future opportunities for the upper hunter

TRANSCRIPT

Whither Upper Hunter?Alan Rai – Principal Economist

FUTURE OPPORTUNITIESAND THREATS• Focus on our competitive

advantages– Agriculture, tourism, equine, energy– Gas?

• Free-trade agreements (FTAs)– Significant opportunities for us – But also threat from foreign rivals

• Diversity in land use:– Conflicting and competing uses of land– Compare longer-run costs and benefits

of alternative uses of land

COMPETITIVE ADVANTAGESWHAT ARE THEY?

• Comparative advantages:– Energy (e.g. renewables)– ‘Agritourism’– Wine– Equine– Advanced manufacturing

• Where are our comparative disadvantages?– Unskilled, cheap labour

• Mass production• Standardised manufacturing

– Our high (labour) costs resemble Germans and Swiss• Yet they have a vibrant manufacturing sector. How?

ChAFTA AND OTHER FTAs

• Our skilled workforce employed in:– Health and Aged Care services– Advanced manufacturing (renewable energy,

medical equipment)

• Our arable land:– Agritourism, wine, equine

PLAY TO OUR STRENGTHS – BUT ALSO POSE THREATS

• FTAs also represent threats– ‘Low-value’ manufacturing

• We must focus on where we are most productive– Accelerates ‘servitisation’

of our industries

OUR DEMOGRAPHIC TRENDSENHANCE OUR ECONOMY’S ‘SERVITISATION’

0

10

20

30

40

50

0

10

20

30

40

50

1996 2006 2016 2026 1996 2006 2016 2026

Population share by age group

Sources: ABS Census of Population and Housing; NSW Dept of Planning and Investment

Hunter Balance Newcastle & Lake Macquarie

0-24

25-54

55-64

65+

ASIA’S DEMOGRAPHIC TRENDSFURTHER BOOST TO ‘SERVITISATION’

0

15

30

45

60

75

0

15

30

45

60

75

1950 1970 1990 2010 2030 1960 1980 2000 2020

Population share by age group

Source: United Nations World Population Prospects - 2012 Revision

China India

0-24

25-54

55-6465+

SOME COAL HARD FACTS

0

2

4

6

8

10

12

14

16

18

2012 2013 2014 2015 2016 2017 2018 2019 2020

Australian thermal coal exportsA$ billion

Sources: Department of Industry; HRF; Index Mundi

Falling export earnings despite surging tonnage

THERMAL COALCOOLING

• Coal industry: from investment to production– Latter 80% less labour intensive than former!– Lack of employment exacerbated by falling prices:

no incentive for new build

• Why are prices falling?– New supply coming online + lower demand

• (Global) oversupply will take time to reduce– Take-or-pay contracts is one barrier

• Why is demand falling?– Short- and longer-term trends– Longer-term: falling carbonised-energy intensity

LONGER-TERM ENERGY TRENDS

(1) Economic development + (2) climate concerns

ENERGY DEMAND TRENDS

0

0.1

0.2

0.3

0.4

0.5

0.6

0

0.1

0.2

0.3

0.4

0.5

0.6

1870 1890 1910 1930 1950 1970 1990 2010 2030

Energy intensity*

* Amount of oil (in tonnes) used to produce one unit of outputSource: BP

Europe

U.S.

China

NOT SO INTENSE

ELECTRICITY: WATT ABOUT IT?

• Renewable electricity generation– New generation is unprofitable (for now) due to low

demand– But longer-term ‘currents’ support renewables investment

• Longer-term currents– We all agree our manufacturing needs to be ‘advanced’– We all think more may be needed to limit global warming

• To keep the rise in global temperatures below 2-2.5 degrees

• An opportunity to invest in these trends– We have the resources in our own backyard to do this!

INVESTMENT‘SHOCKINGLY’ LOW

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Hunter Rest of NSW Hunter Rest of NSW Hunter Rest of NSW

Installed capacity (MW)

* Coal and gas-poweredSource: NSW Trade & Investment

Renewables

Fossilfuels*

Existing Approved Planning stage

RENEWABLESA POWERFUL SURGE

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030 2034

Renewables’ share of electricity generation (%)

Source: BP

Europe U.S.

