foster report no. 3036 february 6, 2015ceadvisors.com › ... › 2015 › 11 ›...

TRANSCRIPT

Foster Report No. 3036 February 6, 2015

FOSTER REPORT NO. 3036 February 6, 2015

i © Concentric Energy Publications, Inc.

Published by Concentric Energy Publications, Inc., a Concentric Energy Advisors, Inc. Company

Concentric Energy Publications, Inc. 293 Boston Post Road West, Suite 500, Marlborough, MA 01752 USA

Website Address: FosterReport.com

Subscriber Inquiries, Maggie Connolly, (508) 263-6222; [email protected] Editor In Chief, Edgar Boshart, (703) 629-0160; [email protected]

Reporter, Kimberly Underwood, (703) 582-8810; [email protected]

This publication is also available electronically through LEXIS/NEXIS services provided by Mead Data Central, Inc. (1-800-346-9759).

Copyright 2015 by Concentric Energy Publications, Inc. All rights reserved. Reproduction in any form whatsoever forbidden without express permission of the copyright owner.

Permission is granted for subscribers registered with the Copyright Clearance Center (CCC) to reproduce material for internal reference or personal use for the price of $10 per copy

plus 50¢ per page per copy. Send payment, with the date, issue and page numbers that are photocopied, to CCC, 222 Rosewood Drive, Danvers, Massachusetts 01923.

Copyright © 2015 by Concentric Energy Publications, Inc. All Rights Reserved. Concentric Energy Publications Trademark used under license from

Concentric Energy Advisors, Inc.

www.ceadvisors.com

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. ii

TABLE OF CONTENTS

FERC

FERC Positions Itself to Be Honest Broker As Public Outcry Takes a More Activist Course, According to Chairwoman LaFleur 1

FERC Submits Fiscal Year 2016 Budget Request of $320 Million to Congress -- 5% Increase Over 2015 Budget 3

FERC POLICY – GAS DAY DEBATE

Natural Gas Industry Uniformly Tells FERC that Data Provided by Electric Grid Operators Fail to Support Any Change to the Start of the Customary Gas Day 5

With Several Recommendations, State Regulators Offer Support and in Some Cases Caution for FERC’s Proposal Regarding Gas Pipeline Recovery of Modernization Costs; PHMSA Recommends Broad Use of Pipeline Modernization Programs 10

FERC ENFORCEMENT

FERC Majority Brings Enforcement Action Against Canadian-Managed U.S. Power Generator That Allegedly Sought to Collect ISO-New England Reimbursements for Standby Role Based on High Fuel Oil Costs When In Fact Cheaper Natural Gas Was Used and Available 15

NATURAL GAS PROJECTS

Pre-filing Review Begins at FERC for the Atlantic Bridge Project, Joined by Algonquin and Maritimes & Northeast Pipeline 18

Tennessee Gas Pipeline Submits FERC Application Seeking Authorization for Broad Run Expansion Project To Deliver Marcellus/Utica Shale Gas Produced by Antero Resources 20

Constitution Blasts Opponents of Its Certificated Constitution Pipeline and Wright Interconnection Projects; In Context of the Clean Water Act, Is a FERC Pipeline Certificate the Equivalent of a License or Permit? 22

Peoples LDCs Object to Proposal of Equitrans to Establish a Zone to Manage Services on Proposed Ohio Valley Connector 26

NATURAL GAS PIPELINE TARIFFS

No FERC Policy Requires ANR Pipeline to Give Original Natural Gas Shipper a Right to Match in Open Season Bidding for Capacity Requested by that Shipper; Commission Addresses Matching Right of Shippers Holding Longer Term Pre-Arranged Deals 27

FERC Accepts a Rate Schedule IBS (Interruptible Balancing Service) Proposed by Equitrans, Subject to Clarification Sought by Peoples’ LDCs 29

Widely Protested Tariff Changes, Including New Imbalance and Flow Management Service and Penalties, Sought by MoGas Pipeline Are Set By FERC for Technical Conference 30

OIL PIPELINE PROJECTS

FERC Determines in Favor of Enbridge Energy’s Scheme to Recover Costs of Its Four-Part Midwestern Project 24, Despite Reservations Aired by Suncor Marketing and Flint Hills Resources 32

ENERGY NEWS ALERT 35

EIA’S GAS STORAGE AND WEEKLY ANALYSIS 42

FOSTER REPORT NO. 3036 February 6, 2015

1 © Concentric Energy Publications, Inc.

FERC

FERC Positions Itself to Be Honest Broker As Public Outcry Takes a More Activist Course, According to Chairwoman LaFleur

FERC is facing new challenges, in a world of growing natural gas production, an increase in gas-fired electricity generation, multiplying environmental

regulations, cyber threats and electric grid reliability concerns, the Commission’s Chair Cheryl LaFleur told a Washington D.C. audience at the National Press Club (NPC) on January 26.

NPC’s president, John Hughes, introduced LaFleur was the first Commission Chairperson to speak at the Club. In some sense her wide-ranging talk and affable interaction with the audience was in keeping with her reputation for being accessible and approachable (see FR for the publication’s interview with her when she became a Commissioner in 2010). LaFleur will serve as Chairwoman several more months – until she switches places with Norman Bay who assumes the post on April 15. She affirmed her plan to remain at the Commission through the second term, which ends in 2019.

LaFleur described herself as an “energy lifer,” with 30 years in the business. Five years ago when she was appointed, FERC was not a household name. Now with energy issues gaining such prominence in the U.S., along with an increased level of activism and protests against the Commission itself, FERC “is in the spotlight. The Commission must maintain a proper course of action, continue to do the daily work of carrying out its regulatory duties, bound by statute,” LaFleur affirmed.

“Examining the underbelly of every energy issue is unsexy, but it is what we do best,” she explained. FERC must balance a trio of core issues when looking at energy projects: reliability, cost, and the environment. How to strike a balance amongst the “cacophony” of different voices is FERC’s charge. Making progress towards this balance requires “real conversations regarding the tradeoffs,” the Chairman continued.

“FERC is not an environmental regulator,” LaFleur stressed. It really is up to the Environmental Protection Agency (EPA) and the states to govern environmental policies. Even so, the Commission will have an active part in implementation of the EPA’s Clean Power Plan (CPP). “Make no mistake, FERC will have a role to play in the CPP’s implementation. I believe that as a nation we can achieve real environmental progress, but only if we can build the necessary infrastructure, both gas and electric, and build the necessary energy markets to make that possible.”

LaFleur suggested that FERC’s role will center on three areas: infrastructure, markets, and being an “honest broker for discussions.” Over the last several months, the Commission has seen “a steady stream of visitors presenting a wide range of views on the CPP,” she acknowledged.

The Commission scheduled several technical conferences to discuss implications of the compliance approaches to the CPP, focusing on electric reliability, wholesale electric markets and operations, and energy infrastructure. A February 19th meeting at FERC’s headquarters will be a national overview, while three additional conferences will focus on regional issues and be staff led. Those conferences are slated to be held in the: (1)Western Region – February 25 in Denver, Colorado; (2) Eastern Region – March 11 in

Source: FERC

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 2

Washington, DC; and (3) Central Region – March 31 in St. Louis, Missouri.

LaFleur expects the energy industry to increase its utilization of generating plants to reduce emissions. This will lead to the construction of new gas-fired power plants, as gas plants are currently most cost-effective. “Natural gas is enabling us to meet our climate goals,” LaFleur stressed. “But gas does have its own issues,” she added. The building of additional pipelines and compressors will be critical. The Commission also is seeing an unprecedented level of activism against the fuel’s production and pipeline siting (see FR No. 3034, pp4-6).

Referring to the recent disruptions at the Commission’s headquarters, both outside and even within the public meeting room, the Chairwoman affirmed that the perpetrators do have their place in the Commission-monitored siting process, and they should play a role, “as these are important issues.” In its siting role under the Natural Gas Act, FERC takes the input of all stakeholders “very seriously.” However, she reiterated that their choice of venue and methods are only disruptive and not consistent with the historical and actual role that the Commission plays.

Within the standard system, FERC is seeing an uptick in the number of filings and advocacy by individuals and the Commission’s Secretary is doing a great job of processing the comments, according to LaFleur. In general, protestors usually are concerned about (1) how pipelines impact the environment; (2) pipeline routes in the vicinity of their local communities; or (3) the greater/or lesser need for pipelines and/or energy production.

