futures trading involves substantial risk of loss and is ... · guy bower’s guide to futures and...

TRANSCRIPT

Guy Bower’s Guide to Futures 2 egaP gnidarT daerpS dna

Web Resources Daniels Trading offer comprehensive, reliable and customer-focused commodity futures brokerage services to address all trading preferences. Their website is also a great place for educational resources on anything relating to futures trading.

Check it out at: www.danielstrading.com

Acknowledgements You will see the charts in this book are kindly provided by eSignal. Over the years, I have used many different systems. One thing I have stuck to is my eSignal. I absolutely love it. Thanks to Mina Delgado and all at eSignal for their ongoing support.

Legal Information Futures trading involves substantial risk of loss and is not suitable for all investors. Past performance is not necessarily indicative of future trading results. Information here is taken from sources believed to be reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. There is no guarantee that the information given here will result in profitable trades. Only you can take responsibility for your trading decisions. This document is meant as education, not advice. © Copyright 2009 Guy Bower. All Rights Reserved. ProTrader LLC. 244 5th Avenue #2741. New York, NY 10001

Guy Bower’s Guide to Futures and Spread Trading Page 3

Contents 1. Introduction 4

2. What are futures? 5

What are futures? 5

Elements of a futures contract 6

Mechanics of Futures Trading 8

Trading Examples 8

Futures Quiz 12

3. What are spreads? 17

What are Spreads? 17

Types of futures spreads 17

Spread Charts 18

More risk or less risk? 21

How to trade spreads 23

Spreads Quiz 24

4. What is seasonality? 27

What is Seasonality? 27

What Drives Seasonality in Markets? 27

Is Seasonal Analysis Technical or Fundamental? 28

Seasonality Quiz 30

5. Putting it all together 32

Summary 32

How the ProTrader Digest does it 33

6. ProTrader Digest offer 37

7. Glossary 38

8. ProTrader Digest Offer (in case you missed the first one) 44

Guy Bower’s Guide to Futures and Spread Trading Page 4

1. Introduction

Welcome and thank you for downloading this book.

I’ve been involved in the financial markets for around 20 years. I started out charting shares and spot currencies when I was in high school. In my 20’s, I worked as an analyst, broker, author and was a director of a managed futures fund. I’ve since started my own broking business, advisory services and even been a CEO of a stock broker and a director of a stock exchange (in Papua New Guinea of all places).

The one thing I have learnt is knowledge is key. I’m not saying you need to know everything. But you have to have an open mind and always been ready to take on new information and new ways to trade.

Five years ago, my focus was on options. In Australia, it was what I was known for. These days, my focus has shifted to something new.

Well what we talk about in this book is not “new” as such, but it will be new to many readers. Trading futures spreads using seasonal analysis has been around for a couple of decades now, but it is evolving. Until recently, I could easily say this was a trading method only professionals know and used.

These days with advent of the internet and free flowing information, seasonal spread trading is getting a wider audience. It’s not a minute too soon either. Anyone invested in the stock market or property in 2008 will know these areas are not ‘be all, end all’ of investment.

Spread trading is by no means the perfect form of trading. However this form of trading did very well in 2008 and it is not correlated in any way to stock or property markets. The memory of 2008 for many investors is not a good one. But sitting still, licking wounds and waiting for stocks to recover is not the best of strategies moving forward.

The book introduces a specific style of trading. It is not designed to give you all the answers, but furnish you with some basic concepts and hopefully whet your appetite for more.

For more information, contact me or visit the website. Oh, also stay tuned for the special offer in the book (or scroll to the end if you cannot wait).

Best regards and good trading!

Guy Bower, 2009 [email protected] www.ProTraderDigest.com

Guy Bower’s Guide to Futures and Spread Trading Page 5

1. What are Futures?

To many people futures trading is considered a risky endeavour and only for the brave hearted among us. This is untrue. Futures trading can be a very rewarding form of investment, but only when approached with the right attitude and strategy.

The legal definition of a futures contract is “a legally binding agreement to buy or sell a specified amount of a commodity or financial instrument at a fixed price some time in the future”.

The original purpose of futures contracts was to provide a facility for people to hedge their price risk.

Example

Through the Chicago Mercantile Exchange you can buy or sell futures contracts based on the S&P500, the top 500 stocks in America. At no point are you buying (selling) the actual stocks, rather you are entering into an agreement to buy (sell) a dollar value based on the S&P500 index value. The contract is represents $250 times the quoted index value.

This market is used by fund managers and private individuals to hedge share portfolios. However the majority of private individuals using this market are short-term traders.

Many readers will be familiar with the concept of ‘going long’. Going ‘long’ simply means to have purchased the asset with the view of that asset increasing in price. When you buy shares you are said to be long shares. A straight forward concept.

The concept of going ‘short’ creates some confusion among new traders. However the concept is not that difficult. Gong short simply means to have sold the contract before you buy it with a view on making a profit from a fall in the price.

Since futures contracts do not involve immediate delivery or settlement of the instrument, it is possible to sell the contract without first owning it. Think about that. A futures contract is just an agreement, not a physical asset. So selling the contract (going short) is just an agreement to sell the underlying asset at a certain price.

Buying back (selling) a short (long) contract to take a profit/loss is referred to as “closing the position”.

What futures contracts are available?

The answer is pretty much any commonly traded commodity or financial asset will most likely have a corresponding futures contract listed somewhere in the world.

There are futures contracts on financial assets such as individual stocks, stock market indices, and short and long term interest rates. There are futures on physical commodities such as wool, wheat, gold, soybeans, lead and oil. There are even futures contracts on more obscure things such as electricity supplies, unleaded petrol and weather temperatures in certain cities.

Guy Bower’s Guide to Futures and Spread Trading Page 6

The list really does go on and on. A futures exchange will list certain futures contracts based on demand from the traders and investors. Most futures exchange started out offering commodity based contracts for producers to hedge price exposure. Today, hedging activity is just a small fraction of volume trades. Instead speculators dominate most markets.

Elements of a futures contract

Underlying asset

In the above example, the underlying asset (or just ‘underlying’) was the S&P500. Specifically it was a cash value equal to $250 times the quotes contract value.

Each futures contract is different. For commodity futures, the contract will be based on a certain physical volume of a specific grade. Gold futures for example are based on 100 troy ounces per contract at a grade of not less than 0.995 fineness.

As mentioned each contract is different. Naturally the quantity and any particular grading of the underlying is an important consideration in hedging any asset.

Delivery Month

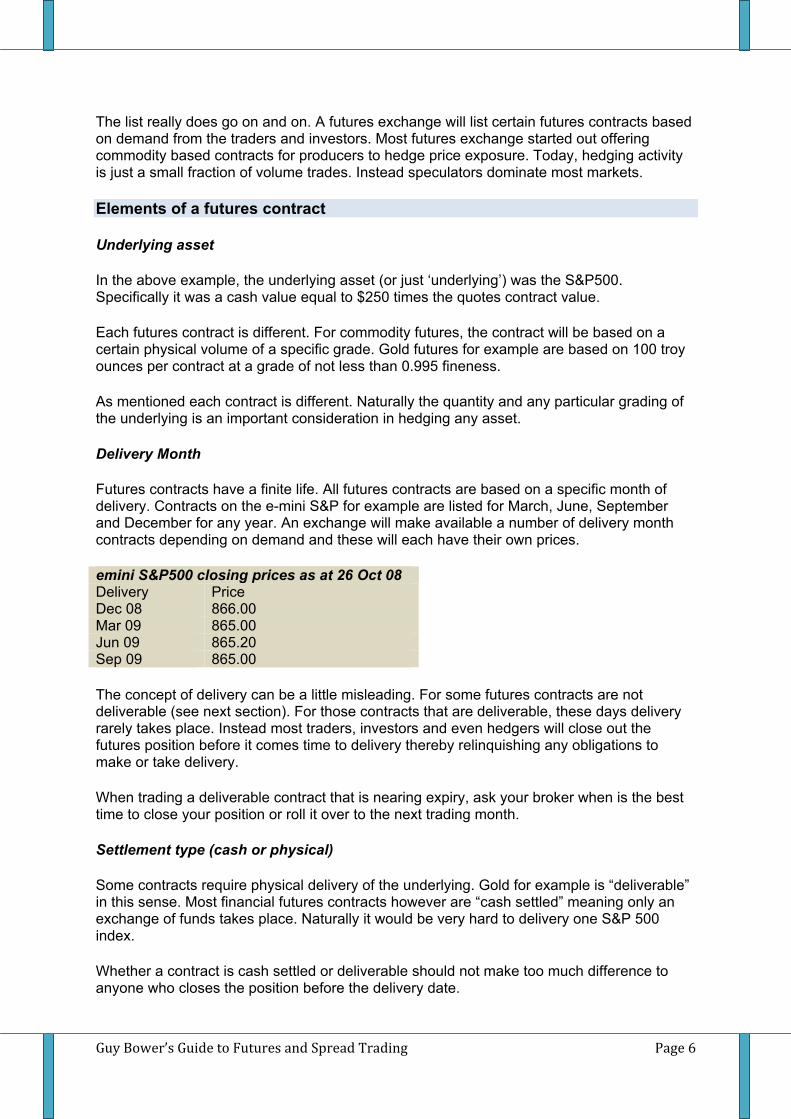

Futures contracts have a finite life. All futures contracts are based on a specific month of delivery. Contracts on the e-mini S&P for example are listed for March, June, September and December for any year. An exchange will make available a number of delivery month contracts depending on demand and these will each have their own prices.

emini S&P500 closing prices as at 26 Oct 08 Delivery Price Dec 08 866.00 Mar 09 865.00 Jun 09 865.20 Sep 09 865.00

The concept of delivery can be a little misleading. For some futures contracts are not deliverable (see next section). For those contracts that are deliverable, these days delivery rarely takes place. Instead most traders, investors and even hedgers will close out the futures position before it comes time to delivery thereby relinquishing any obligations to make or take delivery.

When trading a deliverable contract that is nearing expiry, ask your broker when is the best time to close your position or roll it over to the next trading month.

Settlement type (cash or physical)

Some contracts require physical delivery of the underlying. Gold for example is “deliverable” in this sense. Most financial futures contracts however are “cash settled” meaning only an exchange of funds takes place. Naturally it would be very hard to delivery one S&P 500 index.

Whether a contract is cash settled or deliverable should not make too much difference to anyone who closes the position before the delivery date.

Guy Bower’s Guide to Futures and Spread Trading Page 7

Margin

When buying or selling futures contracts it is not necessary to pay the full price for that contract. Rather futures contracts are ‘margined’. An ‘initial margin’ is like a deposit the trader pays when initiating a position. These funds must be in your account before you are allowed to place a trade. The margin is then held by the Clearing House of the exchange and is returned when the position is closed. Typically an initial margin works out to be but a few percent of the total contract value.

The current initial margin for the e-mini S&P500 Index is $4,860. Remember this is for a contract that is worth $50 times the index value. So at 866 the S&P contract value is $43,400. So for a deposit of $4,860 you can buy and sell the equivalent for $43,400 worth of shares.

Another type of margin is a ‘variation margin’. At the end of each trading day, the Clearing House from any particular futures exchange will settle all profits and losses on all open positions and credit/debit all trading accounts accordingly. This is called the variation margin. Note the positions are not closed. It is just the profit or loss that is settled.

For those readers that have traded equity options, this type of margining is very similar.

Exchange listing

Trading of futures contracts is conducted on a Futures Exchange such as the Chicago Board of Trade or Eurex.

Some exchanges offer electronic trading only. Others offer a pit or floor trading session. Pit trading is also called open outcry. This is the traditional system of trading futures. The contracts are traded by brokers and traders face to face in the exchange itself (the movie ‘Trading Places’ has good example).

In recent years, there has been a push towards electronic trading. Some exchanges such as Eurex and Australia’s ASX are completely electronic. That is there is no open outcry trading floor.

Some exchanges, mostly American ones, persist with open outcry trading and some offer side by side trading – simultaneous open outcry and electronic sessions. While it has made a lot of floor traders obsolete, electronic trading is meant to offer a more efficient price mechanism and thereby offer a fair system to all participants.

