from adapting to transforming in a ch i tilithanging...

TRANSCRIPT

From adapting to From adapting to transforming in a transforming in a

h i tilith i tilitchanging utility changing utility industryindustryEelco de Jong

industryindustry

Georgia Tech Energy SeriesNovember 12th, 2014

Eelco de Jong

CONFIDENTIAL AND PROPRIETARYAny use of this material without specific permission of McKinsey & Company is strictly prohibited

Key themes for todayMCKINSEY PROPRIETARY AND CONFIDENTIAL

Transforming, not adapting

Disruption: glass half empty

Actions that define winners

McKinsey & Company | 1

Are these headlines alarmist or “in-the-money”?MCKINSEY PROPRIETARY AND CONFIDENTIAL

McKinsey & Company | 2

What are the facts?

Demand growth forecasts are being adjusted… down

A f d i EIA AEO P

Historical growth rateLong-term electric consumptionannual growth rate1

2.62.4

As forecasted in EIA AEO, Percent

1.51.8

0.7

1.1 -1.1%

McKinsey & Company | 31 Normalized to 2005-25 CAGR for all AEOs

1960-1990 1990-2010 082004 06 2010

Five technology-based drivers are transforming the industryMCKINSEY PROPRIETARY AND CONFIDENTIAL

Unconventional gas and oil

New “economic pillar” that rebases the value of generation

Centralized renewables

Policy and technology curve leading to commercially competitive build

Distributed generation

Fast decreasing costs improve competitiveness causing relocation of generation to lower voltage

Energy efficiency

Innovations, policies and big data driving next wave of adoption; integrating customer into supply curve

Customer awareness

g g pp y

Customer expectations, experience and activity rising to unparalleled levels

McKinsey & Company | 4

levels

Views on transformation change

When you see a So, despite the risks that

MCKINSEY PROPRIETARY AND CONFIDENTIAL

When you see a disruptive technology

come into your space if you don’t

So, despite the risks that a rapidly growing level of

distributed energy resources penetration and space, if you don t

embrace it… the people who try and cling to the past get

resources penetration and other disruptive challenges

may impose, they are not currently being discussed cling to the past get

rolled overcurrently being discussed

by the investment community and factored

i t th l tiDavid Crane,

CEO NRG

into the valuation

Edison Electric Institute

McKinsey & Company | 5

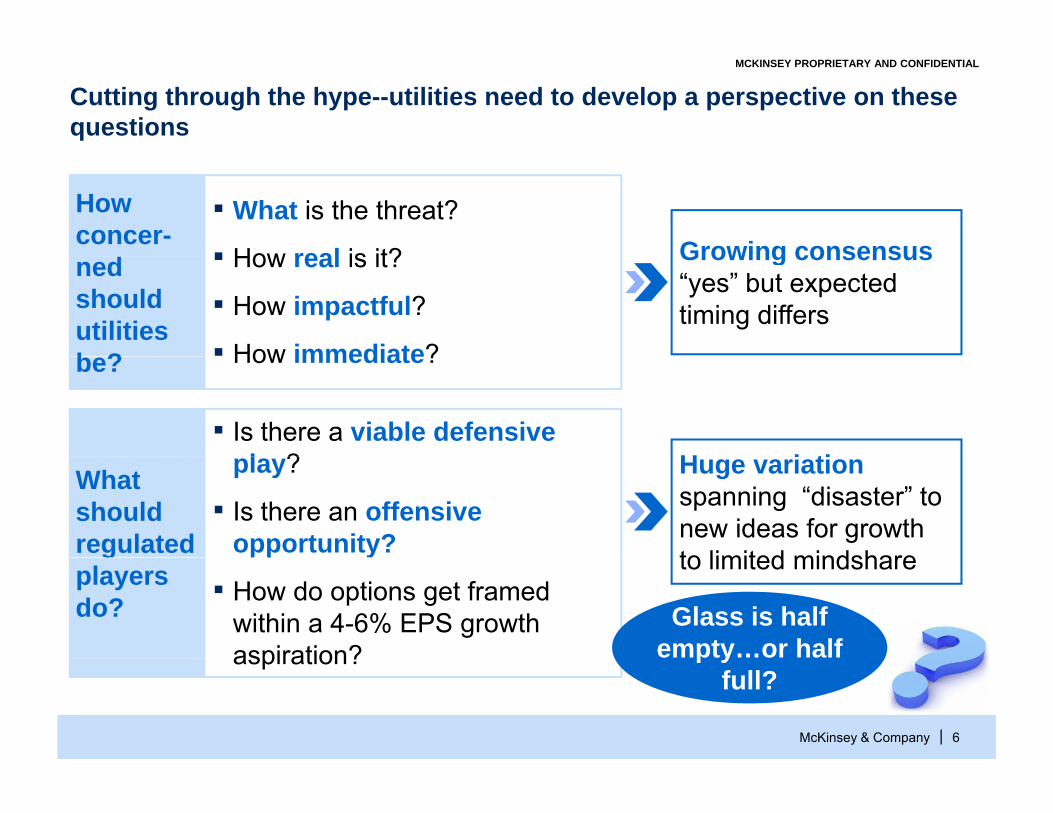

Cutting through the hype--utilities need to develop a perspective on these questions

MCKINSEY PROPRIETARY AND CONFIDENTIAL

Growing consensus▪ What is the threat?

▪ How real is it?

How concer- Growing consensus

“yes” but expected timing differs

▪ How real is it?

▪ How impactful?

▪ How immediate?

nedshould utilities b ? How immediate?be?

H i ti▪ Is there a viable defensive

l ? Huge variation spanning “disaster” to new ideas for growth to limited mindshare

play?

▪ Is there an offensive opportunity?

