future of autonomous driving

TRANSCRIPT

Future of Autonomous DrivingAn Overview of Market & Technology Roadmaps, Changes in

Architecture, Design / Testing / Validation of Automated Vehicles

Prana Natarajan, Team Leader Nick Ford, Sr. Consultant

Automotive & Transportation

A Joint Presentation with

Harald Barth Dr. Anthony Baxendale

Product Marketing Manager Research Manager

© 2013 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of

Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

2

Today‟s Presenters

• Prana leads a team of research analysts covering the chassis & safety systems market, besides tracking

industry trends such as functional safety, 48V power net and automated driving

• Nick is a senior consultant with prior experience of having served a leading chassis & safety systems supplier

as a Global Product Planning Director

• Harald is a highly experienced product marketing manager with immense product-related knowledge in

commercially launching various safety products, now related to automated driving.

• Anthony is a highly experienced research manager with a proven record of developing and delivering high

technology solutions to the automotive, defence, security and telecommunications sectors.

Nick Ford

Sr. Consultant,

Frost & Sullivan

Prana Natarajan : uk.linkedin.com/in/pranat/

Nick Ford: uk.linkedin.com/pub/nick-ford/1/254/566

Anthony Baxendale: uk.linkedin.com/pub/anthony-baxendale/7/754/989 @FS_automotive

