fruit juices and soft drinks bottler for retailers and a

TRANSCRIPT

Annual Report 2012

Fruit juices and soft drinks

bottler for retailers and

A-brands

Refresco • Annual Report 20122

www.refresco.com

Refresco • Annual Report 2012 3

Fruit juices and soft drinks

bottler for retailers and

A-brands

We bring total supply chain solutions to our customers

Refresco • Annual Report 20124

Refresco • Annual Report 2012 5

Contents

Refresco at a Glance Our company 8 Our strategy 9 Key developments in 2012 10 Our locations in Europe 12

Executive Board Report 2012 Foreword 16 Business review 18 Financial performance 24 Prospects for 2013 28 Sustainability 30

Governance Governance structure 36 Executive Board and Supervisory Board 40 Risks 42

Supervisory Board Report 2012 50

Financial Review 2012 Financial Statements 58 Independent Auditor’s Report 116 Ten Years Refresco 117

Contact us 118

Refresco • Annual Report 20126

Refresco at a Glance

Refresco • Annual Report 2012 7

Refresco at a Glance

Our company

We manufacture high quality products in nine countries in Europe. Our key competencies are the manufacture of an extensive range of product and packaging combinations, managing effective supply chains and the development of innovative new products.

Our customersOur customers are leading European retailers and well- known brands (A-brands). We focus on developing tailor-made approaches to hard discounters, buying platforms and full service retailers. To maintain our path of growth, we aim to leverage the on-going trend among A-brands towards outsourcing their production by offering them a pan-European manufacturing platform with efficient supply chains and high quality standards.

Our productsWe manufacture a full range of soft drinks and fruit juices. Our product range includes a wide variety of fruit juices, carbonated soft drinks, ready-to-drink teas, functional/still drinks, energy drinks, sport drinks, waters, and other specialty drinks in a wide range of packaging.

Our peopleWe employ over 3,000 people throughout Europe. Our size brings economies of scale, but it is the ability of our highly skilled people to seize market opportunities and streamline operational processes that makes the difference.

Our MissionOur mission is to be the most reliable and cost effective bottler of soft drinks and fruit juices for leading European retailers and international A-brands and our ambition is to consistently increase the value of our business for the benefit of all our stakeholders. In close liaison with our customers and suppliers, we strive continuously to innovate, optimize, and further improve the sustainability of our supply chain.

Our VisionOur vision is to continue to grow our leading position in the highly fragmented European market. We operate on a local-for-local basis while, at the same time, sharing inter na tional back office support, purchasing power, latest production technology, product and process innovation, and financial resources for expansion. Reliability, quality, and cost competitiveness are crucial to our customers, and they remain our guiding principles in growing our business.

Refresco • Annual Report 20128

Refresco valuesEntrepreneurship,

No-nonsense, Teamwork,

Spirit, Focus.

Our strategy

Our strategy is to maintain and further grow our position as the preferred bottler of soft drinks and fruit juices to retailers and A-brand customers across Europe. We focus on healthy organic growth and on highly selective acquisitions.

Grow with our customersWe aim to expand our customer relationships by providing them with a wide range of product and packaging combi nations and total supply chain solutions in multiple geo graphies. We focus on providing high customer service as well as core innovations through the introduction of new packages, flavors, and varieties of soft drinks and fruit juices. We seek to expand our contract manufacturing business through an increasing number of exclusive long-term supply contracts for particular products and regions, enabling more and more A-brands to focus on brands and marketing rather than on manufacturing. By maintaining close relationships with our customers, we seek to grow with them as they expand their own businesses. We aim to achieve these goals through a combination of reliability, cost price leadership, high-quality product, production flexibility, smart market approaches, and good new product development programs.

We continue to invest in improving production flexibility and cost efficiency in our manufacturing and warehousing operations. We also continue to seek ways to consolidate our

manufacturing footprint in order to maximize utilization of production lines and to optimize economies of scale in production, purchasing, and distribution.

Buy & BuildSince its incorporation in 2000, Refresco has pursued a Buy & Build strategy. Our acquisitions are highly selective and focus on contributing to customer service, economies of scale, and cost effectiveness. They broaden our European presence, expand our product range, and add bottling capacity.

Work towards sustainabilityWe are committed to continuously improving our performance in the area of sustainability. We assess and implement alternative supply chain solutions, raw materials, packaging, and manufacturing processes to improve sustainability of our operations. Our customers expect Refresco to maintain high quality standards and to be innovative and cost-competitive. We expect the same from our suppliers. We work towards managing and reducing the environmental impact of our operations by focusing on energy, water, packaging, and waste. We never compromise on product quality and food safety or on a safe workplace.

Strategic integration: In addition to managing our production

processes efficiently, we partner closely with our customers in the

areas of purchasing, supply chain planning and execution, new product

development, and service.

Refresco • Annual Report 2012 9

Refresco • Annual Report 201210

Refresco at a Glance

Key developments in 2012

• Throughout the year we have taken the deliberate decision to focus on the better contributing volumes and the high growth segments of our business, and this has led to improvement in our financial performance.

• We made significant investments in four new bottling lines in Benelux and Italy to add capacity and to meet our customers’ changing needs and requirements.

• In line with our strategy, we were pleased to take on board a number of new contract manufacturing customers, which will support ongoing organic growth in 2013.

• The Group’s revenues were broadly in line with prior year. Our volumes fell from last year reflecting our commercial decision in late 2011 to let go volumes in the lower margin product categories.

• We completed the integration of Spumador, the largest Italian producer of carbonated soft drinks and water, into Refresco’s governance structure and purchasing schemes.

• We acquired Taja Sp. z o.o., a Polish private label manufacturer of carbonated soft drinks and water, thereby increasing our capacity in the fast growing Polish private label market.

• Rightsizings in Iberia, Italy, and the UK were completed to meet local market conditions and to improve our competitive positions in these markets.

Key performance indicators • Liters produced: 4,943.9 million

(2011: 4,956.6 million)• Revenue: EUR 1,538.3 million

(2011: EUR 1,523.4 million)• Adjusted EBITDA*: EUR 115.5 million

(2011: EUR 111.0 million)• Gross profit margin per liter: 11.7 euro cents

(2011: 11.6 euro cents)• Net cash flow from operating activities: EUR 49.6 million

(2011: EUR 41.8 million)• Net loss: EUR 18.2 million

(2011: EUR 25.9 million)

Refresco • Annual Report 2012 11

6,000

5,000

4,000

3,000

2,000

1,000

0

2008 2009 2010 2011 2012

1,600

1,400

1,200

1,000

800

600

400

200

0

2008 2009 2010 2011 2012

140

120

100

80

60

40

20

0

2008 2009 2010 2011 2012

6,000

5,000

4,000

3,000

2,000

1,000

0

2008 2009 2010 2011 2012

1,600

1,400

1,200

1,000

800

600

400

200

0

2008 2009 2010 2011 2012

140

120

100

80

60

40

20

0

2008 2009 2010 2011 2012

6,000

5,000

4,000

3,000

2,000

1,000

0

2008 2009 2010 2011 2012

1,600

1,400

1,200

1,000

800

600

400

200

0

2008 2009 2010 2011 2012

140

120

100

80

60

40

20

0

2008 2009 2010 2011 2012

Volume (in millions of liters)

* Reconciliation from operating profit to adjusted EBITDA is presented on page 26.

Adjusted EBITDA is not a measure of our financial performance under IFRS,

see page 119. We apply adjusted EBITDA to exclude the effects of certain

exceptional charges that we believe are not indicative of our underlying

operating performance. Such adjustments relate primarily to substantial one-off

restructurings, refinancing costs and costs relating to acquisitions or disposals.

Revenue (EUR millions)

Adjusted EBITDA* (EUR millions)

12 Refresco • Annual Report 2012

Refresco at a Glance

Our locations in Europe

Iberia

Poland

Germany

United Kingdom

France

Italy

Benelux

Refresco GroupRotterdam, The Netherlands

13Refresco • Annual Report 2012

Finland

Benelux

• Maarheeze (NL)

• Bodegraven (NL)

• Hoensbroek (NL)

• Ninove (BE)

Italy

• Caslino al Piano

• Spinone al Lago

• Quarona Sesia

• St. Andrea

• Sulmona

Iberia

• Oliva

• Marcilla

• Alcolea

France

• St. Donat

• St. Alban

• Nuits St. Georges

Germany

• Herrath

• Dachwig

• Grünsfeld

• Erftstadt

• Heerlen (NL)

International*

• Kêty (PL)

• Slemien (PL)

• Nieszawa (PL)

• Kuopio (FIN)

• Durham (UK)

179.6 million

153.0 million

155.5 million

384

428

442

18 bottling lines

22 bottling lines

25 bottling lines

467.2 million

246.0 million

337.0 million

617

570

600

20 bottling lines

11 bottling lines

28 bottling lines

Revenue per region.