What should regulated to limited mindsharey

▪ How do options get framed within a 4-6% EPS growth aspiration?

gplayers do? Glass is half

empty…or half

McKinsey & Company | 6

aspiration? p yfull?

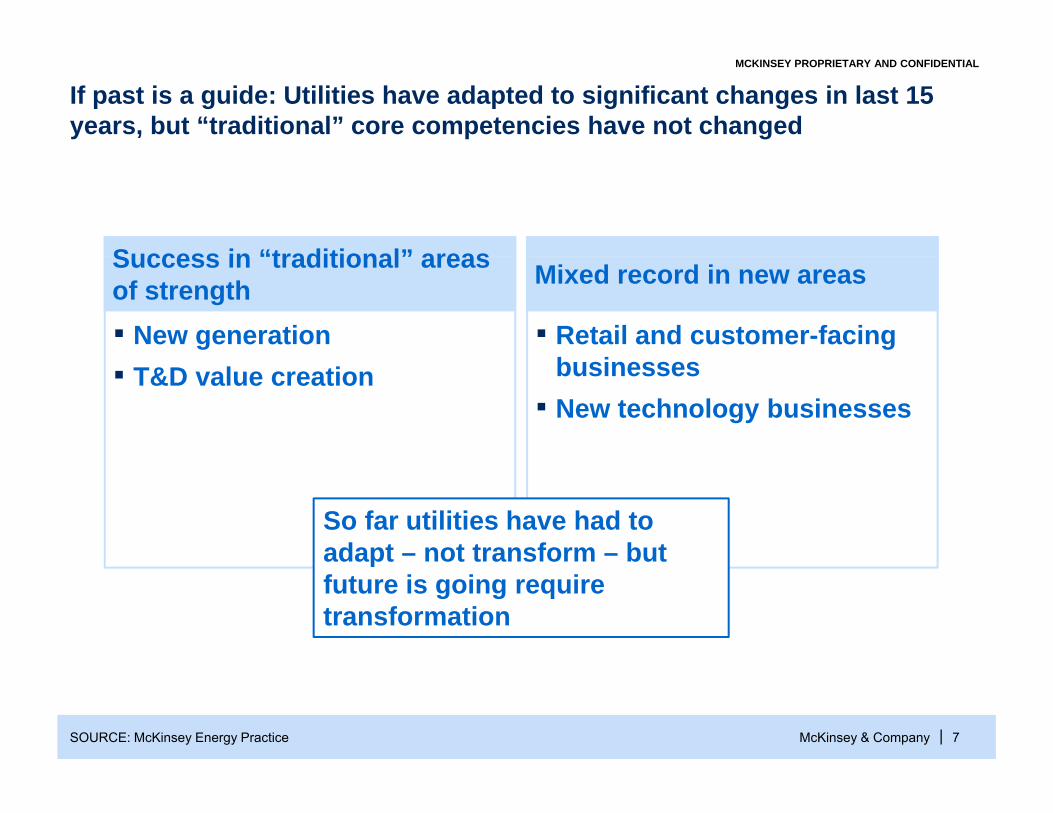

If past is a guide: Utilities have adapted to significant changes in last 15 years, but “traditional” core competencies have not changed

MCKINSEY PROPRIETARY AND CONFIDENTIAL

Success in “traditional” areasSuccess in “traditional” areas of strength Mixed record in new areas

▪ Retail and customer-facing ▪ New generationbusinesses

▪ New technology businesses▪ T&D value creation

So far utilities have had to adapt – not transform – butadapt not transform but future is going require transformation

McKinsey & Company | 7SOURCE: McKinsey Energy Practice

Key themes for todayMCKINSEY PROPRIETARY AND CONFIDENTIAL

Transforming, not adapting

Disruption: glass half empty

Actions that define winners

McKinsey & Company | 8

Trends are having a meaningful impact on load growthDEMAND DESTRUCTION MCKINSEY PROPRIETARY AND CONFIDENTIAL

100% = baseline load forecast for 2023 Kwh load

Calculated demand across selected US States

2%100%

5%

2%

18%

2%2%

-22%7%

83%

5%

Efficiency standards

Competitive efficiency b i

New energy efficient t h l

Utility EE programs /d d

Total demand

Distributed Solar PV

Co-generation

2023 demand

10 year growth

2012 demand

McKinsey & Company | 9SOURCE: McKinsey Electric Power Practice

business models

technology/demand elasticity

Price erosion the key enabler for residential LEDs

Compact fluorescent lights took off

ENERGY EFFICIENCY

… and LED bulbs are rapidly

CFL share1 and ASP

p garound $5-10 …

Retail price of LED retrofit bulb, Dollars

p yapproaching that price point

60

(USD)

60

(Percent)

40

50

40

50

20

30 30

20

0

10

’951990 ’05’00 ’10

10

0

McKinsey & Company | 10SOURCE: U.S. DOE, U.S. EPA, GE Web site

951990 0500 101 U.S. market shares on annual replacement sales.