Dr. Anthony BaxendaleResearch Manager

Future Transport Technologies

MIRA Ltd

Prana T Natarajan

Team Leader,

Frost & Sullivan

Mr. Harald BarthProduct Marketing Manager

Driving Assistance

Valeo

Bietigheim-Bissingen, Germany

3

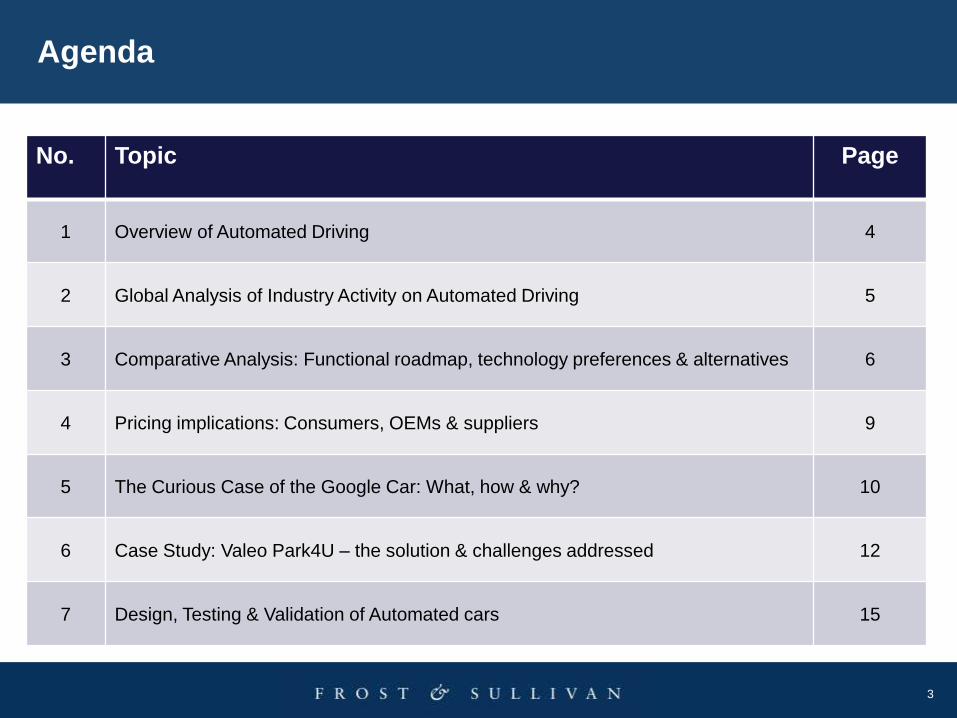

Agenda

No. Topic Page

1 Overview of Automated Driving 4

2 Global Analysis of Industry Activity on Automated Driving 5

3 Comparative Analysis: Functional roadmap, technology preferences & alternatives 6

4 Pricing implications: Consumers, OEMs & suppliers 9

5 The Curious Case of the Google Car: What, how & why? 10

6 Case Study: Valeo Park4U – the solution & challenges addressed 12

7 Design, Testing & Validation of Automated cars 15

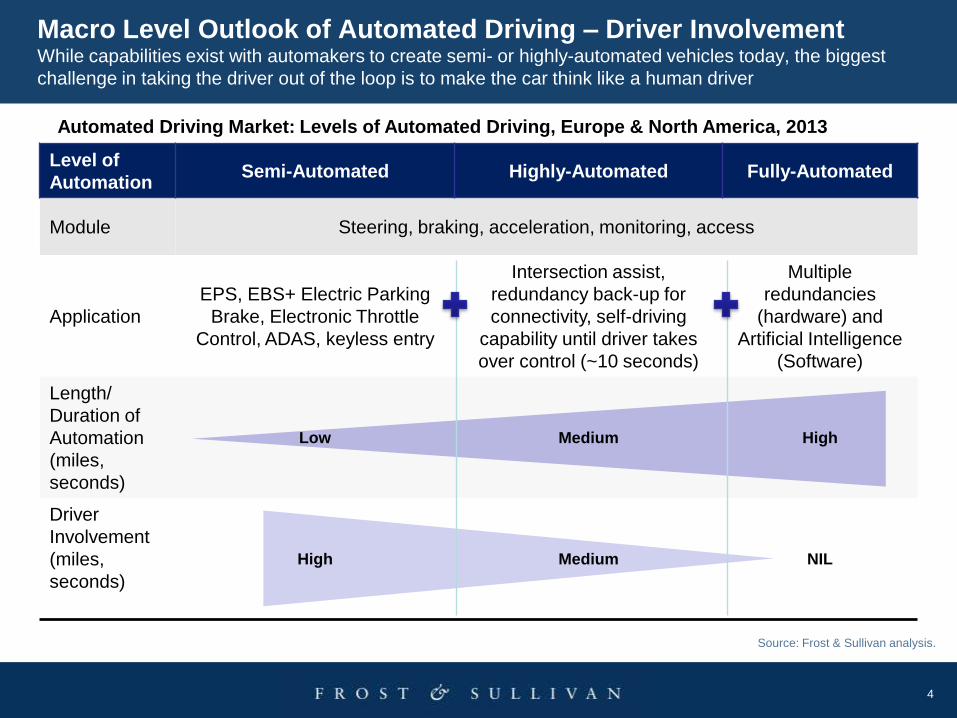

4

Macro Level Outlook of Automated Driving – Driver InvolvementWhile capabilities exist with automakers to create semi- or highly-automated vehicles today, the biggest

challenge in taking the driver out of the loop is to make the car think like a human driver

Level of

AutomationSemi-Automated Highly-Automated Fully-Automated

Module Steering, braking, acceleration, monitoring, access

Application

EPS, EBS+ Electric Parking

Brake, Electronic Throttle

Control, ADAS, keyless entry

Intersection assist,

redundancy back-up for

connectivity, self-driving

capability until driver takes

over control (~10 seconds)

Multiple

redundancies

(hardware) and

Artificial Intelligence

(Software)

Length/

Duration of

Automation

(miles,

seconds)

Low Medium High

Driver

Involvement

(miles,

seconds)

High Medium NIL

Source: Frost & Sullivan analysis.

Automated Driving Market: Levels of Automated Driving, Europe & North America, 2013

