form d2.1 claim for home or first home transfer duty ... · form d2.1. parts e & f only need to...

TRANSCRIPT

Page 1 of 7

FORM OSR – D2.1Version 13 – Effective 18 September 2017

Duties Act 2001 sections 95 and 246HLand Tax Act 2010 section 78(3)Taxation Administration Act 2001 section 113D(1)

Keep this guide for future reference. It contains important information about the concession and your obligations after you receive the concession.

Notes:

• This form includes questions relating to additional foreign acquirer duty (AFAD).

• Each non-Australian transferor and transferee must also complete an identity details annexure when the transaction involves a transfer of real property (e.g. houses, apartments, business premises or vacant land).

By completing and submitting this form, you are declaring that you are eligible for the concession and will comply with your obligations. If you fail to comply, you will be required to repay all or part of the concession amount. Penalty tax and interest may also apply.

It is an offence to falsely claim a concession. The maximum penalty is an additional $12,615.

Meanings of terms used in this form are on page 4 of this guide.

Eligibility

To be eligible for a concession, you must:

• be an individual

• occupy the residence as your home within 1 year of the transfer date

• not dispose of the land, either

– before you occupy the residence as your home, or

– within 1 year after you start to occupy the residence as your home.

There is a strict requirement to not ‘dispose’ (see page 4 of this guide) of the property. If you are unsure how this applies to your situation, you should seek professional advice.

Additional requirements for the first home concession

To be eligible for a first home concession:

• you must be at least 18 years of age

• the home must be your first home.

Your obligations

You must notify us within 28 days if you:

• do not occupy the residence as your home within 1 year of the transfer date

• dispose of the land, either

– before you occupy the residence as your home, or

– within 1 year after you start to occupy the residence as your home.

Failing to notify is an offence—the maximum penalty is an additional $12,615.

Guide to claiming a home or first home transfer duty concession

Page 2 of 7

Where do I lodge my documents?

If you have a legal adviser, you should provide them with the documents for the dutiable transaction you have entered into and the completed Form D2.1. They may assess duty for your transaction if they are a registered self assessor. If you do not have a legal adviser, or settlement or lodging agent, you can lodge with the Commissioner of State Revenue for assessment. Send the form and your documents to GPO Box 2593, Brisbane Qld 4001. You will be notified by email or text message when your documents are received.

How to complete this form

• Each purchaser who is claiming a home or first home concession must complete a separate form.

• Print or type all responses in the boxed spaces, and tick appropriate boxes.

• If you are claiming the concession as trustee, complete the questions in Parts B, C and E of this form as if they refer to the beneficiaries and the beneficiaries are acquiring the land.

Question 1—Details

The claimant must be an individual, unless acting as trustee. Individuals must provide their full name and date of birth.

A trustee of a trust may be eligible for a concession where:

• the trust is not a discretionary or unit trust • all the beneficiaries of the trust are under a legal disability • all of the beneficiaries will occupy the residence as their home.

Trustee companies may enter their name in the first name field and provide one out of an ABN, ACN or ARBN.

All transferees must indicate whether they are a non-Australian entity (see ‘Meaning of terms’). Each non-Australian must also complete an identity details annexure.

This information requirement applies regardless of additional foreign acquirer duty (AFAD). If you are an AFAD transferor or transferee, you must also complete this question.

Question 3—Additional foreign acquirer duty (AFAD)

You are a foreign individual if you are not an Australian citizen or permanent resident. See the ‘Meaning of terms’ for foreign trusts and permanent residents.

A trust is foreign if at least 50% of its interests are trust interests of:• foreign individuals• foreign corporations• trustees of a foreign trust• related persons of any of the above, including partners in a partnership.

Provide the following information for foreign trusts:• Country of establishment—the country where the trust was established. This will not be Australia where the trust

relationship was established or a trust deed was made under the jurisdiction of a country other than Australia.• Country of residence for tax purposes— the country in which the trust is resident for tax purposes. Tax residency

may depend on if the country the trust is in has a tax treaty with Australia. If the trust pays tax in Australia and other countries, state the main other country in which the trust pays tax. Seek professional advice or go to www.ato.gov.au/Individuals/International-tax-for-individuals for more information.

