free exchange financial indulgence - rollins...

TRANSCRIPT

India in trouble

The reckoning

Why India is particularly vulnerable to the turbulence rattling emerging markets

Aug 24th 2013 | MUMBAI | From the print edition

ON THE morning of August 17th most of India’s economic policymakers gathered in the prime minister’s house in Delhi. They were there to launch an official economic history of 1981-97, a period which included the balance-of-payments crisis of 1991. The mood was tense. India, said Manmohan Singh, the prime minister, faced “very difficult circumstances”. “Does history repeat itself?” asked Duvvuri Subbarao, the outgoing head of the Reserve Bank of India (RBI). “As if we learn nothing from one crisis to another?”

The day before Indian financial markets had had their rockiest session for many years. The rupee sank and stockmarkets tumbled. Money-market rates rose. The shares of banks thought to be either full of bad debts or short of deposit funding fell sharply. The sell-off had been made worse by new capital controls introduced on August 14th in response to incipient signs of capital flight. They reduce the amount Indian residents and firms can take out of the country. Foreign investors took fright, fearful that India might freeze their funds too, much as Malaysia did during its crisis in 1998.

India’s authorities have since ruled that out. But markets keep sliding. On August 20th the RBI said it would intervene to try to calm bond yields. The rupee has dropped to over 64 to the dollar, an all-time low and 13% below its level three months ago. It is widely agreed the country is in its worst economic bind since 1991.

India is not being singled out. Since May, when the Federal Reserve first said it might slow the pace of its asset purchases, investors have begun adjusting to a world without ultra-cheap money. There has been a great withdrawal of funds from emerging markets, where most currencies have fallen by 5-15% against the dollar in the past three months. Bond yields have risen from Brazil to Thailand. Some governments have intervened. On July 11th Indonesia raised its benchmark interest rate to bolster its currency. On August 21st its president said he would soon announce further measures to ensure stability.

India, Asia’s third-biggest economy, is more vulnerable than most, however. Economic news has disappointed for two years, with growth falling to 4-5%, half the rate seen during the 2003-08 boom. It may fall further. Consumer-price inflation remains stubborn at 10%. A drive by Palaniappan Chidambaram, the finance minister, to push through a package of reforms and free big industrial projects from red tape has not worked. An election is due by May 2014, adding to uncertainty.

