foreign direct investment & cross border acquisitions

TRANSCRIPT

FOREIGN DIRECT INVESTMENT &

CROSS BORDER ACQUISITION

What is FDI

The investing company may make its overseas investment in a number of ways - either by setting up a subsidiary or associate company in the foreign country, by acquiring shares of an overseas company, or through a merger or joint venture

Strategy for FDI• Firm-Specific Strategy Offering new kind of product or differentiated product. When

product innovation fails to work, a firm may adopt product differentiation strategy. This is done through putting trade mark on the product or branding. Sometimes a firm may adopt different brands for different markets to make them suitable for local markets

• Cost –Economic Strategy Done through lowering cost by moving the firm to the places

where there are cheap factors of production. The cheapness of these factors of production reduces the cost

of production and maintains an edge over other firms.

Benefits of FDI

Availability of scarce factors of production.

Improvement in Balance of Payments through export and import

substitution.

Building of economic and social infrastructure.

Fostering of economic linkages.

Strengthening of the government budget.

Stimulation of national economy. Subsidiaries of Trans-National

Corporations (TNCs), which bring the vast portion of FDI, are

estimated to produce around a third of total global exports (UNCTAD

1999).

MacDougall-Kemp Hypothesis

FDI moves from a capital-abundant economy to a capital-scarce one till the marginal productivity of capital is equal in both the countries

Industrial Organisation TheoryAn MNC with superior technology moves around to different countries to supply innovated product making in turn ample gain

Location-specific Theory

FDI moves to a country with abundant raw material and cheap labour force

The Eclectic ParadigmIt is the combination of three advantages- ownership, location and internalisation that motivates a firm to make FDI

Product Cycle Theory

FDI takes place when the product in question achieves a specific stage in its life cycle

STAGE 1

Innovation stage is characterised with quite newness of product having price-inelastic demand

STAGE 2

Maturing product stage appears when the product turns price-elastic along with similar products in the market

STAGE 3

Standardised product stage with greater price competitiveness motivates firm to start production in a low cost location

STAGE 4

De-maturing stage breaks down product standardisation with sophisticated model of the product being manufactured in high-income countries

Internalisation Approach

Internalisation is a process when an MNC passes on improved technology to its foreign subsidiary at zero/low cost in order to grab the market

Political-Economic TheoryA firm moves from a politically unstable country to a politically stable country

Recent Policy Measures100% FDI allowed in medical devices

Insurance & sub-activities - 26% to 49% FDI

100% FDI allowed in the telecom sector.

100% FDI in single-brand retail.

Removal of restriction in tea plantation sector.

FDI limit raised to 74% in credit information & 100% in asset reconstruction

companies.

Railway sector(Construction, operation and maintenance) - 100% FDI.

FDI limit of 26% in defence sector raised to 49% under Government approval

route.

Foreign Portfolio Investment up to 24% permitted under automatic route.