Average number FTEs during 2012.

* International consists of the UK, Poland and Finland.

Refresco • Annual Report 201214

Executive Board Report 2012

Refresco • Annual Report 2012 15

Foreword

Following the significant input cost increases that our industry faced in 2011, our focus during the past year has been on recovering our margins, rightsizing our business accordingly, and searching for new opportunities to grow our market position. Despite continued high input costs and the depressed economic climate, we are pleased to report that we were able to improve our results by taking firm decisions to focus on the better contributing volumes and on the high growth segments of our business.

The Fast Moving Consumer Goods industry experienced tough competition throughout the year, evident in the pressures on the reported results of retail operators and manufacturers alike. Spain, Portugal, and Italy were those most affected by the economic downturn and these countries saw significant volume decreases at all price levels and in all product segments. Other European countries had to deal with various governmental austerity and budgetary measures, such as value added tax increases and sugar tax. The economic situation clearly slowed the consumption of soft drinks in 2012. In particular, orange juice and apple juice suffered from both the weak economic climate and the high concentrate prices. A-brand promotional activities continued throughout the year and this had a clear effect on our business. Despite the market indicators, we have confidence in the ongoing underlying growth of private label and thereby, also in the future prospects for our business. The growth is driven, on the one hand, by the long and consistent consumer trend towards private label products and, on the other hand, by the increased sophistication of private label products and manufacturers, retail consolidation, and the strong emergence of hard discounters, as well as the increased shelf space as private label becomes more important to retailers’ strategies.

“Our improvement in results was a combination of rightsizing our business and controlling our costs, supported by the on-going

growth of private label.”

Refresco • Annual Report 201216

Aart Duijzer CFO

Hans Roelofs CEO

Refresco • Annual Report 2012 17

Innovation and product co-development are key pillars in our customer relationships and are essential to boosting our organic growth. We believe that creativity toward the consumer as regards attractive price/quality propositions will be key to growing with our customers and to offsetting the effects of the high input costs and the weak economy. On the technology side, the packaging trend towards Aseptic PET should benefit our current Aseptic PET capacity and we are planning to invest further in this.

In 2012, the group’s revenue and volumes were broadly in line with prior year. The modest revenue growth came from a combination of volume increases following the acquisition of Spumador and higher average selling prices as increased input costs were passed on. Excluding Spumador, our volumes fell by 4.7%, reflecting our commercial decision in late 2011 to let go volumes in the lower margin product categories. In the long term, the strength of our business model lies in our ability to achieve the right balance between volume and margin. In line with current volume levels, we started to right-size our manufacturing capacity in the first half of 2012.

As anticipated throughout the year, the benefits of rightsizing and the related cost savings started to flow through to our results in the second half of the year. Our adjusted EBITDA, at EUR 115.5 million, was EUR 4.5 million up on last year. The margin per liter was up on last year, mainly because of the shift from lower margin volumes to higher margin products coupled with our ability to pass on increased input costs. At EUR 18.2 million, the group’s net loss was still a dis appointment, reflecting the lower volumes and the one-time restructuring costs accrued during the year.

As we move forward into 2013 and beyond, our intention is to continue to focus on the top-growth segments of the business. Hard discounters will remain the backbone of our international private label model, complemented by tailor-made approaches to international buying platforms and full service retailers. We will continue to look for opportunities to further

optimize our manufacturing footprint and to maintain our industry cost price leadership.

We expect the challenging business environment to continue in 2013 assuming the economic recession in Europe persists. We estimate only a modest level of growth in the total soft drinks market, though we do believe that private label will continue to outperform the market as a whole and thereby continue to contribute to our operations. Refresco has a strong position in the European private label soft drinks and fruit juices market, and this is complemented by increasing contract manufacturing for A-brands. We aim to increase our share of the contract manufacturing business and to play a central role in A-brand contract manufacturing at a pan- European level. Furthermore, thanks to our strong cash generation and recent refinancing, we enjoy both a strong financial position and the liquidity to develop our business further.

Finally, we would like to thank our customers and suppliers for their cooperation during 2012, and also our own teams across Europe for their dedication and their contribution to Refresco’s operations. We would also like to thank our shareholders, bondholders, and banks for the confidence and trust they have placed in Refresco.

Rotterdam, March 20, 2013

Executive Board Hans Roelofs – CEO Aart Duijzer – CFO

Refresco • Annual Report 201218

Executive Board Report 2012

Business review

As in 2011, the market was characterized by high input costs and continued erosion of consumer disposable income. Our revenues were broadly in line with prior year. Volumes fell from last year, reflecting our commercial decision in late 2011 to let go volumes in the lower margin product categories. We improved our operating results, though lower volumes and one-time business rightsizing costs influenced the net result.

Market overviewHistorically the private label soft drinks market in Europe has enjoyed stable growth. Despite today’s challenging economic situation and the consequent fall in consumer disposable income, we do still believe in the underlying growth of private label. In 2012 the overall soft drinks consumption in Western Europe fell from prior year. Especially the juices segment continued under pressure in 2012 due to high concentrate prices. As these concentrate prices stabilize, we expect the segment to even-out.

Given that the soft drinks manufacturing industry in Western Europe remains highly fragmented, we believe that there is room for further consolidation.

Raw materialsFollowing the massive price increase in 2011, practically all primary raw and packaging materials continued at high levels in 2012. The input markets seemed to stabilize in late 2012, having peaked at record high price levels. We aim to mitigate price fluctuations in raw and packaging materials by for example consistently matching our raw material purchases with closings of tenders, the so-called back-to-back model.

Refresco works with a limited number of strategic suppliers for its key raw materials and packaging materials. A substantial amount of our raw materials is purchased centrally. In 2012, our orange juice supply was sourced mainly from Brazil. We also have our own pressing capacity of not-from concentrated orange juice at

our Oliva manufacturing site in Spain, with the remainder of the fresh orange juice being sourced from Brazil and from other locations in Spain. In 2012 the majority of our apple juice concentrate (sour and sweet) was sourced from Eastern Europe, Poland and Hungary in particular. Due to the European quota system for white sugar the majority of our sugar volume was sourced locally at high EU market prices. On the packaging side we source PET preforms and PET granulate mainly from European manufacturers. Aluminum cans were sourced from European manufacturers and liquid paper board mainly from the three major global suppliers. We are continually looking out improvements in our supply chain solutions that can benefit our customers.

Flexible manufacturing capabilities: Our state-of-the-art manufacturing equipment provides us with

the flexibility to manufacture a full range of products in a wide variety of packaging and to respond

quickly to our customers’ changing needs and requirements.

“Meeting high-volume customers’ requirements

quickly.”

19Refresco • Annual Report 2012

Refresco • Annual Report 201220

Refresco is focused on producing soft drinks and fruit juices in a wide variety of packaging. Our production capabilities enable us to manufacture over 5,500 stock keeping units (SKUs) for both our private label and contract manufacturing

customers. Furthermore, we are also able to develop new packaging and products quickly to meet changing customer requirements and consumer demand, which positions us well to continue to serve our customers and their consumers.

Wide range of product and packaging combinations

Carbonated soft drinks 31.7% (2011: 31.0%)

Waters 24.4% (2011: 22.3%)

Fruit juices 17.4% (2011: 20.1%)

Ready-to-drink teas 11.9% (2011: 12.4%)

Functional and still drinks 10.8% (2011: 8.9%)

Energy drinks and other 3.8%

(2011: 5.3%)

PET 51.5%

(2011: 50.9%)

Aseptic PET 19.3%

(2011: 17.3%)

Carton 18.2%

(2011: 21.1%)

Cans 9.1%

(2011: 9.2%)

Other 1.9%

(2011: 1.5%)

Volume per product category Volume per packaging

Products and packagingWe saw the shift continue from the more expensive product categories, such as 100% fruit juices, to cheaper categories such as fruit drinks and carbonated soft drinks. Orange juice and apple juice were particularly affected by the latest price increases. Despite the slow-down in demand for fruit juices, we believe that the long-term prospects for this category are promising, in particular in juice concepts with added value. In 2012, fruit juices represented 17.4% of our total volume, a decrease of 2.7%-points compared to 2011. Our most recent acquisitions have increased share of the carbonated soft drinks and the water markets by 0.7%-points and 2.1%-points, respectively.

Furthermore, we saw the trend continue away from carton packaging to Aseptic PET. In 2012, 70.8% of our packaging volume consisted of plastic containers (PET and Aseptic PET). We continue to strive for high percentage of recycled PET in our plastic bottles. Liquid paper board accounted for 18.2% of volume and the remaining 11% was packaged in steel and aluminum cans and to a lesser extent in glass and pouches.

