fund manager commentary · performance as at 28 february 2015 26: fund manager commentary –...

TRANSCRIPT

Fund Manager

Commentary

February 2015

Contents

Australian Shares 3

Smaller Companies 5

International Shares 7

Australian Fixed Income 9

International Fixed Income 10

Credit 14

Cash 15

Australian Property 18

International Property 21

Active Balanced 23

Performance as at 28 February 2015 26

Fund Manager Commentary – February 2015 3

Australian Shares

Market review

The S&P/ASX Accumulation Index rose 6.9% during February, the largest monthly gain since 2011.

At a macro level, the Reserve Bank of Australia’s decision to cut interest rates to a record low spurred

a greater general appetite for risk. Similarly, a pledge from ECB officials for continued accommodative

monetary policy settings helped buoy sentiment. A deal between Greek and Eurozone policy makers

also removed a source of concern for the market.

At home, the local earnings season was reasonable, but not inspiring. Aggregate earnings

expectations across the market deteriorated slightly over reporting season, to around -2% for FY15.

This was largely driven by downgrades in resources; however this was more a case of the market

updating its forecasts on the basis of weaker commodity prices rather than a material decline in

underlying conditions. The remainder of the market ex-resources is expected to deliver roughly 7-8%

earnings growth. It was cost control, rather than revenue growth, which drove earnings. At the same

time, the trend towards increased dividend payouts continued. Corporate guidance generally

suggested companies are not overly optimistic about the near-term operating environment.

The resources sector (+11.3%) was the top performer for the month. Energy stocks posted the

strongest gains, driven by a rebound in the price of the Brent crude oil benchmark. Market

heavyweight BHP Billiton also recovered as investors cheered the miner’s commitment to retaining its

progressive dividend policy, alongside cost reduction.

The telecommunication sector (+0.6%) lost steam and was the worst performer over the month as

investors rotated towards more risk-sensitive areas. Similarly, the consumer staples space lagged the

broader market with supermarket giant, Woolworths, punished following a disappointing set of first-

half earnings. Finally, financials (+7.0%) strengthened with another round of healthy results reported

by the “Big Four” banks.

Portfolio performance

The BT Wholesale Core Australian Share Fund returned 6.94% (post-fee, pre-tax) in February 2015,

outperforming its benchmark by 0.02%.

Fund Manager Commentary – February 2015 4

Contributors

Supermarket giant, Woolworths (-3.37%), reported disappointing earnings and acknowledged what

we have asserted for some time - that its prices are too high in the face of increasing competition from

Coles and from discounters such as Aldi. Management indicated it needs to change their pricing but

are yet to offer a concrete strategy. The stock sold off this uncertainty and on the implication that profit

margins are likely to compress.

Diversified financials group, Macquarie (+17.23%) enjoyed strong gains as management indicated

that their full year profit is likely to come in at the upper end of their forecast range – which had itself

been raised in January. Macquarie is enjoying tailwinds from a number of factors, including a pipeline

of corporate action and increased trading volumes, as well as a weaker AUD. The company has

successfully altered its business profile since the GFC, shifting from a reliance on transaction–driven

investment banking to a greater focus on annuity-like income streams from its various leasing

businesses.

Detractors

Telstra (+0.28%) erased earlier gains to finish the month relatively flat. The company delivered a

pleasing earnings result, revealing a jump in first-half profits by 22.4% and significant gains in market

share among mobile subscribers. Looking ahead, there are some concerns over the level of opex.

However, the negatives are more than offset by a number of strengths, including the telco’s well-

entrenched position in the marketplace. Overall it remains our preferred blue chip dividend play over

the longer term, particularly given its ability to achieve low cost earnings growth.

BHP Billiton (+15%) saw its share price rebound from its 5-year low in January. The recovery in the

price of Brent crude oil offered a tailwind to performance, as well as a commitment by management to

maintain the company’s progressive dividend policy. However, going forward we believe the

company’s top line is likely to suffer in the face of weak commodity prices, which remain significantly

below their former peaks. Further, the company is likely to suffer a high capex burden over coming

years. Taken together we prefer to remain underweight the miner.

Fund Manager Commentary – February 2015 5

Strategy and outlook

The portfolio gained broadly in line with the benchmark in February. A return to profitability from

Qantas was beneficial, as was indications from Macquarie Group’s management that the company

should meet the top end of their earnings expectations for the year. The underweight in Woolworths

also helped, as management acknowledged our long-standing concern that its current pricing strategy

– and profit margins – was unsustainable in an increasingly competitive industry. There was a distinct

rotation within the market, as investors sought high quality beta in preference to the defensive yield

stocks. This weighed on our position in Telstra which gave up some of its recent gains.

We increased the exposure to Macquarie Group and to JB HiFi over the reporting season. Macquarie

Group is one of the few companies enjoying cyclical tailwinds, benefiting from low-cost funding costs,

increased trading volumes and a depreciating currency. We like the fact that the company has

increased its exposure to annuity-like assets, such as asset management and aircraft leasing, and is

less dependent on transaction-driven investment banking. JB HiFi delivered a surprisingly good set of

results, given the challenging environment of the past six months. It is displaying good cost control

and improved cash flow and should deliver high single-digit earnings growth for FY15.

We lightened up the position in Suncorp following its results. We have been conscious for some time

that it is in a sweet spot in terms of profit margins and that the environment in its general insurance

business would become incrementally more competitive. This dynamic has started to emerge and,

while the company has a diversified profile and the ability to fund at least one more special dividend, it

is entering a more challenging period. We also reduced the exposure to Telstra following a very

strong run, although it remains our favoured defensive yield stock.

The market is currently at an elevated valuation, leaving it vulnerable in the event of a geopolitical

shock. However, history shows us that the current valuation rating is supported by low rates – this is

augmented by the additional support of QE-fuelled liquidity and increased foreign interest as the AUD

depreciates. As a result, we would not be surprised to see a period of market consolidation, as it

digests its recent gains. There is certainly scope for rotation within the market, as the possibility of US

rate hikes and a marked convergence in yield levels across the market leaves the high yield “bond

proxies” looking vulnerable. In contrast, there are high quality industrial cyclicals delivering earnings

growth at reasonable valuations, often with an increasing dividend yield, which are looking

increasingly attractive.

Fund Manager Commentary – February 2015 6

Smaller Companies

Market review

The S&P Small Ordinaries Index rose 8.4% during February, outperforming the broader index as

investors sought cyclical beta in preference to defensive yield. At a macro level, the Reserve Bank of

Australia’s decision to cut interest rates to a record low spurred a greater general appetite for risk.

Similarly, a pledge from ECB officials for continued accommodative monetary policy settings helped

buoy sentiment. A deal between Greek and Eurozone policy makers also removed a source of

concern for the market.

