forecasting stock returns under economic constraints

TRANSCRIPT

Contents lists available at ScienceDirect

Journal of Financial Economics

Journal of Financial Economics ] (]]]]) ]]]–]]]

http://d0304-40

☆ WeWe alsPastor, SmetricBayesia2013 Wcommetance. Wtheir co

n CorrE-m

atimmervalkan

1 Te2 Te

PleasEcon

journal homepage: www.elsevier.com/locate/jfec

Forecasting stock returns under economic constraints$

Davide Pettenuzzo a,1, Allan Timmermann b,c,d,2, Rossen Valkanov b,n

a Brandeis University, Sachar International Center, 415 South St, Waltham, MA, United Statesb University of California, San Diego, 9500 Gilman Drive, MC 0553, La Jolla, CA 92093, United Statesc CEPR, United Kingdomd CREATES, Denmark

a r t i c l e i n f o

Article history:Received 9 May 2013Received in revised form24 October 2013Accepted 21 November 2013

JEL classification:C11C22G11G12

Keywords:Economic constraintsSharpe ratioEquity premium predictions

x.doi.org/10.1016/j.jfineco.2014.07.0155X/& 2014 Elsevier B.V. All rights reserved.

thank an anonymous referee for many cono thank John Campbell, Wayne Ferson, Beth Pruitt, Guofu Zhou, seminar participantSociety Summer Institute and the 2013 Eun Econometrics, as well as Anthony Lynch, oestern Finance Association meetings in Laknts and suggestions. Xia Meng provided exce are grateful to John Campbell and David

des available.esponding author. Tel.: +1 858 534 0898.ail addresses: [email protected] (D. [email protected] (A. Timmermann),[email protected] (R. Valkanov).l.: +1 781 736 2834.l.: +1 858 534 0894.

e cite this article as: Pettenuzzo, D.,omics (2014), http://dx.doi.org/10.1

a b s t r a c t

We propose a new approach to imposing economic constraints on time series forecasts ofthe equity premium. Economic constraints are used to modify the posterior distribution ofthe parameters of the predictive return regression in a way that better allows the model tolearn from the data. We consider two types of constraints: non-negative equity premiaand bounds on the conditional Sharpe ratio, the latter of which incorporates time-varyingvolatility in the predictive regression framework. Empirically, we find that economicconstraints systematically reduce uncertainty about model parameters, reduce the risk ofselecting a poor forecasting model, and improve both statistical and economic measuresof out-of-sample forecast performance.

& 2014 Elsevier B.V. All rights reserved.

structive comments.lake LeBaron, Luboss at the 2013 Econo-ropean Seminar onur discussant at thee Tahoe, for helpfulellent research assis-Rapach for making

ttenuzzo),

et al., Forecasting stoc016/j.jfineco.2014.07.01

1. Introduction

Equity premium (EP) forecasts play a central role inareas as diverse as asset pricing, portfolio allocation, andperformance evaluation of investment managers.3 How-ever, more than 25 years of research shows that modelsallowing for time-varying return predictability often pro-duce worse out-of-sample forecasts than a simple bench-mark that assumes a constant risk premium. This findinghas led authors such as Bossaerts and Hillion (1999) andWelch and Goyal (2008) to question the economic value of

3 Papers on time series predictability of stock returns include Campbell(1987), Campbell and Shiller (1988), Fama and French (1988, 1989), Ferson andHarvey (1991), Keim and Stambaugh (1986) and Pesaran and Timmermann(1995). Examples of asset allocation studies under return predictability includeAït-Sahalia and Brandt (2001), Barberis (2000), Brennan, Schwartz, and Lagnado(1997), Campbell and Viceira (1999), Kandel and Stambaugh (1996), and Xia(2001). Avramov and Wermers (2006) and Ferson and Schadt (1996) considermutual fund performance under time-varying investment opportunities.

k returns under economic constraints. Journal of Financial5i

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]2

ex ante return forecasts that allow for time-varyingexpected returns.

Economically motivated constraints offer the potentialto sharpen forecasts, particularly when the data are noisyand parameter uncertainty is a concern as in returnprediction models. While economic constraints have pre-viously been found to improve forecasts of asset returns,no broad consensus exists on how to impose such con-straints. For example, Ang and Piazzesi (2003) impose no-arbitrage restrictions to identify the parameters in a termstructure model, Campbell and Thompson (2008) truncatetheir equity premium forecasts at zero and also constrainthe sign of the slope coefficients in return predictionmodels, and Pastor and Stambaugh (2009, 2012) useinformative priors to ensure that the sign of the correla-tion between shocks to unexpected and expected returnsis negative.

This paper proposes a new approach for incorporatingeconomic information via inequality constraints onmoments of the predictive distribution of the equitypremium. We focus on two types of economic constraints.The first, the equity premium constraint, follows the ideaof Campbell and Thompson (2008) and requires theconditional mean of the equity premium to be non-negative.4 It is difficult to imagine an equilibrium settingin which risk averse investors would hold stocks if theirexpected compensations were negative, and so this seemslike a mild restriction. The second stipulates that theconditional Sharpe ratio (SR) has to lie between zero anda predetermined upper bound. The zero lower bound isidentical to the equity premium constraint, and the upperbound rules out that the price of risk becomes too high.The Sharpe ratio of the market portfolio is extensivelyused in finance and, much like the equity premium,academics and investors can be expected to have strongpriors about its magnitude.5 Yet, SR constraints cast asinequality constraints on the predictive moments of thereturn distribution have not, to our knowledge, previouslybeen explicitly explored in the return predictabilityliterature.6

Other studies consider bounds on the maximum Sharperatio in the context of cross-sectional pricing models, whichis different from our focus here. MacKinlay (1995) intro-duces a bound on the maximum squared Sharpe ratio as a

4 Boudoukh, Richardson, and Smith (1993) develop tests for therestriction that the conditional equity risk premium is non-negative.They find that this restriction is violated empirically for the US stockmarket.

5 See Lettau and Wachter (2007, 2011) for recent examples oftheoretical asset pricing models that rely on calibrations using the Sharperatio. For good treatments of the Sharpe ratio and its theoretical andempirical links to asset pricing models, see Cochrane (2001) and Lettauand Ludvigson (2010).

6 Ross (2005) and Zhou (2010) consider constraints on the R2 of thepredictive return distribution. In practice, a close relation exists betweenconstraints on the Sharpe ratio and constraints on the R2. See, e.g.,Campbell and Thompson (2008) for investors with mean variance utility.Wachter and Warusawitharana (2009) also consider priors on the slopecoefficient in the return equation, which translate into priors about thepredictive R2 of the return equation. Shanken and Tamayo (2012) studyreturn predictability by allowing for time-varying risk and specify a prioron the Sharpe ratio.

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

way to distinguish between risk and nonrisk explanationsof deviations from the Capital Asset Pricing Model (CAPM).MacKinlay and Pastor (2000) provide estimates of factorpricing models that condition on a given value of theSharpe ratio. In a Bayesian setting, this corresponds toinvestors having different degrees of confidence in the assetpricing model, with a very large Sharpe ratio correspondingto completely skeptical beliefs about the model.

To incorporate economic information, we develop aBayesian approach that lets us compute the predictivedensity of the equity premium subject to economic con-straints. Importantly, the approach makes efficient use of theentire sequence of observations in computing the predictivedensity and also accounts for parameter uncertainty. Ourapproach builds on the conventional linear prediction modeland simplifies to this model if the economic constraints arenot binding in a particular sample.

The predictive moments of the return distribution getupdated as new data arrive and so the inequality con-straints give rise to dynamic learning effects. To see howthis works, suppose a new observation arrives that, underthe previous parameter estimates, imply a negative con-ditional equity premium. Because this is ruled out, theeconomic constraints can force the posterior distributionof the parameter estimates to shift significantly, evenin situations in which the estimates of the standard linearmodel do not change at all. This effect turns out to beempirically important, particularly for large values of thepredictor variables. Our empirical analysis finds that theposterior variance of the equity premium distribution—one measure of parameter estimation uncertainty—can beseveral times bigger for the unconstrained model com-pared with the constrained models, when evaluated atlarge values of the predictor variables.

Our approach toward incorporating economic constraintsworks very differently from that taken by previous studiessuch as Campbell and Thompson (2008). To highlight thesedifferences, consider the constraint that the equity premiumis non-negative. Campbell and Thompson (2008) impose thisrestriction by truncating the predicted equity premium atzero if the predicted value is negative. While this truncationapproach can be viewed as a first approximation towardimposing moment or parameter constraints, it does notmake efficient use of the information in the theoreticalconstraints. In particular, this approach never learns fromthe information that comes from observing that the esti-mated model implies negative forecasts of the equity pre-mium and so the underlying model continues to repeat thesame mistakes when faced with new data similar to pre-viously observed data. In contrast, our approach constrainsthe equity premium forecast to be non-negative at eachgiven time. This implies that we have T constraints in asample of T observations, not just a single constraint. Everytime a new pair of observations on the predictor variable andreturns becomes available, the non-negativity constraint onthe conditional equity premium is used to rule out values ofthe parameters that are infeasible given the constraint and,hence, to inform the parameter estimates.

In addition to the conditional EP constraint, we explorewhether imposing a lower and an upper bound on theSharpe ratio of the market portfolio provides further

k returns under economic constraints. Journal of Financial5i

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 3

improvements. An upper bound on the Sharpe ratio isequivalent to a time-varying upper bound on the equitypremium that is proportional to the market volatility.The implementation of such a constraint is nontrivial as itinvolves modeling the conditional volatility of the marketportfolio in a predictive regression framework. We use aparsimonious parameterization that allows us to explore timevariation in the conditional first and second moments ofreturns. We find that the SR constraint increases the statisticaland economic gains not only relative to the unconstrainedcase, but also relative to the EP constraint.

