future of iran's oil and its economic implications · the future of iran’s oil and its...

TRANSCRIPT

The Future of Iran’s Oil and Its Economic Implications

Pooya Azadi *, Stanford University Hassan Dehghanpour, University of Alberta Mehran Sohrabi, Heriot-Watt University Kaveh Madani, Imperial College London

Working Paper #1 October 2016

Page 1

About the Stanford Iran 2040 Project

The Stanford Iran 2040 Project is an academic initiative that serves as a hub for researchers all around the world, particularly the Iranian diaspora scholars, to conduct research on economic and technical matters related to long-term development of Iran and evaluate their possible implications in a global context.

The project encourages quantitative and forward-looking research on a broad array of areas relating to Iran's economic development in the long run to envision the future of the country under plausible scenarios. The sectors that will be covered within the first phase of the project include economy, energy, water, environment, food and agriculture, and transport. The project has been co-sponsored by the Hamid and Christina Moghadam Program in Iranian Studies and the Freeman Spogli Institute for International Studies at Stanford.

Stanford Iran 2040 Project

Encina Hall East, Room E017 Stanford University Stanford, CA 94305-6055 www.iranian-studies.stanford.edu/iran2040

Disclaimer

The Stanford Iran 2040 Project is an academic initiative with the sole objective of promoting scientific collaboration in economic and technical areas related to long-term sustainable development of Iran. The project does not advocate or follow any political views or agenda. The contributors are selected solely based on their research skills and the center is not aware of, and not responsible for, the political views of the contributors and affiliates. Likewise, contributors and affiliates are not responsible for the political views of other contributors or affiliates.

Citation and Correspondence

Please cite this working paper as:

P. Azadi, H. Dehghanpour, M. Sohrabi, K. Madani, The Future of Iran’s Oil and Its Economic Implications, Working Paper 1, Stanford Iran 2040 Project, Stanford University, October 2016, https://purl.stanford.edu/mp473rm5524

To whom correspondence should be addressed:

Pooya Azadi, Stanford Iran 2040 Project, Email: [email protected]

Page 2

About the Authors

Pooya Azadi is leading the efforts at the Stanford Iran 2040 Project. He received his B.Eng in Chemical Engineering from the University of Tehran (B.Eng) and his M.A.Sc and PhD from the University of Toronto. Prior to joining Stanford, he worked as a researcher at the universities of Oxford, Cambridge, and MIT for several years. His research interests include energy and environmental sciences, economics, and advanced mathematical modeling.

Hassan Dehghanpour is an Assistant Professor in the Department of Civil and Environmental Engineering at the University of Alberta. His primary research interests include modeling of multiphase flow in porous media. He holds two BS degrees in mechanical and petroleum engineering from Sharif University of Technology, and an MS degree from the University of Alberta and a PhD degree from the University of Texas at Austin, both in petroleum engineering.

Mehran Sohrabi is a Professor of Enhanced Oil Recovery (EOR) in the Institute of Petroleum Engineering at Heriot-Watt University. He has a Bsc, an Msc, and a PhD in Reservoir Engineering and has more than 25 years of experience in various aspects of Reservoir Engineering in particular in the areas of Enhanced Oil Recovery and complex Multi-Phase Flow in Porous Media. Professor Sohrabi leads the Centre for Enhanced Oil Recovery and CO2 Solutions at Heriot-Watt University and is Principal Investigator of a number of joint industry projects (JIP) covering most aspects of EOR.

Kaveh Madani is a Reader in Systems Analysis and Policy at the Centre for Environmental Policy of the Imperial College London. His core research interests and experiences include integrated water, environmental, and energy resources engineering and management.

Page 3

Executive Summary

The unprecedented global support for policies to reduce carbon emissions along with the emergence of new technologies for extraction of oil from unconventional resources have made it increasingly unlikely that Iran’s oil reserves will ever be exhausted. As such, determining the real amounts of Iran’s oil endowments and reserves – which have long been a subject of controversy – is of little practical value now. Rather, focus should be devoted to assess the rate at which Iran can recover oil given its mature fields and underinvested infrastructure.

