foreign activities reporting requirements for exempt

TRANSCRIPT

WHO TO CONTACT DURING THE LIVE PROGRAM

For Additional Registrations:

-Call Strafford Customer Service 1-800-926-7926 x1 (or 404-881-1141 x1)

For Assistance During the Live Program:

-On the web, use the chat box at the bottom left of the screen

If you get disconnected during the program, you can simply log in using your original instructions and PIN.

IMPORTANT INFORMATION FOR THE LIVE PROGRAM

This program is approved for 2 CPE credit hours. To earn credit you must:

• Participate in the program on your own computer connection (no sharing) – if you need to register

additional people, please call customer service at 1-800-926-7926 ext. 1 (or 404-881-1141 ext. 1).

Strafford accepts American Express, Visa, MasterCard, Discover.

• Listen on-line via your computer speakers.

• Respond to five prompts during the program plus a single verification code.

• To earn full credit, you must remain connected for the entire program.

Foreign Activities Reporting Requirements for Exempt

Organizations: Form 990 Schedule F and Other Returns

TUESDAY, JANUARY 14, 2020, 1:00-2:50 pm Eastern

FOR LIVE PROGRAM ONLY

Tips for Optimal Quality FOR LIVE PROGRAM ONLY

Sound Quality

When listening via your computer speakers, please note that the quality

of your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory, please e-mail [email protected]

immediately so we can address the problem.

January 14, 2020

Foreign Activities Reporting Requirements for Exempt Organizations: Form 990 Schedule F and Other Returns

Jackie Coburn, CPA, Tax Senior Manager

Crowe

Kristin Kranich, CPA, Senior Manager International Tax

Crowe

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

Foreign Activities Reporting Requirements

for Exempt Organizations: Form 990

Schedule F and Other Returns

Jackie Coburn

Kristin Kranich

From Crowe LLP

January 14, 2020

© 2019 Crowe LLP 6

Agenda

• Definition of reportable foreign activities

• Form 990 Schedule F • Reporting grants and exempt activities

• Schedule F, Part IV: statements of transfer to or ownership of foreign assets

• Other forms • Form 5471, Information Return of U.S. Persons With Respect to Foreign

Corporations

• Form 926, Transfers of Property to a Foreign Corporation

• Form 8621, Passive Foreign Investment Company

• Form 8865, Return of U.S. Persons With Respect to Certain Foreign

Partnerships

• Form 8858, Information Return of U.S. Persons With Respect to Foreign

Disregarded Entities (FDEs) and Foreign Branches (FBs)

• Form 5713, International Boycott Report

• FINCEN 114

• Case study with illustrations

© 2019 Crowe LLP 7

Your Presenters

Jackie Coburn, CPA

Tax Senior Manager+1 234 234 2345

Kristin Kranich, CPA

Senior Manager International Tax+1 415 590 3878

© 2019 Crowe LLP 8

Notice

• The information provided herein is educational in nature and is based on authorities that

are subject to change. You should contact your tax adviser regarding application of the

information provided to your specific facts and circumstances.

© 2019 Crowe LLP

Definition of Reportable Foreign Activities

9

© 2019 Crowe LLP 10

Form 990, Schedule F Reportable Activities

• Occurs when expenditures over certain $ reporting thresholds exempt

organization’s activities outside of the United States at any point in time during

the applicable tax year.

• Activities conducted outside of the U.S. is broad definition encompassing:

•Conducting fundraising

•Grantmaking

•Holding meetings

•Conference travel

•Speaking at foreign held seminar

•Having offices, employees or other agents in foreign country

•Operating an unrelated business activity

•Undertaking program service activities

•Other

© 2019 Crowe LLP 11

Activities in foreign jurisdictions

• Certain activities performed in foreign jurisdictions could create a taxable presence

and/or filing requirement in the respective country.

• The concept of exemption from income taxes for higher education institutions is

not universal.

• The OECD Commentary notes that a Contracting State may discriminate between its

public bodies and public services in comparison to the public bodies and public services of

the other Contracting State because they never can be in similar legal and factual

circumstances.

• Similarly, a Contracting State may discriminate between its own nonprofit organizations

and nonprofit organizations of the other Contracting State because of the nature of their

activities and their benefit to the Contracting State in which they reside.

• If the activities are being performed in a country with which the U.S. has an

income tax treaty, the defining factor is whether those activities create a

permanent establishment (PE) in the foreign jurisdiction.

© 2019 Crowe LLP 12

Activities in foreign jurisdictions

• A PE under the OECD Model Treaty is a fixed place of business through which

the business of an enterprise is wholly or partly carried on.

• Income attributable to a PE is taxable in the country in which the PE is located,

provided the income falls within the scope of taxable income in the local

jurisdiction.

• Certain activities may give rise to withholding tax in foreign jurisdictions

• If related to UBTI, foreign tax credits in the U.S. may be available

• Opportunities may exist in foreign countries to recoup some or all of the withholding tax

• Even in the absence of a corporate income tax liability in the foreign country,

certain other taxes may apply.

• Employment taxes

• Value added taxes

• Individual income tax liabilities for employees

• There may be potential U.S. reporting requirements related to these activities in

addition to the foreign reporting requirements.

© 2019 Crowe LLP

Form 990 Schedule F

13

© 2019 Crowe LLP 14

Form 990, Schedule F – Purpose

• Gather information activities exceeding certain $ thresholds conducted outside

the U.S.

• At any point in time in the tax year.

• Conducted directly or indirectly through a disregarded entity or partnership.

• Reportable foreign activities:

• Grants and other assistance

• Program related activities & services

• Fundraising activities

• Investment activities/holdings

• Conducting unrelated trade or business

• Maintaining offices, employees or agents outside of U.S. for purpose of

conducting any of the above.