At home, the local earnings season was reasonable, but not inspiring. Aggregate earnings

expectations across the broad market deteriorated slightly over reporting season, to around -2% for

FY15. This was largely driven by downgrades in resources; however this was more a case of the

market updating its forecasts on the basis of weaker commodity prices rather than a material decline

in underlying conditions. The remainder of the market ex-resources is expected to deliver roughly 7-

8% earnings growth. It was cost control, rather than revenue growth, which drove earnings. At the

same time, the trend towards increased dividend payouts continued. Corporate guidance generally

suggested companies are not overly optimistic about the near-term operating environment.

The energy sector posted the strong gains, driven by a rebound in the price of the Brent crude oil

benchmark. Healthcare also did well. The telecommunication sector lost steam and was the worst

performer over the month as investors rotated towards more risk-sensitive areas.

Portfolio performance

The BT Wholesale Smaller Companies Fund returned 7.97% (post-fee, pre-tax) in February,

underperforming its benchmark the S&P/ASX Small Ordinaries Accumulation Index by 0.46%.

The portfolio made strong gains in February, helped by positions in healthcare with Mayne Pharma

Group and Japara Healthcare standing out as notable contributors. Various consumer discretionaries

also did well as the market sought cyclicality and beta. The holding in Village Roadshow detracted as

poor weather hit operations at its theme parks and the cash position also dragged as the market

made strong gains, leaving the portfolio slightly behind the index for the month. The rebound in the

resources space as commodity prices stabilised also dragged on performance, although the portfolio

remains ahead of its index over 6 months and the longer term.

Contributors

Fund Manager Commentary – February 2015 7

Mayne Pharma Group surged in mid-February on news that the company was raising capital to

acquire several US trademarks in order to grow its business there. Institutional businesses made

aggressive bids for the equity placement in a show of approval for Mayne’s expansions plans.

Japara Healthcare bounced back from a weaker January as management indicated that the company

should meet the earning targets listed in its IPO prospectus despite an adverse change in its tax

status as a result of last year’s Federal budget. A strong focus on cost control and high occupancy

rates should offset the negative effects of the tax change.

Detractors

Village Roadshow reported a significant decline in first half profits due primarily to temporary closures

of its theme parks in December and January due to severe rainstorms. Management indicated it

would be controlling costs in order to mitigate this news. Looking forward they are also positive about

upcoming theatrical releases and greater clarity around the issue of online piracy.

Qube Logistics outperformed the index on the back of strong profit growth over H1 FY15. We do not

hold it in the portfolio and it dragged on relative performance as a result.

Strategy and outlook

The market is currently at elevated valuation, leaving it vulnerable in the event of a geopolitical shock.

However, history shows us that the current valuation rating is supported by low rates – this is

augmented by the additional support of QE-fuelled liquidity and increased foreign interest as the AUD

depreciates. As a result, we would not be surprised to see a period of market consolidation, as it

digests its recent gains. The dispersion in valuation and earnings outlook across the market is

conducive to stock picking and we continue to focus on companies that combine strong or improving

cash flow with reasonable valuation. In particular, we are looking for companies that offer niche

products, robust franchises or compelling “turnaround” stories.

There is certainly scope for rotation within the market, as the possibility of US rate hikes and a

marked convergence in yield levels across the market leaves the high yield “bond proxies” looking

vulnerable. In contrast, there are high quality industrial cyclicals delivering earnings growth at

reasonable valuations, often with an increasing dividend yield, which are looking increasingly

attractive.

Fund Manager Commentary – February 2015 8

International Shares

Market review

February was a strong month for global equities across the globe with the MSCI World ex Australia

returning 5.27%, driven by strong performances from the European and Japanese markets.

The European market was buoyed by the substantial quantitative easing package announced by the

ECB and the promise of support for markets. This saw many markets outperform strongly including

Germany (+6.6%), France (+7.5%), Italy (+8.9%), Spain (+7.5%). The key to a sustained rally in these

markets will be signs of a sustainable economic recovery and increasing inflation.

The US market continued its strong run, returning a positive 5.5%, but did see some profit taking into

month end as concerns started to build about the potential impact of rate rises that seem to be getting

closer and closer to being implemented.

In Asia, Japan did well with the Nikkei index returning 6.4%, driven by signs of an economic recovery

and some of the stimulatory packages starting to take effect. China returned 3.1% as further stimulus

cuts from the PBOC helped drive investor sentiment.

Notwithstanding the RBA rate cut and accompanying comments from Glenn Stevens, the AUD rose

against the USD (+0.6%). More broadly the AUD trade weighted index rose marginally against its

largest trading partners (+0.3%).

Portfolio performance

The BT Wholesale Core Global Share Fund returned 4.51% (post fee, pre-tax) in February,

underperforming its benchmark by 0.76%. The result was predominantly due to the underperformance

of North American stock positions, with Japanese and European positions also underperforming their

regional benchmarks over the month.

Thematically, the underperformance in the US was driven by weakness in relative valuation measures

for stock selection, along with momentum signals for industry selection. Investor sentiment and

business quality measures were minor positive contributors over the month. Underperformance in

Japan was largely due to momentum measures, both for stock and industry selection, which

outweighed positive returns to relative valuation signals. European markets produced a minor loss,

with all of valuation, momentum & quality measures showing weakness over February.

In terms of stock/ sector contributions, active sector positioning generated negative returns over the

month - notably the tilt towards Utilities that underperformed the broader market. Stock selection

Fund Manager Commentary – February 2015 9

within sector groups was also negative over the month, notably within Industrials and Information

Technology, offset by strong returns within the Energy sector

At a stock level, the strongest positive contributions came from overweight positions in Pandora

Media, a US headquartered music streaming service, Valero Energy, an American manufacturer &

distributor of transportation fuels; and Humana, a US health insurer.

The largest detractors were underweight positions in: GE, Walt Disney and Citigroup.

Strategy and outlook

Entering March, the Fund maintains its largest sector tilts towards Healthcare and away from

Consumer Staples. Thematically, we are mildly tilted towards higher quality companies with positive

momentum, and away from cheaper industry peers across all regions.

Fund Manager Commentary – February 2015 10

Australian Fixed Income

Market review

During February Australian three-year bond yields fell by 13 basis points to 1.79% from 1.92% and

ten-year yields rose by 5 basis points from 2.40% to 2.45%, with the 3-10s yield curve steepening to

66 basis points.

At its February meeting, the Reserve Bank decided to cut the cash rate by 25 basis points to 2.25%.

The Bank noted that the US economy continued to strengthen, but the Euro Area and Japanese

economies were both weaker than expected. It also noted that China’s growth was in line with policy

makers’ objectives.

The Reserve Bank expects the Australian economy to continue to grow at a below-trend pace with the

unemployment rate expected to peak higher than previously expected. However, a lower exchange

rate is likely to be needed to achieve balanced growth in the economy.

