framing : the potential and prospects for renewable...

TRANSCRIPT

Working on a Proposition

Framing :

The potential and prospects

for renewable energy in South Africa

Richard Worthington - Climate & Energy Programme Manager

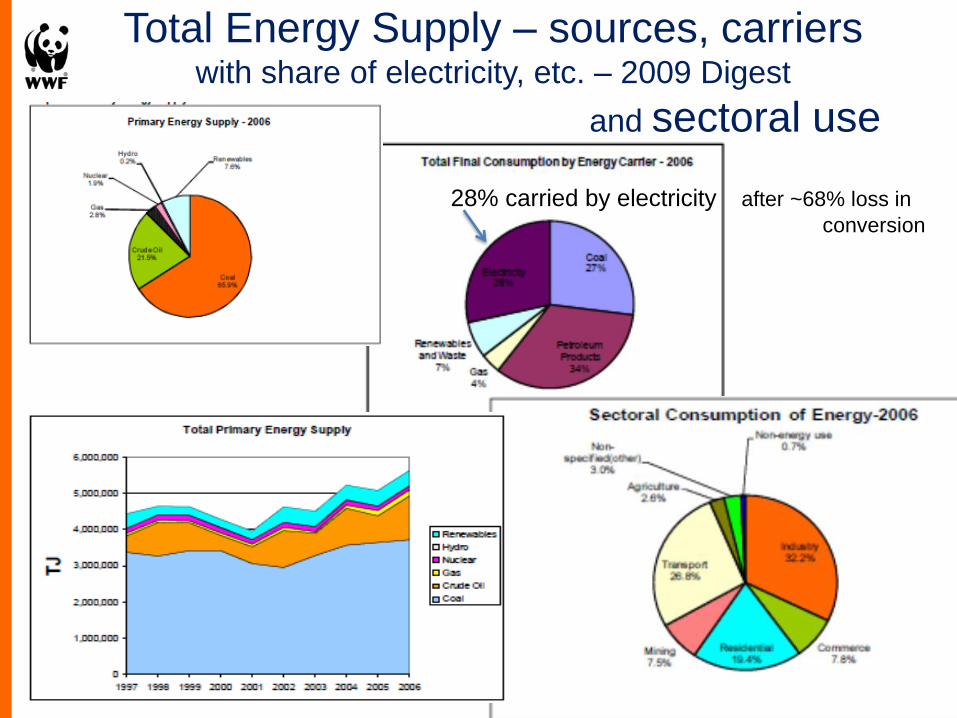

Total Energy Supply – sources, carriers with share of electricity, etc. – 2009 Digest

and sectoral use

28% carried by electricity after ~68% loss in

conversion

Electricity Consumption 2006

[ g r a p h I c ]

Choosing the energy

system we want What do we want? :

Access Affordable

Appropriate – clean and localised

Efficient (incl. economically efficient over time,

with policy continuity and pricing predictability

& requiring resource efficiency)

Reliable

Sufficient, incl. nationally, at scale,

Sustainable

to consider a renewable energy proposition

for South Africa, off grid and on, for optimal

social benefits and long term affordability .

with finance at scale

to deliver employment at scale

the scale appropriate for optimal localisation

Overview of what is being tabled

context

„the ask‟

illustrative build plans

( and impacts – some pending )

What is a proposition? 4 SA

Who will pay and how?

What is possible?

What you consider realistic depends on

your mind-set – the parameters and

framing of your questions. .

When is a just transition possible?

And for how much longer may it be within our grasp?

Context - 2008 incl. mandate from LTMS

Long Term Mitigation Scenarios

July 2008: Cabinet response to the climate challenge :

“…structurally transform the economy … to a climate-friendly path as part of a pro-growth, pro-development and pro-jobs strategy.”

.

November 2008 - WWF-SA:

Cheaper Electricity with Renewable Energy

- Costing a 2020 target for 15% renewable electricity in South Africa – Energy Research Centre (UCT) A. Marquand

SNAPP Sustainable National Accessible

Power Planning Tool

Demystifying the modelling of grid-based electricity supply

in South Africa Building on the 2008 research study showing how electricity could be cheaper

with 15% of supply sourced from renewable energy by 2020, WWF presented an

analysis of a high renewable energy scenario, compared to a fossil- and nuclear-

intensive scenario, using the SNAPP Tool.

Figure 4 – Percentage change from reference in average

cost of electricity for Cases 1A to 3A and nuclear efficiency

2010

Denial or scepticism

Resurrecting issues already rigorously addressed (e.g. IPCC) = denial

Assertion that renewable energy cannot / will not meet SA needs = denial

Two factually incorrect statements indicative of the

denial in the coal / electricity supply industry:

• “SA really has only 2 choices, coal and nuclear”

• “Coal is our most abundant /widely available energy

resource” -

If the total coal reserve of 1 298 000 PJ is used up in 200 years, as often

suggested, and this is compared to the total solar reserve potential over

200 years of 1 700 000 000 PJ, our coal reserves are 0.07% of our

solar potential over 200 years. (Peter Lukey, DEA) – 0.7% over 20 years

„Base load plant‟ is a misleading conceit – part of denialist narrative;

…base load demand is a system management challenge

What is possible? Are past trends a good measure of what is possible?

Climate Solutions 2 (2009) “The key constraint to meeting emissions levels is the speed

at which the economy can make the transformation to low-carbon resources, industries and practices. Today, only three out of 20 industries are moving sufficiently fast enough.”

“…the re-industrialisation process to commence immediately with growth rates of between 24% and 29% every year...” for key technologies

“A comprehensive plan for low-carbon industrial development is an integral part of the solution. Without this, economically disruptive “command-and-control” style government intervention will be necessary to focus industrial production on the climate change challenge.”

