full year results…navitas fy17 full year results presentation – 30 june ... navitas ventures ......

TRANSCRIPT

FULL YEAR RESULTSFor the year ended 30 June 2017

2

• Key Highlights

• Financial Performance

• Strategy and Outlook

Navitas FY17 Full Year Results Presentation – 30 June 2017

Agenda

3

Growth

Navitas FY17 Full Year Results Presentation – 30 June 2017

Continued delivery of strong student experience and

academic outcomes

Creation of the Careers and Industry

Division

Operations streamlined and shared service

implementation progressed

New agreements with University of Idaho and Richard Bland College

signed in the US

5 University Partnership contracts

renewed

Quality Efficiency

170 basis point increase in Careers and Industry

EBITDA margin

Navitas Ventures launched

Average University Pass rates 82%, Retention

87%, Progression 94%

Key Highlights

5% enrolment growth for University Partnerships

4

1. Group revenue decreased by 5%

2. 5% full time enrolment CAGR in FY17

3. KPI commences in FY18

Group KPI’s for 2020 – Update

2020 Target FY17

Quality

Efficiency

Growth

1. Pass rates to 84%1

2. Retention rates to 90%1

1. 18% Group EBITDA Margin

2. 20% SAE EBITDA Margin

3. Annual capex under $20m

1. 5%2 revenue CAGR

2. 5% full time enrolment CAGR

3. 5 new university partnerships

1. Pass rates of 82%

2. Retention rates of 87%

1. Group EBITDA margin flat at 16.3%

2. SAE EBITDA Margin up 80 bps to 14.9%

3. KPI commences in FY18

2 Note: Based on constant currency and CAGR calculated assuming AMEPrevenue reduction excluded from FY17 to FY20. This reduces to 3% CAGRagainst FY17 Group revenue if AMEP revenue is included

1 University Partnerships Division only

Navitas FY17 Full Year Results Presentation – 30 June 2017

Metric

5

University Partnerships strategy

High pass, retention and progression-to-university rates maintained

Uni South Australia, Adelaide, Hertfordshire, Manitoba and Deakin contracts renewed

Optimal College model completed in Australia and North America

Sales and Marketing transformation started

New programs in Engineering, Health Sciences, Business and Sports Science

English language programs and Internships business now integrated

Signed new agreements with the University of Idaho and Richard Bland College

Strong Business Development pipeline Edith Cowan College converted to Joint

Venture model

Navitas FY17 Full Year Results Presentation – 30 June 2017

Extend and enhance

contracts, services and

student outcomes

Grow, retain and support

partners

Develop new products

Continue to improve/maintain high pass, retention and progression rates

Renew all due contracts – Anglia Ruskin University (Nov), Swansea University (Nov) Curtin University (Curtin College - Dec, Singapore – Mar), Brunel (Jan)

Complete Optimal College model in Europe Complete Sales and Marketing

transformation – includes recruitment tech Improve Division efficiency and margin

Expand new programs and products to partners

Explore pathways-to-employment and work integrated learning

Sign new university partners Explore a variety of models to suit different

needs of university partners Develop and target transformation offerings

for partners

VISION - Become the preferred transformation partner to universities around the world

Initiative FY18 FocusFY17 Progress

6

Careers and Industry strategy

Navitas FY17 Full Year Results Presentation – 30 June 2017

Finalise Careers and Industry operational restructure and deliver full integration benefits

Keep improving academic and student experience outcomes

Gain approval for >20 new US programs Develop efficiencies across the Division

New segments developed and expanded Further develop online capability Build or acquire high quality borderless

education organisations aligned to vertical segments

Explore further SAE licensing opportunities

VISION - Provide students with a quality, valued education in segments with strong employment prospects

Initiative FY18 FocusFY17 Progress

Careers and Industry restructure now largely complete

Aligned sectors around Creative, Government Services, Human Services and Health created

4 sub-scale SAE campuses exited

Strong academic & student experience outcomes

SAE US product expansion progressing – 15 new programs approved for delivery

ACAP awarded self-accrediting status SAE and ACAP receive VET Student Loan

accreditation

Market research commenced to identify appropriate new segments

Screening commenced for quality entry options (organic/inorganic)

Partner with Navitas Ventures to explore borderless opportunities

Refocus into industry aligned

vertical segments

Develop future business

opportunities

Increase performance of core – including

academic outcomes

7

Navitas Ventures investing in the future

Navitas FY17 Full Year Results Presentation – 30 June 2017

Projects and initiatives underway - ~$2.5 invested in FY17

Incubation Investment Partnerships

Online career centre. Supporting international students to secure internships

and jobs in the US.