During the month the housing market continued to be bolstered by low interest rates - residential

property prices and housing finance continued to climb with the support of low lending rates.

Employment growth was weak after two months of strength and the unemployment rate kept rising to

6.4% from 6.1% and as a result, wage growth slowed to 2.5%. The CAPEX survey showed the fall in

mining investment has not been offset by non-mining investment and further declines in investment

are expected.

Portfolio performance

The BT Wholesale Fixed Interest Fund returned -0.07% in February (post-fees, pre-tax),

underperforming its benchmark by 0.35%.

In the alpha overlay, losses were mainly from Duration and FX strategies. The Government bond

component underperformed its benchmark with gains from Duration strategies offset by curve

strategies. The Credit component underperformed its benchmark with negative contributions from a

curve position, and a positive contribution from an underweight in the Supranational sector and

overweights in lower rated utility bonds.

Strategy and outlook The Reserve Bank of Australia left the cash rate unchanged at its March meeting although it stated that further monetary policy easing may be appropriate over the period ahead.

Fund Manager Commentary – February 2015 11

The CAPEX survey highlights the problem facing the Australian economy: mining investment is falling sharply and the non-mining sector is not picking the slack up as quickly as the Reserve Bank would like.

The housing market, particularly in Sydney, will be causing some concern although the Reserve Bank also stated that it is working with other regulators to assess and contain risks that may arise from the housing market.

We expect further monetary policy easing from the Reserve Bank. Should fourth quarter gross domestic product data released in early March come out weaker than expected further policy easing could occur as quickly as the April meeting. We do not rule out the cash rate going sub-2% by the end of the year.

Fund Manager Commentary – February 2015 12

International Fixed Income

Market review

International markets were dominated by active central banks and the Greek loan extension

negotiation. US Federal Reserve Chairperson Yellen reiterated that the Fed remains patient in raising

rates and indicated a hike is unlikely in the next couple of meetings. She confirmed that hike decisions

will be data dependant.

US Q4 GDP growth fell short of expectation with 2.6% annualized growth rate. The labour market

continued its strength with better-than-expected nonfarm payrolls. Euro area flash PMI for February

surprised to the upside and lower oil prices are believed to be the factor to a broad-based jump of the

services PMI.

After extended negotiations, the Eurozone Finance Ministers reached an agreement to extend loans

to Greece by four months. The PBC cut the Reserve Requirement Ratio (RRR), but the Politburo

reiterated that "we need to give higher priority to improving the structure of the economy".

Over the month, US and UK bond yields rose by 35 and 47 basis points, respectively. Japanese bond

yields rose by 6 basis points. Australian bond yields outperformed the US by 30 basis points. The

Australian dollar appreciated and the trade weighted index rose by 0.31% over the month.

Portfolio performance

The BT Wholesale Global Fixed Interest Fund returned -1.49% in February (post-fees, pre-tax),

underperforming its benchmark by 0.69%. The physical allocation to domestic credit returned just

above index, adding only marginally to the fund. The PAFI overlay however detracted as positions in

duration, cross-Market FX and macro cost performance through February’s bond market weakness.

Strategy and outlook

The Greek loan extension negotiation was a manifestation of political instability within the Eurozone. It

is highly likely that such events will continue to affect the Eurozone and the global market unless the

economic recovery takes hold. Before the expected benefits from lower energy prices flow through

the economy, energy producers have reacted to the lower prices by cutting supply. Even excluding

energy prices, the core inflation measures across countries are still stuck at low levels and deflation is

taking hold in Europe.

Fund Manager Commentary – February 2015 13

For central banks, deflation risks are a bigger concern than inflation and they will continue to be

dovish and a low interest rate environment will persist. Although the Fed is a little optimistic on the

economic recovery, it is reluctant to raise rates too soon.

Fund Manager Commentary – February 2015 14

Credit

Market review

Cash credit markets spreads were marginally tighter over February, with some support coming from

the stabilisation of global oil commodity prices. Early in the month WTI oil closed over $50 per barrel.

Economic data emanating out of the US remained positive with both better labour force participation

and supportive testimony from Yellen, the Chair of the US Federal Reserve. As a counterpoint to this

the Reserve Bank reduced the cash rate by 0.25 percentage points early in February due to signs of

domestic economic weakness.

Throughout the month all eyes were focused on whether Greece would be able to forge an agreement

with the troika over its debt programme. While many pundits viewed a Greek exit as unlikely it still

remained a risk until near the end of the month when the troika agreed with Greece on a 4 month

extension as it agreed to certain conditions.

From a fundamental bottom up perspective both US and Australian corporates reported semi-annual

and quarterly results, respectively. The results in the US were positive with the overall market

expectations of sales and earnings surprising marginally on the positive side in the face of a hit to

offshore earnings as the US dollar strengthened and energy companies impacted by the lower oil

price. In Australia, on the other hand, industrials which include mining service companies reported

weaker results than anticipated.

During the month the expansion of the spread to swap differential between AAA and BBB stopped.

Since mid-November the differential has grown reflecting an aversion to riskier issuers. In February

this dynamic stopped reflecting a more sanguine view of risk. The Australian iTraxx, the US CDX, and

Euro Main index tightened 13bp, 7bp and 10bp, respectively.

Portfolio performance

The BT Wholesale Enhanced Credit fund returned 0.48% in February (post-fees, pre-tax),

underperforming the benchmark by 0.05%. Negative performance came from the swap curve and an

underweight in select supra-nationals in the 5-7 year tenor, and negative performance from lower

rated utilities, and an underweight in Washington-backed Supra-nationals. Positive performance came

from an overweight in financials and real estate.

Activity over the month consisted of adjusting exposure in financials to take advantage of new

issuance outside the large four banks.

Fund Manager Commentary – February 2015 15

Strategy and outlook

Our macro credit view is neutral. Combined with a slower global growth outlook that has resulted in

stalling market performance, increased volatility, and increased headwinds from geopolitical event

risk, we view it as prudent to take an overall short term neutral view. On a spread to swap basis the

domestic credit index stabilised in February after widening marginally over the past quarter. While we

maintain a more sanguine medium to longer term view we believe recent volatility will persist and

possibly increase in the near term and be injurious to credit performance.

Going forward in the near term risk markets will continue to battle headwinds against the implied

growth outlooks from commodity price weakness, combined with ECB actions, uncertainty over

Greece and shifting expectations on US Fed raising rates. The recent uptick in oil prices has taken

some of the pressure off markets and high yield energy issuers but the recent increase in US oil

inventory levels could be a harbinger of further weakness.

While the global growth pulse is waning, we continue to be constructive on global growth

underpinning corporate creditworthiness as companies use cost control to continue to drive margins

in the absence of top line growth.

Domestically we see growth stagnating and we continue to recommend a defensive approach that is

flat with overweights in operationally resilient sectors such as utilities, staple industrials and

infrastructure that provide a higher yield to index returns. We do not foresee continued strong

compression of spread to swap as experienced in the prior years.