Executive Board Report 2012

Refresco • Annual Report 2012 21

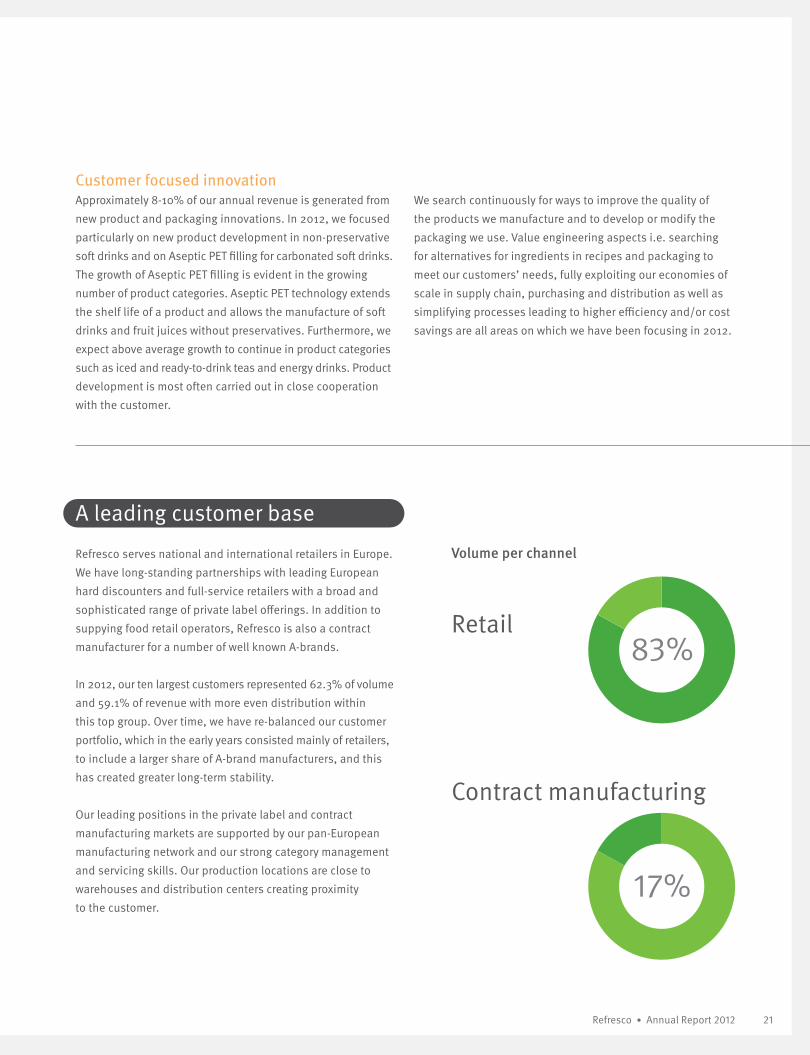

Volume per channel

Customer focused innovationApproximately 8-10% of our annual revenue is generated from new product and packaging innovations. In 2012, we focused particularly on new product development in non-preservative soft drinks and on Aseptic PET filling for carbonated soft drinks. The growth of Aseptic PET filling is evident in the growing number of product categories. Aseptic PET technology extends the shelf life of a product and allows the manufacture of soft drinks and fruit juices without preservatives. Furthermore, we expect above average growth to continue in product categories such as iced and ready-to-drink teas and energy drinks. Product development is most often carried out in close cooperation with the customer.

We search continuously for ways to improve the quality of the products we manufacture and to develop or modify the packaging we use. Value engineering aspects i.e. searching for alternatives for ingredients in recipes and packaging to meet our customers’ needs, fully exploiting our economies of scale in supply chain, purchasing and distribution as well as simplifying processes leading to higher efficiency and/or cost savings are all areas on which we have been focusing in 2012.

A leading customer base Refresco serves national and international retailers in Europe. We have long-standing partnerships with leading European hard discounters and full-service retailers with a broad and sophisticated range of private label offerings. In addition to suppying food retail operators, Refresco is also a contract manufacturer for a number of well known A-brands.

In 2012, our ten largest customers represented 62.3% of volume and 59.1% of revenue with more even distribution within this top group. Over time, we have re-balanced our customer portfolio, which in the early years consisted mainly of retailers, to include a larger share of A-brand manufacturers, and this has created greater long-term stability.

Our leading positions in the private label and contract manufacturing markets are supported by our pan-European manufacturing network and our strong category management and servicing skills. Our production locations are close to warehouses and distribution centers creating proximity to the customer.

Retail

Contract manufacturing

83%

17%

PET 51.5%

(2011: 50.9%)

Aseptic PET 19.3%

(2011: 17.3%)

Carton 18.2%

(2011: 21.1%)

Cans 9.1%

(2011: 9.2%)

Other 1.9%

(2011: 1.5%)

Refresco • Annual Report 201222

People and organizationRefresco employed 3,074 people (FTEs) in 2012 (3,034 in 2011), in the Netherlands, Belgium, Germany, France, Spain, Italy, the UK, Poland, and Finland. The modest increase in headcount was attributable mainly to the acquisitions of Spumador and Taja, partly offset by reorgani za tions completed in Iberia, Italy, and the UK.

Due to local market conditions and decreasing demand, we have terminated our rental contact at the Palma del Rio manufacturing site in Cordoba, Spain. To reflect market conditions and to protect the future prospects of our Iberian business, we have also completed extensive reorganizations at the remaining manufacturing sites. In Italy, we decided to close production at our leased manufacturing site in Gussago following the combination of weak market conditions in the region and the 2011 acquisition of Sulmona. The production at Gussago was transferred to other group-owned manu facturing sites. We have also transferred part of the Caslino al Piano production in the north of the country to our Sulmona manufacturing site in the center of Italy. In the UK, we have completed a restructuring program at our Durham site in order to further reduce our cost base and to improve efficiency in line with current volumes. Regrettably, the restructuring programs also led to redundancies in the countries affected.

At Refresco Group, we have made two significant improvements to our governance model. Firstly, to ensure a strong focus on the opportunities and challenges of today’s markets and to further strengthen the coordination and development of our international

customers, we have established a formal Group Commerce function. Secondly, to support Refresco’s ambitions as a world class manufacturer and to lead our footprint optimization, we have boosted the staff resources of the Group’s Operations function.

Succession management has continued to be a key theme in our Human Resources strategy at Refresco Group. To support our growth targets for the future, we have continued to work to ensure that we properly develop our high potentials and that they find interesting challenges within Refresco. Most of our senior managers have joined Refresco from outside the Group in recent years, and it is our ambition for the coming years to promote more internal Refresco management talent to higher positions across the businesses. We have targeted our recruitment efforts more specifically at middle-management talent, to be coached and developed in-house.

InvestmentsOur investments in acquisitions and capex projects aggre gated EUR 49.7 million in 2012. We invested significant amounts of capex in Germany, Italy, and Benelux, adding new bottling lines and replacing older lines with new technology. The remainder was invested in transferring our manufacturing capacity from closed lines and plants in Italy and Spain into other group-owned manu facturing sites and in replacement projects and modernization of our manufacturing set-up. We see these investments as the foundations for further organic growth and cost savings in 2013.

Executive Board Report 2012

Refresco • Annual Report 2012 23

We acquired Taja, a Polish private label manufacturer of carbonated soft drinks and water, to create a nation-wide footprint and a platform for further customer-driven growth. Taja’s production site in Nieszawa is centrally situated in

Poland, close to the highways leading to the north and mid regions of the country. This acquisition complemented our existing production facilities and distribution lines in the south of the country.

Organizational structure

Refresco Group

Benelux France Italy

Poland

Germany Iberia

UK

International

Finland

Behavioral competencies at RefrescoOur size does bring economies of scale, but it is the ability of our people to seize market opportunities and streamline operational processes that makes the difference. We believe strongly that it is not only knowledge and experience, but also the right mind-set, that are critical to good performance. As a cost price leader, Refresco continuously needs to make its processes smarter, more flexible, and more sustainable. Our skilled production staff play a key role in ensuring that we work in the most efficient and effective manner possible.

Refresco encourages high performing talent to broaden their horizons internationally. Both short-term assignments and long-term career opportunities abroad are encouraged within the Group.

To ensure that the Refresco culture remains embedded within the Group, we recruit, reward, and appraise our people on the basis of behavioral competencies. These behavioral competencies set the standard for the results we expect from our employees and for the behavior essential to achieve the results to which we aspire.

In addition to the competencies we have set out below, our top management team members are identified, assessed, developed, and rewarded on the basis of their vision, leadership, entrepreneurship, and coaching skills.