Optimising the generation and use of electricity has become a central and pressing

challenge for achieving sustainable access to energy services for all, particularly if we are to

avoid severely compromising the prospects of a global ecosystem conducive to human well-

being. Efficiency is key in all aspects, from decentralised services in remote areas

maximising local resource use, to the development of global networks of generation,

transport, storage and demand side management to enable the supply of energy-intensive

industries through the most rational resource use. Compelling communication of the vast potential

of integrated systems management and electronic technology deployment is imperative to inspire the

evolution of social organisation, economics and business dynamics towards optimal resource utilisation. .

Popular perception of what is possible is constrained by what is familiar and

established. Decision makers generally rely on advice from an establishment with vested interests in

avoiding transformative or disruptive change, such that the science of what is possible is marginalised

and optimal solutions are often deemed „unrealistic‟ and rendered „uneconomic‟. Propositions such as a

Vision of 100% Renewable Energy, as advanced in The Energy Report published by WWF in 2011, are

met with a mountain of doubt and inertia. Sometimes such a proposition provokes animosity, but more

often a kindly but sad shaking of the head that dismisses it as improbable. .

Future scenarios of optimal efficiency and more egalitarian use of our natural resources must certainly give rise to scepticism, considered from within our current situation and economic

conventions. Overcoming resistance or uncritical doubt requires a far broader understanding of best

available technologies and what innovation has to offer, both in social organisation as well as technology

deployment. Scepticism, applied to current arrangements as well as future prospects, is what will help us

understand the extensive challenges and constraints that must be overcome if we are to achieve

transformational change, rather than succumb to atrophy and entropy.

Coal costs more than carbon

Act now to protect South Africa‟s scarce

water resources from more coal pollution

NBI Roundtable COP17 19 March 2013 - 14

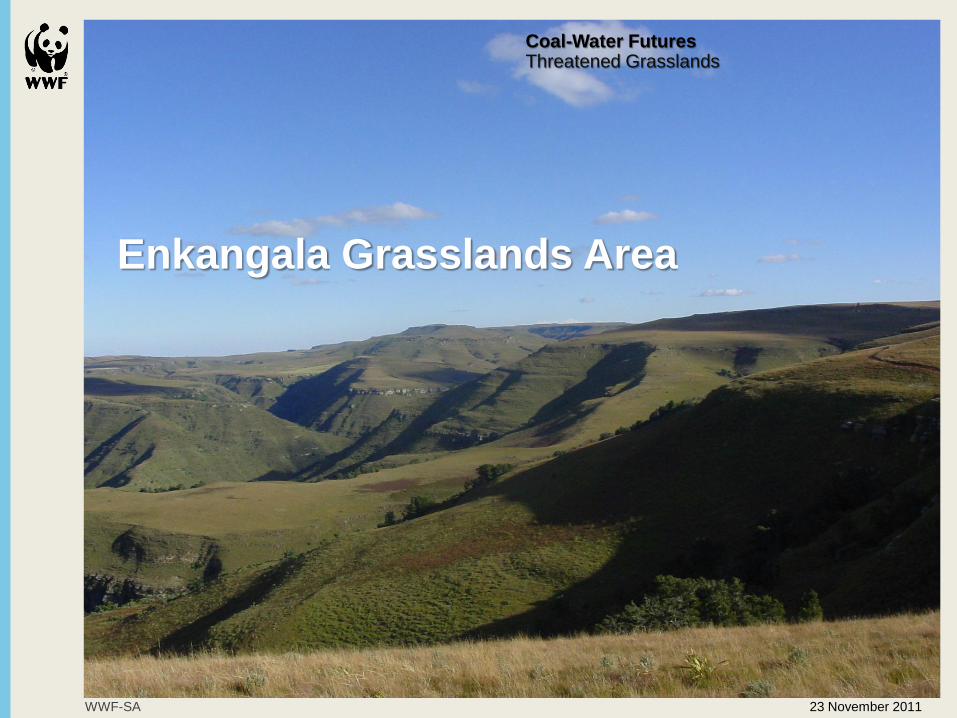

Coal-Water Futures Threatened Grasslands

WWF-SA 23 November 2011

Enkangala Grasslands Area

We cannot afford to lose

more catchments to coal

mining

Abandoned and

ownerless mines in

South Africa

5906

From abandonment of coal mines in

the Olifants until AMD began to

discharge into the Blesbokspruit

44 years

Threatened by

deteriorating water

quality in the Loskop

Irrigation area

Agricultural jobs

Estimated costs to the tax

payer to clean up current list

of abandoned mines

+R30 bill

Coal costs more than

carbon

Presentation to Company Name 17 August 2010 - 16

Photo: © Michel Roggo / WWF-Canon

Rather than being an add-on or afterthought,

the Department sees the need for water to

be mainstreamed and placed at the nucleus

of all planning decisions…”

Water for Growth and Development

Framework, DWAF 2009

What is „the ask‟ ?

Not in GW, or GWh,

but in social benefits .

What is a job-creating energy plan?

& is it also a „climate-safe‟ energy plan? .

What scale of planned deployment is ideal for localisation of

manufacturing?

What should be primary determinant of RE planning and

aggregate deployment, the pace and scale of production

and over-all development ambition ?

Jobs per $1 million invested Industry Direct Indirect Induced TOTAL

Solar 5.4 4.4 3.92 13.72

Biomass 7.4 5.0 4.96 17.36

Smart Grid 4.3 4.6 3.56 12.46

Coal 1.9 3.0 1.96 6.86

Oil and gas 0.8 2.9 1.48 5.18

Nuclear 1.2 1.8 1.2 4.2

Source: Heidi Garrett-Peltier and Robert Pollin,

University of Massachusetts Political Economy and Research Institute.