Attempts at producing improved forecasts of stockreturns have spawned a huge literature that originatedfrom studies by Campbell (1987), Campbell and Shiller(1988), Fama and French (1988, 1989), Ferson and Harvey(1991), and Keim and Stambaugh (1986), who provideconvincing economic arguments and in-sample empiricalresults that some of the fluctuations in returns are pre-dictable because of persistent time variation in expectedreturns. In-sample evidence for predictability is accumu-lating as various new variables have been suggested aspredictors of excess returns (Pontiff and Schall, 1998;Lamont, 1998; Lettau and Ludvigson, 2001; Polk,Thompson, and Vuolteenaho, 2006, among others). Out-of-sample predictability evidence, however, has beenmuch less conclusive. Paye and Timmermann (2006) andLettau and Van Nieuwerburgh (2008) argue that predict-ability weakened or disappeared during the 1990s.Bossaerts and Hillion (1999), Goyal and Welch (2003),and Welch and Goyal (2008) provide an even sharpercritique by arguing that predictability was largely an in-sample or ex post phenomenon that disappears once theforecasting models are used to guide forecasts on new,out-of-sample, data. Rapach and Zhou (2013) provide anextensive review of this literature.

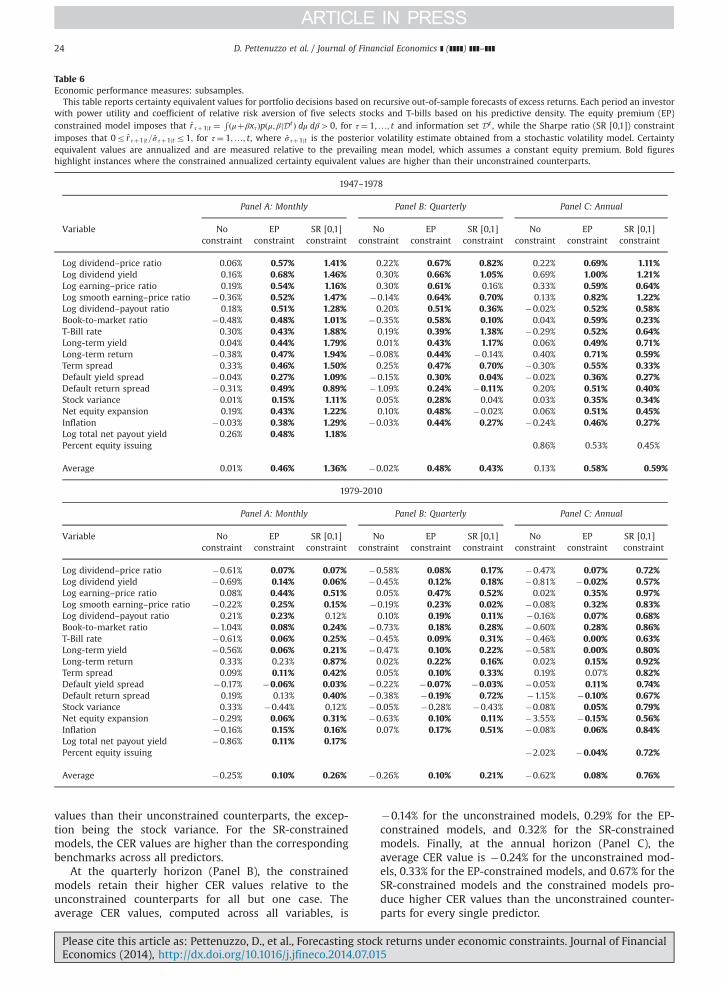

To evaluate our approach empirically, we considerthe large set of predictor variables used by Welch andGoyal (2008). When implemented along the lines proposedin our paper, for nearly all of the predictors and at themonthly, quarterly and annual frequencies, both the EP andSR constraints lead to substantial improvements in thepredictive accuracy of the equity premium forecasts. Acrossall variables, we find that when comparing the uncon-strained with the EP-constrained forecasts, the average out-of-sample R2 improves from �0.53% to 0.19% at themonthly frequency, from �2.33% to 0.47% at the quarterlyfrequency, and from �5.27% to 3.10% at the annual fre-quency. Similarly, comparing the unconstrained with the SRconstrained forecasts, the out-of-sample R2 improves from�0.53% to 0.18% at the monthly frequency, from �2.33% to1.02% at the quarterly frequency, and from �5.27% to 4.11%at the annual frequency. Hence, the improvement in pre-dictive accuracy tends to get larger as the forecast horizon isextended and the effect of estimation error in a conven-tional unconstrained model gets stronger.

Our empirical results corroborate that the Campbelland Thompson (2008) truncation approach improves onthe unconstrained forecasts for a clear majority ofthe predictors. However, we also find that imposing theEP constraint leads to an even larger gain in predictiveaccuracy, relative to the truncation approach, than the

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

truncation approach produces relative to the uncon-strained case. Specifically, at the monthly horizon, thepredictive accuracy improves for 14 out of 16 predictorsand increases the average out-of-sample R2 value by 0.4%.Similar results are found at the quarterly and annualhorizons, for which the EP constraint improves the averageout-of-sample R2 value by 1.5% and 5.2%, respectively, overthe truncated models.

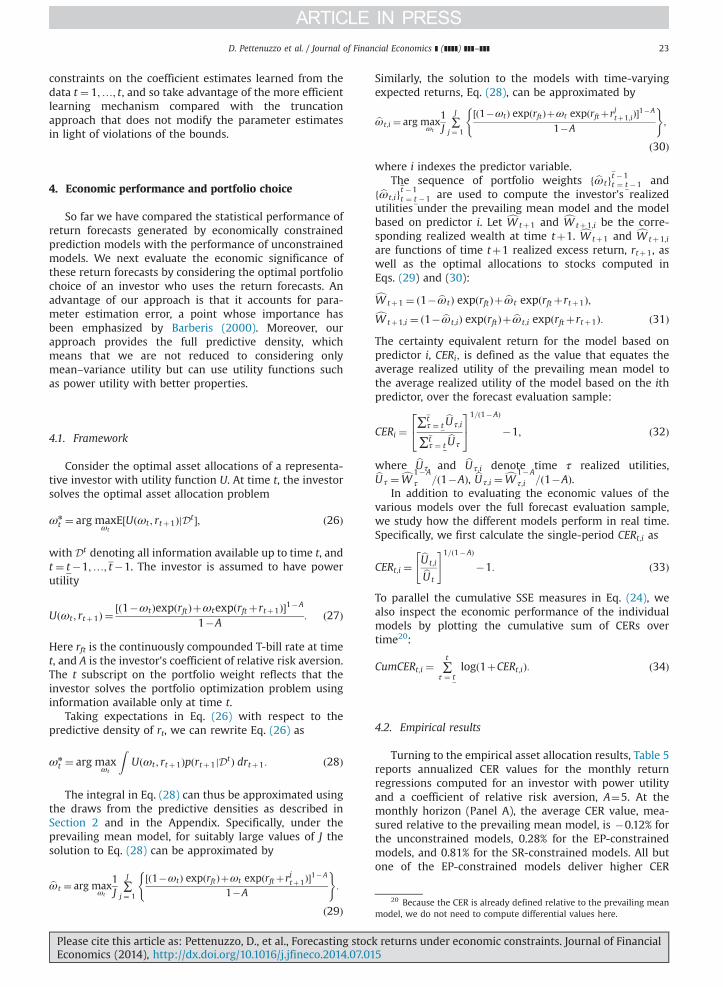

We also consider the economic value of using con-strained forecasts in the portfolio allocation of a represen-tative investor endowed with power utility. In thebenchmark case with a coefficient of relative risk aversionof five, we compare the certainty equivalent return (CER)obtained from using a given predictor relative to theprevailing mean model. The comparison is conducted forthe unconstrained as well as the EP-constrained and theSR-constrained cases at monthly, quarterly, and annualhorizons, for the entire sample and a few subsamples.Here, again, we find that the economic constraints lead tohigher CER values at all horizons and across practically allpredictors (the one exception being the stock variance).Specifically, the EP constraint results in a higher CER(relative to the unconstrained case) of 40–50 basis pointsper year. For the SR-constrained models, the increase isabout twice as high. Consistent with the predictive accu-racy results, we generally find that the SR constraintproduces higher CER improvements than the EP con-straint, which suggests that economically important inter-actions exist between the estimated mean and volatility.Robustness checks reveal that a higher (lower) risk aver-sion coefficient of 10 (2) reduces (increases) the spread inperformance across models, as the investor's willingnessto exploit any predictability is inversely proportional to therisk aversion.

The previous results refer to univariate regressionmodels with a single predictor variable. We also considertwo ways to incorporate multivariate information. First,we consider equal-weighted forecast combinations. Con-sistent with Rapach, Strauss, and Zhou (2010), we find thatsimple forecast combinations improve on the averageforecast performance, particularly for the unconstrainedforecasts that are most adversely affected by parameterestimation error. Second, we consider a diffusion indexapproach that extracts common components from thecross-section of predictor variables followed by uncon-strained or constrained equity premium predictions usingthese components. Empirically, the diffusion indexapproach produces better statistical and economic perfor-mance than the equal-weighted combination approachboth across subsamples and in the full sample. Moreover,this approach works best for the economically constrainedmodels. For example, at the quarterly horizon, the out-of-sample R2 of the diffusion index is 0.42%, 3.02%, and 2.95%for the unconstrained, EP-constrained, and SR-constrainedmodels, respectively, with associated CER values of �0.04%,0.53%, and 0.95% per annum.

