%

-1,993

-14% 65%

54%

50% 48%

2013 2014 2015 2016

Recurring C/I ratio

-176

-20%

9M 2013 Results FY 2013 Results 16 FY 2016 Results 16

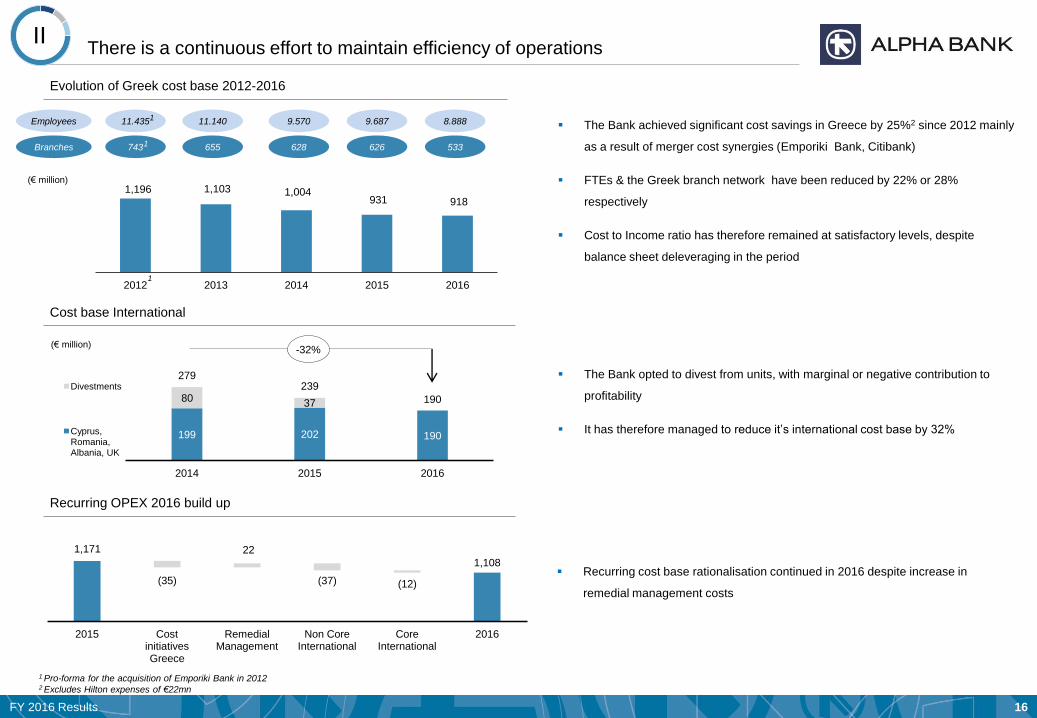

1,196 1,103 1,004 931 918

2012 2013 2014 2015 2016

There is a continuous effort to maintain efficiency of operations II

Evolution of Greek cost base 2012-2016

(€ million)

1 Pro-forma for the acquisition of Emporiki Bank in 2012 2 Excludes Hilton expenses of €22mn

11.435 11.140 9.570 9.687 8.888 Employees

743 655 628 626 533 Branches

Cost base International

(€ million)

199 202 190

80 37

279 239

190

2014 2015 2016

Divestments

Cyprus, Romania, Albania, UK

The Bank achieved significant cost savings in Greece by 25%2 since 2012 mainly

as a result of merger cost synergies (Emporiki Bank, Citibank)

FTEs & the Greek branch network have been reduced by 22% or 28%

respectively

Cost to Income ratio has therefore remained at satisfactory levels, despite

balance sheet deleveraging in the period

The Bank opted to divest from units, with marginal or negative contribution to

profitability

It has therefore managed to reduce it’s international cost base by 32%

1

1

1

-32%

Recurring OPEX 2016 build up

1,171

(35)

22

(37) (12)

1,108

2015 Cost initiatives Greece

Remedial Management

Non Core International

Core International

2016

Recurring cost base rationalisation continued in 2016 despite increase in

remedial management costs

9M 2013 Results FY 2013 Results 17 FY 2016 Results 17

NPL formation by segment - Group Group NPL formation

Decreasing NPL balances in Q4 16 across all business segments II

Note: Write-offs in Q4 16 stood at €322mn

Group NPL ratio at 38.1%

Increased restructuring efforts result in NPL decline

Households NPLs maintained in negative territory suggesting the

peak in 2016

134

307

106 108

(83)

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

45 22 21 35

(62)

35

(55) (18) (66) (80)

Busin

ess

M

ort

gages

C

onsum

er

Cre

dit

84%

NPL Cash

Coverage

78%

46%

520

214 275

110 77

(225)

Q3' 15 Q4' 15 Q1' 16 Q2' 16 Q3' 16 Q4' 16

(€ million)

NPL

38.1%

(€ million)

9M 2013 Results FY 2013 Results 18 FY 2016 Results 18

1.3 1.4 1.4 1.4

2.0

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Non Performing Exposures (NPEs) formation-Greece Group NPE formation

Group NPE formation for Q4 16 declines to 97mn QoQ II

NPE formation in Greece down by -77% yoy

Entries of €0.8bn include new formation and redefaults;

Exits of €0.4bn due to curings, repayments and

liquidations

Restructuring efforts increased by 57% year-on-year

NPE Restructuring effort - Greece

387

844

397

61 100 97

Q3 15 Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

(€ million)

NPE

53.7%

(€ billion)

(€ billion)

17.2

9.0 14.7 0.8

(0.4)

15.1

(0.2)

14.9

10.4

3.9

27.6 12.9

NPEs Greece 30/9/16

Provisions Stock

in Greece 30/9/16

Net NPEs 30/9/16

Entries Exits NPEs 31/12/16

(pre-impairment)

Impairment Q4 16

Net NPEs 31/12/16

EBA FNPLs

EBA NPLs

+57%

NPE formation YoY - Greece

2.8

0.6

FY' 15 FY' 16

-77%

(€ billion)

9M 2013 Results FY 2013 Results 19 FY 2016 Results 19

Cost of Risk declines by 11.3% YoY;

Cash Coverage at 69% for NPLs and 49% for NPEs II

69% 70% 69% 68% 69%

50% 50% 49% 49% 49%

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

NPL Cash coverage NPE Cash coverage

124% NPL Total

Coverage 124% 125% 126% 126%

107% NPE Total

Coverage 106% 106% 108% 108%

€1.3bn €1.2bn

256 350 258 304

€1.6bn

FY 15 FY 16 Q1 16 Q2 16 Q3 16 Q4 16

Impairment losses AQR Impact

CoR,

bps

227 165

1Excluding Asset Quality Review (AQR)

169

(11.3%)

2151

191

Group NPL and NPE Coverage Group CoR down by 1/4 yoy

(€ million)