Fund Manager Commentary – February 2015 16

Cash

Market review

The Reserve Bank of Australia eased monetary policy by 25 basis points at its February meeting,

taking the cash rate to 2.25%. This was the first change in policy since August 2013. The Reserve

Bank’s Statement on Monetary Policy was released shortly after the decision to ease monetary policy

and provided insight into the reasons for the decision.

The Statement on Monetary Policy showed forecasts for economic growth and inflation had fallen

since the November statement. The Reserve Bank expects growth for 2015 to be between 2.25% and

3.25% (revised down by 0.25%) and between 3% and 4% in 2016. Based off these forecasts the

Reserve Bank does not see a return to trend growth until the second half of 2016. On inflation, the

Reserve Bank revised their 2015 and 2016 forecasts lower by 0.25% to a midpoint of 2.5%. On the

currency the Reserve Bank continues to see the exchange rate, despite the depreciation, as being

above its fundamental value given the significant falls in key commodity prices and is providing less

assistance in delivering balanced growth in the economy.

Expectations for a further rate cut increased following the release of weak labour market and CAPEX

data. Employment fell by 12,200 jobs in January and the unemployment rate rose from 6.1% to 6.4%

(that said, employment growth had been strong in recent months and labour data has been volatile

and subject to revisions). Wage inflation data confirmed that the labour market remains weak, with

annual wage inflation at 2.5% being the lowest since the series started in 1998.

The CAPEX report included the first reading for 2015-2016 investment expectations. The report was

very weak with not only mining investment falling (no surprise) but also non-mining investment

intentions disappointing (a fall of 3.1% against prior corresponding period).

The Reserve Bank would have taken some comfort from the rebound in consumer confidence.

According to the Westpac/Melbourne Institute survey, consumer confidence rose by 8% in February

to its highest level since January 2014. Confidence was supported by the rate cut from the Reserve

Bank, the 21% fall in average petrol prices and the 9.7% gain in the stock market since the January

survey.

The NAB business survey continued to reflect a subdued business environment. NAB business

conditions were slightly lower and business confidence slightly higher, albeit at low levels. According

to the survey sales deteriorated considerably, profits eased and employment remained soft. The

manufacturing sector deteriorated considerably. Despite the lower oil price, confidence in the

transport/ utilities sector fell.

Fund Manager Commentary – February 2015 17

In offshore events, much focus was on Greece after the anti-austerity Syriza party formed government

following the election in late January. The Eurozone and Athens came to an agreement on an

extension of the bailout package following the draft proposals put forward by the Greek government.

Greece has now been given until the end of April to submit its detailed reform proposals.

In the United States, the FOMC meeting minutes were more dovish than was expected. According to

the minutes “many participants indicated that their assessment of the balance of risks associated with

the timing of the beginning of policy normalization had inclined them toward keeping the federal funds

rate at its effective lower bound for a longer time” and that “a premature increase in rates might

dampen the apparent solid recovery in real activity and labour market conditions”.

The Australian bond curve steepened over the month, with three year bond yields ending 13 basis

points lower at 1.79% and ten year bonds ending 5 basis points higher at 2.45%. Australian bank bills

rallied strongly after the Reserve Bank’s decision to ease monetary policy, with 90 day bank bills

falling 23 basis points to 2.33%. The Australian market outperformed the US, with US bonds selling

off sharply. US ten year bond yields ended 35 basis points higher at 1.99%.

Portfolio performance

Managed Cash

The BT Wholesale Managed Cash Fund returned 0.19% in February (post fee, pre-tax),

underperforming the benchmark by 0.02%. The fund is well positioned to outperform in March given

the higher running yield than index. The fund ended the month with a weighted average maturity of 69

days (maximum limit of 70 days). With the bank bill curve remaining positively sloped, despite further

monetary policy being priced in in the futures market, we will continue to position the fund longer than

index. Credit exposure remains consistent with prior months with excess spread from A-1 rated

issuers likely to be the main driver of outperformance.

Enhanced Cash

The BT Wholesale Enhanced Cash Fund returned 0.22% in February (post fee, pre-tax),

outperforming its benchmark by 0.01%. Positive performance came from financials, mortgage backed

securities and industrial sectors, while curve and the Itraxx position detracted from performance.

With credit spreads narrowing and our technical analysis models triggering a neutral signal, we closed

our short iTraxx position early in the month. Other activity included reducing exposure to offshore

banks whilst increasing exposure to domestic banks, auto ABS and industrial sectors.

Fund Manager Commentary – February 2015 18

As at the end of the month, the portfolio had a credit spread of 65 basis points over bank bills, an

interest rate duration of 0.18 years and credit spread duration of 1.38 years.

Strategy and outlook

The Reserve Bank of Australia left the cash rate unchanged at its March meeting although stated that

further monetary policy easing may be appropriate over the period ahead.

The CAPEX survey highlights the problem facing the Australian economy: mining investment is falling

sharply and the non-mining sector is not picking the slack up as quickly as the Reserve Bank would

like. The housing market, particularly in Sydney, will be causing some concern although the Reserve

Bank also stated that it is working with other regulators to assess and contain risks that may arise

from the housing market.

We expect further monetary policy easing from the Reserve Bank. Should fourth quarter gross

domestic product data released in early March come out weaker than expected then further policy

easings could occur as quickly as the April meeting. We do not rule out the cash rate going sub-2%

by the end of the year.

Fund Manager Commentary – February 2015 19

Australian Property

Market review The S&P/ASX 200 REIT index was up 3.7% in February, however lagged the broader market which

was up 6.9%, mostly driven by resource stocks. This brings to an end eight consecutive months of

outperformance by the REITs. However, in the rolling year REITs have outperformed the broader

market by almost 21%.

February saw a generally positive earnings season for the REITs. On average net operating income

growth was +2.3% and NTA growth was a solid +4.7%, with the average cap rate compressing 28bp.

The stand out sector was residential trusts with both MGR and SGP showing both margin recovery

and solid sales growth. The weakest results came from the office sector reflecting higher vacancy

(IOF) and still above average incentives (DXS).

Aside from the reporting season, the major REIT news for the month was corporate activity with FDC

and NVN announcing a merger agreement with an all scrip offer at an implied price of $2.55 for NVN.

The major shareholder the Gandel Group (holds 21.6%) has agreed to vote in favour of the merger in

the absence of a higher offer. Morgan Stanley also advised that it would sell the balance sheet assets

of Investa Property Group as well as the management rights to IOF and its wholesale fund.

Depending on price, this may provide IOF with an opportunity to internalize. Also during the month

WFD sold a 47.4% interest in 3 of its lower growth US assets for $440M to O’Connor Capital. This is

consistent with the WFD strategy of selling non-core assets and deploying the funds into its flagship

development pipeline.

