foreign exchange - markets: homepage

TRANSCRIPT

19 September 2012

All material in this training documentation is copyright of Markets International Ltd, Aylworth, Naunton, Cheltenham, Glos GL54 3AH, United Kingdom. No reproduction, in whole or part, by any means, is permitted without express permission in writing from Markets International Ltd.

Foreign Exchange

The foreign exchange market ---------------------------------------------------- 3

Spot exchange rates ---------------------------------------------------------------- 6

How spot rates are quoted ---------------------------------------------------- 7

Reciprocal rates ------------------------------------------------------------------ 9

Some terminology-------------------------------------------------------------- 10

Profit and loss ------------------------------------------------------------------- 11

Position-keeping---------------------------------------------------------------- 13

Dealing and broking --------------------------------------------------------------- 16

Market-making ------------------------------------------------------------------ 16

Broking ---------------------------------------------------------------------------- 17

Electronic trading and broking ---------------------------------------------- 18

Dealing terminology --------------------------------------------------------------- 19

Cross-rates -------------------------------------------------------------------------- 21

Forward exchange rates --------------------------------------------------------- 26

Forward outrights -------------------------------------------------------------- 26

Forward swaps ----------------------------------------------------------------- 30

Discounts and premiums----------------------------------------------------- 33

A forward swap position ---------------------------------------------------------- 37

Historic rate rollovers ------------------------------------------------------------- 46

Cross-rate forwards --------------------------------------------------------------- 49

Outrights -------------------------------------------------------------------------- 49

Swaps ----------------------------------------------------------------------------- 50

Short dates -------------------------------------------------------------------------- 53

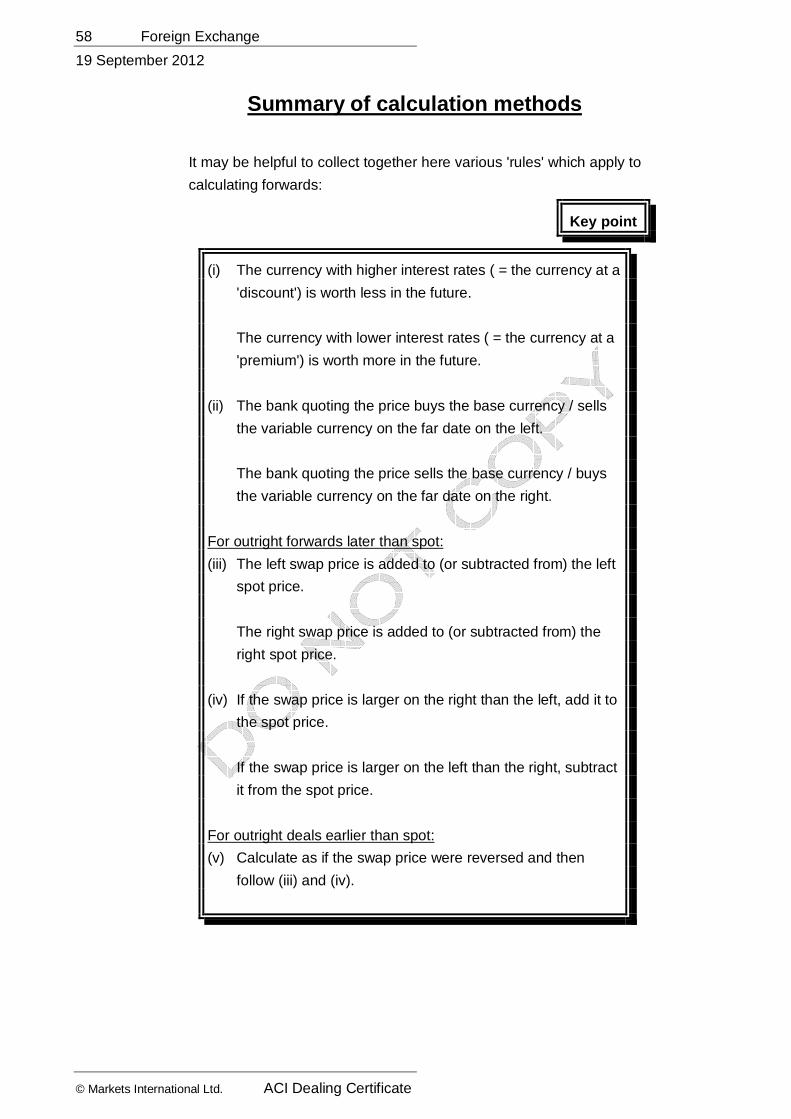

Summary of calculation methods ---------------------------------------------- 58

Hedging a forward with deposits ----------------------------------------------- 60

Disadvantages ------------------------------------------------------------------ 62

Covered interest arbitrage ------------------------------------------------------- 63

Summary of uses of forward FX instruments ------------------------------ 68

Hedging --------------------------------------------------------------------------- 68

Speculation ---------------------------------------------------------------------- 68

Arbitrage -------------------------------------------------------------------------- 68

Precious metals -------------------------------------------------------------------- 69

Pricing ----------------------------------------------------------------------------- 69

Physical delivery v book-entry ---------------------------------------------- 70

The gold fix ---------------------------------------------------------------------- 70

Borrowing gold and forward transactions ------------------------------- 71

Revision exercises ----------------------------------------------------------------- 74

Answers ------------------------------------------------------------------------------ 86

2 Foreign Exchange - Part 1

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Foreign Exchange - Part 1 3

19 September 2012

ACI Dealing Certificate © Markets International Ltd

The foreign exchange market

Throughout this chapter, we have generally used ISO codes (also

used by the SWIFT system) to abbreviate currency names. For the

Dealing Certificate exam, you should recognise the codes for the

currencies of the following countries, affiliated to the ACI:

4 Foreign Exchange - Part 1

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Country Currency Code

Argentina Peso ARS

Australia Dollar AUD

Austria Euro EUR

Bahamas Dollar BSD

Bahrain Dinar BHD

Belgium Euro EUR

Bermuda Dollar BMD

Brazil Real BRL

Bulgaria Lev BGN

Canada Dollar CAD

China Renmimbi yuan CNY

Croatia Kuna HRK

Cyprus Euro EUR

Czech Republic Koruna CZK

Denmark Krone DKK

Egypt Pound EGP

Finland Euro EUR

France Euro EUR

Georgia Lari GEL

Germany Euro EUR

Great Britain &

Channel Islands

Pound GBP

Greece Euro EUR

Hong Kong Dollar HKD

Hungary Forint HUF

Iceland Krona ISK

India Rupee INR

Indonesia Rupiah IDR

Irish Republic Euro EUR

Israel Shekel ILS

Italy Euro EUR

Japan Yen JPY

Jordan Dinar JOD

Kenya Shilling KES

Korea (South) Won KRW

Kuwait Dinar KWD

Lebanon Pound LBP

Luxembourg Euro EUR

Country Currency Code

Macao Pataca MOP

Macedonia Denar MKD

Malaysia Ringgitt MYR

Malta Euro EUR

Mauritius Rupee MUR

Mexico Peso Nuevo MXN

Monaco Euro EUR

Mongolia Tugrik MNT

Netherlands Euro EUR

New Zealand Dollar NZD

Nigeria Naira NGN

Norway Krone NOK

Pakistan Rupee PKR

Panama Balboa PAB

Philippines Peso PHP

Poland Zloty PLN

Portugal Euro EUR

Romania Leu ROL

Russia Ruble RUB

Singapore Dollar SGD

Serbia Dinar RSD

Slovakia Euro EUR

Slovenia Euro EUR

South Africa Rand ZAR

Spain Euro EUR

Sri Lanka Rupee LKR

Sweden Krona SEK

Switzerland Franc CHF

Tanzania Shilling TZS

Thailand Baht THB

Tunisia Dinar TND

United Arab

Emirates

Dirham AED

USA US dollar USD

Zambia Kwacha ZMK

Foreign Exchange 5

19 September 2012

ACI Dealing Certificate © Markets International Ltd

Base currency and variable currency

A convention has also been used that for example, the exchange rate

between USD and JPY is written as 'USD/JPY' if it refers to the

number of JPY equal to 1 USD and 'JPY/USD' if it refers to the

number of USD equal to 1 JPY. The currency code written on the left

is the 'base' currency; there is always 1 of the base unit. The

currency code written on the right is the 'variable' currency (or

'counter' currency or 'quoted' currency); the number of units of this

currency equal to 1 of the base currency varies according to the

exchange rate. Although some people do use the precisely opposite

convention, the one we use here is the more common one and is the

convention used in the ACI exam.

Key point

We always write the base currency on the left.

NOK/SGD, for example, means the number of SGD per NOK

Example 1

The CHF/DKK exchange rate is 4.1235. If I buy CHF 1 million

against DKK, how many DKK do I pay? The number 4.1235 means

the number of DKK per CHF. I therefore pay DKK 4,123,500:

1,000,000 x 4.1235 = 4,123, 500

If instead I buy DKK 1 million, how many CHF do I pay? In this case,

it is CHF 242,512.43:

1,000,000 ÷ 4.1235 = 242,512.43

6 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Spot exchange rates

The basic transaction in the foreign exchange market is a ‘spot’ deal.

As we discussed in the ‘Money Markets’ chapter, a 'spot' transaction

is an outright purchase or sale of one currency for another currency,

for delivery two working days after the dealing date (the date on

which the contract is made). This allows time for the necessary

paperwork and cash transfers to be arranged.

Key point

‘Spot’ is value two working days after trade date

There are however some exceptions. For example, a price for

USD/CAD without qualification generally implies delivery on the next

working day after the dealing day. This is referred to as 'funds'. A

'spot' price (value two working days after the dealing day, as usual)

can generally be requested as an alternative.