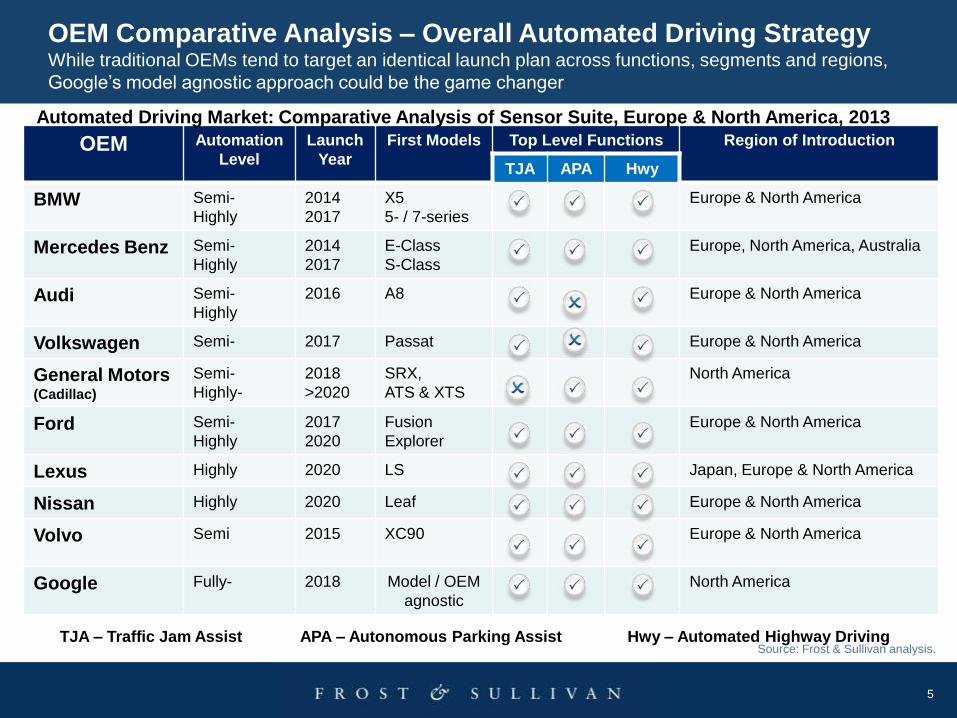

5

OEM Comparative Analysis – Overall Automated Driving StrategyWhile traditional OEMs tend to target an identical launch plan across functions, segments and regions,

Google’s model agnostic approach could be the game changer

OEM Automation

Level

Launch

Year

First Models Top Level Functions Region of Introduction

TJA APA Hwy

BMW Semi-

Highly

2014

2017

X5

5- / 7-series

Europe & North America

Mercedes Benz Semi-

Highly

2014

2017

E-Class

S-Class

Europe, North America, Australia

Audi Semi-

Highly

2016 A8 Europe & North America

Volkswagen Semi- 2017 Passat Europe & North America

General Motors (Cadillac)

Semi-

Highly-

2018

>2020

SRX,

ATS & XTS

North America

Ford Semi-

Highly

2017

2020

Fusion

Explorer

Europe & North America

Lexus Highly 2020 LS Japan, Europe & North America

Nissan Highly 2020 Leaf Europe & North America

Volvo Semi 2015 XC90 Europe & North America

Google Fully- 2018 Model / OEM

agnostic

North America

TJA – Traffic Jam Assist APA – Autonomous Parking Assist Hwy – Automated Highway DrivingSource: Frost & Sullivan analysis.

Automated Driving Market: Comparative Analysis of Sensor Suite, Europe & North America, 2013

