fortune - s1.q4cdn.com

TRANSCRIPT

FORTUNEMINERALS LIMITED

ANNUAL REPORT

2007

2 I FORTUNE MINERALS LIMITED

2007

CORPORATE PROFILE

4 2007 and Recent Corporate Highlights8 Report to Shareholders

OPERATIONS REVIEW12 NICO Cobalt-Gold-Bismuth Project22 Mount Klappan Anthracite Coal Project34 Sue-Dianne Copper-Silver-Gold Project

FINANCIAL REVIEW36 Management’s Discussion and Analysis of

Financial Conditions and Results of Operations50 Management’s Responsibility for Financial Reporting51 Auditor’s Report52 Consolidated Financial Statements

66 Directors, Officers and Corporate Information

Fortune Minerals Limited (TSX: FT) is focussed on the assembly and development of highquality mineral resource projects with the potential to generate strong returns for its share-holders. Fortune currently has interests in three advanced stage projects with productionplanned for two of these projects by the end of the decade, as well as several explorationprojects, all located in Canada.

The Company is proceeding with environmental assessment and mine permitting activitiesfor its NICO cobalt-gold-bismuth deposit near Yellowknife,Northwest Territories,based uponthe positive findings of its independent bankable feasibility study. This study concluded thatthe project shows attractive economics at base case metal price assumptions and very attrac-tive economics at the much higher prices of current commodities markets.

The Company’s world class Mount Klappan anthracite coal project, located near deep-waterport facilities in northwest British Columbia, is in the permitting process after receipt of anindependent positive bankable feasibility study. Metallurgical coal is also being traded atrecord high prices that are substantially higher than those used in the independent feasibil-ity study.

Fortune’s third key project, its Sue-Dianne copper-silver deposit, is located only 25 kilome-tres north of NICO and is a potential future source of mill feed for the process plant plannedfor NICO.

ANNUAL MEETING

The Annual and Special Meeting of Shareholders will be held at The Fairmont Royal YorkHotel,York Room (Mezzanine Level), 100 Front Street West,Toronto,Ontario,M5J 1E3,on the27th day of May, 2008, at 4:30 pm.

For those persons unable to attend, a second, informal meeting for informational purposeswill be held at The London Club, 177 Queens Avenue, London, Ontario, N6A 1J1, on the 28thday of May, 2008, at 4:30 pm.

CONTENTS

2007

ANNUAL REPORT I 3

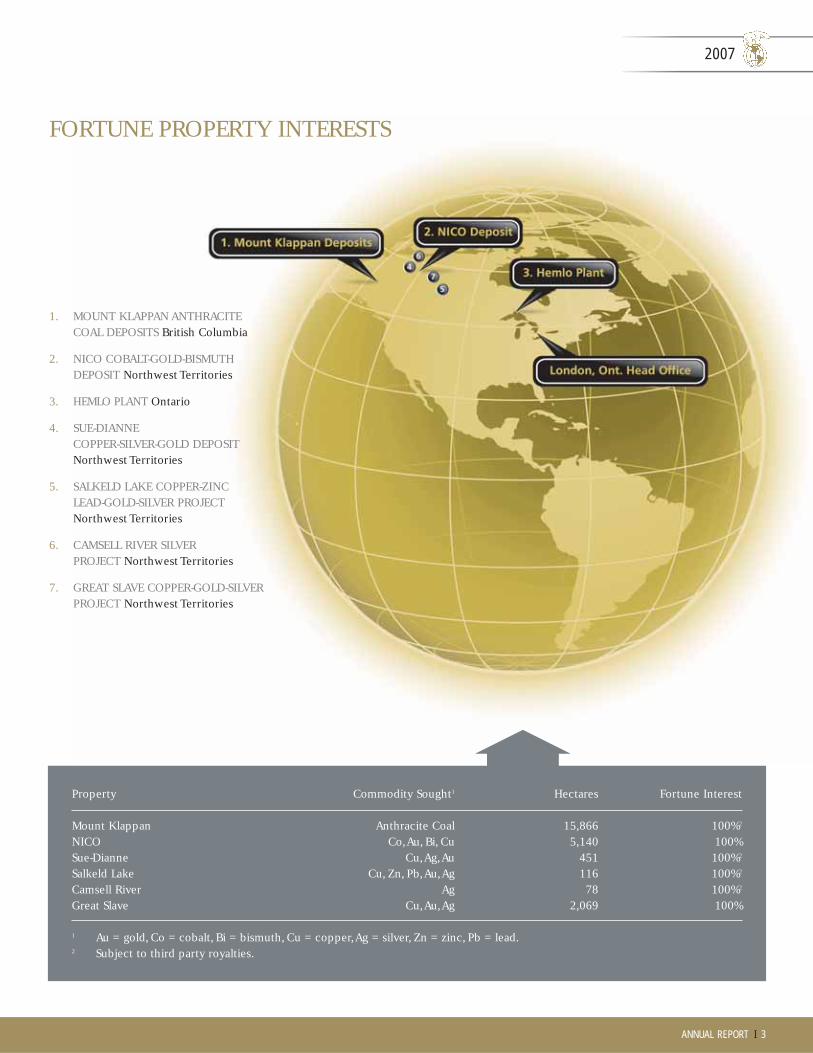

FORTUNE PROPERTY INTERESTS

Property Commodity Sought1 Hectares Fortune Interest

Mount Klappan Anthracite Coal 15,866 100%2

NICO Co,Au, Bi, Cu 5,140 100%Sue-Dianne Cu,Ag,Au 451 100%2

Salkeld Lake Cu, Zn, Pb,Au,Ag 116 100%2

Camsell River Ag 78 100%2

Great Slave Cu,Au,Ag 2,069 100%

1 Au = gold, Co = cobalt, Bi = bismuth, Cu = copper,Ag = silver, Zn = zinc, Pb = lead.2 Subject to third party royalties.

1. MOUNT KLAPPAN ANTHRACITECOAL DEPOSITS British Columbia

2. NICO COBALT-GOLD-BISMUTHDEPOSIT Northwest Territories

3. HEMLO PLANT Ontario

4. SUE-DIANNECOPPER-SILVER-GOLD DEPOSITNorthwest Territories

5. SALKELD LAKE COPPER-ZINCLEAD-GOLD-SILVER PROJECTNorthwest Territories

6. CAMSELL RIVER SILVER PROJECT Northwest Territories

7. GREAT SLAVE COPPER-GOLD-SILVERPROJECT Northwest Territories

2007

4 I FORTUNE MINERALS LIMITED

CORPORATE ACCOMPLISHMENTS

• Increased the Company’s interest in the NICO project from 90% to 100%.

• Commenced the dismantling of the Golden Giant Mine buildings and surface facilities near Hemlo, Ontario for their relocationto NICO.

• Initiated salvage and sale of surplus equipment, recoverable gold, silver, copper, aluminum, stainless and structural steels and otherhigh value materials.

• Conducted a second $10-million underground bulk sample program to verify NICO grades, assess mining conditions, and collect 200tonnes of ore for large-scale pilot plant testing.

• Proceeding with environmental assessment and permitting activities for the planned NICO mine.

• The Federal, Northwest Territories and Tlicho governments, together with private industry committed $1 million for environmentaland engineering studies to improve road access to the NICO project and nearby communities.

• Commenced a $4-million pilot plant leading to improved recoveries from flotation for all metals at NICO.

• Rising demand and constrained supply helped push metal prices higher, which at April 2008 were: US$52/pound of cobalt,US$925/ounce of gold and US$16/pound of bismuth.

• Conducted further fieldwork, environmental baseline studies, and engineering for the proposed Mount Klappan anthracite coal mineand its access corridors in support of the environmental assessment and permitting processes.

• Received input from First Nations, the general public, and various government agencies regarding the Terms of Reference documentdefining the scope of work required for the environmental assessment application for Mount Klappan.

• Examined infrastructure enhancements, which could improve the already robust economic future of the coal project.

• A positive prefeasibility study assessed the possible supply of thermal coal fuel from the mine for power generation.

• The Alaska - Canada Rail Link Feasibility Study, jointly funded by the State of Alaska and Yukon Territory, recommended a railwayconnection from northern British Columbia to Alaska that would run past Mount Klappan. The study also recommended a short-cutto the Port of Prince Rupert that would dramatically reduce the rail haulage distance from Mount Klappan to the port from1,400 kilometres to just over 600 kilometres, materially reducing transportation costs.

• Anthracite markets continued to tighten as the two largest producing nations reduced exports in favour of domestic consumption.Coal prices, which have escalated to approximately US$250/tonne for ultra-low volatile PCI and more than US$300/tonne for premiumcharge carbon products, are expected to remain at high levels for the foreseeable future.

CAPITAL STOCK & FINANCIAL POSITION:

• At year-end, Fortune had working capital of $22.7 million, no debt and total assets of $90.4 million.

• As at April 2008, Fortune had 50,100,107 shares outstanding; 57,888,107 shares fully diluted.

2007 AND RECENT CORPORATE HIGHLIGHTS

20072006200520042003

90

75

60

45

30

15

0

TOTA

L AS

SETS

mill

ions

of

dolla

rs

2006Q4

2007Q1

2007Q2

2007Q3

2007Q4

2008Q1

6.00

5.00

4.00

3.00

2.00

1.00

0

SHAR

E PR

ICE

CD

N$

2007

ANNUAL REPORT I 5

ABOVE: 2007 tour of NICO underground test mining. From left to

right: Luciano Azzolini (Consultant to the Tlicho Lands Protection

Department), Julian Kemp (CFO), Leon Lafferty (Bechoko Chief),

Carl Clouter (Director), Mike Samuels (Manager Process

Development), Eddie Erasmus (Director, Tlicho Lands Protection

Department), Kathryn Neale (Exploration Manager) and Richard

Gardiner (Driller, Ke Te Whii / Procon Joint Venture).

LEFT: Fortune’s Golden Giant Mine headframe and

administration complex near Hemlo, Ontario.

2007

6 I FORTUNE MINERALS LIMITED

CORPORATE OBJECTIVES FOR 2008

ADVANCE NICO PROJECT:

• Complete $4-million pilot plant at SGS Lakefield Research toconfirm the operating parameters in the proposed processplant, proving operations for the downstream processing ofcobalt, gold and bismuth to high value metal products.

• Complete engineering and preparations for relocating theGolden Giant Mine buildings, milling equipment, surfacefacilities and inventory to NICO, including sale of excessinventory, high value materials and equipment.

• Conduct Tlicho land use public consultation meetings andnegotiate Access and Impacts and Benefits agreements.

• Conduct environmental assessment proceedings leadingto decisions by the Wek’ èezhi’i Land and Water Board andDepartment of Indian Affairs and Northern Developmentfor mine development.

• Conduct front-end engineering and design portions of detailedengineering for the proposed mine and plant; tender contractsfor the order of equipment requiring long-lead times.

• Conduct definitive financing negotiations regardingalternatives to fund construction of the proposed NICO mine.

