form – 704 (see rule 65) audit report under section 61 of ... · audit report under section 61 of...

TRANSCRIPT

FORM – 704

(See rule 65)

Audit report under section 61 of the Maharashtra Value Added Tax Act, 2002,

Location

TOFROMPERIOD UNDER AUDIT

AUDIT REPORT AND CERTIFICATION

PART – 1

1. The audit of M/s holder of Tax Payer Identification Number under the Maharashtra Value Added Tax Act, 2002

(hereinafter referred to as “the MVAT Act”) and Tax Payer Identification Number under the Central Sales Tax

Act, 1956 (hereinafter referred to as “the CST Act” ) is conducted by (*)me/us (Chartered accountants/cost

accountant) in pursuance of the section 61 of the MVAT Act .

Maintenance of Books of Accounts, Sales Tax related records and Financial Statements are the responsibility of the

Entity’s Management. Our responsibility is to express an opinion on their Sales Tax related records and Financial

Statements based on our audit. We have conducted our audit in accordance with the auditing standards generally

accepted in India. These standards require that we plan and perform the audit to obtain reasonable assurance about

whether the Sales Tax related records and Financial Statements are free of material mis-statement(s). The audit

includes examining, on a test basis, evidence supporting the amounts and disclosures in the Financial Statements.

An audit also includes assessing the accounting principles used and significant estimates by management as well as

evaluating the overall Financial Statement presentation. We believe that our audit provides a reasonable basis for

our opinion

2.

:

Seal and Signature of Auditor

Name :

1

TABLE - 1

2 (A) I/we have verified correctness of the tax liability of the dealer in respect of below mentioned sales tax returns.

ParticularsSr. No

Dealer is required to file returns (Tick

appropriate Box)1

Monthly Quarterly Six-

Monthly

Annual For

Deemed

Dealers

Dealer has filed all the returns as per given

frequency.

2Yes No

Dealer has maintained stock register.3 Yes No

Verification of the Returns for the period

under Audit.4

Returns verified (Please select the appropriate

box)5

(i) The dealer has filed returns only for the

period in which there is inter-State sales

or sales u/s. 5(2) or 5(3).

(ii) Since there are no interstate sales or

sales u/s. 5(2) or 5(3) in other periods,

the dealer has/has not filed returns for

such periods.

(ii) Return in Form 405

Returns under the Central Sales

Tax Act, 1956.

(i) Returns under the Maharashtra

Value Added Tax Act, 2002(a)

(b)

Subject to *my/our remarks about non-compliance, shortcomings and deficiencies in the returns filed and tax liability

computed and presented in respective schedules and Para-4 of this Part, I/We certify that,- 2 (B).

I/We have obtained all the information and explanations, which to the best of *my/our knowledge and belief, were

necessary for the purposes of the audit.

a).

b). *I/We have read and followed the instructions for preparation of this audit report. Considering the nature of

business of the dealer and the Form in which the dealer is expected to file return(s), we give the information as

required in Part-3 in Schedule I / II / III / IV / V / VI (score out whichever is not applicable) along with the

applicable annexure(s).

:

Seal and Signature of Auditor

Name :

2

The books of account and other sales tax related records and registers maintained by the dealer alongwith sales and

purchase invoices as also Cash Memos and other necessary documents are sufficient for computation the tax

liability under the MVAT Act and the CST Act.

The gross turnover of sales and purchases, determined by us, includes all the transactions of sales and purchases

concluded during the period under audit.

The adjustment to turnover of sales and or purchases is based on entries made in the books of account during the

period under Audit and same are supported by necessary documents.

The deductions claimed from the gross turnover of sales and other adjustments thereto including deduction on

account of goods return, adjustments on account of discounts as also debit/credit notes issued or received on

account of other reasons, are supported by necessary documents and are in conformity with the provisions of the

relevant Act.

Considering the schedule and entry wise classification of goods sold, classification of exempted sales, sales at

reduced rates are correct. The tax leviable on sales is properly computed by applying applicable rate of tax and/or

composition tax.

Computation of set-off admissible in respect of purchases made during the period under Audit and adjustments

thereto are correct. While ascertaining the correctness, *I/We have taken into account the factors such as goods

returned, adjustments on account of discounts as also debit /credit notes issued or received on account of other

reasons and these claims and adjustments are supported by necessary documents. The Set-off is worked out only

on the basis of tax invoices in respect of the purchases.

Wherever the dealer has claimed sales against the declarations or certificates; except as given in Annexure-H and

Annexure-I, all such declarations and certificates are produced before me. I/we have verified the same and they are

in conformity of the provisions related thereto.

Computation of Cumulative Quantum of Benefits (CQB), wherever applicable, is in conformity with the provisions

of the Act in this regard.

The records related to the receipts and dispatches of goods are correct and properly maintained.

The tax invoices in respect of sales are in conformity with the provisions of law.

The Bank statements have been examined by *me/us and they are fully reflected in the books of account.

c).

d).

e).

f).

g).

h).

i).

j).

k).

l).

m).

*I/we certify that *I/we have visited the principal place of business or a place of business from where major

business activity is conducted by the dealer. The dealer is conducting his business from the place/places of

business declared by him as his principal

Due professional care has been exercised while auditing the business and based on my observations of the business

processes and practices, stock of inventory and books of account maintained by the dealer, I fairly conclude that,-

(i) dealer is dealing in the commodities mentioned in the Part-2

of this report;

(ii) sales tax related records of the dealer reflects true and fair

view of the volume and size of the business for period under

audit.

n).

o).

p). I have verified that the purchases effected by the dealer in respect SEZ Unit of the dealer are used in the said Unit.

:

Seal and Signature of Auditor

Name :

3

Out of the aforesaid certificates; the following certificates are negative for the reasons given hereunder:-3.

(a) N.A.

(b) N.A.

(c) N.A.

(d) N.A.

(e) N.A.

(f) N.A.

(g) N.A.

(h) N.A.

(i) N.A.

(j) N.A.

(k) N.A.

(l) N.A.

(m) N.A.

(n) N.A.

(o) N.A.

(p) N.A.

:

Seal and Signature of Auditor

Name :

4

COMPUTATION OF TAX LIABILITY AND RECOMMENDATIONS

4. Computation of tax liability as per Audit:-

A summary of the additional or reduced tax liability payable by the dealer and/or additional or reduced refund due to the

dealer, arising on verification of sales tax returns together with books of account and other related records mentioned herein

above, for the period under audit is as follows:

TABLE-2

Amount as

determined

after audit. (Rs.)

Amount as per

returns (Rs.)

Particulars

Gross Turn-Over of Sales, including taxes as well as

Turn-over of Non- Sales Transactions like Value of

Branch Transfers/ Consignment

Transfers and job work charges

i)

Sr.

No.

Difference

(Rs.)

UNDER MAHARASHTRA VALUE ADDED TAX ACT, 2002

vii) Total credits [(a) to (d) above)] available

(c)

(b) Amount of tax paid under MVAT Act as per

ANNEXURE-A (including interest)

(a) Set-off claimed:

Less: Credits available on account of following:vi)

Credit of tax as per tax deduction at source

certificates (As per ANNEXURE-C).

(d) Any other (please specify)

v) Excess collection under M.V.A.T. Act, 2002

Tax leviable under the M.V.A.T. Act, 2002iv)

iii) Balance Net Turn-over liable for Tax

Less:- Total allowable Deductionsii)

ix) Total amount payable / refundable

xi) Less : Refund adjusted for payment of tax under

the Central Sales Tax Act, 1956

Balance Tax Payable/ Refundable

Less: Refund already granted to dealerxii)

Total Amount of Tax Defferedx)

viii) Add/Less:- Any other

(please specify)

:

Seal and Signature of Auditor

Name :

5

xiii) Total Amount Payable / Refundable

Differential tax liability for nonproduction

of declaration/ certificate as per Annexure-H.

xiv)

Add :

(i) Interest u/s 30(2)

(ii) Interest u/s 30 (4)

vi) Add/Less : Any other ( )

(b) MVAT refund adjusted (if any)

Amount of tax paid under the CST Act

ANNEXURE-B (including interest)

(a)

v) Less : Credits available on account of followings:

CST leviable under the Central Sales Tax Act, 1956

subject to production of declarations listed in

Annexure-I.

Tax

iv)

iii) Balance Net Turn-over liable for Tax

Less:- Total Deductions availableii)

Particulars

Amount as per

returns (Rs.)

Amount as

determined

after audit (Rs.)

Difference

(Rs.)

i)

Sr.

No.

TABLE-3

UNDER CENTRAL SALES TAX ACT, 1956

Gross Turn-Over of Sales (as per Sch. VI)

vii) Balance of tax payable / Refundable

Add:

(a) Interest U/s 9(2) read with Section 30(2) of

MVAT Act.

(b) Interest U/s 9(2) read with Section 30 (4) of

MVAT Act.

viii)

Total Dues Payable /Refundableix)

Excess Central Sales Tax Collectionx)

xi) Differential CST liability for want of declaration

as worked out in Annexure-I.

TABLE-4

:

Seal and Signature of Auditor

Name :

6

ii) Under the Central Sales Tax Act, 1956 0

000TOTAL

Act, 1956

Under the Maharashtra Value Added Tax Act, 2002.

CUMULATIVE QUANTUM OF BENEFITS AVAILED

Sr.

No.

i)

Difference

(Rs.)

Amount as

determined

(Rs.) after audit.

Amount as per

returns (Rs.)Particulars

Disallowance of other Non-admissible claims. (Please Specify)

(a)

8)

7) Excess claim of Set-off or Refund.