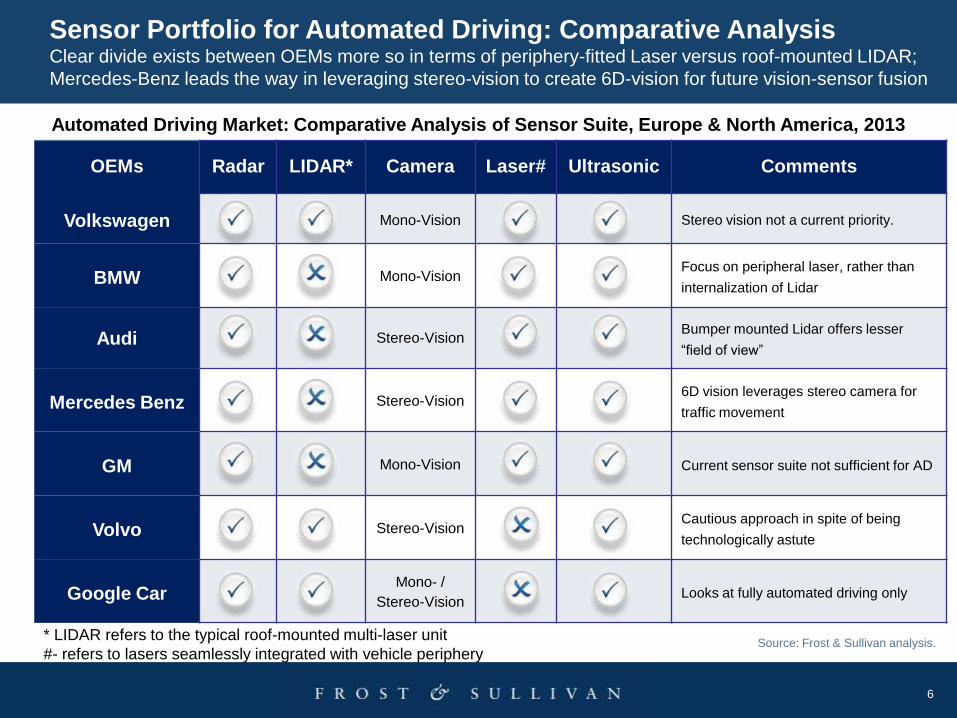

6

OEMs Radar LIDAR* Camera Laser# Ultrasonic Comments

Volkswagen Mono-Vision Stereo vision not a current priority.

BMW Mono-VisionFocus on peripheral laser, rather than

internalization of Lidar

Audi Stereo-VisionBumper mounted Lidar offers lesser

“field of view”

Mercedes Benz Stereo-Vision6D vision leverages stereo camera for

traffic movement

GM Mono-Vision Current sensor suite not sufficient for AD

Volvo Stereo-VisionCautious approach in spite of being

technologically astute

Google CarMono- /

Stereo-VisionLooks at fully automated driving only

Sensor Portfolio for Automated Driving: Comparative AnalysisClear divide exists between OEMs more so in terms of periphery-fitted Laser versus roof-mounted LIDAR;

Mercedes-Benz leads the way in leveraging stereo-vision to create 6D-vision for future vision-sensor fusion

Source: Frost & Sullivan analysis.* LIDAR refers to the typical roof-mounted multi-laser unit

#- refers to lasers seamlessly integrated with vehicle periphery

Automated Driving Market: Comparative Analysis of Sensor Suite, Europe & North America, 2013

7

2010 2016 2020

Autonomous Driving: Application RoadmapWhile ADAS functionalities form the basis for vehicle autonomy, connected solutions ensure getting the most

out of automated driving

Parking

(Autonomous

parallel parking)

Autonomous

emergency

braking

system

Traffic Jam

Assist Semi

Autonomous

steeringEmergency

Steer Assist

Smart Navigation

(Vehicle deciding

on routes)

Automated

Highway

systems

Lane Change

assist

(Partial

Steering

autonomy)

ACCIntersection assist

(powered by V2V V2X)

Automated

valet

retrieval

Platooning

Co-operative

cruise control

Driverless car

Occupant

specific driving

dynamics,

alerts to the

environment

(horn, dim dip)

Automated vehicle taking complete

control of navigation, transmission,

steering, braking and parking.

Source: Frost & Sullivan analysis.

Assisted

Semi-automated

Highly-automated

Cooperative

driving

Towards fully-automated driving

Automated Driving Market: Functional Roadmap, Europe & North America, 2010 - 2020