The plan of the paper is as follows. Section 2 introducesour new methodology for efficiently incorporating theore-tical constraints on the predictive moments of the equitypremium distribution. Section 3 introduces the data andpresents empirical results for both unconstrained and

k returns under economic constraints. Journal of Financial5i

Fig. 1. Equity premium constraint. This figure shows the effect on the parameters μ (shown on the x-axis) and β (shown on the y-axis) from imposing theequity premium constraint μþβxtZ0, as indicated by the shaded area. The solid and dotted lines correspond to the cases in which the predictor value is setto the smallest and largest values attained in sample, and the dashed line depicts the case in which the predictor value is set to its sample average. (a) Logdividend–price ratio, �4:52rxtr�1:87, (b) T-bill rate, 0:0001rxtr0:163, (c) Log dividend–payout ratio, �1:22rxtr1:38.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]4

constrained prediction models using a range of predictorvariables. Section 4 evaluates the economic value ofimposing economic constraints on the forecasts. Section 5presents an extension to incorporate multivariate informa-tion and conducts a range of robustness tests, and Section 6concludes.

2. Methodology

This section describes how we estimate and forecastthe equity premium subject to constraints motivated byeconomic theory. These constraints take the form of

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

inequalities on the conditional equity premium or boundson the conditional Sharpe ratio.

2.1. Economic constraints on the return prediction model

The literature on return predictability commonlyassumes that stock returns, measured in excess of a risk-free rate, rτþ1, is a linear function of lagged predictorvariables, xτ:

rτþ1 ¼ μþβxτþετþ1; τ¼ 1;…; t�1;

ετþ1 �Nð0;σ2εÞ: ð1Þ

k returns under economic constraints. Journal of Financial5i

Exc

ess

retu

rns

(per

cent

)

1920 1925 1930 1935 1940 1945 1950−0.4

−0.2

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Fig. 2. Comparison of in-sample fitted values and out-of-sample forecast under the equity premium constraint and the truncation approach. This figurecompares the in-sample fitted values and out-of-sample predicted excess return for January 1947 under the equity premium constraint versus under thetruncation approach of Campbell and Thompson (2008; CT truncated). We regress excess returns ðrtþ1Þ on an intercept and the lagged log dividend–priceratio, xt over the period January 1927–December 1946: rtþ1 ¼ μþβxtþεtþ1. Estimates from this model are then used to generate in-sample fitted valuesas well as a one-step out-of-sample forecast of excess returns for January 1947. The equity premium constrained model imposes thatr̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt .

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 5

The linear model is simple to interpret and requires estimat-ing only two mean parameters, μ and β, which can readily beaccomplished by ordinary least squares (OLS).

Economic theory generally does not restrict the functionalform of the mapping linking predictor variables, xτ , to theconditional mean of excess returns, rτþ1, so the use of thelinear specification in Eq. (1) should be viewed as anapproximation. However, we argue that economically moti-vated constraints can be used to improve on this model.

2.1.1. Equity premium constraintUnder broad conditions, the conditional equity risk

premium can be expected to be positive.7 This reasoningimplies a constraint on the predictive moments of thedistribution of excess returns. In turn, this has implicationsfor the estimated parameters of the return predictionmodel equation (1). Specifically, to efficiently exploit theinformation embedded in the constraint that the condi-tional equity premium is nonnegative, the parameters μand β should be estimated subject to the constraintμþβxτZ0 at all times8:

μþβxτZ0 for τ¼ 1;…; t: ð2Þ

7 For example, this rules out that stocks hedge against other riskfactors affecting the performance of a market portfolio composed of abroader set of asset classes.

8 Here t refers to the present time, τ¼ 1;…; t�1 indexes all historical(in-sample) observations up to the present point and the out-of-sampleforecast is obtained for τ¼ t.

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

Although this constraint on the predictive moments of theequity premium is not directly a constraint on the modelparameters, θ¼ ðμ;β;σ2

εÞ, it clearly affects these para-meters because they have to be consistent with Eq. (2).Moreover, because the conditional EP constraint has tohold at each time, the number of constraints grows inproportion to the length of the sample size. The seeminglysimple EP constraint in Eq. (2), therefore, potentially yieldsa powerful way to pin down the parameters of the returnforecasting model and obtain more precise estimates.

To see how the constraint in Eq. (2) works to restrictthe μ�β parameter space, consider Fig. 1. Panel a showshow different values of x constrain the admissible set of μand β values when x is always negative (e.g., log dividendyield case). Panel b repeats this exercise when x takes ononly positive values (T-bill case), and Panel c illustrates thecase with a predictor that can take on both negative andpositive values (log dividend payout ratio case). Thesegraphs illustrate that whenever a new observation of xarrives, both small and large values of this predictor canlead to new constraints on the set of feasible parametervalues. Moreover, there are T constraints on the para-meters in a sample with T observations.

Campbell and Thompson (2008, CT) were the first toargue in favor of imposing a non-negative EP constraint.9

They implement this idea by using a truncated forecast,

9 Prior to this, some papers tested non-negativity of the equitypremium. For example, Ostdiek (1998) studies sign restrictions on theex ante equity premium and develops tests for whether this premium isnon-negative using a conditional multiple inequality approach.

k returns under economic constraints. Journal of Financial5i

μ

Intercept

1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005−2

0

2

4

6

8

10x 10−3

β

Slope coefficient

1935 1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005−0.1

−0.05

0

0.05

0.1

0.15

0.2

0.25

0.3

Fig. 3. Comparison of coefficient estimates under the equity premium constraint and the Campbell and Thompson (2008) truncation approach. This figureshows a comparison of the posterior means of the coefficient estimates in the excess return regression rtþ1 ¼ μþβxtþεtþ1. The truncation approach usesunconstrained ordinary least squares to estimate the coefficient estimates, whereas the equity premium constrained model imposes thatr̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt . Coefficient estimates are updated recursively in time from January 1947 toDecember 2010, and the model uses the default yield spread as a predictor.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]6

r̂ tþ1jt , that is simply the largest of the unconstrained OLSforecast and zero:

r̂ tþ1jt ¼maxð0; μ̂tþ β̂ txtÞ; ð3Þ

where μ̂t and β̂ t are the OLS estimates from Eq. (1), i.e.,

ðμ̂t β̂ tÞ0 ¼ ∑t�1

τ ¼ 1zτz0τ

� ��1

∑t�1

τ ¼ 1zτrτþ1

� �; ð4Þ

and zτ ¼ ð1 xτÞ0. This truncation prevents the predictedequity premium from becoming negative, but the theoreticalconstraint is not used by CT to obtain improved estimates ofμ and β in the manner reflected in Fig. 1. Specifically, CTsimply overrule the forecast if it is negative and do notimpose on their parameters that r̂τþ1jt ¼ μ̂tþ β̂ txτZ0 forτ¼ 1;…; t. While an improvement over the simple uncon-strained model, this approach does not make efficient use ofthe theoretical constraints in Eq. (2).

Fig. 2 illustrates how imposing the equity premiumconstraint to hold at all times, both in-sample and out-of-sample, in accordance with Eq. (2) can produce verydifferent forecasts than the CT truncation approach inEq. (3) even in periods in which the unconstrained out-of-sample forecast is non-negative. The figure usesmonthly excess returns and the log dividend price ratioas a predictor variable. The data are described in detail inSection 3. The figure illustrates how an out-of-sampleforecast of excess returns for 1947:01 is generated, usingdata from 1927:01 to 1946:12. Because the truncationconstraint in Eq. (3) is not binding for the out-of-sampleforecast of excess returns in 1947:01, the unconstrained

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

OLS forecast and the truncated forecast use identicalparameter values. Applying these same parameter valuesto the in-sample period (1927:01–1946:12) produces nega-tive fitted mean excess returns in 1928–29, 1936, and 1946.We view this as an undesirable property of the truncationapproach. If the equilibrium equity premium is non-negative, this should be imposed not only on the out-of-sample forecast, but also on the model used to fit historicalexcess returns, i.e., for all periods τ¼ 1;…; t:

Hence, an important difference between our EPapproach in Eq. (2) and the truncation approach is thatthe former restricts the parameter estimates of the pre-diction model and the truncation approach in Eq. (3) nevermodifies the coefficient estimates and operates only on theforecast. To further highlight the importance of this dis-tinction, Fig. 3 plots the posterior mean of the coefficientestimates from 1947 to 2010 for a return model thatincludes the default yield spread as a predictor. The figureshows that the EP constraint leads to different interceptand slope coefficient estimates than the recursive OLSestimates underlying the truncation approach of CT. Spe-cifically, the EP-constrained estimates tend to be smoother,though not generally closer to zero, than their OLS coun-terparts. This reflects the memory of the learning process,whereby the effect of binding constraints from the pastcarries over to future periods.