© 2019 Crowe LLP 15

$ Reporting Thresholds - Form 990 Part IV & Schedule F

Summary- IRS Part IV

Form 990, Part IV,

Line #

$ Reporting

Threshold

Reportable Activities Complete Schedule

Part

Line 14b > $10,000, income or

expenses

activities including

grantmaking,

fundraising, business

investment and

program service

foreign activities.

Part I, General

Information on

Activities Outside of

the United States.

Line 14b > $100,000 value foreign investments Part I, General

Information on

Activities Outside of

the United States

Line 15 > $5,000 grants or other

assistance to foreign

organization(s)

Part II, Grants and

Other Assistance to

Entities Outside of the

United States.

Line 16 > $5,000 grants or other

assistance to foreign

individual(s)

Part III, Grants and

Other Assistance to

Individuals Outside the

United States.

© 2019 Crowe LLP 16

Schedule F – Content and Reporting Methodology

• Utilize same method of accounting as Financial Statements & Form 990.

• Report in U.S. dollars.

• Reporting under FASB ASC 958(SFAS 116) – grants accrued for payment in

future year, should be reported at grant’s present value.

• Determinative factor for grant reporting Schedule F, Parts II & III:

• Grantee meets Schedule F definition of foreign organization or foreign

individual, not:

•Source of grant funds – restricted or unrestricted.

•Filing organization selected the grant recipient.

• IRS instructions do not set forth how much presence or nexus in a foreign

country, instead instructions simply state activities conducted outside the U.S.

• Instructions provide one example of activities not reported at Schedule F:

Expenses incurred for services provided in the U.S. (e.g., telemedicine and services provided over the

internet) that include recipients both inside and outside the U.S. should not be reported in Part I.

© 2019 Crowe LLP 17

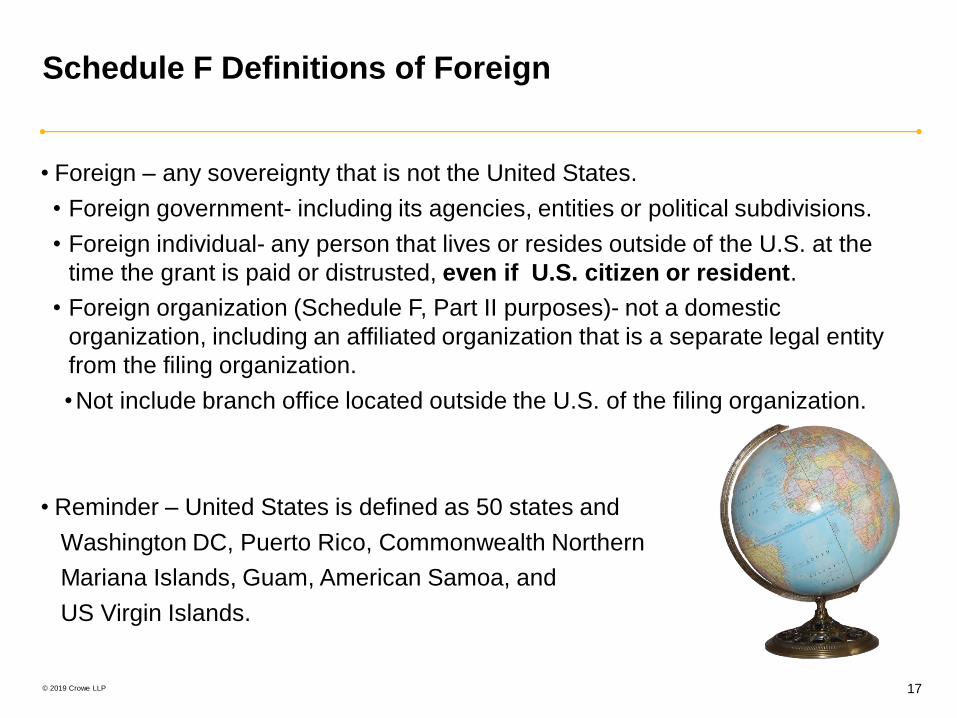

Schedule F Definitions of Foreign

• Foreign – any sovereignty that is not the United States.

• Foreign government- including its agencies, entities or political subdivisions.

• Foreign individual- any person that lives or resides outside of the U.S. at the

time the grant is paid or distrusted, even if U.S. citizen or resident.

• Foreign organization (Schedule F, Part II purposes)- not a domestic

organization, including an affiliated organization that is a separate legal entity

from the filing organization.

•Not include branch office located outside the U.S. of the filing organization.

• Reminder – United States is defined as 50 states and

Washington DC, Puerto Rico, Commonwealth Northern

Mariana Islands, Guam, American Samoa, and

US Virgin Islands.

© 2019 Crowe LLP 18

Schedule F Reporting based on 10 Regions

Schedule F Geographic Regions Countries Included

Antarctica 5th largest continent – no countries. Regulated by Antarctic Treaty System, seven claimant nations.

Central America and the Caribbean Antigua & Barbuda, Aruba, Bahamas, Barbados, Belize, Cayman Islands, Costa Rica, Cuba, Dominica, Dominican Republic,

El Salvador, Grenada, Guadeloupe, Guatemala, Haiti, Honduras, Jamaica, Martinique, Nicaragua, Panama, St. Kitts & Nevis,

St. Lucia, St. Vincent & the Grenadines, Trinidad & Tobago, Turks & Caicos Islands, and British Virgin Islands.