Whether a market is electronic or pit traded is not really an important point to this lesson, but you do need to know on what exchange your markets is trading. Knowledge of different markets comes with time, but these things are also pretty easy to Google.

Price

Last but not least there is the price you can trade the contract. For any one futures contract, the above features are fixed and cannot be changed in the open market place. The price for any futures contract however is determined by supply and demand. The price is the variable.

Guy Bower’s Guide to Futures and Spread Trading Page 8

The mechanics of futures trading

Futures contracts, like shares are traded though a broker. You have to use a futures broker, not a stock broker. Through any futures broker, you can trade any registered futures contract in the world – whether it be gold in New York or share futures in London or the Nikkei from Singapore.

Trading examples Here we are going to learn two strategies: going long and going short.

Going Long If you have traded or invested in anything before, you are already familiar with the concept of going long. This is where you buy a certain asset with the view of it increasing in price. If and when the price does increase, you can close (sell) the position at a profit.

With futures contract you are not buying anything physical. You are essentially entering into an agreement to buy a certain asset on a certain date in the future. Today in the open marketplace you can agree to buy a futures contract at what the market deems to be the price. At some time in the future, perhaps later in the day, you can close out of the position by selling the contract back in the market.

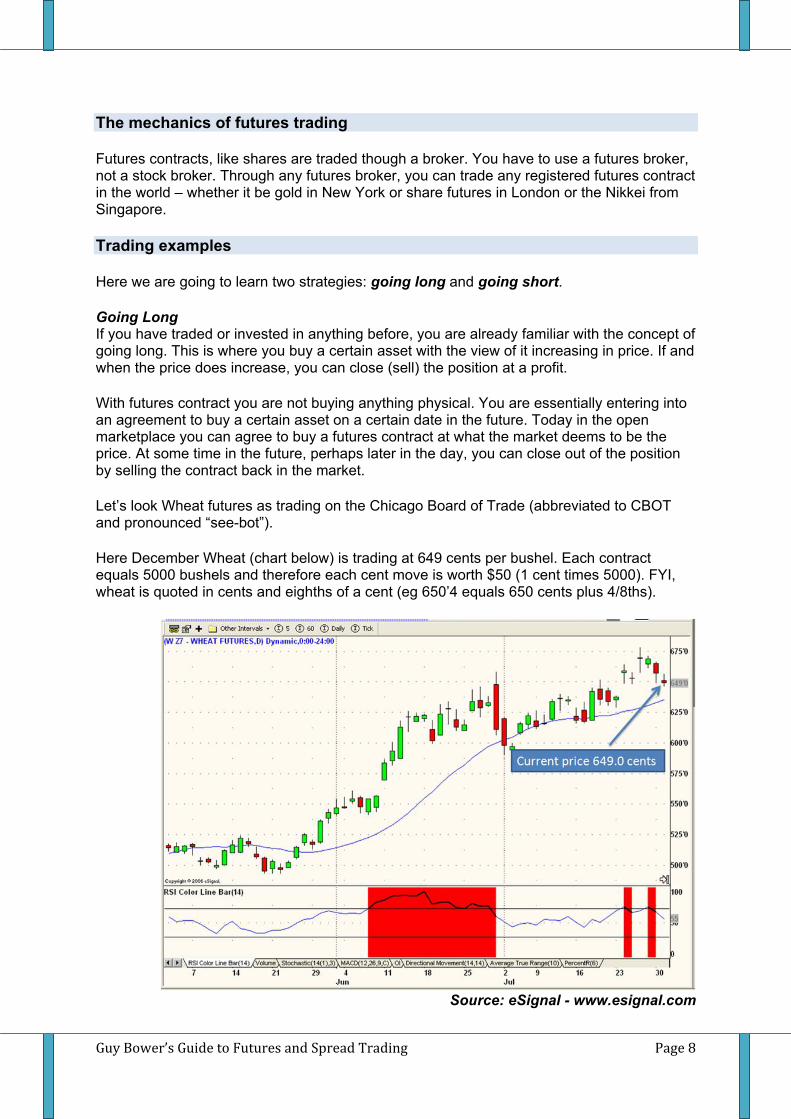

Let’s look Wheat futures as trading on the Chicago Board of Trade (abbreviated to CBOT and pronounced “see-bot”).

Here December Wheat (chart below) is trading at 649 cents per bushel. Each contract equals 5000 bushels and therefore each cent move is worth $50 (1 cent times 5000). FYI, wheat is quoted in cents and eighths of a cent (eg 650’4 equals 650 cents plus 4/8ths).

Source: eSignal - www.esignal.com

Guy Bower’s Guide to Futures and Spread Trading Page 9

Suppose, based on your analysis you think the price of wheat was going to rise in the next few weeks. Here you would buy or “go long” wheat. The process is the same as buying shares or exchange traded funds – except of course you use a futures broker.

Time passes and a couple of weeks later December wheat futures are trading at 684’4. If you were to sell at this price, the trade would show a profit of 35 and 4/8ths cents before commissions. In terms of dollars, this translates to $1775 per contract.

Source: eSignal - www.esignal.com

In this trade, you “went long December wheat” and it showed a nice little profit.

Going Short

Remember with futures, you are not actually buying the physical commodity. You are entering into an agreement based on what the market thinks that commodity will be worth at some time on the future. Any futures trade is just agreement.

In the example above, by going long you entered into an agreement to but December wheat at 649 cents. Two weeks later you sold that agreement back in the market at 684.5, resulting in an overall profit.

If this is only an agreement, why can you enter an agreement to sell instead of buy - and thereby make money from a fall in the market? You can. This is called going short and in this case it is the opposite of going long.

Let’s use an example of a falling market to illustrate. Suppose you read somewhere that the Gold price is dues for a drop. Perhaps there is talk of a few central banks selling their gold reserves and this creates a negative view.

Guy Bower’s Guide to Futures and Spread Trading Page 10

In this instance, you can sell a futures contract in gold and profit from any fall. This is the point where some people get stuck. How can you sell something you do not own? Remember, futures contracts are just agreement on price. There is no actual ownership of the commodity in question.

So by selling a contract, or “going short” you have entered into a contract to sell at this price. At any time before expiration of the contract, you can buy it back in the open market place by buying one contract at the prevailing price.

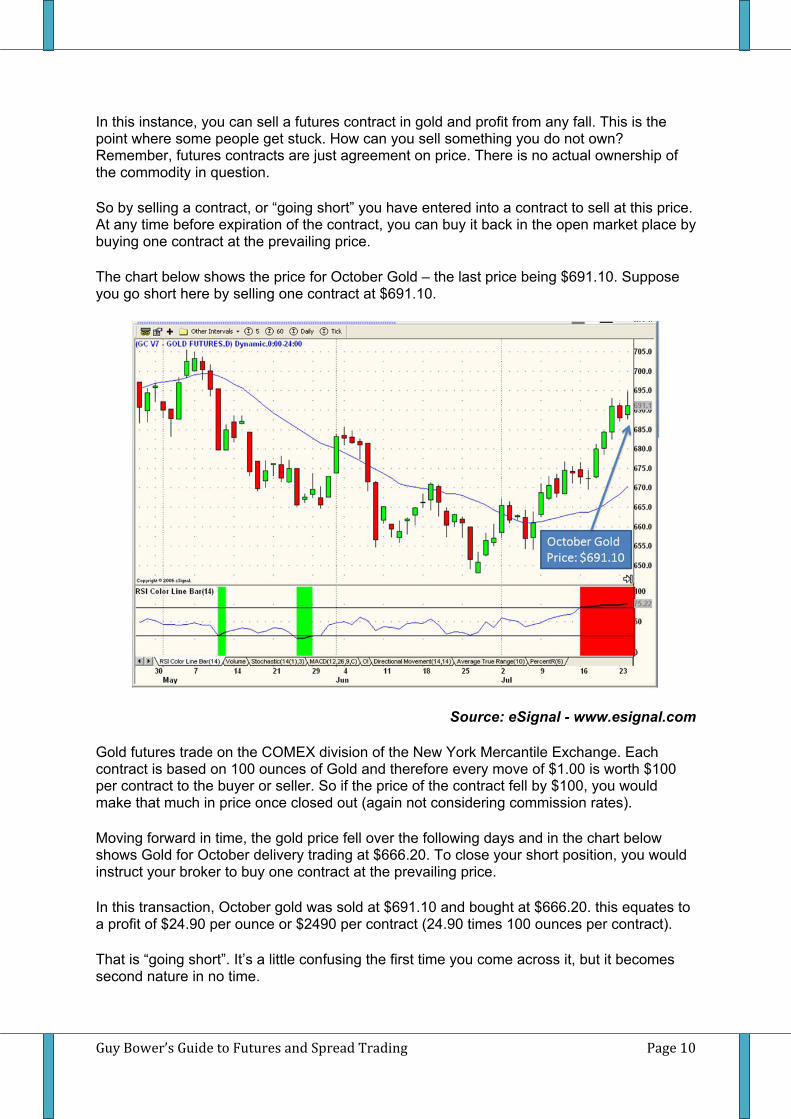

The chart below shows the price for October Gold – the last price being $691.10. Suppose you go short here by selling one contract at $691.10.

Source: eSignal - www.esignal.com

Gold futures trade on the COMEX division of the New York Mercantile Exchange. Each contract is based on 100 ounces of Gold and therefore every move of $1.00 is worth $100 per contract to the buyer or seller. So if the price of the contract fell by $100, you would make that much in price once closed out (again not considering commission rates).

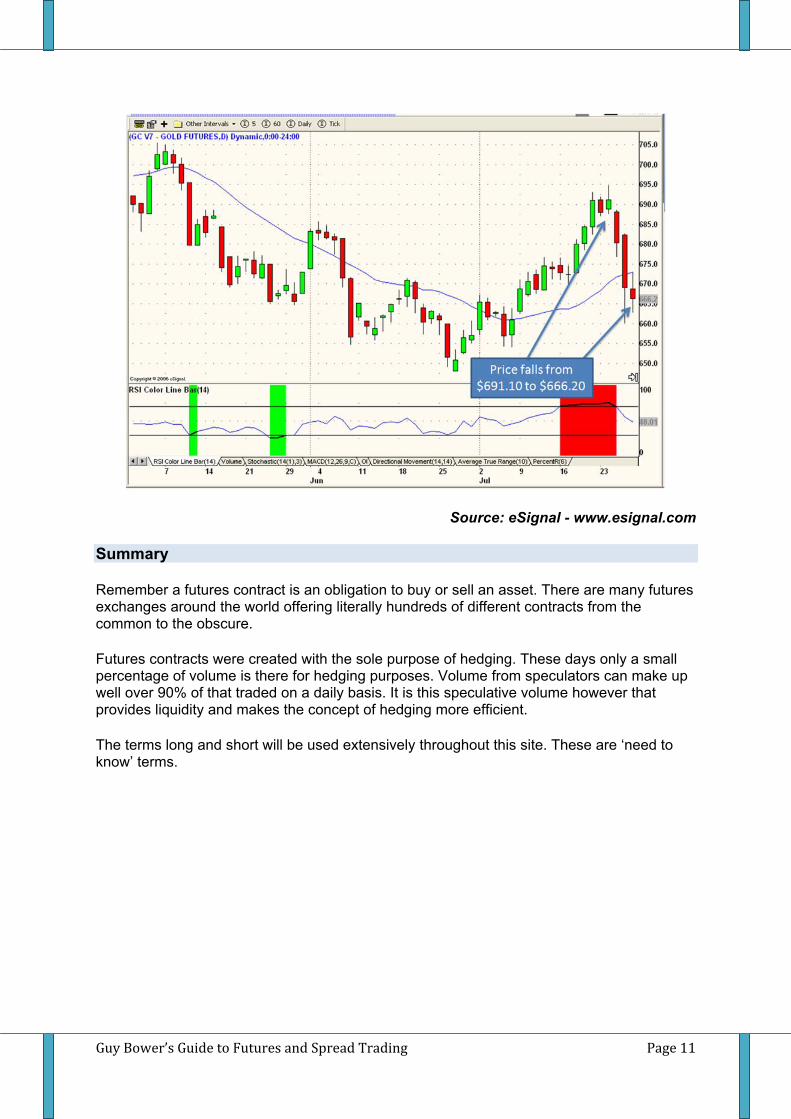

Moving forward in time, the gold price fell over the following days and in the chart below shows Gold for October delivery trading at $666.20. To close your short position, you would instruct your broker to buy one contract at the prevailing price.