6) Computation of Tax at Wrong rate

5) Additional Tax liability on account of Nonproduction of Declarations and

Certificates.

4) Disallowance of High-seas Sales

2) Disallowance of Branch/Consignment Transfers

Disallowance of Inter-state sales or sales under section 6 (2) of CST Act.3)

Additional DuesReasons for additional Dues (Tax)

VAT CST

1)

Sr.

No.

The main Reasons for additional Dues or Refund (Tax and interest thereon)

TABLE-5

Difference in Taxable Turn-over

(b)

9) TOTAL DUES PAYABLE

10) Amount of interest payable (To be calculated form due date to the date

of Audit).

11) TOTAL AMOUNT PAYABLE

5. Qualifications or remarks having impact on the tax liability:-

(a)

:

Seal and Signature of Auditor

Name :

7

i) Pay additional tax liability of Rs.

Sr. No. Particulars MVAT

(Rs.)CST

(Rs.)

Dealer has been recommended to:-6.

Pay back excess refund received of Rs.ii)

Claim additional refund of Rs.iii)

v) Reduce tax liability of Rs.

Reduce the claim of refund of Rs.iv)

Revise closing balance of CQB of Rs.vi)

vii) Pay interest under-section 30(2) of Rs.

For

*Chartered Accountants

/ Cost Accountants

viii) Pay interest under-section 30(4) of Rs.

Name

*(Proprietor/ Partner)

Membership Number

Address:-

Email Id of Chartered

Accountants / Cost

Accountants

Mobile

Telephone

No

Date of Signing the Audit Report in form 704

* Strike out whichever is not applicable.

4. In case dealer is having multi-state activities the Trial Balance for the

business activities in Maharashtra.

3. Balance Sheet and Profit & Loss Account /Income and Expenditure Account.

2. Tax Audit Report under the Income Tax Act, 1961

1. Statutory Audit Report and its Annexures

Encl:

:

Seal and Signature of Auditor

Name :

8

2) Tax payers Identification Number under

MVAT Act, 2002.

(3) Registration Number under CST Act, 1956

(1) Period under the Audit FROM TOA.

1. General information:-

GENERAL INFORMATION ABOUT THE DEALERS BUSINESS ACTIVITIES

PART – 2

Audit report under section 61 of the Maharashtra Value Added Tax Act, 2002,

(See rule 65)

FORM – 704

(1) Name of the Dealer as appearing

on the Registration Certificate. B.

(2) Trade Name (If any):-

(3) Address of the Business (To be given only if

there is change in the Address during the period

as compared with the Registration

Certificate):-

(4) Additional place of business:- (To be given

only if there is change in the Address during

the period as compared with the Registration

Certificate):-

(4) Permanent Account Number

under Income Tax Act, 1961

C. RELATED INFORMATION UNDER OTHER ACTS

No

No

M M Y Y

Yes

Yes

DD

(3) E. C. Number under P.T. Act, 1975

Date of Effect of R.C. under PT

Act

(b) Payments are made as per Returns

(Please Tick appropriate Box).

(a)

(2)

Profession Tax Returns filed for the

period under Audit

(1) R. C. Number under P.T. Act, 1975

:

Seal and Signature of Auditor

Name :

9

Identity of division or unit

A. (1) Specify the divisions or units for which

separate books of account are maintained

2. BUSINESS RELATED INFORMATION

No

YYMM

No

NoYes

Yes

Yes

DD

Service Tax Registration Number, if any(14)

Import Export Code given by DGFT, if any(13)

(12) ECC Number under Central Excise Ac, if

any.

(11) Entitlement Certificate Number, if any

(10) Eligibility Certificate Number, if any.

(9) R.C. Number under Sugarcane Purchase Tax

Act, 1962, if any.

(8) R.C. Number Entry Tax on Goods Act, 2002,

if any.

Returns are filed under the Luxury Tax

Act, 1987 for the period under Audit (a)

(b) Payments are made as per Returns

(Please Tick appropriate Box).

(7)

(6) R. C. Number under Luxury Tax Act, 1987

(5)

Date of Effect of E.C. under PT

Act

(4)

The Profession Tax under above E.C. has

been paid for the period under Audit

(Please Tick appropriate Box)

Name Floor Plot No, Street and

AreaCity Pin District

B. Business Activity in Brief

C. Commodity Dealt in (5 major commodities)

Address of the Place of Business of the dealer

where books of account are keptD.

E. [i] Name and version of accounting software used

:

Seal and Signature of Auditor

Name :

10

Change in accounting software , if any[ii]

The following are the major changes made during

the period of review -F.

[i]

[ii] Changes in the accounting system

Change in the method of valuation of stock

[iii] Change in product line

[iv] New business activity

[v] Other changes, if any [please specify ]

G.

Other (Please Specify)

Second Hand Motor Vehicle DealersMotor Vehicle Dealer

Mandap DecoratorFranchisee Agent

Job workerPSI UnitWorks contractor

Bakery Importer Liquor DealerRetailer

WholesalerResellerRestaurantManufacture

Nature of business (Please tick one or more appropriate boxes, as applicable

Working capital employed by the entity

(Difference between current assets and

current liabilities) - as on the last day of

the period under audit.

Rs.______________________________ I.

Partnership

Others (Please specifyCo-operative SocietyPublic Ltd Co

Pvt. Ltd Co.HUFTrustProprietary

Constitution of the Business (Please tick the appropriate)H.

:

Seal and Signature of Auditor

Name :

11

ACTIVITY CODE3.

Activity Code Activity Description Turn-over

(Rs.)

Rate

of Tax

Tax

1

Particulars of the Bank Account(s) maintained during the period under Audit4.

Name of the Bank Branch BSR

Number

(Give Branch Address, if

BSR Code not known)

Account Number(s)Sr.

No.

1

:

Seal and Signature of Auditor

Name :

12

AUDIT REPORT

PART-3

SCHEDULE-I

Computation of Net Turn-Over of Sales liable to tax1.

Particulars As per return

(Rs.)As per Audit

(Rs.)

Difference

(Rs.)

1 2 3 4 5

a) Gross Turn-Over of Sales, including taxesas

well as Turn-over of Non-Sales Transactions

like Value of Branch Transfers/

Consignment Transfers and job work

charges

b) Less: - Turn-Over of Sales (including taxes

thereon) including inter-State Consignment

Transfers and Branch Transfers Covered

under Schedule II, III, IV or V

c) Balance:- Turn-Over Considered under

this Schedule (a-b)

d) Less: - Value of Goods Return (inclusive of

tax), including reduction of sale price on

account of rate difference and discount.

e) Less:- Net Tax amount (Tax included in sales

shown in (a) above less Tax included in (b)

and (d) above)

f) Less:- Value of Branch Transfers/

Consignment Transfers within the State if tax

is to be paid by an Agent.

g) Less:-Sales u/s 8 (1) i.e. Interstate Sales

including Central Sales Tax, Sales in the

course of Imports, Exports and value of

Branch Transfers/ Consignment transfers

outside the State. (Turn-Over covered

under Schedule-VI).

h) Less:-Sales of tax-free goods specified in

Schedule “A” of MVAT Act

i) Less:-Sales of taxable goods fully exempted

u/s. 8 other than sales under section 8(1) and

covered in Box 1(g) above.

j) Less:- Job work Charges or Labour charges.

k) Less:-Other allowable deductions, if any

(Please specify)

:

Seal and Signature of Auditor

Name :

13

l) Balance: - Net Turn-Over of Sales liable

to tax (c) – (d+e+f+g+h+i+j+k)

Computation of tax payable under the MVAT Act

Rate of

Tax

(%)

As per Returns

Turn-Over of

Sales

liable to tax (Rs.)

Tax Amount (Rs.) Turn-Over of

Sales

liable to tax (Rs.)

As per Audit

Tax Amount (Rs.)Difference in

Tax Amount

7654321

2.

TOTAL

2A) Difference

(Rs.)

As per Audit

(Rs.)

As per return

(Rs.)Sales Tax collected in Excess of the

Amount of Tax payable

Less:-Purchases of the taxable goods from registered

dealers under MVAT Act, 2002 and which are not

eligible for set-off

k)

Less:-Within the State purchases of taxable goods from

un-registered dealers

j)

Less:-Within the State Branch Transfers /

Consignment Transfers received where tax is to be paid

by an Agent

i)

Less:-Inter-State Branch Transfers/ Consignment

Transfers receivedh)

Less:-Inter-State purchasesg)

Less:-Imports (High seas purchases)f)

Less:-Imports (Direct imports)e)

Less:-Value of Goods Return (inclusive of

tax), including reduction of purchase price

on account of rate difference and discount.

d)

Balance:- Turn-Over of Purchases

Considered under this Schedule (a-b)c)

Less:- Turn-Over of Purchases Covered

under Schedule II, III, IV or V

b)

Total Turn-Over of Purchases including taxes, value of

Branch Transfers / consignment transfers received and

Labour/ job work charges.

a)

Difference

(Rs.)As per Audit

(Rs.)

As per return

(Rs.)Particulars

3) Computation of Purchases Eligible for Set-off

:

Seal and Signature of Auditor

Name :

14

Balance: Within the State purchases of taxable

goods from registered dealers eligible for set-off

(c) – (d+e+f+g+h+i+j+k+l+m+n)

o)

n) Less:-Other allowable deductions /reductions, if any.

(Please Specify)

m) Less:-Within the State purchases of taxfree goods

specified in Schedule “A”

l) Less:-Within the State purchases of taxable goods

which are fully exempted from tax u/s 8 but not covered

under section 8(1)

Tax rate wise break-up of Purchases from registered dealers eligible for set-off as per Box 3(o) above4.