ADVANCE MOUNT KLAPPAN PROJECT:

• Advance development of the proposed 3 million tonne perannum Lost-Fox anthracite mine at Mount Klappan throughenvironmental assessment and permitting activities.

• Continue to review strategic options for Mount Klappan,including ongoing discussions with potential joint-ventureand/or investment partners.

• Complete assessment of transportation alternatives, includingslurry pipeline and enhanced trucking options for deliveringcoal products to deep-water port.

• Conduct consultation and advance negotiations with theTahltan and other impacted First Nations particularly regardingenvironmental assessment and Impacts and Benefitsagreements.

GENERAL CORPORATE:

• Continue to build management and staff roster forconstruction, management and operation of the mineswe propose to develop.

• Build relationships with financial institutions and investmentbankers to continue advancing the Company in the investmentcommunity.

2007 AND RECENT CORPORATE HIGHLIGHTS

MANAGEMENT APPOINTMENTS

Added new operational strength to the managementteam with the appointments of:

1. Jim Currie, B.Sc. (Hons), P.Eng.Vice President Operations

2. Mike Samuels, B.Eng.Process Development Manager

3. Nicole Hayduk, LL.B., H.B.A.Contracts Administration Manager

4. Richard Schryer, M.Sc., Ph.D.Manager of Regulatory Affairs

5. Adam Jean, H.B.A., C.A.Controller

6. Pat Moloney, B.Sc., B.Ed.Manager Human Resources

7. Andre Tricoteux, B. Professional ArtsProcurement and Logistics Manager

2007

ANNUAL REPORT I 7

1. 2. 3.

5. 6. 7.

4.

BELOW: Fortune’s outside

hydrometallurgical consulting team

from left to right: Mike Ashbury

(SGS Lakefield), Joe Ferron

(Consultant), Alex Mezei and Marlon

Canizares (SGS Lakefield), Al

Hayden (Consultant), Eliza Ngai and

Debbie Marshall (Aker Kvaerner).

2007

8 I FORTUNE MINERALS LIMITED

REPORT TO SHAREHOLDERS

While the global resources sector had its share of rewards andchallenges in 2007, Fortune Minerals Limited has aggressivelycontinued to advance its two key projects towards targeted productionnear the decade’s end. At Fortune’s now 100%-owned NICO cobalt-gold-bismuth project in the Northwest Territories, the Company hasachieved several important goals, further demonstrating the robusteconomics and viability of this in-house discovery. At the same time,wecontinue to look to optimize our wholly-owned Mount Klappan coalproject in northwest British Columbia – one of the largest, premium,anthracite coal resources on the planet. Still, the road to productionhas been long and challenging,particularly given the volatility of finan-cial and commodity markets. Regardless, Fortune remains focused,determined and strong, confident in our exceptional assets – bothhuman and mineral – and our firm commitment to becoming a leadingCanadian mining company.

Entering 2008, the evidence is everywhere that Fortune is operatingin a world increasingly hungry for the natural resources that representa vital part of Canada’s great heritage. Even as we drive towardsproduction at NICO and Mount Klappan, the global demand andmarket prices for the key commodities contained in our depositscontinue to trend higher, widely achieving near record and evenunprecedented levels.

Our NICO development project contains a significant, near-surfacedeposit with 21.8 million tonnes of reserves containing 760,000ounces of gold, 61 million pounds of cobalt, and 77 million pounds ofbismuth, all within an even larger total resource.While the gold pricerecently broke US$1,000/ounce making NICO a considerable goldasset, its prominent value is in cobalt, a metal in increasing globaldemand for high strength steel alloys and chemicals used to makerechargeable batteries and catalysts. Cobalt, which is predicted todouble in consumption over the next few years, is currently selling inexcess of US$50/pound, compared with the US$16.50/pound used inthe 2007 definitive feasibility study for the NICO development. As oneof the largest deposits of bismuth in the world, NICO also represents aunique source of supply for an environmentally-friendly, non-toxicreplacement for lead. Market prices for bismuth have strengtheneddue to the approximate 15% annual rise in consumption to a currentprice of about US$16/pound as compared with the US$4.50/poundused in our feasibility study. Based upon the current prices of thesemetals, the NICO reserves contain 5.6 million equivalent ounces ofgold and 3.2 million equivalent ounces using feasibility study base casemetal price assumptions, providing an indisputable measure of signifi-cant value in this unique deposit.

At the same time, our Mount Klappan project in northern BritishColumbia, which contains more than 2.8 billion tonnes of high rank,premium anthracite coal in four deposits, also reflects exceptionalvalue. Today, in the wake of sharply higher prices for all coals,particularly metallurgical, this project alone is worth many times theCompany’s current market capitalization. Notably, ultra-low volatilepulverized coal injection (PCI) coal for the steel industry, the principalproduct we plan to produce at Klappan, has escalated to aboutUS$250/tonne,and premium anthracite charge carbon reductants haveappreciated to more than US$300/tonne, both up by more than 200%over last year’s prices, and a trend upon which the investment commu-nity is beginning to take note.

It is also worth remarking that Fortune’s third key project, the Sue-Dianne copper-silver deposit, located only 25 kilometres north ofNICO, has resources of just over 10 million tonnes containing 177million pounds of copper, 977,000 ounces of silver and 23,000ounces of gold. Again, copper and silver have escalated in value andwere recently selling at US$4/pound and US$18/ounce, respectively.

While the very high market prices being paid for virtually all ofthe commodities found at NICO, Mount Klappan and Sue-Dianne,may not be sustained over the long-term, many forecasters expectthat worldwide demand is likely to remain strong, supporting pricesthat are well above historical averages.Such market dynamics providea firm foundation for a substantial multiple of Fortune’s current shareprice and investment potential.

Corporately in 2007, Fortune increased its interest in NICO from90% to 100%, and as part of the same transaction, sold its non-coreFormosa industrial minerals project.The Company also closed a publicoffering of 9,550,000 units at $3.00 per unit for aggregate grossproceeds of $28,650,000, which included the issuance of 1,200,000units pursuant to the full exercise of the agents’ over-allotment option.The net proceeds of this offering are being used principally to fundthe further exploration, engineering and development of NICO; forenvironmental work, engineering and permitting activities at MountKlappan; and, for additional working capital to be used for generalcorporate purposes.

2007

ANNUAL REPORT I 9

Robin E. GoadPresident and CEO

George M. DoumetChairman

Since reporting to you a year ago, we have made several additionalimportant management appointments of highly experienced individualsto oversee critical areas of the Company’s operations.They include therecent appointment of James Currie to the position of Vice PresidentOperations to drive key engineering and development aspects for ourtwo proposed mine developments. Other notable appointments include:Michael Samuels – Process Development Manager; Andre Tricoteux –Procurement and Logistics Manager; Patrick Moloney – Manager ofHuman Resources; Dr. Richard Schryer, Manager of Regulatory Affairs;Nicole Hayduk – Contracts Administration Manager; and, Adam Jean– Controller. These well qualified professionals clearly reflect ourcommitment to continuing to fortify Fortune’s management team tohelp ensure we meet our development objectives. >

FORTUNE REMAINS FOCUSED,

DETERMINED AND STRONG, CONFIDENT

IN OUR EXCEPTIONAL ASSETS – BOTH HUMAN

AND MINERAL – AND OUR FIRM COMMITMENT

TO BECOMING A LEADING CANADIAN

MINING COMPANY.

2008Q1

2007200620052004

300

250

200

150

100

50

0

AVER

AGE

COAL

PRI

CES

US$

/ton

2008Q1

2007200620052004

3.60

3.00

2.40

1.80

1.20

0.60

0AVER

AGE

COPP

ER P

RICE

SU

S$/l

b.

2007

10 I FORTUNE MINERALS LIMITED

Early in 2007, Fortune received the long awaited positive results of itsfull bankable feasibility study for the proposed NICO development that was ledby Micon International Limited (Micon) and supported by several other engi-neering and metallurgical consultants. This assessment concluded that NICOshows attractive economics at conservative “base case” metal price assumptionsusing the two-year average prices of the contained metals in 2005 and 2006, andvery attractive economics at recent prices.As a result of the improved metallur-gical response achieved from flotation in the recent pilot plant test, Micon wasretained to provide a memorandum updating the economics for the NICO devel-opment using a variety of updated metal price sensitivities, current exchangerates,and reflecting the improved recoveries for flotation.Notably,at metal pricesof US$750 to $900/ounce of gold, US$20 to $50/pound of cobalt and US$10 to$16/pound of bismuth, the project generates, on a pre-tax basis, internal rates ofreturn (IRR) that range from 32.3% to 97.2% and 8% discounted net present val-ues (NPV) of $360.7 million to $1.5 billion. However, it should be noted thatthese updated economic sensitivities do not take into account any escalation inoperating or capital costs since the 2007 feasibility study was completed. Basedupon the positive findings in the definitive feasibility study as well as otherachievements, the Company announced plans to proceed with an environmen-tal assessment and permitting for the mine.This is being done in conjunctionwith a number of infrastructure initiatives, including collaboration with govern-ments on planned improvements to critical road access to the proposed mineand isolated Tlicho aboriginal communities.The Company is also pursuing a pow-erline connection to the electrical grid at the Snare hydro complex, 22 kilome-tres to the east of the mine.

The year also included a second $10-million program of underground testmining at NICO to assess the mining conditions and continuity of grade in thegold-rich, higher-grade, lower parts of the deposit, approximately 200 metresbeneath the surface.An “Alimak” raise was also driven to surface to provide ven-tilation for the underground workings and an emergency access. Although theobjective of this and other extensive underground work has been primarily forexploration purposes, most of the pre-production development for the under-ground part of the mine has now been completed as an added result.

Approximately 200 tonnes of ore mined during Phase 1 and 2 of the test min-ing program at NICO were shipped to SGS Lakefield Research Limited inLakefield, Ontario and blended to produce samples indicative of the ores theCompany expects to process during commercial operations at the proposedmine.This ore is being used in a six-month, large-scale, pilot plant test of the dif-ferent parts of the NICO process flow sheet, including crushing, grinding andflotation, as well as bismuth, cobalt and gold hydrometallurgical processing tohigh value metal end-products.The results of the flotation parts of the NICO pilotplant significantly improved predicted recoveries for all three metals, which hasindicated a very material improvement to the project’s economics. Thehydrometallurgical components of the pilot plant are expected to be completedMay 2008.

The Company is also moving ahead with preparations for the relocation toNICO of the Golden Giant Mine buildings, equipment and spare parts inventoryat Hemlo, Ontario, that were purchased in 2006 and 2008 for $3.3 million fromNewmont Canada Ltd.This purchase was made to materially reduce projected

REPORT TO SHAREHOLDERS

2008Q1

2007200620052004

1,050

875

700

525

350

175

0AV

ERAG

E GO

LD P

RICE

SU

S$/o

z.