Team work Behavioral flexibility IntegrityPerformance orientationResults orientation

Refresco • Annual Report 201224

General informationOn May 16, 2011 Refresco issued a total of EUR 360 million in 7.375% senior secured notes and EUR 300 million in senior secured floating rate notes (3 month EURIBOR + 400bps). The notes are due on May 15, 2018. The notes are listed on the Luxembourg Stock Exchange and have been admitted to trading on the unregulated Euro MTF market. In connection with the issue, Refresco obtained a EUR 75 million revolving credit facility (RCF) from a consortium of seven European banks.

Standard & Poor’s (S&P) reduced Refresco’s corporate and senior secured long-term rating from BB- to B+ with negative outlook on July 27, 2012. Moody’s downgraded Refresco’s ratings from B1 to B2 on July 10, 2012, at the same time re-affirming stable outlook.

Acquisition of TajaOn May 29, 2012, we completed the acquisition of Taja Sp. z o.o., a Polish private label manufacturer of carbonated soft drinks and water. The total cash-outflow for the acquisition was EUR 6.0 million which was financed from our available cash resources. The acquisition of Taja did contribute to the Group’s results for the current year, though the effect was not material. Due to its size, Taja’s results are not presented separately in the annual report.

Revenue and expensesGroup revenue totaled EUR 1,538.3 million in 2012, an increase of 1.0% on 2011. Excluding the impact of the Spumador acquisition, which closed in April 2011, revenue fell by EUR 23.4 million or 1.6%. This was attributable to an average 3.1% increase in selling prices offset by volume decreases of 4.7%. The higher average selling prices arose mainly because of increases in raw material and packaging material prices were passed on to our private label customers. In like-for-like comparisons, we have excluded the effects of Spumador acquisition up to mid-April 2012.

Revenue per channel was broadly in line with 2011. Bottling activities for private label customers and A-brands represented 75.1% and 16.6%, respectively, of revenue in 2012. Own value brands and other customers accounted for the remainder of the revenue.

Our commercial decision to let go of some volume in the lower margin product categories in the last quarter of 2011 was positively reflected in our gross margin per liter for 2012 but negatively impacted our annual volumes which decreased by 0.3%. The weak economic climate, downward trend in the total soft drinks market, and substantial volume loss in Iberia due to the tough local market conditions and competition adversely impacted our volumes. Excluding the Spumador acquisition, volume was down by 4.7%. We saw volumes fluctuate significantly towards the end of the year adding to the volatility of the market. This may have been caused in part by the continued A-brand promotions.

• Revenue totaled EUR 1,538.3 million, up 1.0% on 2011• Volume totaled 4,943.9 million litres, down 0.3% on 2011• Gross profit margin per litre was 11.7 euro cents,

up 0.9% on 2011• Adjusted EBITDA was EUR 115.5 million, up 4.1% on 2011• Refresco’s corporate and senior secured credit ratings

are as follows: S&P B+, outlook negative; Moody’s B2, outlook stable

Financial performance

Executive Board Report 2012

Refresco • Annual Report 2012 25

Gross profit margin per liter was EUR 0.117 in 2012 compared to EUR 0.116 in 2011, the slight increase being mainly attributable to the shift away from lower margin volumes towards more profitable products and to our ability to pass on increased input costs toward the end of the year. Furthermore, margins increased despite the shift from juices to carbonated soft drinks and despite water and the addition of lower margin products from acquisitions.

Gross profit margin (as a percentage of revenue) was 37.7% for 2012 and in line with 2011. Passing on input cost increases to our private label customers has a direct impact on our revenue and gross profit margin percentage, but this does not affect the absolute gross profit margin per liter. Consequently, there can be inconsistencies between the fluctuations in gross profit margin percentage and gross profit margin per liter. As input costs can fluctuate significantly over time, our performance should be assessed in terms of gross profit margin per liter.

Raw materials and consumables totaled EUR 959.0 million, an increase of 1.0% on 2011 attributable to increases in the prices of key raw materials and packaging materials partly offset by lower sales volumes.

For most raw and packaging materials, we have a policy of purchasing forward to cover sales positions with customers. Some of the raw materials we require are priced only in USD,

and we mitigate the effect of exchange rate fluctuations by using USD purchase options and forward contracts.

Operating cost decreased by EUR 4.3 million in 2011. Excluding the effects of the Spumador acquisition, impairments, and exceptional costs, the operating costs fell by EUR 14.7 million compared to 2011, reflecting the measures taken to right-size our manufacturing capacity and the cost saving programs implemented.

Employee benefits expense totaled EUR 151.3 million, an increase of 5.1% compared to 2011. The increase was primarily attributable to increased headcount arising from the acquisition of Spumador and to costs related to the rightsizing measures taken in the UK, Spain and Italy. During 2012 the average number of employees (in full-time equivalents) was 3,074 compared to an average of 3,034 in 2011.

Depreciation, amortization, and impairment expense totaled EUR 73.4 million compared to EUR 73.5 million in 2011. Impairment amounted to EUR 7.5 million, arising largely from a write-down of goodwill in the UK due to reduced expected growth in that market, the Uelzen manufacturing plant in Germany and Gussago manufacturing plant in Italy. Impairments in 2011 amounted to EUR 9.1 million. Other operating expenses were EUR 319.9 million, a 3.5% decrease on 2011.

* By location of sales

** International consists of the UK,

Poland and Finland

Revenue per region*

BENELUX

30.3%FRANCE

16.0%GERMANY

21.9%IBERIA

11.7%ITALY

10.1%INTERNATIONAL**

10.0%

Refresco • Annual Report 201226

Rightsizing costs amounted to EUR 6.5 million in 2012, of which EUR 4.4 million related to costs incurred and EUR 1.6 million to impairments. Capex related to restructuring amounted to EUR 5.1 million attributable to the transfers of production capacity. The expected annualized run-rate savings resulting from the rightsizing measures are in the range of EUR 7 to 8 million.

Finance income of EUR 0.6 million was consistent with 2011. Finance expenses totaled EUR 48.4 million, compared to EUR 52.2 million in 2011. The decrease was attributable to lower overall finance costs following the recent refinancing and the 2011 write off of financing costs related to previous financing arrangements. The net amount of finance expenses in 2012 was EUR 47.8 million, representing a 7.2% decrease from EUR 51.5 million in 2011.

The effective tax rate was 44% negative, compared to a blended Group tax rate of 9.8%. The negative effective tax rate arises mainly from non-deductible impairment of goodwill in the UK. Furthermore, the tax effect of losses incurred during the year in the UK was not recognized. There were also some additional prior year tax accruals and some provisions made for tax audits. Income tax expense in 2012 was EUR 5.6 million, compared to EUR 0.1 million in 2011, reflecting the improved operating results.

ResultsThe operating profit in 2012 amounted to EUR 35.2 million compared to EUR 25.7 million in 2011. The improvement was mainly the result of the higher gross profit margins, the rightsizing of our business in line with current volumes, and the further cost savings achieved in 2012.

EBITDA for 2012 was EUR 108.6 million, compared to EUR 99.2 million for 2011. Excluding the rightsizing costs and other one-off items, the adjusted EBITDA was EUR 115.5 million, compared to EUR 111.0 million for 2011, reflecting the higher gross profit margins and the cost savings achieved.

Reconciliation of operating profit to adjusted EBITDA (in millions of euros)

2012 2011Operating profit / (loss) 35.2 25.7

Depreciation, amortization and impairment costs 73.4 73.5

EBITDA 108.6 99.2

Acquisition and other costs 2.1 2.2

Costs refinancing 0.3 8.0

Fair value adjustment acquisition 0.0 0.7

Restructuring cost 4.5 0.0

MtM revaluation US$ options 0.0 0.9

Adjusted EBITDA 115.5 111.0

Executive Board Report 2012

Refresco • Annual Report 2012 27

The loss before taxes amounted to EUR 12.6 million, compared to EUR 25.8 million in 2011. The loss for the year was influenced by lower volumes and one-time costs related to the rightsizing of the business during the year. Balance sheet and financial positionTotal assets amounted to EUR 1,205.1 million at December 31, 2012, compared to EUR 1,262.9 million at December 31, 2011. The balance sheet fluctuations arose mainly from rightsizing our manufacturing capacity, decreased working capital and lower value of derivate financial instruments.

Capex spending was EUR 43.5 million, compared to EUR 41.5 million in 2011 mainly attributable to investments in new bottling lines and the transfer of capacity from closed production sites to other group-owned locations.

Despite the higher raw and packaging material prices working capital decreased by EUR 14.5 million from EUR 91.9 million in at December 31, 2011 to EUR 77.4 million. The decrease is within the range of normal seasonal working capital fluctuations. The cash position at December 31, 2012 was EUR 95.3 million, compared to EUR 89.6 million at December 31, 2011.

The Revolving Credit Facility of EUR 75.0 million was undrawn as of December 31, 2012.

Cash flowIn 2012 Refresco’s net cash generated from operating activities totaled EUR 49.6 million, compared to EUR 41.8 million in 2011. The increase was mainly attributable to higher EBITDA.