As per ReturnsRate of

Tax

(%)Difference in

Tax Amount

As per Audit

Net Turn-Over of

Purchases Eligible

for Set -Off (Rs.)

Tax Amount (Rs.) Tax Amount (Rs.)

7654321

Net Turn-Over of

Purchases Eligible

for Set -Off (Rs.)

TOTAL

Less: - Reduct ion in the

amount of Set-off u/r 53

(2) of the of the

corresponding purchase

price of (Schedule B, C, D

& E) the goods

b) Less: - Reduction in the

amount of Set-off u/r 53

(1) of the corresponding

purchase price of (

Schedule C, D & E) the

goods above

Within the State purchases

of taxable goods from

registered dealers eligible

for set-off as per Box 4

above

a)

Purchase

Value Rs.Tax

Amount Tax

Amount

Purchase

Value Rs.

As per Audit Difference

in Tax

Amount

(Rs.)

Particulars As per Return

5. Computation of Set-off claimed.

:

Seal and Signature of Auditor

Name :

15

d) Amount of Set-off

available (a) – (c+b)

Less: - Reduction in the

amount of Set-off under

any other Sub-rule of rule

53

c)

6) Computation of Tax Payable

Particulars

6A) Aggregate of credit available for the period covered under Audit

As per Audit

(Rs.)

As per Returns

(Rs.)Difference

54321

a) Set off available as per Box 5 (d)

Amount already paid (Details as Per

ANNEXURE-A)b)

c) Excess Credit if any, as per Schedule II, III, IV, or V

to be adjusted against the liability as per this

Schedule

d) Adjustment of ET paid under Maharashtra Tax on

Entry of Goods into Local Areas Act, 2002/ Motor

Vehicle Entry Tax Act, 1987

Amount Credited as per Refund adjustment order

(Details As Per ANNEXURE-A)e)

Any other (Please Specify)f)

Total Available Credit (a+b+c+d+e+f)g)

6B) Sales tax payable and adjustment of CST / ET payable against available credit

a) Sales Tax Payable as per Box 2

b) Interest Payable under Section 30 (2)

c) Excess Credit as per this Schedule adjusted on

account of M.VAT payable, if any, as per Schedule

II, III, IV or V

d) Adjustment on account of CST payable as per

Schedule VI for the period under Audit

e) Adjustment on account of ET payable under the

Maharashtra Tax on Entry of Goods into Local Areas

Act, 2002/Motor Vehicle Entry Tax Act, 1987

f) Amount of Sales Tax Collected in Excess of the

amount of Sales Tax payable, if any, As per Box 2A

g) Total Amount (a+b+c+d+e+f)

6C) Tax payable or Amount of Refund Available

:

Seal and Signature of Auditor

Name :

16

a) Total Amount payable as per Box 6B(g)

b) Aggregate of Credit Available as per Box 6A(g)

c) Total Amount Payable (a-b)

d) Total Amount Refundable (b-a)

54321

:

Seal and Signature of Auditor

Name :

17

AUDIT REPORT

PART-3

SCHEDULE-II

Computation of Net Turn-Over of Sales liable to Composition

Particulars As per Return

(Rs.)As per Audit

(Rs.)

Difference

(Rs.)

Gross Turn-Over of Sales, including taxes as well as

Turn-over of Non- Sales Transactions like Value of

Branch Transfers/ Consignment Transfers and job work

charges

Less: - Turn-Over of Sales (including taxes thereon)

including inter-state Consignments and Branch

Transfers Covered under Schedule I, III, IV or V

Balance:- Turn-Over Considered under this

Schedule (1-2)

a) Total Turn-Over of Sales

b) Less:-Turn-Over of sales of goods excluded from the

Composition Scheme

d) Balance: Net Turn-Over of sales liable to tax under

Composition Scheme (a ) – (b+c)

RESTAURANT, CLUB, CATERER

ETC

1 2 3 4 5

1)

2)

3)

4) RETAILER

c) Less:-Other allowable deductions such as Goods

Returns etc.

5)

a) Total Turn-Over of Sales

6)

a) Total Turn-Over of Sales

BAKER

7) SECOND HAND MOTOR VEHICLES DEALER

a) Total Turn-Over of Sales

b) Less: Allowable deductions

c) Balance: Net Turn-Over of sales liable to tax under

composition option (a – b)

Total Turn-Over of Sales liable to tax under

composition option [4(d) +5(a) +6(a) +7(c)]

8)

:

Seal and Signature of Auditor

Name :

18

9) Computation of tax payable under the MVAT Act

Rate of

Tax

(%)

As per Returns

Turn-Over of

Sales

liable to tax (Rs.)

Tax Amount (Rs.) Turn-Over of Sales

liable to tax (Rs.)

As per Audit

Tax Amount (Rs.) Difference in

Tax Amount

7654321

TOTAL

:

Seal and Signature of Auditor

Name :

19

10) Computation of Purchases Eligible for Set-off

Sr.No. Particulars As per Returns As per Audit Difference

Total Turn-Over of purchases including taxes, value of

Branch Transfers, Consignment Transfers received and

Labour/ job work charges

a)

Less:-Turn-Over of Purchases covered under Schedule

I, III, IV or V

b)

c) Balance:-Turn-Over of Purchases considered under

this Schedule (a-b)

Less:-Value of Goods Return (inclusive of tax),

including reduction of purchase price on account of

rate difference and discount.

d)

Less:-Imports (Direct imports)e)

f) Less:-Imports (High seas purchases)

g) Less:-Inter-State purchases

h) Less:-Inter-State Branch Transfers, Consignment

Transfers received

i) Less:-Within the State Branch Transfers, Consignment

Transfers received where tax is to be paid by an Agent

j) Less:-Within the State purchases of taxable goods from

un-registered dealers

Less:-Purchases of taxable goods from registered

dealers under MVAT Act, and which are not eligible

for set-off

k)

Less:-Within the State purchases of taxable goods fully

exempted from tax u/s 8 other than purchases under

section 8(1)

l)

Less:-Within the State purchases of tax-free goods

specified in schedule “A”

m)

Less:-Other allowable deductions, if any (Please

Specify)

n)

Balance: Within the State purchases of taxable

goods from registered dealers eligible for set-off [c]-

d+e+f+g+h+i+j+k+l+m+n]

o)

:

Seal and Signature of Auditor

Name :

20

1

As per AuditAs per ReturnsSr.

No.

Tax rate wise break-up of Purchases from registered dealers eligible for set-off as per Box 10(o) above11)

Rate

of Tax

(%)

Net Turn-Over

of Purchases

Eligible for Set

–Off (Rs.)

Tax

Amount

(Rs.)

Net Turn-Over

of Purchases

Eligible for Set

–Off (Rs.)

Tax

Amount

(Rs.)

Difference in Tax

Amount (Rs.)

2 3 4 5 6 7

TOTAL

12)

As per AuditAs per ReturnSr.

No.

Computation of set-off claimed.

ParticularsTax

Amount

(Rs.)

Purchase

Value Rs.

Tax

Amount

(Rs.)

Difference

in Tax

Amount

(Rs.)

Purchase

Value Rs.

d) Amount of Set-off available

(a) – (c+b)

c) Less: - Reduction in the

amount of set off under any

other Sub-rule of rule 53

Less: - Reduction in the

amount of set off u/r 53 (2) of

the of the corresponding

purchase price of (Schedule B,

C, D & E) the goods

b) Less: - Reduction in the

amount of set off u/r 53 (1) of

the corresponding purchase

price of (Schedule C, D & E)

the goods

a) Within the State purchases of

taxable goods from registered

dealers eligible for setoff

as per Box 11 above

:

Seal and Signature of Auditor

Name :

21

13) Computation of Tax Payable

DifferenceAs per Audit

(Rs.)

As per Return

(Rs.)

ParticularsSr.No.

Aggregate of credit available for the period covered under Audit.13A)

Set-off available as per Box 12 (d)a)

Amount already paid (Details to entered in

Annexure-A)

b)

Excess Credit if any, as per Schedule I, III, IV, or V to

be adjusted against the liability as per this Schedule

c)

Adjustment of ET paid under Maharashtra Tax on Entry

of Goods into Local Areas Act, 2002/ Motor Vehicle

Entry Tax Act, 1987

d)

Amount Credited as per Refund adjustment order.

((Details as per Annexure-A)

e)

Any other (Please Specify)f)

Total Available Credit (a+b+c+d+e+f)g)

Excess Credit as per this Schedule adjusted on account

of M.VAT payable, if any, as per Schedule I, III, IV or

V

b)

Sales Tax Payable as per Box 9a)

13B) Sales tax payable and adjustment of CST / ET payable against available credit

d) Total Amount Refundable (b-a)

Total Amount Payable (a-b)c)

Total Amount payable as per Box 13B(g)

b) Aggregate of Credit Available as per Box 13A(g)

a)

13C) Tax payable or Amount of Refund Available

g) Total Amount (a+b+c+d+e+f)

f) Interest Payable under Section 30 (2)

e) Amount of Sales Tax Collected in Excess of the amount

of Sales Tax payable, if any (As per Box 6A)

d) Adjustment on account of ET payable under the

Maharashtra Tax on Entry of Goods into Local Areas

Act, 2002/Motor Vehicle Entry Tax Act, 1987

c) Adjustment on account of CST payable as per Schedule

VI for the period under Audit

:

Seal and Signature of Auditor

Name :

22

AUDIT REPORT

SCHEDULE-III

PART-3

Particulars As per Returns

(Rs.)

As per Audit

(Rs.)

DifferenceSr.No.