8

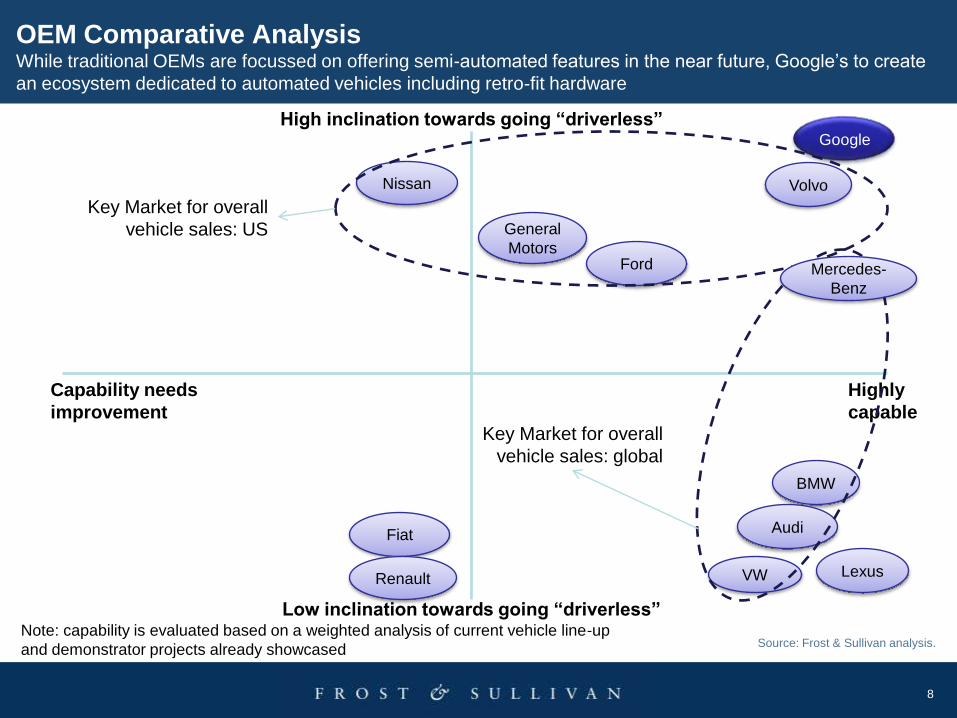

OEM Comparative AnalysisWhile traditional OEMs are focussed on offering semi-automated features in the near future, Google’s to create

an ecosystem dedicated to automated vehicles including retro-fit hardware

Note: capability is evaluated based on a weighted analysis of current vehicle line-up

and demonstrator projects already showcased

Capability needs

improvement

Highly

capable

Low inclination towards going “driverless”

High inclination towards going “driverless”Google

VW

Nissan

General

Motors

BMW

Volvo

Ford

Audi

Lexus

Fiat

Renault

Key Market for overall

vehicle sales: US

Key Market for overall

vehicle sales: global

Mercedes-

Benz

Source: Frost & Sullivan analysis.

9

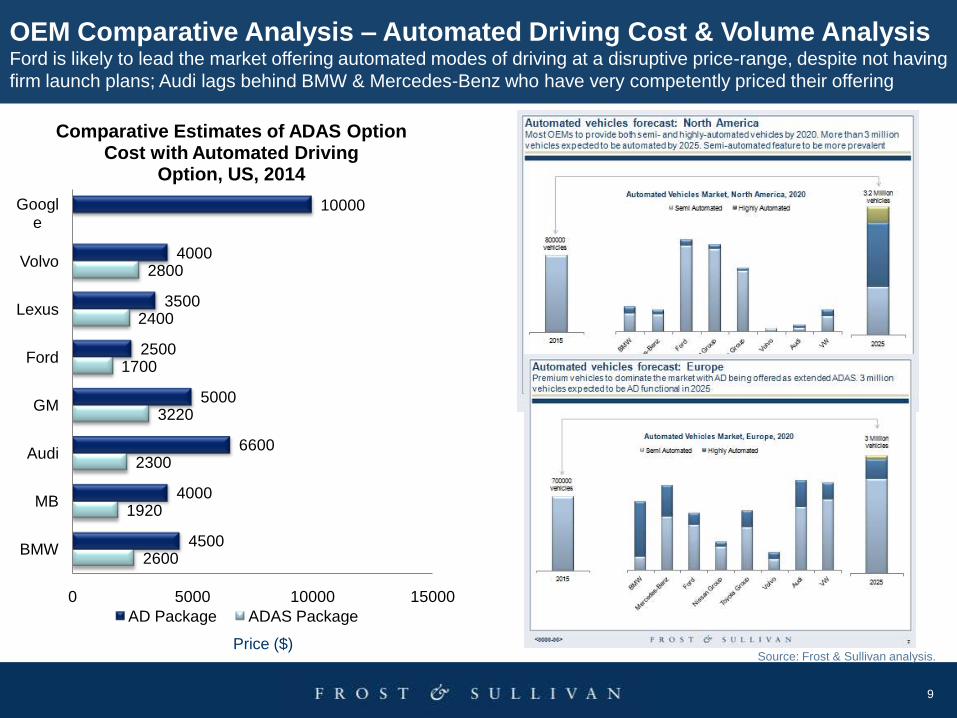

2600

1920

2300

3220

1700

2400

2800

4500

4000

6600

5000

2500

3500

4000

10000

0 5000 10000 15000

BMW

MB

Audi

GM

Ford

Lexus

Volvo

Comparative Estimates of ADAS Option Cost with Automated Driving

Option, US, 2014

AD Package ADAS Package

OEM Comparative Analysis – Automated Driving Cost & Volume AnalysisFord is likely to lead the market offering automated modes of driving at a disruptive price-range, despite not having

firm launch plans; Audi lags behind BMW & Mercedes-Benz who have very competently priced their offering

Price ($)Source: Frost & Sullivan analysis.