Herein, we present a field-by-field analysis of Iran’s crude oil production history and its future projections to 2040. A total of 98 oil fields and reservoirs with a cumulative production of 72 billion barrels since 1913 are considered. Future projections are made based upon the current status of active fields and their existing infrastructure, ongoing and announced projects, and potential production augmentations from undeveloped and undiscovered fields. We found the average annual decline rate of the existing Iranian oil fields (including the impact of maintenance) to be 6.0%, the average productivity of new wells in 2016 to be 1.7 kbbl/d with a year-over-year decline rate of 3.2%, and the average yield from gas injection to be 4.0 kbbl/mcm.

We also show that, in the most likely scenario, Iran’s crude oil production capacity will increase moderately over the coming decades to first reach 4.0 mmbbl/d before 2020, followed by a further increase to 4.4 mmbbl/d before 2030, which can potentially last until 2040 if future exploration and enhanced oil recovery projects are implemented successfully (Figure ES-1). Using the baseline crude price projections by the US Energy Information Administration (EIA), we project that the annual gross revenue of Iran’s crude oil (Figure ES-1) will reach its 2011/12 figure of about $150B (in constant 2016$) by the middle of the next decade.

Figure ES-1. Iran’s crude production in the recent past and its projections for the coming decades (left axis), and the gross revenue of total crude oil production in constant 2016 dollar (right axis). Dashed lines represent upper and lower bounds for Iran’s future oil revenue. NGL production and its corresponding revenue were not included.

Our analysis indicated that, until the middle of next decade, Iran can continue to compensate for the decline in production of its mature fields by exploiting its undeveloped reserves. However, major challenge will come into play from the middle of next decade where retaining the production level will only be possible through operation of many more wells, injection of increasing shares of the produced natural gas, use of artificial lift, and heavy investment in secondary and tertiary recovery practices. Despite the expected growth in gross revenue, the increasing production costs due to the abovementioned factors along with future rise in domestic energy consumption will prohibit considerable growth in oil export profit after 2025.

0

50

100

150

200

250

300

350

400

450

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2015 2020 2025 2030 2035 2040

Gro

ss R

even

ue (2

016$

B)

Prod

uctio

n (m

mbb

l/d)

Developed Greenfields EOR Undiscovered Revenue

Page 4

Introduction

Iran has one of the most diverse economies among the oil-exporting countries in the Middle East. Nevertheless, the oil revenue still constitutes approximately 30% of the government revenues and more than 20% of the real gross value added. Iran’s oil and gas industry is in acute need of technology and capital. To this end, the Iranian government plans to absorb $150-200 billion for its upstream sector within its 6th national five-year development plan by offering some 50 oil and gas projects to international oil companies and foreign investors. The investment in this sector thus far falls under “buyback” contracts which Iran introduced in 1989. Under such contracts, the project ownership reverts back to the National Iranian Oil Company (NIOC) after the development of the fields. To fix some of the issues with the buyback contracts, NIOC is trying to introduce the Iran Petroleum Contract (IPC) which is supposed to be more appealing to investors. One major obstacle against foreign investment in the Iranian oil sector is attributed to the fact that the Iranian constitution prohibits foreign ownership of natural resources. However, it has been announced that the new IPC models could potentially resolve this issue.

Besides the abovementioned challenges, new developments in the global energy market are also likely to have profound and lasting impact on Iran’s oil sector and its economy.

Growing concerns about climate change are translating into policies that will significantly reduce the carbon intensity of global economy and hence lower the attractiveness of fossil fuels in the long run [1]. Recent pledges made by individual countries [2] to limit the rise in global mean temperature by 2oC sets the world’s total remaining carbon budget to 1 trillion tonne, which, in turn, is expected to limit the annual growth rate of global oil demand to 0.6% through 2030 [3].

On the supply side, the shale revolution not only has boosted the global supply but also completely changed the global oil market dynamics. In rough terms, the production cost of the US shale oil lies broadly in the middle of global oil supply cost curve [1]. Development time for a shale project and the life of shale oil wells are substantially shorter than those of the conventional resources, implying that shale oil now acts as a new shock absorber along with OPEC.

