forensic accounting – data using caatts · forensic accounting is the application of accounting...

TRANSCRIPT

Forensic Accounting –Data Mining using CAATTs

© �ikunj S. Shah

Nikunj S. ShahB.Com.,LL.B.,F.C.A.,DISA(ICA),CIA(USA), ACFE

Session Contents

� Forensic Accounting – What is?, Areas, Skills required

� The need for CAATTs

© �ikunj S. Shah

� The need for CAATTs

� Types of CAAT tools

� The process of Fraud Examination using CAATTs

� An Introduction to Excel and IDEA

� Important Functions in Excel to detect Red Flags

� Advance Features in Excel for data analysis

What is Forensic Accounting?

Forensic means “Relating to, used in, or appropriate for courts of law or for public discussion or argumentation” (Am. Heritage Dictionary, 4th ed.)

© �ikunj S. Shah

Accounting means, “a system that provides quantitative information about finances” (WordNet 2.0)

Forensic accounting is the application of accounting skills to provide quantitative financial info. about matters before the courts

Areas of Forensic Accounting

Investigative Auditing

© �ikunj S. Shah

Litigation Support

Skill sets required

Accounting & Business reporting systems

Auditing

standards &

procedures

Evidence Information

© �ikunj S. Shah

Investigative

techniques

Forensic

Accountant

Litigation

processes &

procedures

gathering

Computer

Science

Technology

Criminology

The need for CAATTs

The current business scenario:

�High Volumes

© �ikunj S. Shah

�High Volumes

�Complexities

�Increased reliance on automated systems

�Compliance requirements

The need for CAATTs

The onus of detecting frauds on:

�Board of Directors:

© �ikunj S. Shah

“The prime responsibility for the prevention and detection of fraud (and other illegal acts) is that of the board, as part of its fiduciary responsibility for protecting the assets of the company.” -Para 5.23 “The Cadbury Report” on Corporate Governance, 1992

-Audit Committee shall review the findings of any internal investigations made by the internal auditors into matters where there is suspected fraud or irregularity or a failure of internal control systems of a material nature and report the matter to the board. -Clause 49 of the listing agreement, SEBI

The need for CAATTs

The onus of detecting frauds on:

�CEOs / CFOs:

© �ikunj S. Shah

-Certify that Cash flow does not contain any materially untrue statement or omit any material fact or contain statements that might be misleading

-No transactions entered into by the company during the year which are fraudulent, illegal or violative of the company's code of conduct

-that they have evaluated the effectiveness of the internal control systems of the companyClause 49 of the listing agreement, SEBI

The need for CAATTs

The onus of detecting frauds on:

� Internal Auditors:

© �ikunj S. Shah

� Internal Auditors:

Internal auditors should have sufficient knowledge of fraud to be

able to identify indications that fraud might have been committed.

Statement on Internal Auditing Standards No. 3, IIA

The need for CAATTs

CAATTs – Only practical means for

establishing what the facts really are as

they:

© �ikunj S. Shah

they:

�Help apply intuition, knowledge and skill

with far greater impact

�Identify indicators of fraud or red flags

�Document findingsNote: results of Data Analysis may not constitute a proof for fraud.

Types of CAAT tools

�Spreadsheet software, Database management

systems, Word processors (mobile phones?)

Generalized Audit Software (GAS):

© �ikunj S. Shah

�Generalized Audit Software (GAS):

ACL, IDEA, SoftCAAT

�Concurrent Audit techniques

�Integrated Test Facility (ITF)

�Systems Control Audit Review File (SCRAF)

�Continuous and Intermittent Simulation (CIS)

The process of Fraud Examination

using CAATTs

Categories of Fraud Investigation

�Specific Allegation

© �ikunj S. Shah

�Specific Allegation

�Exception Reporting

The process of Fraud Examination

using CAATTs

The knowledge of a possible fraud

Verify how convincing allegation is

Phase I

Pre Investigation

Phase II

Plan & Design

© �ikunj S. Shah

Verify how convincing allegation is

Arrive at its possible monetary impact

Assign to An investigator

Phase III

Execution

The process of Fraud Examination

using CAATTs

Understand Business, Operations and Controls (both manual and automated)

Phase I

Pre Investigation

Phase II

Plan & Design

© �ikunj S. Shah

Consider appropriateness of using Data Analysis for conducting examination

Determine precise objectives to be achieved from data analysis.