• Overseas registration number—equivalent to an ABN, ACN or ARBN• Foreign Investment Review Board application number—received when originally purchasing the property. Provide

this number regardless of whether an exemption was given. Email [email protected] if you need your application number.

• Other overseas identifier—any other unique identifier separate to the overseas identifier allocated to you in your country of nationality or citizenship (e.g. ID card for individuals; ABN or ACN equivalent that has not been provided as the overseas registration number, or another government-issued identifying number for non-individuals).

Page 3 of 7

Question 5—Age

In special circumstances, we may allow the concession for individuals younger than 18 years of age. To have your circumstances considered, submit your completed form together with full details explaining why you are acquiring the land.

Question 8—Occupation date

This is the date you commenced or will commence occupying the residence as your home. See the public ruling on concessions for homes and first homes (DA085.1).

Question 9—Land acquired

The lot number, plan type, plan number and title reference are shown on the agreement for sale or the title search for the land that you or your solicitor obtained from the Titles Registry.

You also need to identify whether the home is a new house or off the plan.

Question 12—Interest acquired

This is the interest you are acquiring as a result of the transaction. If it is a part interest, express it as a fraction (such as ½ or ½3 ). For example:

• You are buying the property by yourself. Your interest before the transaction is 0 and your interest after the transaction is 1.

• You are buying the property as joint tenant with your spouse. Your interest before the transaction is 0 and your interest after the transaction is ½.

• You own the property jointly with your sister and are buying her share of the property. Your interest before the transaction is ½ and your interest after the transaction is 1.

Question 13—Dutiable value

The dutiable value is the consideration paid or the unencumbered value of the property, whichever is higher. Enter the dutiable value of the entire property not just the interest relating to the transaction.

Also state the value of any non-residential land. You can not claim the concession on any part of the land that will not be used for residential purposes. This includes any part of your residence that you will use for commercial purposes or other residences on the land that you will not live in as your home. See the public ruling on concessions and residential purposes (DA087.1).

Parts E & F—Transferor and other transferee details

A party to a transaction is any person who currently has an interest in the property and any person who will have an interest in the property as a result of a dutiable transaction that is the subject of this form.

Provide the name and current address of all parties to the transaction (other than the person claiming the concession).

• A party that is disposing of property is a transferor—enter the details for the transferors at Part E.• A party to the transaction is a transferee for the transaction if they are acquiring dutiable property (including

transactions where they are acting as an agent for another party—see ‘AFAD transferees’—enter transferee details at Part F.

For each transferee, you also need to tell us the interest in the dutiable property that each transferee is acquiring in the transaction, expressed as a fraction. This excludes any interest that the party held in the property before the dutiable transaction.

For example:• You are the sole purchaser of a home. The interest you are acquiring is 1.• You acquire a home jointly with your spouse. You and your spouse each acquire a ½ interest in the home.• You own a home jointly with your sister. You agree to acquire your sister’s interest in the home. You will acquire a

½ interest in the home in this transaction.

Where more than one transferee is claiming a home or first home concession, each transferee must lodge a separate Form D2.1. Parts E & F only need to be completed by one transferee.

For information on ‘non-Australian entities’ and ‘AFAD Transferees’ see the ‘Meaning of terms’ below.

Provide the following information for foreign trusts:• Country of establishment—the country where the trust was established. This will not be Australia where the trust

relationship was established or a trust deed was made under the jurisdiction of a country other than Australia.• Country of residence for tax purposes—the country in which the trust is resident for tax purposes. Tax residency

may depend on if the country the trust is in has a tax treaty with Australia. If the trust pays tax in Australia and other countries, state the main other country in which the trust pays tax. Seek professional advice or go to www.ato.gov.au/Individuals/International-tax-for-individuals for more information.

• Overseas registration number—equivalent to an ABN, ACN or ARBN

• Foreign Investment Review Board application number—received when originally purchasing the property. Provide this number regardless of whether an exemption was given. Email [email protected] if you need your application number.