In this transaction, October gold was sold at $691.10 and bought at $666.20. this equates to a profit of $24.90 per ounce or $2490 per contract (24.90 times 100 ounces per contract).

That is “going short”. It’s a little confusing the first time you come across it, but it becomes second nature in no time.

Guy Bower’s Guide to Futures and Spread Trading Page 11

Source: eSignal - www.esignal.com

Summary

Remember a futures contract is an obligation to buy or sell an asset. There are many futures exchanges around the world offering literally hundreds of different contracts from the common to the obscure.

Futures contracts were created with the sole purpose of hedging. These days only a small percentage of volume is there for hedging purposes. Volume from speculators can make up well over 90% of that traded on a daily basis. It is this speculative volume however that provides liquidity and makes the concept of hedging more efficient.

The terms long and short will be used extensively throughout this site. These are ‘need to know’ terms.

Guy Bower’s Guide to Futures and Spread Trading Page 12

Futures Quiz OK, let’s have a little Q&A session. Some of these questions test knowledge of basic definitions. Just refer back to the previous pages for these ones. Questions 5-9 require a little math. If you are new to futures and not so good with numbers, don’t be frustrated with this. It will not take long to get the hang of it. Additionally, the good thing is real life calculations rarely get more complicated than this.

Q1. What is a futures contract?

A. The right, but not obligation to sell a commodity or financial instrument at a fixed price some time in the future.

B. A legally binding agreement to buy or sell a specified amount of a commodity or financial instrument at a fixed price some time in the future.

C. The right, but not obligation to buy a commodity or financial instrument at a fixed price some time in the future.

D. All of the above

Q2. What is meant by “going short”?

A. Where you BUY a certain asset with the view of it increasing in price.

B. Where you SELL a certain asset with the view of it increasing in price.

C. Where you BUY a certain asset with the view of it decreasing in price.

D. Where you SELL a certain asset with the view of it decreasing in price.

Q3. What is meant by “going long”?

A. Where you BUY a certain asset with the view of it increasing in price.

B. Where you SELL a certain asset with the view of it increasing in price.

C. Where you BUY a certain asset with the view of it decreasing in price.

D. Where you SELL a certain asset with the view of it decreasing in price.

Guy Bower’s Guide to Futures and Spread Trading Page 13

Q4. If you are short one contract, then buy one contract, you are:

A. Long one contract

B. Short two contracts

C. Short one contract

D. Flat (no position)

The next few questions will require a little research. Reference the “Contract Specifications” link on the ProTraderDigest site.

Q5. Today in the CME S&P500 contract (the full sized one) you bought one contract at 800.00 and sold one contract at 805.00. Excluding commissions, what is your profit?

A. $500

B. zero

C. $1250

D. $250

Q6. What would have been your profit if you had traded the emini S&P500 contract instead?

A. $500

B. zero

C. $1250

D. $250

Q7. Suppose you paid $20 per side in commission, what would be your profit from the transaction in Question 6? (Note “per side” is an industry term meaning the commission payable per contract per transaction).

A. $210

B. $250

C. $230

D. $290

Guy Bower’s Guide to Futures and Spread Trading Page 14

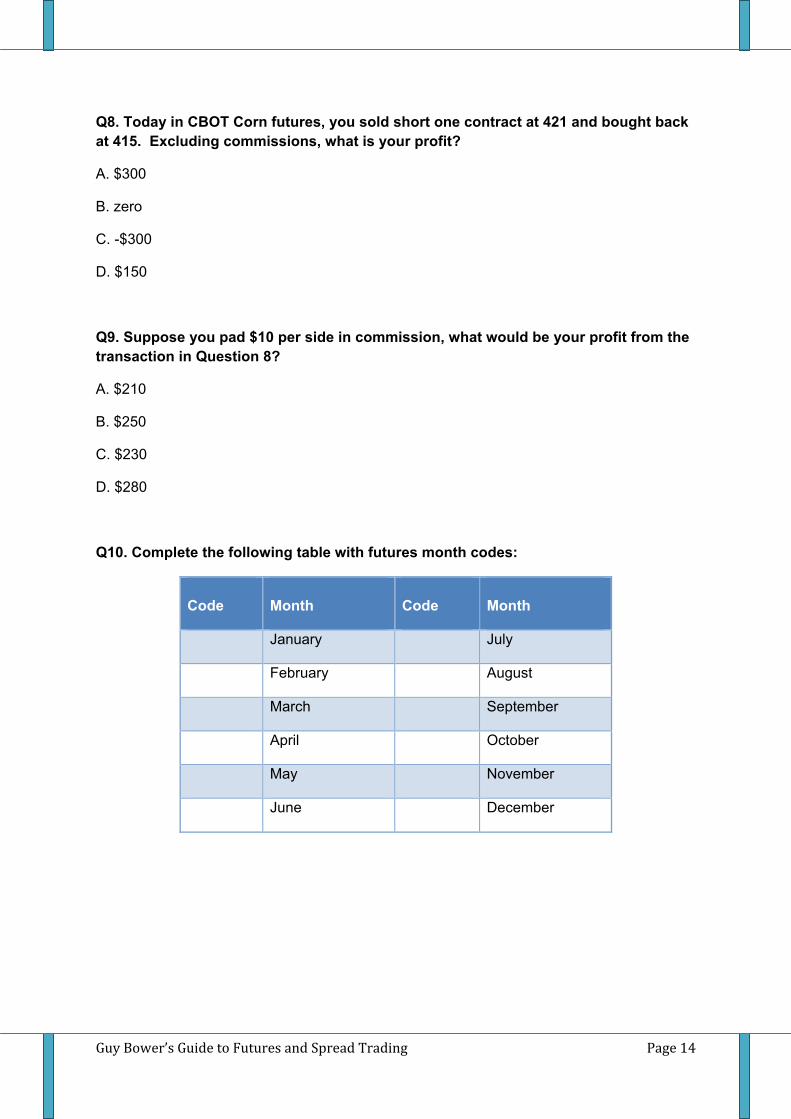

Q8. Today in CBOT Corn futures, you sold short one contract at 421 and bought back at 415. Excluding commissions, what is your profit?

A. $300

B. zero

C. -$300

D. $150

Q9. Suppose you pad $10 per side in commission, what would be your profit from the transaction in Question 8?

A. $210

B. $250

C. $230

D. $280

Q10. Complete the following table with futures month codes:

Code

Month

Code

Month

January July

February August

March September

April October

May November

June December

Guy Bower’s Guide to Futures and Spread Trading Page 15

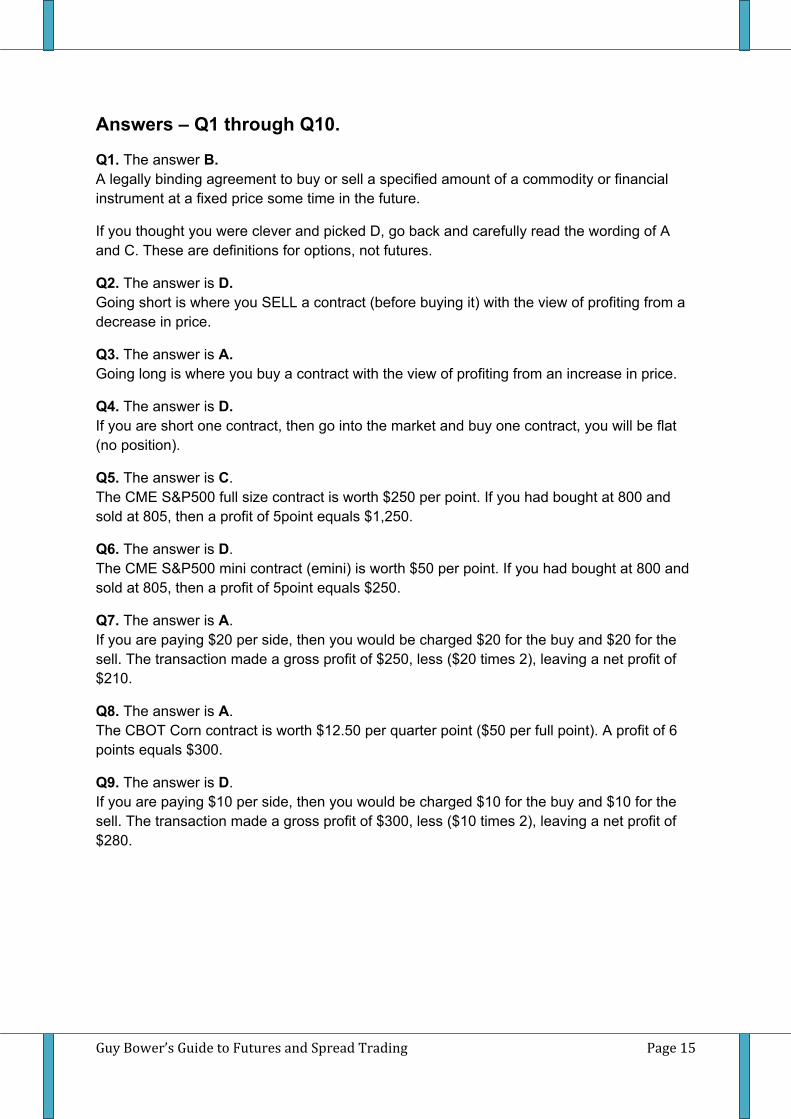

Answers – Q1 through Q10.

Q1. The answer B. A legally binding agreement to buy or sell a specified amount of a commodity or financial instrument at a fixed price some time in the future.

If you thought you were clever and picked D, go back and carefully read the wording of A and C. These are definitions for options, not futures.

Q2. The answer is D. Going short is where you SELL a contract (before buying it) with the view of profiting from a decrease in price.

Q3. The answer is A. Going long is where you buy a contract with the view of profiting from an increase in price.

Q4. The answer is D. If you are short one contract, then go into the market and buy one contract, you will be flat (no position).

Q5. The answer is C. The CME S&P500 full size contract is worth $250 per point. If you had bought at 800 and sold at 805, then a profit of 5point equals $1,250.

Q6. The answer is D. The CME S&P500 mini contract (emini) is worth $50 per point. If you had bought at 800 and sold at 805, then a profit of 5point equals $250.

Q7. The answer is A. If you are paying $20 per side, then you would be charged $20 for the buy and $20 for the sell. The transaction made a gross profit of $250, less ($20 times 2), leaving a net profit of $210.

Q8. The answer is A. The CBOT Corn contract is worth $12.50 per quarter point ($50 per full point). A profit of 6 points equals $300.

Q9. The answer is D. If you are paying $10 per side, then you would be charged $10 for the buy and $10 for the sell. The transaction made a gross profit of $300, less ($10 times 2), leaving a net profit of $280.