Regarding how pipeline construction affects the environment, FERC “must do this right,” LaFleur agreed. Pipelines must be constructed carefully, using the most environmentally-advanced techniques. For

siting, the Commission must carefully route pipes through communities, and this is “something FERC does well.” Very few pipelines come out of FERC’s siting process with the same route that was originally proposed.

As for handling “bigger picture” items, such as whether to “allow” natural gas production or fracking, LaFleur explained that this is outside of FERC’s scope. The Commission does not regulate production or fracking, as these activities remain primarily under scrutiny at the state level. Federal statues dictate that the Commission must consider and act on pipeline applications by assessing the market demand and contractual demand for long-term firm transportation capacity. Under National Environmental Policy Act (NEPA) requirements, the Commission looks closely at the environmental aspects of pipeline siting, including water, soil, and air quality impacts. But this review is “very project-specific,” the Chairman clarified.

Looking ahead, LaFleur acknowledged that “at some point soon the nation is going to have to grapple with” natural gas’ role in helping to meet climate change goals. Moving away from coal-fired generation “and closing down the old stuff” means that the nation will need new generation, the Chairwoman offered. Furthermore, the increased reliance on renewable energy makes generation highly dependent on transmission. Long transmission lines are required to benefit the grid, but the lines don’t benefit everyone, and their siting is also very controversial.

Energy efficiency measures and distributed generation technologies employed under the CPP will also need delivery systems. Having implemented “conservation” programs previously, LaFleur knows that those kinds of programs “are not free, nor are they self-executing.”

FOSTER REPORT NO. 3036 February 6, 2015

3 © Concentric Energy Publications, Inc.

Implementation of the CPP as a whole could be very complicated. States will be able to develop different plans, deciding on what energy sources they will use. However, a state’s resource mix may not automatically be compatible with existing infrastructure, creating a need to reconcile differences, which on a larger scale increases the complexity.

For example, in the Mid-Atlantic’s PJM power region of 13 states, each state could come up with substantially different portfolios, and the system operator would have to dispatch power based on those 13 different plans. EPA, based on input from FERC, would allow extra credit for states and regions to work together, but the process could represent “considerable change and compromise.”

As far as FERC getting authority to “sign off” on state plans, LaFleur believes that level of approval is “a bit strong.” States ultimately must have control, she insisted. If Congress changes FERC’s mandate, “of course the agency will respond.” Yet, she holds, “we are well served having EPA and the states regulate the environment, and having a healthy division of responsibility. FERC has its own role.”

Nonetheless, with generation mix changes, FERC still must enforce market rules and market designs that are necessary for reliability, and “this requires open dialogue,” LaFleur noted. So it follows that FERC’s role as an honest broker in the forthcoming discussion is important. At the upcoming CPP conferences, the Commission will bring together state government partners and other stakeholders to discuss compliance issues associated with the rule. “This will be just the beginning of the dialogue,” according to the FERC Chairwoman. “And we can’t be afraid to say the hard things in regard to these difficult policy issues.”

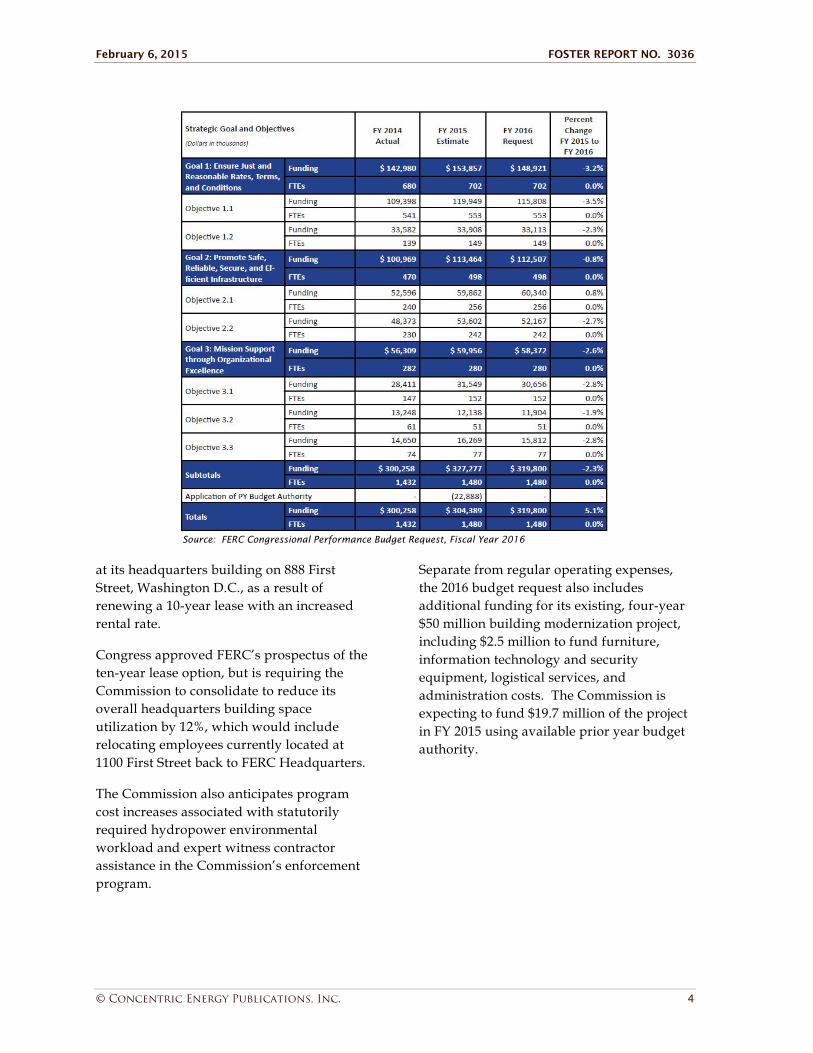

FERC Submits Fiscal Year 2016 Budget Request of $320 Million to Congress -- 5% Increase Over 2015 Budget

On Feb. 2 FERC Chairman Cheryl LaFleur submitted to Congress FERC’s Fiscal Year (FY) 2016 budget request of $320 million, an increase of about $15.4 million over last FY’s budget of $304.4 million or 5%. Since FERC recovers the full costs of its operations through annual charges and filing fees from the industries it regulates, the appropriation request funds necessary expenses in advance until its fee revenues deposited into the Treasury Department offset the appropriation, resulting in a net appropriation of zero.

To execute its mission in fiscal year (FY) 2016, the budget would fund 1,480 full-time equivalent (FTE) employees. To fund activities associated with ensuring just and reasonable rates, the Commission requested 702 FTEs (the same as last year) and $149 million for FY 2016, a funding increase of 4.5%. FERC requested $112.5 million and 498 FTEs (the same as last year) for its role of promoting safe and reliable infrastructure, a 6.1% increase over FY 2015 funding levels. To assist FERC in operating in an efficient, responsive and transparent manner -- including its headquarters’ modernization project, managing its employees, upgrading its e-library record system, and implementing a pilot cloud-based storage program -- the Commission requested 280 FTEs and $58.3 million in funding, a 4.6% increase.

FERC’s natural gas regulation activities would receive 282 FTEs, the same level as in FY 2015, along with funding of $61 million, a 2.9% decrease compared to FY 2015.

The request reflects the necessary resources to support mandatory increases in salaries and benefits associated with a 1.0% pay raise in FY 2016. In addition, the budget would fund the $7 million increase in rent (or 29%)

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 4

at its headquarters building on 888 First Street, Washington D.C., as a result of renewing a 10-year lease with an increased rental rate.

Congress approved FERC’s prospectus of the ten-year lease option, but is requiring the Commission to consolidate to reduce its overall headquarters building space utilization by 12%, which would include relocating employees currently located at 1100 First Street back to FERC Headquarters.

The Commission also anticipates program cost increases associated with statutorily required hydropower environmental workload and expert witness contractor assistance in the Commission’s enforcement program.

Separate from regular operating expenses, the 2016 budget request also includes additional funding for its existing, four-year $50 million building modernization project, including $2.5 million to fund furniture, information technology and security equipment, logistical services, and administration costs. The Commission is expecting to fund $19.7 million of the project in FY 2015 using available prior year budget authority.

Source: FERC Congressional Performance Budget Request, Fiscal Year 2016

FOSTER REPORT NO. 3036 February 6, 2015

5 © Concentric Energy Publications, Inc.