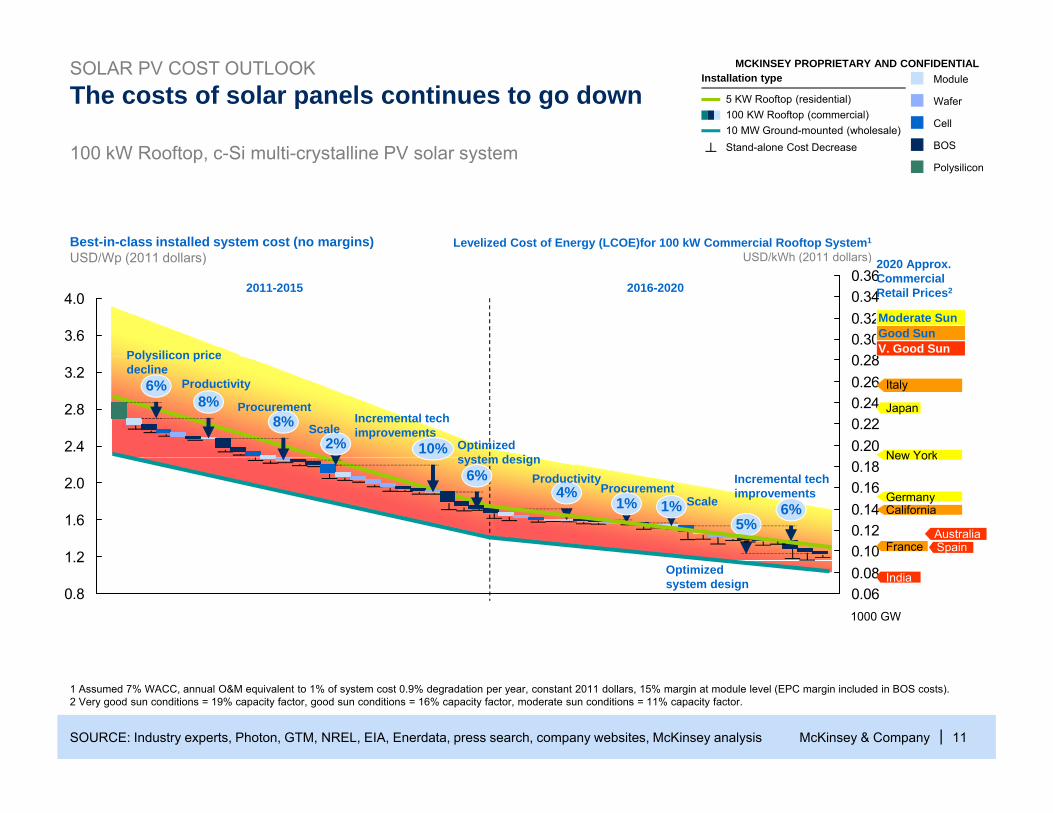

100 kW Rooftop c-Si multi-crystalline PV solar system

The costs of solar panels continues to go down Wafer

BOS

Cell

ModuleSOLAR PV COST OUTLOOK Installation type

5 KW Rooftop (residential)100 KW Rooftop (commercial)

Stand-alone Cost Decrease10 MW Ground-mounted (wholesale)

MCKINSEY PROPRIETARY AND CONFIDENTIAL

Best-in-class installed system cost (no margins)USD/Wp (2011 dollars)

100 kW Rooftop, c Si multi crystalline PV solar systemPolysilicon

Levelized Cost of Energy (LCOE)for 100 kW Commercial Rooftop System1

USD/kWh (2011 dollars)USD/Wp (2011 dollars)

0 280.300.320.340.36

3.6

4.02011-2015 2016-2020

Polysilicon price

USD/kWh (2011 dollars) 2020 Approx. Commercial Retail Prices2

V. Good SunGood SunModerate Sun

0.200.220.240.260.28

2.4

2.8

3.2

8%2%

6%8%

10%

Productivity

Procurement

Optimized s stem design

ScaleIncremental techimprovements

Polysilicon pricedecline

Italy

New York

Japan

0.100.120.140.160.18

1 2

1.6

2.01% 6%

6%4%

1%5%

system designProductivity

ProcurementScale

Incremental techimprovements Germany

California

FranceAustralia

New York

Spain

0.060.08

0.8

1.2Optimized system design India

1000 GW

McKinsey & Company | 11SOURCE: Industry experts, Photon, GTM, NREL, EIA, Enerdata, press search, company websites, McKinsey analysis

1 Assumed 7% WACC, annual O&M equivalent to 1% of system cost 0.9% degradation per year, constant 2011 dollars, 15% margin at module level (EPC margin included in BOS costs). 2 Very good sun conditions = 19% capacity factor, good sun conditions = 16% capacity factor, moderate sun conditions = 11% capacity factor.