Note: Multipliers derived using IMPLAN 2.0 with 2007 data. Infrastructure multipliers and assumptions are presented in

"How Infrastructure Investments Support the U.S. Economy: Employment, Productivity and Growth," Political Economy

Research Institute, January 2009,

http://www.peri.umass.edu/236/hash/efc9f7456a/publication/333/

In SA Context : JOBS

Looks like the nuclear industry has managed to

become more labour-intensive, even as its share

of global supply declines

Renewable Investment Growth REN 21,

IEA 2010

Key Findings 2012

The Energy Report

Global wind power growth

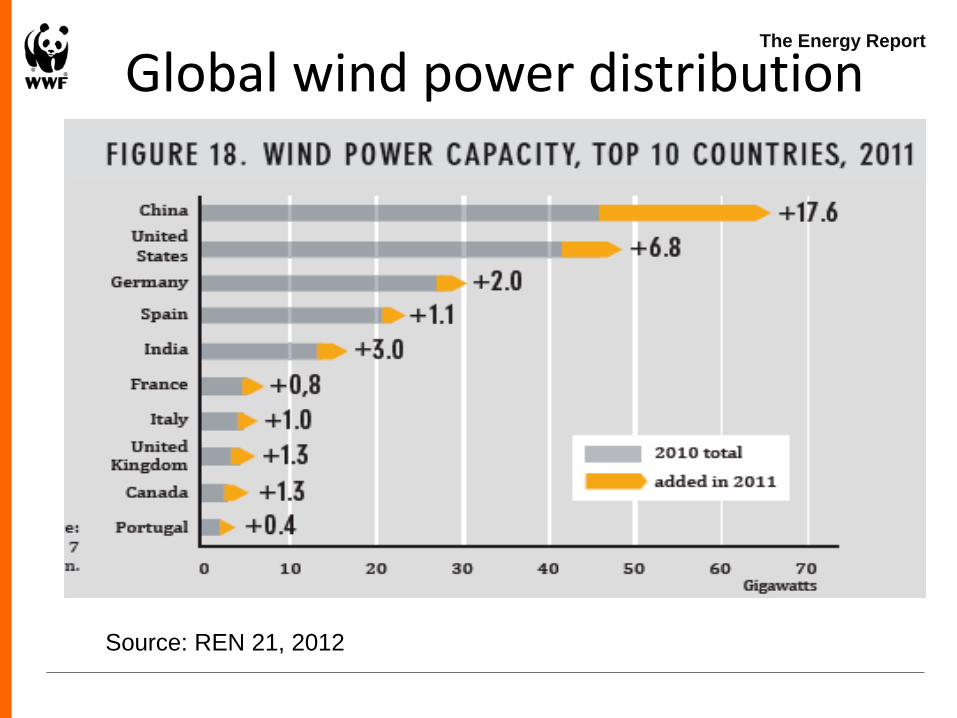

Source: REN 21, 2012

The Energy Report

Global wind power distribution

Source: REN 21, 2012

Wind power Growth in 2012 II

The Energy Report

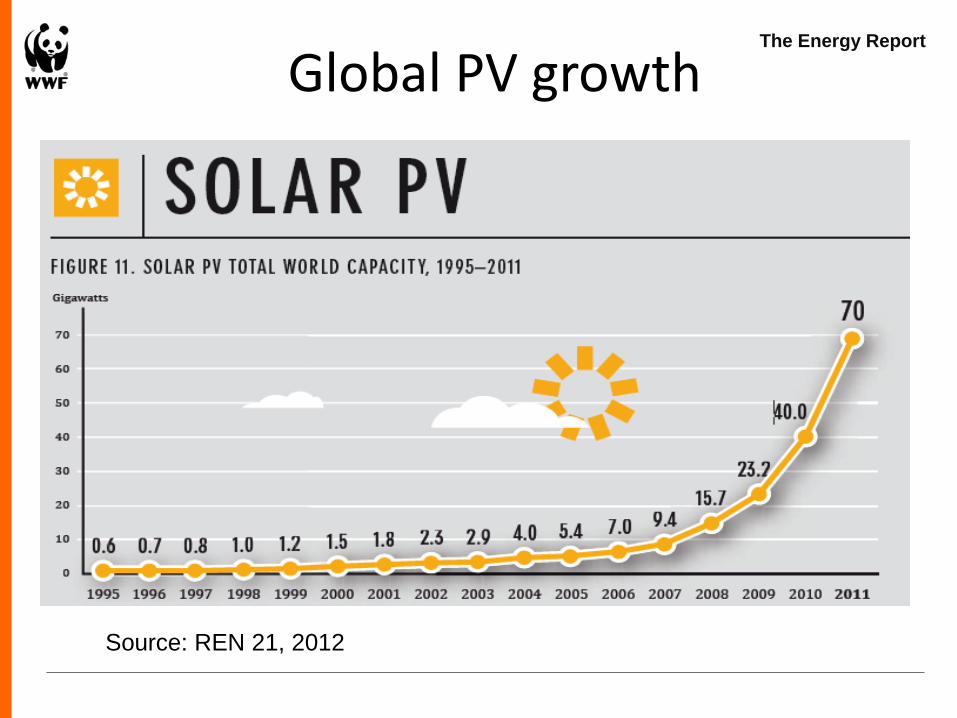

Global PV growth

Source: REN 21, 2012

The Energy Report

Global CSP growth

Source: REN 21, 2012

Stephan Singer (WWF EPO):

• there is hope – renewable implementation and investments grow strongly

• However, not strong enough to curb growth in fossil fuels

• 2011 investments in oil and gas infrastructure alone were about 3 times those of investments in RES

• But - jobs in RES worldwide are almost 10 times higher than those in the six largest fossil fuel companies (Exxon, BP, Chevron, Shell, Conoco, Gazprom) together

Jobs in RES 2011 (+20% in one year)

Source: REN 21, 2012

Carbon budgeting

The term carbon budget (CB) may be understood as an hypothetical allocation of a specified quantity of emissions of greenhouse gases (as listed in the UNFCCC) over a set period of time, to an identified sector, sub-sector, activity or entity.