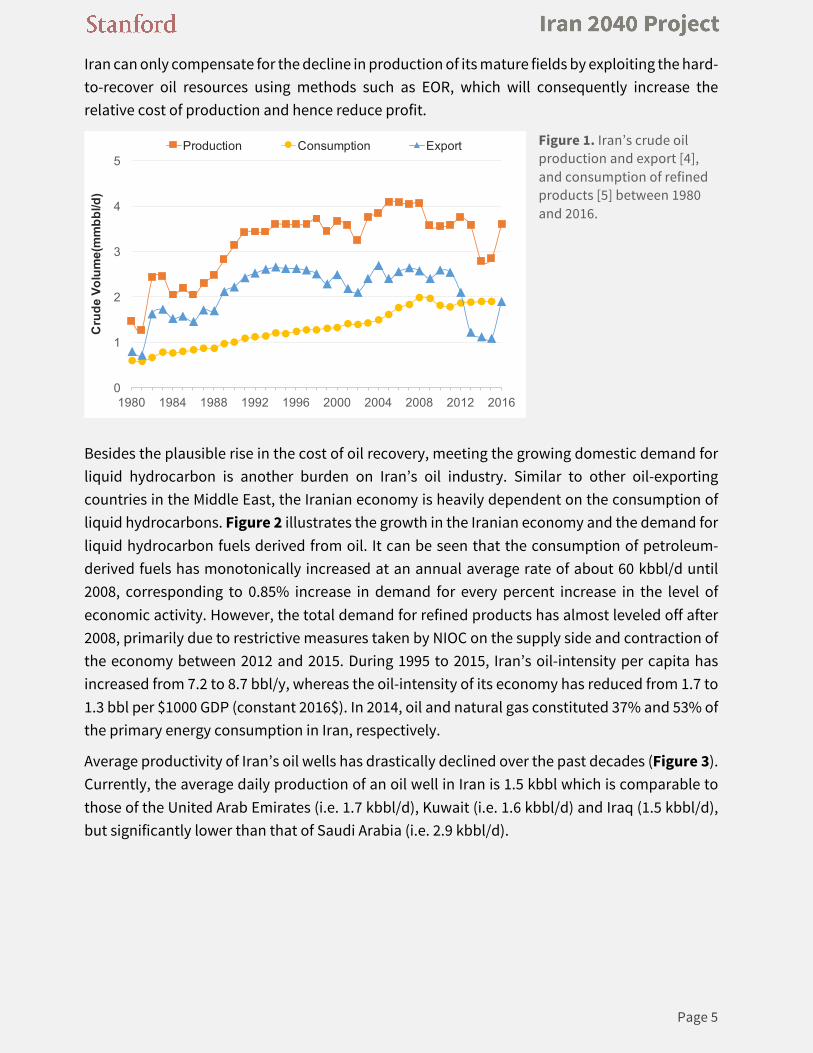

Figure 1 depicts Iran’s crude oil production, export, and consumption of refined products since 1980. Current sustainable capacity of Iran for extraction of the crude oil is estimated at 3.7 mmbbl/d. Over the past two decades, the production capacity of Iran has fluctuated over a relatively narrow range between 3.6 and 4.1 mmbbl/d. Iran’s oil export started short after the development of first oil fields and peaked at 5.5 mmbbl/d in the mid-1970s but collapsed to less than 1 mmbbl/d after the 1979 Revolution. Although the exports recovered later and stabilized at about 2.2 mmbbl/d, it declined again to less than 1 mmbbl/d following the implementation of international sanctions on Iran in 2011-2012.

With the average production cost of less than $10 per barrel, most of Iranian crude oil lies near the bottom of the global oil cost curve. However, as discussed later, in the medium to long term

Page 5

Iran can only compensate for the decline in production of its mature fields by exploiting the hard-to-recover oil resources using methods such as EOR, which will consequently increase the relative cost of production and hence reduce profit.

Figure 1. Iran’s crude oil production and export [4], and consumption of refined products [5] between 1980 and 2016.

Besides the plausible rise in the cost of oil recovery, meeting the growing domestic demand for liquid hydrocarbon is another burden on Iran’s oil industry. Similar to other oil-exporting countries in the Middle East, the Iranian economy is heavily dependent on the consumption of liquid hydrocarbons. Figure 2 illustrates the growth in the Iranian economy and the demand for liquid hydrocarbon fuels derived from oil. It can be seen that the consumption of petroleum-derived fuels has monotonically increased at an annual average rate of about 60 kbbl/d until 2008, corresponding to 0.85% increase in demand for every percent increase in the level of economic activity. However, the total demand for refined products has almost leveled off after 2008, primarily due to restrictive measures taken by NIOC on the supply side and contraction of the economy between 2012 and 2015. During 1995 to 2015, Iran’s oil-intensity per capita has increased from 7.2 to 8.7 bbl/y, whereas the oil-intensity of its economy has reduced from 1.7 to 1.3 bbl per $1000 GDP (constant 2016$). In 2014, oil and natural gas constituted 37% and 53% of the primary energy consumption in Iran, respectively.