During the month the Australian 10 year bond rate was virtually flat and ended the month at 2.47%.

However, following solid economic data in their respective economies, US bonds were up 35bp to 2%

and UK bonds were up 47bp to 1.95%. The RBA cut the cash rate by 25bp to 2.25%, the first move

since August 2013, with the Bank expecting a prolonged period of sub-trend growth and the jobless

rate to be a little higher than previously anticipated.

Portfolio performance

The BT Wholesale Property Securities Fund returned 3.44% in February (post-fee, pre-tax),

underperforming its benchmark by 0.25%. The portfolio underperformed over the month with positive

attribution coming from our overweight positions in Lifestyles Communities, Arena REIT and Novion

Property Group as well as out underweight position in Dexus Property Group. Negative attribution

came from our underweight positions in Cromwell and Stockland Group (we are closing this

underweight) and as well as our overweight positions in Australian Agricultural, Federation Centres

and Westfield Corporation.

Fund Manager Commentary – February 2015 20

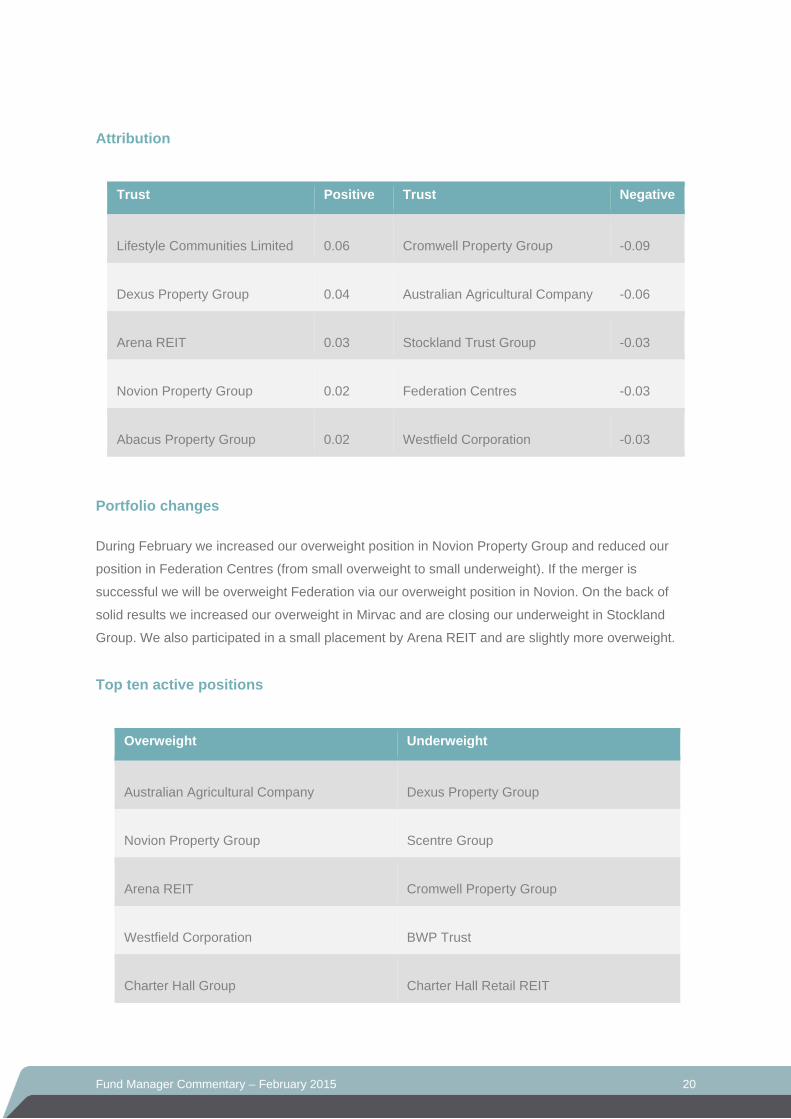

Attribution

Trust Positive Trust Negative

Lifestyle Communities Limited 0.06 Cromwell Property Group -0.09

Dexus Property Group 0.04 Australian Agricultural Company -0.06

Arena REIT 0.03 Stockland Trust Group -0.03

Novion Property Group 0.02 Federation Centres -0.03

Abacus Property Group 0.02 Westfield Corporation -0.03

Portfolio changes

During February we increased our overweight position in Novion Property Group and reduced our

position in Federation Centres (from small overweight to small underweight). If the merger is

successful we will be overweight Federation via our overweight position in Novion. On the back of

solid results we increased our overweight in Mirvac and are closing our underweight in Stockland

Group. We also participated in a small placement by Arena REIT and are slightly more overweight.

Top ten active positions

Overweight Underweight

Australian Agricultural Company Dexus Property Group

Novion Property Group Scentre Group

Arena REIT Cromwell Property Group

Westfield Corporation BWP Trust

Charter Hall Group Charter Hall Retail REIT

Fund Manager Commentary – February 2015 21

Strategy and outlook

The sector is priced on an FY15 dividend yield of 4.8%, FY15 AFFO yield of 5.2% and a PE ratio of

17.5 times. Earnings and balance sheets are stable with sector gearing currently standing at 32%. We

expect supportive funding costs, positive spread investing and cost cutting to drive earnings and the

performance of the sector in the medium term. Given AREITs do not have the lowest cost of capital (a

mantle held by both pension and sovereign funds) we would not expect significant equity capital

issuance for some time.

Fund Manager Commentary – February 2015 22

International Property

Market review

Performance of the global property securities market (on an ex-Australia basis) as measured by the

UBS Global Real Estate Investors Index fell in February, posting a total return of -1.54%. North

America (down -3.55%) posted the largest loss. Asia Pacific was up 0.10% while Europe posted a

gain of 4.21%. In Asia, New Zealand, Singapore and Japan posted gains, while Hong Kong was in

negative territory. In Europe, all countries posted a positive return and were led by Austria, Italy, and

Sweden. Within North America, the U.S. had negative returns and Canada was positive.

Portfolio performance

The BT Wholesale Global Property Securities Fund returned -1.59% in February (post-fee, pre-tax),

underperforming its benchmark by 0.05%.

The top five contributors this month were Hilton Worlwide, Digital Realty, Realty Income Corp,

Alexander & Baldwin, and Faberge. The top five detractors were Dupont Fabros, Taubman Centers,

Immofinanz Immobilien, American Assets, and Swiss Prime Site.