East Asia and the Pacific Australia, Brunei, Burma, Cambodia, China (including Hong Kong), East Timor, Fiji, Indonesia, Japan, Kiribati, Korea, Laos,

Malaysia, Marshall Islands, Micronesia, Mongolia, Nauru, New Zealand, North Korea, Palau, Papua New Guinea, Philippines,

Samoa, Singapore, Solomon Islands, South Korea, Taiwan, Thailand, Timor-Leste, Tonga, Tuvalu, Vanuatu, and Vietnam.

Europe Albania, Andorra, Austria, Belgium, Bosnia & Herzegovina, Bulgaria, Croatia, Czech Republic, Denmark, Estonia, Finland,

France, FYR Macedonia, Germany, Greece, Greenland, Holy See, Hungary, Iceland, Ireland, Italy, Kosovo, Latvia,

Liechtenstein, Lithuania, Luxembourg, Monaco, Montenegro, Netherlands, Norway, Poland, Portugal, Romania, San Marino,

Serbia, Slovakia, Slovenia, Spain, Sweden, Switzerland, Turkey, and the United Kingdom (England, Northern Ireland,

Scotland, and Wales).

Middle East and North Africa Algeria, Bahrain, Djibouti, Egypt, Iran, Iraq, Israel, Jordan, Kuwait, Lebanon, Libya, Malta, Morocco, Oman, Qatar, Saudi

Arabia, Syria, Tunisia, United Arab Emirates, West Bank and Gaza, and Yemen.

North America Canada and Mexico, but not the United States.

Russia and neighboring statesArmenia, Azerbaijan, Belarus, Georgia, Kazakhstan, Kyrgyzstan, Moldova, Russia, Tajikistan, Turkmenistan, Ukraine, and

Uzbekistan.

South AmericaArgentina, Bolivia, Brazil, Chile, Colombia, Ecuador, French Guiana, Guyana, Paraguay, Peru, Suriname, Uruguay, and

Venezuela.

South AsiaAfghanistan, Bangladesh, Bhutan, India, Maldives, Nepal, Pakistan, and Sri Lanka.

Sub-Saharan Africa Angola, Benin, Botswana, Burkina Faso, Burundi, Cameroon, Cape Verde, Central African Republic, Chad,

Comoros, Democratic Republic of the Congo, Republic of the Congo, Cote D'Ivoire, Equatorial Guinea, Eritrea,

Ethiopia, Gabon, Gambia, Ghana, Guinea, Guinea Bissau, Kenya, Lesotho, Liberia, Madagascar, Malawi, Mali,

Mauritania, Mauritius, Mozambique, Namibia, Nigeria, Rwanda, Sao Tome & Principe, Senegal, Seychelles,

Sierra Leone, Somalia, South Africa, Sudan, Swaziland, Tanzania, Togo, Uganda, Zambia, and Zimbabwe.

© 2019 Crowe LLP 19

Form 990, Schedule F, Part I, Lines 1 & 2 – Monitoring &

Making Grants Outside the United States

• Lines 1 and 2: Only required for grant making organizations making grants,

directly or indirectly, to foreign organizations, foreign governments, or foreign

individuals.

• If the foreign grants made are not large enough to trigger completing Part II or

III, still answer lines 2 and 3.

• Explaining how determines, monitors and maintains records to:

• Selection criteria.

• Substantiate grants are used as intended.

• Grantees’ eligibility.

© 2019 Crowe LLP 20

Foreign Investments – Schedule F, Part I, Line 3

• Report investments separately on Line 3 from other activities in a particular

region.

• Aggregate all investments in an IRS defined foreign geographic region.

•Excludes foreign investments held indirectly through a U.S. partnership or U.S.

corporation, because domicile of direct owner is not foreign.

• Only complete columns (a), (d) and (f) of Schedule F, Line 3.

• Value in column (f) – can be rounded to the nearest $1,000.

• Geographic area determined based on legal domicile of the investment.

• Country whose law governs the entity’s internal affairs.

© 2019 Crowe LLP 21

Foreign Investments – Schedule F, Part I, Line 3 (continued)

• Funds transferred into non-interest bearing accounts outside of the U.S. to be

used in a organization’s program services are not reportable as Schedule F, Part

I, line 3 investments.

• May cause reporting once utilized or spent for program services.

• Foreign investments information gathering tips:

• Utilize the filing organization’s financial statement footnote rollforward

workpapers for alternative investments.

• Investment rollforward for FMV as of EOY.

• Consider adding a column for the investment's country of domicile or Schedule

F geographic regions.

•Ascertain country of domicile for foreign investments not traded on exchange

reading their financial statements.

•First or second footnote in GAAP issued financial statements is generally

labeled Nature of Operations, and will include the entity type and legal

domicile.

© 2019 Crowe LLP 22

Schedule F, Part II- Grants and Other Assistance to

Organizations or Entities Outside of the U.S.

• Complete Part II if the organization answered "Yes" on Form 990, Part IV, line 15.

• Form 990, Part IX, Column (A), line 3, more than $5,000 in grants or assistance,

including program related investments to:

•Foreign organization or entity

•Foreign government

•U.S. domestic organization later granting to a designated foreign

organization.

• By recipient organization – not grouping all grantees within an IRS defined

region.

• No need to complete box (a) Name of organization or (b) IRS code section and

EIN.

• Must complete Part II, starting with (c), Region and then the applicable columns.

• Determine the Region, column (c) by:

• Grantee organization’s principal foreign office.

• No foreign office – where grant funds will be used.

© 2019 Crowe LLP 23

Schedule F, Part III- Grants & Other Assistance to

Individuals Outside the U.S.

• Required if yes to Form 990, Part IV, line 16 and the amount reported on Form

990, Part IX, Line 3, column (A) is > $5,000.