FERC POLICY – GAS DAY DEBATE

Natural Gas Industry Uniformly Tells FERC that Data Provided by Electric Grid Operators Fail to Support Any Change to the Start of the Customary Gas Day

According to the opinion of many natural gas industry companies and organizations, in filings made at FERC on or about Feb. 2, data provided to the Commission by U.S. electric grid operators do not make a case for changing the start of the Gas Day. The statistics from the six regional transmission organizations (RTOs) and independent system operators (ISOs)1 “clearly confirm” that there is not a nationwide problem during the morning electric load ramp up that is associated with the current start time, claimed the New England Local Distribution Companies (LDCs), American Public Gas Association (APGA), Natural Gas Council (NGC), and Coalition for Enhanced Electric and Gas Reliability, in separate filings. The problems, “if they exist,” occur mainly in the Northeast, in the view of some.

While some of the data submitted at the request of FERC illustrate that gas-fired power generators experienced outages related to fuel in the past, the gas organizations insisted there was no data indicating that the cause of the lack of fuel was related to the Gas Day. In addition, according to them, the data reveal that there was no measured increase in outages during the morning ramp period than at other times during the day.

In the commenters’ view, the Commission lacks the record of evidence required under

1 PJM Interconnection, LLC (PJM); Southwest Power Pool,

Inc. (SPP); ISO New England Inc.; Midcontinent Independent System Operator, Inc. (MISO); New York Independent System Operator, Inc. (NYISO); and California Independent System Operator Corp. (CAISO) all filed data as requested at FERC.

the section 5 of the Natural Gas Act (NGA) to justify changing the start of the Gas Day from 9:00 a.m. Central Clock Time (CCT) to 4:00 am CCT. The NGC’s comments, anchored by a group of ten natural gas industry-related associations2, questioned the data filings, claiming that the information failed to provide a sufficient record evidence for the Commission to move the Gas Day start. The RTO/ISO responses “confirm” that there is no nationwide issue associated with a 9:00 am CCT start time, and as such FERC should retain the 9:00 am national standard.

Given the dearth of evidence, the NGC stated: “Now that FERC’s attention is finally focused on addressing regional power market fuel assurance improvements,” the gas industry’s hope is that “both the Commission and RTOs/ISOs will recognize that changing the start of the Gas Day is not the answer to creating measured improvements in fuel assurance.” RTOs/ISOs are “actively” pursuing regional solutions already, and these “are working,” the Electric and Gas Reliability Coalition suggested.

As part of its proceedings in RM14-2, the Commission is concerned that the current start of the Gas Day occurs in the middle of the morning ramp in some regions, “creating a situation where electric load is increasing at the same time natural gas-fired generators may be running out of their daily nominations of natural gas transportation service.” FERC proposed in a Notice of Proposed Rulemaking (NOPR) to move the start of the Day earlier, in part to address instances in which those generators reduce their electric output (or de-rate) during the morning ramp period in order to balance their remaining scheduled natural gas transportation capacity for that day.

2 The following groups made the joint filing: The American

Forest & Paper Association; the American Gas Association; America’s Natural Gas Alliance; the American Public Gas Association; the Gas Processors Association; the Independent Petroleum Association of America; the Interstate Natural Gas Association of America; the Process Gas Consumers Group; and the Texas Pipeline Association.

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 6

After receiving a barrage of comments from all sides of the Gas Day debate in late November (FR Nos. 3031, pp15-25; 3031, pp13-15; and 3028, pp4-14), FERC’S Office of Energy Policy and Innovation (OEPI) sent letters to the RTOs/ISOs on Dec. 12, requesting information on generators running out of their daily nominations during the morning electric ramp -- to the extent this occurs in their regions.3

Details of the Responses. The comments on the data from the gas industry all overwhelmingly assert that the grid operators have not demonstrated a “causal link” between generator de-rate issues and the current start time of the Day. Furthermore, the Commission’s data requests had failed to seek information regarding the type of gas supply arrangements made by the generators who de-rated their capacity. Without that information, the gas parties argued that the Commission cannot fully understand the reasons for de-rates and the behavior of generators. In addition, if shippers do not contract for sufficient transportation capacity, supply or swing services to meet its electric burn obligation, a de-rate problem would exist irrespective of when the Gas Day begins. Generators in a region relying only on interruptible contracts thus “should bear the risks and should not force changes to the nationwide energy industry simply as a result of the choices.”

Gas Council. Three regions indicated no issue with their morning electric ramp associated with the current Gas Day, noted the NGC. CAISO stated that it “has not located any record of a natural gas-fired generator notifying the CAISO that the generator had to de-rate a unit during the hours of 3:00 am and 9:00 am CCT because the generator exhausted its daily nomination of natural gas

3 FERC requested the data submissions by Jan. 22 (after

extending the deadline by 10 days as desired by the RTOs/ISOs) and requested comments in response to the data filings by Feb. 2.

transportation service prior to the end of the gas day.” Natural gas-fired generators operating in the CAISO balancing authority generally do not face problems securing sufficient fuel to meet the morning electric ramp under existing electric and gas market timelines.

Similarly, MISO has not experienced any significant impacts caused by generators running out of natural gas during the morning ramp. SPP, while not making a direct assertion as to whether it believes the current start time has impacted generator de-rates in its region, does not collect data that would allow it to accurately assess the underlying causes of de-rates. Also, out of a total of 5,603 outages in SPP during the two-year period (2013-2014), only one-fourth (1,461) of the outages occurred in the morning ramp, which is no more outages during the morning timeframe than the number of outages that occurred during all other hours of the day, declared the Council.

Moreover, the other three RTOs and ISOs failed to show any direct correlation between generator de-rates and the 9:00 am start, since: (1) the data collected is too vague to accurately reflect the true cause of generator outages; (2) the reported outages during the reporting timeframes are not out of proportion with the de-rates experienced during other times of day; and (3) there is no evidence that regional reliability has been impacted by the current Gas Day.

MISO, SPP, PJM and ISO-NE each acknowledged that their current information collection systems were inadequate to provide a level of specificity required to conclude if de-rates occurred due to exhaustion of gas nominations, NGC commented. The systems do not reveal whether outages occurred due to a generator running out of nominated gas, nor do the “cause codes” submitted by PJM and NYISO reveal the actual reasons for the listed instances of outages or de-rates.

FOSTER REPORT NO. 3036 February 6, 2015

7 © Concentric Energy Publications, Inc.

The cause codes provided by the generators to PJM and NYISO are “so vague that they are useless for purposes of understanding the root cause of the specific problem experienced by the generators,” the NGC complained. A “lack of fuel” can be attributed to any number of factors, including a generator’s decision not to purchase available supplies if it found that it was not in its economic best interest to do so. Such vague terms could also reflect a generator’s inability or decision not to procure the quantity of delivered gas or the types of arrangements it may have needed to meet its dispatch obligations.

This makes it impossible to determine whether the generators contracted for firm or interruptible transportation, whether they made adequate advance arrangements with marketers or producers to secure delivered gas, or whether the regional operator gave unexpected dispatch orders – and these issues would exist irrespective to the start of the Gas Day.

NGC strongly encouraged grid operators and the Commission “to take a very hard look” to identify how these issues could persist over the long-term for a single generator.

Turning to the instances in which outages were due to a pipeline Operational Flow Order (OFO), NGC argued that that problem too could not be linked to when the Gas Day begins. When a generator de-rates during an OFO, (1) it likely over-relied on the pipeline to provide more flexibility for hourly takes than the generator contractually was entitled to take, and that the pipeline contractually was obligated to provide, or (2) it likely relied on interruptible transportation (and sometimes secondary firm transportation) that subsequently was restricted in order for the pipeline to meet its firm contractual obligations.

Without more specificity in terms of what caused an outage or de-rate for a particular generator, the information provided in these

submissions cannot be relied upon to develop an understanding of the problems experienced by gas-fired generators in their region, let alone to support a change to the start of the Gas Day, NGC concluded. “Unsupported assertions that generators would be ‘better positioned’ with an earlier Gas Day” or data that relies on vague outage codes are not sufficient record evidence to satisfy the Commission’s NGA burden necessary to change the current national 9:00 am start of the nominations process.

Believing that their “collective experience” in the region can assist in providing insight into the ISO-NE’s data responses, the New England LDCs4 similarly told FERC that the ISO’s data “does not demonstrate” that a change in the Gas Day would resolve issues regarding generator de-rates in New England. Moreover, the data responses of ISOs and RTOs in regions outside of the Northeast “make clear” that they have no information supporting a change.