10

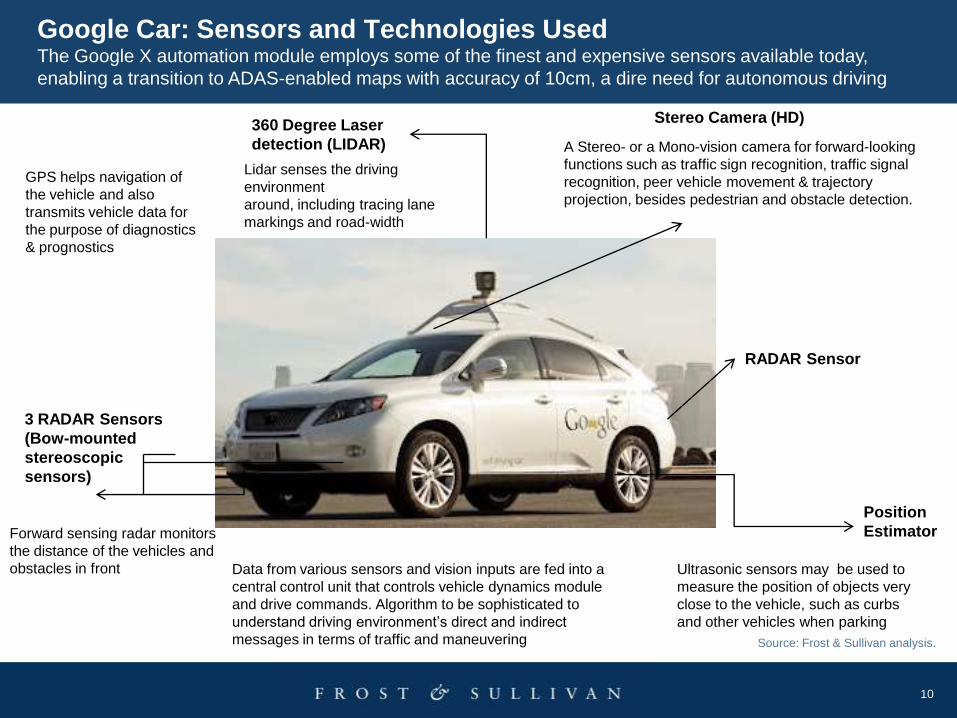

Google Car: Sensors and Technologies UsedThe Google X automation module employs some of the finest and expensive sensors available today,

enabling a transition to ADAS-enabled maps with accuracy of 10cm, a dire need for autonomous driving

3 RADAR Sensors

(Bow-mounted

stereoscopic

sensors)

RADAR Sensor

Position

Estimator

Stereo Camera (HD)360 Degree Laser

detection (LIDAR) A Stereo- or a Mono-vision camera for forward-looking

functions such as traffic sign recognition, traffic signal

recognition, peer vehicle movement & trajectory

projection, besides pedestrian and obstacle detection.

Lidar senses the driving

environment

around, including tracing lane

markings and road-width

GPS helps navigation of

the vehicle and also

transmits vehicle data for

the purpose of diagnostics

& prognostics

Ultrasonic sensors may be used to

measure the position of objects very

close to the vehicle, such as curbs

and other vehicles when parking

Data from various sensors and vision inputs are fed into a

central control unit that controls vehicle dynamics module

and drive commands. Algorithm to be sophisticated to

understand driving environment’s direct and indirect

messages in terms of traffic and maneuvering

Forward sensing radar monitors

the distance of the vehicles and

obstacles in front

Source: Frost & Sullivan analysis.