Distribution of profitsConsistent with 2011, the Executive Board’s proposal is that the Annual Meeting of Shareholders deducts the net loss from retained earnings. The balance sheet presented in this report for the period ended December 31, 2012, is before appropriation of the result for the financial year 2012.

Refresco • Annual Report 201228

Prospects for 2013

Assuming the high input costs persist and the purchasing power of the European consumer continues to come under pressure, in general, we see the difficult market conditions that prevailed in 2012 continuing in 2013. The current economic depression has made it more difficult to forecast the prospects for the soft drinks market as a whole and has led to increased volatility in market volumes. We believe, however, that the prospects for the European soft drinks industry generally, and the private label market in particular, continue to be encouraging.

The downtrend in consumer spending and the increasing unpredictability of consumer behavior is expected to continue. Even in this challenging environment, we expect Refresco to be able to bolster its position as the preferred bottler for retailers and A-brand customers. Refresco’s size enables us to take advantage of a wide variety of purchase and supply chain positions and opportunities in the areas of both pricing and sourcing of raw materials and packaging materials.

Our unique European presence and relationships with international customers, combined with our ability to offer total supply chain solutions and an extensive portfolio of soft drinks and fruit juices offerings, are expected to be strengths in this ever-changing market.

Results 2013Our results in 2013 will largely depend on the volumes we achieve in our tenders and in the soft drinks market as a whole. Our performance will also depend on our ability to find new growth opportunities with retail customers and A-brands. Overall, we expect modest upward trends in revenue and volumes as well as an increase in adjusted EBITDA supported by both the expected on-going growth of private label and increases in A-brand contract manufacturing and the rightsizing measures implemented in 2012 in our manufacturing footprint. We expect input cost levels for 2013 to be generally flat.

We expect R&D spending to be in line with 2012 and the number of employees to remain stable or show some decline as we seek further opportunities to optimize our manufacturing footprint. We expect capex spending to be slightly above 2012 due to planned investments.

Executive Board Report 2012

Continue to improve cost efficiencies:

We plan to continue to invest in improving

production flexibility and cost efficiencies in our

manufacturing and warehousing operations.

We rely on a fully outsourced external logistics

network to distribute our products to retail

warehouses throughout Europe.

29Refresco • Annual Report 2012

Executive Board Report 2012

Sustainability

As a leading European soft drinks and fruit juices bottler for retailers and A-brands, Refresco recognizes its responsibilities to stake holders and to the environment. We are committed to manufacturing quality products in a sustainable manner, while consistently increasing the value of our business for all our stakeholders. We acknowledge that sustainability means conti nuous improvement, and we are fully geared up to developing sustainability performance in all areas of our operations, such as: • Creating sustainable supply chain solutions • Managing and reducing the environmental impact of our manufacturing operations • Enhancing safety, development, and training

Refresco’s approach to sustainabilityRefresco aims for a continuous broadening of its sustainability approach. Key areas of quality, environment, safety, and health are managed, reported, and monitored at a local level in each country in which we operate. Furthermore, each country has established a number of special sustainability initiatives, including, amongst others, carbon footprint reduction, waste water treatment, gas- electricity production, and community programs.

In 2012 we established a global platform of sustainability ambassadors, including the senior managers of each Refresco country of operations. The aim of this platform is to continuously evaluate our customers’ and stakeholders’ requirements, share best practices, and integrate our local sustainability programs into the Group’s operations and reporting systems. The platform will continue to develop group level performance indicators in the key areas of environment, sourcing, quality, health and safety, as well as in the related reporting systems.

Refresco’s approach to sustainability is very much hands-on. It is built on our strategy of further expanding our position as preferred bottler to retailers and A-brand customers in the European market. Furthermore, it reflects our mission to be the most reliable and cost effective bottler of soft drinks and fruit juices in Europe.

30 Refresco • Annual Report 2012

Food quality and safety: All our operating sites

are certified under either the International Food

Standard (IFS) or, in the UK, the British Retail

Consortium (BRC) protocol, as well as under

ISO 14001 standards, and the majority of our

sites are ISO 9001 certified. To ensure food

safety and quality, every production site has

implemented its own quality system (HACCP)

based on the critical control and quality points

in its production processes. Furthermore, our

sites are regularly audited by our retail and

A-brand customers.

As we seek to establish and maintain lasting partnerships with our customers, we realign our operations with their requirements on sustainability. In practice, we help our customers to achieve their sustainability targets by evaluating and implementing alternative supply chain solutions, materials, and manufacturing processes. Our flexible sourcing and bottling capabilities allow us to serve each customer in line with its individual needs.

We aim to build long-term relationships with our strategic suppliers based on respect, trust, mutual benefit, and joint product development. Our customers expect Refresco to maintain high quality standards and to be cost-competitive. We expect the same from our suppliers.

Where we are in a position to exert influence, we continuously search for opportunities to manage and reduce the environmental impact of our manufacturing operations in the areas of energy consumption, water consumption, packaging, and waste.

Our manufacturing locations focus on safety in the workplace and they maintain a zero accident policy which is monitored locally and reported and followed-up centrally. Within Refresco, we invest in talent and in management development to bring out the best in our organization and in our people.

31Refresco • Annual Report 2012

Our commitments• To meet and exceed our customers’ sustainability

requirements• To launch at least one major sustainability project

each year in the Group• To engage our major partners in dialogue regarding

the Refresco Sustainability Strategy• To continuously search for opportunities to manage

and reduce our environmental impact and for ways to take appropriate action

• To maintain a zero accident policy• To develop our people’s talents

Refresco • Annual Report 201232

Executive Board Report 2012

Sustainable supply chainSafety, quality, and supply reliability are at the heart of our supply chain partnerships. This fundamental principle precludes the use of unauthorized suppliers, manufacturing procedures, and activities that may prejudice Refresco’s standards or the sustainability of its businesses. If they wish to maintain an on-going and long-term business relationship with Refresco, suppliers must comply with prevailing legislation and with socially and environmentally sustainable business practices and they must be both cost competitive and continuously focused on improvement. Refresco representatives visit and audit key suppliers on a regular basis. Suppliers are evaluated in terms of such matters as their buildings and premises, food safety, good manufacturing practices, process controls, control of surrounding products, product identification and traceability, business principles including compliance of all local laws and environmental sustainability. Suppliers must have valid international quality certification in place.

We expect our suppliers to:• Ensure appropriate quality in compliance with our

strict requirements• Operate in compliance with the respective local laws,

including the social standards for human rights• Supply at a competitive price• Adhere to timely delivery• Provide good after-sales service• Safeguard safety and health• Commit to strict confidentiality• Mutually invest in a long term partnership and

aims for continuous improvements

Refresco requires that its trading partners who buy raw and packaging materials themselves for their own products ensure that their suppliers comply with the same conditions that Refresco expects from its own suppliers.

Sourcing of orange juice and sugar plays a major role in our supply chain. Refresco is one of the world’s five biggest buyers of Frozen Concentrated Orange Juice and Not-From- Concentrate Orange Juice. We aim to maintain robust long-term relationships with our strategic raw materials

suppliers based on respect, trust, mutual benefit, and joint product and process development.

In addition to global sourcing, we source Not-From- Concentrate fruit juices locally in southern Europe. On the packaging side, we work to identify sustainable alternatives for our customers.

Minimizing the environmental impacts of our manufacturing operations

EnergyEnergy consumption is important to us, both in maintaining our cost price leadership and in minimizing the negative environmental impact of our operations. Cooling, warming, machinery, and compressed air form the bulk of our energy consumption. Our aim here is to reduce energy consumption by optimal utilization of our machinery and investment in reduced energy equipment.

WaterWater is a key ingredient to many of our products. We have several fresh water wells, and protecting these is crucial to us in ensuring the quality of our products. Furthermore, we closely monitor the water/product ratio in our manufacturing processes, with the aim of reducing water consumption.

PackagingRefresco continues to take steps to reduce the aggregate amount of material used in its primary and secondary packaging. Lightweight packaging, closures, and secondary packaging are becoming the norm throughout Refresco, as light-weighting has become one of the major drivers in the soft drinks industry for addressing the environmental concerns surrounding plastic bottles and coping with major cost price increases of PET over the past years. We participate in a project for the development of sustainable PET bottle from bio-materials. Furthermore, Refresco has set goals to increase the recyclability of its packaging materials.

Logistics and transportationWith the locations of our manufacturing plants we are able to supply at short transportation lines and to provide the needed proximity to our customers. By combining deliveries of different products and customers, our aim is to have only fully loaded trucks and optimal pallet usage. Other initiatives include the usage of biogas trucks and LHVs (Longer Heavier Vehicles) and exploring alternatives such as truck-on-train transportation. In our search for optimal efficiency transpor tation with minimum impact on the environment, we place high priority on identifying suppliers that have a similar approach and can make a meaningful contribution to a sustainable supply chain.