Artificial Intelligence powered language coaching for Chinese students

Using Blockchain to issue and manage education credentials SaaS platform connecting agents, students

and University admissions teams.

Online synchronous, unaccredited management and leadership skills.

Pathways to post-graduate education.

Australia’s Edtech Acceleration Network for Scalable Borderless Education.

8

FINANCIAL PERFORMANCE

David Buckingham CFO

9

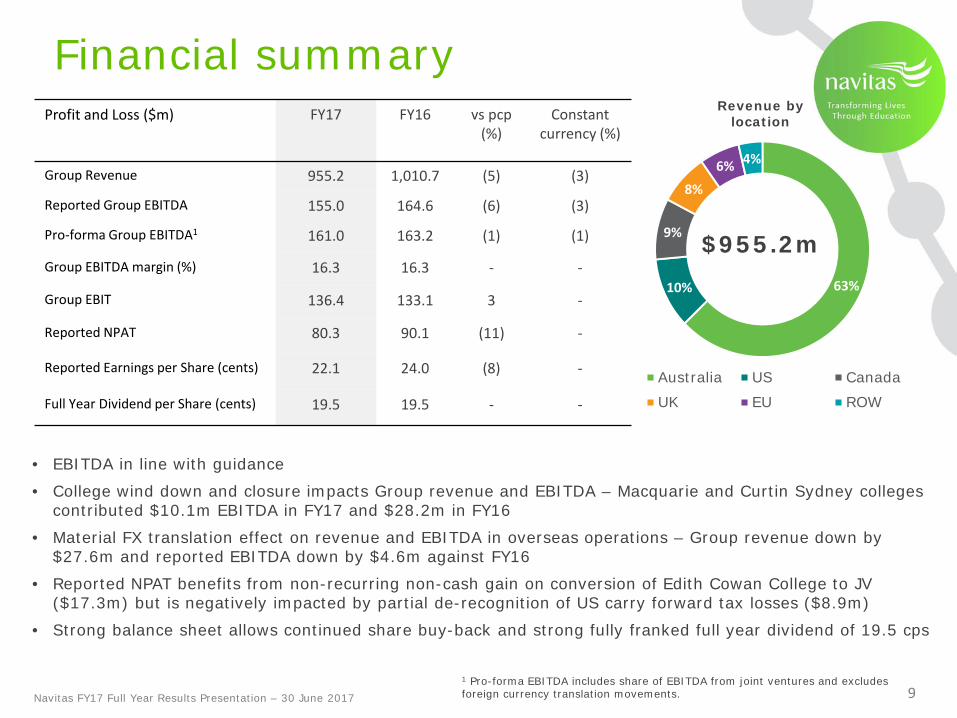

Profit and Loss ($m) FY17 FY16 vs pcp(%)

Constant currency (%)

Group Revenue 955.2 1,010.7 (5) (3)

Reported Group EBITDA 155.0 164.6 (6) (3)

Pro-forma Group EBITDA1 161.0 163.2 (1) (1)

Group EBITDA margin (%) 16.3 16.3 - -

Group EBIT 136.4 133.1 3 -

Reported NPAT 80.3 90.1 (11) -

Reported Earnings per Share (cents) 22.1 24.0 (8) -

Full Year Dividend per Share (cents) 19.5 19.5 - -

Financial summary

Navitas FY17 Full Year Results Presentation – 30 June 2017

• EBITDA in line with guidance

• College wind down and closure impacts Group revenue and EBITDA – Macquarie and Curtin Sydney colleges contributed $10.1m EBITDA in FY17 and $28.2m in FY16

• Material FX translation effect on revenue and EBITDA in overseas operations – Group revenue down by $27.6m and reported EBITDA down by $4.6m against FY16

• Reported NPAT benefits from non-recurring non-cash gain on conversion of Edith Cowan College to JV ($17.3m) but is negatively impacted by partial de-recognition of US carry forward tax losses ($8.9m)

• Strong balance sheet allows continued share buy-back and strong fully franked full year dividend of 19.5 cps

1 Pro-forma EBITDA includes share of EBITDA from joint ventures and excludes foreign currency translation movements.

Revenue by location

63%10%

9%

8%

6% 4%

Australia US CanadaUK EU ROW

$955.2m

10

Stable University Partnerships margin

Navitas FY17 Full Year Results Presentation – 30 June 2017Note 1. $64.3m of revenue and $9.7m of EBITDA reclassified to University Partnerships in FY16 following the restructuring of ELICOS colleges to the Division. All comparative periods adjusted accordingly.