Carbon budgeting should seek to discover the optimal allocation of emissions allowances. It should take account of the likely consequences of over-all distribution of the total resource, as well as of exceeding the proposed allocations, but it does not require setting an absolute limit on this total; indeed it could be undertaken purely in terms of proportional or percentage allocation of whole of unspecified size. It could be approached starting with:

Hypothetical Allocation of National Emissions (HANE)

Comparing IRP 2010 (policy-adjusted scenario)

with a high renewable energy scenario cost increase ~10% with emissions reduction ~27%

Ref Case: IRP 2010 45% RE; Slow Kusile, as replacement for early coal retirement; no nuclear

0

50

100

150

200

250

300

350

0

0.05

0.1

0.15

0.2

0.25

0.3

Average cost (R/kWh) - units: R / kWh

GHG emissions - units: Mt CO2-eq

0

50

100

150

200

250

300

350

0

0.05

0.1

0.15

0.2

0.25

0.3

Average cost (R/kWh) - units: R /kWh

PRESENTATION TO SAFCEI ENERGY WORKSHOP OCTOBER 2012

Comparing IRP 2010 with 37% RE cost increase ~3% with emissions reduction ~15%

Ref Case: IRP 2010 37% re; 3 units Kusile; no nuke

0

50

100

150

200

250

300

350

0

0.05

0.1

0.15

0.2

0.25

0.3

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Average cost (R/kWh) - units: R / kWh

GHG emissions - units: Mt CO2-eq

0

50

100

150

200

250

300

350

0

0.05

0.1

0.15

0.2

0.25

0.3

2010 2012 2014 2016 2018 2020 2022 2024 2026 2028 2030

Average cost (R/kWh) - units: R / kWh

GHG emissions - units: Mt CO2-eq

PRESENTATION TO SAFCEI ENERGY WORKSHOP OCTOBER 2012

IRP2010 vs. 37% RE with half Kusile Reference annual investment requirement

Scenario annual investment requirement

0

10000

20000

30000

40000

50000

60000

70000

80000

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029

R m

illio

n

Annual investment requirement

Existing coal Large Existing coal Small OCGT liquid fuels

PWR nuclear Hydro Landfill gas

Biomass Supercritical coal Existing imported hydro

Wind 29% availability Solar CSP Solar PV

OCGT nat gas CCGT Fluidised Bed Combustion Coal

Coal imported Hydro imported new CCGT gas imported

IGCC Pumped storage

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

100000

2005 2007 2009 2011 2013 2015 2017 2019 2021 2023 2025 2027 2029R

mill

ion

Annual investment requirement

Existing coal Large Existing coal Small

OCGT liquid fuels PWR nuclear

Hydro Landfill gas

Biomass Supercritical coal

Existing imported hydro Wind 29% availability

Solar CSP Solar PV

OCGT nat gas CCGT

Fluidised Bed Combustion Coal Coal imported

Hydro imported new CCGT gas imported

IGCC Pumped storage

PRESENTATION TO SAFCEI ENERGY WORKSHOP OCTOBER 2012

Reference & Scenario electricity system costs and average electricity cost

Ref Case – IRP2010 37% RE; half Kusile; Ext’d DSM

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

2005 2008 2011 2014 2017 2020 2023 2026 2029R

and

s /

kWh

R m

illio

n

Existing coal Large Existing coal Small

OCGT liquid fuels PWR nuclear

Hydro Landfill gas

Biomass Supercritical coal

Existing imported hydro Wind 29% availability

Solar CSP Solar PV

OCGT nat gas CCGT

Fluidised Bed Combustion Coal Coal imported

Hydro imported new CCGT gas imported

IGCC Pumped storage

carbon tax Average electricity cost

Average an elec cost with carbon tax

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

2005 2008 2011 2014 2017 2020 2023 2026 2029

R m

illio

n

carbon tax Pumped storage

IGCC CCGT gas imported

Hydro imported new Coal imported

Fluidised Bed Combustion Coal CCGT

OCGT nat gas Solar PV

Solar CSP Wind 29% availability

Existing imported hydro Supercritical coal

Biomass Landfill gas

Hydro PWR nuclear

OCGT liquid fuels Existing coal Small

Existing coal Large Average annual electricity cost (R/kWh)

Average an elec cost with carbon tax

PRESENTATION TO SAFCEI ENERGY WORKSHOP OCTOBER 2012

The Energy

Report

Pathway to a fully

sustainable

global energy

system by 2050

3 February 2011

The Energy Report

The Energy Report 100% Renewable Energy by 2050

A world powered by 100%

renewable, sustainable

energy by mid-century

In all of our hands - policy-

makers, investors, corporate

leaders, communities and

individuals.

Stop fossil fuel pollution;

save money; address

climate change; improve

health; no nuclear risks;

new jobs; innovation;

protect nature

Extensive electrification of

transport; enhanced energy

conservation; smart grids;

sustainable energy for all

Conserving energy & reducing demand; electrification;

equity; investment; land/water/sea-use implications;

governance; lifestyle choices - behaviour changes &

public attitudes; innovation and R&D

A VISION

A SCENARIO

SOLUTIONS

CHALLENGES

BENEFITS

3 February 2011 - 72

Access Some of the greatest social benefits of renewable energy

technology use are found beyond grid-based electricity supply, in

decentralised and community-based development

Electricity – on grid

This account of the proposition does not detail the knock-on benefits for local

development and ensuring sustainable access to locally affordable energy

services that robust renewable energy industries can deliver, though such co-

benefits are of far greater valuable for addressing poverty and inequality than

the grid-supply proposition and are being taken up in other work – including the WWF South Africa Energy Access Initiative.