Average productivity of Iran’s oil wells has drastically declined over the past decades (Figure 3). Currently, the average daily production of an oil well in Iran is 1.5 kbbl which is comparable to those of the United Arab Emirates (i.e. 1.7 kbbl/d), Kuwait (i.e. 1.6 kbbl/d) and Iraq (1.5 kbbl/d), but significantly lower than that of Saudi Arabia (i.e. 2.9 kbbl/d).

0

1

2

3

4

5

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016

Cru

de V

olum

e(m

mbb

l/d)

Production Consumption Export

Page 6

Figure 2. The real GDP (constant 2016$B) and demand for refined products (kbbl/d), both in log.

Figure 3. Number of producing oil wells (left axis) and the average well productivity (right axis). Data points between 2012 and 2015 do not reflect true well productivities as production was significantly lower than the capacity in that period.

Here, we first determine the values of the four most influential parameters on Iran’s crude production capacity. These parameters were the annual decline rate of the Iranian oil fields, temporal changes in the productivity of new wells, and the yield of the marginal crude that is produced by the injection of natural gas. We then present a bottom-up projection of Iran’s future crude production by estimating the future productions of individual oil fields and reservoirs. Furthermore, we use the predicted future production in conjunction with the EIA’s future oil price forecast to project the range of Iran’s future oil revenue. Finally, we demonstrate how the distribution of depletion level of Iran’s oil fields will change in the future and discuss its technical and economic implications.

5.0

5.5

6.0

6.5

7.0

7.5

8.0

5.0

5.5

6.0

6.5

7.0

7.5

8.0

1995 2000 2005 2010 2015

Refin

edProdu

ctsD

eman

d

Rea

l GD

P

Real GDP Refined Products Demand

0

1

2

3

4

5

0

500

1000

1500

2000

2500

1990 1995 2000 2005 2010 2015

Wel

l Pro

duct

ivity

(kbb

l/d)

Num

ber o

f Pro

duci

ng W

ells

Producing wells Average well productivity

Page 7

Methods The analysis presented here is solely based on the data available in the public domain, which was compiled and fed into two types of models as listed in Table 1. The production capacity surrogate model takes the initial capacity at t0 along with annual gas injection (Figure 4) and well drilling data (Figure 5) to reproduce the real-world annual production capacity in the future years (t>t0). The inputs to this model were compiled from the time series data published annually by both domestic and international organizations including OPEC [4], EIA [5], CBI [6], NIOC [7], and IEA [8]. The model has four free parameters, i.e. average decline rate of producing wells, average new well productivity at t0, year-over-year decline in average new well productivity, and marginal crude production yield from gas injection, which is defined as the total production minus the expected baseline production in the absence of gas injection. The values of these parameters were estimated using the least square regression to crude capacity data from 1991 to 2015. Subsequently, as explained below, the outputs were used in the second model to forecast future changes in the crude production capacity. In order to adjust for the average active time of a new well within its first year of production, only half of its nominal production rate was accounted in the calendar year in which the well was completed. The model was fitted to the production capacity data rather than the actual production values as the latter can be, and in fact has been, affected by exogenous factors not considered in the model such as international sanctions.