• Results impacted by the final wind down and closure of Macquarie and Curtin Sydney colleges, tough UK environment, conversion of a college to a JV ($17.3m revenue reduction vs pcp) and adverse FX translation movements

• Underlying EFTSU increased 5% and price by 2.5% in FY17

• Margin impacted by closure of colleges

• New colleges with the University of Idaho and Richard Bland College in the US

• 5 contracts renewed and Edith Cowan College converted to a Joint Venture

• Implementation of optimal college model to standardise and enhance best practice

FY17 Revenue Distribution

FY17 FY161 vs pcp (%) Constant currency

(%)

Revenue ($m) 574.1 635.4 (10) (7)

EBITDA ($m) 131.3 146.9 (11) (8)

Margin (%) 22.9 23.167%

22%

11%

Australasia North America Europe

$574.1m

11

University Partnerships enrolments increase 8% in semester 2 2017

Prior periods exclude the Equivalent Full Time Student Unit (EFTSU) of closed colleges – see prior ASX announcements for more detailsNavitas FY17 Full Year Results Presentation – 30 June 2017

• North American enrolments flat compared to pcp with growth in Canada offset by decline in the US

• Overall demand remains strong for both countries but US visa rejection rates increased under the new US administration

• UK enrolments drop 3% in semester 2 2017 - traditionally small semester• Regulatory environment continues to be restrictive

• 16% growth in Australasian colleges• Growth enabled by ongoing demand for Australian and NZ universities and

stable regulatory regime

14,0

36 15,9

91

13,5

46

14,6

76

17,6

79

14,3

29

14,9

73

19,0

47

15,5

19

0%

2%

4%

6%

8%

10%

12%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

1403 1501 1502 1503 1601 1602 1603 1701 1702

University Partnerships EFTSU

EFTSU Growth rate

12

Careers and Industry improves margin

Navitas FY17 Full Year Results Presentation – 30 June 2017

• Division created in FY17 from merger of SAE and Professional and English Programs

• SAE revenue growth masked by adverse foreign currency movements. Revenue growth in several core markets. Strong Australian result despite some impact from changed Vocational funding rules

• Margin growth of 170 bps driven by one-off increase in AMEP clients and effective cost control

• New SAE campus in Germany and expansion into Canada

• SAE campuses relocated or refurbished to allow growth – Sydney, Berlin, Hamburg, Paris, London

• Reduced AMEP contracts in retender – FY18 EBITDA to decrease by $14.0m from 1 July 2017

• Recent UK Court of Appeal rejection of SAE VAT case, appeal being considered. $5.0m outstanding liability paid in H1 FY17 and $3.0m expense incurred in FY17. UK business already restructured.

FY17 Revenue Distribution

FY17 FY16 vs pcp(%)

Constant currency (%)

Professional and English Programs revenue ($m)

174.4 165.6 5 N/A

SAE revenue ($m) 200.7 202.8 (1) 3

Careers and Industry revenue ($m) 375.1 368.4 2 4

Professional and English Programs EBITDA ($m)

31.1 25.4 22 22

SAE EBITDA ($m) 29.9 28.5 5 5

Careers and Industry EBITDA ($m) 61.0 53.9 13 13

Professional and English Programs margin (%)

17.8 15.4

SAE margin (%) 14.9 14.1

Careers and Industry margin (%) 16.3 14.6

35%

32%

19%

10%4%

Australia US GSA SW EU UK

$375.1m

13

Cash flow and key debt metrics

Navitas FY17 Full Year Results Presentation – 30 June 2017

• Operating cash flow impacted heavily in H1 FY17 by unwind of deferred revenues relating to closing colleges, conversion of a college to a JV and make good payments to exit old Sydney property.