Key point

USD/CAD is usually traded for value next day (‘funds’)

Another problem arises in trading Middle East currencies where the

relevant markets are closed on Friday but open on Saturday or

Sunday. A USD/AED spot deal on Wednesday would need to have a

split settlement date: the USD would be settled on Friday, but the

AED on Saturday.

If the spot date falls on a public holiday in one or both of the centres

of the two currencies involved, the following working day is taken as

the spot value date. If the intervening day (between today and spot)

is a holiday in one of the two centres, the spot value date is often also

delayed by one day.

Example 2

If a spot GBP/USD deal is transacted on Thursday 31 August, it

would normally be for value Monday 4 September. If this date is a

holiday in the UK however, it would normally be for value Tuesday 5

September.

Foreign Exchange 7

19 September 2012

ACI Dealing Certificate © Markets International Ltd

How spot rates are quoted

When quoting against the EUR, it is the practice in the interbank

market to quote most currencies in terms a varying number of units of

currency per 1 EUR. In other words, the EUR is, by convention,

always the base currency if it is one of the two currencies involved.

Similarly, apart from the EUR, it is the interbank convention to quote

all currencies against GBP using GBP as the base currency. Apart

from the EUR and GBP, currencies quoted against the AUD and NZD

use the AUD and NZD as the base. Again, apart from the EUR, GBP,

AUD and NZD, all rates against the USD are always quoted interbank

with the USD as the base currency.

Next in this ‘hierarchy’ probably comes the CHF, which in most (but

not all) markets is quoted as the base currency against anything other

than the EUR, GBP, AUD, NZD and USD.

In the currency futures markets, as opposed to the interbank market,

quotations against the USD usually have USD as the variable

currency.

Although dealing is possible between any two convertible currencies

- for example, NZD against EUR or CHF against JPY - the

interbank market has historically quoted mostly against USD, so

reducing the number of individual rates that needed to be quoted.

The exchange rate between any two non-USD currencies could then

be calculated from the rate for each currency against USD. A rate

between any two currencies, neither of which is the USD, has

historically been known as a ‘cross-rate’. Nowadays, the term ‘cross-

rate is also used more widely to mean any exchange rate calculated

from two other rates - so, for example, a GBP/SEK rate could be

calculated by combining a EUR/GBP rate and a EUR/SEK rate.

Key point

A ‘cross-rate’ is an exchange rate calculated by combining two

other rates (historically, a non-USD rate calculated by

combining two USD-based rates).

8 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

The non-USD rates (for example EUR/GBP, EUR/JPY, EUR/CHF)

have increasingly been traded between banks in addition to the USD-

based rates. This sometimes reflects the importance of the

relationship between the pair of currencies. The economic

relationship between CHF and EUR, for example, is closer than the

relationship between CHF and USD. It is therefore more true

nowadays to say that the USD/CHF exchange rate is a function of the

EUR/USD rate and the EUR/CHF rate, rather than that the EUR/CHF

rate is a function of the EUR/USD rate and the USD/CHF rate. The

principle of calculating cross-rates remains the same however.

As in other markets, a bank normally quotes a two-way price,

whereby it indicates at what level it is prepared to buy the base

currency against the variable currency (the 'bid' for the base currency

- a cheaper rate), and at what level it is prepared to sell the base

currency against the variable currency (the 'offer' of the base currency

- a more expensive rate).

Example 3

If a bank is prepared to buy USD for 1.4375 Swiss francs, and sell

USD for 1.4385 Swiss francs, the USD/CHF rate would be quoted as:

1.4375 / 1.4385.

The quoting bank buys the base currency (in this case USD) on the

left and sells the base currency on the right. If the bank quotes such

a rate to a company or other counterparty, the counterparty would sell

the base currency on the left, and buy the base currency on the right

- the opposite of how the bank itself sees the deal.

In the money market, the order of quotation is not important and it

does differ between markets. From a quotation of either '5.80% /

5.85%' or '5.85% / 5.80%', it is always clear to the customer that the

higher rate is the offered rate and the lower rate is the bid rate. In

foreign exchange however, the market-maker's bid for the base

currency (the lower number in a spot price) is always on the left. This

is particularly important in forward prices.

Foreign Exchange 9

19 September 2012

ACI Dealing Certificate © Markets International Ltd

The difference between the two sides of the quotation is known as the

'spread'. Historically, a two-way price in a cross-rate would have a

wider spread than a two-way price in a USD-based rate, because the

cross-rate constructed from the USD-based rates would combine

both the spreads. Now however, the spread in say a EUR/CHF price

might typically be proportionally narrower than a USD/CHF spread,

because it is more the EUR/CHF price that is 'driving' the market, as

noted above, rather than the USD/CHF price.

Key point

The ’bid’ is the price on the left, at which the quoting bank buys

the base currency.

The ‘offer’ is the price on the right, at which the quoting bank

sells the base currency.

The ‘spread’ is the difference between the bid and the offer.

In some markets, there is a convention to adjust exchange rates to a

number which that market considers more ‘user-friendly’. For

example, if the CHF/DKK exchange rate is 4.5278, it would be quoted

in the London market as ‘4.5278’ but might be quoted in the

Copenhagen market as ‘452.78’ - i.e. as the number of DKK equal to

100 CHF rather than 1 CHF. Similarly, a JPY/CHF rate of 0.014385

might be quoted in some markets as ‘1.4385’.

Exercises

1 The SGD/NOK exchange rate is quoted as 2.9584. Does this exchange rate express the number of Norwegian kroner equal to 1 Singapore dollar, or the number of Singapore dollars equal to one Norwegian krone?

See ‘Answers’ at the end of this chapter

Reciprocal rates

Any quotation with a particular currency as the base currency can be

converted into the equivalent quotation with that currency as the

variable currency by taking its reciprocal.

10 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Example 4

A USD/CHF quotation of 1.4375 / 1.4385 can be converted to a

CHF/USD quotation of (1 :- 1.4375) / (1 :- 1.4385). However, this

would still be quoted with a smaller number on the left, so that the two

sides of the quotation are reversed: 0.6952 / 0.6957. In either case,

the bank buys the base currency against the variable currency on the

left, and sells the base currency against the variable currency on the

right.

Exercises

2 The SEK/NOK exchange rate is 1.0523 / 28. What is the reciprocal rate?

See ‘Answers’ at the end of this chapter

Some terminology Rates are typically quoted to 1

100th of a cent etc. (known as a 'point' or

a 'pip'). For example the USD/CHF rate would usually be quoted to

four decimal places as '1.4375 / 1.4385'. This depends on the size of

the number however and in the case of USD/JPY for example, the

convention is to use 2 decimal places. In a USD/JPY quote of

'105.05 / 105.15' for example, '15 points' means 0.15 JPY. In both

cases, one point is thus one unit of the last decimal place quoted.

Example 5

When trading USD/CHF in an amount of USD 1 million, the value of

one point is CHF 100. In other words, CHF 100 is the size of the

profit or loss made on the deal if the exchange rate moves one point:

1,000,000 x CHF 0.0001 = CHF 100

‘The points’ quoted generally mean the final two digits of the number.

All the digits before these last two digits are known as the ‘big figure’.

As the big figure does not change in the short term, dealers generally

do not quote it when dealing in the interbank market. In the example

above (1.4375 / 1.4385) the quotation would therefore be given as

simply as the points: '75 / 85'. However when dealers are quoting a

rate to a corporate client they will often mention the big figure also. In

this case, the quotation would be '1.4375 / 85'. One big figure means

100 points, so that if the rate moves from 1.4375 to 1.4475, it is said

to have moved by one big figure.

Foreign Exchange 11

19 September 2012

ACI Dealing Certificate © Markets International Ltd

Key point

A ‘point’ is one unit of the last decimal place in the exchange

rate.

Exchange rates are typically quoted in ‘points’ or ‘pips’, usually

the last two decimal places.

The ‘big figure’ is the first part of the exchange rate, excluding

the points.

A change in the rate of ‘one big figure’ generally means a

change of ‘100 points’.

A ‘long’ position is a surplus of purchases over sales of a given

currency - i.e., a position which benefits from a strengthening of that

currency. Similarly, a ‘short’ position is a surplus of sales over

purchases of a given currency, which benefits from a weakening of

that currency. A ‘square’ position is one which is neither long nor

short - i.e. one in which the sales and purchases are equal.

A ‘yard’ of a currency is an American billion units of that currency (i.e.

1,000,000,000 units).

‘Cable’ is a nickname for the GBP/USD exchange rate.

If one party asks another for a two-way price and then chooses to

deal on the bid side of the price, he is said to ‘hit’ the bid. If he

chooses to deal on the offer side of the price, he is said to ‘lift’ the

offer.

Occasionally a dealer will narrow the bid / offer spread to zero - i.e.

he will quote a single price and the party asking for the price can

choose whether he will buy or sell at that price. This is known as a

‘choice’ price.

Profit and loss

To earn profit from dealing, the bank's objective is clearly to sell the

base currency at the highest rate it can against the variable currency

and buy the base currency at the lowest rate.

12 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Example 6

Deal 1: Bank buys USD 1,000,000 against CHF at 1.4830

Deal 2: Bank sells USD 1,000,000 against CHF at 1.4855

Cashflows

USD CHF

Deal 1: + USD 1,000,000 - CHF 1,483,000

Deal 2: - USD 1,000,000 + CHF 1,485,500

Net result: + CHF 2,500

The value of a single point depends on the number of decimal places

in the exchange rate.

Example 7

I buy USD 1 million against CHF when spot USD/CHF is 1.5835.

Later in the day, I close my position by selling USD 1 million again

when spot USD/CHF is 1.5836. I thus have a profit of 1 point.