Localisation is important not just at national level, but at local level also the

benefits through local resource use, building value from the bottom up…

community-based project development will benefit from economies of scale

while arriving at optimal resource efficiency…

…this is elaborated in Smart Energy Planning – to follow

The Scenario – Key Elements The Ecofys Scenario

SOURCE: Ecofys Energy Scenario, 2010

3 February 2011 - 31

The Energy Report

Electrification is Key The Ecofys Scenario

0

100

200

300

400

500

2000 2010 2020 2030 2040 2050

EJ/a

0

100

200

300

400

500

2000 2010 2020 2030 2040 2050

EJ/

a

0

100

200

300

400

500

2000 2010 2020 2030 2040 2050

EJ/

a

0

100

200

300

400

500

2000 2010 2020 2030

EJ/

a

Other

Electricity

All values in final energy; *approximation

The Energy

Report

Shell

Blueprints*

Advanced

[R]evolution „10

WEO „09

Reference

SOURCE: Ecofys Energy Scenario, 2010

3 February 2011 - 55

The Energy Report

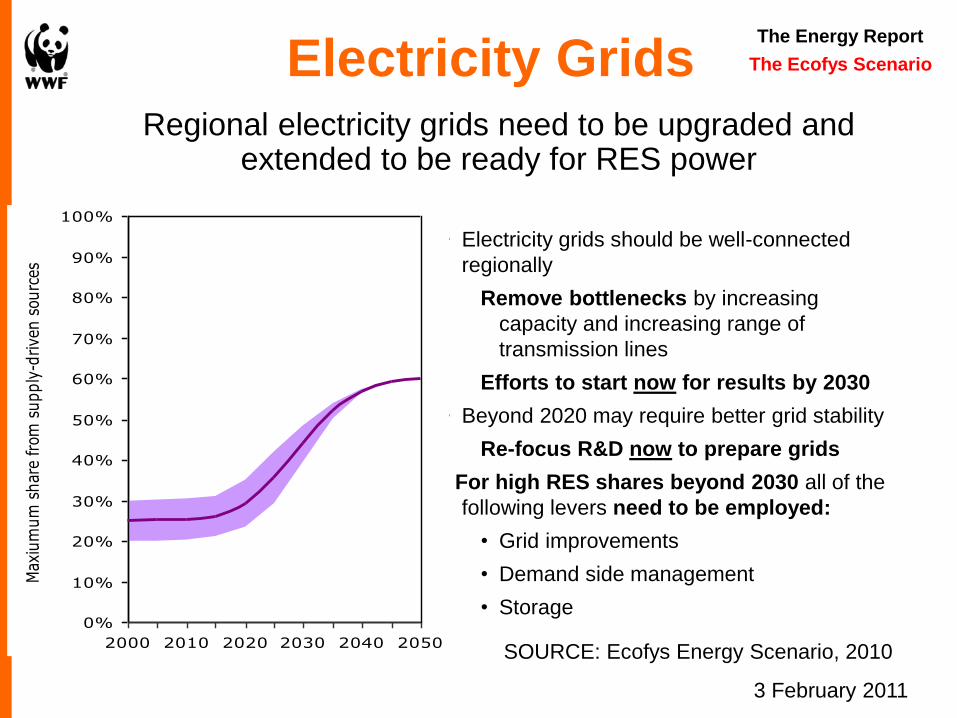

Electricity Grids Regional electricity grids need to be upgraded and

extended to be ready for RES power

• Electricity grids should be well-connected

regionally

Remove bottlenecks by increasing

capacity and increasing range of

transmission lines

Efforts to start now for results by 2030

• Beyond 2020 may require better grid stability

Re-focus R&D now to prepare grids

For high RES shares beyond 2030 all of the

following levers need to be employed:

• Grid improvements

• Demand side management

• Storage

Limit placed on

supply-driven

electricity: PV,

Wave and Wind

The Ecofys Scenario

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2010 2020 2030 2040 2050

Max

ium

um

shar

e fr

om s

upply

-drive

n s

ourc

es

SOURCE: Ecofys Energy Scenario, 2010

3 February 2011

The Energy Report

Total Investments and Savings Total global annual cost results for Energy Scenario

The Ecofys Scenario

SOURCE: Ecofys Energy Scenario, 2010

The Energy Report

SNAPP 3 (beta 5) new projections &

illustrative new build plans potential planning scenarios

Demand 2 Projections:

Govt plans: i.e. IRP2010 - System Operator‟s „Medium Outlook‟ + DSM – extrapolated to 2040

CSIR Moderate with Moderate DSM /„Tight version of Smart Track‟: EGI projection

Supply Reference Case (IRP2010 extrapolated to 2040) plus 3 approaches:

Strong Change – grow RE as rapidly as reasonable with no „new‟ coal, Kusile gradual start-up and

a little early coal retirement ( CHECK – roughly 2 plants close 2 years early); no new nuclear;

RE and Gas – grow RE rapidly early and bring in gas at scale from about 2030, with no „new‟ coal,

Kusile gradual start-up and a little early coal retirement; no new nuclear;

Gentle / slow RE, with new nuclear build [at „current‟ cost of $6 000/kW, start-up 2025],

Kusile on schedule; little more coal and no early retirement

Over-supply / over-estimated demand? Lack of EE & DSM vs stronger GDP growth

and/or

EE & DSM with electrification (growing electricity share of total energy supply) .