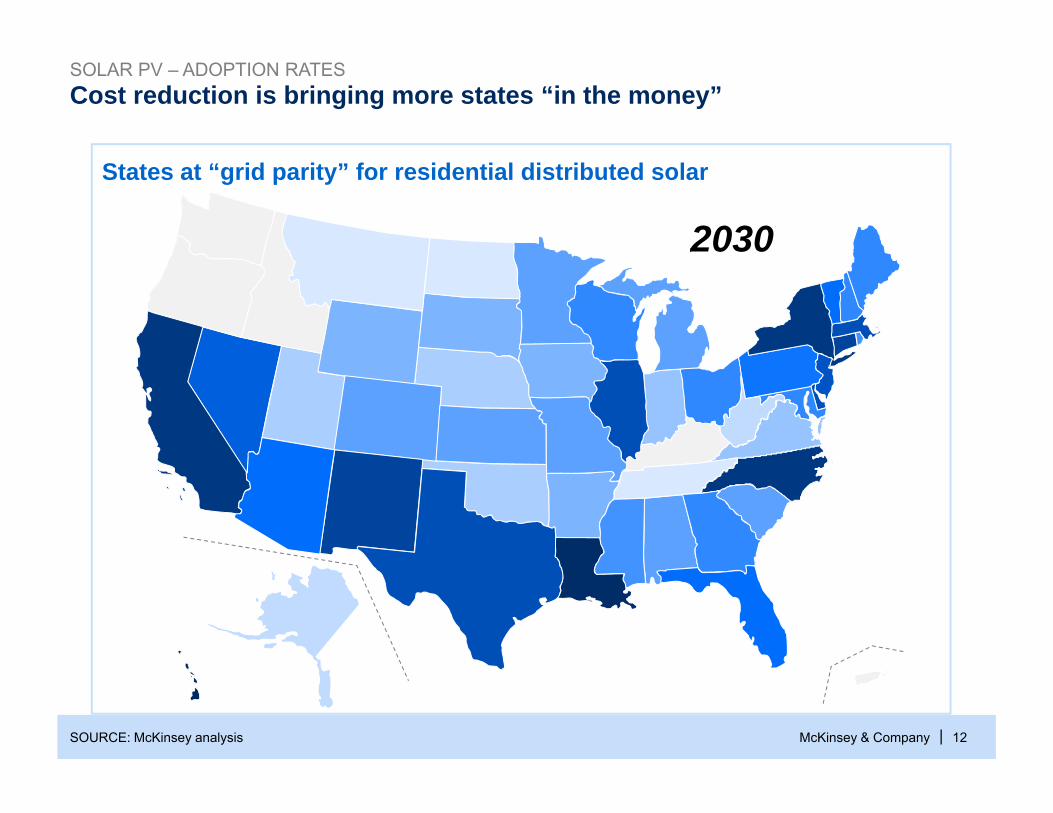

Cost reduction is bringing more states “in the money”SOLAR PV – ADOPTION RATES

20122013201420152016201920202021202220232024202520262027202820292030

States at “grid parity” for residential distributed solar

McKinsey & Company | 12SOURCE: McKinsey analysis

Actual observed installation rates: rapid solar uptake at “grid parity”SOLAR PV – ADOPTION RATES

5.0

Solar adoption rate% of total demand erosion in that year

HIAZ

3.0

2.5 NMNJ3

HI

1.5

2.0

NJ-Com3

GermanyNV

1.0

0.5

NJ Com

060400-20-40-60-140 20-30-50 10-10 30 50 70

McKinsey & Company | 13SOURCE: BMU, BSW, GTM Research, Ventyx Energy Velocity, press search; team analysis

Price discount %Solar LCOE (incl. incentives) vs. residential rate

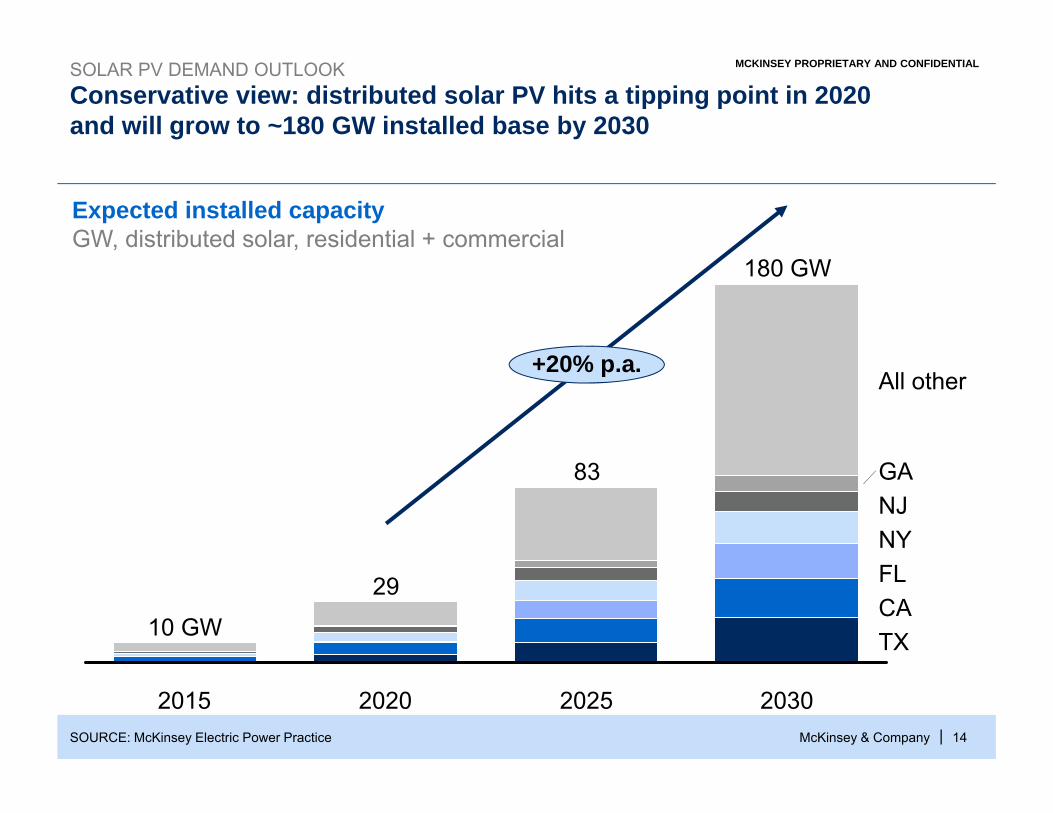

Conservative view: distributed solar PV hits a tipping point in 2020 and will grow to ~180 GW installed base by 2030

SOLAR PV DEMAND OUTLOOK MCKINSEY PROPRIETARY AND CONFIDENTIAL

Expected installed capacityGW, distributed solar, residential + commercial

20%

180 GW

+20% p.a.All other

GANJNY

83

29

10 GW TXCAFL

McKinsey & Company | 14

2015 203020252020SOURCE: McKinsey Electric Power Practice

Winning players are aggressively working down “soft costs” NORTH AMERICA SOLAR COST FOCUS MCKINSEY PROPRIETARY AND CONFIDENTIAL

3.32

Expected reduction in installed PV solar system costs – residential

USD/Wp

1.421.63

3.32

0.520.67

0 43

0.380.320.59 0.68

0.43

Installer margin

2011 Others1Installationlabor

Customer acquisition

2020

McKinsey & Company | 15SOURCE: McKinsey analysis, Expert interviews, NREL, LBNL

1 Includes Sales Tax, Permit Fees and PII (permitting inspection and interconnection)2 Variability based on sales tax cut realization of 50% in pessimistic scenario