Cashflows

USD CHF

Deal 1: + USD 1,000,000 - CHF 1,583,500

Deal 2: - USD 1,000,000 + CHF 1,583,600

Net result: + CHF 100

Therefore the value of 1 point in USD/CHF, on a deal of USD 1

million, is CHF 100.

Example 8

I buy USD 1 million against JPY when spot USD/JPY is 118.35. Later

in the day, I close my position by selling USD 1 million again when

spot USD/JPY is 118.36. I thus have a profit of 1 point.

Cashflows

USD JPY

Deal 1: + USD 1,000,000 - JPY 118,350,000

Deal 2: - USD 1,000,000 + JPY 118,360,000

Net result: + JPY 10,000

Therefore the value of 1 point in USD/JPY, on a deal of USD 1

million, is JPY 10.000.

Foreign Exchange 13

19 September 2012

ACI Dealing Certificate © Markets International Ltd

Dealers generally operate on the basis of small percentage profits but

large turnover. These rates will be good for large, round amounts.

For very large amounts, or for smaller amounts, a bank would

normally quote a wider spread. The amount for which a quotation is

'good' (that is, a valid quote on which the dealer will deal) will vary

with the currency concerned and market conditions.

Quoting a rate

When a dealer is asked for a quote, and he particularly wishes to buy

or sell himself, he will tend to adjust the price he is quoting, slightly up

or down from the prevailing market rate, in order to try to achieve his

desired result. For example if I wish to buy, then I might raise my bid

slightly. Then if the counterparty asking me for a price is a seller, he

will be attracted by my bid price rather than anyone else’s and sell to

me (which is what I want). At the same time, I might also raise my

offer slightly, because I do not wish him to lift my offer, because I do

not wish to sell. The result is that both my bid and my offer might be

slightly higher than the rates being quoted generally in the market.

Position-keeping

At any time, a dealer needs to know what is his position resulting from

the net of all the deals he has undertaken during the day so far. He

also needs to know what is the average exchange rate of this net

position, so that he can compare it with the current market rate to see

whether or not the position is profitable. At the end of the day, he

might not close out the position, but will in that case need to ‘mark to

market’ the position - i.e. calculate the unrealised profit or loss on

the position so far. This is achieved by calculating what the profit or

loss would be if he did in fact close out the position out at the current

rate (i.e. the end-of-day closing market rate).

14 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Example 9

You undertake three spot deals in USD/CHF as follows.

Sell USD 4 million at 1.6723

Buy USD 1 million at 1.6732

Buy USD 5 million at 1.6729

The market closes at 1.6730.

What is your position? What is the average rate of this position?

What is your net profit or loss?

USD CHF

- 4,000,000 at 1.6723: + 6,689,200

+ 1,000,000 at 1.6732: - 1,673,200

+ 5,000,000 at 1.6729: - 8,364,500

Position: + 2,000,000 - 3,348,500

Average rate: 67425.1000,000,2500,348,3 =

- 2,000,000 at 1.6730: + 3,346,000

Loss: - 2,500

The position is therefore long USD 2 million. The average rate is

1.67425. The loss is CHF 2,500. This loss could be expressed in

USD by converting it into USD at the spot rate, or in any other

currency by converting it at the appropriate spot rate.

Exercise

3 You are short EUR/CHF and need to square your position. On which of the following prices quoted to you will you deal?

a. 1.5920 / 30 b. 1.5915 / 25 c. 1.5925 / 35 d. 1.5922 / 28

Foreign Exchange 15

19 September 2012

ACI Dealing Certificate © Markets International Ltd

4 You are a dealer with a short position in USD against EUR. A counterparty calls you for a price in EUR/USD. The market is currently 0.9503 / 08. Which of the following prices might you quote if you now wish to reduce the size of your position?

a. 0.9502 / 07 b. 0.9503 / 08 c. 0.9504 / 09

5 If the spot AUD/USD exchange rate is quoted as 0.5413, what is the value of 1 ‘point’ on a deal of 1 million of the base currency? If the spot USD/JPY exchange rate is quoted as 107.13, what is the cash value of 1 ‘point’ on a deal of 1 million of the base currency?

6 Spot EUR/CHF is quoted to as 1.5318 / 23. You buy CHF 3,000,000. How many EUR do you sell?

7 You buy USD 10 million against CAD at 1.3785 and sell USD 10 million at 1.3779. What is your profit or loss in CAD?

8 You are a dealer. A customer asks you for a CHF/USD price. You quote him 0.6330 / 38 and he buys CHF 5 million from you. You want to cover this position in the market and therefore deal on a price of USD/CHF 1.5783 / 88 quoted to you by another bank, for exactly the same amount of CHF 5 million. What profit or loss in USD have you made?

9 You sell EUR 5 million against USD at 0.9320, you buy EUR 2 million at 0.9325, you buy EUR 4 million at 0.9330 and you sell EUR 3 million at 0.9327. The market closes at 0.9328 and the closing rate for GBP/USD is 1.4730. At the end of the day, what is your EUR/USD position? What is the average rate of this position? What is your total net profit or loss in GBP?

See ‘Answers’ at the end of this chapter

16 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Dealing and broking

Market-making

In any market, a market-maker is a dealer who sets out to ‘make a

market’ in some instrument or commodity - that is, he will quote a

two-way price in it, if asked to do so by someone else who wants to

buy or sell (or borrow or lend). In some markets, market-makers are

officially designated as such by the relevant authorities and are

obliged to make two-way prices at all times. This is not the case in

the foreign exchange markets. A dealer who considers himself a

market-maker in, say, GBP/USD, will try to quote a two-way

GBP/USD price all the time, but he might occasionally choose not to

quote or to quote only a bid or only an offer. As well as giving quotes,

a market-maker also asks other banks for quotes.

The market-maker seeks to make a profit from the bid/offer spread

that he quotes. If he quotes the same two-way price to two different

customers, and each customer deals for the same amount but on a

different side of the price, the market-maker profits by the spread. In

practice of course, customers will not be paired tidily like this but, over

time, the market maker nevertheless hopes to earn a profit in this way

on average.

By providing prices to the market, the market-maker hopes that many

counterparties will deal with him, thereby providing him in return with

information on who is buying and who is selling. These information

flows help the market-maker to decide on the likely direction of the

market, which in turn helps him in his position-taking. Being ready to

quote prices also helps the bank in maintaining its relationships

generally with its counterparties.

The risk of course is that the market moves against him after a

customer has dealt. The market-maker could remove that risk by

always covering his own resulting position immediately. However, if

he did that, he would make no profit because he would be dealing at

a similar price with another bank. Also, it might not be possible for

the market-maker to cover the position quickly enough, before the

market has moved against him, so that he actually makes a loss,

rather then just breaks even.

Foreign Exchange 17

19 September 2012

ACI Dealing Certificate © Markets International Ltd

It might also be the case that the position given to the market-maker

by the customer is one which the market-make likes, so that he seeks

to make profit by running the position for a time. The risk here of

course, as always with a speculative position, is that the market-

maker might be wrong in his view of the market.

Note that in all this, the ‘customer’ might himself also be a bank, and

possibly a market-maker. He is considered the customer here

because he is the one asking for the price, rather than the one

quoting it. He is the ‘price-taker’, rather than the ‘price-maker’. This

party, which deals at another bank’s price, is known as the

‘aggressor’.

Broking

A deal is undertaken between two counterparties. Each counterparty

then has a position and is known as a ‘principal’ in the transaction. It

is possible that the deal is arranged through a third party agent,

known as a ‘broker’. In the foreign exchange and money markets, a

broker is a ‘name-passing’ broker. This means that he is never a

principal himself in the chain of transactions, but only passes the

names of the two counterparties (the principals) to each other. The

function of a broker is to aid the process of price discovery in the

market, to disseminate these prices, and to match buyers with sellers.

Market-makers keep the broker aware of their bid/offer prices. When

a customer calls the broker, he will select the best bid currently given

to him by a market-maker, and also the best offer currently given to

him by a market-maker, and pass this resulting bid/offer to the

customer. If the customer deals on one side or the other, the broker

immediately tells whichever market-maker gave him that price. That

market-maker has now dealt with the customer. The broker is only

acting as a go-between in this - at no point in the process is he

acting as principal himself. In return for this service, the dealing

parties pays the broker a commission (‘brokerage’) for each deal

transacted.

Until the deal has been finalised, the broker maintains confidentiality.

He does not pass the name of either party to the other until he is

satisfied that they intend to deal, subject to each having a sufficient

credit line for the other.

18 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

In some markets other than those we are discussing here (for

example in the futures markets), the term ‘broker’ applies to someone

who does take a position as principal, at least for a short time.

Electronic trading and broking

We have so far been implying that the market-maker, the broker and

the customer are all speaking to each other, probably by telephone.

The broker in such a situation is known as a ’voice-broker’.

Increasingly however, dealing and broking is carried out

electronically. An electronic broker, such as EBS, is a computer

system into which market-makers feed prices. The system

disseminates the best bid and offer prices to users in the same way

that a voice-broker does. Counterparties who have access to the

system are able to deal on these prices. The identity of each of the

counterparties is not revealed to the other until the deal is done. The

system requires information regarding the credit lines that each of the

participants has for each of the others.

With voice brokers, in both FX and deposit transactions, it is typical

for each party to pay brokerage to the broker, at a rate which has

been negotiated individually for all such business between that bank

and the broker. With Reuters and EBS, it is only the aggressor who

pays the brokerage.

An automated trading system (ATS) is similarly an electronic system

through which dealers can communicate with each other, as an

alternative to dealing over the telephone. This is often a dedicated

system belonging to a particular bank, for dealing with its own

customers. An on-line trading system such as FXall is an ATS

allowing end-users the ability to deal via the internet with any of a

group of participating banks.

Foreign Exchange 19

19 September 2012

ACI Dealing Certificate © Markets International Ltd

Dealing terminology

The following remarks all relate to the spot foreign exchange market.