2008Q1

2007200620052004

48

40

32

24

16

8

0AVER

AGE

COBA

LT P

RICE

SU

S$/l

b.

2008Q1

2007200620052004

15.00

12.50

10.00

7.50

5.00

2.50

0AVER

AGE

BISM

UTH

PRIC

ESU

S$/l

b.

GOLD

COBALT

BISMUTH

METALLURGICAL COAL

COPPER

2007

ANNUAL REPORT I 11

capital costs for the NICO project, but since acquiring the assets, theCompany has identified a wide range of recoverable metals, other highvalue materials, and surplus equipment that are being sold to generate asignificant source of income from the asset.

Meanwhile, Fortune achieved several advances at its wholly-ownedanthracite coal project at Mount Klappan in northwest British Columbiaduring the year in line with the Company’s dual-track efforts to advancethe project while also examining opportunities to bring in a significantpartner to help develop this asset. Fortune is involved in discussionswith several large international organizations interested in pursuingsome form of joint-partnership to develop our world class project.Mount Klappan is capable of producing a range of high value coal prod-ucts for global markets making the project a compelling investment forcompanies determined to find new sources of supply.

The Mount Klappan deposits straddle the B.C. Rail right-of-way andthe railway roadbed provides road access to Highway 37 and the portof Stewart. Track has also been installed to within 100 kilometres southof the proposed mine, providing a potential future rail link to the Portof Prince Rupert. While Fortune continued to complete engineeringand environmental surveys of the proposed mine, studies were alsoconducted to examine a number of alternatives to improve transporta-tion of coal products from the site to the ports. This included animproved truck haulage option to Stewart by utilizing large haul truckson the proposed short-cut road to be built between the site and a trans-fer facility to be located near Bell II together with the use of larger high-way compliant trucks between this transfer facility and Stewart. Thesetrucks would be larger than were contemplated by Marston CanadaLtd. (Marston) in their 2005 full bankable feasibility study for Klappan.In addition, a number of options have been examined for improvingthe storage and loading of coal at the port of Stewart.At the same time,Fortune also commissioned a study from Marston and Pipeline SystemsInc. to examine the merits of transporting coal from Klappan toStewart or Prince Rupert using a slurry pipeline.All of these studies arenearing completion and the Company expects to announce the

favoured transportation alternative in conjunction with a proposedexpansion of production from 1.5 to 3 million tonnes of clean coal perannum.

Further, a feasibility study completed in 2007 concerning a poten-tial Alaska - Canada Rail Link was jointly funded by the State of Alaskaand Yukon Territory. This study recommends a railway connectionfrom Alaska through the Yukon and northern British Columbia, to thecontinental United States that would include a segment running pastMount Klappan.The study also recommends a short-cut that woulddramatically reduce the rail haulage distance of coal products fromMount Klappan to Prince Rupert from 1,400 kilometres to just over600 kilometres and materially reduce transportation costs.Althoughan attractive scenario for transportation of products from Klappan,such a railway initiative is unlikely to be available for timely develop-ment of the mine.

Meanwhile, the Company continued to advance the environmentalassessment for the mine by submitting its Terms of Reference for pub-lic, regulatory and First Nation comment for a truck haulage option tothe port of Stewart.

2007 and early 2008 have been marked by progress and strengthen-ing of our relationships with First Nations people at both NICO andMount Klappan,where we have worked closely with representatives ofboth the Tlicho and Tahltan communities. Our focus has been on com-pleting agreements that promote a clearer understanding of our busi-ness and plans, as well as on developing suitable business, infrastruc-ture and employment opportunities for members of these and othernearby communities. In every case, we are looking to tangibly demon-strate our commitment to contributing positively to the people livingin the region, providing potential benefits from each project, respect-ing local societies and minimizing impacts on the environment.At thesame time, we continue to build critical, open relationships with gov-ernment regulators and other involved stakeholders.

Looking back over the past year, we are very pleased with the oper-ational, corporate, financial, and personnel progress that has beenaccomplished and we continue to be encouraged by the price anddemand trends evident throughout our most important commoditymarkets. The Company’s Board of Directors, executive managementand operational team remain confident in our plans to develop theexceptional properties that underpin Fortune’s true value. We movesteadily closer to our goal of becoming a successful minerals producer.

George Doumet, Robin Goad,Chairman President and C.E.O.

THE GLOBAL DEMAND AND

MARKET PRICES FOR THE KEY

COMMODITIES CONTAINED IN OUR

DEPOSITS CONTINUE TO TREND HIGHER,

WIDELY ACHIEVING NEAR RECORD AND

EVEN UNPRECEDENTED LEVELS.

Base case metal prices for bankable feasibility studies.

In the coal prices graph: ULV PCI Coking Coal

2007

12 I FORTUNE MINERALS LIMITED

NICOCOBALT-GOLD-BISMUTH PROJECT

Introduction:

Fortune’s 100%-owned NICO project in Canada’s Northwest Territories contains a

near-surface deposit of cobalt, gold and bismuth, which is targeted for production

in late 2010. NICO is located 160 kilometres northwest of the City of Yellowknife,

the regional centre of government and an existing mining community. The leas-

es containing the deposit are located on Tlicho lands, 50 kilometres north of the

community of Wha Ti and 85 kilometres north of Behchoko and Highway 3 to

Edmonton, Alberta. Current access to NICO is from a government winter road,

which passes within 6 kilometres of the property and has been extended to the

site. The governments of Canada, the Northwest Territories and Tlicho, together

with private industry, are planning to re-align and upgrade this to an all-season

road for which consultation, engineering and environmental work are now

underway.NICO is only 22 kilometres west of the Snare hydro complex, which the

Northwest Territories Power Corp.is planning to expand.Fortune intends to estab-

lish a connection to this electrical grid for the proposed NICO mine.

2007

ANNUAL REPORT I 13

BELOW: 2007 NICO mine site showing portal, service complex,

waste rock dumps and ore stockpiles.

2007

14 I FORTUNE MINERALS LIMITED

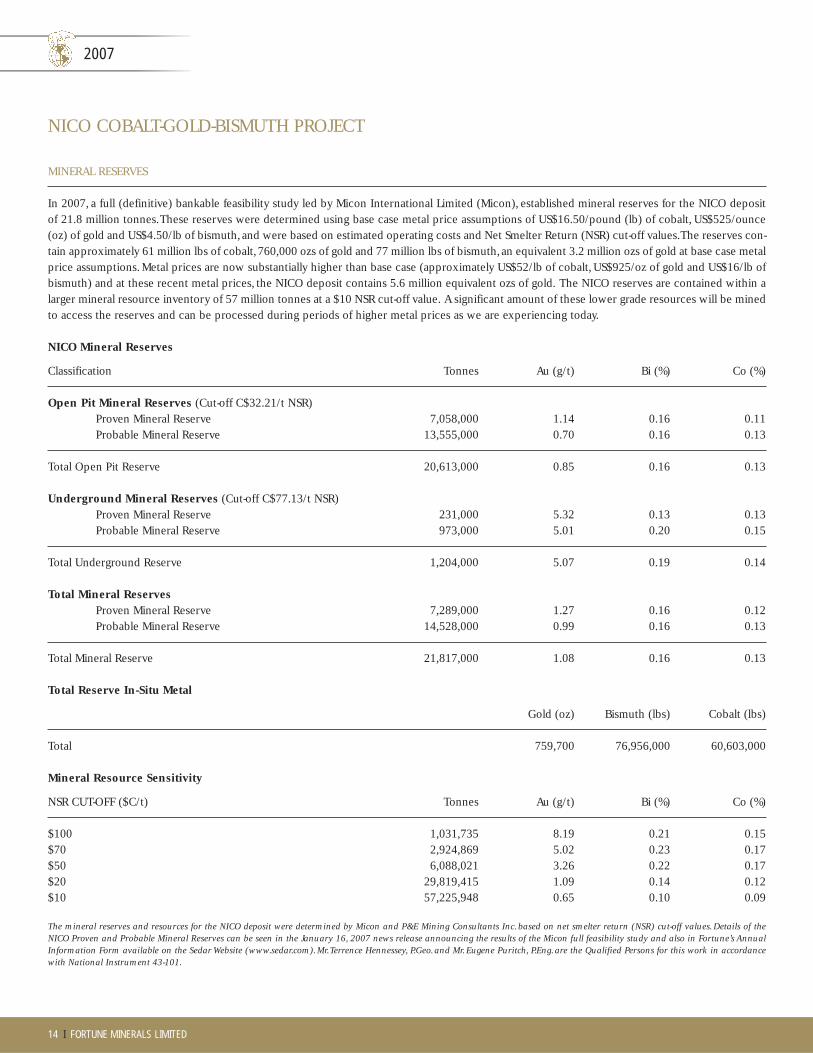

MINERAL RESERVES

In 2007, a full (definitive) bankable feasibility study led by Micon International Limited (Micon), established mineral reserves for the NICO depositof 21.8 million tonnes.These reserves were determined using base case metal price assumptions of US$16.50/pound (lb) of cobalt, US$525/ounce(oz) of gold and US$4.50/lb of bismuth,and were based on estimated operating costs and Net Smelter Return (NSR) cut-off values.The reserves con-tain approximately 61 million lbs of cobalt,760,000 ozs of gold and 77 million lbs of bismuth,an equivalent 3.2 million ozs of gold at base case metalprice assumptions. Metal prices are now substantially higher than base case (approximately US$52/lb of cobalt, US$925/oz of gold and US$16/lb ofbismuth) and at these recent metal prices, the NICO deposit contains 5.6 million equivalent ozs of gold. The NICO reserves are contained within alarger mineral resource inventory of 57 million tonnes at a $10 NSR cut-off value. A significant amount of these lower grade resources will be minedto access the reserves and can be processed during periods of higher metal prices as we are experiencing today.

NICO Mineral Reserves

Classification Tonnes Au (g/t) Bi (%) Co (%)

Open Pit Mineral Reserves (Cut-off C$32.21/t NSR)Proven Mineral Reserve 7,058,000 1.14 0.16 0.11Probable Mineral Reserve 13,555,000 0.70 0.16 0.13

Total Open Pit Reserve 20,613,000 0.85 0.16 0.13

Underground Mineral Reserves (Cut-off C$77.13/t NSR)Proven Mineral Reserve 231,000 5.32 0.13 0.13Probable Mineral Reserve 973,000 5.01 0.20 0.15

Total Underground Reserve 1,204,000 5.07 0.19 0.14

Total Mineral Reserves Proven Mineral Reserve 7,289,000 1.27 0.16 0.12Probable Mineral Reserve 14,528,000 0.99 0.16 0.13

Total Mineral Reserve 21,817,000 1.08 0.16 0.13

Total Reserve In-Situ Metal

Gold (oz) Bismuth (lbs) Cobalt (lbs)

Total 759,700 76,956,000 60,603,000

Mineral Resource Sensitivity

NSR CUT-OFF ($C/t) Tonnes Au (g/t) Bi (%) Co (%)

$100 1,031,735 8.19 0.21 0.15$70 2,924,869 5.02 0.23 0.17$50 6,088,021 3.26 0.22 0.17$20 29,819,415 1.09 0.14 0.12$10 57,225,948 0.65 0.10 0.09

The mineral reserves and resources for the NICO deposit were determined by Micon and P&E Mining Consultants Inc. based on net smelter return (NSR) cut-off values. Details of theNICO Proven and Probable Mineral Reserves can be seen in the January 16, 2007 news release announcing the results of the Micon full feasibility study and also in Fortune’s AnnualInformation Form available on the Sedar Website (www.sedar.com). Mr.Terrence Hennessey, P.Geo. and Mr. Eugene Puritch, P.Eng. are the Qualified Persons for this work in accordancewith National Instrument 43-101.