• Other overseas identifier—any other unique identifier separate to the overseas identifier allocated to you in your country of nationality or citizenship (e.g. ID card for individuals; ABN or ACN equivalent that has not been provided as the overseas registration number, or another government-issued identifying number for non-individuals).

Part G—Declaration

An administrator appointed under the Guardianship and Administration Act 2000 may sign this declaration on behalf of claimants with impaired capacity.

Meaning of termsAFAD residential land

AFAD (additional foreign acquirer duty) residential land is land in Queensland that is, or will be, solely or primarily used for residential purposes when certain other criteria are met (see the Duties Act). A reference to AFAD residential land includes chattels that are acquired in the same dutiable transaction as the land where the use is directly linked to, or is incidental to, the use and occupation of the land.

AFAD transferees

For AFAD, ‘transferee’ refers to the acquirer(s) for the transaction (see s. 233 of the Duties Act).

For each transferee, you will need to advise if they are a foreign person—that is, a foreign individual, foreign corporation or trustee of a foreign trust.

You are a foreign individual if you are not an Australian citizen or permanent resident.

A foreign corporation is one that is incorporated outside Australia or in which foreign persons, or related persons of foreign persons, have a controlling interest of at least 50%.

A trust is foreign trust if at least 50% of its interests are trust interests of:

• foreign individuals

• foreign corporations

• trustees of a foreign trust

• related persons of any of the above, including partners in a partnership.

Where a person is appointed in writing as an agent for another person (the principal) and, under the appointment, the agent enters into an agreement for the transfer of dutiable property on behalf of the principal, the agent is considered to be the transferee when answering the questions under Part C. (See s. 22(3) of the Duties Act.)

Where a transferee enters into an agreement for the transfer of dutiable property for, or for the benefit of, a company proposed to be registered under the Corporations Act 2001 (Cwlth), the transferee under the agreement is considered to be the transferee for the agreement transaction when answering the questions under Part C.

Dispose

Relating to land or a residence, means transferring, leasing or otherwise granting exclusive possession of part or all of the property to another person.

This may include selling the property or renting out 1 or more rooms.

Where a concession relates to leasehold land, you dispose of the land when you surrender the lease.

Page 4 of 7

You do not dispose of the property when:

• the transferor continues to occupy the property after the transfer date but vacates it within 6 months of the transfer date

• the existing tenants continue to occupy the property after the transfer date but vacate it at the end of the current lease term or within 6 months of the transfer date, whichever happens first. However, the lease arrangement needs to have been in place before the transfer date

• an intervening event occurs, such as a natural disaster, or the death or incapacity of the transferee

• you transfer part of the land to your spouse and the transfer is exempt from duty under section 151 of the Duties Act

• you are acquiring residential land that is an accommodation unit in a retirement village and you enter into a retirement village leasing arrangement for the unit.

See the Residential Tenancies Authority (www.rta.qld.gov.au) for more information on leasing arrangements and obligations on giving tenants notice to leave.

Dutiable value

This is either the unencumbered value of the property (usually the market value) or the amount you agree to pay (your consideration) for the transaction—whichever is higher.

Exclusive possession

Generally, the right to exclude all others, including the owner, from all or part of a property.

Whether exclusive possession has been granted depends on the:

• terms of the written agreement, where there is one

• facts and circumstances of the arrangement, where there is no written agreement.

Exclusive possession may also be granted by law. For example, the Residential Tenancies and Rooming Accommodation Act 2008 applies to certain renting arrangements. You should seek professional advice before arranging to rent out all or any part of your home.

See the Residential Tenancies Authority (www.rta.qld.gov.au) for more information on leasing arrangements and obligations.

First home

A home is your first home if before acquiring the home you have never:

• held an interest in residential land anywhere in the world except as trustee for another person, lessee (where you rented the residence) or holder of a security interest

• received the first home vacant land concession.

Foreign individual

You are a foreign individual if you are not an Australian citizen or permanent resident.

Foreign trust

A trust is foreign if at least 50% of its interests are trust interests of:

• foreign individuals

• foreign corporations

• trustees of a foreign trust

• related persons of any of the above, including partners in a partnership.