Guy Bower’s Guide to Futures and Spread Trading Page 16

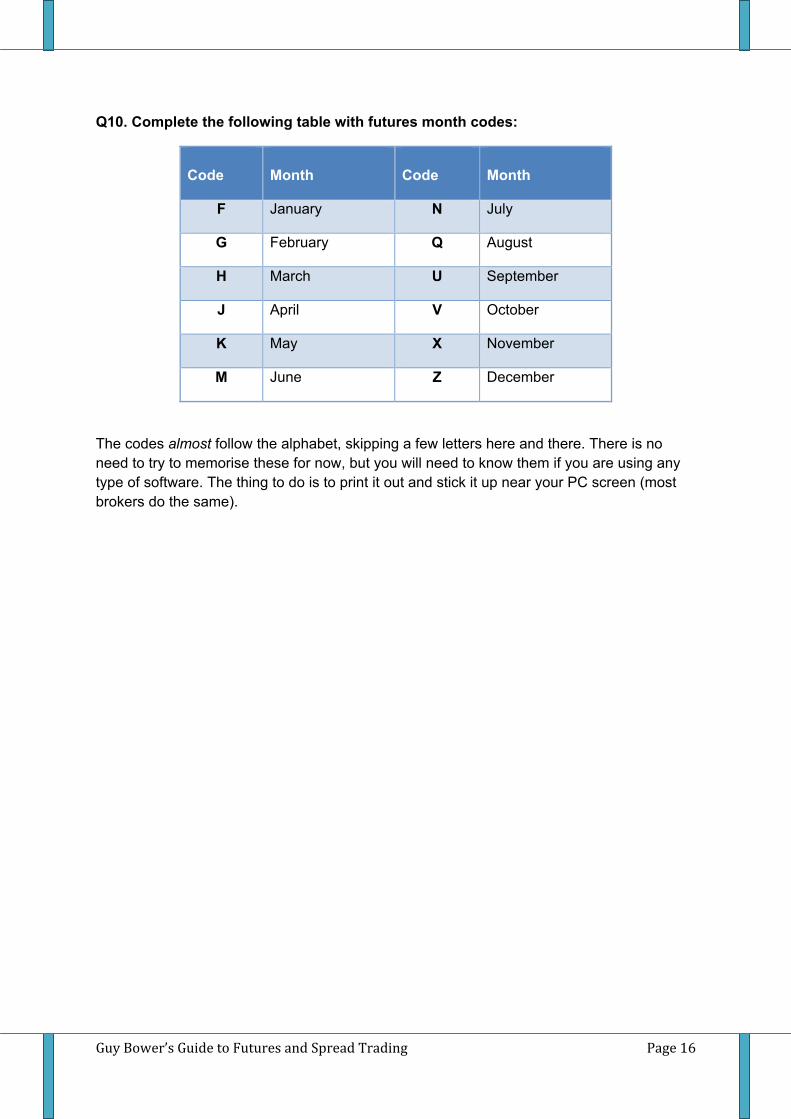

Q10. Complete the following table with futures month codes:

Code

Month

Code

Month

F January N July

G February Q August

H March U September

J April V October

K May X November

M June Z December

The codes almost follow the alphabet, skipping a few letters here and there. There is no need to try to memorise these for now, but you will need to know them if you are using any type of software. The thing to do is to print it out and stick it up near your PC screen (most brokers do the same).

Guy Bower’s Guide to Futures and Spread Trading Page 17

2. What are Spreads? Spread trading is an integral part of the ProTrader Digest offering. This lesson should give you the basic concept of spread trading. Here, we are just covering a few definitions.

What are spreads?

A spread is where you buy one asset (contract, share, bond etc) and sell something related or similar with a view to profit from a change in the price differential. Here are some examples of spread trades:

Buy (long) Sell (short) Why trade the spread?Apple Microsoft You may have a view that the earnings in one

technology company are too high relative to the other and the stock prices are set to realign accordingly.

Dec Crude Oil futures

June Crude Oil futures

This is a futures spread where you buy and sell the same market, but in different contract months. Temporary production or seasonal demand factors can make this kind of spread move.

Live Cattle futures

Lean Hogs futures

This is a spread where you buy one market and short sell a related market. Differing production and consumption estimates for each market can often provide good trading opportunity.

These are not recommendations for trades. They are just examples of spread trades. All spread trades are just positions where you expect the difference in price to move in your favour. As for futures spreads, these are simply spreads trades in futures contracts (as per the last two examples above and the following examples).

Types of futures spreads

We’ll be looking at two types of spreads using futures contracts.

Intra-commodity spreads

This is where you buy one delivery month and sell another in the same commodity (e.g. simultaneously buy August Soybeans and sell November Soybeans). These are also called “calendar” or “time” spreads for obvious reasons.

Inter-market spreads

There are also inter-commodity spreads where you buy one commodity and sell a related commodity (e.g. buy December Live Cattle, sell December Lean Hogs).

Guy Bower’s Guide to Futures and Spread Trading Page 18

Sometimes it is easy to confuse the terms inter and intra. Don’t worry about this so much. It’s more important that you know the basic idea. Both types of spreads simply try to make money from the change in relative prices of the contract.

At this stage, all you need to understand is the concept of going long one contract and short another simultaneously. There is really not a lot to it. A spread trade is all about making money from the relative change in prices.

Spread charts

If you are reading up on spread trading elsewhere, you’ll need to understand how spread charts are displayed.

Generally speaking you will calculate the spread as the bought(long) side minus the sold(short) side. Some books on spread trading will show the near contract month minus the distant month for intra-market spreads, but this is a little confusing.

For this lesson, we’ll stick with ‘bought less sold’. This is also the way we display things on the eSignal charts shown throughout.

Examples of futures spreads

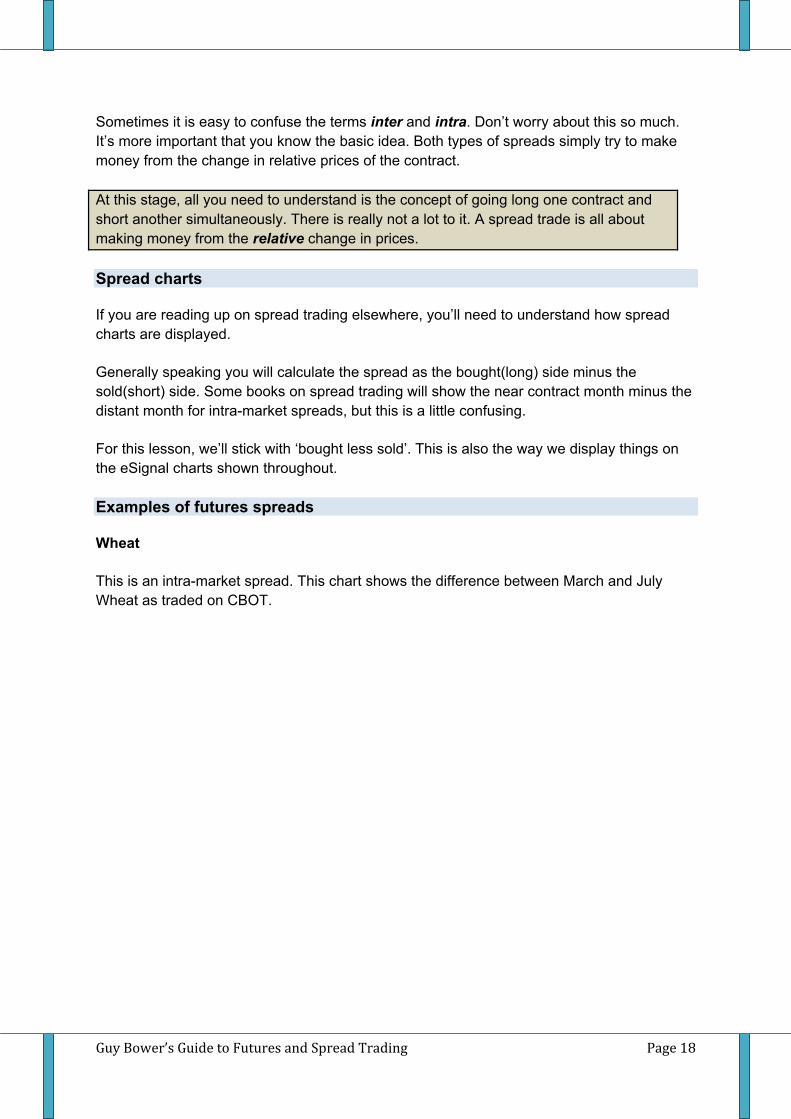

Wheat

This is an intra-market spread. This chart shows the difference between March and July Wheat as traded on CBOT.

Guy Bower’s Guide to Futures and Spread Trading Page 19

Source: eSignal - www.esignal.com

As you can see, the period leading up to October it was very quiet. Then it just exploded! Spreads don’t normally behave this dramatically, but occasionally they do. Not good if you are on the wrong side of it, but great if you are.

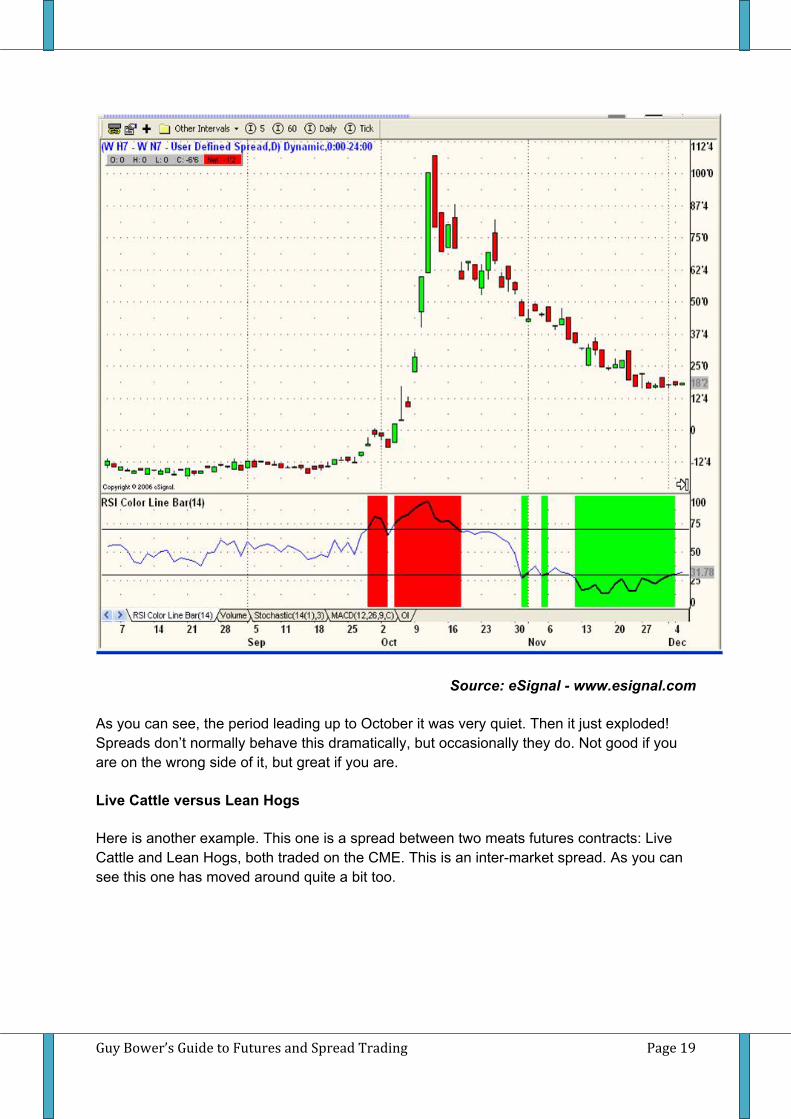

Live Cattle versus Lean Hogs

Here is another example. This one is a spread between two meats futures contracts: Live Cattle and Lean Hogs, both traded on the CME. This is an inter-market spread. As you can see this one has moved around quite a bit too.