1. PART-A Computation of Net Turnover of Sales liable to tax:

l) Less:-Sales u/s 8 (1) i.e. Interstate Sales including

Central Sales Tax, Sales in the course of imports,

exports and value of Branch Transfers/ Consignment

transfers outside the State (Schedule-VI)

k) Less:-Value of Branch Transfers/ Consignment

Transfers within the State if the tax is to be paid by the

Agent.

j) Less:-Net Tax amount (Tax included in sales shown in

(a) above less Tax included in (b) and (d) above)

Balance:- Net turnover of sales including, taxes, as well

as turnover of non sales transactions like Branch

Transfers / Consignment Transfers and job works

charges, etc [ (e) – (f+g+h)]

i)

h) Turnover of sales (excluding taxes) relating to on-going

leasing contracts (Computation of turnover of sales

liable to tax to be shown in Part D)

g) Turnover of sales (excluding taxes) relating to on-going

works contracts (Computation of turnover of sales

liable to tax to be shown in Part C)

Less:-Turnover of sales under composition scheme(s),

other than Works Contracts under composition option

(Computation of turnover of sales liable to tax to be

shown in Part B)

f)

e) Balance: -Turnover of sales including, taxes as well as

turnover of non sales transactions like value of Branch

Transfer, Consignment Transfers, job work charges etc

[(c)-(d)]

d) Less:-Value of Goods Return (inclusive of tax),

including reduction of sales price on account of rate

difference and discount.

c) Balance:- Turn-Over Considered under

this Schedule (a-b)

Less: - Turn-Over of Sales (including taxes thereon)

including inter-state Consignments and Branch

Transfers Covered under Schedule I, II, IV or V

b)

a) Gross turnover of sales including, taxes as well as

turnover of non sales transactions like value of Branch

Transfer, Consignment Transfers, job work charges etc

1 2 3 4 5

:

Seal and Signature of Auditor

Name :

23

s) Total:- Net Turnover of Sales Liable to tax [(i) -

(j+k+l+m+n+o+p+q+r)]

r) Other allowable reductions/deductions, if any (Please

specify)

q) Less:- Labour/Job work charges

p) Sales of tax-free goods specified in Schedule A

o) Amount paid by way of price for sub-contract

n) Non-taxable Labour and other charges / expenses for

Execution of Works Contract

Less:-Sales of taxable goods fully exempted u/s. 8 other

than sales under section 8(1) and covered in Box 1(l)

m)

Difference

(Rs.)

As per Audit

(Rs.)

As per Returns

(Rs.)

ParticularsSr.

No.

2. PART-B Computation of Net Turnover of Sales liable to tax under Composition:

A) Turnover of sales (excluding taxes) under composition

scheme(s) [Same as 1(f)]

RETAILERB)

a) Total Turnover of Sales

b) Less:-Turnover of sales of goods excluded from the

Composition Scheme

c) Less:-Allowable deductions such as Goods

Return etc.

d) Balance: Net turnover of sales liable to tax under

composition option [ (a) – (b+c)]

C) RESTAURANT , CLUB, CATERER ETC.

Total Turnover of Salesa)

D)

a) Total Turnover of Sales

BAKER

E)

Total Turnover of Salesa)

SECOND HAND MOTOR VEHICLE DEALER

b) Less: Allowable reductions / deductions

c) Balance: Net turnover of sales liable to tax under

composition option (a – b)

Total net turnover of sales liable to tax under

composition option [2(B)(d)+2(C ) (a)+2(D)(a)

+2(E)(c )]

F)

1 2 3 4 5

3. PART-C

Computation of net turnover of sales relating to on-going works contracts liable to tax under section

96(1)(g) the MVAT Act, 2002:

As per Returns

(Rs.)As per Audit

(Rs.)

Difference

(Rs.)

Particulars

:

Seal and Signature of Auditor

Name :

24

2 3 4 51

c) Balance: Net turnover of sales liable to tax (a –b)

b) Less: Turnover of sales exempted from tax

a) Turnover of sales (excluding taxes) Relating to

On-going Leasing Contract [same as Box 1(h)]

Particulars As per Returns

(Rs.)

As per Audit

(Rs.)

Difference

(Rs.)

PART-D

Computation of net turnover of sales relating to on-going leasing contracts liable to tax under Section 96(1) (f)

of the MVAT Act, 2002:

4.

e) Balance: Net turnover of sales liable to tax /

composition [(a)] –[ (b+c+d)]

d) Less:-Deductions u/s 6(A) of the ‘Earlier Law’

Less:-Deductions u/s 6 of the ‘Earlier Law’c)

Less:-Turnover of sales exempted from taxb)

a) Turnover of sales (excluding tax / composition) during

the period [Same as Box 1(g)]

5) Computation of tax payable under the MVAT Act

Rate of

Tax

(%)

As per Returns

Turn-Over of

Sales

liable to tax (Rs.)

Tax Amount (Rs.) Turn-Over of

Sales

liable to tax (Rs.)

As per Audit

Tax Amount (Rs.)Difference in

Tax Amount

7654321

TOTAL

Sales Tax collected in Excess of the

Amount of Tax payable

Difference

(Rs.)

As per Audit

(Rs.)As per return

(Rs.)

5A)

Computation of Purchases Eligible for Set-off6)

Particulars Difference

(Rs.)

As per Audit

(Rs.)

As per Returns

(Rs.)

Balance:- Turn-Over of Purchases Considered

under this Schedule (a-b)

c)

Less:- Turn-Over of Purchases Covered under

Schedule I, II, IV or V

b)

a) Total Turn-Over of Purchases including taxes, value of

Branch Transfers / consignment transfers received and

Labour/ job work charges.

:

Seal and Signature of Auditor

Name :

25

k) Less:-Purchases of the taxable goods from registered

dealers under MVAT Act, 2002 and which are not

eligible for set-off

Less:-Within the State purchases of taxable goods from

un-registered dealers

j)

Less:-Within the State Branch Transfers / Consignment

Transfers received where tax is to be paid by an Agent

i)

h) Less:-Inter-State Branch Transfers/ Consignment

Transfers received

Less:-Inter-State purchasesg)

f) Less:-Imports (Direct imports)

e) Less:-Imports (High seas purchases)

Less:-Value of Goods Return (inclusive of tax),

including reduction of purchase price on account of rate

difference and discount.

d)

Balance: Within the State purchases

of taxable goods from registered dealers eligible for

set-off (c) – (d+e+f+g+h+i+j+k+l+m+n)

o)

Less:-Other allowable deductions /reductions, if any.

(Please Specify)

n)

m) Less:- Within the State purchases of

tax-free goods specified in Schedule A

Less:-Within the State purchases of taxable goods

which are fully exempted from tax u/s 8 but not

covered under section 8(1)

l)

7) Tax rate wise break-up of Purchases from registered dealers eligible for set-off as per Box 6(o) above

Rate of

Tax

(%)

As per Returns

Net Turnover of

Purchases

Eligible for Set

–Off (Rs.)

Tax Amount

(Rs.)

As per Audit

Tax Amount

(Rs.)

Difference in

Tax

(Rs.)

Net Turnover of

Purchases

Eligible for Set

–Off (Rs.)

Sr.

No.

TOTAL

8)

As per AuditAs per ReturnSr.

No.

Computation of set-off claim.

ParticularsTax

Amount

Purchase

Value Rs.

Tax

Amount

Difference

in Tax

Amount

(Rs.)

Purchase

Value Rs.

Within the State purchases of

taxable goods from registered

dealers eligible for setoff

as per Box 7 above

a)

:

Seal and Signature of Auditor

Name :

26

b)

d) Amount of Set-off available

(a) – (c+b)

Less: - Reduction in the

amount of set off under any

other Sub-rule of rule 53

c)

Less: - Reduction in the

amount of set off u/r 53 (2) of

the of the corresponding

purchase price of (Schedule B,

C, D & E) the goods

Less: - Reduction in the

amount of set off u/r 53 (1) of

the corresponding purchase

price of (Schedule C, D & E)

the goods

9)

DifferenceAs per Audit

(Rs.)

As per Returns

(Rs.)

ParticularsSr.

No.

Computation of Tax Payable

9A) Aggregate of credit available

Set off available as per Box 8 (d)a)

b) Amount already paid (Details as Per ANNEXURE-A)

c) Excess Credit if any, as per Schedule I, II, IV, or V to

be adjusted against the liability as per this Schedule

d) Adjustment of ET paid under Maharashtra Tax on Entry

of Goods into Local Areas Act, 2002/ Motor Vehicle

Entry Tax Act, 1987

Amount Credited as per Refund adjustment order

(Details as Per ANNEXURE-A)

e)

f) Works Contract TDS

g) Any other ( Please Specify)

f) Interest Payable under Section 30 (2)

Amount of Sales Tax Collected in Excess of the amount

of Sales Tax payable, if any (As per Box 5A)

e)

d) Adjustment on account of ET payable under the

Maharashtra Tax on Entry of Goods into Local Areas

Act, 2002/Motor Vehicle Entry Tax Act, 1987

Adjustment on account of CST payable as per Schedule

VI for the period under Audit

c)

b) Excess Credit as per this Schedule adjusted on account

of M.VAT payable, if any, as per Schedule I, II, IV or V

a) Sales Tax Payable Box 5

2 3 4 51

9B) Sales tax payable and adjustment of CST / ET payable against available credit

Total Available Credit (a+b+c+d+e+f+g)h)

:

Seal and Signature of Auditor

Name :

27

Total Amount refundable (b-a)d)

Total Amount Payable (a-b)c)

b) Aggregate of Credit Available as per Box 9A(h)

a) Total Amount payable as per Box 9B(g)

Tax payable or Amount of Refund Available9C)

g) Total Amount.(a+b+c+d+e+f)

:

Seal and Signature of Auditor

Name :

28

AUDIT REPORT

SCHEDULE-IV

PART-3

Expansion UnitNew Unit

Deferment of tax payableExemption from tax

Type of Unit

Mode of incentive

Please tick whichever is applicable

c)

b)

a)

Certificate of Entitlement (COE) No Eligibility Certificate (EC) No.1)

2)

3)

:

Seal and Signature of Auditor

Name :

29

4) Computation of Net Turnover of Sales liable to tax

Sr.