Key themes for todayMCKINSEY PROPRIETARY AND CONFIDENTIAL

Transforming, not adapting

Disruption: glass half empty

A ti d fi i iActions defining winners

McKinsey & Company | 16

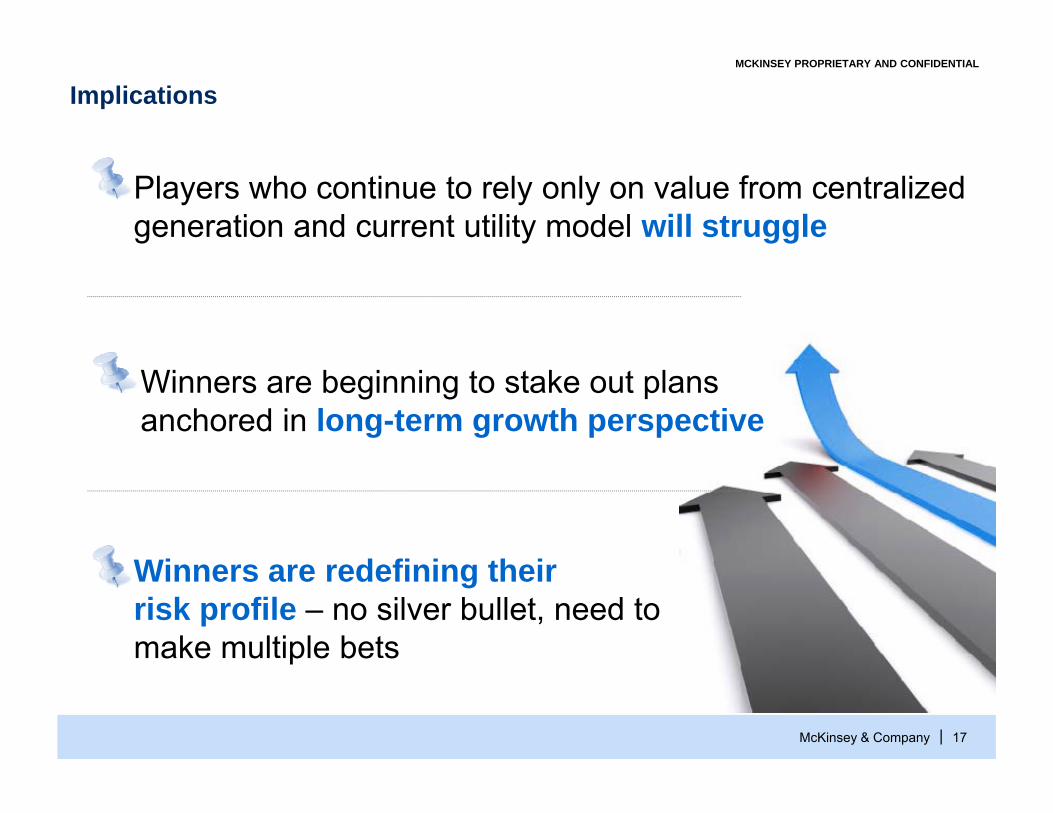

ImplicationsMCKINSEY PROPRIETARY AND CONFIDENTIAL

Players who continue to rely only on value from centralized generation and current utility model will struggle

Winners are beginning to stake out plans anchored in long-term growth perspective

Winners are redefining their risk profile – no silver bullet, need to make multiple bets

McKinsey & Company | 17

a e u p e be s

McKinsey’s view is that companies need to simultaneously manage “three horizons” to take the glass half-full approach

MCKINSEY PROPRIETARY AND CONFIDENTIAL

“Find ways to grow”

“Find new ways to change the industry”

“Sustain earnings growth to invest in the future”

“Find ways to grow”

Find new growth

Adopt new business models

Optimize the core

Find new growth opportunities

▪ Master new technologies and products

▪ Get close to the▪ Protect the core

b i ▪ Get close to the customer

▪ Innovate the business model – including rate

business▪ Invest in growth

opportunities: transmission,

▪ Optimize operational performance

▪ Sustain EPS in a tough structuresrenewables

▪ M&A?