o H2 FY17 net working capital returned to normalised level of $1.1m• Gross capex of $81.7m – net capex of $44.1m after lease incentive of $37.6m for new Sydney

premises o Capex expected to drop to <$20.0m in FY18

• Closing net debt of $186.0m (FY16: $56.2m)• Gearing ratio of 1.48 x, interest cover of 26.8x• Net cash of $86.6m includes $41.7m of cash in the Tuition Protection Service• Buy-back 69% complete - $69.8m spend in FY17

($m) FY17 FY16

EBITDA 155.0 164.6

Net working capital (47.5) 1.4

Lease incentive contributions 37.6 9.8

Tax (37.8) (46.3)

Net interest (5.8) (3.7)

Operating cash flow 101.5 125.8

Capex (81.7) (43.7)

Disposal of subsidiary cash (8.2) (1.2)

Other investments (3.2) (0.8)

Net cash flow before financing 8.4 80.1

14NAVITAS FY17 FULL YEAR RESULTS PRESENTATION – 30 JUNE 2017

STRATEGY AND OUTLOOK

Rod Jones, Group CEO

15

MEASURES OF SUCCESS

VISION

PURPOSE

Transform lives by increasing student access to quality tertiary education

Conviction Drive Adventurous Rigour Genuine Respect

To be universally recognised as one of the world’s most trusted learning organisation

UNIVERSITY PARTNERSHIP (UP) BUSINESSES

The preferred transformation partner to universities around the world

CAREERS AND INDUSTRY (CI) BUSINESSES

Providing students with a quality, valued education in segments with strong

employment prospects

Australasia North America Europe Creative Human

ServicesGovt.

Programs Health Incubation Investment Partnerships

NAVITAS VENTURES

Scaling ideas and growing teams that unleash human potential and transform the way the

world learns

EBITDAMargin

Partner NPS

Contract renewal

Student progression

Employee engagement

Senior retention New partners EBITDA EVAEFTSUStudent

commencements

WORLD CLASS QUALITY

LEADINGEFFICIENCY

SUSTAINABLEGROWTH

Clear strategic direction –aligned with operational goals

Navitas FY17 Full Year Results Presentation – 30 June 2017

2020 TARGETSPass rates Retention

ratesGrp EBITDA

marginSAE EBITDA

marginCapex per

annumRevenue

CAGRNew UP

Agreemt’sUP EFTSU

CAGR

16

Repositioning Navitas

Navitas FY17 Full Year Results Presentation – 30 June 2017

HORIZON

FY16 – FY17SIMPLIFICATION• Continue to focus on student

outcomes and experience• Establish global integrated and

simplified structure• Prioritise projects and initiatives• Establish new capabilities, both people

and operationally

FY18 – FY20EXPANSION• Build strong Australasian position • Secure NA and EU markets• Build beyond pathways with

University Partners on multiple agendas

• Consolidate industry focused offerings with new Careers and Industry division

• Growth and innovation through new Ventures

FY20+ENDURANCE• Repositioned University Partnerships

working on internationalisation, digitisation and supporting agendas

• Long-term industry partnerships developed with multiple offerings

• Ventures delivering new core offerings for growth and diversification, driving innovation and mitigating disruption

1

HORIZON 3

HORIZON 2

17

• Demand for education services growing globally despite uncertainty in some markets

• Navitas well positioned with a track record of delivering quality outcomes, a global network and a strong innovation pipeline now in place

• No income from closed colleges in FY18

• C&I EBITDA to decrease $14.0m from 1 July 2017 following AMEP retender

• Navitas 2020 growth targets

o 5% Group CAGR revenue

o 18% Group EBITDA margin

o 5% University Partnerships enrolment CAGR

o <$20.0m capex per annum

Outlook

Navitas FY17 Full Year Results Presentation – 30 June 2017

18

APPENDIX

19

Navitas – a globally diverse education provider

US RevenueFY13 - 3.8%

FY17 - 10.5%

ROW RevenueFY13 - 6.6%FY17 - 3.7%

EU RevenueFY13 - 6.1%FY17 - 6.0%

UK RevenueFY13 - 6.6%FY17 - 7.7%

Canada Revenue

FY13 - 5.9%FY17 - 9.2%

Aus RevenueFY13 - 71.1%FY17 - 62.9%

FY17 Group revenue $955.2mFY13 Group revenue $729.6m

20

Careers and Industry DivisionUniversity Partnerships Division

Navitas Ventures

Navitas Corporate

Navitas’ PurposeTransform lives by increasing student access to quality tertiary education