201

20 FY 2016 Results 20

III. FY 16 Performance

1. Balance Sheet

9M 2013 Results FY 2013 Results 21 FY 2016 Results 21

5.7

4.4

0.8

44.9

3.4

5.5

1.5

Sep-16

5.7

4.5

0.8

44.4

2.7

5.3

1.5

Dec-16

4.1

8.9

0.3

18.1

13.8

5.5

15.3

Sep-16

66.2

32.0

ELA

ECB

Time

deposits

Core

deposits

Debt

securities

Equity

Other

Liquidity

3.9

9.1

0.6

18.6

14.4

5.2

13.2

Dec-16

64.9

Net loans

PPE

DTA

Other

EFSF bonds

Securities

Cash

66.2

Balance Sheet composition III

Liabilities and equity split Asset split

P&L Asset Quality Capital Balance Sheet

(€ billion) (€ billion)

Net loans

PPE

DTA

Other

EFSF bonds

Securities

Cash

P&L

32.9

ELA

ECB

Time

deposits

Core

deposits

Debt

securities

Equity

Other

64.9

22 FY 2016 Results 22

III-2. Pre Provision Income

9M 2013 Results FY 2013 Results 23 FY 2016 Results 23

Resilient core PPI; NII supported by reduced cost of funding III

P&L Asset Quality Liquidity Capital Balance Sheet

Negative contribution of loans to NII counterbalanced mainly by wholesale

funding

(€ million)

4.8 4.4 5.8 5.5 5.2

19.6 19.7 16.9 15.3 13.2

24.4 24.1 22.7 20.8

18.3

1.67% 1.59% 1.48% 1.29%

1.21%

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

ECB ELA Funding Cost incl. Pillar II fees

Central Banks funding balances & cost continue to decline

(47) (50) (49) (51) (51)

(110) (91) (85) (71) (60)

551 530 521 517 512

85 87 89 86 89

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Bonds & other

Loans

Funding

Depos

477 479

Core PPI breakdown 1

578 564 570 578 586

(307) (273) (270) (281) (285)

271

291 300 297 302

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Operating Income Operating Expenses PPI

(€ million)

476

1 Excluding VISA gain

(€ billion)

481 490

9M 2013 Results FY 2013 Results 24 FY 2016 Results 24

(€ billion)

End of

quarter

balances

(bps)

18.3 17.5 18.2 18.1 18.6

13.1 13.5 13.5 13.8 14.4

31.4 31.0 31.7 32.0 32.9

(61) (67) (67) (66) (65)

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Core deposits Time deposits

Group deposits spread

Loan and deposit spreads III

929 930 915 907 906

734 726 724 720 716

488 472 476 471 474

432 429 427 427 424

260 262 261 261 261

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Consumer Credit - Greece

Small Business Loans - Greece

SEE

Medium & Large Business - Greece

Mortgages - Greece

Reduced net loan balances with declining spreads

Lending spreads

(bps)

(bps)

P&L Asset Quality Liquidity Capital Balance Sheet

Deposit mix & cost evolution

(14) (25)

(31) (34) (34)

(113) (122)

(108) (103) (97)

(127) (122) (112) (106) (102)

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Sight and Savings - Greece

SE Europe

Time Deposits - Greece

Deposit spreads

(bps)

End of

quarter

balances

46.2 45.8 45.5 44.9 44.4

460 454 451 448 445

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Net Loans Group loans spread

(€ billion)

44%

56%

% Total

9M 2013 Results FY 2013 Results 25 FY 2016 Results 25

Operating expenses III

P&L Asset Quality Liquidity Capital Balance Sheet

€ million FY 16 FY 15 yoy %

Staff costs (501) (519) (3.5%)

General expenses (510) (513) (0.5%)

Depreciation and amortisation

expenses (97) (103) (5.0%)

Recurring OPEX (1,108) (1,134) (2.3%)

Integration costs (6) (9) (33.8%)

Extraordinary/one-off costs (111) (123) (9.9%)

Total OPEX (1,225) (1,267) (3.3%)

132 126 125 124 125

148 122 121 133 135

27

25 23 24 25

307

273 270 281 285

Q4 15 Q1 16 Q2 16 Q3 16 Q4 16

Depreciation & amortisation expenses

General expenses

Staff costs

Recurring OPEX Evolution

(€ million)

1,032 1,024

941 929 897 882

856 820

721

Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

Branches

Bulg

-83 FYROM

-18

o/w Gr 628 627 627 627 626 612 592 565 533

Employees

17,404

15,202 15,149

14,371 14,210 13,856 13,695 13,569 13,481

11,863

Sep-14 Dec-14 Mar-15 Jun-15 Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

Citi

+719

VSS Gr

-2,208 Bulg

-744 FYROM

-240

VSS Cy

-249

o/w Gr 11,781 9,570 9,625 9,680 9,687 9,687 9,679 9,670 9,653 8,888

Serbia

-836

Serbia

-67

26 FY 2016 Results 26

III-3. Asset Quality

9M 2013 Results FY 2013 Results 27 FY 2016 Results 27

Total coverage at 125%

(€ billion)

Coverage of Group non performing loans III

P&L Asset Quality Liquidity Capital Balance Sheet

79% 79% 79% 78% 78%

55% 133%

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Collateral Coverage

Total NPL Coverage

47% 47% 45% 45% 46%

69% 115%

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Collateral Coverage

Total NPL Coverage

80% 80% 80% 81% 82% 84%

29% 113%

Sep-15 Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Collateral Coverage

Total NPL

Coverage

69% 70% 69% 68% 69%

56% 125%

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16 Collateral Coverage

Total NPL Coverage

Evolution of coverage for the Group

Busin

ess

Mort

gages

Consum

er

Cre

dit

Cash coverage for the Group at 69% or 125% including collateral coverage of 56%

Total coverage in all segments is well above the 100% mark

69%

56%

125%

NPL Coverage

Collateral

Cash

51.6

19.6 13.4

8.7

3.4

2.5

60.3

23.0

15.9

Gross Loans NPLs Provisions stock

Abroad

Greece 38.1%

NPL ratio

69%

Cash

coverage

38.0%

39.1%

74%

68%

9M 2013 Results FY 2013 Results 28 FY 2016 Results 28

Non-performing exposures (NPEs) also include non-performing forborne loans IΙI

P&L Asset Quality Liquidity Capital Balance Sheet

44.4 (23.0)

(7.6) (1.7)

15.9

60.3

37.3

27.9

Gross loans IFRS NPLs (90 dpd)

Performing loans

FNPLs <90dpd

Individually impaired¹

Performing exposures

NPE perimeter includes NPLs and performing restructured loans

ECB methodology separates the 90 days past due, IFRS non-

performing loans from non-performing exposures (NPE)

The difference between IFRS NPLs and NPEs comes from two areas:

Forborne non performing loans (FNPLs) that are loans currently

below 90dpd, but under full EBA definitions must be considered

as non performing for at least 12 months after the forbearance

measures have been applied

Loans which are either individually impaired or “unlikely to pay”

and are currently below 90dpd, but under full EBA definitions

are considered as non performing exposures (NPEs)

1

1 2

38% 54%

NPL

Ratio

69% 49%

NPL

Coverage

NPE

Ratio

NPE

Coverage

NPE adjustment

(€ billion)