The field-specific model contains historical crude production data, original oil-in-place, ultimately recoverable resource (URR), depletion level, and crude API for each field (or in some cases, reservoir). URR is defined as the amount of crude that can be commercially produced from an oil field over its entire lifetime. Field depletion level is defined as the ratio of cumulative production of a field at a given time to its URR. A total of 98 oil fields and reservoirs with cumulative production of 72 billion barrels (BBL) between 1913 and 2016 were considered. The dataset was populated by individual values compiled from a large number (e.g. hundreds) of reports, papers, and news pages. Field-specific future projections were made based upon the past production history, depletion level, remaining recoverable resource (RRR) and the ongoing and announced projects for the respective field. Potential production augmentations from undeveloped and undiscovered fields have also been considered in the analysis. Future production from the large greenfields are based on their development plans. For undiscovered resources and greenfields with no publicly announced development plans, the plateau production rate was assumed to be equal to the rate at which the field becomes fully exhausted if production lasts at such rate for 30 years. The average lead time between the final investment decision and the first oil production is 5-6 years in Iran [9]. Therefore, it was assumed that a 10-year lag exists between the discovery date and the first oil production. We also assumed that in the period between now and 2030, reserve discovery will continue to occur at a constant rate of 500 mmbbl per annum. This would bring the sum of all reserve discoveries between 1995 and 2030 to 33 BBL (Figure 6), which is still 38% lower than the USGS estimated figure for Iran’s

Page 8

discoverable reserves (i.e. 53 BBL).

Table 1. The two models used in the analysis and their main inputs and outputs. Model Inputs Outputs Production capacity surrogate model

Initial production capacity, gas injection volume, and number of new oil wells

Average decline rate, new well productivity, year-over-year decline in new well productivity, and yield of additional oil recovery by gas injection

Field-specific model

Historical annual production rate, initial oil-in-place, ultimate reserve, crude API, future development plans and EOR, and estimates of future reserve discoveries and gas injection

Future production, depletion level change, and average API of Iranian crude

Figure 4. Historical data and future forecasts of annual gas injection and its previous targets (left axis), and cumulative (right axis) gas injection to Iranian crude reservoirs. Annual injection targets represent previous goals for gas injection for pressure maintenance in 24 declining Iranian oil fields [10]. These targets were set at different times based on NIOC’s forecasted natural gas balances.

It was also assumed that the gas injection rate will increase at a rate of 10 mcm per year. This would mean that the gas injection will reach 335 mcm/d in 2040 (Figure 4). This seemingly higher-than-usual growth is justified based on Iran’s ambitious plans for increasing its natural gas production in the next decades which would subsequently make more gas available for injection. According to the latest EIA projection[11], Iran can ramp up its marketable natural gas production from 500 mcm/d in 2015 to 1000 mcm/d in 2040, while NIOC plans to reach the 1000 mcm/d target as early as 2020. In addition to marketable and injected natural gas, Iran flared 30 mcm/d of its associated gas in 2015, which potentially can be reinjected in the oil reservoirs in the future. The development of natural gas distribution in Iran has recently reached a level where upwards of 90% of people currently have access to the natural gas for their residential uses and hence the demand growth rate in this sector is likely to decrease in the future. Also, Iran has considerably increased the share of natural gas in its fuel mix for power generation to avoid liquid consumption at power plants and, as a result, the future growth rate in this sector is also likely to decline. Although unprecedented, we believe that our assumption of an annual increase rate of 10 mcm/d for gas injection represents a realistic scenario. The current capacity of Iran’s

0

2

4

6

8

10

12

14

0

50

100

150

200

250

300

350

1980 1990 2000 2010 2020 2030 2040

Cum

ulat

ive

Inje

ctio

n (b

cm)

Gas

Inje

ctio

n (m

cm/d

)

Annual injection Target Cumulative injection

Page 9

gas injection infrastructure is estimated at 200 mcm/d.

Figure 5. Number of oil wells and total number of wells drilled (left axis), and number of active rigs (right axis).

Figure 6. Historical data (1998 – 2015) and future estimates of annual (left) and cumulative (right) reserve discovery.

Throughout this report, the production values exclusively represent crude oil and do not include other types of liquids such as NGL. Likewise, the resources and reserves reported here solely refer to those of crude oil. Also, it is worth noting that no explicit assumption was made for the number of new wells to be drilled in the time horizon of this study (i.e. 2016 to 2040) as it was indirectly accounted for through consideration of development projects. Gross revenues under different scenarios were calculated based on Brent future price forecasts by EIA [11] and adjusted based on the historical data over the past five years to account for the difference between the price of Brent and average price of the Iranian crude. No price discount was applied to the crude consumed domestically when calculating the gross revenue.