Home

A residence that the owner has occupied as their principal place of residence within 1 year of the transfer date for the residential land.

Individual

An individual means a natural person.

Page 5 of 7

Page 6 of 7

New building

A new building is residential premises that is one of the following:

• has not previously been sold or transferred as residential premises (e.g. purchasing a new home directly from a developer)

• has been built, or contains a building that has been built, to replace demolished premises on the same land• has been created through substantial renovations.

Substantial renovations are generally renovations in which all, or most, of the structural and/or non-structural components of a building are removed or replaced. Most of the rooms in the building must have been affected, and the renovations must have affected the building as a whole. The sale of substantially renovated residential premises generally attracts a GST liability.

To the best of your knowledge, identify if the residential premises is a new building.

Non-Australian entity

A non-Australian entity refers to:• individuals who are not Australian citizens (non-Australian individuals include permanent residents).• companies incorporated outside Australia• trusts with a country of tax residence that is not Australia• other bodies (e.g. body politic, corporation sole) formed outside Australia.

If you are an individual with dual citizenship, you are only a non-Australian entity if neither citizenship is Australian.

NotifyYou notify the Commissioner of State Revenue by submitting a notice for reassessment—transfer duty home and vacant land concessions (Form D2.4) together with the original stamped documents. The form is available at www.publications.qld.gov.au.

Qualified witness

A qualified witness is one of the following:

• justice of the peace

• commissioner for declarations

• solicitor.

Permanent resident

A permanent resident holds a permanent visa, or is a New Zealand citizen with a special category visa, as defined by the Migration Act 1958 (Cwlth).

Residence

A building or part of a building in Queensland that is:

• fixed to land

• designed, or approved by a local government, for human habitation by a single family unit

• used for residential purposes.

Residential land

Land or the part of land in Queensland on which a residence is constructed.

This includes the area immediately surrounding the residence if that area is not used commercially.

See section 86A of the Duties Act for a full definition.

Residential off-the-plan purchases

A residential off-the-plan purchase occurs when you enter into a contract to purchase new residential property before construction is completed. An off-the-plan purchase generally involves a proposed lot where the title is yet to be registered. Settlement of the contract cannot occur until certain events have happened (e.g. where the owner of the land has not completed all capital works required before the title can issue, such as boundaries, roads, and telephone and electricity connections; or where an apartment block is being built).

Transfer date

The date you’re entitled to possess the property.

This is usually the date of settlement or the date the land is vested in your name.

See the public ruling on concessions for homes and first homes (DA085.1).

Unencumbered value

The value of the property being transferred disregarding any encumbrance; for example, money owed under a mortgage.

See section 14 of the Duties Act for a full definition.

Commissioner of State RevenueGPO Box 2593

Brisbane Qld 4001Email: [email protected]

Ph: 1300 300 734Visit www.qld.gov.au/osr for information about duties and other state taxes.

The Office of State Revenue is collecting the information on this form on behalf of the Commissioner of State Revenue for the purposes of administering state revenue. This is authorised by the Duties Act 2001, the Land Tax Act 2010 and the Taxation Administration Act 2001. Your personal information may be disclosed without your consent in circumstances outlined in the Taxation Administration Act or as otherwise authorised by law. It is the Office of State Revenue’s usual practice to disclose personal information collected on this form to the Australian Taxation Office and other Australian state and territory revenue offices in accordance with the Taxation Administration Act.

© The State of Queensland (Queensland Treasury)Page 7 of 7

Page 1 of 8

FORM OSR – D2.1Version 13 – Effective 18 September 2017

Duties Act 2001 sections 95 and 246HLand Tax Act 2010 section 78(3)Taxation Administration Act 2001 section 113D(1)

Claim for home or first home transfer duty concession

Part A – Transferee details

About this formComplete this form if you are acquiring a residence that you will occupy as your home or first home.

Note: This form includes questions relating to additional foreign acquirer duty (AFAD).

Before you begin, read the ‘Guide to claiming a home or first home transfer duty concession’ to ensure you are eligible for the concession and understand your obligations.