• Reporting threshold grants to foreign individuals in total.

• Not required provide individual’s name(s) – reporting based on type of

assistance, then geographic regions.

• Foreign individual- any person that lives or resides outside of the U.S. at the time

the grant is paid or distributed, even if U.S. citizen or resident.

• Assistance to unspecified individuals through another organization (foreign)

are reported at grants to foreign organization at Schedule F, Part II, not Part III.

•Must be earmarked for specific individual to report at Part III.

• Column (a) – should be specific type of assistance.

•Do not use charitable, educational, religious, or scientific.

© 2019 Crowe LLP 24

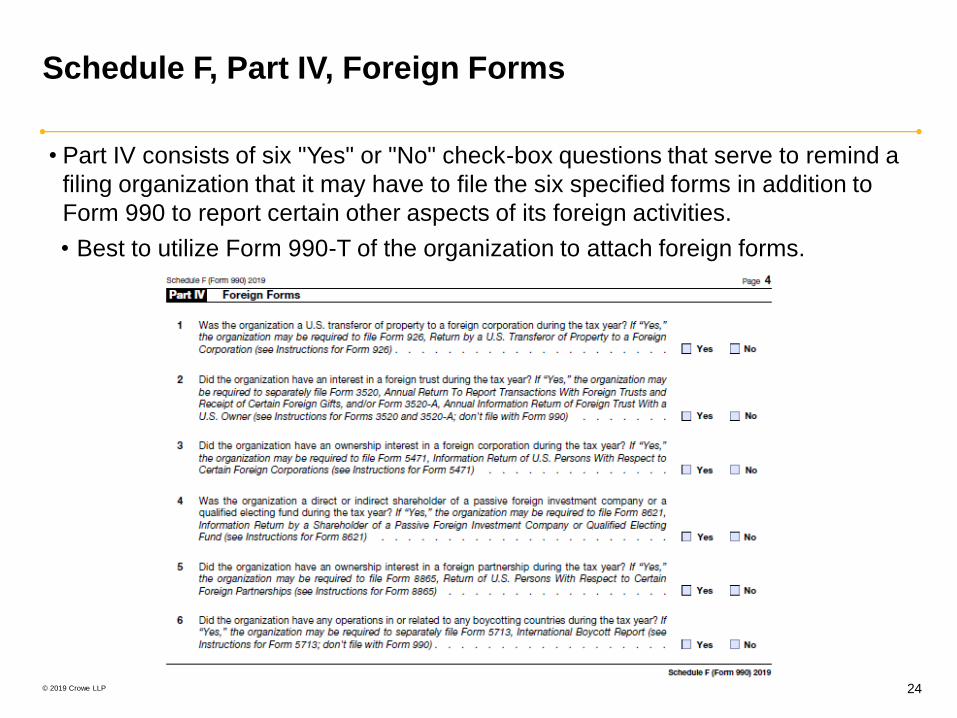

Schedule F, Part IV, Foreign Forms

• Part IV consists of six "Yes" or "No" check-box questions that serve to remind a

filing organization that it may have to file the six specified forms in addition to

Form 990 to report certain other aspects of its foreign activities.

• Best to utilize Form 990-T of the organization to attach foreign forms.

© 2019 Crowe LLP 25

Schedule F, Part V, Supplemental Information

• Used for supplemental information requested in Form 990, Schedule F or for

explanations where the filing organizations feels necessary.

• IRS required additional information:

• Part I, Line 2 – information regarding the procedures for monitoring the use of

grants or other assistance outside of the U.S.

• Part I, Line 3, column (f)- method of accounting for expenditures.

• Part II, Line 1 and Part III – method used to report grants and noncash

assistance on the organization’s financial statements.

• Part III, column (c)- how estimated number of recipients reported.

© 2019 Crowe LLP 26

Form 990, Schedule F - Information Gathering

Suggestions

• Add sort field or flag for foreign activities to build reporting capability:

• Donations, grant applications and awards.

•Uncover foreign fundraising or foreign activities to fulfill awards.

• Contracts software system.

• Business expense reimbursement system.

• Vendor set up and foreign vendor reports.

• Accounts payable for foreign vendors.

•Form 1042/1099 reporting group- inquire any Forms W-8 series.

• Travel department or travel agency utilized.

• Consult with internal legal counsel:

• VISA applications/assistance – students, researchers, etc. on appropriate VISA

type, not necessarily tourist visa.

• Contract negotiations

• Investments- Custodian statements & alternative investments rollforward and

underlying financial statements

© 2019 Crowe LLP

Other Forms

28

© 2019 Crowe LLP 29

Foreign Reporting Consequences of Foreign

Investments and Activities

• An understanding of each investment/activity is necessary to determine the

international filing requirements.

• Direct investments in domestic partnerships• Will need to look to the underlying investments made by the partnership

• Direct investments in domestic corporations• Underlying foreign investments made will not be reportable

• Direct investments in foreign partnerships• Will need to report the direct investment as well as any relevant underlying investments

• Direct investments in foreign corporations• Will need to report the direct investment

© 2019 Crowe LLP 30

Foreign Reporting Consequences of Alternative

Investments

• The entity type in the local jurisdiction may not be indicative of how it is treated in the U.S.

• Check-the-box rules allow U.S. owners to choose the U.S. tax treatment of certain foreign

entities

• Often times certain structures are set up in a way to keep tax exempt entities from having

UBTI

• It is important to find out from the investment managers how the entities are treated in the

U.S. because it affects which forms may be required to be filed

© 2019 Crowe LLP 31

International Disclosures

• Investments in foreign partnerships and foreign corporations may give rise to additional filings

with the IRS.