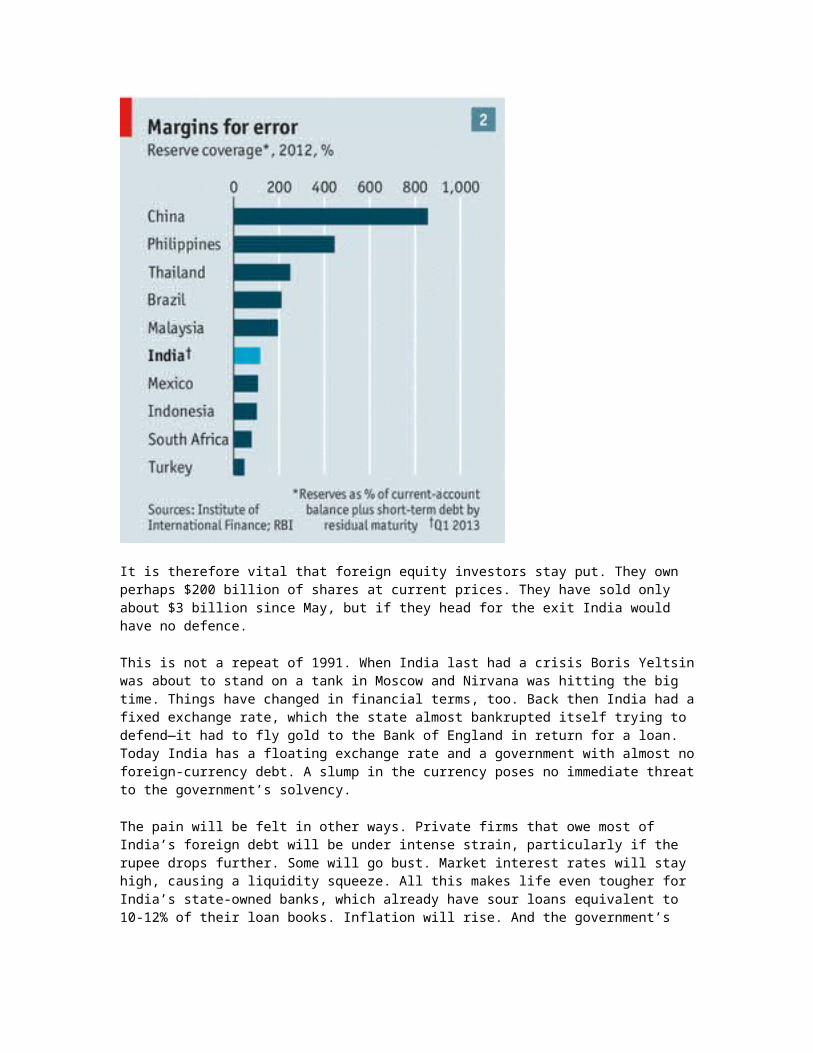

India’s dependence on foreign capital is also high and has risen sharply. The current-account deficit soared to almost 7% of GDP at the end of 2012, although it is expected to be 4-5% this year. External borrowing has not risen by much relative to GDP—the ratio stands at 21% today—but debt has become more short-term, and therefore riskier. Total financing needs (defined as the current-account deficit plus debt that needs rolling over) are $250 billion over the next year. India’s reserves are $279 billion, giving a coverage ratio of 1.1 times. That has fallen sharply from over three times in 2007-08 (see chart 1) and leaves India looking weaker than many of its peers (see chart 2).

It is therefore vital that foreign equity investors stay put. They own perhaps $200 billion of shares at current prices. They have sold only about $3 billion since May, but if they head for the exit India would have no defence.

This is not a repeat of 1991. When India last had a crisis Boris Yeltsin was about to stand on a tank in Moscow and Nirvana was hitting the big time. Things have changed in financial terms, too. Back then India had a fixed exchange rate, which the state almost bankrupted itself trying to defend—it had to fly gold to the Bank of England in return for a loan. Today India has a floating exchange rate and a government with almost no foreign-currency debt. A slump in the currency poses no immediate threat to the government’s solvency.

The pain will be felt in other ways. Private firms that owe most of India’s foreign debt will be under intense strain, particularly if the rupee drops further. Some will go bust. Market interest rates will stay high, causing a liquidity squeeze. All this makes life even tougher for India’s state-owned banks, which already have sour loans equivalent to 10-12% of their loan books. Inflation will rise. And the government’s finances will be under strain as the cost of its subsidies on imported fuel gets bigger.

There is probably little the authorities can do to shore up the currency in the short term. The rupee is one of the world’s most actively traded currencies and at least half the turnover is abroad. Privately, officials reckon the rupee’s fair value, taking into account India’s higher inflation and productivity over the past few years, is a little less than 60 per dollar, so the market has yet to overshoot wildly. Raghuram Rajan, the incoming governor of the RBI, is likely to take a hands-off approach.

That doesn’t mean the government will—or should. On August 19th it banned the import through airports of duty-free flat-screen TVs, which Indians can often be seen heaving through check-in at Dubai. It may seek to raise duties further on gold imports, which Indians are addicted to in part because it is seen as a hedge against inflation. Gross gold imports were 3% of GDP last year, blowing a huge hole in the external finances. History suggests the higher taxes on gold imports are, the worse smuggling gets. But India imports 800-odd tonnes of bullion a year. That’s a lot of gold to hide in suitcases.

The government will also try to persuade the Supreme Court to lift its ban on iron-ore exports, imposed after a series of corruption scams. At its peak this industry generated exports worth about 0.4% of GDP, although experts doubt that mothballed mines can be ramped up fast. The government may also cut fuel subsidies. That would reduce demand for imported fuel and help it hit a fiscal-deficit target of about 7% of GDP (including India’s states).

The longer-term solution to the balance-of-payments problem may be to ramp up India’s manufacturing sector, and thus its industrial exports. But that will take a big improvement in the business climate, not just a cheap currency. Despite the rupee’s 27% tumble in the past three years there is scant sign of global manufacturers shifting production to India.