Meanings of terms used in this form are on page 4 of the guide.

There is a strict requirement to not ‘dispose’ (see page 4 of the guide) of the property. If you are unsure how this applies to your situation, you should seek professional advice.

1. Details

First name

Middle names

Surname

Date of birth D D M M Y Y Y Y

Is the transferee acting as a trustee?

Yes Provide trust name below.

No

ABN ACN ARBN

Trust name

Is the transferee a non-Australian entity?

Yes Complete an identity details annexure.

No

2. Contact details

Current street address

Suburb State

Country Postcode

Mobile number + ( ) Phone number + ( )

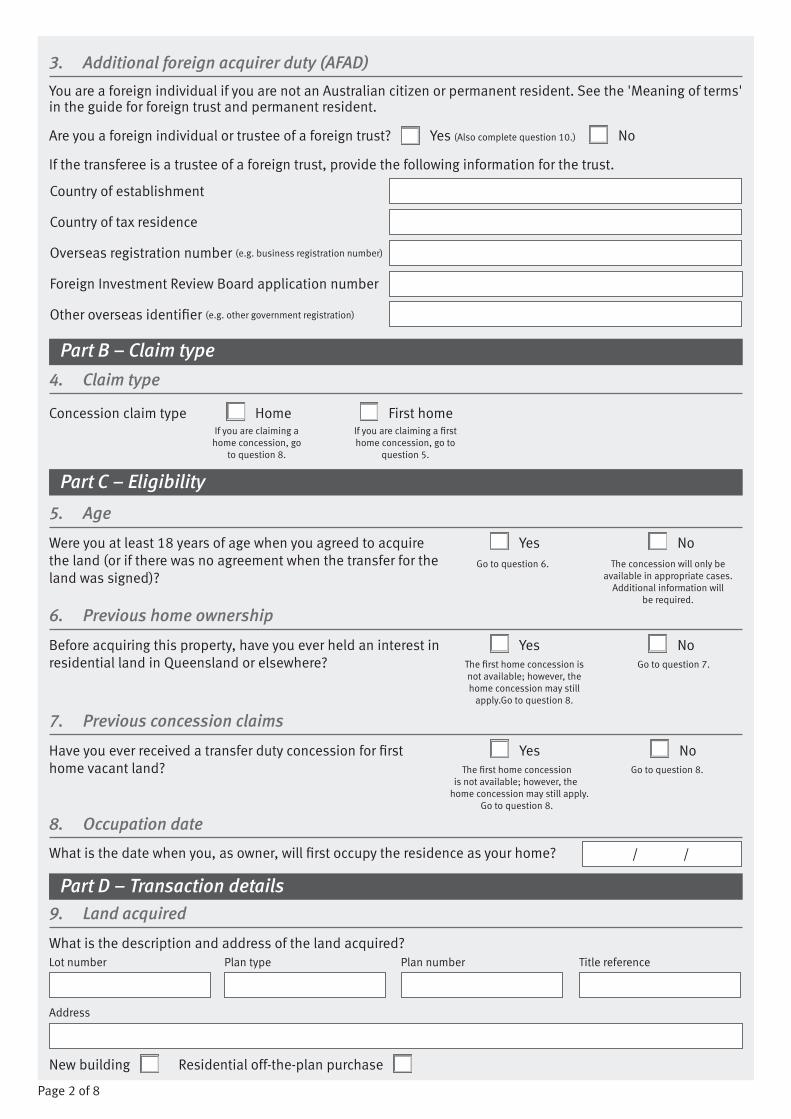

3. Additional foreign acquirer duty (AFAD)

You are a foreign individual if you are not an Australian citizen or permanent resident. See the 'Meaning of terms' in the guide for foreign trust and permanent resident.

Are you a foreign individual or trustee of a foreign trust? Yes (Also complete question 10.) No

If the transferee is a trustee of a foreign trust, provide the following information for the trust.