11

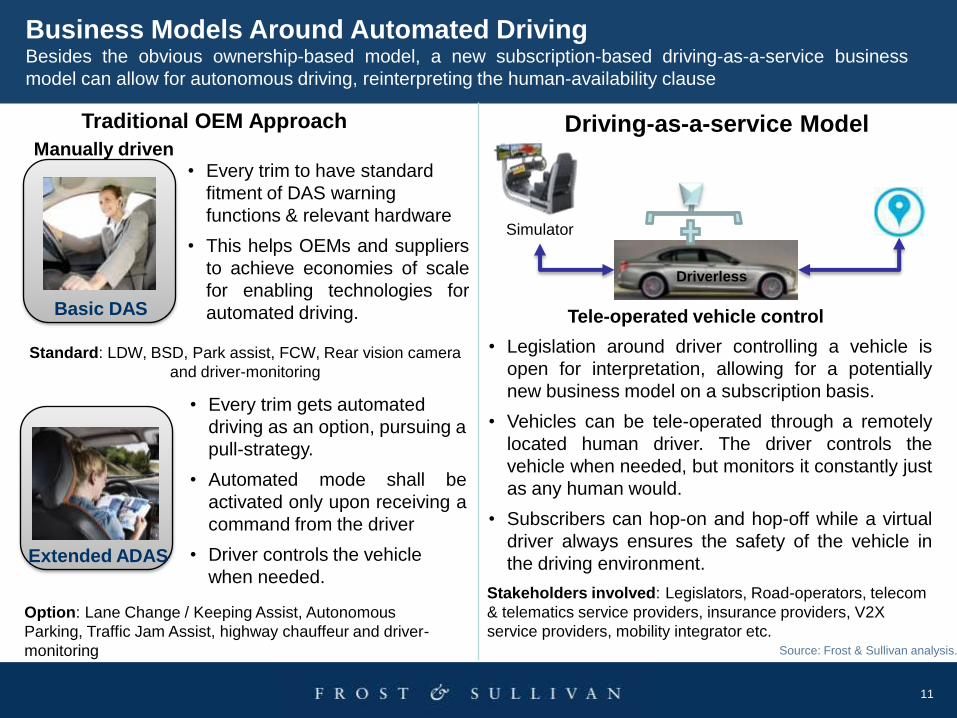

Business Models Around Automated DrivingBesides the obvious ownership-based model, a new subscription-based driving-as-a-service business

model can allow for autonomous driving, reinterpreting the human-availability clause

Manually driven

Basic DAS

Extended ADAS

Traditional OEM Approach

• Every trim to have standard

fitment of DAS warning

functions & relevant hardware

• This helps OEMs and suppliers

to achieve economies of scale

for enabling technologies for

automated driving.

• Every trim gets automated

driving as an option, pursuing a

pull-strategy.

• Automated mode shall be

activated only upon receiving a

command from the driver

• Driver controls the vehicle

when needed.

Standard: LDW, BSD, Park assist, FCW, Rear vision camera

and driver-monitoring

Option: Lane Change / Keeping Assist, Autonomous

Parking, Traffic Jam Assist, highway chauffeur and driver-

monitoring

Driverless

Driving-as-a-service Model

Tele-operated vehicle control

• Legislation around driver controlling a vehicle is

open for interpretation, allowing for a potentially

new business model on a subscription basis.

• Vehicles can be tele-operated through a remotely

located human driver. The driver controls the

vehicle when needed, but monitors it constantly just

as any human would.

• Subscribers can hop-on and hop-off while a virtual

driver always ensures the safety of the vehicle in

the driving environment.

Stakeholders involved: Legislators, Road-operators, telecom

& telematics service providers, insurance providers, V2X

service providers, mobility integrator etc.

Simulator

Source: Frost & Sullivan analysis.