genvironment

▪ Create headroom to fund future growth

McKinsey & Company | 18

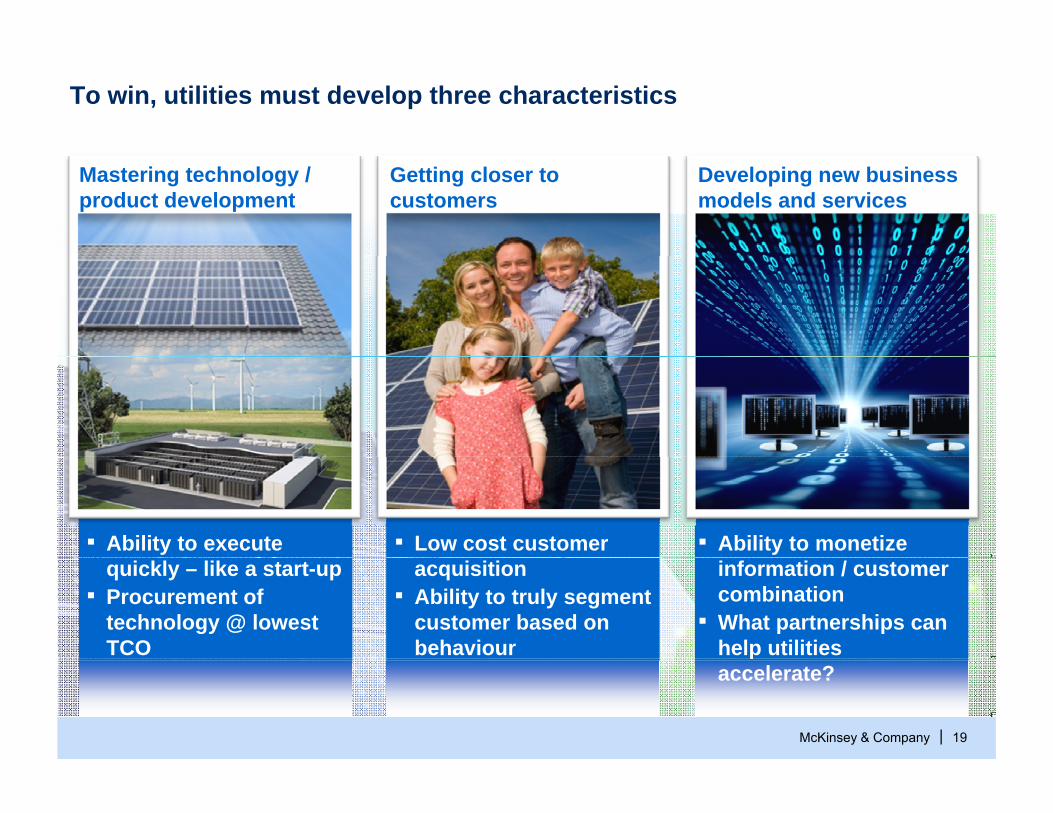

To win, utilities must develop three characteristics

Mastering technology / product development

Getting closer to customers

Developing new business models and services

▪ Ability to execute ▪ Low cost customer ▪ Ability to monetize quickly – like a start-up

▪ Procurement of technology @ lowest TCO

acquisition▪ Ability to truly segment

customer based on behaviour

information / customer combination

▪ What partnerships can help utilities

McKinsey & Company | 19

paccelerate?

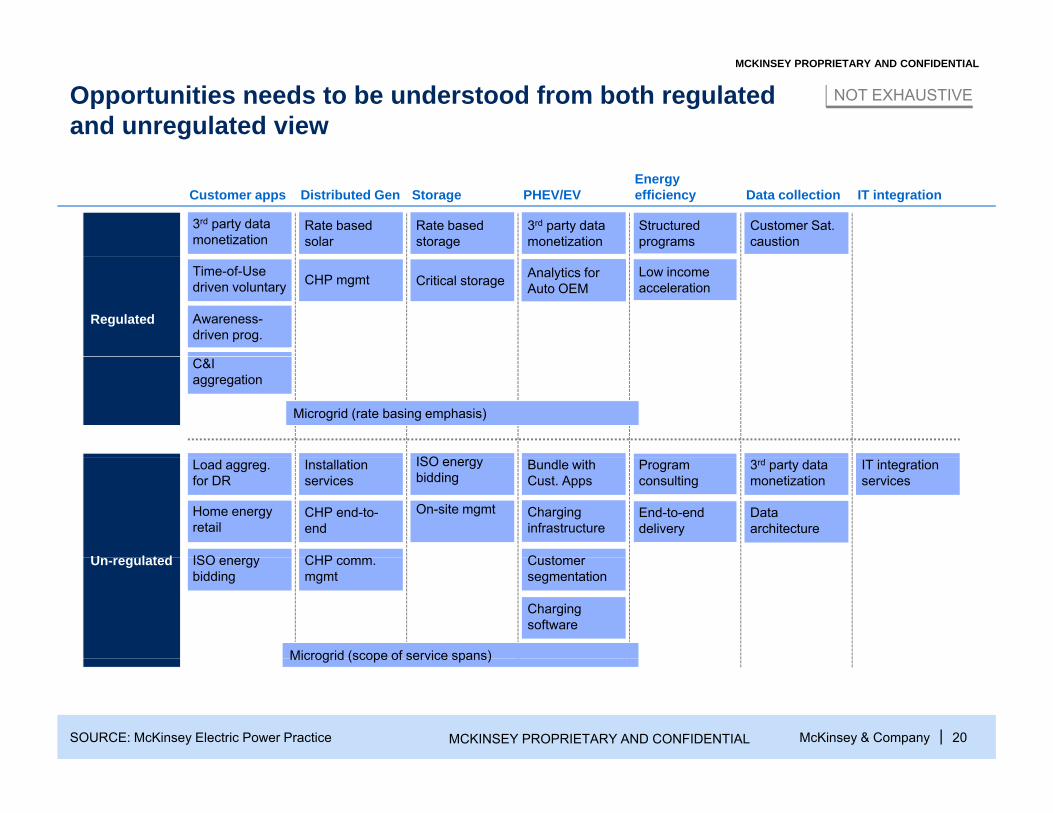

Opportunities needs to be understood from both regulated and unregulated view

NOT EXHAUSTIVE

MCKINSEY PROPRIETARY AND CONFIDENTIAL

Customer apps Distributed Gen Storage PHEV/EVEnergy efficiency Data collection IT integration

Rate based solar

3rd party data monetization

Rate based storage

3rd party data monetization

Structured programs

Customer Sat. caustion

Analytics for Auto OEM

Regulated

CHP mgmt Critical storageTime-of-Use driven voluntary

Awareness-driven prog.