Guy Bower’s Guide to Futures and Spread Trading Page 20

Source: eSignal - www.esignal.com

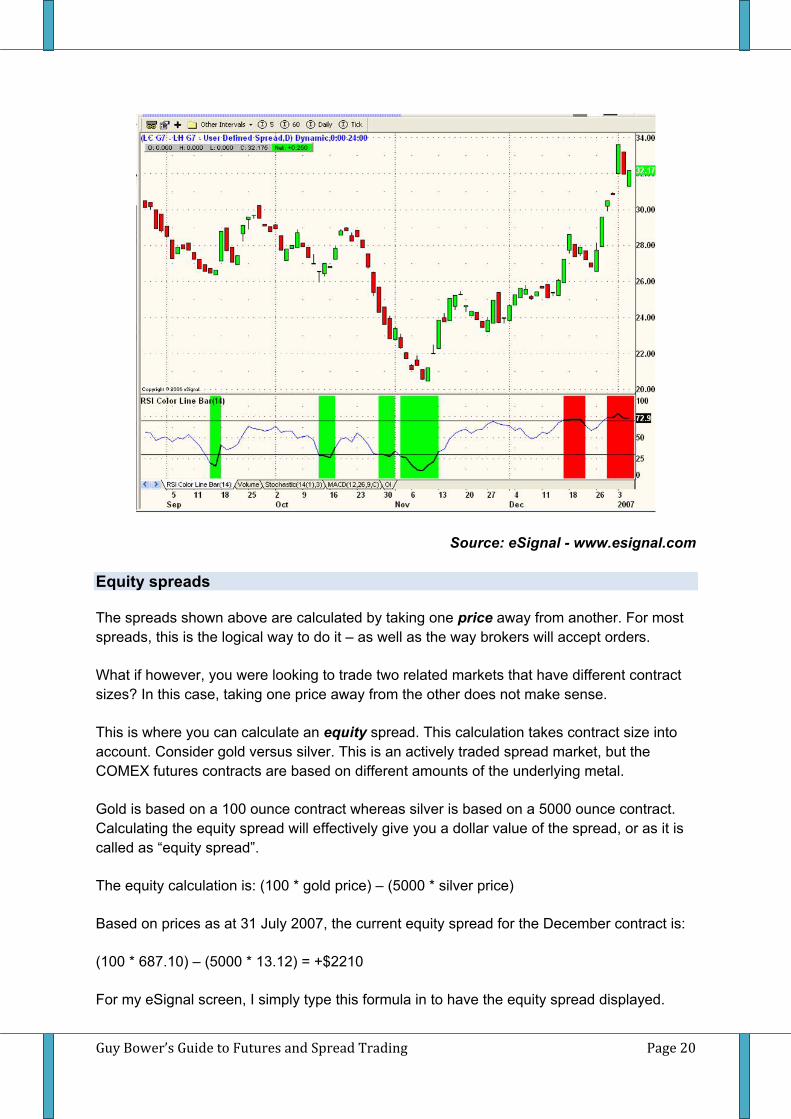

Equity spreads

The spreads shown above are calculated by taking one price away from another. For most spreads, this is the logical way to do it – as well as the way brokers will accept orders.

What if however, you were looking to trade two related markets that have different contract sizes? In this case, taking one price away from the other does not make sense.

This is where you can calculate an equity spread. This calculation takes contract size into account. Consider gold versus silver. This is an actively traded spread market, but the COMEX futures contracts are based on different amounts of the underlying metal.

Gold is based on a 100 ounce contract whereas silver is based on a 5000 ounce contract. Calculating the equity spread will effectively give you a dollar value of the spread, or as it is called as “equity spread”.

The equity calculation is: (100 * gold price) – (5000 * silver price)

Based on prices as at 31 July 2007, the current equity spread for the December contract is:

(100 * 687.10) – (5000 * 13.12) = +$2210

For my eSignal screen, I simply type this formula in to have the equity spread displayed.

Guy Bower’s Guide to Futures and Spread Trading Page 21

Source: eSignal - www.esignal.com

There are only a few markets in which you’ll see equity spreads. Some of these are: Gold versus Silver, NYMEX energy spreads, CBOT soybean oil versus other grains and some CME FX cross rate spreads.

Overall, this is not an important part of the eBook, but it is something that needs to be mentioned.

Spreads: more risk, less risk?

You’ll often hear people talk about the reduced risk of spread trading. In the majority of cases this is very true – spreads to have less risk than outright futures positions.

This does actually make sense. A spread between two calendar months in the same market will in most cases be significantly lower in volatility than that of the underlying market.

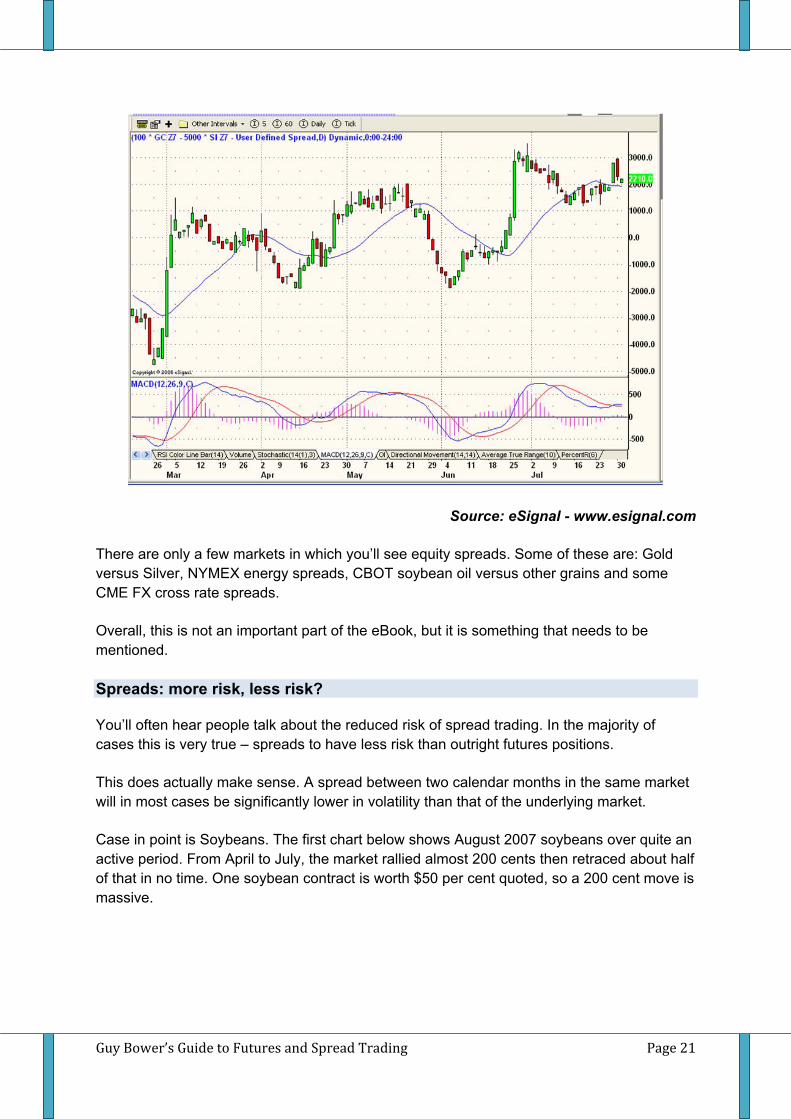

Case in point is Soybeans. The first chart below shows August 2007 soybeans over quite an active period. From April to July, the market rallied almost 200 cents then retraced about half of that in no time. One soybean contract is worth $50 per cent quoted, so a 200 cent move is massive.

Guy Bower’s Guide to Futures and Spread Trading Page 22

Source: eSignal - www.esignal.com

Compare this to a Soybean spread chart. The next chart shows August versus March Soybeans. Over the same period in which Soybeans rallied almost 200pts, the spread had a range of about 25pts.

Source: eSignal - www.esignal.com

This example is typical of many spreads, but it less applicable to inter-market spreads (spreading one market versus another).

Guy Bower’s Guide to Futures and Spread Trading Page 23

Opening, closing and intraday prices

Generally speaking spread traders are more active during the opening and closing minutes of the trading session. This is because many spread traders take a longer term view. The type of trades we will look at in this eBook are no different. They are longer term trades.

For us the closing spread price – or at least the prices seen in the closing minutes are the most important.

How to trade spreads

Ah, now this is what the site is all about! The approach one can take as a spread trader is varied. Some spread traders will focus on interest rate markets and effectively trade interest rate expectations. Others will base trades on technical analysis, or company takeover activity. Just like any style of trading out there, there are spread traders that will have different ideas, views and theories.

The ProTrader Digest looks at seasonal spread trading. The next lesson explains the concept of seasonality.

Guy Bower’s Guide to Futures and Spread Trading Page 24

Spread Quiz OK, let’s get going with some more questions. Here we will look at a few definitions, then ask some question that require logic. Some of the questions may seem a little odd. However the purpose is not to test your knowledge so much as it is to get you thinking about why you would trade spreads.

Q11. What is an intra-commodity spread?

A. This is where you buy one commodity and sell an un-related commodity.

B. This is where you buy one commodity and sell a related commodity to profit from a move in the price differential.

C. This is where you buy one delivery month and sell another in the same commodity to profit from a move in the price differential.

Q12. What in an inter-commodity spread?

A. This is where you buy one commodity and sell an un-related commodity.

B. This is where you buy one commodity and sell a related commodity to profit from a move in the price differential.

C. This is where you buy one delivery month and sell another in the same commodity to profit from a move in the price differential.

Q13. What is an equity spread?

A. It is simply the price of one contract minus the price of another.

B. This is where the value of the spread is calculated using the dollar values of the underlying contracts, rather than the point value.

C. It is where what is bought and what is a sold is exactly “equal”.

Q14. Crazy Jack, your trader friend, told you he just put on a spread trade where he bought the December S&P500 and sold the June Ethanol contract? Why is he crazy?

A. You cannot spread a December contract versus a June contract

B. He has a 70’s style moustache.

C. This is not a “spread” trade as such since the two contracts are not related.

D. All of the above.

Guy Bower’s Guide to Futures and Spread Trading Page 25

Q15-Q20. Which of these trades are NOT spread trades?

Q15. Long December Eurodollars Short June Eurodollars

Q16. Long December Lean Hogs Short December Live Cattle

Q17. Long December Live Cattle Short November Feeder Cattle

Q18. Long December 10yr Treasury Notes Short December 30yr Treasury Bonds

Q19. Long July Sugar Short July Cocoa

Q20. Long November Soybeans Short November Orange Juice

Guy Bower’s Guide to Futures and Spread Trading Page 26

Answers – Q11 through Q20.

Q11. The answer is C. This is where you buy one delivery month and sell another in the SAME commodity to profit from a move in the price differential.

Q12. The answer is B. This is where you buy one commodity and sell a RELATED commodity to profit from a move in the price differential.

Q13. The answer is B. This is where the value of the spread is calculated using the dollar values of the underlying contracts, rather than the point value. Equity spreads are used when the contract size of two related contracts are different. For example Silver and Gold contracts have different underlying contract sizes and therefore when quoting a spread, you would use the equity value, rather than the point value.

Q14. The answer is C. The contracts are not related. The answer is also B, but you were not to know he had a moe.

Q15 through to Q18

All of these are spread trades as they involve buying and selling related contracts. They can therefore be considered ‘spread trades’.

Q19 and Q20

Technically, these are not spread trades as such as they are unrelated contracts. While they are all crops, strictly speaking, they are not related. They grow in different regions and have different cycles. For a buy/sell combination of trades to be considered a spread trade, the contracts need to have a strong relationship (or “high correlation” in statistics jargon).

Guy Bower’s Guide to Futures and Spread Trading Page 27

3. What is Seasonality?

Seasonality refers to a pattern that depends on, or is controlled by, the time of the year. Seasonality appears in many places. For example, sales of Christmas cards logically peak before Christmas. Accounting business peaks around end of financial year. Sales of red roses peak just before 14th February. Many businesses, products and statistics are subject to seasonal variations. For the trader, it can mean opportunity.

What drives seasonal patterns in markets?