No.DifferenceAs per Audit

(Rs.)

As per Returns

(Rs.)

Particulars

1 5432

Gross turnover of sales including, taxes as well as

turnover of non sales transactions like value of Branch

Transfers, Consignment transfers and job work charges

etc.

a)

Less: - Turn-Over of Sales (including taxes thereon)

including inter-state Consignments and Branch

Transfers Covered under Schedule I, II, III or V

b)

c) Balance:- Turn-Over Considered

under this Schedule (a-b)

Less:-Value of Goods Return (inclusive of tax),

including reduction of sale price on account of rate

difference and discount.

d)

e) Less:-Net Tax amount (Tax included in sales shown in

(c) above less Tax included in (a) and (d) above)

f) Less:-Value of Branch Transfers / Consignment

Transfers within the State if is to be paid by the Agent.

Less:-Sales u/s 8 (1) i.e. Interstate Sales including

Central Sales Tax, Sales in the course of imports,

exports and value of Branch Transfers/ Consignment

transfers outside the State.

g)

Less: - Sales of tax-free goods specified in Schedule Ah)

Less:-Sales of taxable goods fully exempted u/s. 8(4)

[other than sales under section 8 (1) and shown in Box

4(g)]

i)

j) Less:-Sales of taxable goods fully exempted u/s. 8

[other than sales under section 8(1) and 8 (4) and shown

in Box 4(g)]

Less:-Job/Labour work chargesk)

l) Less:-Other allowable reductions/deductions, if any

Balance Net Turnover of Sales liable to tax [c]

–[d+e+f+g+h+i+j+k+l]

m)

:

Seal and Signature of Auditor

Name :

30

Computation of Sales tax payable under the MVAT Act 5)

As per Returns As per AuditSr.

No.

Rate of

Tax

(%) Turnover of

Sales

liable to Tax (Rs.)

Tax Amount

(Rs.)Turnover of

Sales

liable to Tax (Rs.)

Tax Amount

(Rs.)

Difference in

Tax

(Rs.)

1 2 3 4 5 6 7

I Turn-Over of Sales eligible for incentive (Deferment of Tax)

0 0 0 0 01

Sub-Total A 0 0 0 0 0

As per Returns As per AuditSr.

No.

Rate of

Tax

(%) Turnover of

Sales

liable to Tax (Rs.)

Tax Amount

(Rs.)Turnover of

Sales

liable to Tax (Rs.)

Tax Amount

(Rs.)

Difference in

Tax

(Rs.)

1 2 3 4 5 6 7

II Other Sales (Turn-Over of Sales Non-eligible for Incentives)

0 0 0 0 01

Sub-Total B 0 0 0 0 0

III 0 0 0 0 0Total

As per AuditAs per Returns Difference 5A) Sales Tax collected in Excess of the

Amount of Tax payable

6)

54321

Computation of Purchases Eligible for Set- off

Sr.

No.

As per Audit

(Rs.)

Difference

(Rs.)

As per Returns

(Rs.)

Particulars

Total Turn-Over of Purchases including taxes, value of

Branch Transfers / consignment transfers received and

Labour/ job work charges.

a)

b) Less:- Turn-Over of Purchases Covered

under Schedule I, II, III or IV

Balance:- Turn-Over of Purchases Considered

under this Schedule (a-b)

c)

Less:-Value of Goods Return (inclusive of tax),

including reduction of purchase price on account of rate

difference and discount.

d)

:

Seal and Signature of Auditor

Name :

31

e) Less:-Imports (Direct imports)

Less:-Imports (High seas purchases)f)

g) Less:-Inter-State purchases

Less:-Inter-State Branch Transfers/ Consignment

Transfers received

h)

i) Less:-Within the State Branch Transfers / Consignment

Transfers received where tax is to be paid by an Agent

Less:-Within the State purchases of taxable goods from

un-registered dealers

j)

k) Less:-Purchases of the taxable goods from registered

dealers under MVAT Act, 2002 and which are not

eligible for set-off

l) Less:-Within the State purchases of taxable goods

which are fully exempted from tax u/s 8 [other than u/s

8(1)] and 41(4)

m) Less:-Within the State purchases of taxfree goods

specified in Schedule “A”

n) Less:-Other allowable deductions /reductions, if any.

(Please Specify)

o) Balance: Within the State purchases of taxable

goods from registered dealers eligible for set-off

(c) – (d+e+f+g+h+i+j+k+l+m+n)

7) Tax rate wise break-up of Purchases from registered dealers eligible for set-off as per Box 6(o) above

Rate of

Tax

(%)

As per Returns

Net Turnover of

Purchases

Eligible for Set

–Off (Rs.)

Tax Amount

(Rs.)

As per Audit

Tax Amount

(Rs.)

Difference in

Tax Amount

(Rs.)

Net Turnover of

Purchases

Eligible for Set

–Off (Rs.)

Sr.

No.

7654321

TOTAL

:

Seal and Signature of Auditor

Name :

32

8)

Difference

in Tax

Amount

(Rs.)

Tax

Amount

As per Audit

Purchase

Value Rs.

Tax

Amount

Purchase

Value Rs.

As per ReturnParticulars

Sr.

No.

Computation of set-off claim.

a)

b)

c)

d)

Less: - Reduction in the

amount of set off u/r 53 (1) of

the corresponding purchase

price of (Schedule C, D & E)

the goods

Less: - Reduction in the

amount of set off u/r 53 (2) of

the of the corresponding

purchase price of (Schedule

B, C, D & E) the goods

Less: - Reduction in the

amount of set off under any

other Sub-rule of rule 53

Amount of Refund Set-off

available (a) – (c+b)

Within the State purchases of

taxable goods from registered

dealers eligible for setoff

as per Box 7 above

e) Amount of Refund relating

to Raw Materials for use in

manufacture of goods

eligible or incentives

f) Amount of Set-off relating

other purchases.

Amount Credited as per Refund adjustment order

(Details as Per ANNEXURE-A)

e)

Adjustment of ET paid under Maharashtra Tax on Entry

of Goods into Local Areas Act, 2002/ Motor Vehicle

Entry Tax Act, 1987

d)

Excess Credit if any, as per Schedule I, II, III, or V to

be adjusted against the liability as per this Schedule

c)

b) Amount already paid (Details as Per ANNEXURE-A)

DifferenceAs per Audit

(Rs.)

As per Returns

(Rs.)

ParticularsSr.

No.

Computation of Tax Payable9)

1 2 3 4 5

Refund or Set off available as per Box 8 (f)a)

Aggregate of credit available for the period covered under Audit9A)

:

Seal and Signature of Auditor

Name :

33

g) Total Available Credit (a+b+c+d+e+f)

Any other ()f)

9B) Sales tax payable and adjustment of CST / ET payable against available credit

a) Sales Tax Payable as per Box 5 (III)

Less:- Sales Tax deferred as per Box-5 I.(e)

b) Excess Credit as per this Schedule adjusted on account

of M.VAT payable, if any, as per Schedule I, II, III or V

c) Adjustment on account of CST payable as per Schedule

VI for the period under Audit

d) Adjustment on account of ET payable under the

Maharashtra Tax on Entry of Goods into Local Areas

Act, 2002/Motor Vehicle Entry Tax Act, 1987

e) Amount of Sales Tax Collected in Excess of the amount

of Sales Tax payable, if any As per Box 5A

f) Interest Payable under Section 30 (2)

g) Total Amount.(a+b+c+d+e+f)

2 3 4 51

Total Amount refundable (b-a)d)

Total Amount Payable (a-b)c)

Aggregate of Credit Available as per Box 9A(g)b)

Total Amount payable as per Box 9B(g)a)

Tax payable or Amount of Refund Available9C)

COE No.

Location of the Unit

ToFromEligibility Period

10 A Details of benefits availed under the package Scheme of Incentives(Details to be given Separately for each EC)

10 a Calculatin of Cumulative Quantum of Benefits (CQB) Under-rule 78(2)(a)

As per AuditAs per ReturnsRate of tax

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

CQB Amount

( Rs.)

Difference in

CQB Amout

54b4a3b3a21

Sr.

NoCQB Amount

( Rs.)

0 0 0 0 0

Sub Total a 00 0 0 0

:

Seal and Signature of Auditor

Name :

34

10 b Calculatin of Cumulative Quantum of Benefits (CQB) Under-rule 78(2)(b)

As per AuditAs per ReturnsRate of tax

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

CQB Amount

( Rs.)

Difference in

CQB Amout

54b4a3b3a21

Sr.

NoCQB Amount

( Rs.)

0 0 0 0 0

Sub Total b 00 0 0 0

Total A + B 0 0 0 0 0

10 D Calculation of deferment benefit Under-rule 81

Sr.

No

Particulars

As per Returns

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

As per Audit

Difference in

CQB AmoutAmount

( Rs.)

(Deferrable)

Amount

( Rs.)

(Deferrable)

a)

b)

c)

Amount of

MVAT payable

Amount of CST

payable

Total amount of

tax deferred (a+b)

10 E Status of CQB u/r 78 / Tax deferment u/r 81

ParticularsSr.