NICO COBALT-GOLD-BISMUTH PROJECT

2007

ANNUAL REPORT I 15

BANKABLE FEASIBILITY STUDY

The Micon full feasibility study for the NICO development was released in January 2007 and concluded that the project shows attractive econom-ics at base case metal price assumptions and very attractive economics at the higher prices paid for these metals since the study was completed. Inaddition to Micon, this study involved a number of other engineering companies retained to work on specific parts of the project, including Met-Chem Canada Inc., Golder Associates Ltd, P&E Mining Consultants Inc., EBA Engineering Ltd, KVK Consulting Associates Inc. and EHA EngineeringLtd.The feasibility study was a comprehensive engineering, economic, social and environmental evaluation of the project’s viability.Typically pre-pared to +/- 15% precision, such studies are normally used by financial institutions to assess the credit worthiness of a proposed development.Thefeasibility study used the two-year trailing average prices for metals as at January 2007 as base case (US$ 16.50/lb of cobalt, US$525/oz of gold, andUS$ 4.50/lb of bismuth) and an exchange rate of US$0.84:C$1.00.

At the time this Annual Report was being prepared (April 2008),prices for these metals had increased to US$52/lb of cobalt,US$925/oz of gold, andUS$16/lb of bismuth and the exchange rate was US$0.97/C$1.00. Fortune retained Micon to prepare a memorandum to assess the impact on NICOproject economics as a result of the current Canadian dollar exchange rate, the higher metal prices at the present time as well as various metal pricesensitivities, and also taking into account the higher metal recoveries from flotation that were attained in its SGS Lakefield Research Limited (SGSLakefield) pilot plant results achieved to date. No increases in operating or capital costs are being included in these revised estimates.

The feasibility study results and updated economics for a number of metal price sensitivities are as follows:

2007 Feasibility 2007 Study Base Updated Base

Feasibility Study Case1 – new Case1,2 – higher Economics usingBase Case flotation results metal prices Current Prices1,2

Metal Price Assumptions3 $525/$16.50/$4.50 $525/$16.50/$4.50 $750/$20/$10 $900/$50/$16Exchange Rate Assumptions US$0.84 = C$1 US$0.84 = C$1 US$0.97 = C$1 US$0.97 = C$18% discounted Net Present Value (NPV) C$ 91.8 million C$ 143.7 million C$ 360.7 million C$ 1.5 billionPre-tax Internal Rate of Return (IRR) 15.3% 18.3% 32.3% 97.2%Annual Gold Production - years 1 & 2 69,000 oz. 70,000 oz. 70,000 oz. 70,000 oz.Annual Gold Production - years 3 to 15 24,000 oz. 24,000 oz. 24,000 oz. 24,000 oz.Annual Cobalt Production - 99.8% cobalt cathode 3.25 million lbs. 3.46 million lbs. 3.46 million lbs. 3.46 million lbs.Annual Bismuth Output4 3.23 million lbs. 3.59 million lbs. 3.59 million lbs. 3.59 million lbs.Initial Capital Costs C$ 215.2 million C$ 215.2 million C$ 215.2 million C$ 215.2 millionAverage Production Cash Costs –

Cobalt (net of by-product credits) US$ 7.05/lb. US$ 6.34/lb. US$ 1.41/lb. US$ (5.51)/lb.Average Production Cash Costs –

per equivalent gold ounce US$ 321/oz. US$ 304/oz. US$ 349/oz. US$ 203/oz.

1 The results of recent pilot plant testing with the fresh ore bulk sample showed improved metallurgical response, compared with the earlier, small scale testing conducted with drillcore samples and on which the feasibility study was based.The recovery levels to final products predicted from the pilot plant results, compared with the recovery values used inthe feasibility study, are improved for all three economic metals.The new calculated recoveries for life-of-mine production for cobalt and bismuth are respectively 5% and 6% high-er than in the 2007 feasibility study, while gold recovery is close to 1% higher.

2 Update economics are based on the operating and capital cost estimates from the 2007 feasibility study and have not been adjusted for inflation and well known recent cost esca-lations prevalent in the industry. To assess possible cost increases, refer to the following sensitivity analysis:

(i) For a $25 million increase in life-of-mine capital, NPV is reduced by $17.0 million and $8.2 million for the two scenarios presented, respectively;(ii) For a 10% increase in operating costs, NPV is reduced by $36.8 million and $35.9 million for the two scenarios presented, respectively.

3 US$ per ounce of gold / US$ per pound of cobalt / US$ per pound of bismuth.

4 Bankable feasibility study assumed production of 45% bismuth concentrate, but current plans are to produce 90% bismuth cement.

2007

16 I FORTUNE MINERALS LIMITED

NICO COBALT-GOLD-BISMUTH PROJECT

NICO LAKE

PEANUT LAKE

GRID POND

PONDLITTLE GRID

ABOVE: 3-dimensional view of the proposed NICO mine.

RIGHT: Plan of the minesite, open pit and waste rock and

tailings impoundment areas.

2007

ANNUAL REPORT I 17

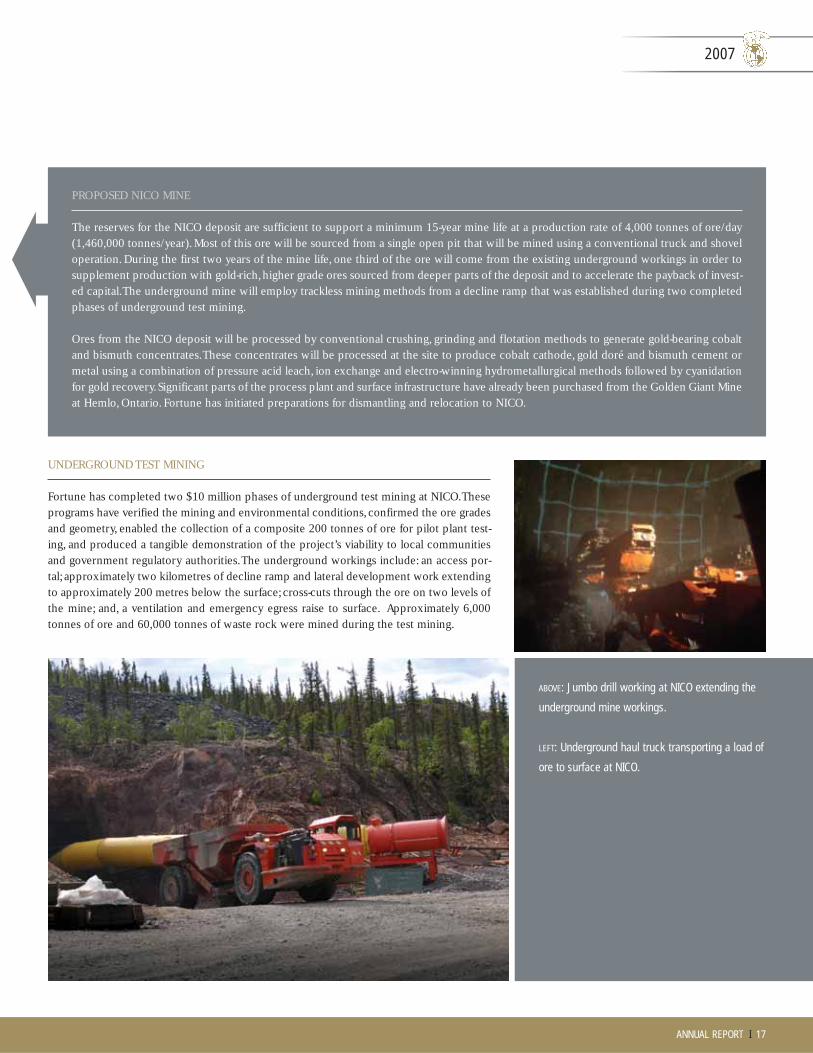

UNDERGROUND TEST MINING

Fortune has completed two $10 million phases of underground test mining at NICO.Theseprograms have verified the mining and environmental conditions,confirmed the ore gradesand geometry, enabled the collection of a composite 200 tonnes of ore for pilot plant test-ing, and produced a tangible demonstration of the project’s viability to local communitiesand government regulatory authorities.The underground workings include: an access por-tal; approximately two kilometres of decline ramp and lateral development work extendingto approximately 200 metres below the surface;cross-cuts through the ore on two levels ofthe mine; and, a ventilation and emergency egress raise to surface. Approximately 6,000tonnes of ore and 60,000 tonnes of waste rock were mined during the test mining.

PROPOSED NICO MINE

The reserves for the NICO deposit are sufficient to support a minimum 15-year mine life at a production rate of 4,000 tonnes of ore/day(1,460,000 tonnes/year). Most of this ore will be sourced from a single open pit that will be mined using a conventional truck and shoveloperation. During the first two years of the mine life, one third of the ore will come from the existing underground workings in order tosupplement production with gold-rich,higher grade ores sourced from deeper parts of the deposit and to accelerate the payback of invest-ed capital.The underground mine will employ trackless mining methods from a decline ramp that was established during two completedphases of underground test mining.

Ores from the NICO deposit will be processed by conventional crushing, grinding and flotation methods to generate gold-bearing cobaltand bismuth concentrates.These concentrates will be processed at the site to produce cobalt cathode, gold doré and bismuth cement ormetal using a combination of pressure acid leach, ion exchange and electro-winning hydrometallurgical methods followed by cyanidationfor gold recovery.Significant parts of the process plant and surface infrastructure have already been purchased from the Golden Giant Mineat Hemlo, Ontario. Fortune has initiated preparations for dismantling and relocation to NICO.

ABOVE: Jumbo drill working at NICO extending the

underground mine workings.

LEFT: Underground haul truck transporting a load of

ore to surface at NICO.