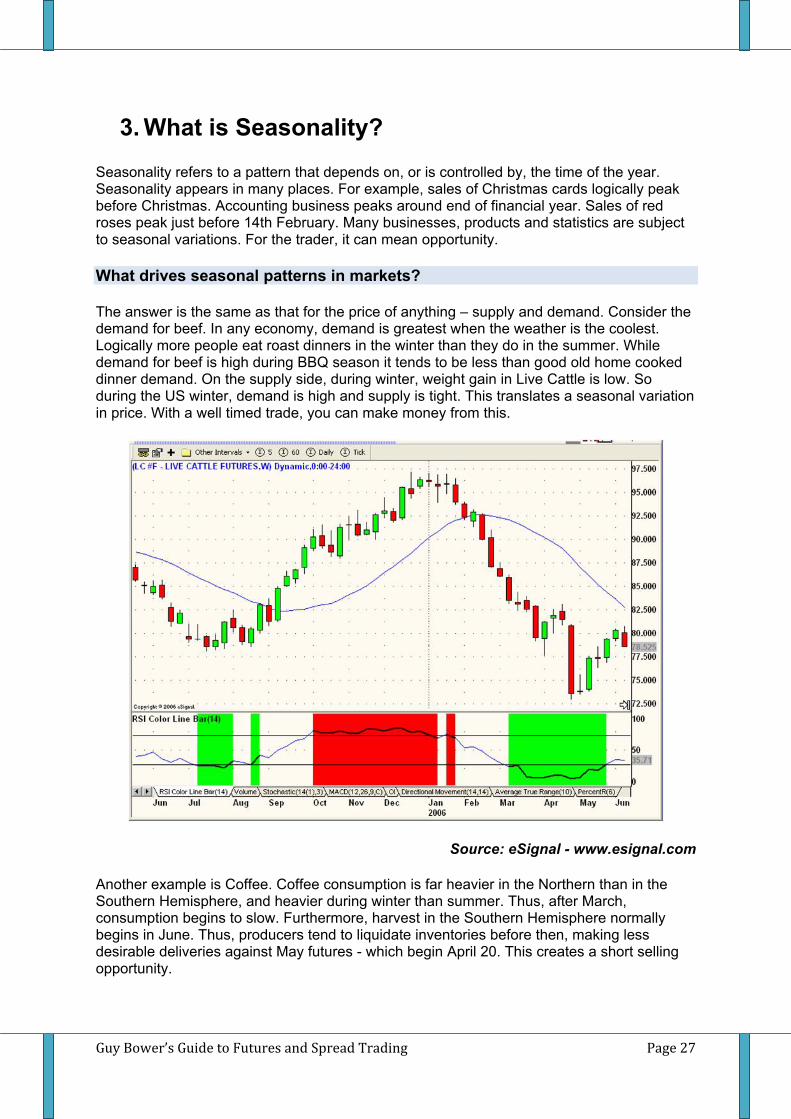

The answer is the same as that for the price of anything – supply and demand. Consider the demand for beef. In any economy, demand is greatest when the weather is the coolest. Logically more people eat roast dinners in the winter than they do in the summer. While demand for beef is high during BBQ season it tends to be less than good old home cooked dinner demand. On the supply side, during winter, weight gain in Live Cattle is low. So during the US winter, demand is high and supply is tight. This translates a seasonal variation in price. With a well timed trade, you can make money from this.

Source: eSignal - www.esignal.com

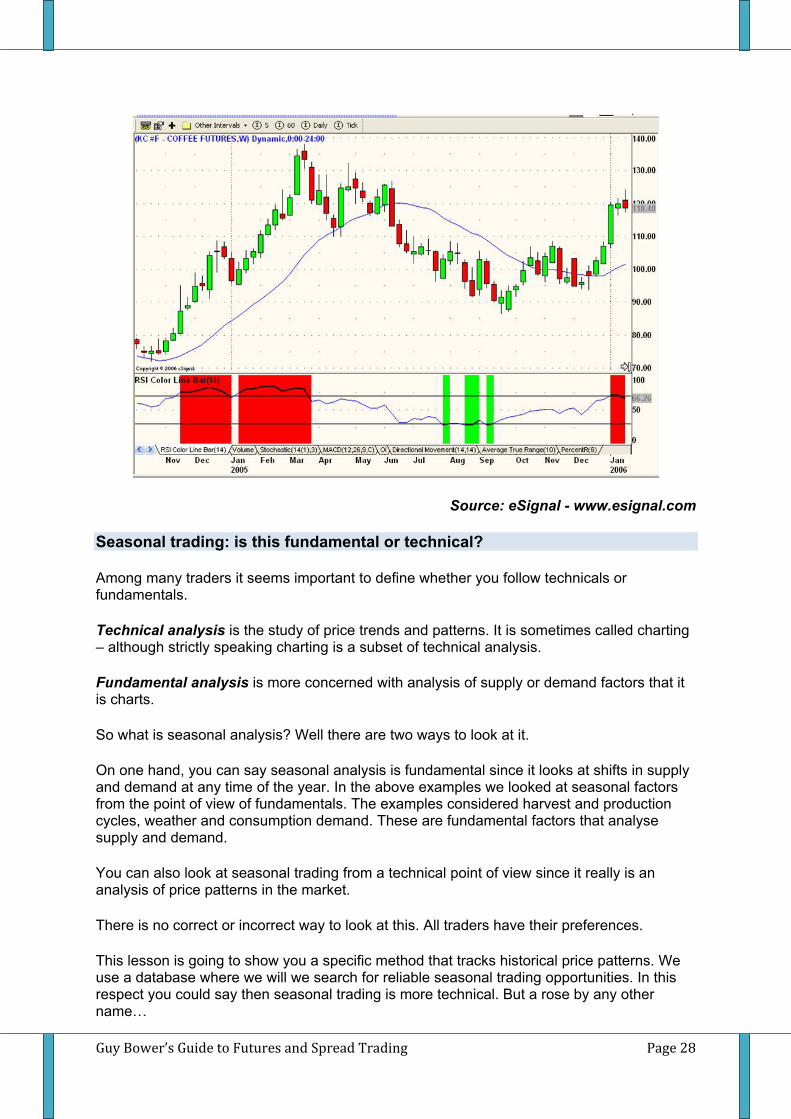

Another example is Coffee. Coffee consumption is far heavier in the Northern than in the Southern Hemisphere, and heavier during winter than summer. Thus, after March, consumption begins to slow. Furthermore, harvest in the Southern Hemisphere normally begins in June. Thus, producers tend to liquidate inventories before then, making less desirable deliveries against May futures - which begin April 20. This creates a short selling opportunity.

Guy Bower’s Guide to Futures and Spread Trading Page 28

Source: eSignal - www.esignal.com

Seasonal trading: is this fundamental or technical?

Among many traders it seems important to define whether you follow technicals or fundamentals.

Technical analysis is the study of price trends and patterns. It is sometimes called charting – although strictly speaking charting is a subset of technical analysis.

Fundamental analysis is more concerned with analysis of supply or demand factors that it is charts.

So what is seasonal analysis? Well there are two ways to look at it.

On one hand, you can say seasonal analysis is fundamental since it looks at shifts in supply and demand at any time of the year. In the above examples we looked at seasonal factors from the point of view of fundamentals. The examples considered harvest and production cycles, weather and consumption demand. These are fundamental factors that analyse supply and demand.

You can also look at seasonal trading from a technical point of view since it really is an analysis of price patterns in the market.

There is no correct or incorrect way to look at this. All traders have their preferences.

This lesson is going to show you a specific method that tracks historical price patterns. We use a database where we will we search for reliable seasonal trading opportunities. In this respect you could say then seasonal trading is more technical. But a rose by any other name…

Guy Bower’s Guide to Futures and Spread Trading Page 29

What we have covered so far:

• We have defined futures contracts. We know what long and short is. • We put long and short together and defined spread trading. • We showed some examples of seasonal analysis.

Step by step this lesson is taking you through to a specific trading method. The nuts and bolts are in the regular updates – and they are designed so you learn as you go along. The next article will look at how the updates are structured and help get you going.

Guy Bower’s Guide to Futures and Spread Trading Page 30

Seasonality Quiz OK, here are some more questions. The goal here is to have you start thinking about what might be seasonal and what is not. That’s all.

21. What is seasonality?

A. It is a pattern that depends on, or is controlled by, the time of the year.

B. It is the same as spread trading.

C. It is Christmas.

D. It is a type of trading where you make money as the seasons change.

22. Seasonal analysis is:

A. A type of technical analysis.

B. A type of fundamental analysis.

C. It is both technical and fundamental analysis.

D. Too hard to generalize into the above categories

Q23-Q30. Do you think the following scenarios are “seasonal”?

Q23. Yes/ No – Mid-year maturing and harvest time for US grain crops.

Q24. Yes/ No – In the US, April tax payments see a drop in bank deposits. This creates a strain on bank liquidity and puts pressure on interest rates in preceding months as banks compete for funds.

Q25. Yes/ No – Mid-year Coffee harvest in Brazil.

Q26. Yes/ No – In the Gulf of Mexico, hurricane season causing oil refinery shut down and transportation difficulties.

Q27. Yes/ No – January harvest time for Wheat crops in Australia.

Q28. Yes/ No – Hot summer months seeing a pick-up in energy (Natural Gas) demand given an increase in use of air conditioners.

Q29. Yes/ No – Cold winter months seeing a pick-up in energy demand (Heating Oil) given usage of heaters.

Q30. Yes/ No – October harvest of Cocoa in Africa.

Guy Bower’s Guide to Futures and Spread Trading Page 31

Answers – Q21 through Q30

Q21. The answer is A. It is simply a pattern that depends on, or is controlled by, the time of the year. It is NOT the same as spread trade. Seasonal analysis can be used to help select trades, spreads or otherwise.

Q22. Well this is bit of a trick question. The real answer is seasonal analysis can be viewed as a type of technical analysis or a type of fundamental analysis or combination of both. The answer in this case is D. That is, seasonal analysis is sometimes technical analysis. Other times it is based off fundamental analysis. Other times it is a combination of both.

There is no need to get too caught up with definitions here. We just need to understand the concepts.

Answers for Q23-Q30 The answers to all these questions is YES. All of these factors are seasonal in nature and they create some really interesting trading opportunities.

So do you need to know all this stuff to start trading? NO. That’s what the ProTrader Digest does. It actually takes years and years to learn this information and in a way, you never stop learning.

The ProTrader Digest however is designed to make it easy. We sift through all the data and present attractive seasonal trading ideas based on everything we have discussed here. Everything is spelt out, so it’s easy to understand.

Guy Bower’s Guide to Futures and Spread Trading Page 32

4. Putting it all together OK, in the previous lessons we defined introduced the concept of futures trading. We first looked at the basics of futures contracts. We covered definitions and examples of gong long and going short.

Definitions: Futures contract: A legally binding agreement to buy or sell a specified amount of a commodity or financial instrument at a fixed price sometime in the future.

Go long: To buy an asset in expectation of it increasing in value.

Go short: To sell an asset without first owning it with the expectation of it decreasing in value.

In the second lesson, we introduced the concept of a spread. A spread is simply the combination of a long and a short position, spread across different expiry months or related contracts. In this lesson we spoke about going long one contract and short another simultaneously. A spread trade is all about making money from the relative change in prices.

Definitions: Intra-commodity spreads This is where you buy one delivery month and sell another in the same commodity (e.g. simultaneously buy August Soybeans and sell November Soybeans). These are also called "calendar" or "time" spreads for obvious reasons.

Inter-market spreads There are also inter-commodity spreads where you buy one commodity and sell a related commodity (e.g. buy December Live Cattle, sell December Lean Hogs).

Sometimes it is easy to confuse the terms inter and intra. Don't worry about this so much. It's more important that you know the basic ideas. Both types of spreads simply try to make money from the change in relative prices of the contracts.

In the third lesson we introduced the concept of seasonal analysis.

Definition: Seasonality refers to a pattern that depends on, or is controlled by, the time of the year.

Seasonality appears in many places. For example, sales of Christmas cards logically peak before Christmas. Accounting business peaks around end of financial year. Sales of red roses peak just before 14th February. Many businesses, products and statistics are subject to seasonal variations. For the trader, it can mean opportunity.

Guy Bower’s Guide to Futures and Spread Trading Page 33

How my ‘ProTrader Digest’ newsletter does it

So what now? The ProTrader Digest site specializes in spread trading. I look at both futures and options markets, although there is a focus more on futures.

So in this eLesson, we'll take a look at the approach to new trading ideas. The ProTrader site posts new trading ideas to the section titles "New Trades".

Generally speaking there are 3-6 new trades trading ideas posted per month. Next is a sample of a NEW TRADE as posted on the ProTrader Digest site. We have added comments on how to interpret each section.