China

LAND USE IN THE HUNTER BALANCEAs at July 2013

Agriculture(54%)

Conservation(2%)

Urban(14%)

Mining(31%)

Sources: Australian Bureau of Statistics; HRF

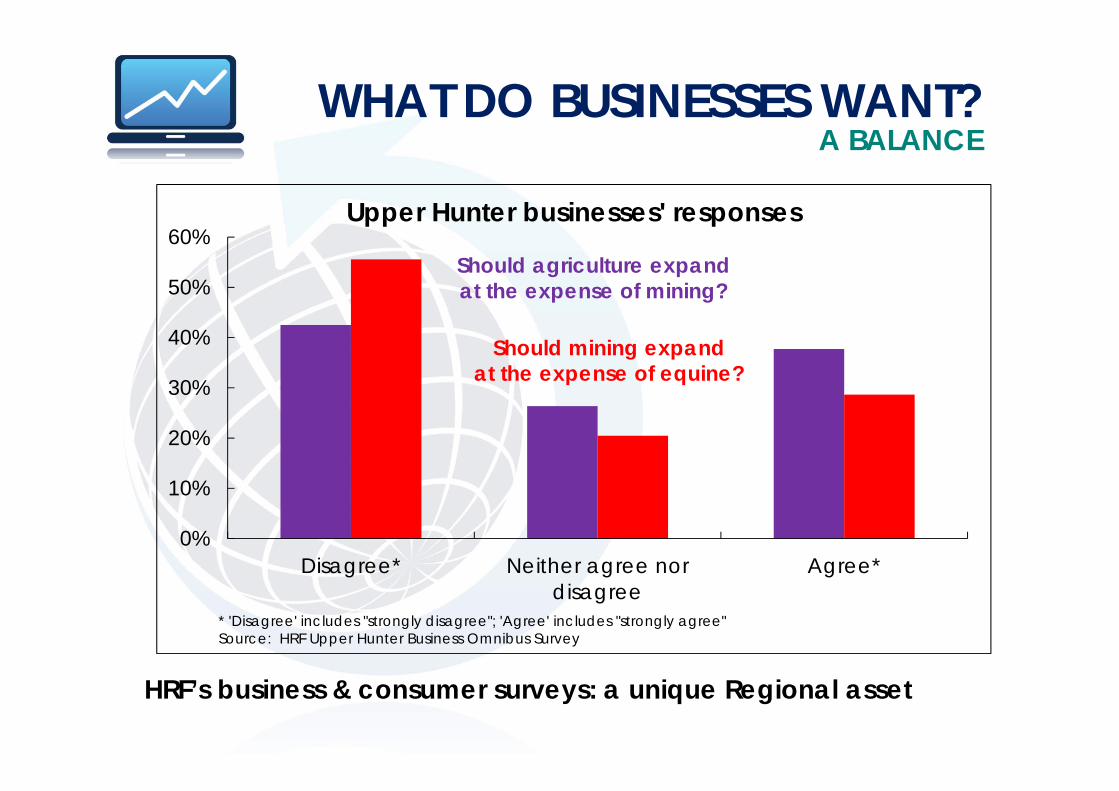

HRF’s business & consumer surveys: a unique Regional asset

WHAT DO BUSINESSES WANT?A BALANCE

0%

10%

20%

30%

40%

50%

60%

Disagree* Neither agree nordisagree

Agree*

Upper Hunter businesses' responses

* 'Disagree' includes "strongly disagree"; 'Agree' includes "strongly agree"Source: HRF Upper Hunter Business Omnibus Survey

Should agriculture expandat the expense of mining?

Should mining expandat the expense of equine?

LAND USE CLAIMS

• Conflicting, diverse land use claims– Mining, equine, wine, agritourism– How to compare & contrast these?

• Cost-benefit analysis over the life cycle– For each (genuine) proposed use of land– Cumulative impacts; include costs of remediation– Balance short-term benefits over longer-term costs– (Opportunity) cost of forgone alternatives

• Not easy to do….but is vitally important!

A BALANCE MUST BE STRUCK

• One-on-one, interviews of 54 Hunter manufacturers• 600+ senior researcher hours• 12 advisory group stakeholders

CARPE DIEM!NEEDS STRATEGIC THINKING

• HRF’s Manufacturing Our Future project– Example of HRF’s regional research capabilities– Q: what differentiates improving from declining

manufacturers?

• What is the recipe for success?– formal strategic business plans– hooked into global supply chains and networks– focused on design and other high-value segments of

the supply chain– are innovative (e.g. technology adoption; a focus on

‘servitisation’ and customisation)

• ‘Ingredients’ are not unique to manufacturers

Delivering insights that move the Hunter forward

Thank you