Anyway, prior to moving the start of the day, FERC has a burden under the NGA to show that the existing 9:00 am start time is unjust and unreasonable. The data provided by the ISOs and RTOs “confirms that there is no factual basis upon which the Commission can conclude that the 9:00 am start time is unjust and unreasonable,” the LDCs stated.

Based on the statistics, three of the six RTOs -- CAISO, MISO, and SPP -- had no trouble with generator de-rates during the morning ramp hours, and they are spread throughout the country in the West, Midwest and parts of the South. Since the Northwest, Southwest, and Southeast do not have ISOs and RTOs, the Commission received no data regarding de-rates in those areas. It is only in the Northeast -- in ISO-NE, NYISO, and PJM -- that generators de-rated, and the statistics “simply

4 The New England LDCs have joined the Coalition for

Enhanced Electric and Gas Reliability and support the Coalition’s filed comments on the matter.

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 8

do not demonstrate” that de-rates were due to the generators “running out of gas”. Neither NYISO nor PJM reach the conclusion that moving the start of the Day to 4:00 am would reduce the number of generators de-rating during the morning ramp, the New England LDCs stated.

According to the LDCs, NYISO’s data indicates that de-rates were more likely related to limitations on natural gas customers’ ability to receive/take gas, such as OFOs that require gas customers to operate within tight tolerances, or generator-specific issues that might, or might not, be related to the availability of gas supply.

In ISO-NE, the gas utilities said, de-rates occurred on 49 days in 2013 and 2014. However, on 47 of the 49 days (96%) only one or two generators de-rated between 4:00 am and 9:00 am. “Clearly, gas-fired generators in New England are not facing a systemic de-rating problem during the morning ramp period.” In addition, de-rates reflect fairly small reductions in available energy and capacity. ISO-NE’s data show that on 23 of the 49 days on which de-rates occurred (47%), the total reduction was 337 MW or less. As New England has a substantial number of gas-fired generators with a total hourly capability of 13,600 MW, “this reduction is minimal.”

Furthermore, the LDCs suggested there is no correlation between generator de-rates and pipeline OFOs. On the 49 days in which ISO-NE experienced de-rates, pipelines had issued OFOs on only three of those days (6%).

“Thus, generators in the region were not often required to de-rate on days when pipeline capacity was most restricted and balancing would have been the most difficult,” stressed the LDCs. On days when pipelines do not issue OFOs, most shippers have flexibility with respect to gas supply arrangements, so the fact that most de-rates occurred on days without OFOs indicates that the de-rates were

not the result of generators coming up short on gas.

Lastly, the New England-based gas utilities told FERC that they too face their own morning ramps due to natural gas heating loads, yet “to the best of the New England LDCs’ knowledge” the gas utilities faced “no problems” in obtaining sufficient gas to cover the morning ramp period on the exact days that the generator de-rates occurred. LDCs often have firm gas supply arrangements, including firm transportation, storage, and commodity arrangements, in order to ensure that gas supplies will be available when needed – including during morning ramp. “If gas-fired generators lack firm gas supply arrangements, a change in the start of the Gas Day would do nothing to ensure that they can obtain gas supplies when necessary.”

Coalition. Echoing the sentiment of the other commenters, the Coalition for Enhanced Electric and Gas Reliability, which includes scores of local distribution companies (LDCs), combined electric and gas utilities, marketers, and others, also claimed that the data responses lack evidence that moving up the Gas Day start time would improve reliability or enhance electric-gas coordination, mainly because: (1) the RTO/ISO responses did not identify significant, national concerns regarding the start of the Gas Day; (2) the data does not provide sufficient support for changing the existing start; and (3) even in those regions where pipeline capacity constraints and electric-gas coordination challenges exist, efforts are already under way to proactively address the regional concerns, making a change to the start of the Gas Day unnecessary.

Even the ISO-NE, which is the only grid operator that expressed concern about the start of the nominations cycle, was unable to submit data that supported changing the start. That ISO’s data does indicate that generator reductions due to fuel limitations decreased

FOSTER REPORT NO. 3036 February 6, 2015

9 © Concentric Energy Publications, Inc.

from 2013 to 2014 by more than 20%, a sign that other solutions being pursued by ISO-NE to address the regional coordination problems are having a positive impact.

The lack of detail from generators, some of which relied on codes from the Generator Availability Data System (GADS), does not allow grid operators to specifically address whether a generator exhausted its daily nomination of gas service anyway.

Without more specific data demonstrating that the current start time is unjust and unreasonable, any change by the Commission at this point would be “legally deficient and open to judicial challenge,” the Coalition believes. Instead, the Coalition claimed it is reasonable to conclude that based on the data provided in this proceeding changing the start of the Gas Day will not have a material, positive impact on electric reliability and “would come at the expense of detrimental reliability, safety and cost impacts.”

With the same message to the Commission, APGA5 stressed that FERC’s data requests “made very clear” what the OEPI staff was looking for: any data not present in the record to support the NOPR Gas Day proposal. The data submitted by the various RTOs/ISOs “does not support the thesis that there is a link between the start of the Gas Day and the reliability of gas-fired generators,” APGA said.

If anything, the record confirms to the APGA the importance of retaining the current start time, accepting the supported changes being proffered to the gas nomination cycles, and directing the electric industry to take important self-help steps to foster greater reliability, “including but not limited to securing firm transportation capacity to move their gas supplies to generators or installing adequate dual fuel capability or investing in

5 In addition to individual comments, APGA also supports

the NGC’s joint comments.

gas storage facilities or making other infrastructure investments to ensure the availability of a firm power supply during peak periods.”

While some RTO/ISOs “were more forthcoming than others” in their responses, “the bottom line” is that none of them has any data reflecting the number or duration of de-rates between 3 am to 9 am due to the generators having exhausted their daily nomination of gas transportation service prior to the end of the Gas Day. ISO-NE, which is strongly advocating an earlier Gas Day start, only speculated that if a de-rate occurred between 3 am and 9 am the “likely cause” was exhaustion of the gas nomination.

However, APGA disagrees with ISO-NE’s causation theory. For the municipal group, “the truth of the matter” is that de-rates due to so-called fuel availability or fuel-related events “occur all day long” in each of the RTO/ISOs, are generally proportional to the period of time examined, and can be attributable to a host of factors. Fuel-related outages and de-rates have many causes and there is no reliable evidence that the start of the Gas Day is a relevant, distinguishing factor that warrants the change in the start, APGA stated.

Factors that cause de-rates could include: insufficient firm pipeline and/or LDC capacity to transport the gas; operational issues on the pipeline and/or the LDC; economic issues related to the price of gas or the price of secondary market capacity at the particular time; and force majeure events at the wellhead, on the pipeline, at a storage facility, on the LDC, and/or at the generator – not the start time of the Gas Day.

APGA suggested that the proposed changes in the NAESB-proposed nomination cycles will help the most to eliminate generators’ morning ramp issues. FERC also is beginning to understand the importance of addressing New England’s over-reliance of gas-fired

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 10

generators on non-firm transportation capacity – a problem that will not be cured by any of the measures proposed in the NOPR. The Commission appears to be addressing this, on the other hand, in the AD13-7 and AD14-8 proceedings and related technical conferences, observed the municipal gas group.

With Several Recommendations, State Regulators Offer Support and in Some Cases Caution for FERC’s Proposal Regarding Gas Pipeline Recovery of Modernization Costs; PHMSA Recommends Broad Use of Pipeline Modernization Programs

Offering specific recommendations based on their state’s experience regulating local gas distribution companies (LDCs), a few state utility commissions recently offered cautious approval of FERC’s pending Policy Statement, Cost Recovery Mechanisms for Modernization of Natural Gas Facilities (PL15-1), in filings at the Commission.6 The state regulators -- including the Michigan Public Service Commission (PSC); the North Carolina Utilities Commission (NCUC); Kansas Corporation Commission (KCC); and New York Public Service Commission (NYPSC) – some of which had implemented the kind of mechanisms FERC is considering, suggested strengthening some of the measures to make sure pipelines do not over-recover costs.