Navitas FY17 Full Year Results Presentation – 30 June 2017

The University Partnerships Division is a leading provider of pre-university and university

pathway programs with 34 colleges across Australia, US, UK, Canada,

NZ and Sri Lanka

The Careers and Industry Division provides industry focused vocational

and higher education programs across the Creative, Health, Human Services and Government Services

segments

Navitas Ventures scales ideas and invest in new education models and technology

Navitas (ASX: NVT) is a leading global education provider with over 120 colleges and campuses across 31 countries offering an extensive range of

educational services to students, clients and professionals. Navitas is an ASX200 company.

% of FY17 Group Revenue

60% 40%

% of FY17 Group Revenue

About Navitas

21

Market summary for external pathway programs

Source: Global flow of tertiary level students, UNESCO Institute of Statistics; US Dept of Education; Australian Dept of Education and Training; UK Dept of Business, Innovation and Skills; Global Affairs Canada.

Navitas FY17 Full Year Results Presentation – 30 June 2017

Australia• 39 universities• ~20 pathway colleges – 12 Navitas• 266k international tertiary students• International enrolments as a % of students –

18%• Government strategy – increase total

international enrolments by 45% to 720k by 2025

UK• 130 universities• ~55 pathway colleges – 10 Navitas• 428k international tertiary students• International enrolments as a % of students –

18.0%• Government strategy – increase sector value

by 66% to GBP30b by 2020

US• ~2,000 universities• ~55 pathway colleges - 7 Navitas• 842k international tertiary students• International enrolments as a % of students –

4%• Government strategy – focused on domestic

benefits, no targets

Canada• 49 universities• 2 pathway colleges – both Navitas• 151k international tertiary students• International enrolments as a % of students –

10.0%• Government strategy – increase total

international enrolments by 34% to 450k by 2022

Demand for international education continues to grow due to increases in population and middle class wealth in developing countries while investment in tertiary infrastructure lags

GLOBAL

22

Financial metrics

980.3878.2

731.7688.5643.8556.7

470.7345.4

955.21,010.7

FY11FY10FY09FY08 FY15FY14FY13FY12 FY17FY16

80.390.1

71.8

51.6

74.673.177.464.3

49.237.4

FY12FY11FY10FY09 FY16FY15FY14FY13 FY17FY08

Revenue ($m)

Underlying EBITDA ($m)155.0

164.6163.1144.9

130.0126.8121.196.7

77.163.4

FY17FY16FY15FY14FY13FY12FY11FY10FY09FY08

Reported NPAT ($m)

33.937.737.5

33.8

19.718.5

25.330.5

22.928.3

FY17FY16FY15FY14FY13FY12FY11FY10FY09FY08

19.519.519.519.519.520.7

18.8

14.310.9

19.5

FY17FY08 FY16FY15FY14FY13FY12FY11FY10FY09

Operating cash flow (cps)

Reported Earnings (cps)22.1

24.0

19.1

13.7

19.919.521.7

18.8

14.310.8

FY17FY13FY12FY11FY10FY09FY08 FY16FY15FY14

Dividends (cps)

Navitas FY17 Full Year Results Presentation – 30 June 2017

23

Detailed P&L – 5 years

Navitas FY17 Full Year Results Presentation – 30 June 2017

Navitas Ltd GrowthFY13 FY14 FY15 FY16 FY17 CAGR*

Operating RevenueUP 474,952 560,551 628,219 635,411 574,129 5%SAE 114,934 150,319 185,450 202,822 200,662 15%PEP 137,138 162,848 162,130 165,618 174,392 6%Corporate 2,537 2,255 2,342 4,584 4,321 14%

Total operating revenue 729,561 875,973 978,141 1,008,435 953,504 7%

Expenses (599,559) (731,044) (815,034) (843,854) (798,456) 7%

Underlying EBITDA # 130,002 144,929 163,107 164,581 155,048 5%

Depreciation (15,492) (24,593) (27,318) (30,767) (32,259) 20%

Underlying EBITA # 114,510 120,336 135,789 133,814 122,789 2%

Amortisation (863) (749) (749) (749) (604) -9%

Underlying EBIT # 113,647 119,587 135,040 133,065 122,185 2%

Net Interest (paid)/received (7,590) (6,238) (3,823) (3,998) (5,778) -7%Share of equity accounted JV profits (losses) - - - (974) 271 n/a