Guy Bower’s Guide to Futures and Spread Trading Page 34

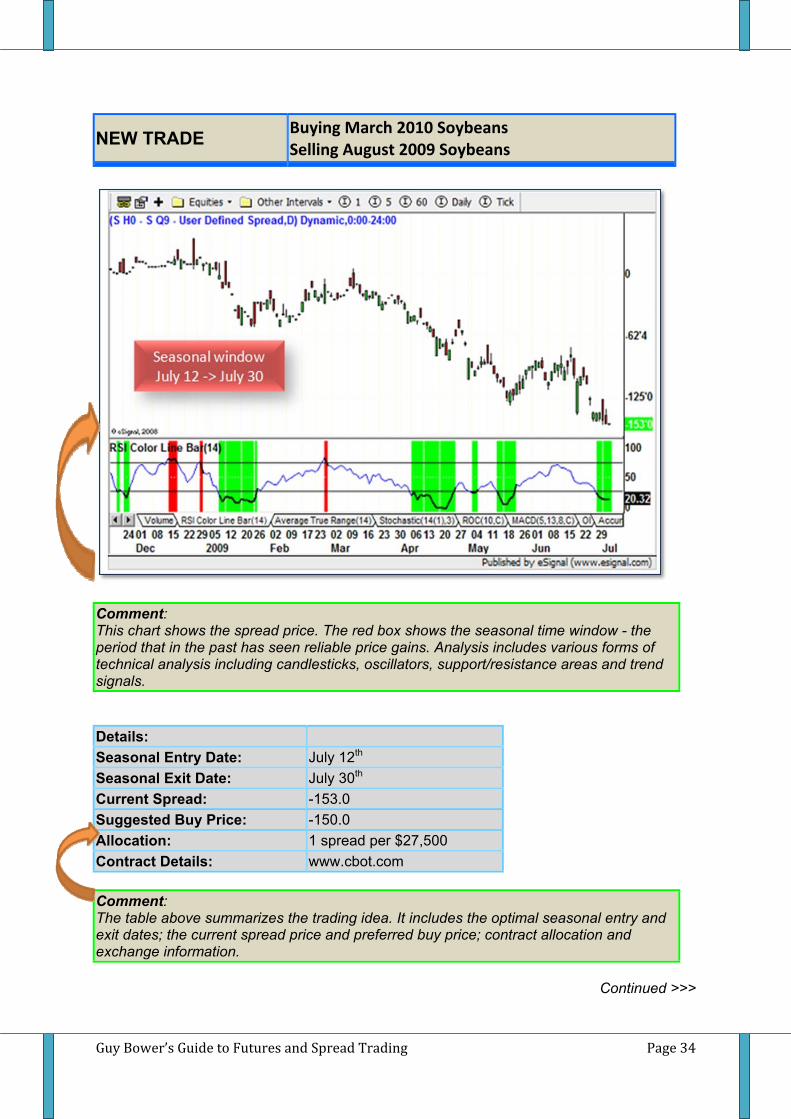

NEW TRADE Buying March 2010 Soybeans Selling August 2009 Soybeans

Details: Seasonal Entry Date: July 12th Seasonal Exit Date: July 30th Current Spread: -153.0 Suggested Buy Price: -150.0 Allocation: 1 spread per $27,500 Contract Details: www.cbot.com Comment: The table above summarizes the trading idea. It includes the optimal seasonal entry and exit dates; the current spread price and preferred buy price; contract allocation and exchange information.

Continued >>>

Comment: This chart shows the spread price. The red box shows the seasonal time window - the period that in the past has seen reliable price gains. Analysis includes various forms of technical analysis including candlesticks, oscillators, support/resistance areas and trend signals.

Guy Bower’s Guide to Futures and Spread Trading Page 35

Commentary This one is just as much a technical trade as it is a seasonal one. On the technical front this spread was near parity just three months ago. From March through May, it fell by around 125pts and the last couple of weeks has extended that loss by another 25pts or so. Looking at the charts, naturally oscillators such as RSI and Slow Stochs are oversold, but we still have trend signals pointing lower. With those details alone, you'd say the signals are mixed. However, we are looking at a spread. With spreads, oscillator signals tend to work a little better than trend signals, particularly after large or extreme moves. So this trade is a bet that the spread is oversold and has the potential to bounce. As far as seasonal data goes, there is a strong pattern that runs from mid July until the end. In early to mid-July, the market does not know what the new crop will bring. As such, there seems to be a premium built into the nearer month, perhaps a 'just in case' premium. As we move into late July however, better estimates on new crop emerge and the market transfers its focus to the more deferred contracts (new crop contracts). The bottom line is the August contract tends to suffer versus the deferred contracts including March2010. As such buying the March and selling the August contracts has proven to be a reliable strategy.

Comment: The “Commentary” details the reasoning behind the trading idea. We look at seasonal factors, fundamental factors and technical factors relevant to the trade. Historical performance This trade has been profitable 15 times in the last 15 years – a success rate of 100%. Over this time, the trade has averaged a profit of around $1,200 per contract spread.

Comment: Here we show the historical performance of the trading idea. Generally speaking, all trades have a very high probability of success. Order placement "Buy X March and sell August Soybeans at 150 or wider." X = contract allocation. Optimal contract allocation is one spread per $27,500.

Comment: This section shows how you would place an order with a broker and how much to trade based on certain risk parameters. Risk This spread is volatile right now, so there is a wider dollar stop that usual. However there is a larger allocation level to compensate. Recommended stop loss is 27pts ($1350us) below entry.

Comment: This section suggests stop loss price based on closing prices.

Guy Bower’s Guide to Futures and Spread Trading Page 36

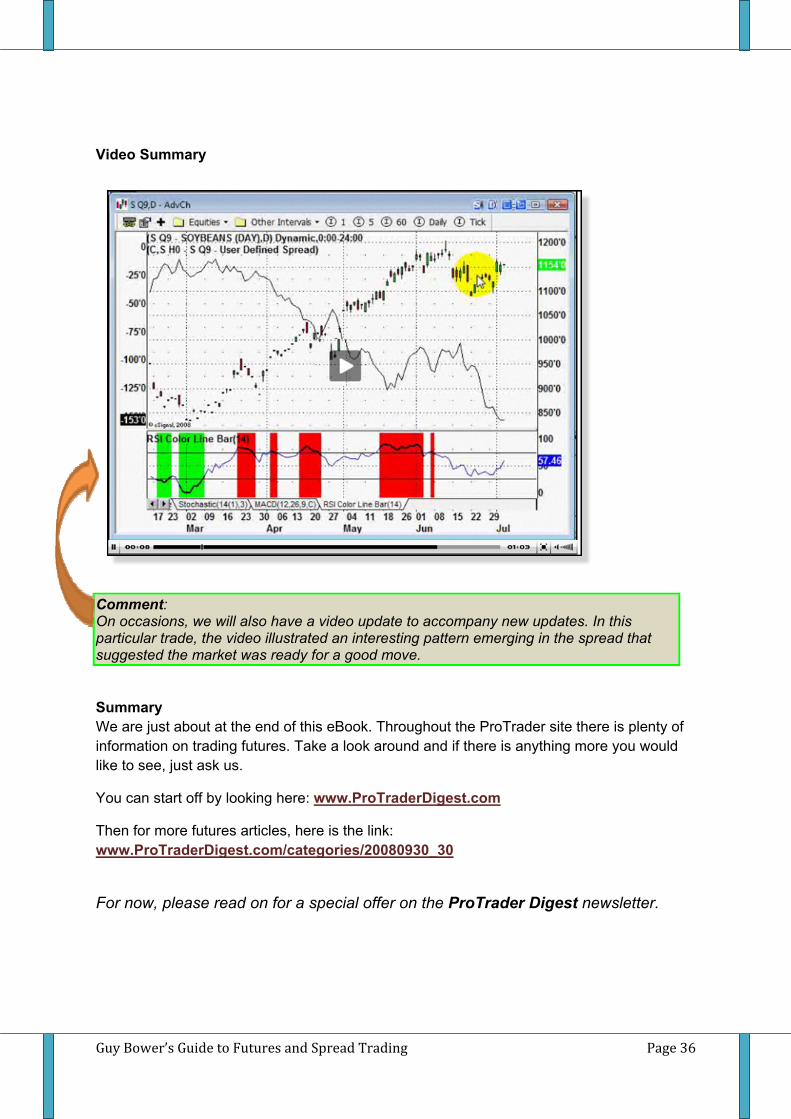

Video Summary

Comment: On occasions, we will also have a video update to accompany new updates. In this particular trade, the video illustrated an interesting pattern emerging in the spread that suggested the market was ready for a good move.

Summary We are just about at the end of this eBook. Throughout the ProTrader site there is plenty of information on trading futures. Take a look around and if there is anything more you would like to see, just ask us.

You can start off by looking here: www.ProTraderDigest.com

Then for more futures articles, here is the link: www.ProTraderDigest.com/categories/20080930_30

For now, please read on for a special offer on the ProTrader Digest newsletter.

Guy Bower’s Guide to Futures and Spread Trading Page 37

5. ProTrader Digest offer So what does the ProTrader Digest do?

The internet is full of people selling get rich quick systems, trading robots and other nonsense. I am not about to join those ranks. My goal is not to compete in a market where people are sold empty promises and silly claims.

I offer a trade education service that:

has a track record. While the world crumbled in 2008, seasonal spread trading showed fantastic results.

is written by a proven trader, author and educator with real world credibility. I have been there and done that: made money, lost money, learnt the ropes.

is completely transparent. I do not take your money and tell you about the returns later. I give you the trade signals and you make the decision to trade. It gives you the power, not some financial adviser.

has no management fees, no performance fees and no huge joining fees. All you pay is a monthly subscription fee – and you can cancel any time you want. No contracts!

100% satisfaction guarantee. There are no subscription contracts. You can cancel at any time and have no more to pay. Plus if you are not happy within the first 60days, I’ll refund every cent you’ve paid.

For readers of this eBook, I am offering a 10% discount on the monthly subscription rate of us$199/month. To take up this offer, go to www.ProTraderDigest.com and when prompted type in the code: “ebook”. This offer will be available for a limited time.

It’s that easy. However if you have more questions, please email at the address below. Best regards and good trading!

Guy Bower [email protected]

Guy Bower’s Guide to Futures and Spread Trading Page 38

6. Futures and Options Glossary

Adapted from my book Options: A Complete Guide for Investors and Traders

Ask volatility: The level of implied volatility such that the fair value of an option equals the ask price.

Arbitrage: A strategy involving the purchase of one position and the sale of a similar position to profit from a pricing difference. A market maker will regularly trade arbitrage strategies.

Arbitrageur: One who trades in arbitrage strategies.

Back month: Refers to options/futures with distant expiries (as opposed to front or near month). A calendar spread involves buying (selling) the front month and selling (buying) the back month.

Bear: (Or bearish) depicts a negative view on the market. For example, ‘I am bearish' is the same as saying ‘I think the market is will fall'. Opposite of bull.

Bear call spread: This is a type of vertical spread (that is both options have the same expiry). It involves selling one call strike and buying a higher call strike. The trade is placed at a credit and therefore also comes under the heading of a credit spread.

Bear put spread: This is a type of vertical spread (that is both options have the same expiry). It involves buying one put strike and selling a lower put strike. The trade is placed at a debit and therefore also comes under the heading of a debit spread.

Bid: The price at which someone is willing to buy an option.

Bid and asked: The most common way a price for an option is quoted. This is the highest bid price and the lowest ask price. For example, ‘the May 750 call is currently 50/55'. This means the highest bid is 50 and the lowest offer is 55.

Bid-asked spread: The difference between the highest bid price and the lowest ask price.

Bid up: When demand pushes the price for an asset higher it is said to be ‘bid up'.

Breakeven: In options, this normally refers to the price of the underlying market at which an options strategy will not lose and not gain. For example, the breakeven price at expiry for a $100 call purchased for $10 is $110.

Breakout: Generally refers to a movement in the underlying market where the price moves higher or lower (that is does not stay the same). Trades such as long straddles and strangles benefit from breakouts.

Guy Bower’s Guide to Futures and Spread Trading Page 39

Broker: A company that is licensed to transact in (option) markets. Quite often the term broker is also applied to the individual adviser or representative of the broking company. Strictly speaking, however, this is not correct.

Bull: (Or bullish) depicts a positive view on the market. For example ‘I am bullish' is the same as saying ‘I think the market is will increase'. Opposite of bear.

Bull put spread: This is a type of vertical spread (that is both options have the same expiry). It involves buying one put strike and selling a higher put strike. The trade is placed at a credit and therefore also comes under the heading of a credit spread.

Butterfly spread: A combination of a long (short) strangle and a short (long) straddle.

Bid volatility: The level of implied volatility such that the fair value of an option equals the bid price.

Calendar spread: A strategy that involves buying (selling) a call (put) with one expiry and selling (buying) another call (put) is a different month.

Call option: A contract that gives the buyer the right to buy the underlying asset within a certain amount of time as a specified priced.