2007

18 I FORTUNE MINERALS LIMITED

GOLDEN GIANT MINE, HEMLO, ONTARIO

Fortune is moving ahead with plans to relocate Hemlo’s Golden GiantMine mill, surface facilities, equipment and spare parts inventory toNICO. The Company acquired these assets in 2006 from NewmontCanada Ltd. for $3.3 million and recently purchased additional assets atGolden Giant,which collectively will significantly reduce projected cap-ital costs for NICO’s development.The Company has begun to salvagehigh value process, electrical and technical equipment for relocation toa staging site for reconditioning and transport to NICO after receipt ofapplicable permits. Fortune is also assembling the surplus equipmentand has begun selling it on the used equipment market. Fortune hasidentified certain amounts of gold, silver and other valuable metals thatare contained in materials and residues within certain equipment at themine. These materials and residues will be collected and the metalsrecovered and sold to generate revenue from these assets.Fortune is fur-ther reducing its net cost of dismantling the facilities through theplanned collection of other high value materials, including stainless andstructural steels, aluminum, copper and other metals, which theCompany will sell for scrap. Fortune is building a team of internal peo-ple, contractors and suppliers to continue the planning for the salvageand sale of materials and equipment, as well as for the dismantling andrelocation of the mill and equipment needed at the NICO site. Fortuneis not responsible for environmental liabilities at the Hemlo site otherthan to remove the acquired assets to their foundations.

ENGINEERING, ENVIRONMENTAL ASSESSMENT AND PERMITTING

Fortune has begun a number of activities related to engineering and permitting for the NICO development. This includes retaining AkerKvaerner E&C, a division of Aker Kvaerner Canada Inc. to prepare aMETSIM® model for the processing of NICO ores based on the metallur-gical flow sheet developed in the Micon definitive feasibility study. AkerKvaerner was also contracted to conduct a logistics and transportationstudy for the future construction of the NICO project and recentlyentered into an agreement with Fortune to conduct Front-End Engineer-ing and Design (FEED) for the mine.

Fortune has filed its requisite land use and water license applicationswith the Wek’ èezhi’i Land and Water Board. It has also entered into dis-cussions with the Tlicho Government with respect to access as well asImpacts and Benefits agreements. During 2007, Fortune, GolderAssociates Ltd. and representatives of the Tlicho First Nation, continuedwork on environmental baseline studies at NICO in preparation for theenvironmental assessment (EA) process in 2008. Since 1997, work hasincluded aquatic, vegetation and wildlife biology surveys, hydrology,hydrogeology, geochemistry, meteorology, archaeology, socio-economicand traditional use studies that will be used to assess potential impactsof the project and develop mitigation strategies to minimize any effectto the local environment. Environmental test work has also been con-ducted at SGS Lakefield examining the waste products that would beproduced from the NICO process plant.Fortune is targeting commence-ment of production at NICO in late 2010.

NICO COBALT-GOLD-BISMUTH PROJECT

PILOT PLANT

Fortune is conducting a $4-million pilot plant at SGS Lakefield Research in Ontario to test the processing of ores from the NICO deposit.The pilot plant will provide a model for detailed engineering and planning for the NICO process plant, and will confirm process condi-tions, metal recoveries and the metallurgical flow sheet.Approximately 200 tonnes of ore from the NICO deposit has been delivered toLakefield, and the crushing, grinding and flotation components have been completed.Test runs for the downstream hydrometallurgicalcomponents of the process plant, including pressure acid leach tests of the cobalt and bismuth concentrates,have also been completed inpreparation for the major hydrometallurgical components of the pilot scheduled to be conducted in April 2008.

Notably, results of the flotation work have determined that recoveries from flotation will be significantly higher than the recoveries usedin the Micon feasibility study and will have a significant positive impact on project economics.The new calculated recoveries for life-of-mine production for cobalt and bismuth are respectivey 5% and 6% higher than in the 2007 feasibility study, while gold recovery is closeto 1% higher. A number of other qualitative improvements were achieved in the pilot plant, including confirmation of work indexes,quickrecovery of the process after upsets, and verification of the use of a high percentage of re-cycled process water.The hydrometallurgicalcomponents of the pilot plant are expected to be completed in May 2008.

2007

ANNUAL REPORT I 19

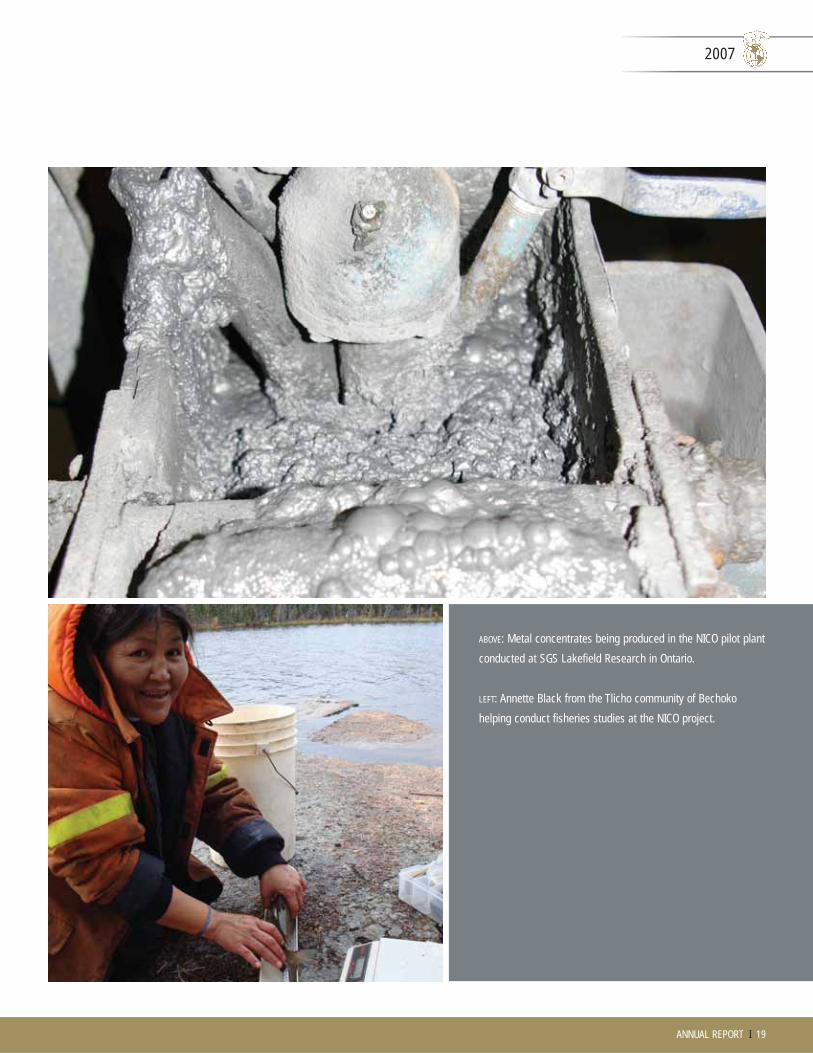

ABOVE: Metal concentrates being produced in the NICO pilot plant

conducted at SGS Lakefield Research in Ontario.

LEFT: Annette Black from the Tlicho community of Bechoko

helping conduct fisheries studies at the NICO project.

2007

20 I FORTUNE MINERALS LIMITED

NICO METAL MARKETS

NICO contains significant amounts of cobalt, gold and is alsoone of the world’s largest bismuth deposits. Cobalt is the domi-nant metal, by value, in the deposit and is a high-strength, mag-netic metal, which has seen a relatively steady 20-year increasein demand driven by a number of traditional and new chemicaland metallurgical applications.The greatest market growth hasbeen in chemicals, primarily for the manufacture of recharge-able batteries and catalysts. As consumers’ need has grown forportable electronic products, cellular telephones, computers,power tools, MP3 players, toys and other electronic devices, sodoes the market for high performance rechargeable batteries,primarily, cobalt bearing nickel metal hydride and lithium ionbatteries.Approximately five pounds of cobalt is also containedin the batteries used to power hybrid-electric vehicles whosepopularity is growing in step with concerns over fuel costs andthe environment.Cobalt catalysts are also required in petroleumrefining, liquid natural gas and the manufacture of automobiletires and plastics. Metallurgical uses for cobalt include super-alloys for the aerospace industry, cutting tools, cemented car-bides and industrial magnets. There are still more markets forcobalt in food additives (vitamin B12), pigments and audiorecording tape. In 2007, the cobalt market consumed approxi-mately 65,000 tonnes, double the consumption of eight yearsago. Consumption is expected to double again to 120,000tonnes in the next few years, particularly as a result of its newapplications and Asian economic growth,primarily in China andIndia. Today, the price for 99.8% cobalt metal is more than US$50/lb compared with historical long-term averages of betweenUS$15 and US$20/lb.

NICO COBALT-GOLD-BISMUTH PROJECT

BATTERIES - 23%

PIGMENTS - 9%

RECORDING MATERIALS - 2%

ADHESIVES & DRYERS - 8%

SUPERALLOYS - 21%

CATALYSTS - 11%

MAGNETS - 7%

HARDFACING ALLOYS - 8%

CARBIDES - 11% 20072006200520042003

70

60

50

40

30

20

10

0

COBA

LT M

ARKE

TT

hou

sand

s of

Ton

nes

COBALT USES

BELOW: Cobalt lithium ion and nickel metal hydride batteries are used to

power personal portable electronic devices and hybrid-electric vehicles.

Cobalt catalysts are used to manufacture radial tires.

2007

ANNUAL REPORT I 21

20072006200520042003

18

15

12

9

6

3

0

BISM

UTH

MAR

KET

Th

ousa

nds

of T

onne

s

METALLURGICAL - 26.4%(Steel, Free Cutting,

Greases)

FUSIBLE ALLOYS - 8.8%(LMPA, Solder)

OTHERS - 7.6%

CHEMICALS - 57.2%(Electronics, Lead

Oxide Replacement,Pharma, Pigments,

Misc. Chemicals)

BISMUTH USES

Although not widely known by investors, bismuth is a relativelyuncommon and inert metal, recognized by scientists as one of thesafest metals on the periodic table.This makes it ideal for numerouspharmaceuticals and medicines, including Pepto-Bismol™, as well asbandage dressings, cosmetics, and medical devices. Bismuth’s otherunusual properties include its very high density, low melting temper-ature,and the fact that,like water,it expands upon solidification (cool-ing), making it ideally suited for a variety of chemicals and fusiblealloys, particularly dimensionally stable alloys and compounds. Bis-muth is unique as it has physical properties similar to lead, but it isnon-toxic. As a result of increasing health and environmental con-cerns,bismuth is replacing lead in a number of applications includingin solders for plumbing and electronics, as well as in brasses, alloysused in hot-dip galvanizing, paint pigments, ammunition, radiationshielding and free-cutting steel. Bismuth consumption, which wasabout 15,000 tonnes in 2007, has been growing at a rate of between10% and 15% in each of the past five years. Again,much of this grow-ing demand has come from Asia. However, supply constraints haveheld back the bismuth market, an issue being exacerbated by the factthat most bismuth production comes as a by-product from lead min-ing.Thus, as lead consumption is constrained by concerns over toxi-city,bismuth is expected to remain in tight supply.Bismuth is current-ly selling for about US$ 16/lb, compared with just under US$5/lb in2006.