Underlying net profit before tax # 106,057 113,349 131,217 128,093 116,678 2%

Income tax (31,006) (32,099) (39,564) (37,330) (50,072) 13%

Underlying NPAT # 75,051 81,250 91,653 90,763 66,606 -3%

Outside equity interest (476) 782 (301) (685) (532) 3%

Underlying NPAT attributable to Navitas # 74,575 82,032 91,352 90,078 66,074 -3%

Statutory NPAT 75,051 50,802 72,111 90,763 80,869 2%Statutory NPAT attributable to members 74,575 51,584 71,810 90,078 80,337 2%

# excluding impairment of goodwill and one off gains* Cumulative Annual Growth Rate from FY13 to FY17

24

ACAP – Australian College of Applied Psychology

AMEP – Adult Migrant English Program

ASX – Australian Securities Exchange

C&I – Careers and Industry

CPS – Cents Per Share

EFS – English and Foundation Skills

EBITDA – Earnings Before Interest Tax, Depreciation and Amortisation

ELICOS – English Language Intensive Courses for Overseas Students

HE – Higher Education

HSA – Health Skills Australia

NCPS – Navitas College of Public Safety

NPAT – Net Profit After Tax

PCP – Prior Corresponding Period

PEP – Professional and English Programs

SAE – School of Audio Engineering, now known as SAE

SAIBT – South Australian Institute of Business and Technology

SEE – Skills for Education and Employment

SSVF – Simplified Student Visa Framework

TEQSA – Tertiary Education Quality Standards Agency

UP – University Partnerships

VET – Vocational Education and Training

VFH – VET FEE-HELP

VSL – VET Student Loan

WACC – Weighted Average Cost of Capital

Glossary

Navitas FY17 Full Year Results Presentation – 30 June 2017

25

Disclaimer• This document has been prepared by Navitas Limited ABN 69 109 613 309 ("Navitas" or the "Company").

Information in this document should be read in conjunction with other Navitas announcements made to theASX and available at www.navitas.com or www.asx.com. By accessing or attending this presentation youacknowledge that you have read, understood and agree with the following statements.

• This document has been prepared for information purposes only and does not take into account yourindividual investment objectives, including the merits and risks involved in an investment in Navitas shares,or your financial situation or particular needs, and is not investment, financial product, legal, tax oraccounting advice or opinion.

• You should make your own independent investigation and assessment of Navitas and its shares and obtainany professional advice you require before making any investment decision based on your investmentobjectives and financial circumstances. An investment in Navitas shares is subject to investment and otherknown and unknown risks, some of which are beyond the control of Navitas, including possible delays inrepayment and loss of income and principal invested. Navitas does not guarantee any particular rate ofreturn or the performance of Navitas, nor does it guarantee the repayment of capital from Navitas or anyparticular tax treatment.

• No representation, warranty or guarantee, express or implied, is made by Navitas, its subsidiaries or theirrespective directors, officers, employees or agents, nor any other person (the “Beneficiaries”) as to thefairness, accuracy, completeness, reliability or correctness of the information, opinions and conclusionscontained in this document (including, without limitation, any estimates, calculations, projections orforward looking statements). No action should be taken on the basis of the information, and no reliancemay be placed for any purpose on the accuracy or completeness of the information or opinions contained inthis document. To the maximum extent permitted by law, the Beneficiaries exclude and disclaim all liability,including, without limitation, any liability arising from fault or negligence, for any direct or indirect loss ordamage which may be suffered by any person through relying on anything contained in or omitted fromthis document.

• The distribution of this document in jurisdictions other than Australia may also be restricted by law and anysuch restrictions should be observed. Any failure to comply with such restrictions may constitute a violationof applicable securities laws.

• This document does not constitute an offer, invitation, solicitation, advice or recommendation with respectto the issue, purchase or sale of Navitas shares in any jurisdiction.

• All references to dollars, cents or $ in this document are to Australian currency, unless otherwise stated.

Navitas FY17 Full Year Results Presentation – 30 June 2017