Net loans

Provisions

2

9.9 9.9 9.8 9.4 9.0

6.8 7.0 7.3 7.7 8.2

16.7 16.9 17.1 17.2 17.2

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

EBA Net FNPL

EBA Net NPLs

(€ billion)

Group Net NPEs evolution

1 Including Unlikely to Pay

9M 2013 Results FY 2013 Results 29 FY 2016 Results 29

Detailed overview of Alpha Bank’s asset quality by portfolio - Group IIΙ

(€ billion) Wholesale SBL Mortgages Consumer Total

Gross loans 26.0 6.6 20.3 7.4 60.3

(-) Provisions (7.1) (2.9) (3.3) (2.6) (15.9)

Net loans 18.9 3.7 17.0 4.8 44.4

NPLs 7.8 5.1 7.1 3.1 23.0

NPL ratio 29.9% 76.4% 34.9% 41.9% 38.1%

NPEs 12.6 5.7 9.5 4.6 32.4

NPE ratio 48.6% 86.3% 46.6% 61.8% 53.7%

NPL collateral 4.5 2.6 4.9 0.9 12.8

NPE collateral 7.5 3.0 6.7 1.1 18.3

Coverage ratio

NPLs 7.8 5.1 7.1 3.1 23.0

(+) Forborne NPLs < 90 dpds 3.2 0.6 2.3 1.5 7.6

(+) Individually impaired1 1.6 0.0 0.1 0.0 1.7

NPEs 12.6 5.7 9.5 4.6 32.4

Forborne NPLs >90dpd 1.2 1.1 1.8 1.4 5.6

Forborne NPLs <90dpd 3.2 0.6 2.3 1.5 7.6

Performing forborne 0.6 0.3 3.5 0.7 5.1

Total forborne 5.0 2.1 7.6 3.6 18.3

92% 57% 57% 50% 46% 35%

84% 57% 69%

49%

58%

59% 51% 52% 69% 71%

29%

24%

56% 56%

149%

116% 107% 103% 115%

105% 113%

81%

125% 106%

NPL NPE NPL NPE NPL NPE NPL NPE NPL NPE

Total

Collateral

Cash

1 Including unlikely to pay

P&L Asset Quality Liquidity Capital Balance Sheet

9M 2013 Results FY 2013 Results 30 FY 2016 Results 30

Loans perimeter managed by NPL Units

NPL Workout Units Analysis III

19.6

0.4

13.7

5.5

32.0 23.9

5.0

3.1

51.6 24.3

18.8

8.6

Total Loans Greece

Non-NPL Management

Units

Retail NPL Management

Unit

WHL NPL Management

Unit

Performing

NPLs

(€ billion)

P&L Asset Quality Liquidity Capital Balance Sheet

NPL Workout Units balances breakdown by segment

5.8 2.9

5.0 4.3 1.2

19.2

3.4

1.0

0.7 1.5

1.6

8.1

9.2

3.9 5.7 5.8

2.8

27.3

Mortgages Consumer SBLs SMEs Corporates Total

Performing

NPLs

Retail

€18.8bn

Wholesale

€8.6bn

1 Including leasing, factoring and International Unit Greece

(€ billion)

Retail NPL Unit manages all retail exposures which are >1dpd and total €18.8bn

In retail c. 3,000 FTEs broken down in

c.600 in Retail NPL Unit

c.480 in branches

c.1,900 in collection and legal firms

WHL NPL Unit manages €8.6bn, out of which €3.1bn are performing loans1

In wholesale c.143 FTEs broken down in (legal outsourcing excluded):

Management & Monitoring: 28 FTEs

Workout: 47 FTEs

Permanent arrears: 68 FTEs

9M 2013 Results FY 2013 Results 31 FY 2016 Results 31

CEPAL - The 1st independent licensed NPL servicer goes live in Greece III

CEPAL was the 1st company to be licensed as a Servicer in Greece.

CEPAL is a partnership between Centerbridge Partners (CP), which has strong track

record in setting up such ventures, and will be the majority shareholder, and Alpha

Bank, which will maintain a minority stake

Strong management team with international experience

The two parties committed significant resources to ramp up the operations of the

Servicer and create independent infrastructure (in terms of Human Resources, IT

infrastructure, processes, etc.)

The platform will service both secured and unsecured retail NPL portfolios

CEPAL is expected to play a significant role in the development of the secondary

market for NPLs as it has been set up as an independent open platform with the aim

to target various clients in the Greek market

The Servicer is part of the bank’s operational plan for NPEs submitted to SSM in

2016. Through the Servicer the Bank aims to:

Alpha Bank to initially assign €4bn to CEPAL, whereas the intention is to increase the

assigned volumes, subject to the Servicer’s performance

Key performance indicators will monitor the performance of the Servicer

The servicer

Introduce international best practices and systems to the Greek NPL servicing market

Consolidate and integrate NPL management & servicing of the bank’s own retail portfolio.

Create a separate specialized business unit to allow for optimized efficiency and performance through scale, human capital investment, talent retention and incentive based compensation structures

Leverage technologies successfully implemented in other markets

Pursue mainly amicable long term NPL solutions with clients, including innovative for the Greek market Real Estate solutions

P&L Asset Quality Liquidity Capital Balance Sheet

32 FY 2016 Results 32

III-4. Liquidity

9M 2013 Results FY 2013 Results 33 FY 2016 Results 33

Eurosystem funding reduced further in Q4 by 2.5bn by deposit inflows, sales of EFSF

bond and a securitisation transaction III

3.2 2.5 2.2

0.5 0.7 0.7

1.9 1.9 1.9

5.0

2.0 2.0 2.0

14.6 14.1 14.0

1.7

0.7 0.5

Sep-16 Dec-16 Feb-17

Pillar II

Securitisations

Bonds

Loans

EFSF Bonds

23.9

22.0

ELA

16.5

ECB

4.8

ECB

5.6

ECB

5.2

ELA

16.8

21.3

ELA

18.3

Eurosystem collateral pool (cash values)

(€ billion)

5.5 5.2 4.8

(1.2) (1.0) (0.3) (0.3)

0.3

15.3

13.2 13.0

20.8

18.3 17.8

Sep-16 Deposits Inflows

Securities Disposal

Secutitisation SME

Other B/S items

Interbank Repo

Dec-16 Feb-17

ECB ELA

Cash

Buffer 3.0 3.6 3.5

o/w 2.2

EFSF

bonds

Eurosystem funding QoQ reduction

(€ billion)