No

a)

b)

c)

d)

Sanctioned monetary ceiling

Opening balance of the monitory ceiling at the

beginning of the period for which the return is filed

Less : Amount of CQB / Tax deferment for the period

of this return as per Box 10 C or 10 -D (c),

as the case may be

Less : Amount of Refund claimed as per Rule 79 (2)

Less:-Benefit of Luxury Tax claimed for TIS-99 under

Luxury Tax Act, 1987 for the period of audit

e)

f) Closing balance of the monitory ceiling at the end of the

period [(b) - (c + d+e)]

DifferenceAs per AuditAs per Returns

COE No.

Location of the Unit

ToFromEligibility Period

11 A Details of benefits availed under the package Scheme of Incentives(Details to be given Separately for each EC)

:

Seal and Signature of Auditor

Name :

35

11 a Calculatin of Cumulative Quantum of Benefits (CQB) Under-rule 78(2)(a)

As per AuditAs per ReturnsRate of tax

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

CQB Amount

( Rs.)

Difference in

CQB Amout

54b4a3b3a21

Sr.

NoCQB Amount

( Rs.)

0 0 0 0 0

Sub Total a 00 0 0 0

11 b Calculatin of Cumulative Quantum of Benefits (CQB) Under-rule 78(2)(b)

As per AuditAs per ReturnsRate of tax

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

CQB Amount

( Rs.)

Difference in

CQB Amout

54b4a3b3a21

Sr.

NoCQB Amount

( Rs.)

0 0 0 0 0

Sub Total b 00 0 0 0

Total A + B 0 0 0 0 0

11 D Calculation of deferment benefit Under-rule 81

Sr.

No

Particulars

As per Returns

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

As per Audit

Difference in

CQB AmoutAmount

( Rs.)

(Deferrable)

Amount

( Rs.)

(Deferrable)

a)

b)

c)

Amount of

MVAT payable

Amount of CST

payable

Total amount of

tax deferred (a+b)

:

Seal and Signature of Auditor

Name :

36

11 E Status of CQB u/r 78 / Tax deferment u/r 81

ParticularsSr.

No

a)

b)

c)

d)

Sanctioned monetary ceiling

Opening balance of the monitory ceiling at the

beginning of the period for which the return is filed

Less : Amount of CQB / Tax deferment for the period

of this return as per Box 11 C or 11 -D (c),

as the case may be

Less : Amount of Refund claimed as per Rule 79 (2)

Less:-Benefit of Luxury Tax claimed for TIS-99 under

Luxury Tax Act, 1987 for the period of audit

e)

f) Closing balance of the monitory ceiling at the end of the

period [(b) - (c + d+e)]

DifferenceAs per AuditAs per Returns

COE No.

Location of the Unit

ToFromEligibility Period

12 A Details of benefits availed under the package Scheme of Incentives(Details to be given Separately for each EC)

12 a Calculatin of Cumulative Quantum of Benefits (CQB) Under-rule 78(2)(a)

As per AuditAs per ReturnsRate of tax

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

CQB Amount

( Rs.)

Difference in

CQB Amout

54b4a3b3a21

Sr.

NoCQB Amount

( Rs.)

0 0 0 0 0

Sub Total a 00 0 0 0

12 b Calculatin of Cumulative Quantum of Benefits (CQB) Under-rule 78(2)(b)

As per AuditAs per ReturnsRate of tax

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

CQB Amount

( Rs.)

Difference in

CQB Amout

54b4a3b3a21

Sr.

NoCQB Amount

( Rs.)

0 0 0 0 0

Sub Total b 00 0 0 0

Total A + B 0 0 0 0 0

:

Seal and Signature of Auditor

Name :

37

12 D Calculation of deferment benefit Under-rule 81

Sr.

No

Particulars

As per Returns

Turnover of sales

eligible goods liable

to tax (Rs.)

Turnover of sales

eligible goods liable

to tax (Rs.)

As per Audit

Difference in

CQB AmoutAmount

( Rs.)

(Deferrable)

Amount

( Rs.)

(Deferrable)

a)

b)

c)

Amount of

MVAT payable

Amount of CST

payable

Total amount of

tax deferred (a+b)

12 E Status of CQB u/r 78 / Tax deferment u/r 81

ParticularsSr.

No

a)

b)

c)

d)

Sanctioned monetary ceiling

Opening balance of the monitory ceiling at the

beginning of the period for which the return is filed

Less : Amount of CQB / Tax deferment for the period

of this return as per Box 12 C or 12 -D (c),

as the case may be

Less : Amount of Refund claimed as per Rule 79 (2)

Less:-Benefit of Luxury Tax claimed for TIS-99 under

Luxury Tax Act, 1987 for the period of audit

e)

f) Closing balance of the monitory ceiling at the end of the

period [(b) - (c + d+e)]

DifferenceAs per AuditAs per Returns

:

Seal and Signature of Auditor

Name :

38

SCHEDULE-V

PART-3

AUDIT REPORT

1)

Difference

Amount (Rs.)

As per Audit

Amount (Rs.)

As per Returns

Amount (Rs.)

ParticularsSr.

No.

Computation of Net Turnover of Sales liable to tax

a) Gross turnover of sales including, taxes as well as

turnover of non sales transactions like value of Branch

Transfer, Consignment Transfers, job work charges etc

b) Less:- Turn-Over of Sales (including taxes thereon)

including inter-state Consignments and Branch

Transfers Covered under Schedule I, II, III, or IV

c) Balance:- Turn-Over Considered under

this Schedule (a-b)

d) Less:-Value of Goods Return (inclusive of tax),

ncluding reduction of sale price on account of rate

difference and discount.

e) Less:-Net Tax amount (Tax included insales shown in

(c) above less Tax included in (a) and (d) above)

f) Less:-Value of Consignment Transfers within the State

if is to be paid by the Agent.

g) Less:-Sales u/s 8 (1) i.e. Interstate Sales including

Central Sales Tax, Sales in the course of imports,

exports and value of Branch Transfers/ Consignment

transfers outside the State

h) Less:-Sales of tax-free goods specified in Schedule A

i) Less:-Sales of taxable goods fully exempted u/s. 8(1)

[other than sales under section 8 (1) and shown in Box

1(g)] and 41 (4)

j) Less:-Job/Labour work charges

k) Less:-Other allowable reductions/ deductions, if any

(Please specify)

l) Balance Net Turn-Over of sales liable to tax [c] –

[d+e+f+g+h+i+j+k]

2)

Sr.

No.

Computation of tax payable under the MVAT Act

Tax

Amount

(Rs.)

Tax

Amount

(Rs.)

Difference

(Rs.)

Turnover of

Sales liable to

Tax (Rs.)

Quantity

(Liter)

Rate of

Tax

Sch. Entry

No

Turnover of

Sales liable to

Tax (Rs.)

Quantity

(Liter)

00000D5(a)(i)b)

:

Seal and Signature of Auditor

Name :

39

00000Rs. OneD5(a)(i)c)

00000D5(a)(ii)d)

00000Rs. OneD5(a)(ii)e)

00000D5(b)f)

00000Rs. OneD5(b)g)

00000D6h)

00000D7i)

00000D8j)

00000D9k)

00000D10(a)(i)l)

00000Rs. OneD10(a)(i)m)

00000Sch D. Goods

(Inter Oil Co.

Sales of Notified

Motor Sprits)

a)

00000D10(a)(ii)n)

00000Rs. OneD10(a)(ii)o)

00000D10(b)p)

00000Rs. OneD10(b)q)

000 00(A) Sub-total (a to q)

000004%C8s)

000004%C27t)

000004%C58u)

000 00(B) Sub-total (r to t)

000004%Othersv)

0000012.5%Othersw)

000 00(C) Sub-total (u to v)

Sales Tax collected in Excess of the Amount of

Tax payable

2A) DifferenceAs per AuditAs per Returns

TOTAL (A+B+C)

3) Computation of Purchases Eligible for Set- off

Sr.

No.

As per Audit

(Rs.)

Difference

(Rs.)

As per Returns

(Rs.)

Particulars

Total Turn-Over of Purchases including taxes, value of

Branch Transfers / consignment transfers received and

Labour/ job work charges.

a)

b) Less:- Turn-Over of Purchases Covered

under Schedule I, II, III or V

:

Seal and Signature of Auditor

Name :

40

Balance:- Turn-Over of Purchases Considered

under this Schedule (a-b)

c)

Less:-Value of Goods Return (inclusive of tax),

including reduction of purchase price on account of rate

difference and discount.

d)

e) Less:-Imports (Direct imports)

Less:-Imports (High seas purchases)f)

g) Less:-Inter-State purchases

Less:-Inter-State Branch Transfers/ Consignment

Transfers received

h)

i) Less:-Within the State Branch Transfers / Consignment

Transfers received where tax is to be paid by an Agent

Less:-Within the State purchases of taxable goods from

un-registered dealers

j)

k) Less:-Purchases of the taxable goods from registered

dealers under MVAT Act, 2002 and which are not

eligible for set-off

l) Less:-Within the State purchases of taxable goods

which are fully exempted from tax u/s 8 [other than u/s

8(1)] and 41(4)

m) Less:-Within the State purchases of taxfree goods

specified in Schedule “A”

n) Less:-Other allowable deductions /reductions, if any.

(Please Specify)

o) Balance: Within the State purchases of taxable

goods from registered dealers eligible for set-off

(c) – (d+e+f+g+h+i+j+k+l+m+n)

4) Tax rate wise break-up of Purchases from registered dealers eligible for set-off as per Box 3(o) above

Rate of

Tax

(%)

As per Returns

Net Turnover of

Purchases

Eligible for Set

–Off (Rs.)