The North America portfolio returned -3.47% in February before fees, outpacing the UBS U.S. &

Canada Investor’s Index by 8 basis points. Modest outperformance relative to the benchmark was

driven by positive sector allocation results, which were partially offset by negative stock selection

results. In terms of sector allocation, positive results were attributable to the portfolio’s underweight to

the underperforming health care and triple net lease sectors, as well as an overweight to the

outperforming office sector. Regarding stock selection, results were weakest in the regional mall,

office, and health care sectors and were strongest in the shopping centre, apartment, and hotel

sectors. Among the portfolio’s holdings, top individual contributors to relative performance included

overweight positions in outperforming Hilton Worldwide Holdings (HLT) and Alexander & Baldwin

(ALEX), and a lack of exposure to underperforming Digital Realty Trust (DLR). Detractors most

notably included overweight positions in underperforming DuPont Fabros Technology (DFT) and

Taubman Centers (TCO), and a lack of exposure to outperforming SL Green Realty (SLG).

The European portfolio returned 4.25% in February before fees, beating the regional UBS benchmark

by 4 basis points. Outperformance relative to the benchmark was driven by positive stock selection

results, while country allocation results were largely neutral. In terms of stock selection, results were

strongest in the United Kingdom, Germany, and Finland and were weakest in the Switzerland,

France, and Netherlands. Among the portfolio’s holdings, top contributors to relative performance

included a lack of exposure to underperforming Intu Properties Plc. (U.K.) and overweight positions in

Fund Manager Commentary – February 2015 23

outperforming Unite Group Plc. (U.K.) and Fabege AB (Sweden). Detractors most notably included a

lack of exposure to outperforming Immofinanz AG (Austria) and Hufvudstaden AB Class A (Sweden),

and an overweight position in underperforming Gecina SA (France).

The Asian portfolio returned -0.08% in February before fees, lagging the regional UBS benchmark by

18 basis points. Underperformance relative to the benchmark was driven by negative stock selection

results in Hong Kong, Japan, and Singapore. Among the portfolio’s holdings, top detractors to

relative performance included a lack of exposure to outperforming Aeon Mall Co. Ltd. (Japan) and

Mori Trust Sogo REIT (Japan), and an underweight position in outperforming Frontier Real Estate

Investment Corp. (Japan). Contributors most notably included overweight positions in outperforming

Kenedix Retail REIT (Japan) and Mitsui Fudosan Co. Ltd. (Japan), and an underweight position in

underperforming Wharf Holdings Ltd. (Hong Kong). Country allocation results were largely neutral.

Strategy and outlook

North America – With US growth firming, the Federal Reserve ended its bond purchase program in

October and tweaked the “considerable time” language in its policy statement that was seen as

guaranteeing that a Fed Funds rate hike was at least 6 months away. Still, low inflation and anaemic

growth in most other major economies have resulted in extremely low sovereign yields in the rest of

the world, and flows have been moving into dollar denominated assets of all kinds. These flows

pushed the 10 year Treasury yield down from 2.51% to 2.17% during the fourth quarter (and even

lower in the first days of 2015), and while we do expect higher bond yields eventually it is not at all

clear when rates will rise. The Fed continues to maintain that it will be “patient” in normalizing

monetary policy.

This low yield environment has been good to the US REIT sector, as it returned 14.2% during the

fourth quarter alone, capping an extremely strong year where the sector delivered total returns just

over 30%. As of the end of December, US REITs are slightly above long term normalized valuations

but nowhere near the extremes seen in the 2011-12 period. REITs continue to look relatively

expensive versus other equities, slightly above normal versus the underlying real estate and

substantially more attractive than usual versus bonds as REIT dividend yields offer a healthy spread

to bond yields. Along with this yield cushion, earnings growth should offset the impact of slow to

moderate increases in interest rates, though we do expect some volatility in the REIT market near

Fed policy decisions. Going forward, we expect gains to be driven more by these improving earnings

fundamentals than by additional multiple expansion.

Real estate fundamentals continue to support earnings growth for the REITs. Apartment vacancy

levels have levelled off at healthy levels, but vacancy rates in other property types continue to trend

downward slowly. Supply risk continues to be limited on a national level, with only the apartment

sector back to long-term construction averages. A few select office and industrial markets are also

Fund Manager Commentary – February 2015 24

seeing some supply growth, but it is generally being built to fill very strong demand in these same

markets. More encouragingly, rents are now moving up in all property types, and some longer-lease

property types are transitioning into an environment where leases will be signed at higher rents than

the in-place ones, providing a boost to net operating income. We expect high single digit earnings

growth across the REIT sector in 2015.

Europe – The current low interest rate environment is positive for a stable yielding asset class like real

estate. The gap between property yields on the one side and bond yields and real estate financing

costs on the other side continues to be high. The overall risk of declining rents is limited as new

supply of assets is low in most markets. A deflationary environment would be a negative for property

equities in Continental Europe, however, as the leases are linked to inflation. Overall, European

REITs are trading at a 9% premium to net asset values. European REITs offer an attractive, relatively

low risk, and growing earnings yield of 4.8%, and the dividend yield is 3.5% as not all earnings are

paid out as dividends.

Asia – With the strong outperformance by JREITs this year, valuations in Japan are the most

expensive within our investment universe. However, we do expect valuations to remain elevated due

to the Bank of Japan’s purchase program, which acts somewhat as a “back-stop” to share price

performance. The average dividend yield for JREITs is over 250 basis points higher than the

Japanese government bond yield, and this remains an attractive asset class to pure yield investors.

Valuations in the rest of the region are at a small discount to fair value. Property fundamentals remain

positive with strong demand for assets across the region, particularly in Japan and Australia where

cap rates are still trading at an attractive spread over bond yields. This continues to drive cap rate

compression in these countries. Rents are improving as vacancies are showing improvement across

the region, supporting growth in asset values. We expect currency risk to be a likely headwind to U.S.

dollar returns for the region with Asian currencies expected to remain weak.

Fund Manager Commentary – February 2015 25

Active Balanced

Market review

February was a very strong month for equities with the Australian market the S&P/ASX300

Accumulation Index returning +6.9% - its strongest monthly performance since Oct 2011. Resources

(+11.3%) outperformed the market ex-resources (+6.1%) for the first time in six months, led by Metals

& Mining (+12.2%).

Despite a subdued reporting season, the rate cut early in the month buoyed the market to new highs

with yield stocks in particular remaining very attractive.

Global equities also followed a similar path as the MSCI World ex Australia returned 5.27%, driven by

strong performance of European and Japanese markets. The European market was buoyed by the

substantial quantitative easing package announced by the ECB and the promise of support for

markets. This saw many markets outperform strongly including Germany (+6.6%), France (+7.5%),

Italy (+8.9%), Spain (+7.5%). The key to a sustained rally in these markets will be signs of a

sustainable economic recovery and increasing inflation.

The US market continued its strong run in returning a positive 5.5%. However, we did see some profit

taking into month end as concerns started to build about the potential impact of rate rises that seem to

be getting closer and closer to being implemented.

In Asia, Japan did well as with the Nikkei index returning 6.4% driven by signs of an economic

recovery and some of the stimulatory packages starting to take effect. China was solid returning 3.1%

as further stimulus cuts from the PBOC helped drive investor sentiment.