Enhancing safety, development, and training Qualified employees are the key strength of our operations. Through specific training programs, we aim to create safe workplaces and to meet our own expectations and the expectations of our stakeholders in the areas of quality, safety, and health. Conducting and undergoing internal and external audits, and also dealing with complaints, keep us focused and result in the continuous development and improvement of our processes. Our ambition is to achieve and maintain a “zero accident” workplace.

Finally, our belief in the “first time right” principle in quality management enhances not only our cost efficiency, but also our environmental performance.

“Reducing environmental impacts

of our operations.”

Environmental management: Throughout our production sites,

we have implemented the ISO-standard 14001 on environmental

management, aimed at ensuring compliance with the various

environmental regulations applicable, as well as with the food

products regulations.

33Refresco • Annual Report 2012

Refresco • Annual Report 201234

Governance

Refresco • Annual Report 2012 35

Refresco • Annual Report 201236

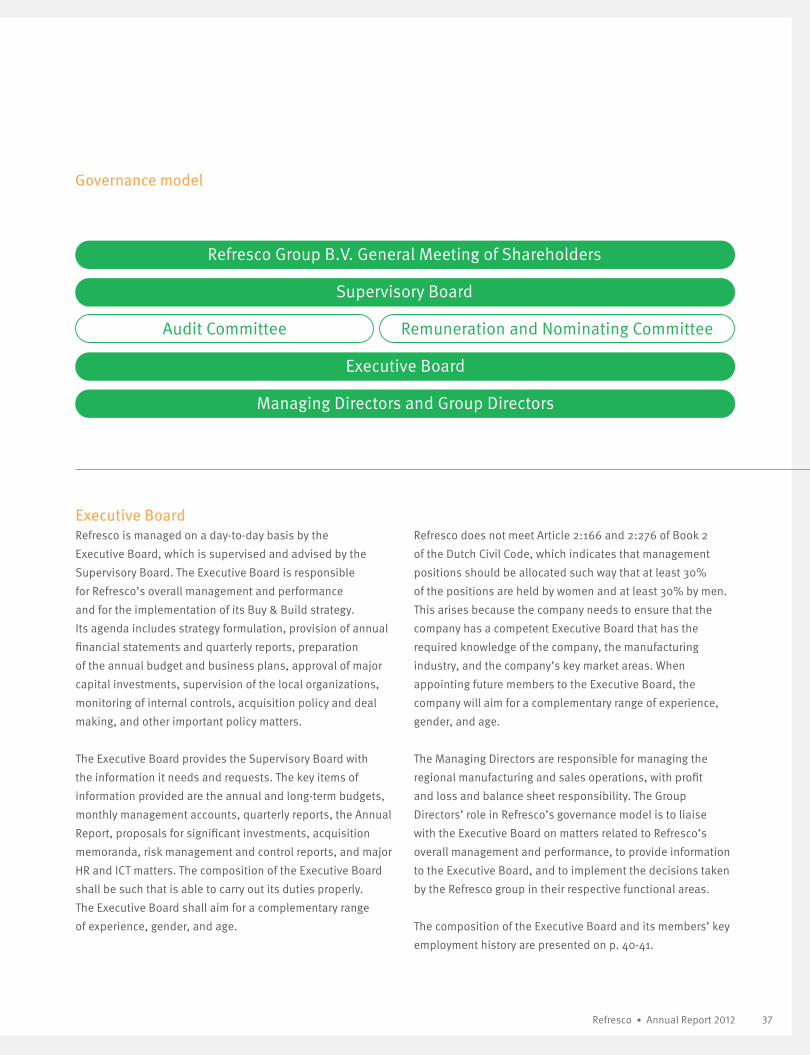

Governance structure

Refresco’s governance structure is decentralized, enabling the company to respond quickly to changes in market conditions and customer needs.

Regulatory environmentRefresco Group B.V. is a private limited liability company (“besloten vennootschap”) incorporated under the laws of The Netherlands. The company complies with the Dutch Civil Code and its Articles of Association.

Refresco complies with the indenture and offering circular relating to the senior secured notes and with the rules of the unregulated Euro MTF market operated by the Luxembourg Stock Exchange pertaining to financial reporting and disclosure. Neither the notes nor the company fall under the Act on Financial Supervision, the Act on the Supervision of the Securities Trade in The Netherlands, or the Dutch Corporate Governance Code.

Refresco’s corporate governance structure reflects those principles of the Dutch Corporate Governance Code which it considers to be beneficial to and supportive of its governance structure.

Corporate structureOur corporate structure consists of one international central office and 25 production sites. The Group produces and sells in nine European countries: The Netherlands, Belgium, Germany, France, Spain, Italy, the UK, Poland, and Finland. The local organizations are close to their customers and can be responsive to their needs while acting consistently across the Group. They are led by highly experienced and professional management teams, which meet regularly to ensure operating consistency across the Refresco Group.

A relatively small central team coordinates the central functions of strategy, business development, purchasing, commerce, manufacturing, supply chain & quality, finance and control, and human resources management. The central team achieves economies of scale and provides the local organizations with the tools to run the Group’s business in the most optimal manner possible. Each team member has a high level of independence and discretion in terms of developing individual ideas that contribute to the company’s best interests. What connects them is their deep understanding of the business and their can-do attitude.

Refresco Group has a two-tier board structure, with an Executive Board that manages the Group on a day-to-day basis and a Supervisory Board. The Executive and Supervisory Boards meet regularly.

Governance

Refresco • Annual Report 2012 37

Refresco Group B.V. General Meeting of Shareholders

Supervisory Board

Audit Committee Remuneration and Nominating Committee

Governance model

Executive BoardRefresco is managed on a day-to-day basis by the Executive Board, which is supervised and advised by the Supervisory Board. The Executive Board is responsible for Refresco’s overall management and performance and for the implementation of its Buy & Build strategy. Its agenda includes strategy formulation, provision of annual financial statements and quarterly reports, preparation of the annual budget and business plans, approval of major capital investments, supervision of the local organizations, monitoring of internal controls, acquisition policy and deal making, and other important policy matters.

The Executive Board provides the Supervisory Board with the information it needs and requests. The key items of information provided are the annual and long-term budgets, monthly management accounts, quarterly reports, the Annual Report, proposals for significant investments, acquisition memoranda, risk management and control reports, and major HR and ICT matters. The composition of the Executive Board shall be such that is able to carry out its duties properly. The Executive Board shall aim for a complementary range of experience, gender, and age.

Refresco does not meet Article 2:166 and 2:276 of Book 2 of the Dutch Civil Code, which indicates that management positions should be allocated such way that at least 30% of the positions are held by women and at least 30% by men. This arises because the company needs to ensure that the company has a competent Executive Board that has the required knowledge of the company, the manufacturing industry, and the company’s key market areas. When appointing future members to the Executive Board, the company will aim for a complementary range of experience, gender, and age.

The Managing Directors are responsible for managing the regional manufacturing and sales operations, with profit and loss and balance sheet responsibility. The Group Directors’ role in Refresco’s governance model is to liaise with the Executive Board on matters related to Refresco’s overall management and performance, to provide information to the Executive Board, and to implement the decisions taken by the Refresco group in their respective functional areas.

The composition of the Executive Board and its members’ key employment history are presented on p. 40-41.

Executive Board

Managing Directors and Group Directors

Innovation: Each of our business units employs a

dedicated research and development team. These

teams are responsible for, among other things,

performing quality testing on our products,

developing new technologies and processes

and introducing energy-friendly technology.

Supervisory BoardThe Supervisory Board is responsible for supervising and advising the Executive Board and for overseeing the general direction of the company’s operations and strategy.

The Supervisory Board consists of seven members appointed by the General Meeting of Shareholders.

The articles of association state that certain strategic or otherwise important decisions require the prior approval of the Supervisory Board. These include acquisitions, loan redemptions, and significant changes in the identity or nature of the company or its businesses. Each year the budget is prepared by the Executive Board and submitted to the Supervisory Board for its approval.

Refresco does not meet Article 2:166 and 2:276 of Book 2 of the Dutch Civil Code, which indicates that Supervisory Board positions should be allocated such way that at least 30% of the positions are held by women and at least 30% by men. This arises because the company needs to ensure that the company has a competent Supervisory Board that has the required knowledge of the company, the manu facturing industry, and the company’s key market areas. When appointing future members to the Supervisory Board, the company will aim for a complementary range of experience, gender, and age.

Governance

Refresco • Annual Report 201238

“We put great emphasis on quality

and food safety.”