-€2.5bn

Including

proceeds of

Hilton sale

€143mn

P&L Asset Quality Liquidity Capital Balance Sheet

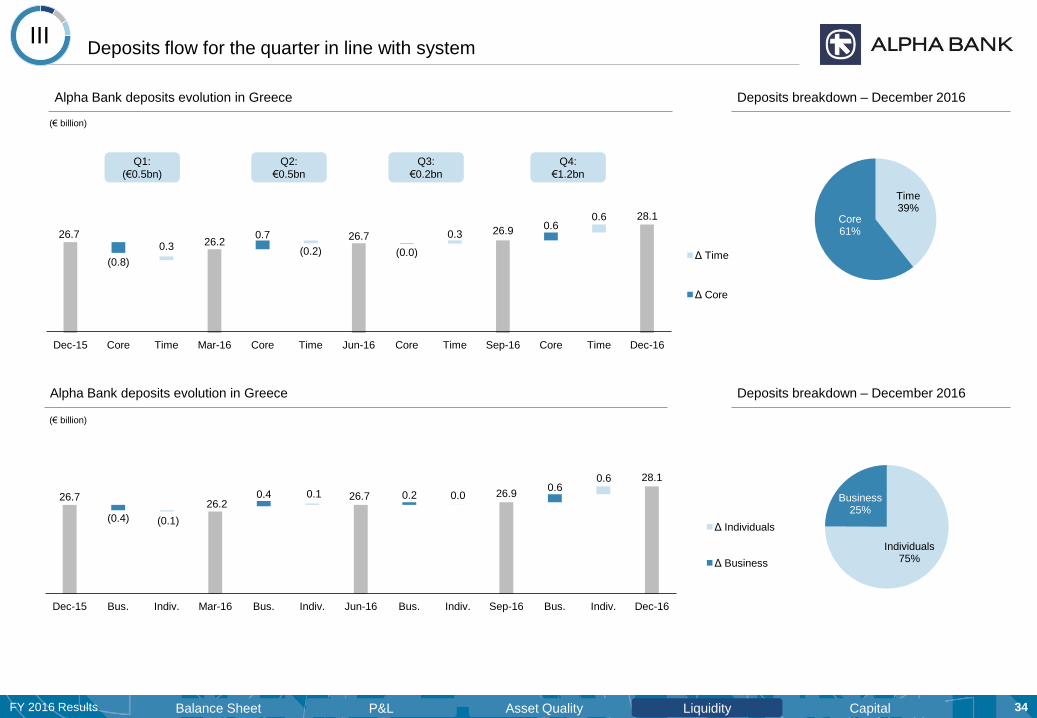

9M 2013 Results FY 2013 Results 34 FY 2016 Results 34

Individuals 75%

Business 25%

26.7 26.2

26.7 26.9

28.1

(0.8)

0.7

(0.0)

0.6

0.3 (0.2)

0.3

0.6

Dec-15 Core Time Mar-16 Core Time Jun-16 Core Time Sep-16 Core Time Dec-16

Δ Time

Δ Core

Alpha Bank deposits evolution in Greece

Deposits flow for the quarter in line with system III

26.7 26.2

26.7 26.9

28.1

(0.4)

0.4 0.2 0.6

(0.1)

0.1 0.0

0.6

Dec-15 Bus. Indiv. Mar-16 Bus. Indiv. Jun-16 Bus. Indiv. Sep-16 Bus. Indiv. Dec-16

Δ Individuals

Δ Business

Q1:

(€0.5bn)

Q2:

€0.5bn

P&L Asset Quality Liquidity Capital Balance Sheet

Deposits breakdown – December 2016

Q3:

€0.2bn

Alpha Bank deposits evolution in Greece

Deposits breakdown – December 2016

Time 39%

Core 61%

(€ billion)

(€ billion)

Q4:

€1.2bn

35 FY 2016 Results 35

III-5. Capital

9M 2013 Results FY 2013 Results 36 FY 2016 Results 36

45.8 45.6

(0.3) (0.1)

0.1

3.9 4.0

1.1 1.0

50.8 50.5

Sep-16 Credit Risk Market Risk Operational Risk

Dec-16

Market Risk

Operational Risk

Credit Risk

III

P&L Asset Quality Liquidity Capital Balance Sheet

Common Equity Tier I Ratio of 17.1%; Fully Loaded ratio at 16.7%

9,077 8,706 8,631 8,662

(371) (76)

31

Ordinary Equity

Intangibles Tangible book value

Regulatory Adjustments

CET1 capital =

Tier I capital

Lower Tier II

Total Regulatory

Capital

Equity to regulatory capital bridge

(€ million)

Dec-16 DTA/Tax Credit impact Phased-in Fully loaded

CET1 (€bn) 4.2 4.0

RWAs1 (€bn) 5.1 5.1

€3.4bn Tax Credit

€0.7bn Other DTA

€3.4bn Tax Credit

€0.2bn Tax Losses

€0.7bn Other DTA

€1.7bn DTA

€3.4bn Tax Credit

16.8% 6 bps 11bps 5 bps 17.1% 16.7%

CET 1 Sep-16

Period Result

AFS Reserve

RWA impact / Other

CET 1 Dec-16

Fully loaded CET1 Dec-16

CET1 ratio build up impacted by decrease of Credit RWAs and a profitable quarter

CET1

capital 8,560 8,631 8,460

(€ million)

1 Risk weighting is100% for the Tax Credit and 250% for the Other DTA

RWAs/ Assets

(€ billion)

Group Risk Weighted Assets (RWAs) development

78% 13.5% Tangible book value/

Tangible Assets

37 FY 2016 Results 37

IV. Appendix

9M 2013 Results FY 2013 Results 38 FY 2016 Results 38

Business Volumes IV

(€ million) Dec 2016 Sep 2016 Jun 2016 Mar 2016 Dec 2015

%

Dec 2016 /

Dec 2015

Group Gross Loans 60,316 60,821 61,418 61,895 62,015 (2.7%)

Mortgages 20,260 20,480 20,541 20,794 20,840 (2.8%)

Consumer Loans 5,749 5,876 5,858 5,848 5,872 (2.1%)

Credit Cards 1 1,676 1,637 1,593 1,409 1,425 17.6%

Small Business Loans 6,640 6,781 6,788 6,792 6,726 (1.3%)

Medium and Large Business Loans 1 25,991 26,047 26,637 27,052 27,151 (4.3%)

of which:

Greece 51,606 51,440 51,975 52,261 52,472 (1.7%)

Mortgages 16,714 16,769 16,834 17,102 17,150 (2.5%)

Consumer Loans 5,225 5,205 5,197 5,161 5,184 0.8%

Credit Cards 1 1,638 1,587 1,543 1,359 1,373 19.3%

Small Business Loans 6,573 6,710 6,712 6,715 6,656 (1.2%)

Medium and Large Business Loans1 21,456 21,169 21,689 21,924 22,109 (3.0%)

of which: Shipping Loans 2,004 1,914 1,938 1,858 1,910 4.9%

Southeastern Europe 8,448 9,082 9,123 9,238 9,164 (7.8%)

Accumulated Provisions (15,907) (15,951) (15,922) (16,069) (15,829) 0.5%

Group Net Loans 44,409 44,870 45,496 45,826 46,186 (3.8%)

Customer Assets 38,342 37,498 37,254 36,643 37,097 3.4%

of which:

Group Deposits 32,946 31,970 31,667 30,963 31,434 4.8%

Sight & Savings 18,572 18,148 18,155 17,456 18,313 1.4%

Time deposits & Alpha Bank Bonds 14,375 13,821 13,512 13,507 13,122 9.5%

Greece 28,062 26,877 26,659 26,204 26,744 4.9%

Sight & Savings 17,021 16,444 16,483 15,823 16,640 2.3%

Time deposits & Alpha Bank Bonds 11,041 10,433 10,177 10,381 10,103 9.3%

Southeastern Europe 4,111 4,294 4,213 3,956 3,866 6.3%

Money Market Mutual Funds 593 664 739 774 800 (25.9%)

Other Mutual Funds 1,286 1,224 1,225 1,221 1,176 9.3%

Private Banking 3,518 3,641 3,623 3,685 3,686 (4.6%)

1 Reclassification of €193mn in Q2 16 from Medium & Large Business Loans to Credit Cards

9M 2013 Results FY 2013 Results 39 FY 2016 Results 39

Passenger 9%

Containers 9%

Product Tankers 13%

Panamax 8%

Suezmax 8% VLCC 8%

Handy max/ Handy size

20%

Panamax 16%

Capesize 9%

Tankers

37%

Dry Bulk

45%

Wholesale loans portfolio structure – Group

Shipping loans portfolio structure

€2.0bn

Diversified business book and shipping portfolio IV

€2.0bn of exposure, to top-names

The portfolio is split into tankers by 37%, containers 9%,

passenger 9% and the rest is dry bulk

Duration of loan portfolio at 5 years

NPL ratio at 9%

Wholesale loans 43%

SBLs 11%

Consumer loans 9%

Credit Cards 3%

Mortgages 34%

Group loans breakdown (FY 16 data)

€60.3bn

Industry 23%

Trade 21%

Construction 17%

Transportation 3%

Tourism 7%

Shipping 6%

Real Estate 7%

Services 6%

Other 10%

€26.0bn

9M 2013 Results FY 2013 Results 40 FY 2016 Results 40

(€ million)

Alpha Private Bank balance increased with Citi acquisition Asset Management impacted by the adverse operating environment

(€ million)

Wealth Management evolution IV

447

158 208

938

916 927

253

157

230

1,638

1,231

1,365

Dec-14 Dec-15 Dec-16

Other AUM Non Money Market Mututal Funds Money Market Mutual Funds

103 98 169

1,296

1,789

2,601

2,085

2,219

1,582 3,484

4,107

4,352

Dec-14 Dec-15 Dec-16

Discretionary Advisory Execution Only

9M 2013 Results FY 2013 Results 41 FY 2016 Results 41

SEE Operations 1 IV

(€ million) Cyprus Δ% Romania Δ% Albania Δ% TOTAL Δ%

Dec-16 yoy yoy yoy yoy

Deposits 1,944 15.4% 1,729 25.0% 438 8.3% 4,111 6.3%

Gross Loans 5,309 0.4% 2,771 (0.8%) 368 0.1% 8,448 (7.8%)

Mortgages 2,472 0.1% 994 4.0% 69 3.2% 3,534 (3.8%)

Consumer Credit 264 (5.6%) 243 (9.7%) 25 22.7% 533 (21.8%)

Businesses 2,573 1.4% 1,534 (2.1%) 274 (2.3%) 4,381 (8.9%)

NPL ratio 55.6% 14.0% 15.8%

NPL Cash coverage 70% 100% 59%

NPL Total coverage 118% 160% 143%

Total Operating Income 160.9 6.9% 140.8 15.6% 20.2 (6.6%) 321.9 9.5%

Operating Expenses

(pre-O/H allocation)1 (52.5) (6.3%) (93.4) (0.5%) (15.0) 4.4% (161.0) (3.6%)

Impairment Losses (225.3) (15.7%) (34.3) (25.4%) (14.2) (84.1%) (273.8) (14.7%)

Profit Before Tax

(pre- O/H allocation) 2 (116.9) … 13.1 … (9.1) … (112.8) (41.9%)

Branches 22 130 35 187

Employees 656 1,832 415 2,903

1 Country View 2 Excluding VSS Cyprus of €31mn

9M 2013 Results FY 2013 Results 42 FY 2016 Results 42

Alpha Bank Group IV

(€ million) FY 2016 FY 2015 yoy % change

Net interest income 1,924.1 1,897.5 1.4%

Net fee and commission income 317.9 308.6 3.0%

Income from financial operations 84.9 (46.9) …

Other Income 56.8 51.8 9.7%

Operating Income 2,383.7 2,211.0 7.8%

Staff costs (500.9) (519.1) (3.5%)

General expenses (510.0) (512.8) (0.5%)

Depreciation and amortization expenses (97.4) (102.6) (5.0%)

Recurring Operating expenses (1,108.3) (1,134.4) (2.3%)

Integration costs (6.0) (9.1) (33.8%)

Extraordinary costs1 (111.2) (123.4) (9.9%)

Total Operating expenses (1,225.5) (1,266.9) (3.3%)

Impairment losses (1,168.0) (2,987.6) (60.9%)

Profit / (Loss) before income tax (9.7) (2,043.5) (99.5%)

Income Tax 29.2 806.8 …

Profit/ (Loss) after income tax 19.5 (1,236.7) …

Profit / (Loss) after income tax from continuing operations 19.5 (1,236.7) …

Profit / (Loss) after income tax from discontinued operations 22.8 (134.8) …

Profit / (Loss) attributable to shareholders 42.1 (1,371.7) …

Net interest Margin (NIM) 2.9% 2.7%

1 Including VSS Cyprus of €31mn in H1 16

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 43 FY 2016 Results 43

Alpha Bank Group IV

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Net interest income 490.1 481.2 476.8 476.0 479.4 480.2 472.6 465.3

Net fee and commission income 81.2 81.1 78.5 77.1 82.0 68.2 76.1 82.3

Income from financial operations 16.0 9.1 56.8 3.0 (90.4) 8.6 9.5 25.3

Other Income 14.9 15.9 14.8 11.2 16.2 9.3 15.3 11.0

Operating Income 602.2 587.3 626.9 567.3 487.3 566.3 573.6 583.9

Staff costs (125.1) (124.1) (125.5) (126.2) (132.0) (129.1) (127.5) (130.5)

General expenses (134.9) (132.8) (121.3) (121.1) (148.1) (126.4) (123.3) (115.0)

Depreciation and amortization expenses (24.7) (24.3) (23.1) (25.3) (26.5) (25.8) (25.3) (25.0)

Recurring Operating expenses (284.6) (281.2) (269.8) (272.7) (306.6) (281.3) (276.1) (270.4)

Integration costs (3.9) (0.4) (1.2) (0.5) (2.7) (3.3) (2.0) (1.1)

Extraordinary costs1 (66.9) 0.2 (16.6) (27.9) (110.3) (24.1) 8.8 2.3

Total Operating expenses (355.5) (281.4) (287.6) (301.0) (419.6) (308.7) (269.3) (269.3)

Impairment losses (303.9) (258.2) (350.0) (255.9) (633.3) (257.7) (1,672.4) (424.1)