Low income acceleration

Analytics for Auto OEM

C&I aggregation

ISO

Microgrid (rate basing emphasis)

U l t d

ISO energy bidding

Installation services

Load aggreg. for DR

Home energy retail

On-site mgmtCHP end-to-end

Bundle with Cust. Apps

Charging infrastructure

C tISO CHP

3rd party data monetization

IT integration services

Program consulting

End-to-end delivery

Data architecture

Un-regulated Customer segmentation

ISO energy bidding

CHP comm. mgmt

Charging software

Microgrid (scope of service spans)

McKinsey & Company | 20MCKINSEY PROPRIETARY AND CONFIDENTIALSOURCE: McKinsey Electric Power Practice

Microgrid (scope of service spans)

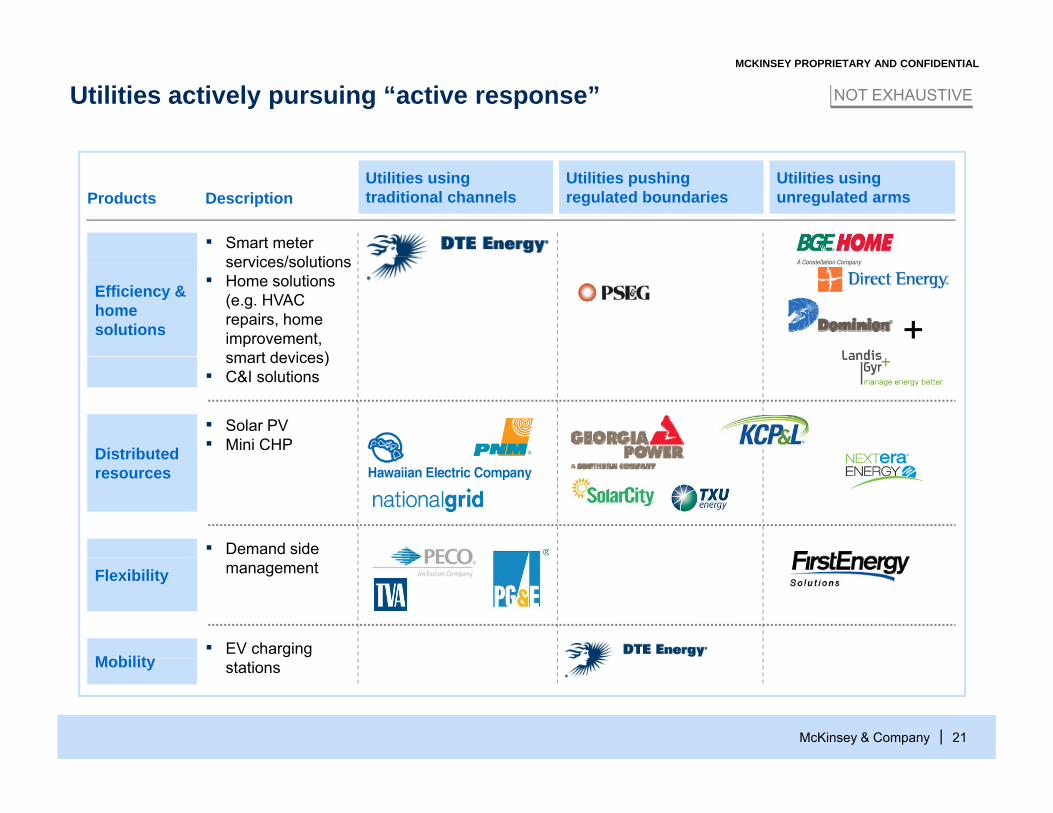

NOT EXHAUSTIVEUtilities actively pursuing “active response”MCKINSEY PROPRIETARY AND CONFIDENTIAL

Utilities using unregulated arms

Utilities pushing regulated boundaries

Utilities using traditional channelsProducts

▪ Smart meter i / l ti

Description

Efficiency & home solutions

services/solutions▪ Home solutions

(e.g. HVAC repairs, home improvement, smart devices)

+smart devices)

▪ C&I solutions

Distributed

▪ Solar PV▪ Mini CHPDistributed

resources

▪ Demand side

M bilit▪ EV charging

Flexibility management

McKinsey & Company | 21

Mobility stations

The challenge – utilities need to think “beyond commodities”

Energy retailers bundled free energy

Old model“The pure-play energy manager”

“

New model: make money on the added services

bundled free energy management and services products

▪ “Energy management package”: $8.99/month plus one-time $50 activation fee (on top of standard home security package)home security package)

▪ Includes 1 smart thermostat, 1 appliance control, 12 EE light bulbs and home energy monitoring/advice

“The digital home provider” ▪ Energy management controls and

monitoring bundled with home automation / security package from incumbent telco or cableco

McKinsey & Company | 22SOURCE: McKinsey Energy Practice

€/MWh €/customer

Companies are exploring alternatives to our current rate model

Challenge Examples

No accurate price▪ Can we sustain a volumetric rate vs. largely

fixed cost base?No accurate price signals ▪ Net metering -- who is paying for back-up and

grid?

No cost recovery of core services

▪ Services that are “free”: universal access, back-up power

▪ Are customers willing to pay the full costs of g p ythese?

▪ What if utilities were allowed to build distributed solar?Limited ability to play in

competitive sectorssolar?

▪ What would happen if utilities would be in charge of your energy efficiency?