We have included a similar section at the end of the Money Markets

chapter. Where the terminology is the same in the two areas, we

have repeated it.

In all the following situations, the ‘customer’ is the party initiating the

conversation - i.e. the party asking the other party to quote a price for

a foreign exchange deal. This customer might be another bank, or a

corporate or other organisation. The two parties might be dealing via

a broker.

• Unless otherwise specified, there is a general understanding

in the market that the parties are discussing buying and selling

the base currency (rather then the variable currency) and that

amounts are in millions. For example, “I buy five” would mean

“I buy 5 million of the base currency and sell an amount of the

variable currency in exchange”.

• If the quoting dealer says “I bid …” or “I pay …”, he means

that he would like to buy the base currency at a certain price.

• If the quoting dealer says “I offer at …”, he means that he

would like to sell the base currency at a certain price

• If the quoting dealer says “Either way”, “Choice” or “Your

choice”, he means that he is quoting the same price for both

bid and offer.

• “Firm” or “Firm price” means that the price quoted is valid and

can be traded on.

• “For indication”, “Indication”, “For information” or “For level”

however means that the quote given is only indicative and

should be confirmed before a trade is proposed.

• If the broker says that a quote is “under reference”, he means

that the rate quoted might no longer be valid and must be

confirmed before any trades can be agreed.

20 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

• If the quoting dealer says “Your risk”, he is warning the other

party (the broker or the customer) that the price may have to

be re-quoted.

• If the broker or the customer says “My risk”, he is

acknowledging that the price may have to be re-quoted.

• If the quoting dealer says “Off”, he is cancelling any existing

bids or offers he has quoted, with immediate effect.

• If the quoting dealer says “Checking”, he means that he is

checking that he has a credit line available for the customer

before he can agree the deal.

• If the customer or the broker says “Mine” or “I buy” or “I take”,

this means that he accepts the other party’s quote and wishes

to buy the base currency at the offered rate for the amount

proposed. For example if one dealer wishes to buy USD 5

million from another who is quoting him a USD/CHF price, he

will say "5 mine"; this means "I wish to buy from you 5 million

of the base currency and sell the other currency, at your

offered price". Similarly, if he wishes to sell USD 5 million, he

will say "5 yours", meaning "I wish to sell you 5 million of the

base currency and buy the other currency, at your bid price".

Key point

“5 mine” said by the price-taker means he wishes to buy 5

million units of the base currency.

“5 yours” means he wishes to sell 5 million units of the base

currency.

• If the customer or the broker says “Yours” or “I sell” or “I give”,

this means that he accepts the quote and wishes to sell the

base currency at the bid rate for the amount proposed.

• Similarly, “Given” means that a deal has been proposed and

agreed at the bid price quoted, and “Taken” means that a deal

has been proposed and agreed at the offered price quoted.

• “Done” means that the deal is agreed as proposed.

Foreign Exchange 21

19 September 2012

ACI Dealing Certificate © Markets International Ltd

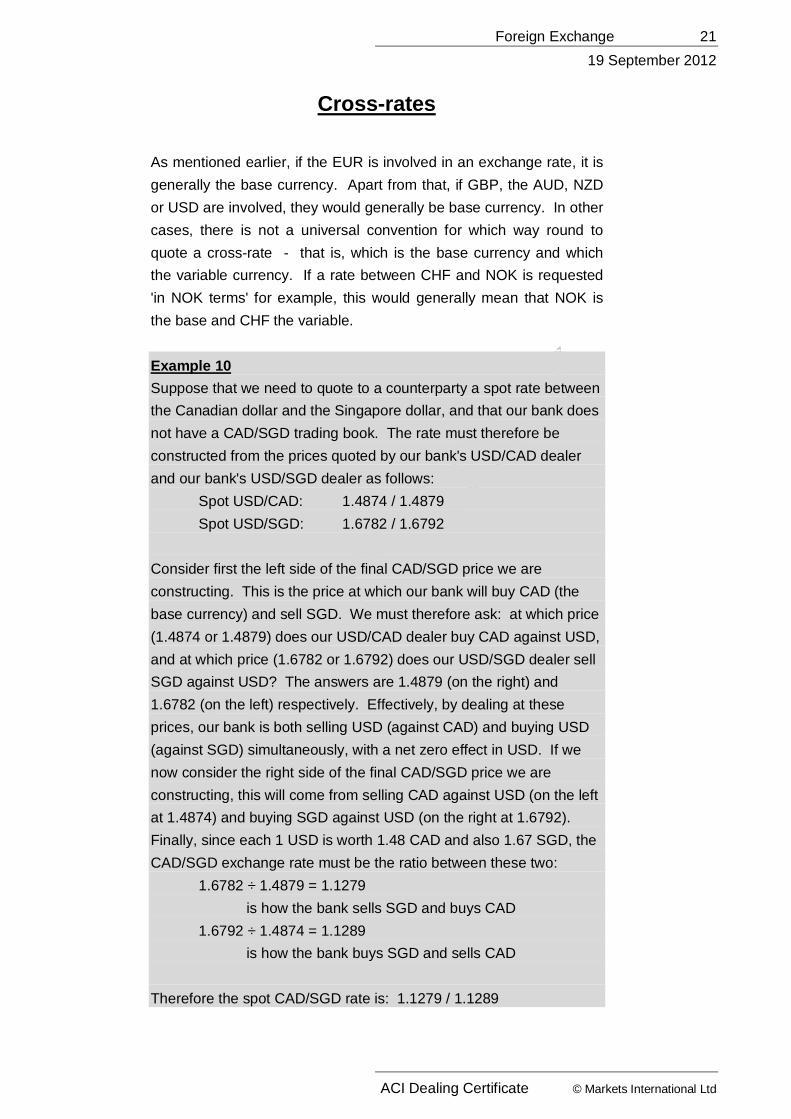

Cross-rates

As mentioned earlier, if the EUR is involved in an exchange rate, it is

generally the base currency. Apart from that, if GBP, the AUD, NZD

or USD are involved, they would generally be base currency. In other

cases, there is not a universal convention for which way round to

quote a cross-rate - that is, which is the base currency and which

the variable currency. If a rate between CHF and NOK is requested

'in NOK terms' for example, this would generally mean that NOK is

the base and CHF the variable.

Example 10

Suppose that we need to quote to a counterparty a spot rate between

the Canadian dollar and the Singapore dollar, and that our bank does

not have a CAD/SGD trading book. The rate must therefore be

constructed from the prices quoted by our bank's USD/CAD dealer

and our bank's USD/SGD dealer as follows:

Spot USD/CAD: 1.4874 / 1.4879

Spot USD/SGD: 1.6782 / 1.6792

Consider first the left side of the final CAD/SGD price we are

constructing. This is the price at which our bank will buy CAD (the

base currency) and sell SGD. We must therefore ask: at which price

(1.4874 or 1.4879) does our USD/CAD dealer buy CAD against USD,

and at which price (1.6782 or 1.6792) does our USD/SGD dealer sell

SGD against USD? The answers are 1.4879 (on the right) and

1.6782 (on the left) respectively. Effectively, by dealing at these

prices, our bank is both selling USD (against CAD) and buying USD

(against SGD) simultaneously, with a net zero effect in USD. If we

now consider the right side of the final CAD/SGD price we are

constructing, this will come from selling CAD against USD (on the left

at 1.4874) and buying SGD against USD (on the right at 1.6792).

Finally, since each 1 USD is worth 1.48 CAD and also 1.67 SGD, the

CAD/SGD exchange rate must be the ratio between these two:

1.6782 ÷ 1.4879 = 1.1279

is how the bank sells SGD and buys CAD

1.6792 ÷ 1.4874 = 1.1289

is how the bank buys SGD and sells CAD

Therefore the spot CAD/SGD rate is: 1.1279 / 1.1289

22 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

In summary therefore, to calculate a spot rate from two other rates

which share the same base currency (in our example this was USD),

divide opposite sides of the exchange rates. Following the same

logic shows that to calculate a spot rate from two other rates which

share the same variable currency (also USD in the following

example), we again need to divide opposite sides of the exchange

rates:

Example 11

Spot EUR/USD: 1.2166 / 1.2171

Spot AUD/USD: 0.6834 / 0.6839

The EUR/USD dealer buys EUR and sells USD at 1.2166 (on the

left). The AUD/USD dealer sells AUD and buys USD at 0.6839 (on

the right). Therefore:

1.2166 ÷ 0.6839 = 1.7789

is how the bank buys EUR and sells AUD

Similarly:

1.2171 ÷ 0.6834 = 1.7809

is how the bank sells EUR and buys AUD

Therefore the spot EUR/AUD rate is: 1.7789 / 1.7809

Finally, to calculate a rate from two rates where the common currency

is the base currency in one quotation but the variable currency in the

other, following the same logic through again shows that we multiply

the same sides of the exchange rates:

Foreign Exchange 23

19 September 2012

ACI Dealing Certificate © Markets International Ltd

Example 12

Spot EUR/USD: 1.2166 / 1.2171

Spot USD/SGD: 1.6782 / 1.6792

The EUR/USD dealer buys EUR and sells USD at 1.2166 (on the

left). The USD/SGD dealer buys USD and sells SGD at 1.6782 (on

the left). Also, since each 1 EUR is worth 1.21 USD, and each of

these USD is worth 1.67 SGD, the EUR/SGD exchange rate must be

the product of these two numbers.