0

20

40

60

80

100

120

140

0

50

100

150

200

250

300

350

1990 1995 2000 2005 2010 2015

Act

ive

Rig

s

Wel

ls D

rille

d

All Wells Oil Wells Active Rigs

0

10

20

30

40

50

60

0

1

2

3

4

5

6

1995 2000 2005 2010 2015 2020 2025 2030

Cum

ulat

ive

Dis

cove

ry (B

BL)

Ann

ual D

isco

very

(BB

L/y)

Annual Discovery Cumulative Discovery

Page 10

Results and Discussion

In this section, we first present the results obtained from the surrogate model and discuss their implications for Iran’s future oil production. Subsequently, using the field-specific model described before, we show how Iran’s future crude production profile will likely evolve through 2040. We determine the shares of the currently producing fields, greenfields, EOR, and undiscovered fields in the future production mix.

Parameter estimation results obtained by fitting the described surrogate model to the crude production capacity data of the past 25 years are given in Table 2. The average model response error was 4%.

Table 2. Estimated values of parameters for Iran’s crude production capacity surrogate model. Parameter Value Unit Apparent decline rate 6.0 %/y Average productivity of new wells in 2016 1.7 kbbl/d Year-over-year decline in productivity of new wells 3.2 %/y

Average additional recovery by gas injection 4.0 kbbl/mcm We found that, the apparent (or observed) decline rate of the Iranian oil fields was 6.0% per year. We define the apparent decline rate as an aggregated change in crude production due to inherent decline of the fields (negative) and impact of maintenance activities and well workover (positive) – suggesting that the average inherent decline rate of the Iranian oil fields is certainly upwards of 6.0%. In other words, if the gas injection and well workover activities are kept at their current levels and no new well is brought into production, the production capacity would diminish at 6% per annum, which translates into 240 kbbl/d at the current production rate.

Other important parameters obtained from model fitting are the average productivity of new wells and the rate at which it changes over time. As drilling activities typically encompass both greenfield development and infill drilling in brownfields, productivities of new wells in these two types of fields serve as the de facto bounds for the average productivity of new wells drilled in each year. A review of new plans for the next round of field development projects reveals that the average (expected) production from a new well is approximately 1.9 kbbl/d, whereas the average productivity of all producing wells is currently equal to 1.5 kbbl/d (Figure 3). We found that the average production rate of a newly completed well in 2016 was equal to 1.7 kbbl/d (Table 2), which falls well within its plausible range of values as explained above.

The third parameter was introduced to capture the temporal changes in average productivity of new wells on a year-over-year basis. It was found that, in the timeframe between 1991 and 2016, the average productivity of new wells within the first year of their completion has dwindled from 3.8 to 1.7 kbbl/d – indicating a 3.2% annual decline rate.

The last parameter takes into account the yield of the marginal crude recovery through gas injection. Immiscible gas injection and its effectiveness for improved crude recovery from the

Page 11

Iranian oil fields is not a well-understood concept and a wide range of values has been reported, or simply assumed, for the yield of the marginal crude recovery by immiscible gas injection [10][12][13]. The ambiguity in the actual impact of immiscible gas injection is attributed to several factors such as the geological differences among the fields, field depletion levels, crude characteristics, and injection-to-production ratio. We estimated that the average amount of marginal crude produced via injection of natural gas into the Iranian oil fields to be 4.0 kbbl/mcm.

In the second part of our analysis, as outlined in the previous section, we employed a field-specific model, comprising annual production data and the resource and reserve data of all Iranian oil fields to project Iran’s future crude production capacity. We used parameters values obtained from the surrogate model along with the field-specific production history and future development plans to project future production of each field. The development plans considered herein were based on the ongoing projects, announced plans, and/or plausible scenarios for future development given the amount of reserve and the crude characteristics of each field.

Figure 7 shows our projections of Iran’s future crude production from existing, green-, and undiscovered fields including additional recovery attributable to gas injection and infill drilling. Crude production capacity by implementing EOR techniques is presented separately. In order to put the results into context, crude production and revenue in the recent past are also shown.