India’s position could still get worse. But assuming things stabilise, when the official histories come to be written about 2013, what might they say? Most likely that the rupee’s slump caused a severe shock to the economy that made a recovery in growth rates even harder. But perhaps, also, that it prompted a more serious debate about the policies that India needs to become less vulnerable to the whims of an unforgiving world.

Free exchange Financial indulgence

Cheap credit is tempting emerging markets towards risky borrowing

Apr 5th 2014 | From the print edition

“ORIGINAL sin” in the economic scriptures differs slightly from its theological counterpart. It is the observation, made in the aftermath of the emerging-market crises of the 1990s, that most countries are unable to borrow from foreigners in their own currency. Foreign-currency borrowing damns them, in times of trouble, to a vicious downward spiral: a loss of faith in a country’s currency makes its debts harder to repay. That in turn further reinforces doubts about its currency.

Of late this doctrine has begun to look a bit old-fashioned. Financial globalisation has freed many developing economies from the need to go cap in hand to foreign financial markets. With investors willing to lend in local markets (and often in the local currency), they have sharply reduced their overseas borrowing over the past decade. Yet some economists worry that their salvation remains incomplete. Old vulnerabilities are creeping back.

The 1990s crises were a Damascene moment for emerging markets, prompting broad changes in policy. Many developing countries managed to introduce serious fiscal and monetary reform. This cut overall borrowing needs and also reassured adventurous rich-world investors who were considering a plunge into emerging economies’ domestic bond markets. Most abandoned hard-currency pegs, smoothing their adjustment to shifting capital flows, and many accumulated large stocks of foreign-exchange reserves. Above all emerging markets sought to escape original sin.

Financial integration has helped. The International Monetary Fund’s latest Global Financial Stability Report points out that gross capital flows to emerging markets roughly quintupled from 2000 to 2010. From 2002 to 2010 the share of emerging-market debt issued in foreign markets dropped from 27% to 12% (see chart, left panel). This, in turn, helped governments reduce their vulnerability to sudden swings in exchange rates. In 1998 nearly a third of Turkey’s marketable government debt and more than half of that in Mexico was denominated in a foreign currency. By 2010 the share in both economies was below 20%.

That discipline has, however, begun to erode. In the aftermath of the global financial crisis, rich-world central banks unleashed a flood of liquidity to support their own sickly economies. As the deluge depressed interest rates investors went hunting abroad for better returns. Governments in emerging markets have mostly remained disciplined through this onslaught; the share of emerging-market government debt issued in foreign markets has continued to drop, from 12% in 2008 to 8% last year. Private firms, however, have been more likely to succumb to temptation.

Emerging-market companies have begun issuing foreign-currency-denominated debt with gusto: $1.3 trillion of it was outstanding in 2013, up from $597 billion in 2009, according to Nomura, a Japanese bank. As a result, foreign borrowing as a share of all emerging-economy borrowing has been climbing. Banks are leading the way. Since late 2008 the share of debt issued by financial firms abroad has risen steeply, from 15% to 22%, the IMF says.

Moreover, official figures on external borrowing may not capture the entire picture because of “hidden debt” being accumulated by emerging-market firms. Conventional measures typically include debt securities issued domestically and official cross-border bank lending—but not bonds issued in foreign markets by emerging-market multinationals. In a 2013 paper Hyun Song Shin, of Princeton University, and Laura Yi Zhao, of the Asian Development Bank, warned that nonfinancial firms may be borrowing cheaply abroad to make loans at home.

If bonds issued abroad by the foreign subsidiaries of Indian and Chinese firms are included in their national statistics, then the foreign-currency debt of non-financial firms looks twice as large as under the usual measure. Foreign issuance by Brazilian firms more than doubles its stock of private-sector external debt, according to a new Inter-American Development Bank report. Growth in this hidden debt has soared since 2008.

Whether these excesses amount to mortal sin is not easy to judge. New debt estimates assembled by Nomura take account of countries’ foreign-currency exposure via “hidden” offshore bonds. Such borrowing

makes some economies look shakier, it reckons, but not much. Hidden debt in Brazil and Russia amounts to 5% or more of GDP. But overall foreign-currency exposure is generally below the average of the past two decades (see chart, right panel). Nomura’s adjustment raises China’s foreign-currency debt from 9.2% of GDP to 9.3%: hardly the stuff of doom.