Tax Amount

(Rs.)

As per Audit

Tax Amount

(Rs.)

Difference in

Tax

(Rs.)

Net Turnover of

Purchases

Eligible for Set

–Off (Rs.)

Sr.

No.

TOTAL

5)

Difference

in Tax

Amount

(Rs.)

Tax

Amount

As per Audit

Purchase

Value Rs.

Tax

Amount

Purchase

Value Rs.

As per ReturnParticulars

Sr.

No.

Computation of set-off claimed.

b) Within the State purchases of

taxable goods from registered

dealers eligible for setoff

as per Box 3 (o) above

:

Seal and Signature of Auditor

Name :

41

b)

c)

d) Amount of Set-off available

(a) – (c+b)

Less: - Reduction in the

amount of set off under any

other Sub-rule of rule 53

Less: - Reduction in the

amount of set off u/r 53 (2) of

the of the corresponding

purchase price of (Schedule B,

C, D & E) the goods

Less: - Reduction in the

amount of set off u/r 53 (1) of

the corresponding purchase

price of (Schedule C, D & E)

the goods

Tax payable or Amount of Refund Available6C)

g) Total Amount.(a+b+c+d+e+f)

f) Interest Payable under Section 30 (2)

Amount of Sales Tax Collected in Excess of the amount

of Sales Tax payable, if any (As per Box 2A)

e)

d) Adjustment on account of ET payable under the

Maharashtra Tax on Entry of Goods into Local Areas

Act, 2002/Motor Vehicle Entry Tax Act, 1987

Adjustment on account of CST payable as per Schedule

VI for the period under Audit

c)

b) Excess Credit as per this Schedule adjusted on account

of M.VAT payable, if any, as per Schedule I, II, IV or

IV

a) Sales Tax Payable Box 5

Total Available Credit (a+b+c+d+e+f)g)

Any other (Please Specify)f)

e) Amount Credited as per Refund adjustment order

(Details as Per ANNEXURE-A)

Adjustment of ET paid under Maharashtra Tax on Entry

of Goods into Local Areas Act, 2002/ Motor Vehicle

Entry Tax Act, 1987

d)

Excess Credit if any, as per Schedule I, II, IV, or IV to

be adjusted against the liability as per this Schedule

c)

Amount already paid (Details as Per ANNEXURE-A)b)

a) Set off available as per Box 5 (d)

Aggregate of credit available6A)

Computation of Tax Payable

Sr.

No.

Particulars As per Returns

(Rs.)

As per Audit

(Rs.)

Difference

6)

6B) Sales tax payable and adjustment of CST / ET payable against available credit

:

Seal and Signature of Auditor

Name :

42

Total Amount Refundable (b-a)d)

Total Amount Payable (a-b)c)

b) Aggregate of Credit Available as per Box 6A(g)

a) Total Amount payable as per Box 6B(g)

:

Seal and Signature of Auditor

Name :

43

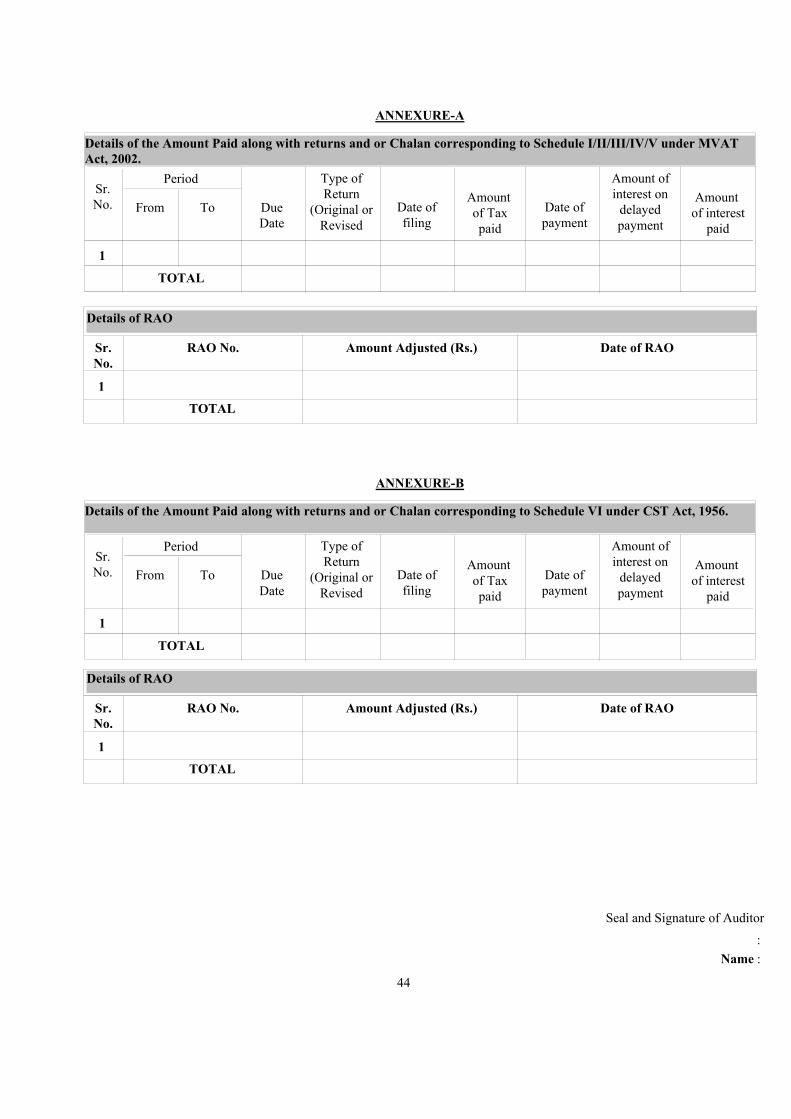

ANNEXURE-A

Details of the Amount Paid along with returns and or Chalan corresponding to Schedule I/II/III/IV/V under MVAT

Act, 2002.

Sr.

No.

Period

From To Due

Date

Type of

Return

(Original or

Revised

Date of

filing

Amount

of Tax

paid

Date of

payment

Amount of

interest on

delayed

payment

Amount

of interest

paid

1

TOTAL

Details of RAO

Date of RAOAmount Adjusted (Rs.)RAO No.Sr.

No.

1

TOTAL

ANNEXURE-B

Details of the Amount Paid along with returns and or Chalan corresponding to Schedule VI under CST Act, 1956.

Sr.

No.

Period

From To Due

Date

Type of

Return

(Original or

Revised

Date of

filing

Amount

of Tax

paid

Date of

payment

Amount of

interest on

delayed

payment

Amount

of interest

paid

1

TOTAL

Details of RAO

Date of RAOAmount Adjusted (Rs.)RAO No.Sr.

No.

1

TOTAL

:

Seal and Signature of Auditor

Name :

44

Details of Tax Deducted at Source (TDS) certificates received corresponding to item (vi) (c ) of Table No.-2 of Part-1.

ANNEXURE C

Amount of

TDS as per

certificate.

Sr.

No.

TIN No. of

the

employer, if any

Date of

Certificate.Name of the employer

deducting the taxAddress of the employer

deducting the tax

1

TOTAL

ANNEXURE-D

Details of Tax Deducted at Source (TDS) certificates issued.

Sr.

No.

Interest

payable

if any

Amount

paid (Rs.)

Name of the

Dealer

TIN if

any

Turnover

on which

TDS made

Amount of

tax to be

deducted.

(Rs)

Amount of

tax

deducted.

(Rs)

1

TOTAL

:

Seal and Signature of Auditor

Name :

45

ANNEXURE E

Computation Of Set-Off Claim On The Basis Of Tax Paid Purchases Effected From Registered Dealers.

SECTION-1:-Total tax paid purchases effected from the Local Supplier during the period under Audit

Gross Total (c+d)

e

Tax Amount

d

Net Purchase Value

cba

Particulars/

Tax Rate (%)

Sr.

No.

0 0 01

000TOTAL

SECTION-2:-Details of Tax paid purchases on which Set-off is not admissible U/R 54 (Out of Section-1)

Gross Total (c+d)

e

Tax Amount

d

Net Purchase Value

cba

Particulars/

Tax Rate (%)

Sr.

No.

0 0 01

000TOTAL

SECTION-3:-Details of Tax paid purchases of Capital Assets on which full set-off is available (Out of Section-1)

Gross Total (c+d)

e

Tax Amount

d

Net Purchase Value

cba

Particulars/

Tax Rate (%)

Sr.

No.

0 0 01

000TOTAL

(Note:- For each sub-rule a separate Table is to be used)

SECTION-4:-Details of Tax paid purchases on which set-off is admissible after reduction under rule 53.

Sr.

No.

Reduction,

if any

Rule under

which the

set-off is

claimed

Tax Rate Net

Purchases

value

Tax Total

(d+e)

Tax amount

eligible

for set-off

(e-g)

b c d e f g ha

1

TOTAL

:

Seal and Signature of Auditor

Name :

46

SECTION 5-Details of Total Tax paid purchases Effected from Registered Dealers on which Full Set-off is calculated

and allowed as per Rule 52. (Section-1 less Section 2 to 4)

Sr.

No.Tax Amount Gross Total (3+4)Net Purchase Value

Particulars/

Tax Rate (%)

4321 5

1

TOTAL

SECTION-6:-Amount of Total Set-off Available to Dealer

Set-off determined by

auditor

Difference (c-d)Amount of Set-off claimed

by the dealer in Return

dcba e

Particulars/

Tax Rate (%)

Sr.

No.