Nov 2013 I 12

Nov 2013

Valeo Park4U® – The solution & challenges addressed

Harald BarthProduct Marketing Manager Driving Assistance

Valet Park4U®Intuitive Driving

Nov 2013 I 13

Valeo Park4U® – The Solution

78 vehicle models from 18 brandsAffordable luxury for everyday‟s life

From Semi- to Fully-automated Parking The future: Park4U® Remote / Valet Park4U®

Control Unit

Sensors

Push button

Source: Valeo

Nov 2013 I 14

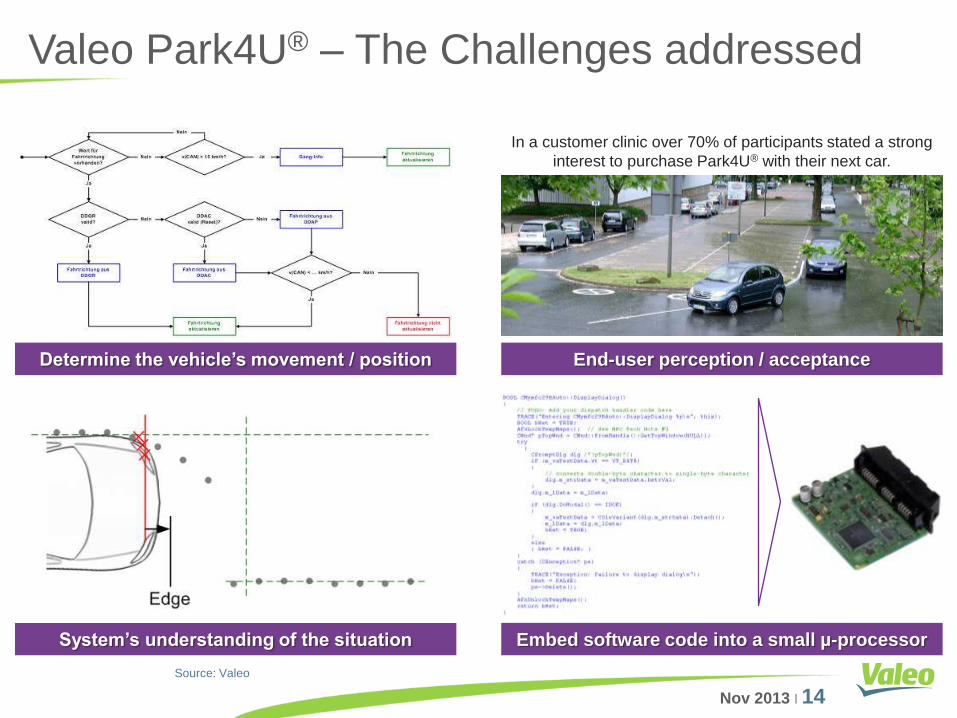

Valeo Park4U® – The Challenges addressed

End-user perception / acceptanceDetermine the vehicle‟s movement / position

System‟s understanding of the situation Embed software code into a small µ-processor

In a customer clinic over 70% of participants stated a strong

interest to purchase Park4U® with their next car.

Source: Valeo

Meeting the Design Challenges of Autonomous Vehicles Balancing a high degree of system authority with a complex operating environment and security aspects

requires a „System of systems‟ approach

MIRA’s slide can only be viewed by watching the analyst briefing. Click the below link to access the on-demand recording.

http://www.frost.com/prod/servlet/analyst-briefing-detail.pag?mode=open&sid=286359044

The Need for System Resilience A paradigm change in the design of highly automated vehicle systems requires a “system of systems”

approach to design and assurance

MIRA’s slide can only be viewed by watching the analyst briefing. Click the below link to access the on-demand recording.

http://www.frost.com/prod/servlet/analyst-briefing-detail.pag?mode=open&sid=286359044

Requirements for the Design Process of Autonomous VehiclesTo implement the resilience approach, a development process incorporating disruption management is required

MIRA’s slide can only be viewed by watching the analyst briefing. Click the below link to access the on-demand recording.

http://www.frost.com/prod/servlet/analyst-briefing-detail.pag?mode=open&sid=286359044

Systems Engineering Framework for Autonomous VehiclesBased on a traditional automotive V-model lifecycle process, additional parallel stages are

needed to cope with disruptions

MIRA’s slide can only be viewed by watching the analyst briefing. Click the below link to access the on-demand recording.

http://www.frost.com/prod/servlet/analyst-briefing-detail.pag?mode=open&sid=286359044

Towards Autonomous Driving

Strategic Review and Assessment of Future Opportunities

and Implications for the Automotive Industry with the Advent

of Autonomous Driving

Workshop Proposal

November 2013

20

www.twitter.com/FS_Automotive

Follow Frost & Sullivan on

Facebook, LinkedIn, SlideShare, and Twitter

http://www.facebook.com/FrostandSullivan

http://www.linkedin.com/groups?gid=4480787&trk=hb_side_g

http://www.slideshare.net/FrostandSullivan

21

For Additional Information

Harald Barth

Product Marketing Manager

Driving Assistance

Mobile: +49(0)176-3000 4025

Dr. Anthony Baxendale

Research Manager

Future Transport Technologies

+44 (0) 24 7635 5559

Prana Natarajan

Team Leader – Chassis &Safety

Automotive & Transportation

+44 (0) 20 7915 7871

Nick Ford

Consultant

Automotive & Transportation

+44 (0) 1454 880096