Call premium: The price paid or received for a call option.

Close: The last traded price for a share, futures contract or options contract in a trading session. Most often for options an official settlement price will be quoted as the close since the last traded price may not be up to date.

Closing purchase: This involves buying back a short position in order to exit the position.

Closing sale: This involves selling a long position in order to exit the position.

Commission: The fee paid to the broker for transacting.

Condor: A strategy involving a long (short) strangle at certain strike prices with a short (long) strangle with a wider strike price interval.

Covered call: A strategy involving a long position in the underlying (for example, shares) and a short position in call options.

Covered put: A strategy involving a short position in the underlying (for example, futures) and a short position in put options.

Credit spread: A strategy involving a spread that is placed at a net credit or inflow of funds.

Debit spread: A strategy involving a spread that is placed at a net debit or outflow of funds.

Deep-in-the-money: Refers to an option that has a large intrinsic value. A deep-in-the-money option will have little time value and a very high delta.

Delta: The rate of change in the option premium given a change in the underlying.

Guy Bower’s Guide to Futures and Spread Trading Page 40

Delta neutral: A position where the total delta is zero or near zero. In other words, the position will not lose or gain given a small change in the underlying.

Delta position: The delta for a total position (a position with more than one option). This is calculated simply by adding up the deltas for an individual position.

Discount brokers: A broker than offers execution only (no advice).

Downside: A fall in the market or a reference to the risk in a position.

Equity option: Referring to an option on a parcel of equities.

ETO: Abbreviation of exchange traded option and refers to any option that is made available for trading on a recognized exchange.

European style option: An option that can be exercised at expiry only.

Exchange: The organisation that makes options/futures/shares available for trading.

Execution: A transaction in the market.

Exercise: The conversion of the option into a long or short position in the underlying asset.

Exercise price: The price at which as option can be exercised. Also called strike price.

Expiration cycle: Refers to the frequency of option expiries made available by an exchange. Some options and futures have what is called a quarterly expiration cycle. This means the options expire in March, June, September and December,

Expiration date: The day on which trading for an option ceases. Not all options have the same expiration date, so it pays to check this out before trading.

Fair value: A value for an option that is produced by using an option pricing model such as the Black-Scholes Option Pricing Model.

Fill: An executed order.

Front month: Refers to options/futures with the nearest expiry (as opposed to back). A calendar spread involves buying (selling) the front month and selling (buying) the back month.

Fundamental analysis: A method of analysis that studies supply and demand factors.

Futures contract: An agreement to purchase or sell a given asset at a specific time in the future at a specific price. Future contracts are traded on recognized exchanges with standardized features and transferable ownership.

Gamma: The rate of change in the delta given a move in the market.

Go long: To buy an asset in expectation of it increasing in value.

Guy Bower’s Guide to Futures and Spread Trading Page 41

Go short: To sell an asset without first owning it with the expectation of it decreasing in value.

Illiquid market: A market in which there is little volume traded.

Index options: Option based on a stock index such at the S&P100.

In-the-money: An option that has intrinsic value.

Leg: One part of a multi option strategy. For example, a bull call spread has two legs-a long call and a short call.

Limit move: Some futures contracts have a maximum daily change allowed by the exchange. Once the market price reaches this maximum amount or limit, all trading ceases. A limit move is where the market trades to that maximum level.

Liquidity: Refers to the degree of volume traded in a market. The more volume a market trades, the more liquid it is.

Long: A bought position in an asset with the expectation that the price will increase.

Make a market: To offer a bid and ask price in a market. This is the job of a market maker.

Margin: The deposit required to trading in futures and futures options.

Margin call: A request for more funds after an open position loses money.

Mark-to-market: The process where the profit or loss from a futures or futures option position is accounted for at the end of each day. Profits are credited to your account and losses are debited.

Market maker: One who regularly offers both buy and sell prices in the market. By offering both a buy price and a sell price, he/she ‘makes a market'. Market makers are normally professionally recognized participants in the market.

Market value: The most recent value for an asset.

Naked position: Usually referring to an outright short position (such as a short call or a short put) without any related hedge or spread component.

Narrowing the spread: This will either refer to the spread between two options (or futures) prices or the spread between the bid and offer prices. The concept of narrowing means a decrease in the absolute value of a spread. For example, ‘the spread between the March and June 2000 calls has narrowed from 50pts to 45pts'.

Near-the-money: An option with a strike price that is close to being at-the-money

OEX: The name and code for the S&P100 index options as traded on the CBOE.

Offer: The lowest price at which someone is willing to sell. Also known as ‘ask'.

Guy Bower’s Guide to Futures and Spread Trading Page 42

Opening transaction: A transaction in which the intention is to create or increase a position in a given series of options. Opposite of closing transaction.

Open interest: The total number of option contracts that exist in the market. The term also applies to futures contracts.

Option holder: One who is long an option.

Option writer: One who is short an option.

Out-of-the-money: An option with no intrinsic value.

Premium: The price paid or payable for an option.

Put option: A contract that gives the buyer the right to sell the underlying asset within a certain amount of time at a specified priced.

Quote: The current price of an option, normally given as both the bid and ask prices. For example, a quote for the March 1500 call might be 40/50-meaning 40 bid and 50 offered. Most brokers will say something like ‘40 bid, 50 offered', or, more simply, ‘40,50'.

Ratio backspread: The opposite of a regular ration call or put spread. That is you sell a call (put) then buy two or more calls (puts).

Ratio call spread: A strategy where you buy a near-the-money call and sell two or more further out-of-the-money calls.

Ratio put spread: A strategy where you buy a near-the-money put and sell two or more further out-of-the-money puts.

Short: To sell an asset without first owning it with the intention of profiting from a fall in the value of that asset.

Spread: This refers to the difference between two options (or futures) prices or the spread between the bid and offer prices.

Straddle: A strategy involving the purchase or sale of a call and put at the same strike price with the same expiry.

Stop-loss: The point at which a losing position is closed or is to be closed.

Strangle: A strategy involving the sale of a call and put at different strike prices with the same expiry.

Strike price (exercise price): The price of the underlying at which an option can be bought or sold when exercised.

Style: Refers to the expiration style of an option-American or European.

Synthetic long call: A combination of a long put and long underlying.

Synthetic long put: A combination of long call and short underlying.

Guy Bower’s Guide to Futures and Spread Trading Page 43

Synthetic long underlying: A combination of a long call and a short put with the same expiry and strike price.

Synthetic short call: A combination of short put and short underlying.

Synthetic short put: A combination of short call and long underlying.

Synthetic short underlying: A combination of short call and long put.

Technical analysis: Market analysis involving the study of past data such as charts patterns and moving averages.

Theoretical value: The value of an option that is calculated using an option pricing model. Also called fair value.

Theta: The chance in the option premium given the passing of one day.

Tick: The smallest possible movement in an asset.

Time decay: The erosion of time premium given the passing of time.

Time premium: The value of an option excluding intrinsic value. All options will have some theoretical or actual time value given a certain time to expiration. Time value is at its greatest for options at-the-money and options with a longer time to expiry.

Time value: The value of the option premium excluding intrinsic value. Also, but rarely, called extrinsic value.

Trigger point: The point in the underlying market where you would act to either close or adjust a position.

Triple witching day: A day where there are expirations in three different futures/options contracts. The third Friday of every quarterly month (March, June, Sep, Dec) has the expiries of index options and index futures and index futures options. Just recently this has come to be known as ‘quadruple witching' since the recently introduced single stock futures also expire on the 3rd Friday.

Type: Call or put.

Uncovered option: An unhedged option position.

Vega: The change in the option premium given a change in interest rates (cost of carry).

Volatility: The degree of variability in an asset. This is measured using past data or estimated/implied using option prices and other information.

Volatility skew: Compares implied volatility across different strike prices (either puts or calls with the same expiry month). 99.9% of the time, these volatilities will not be the same and therefore the range of volatilities are skewed in one direction or the other.

Guy Bower’s Guide to Futures and Spread Trading Page 44

7. ProTrader Digest offer OK, so this is reprinted from an earlier page, but you cannot blame a ‘Guy’ for trying.

So what does the ProTrader Digest do?

The internet is full of people selling get rich quick systems, trading robots and other nonsense. I am not about to join those ranks. My goal is not to compete in a market where people are sold empty promises and silly claims.

I offer a trade education service that:

has a track record. While the world crumbled in 2008, seasonal spread trading showed fantastic results.

is written by a proven trader, author and educator with real world credibility. I have been there and done that. Made money, lost money, learnt the ropes.

is completely transparent. I do not take your money and tell you about the returns later. I give you the trade signals and you make the decision to trade. It gives you the power, not some financial adviser.

has no management fees, no performance fees and no huge joining fees. All you pay is a monthly subscription fee – and you can cancel any time you want. No contracts!

100% satisfaction guarantee. There are no subscription contracts. You can cancel at any time and have no more to pay. Plus if you are not happy within the first 60days, I’ll refund every cent you’ve paid.

For readers of this eBook, I am offering a 10% discount on the monthly subscription rate of us$199/month. To take up this offer, go to www.ProTraderDigest.com and when prompted type in the code: “ebook”. This offer is limited.

It’s that easy. However if you have more questions, please email at the address below. Best regards and good trading!

Guy Bower [email protected]

Guy Bower’s Guide to Futures 54 egaP gnidarT daerpS dna

Disclaimer

© Copyright 2009 Guy Bower. All Rights Reserved. ProTrader LLC. 244 5th Avenue #2741. New York, NY 10001

THIS MATERIAL IS CONVEYED AS A SOLICITATION FOR ENTERING INTO A DERIVATIVES TRANSACTION.

THIS MATERIAL HAS BEEN PREPARED BY A DANIELS TRADING BROKER WHO PROVIDES RESEARCH MARKET COMMENTARY AND TRADE RECOMMENDATIONS AS PART OF HIS OR HER SOLICITATION FOR ACCOUNTS AND SOLICITATION FOR TRADES. DANIELS TRADING, ITS PRINCIPALS, BROKERS AND EMPLOYEES MAY TRADE IN DERIVATIVES FOR THEIR OWN ACCOUNTS OR FOR THE ACCOUNTS OF OTHERS. DUE TO VARIOUS FACTORS (SUCH AS RISK TOLERANCE, MARGIN REQUIREMENTS, TRADING OBJECTIVES, SHORT TERM VS. LONG TERM STRATEGIES, TECHNICAL VS. FUNDAMENTAL MARKET ANALYSIS, AND OTHER FACTORS) SUCH TRADING MAY RESULT IN THE INITIATION OR LIQUIDATION OF POSITIONS THAT ARE DIFFERENT FROM OR CONTRARY TO THE OPINIONS AND RECOMMENDATIONS CONTAINED THEREIN.

PAST PERFORMANCE IS NOT NECESSARILY INDICATIVE OF FUTURE PERFORMANCE. THE RISK OF LOSS IN TRADING FUTURES CONTRACTS OR COMMODITY OPTIONS CAN BE SUBSTANTIAL, AND THEREFORE INVESTORS SHOULD UNDERSTAND THE RISKS INVOLVED IN TAKING LEVERAGED POSITIONS AND MUST ASSUME RESPONSIBILITY FOR THE RISKS ASSOCIATED WITH SUCH INVESTMENTS AND FOR THEIR RESULTS.

YOU SHOULD CAREFULLY CONSIDER WHETHER SUCH TRADING IS SUITABLE FOR YOU IN LIGHT OF YOUR CIRCUMSTANCES AND FINANCIAL RESOURCES. YOU SHOULD READ THE “RISK DISCLOSURE” ACCESSED AT DANIELSTRADING.COM. DANIELS TRADING IS NOT AFFILIATED WITH NOR DOES IT ENDORSE ANY TRADING SYSTEM, NEWSLETTER OR SIMILAR SERVICE. DANIELS TRADING DOES NOT GUARANTEE OR VERIFY ANY PERFORMANCE CLAIMS MADE BY SUCH SYSTEMS OR SERVICES.

STRATEGIES USING COMBINATIONS OF POSITIONS, SUCH AS SPREAD AND STRADDLE POSITIONS MAY BE AS RISKY AS TAKING A SIMPLE LONG OR SHORT POSITION.