Therefore:

1.2166 x 1.6782 = 2.0417

is how the bank buys EUR and sells SGD

Similarly:

1.2171 x 1.6792 = 2.0438

is how the bank sells EUR and buys SGD

Therefore the spot EUR/SGD rate is: 2.0417 / 2.0438

Calculation Summary

To calculate an exchange rate from two other rates:

from two rates with the same base currency or the same

variable currency:

divide opposite sides of the exchange rates

from two rates where the base currency in one is the same as

the variable currency in the other:

multiply the same sides of the exchange rates

The examples above all construct cross-rates from exchange rates

involving the USD (which is often the case). The same approach

applies when constructing other rates: considering the way in which

each of the two separate dealers will deal to create the rate, gives the

construction:

24 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

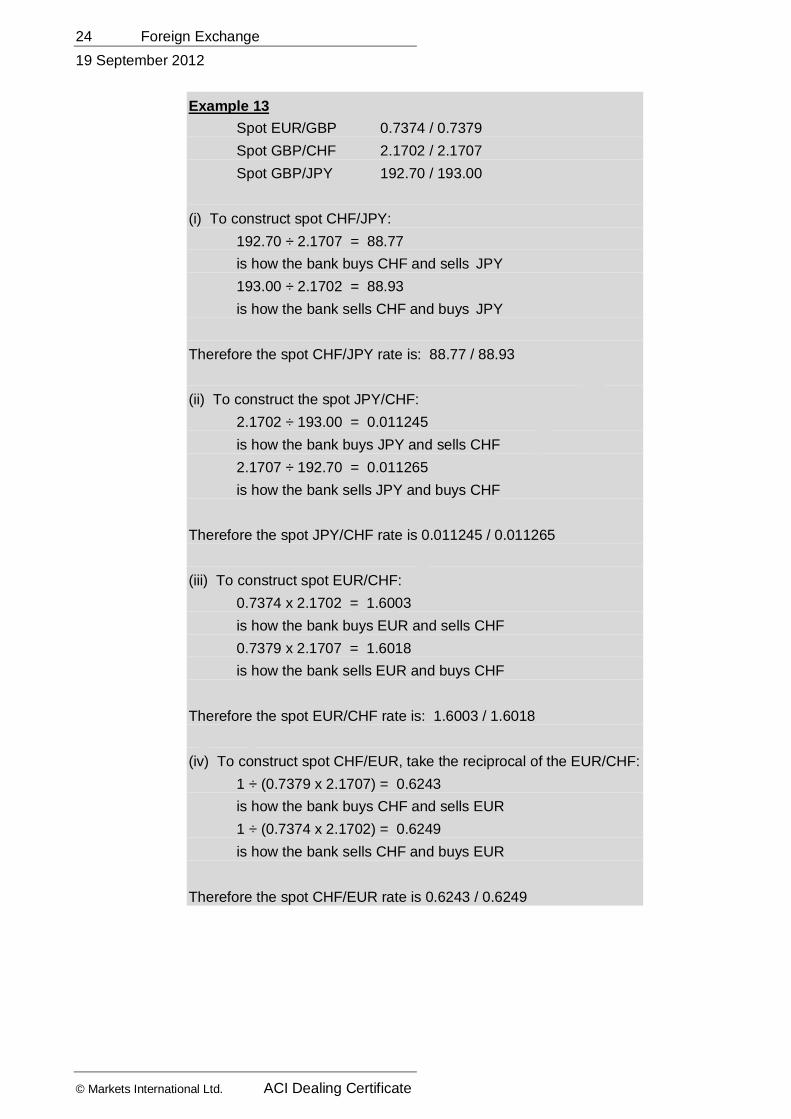

Example 13

Spot EUR/GBP 0.7374 / 0.7379

Spot GBP/CHF 2.1702 / 2.1707

Spot GBP/JPY 192.70 / 193.00

(i) To construct spot CHF/JPY:

192.70 ÷ 2.1707 = 88.77

is how the bank buys CHF and sells JPY

193.00 ÷ 2.1702 = 88.93

is how the bank sells CHF and buys JPY

Therefore the spot CHF/JPY rate is: 88.77 / 88.93

(ii) To construct the spot JPY/CHF:

2.1702 ÷ 193.00 = 0.011245

is how the bank buys JPY and sells CHF

2.1707 ÷ 192.70 = 0.011265

is how the bank sells JPY and buys CHF

Therefore the spot JPY/CHF rate is 0.011245 / 0.011265

(iii) To construct spot EUR/CHF:

0.7374 x 2.1702 = 1.6003

is how the bank buys EUR and sells CHF

0.7379 x 2.1707 = 1.6018

is how the bank sells EUR and buys CHF

Therefore the spot EUR/CHF rate is: 1.6003 / 1.6018

(iv) To construct spot CHF/EUR, take the reciprocal of the EUR/CHF:

1 ÷ (0.7379 x 2.1707) = 0.6243

is how the bank buys CHF and sells EUR

1 ÷ (0.7374 x 2.1702) = 0.6249

is how the bank sells CHF and buys EUR

Therefore the spot CHF/EUR rate is 0.6243 / 0.6249

Foreign Exchange 25

19 September 2012

ACI Dealing Certificate © Markets International Ltd

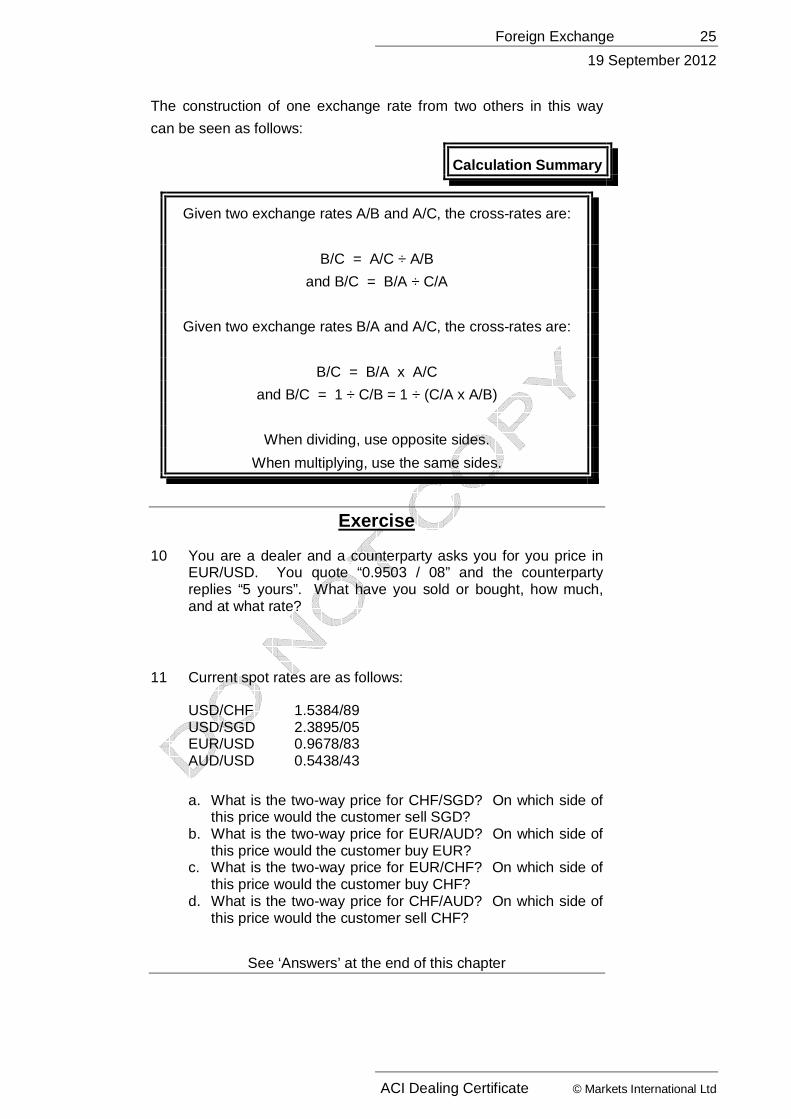

The construction of one exchange rate from two others in this way

can be seen as follows:

Calculation Summary

Given two exchange rates A/B and A/C, the cross-rates are:

B/C = A/C ÷ A/B

and B/C = B/A ÷ C/A

Given two exchange rates B/A and A/C, the cross-rates are:

B/C = B/A x A/C

and B/C = 1 ÷ C/B = 1 ÷ (C/A x A/B)

When dividing, use opposite sides.

When multiplying, use the same sides.

Exercise

10 You are a dealer and a counterparty asks you for you price in EUR/USD. You quote “0.9503 / 08” and the counterparty replies “5 yours”. What have you sold or bought, how much, and at what rate?

11 Current spot rates are as follows:

USD/CHF 1.5384/89 USD/SGD 2.3895/05 EUR/USD 0.9678/83 AUD/USD 0.5438/43

a. What is the two-way price for CHF/SGD? On which side of

this price would the customer sell SGD? b. What is the two-way price for EUR/AUD? On which side of

this price would the customer buy EUR? c. What is the two-way price for EUR/CHF? On which side of

this price would the customer buy CHF? d. What is the two-way price for CHF/AUD? On which side of

this price would the customer sell CHF?

See ‘Answers’ at the end of this chapter

26 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Forward exchange rates

Forward outrights

Although 'spot' is settled two days in the future, it is not considered in

the foreign exchange market as 'future' or 'forward', but as the

baseline from which all other dates (earlier or later) are considered.

A 'forward outright' is an outright purchase or sale of one currency in

exchange for another currency for settlement on a fixed date in the

future other than the spot value date. Rates are quoted in a similar

way to those in the spot market, with the quoting bank buying the

base currency 'low' (on the left side) and selling it 'high' (on the right

side). In some emerging markets, forward outrights are non-

deliverable and are settled in cash against the spot rate at maturity as

a contract for differences (see later).

Example 14

The spot EUR/USD rate is 1.2166 / 1.2171, but the rate for value one

month after the spot value date is 1.2186 / 1.2193.