Living on a prayer

If there is little sign of imminent disaster, there is good reason to be vigilant. The flood of money from America and Britain may soon dry up, but the euro zone and Japan seem likely to keep providing yield-hungry investors, eager to lend on tempting terms. The trend towards foreign borrowing bears watching.

What is more, having only a small foreign-currency exposure may no longer be enough to protect emerging economies from swings in global sentiment—and monetary conditions. The financial maturation that allowed emerging economies to do more of their borrowing locally has necessarily raised foreign participation in local-government bond markets. In some economies, the share of local-market government debt owned by foreigners has more than doubled since 2009.

Investors continue to do a poor job discriminating between developing markets based on the underlying health of their economy. And stampeding capital can still apply uncomfortable financial pressure, as the market wobbles of the past year revealed. Falling currencies may hurt exposed firms’ balance-sheets, thereby weakening investment and the outlook for growth. An abrupt growth slowdown looks preferable to the crises of the late 1990s. But it is no Eden.

The Economist

Dollar imperialism 1Emerging marks

Feb 3rd 2014, 19:00 by S.C. | HONG KONG

WITH emerging markets still in some turmoil, it is easy to believe they are victims of something. But of what, exactly? In the past five days, four of our finest economists have proposed three answers.

1. Emerging markets are victims of the Fed, argues Raghuram Rajan, governor of India's central bank, the Reserve Bank of India (RBI).

2. They are victims of a "foreign-finance fetish", argue Dani Rodrik of Princeton and Arvind Subramanian of the Peterson Institute for International Economics.

3. They are, at bottom, victims of the rich world's "secular stagnation", argues Paul Krugman of the New York Times.

Over the next couple of posts, I hope to show there is an intellectual thread connecting these three positions. To give away the punchline: they all reject the optimistic view of the international monetary system best articulated in Rose (2006) and they are all working off the less appetising menu presented by Rey (2013) .

Let's start with Mr Rajan. A temperate man, the RBI governor seems, if not actually disgruntled, then far from gruntled, as Wodehouse would say. He believes that the Fed's unilateral tightening (ie, its decision to slow its bond purchases in December and again last month) betrays the spirit of multilateral loosening that followed the 2008-9 global financial crisis. His interview with Bloomberg TV India on January 30th is well worth watching (especially from 8m57s to 14m02s). In it, he makes several arguments.

i) The emerging markets were hurt both by the rich world's dramatic monetary easing half a decade ago and by the withdrawal of that easy money in recent months. In particular, "the easy money which flowed into their economies...made it easier to forget about the necessary reforms, the necessary fiscal actions that had to be taken."

ii) After the Lehman shock, the emerging markets did their bit to support global growth "with huge fiscal and monetary stimulus" of their own. But the "international monetary cooperation" shown at that time has since "broken down". In withdrawing monetary easing, industrial countries [ie America] are worrying only about their own economies, leaving the emerging markets to adjust as best they can.

iii) Emerging markets cannot leave that adjustment entirely to market prices, letting capital flow out and the exchange rate fall. This is because in emerging markets, the "fundamentals" and the "institutions" are not always "well anchored". As a result, "volatility feeds on itself".

iv) If emerging markets have to adjust on their own, they will. But the industrial countries "may not like the kinds of adjustments we will be forced to do down the line."

Mr Rajan's complaint--some have called it a rant--did not come out of nowhere. His argument echoes a closely reasoned 2011 report called "Rethinking Central Banking", published by the Brookings Institution and written by a committee of 16 respected economists, of which he was one. That report urged big central banks to "internalise the spillover effects of their policies", recommending that they meet at regular intervals to consider, and publicly report upon, the consequences of their decisions for everyone else. "Where appropriate, [large-country central banks] should consider coordinated action to help stabilise the global economy in times of stress," the report concluded.

One of Mr Rajan's co-authors for that report was Dani Rodrik, now at the Institute for Advanced Studies at Princeton. It may, therefore, have come as a surprise to the RBI governor when his criticism of Fed unilateralism (as well as similar concerns voiced by his peers) attracted a swift and sharp rebuttal from none other than Mr Rodrik, together with another of his former co-authors, Arvind Subramanian. In a nicely written piece for Bloomberg, the pair offered their response to the "crescendo of complaints", from Istanbul to Mumbai, about "dollar imperialism".