Profit / (Loss) before income tax (57.1) 47.8 (10.8) 10.4 (565.7) (0.2) (1,368.2) (109.5)

Income Tax 61.8 (8.1) (9.5) (14.9) 83.6 413.8 318.6 (9.2)

Profit/ (Loss) after income tax 4.7 39.7 (20.3) (4.5) (482.0) 413.6 (1,049.5) (118.7)

Profit / (Loss) after income tax from continuing operations 4.7 39.7 (20.3) (4.5) (482.0) 413.6 (1,049.5) (118.7)

Profit / (Loss) after income tax from discontinued operations 15.4 1.5 3.5 2.3 (51.0) 0.1 (86.7) 2.9

Profit / (Loss) attributable to shareholders 20.1 41.1 (16.8) (2.2) (533.1) 413.6 (1,136.3) (116.0)

Net interest Margin (NIM) 3.0% 2.9% 2.8% 2.8% 2.8% 2.7% 2.6% 2.6%

1 Including VSS Cyprus of €31mn in H1 16

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 44 FY 2016 Results 44

Group Results by Business Unit IV

(€ million)

Retail Commercial &

Corporate SE Europe

Investment Banking &

Treasury

Asset

Management Other Group

Jan-Dec Jan-Dec Jan-Dec Jan-Dec Jan-Dec Jan-Dec Jan-Dec

2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015 2016 2015

Operating Income 1,119.8 1,137.1 833.7 874.8 321.9 293.9 36.4 (68.3) 48.7 60.8 23.2 (87.2) 2,383.7 2,211.0

Net Interest Income 1,001.7 1,027.2 684.8 728.4 257.8 272.1 (38.3) (147.2) 14.7 16.4 3.4 0.6 1,924.1 1,897.5

Net fee and Commission Income 111.3 106.8 136.3 134.0 25.0 26.2 8.3 (3.2) 35.6 43.5 1.5 1.4 317.9 308.6

Income from Financial Operations 6.9 6.6 4.7 4.8 29.6 (10.3) 64.2 76.2 1.4 3.0 (21.9) (127.2) 84.9 (46.9)

Other Income 0.0 (3.5) 7.9 7.5 9.5 5.9 2.3 5.9 (2.9) (2.0) 40.1 38.1 56.8 51.8

Operating Expenses (664.3) (669.7) (153.5) (148.3) (213.9) (182.1) (29.7) (31.4) (26.7) (30.4) (137.4) (205.0) (1,225.5) (1,266.9)

Staff Costs (279.8) (293.3) (87.2) (85.1) (116.3) (88.4) (13.0) (13.9) (16.5) (17.8) (26.6) (85.4) (539.5) (583.9)

General Expenses (331.1) (321.9) (46.1) (43.9) (87.2) (84.5) (14.6) (15.4) (8.6) (10.5) (101.0) (104.2) (588.5) (580.4)

Depreciation (53.4) (54.5) (20.2) (19.3) (10.3) (9.1) (2.1) (2.2) (1.6) (2.1) (9.8) (15.4) (97.4) (102.6)

Impairment Losses (352.2) (1,328.4) (536.4) (1,334.6) (273.8) (321.0) 0.0 (2.6) 0.0 0.0 (5.6) (1.2) (1,168.0) (2,987.6)

Profit / (Loss) before tax 103.3 (861.0) 143.8 (608.1) (165.8) (209.2) 6.7 (102.3) 22.0 30.4 (119.8) (293.4) (9.7) (2,043.5)

1 Including VSS Cyprus of €31mn in H1 16

Note: P&L numbers restated for the sale of Serbia

1

1

9M 2013 Results FY 2013 Results 45 FY 2016 Results 45

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Operating Income 276.7 279.7 280.2 283.2 294.9 298.3 286.9 257.0

Net Interest Income 247.0 248.7 250.5 255.5 266.9 273.6 256.6 230.1

Net fee and Commission Income 27.8 29.3 27.9 26.3 28.4 23.9 29.0 25.5

Income from Financial Operations 1.9 1.7 1.8 1.5 1.2 1.8 1.7 1.9

Other Income - - - - (1.7) (1.0) (0.3) (0.5)

Operating Expenses (170.8) (167.3) (166.3) (159.9) (175.2) (171.2) (163.2) (160.0)

Staff Costs (70.1) (69.6) (70.6) (69.5) (74.5) (71.3) (72.0) (75.6)

General Expenses (87.2) (84.4) (82.5) (77.0) (86.4) (86.0) (77.9) (71.6)

Depreciation (13.5) (13.4) (13.1) (13.4) (14.3) (14.0) (13.3) (12.8)

Impairment losses (21.5) (164.7) (96.7) (69.3) (68.9) (192.0) (923.5) (144.0)

Profit / (Loss) before tax 84.3 (52.3) 17.2 54.1 50.8 (65.0) (799.8) (47.0)

RWA e 20,108 20,074 19,882 20,104 20,434 20,325 20,415 20,295

Results I Retail Business Unit IV

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 46 FY 2016 Results 46

Results I Commercial & Corporate Business Unit IV

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Operating Income 205.2 206.7 208.9 212.9 222.5 224.4 218.6 209.3

Net Interest Income 166.6 169.2 172.5 176.6 183.8 189.0 182.4 173.2

Net fee and Commission Income 35.3 34.0 33.3 33.7 35.7 33.0 31.8 33.5

Income from Financial Operations 1.4 1.2 1.3 0.9 0.6 0.6 2.6 1.1

Other Income 2.0 2.3 1.9 1.7 2.4 1.7 1.9 1.5

Operating Expenses (39.7) (38.5) (37.9) (37.4) (39.5) (38.0) (35.9) (34.9)

Staff Costs (22.1) (21.8) (21.9) (21.4) (22.8) (21.3) (20.6) (20.5)

General Expenses (12.4) (11.6) (11.1) (11.0) (11.6) (11.8) (10.6) (10.0)

Depreciation (5.3) (5.0) (4.9) (4.9) (5.1) (4.9) (4.7) (4.5)

Impairment losses (124.8) (54.5) (204.4) (152.8) (420.2) (17.3) (666.3) (230.8)

Profit / (Loss) before tax 40.7 113.8 (33.4) 22.7 (237.2) 169.1 (483.6) (56.4)

RWA e 18,063 18,199 18,459 18,345 17,970 17,980 18,649 18,896

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 47 FY 2016 Results 47

Results I Asset Management Business Unit IV

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Operating Income 13.3 11.9 11.8 11.7 14.6 10.6 16.5 19.2

Net Interest Income 3.8 3.3 3.6 4.0 4.1 4.1 4.1 4.0

Net fee and Commission Income 9.6 9.4 8.5 8.1 8.8 7.2 12.1 15.3

Income from Financial Operations 1.0 0.1 0.1 0.2 2.4 (0.1) 0.5 0.2

Other Income (1.1) (0.9) (0.4) (0.5) (0.8) (0.7) (0.3) (0.3)