The linear-normal prediction model implies that the xvariables have unbounded support. We view this model asan approximation. We assume that investors impose the EPand SR constraint conditional only on the data they haveseen up to a given time, τ¼ 1;…; t. This makes the length of

k returns under economic constraints. Journal of Financial5i

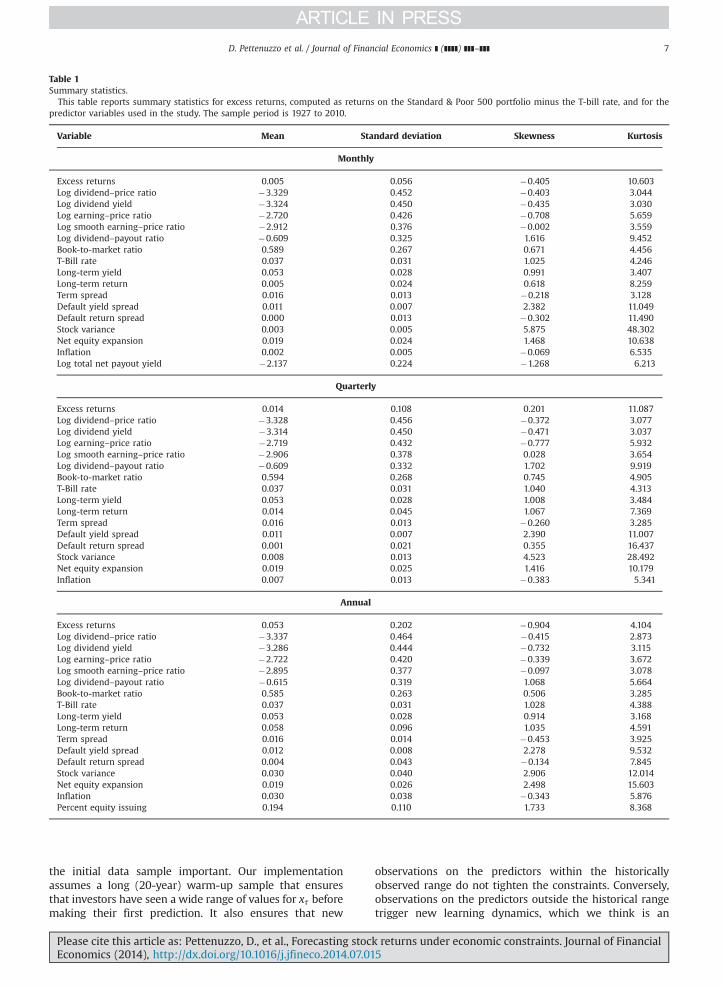

Table 1Summary statistics.

This table reports summary statistics for excess returns, computed as returns on the Standard & Poor 500 portfolio minus the T-bill rate, and for thepredictor variables used in the study. The sample period is 1927 to 2010.

Variable Mean Standard deviation Skewness Kurtosis

Monthly

Excess returns 0.005 0.056 �0.405 10.603Log dividend–price ratio �3.329 0.452 �0.403 3.044Log dividend yield �3.324 0.450 �0.435 3.030Log earning–price ratio �2.720 0.426 �0.708 5.659Log smooth earning–price ratio �2.912 0.376 �0.002 3.559Log dividend–payout ratio �0.609 0.325 1.616 9.452Book-to-market ratio 0.589 0.267 0.671 4.456T-Bill rate 0.037 0.031 1.025 4.246Long-term yield 0.053 0.028 0.991 3.407Long-term return 0.005 0.024 0.618 8.259Term spread 0.016 0.013 �0.218 3.128Default yield spread 0.011 0.007 2.382 11.049Default return spread 0.000 0.013 �0.302 11.490Stock variance 0.003 0.005 5.875 48.302Net equity expansion 0.019 0.024 1.468 10.638Inflation 0.002 0.005 �0.069 6.535Log total net payout yield �2.137 0.224 �1.268 6.213

Quarterly

Excess returns 0.014 0.108 0.201 11.087Log dividend–price ratio �3.328 0.456 �0.372 3.077Log dividend yield �3.314 0.450 �0.471 3.037Log earning–price ratio �2.719 0.432 �0.777 5.932Log smooth earning–price ratio �2.906 0.378 0.028 3.654Log dividend–payout ratio �0.609 0.332 1.702 9.919Book-to-market ratio 0.594 0.268 0.745 4.905T-Bill rate 0.037 0.031 1.040 4.313Long-term yield 0.053 0.028 1.008 3.484Long-term return 0.014 0.045 1.067 7.369Term spread 0.016 0.013 �0.260 3.285Default yield spread 0.011 0.007 2.390 11.007Default return spread 0.001 0.021 0.355 16.437Stock variance 0.008 0.013 4.523 28.492Net equity expansion 0.019 0.025 1.416 10.179Inflation 0.007 0.013 �0.383 5.341

Annual

Excess returns 0.053 0.202 �0.904 4.104Log dividend–price ratio �3.337 0.464 �0.415 2.873Log dividend yield �3.286 0.444 �0.732 3.115Log earning–price ratio �2.722 0.420 �0.339 3.672Log smooth earning–price ratio �2.895 0.377 �0.097 3.078Log dividend–payout ratio �0.615 0.319 1.068 5.664Book-to-market ratio 0.585 0.263 0.506 3.285T-Bill rate 0.037 0.031 1.028 4.388Long-term yield 0.053 0.028 0.914 3.168Long-term return 0.058 0.096 1.035 4.591Term spread 0.016 0.014 �0.453 3.925Default yield spread 0.012 0.008 2.278 9.532Default return spread 0.004 0.043 �0.134 7.845Stock variance 0.030 0.040 2.906 12.014Net equity expansion 0.019 0.026 2.498 15.603Inflation 0.030 0.038 �0.343 5.876Percent equity issuing 0.194 0.110 1.733 8.368

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 7

the initial data sample important. Our implementationassumes a long (20-year) warm-up sample that ensuresthat investors have seen a wide range of values for xτ beforemaking their first prediction. It also ensures that new

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

observations on the predictors within the historicallyobserved range do not tighten the constraints. Conversely,observations on the predictors outside the historical rangetrigger new learning dynamics, which we think is an

k returns under economic constraints. Journal of Financial5i

−0.01 −0.005 0 0.005 0.01 0.015 0.02 0.0250

50

100

150

200

250

−0.4 −0.3 −0.2 −0.1 0 0.1 0.2 0.30

5

10

15

−1 −0.5 0 0.5 1 1.50

0.5

1

1.5

2

2.5

Log dividend−price ratio

T−Bill rate

Default yield spread

Fig. 4. Slope coefficient of predictors under constrained and unconstrained models. This figure shows the posterior density of the slope coefficient, β, froma regression of monthly excess returns ðrtþ1Þ on an intercept and a lagged predictor variable, xt: rtþ1 ¼ μþβxtþεtþ1. The equity premium constrainedmodel imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt , and the Sharpe ratio constraint imposes that0r r̂ τþ1jt=σ̂ τþ1jtr1, for τ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate obtained from a stochastic volatility model. The posterior densityestimates shown here are based on the full sample at the end of 2010. Panels A, B, and C use the log dividend–price ratio, T-bill rate, and the default yieldspread as the predictor, respectively.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]8

attractive feature of our setup. Moreover, we condition onthe predictor variables, treating them as exogenous insteadof as part of the data being modeled.

2.1.2. Sharpe ratio constraintIn this subsection, we explore a novel way of sharpen-

ing the forecasts of excess market returns, namely, byplacing constraints on the conditional Sharpe ratio of themarket portfolio. Such constraints could be motivatedfrom an asset pricing perspective, as the Sharpe ratio isfrequently used in the calibration and evaluation of struc-tural asset pricing models.10 For US data, the Sharpe ratiohas been found to be time-varying and countercyclical(Brandt, 2010; Lettau and Ludvigson, 2010). More impor-tant, the empirical Sharpe ratio appears more volatile thanwhat the leading asset pricing models would suggest. Thisempirical fact has been labeled the “Sharpe ratio varia-bility puzzle” by Lettau and Ludvigson (2010). Naturally,the Sharpe ratio is most often used for portfolio perfor-mance evaluation [see Brandt, 2010 for a review article].

10 See Cochrane (2001) for a textbook treatment of the Sharpe ratio'suse in evaluating asset pricing models. Lettau and Ludvigson (2010)review whether some leading asset pricing models can replicate thestylized facts regarding the Sharpe ratio in the US. Lettau and Wachter(2007, 2011) use the Sharpe ratio in the calibration of their assetpricing model.

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

Given all the theoretical and empirical work on thissubject, most academics and practitioners are likely tohave some priors about what constitutes a reasonableSharpe ratio.

The conditional Sharpe ratio depends on both theconditional mean and volatility of the return distribution.Because time variation in volatility is a well-documentedfact in empirical finance (see, e.g., Andersen, Bollerslev,Christoffersen, and Diebold, 2006), we modify Eq. (1):

rτþ1 ¼ μþβxτþexpðhτþ1Þuτþ1; ð5Þwhere hτþ1 denotes the (log of) return volatility at timeτþ1 and uτþ1 �Nð0;1Þ. Following common stochasticvolatility models, log volatility is assumed to evolve as adriftless random walk,

hτþ1 ¼ hτþξτþ1; ð6Þwhere ξτþ1 �Nð0;σ2

ξÞ and uτ and ξs are mutually inde-pendent for all τ and s.