We found that Iran’s total crude production capacity is likely to reach 4.0 mmbbl/d before 2020, followed by a further increase before reaching a plateau level of 4.4 mmbbl/d in the middle of the next decade. Our model predicts that the production capacity of the producing fields may shrink from 3.7 mmbbl/d to 2.5 mmbbl/d by 2040. Daily production capacity from greenfields (i.e. undeveloped fields) is projected to monotonously increase by 90 kbbl on an annual basis and reach 1.0 mmbbl/d by 2027, but then declines at an average annual rate of 27 kbbl/d to yield 650 kbbl/d in 2040. Reserves that are likely to be discovered beyond 2016 will potentially come online after 10 years. Assuming a constant discovery rate of 500 mmbbl/y (Figure 6), we estimate the contribution from undiscovered reserves to reach approximately 700 kbbl/d in 2040. Finally, we project that marginal crude recovery via implementation of EOR methods start to materialize from the second half of the next decade, giving rise to nearly 500 kbbl/d oil production by 2040.

The production projection explained above in conjunction with the EIA’s projections of future crude prices [11] were employed to estimate the possible range of Iran’s gross revenue from crude production (Figure 7). The baseline projection (solid line in Figure 7) is based on EIA’s reference scenario, while the upper and lower bounds for gross revenue (dashed lines in Figure 7) correspond to the high and low oil price scenarios of EIA’s crude price projection, respectively.

For the baseline scenario, the annual gross revenue will initially increase at a rate of $16B/y to become $113B by 2020, followed by a significant slump in the growth rate, causing the revenue to remain below its 2011/12 amount of $150B until 2026. The gross revenue is projected to reach

Page 12

$220B by the end of the time horizon considered in this study (i.e. 2040).

However, owing to inherent inelasticity and uncertainty of the oil market, future oil prices, and hence Iran’s oil revenue, can vary within a wide range (Figure 7). In the case of high oil price scenario, Iran can retrieve its 2011/12 revenue within the next few years, whereas under the low oil price scenario it may never reach that level of revenue even by 2040.

It was also projected that the average API of the Iranian crude will decrease by 1.3 degree by 2040 compared to its baseline value in 2016.

Figure 7. Projections of Iran’s crude production (mmbbl/d) and gross revenue (2016$B) in the coming decades.

Besides the future projection for the crude production capacity, another important outcome of our field-specific model is the depletion level distribution of the oil fields and reservoirs. Depletion level is a key factor in determining how easily oil can be extracted from an oil field and hence has a strong influence on oil production cost. In order to create a holistic view of temporal variation in the Iranian oil fields depletion levels, they have been categorized into the following groups: undeveloped fields (i.e. 0% DL), 0 - 25% DL, 25 - 50% DL, 50 - 75% DL, and above 75% DL. At any given time, based on its cumulative production and ultimate recoverable resource, each field (or reservoir) was assigned to one of the above groups.

Generally, the depletion level at the peak production is positively correlated with the field size [14]. In case of fields with more than 1 BBL of oil reserves, which constitute the majority of Iran’s proven reserves, the mean depletion level at peak production is 36±16% [14]. Therefore, it can be assumed that the peak production of most Iranian fields occur when their depletion levels are in the range category of 25 to 50%, while those that fall into the 0 to 25% depletion level category are unlikely to be in decline yet, and those with depletion levels higher than 50% are very likely to be in decline.

Reserves that are assumed to be discovered in future explorations were treated in a similar manner to the existing fields. Time-specific production rates from each group was obtained by adding the production rates of all fields and reservoirs that fall into that group. Figure 8 presents

0

50

100

150

200

250

300

350

400

450

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2010 2015 2020 2025 2030 2035 2040

Gro

ss R

even

ue (2

016$

B)

Prod

uctio

n (m

mbb

l/d)

Developed Greenfields EOR Undiscovered Revenue

Page 13

the current and projected shares of depletion level groups in Iran’s oil reserves and production.

In 2016, Iran’s crude reserves distribution by the extent of depletion were: 12 BBL of 0% DL (undeveloped), 32 BBL of 0 - 25% DL, 32 BBL of 25-50% DL, 17 BBL of 50-75% DL, and 4 BBL of 75-100% DL. By 2025, all fields that are presently undeveloped will be in production. As such, only future discoveries occurring between 2016 and 2025 will make up the undiscovered reserves in 2025 (i.e., < 5 BBL). Also, share of the production from mature fields (i.e., DL >50%) will be somewhat smaller in 2025 compared with its current value. However, going beyond the middle of the next decade, the production will shift radically towards the mature fields such that in 2040, over 70% of the production (i.e. 2.3 mmbbl/d) will be extracted from the fields with depletion levels greater than 50%. This result not only highlights the importance of extensive investment in artificial lift, well stimulation, and enhanced oil recovery, but also implies a marked increase in the operating costs associated with the production of crude oil, which, in turn, translates into lower profit margins.