• Why are we concerned?

• PENALTIES!

• BEWARE – State attachments as well

• Additional filing requirements:

• Form 926, Return by a U.S. Transferor of Property to a Foreign Corporation

• Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt for Certain Foreign

Gifts

• Form 5471, Information Return of U.S. Persons with respect to Certain Foreign Corporations

• Form 8621, Information Return by a Shareholder of a Passive Foreign Investment Company or Qualified

Electing Fund

• Form 8858, Information Return of U.S. Persons with respect to Foreign Disregarded Entities

• Form 8865, Return of U.S. Persons with respect to Certain Foreign Partnerships

• Form 8886, Reportable Transaction Disclosure Statement

• FinCEN 114, Report of Foreign Bank and Financial Accounts

© 2019 Crowe LLP 32

Tax Reform Highlights

© 2019 Crowe LLP 33

U.S. Shareholder of a Controlled Foreign Corporation (CFC)

• In general, when a U.S. person owns at least 10% of a CFC, that person is a U.S.

Shareholder for Subpart F purposes

• Prior to tax reform, the U.S. Shareholder determination was made only on the

basis of voting power.

• Post TCJA, the definition of U.S. Shareholder is expanding to include a U.S.

person that owns at least 10% of the value of the CFC.

• The expanded “vote or value” definition applies to tax years beginning after

12/31/17.

• A foreign Corporation is a CFC when it is more than 50% owned by U.S.

Shareholders.

• Downward attribution:

• Post TCJA, ownership can be attributed downward to make a foreign corporation

a CFC that would have otherwise not been a CFC prior to TCJA.

© 2019 Crowe LLP 34

Global Intangible Low-Taxed Income (GILTI)

© 2019 Crowe LLP 35

• Application:

• GILTI applies to all 10% U.S. Shareholders of CFCs, not just corporations

• 50% GILTI deduction only available to C corporations

• GILTI can apply to foreign owned U.S. corporations who have foreign subsidiaries

• No GILTI deficit carryover in or out

• Foreign Tax Credit:

• GILTI is a new Foreign Tax Credit Basket (Limitation)

• No carryforward of foreign taxes “into or out of “ GILTI, tested loss taxes are lost

• Required expense allocations against GILTI income for foreign tax credit purposes can

increase US tax

• Impact to Tax Exempt Organizations:

• GILTI inclusion creates a deemed dividend

• Even though a deemed dividend is created, it may not be taxable

• Will create additional compliance efforts to properly prepare Form 5471 for US

shareholders of CFCs

• Subpart F income is an exclusion from GILTI which will minimize the GILTI impact with

respect to tax exempt entities

Other Observations on GILTI

© 2019 Crowe LLP 36

Form 5471 – Foreign Corporations

© 2019 Crowe LLP 37

Form 5471 – Foreign Corporations

• Categories of Filers• Category 1 – U.S. shareholder of a foreign corporation that is a section 965 specified foreign corporation

at any time during any tax year of the foreign corporation and who owned that stock on the last day in the year on which it was an SFC, taking into account the regulations under section 965.

• Category 2 – U.S. citizen or resident who is an officer or director a foreign corporation in which a U.S. person has acquired stock meeting the 10% ownership requirement or acquires an additional 10% or more of the outstanding stock of a foreign corporation.

• Category 3 – U.S. person who acquires stock in a foreign corporation which when added to stock already owned meets the 10% stock ownership requirement, a person who becomes a U.S. shareholder while owning more than 10%, or a U.S. person who disposes of sufficient stock to reduce his or her interest to less than 10%.• Most common for tax exempt organizations due to alternative investments

• Category 4 – U.S. person who had control of a foreign corporation during the annual accounting period of the foreign corporation. • Control is greater than 50% of the vote or value of the stock• Note – this category used to require control for at least 30 days but that was changed in 2018

• Category 5 – U.S. shareholder who owns stock in a foreign corporation that is a controlled foreign corporation at any time during any tax year of the foreign corporation, and who owned that stock on the last day in that year on which it was a CFC. • Beginning with tax years of foreign corporations after December 31, 2017, for purposes of Category 5, a U.S.

shareholder is a U.S. person who owns greater than 10% of the vote or value (previously just vote)

© 2019 Crowe LLP 38

Controlled Foreign Corporation (CFC)

• Definition Of A CFC

• Foreign corporation owned more than 50% by U.S. Shareholders

• Ownership measured by greater of vote or value

• Definition Of A U.S. Shareholder

• U.S. person who owns at least 10% of the total vote or value in a foreign corporation

• Actual, indirect, and constructive ownership all apply to the 10% test

• Definition Of A U.S. Person

• U.S. citizen or resident, domestic corporation or partnership, and certain estates and trusts

not classified as foreign

• Definition Of Specified Foreign Corporation

• A CFC, or

• Any foreign corporation with respect to which one or more domestic corporation is a U.S.

shareholder

© 2019 Crowe LLP 39

Form 5471 – 2018 Substantial Changes

© 2019 Crowe LLP 40

Form 5471 – 2019 Additional Changes

• Schedule G – Additional questions related to disallowed interest expense under Section

163(j)

• Schedule I – Subpart F inclusions broken out into separate categories of Subpart F

• Foreign personal holding company income

• Foreign base company sales income

• Foreign base company services income

• Schedule E – Updates to taxes related to previously taxed E&P

• Schedule I-1 – Breakout of interest income

• Schedule J and P – Additional previously taxed E&P pools

© 2019 Crowe LLP 41

Form 926 – Transfers to Foreign Corporations

• Used to report certain transfers of property to a foreign corporation.