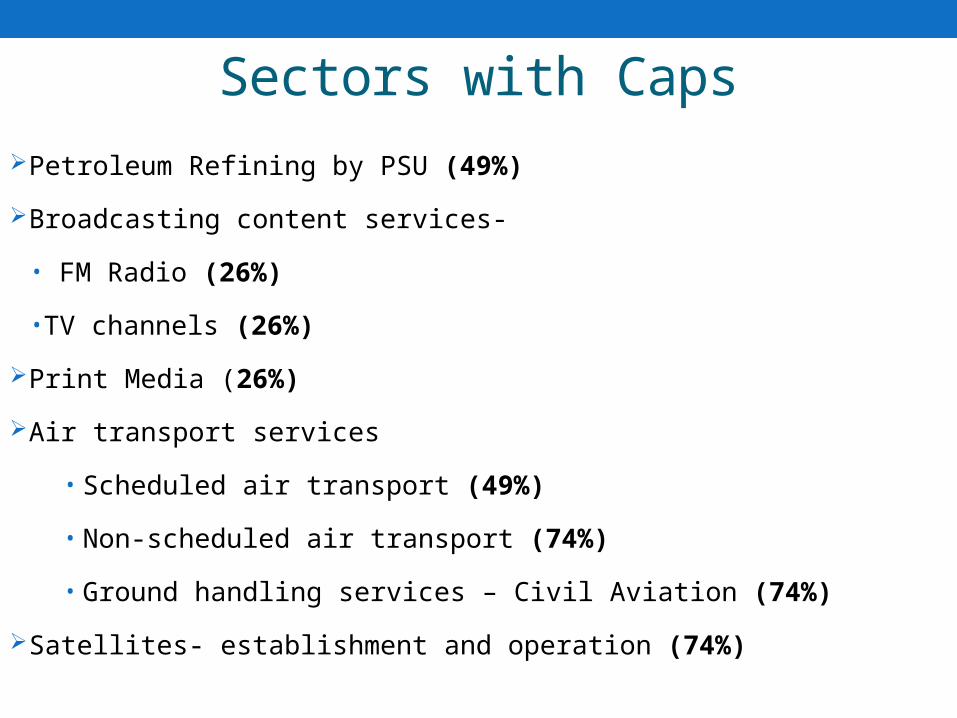

Sectors with CapsPetroleum Refining by PSU (49%)

Broadcasting content services-

• FM Radio (26%)

•TV channels (26%)

Print Media (26%)

Air transport services

• Scheduled air transport (49%)

• Non-scheduled air transport (74%)

• Ground handling services – Civil Aviation (74%)

Satellites- establishment and operation (74%)

Banking Sector

• Private Sector Banking : (74%)

• Public Sector Banking (20%)

Private security agencies (49%)

Commodity exchanges (49%)

Credit information companies (74%)

Infrastructure companies (49%)

Insurance and sub-activities (49%)

Power (49%)

Defence (49%)

MEASURES OF CONTROL The home Govt. can prohibit any investment in, or any technical

collaboration with a particular host country

It can design fiscal and monetary disincentives to deter any

outflow of investment

The home govt. can tighten the approval rules and regulations

ultimately restricting FDI outflow

The govt. can introduce extra territorially provisions and can

interfere with activities of its MNC’s foreign subsidiary

The home govt. can design the anti – trust law that can trim its

MNC’s wings to operate in foreign markets

CROSS BORDER

ACQUISITIONS

Objectives behind Cross Border Acquisitions

Top priority is profit growth and companies. Increased opportunities and cheaper alternatives to building companies internally. Increase company’s efficiency in production. Easing the process of joining operations in order to share technology while also reducing costs. Creating economic value. Additional value comes from the “synergies” created by the reconfiguration. Increasing economies of scale and expanding market reach. Releases capital for reinvestment.

Example: Acquisition between Walmart and South-African based Massmart

.

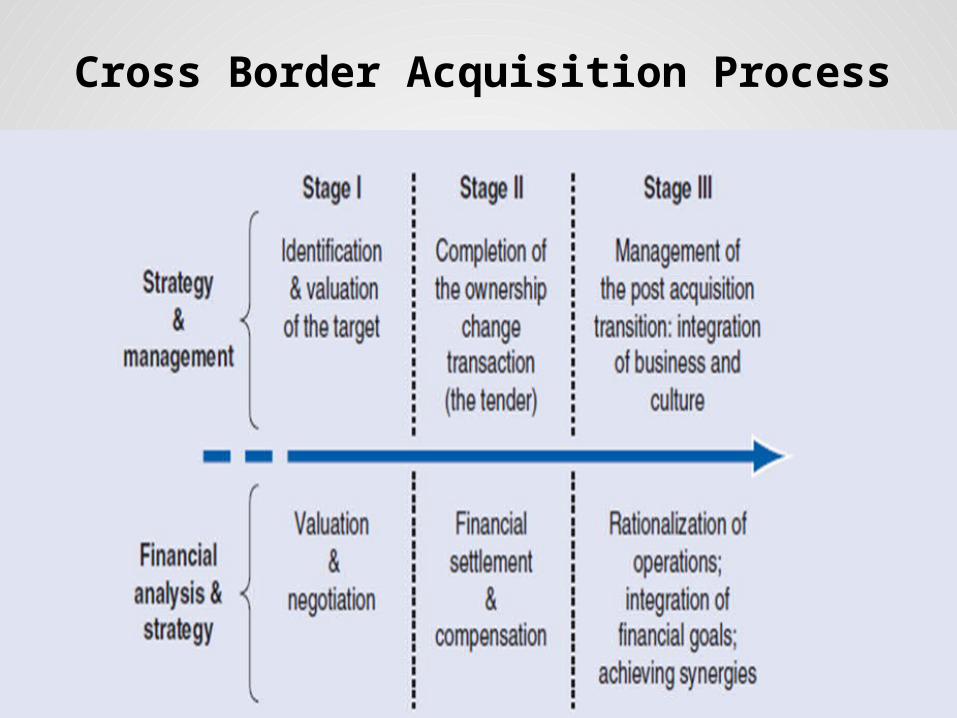

Cross Border Acquisition Process

Aspects to be concentrated before a cross border acquisition

• Understanding of Globals Accounting Differences (GAAP & IFRS)

• Understanding of Regulatory Environments.