Operating Expenses (6.8) (6.6) (6.7) (6.6) (7.1) (7.0) (7.6) (8.7)

Staff Costs (4.0) (4.1) (4.2) (4.3) (4.9) (4.5) (4.1) (4.3)

General Expenses (2.5) (2.1) (2.1) (1.9) (1.6) (2.0) (3.0) (4.0)

Depreciation (0.4) (0.4) (0.4) (0.4) (0.6) (0.5) (0.5) (0.5)

Impairment losses - - - - - - - -

Profit / (Loss) before tax 6.6 5.3 5.1 5.1 7.5 3.6 8.8 10.5

RWA e 293 308 315 326 349 363 362 323

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 48 FY 2016 Results 48

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Operating Income 55.8 (2.0) 13.6 (30.9) (12.0) (47.9) (19.5) 11.0

Net Interest Income 8.3 (6.1) (16.8) (23.7) (44.3) (54.5) (38.6) (9.7)

Net fee and Commission Income 2.1 1.6 2.3 2.2 1.9 (2.7) (3.4) 0.9

Income from Financial Operations 43.5 0.2 26.3 (5.7) 27.2 9.5 19.9 19.6

Other Income 2.0 2.3 1.8 (3.8) 3.2 (0.3) 2.7 0.3

Operating Expenses (7.8) (7.4) (7.3) (7.2) (8.9) (7.8) (7.9) (6.8)

Staff Costs (3.4) (3.2) (3.3) (3.1) (3.9) (3.3) (3.4) (3.3)

General Expenses (3.9) (3.7) (3.5) (3.5) (4.4) (4.0) (3.7) (3.3)

Depreciation (0.5) (0.5) (0.5) (0.5) (0.6) (0.5) (0.8) (0.3)

Impairment losses - - - - (2.6) - - -

Profit / (Loss) before tax 48.0 (9.5) 6.3 (38.1) (23.4) (55.7) (27.4) 4.2

RWA e 4,891 4,993 5,198 5,350 5,215 5,142 5,197 4,738

Results I Investment Banking & Treasury Business Unit IV

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 49 FY 2016 Results 49

Results I SE Europe Business Unit IV

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Operating Income 73.3 80.5 91.6 76.5 75.3 84.3 76.7 57.5

Net Interest Income 63.6 65.1 65.9 63.2 69.0 67.6 67.9 67.6

Net fee and Commission Income 5.8 6.6 6.4 6.3 6.5 6.6 6.2 6.9

Income from Financial Operations 0.1 6.1 18.2 5.2 (2.8) 9.0 1.2 (17.8)

Other Income 3.8 2.8 1.2 1.8 2.6 1.1 1.4 0.8

Operating Expenses1 (49.2) (42.4) (44.8) (77.5) (51.6) (44.7) (42.3) (43.5)

Staff Costs1 (19.9) (19.4) (21.0) (56.0) (24.3) (21.5) (20.9) (21.8)

General Expenses (26.5) (20.6) (21.2) (18.9) (24.9) (20.9) (19.3) (19.4)

Depreciation (2.7) (2.5) (2.6) (2.6) (2.4) (2.2) (2.2) (2.3)

Impairment losses (152.0) (39.0) (49.0) (33.8) (140.5) (48.5) (82.6) (49.3)

Profit / (Loss) before tax1 (127.9) (0.9) (2.2) (34.7) (116.7) (8.9) (48.2) (35.3)

RWA e 6,223 6,345 6,652 6,888 7,356 7,826 8,116 8,403

1 Including VSS Cyprus of €31mn in H1 16

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 50 FY 2016 Results 50

Results I Other Business Unit IV

(€ million) Q4 2016 Q3 2016 Q2 2016 Q1 2016 Q4 2015 Q3 2015 Q2 2015 Q1 2015

Operating Income (22.2) 10.5 20.8 13.9 (108.0) (3.3) (5.7) 29.8

Net Interest Income 0.9 0.9 1.2 0.4 (0.2) 0.4 0.2 0.1

Net fee and Commission Income 0.6 0.2 0.1 0.6 0.7 0.1 0.3 0.2

Income from Financial Operations (31.9) (0.1) 9.2 0.9 (119.0) (12.2) (16.3) 20.3

Other Income 8.2 9.5 10.4 12.0 10.5 8.4 10.1 9.2

Operating Expenses (81.1) (19.1) (24.6) (12.6) (137.4) (40.0) (12.4) (15.2)

Staff Costs (10.2) (7.7) (5.5) (3.2) (68.7) (6.6) (5.1) (5.0)

General Expenses (68.7) (8.9) (17.6) (5.9) (65.2) (29.9) (3.5) (5.6)

Depreciation (2.3) (2.5) (1.5) (3.5) (3.5) (3.5) (3.8) (4.5)

Impairment losses (5.6) (0.0) 0.0 (0.0) (1.2) (0.0) (0.0) (0.0)

Profit / (Loss) before tax (108.9) (8.6) (3.7) 1.4 (246.6) (43.3) (18.1) 14.6

RWA e 1,109 1,149 1,126 1,119 1,149 1,146 1,087 1,008

Note: P&L numbers restated for the sale of Serbia

9M 2013 Results FY 2013 Results 51 FY 2016 Results 51

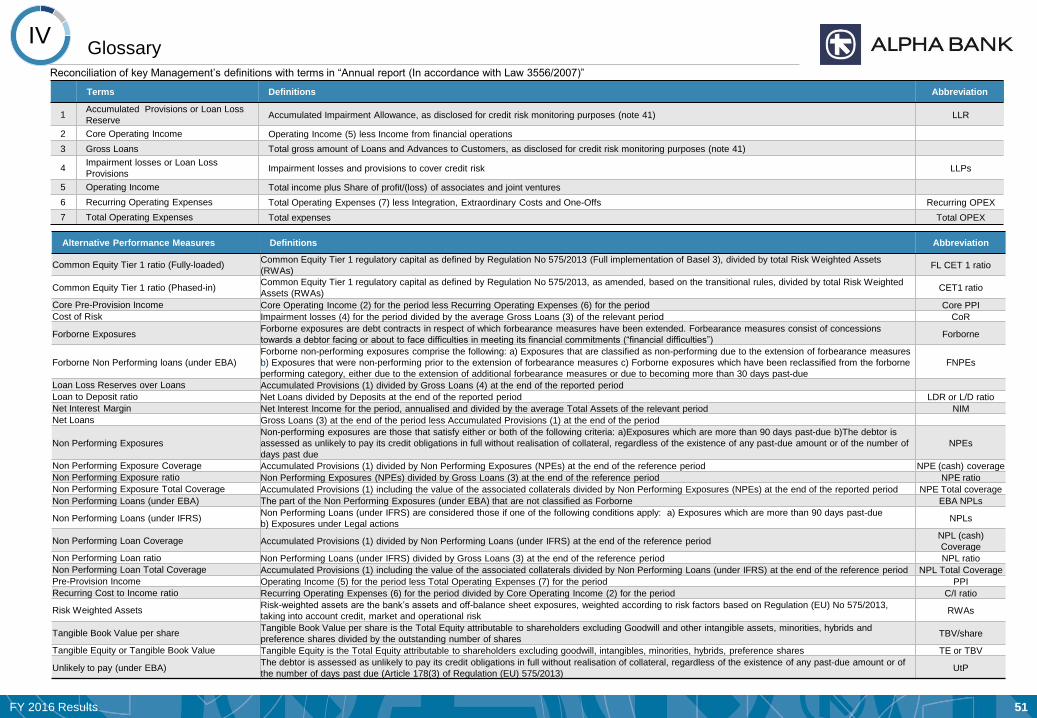

Terms Definitions Abbreviation

1 Accumulated Provisions or Loan Loss

Reserve Accumulated Impairment Allowance, as disclosed for credit risk monitoring purposes (note 41) LLR