Next, define the (approximate) annualized conditionalSharpe ratio at time τ as

SRτþ1jτ ¼ffiffiffiffiH

pðμþβxτÞ

expðhτþ0:5σ2ξÞ; ð7Þ

where H denotes the number of observations per year (i.e.,H¼ 12, 4; and 1 with monthly, quarterly, and annual data,respectively). We assume that the conditional Sharpe ratio

k returns under economic constraints. Journal of Financial5i

−0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.025 0.030

100

200

300mean

−0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.025 0.030

100

200

300mean − 2 standard deviations

−0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.025 0.030

100

200

300mean + 2 standard deviations

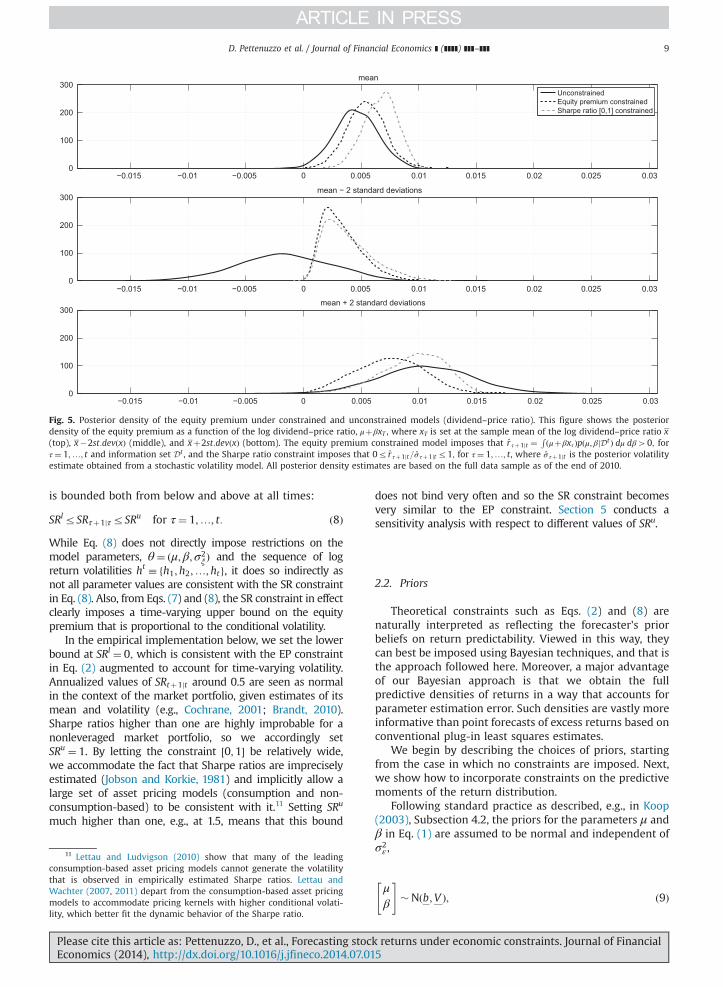

Fig. 5. Posterior density of the equity premium under constrained and unconstrained models (dividend–price ratio). This figure shows the posteriordensity of the equity premium as a function of the log dividend–price ratio, μþβxT , where xT is set at the sample mean of the log dividend–price ratio x(top), x�2st:devðxÞ (middle), and xþ2st:devðxÞ (bottom). The equity premium constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; forτ¼ 1;…; t and information set Dt , and the Sharpe ratio constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; for τ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatilityestimate obtained from a stochastic volatility model. All posterior density estimates are based on the full data sample as of the end of 2010.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 9

is bounded both from below and above at all times:

SRlrSRτþ1jτrSRu for τ¼ 1;…; t: ð8Þ

While Eq. (8) does not directly impose restrictions on themodel parameters, θ¼ ðμ;β;σ2

ξÞ and the sequence of logreturn volatilities ht � fh1;h2;…;htg, it does so indirectly asnot all parameter values are consistent with the SR constraintin Eq. (8). Also, from Eqs. (7) and (8), the SR constraint in effectclearly imposes a time-varying upper bound on the equitypremium that is proportional to the conditional volatility.

In the empirical implementation below, we set the lowerbound at SRl ¼ 0; which is consistent with the EP constraintin Eq. (2) augmented to account for time-varying volatility.Annualized values of SRtþ1jt around 0.5 are seen as normalin the context of the market portfolio, given estimates of itsmean and volatility (e.g., Cochrane, 2001; Brandt, 2010).Sharpe ratios higher than one are highly improbable for anonleveraged market portfolio, so we accordingly setSRu ¼ 1. By letting the constraint ½0;1� be relatively wide,we accommodate the fact that Sharpe ratios are impreciselyestimated (Jobson and Korkie, 1981) and implicitly allow alarge set of asset pricing models (consumption and non-consumption-based) to be consistent with it.11 Setting SRu

much higher than one, e.g., at 1.5, means that this bound

11 Lettau and Ludvigson (2010) show that many of the leadingconsumption-based asset pricing models cannot generate the volatilitythat is observed in empirically estimated Sharpe ratios. Lettau andWachter (2007, 2011) depart from the consumption-based asset pricingmodels to accommodate pricing kernels with higher conditional volati-lity, which better fit the dynamic behavior of the Sharpe ratio.

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

does not bind very often and so the SR constraint becomesvery similar to the EP constraint. Section 5 conducts asensitivity analysis with respect to different values of SRu.

2.2. Priors

Theoretical constraints such as Eqs. (2) and (8) arenaturally interpreted as reflecting the forecaster's priorbeliefs on return predictability. Viewed in this way, theycan best be imposed using Bayesian techniques, and that isthe approach followed here. Moreover, a major advantageof our Bayesian approach is that we obtain the fullpredictive densities of returns in a way that accounts forparameter estimation error. Such densities are vastly moreinformative than point forecasts of excess returns based onconventional plug-in least squares estimates.

We begin by describing the choices of priors, startingfrom the case in which no constraints are imposed. Next,we show how to incorporate constraints on the predictivemoments of the return distribution.

Following standard practice as described, e.g., in Koop(2003), Subsection 4.2, the priors for the parameters μ andβ in Eq. (1) are assumed to be normal and independent ofσ2ε ,

μβ

" #�Nðb;V Þ; ð9Þ

k returns under economic constraints. Journal of Financial5i

−0.02 −0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.025 0.030

100

200

300mean

−0.02 −0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.025 0.030

100

200

300mean − 2 standard deviations

−0.02 −0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.025 0.030

100

200

300mean + 2 standard deviations

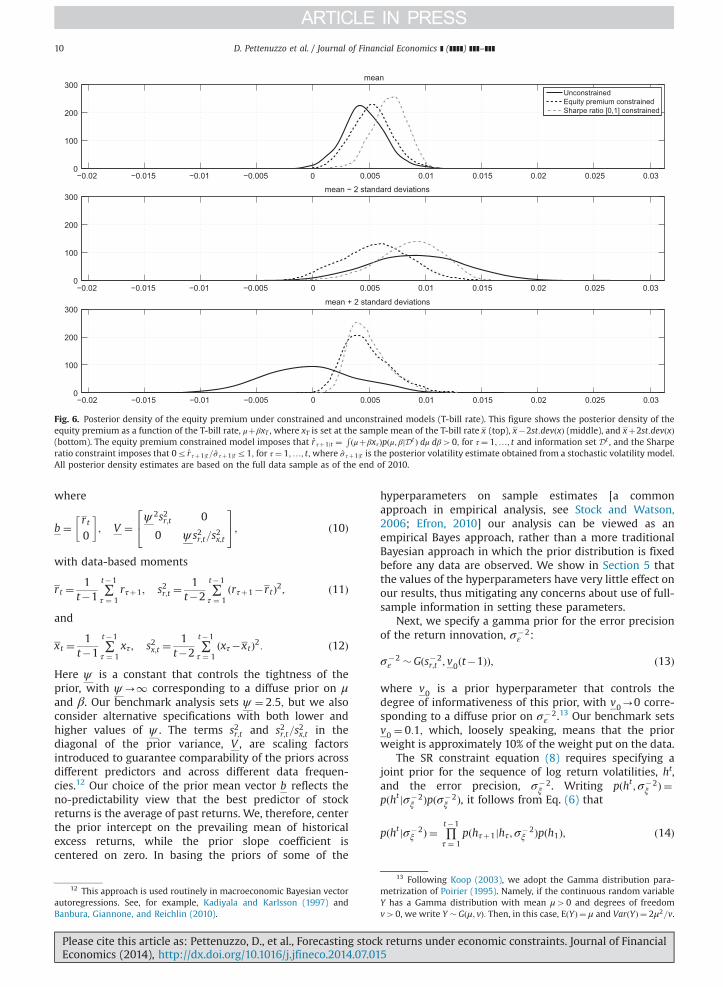

Fig. 6. Posterior density of the equity premium under constrained and unconstrained models (T-bill rate). This figure shows the posterior density of theequity premium as a function of the T-bill rate, μþβxT , where xT is set at the sample mean of the T-bill rate x (top), x�2st:devðxÞ (middle), and xþ2st:devðxÞ(bottom). The equity premium constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt , and the Sharperatio constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; for τ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate obtained from a stochastic volatility model.All posterior density estimates are based on the full data sample as of the end of 2010.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]10

where

b ¼ rt0

� �; V ¼

ψ 2s2r;t 0

0 ψ s2r;t=s2x;t

24 35; ð10Þ

with data-based moments

rt ¼1

t�1∑t�1

τ ¼ 1rτþ1; s2r;t ¼

1t�2

∑t�1

τ ¼ 1ðrτþ1�rtÞ2; ð11Þ

and

xt ¼1

t�1∑t�1

τ ¼ 1xτ ; s2x;t ¼

1t�2

∑t�1

τ ¼ 1ðxτ�xtÞ2: ð12Þ

Here ψ is a constant that controls the tightness of theprior, with ψ-1 corresponding to a diffuse prior on μand β. Our benchmark analysis sets ψ ¼ 2:5; but we alsoconsider alternative specifications with both lower andhigher values of ψ . The terms s2r;t and s2r;t=s

2x;t in the

diagonal of the prior variance, V , are scaling factorsintroduced to guarantee comparability of the priors acrossdifferent predictors and across different data frequen-cies.12 Our choice of the prior mean vector b reflects theno-predictability view that the best predictor of stockreturns is the average of past returns. We, therefore, centerthe prior intercept on the prevailing mean of historicalexcess returns, while the prior slope coefficient iscentered on zero. In basing the priors of some of the

12 This approach is used routinely in macroeconomic Bayesian vectorautoregressions. See, for example, Kadiyala and Karlsson (1997) andBanbura, Giannone, and Reichlin (2010).