That term, "dollar imperialism", is associated with Vyacheslav Molotov, the Soviet diplomat after whom a certain cocktail was named. It is an incendiary topic, which I hope to explore a bit further in my next post.

Dollar imperialism 3Tactless tapering

Feb 5th 2014, 10:18 by S.C. | HONG KONG

IN THE Financial Times, Willem Buiter, the outspoken chief economist at Citi, adds his voice to the chorus of complaints about Fed unilateralism. By failing even to mention the overseas effects of its tapering, the Fed has displayed bad manners, Mr Buiter argues. He supports the plaintive call by Raghu Rajan, governor of the Reserve Bank of India (RBI), for more co-operation between central banks.

The dollar is imperial; the Fed is parochial. That seems to be the nub of the problem. If so, there are two logical solutions. One is to limit the dollar's sway. The other is to expand the Fed's sympathies.

The first is difficult. The second, potentially illegal. The Fed's parochialism is the product of both economic circumstance and legislative design. It is required by law to care about US inflation, US employment and long-term US interest rates. This limited circle of concern is hardly unique to the Fed. Central banks around the world pay attention to everything that affects their economies. They do not pay attention to everything their economies affect.

That is as true of Raghu Rajan's Reserve Bank of India as it is of the Federal Reserve. Earlier this week, Amando Tetangco, who heads the central bank of the Philippines, warned that interest-rate "tweaks" by emerging economies might backfire, increasing financial volatility. Did Mr Rajan take that into account before tweaking rates last month? In the policy statement and conference calls accompanying his decision, he talked about the emerging-market turmoil only insofar as it affected India. He mentioned the Philippines not at all.

The RBI's statements do, of course, pay close attention to global economic forces. The Fed's recent statements, on the other hand, "could have been written by the central bank of a closed economy," according to Mr Buiter. But that is because the US economy is relatively closed (de facto if not de jure). Trade was equivalent to only 31% of its GDP in 2012. Over 140 countries have reported a higher ratio.

Cross-border financial flows are, of course, enormous. But since America's foreign liabilities are mostly priced in its own currency, they fall when the dollar falls. The things the Fed is legally obliged to care about (inflation and employment) respond only sluggishly to fluctuations in the exchange rate. It is but a small exaggeration to say that the only country that does not care about the dollar is America itself.

The Fed's legal constraints, Mr Buiter fully understands and acknowledges. "If the Fed were to attach any intrinsic weight to the effect of its actions on the rest of the world, it might be in violation of its legal mandate," he writes. His quarrel is not, in fact, with the Fed's mandate. It is instead with its analysis. Or, to be more precise, with the analysis he reads into their silence.

Since the Fed has not recently acknowledged the foreign repercussions of its tapering policy, Mr Buiter worries that it has not noticed those repercussions. "The Fed's silence on the external impact of its policies may indicate that it believes there are no external effects."

But that is surely too much of a stretch. The Fed must know its policies have had international consequences (even if it does not appreciate their full extent). It probably does not yet believe those external effects will come back to haunt America. That is the most you can read into its silence. To repeat: the Fed cares about (and therefore talks about) everything that affects America, not everything America affects.

External effects do not always remain safely external, of course. The foreign repercussions of Fed policy (which may include an unsustainable boom and bust in the big emerging markets) might have domestic repercussions for the US. "Through trade and financial linkages, financial and economic distress in foreign markets can come home to roost," Mr Buiter warns. But if and when that happens, you can be pretty sure

the Fed will mention it. In fact, the Fed will probably do something about it. It might even call Mr Rajan to discuss it.

Bloomberg

Emerging Markets’ Victimhood Narrative

By Dani Rodrik and Arvind Subramanian Jan 31, 2014 4:38 PM ET

A woman shops at a spice market in Istanbul, Turkey.

From Istanbul to Brasilia to Mumbai comes a crescendo of complaints about dollar imperialism. Heads of state and central bank governors allege that the policies of central banks in industrial countries, especially the U.S. Federal Reserve, pursued in self-interest, are wreaking havoc in emerging-market economies. This allegation is mostly unfair. Emerging markets aren’t hapless and undeserved victims; for the most part they are simply reaping what they sowed.