2 Core Operating Income Operating Income (5) less Income from financial operations

3 Gross Loans Total gross amount of Loans and Advances to Customers, as disclosed for credit risk monitoring purposes (note 41)

4 Impairment losses or Loan Loss

Provisions Impairment losses and provisions to cover credit risk LLPs

5 Operating Income Total income plus Share of profit/(loss) of associates and joint ventures

6 Recurring Operating Expenses Total Operating Expenses (7) less Integration, Extraordinary Costs and One-Offs Recurring OPEX

7 Total Operating Expenses Total expenses Total OPEX

Glossary IV

Reconciliation of key Management’s definitions with terms in “Annual report (In accordance with Law 3556/2007)”

Alternative Performance Measures Definitions Abbreviation

Common Equity Tier 1 ratio (Fully-loaded) Common Equity Tier 1 regulatory capital as defined by Regulation No 575/2013 (Full implementation of Basel 3), divided by total Risk Weighted Assets

(RWAs) FL CET 1 ratio

Common Equity Tier 1 ratio (Phased-in) Common Equity Tier 1 regulatory capital as defined by Regulation No 575/2013, as amended, based on the transitional rules, divided by total Risk Weighted

Assets (RWAs) CET1 ratio

Core Pre-Provision Income Core Operating Income (2) for the period less Recurring Operating Expenses (6) for the period Core PPI

Cost of Risk Impairment losses (4) for the period divided by the average Gross Loans (3) of the relevant period CoR

Forborne Exposures Forborne exposures are debt contracts in respect of which forbearance measures have been extended. Forbearance measures consist of concessions

towards a debtor facing or about to face difficulties in meeting its financial commitments (“financial difficulties”) Forborne

Forborne Non Performing loans (under EBA)

Forborne non-performing exposures comprise the following: a) Exposures that are classified as non-performing due to the extension of forbearance measures

b) Exposures that were non-performing prior to the extension of forbearance measures c) Forborne exposures which have been reclassified from the forborne

performing category, either due to the extension of additional forbearance measures or due to becoming more than 30 days past-due

FNPEs

Loan Loss Reserves over Loans Accumulated Provisions (1) divided by Gross Loans (4) at the end of the reported period

Loan to Deposit ratio Net Loans divided by Deposits at the end of the reported period LDR or L/D ratio

Net Interest Margin Net Interest Income for the period, annualised and divided by the average Total Assets of the relevant period NIM

Net Loans Gross Loans (3) at the end of the period less Accumulated Provisions (1) at the end of the period

Non Performing Exposures

Non-performing exposures are those that satisfy either or both of the following criteria: a)Exposures which are more than 90 days past-due b)The debtor is

assessed as unlikely to pay its credit obligations in full without realisation of collateral, regardless of the existence of any past-due amount or of the number of

days past due

NPEs

Non Performing Exposure Coverage Accumulated Provisions (1) divided by Non Performing Exposures (NPEs) at the end of the reference period NPE (cash) coverage

Non Performing Exposure ratio Non Performing Exposures (NPEs) divided by Gross Loans (3) at the end of the reference period NPE ratio

Non Performing Exposure Total Coverage Accumulated Provisions (1) including the value of the associated collaterals divided by Non Performing Exposures (NPEs) at the end of the reported period NPE Total coverage

Non Performing Loans (under EBA) Τhe part of the Non Performing Exposures (under EBA) that are not classified as Forborne EBA NPLs

Non Performing Loans (under IFRS) Non Performing Loans (under IFRS) are considered those if one of the following conditions apply: a) Exposures which are more than 90 days past-due

b) Exposures under Legal actions NPLs

Non Performing Loan Coverage Accumulated Provisions (1) divided by Non Performing Loans (under IFRS) at the end of the reference period NPL (cash)

Coverage

Non Performing Loan ratio Non Performing Loans (under IFRS) divided by Gross Loans (3) at the end of the reference period NPL ratio

Non Performing Loan Total Coverage Accumulated Provisions (1) including the value of the associated collaterals divided by Non Performing Loans (under IFRS) at the end of the reference period NPL Total Coverage

Pre-Provision Income Operating Income (5) for the period less Total Operating Expenses (7) for the period PPI

Recurring Cost to Income ratio Recurring Operating Expenses (6) for the period divided by Core Operating Income (2) for the period C/I ratio

Risk Weighted Assets Risk-weighted assets are the bank’s assets and off-balance sheet exposures, weighted according to risk factors based on Regulation (EU) No 575/2013,

taking into account credit, market and operational risk RWAs

Tangible Book Value per share Tangible Book Value per share is the Total Equity attributable to shareholders excluding Goodwill and other intangible assets, minorities, hybrids and

preference shares divided by the outstanding number of shares TBV/share

Tangible Equity or Tangible Book Value Tangible Equity is the Total Equity attributable to shareholders excluding goodwill, intangibles, minorities, hybrids, preference shares TE or TBV

Unlikely to pay (under EBA) The debtor is assessed as unlikely to pay its credit obligations in full without realisation of collateral, regardless of the existence of any past-due amount or of

the number of days past due (Article 178(3) of Regulation (EU) 575/2013) UtP

9M 2013 Results FY 2013 Results 52 FY 2016 Results 52

ALPHA BANK

40, Stadiou Street, 102 52

Athens, Greece

Internet : www.alpha.gr

Reuters : ACBr.AT (shares), GRALFAw.AT (warrants)

Bloomberg : ALPHA GA (shares), ALPHAW GA (warrants)

Vassilios Psaltis Lazaros Papagaryfallou

General Manager – CFO Executive General Manager

[email protected] [email protected]

+30 210 326 2181 +30 210 326 4017

Dimitrios Kostopoulos Elena Katopodi

Manager Assistant Manager

Investor Relations Division Investor Relations Division

[email protected] [email protected]

+30 210 326 4082 +30 210 326 4184

Stella Traka Marios-Ioannis Deportou

Senior Investor Relations Officer Senior Investor Relations Officer

[email protected] [email protected]

+30 210 326 4182 +30 210 326 4199

E-mail : [email protected]

Tel : +30 210 326 4082

+30 210 326 4010

+30 210 326 4185

Alpha Bank Contacts