The 'spread' (the difference between the bank's buying price and the

bank's selling price) is wider in the forward quotation than in the spot

quotation. Also, in this example, the EUR is worth more in the future

than at the spot date. EUR 1 buys USD 1.2186 in one month's time

as opposed to 1.2166 at present. In a different example, the EUR

might be worth less in the future than at the spot date.

The forward outright rate can be seen both as the market's

assessment of where the spot rate will be in the future and as a

reflection of current interest rates in the two currencies concerned.

Consider for example the following 'round trip' transactions, all

undertaken simultaneously:

(i) Borrow USD for 3 months starting from spot value date.

(ii) Sell USD and buy EUR for value spot.

(iii) Deposit the purchased EUR for 3 months starting from spot

value date.

(iv) Sell forward now the EUR principal and interest which mature

in 3 months' time, into USD.

Foreign Exchange 27

19 September 2012

ACI Dealing Certificate © Markets International Ltd

In general, the market will adjust the forward price for (iv) so that

these simultaneous transactions generate neither a profit nor a loss.

This is the theory of ‘interest rate parity’. When the four rates

involved are not in line (USD interest rate, EUR/USD spot rate, EUR

interest rate and EUR/USD forward rate), there is in fact opportunity

for arbitrage - making a profit by round-tripping. That is, either the

transactions as shown above will produce a profit or exactly the

reverse transactions (borrow EUR, sell EUR spot, deposit USD and

sell USD forward) will produce a profit. The supply and demand

effect of this arbitrage activity is such as to move the rates back into

line. If in fact this results in a forward rate which is out of line with the

market's 'average' view, supply and demand pressure will tend to

move the spot rate or the interest rates until this is no longer the case.

In more detail, the transactions might be as follows:

(i) Borrow USD 100

The principal and interest payment at maturity will be:

USD

×+×360days

rate interestcurrency variable1100

(ii) Sell USD 100 for EUR at spot rate to give EUR (100 :- spot)

(iii) Invest EUR (100 :- spot).

The principal and interest returned at maturity will be:

EUR ( )

×+×÷360days

rate interestcurrency easb1spot100

(iv) Sell forward this last amount at the forward exchange rate to

give:

( )

outright forward

360days

rate interestcurrency easb1spot100 USD

×

×+×÷

The supply and demand effect of’ arbitrage’ activity (i.e. round-

tripping deliberately, to make a profit out of the fact that the rates are

not all in line with each other) will tend to make the amount in (iv) the

same amount as that in (i), so that:

28 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

forward outright = ( )( )

( )( )360days

360days

rate interestcurrency easb1

rate interestcurrency eiablvar1spot

×+

×+×

Calculation Summary

Interest rate parity

forward outright =

( )( )( )( )

yeardays

yeardays

rate interestcurrency base1

rate erestint currency iablevar1spot

×+

×+×

You will need this formula for the exam. On the ACI formula

sheets provided in the exam, it appears as follows. Check

now that you can find it and understand how to use it.

currency base

currency base

currency quoted

currency quoted

basis annual

countday x rate interest1

basis annual

countday x rate interest1

rate spot rate forward

+

+=

Notice that the length of the year may be 360 or 365, and might be

different for the two currencies.

Example 15

31-day USD interest rate: 5%

31-day EUR interest rate: 3%

Spot EUR/USD rate: 1.2168

Then forward outright = ( )( )( )( ) 2189.1

03.01

05.012168.1

36031

36031

=×+

×+×

Foreign Exchange 29

19 September 2012

ACI Dealing Certificate © Markets International Ltd

In theory, to calculate the right-hand side of the outright price (where

the bank sells EUR to the customer against USD for outright value

one month forward as in the above example), one could use:

• the right-hand side of the spot price (the offer)

• the offered interest rate for USD and

• the bid interest rate for EUR.

One could then use the bid price for the spot, the bid interest rate for

USD and the offered interest rate for EUR to determine the other side

of the outright price. For the purpose of the ACI exam, this would be

expected.

Note however, that this generally produces a rather large spread. It

would be more realistic to use middle prices throughout, to calculate a

middle price for the outright, and then to spread the two-way outright

price around this middle price. In practice, a dealer does not

recalculate outright prices continually in any case, but takes them

from the market just as the spot dealer takes spot prices.

Example 16

31-day USD interest rate: 4.9 / 5.0%

31-day EUR interest rate: 3.0 / 3.1%

Spot EUR/USD rate: 1.2158 / 68

Using the offered interest rate for USD and the bid interest rate for

EUR:

forward outright = ( )( )( )( ) 2189.1

03.01

05.012168.1

36031

36031

=×+

×+×

Using the bid interest rate for USD and the offered interest rate for

EUR:

forward outright = ( )( )( )( ) 2177.1

031.01

049.012158.1

3603136031

=×+×+

×

The outright price is therefore 1.2177 / 1.2189.

30 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Forward swaps

Although forward outrights are an important instrument, trading banks

do not in practice deal between themselves in forward outrights, but

rather in forward 'swaps', where a forward swap is the difference

between the spot and the forward outright. The reason for not

dealing in outrights will become clear later. The forward outright rate

can therefore be seen as a combination of the current spot rate and

the forward swap rate (which may be positive or negative) added

together.

Key point

forward outright = spot + forward swap

Example 17

Spot EUR/USD: 1.2166 / 1.2171

Forward swap: 0.0145 / 0.0150

Forward outright = spot + swap

In this case: 1.2166 + 0.0145 = 1.2311

1.2171 + 0.0150 = 1.2321

Therefore the forward outright is 1.2311 / 1.2321

Putting this the other way round, it is equally true that:

Key point

forward swap = forward outright - spot

Example 18

Spot EUR/USD: 1.2166 / 1.2171

Forward outright: 1.2311 / 1.2321

forward swap = forward outright - spot

In this case: 1.2311 - 1.2166 = 0.0145

1.2321 - 1.2171 = 0.0150

Therefore the forward swap is 0.0145 / 0.0150

Foreign Exchange 31

19 September 2012

ACI Dealing Certificate © Markets International Ltd

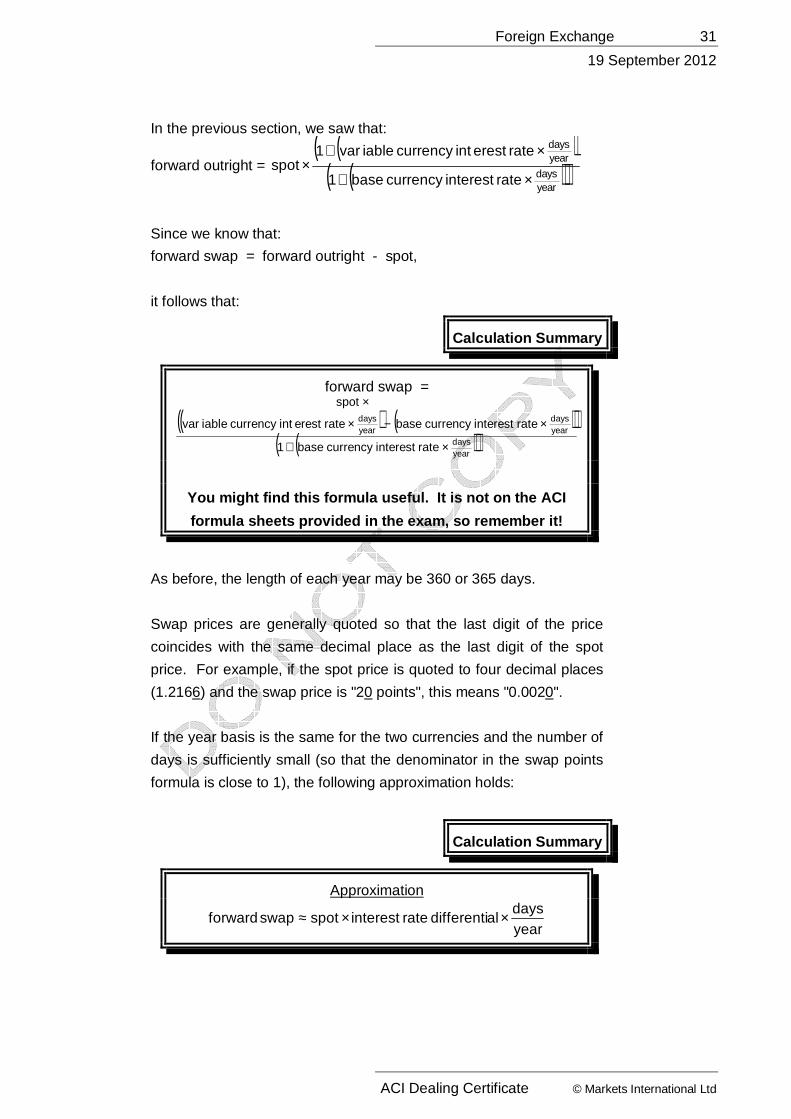

In the previous section, we saw that:

forward outright = ( )( )

( )( )yeardays

yeardays

rate interestcurrency base1

rate erestint currency iablevar1spot

×+

×+×

Since we know that:

forward swap = forward outright - spot,

it follows that:

Calculation Summary

forward swap =

( ) ( )( )( )( )

yeardays

yeardays

yeardays

rate interestcurrency base1

rate interestcurrency baserate erestint currency iablevar

spot

×+

×−×

×

You might find this formula useful. It is not on the ACI

formula sheets provided in the exam, so remember it!

As before, the length of each year may be 360 or 365 days.

Swap prices are generally quoted so that the last digit of the price

coincides with the same decimal place as the last digit of the spot

price. For example, if the spot price is quoted to four decimal places

(1.2166) and the swap price is "20 points", this means "0.0020".