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

hyperparameters on sample estimates [a commonapproach in empirical analysis, see Stock and Watson,2006; Efron, 2010] our analysis can be viewed as anempirical Bayes approach, rather than a more traditionalBayesian approach in which the prior distribution is fixedbefore any data are observed. We show in Section 5 thatthe values of the hyperparameters have very little effect onour results, thus mitigating any concerns about use of full-sample information in setting these parameters.

Next, we specify a gamma prior for the error precisionof the return innovation, σ�2

ε :

σ�2ε � Gðs�2

r;t ; v0ðt�1ÞÞ; ð13Þ

where v0 is a prior hyperparameter that controls thedegree of informativeness of this prior, with v0-0 corre-sponding to a diffuse prior on σ�2

ε .13 Our benchmark setsv0 ¼ 0:1; which, loosely speaking, means that the priorweight is approximately 10% of the weight put on the data.

The SR constraint equation (8) requires specifying ajoint prior for the sequence of log return volatilities, ht,and the error precision, σ�2

ξ . Writing pðht ;σ�2ξ Þ ¼

pðht jσ�2ξ Þpðσ�2

ξ Þ, it follows from Eq. (6) that

pðht jσ�2ξ Þ ¼ ∏

t�1

τ ¼ 1pðhτþ1jhτ ;σ�2

ξ Þpðh1Þ; ð14Þ

13 Following Koop (2003), we adopt the Gamma distribution para-metrization of Poirier (1995). Namely, if the continuous random variableY has a Gamma distribution with mean μ40 and degrees of freedomv40, we write Y � Gðμ; vÞ: Then, in this case, EðYÞ ¼ μ and VarðYÞ ¼ 2μ2=v.

k returns under economic constraints. Journal of Financial5i

−0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.0250

50

100

150

200

250mean

−0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.0250

50

100

150

200

250mean − 2 standard deviations

−0.015 −0.01 −0.005 0 0.005 0.01 0.015 0.02 0.0250

50

100

150

200

250mean + 2 standard deviations

Fig. 7. Posterior density of the equity premium under constrained and unconstrained models (default spread). This figure shows the posterior density ofthe equity premium as a function of the default yield spread, μþβxT , where xT is set at the sample mean of the default yield spread x (top), x�2st:devðxÞ(middle), and xþ2st:devðxÞ (bottom). The equity premium constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t andinformation set Dt , and the Sharpe ratio constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; for τ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimateobtained from a stochastic volatility model. All posterior density estimates are based on the full data sample as of the end of 2010.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 11

with hτþ1jhτ ;σ�2ξ �Nðhτ ;σ2

ξÞ: Thus, to complete the priorelicitation for pðht ;σ�2

ξ Þ; we need to specify priors only forh1, the initial log volatility, and σ�2

ξ . We choose these fromthe normal-gamma family as follows:

h1 �Nðlnðsr;tÞ; khÞ ð15Þ

and

σ�2ξ � Gð1=kξ;1Þ: ð16Þ

We set kξ ¼ 0:01 and choose the remaining hyperpara-meters in Eqs. (15) and (16) to imply uninformative priors,allowing the data to determine the degree of time varia-tion in the return volatility. Accordingly, we specifykh ¼ 10, and set the degrees of freedom for σ�2

ξ to 1.Section 5 discusses robustness of our results with respectto changes in the priors.

2.3. Imposing economic constraints

We next describe how we impose the economic con-straints on the model parameters. Starting with the EPconstraint, we modify the priors on μ and β in Eq. (9) to

μβ

" #�Nðb;V Þ; μ;βAAt ; ð17Þ

where At is a set such that

At ¼ fμþβxτZ0; τ¼ 1;…; tg: ð18Þ

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

Similarly, for the SR constraint, we restrict the priors onfμ;β;σ�2

ξ ;h1;h2;…;htgA ~At , where ~At is a set satisfying

~At ¼ fSRlrSRτþ1jτrSRu; τ¼ 1;…; tg; ð19Þand SRτþ1jτ is given in Eq. (7).

The Appendix provides details of how we estimate theparameters and compute forecasts for the unconstrainedand constrained models.

As a final point about the above analysis, we note thatthe boundaries of the constraints in Eqs. (2) and (8) areconstants (0, SRl; and SRu), motivated by economic con-siderations. However, one could view the boundariesthemselves as being parameters with associated priors.In that case, our specification corresponds to havingdogmatic priors on these specific parameters. This general-ization could be less meaningful for constraints that arereadily imposed by economic theory (such as the zerolower bound on the equity premium and Sharpe ratio)than for others (such as the upper bound on the Sharperatio). From an econometric perspective, updating priorsabout the boundary parameters is nontrivial. Given thatthe benefits of such a generalization are not clear, whilethe tractability and computational costs of imposing it aresubstantial, we conduct our empirical analysis by imposingthe constraints in Eqs. (2) and (8) as discussed above.

3. Empirical results

This section presents data and empirical results usingthe methods for incorporating economic constraintsdescribed in Section 2 to predict the equity premium.

k returns under economic constraints. Journal of Financial5i

Exc

ess

retu

rn fo

reca

sts

Log dividend−price ratio

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

0

5

10

x 10−3

Exc

ess

retu

rn fo

reca

sts

T−Bill rate

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

−0.015−0.01−0.00500.0050.01

Exc

ess

retu

rn fo

reca

sts

Default yield spread

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

0246810

x 10−3

Fig. 9. Out-of-sample equity premium forecasts under unconstrained and constrained models. Each month we regress excess returns ðrtþ1Þ on an interceptand a lagged predictor, xt: rtþ1 ¼ μþβxtþεtþ1. Estimates from this model are then used to generate recursive one-step out-of-sample forecasts of excessreturns and the process is repeated up to the end of the sample in 2010. The equity premium constrained model imposes thatr̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt , and the Sharpe ratio constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1, τ¼ 1;…; t,where σ̂ τþ1jt is the posterior volatility estimate obtained from a stochastic volatility model. The three graphs use different predictor variables: the logdividend–price ratio (top), the T-bill rate (middle), and the default yield spread (bottom).

−0.02 0 0.02 0.04 0.06 0.08−2

0

2

4

6

8

10 x 10−3

T−Bill rate

Pos

terio

r mea

n

−0.02 0 0.02 0.04 0.06 0.080

0.5

1

1.5

2 x 10−5

T−Bill rate

Pos

terio

r var

ianc

e

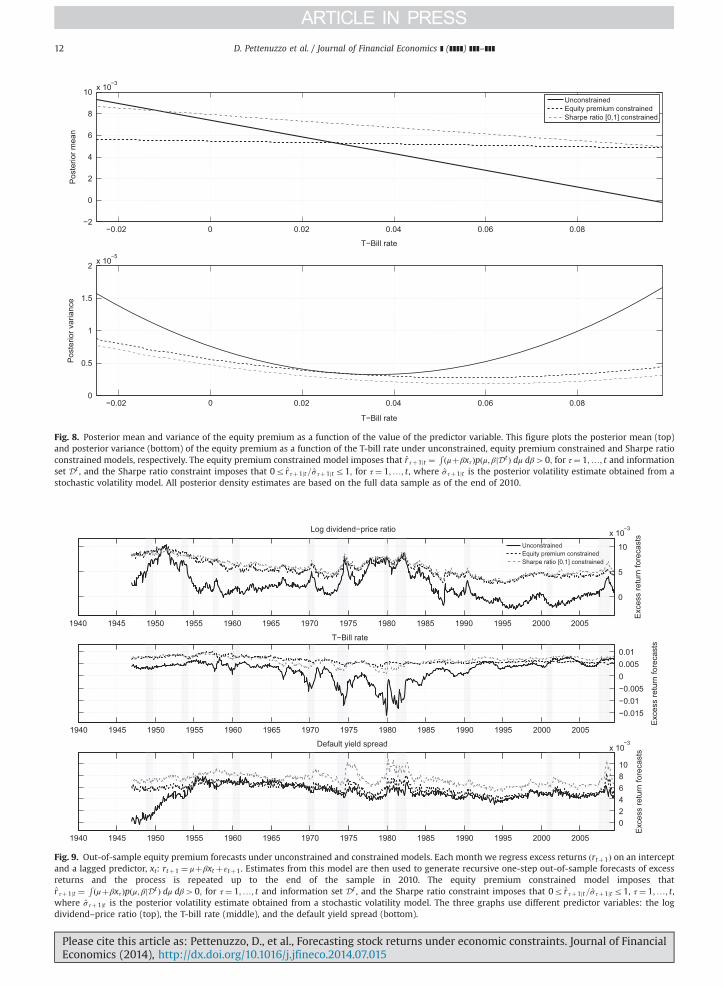

Fig. 8. Posterior mean and variance of the equity premium as a function of the value of the predictor variable. This figure plots the posterior mean (top)and posterior variance (bottom) of the equity premium as a function of the T-bill rate under unconstrained, equity premium constrained and Sharpe ratioconstrained models, respectively. The equity premium constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and informationset Dt , and the Sharpe ratio constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; for τ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate obtained from astochastic volatility model. All posterior density estimates are based on the full data sample as of the end of 2010.