For example, Michigan PSC urged FERC to limit the use of a tracker mechanism to recover only capital costs that are “required” by new state or federal regulations to ensure that pipelines are not using the vehicle to recover discretionary expenditures. According to North Carolina regulators, FERC’s five proposed standards may not be adequate

6 FR’s previous coverage of PL15-1 found gas producers,

marketers and end users disagreeing with gas pipelines and gas distributors over whether FERC should allow pipelines to surcharge customers for recovery of natural gas system modernization costs (see FR No. 3035, pp1-14).

enough to protect ratepayers from over-recovery of costs by pipelines. Pipelines should not be provided incentives to make the investments that they already should and do make to fulfill their obligations to provide safe and reliable service. Therefore, as part of a request to obtain a tracker, FERC should require a pipeline to clearly identify for each project the proposed costs to recover via the tracker, and identify the specific new safety or environmental requirement that the project is designed to fulfill.

NCUC also had concerns with the uncertainty of policies that would require interstate pipelines to make upgrades and improvements, leaving unknown the full breadth of compliance costs. “At this time, it is therefore not possible to determine whether existing rate levels or existing regulations and policies are adequate to comply with these additional requirements,” the regulators said. Such an analysis should be completed before the Commission undertakes any change to its current policy against trackers.

Kansas regulators suggested that FERC keep a tight lid on what it considers “eligible costs” for recovery in a tracker mechanism. The expansion of the tracker to include a broader category of costs “is undesirable because a catch-all category would be subject to abuse.” For regulators in New York, one of the main concerns is reducing a pipeline’s return on equity (ROE), if a surcharge is allowed. The NYPSC urged the Commission to consider a pipeline’s incremental reduction in risk due to the proposed surcharge and reduce a pipeline’s ROE accordingly.

From the Federal angle, the Pipeline and Hazardous Materials Safety Administration (PHMSA), the federal agency responsible for enforcing pipeline safety, wants to see FERC consider options to address gas pipeline modernization programs outside of a company-specific rate case.

FOSTER REPORT NO. 3036 February 6, 2015

11 © Concentric Energy Publications, Inc.

NOPR. The Commission’s November 20, 2014 proposed Policy Statement on cost recovery mechanisms for modernization of natural gas facilities creates an analytical framework that would allow pipelines to recoup modernization costs necessary for efficient and safe operation of pipeline systems and compliance with new regulations expected soon to be promulgated by the likes of the Pipeline and Hazardous Materials Safety Administration (PHMSA) and Environmental Protection Agency (EPA) and perhaps other agencies.

The Commission proposed to follow five standards that a pipeline would need to satisfy in order to establish a tracker: (1) review of existing rates; (2) eligible costs; (3) avoidance of cost shifting; (4) periodic review of the surcharge; and (5) shipper support. These characteristics are patterned after a recent recently approved contested settlement involving Columbia Gas Transmission, LLC (2013), which included a tracking mechanism to recover substantial pipeline modernization costs.

PHMSA. As the federal agency responsible for overseeing pipeline safety, PHMSA “strongly supports” FERC’s proposed Policy Statement. While an affordable and reliable energy supply is critical to public safety and the nation’s economy, operators may delay pipeline repair and replacement due to cost concerns, at significant risk to public safety and the environment. The majority of pipelines were constructed prior to the establishment of federal pipeline safety regulations: 12% of interstate gas transmission and hazardous liquids pipelines were built prior to 1950. Alone, 59% of gas lines were built before 1970 and 69% were built before 1980.

The Commission’s Policy Statement would provide alternative rate recovery mechanisms for pipeline modernization for companies who seek a rate review, but PHMSA is concerned

that the number of companies actually expected to seek a rate review in the near future “is somewhat limited.” As such, PHMSA encouraged FERC to consider mechanisms that allow for alternative rate recovery without a full rate review. “Also, we further recommend that FERC consider mechanisms that allow operators to seek rate recovery for modernization projects even if the pipeline involved may not be in violation of applicable regulations.”

The agency also encouraged the Commission to work with agencies in states that do not have recovery mechanisms so that they “could take advantage of FERC’s cost recovery model and adopt it at the state level where appropriate.”

Michigan PSC. Michigan’s regulators support the Commission’s efforts to offer a tracking mechanism that would allow recovery of pipeline modernization costs. Claiming first-hand experience in these kinds of matters, the Michigan regulators made several recommendations. The PSC has approved recovery mechanisms for 3 natural gas utilities in Michigan -- SEMCO Energy Gas Co., Consumers Energy Co., and DTE Gas Co. The state sanctioned trackers allow the LDCs to recover costs associated with pipeline safety, such as replacing old and inefficient compressors, leak-prone pipes and performing other necessary infrastructure improvements and upgrades.

The MPSC developed approval of the LDC recovery mechanisms in the context of full general rate cases that evaluated the just and reasonableness of the utilities’ underlying rates. With approval of a tracker mechanism, each LDC is required to file annual reports with PSC discussing the specific capital improvements made during the previous calendar year. This allows for PSC staff to investigate each utility’s compliance with the approved safety mechanism, the regulators explained.

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 12

Given its experience, Michigan encouraged FERC to approve the use of recovery mechanisms within the context of a section 4 rate case (pursuant to the Natural Gas Act, NGA), especially in circumstances where the amount of investment in question has more than a de minimus impact on rates. Such a policy would provide an expedited surcharge or tracker mechanism for circumstances where the capital costs do not exceed 10% of the rate base reflected in the pipeline’s existing rates.

In circumstances where capital costs are greater than 10% of the rate base, pipelines should be required to seek such recovery in a full rate filing. FERC then could judge the appropriateness of the expedited surcharge or tracker on a pipeline-by-pipeline basis, with specific consideration given to the size of the capital costs relative to the size of the pipeline’s existing rate base.

Additionally, the Michigan PSC recommended that FERC require each pipeline using the tracker to file an annual reconciliation of the projects completed and costs in the docket approving a surcharge or tracker. “This would provide a trail of the projects and costs for all interested parties, would help ensure that the companies are not including projects or costs that should not be included, and does not violate the limitations of costs to no more than 10% of the rate base,” the PSC said.

Commenting on FERC’s proposal to extend the 5 guiding principles that served as a basis for the Commission’s approval of the Columbia Gas settlement filing to all pipelines via the Policy Statement, the MPSC believes those principles would “serve as a solid foundation,” provided that they are “mandatory conditions and not simply intended to be optional guidelines.”

Additionally, FERC needs to factor in several other considerations “to eliminate ambiguity and to provide for the proper balance of

pipeline and consumer protections,” including the following:

• FERC should limit an expedited surcharge or tracker rate mechanism to mandate that carrying costs associated with the capital costs and any rate base treatment are subject to a section 4 rate filing.

• FERC should not establish a framework for pipelines to accelerate the recovery of contemplated, one-time capital costs, as it may be excessive to provide the pipeline with the ability to accelerate the rate recovery period and to also permit the pipeline to recover depreciation expense plus a return on the unamortized balance of the expenditure. Instead, a pipeline should be permitted to recover a return on its capital investments, which takes into consideration the normal depreciation period and a return on the declining rate base.

• FERC should limit the mechanism to recover only capital costs that are “required” by new state or federal regulations in order to ensure that pipelines are not using the vehicle to recover discretionary expenditures; the Commission’s language in its Policy Statement proposal is too vague in this respect.

• FERC should require that such capital costs in a mechanism be depreciated consistent with the currently applicable depreciation rates for such assets, which would allow pipelines the ability to receive a return on capital investments but also protect ratepayers from a unilateral increase to rate base outside of a pipeline elected section 4 proceeding.

• All amounts approved as part of a safety/modernization surcharge or tracker mechanism must be actually

FOSTER REPORT NO. 3036 February 6, 2015

13 © Concentric Energy Publications, Inc.

expended consistent with the intended purpose; or all amounts collected should be refunded, with interest, to ratepayers after a designated period of time.

North Carolina Utilities Commission. The NCUC offered a more cautious view of the Commission’s proposal “to change its long-standing policy against the use of trackers.” While NCUC supports policies that provide pipelines with appropriate incentives to maintain and modernize their facilities, those incentives must be viewed in the context of the NGA’s requirement that rates be just and reasonable.

Until new pipeline safety or modernization requirements are established, it is impossible to estimate “even the relevant universe” of potential additional costs pipelines may need to incur, the regulators said. Absent that data, there is an insufficient basis to support a finding that the existing regulations requiring pipelines to design their rates based on projected units of service is inadequate or results in unjust and unreasonable rates.

In the view of North Carolina’s regulators, FERC’s 5 proposed standards “must be strictly applied” in order to help ensure that ratepayers are not burdened with excessive rates. As drafted, the standards may not be adequate to protect ratepayers from over-recovery of costs by pipelines.