• Understanding of Foreign & Domestic Tax Considerations.

• Understanding of Impact of acquisition on Financial Reporting.

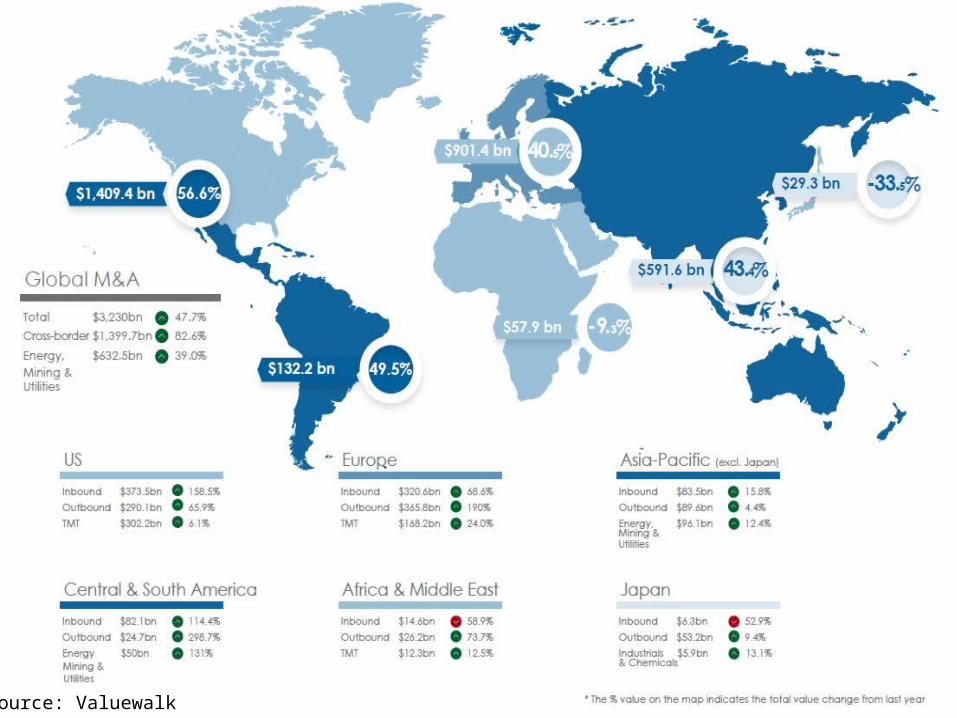

Globally - M&A transactions totaled $24.5 trillion from 2004-2013.

$8.7 trillion worth were cross-border transactions$6.7 trillion were deals in which majority control of the target company changed hands.

Global volume for cross-border acquisitions, 2004-2013Billions of nominal dollarsE&Y