Please cite this article as: Pettenuzzo, D., et al., Forecasting stock returns under economic constraints. Journal of FinancialEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.015i

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]12

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 13

3.1. Data

Our empirical analysis uses data on stock returns alongwith a set of 17 predictor variables originally analyzed inWelch and Goyal (2008) and subsequently extended up to

1940 1945 1950 1955 1960 1965 1970 1975

Fig. 10. Volatility forecasts. This figure shows the one-step-ahead recursivedistribution based on the stochastic volatility model that uses the log dihtþ1 ¼ htþξtþ1.

Log dividend−pric

1935 1940 1945 1950 1955 1960 1965 1970 1975

T−Bill rate

1935 1940 1945 1950 1955 1960 1965 1970 1975

Default yield spr

1935 1940 1945 1950 1955 1960 1965 1970 1975

Fig. 11. Conditional Sharpe ratios. This figure shows the time series of conditiobased on the unconstrained, equity premium constrained, and Sharpe ratio conststochastic volatility (SV)]. The three graphs use different predictor variables: the lspread (bottom).

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

2010 by the same authors. Stock returns are computedfrom the Standard and Poor's (S&P) 500 index and includedividends. A short T-bill rate is subtracted from stockreturns to capture excess returns. Data samples varyconsiderably across the individual predictor variables. To

Exc

ess

retu

rn v

olat

ility

1980 1985 1990 1995 2000 20050

0.05

0.1

conditional volatility forecasts computed from the predictive returnvidend–price ratio as predictor, rtþ1 ¼ μþβ logðDt=Pt Þþexpðhtþ1Þutþ1,

Ann

ualiz

ed S

harp

e ra

tio

e ratio

1980 1985 1990 1995 2000 2005

0

0.5

1

Ann

ualiz

ed S

harp

e ra

tio

1980 1985 1990 1995 2000 2005−1

−0.5

0

0.5

1

Ann

ualiz

ed S

harp

e ra

tio

ead

1980 1985 1990 1995 2000 2005

0

0.5

1

nal Sharpe ratios computed from the predictive density of excess returnsrained models [the last computed under both constant volatility (CV) andog dividend–price ratio (top), the T-bill rate (middle), and the default yield

k returns under economic constraints. Journal of Financial5i

1965 1970 1975 1980

0.01

0.02

0.03

0.04

0.05

Unconstrained μ

1965 1970 1975 1980

0.01

0.02

0.03

0.04

0.05

Equity premium constrained μ

1965 1970 1975 1980

−1

−0.8

−0.6

−0.4

−0.2

0

Unconstrained β

1965 1970 1975 1980

−1

−0.8

−0.6

−0.4

−0.2

0

Equity premium constrained β

Fig. 12. Posterior probability intervals for the parameters of the return prediction model. Each month we update the posterior density of the parametersμ; β of the return prediction model rtþ1 ¼ μþβxtþεtþ1 ; where xt is the T-bill rate and rtþ1 is the return on the Standard & Poor 500 index, measured inexcess of the T-bill rate. We then compute posterior probability intervals for these parameter estimates. Left-hand graphs report the ð2:5;97:5Þ percentileposterior probability intervals for the parameters of the unconstrained model, and right-hand graphs show results for the equity-premium constrainedmodel. The equity premium constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40 for all τ¼ 1;…; t and information set Dt . All densityestimates are updated recursively through time.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]]14

be able to compare results across the individual predictorvariables, we use the longest common sample, that is,1927–2010. In addition, we use the first 20 years of data asa training sample. For example, for the monthly data weinitially estimate our regression models over the periodJanuary 1927–December 1946, and we use the estimatedcoefficients to forecast excess returns for January 1947.We next include January 1947 in the estimation sample,which becomes January 1927–January 1947, and we usethe corresponding estimates to predict excess returns forFebruary 1947. We proceed in this recursive fashion untilthe last observation in the sample, thus producing a timeseries of one-step-ahead forecasts spanning the timeperiod from January 1947 to December 2010.

The identity of the predictor variables, along withsummary statistics, is provided in Table 1. Most variablesfall into three broad categories: (1) valuation ratios captur-ing some measure of fundamentals to market value suchas the dividend price ratio, the dividend yield, the earn-ings–price ratio, the ten-year earnings–price ratio, or thebook-to-market ratio; (2) measures of bond yields captur-ing level effects (the three-month T-bill rate and the yieldon long term government bonds), slope effects (the termspread), and default risk effects (the default yield spreaddefined as the yield spread between BAA- and AAA-ratedcorporate bonds, and the default return spread defined asthe difference between the yield on long-term corporateand government bonds); and (3) estimates of equityrisk such as the long-term return and stock variance(a volatility estimate based on daily squared returns).

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

Furthermore, three corporate finance variables are con-sidered, namely, the dividend payout ratio (the log of thedividend-earnings ratio), net equity expansion (the ratio of12-month net issues by NYSE-listed stocks over the year-end market capitalization), and percent equity issuing (theratio of equity issuing activity as a fraction of total issuingactivity) as well as a macroeconomic variable, inflation(the rate of change in the consumer price index). Wefollow Welch and Goyal (2008) and, for monthly andquarterly data, lag inflation an extra period to accountfor the delay in releases of the consumer price index.

To make our results comparable to studies from theliterature on return predictability such as Campbell andThompson (2008) and Welch and Goyal (2008), we focuson univariate regressions with a single predictor variable.However, we also consider how our approach can beextended to incorporate multivariate information (seeSection 5). Finally, because there are too many variablesto cover in detail, we focus our analysis on three pre-dictors: the log dividend–price ratio, the T-bill rate, andthe default yield spread, all of which have featuredprominently in the literature on return predictability.

3.2. Coefficient estimates and predictive densities

As shown in Figs. 1–3, the economic constraints on thepredictive moments of the return distribution affect theparameter estimates in a way that reflects the entire sequenceof data points. This gives rise to parameter estimates that arevery different from the standard, unconstrained ones typically

k returns under economic constraints. Journal of Financial5i

Table 2Out-of-sample forecast performance (monthly).

This table reports the out-of-sample R2 of unconstrained and constrained univariate prediction models for the monthly excess return, rtþ1, measured relative to the prevailing mean model:

R2OoS ¼ 1�

∑t �1τ ¼ t �1ðrtþ1� r̂ tþ1jt Þ2

∑t �1τ ¼ t �1ðrtþ1�r tþ1jt Þ2

;

where r̂ tþ1jt is the mean of the predictive return distribution based on a regression of monthly excess returns on an intercept and a lagged predictor variable, xt: rtþ1 ¼ μþβxtþεtþ1. r tþ1jt is the forecast from the

prevailing mean model, which assumes that β¼ 0. The Campbell and Thompson (CT) truncation approach sets r̂ tþ1jt ¼maxð0; μ̂ tþ β̂ txt Þ, where μ̂t and β̂ t are the time t ordinary least squares estimates of μ and β.The equity premium (EP) constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt , and the Sharpe ratio (SR [0,1]) constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1, forτ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate obtained from a stochastic volatility model. Panel A shows results for the full sample (1947–2010), while panels B and C report results for the subsamples1947–1978 and 1979–2010. Also reported are averages across all predictor variables. Bold figures highlight instances in which the constrained ROoS

2is higher than its unconstrained counterpart. We measure

statistical significance relative to the prevailing mean model using the Clark and West (2007) test statistic. nsignificance at 10% level; nnsignificance at 5% level; nnnsignificance at 1% level.

Panel A: full sample (1947–2010) Panel B: 1947–1978 Panel C: 1979–2010

Variable No CT EP SR [0,1] No CT EP SR [0,1] No CT EP SR [0,1]constraint truncation constraint constraint constraint truncation constraint constraint constraint truncation constraint constraint

Log dividend–price ratio 0.10%n 0.25%nn 0.64%nnn 0.49%nn 1.01%nn 1.01%nn 1.31%nnn 1.03%nn �0.59% �0.33% 0.14% 0.08%Log dividend yield �0.16%nn 0.31%nn 0.76%nnn 0.54%nn 0.97%nnn 1.18%nnn 1.55%nnn 1.05%nn �1.01% �0.35% 0.17% 0.16%Log earning–price ratio �1.38%n �0.45%nn 0.25%n 0.30%n �1.17%n �0.80%n 0.18% 0.43% �1.54% �0.19% 0.31% 0.20%Log smooth earning–price ratio �0.79%n 0.07%nn 0.48%nn 0.47%nn �0.14%n 0.26%n 0.81%nn 0.94%nn �1.28% �0.07% 0.23% 0.12%Log dividend–payout ratio �1.57% �1.29% �0.12% 0.03% �2.64% �2.64% �0.32% 0.23% �0.76% �0.26% 0.03% �0.12%Book-to-market ratio �1.40% �0.88% 0.02% 0.04% �0.42% �0.49% 0.08% 0.06% �2.14% �1.17% �0.03% 0.02%T-Bill rate 0.01%n 0.20%n 0.10% 0.54%nn 1.50%nn 1.21%nn 0.28% 1.40%nnn �1.11% �0.57% �0.04% �0.11%Long-term yield �0.94%n 0.20%nn 0.31%nn 0.55%nnn �0.47%n 1.02%nn 0.78%nn 1.43%nnn �1.30% �0.42% �0.04% �0.11%Long-term return �0.74% �0.62% 0.19% 0.53%nn �1.90% �1.61% 0.31% 1.25%nn 0.13% 0.13% 0.10% �0.02%Term spread 0.06% 0.04% 0.05% 0.24%n 0.41% 0.41% 0.14% 0.53%n �0.20% �0.23% �0.02% 0.02%Default yield spread �0.19% �0.18% 0.18% �0.08% �0.24% �0.22% 0.53%nn 0.22% �0.15% �0.15% �0.07% �0.31%Default return spread �0.24% �0.39% 0.15% �0.30% �0.97% �0.97% 0.37% �0.42% 0.32% 0.05% 0.00% �0.20%Stock variance 0.24% 0.11% �0.17% �0.29% �0.07% �0.07% 0.36%n 0.08% 0.48% 0.24% �0.57% �0.56%Net equity expansion �0.79% �0.77% �0.01% �0.08% 0.08% 0.12% 0.15% 0.03% �1.45% �1.44% �0.13% �0.16%Inflation �0.13% �0.13% 0.07% �0.12% �0.05% �0.05% 0.14% 0.36% �0.20% �0.20% 0.02% �0.47%Log total net payout yield �0.49%n 0.09%n 0.18% �0.01% 1.44%nnn 1.21%nn 0.45%n 0.25% �1.97% �0.76% 0.00% �0.17%

Average �0.53% �0.22% 0.19% 0.18% �0.17% �0.03% 0.44% 0.55% �0.80% �0.36% 0.01% �0.10%

Pleasecite

thisarticle

as:Petten

uzzo,D

.,etal.,Forecastin

gstock

return

sunder

econom

iccon

straints.Jou

rnalofFin

ancial

Econom

ics(2014),h

ttp://d

x.doi.org/10.1016/j.jfin

eco.2014.07.015i

D.Pettenuzzo

etal./

Journalof

FinancialEconom

ics](]]]])

]]]–]]]

15

Table 3Out-of-sample forecast performance (quarterly).