Gold is also an important co-product at NICO. In the past year,prices for gold have increased by 50%, rising from approximatelyUS$650/oz to over US$1,000/oz in April 2008. Although there is awide range of forecasts for the price of gold in the future, almost allagree that a combination of geo-political uncertainties are drivinginvestors to gold as a store of wealth.This coupled with increasingdemand in jewellery and industrial uses are likely to sustain recentprices for many years to come.

BELOW: Bismuth is the active ingredient in Pepto-Bismol™ and other

medicines, but growth in the market is primarily as a non-toxic

replacement for lead in various products, including paint pigments

and solders for plumbing and electronics.

2007

22 I FORTUNE MINERALS LIMITED

MOUNT KLAPPANANTHRACITE COAL PROJECT

Introduction:

Fortune’s coal licenses cover more than 150 square kilometres in Tahltan traditional

territory in northwest British Columbia and host the “World Class” Mount Klappan

anthracite coal project. Fortune is actively proceeding towards developing an open

pit mine, wash plant and site infrastructure at Klappan to produce ultra-low volatile,

pulverized coal injection (PCI) product for the overseas steel industry. At the same

time, the Company is considering various strategic alternatives for the development

of the project. In addition to ongoing baseline environmental data collection activi-

ties and the continuation of the environmental assessment (EA) process, Fortune is

examining a number of potential infrastructure options that could materially

improve the economics of the project. Fortune is targeting the start-up of production

for Mount Klappan at the end of 2010. Fortune’s licenses straddle the B.C. Railway

right-of-way, 150 kilometres northeast of the port of Stewart and 330 kilometres

northeast of the port of Prince Rupert. The railway roadbed provides road access to

the site from Highway 37 and track has been installed south of the project to within

100 kilometres of the proposed mine.

2007

ANNUAL REPORT I 23

BELOW: 3-dimensional conceptual model of the proposed

Lost-Fox mine at Mount Klappan looking west from the

B.C. Railway right-of-way.

2007

24 I FORTUNE MINERALS LIMITED

MOUNT KLAPPAN RESOURCES AND RESERVES

Mount Klappan is one of the largest undeveloped resources of high rank anthracite coal in the world.In 2002,Marston Canada Ltd.(Marston) estimated Klappan’s four resource areas – the Lost-Fox,Hobbit-Broatch,Sumittand Nass deposits – contain more than 2.8 billion tonnes of in-situ coal resources of which 108 million tonnesare classified as Measured, 123 million tonnes as Indicated, and 2.6 billion tonnes are in the Inferred andSpeculative classes. In 2005, Marston updated the resources for the Lost-Fox deposit area. Marston alsoassessed the deposit in an updated full Bankable Feasibility Study (2005 BFS) later that year verifying Provenand Probable Reserves of 102 million tonnes of in-situ coal that would produce 60 million product tonnes ofultra-low volatile PCI metallurgical coal for the overseas steel industry. The feasibility study concluded attrac-tive rates of return for the development under a variety of production and coal price scenarios that wouldsupport a minimum 20 year mine-life at a production rate of 3 million tonnes/year.In 2007,Marston also com-pleted a pre-feasibility economic assessment of a thermal coal option for the Lost-Fox deposit at MountKlappan.This study identified reserves of 106 million in-situ tonnes that would support a minimum 25-yearmine life at an annual production rate of 1.1 million tonnes/year of thermal coal and 124,000 tonnes/year ofa premium metallurgical charge carbon by-product.

MOUNT KLAPPAN RESOURCES

Area Measured Indicated Demonstrated Inferred Speculative(MT) (MT) (MT) (MT) (MT)

Lost-Fox 107.9 109.5 217.4 91.5 749.6Hobbit-Broatch – 13.5 13.5 258.4 753.0Summit – – – 9.6 508.9Nass – – – – 201.5

Total 107.9 123.0 230.9 359.5 2,213.0

LOST-FOX METALLURGICAL COAL RESERVES

In Situ Coal Reserves (MT) 10% Ash Product Reserves (MT)Proven Probable Total In-Situ Proven Probable Total Product

85.6 16.1 101.7 51.6 9.2 60.8

LOST-FOX THERMAL COAL RESERVES

ROM Coal Reserves (MT)Proven Probable Total Reserves (MT) ROM Coal Strip Ratio (Bcm/t)

89.5 16.8 106.3 6.6 - life of mine (5.9 - 1st 25 yrs)

MT = millions of tonnes ROM = Run-of-MineBcm/t = bank cubic metres/tonne

The Mount Klappan mineral resource and mineral reserve estimates were prepared in 2002, 2005, and 2007, respectively, by Marston Canada Ltd. in compliance with NationalInstrument 43-101.Richard Marston, P.E. is the Qualified Person responsible for the estimates.For further information on the details of these estimates, please refer to the Company’s dis-closures on the Sedar website at www.sedar.com.

MOUNT KLAPPAN ANTHRACITE COAL PROJECT

2007

ANNUAL REPORT I 25

ABOVE: Mount Klappan pilot plant conducted by Gulf Canada in

1985-86. 100,000 tonnes of anthracite products were produced

for trial cargos to select customers in North America, Asia and

Europe.

LEFT: Test mining the “I-Seam” in the Lost-Fox deposit in

1985-86.

2007

26 I FORTUNE MINERALS LIMITED

3-dimensional model (above) and plan view (right) of

the proposed Lost-Fox open pit, waste dumps and site

infrastructure at Mount Klappan.

MOUNT KLAPPAN ANTHRACITE COAL PROJECT

2007

ANNUAL REPORT I 27

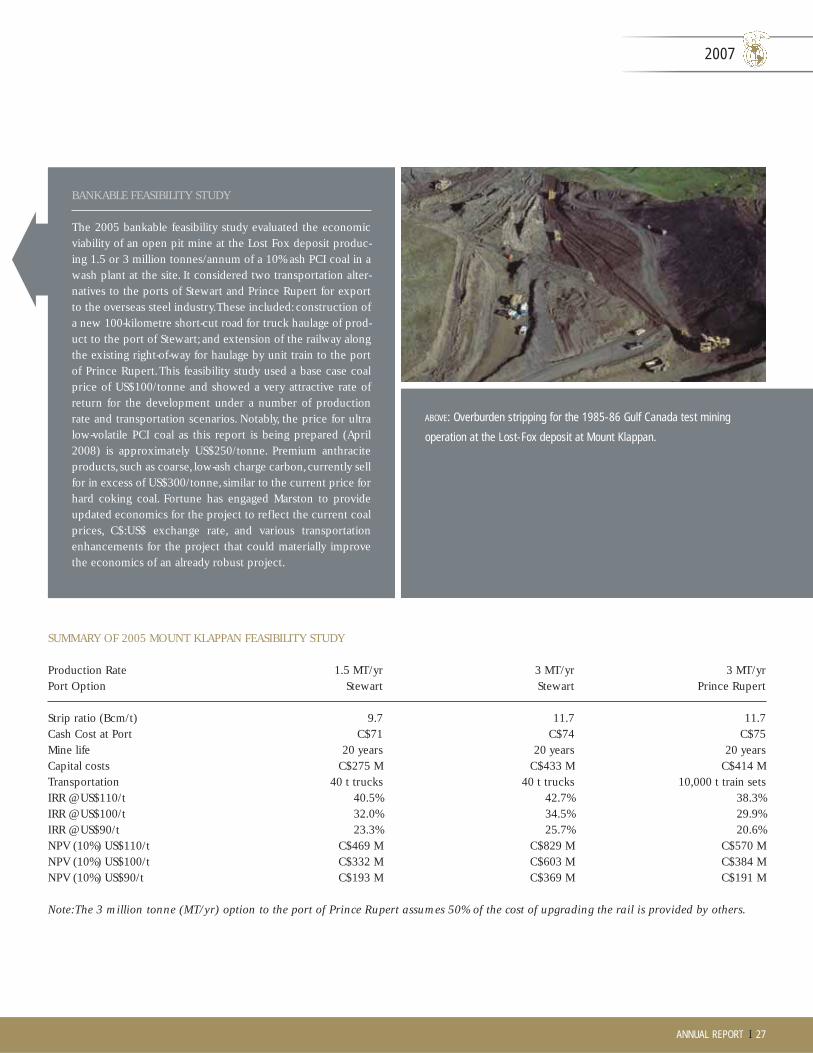

SUMMARY OF 2005 MOUNT KLAPPAN FEASIBILITY STUDY

Production Rate 1.5 MT/yr 3 MT/yr 3 MT/yrPort Option Stewart Stewart Prince Rupert

Strip ratio (Bcm/t) 9.7 11.7 11.7Cash Cost at Port C$71 C$74 C$75Mine life 20 years 20 years 20 yearsCapital costs C$275 M C$433 M C$414 MTransportation 40 t trucks 40 t trucks 10,000 t train setsIRR @ US$110/t 40.5% 42.7% 38.3%IRR @ US$100/t 32.0% 34.5% 29.9%IRR @ US$90/t 23.3% 25.7% 20.6%NPV (10%) US$110/t C$469 M C$829 M C$570 MNPV (10%) US$100/t C$332 M C$603 M C$384 MNPV (10%) US$90/t C$193 M C$369 M C$191 M

Note:The 3 million tonne (MT/yr) option to the port of Prince Rupert assumes 50% of the cost of upgrading the rail is provided by others.

BANKABLE FEASIBILITY STUDY

The 2005 bankable feasibility study evaluated the economicviability of an open pit mine at the Lost Fox deposit produc-ing 1.5 or 3 million tonnes/annum of a 10% ash PCI coal in awash plant at the site. It considered two transportation alter-natives to the ports of Stewart and Prince Rupert for exportto the overseas steel industry.These included: construction ofa new 100-kilometre short-cut road for truck haulage of prod-uct to the port of Stewart; and extension of the railway alongthe existing right-of-way for haulage by unit train to the portof Prince Rupert.This feasibility study used a base case coalprice of US$100/tonne and showed a very attractive rate ofreturn for the development under a number of productionrate and transportation scenarios. Notably, the price for ultralow-volatile PCI coal as this report is being prepared (April2008) is approximately US$250/tonne. Premium anthraciteproducts, such as coarse, low-ash charge carbon,currently sellfor in excess of US$300/tonne, similar to the current price forhard coking coal. Fortune has engaged Marston to provideupdated economics for the project to reflect the current coalprices, C$:US$ exchange rate, and various transportationenhancements for the project that could materially improvethe economics of an already robust project.

ABOVE: Overburden stripping for the 1985-86 Gulf Canada test mining

operation at the Lost-Fox deposit at Mount Klappan.

2007

28 I FORTUNE MINERALS LIMITED

ANTHRACITE MARKET

Anthracite is a high rank,high quality,premium coal with very high carbon and energy content combined with the lowest moisture and volatile con-tent compared to other types of coal. Anthracite deposits account for only about 1% of world coal reserves, making it relatively scarce. Its uniqueproperties make anthracite suitable for use in a broad range of premium metallurgical, thermal, water purification and composite materials applica-tions. In addition, it is used for fuels to manufacture cement and generate electricity.