Country of establishment

Country of tax residence

Overseas registration number

Foreign Investment Review Board application number

Other overseas identifier

4. Claim type

Concession claim type Home First home

5. Age

Were you at least 18 years of age when you agreed to acquire Yes Nothe land (or if there was no agreement when the transfer for the land was signed)?

6. Previous home ownership

Before acquiring this property, have you ever held an interest in Yes Noresidential land in Queensland or elsewhere?

7. Previous concession claims

Have you ever received a transfer duty concession for first Yes Nohome vacant land? The first home concession Go to question 8. is not available; however, the home concession may still apply. Go to question 8.

8. Occupation date

What is the date when you, as owner, will first occupy the residence as your home?

9. Land acquired

What is the description and address of the land acquired?Lot number Plan type Plan number Title reference

Address

New building Residential off-the-plan purchase

Part C – Eligibility

Part D – Transaction details

Go to question 6. The concession will only be available in appropriate cases.

Additional information will be required.

The first home concession is not available; however, the home concession may still

apply.Go to question 8.

Go to question 7.

Page 2 of 8

(e.g. other government registration)

(e.g. business registration number)

/ /

If you are claiming a home concession, go

to question 8.

If you are claiming a first home concession, go to

question 5.

Part B – Claim type

Page 3 of 8

10. AFAD residential land

Is the land used solely or primarily for residential purposes, or will it be in the future?

Yes Value of AFAD residential land

No

11. Transfer date

What is the transfer date for the land?

12. Your interest in the property

What interest did you hold in the property before the transaction?

What interest will you hold in the property after the transaction?

13. Dutiable value

What is the dutiable value of the entire property?

If this property includes non-residential property, what is the dutiable value of the

non-residential property?

Provide details for all transferors. Attach additional pages if required.

14. Transferor 1 details

Complete the details for the individual or non-individual transferor, and note if they are a trustee and non-Australian entity.

Individual

First name

Middle names

Surname

Date of birth D D M M Y Y Y Y

TrusteeIs the transferor acting as trustee? Yes No

Trust name

Non-Australian entityIs the transferor a non-Australian entity?

Yes Complete an identity details annexure.

No

Your share in the ownership of the property that is being acquired expressed as a fraction (such as 1/2, 1/3, 1/4) or 1 if you are the sole owner of the property.

/ /

Non-individual (e.g. company, trust)

Entity name

ABN ACN ARBN

(This includes chattels where the use is directly linked to, or is incidental to, the use and occupation of the land.)

Part E – Transferor details

$

Page 4 of 8

Contact details

Care of

Current street address

Suburb State

Country Postcode

Mobile number + ( ) Phone number + ( )

Contact name

15. Transferor 2 details

Complete the details for the individual or non-individual transferor, and note if they are a trustee and non-Australian entity.

Individual

First name

Middle names

Surname

Date of birth D D M M Y Y Y Y

TrusteeIs the transferor acting as trustee? Yes No

Trust name

Non-Australian entityIs the transferor a non-Australian entity?

Yes Complete an identity details annexure.

No

Contact details

Care of

Current street address

Suburb State

Country Postcode

Mobile number + ( ) Phone number + ( )

Contact name

Non-individual (e.g. company, trust)

Entity name

ABN ACN ARBN

Provide name of person responsible for the entity (e.g. name of director or

company secretary).

Provide name of person responsible for the entity (e.g. name of director or

company secretary).

Page 5 of 8

Provide details for all transferees other than the person claiming the concession. Attach additional pages if required.

16. Transferee 1 details

Complete the details for the individual or non-individual transferee, and note if they are a trustee and non-Australian entity.

Individual

First name

Middle names

Surname

Date of birth D D M M Y Y Y Y

TrusteeIs the transferee acting as trustee? Yes No

Trust name

Non-Australian entityIs the transferee a non-Australian entity?

Yes Complete an identity details annexure.

No

Additional foreign acquirer dutyIs the transferee a foreign person? Yes No Is the transferee an agent who is a

Yes No

foreign person, acting for a principal?

Is the principal a foreign person? Yes No If the transferee is a trustee of a foreign trust, provide the following information for the trust.