McKinsey & Company | 23SOURCE: McKinsey

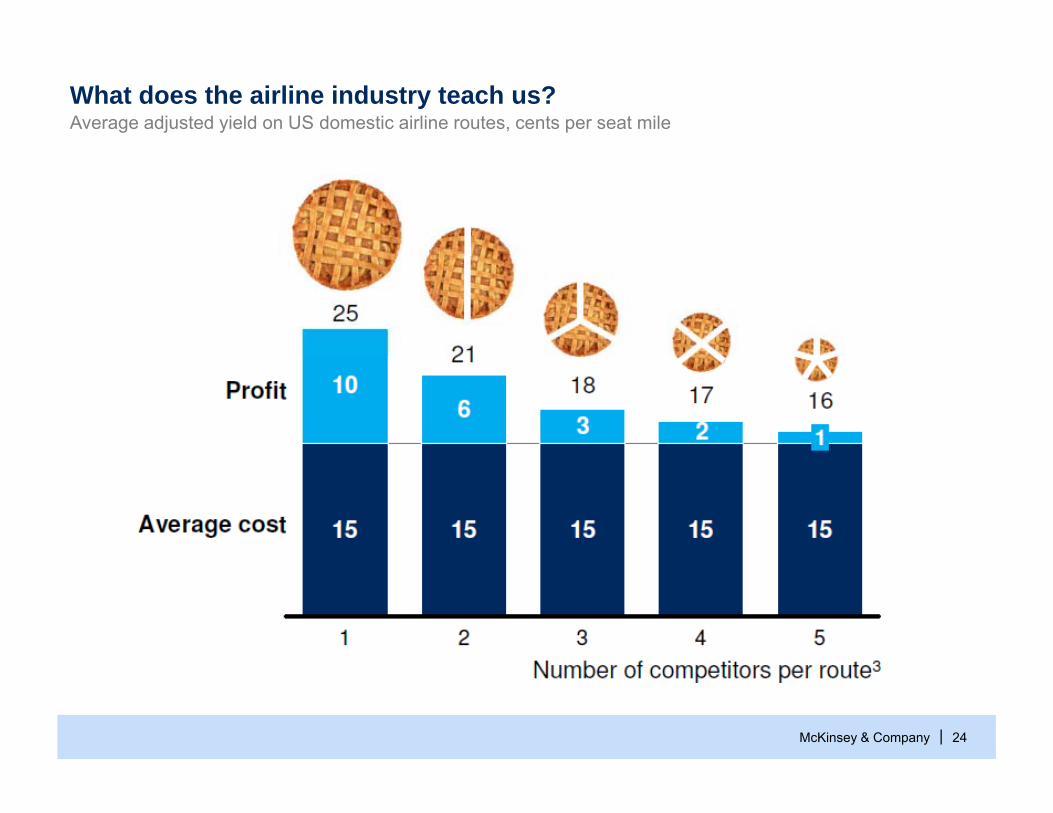

What does the airline industry teach us? Average adjusted yield on US domestic airline routes, cents per seat mile

McKinsey & Company | 24

Organized

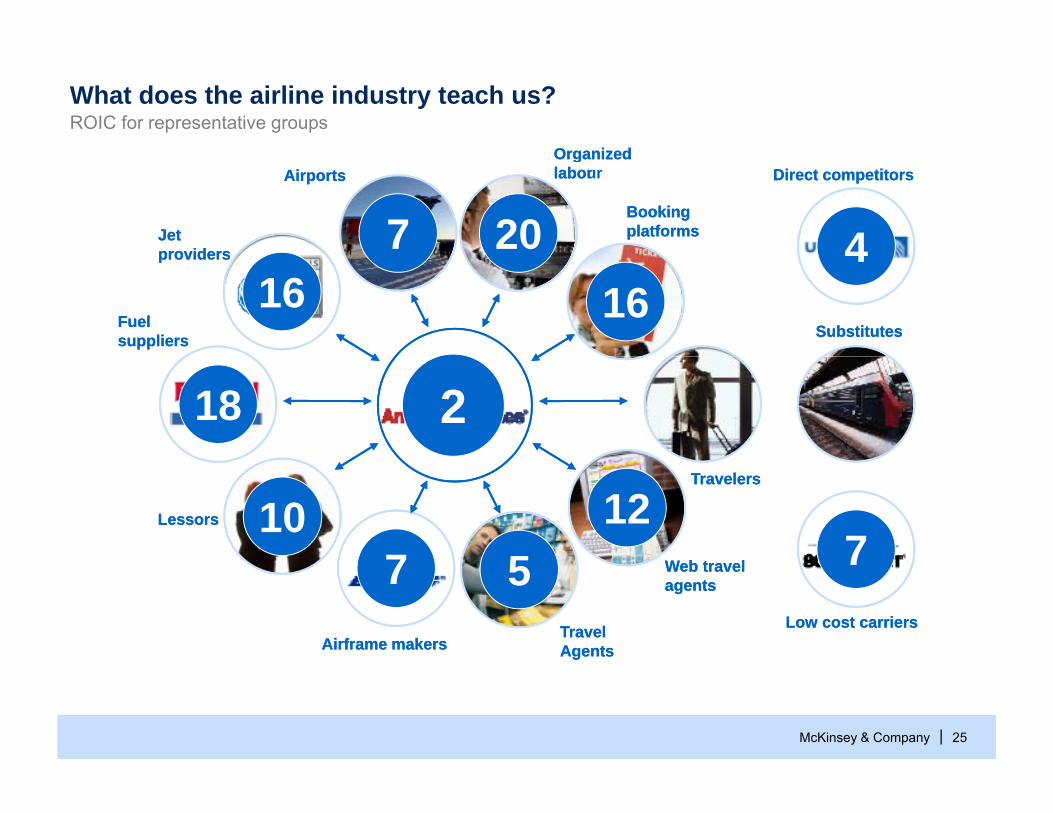

What does the airline industry teach us? ROIC for representative groups

Organized

Jet providers

Booking platforms

Organized labour Direct competitorsAirports

Jet providers

Booking platforms

Organized labor Direct competitorsAirports

207 4providers

Fuel suppliers Substitutes

providers

Fuel suppliers Substitutes

16 164

18 2

Lessors

Travelers

Lessors

Travelers

107 5

127

Airframe makersTravel Agents

Web travel agents

Low cost carriersAirframe makers

Travel Agents

Web travel agents

Low cost carriers

7 5 7

McKinsey & Company | 25

gg

Glass half full or half empty?

McKinsey & Company | 26