If the year basis is the same for the two currencies and the number of

days is sufficiently small (so that the denominator in the swap points

formula is close to 1), the following approximation holds:

Calculation Summary

Approximation

yeardays

aldifferenti rate interestspotswap forward ××≈

32 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Example 19

31-day USD interest rate: 5%

31-day EUR interest rate: 3%

Spot EUR/USD rate: 1.2168

forward swap = ( ) ( )( )

( )( )36031

36031

36031

03.01

03.005.01.2168

×+

×−××

= 0.0021 or + 21 points

Approximate swap = ( ) points 21)36031

(0.021.2168 +=×+×

The following example shows that the approximation is generally not

accurate enough for longer periods. It also becomes less accurate as

the base currency interest rate increases.

Example 20

1-year USD interest rate: 5%

1-year EUR interest rate: 3%

Spot EUR/USD rate: 1.2168

( ) ( )( )

( )( )360365

360365

360365

03.01

03.005.01.2168=swap Forward

×+

×−××

= + 0.0239 or + 239 points

Approximate swap = ( ) points +247360365

0.021.2168 =×+×

Exercises

12 What is the theoretical 6-month outright price for EUR/USD, based on the following rates? The 6-month period is 181 days.

EUR/USD spot: 1.2120 EUR 6-month interest rate: 3.20% USD 6-month interest rate: 4.70%

13 What is the theoretical two-way 3-month swap price for USD/CHF, based on the following borrowing and lending rates? The 3-month period is 92 days.

USD/CHF spot: 1.7120 / 26, USD 3-month interest rate: 5.10 / 5.20% CHF 3-month interest rate: 2.70 / 2.80%

Foreign Exchange 33

19 September 2012

ACI Dealing Certificate © Markets International Ltd

14 The Eurosterling interest rate for one year (a period of exactly 365 days) is 5.9 / 6.0%. The EuroSwiss franc interest rate for the same period is 3.0 / 3.1%. The spot rate today is GBP/CHF 2.1580 / 90. What is the theoretical two-sided GBP/CHF forward outright price for one year forward?

See ‘Answers’ at the end of this chapter

Discounts and premiums

It can be seen from the formulas given above that when the base

currency interest rate is lower than the variable currency rate, the

forward outright exchange rate is always greater than the spot rate.

That is, the base currency is worth more forward units of the variable

currency forward than it is spot. This can be seen as compensating

for the lower interest rate: if I deposit money in the base currency

rather than the variable currency, I will receive less interest.

However, if I sell forward the maturing deposit amount, the forward

exchange rate is correspondingly better. In this case, the base

currency is said to be at a 'premium' to the variable currency, and the

forward swap price must be positive.

The reverse also follows. In general, given two currencies, the

currency with the higher interest rate is at a 'discount' (worth fewer

units of the other currency forward than spot) and the currency with

the lower interest rate is at a 'premium' (worth more units of the other

currency forward than spot). When the variable currency is at a

premium to the base currency, the forward swap points are negative;

when the variable currency is at a discount to the base currency, the

forward swap points are positive.

When the swap points are positive, and the forward dealer applies a

bid/offer spread to make a two-way swap price, the left price is

smaller than the right price as usual. When the swap points are

negative, he must similarly quote a "more negative" number on the

left and a "more positive" number on the right in order to make a

profit. However, the minus sign " - " is generally not shown. The

result is that the larger number appears to be on the left. As a result,

whenever the swap price appears larger on the left than the right, it is

in fact negative, and must be subtracted from the spot rate rather

than added.

34 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Key point

The currency with the higher interest rate is worth less forward

than spot in terms of the other currency and is said to be at a

forward ‘discount’. If it is the base currency, the forward points

are negative and appear to be quoted ‘high’ to ‘low’.

The currency with the lower interest rate is worth more forward

than spot in terms of the other currency and is said to be at a

forward ‘premium’. If it is the base currency, the forward points

are positive and are quoted ‘low’ to ‘high’.

Example 21

German interest rate: 3%

US interest rate: 5%

EUR is at a premium to USD

USD is at a discount to EUR

Forward swap points are positive

Example 22

The EUR is at a premium to the USD, and the swap rate is quoted as

20 / 22.

Spot EUR/USD: 1.2166 / 71

1-month swap 20 / 22

1-month outright: 1.2186 / 1.2193

The spot EUR will purchase USD 1.2166; the forward EUR will

purchase USD 1.2186. The EUR is therefore worth more in the

future, and is thus at a forward premium.

Example 23

Spot EUR/JPY: 144.25 / 144.30

1-month swap: 2.30 / 2.20

1-month outright: 141.95 / 142.10

The spot EUR will purchase JPY 144.25; the forward EUR will

purchase JPY 141.95. The EUR is therefore worth less in the future

and is thus at a forward discount.

Foreign Exchange 35

19 September 2012

ACI Dealing Certificate © Markets International Ltd

If a forward swap price includes the word 'par' it means that the spot

rate and the forward outright rate are the same: 'par' in this case

represents zero. 'A/P' is 'around par', meaning that the left-hand side

of the swap must be subtracted from spot and the right-hand side

added. This happens when the two interest rates are the same or

very similar.

Example 24

Spot USD/CAD: 1.4695 / 00

1-year swap: 6 / 4 A/P

Forward outright: 1.4689 / 1.4704

This is often written -6 / +4, which means the same as 6 / 4 A/P but

indicates more clearly how the outrights are calculated.

Beware!

Terminology

It is important to be careful about the terminology regarding

premiums and discounts. The clearest terminology for example

is to say that "the EUR is at a premium to the USD" or that "the

USD is at a discount to the EUR "; there is then no ambiguity. If

however a dealer says that "the EUR/USD is at a discount",

then what he means depends on where he is! In the UK market,

he generally means that the variable currency, USD, is at a

discount and that the swap points are to be added to the spot.

Similarly, if he says that "the GBP/JPY is at a premium", he

means that the variable currency, JPY, is at a premium and that

the points are to be subtracted from the spot. In other countries

however, he would mean the opposite.

Covering an outright position

When a trading bank quotes a forward outright price to a customer, it

has constructed the price from a spot price (which represents the FX

element of the price) and a forward swap price (which represents the

interest rate differential). Of these two, it is the spot price which is the

more volatile. If the customer deals on the price quoted, and the

bank wishes to cover the position by undertaking a spot deal and a

forward swap deal with other banks, it is therefore the spot which

must be covered urgently.

36 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Quoting a forward outright

Typically, when a corporate customer asks for a forward outright, the

bank quotes simply the outright rate. If the customer asking for a

forward outright price is another bank however, the bank quoting will

often give the two component parts of the price - the forward swap

points and the spot.

Exercises

15 Given the following rates, what would be the two-way quote for a 1-month USD/CHF forward outright?

USD/CHF spot: 1.7410 / 20 l month: 123 / 126

a. 1.7536 / 1.7543 b. 1.7284 / 1.7297 c. 1.7287 / 1.7294 d. 1.7533 / 1.7546

16 A client wishes to sell USD against GBP 3 months forward. The spot rate is 1.4340 / 1.4350 and the forward points are 72 / 68. At what outright rate will the client deal?

a. 1.4282 b. 1.4268 c. 1.4412 d. 1.4418

17 USD and EUR 3-month rates are the same. The USD yield curve is more negative than the EUR curve.

a. The 1-month EUR/USD forward points are negative. b. The 1-month EUR/USD forward points are positive. c. The 1-month EUR/USD forward points are at par. d. There is not enough information to tell.

18 The swap points for 3 months (92 days) are -173 and the swap points for 4 months (124 days) are -221. Assuming straight-line interpolation, what are the points for 98 days?

See ‘Answers’ at the end of this chapter

Foreign Exchange 37

19 September 2012

ACI Dealing Certificate © Markets International Ltd

A forward swap position

In order to see why a bank trades in forward swaps rather than

forward outrights, consider how the following swap and outright rates

change as the spot rate and interest rates move:

spot rate

EUR interest rate

USD interest rate

31-day forward outright

31-day forward swap

1.2168 3.0% 5.0% 1.2189 + 0.0021

1.2268 3.0% 5.0% 1.2289 + 0.0021

1.2268 3.5% 5.0% 1.2284 + 0.0016

A movement of 100 points in the exchange rate from 1.2168 to

1.2268 has not affected the forward swap price (to 4 decimal places).

A change in the interest rate differential from 2.0% to 1.5% however

has changed it significantly. Essentially, a forward swap is an interest

rate instrument rather than a currency instrument; when banks take

forward positions, they are taking an interest rate view rather than a

currency view. If bank dealers traded outrights, they would be

combining two related but different markets in one deal, which is less

satisfactory.

Key point

A forward FX swap price represents the interest rate differential

between the two currencies.

The table above suggests that the forward rate is unaffected by a

change in the spot rate. In fact, it is affected, but only to a relatively

small extent. The effect can be significant, however, with a large

change in the spot rate, and the effect is more significant for longer-

dated forwards than for shorter-dated ones, and also when the

interest rate differential between the currencies is greater.

The forward swap deal itself is an exchange of one currency for

another currency on one date, to be reversed on a given future date.

Thus for example when the bank sells EUR outright to a counterparty,

it may be seen as doing the following:

38 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

spot deal: Bank's spot dealer sells EUR spot

forward swap deal: .

{ Bank's forward dealer buys EUR spot

Bank's forward dealer sells EUR forward

net effect: Bank sells EUR forward outright

Therefore on a EUR/USD 1-month forward swap quote of 20 / 22, the

bank quoting the price does the following:

20 / 22

sells EUR spot buys EUR spot

buys EUR forward sells EUR forward

A forward foreign exchange swap is therefore a temporary purchase

or sale of one currency against another. An equivalent effect could

be achieved by borrowing one currency for a given period, while

lending the other currency for the same period. This is an extremely

important relationship and is why the swap rate formula reflects the

interest rate differential (generally based on Eurocurrency interest

rates rather than domestic interest rates) between the two currencies,

converted into foreign exchange terms.