World annual production of anthracite is approximately 400 million tonnes,most of which is consumed locally for power generation.Notably,Chinaproduces half of the world’s anthracite and, as a result of increasing domestic steel production and power generation, has recently become a netimporter.Vietnam, the world’s second largest producer, has also recently started curtailing exports in order to satisfy their own domestic energyrequirements. These export reductions,combined with increasing global consumption, are restricting supply in traditional markets in other parts ofAsia as well as Europe and North and South America. There are only three significant new anthracite projects in the development stream: MountKlappan plus one in each of Russia and China. Due to growing domestic consumption in Russia and China, it is unlikely production from thesedeposits will supply the export metallurgical coal market. Consequently, Mount Klappan is well positioned to service the growing global demand.Prices for anthracite products have been increasing and currently range from US$100 to more than US$300/tonne. Metallurgical products currentlysell for between US$125 and more than US$300/tonne and filter media commands a similar US$300/tonne price.

Anthracite use is growing in a number of metallurgical applications.The largest growth in the market is as a source of carbon and energy in pulver-ized coal injection (PCI) products used in the steel industry. Coal injection of finely powdered coal sprayed directly into the blast furnace reducesthe consumption of coke, making it a more efficient and cost effective method of manufacturing steel over conventional blast furnace technology.Injection processes favour the high carbon and low volatile content of anthracite, which allows for higher injection rates over PCI products pro-duced from lower rank and higher volatile content bituminous coals.The natural high carbon content of anthracite also makes it suitable for use asa blend coal to reduce consumption of coke in conventional steel industry blast furnaces.The global steel industry also uses anthracite for its sinter-ing plants and as a binding agent to make iron ore pellets. Coarse, low-ash anthracite is used as a reductant in aluminium and titanium processingand as charge carbon used in electric arc furnace steel manufacturing processes.Sized,low-ash anthracite is also used to make carbon filters for waterpurification and carbon composite materials.

Mount Klappan Clean Coal Quality – 10% Ash PCI Product

Specification (air dried basis) Mean

Residual Moisture 0.9%Ash 10%Volatile Matter 6.5%Fixed Carbon 82.6%Sulphur 0.5%Gross Calorific Value 31.1 GJ/tGross Calorific Value 7,423 Kcal.KgGross Calorific Value 13,352 Btu/lbHGI 40-45Size 0-50 mm

MOUNT KLAPPAN ANTHRACITE COAL PROJECT

Thermal uses for anthracite include smokeless fuels used forspace heating, the manufacture of heating and cooking bri-quettes and kiln fuels used to make cement and lime.Approximately 40% of the world's electricity is generated fromcoal-fired thermal power plants, many of which are configuredto burn anthracite. Notably, anthracite is a preferred fuel sourcefor new “clean coal” technologies for power generation thatreduce greenhouse gas emissions by gasification of coal priorto combustion.The high cost of oil is also making gasificationand coal-to-oil liquefaction technologies economically attrac-tive.This technology has been used for decades to make supe-rior quality synthetic diesel and jet fuels in South Africa andnew plants are now being constructed in China, the U.S.A. andother parts of the world. Notably, a recent study prepared bythe Massachusetts Institute of Technology on the future of coalconcluded that its use is inevitable and will increase for bothpower consumption and as an alternative source of syntheticfuels. It also concluded that carbon capture and geologicsequestration of greenhouse gasses will likely be necessary inthe future, and even with the additional related costs, will becheaper and represents a more secure source of energy supplythan other fossil fuels including oil and natural gas.

2007

ANNUAL REPORT I 29

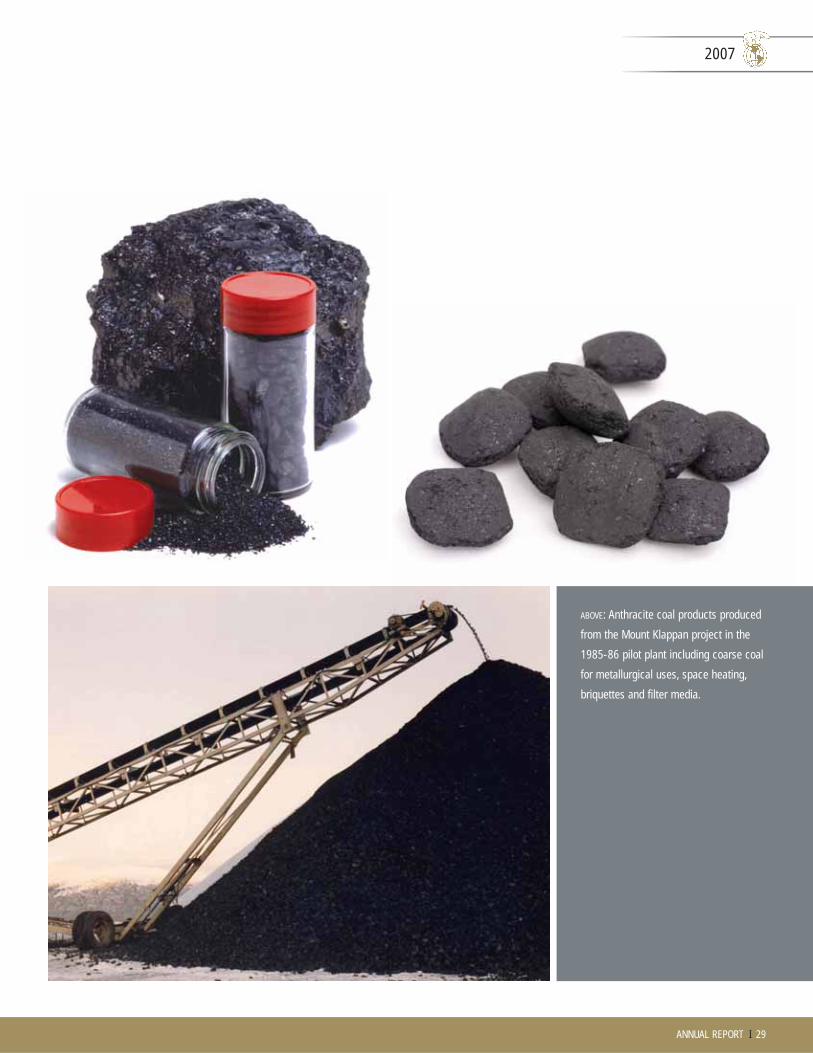

ABOVE: Anthracite coal products produced

from the Mount Klappan project in the

1985-86 pilot plant including coarse coal

for metallurgical uses, space heating,

briquettes and filter media.

2007

30 I FORTUNE MINERALS LIMITED

ABOVE: One of four shipments of coal being

loaded at the port of Stewart from the

1985-86 trial cargo.

RIGHT: Modified tridem axle trucks being

considered for haulage of coal products

from Mount Klappan.

MOUNT KLAPPAN ANTHRACITE COAL PROJECT

2007

ANNUAL REPORT I 31

JOINT VENTURE DISCUSSIONS

The 2005 feasibility study for Mount Klappan assessed a number of development scenarios including1.5 and 3 million tonnes/year production rates and rail and truck transportation options to Stewartand Prince Rupert. However, development scenarios have also been examined that assessed highertonnage production rates and developments including a rail link to the Port of Prince Rupert.Theseinclude an in-house assessment of a 5-million tonnes/year mine with the construction of the railwayshort-cut to Prince Rupert, which shows very attractive economics. Fortune has also investigated thepotential for projects producing multiple products including coal gasification,coal-to-oil liquefaction,and integration with Shell Canada’s coalbed methane project, which is testing an 8-trillion cubic footgas target on overlapping and contiguous licenses. Most of these projects are much greater in scopethan Fortune could currently undertake, but would produce economic returns that would be veryattractive to a larger company.Therefore, Fortune is conducting discussions with potential joint ven-ture partners, including coal, power, oil and gas, and international trading companies.A key objectivewould be to gain the support of a major organization with the financial ability and commitment toaggressively advance the project on a large enough scale to generate economies that reflect the truevalue inherent in this world-class asset.

TRANSPORTATION INITIATIVES

While Fortune is continuing permitting application activities for an export metallurgical coal mine with truck haulage to the port ofStewart, it is also examining a number of enhancements that could materially improve the economics of the project through more efficientmovement of products from the mine to the two available export port options. Fortune engaged AllNorth Engineering to complete engi-neering of the short-cut road between the mine site and Highway 37 for truck haulage of coal products to the port of Stewart. AllNorthand Marston have also been working on more efficient truck configuration options for the truck haul at an expanded 3-million tonnes/yearproduction rate.These include utilization of large, off-road trucks for the short-cut haul road that could handle payloads of 110 tonnes ormore.This would involve re-load from a surge pile at the highway to custom built 44-tonne, highway compliant, tridem axle trucks for theremaining haul on the highway to Stewart.The port facilities would also be modified from what was initially proposed in the 2005 feasi-bility study by the construction of storage facilities on the perimeter of Stewart to eliminate heavy truck traffic through the centre of town.Coal would be transported to an upgraded ship-loader by a high-speed conveyor system capable of handling the coal at a rate of 2,000tonnes/hour to eliminate port congestion and limitations for space at the dockside.

Fortune has also been conducting economic assessments of the viability of transporting coal using a slurry pipeline from its proposedMount Klappan mine to the ports of Stewart and Prince Rupert. Initial scoping level assessments showed very attractive economics forthis transportation alternative by materially reducing operating costs to the ports as compared to the previously evaluated truck or railtransportation options.A slurry pipeline would also help mitigate the future impacts of increasing fuel and labour costs. Further study isbeing undertaken to consider such an option through more rigorous pre-feasibility level engineering assessments.

An independent feasibility study was completed in 2007 concerning a potential Alaska - Canada Rail Link and was jointly funded by theYukon and Alaska governments. This study recommends a railway connection from Alaska through the Yukon and northern BritishColumbia to the continental United States that would include a segment running past Mount Klappan.The study also recommends a short-cut to the Port of Prince Rupert that would dramatically reduce the rail haulage distance of coal products from Mount Klappan to PrinceRupert from 1,400 kilometres to just over 600 kilometres.Further, if built, such a rail line would eliminate most of the costs associated withconstruction of transportation infrastructure for Mount Klappan. Although a very attractive development option for Mount Klappan, thisrail option would take several years of environmental and engineering studies and is too large a project for Fortune to undertake.TheCompany is, therefore, focusing on the truck haulage option to Stewart.