• May need to file this form even if you aren’t required to file a 5471

• Transfers by a partnership are deemed to be made by the domestic partners of the partnership and not the partnership. Each domestic partner is deemed to transfer his or her proportionate share of the property.

• Transfers of cash

• Must be reported if immediately after the transfer the person holds directly or indirectly at least 10% of the vote or value of the foreign corporation or

• The amount of cash transferred by the person to the foreign corporation during the 12 month periodending on the date of the transfer exceeds $100,000

• Certain exceptions apply for certain types of property contributed in exchanges described in section 354 or 356 (certain exchanges involving stock or securities)

• All other property transfers not specifically excepted in the Regs. MUST be reported REGARDLESS of the amount transferred (foreign currency, “other property,” inventory, etc.)

© 2019 Crowe LLP 42

Schedule K-1, Sample Form 926 Footnote

© 2019 Crowe LLP 43

Form 926 – Transfers in Foreign Corporation

• The amount of cash transferred by the person to the foreign corporation during the 12

month period ending on the date of the transfer exceeds $100,000

© 2019 Crowe LLP 44

Potential Indications of a Form 5471 Filing Requirement

Based on Form 926 Answers

1. Ownership Change

If the “Before” ownership

is less than 10% and

after is greater than 10%

or if the % increases by

greater than 10%, will be

a Category 3 filer2. US Shareholder in a CFC

If the answer to the above question is Yes

and the ownership % above is greater than

10%, you may be required to file as a

Category 5 filer. If the ownership % above is

greater than 50%, you will be filing as a

Category 4 filer

© 2019 Crowe LLP 45

Form 8621 – Investments in Passive Foreign Investment

Companies (PFICs)

• What is a PFIC?

• A foreign corporation that meets either the income test or the asset test

• Income test – 75% or more of the corporation’s gross income for its taxable year is passive income

• Asset test – At least 50% of the average assets held by the foreign corporation during the taxable year are assets that produce passive income or that are held for the production of passive income

• PFIC rules are very complicated

• Exempt entities cannot make a QEF election

• Exempt entities are subject to rules of section 1291 if they are a shareholder of a PFIC and the dividend received is taxable under Subchapter F

© 2019 Crowe LLP 46

Form 8865 – Foreign Partnerships

• Categories of Filers

• Category 1 – U.S. person who controlled the foreign partnership at any time during the

partnership’s tax year.

• Control is ownership of more than a 50% interest based on profits, income, or deductions

• Category 2 –U.S. person who at any time during the tax year of the foreign partnership

owned a 10% or greater interest in the partnership while the partnership was controlled

by U.S. persons each owning at least 10%.

• Cannot be a category 2 if anyone is a category 1

• Category 3 – U.S. person who contributed property during that person’s tax year

to a foreign partnership in exchange for an interest in the partnership if the

person owned directly or indirectly at least a 10% interest in the foreign

partnership immediately after the contribution or the value of the property

contributed when added to all transfers in the last 12 months exceeds $100,000.

• If a domestic partnership contributes to a foreign partnership and the domestic partnership files

Form 8865, the partners will not be required to file

• Category 4 – U.S. person who had an acquisition, disposition, or change in ownership of

10% or more.

© 2019 Crowe LLP 47

Schedule K-1, Sample Form 8865 Footnote

© 2019 Crowe LLP 48

Form 8858 – Foreign Disregarded Entities and Foreign

Branches

Who Must File• A U.S. person that is a tax owner of an FDE or operates an FB at any time during the U.S. person's tax year or annual

accounting period.

• A U.S. person that directly (or indirectly through a tier of FDEs or partnerships) is a tax owner of an FDE or operates an

FB.

• Certain U.S. persons that are required to file Form 5471 with respect to a controlled foreign corporation (CFC) that is a

tax owner of an FDE or operates an FB at any time during the CFC's annual accounting period.

• Certain U.S. persons that are required to file Form 8865 with respect to a controlled foreign partnership (CFP) that is a

tax owner of an FDE or operates an FB at any time during the CFP's annual accounting period.

• A U.S. partnership that directly (or indirectly through a tier of FDEs or partnerships) is a tax owner of an FDE or operates

an FB.

• A U.S. corporation that is a partner in a U.S. partnership, which is required to file a Form 8858 because the U.S.

partnership is the tax owner of an FDE or an FB. Even though the U.S. corporation is not the tax owner of the FDE

and/or the FB, the U.S. corporation must complete lines 1 and 2 of the identifying information section and report its

distributive share of the items on lines 10 through 13 of Schedule G for each FDE and FB of the U.S. partnership. The

U.S. partnership must furnish all information necessary to the U.S. corporate partner for the partner to complete the

Form 8858.

© 2019 Crowe LLP 49

Form 8858 – Foreign Disregarded Entities and Foreign

Branches

Definitions

• Foreign Disregarded Entity

• An entity that is not created or organized in the United States and that is disregarded as an entity separate from its owner for U.S. income tax purposes under Regulations sections 301.7701-2 and 301.7701-3

• Foreign Branch

• An FB is defined in Regulations section 1.367(a)-6T(g). For purposes of filing a Form 8858, an FB also includes a qualified business unit (QBU) defined in Regulations section 1.989(a)-1(b)(2)(ii).• QBU is a separate and clearly identified trade or business provided separate books and records are

kept

• 2018 was the first year Form 8858 was expanded to include foreign branches. This is an important change for exempt organizations operating branches in foreign countries.

• Tax Owner

• The person that is treated as owning the assets and liabilities of the FDE for purposes of U.S. income tax law.

• Direct Owner

• The direct owner of an FDE is the legal owner of the disregarded entity.