Fixed interest markets were slightly positive in Australia but negative globally as the US bond market

started to price in rising interest rates which saw bond yields increase slightly during the month.

Notwithstanding the RBA rate cut and accompanying comments from Glenn Stevens, the AUD rose

against the USD (+0.6%). More broadly the AUD trade weighted index rose marginally against its

largest trading partners (+0.3%).

Portfolio performance

The BT Wholesale Active Balanced Fund returned 3.13% (post fee, pre-tax) in February,

underperforming its benchmark by 0.44%.

Fund Manager Commentary – February 2015 26

Returns for February were driven by very positive equity markets both domestically and globally and

Australian listed property market driven by the cut in interest rates in Australia and central bank action

in Europe.

For the month the largest contribution was from our Australian equities exposure which delivered a

strong 7.01% which slightly outperformed the index, as some of our key exposures delivered strong

results during earnings season including Qantas, Telstra and Resmed.

Our global equities exposure also added 4.30% although it did underperform the index slightly as our

stock selection in the US underperformed. Our overweight European exposure and emerging markets

exposure did outperform and add value.

From a tactical perspective our overweight global and domestic equities unfortunately did not

compensate from overweight bond and oil and copper positions which detracted, leaving a small

negative contribution for the month from our tactical asset allocation strategy.

.

Strategy and outlook

The focus on the markets now post-reporting season will be on what’s happening offshore - primarily

China and the US - to see if there are any signs of concern for Australian companies and the

economy. Domestically there will also be a strong focus on the RBA.

The Reserve Bank of Australia left the cash rate unchanged at its March meeting although it stated

that further monetary policy easing may be appropriate over the period ahead. The CAPEX survey

highlights the problem facing the Australian economy: mining investment is falling sharply and the

non-mining sector is not picking the slack up as quickly as the Reserve Bank would like. The housing

market, particularly in Sydney, will be causing some concern although the Reserve Bank also stated

that it is working with other regulators to assess and contain risks that may arise from the housing

market.

We expect further monetary policy easing from the Reserve Bank. Should fourth quarter gross

domestic product data released in early March come out weaker than expected further policy easing

could occur as quickly as the April meeting. We do not rule out the cash rate going sub-2% by the end

of the year.

Near term, risk markets will continue to battle headwinds from commodity price weakness, uncertainty

over Greece and shifting expectations on US Fed raising rates. Volatility will be a constant feature

during 2015 and we continue to ensure our portfolio remains well balanced.

Fund Manager Commentary – February 2015 27

Performance as at 28 February 2015

FYTD 1 year 2 Years 3 Years 5 Years Since(pa) (pa) (pa) (pa) Incp. (pa)

Australian Shares - All CapBT Wholesale Core Australian Share Fund APIR - RFA0818AUTotal Return (post-fee, pre-tax) 6.94 12.33 8.94 14.34 16.01 14.21 16.35 9.78 10.63Total Return (pre-fee, pre-tax) 7.00 12.55 9.37 14.94 16.93 15.12 17.28 10.66 11.66Benchmark 6.92 12.62 7.52 12.98 14.19 12.17 15.79 9.55 10.63

BT Wholesale Imputation Fund APIR - RFA0103AUTotal Return (post-fee, pre-tax) 6.50 12.08 8.67 13.98 15.49 12.55 15.10 8.90 10.70Total Return (pre-fee, pre-tax) 6.57 12.33 9.16 14.67 16.53 13.57 16.14 9.89 11.73Benchmark 6.92 12.62 7.52 12.98 14.19 12.17 15.79 9.55 9.44

BT Wholesale Focus Australian Share Fund APIR - RFA0059AUTotal Return (post-fee, pre-tax) 7.41 13.05 10.63 15.91 18.62 16.67 17.39 10.18 9.97Total Return (pre-fee, pre-tax) 7.48 13.27 11.05 16.49 19.52 17.55 18.28 11.04 11.06Benchmark 6.92 12.62 7.52 12.98 14.19 12.17 15.79 9.55 8.24

BT Wholesale Ethical Share Fund APIR - RFA0025AUTotal Return (post-fee, pre-tax) 6.77 13.19 10.45 15.81 17.53 14.26 16.04 9.22 9.27Total Return (pre-fee, pre-tax) 6.85 13.46 10.97 16.54 18.65 15.35 17.14 10.26 10.35Benchmark 6.92 12.62 7.52 12.98 14.19 12.17 15.79 9.55 8.74

Australian Shares - Mid CapBT Wholesale MidCap Fund APIR - BTA0313AUTotal Return (post-fee, pre-tax) 6.20 13.10 12.21 16.91 18.38 16.23 16.39 12.04 9.79Total Return (pre-fee, pre-tax) 6.19 13.38 12.97 17.87 19.88 18.44 18.68 14.11 12.43Benchmark 6.78 13.68 9.45 16.11 17.04 11.64 11.53 8.01 3.30

Australian Shares - Small CapBT Wholesale Smaller Companies Fund APIR - RFA0819AUTotal Return (post-fee, pre-tax) 7.97 8.44 1.44 7.63 6.47 7.70 10.70 11.26 13.53Total Return (pre-fee, pre-tax) 8.07 8.78 2.07 8.52 7.79 9.04 12.09 12.58 14.81Benchmark 8.43 9.93 -0.59 6.73 3.11 -0.31 -1.01 1.42 7.50

Australian Shares - Micro CapBT Wholesale MicroCap Opportunities Fund APIR - RFA0061AUTotal Return (post-fee, pre-tax) 11.23 13.54 10.22 20.20 18.19 19.58 18.28 19.60 19.25Total Return (pre-fee, pre-tax) 12.00 14.98 13.56 24.58 23.34 26.56 24.99 25.99 25.26Benchmark 8.43 9.93 -0.59 6.73 3.11 -0.31 -1.01 1.42 0.86

International SharesBT Wholesale Core Global Share Fund APIR - RFA0821AUTotal Return (post-fee, pre-tax) 4.51 11.99 22.81 24.79 23.11 32.29 27.26 15.65 5.61Total Return (pre-fee, pre-tax) 4.59 12.27 23.41 25.61 24.29 33.56 28.48 16.73 6.79Benchmark 5.27 11.48 22.52 24.21 23.59 31.72 26.43 14.91 7.15PropertyBT Wholesale Property Securities Fund APIR - BTA0061AUTotal Return (post-fee, pre-tax) 3.44 16.01 17.80 25.73 34.85 17.61 22.48 14.80 7.66Total Return (pre-fee, pre-tax) 3.49 16.18 18.18 26.30 35.75 18.38 23.26 15.52 8.50Benchmark 3.69 16.41 17.63 25.53 34.91 18.39 23.13 14.86 7.46