1

Reasons for Excess or Short claim Set-off:-

TOTAL

Financial Ratios for the year under audit and other information.

ANNEXURE -F

Gross Profit to Gross Sales1.

Method of computation

and observations, if anyPrevious YearCurrent YearParticulars

(a) As per Profit & Loss A/c

Net Profit before tax to Gross Sales2.

Ratio Net Local Sales in Maharashtra State to Total

Sales (Rs) (excluding tax under VAT & CST Acts.)

1.

Particulars

(To be reported as determined by the Auditor)Current

Year

Previous

Year

Method of computation

and observations, if any

Information to be furnished in relation to the sales effected within/from Maharashtra(b)

Ratio of Inter-State Stock Transfer from Maharashtra

State to Total Sales (Rs.)

2.

Ratio of Non Sales (e.g. Job work, Labour charges,

etc) receipts to Total Sales (Rs.)

3.

:

Seal and Signature of Auditor

Name :

47

Ratio of Net Local Sales from row 1 to inter-State

stock transfer

4.

Ratio of Net Local Sales of taxable goods to net sales

from row 1

5.

Ratio of net Local Sales of tax-free goods to net sales

from row 1

6.

Percentage of net inter-State sales excluding Export

to net sales from row 1

7.

Ratio of Export sales to net sales from row 18.

Ratio of Gross receipts to Gross Turn Over of Sales9.

10. Ratio of set-off claimed to net sales from row 1

Ratio of Gross Tax (MVAT & CST) to turnover of

net sales from row 1

11.

Ratio of Closing stock of finished goods to Net Sales

from row 112.

Opening stock of finished goods including WIP (in

Maharashtra) Rs.

13.

Closing stock of finished goods including WIP (in

Maharashtra) Rs.

14.

Details of Declarations or Certificates (in Form-H) not received

ANNEXURE -H

Differential

tax liability

(Rs.)

(Col. 9-Col.

6)

Rate of

tax

applicable

(Local

Rate)

Taxable

Amount

(Rs.) Net

Invoice

Date

Invoice

No.

Name of the Dealer who has issued

Declarations or Certificates

Sr.

No.TIN, if

applicable

2 4 51 6 7 83

1

Total

:

Seal and Signature of Auditor

Name :

48

Declarations or Certificates not received Under Central Sales Tax Act, 1956. (other than Form-H)

ANNEXURE -I

Differential

tax liability

(Rs.)

(Col.

9-Col. 6)

Amount

of Tax

(as per

co-8)

Rate of

tax

applicable

(Local

Rate)

Tax

Amount

(Rs.)

Taxable

Amount

(Rs.) Net

Invoice

Date

Invoice

No.

Declaration

or Certificate

type (specify

form or

certificate

type)*

Name of the

Dealer who

has issued

Declarations

or

Certificates

Sr.

No.TIN, if

applicable

2 4 51 6 7 8 9 103

1

Total

CUSTOMER-WISE VAT SALES

ANNEXURE -J

(Section 1)

A. Information of Claimant Dealer

TIN of Claimant

Dealer

Period Covered

Under Audit

(DD/MM/YYYY

ToFromOther Local

Taxable

SALES Rs.

B. List of CUSTOMER WISE SALES on which VAT is charged separately.

Sr. No. TIN of Customers Net Taxable Amount Rs. Output VAT

Amount Rs.

Gross

Total Rs.

54321

SALES

* Net Taxable Amount means – Sales Amount on which VAT is charged separately.

* Gross Amount means – Total Value of Sales to Customer including, VAT, insurance, freight,

any other charges etc shown separately in invoices.

* Other Local Taxable Sales means- the sales which are inclusive of tax i.e. the taxable sales where

the taxes are not collected separately.

:

Seal and Signature of Auditor

Name :

49

SUPPLIERS WISE VAT PURCHASES

ANNEXURE -J

(Section 2)

A. Information of Claimant Dealer

TIN of Claimant

Dealer

Period Covered

Under Audit

(DD/MM/YYYY

)

ToFromOther Local

Taxable

PURCHASE Rs.

B. List of SUPPLIERS WISE PURCHASES on which VAT is charged separately.

Sr. No. TIN of Suppliers Net Taxable Amount Rs. Input VAT

Amount Rs.

Gross

Total Rs.

54321

PURCHASES

Total

* Net Taxable Amount means – Purchase Amount on which VAT is charged separately.

* Gross Amount means – Total Value of Purchases of Supplier including, VAT, insurance, freight,

any other charges etc shown separately in invoices.

* Other Local Taxable Purchases means- the purchase which are inclusive of tax i.e. the taxable

purchases where the taxes are not collected separately.

:

Seal and Signature of Auditor

Name :

50

CUSTOMER WISE DEBIT NOTE OR CREDIT NOTE

ANNEXURE -J

(Section 3)

A. Information of Claimant Dealer

TIN of Claimant

Dealer

SALES CR/DR NOTE / GOODS

RETURN

Period Covered

Under Audit

(DD/MM/YYYY

)

ToFrom

B. List of CUSTOMER WISE DEBIT NOTE / CREDIT NOTES on which VAT is charged separately.

Sr. No. TIN of Customers Net Taxable Amount Rs. Output VAT

Amount Rs.

Gross

Total Rs.

54321

Total

* Note – The details in respect of Credit Notes / Debit Notes to be submitted only when there is

variation in sale price in respect of goods sold.

:

Seal and Signature of Auditor

Name :

51

SUPPLIER WISE DEBIT NOTE OR CREDIT NOTE

ANNEXURE -J

(Section 4)

A. Information of Claimant Dealer

TIN of Claimant

Dealer

PURCHASES CR/DR NOTE /

GOODS RETURN

Period Covered

Under Audit

(DD/MM/YYYY

)

ToFrom

B. List of SUPPLIER WISE DEBIT NOTE / CREDIT NOTEon which VAT is charged separately.

Sr. No. TIN of Customers Net Taxable Amount Rs. Input VAT

Amount Rs.

Gross

Total Rs.

54321

* Note – The details in respect of Credit Notes / Debit Notes to be submitted only when there is variation in purchase

price in respect of goods purchased.

Total

ANNEXURE -K

Determination of Gross Turnover of Sales and Purchases along with reconciliation with Profit and Loss

Account, Trial Balance/ Sales and Purchase register.”

:

Seal and Signature of Auditor

Name :

52

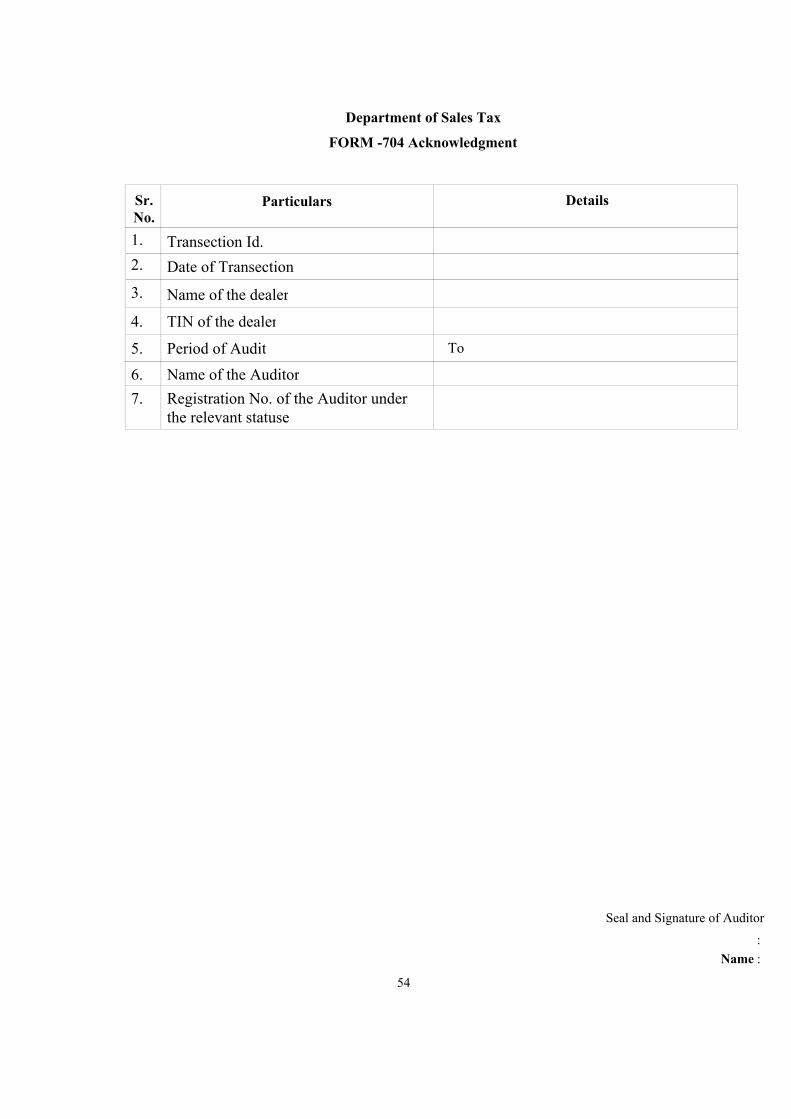

STATEMENT OF SUBMISSION OF AUDIT REPORT IN FORM-704

Place :

Date :

under the transaction id

It is further acknowledged that the said audit report has been uploaded by me on the website www.mahavat.gov.in

(Name of Chartered Accountant)

of the Maharashtra Value Added Tax Act, 2002 and have received audit report in form 704 certified by the said

(Name of Chartered Accountant), under the provisions of section 61

byTohave been duly audited for the periodV/C,