Start first with the strange symmetry of the complaints. When the Fed relaxed its policy via quantitative easing, emerging-market countries, especially Brazil, complained about the wall of money flooding their markets and putting upward pressure on their currencies. Now, with the Fed slowly unwinding the program, the complaint from emerging economies is that capital is fleeing. The Fed is damned regardless of whether it dams the supply of dollars or undams it. The Fed has received scant word of thanks for propping up the U.S. and, hence, the world economy at a time when policy elsewhere (especially in Europe) was so counterproductive.

Then there is the complaint about the asymmetry of cooperation. Emerging markets had supported global growth through huge fiscal and monetary stimulus in the aftermath of the Lehman Brothers Holdings Inc. crisis. However, as emerging markets experience volatility today, action or concern from industrial countries isn’t forthcoming. The problem with this nonreciprocal argument is, simply, that the stimulus enacted in 2008 and 2009 was entirely self-interested. The Fed may not be internalizing the objectives and constraints of other countries today, but neither did emerging markets act on the behalf of the Fed then. It isn’t convincing to cloak self-interest as unselfish cooperation.

The victimhood narrative is further misplaced for two broader reasons. Many large emerging-market countries have consciously and enthusiastically embraced financial globalization. Yes, the foreign finance fetish reigned as the prevailing ideology in the run-up to the Lehman crisis. But there were no domestic compulsions forcing these countries to so ardently woo foreign capital. Last summer, when a bout of volatility hit the fragile five -- Brazil, India, Indonesia, South Africa and Turkey -- many of them responded by trying to open up their economies and enact policies to attract even more capital.

Over the last five years in India, every episode of rupee pressure has provoked a relaxation of regulations on foreign inflows, which has rendered the economy vulnerable to the next rupee shock, which, in turn, provokes the next liberalization and so on. In Turkey, policy makers spun a tale of invulnerability to shocks and contagion even as the economy’s growth was driven by a flood of short-term capital inflows. China provides an instructive contrast. China has chosen to insulate itself from foreign capital and has correspondingly been less affected by the vagaries of Fed actions and the fickleness of foreign finance. Chinese policies aren’t blameless, but their economic insulation has afforded them the luxury of being the recipient of complaints rather than the distributor.

Having chosen to embrace financial globalization, emerging market countries then proceeded to follow economic policies that were bound to create volatility. The fragile five ran up large current account deficits; some of them also had high inflation and large fiscal deficits. These countries lapped up foreign funds instead of tightening lending regulations and imposing prudential controls. Political turmoil and looming uncertainty in the run-up to elections have compounded the problem.

It is evident that the world economy could do better with more international coordination. But the fact is that the emerging economies’ troubles are domestically generated problems and not the fault of foreigners. The complaint of emerging-market countries seems a classic case of blaming outsiders for choices and actions that have been predominantly domestic.

Emerging markets need to wake up to what many should have long known: Financial globalization is a decidedly mixed blessing. It is a source of volatility, and it exposes a country to the actions of others, especially the U.S., a nation with no obligation to charity.

(Dani Rodrik is a professor at the Institute for Advanced Study in Princeton, New Jersey, and Arvind Subramanian is senior fellow at the Peterson Institute for International Economics.)

Bloomberg

China Rebuts Lew as Emerging Markets Keep Up Pressure on Fed

By Shamim Adam, Michael Heath and Svenja O’Donnell Feb 22, 2014 11:06 PM ET

Scaffolding stands at a construction site close to the business district of Wanchai,... Read More

Feb. 23 (Bloomberg) -– China (CNGDPYOY) led developing markets in hitting back at the U.S. as India and South Africa kept up pressure on the Federal Reserve to consider the spillover effects of tapering its bond-buying program.

A day after Treasury Secretary Jacob J. Lew questioned the pace of China’s economic opening, Chinese Finance Minister Lou Jiwei said yesterday the U.S. recovery had been buoyed by monetary policy rather than structural changes. Indian central bank Governor Raghuram Rajan said countries should ensure tightening doesn’t upset the global economy and is done in a measured way.