In other words strong efficiency and demand side management efforts to moderate demand are off-set

by changing energy carrier e.g. electrification of transport, hospital boilers and/or strong GDP growth…

Two demand projections: ‘IRP Extended’ and CSIR Mod+DSM

Diff of Moderate and Extended DSM

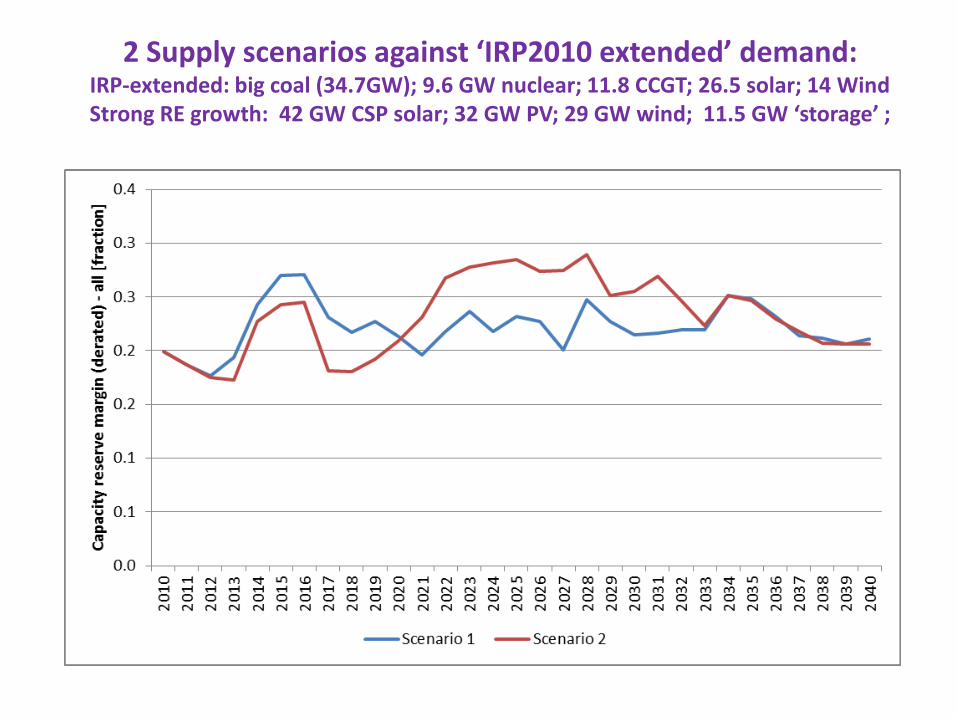

2 Supply scenarios against ‘IRP2010 extended’ demand: IRP-extended: big coal (34.7GW); 9.6 GW nuclear; 11.8 CCGT; 26.5 solar; 14 Wind Strong RE growth: 42 GW CSP solar; 32 GW PV; 29 GW wind; 11.5 GW ‘storage’ ;

Reference Case: ‘Govt plans’

Strong RE Strong RE Installed Capacity

2 Supply scenarios against ‘IRP2010 extended’ demand: IRP-extended: big coal (34.7GW); 9.6 GW nuclear; 11.8 CCGT; 26.5 solar; 14 Wind Strong RE growth: 42 GW CSP solar; 32 GW PV; 29 GW wind; 11.5 GW ‘storage’ ;

Reference Case: ‘Govt plans’

Strong RE Capital Cost

2 Supply scenarios against ‘IRP2010 extended’ demand: Share of RE & Share of coal

Coal share

RE share of supply

2 Supply scenarios against ‘IRP2010 extended’ demand: IRP-extended: big coal (34.7GW); 9.6 GW nuclear; 11.8 CCGT; 26.5 solar; 14 Wind Strong RE growth: 42 GW CSP solar; 32 GW PV; 29 GW wind; 11.5 GW ‘storage’ ;

2 Supply scenarios against ‘IRP2010 extended’ demand: IRP-extended: big coal (34.7GW); 9.6 GW nuclear; 11.8 CCGT; 26.5 solar; 14 Wind Strong RE growth: 42 GW CSP solar; 32 GW PV; 29 GW wind; 11.5 GW ‘storage’ ;

Greenhouse Gas Emissions

2 Supply scenarios against ‘IRP2010 extended’ demand: IRP-extended: big coal (34.7GW); 9.6 GW nuclear; 11.8 CCGT; 26.5 solar; 14 Wind Strong RE growth: 42 GW CSP solar; 32 GW PV; 29 GW wind; 11.5 GW ‘storage’ ;