© 2019 Crowe LLP 50

Form 5713 – International Boycott Report

• Must be filed by US persons that have operations in a boycotting country, or with the

government, a company, or a national of a boycotting country.

• The following must also file:

• A member of a controlled group, a member of which has operations

• A U.S. shareholder of a foreign corporation that has operations

• A partner in a partnership that has operations

• A person treated as the owner of a trust that has operations

• Operations – All forms of business or commercial activities and transactions, whether or

not productive of income, including, but not limited to: selling, purchasing, leasing,

licensing, banking, financing, and similar activities, extracting, processing,

manufacturing, producing, constructing, transporting, performing activities related to the

activities above (for example, contract negotiating, advertising, site selection, etc.), and

performing services, whether or not related to the activities above.

© 2019 Crowe LLP 51

Form 5713 – International Boycott Report

• Boycotting country – Any country that is on the list maintained by the Secretary of the

Treasury under section 999(a)(3).

• Currently this includes the following:

• Iraq

• Kuwait

• Lebanon

• Libya

• Qatar

• Saudi Arabia

• Syria

• United Arab Emirates

• Yemen

• Any other country in which you have operations and of which you know (or have

reason to know) requires any person to cooperate with or participate in an international

boycott.

© 2019 Crowe LLP

FINCEN 114

53

© 2019 Crowe LLP 54

Report of Foreign Bank Accounts (“FinCEN 114”)

• US persons are generally required to file FinCEN 114 if

• they have a financial interest in, or they have “signature or other authority” over one or more foreign financial accounts, and

• The aggregate value of the foreign accounts exceeds $10,000 at any time during the calendar year.

• Requirement generally applies to:

• Individuals

• Corporations

• Partnerships

• LLC’s

• Trusts

• Timely filing procedures:

• Calendar year basis

• Due date is April 15th regardless of year end• An automatic 6-month extension is also available

• MUST be filed electronically

© 2019 Crowe LLP 55

Definition of “Signature or Other Authority”

• A U.S. person has signature or other authority over a foreign financial account if

such person (alone or in conjunction with another) can control the disposition of

assets through direct communication (whether in writing or otherwise) with the

foreign financial institution.

• NOTE: “Signature or other authority” is explicitly limited to individuals only

• Preamble: “The test for determining…signature or other authority is whether the

foreign financial institution will act upon a direct communication from that individual

regarding disposition of assets.”

© 2019 Crowe LLP 56

Foreign Reporting Penalties

• Form 5471 – $10,000 penalty may be assessed for failure to file or filing an

incomplete form as well as foreign tax credit reduction of 10%

• Form 8865

• Category 1 and 2 filers – $10,000 penalty for failure to file complete or accurate form as

well as foreign tax credit reduction of 10%.

• Category 3 filer – 10% of the fair market value of the property contributed with a maximum

penalty of $100,000

• Category 4 filer – $10,000 penalty with an additional penalty for each month late after

receiving notice from the IRS with a maximum penalty of $50,000

• Form 926

• 10% of the fair market value of the property contributed with a maximum penalty of

$100,000

• FinCEN 114

• Failure to file – $10,000 unless reasonable cause is shown and all income related to the

account has been reported

• Willful failure to file – $100,000 or 50% of the account balance

© 2019 Crowe LLP

Case Study

© 2019 Crowe LLP 58

Form 990, Schedule F, Case Study 1

Amount Spent Activity Undertaken

$1,000,000 Grant to the World Health Organization, Geneva Switzerland

$200,000 (FMV at tax year end) Investment in a foreign hedge fund domiciled in Cayman Islands.

$10,000 Held annual board meeting in Mexico (travel, lodging, meals in Mexico)

$12,000 Paid a German Company for software and related consulting utilized in the

U.S. to manage its operations, both in U.S. and in foreign countries.

$12,400 Opened an office in Jakarta, Indonesia with two employees. Salary to

Jakarta employees, rent and related office expenditures in Jakarta.

$15,600 Opened an office in Nairobi, Kenya with three employees. Salary to Kenya

employees, rent and related Kenya office expenses.

$2,500 + $2,500 Jakarta office Issued 2 grants to two different agricultural organizations for

crop feasibility research: $5,000 in total grants to two different organizations

$2,500/each.

$6,000 + $4,000 Nairobi office made 2 grants two different organizations $6,000 and $4,000

$2,000 Jakarta office granted $2,000 to one individual farmer.

$4,000 Nairobi office granted $4,000 to one individual farmer.

Organization X, a U.S. §501(c)(3) organization with headquarters in New York

helps foreign nonprofit organizations and low income foreign individuals expand

agricultural development in underdeveloped foreign countries. During the 2019 tax

year, Organization X did the following:

© 2019 Crowe LLP 59

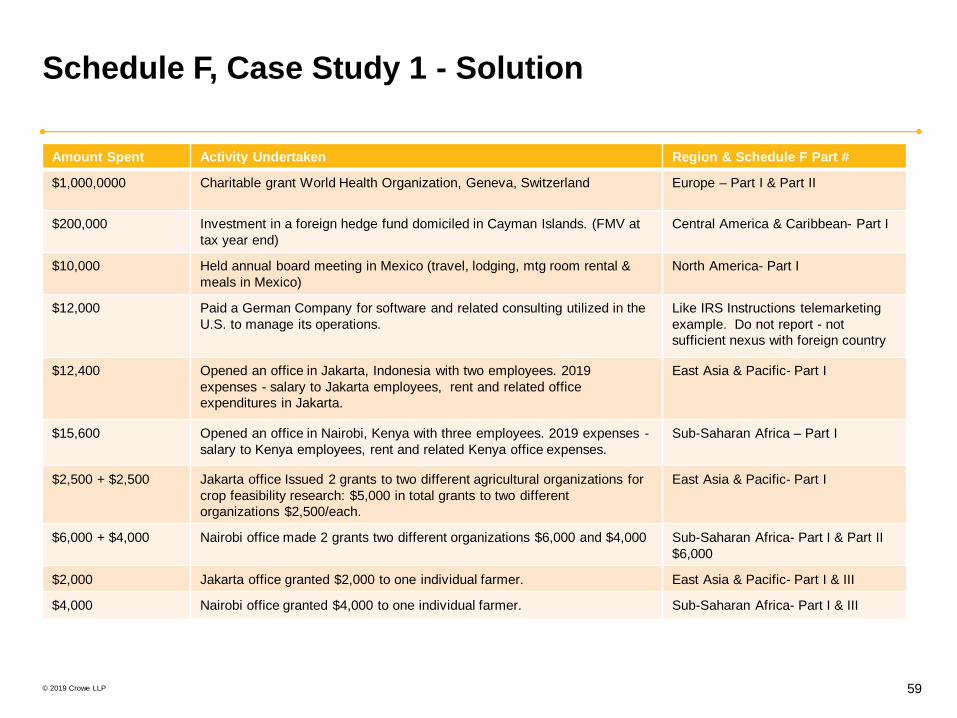

Schedule F, Case Study 1 - Solution

Amount Spent Activity Undertaken Region & Schedule F Part #

$1,000,0000 Charitable grant World Health Organization, Geneva, Switzerland Europe – Part I & Part II

$200,000 Investment in a foreign hedge fund domiciled in Cayman Islands. (FMV at

tax year end)

Central America & Caribbean- Part I

$10,000 Held annual board meeting in Mexico (travel, lodging, mtg room rental &

meals in Mexico)

North America- Part I

$12,000 Paid a German Company for software and related consulting utilized in the

U.S. to manage its operations.

Like IRS Instructions telemarketing

example. Do not report - not

sufficient nexus with foreign country

$12,400 Opened an office in Jakarta, Indonesia with two employees. 2019

expenses - salary to Jakarta employees, rent and related office

expenditures in Jakarta.

East Asia & Pacific- Part I

$15,600 Opened an office in Nairobi, Kenya with three employees. 2019 expenses -

salary to Kenya employees, rent and related Kenya office expenses.

Sub-Saharan Africa – Part I

$2,500 + $2,500 Jakarta office Issued 2 grants to two different agricultural organizations for

crop feasibility research: $5,000 in total grants to two different

organizations $2,500/each.

East Asia & Pacific- Part I

$6,000 + $4,000 Nairobi office made 2 grants two different organizations $6,000 and $4,000 Sub-Saharan Africa- Part I & Part II

$6,000

$2,000 Jakarta office granted $2,000 to one individual farmer. East Asia & Pacific- Part I & III

$4,000 Nairobi office granted $4,000 to one individual farmer. Sub-Saharan Africa- Part I & III

© 2019 Crowe LLP 60

Solution, Schedule F, Case Study 1- Part I

© 2019 Crowe LLP 61

Solution, Schedule F, Case Study 1- Parts II & III

© 2019 Crowe LLP 62

Solution, Schedule F, Case Study 1- Part V

© 2019 Crowe LLP 63

Solution – Other Foreign Reporting Considerations

Amount Spent Activity Undertaken

$200,000 (FMV at tax year end) Investment in a foreign hedge fund domiciled in Cayman Islands.

Amount Spent Activity Undertaken

$12,400 Opened an office in Jakarta, Indonesia with two employees. Salary to

Jakarta employees, rent and related office expenditures in Jakarta.

$15,600 Opened an office in Nairobi, Kenya with three employees. Salary to Kenya

employees, rent and related Kenya office expenses.

Amount Spent Activity Undertaken

$12,000 Paid a German Company for software and related consulting utilized in the

U.S. to manage its operations, both in U.S. and in foreign countries.

• Potential 926 or 8865 requirement related to contribution and type of entity

• Potential 8858 requirement to report foreign branch activity

• Potential withholding obligation on payment to foreign persons

and/or collection of W-8BEN-E form

Thank You

“Crowe” is the brand name under which the member firms of Crowe Global operate and provide professional services, and those f irms together form the Crowe Global network of independent audit, tax, and consulting firms. Crowe may be used to refer to indiv idual firms, to several such

firms, or to all firms within the Crowe Global network. The Crowe Horwath Global Risk Consulting entities, Crowe Healthcare Risk Consulting LLC, and our affiliate in Grand Cayman are subsidiaries of Crowe LLP. Crowe LLP is an Indiana limited liability partnership and the U.S member

firm of Crowe Global. Services to clients are provided by the individual member firms of Crowe Global, but Crowe Global itself is a Swiss entity that does not provide services to clients. Each member firm is a separate legal entity responsible only for its own acts and omissions and not

those of any other Crowe Global network firm or other party. Visit www.crowe.com/disclosure for more information about Crowe LLP, its subsidiaries, and Crowe Global. The information in this document is not – and is not intended to be – audit, tax, accounting, advisory, risk, performance,

consulting, business, financial, investment, legal, or other professional advice. Some firm services may not be available to attest clients. The information is general in nature, based on existing authorities, and is subject to change. The information is not a substitute for professional advice or

services, and you should consult a qualified professional adviser before taking any action based on the information. Crowe is not responsible for any loss incurred by any person who relies on the information discussed in this document. Visit www.crowe.com/disclosure for more information

about Crowe LLP, its subsidiaries, and Crowe Global. © 2019 Crowe LLP.64