Refresco • Annual Report 2012 39

The Supervisory Board has set up the Remuneration and Nominating Committee and the Audit Committee. The Remuneration and Nominating Committee reviews the Executive Board’s proposals concerning the remuneration policies for the Group. The Supervisory Board has delegated to the Audit Committee the tasks of supervising the internal and external audit procedures and of discussing and reviewing accounting policies and estimates. Charters are in place for both committees, which establish clear accountability. The Supervisory Board meetings also address other functions, such as HR, ICT, and risk management. The Chairman of the Supervisory Board is responsible for leading the Supervisory Board and also acts as a sounding board for the Executive Board.

The composition of the Supervisory Board and its members’ key employment history are presented on p. 40-41.

Code of conduct As a general principle, Refresco conducts all business operations with honesty, integrity, and transparency. Refresco operates as an open, transparent company which meets all legitimate requests for information, unless business or personal circumstances of those involved require confidentiality.

Refresco expects its employees to work with honesty, integrity, and respect for others. High standards of personal behavior must be observed in relationships with colleagues as well as in dealings with suppliers, agents, professional advisers, shareholders, banks, and other third parties.

Refresco recognizes that responsibility, reliability, and integrity are essential preconditions in terms of dealing with third parties such as suppliers, customers, and other stake-holders. Therefore Refresco will always act in good faith and expects its employees to refrain from acts that may prejudice these preconditions.

The Code of Conduct is published in its entirety on our website: www.refresco.com/our-company/#governance

Executive Board and Supervisory Board

Refresco • Annual Report 201240

Hans Roelofs

Chief Executive Officer (1963)

Aalt Dijkhuizen Member of the Supervisory Board (1953)

Aart Duijzer

Chief Financial Officer (1963)

Yiannis Petrides Chairman of the Supervisory Board (1958)

CEO Refresco since March 2007. Before joining Refresco Mr. Roelofs was CEO of Dumeco, a private label meat producer and processor. Mr. Roelofs started his career at Nutreco, rising to Managing Director of the Agri-Food Business and is a graduate of Wageningen University.

CFO Refresco since December 2000 and one of the co-founders of the company. Mr. Duijzer previously worked as Finance Director of the Continental European division of Hazlewood Foods Plc. Mr. Duijzer started his career at KPMG and holds a master’s degree in business economics from the Erasmus University in Rotterdam and is a Dutch chartered accountant.

Chairman of the Supervisory Board as from Jan 1, 2013. Mr. Petrides has broad experience in the FMCG and soft drinks industries. He is Vice-chairman of the Board of Directors of Campofrio Food Group, Vice-chairman of Board of Largo and a member of the Board of Puig. Mr. Petrides holds a BA/MBA degree from Cambridge University and an MBA from the Harvard Business School.

Member of the Supervisory Board since October 2009. Mr. Dijkhuizen is President and Chairman of Wageningen UR (University & Research centre) in The Netherlands since 2002 and he worked in the 90-ies as a professor specializing in animal health at the university. Between 1998 and 2002 he worked for Nutreco as Managing Director of the Business Group Agri Northern Europe.

Governance

The composition of the Executive Board and Supervisory Board is as of January 1, 2013. Mr. Yiannis Petrides was appointed as the new Chairman of the

Supervisory Board effective as of January 1, 2013. Mr. Marc Veen was Chairman of the Supervisory Board for the periods 2000-2003 and 2006-2012.

Refresco • Annual Report 2012 41

Pieter de Jong Member of the Supervisory Board (1964)

Hilmar Thor Kristinsson Member of the Supervisory Board (1971)

Peter Paul Verhallen Member of the Supervisory Board (1956)

Jon Sigurdsson Member of the Supervisory Board (1978)

Thorsteinn Jonsson Member of the Supervisory Board (1963)

Member of the Supervisory Board since May 2010. Mr. de Jong is Managing Director at 3i Europe plc Benelux. Before joining 3i in 2004, Mr. de Jong was managing director at Eiffel, a specialist services provider in Legal and Finance, and head of the advisory department at NIBC.

Member of the Supervisory Board since May 2006. Mr. Jonsson was the operator and owner of Vifilfell, the leading soft drinks bottler in Iceland from 1996 to 2011. Before working for Vifilfell he worked for the Federation of Icelandic Industries and for the Central Bank of Iceland as an economist.

Member of the Supervisory Board since August 2009. Mr. Kristinsson is also Vice Chairman of the Board of Norvestia Oyj. He has worked for Kaupthing as a director of a closed end equity fund and a pension fund and is Kaupthing’s nominated director on the board of directors of Ferskur Holding 1 B.V.

Member of the Supervisory Board since April 2009. In the past Mr. Sigurdsson served as CEO of Stodir from 2007 to 2010 and worked for Landsbanki hf. Currently he is the General Manager of Straumnes Ráðgjöf ehf and a partner at GAM Management ehf.

Member of the Supervisory Board since October 2009. Mr. Verhallen is a member of the Board of Hoogwegt Group and a management consultant. From 1996 to 1998 Mr. Verhallen was CFO and member of the Executive Board of Nutreco. Prior to that, Mr. Verhallen was a partner at KPMG in The Netherlands. Mr. Verhallen is a Dutch chartered accountant.

Refresco • Annual Report 201242

Strategic risksRisks related to the global financial and economic situation Historically, our results of operations have been influenced, and will continue to be influenced, by the general state of the global economy and consequently our income and results of operations depend, to a certain extent, on the performance of the global economy.

The continued weak economic situation in Europe has impacted the economies and markets in which we operate. The economic crisis has resulted in increased volatility and tighter credit markets, as well as in a lower level of liquidity in many financial markets. If these conditions persist or recur, they may negatively affect the future availability, terms, and cost of credit.

The timing and nature of any recovery in worldwide financial markets and in the global economy remain uncertain, and there can be no assurance that market conditions will improve in the near future. There can also be no assurance that market conditions

will not deteriorate, and this could cause demand in the soft beverage market to decline or remain at low levels for an extended period of time, having a material adverse effect on our business, financial condition, and results of operations.

How we address these risksWe have taken cost saving and re struc turing steps to protect the company’s financial health and to further strengthen our competitive position in the current economic situation. Working capital management continues to be a key area of attention to us. As a result, the cash position is strong and working capital control remains tight. A healthy cash flow is crucial and we are looking into as many alternatives as possible to maintain this.

We place great emphasis on long- standing relationships with European banks. Furthermore, we aim for conti nuous dialogue with our investment community to provide them with sufficient, timely,

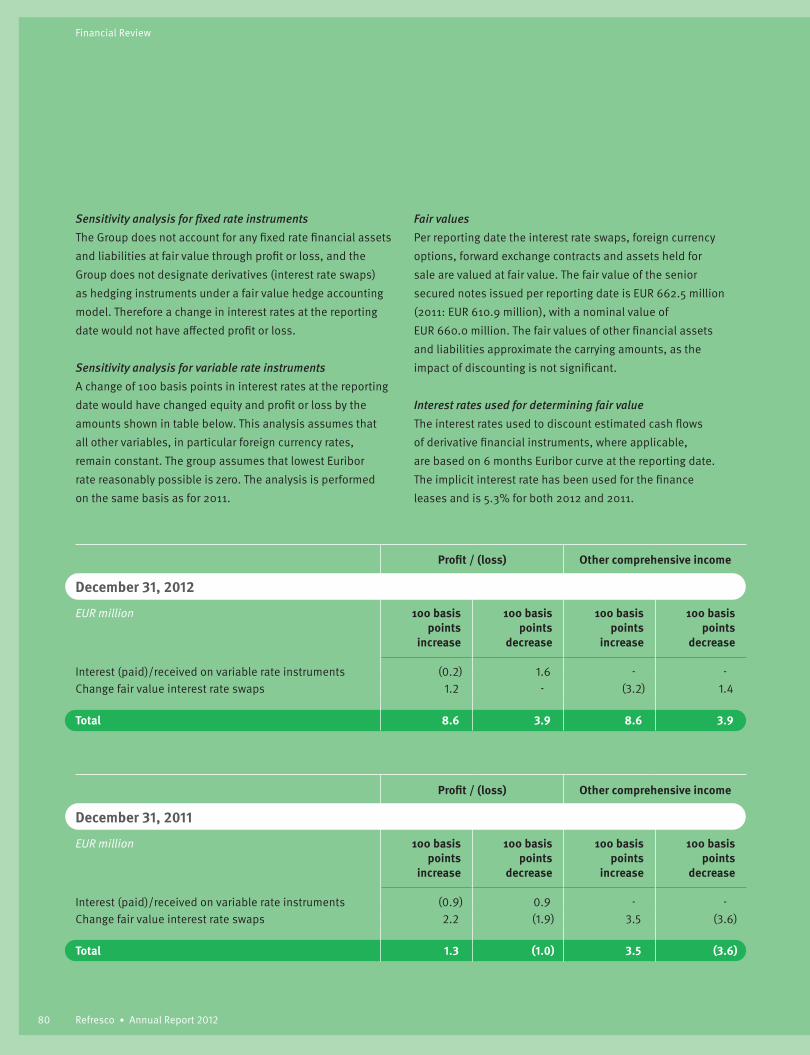

RisksWe set out in this section our primary strategic, operational, financial, and other risks. The risks and uncertainties we describe in this chapter are not necessarily the only ones we face. Additional risks and uncertainties of which we are not aware or that we currently believe are immaterial, may also adversely affect our business, financial condition, or results of operations. Financial risks are also explained in more detail in the Notes to the Consolidated Financial Statements on page 74.