Average cost per kWh

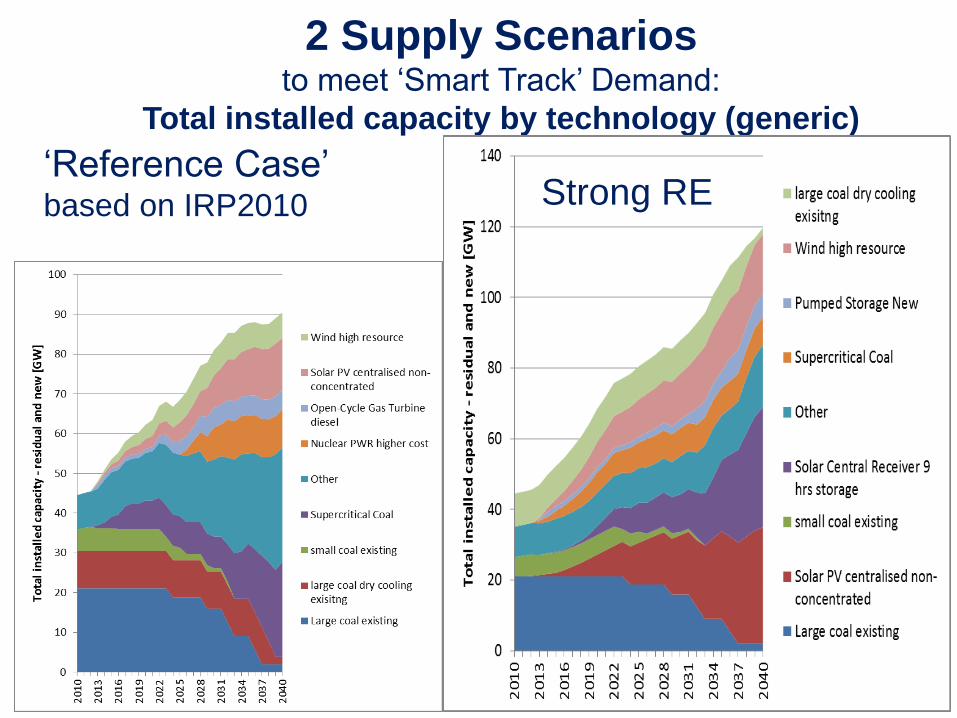

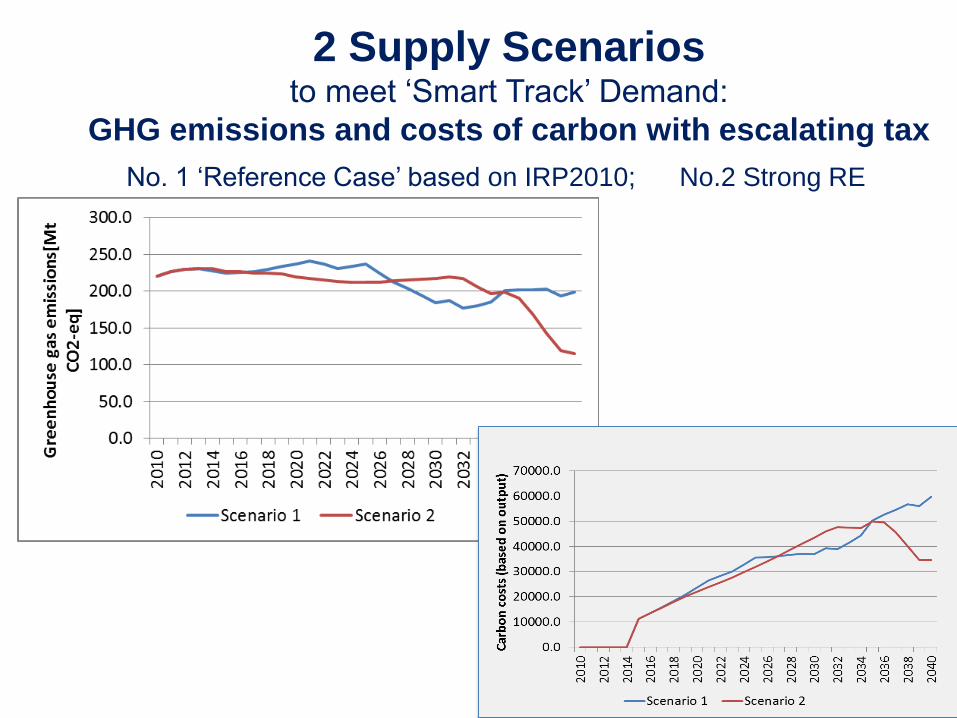

2 Supply Scenarios to meet „Smart Track‟ Demand:

Total installed capacity by technology (generic)

„Reference Case‟ based on IRP2010 Strong RE

2 Supply Scenarios to meet „Smart Track‟ Demand:

Total cost of supply (nuclear at $6000/W): – R50 – 350 billion

„Reference Case‟ based on IRP2010

Strong RE

2 Supply Scenarios to meet „Smart Track‟ Demand:

Share of renewable energy and coal

illustrative

2 Supply Scenarios to meet „Smart Track‟ Demand:

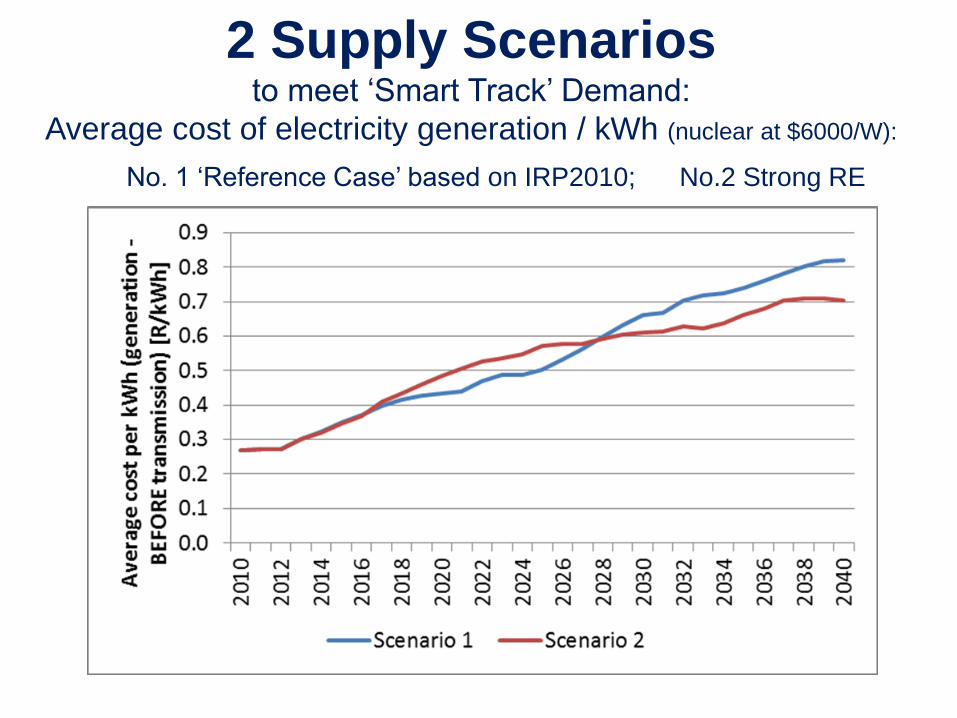

Average cost of electricity generation / kWh (nuclear at $6000/W):