Determine data required

Phase III

Execution

The process of Fraud Examination

using CAATTs

Request data

Store files and MD5s

Phase I

Pre Investigation

Phase II

Plan & Design

© �ikunj S. Shah

Import data

Perform tests

Evaluate results

Conclude & determine further course of action

Phase III

Execution

An Introduction to Excel and IDEA

A comparison of popular tools used for

data analysis: GAS & Excel

© �ikunj S. Shah

Feature GAS Excel

Row Limitation No Yes (1048576)

Features specific to

Investigation and Audit

Yes No

Automatic Documentation Yes No

Allows data to be changed No Yes

An Introduction to Excel and IDEA

Tests and Excel Functions and Features

for data analytics:Test Function/Feature

© �ikunj S. Shah

Test Function/Feature

Verify that values in transaction files match

with master files

VLOOKUP

Identify Duplicate vendor payments IF, AND, OR

Select Samples RAND

Extract transactions matching multiple

criteria

Auto Filters, Advance

Filters

Stratify Payments, Summarise discounts

by sales person, etc.

Pivot Tables

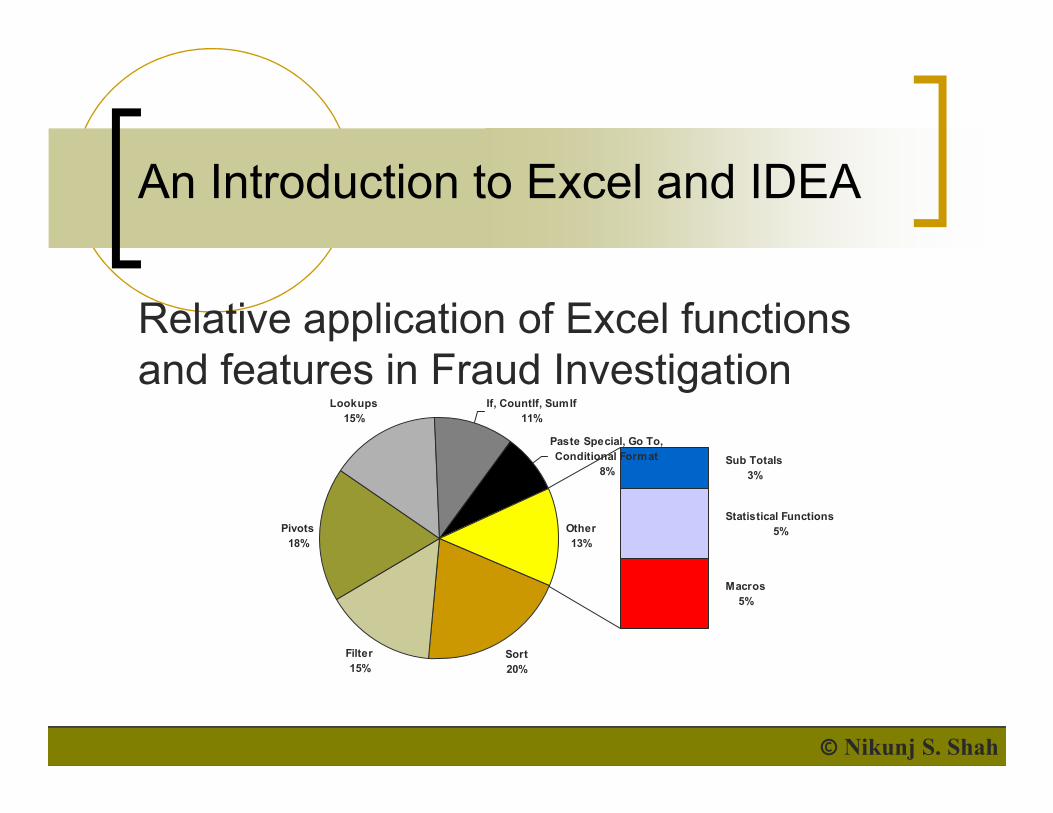

An Introduction to Excel and IDEA

Relative application of Excel functions

and features in Fraud InvestigationLookups If, CountIf, SumIf

© �ikunj S. Shah

Sort

20%

Filter

15%

Pivots

18%

Lookups

15%

If, CountIf, SumIf

11%

Paste Special, Go To,

Conditional Format

8%Sub Totals

3%

Statistical Functions

5%

Macros

5%

Other

13%

Important Functions in Excel to

detect Red Flags

�=IF() function to Detect ‘Gaps’

�=IF & =AND() function to implement ‘Same Same

Same’ and ‘Same Same Different’ Audit test

© �ikunj S. Shah

Same’ and ‘Same Same Different’ Audit test

�Detect sales made at other than authorized rates

�Advance Features in Excel for Analysis (Advance

Filters and Pivots)

�Implement the 80-20 principal to detect high

value (maybe high risk) items

Detecting Gaps:

© �ikunj S. Shah

Finding: Cheques not recorded in the Books

‘Same Same Same’ test:

© �ikunj S. Shah

Finding: Duplicate Vendor Payments

‘Same Same Different’ test:

© �ikunj S. Shah

Finding: Duplicate Vendor Payments?

Sales made at other than

authorized rates:

© �ikunj S. Shah

Finding: Was the sale of Product Code A003 to Venus Enterprises @ Rs.

15/- justifiable?