2007

32 I FORTUNE MINERALS LIMITED

ENVIRONMENT

Fortune has been actively collecting baseline environmental data around Mount Klappan and is in the environmental assessment process. RescanEnvironmental Services Ltd.and their Tahltan First Nation joint venture partner Rescan Tahltan Environmental Consultants (RTEC) are Fortune's envi-ronmental consultants for the project. Since the fall of 2004 they have been conducting a number of environmental baseline studies at the proposedmine site and along the potential transportation corridors. In addition to the current studies, the project has benefited from several similar studiesundertaken in the 1980s by Gulf Canada Resources Ltd.These studies included traditional use, archaeology, socio-economics, human health/countryfoods, land use, soils, vegetation, wildlife, habitat mapping, ground water, surface waters, water quality, wetlands, fisheries, meteorology and metalleaching/acid rock drainage potential. Although many are considered complete, these studies are continuing in order to add to the baseline data.

Fortune is also developing the project description in preparation for finalizing the Terms of Reference (TOR) for the environmental assessment.Progress on the project description was temporarily suspended in late 2007 pending completion of alternative transportation scenario analyses andis expected to resume in 2008. Preparation of the previous draft TOR, completed in 2007, involved considerable consultations and discussions withFirst Nations, government agencies and the general public.The Company plans to submit its final application for its environmental certificate laterthis year subject to the finalization of the TOR. Detailed engineering will be undertaken following receipt of the certificate.

FIRST NATION PARTICIPATION

Another major aspect of our development plans for the Mount Klappan deposit concerns our consultations with the area First Nations. Specifically,Fortune is in discussions with the Tahltan Central Council and other First Nations with respect to communications,environmental assessment,Impactand Benefits and other agreements.

RIGHT: Fortune’s environmental surveys for Mount Klappan are

conducted with participation by members of the Tahltan and

other impacted First Nations groups.

MOUNT KLAPPAN ANTHRACITE COAL PROJECT

2007

ANNUAL REPORT I 33

ABOVE: Valley being considered for the short-cut haul road to

Mount Klappan from Highway 37.

LEFT: Hydrology, fisheries and other environmental surveys being

conducted for the proposed haul road to Mount Klappan.

2007

34 I FORTUNE MINERALS LIMITED

SUE-DIANNECOPPER-SILVER-GOLD PROJECT

Introduction:

Early in 2008, Fortune released a new, NI 43-101 compliant resource estimate

for its wholly-owned Sue-Dianne copper-silver project. The independently pre-

pared report estimates that the deposit has indicated resources of 8,444,000

tonnes and inferred resources totaling 1,620,000 million tonnes. This report,

prepared by “Qualified Persons” B. Terrence Hennessey, P.Geo. of Micon and

Eugene J. Puritch, P.Eng. of P&E Mining Consultants, used a 0.40% copper cut-

off grade. The near surface deposit is amenable to low cost open pit mining

and remains open at depth. Metallurgical tests carried out at SGS Lakefield

indicate high recoveries can be achieved for copper, silver and gold from this

deposit using simple flotation, and that a high value cathode copper product

could be produced in the same plant that Fortune plans to construct at NICO.

Located just 25 km north of NICO, Sue-Dianne presents an excellent opportu-

nity to supply incremental mill feed to extend the life of the NICO plant, sub-

ject to more detailed engineering and receipt of applicable permits.

2007

ANNUAL REPORT I 35

SUE DIANNE RESOURCE ESTIMATES

(@0.40% Cu Cut-Off Grade)

Indicated Inferred

Tonnes 8,444,000 1,620,000Cu (%) 0.80 0.79Au (g/t) 0.07 0.07Ag (g/t) 3.20 2.40Cu (millions lbs) 149.10 28.30Au (oz) 19,000 3,600Ag (oz) 855,000 122,000

The mineral resource estimates for the Sue-Dianne project were determined by MiconInternational Limited and P&E Mining Consultants Inc. based on assay data and engineeringstudies. Details of the Sue-Dianne mineral reserves can be seen in the February 22, 2008 newsrelease announcing the results of the Micon technical report dated March 2008, and alsoFortune’s Annual Information Form available on the Sedar website (www.sedar.com). Mr.Terrence Hennessey, P.Geo. and Mr. Eugene Puritch, P.Eng. are Qualified Persons for this work inaccordance with National Instrument 43-101.

BELOW: Block model of the Sue-Dianne copper-silver-gold

deposit (red) with drill holes and open pit optimization.

2007

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIALCONDITIONS AND RESULTS OF OPERATIONSYear ended December 31, 2007

This Management’s Discussion and Analysis of Fortune Minerals Limited (“Fortune” or the “Company”) is dated February 27, 2008 and shouldbe read in conjunction with the Company’s Annual Audited Consolidated Financial Statements for the year ended December 31,2007 preparedin accordance with Canadian generally accepted accounting principles.All dollar amounts are presented in Canadian dollars.

SELECTED ANNUAL INFORMATION

2007 2006 2005

Total revenues $699,550 $596,034 $579,688Net income (loss) 2,196,067 (39,205) (402,718)Basic and fully diluted income

(loss) per common share 0.05 – (0.01)Total assets 90,353,718 60,236,785 47,851,896Total long term

financial liabilities – – –

SUMMARY OF QUARTERLY RESULTS

2007Dec-31 Sep-30 Jun-30 Mar-31

Revenues $294,749 $203,966 $91,495 $109,340Net income (loss) 2,457,888 (119,701) (112,496) (29,624)Basic and fully diluted

income (loss) percommon share 0.05 – – –

2006Dec-31 Sep-30 Jun-30 Mar-31

Revenues $71,354 $256,385 $128,793 $139,502Net income (loss) 18,856 189,991 (102,386) (145,666)Basic and fully diluted

income (loss) percommon share – – – –

Julian KempVice President Finance and

Chief Financial Officer

36 I FORTUNE MINERALS LIMITED

2007

ANNUAL REPORT I 37

OVERVIEW

Fortune is a natural resource company with diversified assets, all of which are located in Canada. Currently, the Company is involved in theexploration and development of coal,specialty metals,base metals and precious metals properties.Fortune is making the transition from explo-ration company to mineral producer. The Company’s most significant assets are the Mount Klappan anthracite coal project in northwestBritish Columbia and the NICO cobalt-gold-bismuth project in the Northwest Territories.

Fortune is committed to bringing both of its principal projects into production and accordingly, the Company is evaluating its strategic optionsto allow for the development of these assets in similar timeframes. Fortune intends to develop its NICO project independently, whereas theCompany is contemplating various potential transactions to develop Mount Klappan with a development or joint venture partner. Such a jointventure would be undertaken with the expectation that, with the right business partner(s), the project will ultimately be developed on a larg-er, more profitable scale than Fortune is contemplating on its own. Further, such an arrangement is expected to address issues concerning thefinancing required for putting both projects into commercial production at the same time.The Company’s transition to becoming a produc-er has been facilitated by the successful completion of positive feasibility studies and environmental studies, which have been produced forboth projects. Both feasibility studies have identified sufficient reserves to support long-life mines and the environmental studies have accu-mulated extensive environmental baseline data required to navigate the environmental assessment process.The Company has also completedthe steps required to commence the regulatory permitting process. Operational alternatives are being evaluated to enhance the economics ofeach project, including various construction, processing and transportation options. In addition, the Company has augmented its board andmanagement team and maintained a strong financial position. While it is taking longer than anticipated to achieve certain key milestones,including the negotiation of appropriate agreements with First Nations,obtaining various required permits and arranging project funding,man-agement continues to seek proactive ways to manage the risks that delay or extend the time it takes to conclude these and other necessarytasks.

Fortune offers its investors exposure to a unique combination of commodities with positive long term fundamentals. The markets foranthracite, cobalt, gold and bismuth all demonstrate growing demand and strong prices which has more than offset the strengtheningexchange rate between the Canadian and U.S. dollars. For its feasibility studies, the Company used what management believed to be conser-vative price assumptions.These prices compared to approximate current market prices together with the estimated Canadian dollar equiva-lents are as follows:

Unit of Feasibility Study Market Prices atMeasure Assumptions February 27, 2008 (1)

US$ C$ US$ C$

Anthracite Coal (2) Tonne 100 125 150(3) 150(3)

Cobalt Pound 16.50 19.64 50.00 50.00Gold Ounce 525 625 950 950Bismuth Pound 4.50 5.36 15.00 15.00

(1) Estimated prices based on either publicly quoted prices or Fortune’s internal data generated from industry sources.(2) The Mount Klappan feasibility study was based on producing one bulk product being a 10% ash pulverized coal injection (“PCI”)

product.(3) Estimated market price for a premium anthracite PCI product.Various anthracite coal products are trading between US$100 to

over US$300 per tonne. >

2007

38 I FORTUNE MINERALS LIMITED

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITIONSAND RESULTS OF OPERATIONSYear ended December 31, 2007

These price increases reflect market realities both on a demand and supply side. Coal is used to generate 40% of the world’s electricity and isa principal ingredient in the manufacture of steel and other metals. Increasing use of anthracite in these and other applications has resulted inChina (the largest anthracite producer) becoming a net importer, and Vietnam, the second largest producer and exporter, curtailing exports infavour of domestic requirements.The consumption of cobalt is forecast to increase between 8-12% in 2008 and the market has averaged about10% compounded growth per year for the last several years driven primarily by its use in high performance rechargeable batteries,high strengthsteel alloys and catalysts.Growing concerns about the U.S.economy and increasing demand has contributed to significant increases in the priceof gold and it continues to be used as a store of wealth. Bismuth consumption is also increasing principally as a replacement for lead due to itsinert properties and concerns for lead toxicity. Bismuth, a relatively rare metal, has limited supply dominated by China. Globally, the supply ofthese commodities are impacted by rising production costs as a result of increasing costs for steel, fuel, labour and power, increasing regulato-ry costs, resource nationalism and depletion of near-surface higher grade deposits.

Looking ahead, Fortune’s management continues to pursue the implementation of an appropriate strategic alternative related to MountKlappan, is undertaking negotiations with affected First Nations to reach agreements related to environmental assessment funding, access,impacts and benefits, is navigating the permitting process, is enhancing its management skill and depth and is looking to arrange appropriateforms of project financing.

Fortune’s total cash expenditures for exploration and development activities over the last three years were: 2007 – $15,622,043; 2006 –$17,912,606; and 2005 – $7,270,061. Most of these expenditures were on the Company’s Mount Klappan and NICO projects.Total deferredexploration and development expenditures were $53,546,669 as at December 31, 2007, as compared to $37,647,706 as at December 31, 2006.

The Company’s 2007 project related expenditures for NICO focused on the underground bulk sample program, metallurgical test work includ-ing the pilot plant in progress, salvage and dismantling activities at the Golden Giant Mine site, and engineering,environmental studies and com-munity consultation activities. For Mount Klappan, expenditures were focused on examining mine and infrastructure enhancements, planningand engineering design work, environmental studies, and community consultation activities. The actual cash exploration and developmentexpenditures for NICO and Mount Klappan totalled $15.6 million and exceeded the forecast expenditures by $1.6 million due to additionalengineering, project enhancement activities and environmental work that was carried out in addition to originally forecasted activities.