BT Wholesale Global Property Securities Fund APIR - RFA0051AUTotal Return (post-fee, pre-tax) -1.59 7.08 12.97 16.76 25.08 16.49 18.71 17.99 10.95Total Return (pre-fee, pre-tax) -1.52 7.33 13.51 17.50 26.25 17.58 19.82 19.10 11.96Benchmark -1.54 7.60 13.67 17.51 26.90 16.96 19.25 18.64 10.58Fixed InterestBT Wholesale Fixed Interest Fund APIR - RFA0813AUTotal Return (post-fee, pre-tax) -0.07 3.91 6.93 8.32 11.93 6.93 7.38 7.44 7.08Total Return (pre-fee, pre-tax) -0.03 4.04 7.19 8.68 12.49 7.47 7.91 7.94 7.65Benchmark 0.28 3.61 5.58 6.96 10.31 6.63 7.14 7.34 7.20

BT Wholesale Global Fixed Interest Fund APIR - RFA0032AUTotal Return (post-fee, pre-tax) -1.49 2.67 6.45 8.61 11.28 6.87 6.98 7.48 7.03Total Return (pre-fee, pre-tax) -1.45 2.80 6.73 8.99 11.87 7.44 7.53 8.02 7.63Benchmark -0.80 2.84 5.23 7.53 10.46 7.19 7.13 8.11 7.88

BT Wholesale Enhanced Credit Fund APIR - RFA0100AUTotal Return (post-fee, pre-tax) 0.48 3.11 4.52 5.73 8.72 6.59 7.59 7.56 6.26Total Return (pre-fee, pre-tax) 0.51 3.23 4.76 6.05 9.21 7.07 8.07 8.04 6.80Benchmark 0.53 3.23 4.66 5.88 8.71 6.55 7.45 7.42 6.39Cash & IncomeBT Wholesale Enhanced Cash Fund APIR - WFS0377AUTotal Return (post-fee, pre-tax) 0.22 0.75 1.51 2.06 3.34 3.34 4.21 4.99 5.28Total Return (pre-fee, pre-tax) 0.24 0.82 1.64 2.23 3.59 3.60 4.47 5.25 5.64Benchmark 0.21 0.69 1.36 1.83 2.73 2.76 3.08 3.79 5.32

BT Wholesale Managed Cash Fund APIR - WFS0245AUTotal Return (post-fee, pre-tax) 0.19 0.64 1.28 1.72 2.59 2.69 3.02 3.73 6.95Total Return (pre-fee, pre-tax) 0.21 0.69 1.39 1.87 2.82 2.91 3.25 3.95 7.26Benchmark 0.21 0.69 1.36 1.83 2.73 2.76 3.08 3.79 7.04

BT Wholesale Monthly Income Plus Fund APIR - BTA0318AUTotal Return (post-fee, pre-tax) 0.84 3.63 4.58 6.44 8.26 6.78 7.08 6.26 6.70Total Return (pre-fee, pre-tax) 0.89 3.80 4.92 6.90 8.97 7.49 7.78 6.90 7.36Benchmark 0.17 0.60 1.23 1.66 2.51 2.60 2.92 3.62 3.59

DiversifiedBT Wholesale Active Balanced Fund APIR - RFA0815AUTotal Return (post-fee, pre-tax) 3.13 9.19 11.68 14.91 16.92 14.52 14.43 9.70 8.04Total Return (pre-fee, pre-tax) 3.20 9.45 12.21 15.64 18.04 15.61 15.52 10.74 9.13Benchmark 3.57 8.17 8.85 12.09 14.23 12.63 13.51 9.50 7.76

(%)1 Month 3 Months 6 Months

For more information Please call 1800 813 886, contact your Business Development Representative or visit btim.com.au

All returns calculated by BT Investment Management (Fund Services) Limited, ABN 13 161 249 332, AFSL 431426 (BTIM). No part

of this Fund Manager Commentary (Commentary) is to be circulated without this page attached.

This Commentary is dated 13 March 2015 and has been prepared by BTIM. The information in this Commentary is for general

information only and should not be considered as a comprehensive statement on any of the matters described and should not be

relied upon as such. The information contained in this Commentary may contain material provided directly by third parties and is

believed to be accurate at its issue date. While such material is published with necessary permission, neither BTIM nor any

company in the Westpac Group of companies accepts any responsibility for the accuracy or completeness of this information or

otherwise endorses or accepts any responsibility for this information. Except where contrary to law, BTIM intends by this notice to

exclude liability for this material.

This Commentary has been prepared without taking into account your objectives, financial situation or needs. Furthermore, it is not

intended to be relied upon for the purpose of making investment decisions and is not a replacement of the requirement for individual

research or professional tax advice. Because of this, before acting on this information, you should seek independent financial and

taxation advice to determine its appropriateness having regard to your individual objectives, financial situation and needs.

BTIM does not give any warranty as to the accuracy, reliability or completeness of the information contained in this Commentary.

This Commentary is not to be published without the prior written consent of BTIM. An investment in the portfolios referred to in this

Commentary is not an investment in, deposit with or any other liability of the Westpac Banking Corporation (ABN 33 007 457 141)

(the Bank) or any other company in the Westpac Group of companies. BTIM is a member of the Westpac Group. An investment in

the funds is subject to investment risk, including possible delays in repayment of withdrawal proceeds and loss of income and

principal invested. Neither the Bank, BTIM nor any other company in the Westpac Group stands behind or otherwise guarantees

the capital value or investment performance of the funds or any particular rate of return.

Performance data (post-fee) assumes reinvestment of distributions and is calculated using exit prices, net of management costs.

Performance data (pre-fee) is calculated by adding back management costs to the (post-fee) performance. Past performance is not

a reliable indicator of future performance. The term ‘benchmark’ refers to the index or measurements used by an investment

manager to assess the relative risk and the performance of an investment portfolio.

BTIM is the issuer of the following products:

BT Wholesale Core Australian Share Fund

BT Wholesale Imputation Fund

BT Wholesale Focus Australian Share Fund

BT Wholesale Ethical Share Fund

BT Wholesale Smaller Companies Fund

BT Wholesale MidCap Fund

BT Wholesale Core Global Share Fund#

BT Wholesale Global Fixed Interest Fund

BT Wholesale Enhanced Credit Fund

BT Wholesale Fixed Interest Fund

BT Wholesale Property Investment Fund

BT Wholesale Global Property Securities Fund

BT Wholesale Managed Cash Fund

BT Wholesale Enhanced Cash Fund

BT Wholesale Active Balanced Fund

A product disclosure statement (PDS) is available for each of the above products and can be

obtained by contacting BTIM on 1800 813 886, by visiting btim.com.au. You should consider

the relevant PDS in deciding whether to acquire, or to continue to hold, the product. BT® is a

registered trade mark of BT Financial Group Pty Ltd and is used under licence.

# AQR began managing international equity for BT Financial Group in June 2006.