Country of establishment

Country of tax residence

Overseas registration number

Foreign Investment Review Board application number

Other overseas identifier

Non-individual (e.g. company, trust)

Entity name

ABN ACN ARBN

Part F – Other transferee details

(e.g. business registration number)

(e.g. other government registration)

Page 6 of 8

Contact details

Care of

Current street address

Suburb State

Country Postcode

Mobile number + ( ) Phone number + ( )

Contact name

17. Transferee interest acquired

Interest acquired

18. Transferee 2 details

Complete the details for the individual or non-individual transferee, and note if they are a trustee and non-Australian entity.

Individual

First name

Middle names

Surname

Date of birth D D M M Y Y Y Y

TrusteeIs the transferee acting as trustee? Yes No

Trust name

Non-Australian entityIs the transferee a non-Australian entity?

Yes Complete an identity details annexure.

No

Additional foreign acquirer dutyIs the transferee a foreign person? Yes No Is the transferee an agent who is a

Yes No

foreign person, acting for a principal?

Is the principal a foreign person? Yes No

Non-individual (e.g. company, trust)

Entity name

ABN ACN ARBN

Provide name of person responsible for the entity (e.g. name of director or

company secretary).

The ownership share of the property acquired by the transferee expressed as a fraction, such as 1/2, 1/3, 1/4, or 1 if the transferee acquired all of the property.

Page 7 of 8 © The State of Queensland (Queensland Treasury)

If the transferee is a trustee of a foreign trust, provide the following information for the trust.

Country of establishment

Country of tax residence

Overseas registration number

Foreign Investment Review Board application number

Other overseas identifier

Contact details

Care of

Current street address

Suburb State

Country Postcode

Mobile number + ( ) Phone number + ( )

Contact name

19. Transferee interest acquired

Interest acquired The ownership share of the property acquired by the transferee expressed as a fraction, such as 1/2, 1/3, 1/4, or 1 if the transferee acquired all of the property.

Provide name of person responsible for the entity (e.g. name of director or

company secretary).

Page 8 of 8 © The State of Queensland (Queensland Treasury)

Part G – Declaration

For registered self assessors only:

Client number Transaction number

Commissioner of State RevenueGPO Box 2593

Brisbane Qld 4001Email: [email protected]

Ph: 1300 300 734Visit www.qld.gov.au/osr for information about duties and other state taxes.

The Office of State Revenue is collecting the information on this form on behalf of the Commissioner of State Revenue for the purposes of administering state revenue. This is authorised by the Duties Act 2001, the Land Tax Act 2010 and the Taxation Administration Act 2001. Your personal information may be disclosed without your consent in circumstances outlined in the Taxation Administration Act or as otherwise authorised by law. It is the Office of State Revenue’s usual practice to disclose personal information collected on this form to the Australian Taxation Office and other Australian state and territory revenue offices in accordance with the Taxation Administration Act.

There is a strict requirement to not ‘dispose’ (see page 4 of the guide) of the property. If you are unsure how this applies to your situation, you should seek professional advice.You must sign this declaration in the presence of a qualified witness. I declare:(a) I have read the ‘Guide to claiming a home or first home transfer duty concession’ and will keep it for future

reference.(b) I have occupied or will occupy the residence as my home within 1 year of the transfer date.(c) I will notify the Commissioner of State Revenue within 28 days if I: i. do not occupy the residence as my home within 1 year of the transfer date or ii. dispose of the land, either • before I occupy the residence as my home or • within 1 year after I start to occupy the residence as my home.(d) The information supplied to the Commissioner of State Revenue in Parts A–D of this form is true and

correct (the information on whether the property is a 'new building' is true and correct to the best of my knowledge); and the information in Parts E–F is true and correct to the extent it was provided to me.

I understand that if I do not comply with these obligations I will be required to repay all or part of the concession amount and pay any associated penalty tax and interest. I understand that to make a false claim for the concession may result in an additional penalty and/or prosecution.I make this solemn declaration conscientiously believing the same to be true, and by virtue of the provisions of the Oaths Act 1867.

Signature Date

Name

Qualified witness signature Date

Qualified witness name