NCUC offered several stipulations to strengthen the proposed standards, including requiring that a pipeline’s base rates be reviewed through a full NGA general rate proceeding or via a collaborative effort between the pipeline and its customers. The latter would be “an essential prerequisite” to a pipeline being allowed a modernization costs tracker. In the event a negotiated resolution is not reached, a full NGA rate case is necessary before a tracker is instituted. Also, eligible costs must be limited to one-time capital costs incurred to meet safety or

environmental regulations, and the pipeline must specifically identify each capital investment to be recovered by the surcharge.

Kansas Regulators. Striking a similar tone, the KCC said it supports a system modernization cost tracker provided that “adequate safeguards” protect against excess rates. “Generally, as long as a tracking mechanism is properly designed, the KCC does not oppose such trackers,” the regulators indicated.

The types of costs appropriate to be included in a surcharge or tracking mechanism are typically limited to expenses or capital expenditures that meet the following characteristics: the costs are (1) outside the control of the utility; (2) are variable and their incurrence is unpredictable; and (3) are likely to cause material financial harm if subjected to the normal ratemaking process. Permitting normal costs to be recovered through a tracker inhibits a pipeline’s incentives to minimize costs and increase service.

To assure that existing rates are just, a pipeline’s base rates must have been recently reviewed, either by means of a general section 4 rate proceeding or through a collaborative effort between the pipeline and customers. KCC opposes the filing of a Cost & Revenue (C&R) study as an alternative to a section 4 determination, given the KCC’s experience litigating pipeline rate cases before the Commission. C&R Studies are inadequate because they do not provide the level of detail contained in a section 4 filing. Also, if parties or the Commission do not believe the pipeline’s rates are just and reasonable based on a C&R Study, the heavy burdens of NGA section 5 are placed on them, rather than on the pipeline.

“The burden should rest on the pipeline to demonstrate that its base rates are just and reasonable, and that process should not envision shifting the burden to those who

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 14

disagree with the adequacy of the pipeline’s showing,” the KCC observed.

In lieu of filing a C&R Study, as an alternative, the KCC recommended requiring the justness and reasonableness of the pipeline’s base rates to be based upon a Commission determination made in a general rate case within a relatively short period, not more than three (3) years, prior to the filing of the pipeline’s tracker application.

In addition, the KCC opposes the expansion of “eligible costs” in a tracker to include “other capital costs shown to be necessary for the safe or efficient operation of the pipeline.” The expansion of the tracker to include a broader category of costs is undesirable because the catch-all category would be subject to abuse. Moreover, there is no compelling reason to expand the scope of the limited and focused tracker to include “other” costs, recovery of which is adequately provided for by existing cost recovery mechanisms.

As an exception to general ratemaking practice, the modernization cost tracker should be limited to costs facing interstate pipelines as a result of imposition of new environmental and safety standards over which the pipelines have no real control. Costs that are not shown to be required by PHMSA or EPA regulations should be subject to traditional ratemaking practice.

Moreover, KCC agrees that inclusion of mechanisms to prevent cost shifting “must be an essential element” of any surcharge or tracker mechanism. Here, such mechanisms are likely best developed on a case-by-case basis, tailored to the particulars of the individual pipeline’s tariff and rate structures as well as to the characteristics of the markets served by the pipeline.

In addition, the KCC strongly endorses conditioning pipelines’ access to the proposed modernization cost tracker on a requirement

for periodic true-up of the pipeline’s base rates. FERC has the legal authority to condition pipelines’ continued access to a cost tracker including imposing an enforceable undertaking to periodically refile the pipeline’s base rates. Absent periodic rate review, the very real risk exists that, over time, pipeline rates will depart materially from actual costs by reason of the operation of the modernization cost tracker.

Lastly, the KCC does not oppose extension of the use of accelerated amortization methodologies, calling the idea a “novel concept” that should be explored further.

New York Regulators. The NYPSC wants the Commission to reduce a pipeline’s approved ROE if the proposed cost recovery mechanism is allowed. These regulators argued that the effect of a cost-tracker mechanism on risk was similar to that of Straight Fixed-Variable (SFV) rate design. FERC’s support of SFV rate design, since its adoption in Order 636, has already led to a reduction in risk of pipeline’s under-recovering revenues. By guaranteeing interstate pipelines set revenue recovery, cost-trackers further reduce any risk of under-recovery inherent in rate design based on estimated units of service. Therefore, during pipeline rate cases the Commission should consider the incremental reduction of risk due to the tracker, and the pipeline’s ROE should be reduced accordingly.

FERC’s proposed Policy Statement is based on the Columbia settlement, which it found to be just and reasonable primarily because the settlement, the product of a review of Columbia's base rates, resulted in a base rate reduction and $50 million refund to firm shippers. However, a base rate reduction or refund is not one of the Commission's proposed standards for approving modernization surcharges. In lieu of such a requirement, the Commission should review and reduce a pipeline’s allowed ROE to reflect

FOSTER REPORT NO. 3036 February 6, 2015

15 © Concentric Energy Publications, Inc.

risk reduction and ensure that rates are just and reasonable, the NYPSC stated.

In approving the Columbia Gas settlement, FERC found that Columbia Gas would be subject to continuing risk of cost under-recovery, in part because a billing determinant floor was established for calculating the capital cost recovery mechanism. Columbia Gas would impute the revenue that it would achieve by charging the maximum rate for service at the level of the billing determinant floor before truing up any cost under-recoveries. While requiring a billing determinant floor for the surcharge does allow some risk to remain with the pipeline, a tracker mechanism still reduces a pipeline’s risk and transfers it to shippers, the NYPSC warned.

NYPSC also said the Commission should require concurrent base rate review with the establishment of the surcharge. A section 4 rate proceeding or a collaborative effort would be the proper forum for risk analysis and corresponding ROE reduction.

FERC ENFORCEMENT

FERC Majority Brings Enforcement Action Against Canadian-Managed U.S. Power Generator That Allegedly Sought to Collect ISO-New England Reimbursements for Standby Role Based on High Fuel Oil Costs When In Fact Cheaper Natural Gas Was Used and Available

A majority of Commissioners at FERC supported an order to show cause issued on 2/2/15, plus a notice of proposed penalty naming possible violators of its power market manipulation rules as follows: Maxim Power Corp., Maxim Power (USA), Inc., Maxim Power (USA) Holding Co. Inc., Pawtucket Power Holding Co., LLC, Pittsfield Generating Co., LP

(collectively “Maxim”) and Kyle Mitton.7 The Commission’s enforcement staff (IN15-4) apparently found evidence that these entities were parties to a scheme to obtain payments for reliability dispatches based on the price of expensive fuel oil when Maxim in fact burned much less costly natural gas.

Commissioner Tony Clark dissented. Having reviewed the OE Staff Report and Maxim’s responses, he did not find that the record sufficiently supports the Commission moving forward with the order to show cause. Nonetheless, Clark stated, “in the next phase of the proceeding, both FERC Enforcement Staff and the Respondents will have an opportunity to more fully develop the record. As such, I make no prejudgment as to the final disposition.”

The Respondents were asked to show cause why they should not be assessed civil penalties in the following amounts: (1) Maxim and its Named Subsidiaries (jointly and severally): $5,000,000; and (2) Kyle Mitton: $50,000.8 Respondents may also seek a modification of those amounts. The Commission’s order drew 7 Maxim Power Corp. is a Canadian firm based in Calgary,

traded on the Toronto Stock Exchange. Through wholly-owned subsidiaries, it owns power plants in Canada, France, and the U.S. The Canadian parent’s wholly owned U.S. subsidiary, Maxim Power (USA), Inc., itself has several layers of wholly-owned subsidiaries, including the Respondents in this proceeding. Through these subsidiaries, Maxim USA (and its Canadian parent) own and control 3 power plants in New England that sell into ISO-NE.

A January 2013 Memorandum confirmed that (1) in all respects relevant to this investigation, Maxim Power personnel in Calgary (in particular, the company’s Energy Marketing Group) manage and control the Maxim Subsidiaries and (b) none of the Maxim Subsidiaries has any employees. Maxim's Energy Marketing Group has been working in the US Northeast markets since the acquisition of Pawtucket in November 2005.

8 The Enforcement Staff Report concluded: “It is a fair inference that Mitton believed he would personally benefit if he were able to obtain millions of dollars of additional revenue for Maxim by being paid as though Maxim had burned expensive oil when in fact it burned much cheaper gas.” However, among other defenses Mitton had argued that the Federal Power Act does not authorize the Commission to hold individuals liable under the Anti-Manipulation Rule. However, the key staff report points out that the Commission “has long since resolved that issue,” concluding in Order No. 670 that the term “[a]ny entity” in the FPA and the Natural Gas Act is a “deliberately inclusive term” that includes “any person or form of organization . . . .”