Source: Valuewalk

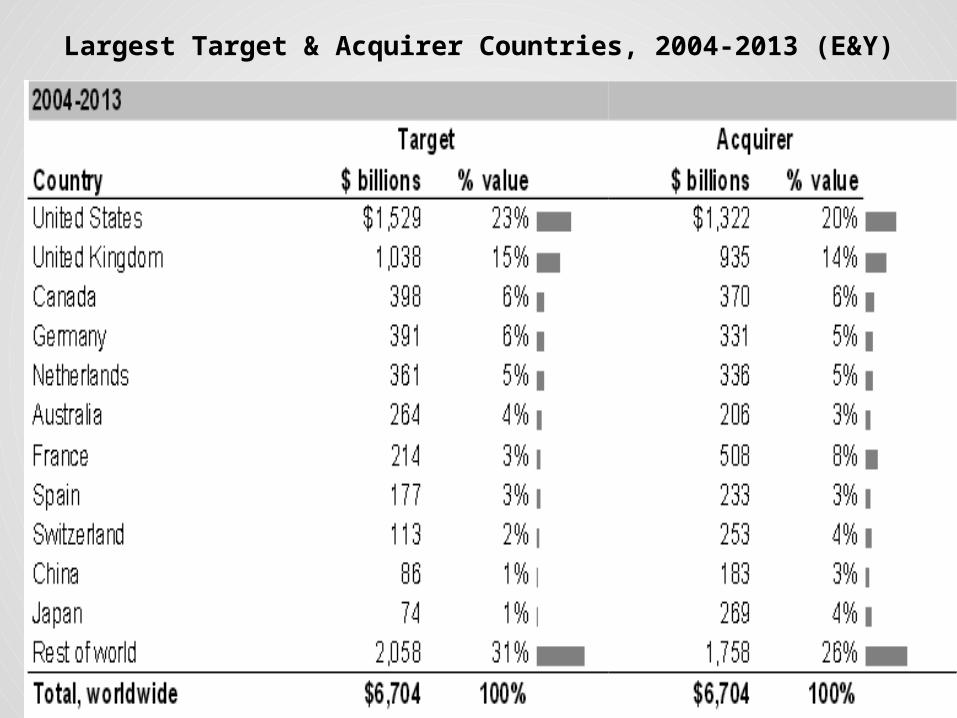

Largest Target & Acquirer Countries, 2004-2013 (E&Y)

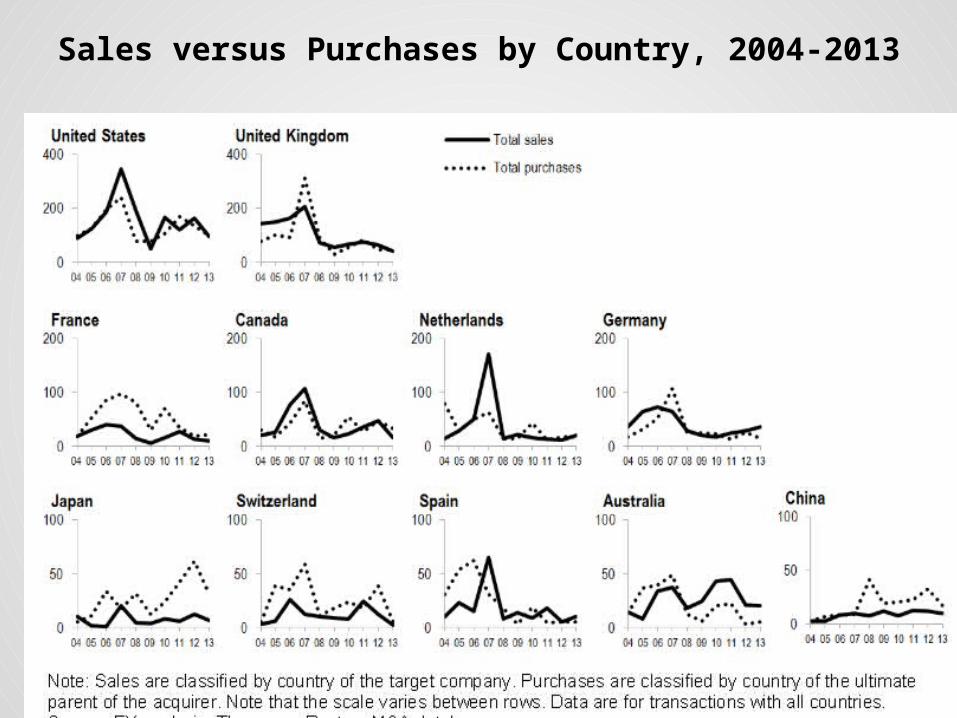

Sales versus Purchases by Country, 2004-2013

Role of Cross Border Acquisitions on U.S. EconomyUS companies are the acquirer in 20% of cross-border M&A by value

and the target in 23% by value. (E&Y 2014-15)

Price premiums paid in M&A transactions

Acquirer Target Company

Country targeted

Deal value ($ ml)

Industry

Tata Steel Corus Group plc

UK 12,000 Steel

Hindalco Novelis Canada 5,982 Steel

Videocon Daewoo Electronics Corp.

Korea 729 Electronics

Dr. Reddy's Labs

Betapharm Germany 597 Pharmaceutical

Suzlon Energy Hansen Group Belgium 565 Energy

HPCL Kenya Petroleum Refinery Ltd.

Kenya 500 Oil and Gas

Ranbaxy Labs Terapia SA Romania 324 Pharmaceutical

Tata Steel Natsteel Singapore 293 Steel

Videocon Thomson SA France 290 Electronics

VSNL Teleglobe Canada 239 Telecom

Leading Cross Border Acquisitions India & World