Figure 8. Estimated distribution of Iran’s oil fields depletion levels in 2016, 2025, and 2040 (left axis) and the respective productions from each of these depletion ranges (right axis). NGL reserves and production are not included.

0.0

0.5

1.0

1.5

2.0

0

10

20

30

40

Undev. 0-25% 25-50% 50-75% 75-100%

Prod

uctio

n R

ate

(mm

bbl/d

)

Res

erve

s (B

BL)

Reserves Production Rate

0.0

0.5

1.0

1.5

2.0

0

10

20

30

40

Undev. 0-25% 25-50% 50-75% 75-100%

Prod

uctio

n R

ate

(mm

bbl/d

)

Res

erve

s (B

BL)

2025

0.0

0.5

1.0

1.5

2.0

0

10

20

30

40

Undev. 0-25% 25-50% 50-75% 75-100%

Prod

uctio

n R

ate

(mm

bbl/d

)

Res

erve

s (B

BL)

Depletion Level

2040

2016

Page 14

Concluding Remarks

Besides recent developments in the underlying principles of the global energy market that adversely impact oil-dependent economies, Iran, despite its vast reserves, faces significant hurdles to boost its crude production in the mid- to long-term. Having produced over 72 BBL of oil so far, Iran’s oil industry is moving to a new era where the natural decline of its mature fields can only be offset through exploitation of the hard-to-recover oil (e.g. heavy oil, EOR, and deep water). The pace of this transformation becomes much faster from the middle of next decade.

It was estimated that the average annual decline rate of Iranian oil fields (including the impact of maintenance) to be 6.0%, average new well productivity in 2016 to be 1.7 kbbl/d with a year-over-year decline rate of 3.2%, and average gas injection yield of 4.0 kbbl/mcm.

Based on projections for future production of individual fields, we expect Iran to soon boost its crude production capacity and reach 4.0 mmbbl/d. The production capacity was projected to reach 4.4 mmbbl/d before 2030, and stay at that level until 2040 provided that the future exploration and enhanced oil recovery projects are implemented successfully. Using the baseline crude price projections by the US Energy Information Administration (EIA), we project that the annual gross value of Iran’s crude will reach its 2011/12 record-high figure of $150B (in constant 2016$) around the middle of the next decade.

Acknowledgement

The authors would like to thank Dr. Hamidreza Tabarraei from the International Monetary Fund (IMF) for his help with the economic analysis.

Nomenclature

bbl Barrel BBL Billion barrels bcm Billion cubic meter CBI Central Bank of Iran DL Depletion level EIA U.S. Energy Information Administration EOR Enhanced Oil Recovery IEA International Energy Agency kbbl Thousand barrels mcm Million cubic meter mmbbl Million barrels NGL Natural gas liquids NIOC National Iranian Oil Company OPEC Organization of Petroleum Exporting Countries RRR Remaining recoverable resource URR Ultimately recoverable resource

Page 15

References

[1] Spencer Dale, Society of Business Economics Annual Conference, 2015

[2] Outcomes of the U.N. Climate Change Conference in Paris, Center for Climate and Energy Solution, December 2015

[3] Energy and Climate Change, International Energy Agency, 2015

[4] Organization of Petroleum Exporting Countries (OPEC), www.opec.org

[5] U.S. Energy Information Administration (EIA), International Energy Statistics, www.eia.gov

[6] Central bank of Iran, Economic Time Series Database, www.cbi.ir

[7] National Iranian Oil Company (NIOC), www.nioc.ir

[8] International Energy Agency, www.iea.org

[9] World Energy Outlook 2015, International Energy Agency

[10] Mohsen Renani et al., Journal of Economic Research, 84, 2008, pp119-150

[11] International Energy Outlook 2016, US EIA

[12] Asgar Abnavi et al., Ekteshaf & Tolid (in Farsi), 89, 2010

[13] Abolghasem Bashiri, Ekteshaf & Tolid (in Farsi), 77, 2011

[14] Mikael Hook et al., Philosophical Transactions of the Royal Society A, 372, 2014