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 16

on recommendations of OE Staff’s earlier Report. The scheme achieved (until reversed by the ISO’s monitor) $2.99 million in unjust profits, lasted 45 days, and was implemented by personnel with substantial authority in an organization with more than 10 employees. Maxim cooperated with the investigation.

This case presents allegations by OE staff of Respondents’ violation of the Commission’s Prohibition of Energy Market Manipulation, and of Maxim’s alleged violation of section 35.41(b) of the Commission’s rules. These allegations arose out of an investigation conducted by OE staff and are described in the Enforcement Staff Report and Recommendation submitted to the Commission on January 16.

Applying the Penalty Guidelines, the Commission’s staff had requested a penalty of $5,000,000 on Maxim. Because the same conduct violated both the Anti-Manipulation Rule and section 35.41(b) of the regulations, Staff did not recommend a separate penalty for the latter violation. Given Mitton’s central role in the scheme “but taking his financial circumstances into account (Mitton’s annual salary for 2013 was C$120,000 with a $20,000 bonus), staff requested a penalty of $50,000 for his violation of the Anti-Manipulation Rule.

The OE Staff Report alleges that, principally through its employee Kyle Mitton, Maxim engaged in a series of transactions with ISO-New England (ISO-NE) and misleading communications with the ISO-NE Internal Market Monitor (IMM) for the purpose of obtaining “inflated make-whole payments at high fuel oil prices” when a Maxim plant was dispatched for reliability, “even though the plant was actually burning much less expensive natural gas.”9

9 Because the ISO-NE IMM later applied mitigation to recoup

what it viewed as excessive payments to Maxim, the Staff Report does not seek additional disgorgement.

During July and August 2010, Maxim regularly submitted Day Ahead offers to ISO-NE at high oil prices, but on 22 days when it got reliability commitments Maxim allegedly burned much less expensive gas to produce all or almost all of the plant’s energy.

As explained by staff, since Maxim’s plant was being called on to ensure the reliable operation of the grid, “rather than because of economics,” the ISO’s rules provided that Maxim could be paid make-whole payments (called Net Period Commitment Payments) based on its fuel price. The Report alleges that when the IMM asked Maxim about its offers, Maxim (through Mitton) responded with communications giving the impression that Maxim was unable to obtain gas and was therefore burning more expensive oil. Maxim gave those responses to the IMM even though on many days Mitton had bought large quantities of gas before submitting a Day Ahead offer based on oil prices.

Maxim’s advance gas purchases show that it expected the key Pittsfield power plant to be committed for reliability, staff decided. That Maxim was not surprised to get reliability awards is also shown by its own conduct in making advance purchases of gas during the period of this strategy. Moreover, the incorrect impression that Maxim successfully communicated to the IMM is “particularly egregious.”

In its communications with the IMM in July and August 2010, Maxim intentionally conveyed false impressions and omitted material information. Section 35.41(b) of the regulations does not require intent; that is, a market participant can violate the rule simply through lack of due diligence. “Here, however, the violations were deliberate and intentional,” staff charged.

Maxim owns three electric power generators that participate in markets administered by ISO-New England. All 3 of Maxim’s New England plants can burn either gas or oil (are

FOSTER REPORT NO. 3036 February 6, 2015

17 © Concentric Energy Publications, Inc.

dual-fuel). The focus of this FERC proceeding is Maxim’s plant in Pittsfield, Massachusetts, which Maxim acquired in 2008. Pittsfield can burn either fuel oil or natural gas to generate electricity, although it typically burns gas, which staff said is almost always much cheaper on a per-MWh basis.

The violations purportedly stemmed from a strategy employed by Maxim and Mitton in the summer of 2010 to collect payments from ISO-NE for reliability dispatches. Maxim executive Kyle Mitton developed and implemented this strategy. The strategy described in this report is one of three identified in a 11/3/14 Notice of Alleged Violations by Maxim and its personnel. Enforcement’s investigation of the other two strategies continues.

According to staff’s report, although the Pittsfield plant is relatively inefficient (and its energy offers are usually above-market rates), the ISO often needs to dispatch Pittsfield for reliability when loads are high. When ISO-NE does so, it ordinarily provides “make-whole” payments to Maxim for the difference between the plant’s offer price and lower market rates.

In July and August 2010 Maxim offered Pittsfield to ISO-NE based on high oil prices. The report said that even though Pittsfield’s offer prices were usually far above market rates and thus did not clear the Day Ahead market based on price, ISO-NE regularly needed Pittsfield “for reliability reasons” during those hot summer months, and committed the plant many times on that basis.

Because it was being committed for reliability, Maxim expected to be, and initially was, paid “an out-of-market payment” based on its offer price – that is, at high oil prices – even though it was actually burning much cheaper natural gas. As a result, Maxim collected extra payments averaging more than $135,000/d on the days it received Day Ahead commitments after offering based on oil prices, and then burned gas.

Apparently when the IMM asked Maxim in mid-July 2010 why it was offering Pittsfield at such high prices, Maxim gave answers that created the false impression that Maxim had to use high-priced oil because the Pittsfield plant itself was having problems obtaining gas.

Maxim actually was not only able to procure gas to satisfy nearly 100% of its commitments, but in many cases had already purchased large quantities of gas for next day delivery when it submitted offers based on oil prices. Enforcement staff determined that these purchases show that Maxim was expecting reliability commitments for the next day, and planned, after offering Pittsfield based on oil prices, to burn gas for much if not all of any commitment period.

Maxim received $2.99 million in excessive payments from this strategy, alleged staff. The ISO later recouped these payments after the IMM discovered (with no help from Maxim) what Maxim had done.

How the RTO System Works. ISO-NE operates both “Day Ahead” and “Real Time” markets for energy. The Day Ahead market operates one day ahead of the date on which the energy is actually delivered (the “operating date”). The Real Time market operates on the day the energy is transmitted, and prices and dispatch levels are resolved on a five-minute basis.

ISO-NE schedules Day Ahead awards (or “unit commitments”) to power plants via (1) marketplace awards, reflecting units committed based on a plant’s economics (or “merit”), that is, because the plant’s offer price is competitive (or “economic”); or (2) resources committed for reliability purposes (i.e., in some cases, a plant is needed to ensure that the ISO-NE grid can run reliably). A plant may clear the Day Ahead market, even if it is very expensive, because of a reliability need. A plant committed because of a reliability need may qualify for Net Commitment Period Compensation (NCPC), commonly known as make-whole payments, depending on the circumstances.

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 18

ISO-NE passes through the costs of NCPC payments to load-serving entities, which in turn pass those costs along to households, businesses, nonprofits, and government entities as part of retail electricity bills. Excessive make-whole payments therefore translate into higher electricity bills for consumers.

Like other ISOs and RTOs, ISO-NE has tariff rules designed to prevent generators from unfairly exploiting their market power when they are needed for reliability. In particular, ISO-NE’s rules seek to prevent generators from extracting excessive make-whole (in this case, NCPC) payments when they are dispatched to ensure that the New England grid continues to operate reliably.

The NCPC rules in place during 2010 were the result of an 8/5/09 tariff filing by ISO-NE, which was approved in relevant part by the Commission in October 2009. Under the rules applicable at the time, New England market participants were eligible to receive NCPC payments when a resource is dispatched out of economic merit for reliability purposes and the fuel and variable operating and maintenance (O&M) costs of operating the resource, as reflected in its time-based Supply Offer, exceeded the revenue paid to the market participant in the energy markets.

Specifically, NCPC payments to generators needed for reliability were limited to 110% of the unit’s reference levels. “As Maxim knew, reference levels for oil were, during this period (and almost always) much higher than reference levels for gas. By misleading the IMM about what fuel it burned, Maxim collected millions of dollars in NCPC payments for reliability dispatches at prices based on oil that were far above its actual (gas) costs. Only a later intervention by the IMM protected New England ratepayers from being charged these additional millions of dollars,” the OE staff had concluded in the report conveyed to the full Commission.