No. 1 „Reference Case‟ based on IRP2010; No.2 Strong RE

2 Supply Scenarios to meet „Smart Track‟ Demand:

GHG emissions and costs of carbon with escalating tax

No. 1 „Reference Case‟ based on IRP2010; No.2 Strong RE

Presentation title can go here

Secondary information

XX-XX Month, Year

Additional information can run

Underneath if neccessary

Topic can go here

Some ideas…

© E

dw

ard

Pa

rke

r / W

WF

-Can

on

Common thread in draft proposition for RE

and Smart Electricity Planning is an orientation to: .

Planning for success

• Success in energy conservation, efficient use and system

and demand side management;

• Success in developing local manufacturing for RETs and

supply-side system management, as well as storage

(batteries and fuel cells; micro-power);

• Success in developing a smart grid and use interfacing;

• Success in achieving universal access to modern energy,

incl. transition from unsustainable and harmful fuel use

(~8% „traditional‟ biomass) to efficient and healthy utilisation

of local energy resources

Programmatic approach

REBID approach not adequate or sufficient – not an application

of feed-in tariffs; precludes most economies of scale

for scaling up with localisation .

Is there space for new players in key materials production, e.g.

glass and reflective materials…

( We have a state-owned mining company )

Would we benefit from a state-owned RE company?

Will Sasol become a big player in CSP? How SA is Sasol?

Are national borders appropriate parameters or barriers for

assessing success in renewable energy development?

Can SA electricity supply industry be saved from Eskom?

– access to the wires be delivered from Eskom control?

Is regulator too constrained (captured) to act in public interest?

Finance

Patient capital

Conflating competitiveness with short term gain

/ return on capital

Just as efficiency conflated with rate of return

R500 billion dormant in private sector?

Saliem Fakir

Head – Living Planet Unit

Manisha Gulati

Energy Economist

Carbon Tax in South Africa

May 18, 2012

SCRAP the CAP On renewable energy

imposed by IRP 2010

Seize Your Power

Facts

that have yet to permeate public consciousness, or relevant boardrooms

• There is more than enough renewable energy (RE) for all human needs • Inefficient resource use is destroying our life-support systems • Decreasing energy return on energy invested in fossil fuels • Can’t afford to burn currently available fossil hydro-carbon

reserves (the portion of known resources considered economically viable under recent market conditions)

Fossil hydro-carbons are not cheap, but cost-deferring

Energy from burning fossils fuels should not be our benchmark

What is possible?

Close to 100% RE by about mid-century

Financing vehicle with government / climate bonds,

pension fund regulatory reform and really

Independent System Operator .

Decade Down Bonuses and share options? .

International finance or patient private capital?

Seize Your Power

Thank you www.panda.org

© 2010, WWF. All photographs used in this presentation are copyright protected and courtesy of the WWF-Canon Global Photo Network and the respective photographers.

WWF Mission ©

Mu

rat

Se

lam

/ W

WF

Nep

al

19 March 2013 - 66

To stop the degradation of the planets natural environment and to build a future in which humans live in harmony with nature.

Source: OPEC Secretariate 2011, BP 2011, IEA 2011, IPCC 2007

The global GHG budget (400 ppm) requires retiring about 60% of all known conventional fossil fuel recoverable reserves until 2050 (if CCS is excluded – with CCS, perhaps use 50%? 60%?)

Gt CO2e

GAP

2010 - 2050

?

MARKETS NEED ALIGNING WITH

CLIMATE POLICY OBJECTIVES

IEA World

Energy

Outlook

Scenarios

Markets not

following

required

pathway 1,000

2,000

3,000

4,000

5,000

6,000

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

Mtoe 450ppm Current po licy New Policies

IEA RECOGNISES THE CARBON

BUBBLE:

LOCK-IN OR STRANDED ASSETS?

745 GtCO2

Proven coal, oil & gas reserves

owned by listed companies

2860 GtCO2

Total proven coal, oil and gas reserves

“without a significant deployment of CCS, more than TWO THIRDS

of current proven fossil-fuel reserves cannot be commercialised in a 2 °C world before 2050.”

884 GtCO2 2012 -50 budget for (50% chance) of 2 degrees

IEA (Nov 2012)

World Energy

Outlook

Some questions…

• What is the best deployment of

the limited emissions space

left to achieve South Africa‟s

development needs?

• What monitoring will help us to

ensure that we are on a

suitable emissions trajectory?

• What are the areas of

opportunity for both emissions

reduction outcomes and

development outcomes?

• What new industrial activities

or manufacturing should we

anticipate in South Africa? • What sectors or new activities

or processes are likely, globally

or regionally, to require

substantial carbon allocation in

future?

“Industry,

manufacturing etc.” Breakaway

NCCRP Implementation Conference 21 November 2012

SA RESERVES EXCEED CARBON BUDGET

16.4 = LTMS Required

by Science budget

EROEI of electricity generation

by Jamie Bull

Technology Average EROEI Average EIRR Average lifespan Number found

Coal no CCS 5.5 17% 31 11

Coal w. CCS 1.5 8% 23 2

Solar thermal elec. 9.9 40% 25 7

Gas no CCS 3.5 11% 32 5

Gas w. CCS 2.2 13% 23 2

Nuclear 10.9 36% 29 50

PV 8.3 34% 24 46

Tidal range 115.9 97% 120 1

Tidal stream 14.9 74% 20 2

Wind 25.0 125% 21 108

Wave 12.0 60% 20 2