Our quality control and assurance programs are

designed to comply with the strictest European

requirements for safe food manufacturing.

Governance

and accurate information regarding Refresco’s operations and financial performance.

Refresco completed a structural refinancing of the company in 2011 by issuing senior secured notes totaling EUR 660.0 million and by obtaining a EUR 75.0 million revolving credit facility (RCF) from a consortium of European banks. This refinancing provides Refresco with a wider financing horizon, increased flexibility for integration, and greater headroom for acquisitions. The senior secured notes mature in 2018 and the RCF in 2017. The RCF was undrawn as of December 31, 2012.

Risks of a cyclical downturn reducing sales volumes and/or marginsMuch of Refresco’s revenue comes from economies that have been affected by the economic depression in Europe, and this has adversely impacted consumer markets and triggered changes in consumer behavior. Refresco’s business is largely dependent on continued

consumer demand, and lower consumer spending may reduce sales volumes and affect revenue and profitability. Recent years have demonstrated that the private label soft drinks and fruit juices market is less sensitive to an economic downturn than other Fast Moving Consumer Goods (FMCG) markets.

However, the margin pressures facing our retail customers remain severe, and we see increased promotional activities for A-brand soft drinks, adding to market volatility.

How we address these risksTo mitigate the risks of adverse effects in any one category, our strategy aims to diversify, in terms of products, customers and geography. Refresco closely monitors performance in the more volatile markets as well as at its customers and suppliers, and strives to respond quickly to protect its business. If deemed necessary, measures will be taken to align operations with adapted customer demand.

In 2012 we carried out a comprehensive review of our stock keeping units (SKUs) to respond to current consumer demand and we let go of some lower margin product volumes. We also right sized our manufacturing capacity to be in line with current volumes.

Operational risksRisks related to price fluctuations and supply side developments Consolidation in the soft drinks market has resulted in a reduced number of key raw materials and packaging materials suppliers. The manufacture of our products is highly dependent on an adequate supply of raw materials and packaging materials, most of which are only available from a limited number of suppliers. The loss of any one of such suppliers could disrupt our supply chain, which could reduce the utilization rates of our production sites and disrupt deliveries to customers, and in turn have a material adverse effect on our business, financial condition, and results of operations.

43Refresco • Annual Report 2012

Refresco • Annual Report 201244

Although we have a policy of purchasing forward contracts for most raw materials and packaging materials to cover sales positions with customers there can be no assurance that such hedging measures will be effective. The limited number of suppliers for these materials weakens our negotiating positions and many customers do not commit to fixed volumes which may cause mismatch in our hedging. If the cost of raw materials or packaging materials increases, we may be unable to pass these costs on, in a full or timely manner, to our customers, and our competitors may have taken a long or short position that could provide them with an advantage. Any inability to pass these increases on fully to our customers on a timely basis or a fall in sales volumes due to price increases could have a material adverse effect on our business, financial condition, and results of operations.

Price fluctuations do not generally affect us where we act solely as a contract manufacturer of products on behalf of A-brand customers. Some of our A-brand customers direct us to purchase raw materials and packaging materials on their behalf and in accor dance with their specifications, including vendor selection and pricing terms. In such cases, we pass the cost of such purchases directly on to our A-brand customers.

In addition, our production sites use a significant amount of electricity, natural gas, and other energy sources. Fluctuations in the prices of fuel and other energy sources for which we do not have long-term pricing commitments or arrangements would affect our

operating costs, which could impact our business, financial condition, and results of operations.

How we address these risksWe have strong relationships with the majority of these suppliers and we have been able to hedge part of our requirements through medium-term contracts.

In 2012, the cost of many raw materials and packaging materials remained at high levels. In general, we purchase raw materials and commodities through forward contracts in order to cover sales positions with our customers, a policy called “back-to-back coverage”. The remaining risks are substantially mitigated through a combination of sales price increases, supply chain savings, and improvements in mix. Where appropriate, we also use exchange-traded futures to hedge price movements, especially in U.S. dollar purchases. Partly as a result of the recent acquisitions, Refresco has increasingly become a comprehensive soft drinks bottler rather than mainly a fruit juice producer. This has reduced the supply-side risk associated with vulnerability to individual commodities, raw materials, and packaging and also to the countries that supply them.

Risks related to seasonality Our sales are subject to seasonality. Recent acquisitions have contributed to the seasonal nature of our business through shifts in product portfolio towards carbonated soft drinks and water. Sales are generally higher in the summer months of April through September and lower during the winter months of October through March. While these factors lead to a natural

seasona lity in our sales, unseasonable weather can also significantly affect our sales and profitability compared to previous comparable periods. For example, during prolonged periods of unseasonably hot weather, consumers tend to switch to products such as water and RTD teas that may have lower profit margins as well as require us to adjust our product mix in other ways. Consequently, our operating results may fluctuate quarter to quarter. We also tend to experience a period of higher sales around the Christmas/New Year holiday period in late December through early January. Consequently, our operating results can fluctuate. Any inability to adapt to our customers’ requirements in terms of seasonality may result in lost sales which we are unable to recover and this could have a material adverse effect on our business, financial condition, and results of operations.

How we address these risksWe partner closely with customers on supply chain planning and execution to ensure optimal utilization of our manufacturing plans during low and high seasons. We have taken steps to increase the flexibility of our cost base to improve our adaptability to volume fluctuations.

Risks related to customer concentrationRefresco deals with several large customers but as the company grows through acquisition, concentration on individual customers has decreased. In 2012, our ten largest customers represented approximately 59.1% of revenue.

How we address these risksOver time, Refresco has re-balanced its customer portfolio, which in the early

Governance

Refresco • Annual Report 2012 45

years consisted mainly of retailers, with a larger share of A-brand manufacturers, creating greater long-term stability. Whereas contracts with retailers are renegotiated annually, we close bottling agreements with A-brand manufacturers for 3 to 5 years, thereby creating greater capacity utilization. We carefully manage our international customer relationships, monitoring growth and profitability and where necessary adjusting costs, complexity, and capacity. In 2012 we strengthened the Group Commerce function to ensure a strong focus on the opportunities and challenges in today’s markets and to further strengthen the coordination and development of our international customers. In order to reduce exposure to credit risk, we subject our customers to credit limits and creditworthiness tests, and sales are subject to payment conditions that are common practice in each country in which we operate. Material losses because of credit risk are not likely, especially due to the geographic diversification of our operations. We carefully monitor the effects of the economic downturn on our customers. As our customers are leading European or global retailers and A-brand companies, we do not insure credit risks.

The Group does not have any significant concentration of credit risk. Risks related to food safetyBecause the supply chain has become more and more globalized, increasing levels of regulatory and consumer focus continue to render food safety one of Refresco’s most significant business risks. Refresco may be faced with food- related problems, including dis ruptions to the supply chain caused by foodborne

illnesses, and these may have a material adverse effect on Refresco’s reputation, business, financial condition, and results of operations.

How we address these risksTo mitigate these risks and to ensure food safety and quality, all production sites have implemented their own quality system (HACCP) based on the critical control and quality points in their production processes. Additionally, to further ensure food safety, all production sites have been certified either under the International Food Standard (IFS) or, in the UK, under the British Retail Consortium (BRC) protocol. In many cases our manufacturing sites are also annually certified by A-brand customers. Refresco representatives also regularly visit and audit key suppliers and the results of these visits determine whether we accept, continue, or discontinue these relationships. Notwithstanding economic circumstances, Refresco remains dedicated to its quality standards.

Risks related to continuity of productionOperations at our production sites could be adversely affected by extra ordinary events, including fire, explosion, release of high-temperature steam or water, structural collapse, chemical spill, mechanical failure, extended or extraordinary maintenance, road construction or closures of primary access routes, severe weather conditions, directives from government agencies, or power interruptions. Any prolonged interruption at our production sites could materially reduce our production, sales revenue, and results of operations.

Any sustained interruption in production at any of our main production sites

could have a material adverse effect on our business, financial condition, and results of operations.

How we address these risksRefresco continues to invest significantly in its production sites and continuously strives for improvements in its health, safety, and environmental practices.