As Group of 20 finance ministers and central bank governors began their two-day meeting in Sydney yesterday trying to find common ground to support economic growth, officials are less unified on monetary policy. While the U.S. and fellow industrial countries have put the onus on their emerging counterparts to get their houses in order to withstand volatility, developing-market officials want policy calibration.

“The tension is likely to continue,” said Tomo Kinoshita, chief economist at Nomura Holdings Inc. in Tokyo. “China is on the side of the emerging economies rather than on the side of the advanced economies.”

Chinese Finance Minister Lou Jiwei said the U.S. recovery had been "helped by monetary... Read More

Nations including South Africa, Brazil and India have seen their currencies rattled as the Fed begins to dial-back unprecedented stimulus measures. The MSCI Emerging Markets Index has lost 4.3 percent so far this year, its worst annual start since 2010.

Lew Vs Lou Lew, speaking in Sydney on Feb. 21, said while China wants “to move in the right direction” on opening its economy, “I have yet to see the signs that they are moving with the speed that we would want.”

Turning the tables yesterday, China’s Lou said while developed countries now seem very positive about their growth prospects, “that may not be totally true.”

“Take the U.S. for example: Its recovery is being helped by monetary policy and not much by structural adjustment,” he told Bloomberg News. “They have always been saying that China should boost its consumption ratio and the U.S. should boost its investment ratio, but that structural change is not happening in the United States.”

The Fed has kept rates low to spur the economy as a budget deficit restricted President Barack Obama’s administration’s ability to stimulate demand. The unprecedented monetary stimulus steered investors toward emerging markets in search of yield, a process that is reversing along with the Fed’s taper.

U.S. Treasury Secretary Jacob J. Lew, right, and French Finance Minister Pierre... Read More

G-20 Backing The G-20 is backing the normalization of monetary policy in advanced economies in line with stronger growth, according to a draft communique seen by Bloomberg News. The final statement is scheduled to be released today.

“It will take a fair amount of turmoil to move any industrial country’s monetary policy away from looking at its own situation first,” Rajan said in an interview with the Australian Financial Review. “That said, I think the international community has some responsibility -- not just the multi-lateral organizations -- but everybody, to ensure we all come out of this together rather than piecemeal.”

G-20 delegates have held extensive discussions on the impact of U.S. tapering on emerging markets and the direction of the global economy, Australian Treasurer Joe Hockey, who is hosting the meeting, told reporters in Sydney today.

Job Creation “I don’t think there’s a person in the room that doesn’t believe that if we’re going to create more jobs, we’re going to have to undertake structural reform in our economy,” he said.

South Africa wants agreement within the G-20 on the coordination of economic policies as it pushes for stronger acknowledgment of the impact of the Fed’s moves on smaller nations, Deputy Finance Minister Nhlanhla Nene said in an interview yesterday.

The Fed should seek a consensus among global counterparts on “what is the optimum level of withdrawal that the world economy can manage,” India’s Economic Affairs Secretary Arvind Mayaram said in Sydney Feb. 21.

Growth Reversal Strengthening in developed economies and a slowdown in growth in China, India, Brazil and elsewhere reverses the trend that had shaped global growth since 2008. Carlos Cozendey, Brazil’s deputy finance minister, said yesterday in Sydney that the Fed had helped reduce emerging markets’ concern over tapering, saying it would be mindful of spillovers.

A number of emerging markets have not undertaken reforms that are needed in their economies, U.K. Chancellor of the Exchequer George Osborne said in an interview in Sydney today.

“There’s no doubt that there are risks to the global economy and problems in emerging markets are some of the most evident risks,” Osborne said. “But it’s important to note that it’s not all emerging markets” and it “somewhat exposes the charge you hear that this is all due to U.S. monetary policy and western monetary policy,” he said.

Emerging markets may not forget easily should their concerns go unheeded. After learning from the Asian financial crisis of the late 1990s to accumulate reserves, allow flexible exchange rates and not have too much foreign-currency debt, this episode is teaching them another lesson, said Eswar Prasad, a former International Monetary Fund economist who now teaches economics at Cornell University in Ithaca, New York.

“The next time if capital does start flowing in, every one of these economies is going to use the opportunity to accumulate more reserves” and prevent currency appreciation, Prasad said. “We will be seeing some complaints coming from the advanced economies when this starts happening.”