NATURAL GAS PROJECTS

Pre-filing Review Begins at FERC for the Atlantic Bridge Project, Joined by Algonquin and Maritimes & Northeast Pipeline

On 1/30/15 Algonquin Gas Transmission, LLC and Maritimes & Northeast Pipeline, LLC (PF15-12) jointly requested approval from Commission staff to initiate the Pre-Filing Review Process for the proposed Atlantic Bridge Project, designed “to deliver critically needed natural gas supplies that will meet immediate and future supply and load growth requirements in the Northeast market area.” The target in-service date for the project is 11/1/2017. The filers anticipate submitting the certificate application in September 2015.

The Atlantic Bridge Project will create additional firm pipeline capacity necessary to deliver 222,000 Dth/d of natural gas to the northeastern U.S., connecting a receipt point on Algonquin’s system at Mahwah in Bergen County, New Jersey with delivery points on the Algonquin’s and Maritimes’ systems. The application explains that the capacity will be created primarily “through take up and relay, looping and additional compression” on the existing Algonquin system, as well as bi-directional flow on the existing Maritimes system.

The applicants held an open season for the Atlantic Bridge Project from 2/2/14 through 3/31/14 and as a result executed precedent agreements with 6 shippers for firm transportation on the facilities. Algonquin held a reverse open season last month, and received no offers to turn back capacity.

The shippers that signed on, including both distribution companies and end users, subscribed to incremental transportation capacity for deliveries in both southern and

FOSTER REPORT NO. 3036 February 6, 2015

19 © Concentric Energy Publications, Inc.

northern New England, as well as to specific end use markets in the Canadian Maritime provinces. In addition, Algonquin and Maritimes are negotiating with additional potential shippers that seek capacity for deliveries on or at the end of Maritimes’ system.

The application explains that demand for natural gas has continued to grow in the Northeast as the region seeks “additional access to an economic source of fuel that is domestically produced, clean-burning and efficient.” It is also clarified in the document that “with significant Project shipper volumes designed to flow on both the Algonquin and Maritimes systems, this Project will provide increased pipeline capacity through critical constraint points and satisfies a different purpose from the Algonquin Incremental Market Project.” The AIM Project was designed to meet the needs of southern New England distribution companies for incremental transportation capacity beginning in November 2016.

The Atlantic Bridge Project will consist of approximately 23.9 miles of new mainline pipeline. Construction and installation will involve: (1) 1.2 miles of removal and replacement of 26-inch diameter pipeline with 42-inch pipeline in Rockland County, New York, upstream of Algonquin’s existing

Ramapo Compressor Station; (2) 5.9 miles of removal and replacement of existing pipeline with 42-inch diameter pipeline in Westchester County, New York, downstream of Algonquin’s existing Stony Point Compressor Station; (3) 3.8 miles of removal and replacement of smaller pipeline with 42-inch pipe in Fairfield County, Connecticut, downstream of Algonquin’s existing Southeast Compressor Station; (4) 10.4 miles of 36-inch diameter pipeline loop extension in three Connecticut counties downstream of Algonquin’s existing Cromwell Compressor Station; and (5) 2.6 miles of 36-inch diameter pipeline loop in Windham County, Connecticut, downstream of Algonquin’s existing Chaplin Compressor Station.

The proposal includes a plan to construct approximately 12.3 miles of lateral pipeline, comprised of 2.2 miles of 12-inch diameter pipeline loop on Algonquin’s existing G-2 System in Newport County, Rhode Island; 10.1 miles of 30-inch pipe loop on Algonquin’s existing Q-1 System in Norfolk County, Massachusetts; plus installation of facilities at two existing Algonquin Compressor Stations for an additional 18,615 horsepower (hp).

The project will directly affect approximately 294 landowners or 374 tracts along the pipeline portion.

February 6, 2015 FOSTER REPORT NO. 3036

© Concentric Energy Publications, Inc. 20

Tennessee Gas Pipeline Submits FERC Application Seeking Authorization for Broad Run Expansion Project To Deliver Marcellus/Utica Shale Gas Produced by Antero Resources

On January 30 Tennessee Gas Pipeline Co. LLC (CP15-77) submitted to FERC its application seeking authorization to install compression facilities to be located in Kentucky, Tennessee, and West Virginia, and to abandon other facilities, located in Kentucky, referred to as the Broad Run Expansion Project. The proposal is comprised of two components: (1) the Market Component, involving construction, installation, operation and maintenance of compression and related facilities in order to enable Tennessee to provide up to 200,000 Dth/d of firm incremental transportation service “to meet a specified market need”; and (2) the Replacement Component, involving the replacement of older, less efficient compression facilities with new, more efficient facilities at two compressor stations.

In addition to the certificate authority, Tennessee requested that the Commission authorize (pursuant to NGA section 7(b)) the abandonment of certain compression facilities that will be replaced with new facilities as part of the project. “Although these replacements of compressor facilities would not typically require specific abandonment authority,” Tennessee explained it is seeking that authority in this proceeding “since the replacement of these facilities is an integral part of the Project for which Tennessee is seeking certificate authority herein.” Tennessee does not propose to abandon any transportation service as part of the project.

Tennessee asked the Commission for the certificate and abandonment authorizations by 1/31/16, with an eye to complete construction by the 11/1/17 in-service date requested by the key shipper, Antero Resources Corp.

According to the application, this sole shipper executed a binding precedent agreement that provides the market support for the Market Component. The project will deliver natural gas produced in the Utica and Marcellus Shale supply areas to markets in the southeastern U.S.

In order to meet this demand, Tennessee proposes to (1) construct 4 new greenfield compressor stations (two in West Virginia, one in Kentucky and one in Tennessee), and (2) modify 2 existing compressor stations along Tennessee’s system in Kentucky. Each of the new compressor stations is located in close proximity to Tennessee’s existing 100, 500, and 800 Lines.

Besides serving the growing demand for firm transportation to markets in the Southeast, Tennessee said its project will also improve the efficiency and reduce certain emissions by replacing certain less efficient older existing compression facilities with newer, more efficient, cleaner burning, and lower emission compressor units.

Tennessee will provide firm transportation for Antero pursuant to a long-term service agreement under Rate Schedule FT-A of Tennessee’s FERC Gas Tariff and Tennessee’s blanket certificate under Part 284, Subpart G of the regulations.

The estimated cost of the Market Component and Replacement Component, including contingency, overheads, and Allowance for Funds Used During Construction (AFUDC), is approximately $337.9 million and $68.5 million, respectively. Tennessee is proposing an incremental recourse rate under Rate Schedule FT-A for firm transportation on the Market Component facilities.

Since installation of compressor station facilities at existing Compressor Stations 106 and 114 pertain to both the Market Component and the Replacement Component, Tennessee proposes to allocate the cost of

FOSTER REPORT NO. 3036 February 6, 2015

21 © Concentric Energy Publications, Inc.

construction at these stations to each project component on a percentage basis. The percentages are based on the horsepower (hp) attributable to the Market Component and to the Replacement Component, as compared to the total hp being installed at each compressor station.

Tennessee held a binding Open Season for the Market Component from 3/25/14 to 4/11/14, offering 200,000 Dth/d expansion capacity from (1) a new point of interconnection, or (2) a mutually agreeable receipt point on Tennessee’s Broad Run Lateral in Zone 3 of its system to one or more mutually agreeable delivery points in Zone 1.

The open season notice also included solicitation for firm transportation service of up 590,000 Dth/d for the “Broad Run System Flexibility Project” to be made available through (1) the use of capacity reserved pursuant to Tennessee’s tariff, and (2) the installation of certain appurtenant facilities and modifications to allow for bidirectional flow of gas on Tennessee.

The construction and installation of appurtenant facilities for the Broad Run System Flexibility Project commenced last July, with the estimated in-service dates of 11/1/15 for Phase I of that project and 11/1/16 for Phase II.

In the open season, Tennessee offered firm expansion capacity for the Market Component at either an incremental maximum recourse rate, to be established through this certificate proceeding, or a negotiated rate, plus fuel and applicable surcharges. Antero, the winning bidder, selected the negotiated rate option. One party, in addition to Antero, submitted a bid during the open season for a portion of the capacity, but Antero was awarded the full 200,000 Dth/d of Market Component capacity.

Actually, before the open season began Tennessee executed a binding Precedent Agreement with Antero for the 200,000 Dth/d

for a 15-year term, reflecting the commercial terms and conditions for its commitment to participate as Original Foundation Shipper. The project shipper has a one-time contractual right to extend the primary term of its firm service agreement at the same negotiated rate that was in effect during the primary term. Any subsequent extensions after the initial extended term would be at the applicable maximum recourse rate for service on the facilities.