Although only one single price is dealt (the swap price), the

transaction has two separate settlements:

(i) a settlement on the spot value date

(ii) a settlement on the forward value date

The dealer always ‘buys and sells’ (meaning that he buys for value on

the near date, spot and simultaneously agrees to sell again for value

on the far date) or he ‘sells and buys’ (the reverse).

Key point

A forward swap deal always involves settlements on two dates:

it is always a ‘buy and sell’ or a ‘sell and buy’.

We can see that an FX swap is approximately equivalent to a

borrowing plus a lending, as follows. Firstly, the cashflows have the

same pattern:

Foreign Exchange 39

19 September 2012

ACI Dealing Certificate © Markets International Ltd

cashflows from FX swap to ‘buy and sell’ USD agains t CHF:

spot forward

‘buy and sell’ USD: USD inflow USD outflow

‘sell and buy’ CHF: CHF outflow CHF inflow

cashflows from borrowing USD and lending CHF:

spot forward

borrow USD: USD inflow USD outflow

lend CHF: CHF outflow CHF inflow

Secondly, we know that the swap price is derived mathematically

from the borrowing and lending interest rates. So we would expect

the two sets of transactions to be equivalent.

Key point

Very important!

An FX swap to ‘buy and sell’ the base currency is equivalent to

borrowing the base currency and lending the variable currency.

And vice versa

Terminology

If a forward dealer is ‘long’, he has ‘bought and sold’ the base

currency against the variable currency. This is equivalent to

borrowing the base currency and lending the variable currency.

It is therefore equivalent to a money-market dealer being ‘long’

of the base currency by borrowing it, so the terminology is

consistent.

If a forward dealer is ‘short’, he has ‘sold and bought’ the base

currency against the variable currency.

However , this terminology is not used consistently worldwide.

Some dealers will use ‘long’ and ‘short’ in the opposite sense

from the one explained here!

40 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

If a forward dealer has bought and sold EUR (in that order) as a

speculative position, what interest rate view has he taken? He has

effectively borrowed EUR and lent USD for the period. The answer is

therefore the same as the answer to the question ‘why would the

dealer borrow EUR and/or lend USD?’ He probably expects EUR

interest rates to rise (so that he can re-lend them at a higher rate)

and/or USD rates to fall (so that he can re-borrow them at a lower

rate). In fact the important point is that the interest differential should

move in the EUR's favour. For example, even if EUR interest rates

fall rather than rise, the dealer will still make a profit as long as USD

rates fall even further.

When a bank quotes a swap rate, it quotes in a similar manner to a

spot rate. The bank buys the base currency forward on the left, and

sells the base currency forward on the right. It is very important to

remember this; it is true for the swaps we are looking at here, and

also for short-date swaps and forward-forwards as we see later.

Key point

Very important!

A spot dealer quoting a price buys the base currency on the left

and sells the base currency on the right.

A forward dealer quoting a price ‘sells and buys’ the base

currency on the left and ‘buys and sells’ the base currency on

the right.

Foreign Exchange 41

19 September 2012

ACI Dealing Certificate © Markets International Ltd

Example 25

A dealer quotes a EUR/GBP 6-month swap to a customer as 189 /

187. The customer deals at 189. What has the customer done?

The deal is done at the left side of the price. Therefore the dealer

‘sells and buys’ the base currency (EUR in this case). Therefore the

customer must be ‘buying and selling’ the base currency.

Thus the customer buys EUR and sells GBP for value on the near

date (spot) and sells EUR and buys GBP for value on the far date (6

months). The difference between the settlement rates used for the

two settlements will be -189 points.

There is no net outright position taken, and the spot dealer's spread

will not be involved, but some benchmark spot rate will nevertheless

be needed in order to arrive at the settlement rates. As the swap is a

representation of the interest rate differential between the two

currencies quoted, as long as the 'near' and 'far' settlement rates

preserve this differential, it does not generally make a large difference

which exact spot rate is used as a base for adding or subtracting the

swap points. The rate - often a middle rate - must however

normally be a current rate and is generally suggested by the dealer

quoting the swap.

42 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Example 26

Spot EUR/USD: 1.2166 / 1.2171

31-day USD interest rate: 5.0%

31-day EUR interest rate: 3.0%

31-day forward swap: 20 / 22

Our bank's dealer expects EUR interest rates to rise. He therefore

asks another bank for its price, which is quoted as 20 / 22. Our

dealer buys and sells EUR 10 million at a swap price of 20 (that is, +

0.0020). The spot rate is set at 1.2168 and the forward rate at

1.2188. The cashflows are therefore:

spot 31 days forward

buy EUR 10,000,000 sell EUR 10,000,000

sell USD 12,168,000 buy USD 12,188,000

Immediately after dealing, EUR rates in fact fall rather than rise, but

USD rates also fall, as follows:

Spot EUR/USD: 1.2166 / 1.2171

31-day USD interest rate: 4.5%

31-day EUR interest rate: 2.75%

31-day forward swap: 17 / 19

Our dealer now asks another counterparty for a price, is quoted 17 /

19, and deals to close out his position. Thus he now sells and buys

EUR at a swap price of 19 (that is, + 0.0019). The spot rate is set at

1.2168 again and the forward rate at 1.2187. The new cashflows are:

spot 31 days forward

sell EUR 10,000,000 buy EUR 10,000,000

buy USD 12,168,000 sell USD 12,187,000

The net result is a profit of USD 1,000, 31 days forward. The dealer

has made a profit because the interest differential between EUR and

USD has narrowed from 2.0% to 1.75%, even though it did not

narrow in the way he expected.

Foreign Exchange 43

19 September 2012

ACI Dealing Certificate © Markets International Ltd

In general:

Key point

A forward dealer expecting the interest rate differential to move

in favour of the base currency (for example, base currency

interest rates rise or variable currency interest rates fall) will

'buy and sell' the base currency. This is equivalent to borrowing

the base currency and depositing in the variable currency.

And vice versa

Valuation of a forward position

In the example above, we valued the result of two swaps, where the

second swap neatly offset the first. In practice, a dealer will have

many swaps on his book, resulting in many cashflows in different

currencies on different dates. The entire book can be valued by

calculating the present value of each cashflow separately and then

adding up all the present values - some positive and some negative

- to calculate an NPV. As discussed in the ‘Financial Arithmetic’

chapter, a present value is the ‘worth’ of a future cashflow, so the

NPV of a series of cashflows represents the true value of that series

of cashflows.

Terminology again

If the interest rate differential between the two currencies widens (i.e.

the interest difference becomes larger) then the forward swap points

will also become larger in absolute terms - i.e. a positive number will

become more positive, and a negative number will become more

negative. Because of this, the terminology ‘wider’ is used for larger or

swap points.

Suppose for example that the current swap points are ’78 / 76’ (which

means ‘-78 / -76’). If the interest differential becomes wider (i.e. the

two interest rates move further apart), then the swap points might

move, for example, to ’81 / 79’ (which means ‘-81 / -79’). The points

would be said to have ‘widened’. This means that the points have

become larger in absolute terms, and has nothing to do with the

bid/offer spread. Similarly, if the points are said to ‘narrow’, this

means that they become smaller in absolute terms - positive points

become less positive, or negative points become less negative.

44 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Key point

Terminology

If positive swap points become more positive, or negative points

become more negative, they are said to ‘widen’. If positive

swap points become less positive, or negative points become

less negative, they are said to ‘narrow’.

Exercises

19 You wish to take a particular speculative position and ask a bank for a 3-month USD/CHF swap price. It is quoted to you as 127 / 122 and you deal at 127. What is your expectation for market movements?

20 EUR/USD forward swaps are as follows. What can you say about the EUR and USD yield curves?

6 months: 10 / 5 12 months: 5 / 10

21 The NOK/SEK 3-month forward points move from 20 / 35 to 35 / 20. If the spot rate has not changed and Norwegian interest rates have not changed, this might suggest that:

a. Swedish interest rates have fallen. b. Swedish interest rates have risen. c. Swedish interest rates have remained the same but the

market expects rates to rise in 3 months’ time. d. Swedish interest rates have remained the same but the

market expects rates to fall in 3 months’ time.

22 Spot USD/CHF is 1.7150. The 3-month swap is quoted as 124 / 120. A customer buys and sells CHF. What settlement rates are set on the deal?

a. Spot: 1.7150, 3 months: 1.7274 b. Spot: 1.7150, 3 months: 1.7220 c. Spot: 1.7150, 3 months: 1.7026 d. Spot: 1.7150, 3 months: 1.7030

Foreign Exchange 45

19 September 2012

ACI Dealing Certificate © Markets International Ltd

23 The 3-month USD/CHF swap is quoted to you as 45 / 55. You buy and sell CHF. Later in the day, the 3-month swap is quoted to you as 65 / 75 and you close your position. Ignoring spot rate movements and NPV, have you made a profit or a loss?

24 What would be the impact of a decrease in CHF interest rates on the profitability of a short forward outright position in USD/CHF?

a. Positive b. Negative c. It depends on what happens to USD interest rates d. None

See ‘Answers’ at the end of this chapter

46 Foreign Exchange

19 September 2012

© Markets International Ltd. ACI Dealing Certificate

Historic rate rollovers

We have mentioned above that the settlement rates (spot and

forward) for a forward swap deal must generally be based on a

current market spot rate. This is because deals at non-current rates

might result in concealment of a profit or loss, in fraud, in tax evasion

or in ‘hidden’ unauthorised lending to the counterparty. For example,

if a customer has taken a speculative position which has made a loss,

a historic rate rollover enables it to roll the loss over to a later date