This table reports the out-of-sample R2 of unconstrained and constrained univariate prediction models for the quarterly excess return, rtþ1, measured relative to the prevailing mean model:

R2OoS ¼ 1�

∑t �1τ ¼ t �1ðrtþ1� r̂ tþ1jt Þ2

∑t �1τ ¼ t �1ðrtþ1�r tþ1jt Þ2

;

where r̂ tþ1jt is the mean of the predictive return distribution based on a regression of monthly excess returns on an intercept and a lagged predictor variable, xt: rtþ1 ¼ μþβxtþεtþ1. r tþ1jt is the forecast from the

prevailing mean model, which assumes that β¼ 0. The Campbell and Thompson (CT) truncation approach sets r̂ tþ1jt ¼maxð0; μ̂ tþ β̂ txt Þ, where μ̂t and β̂ t are the time t ordinary least squares estimates of μ and β.The equity premium (EP) constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt , and the Sharpe ratio (SR [0,1]) constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; forτ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate obtained from a stochastic volatility model. Panel A shows results for the full sample (1947–2010), while panels B and C report results for the subsamples1947–1978 and 1979–2010. Also reported are averages across all predictor variables. Bold figures highlight instances in which the constrained ROoS

2is higher than its unconstrained counterpart. We measure

statistical significance relative to the prevailing mean model using the Clark and West (2007) test statistic. nsignificance at 10% level; nnsignificance at 5% level; nnnsignificance at 1% level.

Panel A: full sample (1947–2010) Panel B: 1947–1978 Panel C: 1979–2010

Variable No CT EP SR [0,1] No CT EP SR [0,1] No CT EP SR [0,1]constraint truncation constraint constraint constraint truncation constraint constraint constraint truncation constraint constraint

Log dividend–price ratio �0.16%nn 1.20%nn 2.11%nnn 1.68%nnn 3.22%nnn 3.72%nnn 4.27%nnn 3.07%nnn �3.10% �0.98% 0.24% 0.47%Log dividend yield 0.75%nn 1.86%nn 2.04%nnn 1.88%nnn 4.19%nnn 4.18%nnn 4.04%nnn 3.38%nnn �2.22% �0.14% 0.32% 0.57%Log earning–price ratio �6.33%n �2.42%nn 0.70%nn 0.92%nn �4.65%nn �3.37%nn 0.78%n 1.60%nn �7.78% �1.60% 0.63% 0.33%Log smooth earning–price ratio �3.58%nn 0.50%nn 1.57%nn 1.60%nn �0.80%nn 1.77%nn 3.03%nn 2.96%nnn �5.98% �0.60% 0.30% 0.41%Log dividend–payout ratio �3.69% �3.02% 0.04% 0.81%nn �5.16% �5.16% �0.04% 1.75%nnn �2.42% �1.17% 0.11% 0.00%Book-to-market ratio �6.24% �3.16% �0.15% 0.96%n �1.64% �1.22% 0.04% 1.64%n �10.23% �4.84% �0.32% 0.37%T-Bill rate �0.53% 0.47% 0.01% 1.87%nnn 2.40% 2.92%nn 0.34% 3.87%nnn �3.06% �1.65% �0.27% 0.14%Long-term yield �2.70% 0.39%n 0.61%n 1.55%nnn �1.82% 2.32%nn 1.51%nn 3.41%nnn �3.45% �1.27% �0.16% �0.06%Long-term return �0.64% �0.32% 0.44% 0.66% �0.41% �0.41% 0.68% 1.46% �0.84% �0.25% 0.24% �0.03%Term spread 0.11% 0.16% 0.04% 1.21%nn 1.06% 1.06% 0.39% 2.17%nn �0.71% �0.61% �0.25% 0.38%Default yield spread �0.82% �0.74% 0.50% 0.42% �0.94% �0.75% 1.79%nn 1.49%n �0.72% �0.72% �0.62% �0.51%Default return spread �6.14% �5.43% �1.22% 0.77%n �11.02% �9.48% �1.33% 0.83%n �1.92% �1.92% �1.12% 0.72%Stock variance �0.14% �0.14% 0.12% �0.26% 0.01% 0.01% 1.66%nnn 1.53%nn �0.26% �0.26% �1.22% �1.81%Net equity expansion �4.91% �4.77% �0.19% 0.29% �0.47% �0.26% 0.28% 0.87% �8.75% �8.68% �0.60% �0.20%Inflation 0.01% 0.01% 0.40% 0.95%nn �0.26% �0.26% 0.81% 1.63%nnn 0.25% 0.25% 0.05% 0.35%

Average �2.33% �1.03% 0.47% 1.02% �1.09% �0.33% 1.22% 2.11% �3.41% �1.63% �0.18% 0.08%

Pleasecite

thisarticle

as:Petten

uzzo,D

.,etal.,Forecastin

gstock

returnsunder

econom

iccon

straints.Jou

rnalofFin

ancial

Econom

ics(2014),h

ttp://d

x.doi.org/10.1016/j.jfin

eco.2014.07.015i

D.Pettenuzzo

etal./

Journalof

FinancialEconom

ics](]]]])

]]]–]]]

16

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 17

applied in the literature on return predictability. To betterunderstand the effect of the constraints, we begin by studyingthe posterior distribution of the parameter estimates.

Fig. 4 plots the posterior density for the slope coeffi-cient, β, in the equity premium equation (1) using eitherthe log dividend–price ratio (top panel), the T-bill rate(middle), or the default yield spread (bottom) as predic-tors. Posterior densities are displayed for the uncon-strained case (solid line), the EP constraint (dark dash-dotted line), and the SR constraint (light dark-dotted line).In each case, the unconstrained posterior density for β isconsiderably wider than those of the constrained densi-ties, suggesting that the economic constraints reduceparameter uncertainty. Moreover, whereas the uncon-strained posterior densities are symmetric, the constrainedones are asymmetric in a direction that mostly reflects thatthe equity premium has to be non-negative. For example,for the log dividend price ratio, which is always negative,the EP constraint rules out large positive values of β, whichcould otherwise induce a negative equity premium. Con-versely, the constrained posterior distributions rule outlarge negative values of β for variables that take onpositive values such as the T-bill rate and the default yieldspread. The upper bound on the Sharpe ratio also mattersfor the posterior distribution of β, however, which helpsexplain why for positive predictors such as the T-bill ratethe posterior distribution of β under the SR constraint isshifted to the left compared with its distribution under theEP constraint.14

To evaluate the economic significance of the changes inthe parameter estimates caused by the constraints, wenext compare the ex ante equity premium under theunconstrained and constrained models. To this end,Figs. 5–7 show the predictive densities for the equitypremium, computed as of the end of the sample (Decem-ber 2010). To illustrate how expected returns depend onthe value taken by the predictor, we show the predictivedensities conditional on xT ¼ x as well as xT ¼ x72� SEðxÞ,where x and SEðxÞ are the full-sample average and stan-dard deviation of x; respectively.

First consider the results based on the log dividend–price ratio, logðD=PÞ (Fig. 5). This predictor is alwaysnegative and the associated posterior estimates of β arecentered on a positive value. Comparing the plots for thethree values of x illustrates how the constraints work.When logðD=PÞ is set at its sample mean (top panel), thethree posterior densities have comparable spreads,although the unconstrained model has a lower mean thanthe EP-constrained and SR-constrained models. Reducingthe log dividend–price ratio to two standard errors belowits mean (middle panel) results in a very different picture.The unconstrained posterior density for the equity pre-mium is now much more dispersed and shifted far furtherto the left, whereas the two constrained forecasts havemore probability mass to the right of zero with a tighter

14 Differences between the restricted densities do not always occurin the tail that one would expect. This happens because the upperconstraint can be satisfied by simultaneously reducing large negativeslope coefficients (as in the T-bill rate model) and shifting the density forthe intercept, μ, to the right.

Please cite this article as: Pettenuzzo, D., et al., Forecasting stocEconomics (2014), http://dx.doi.org/10.1016/j.jfineco.2014.07.01

support. When logðD=PÞ is very low (middle panel), thelower bounds imposed by the EP and SR constraints bind,thus preventing the probability mass from shifting to theleft, which otherwise happens mechanically in a linearmodel (as can be seen for the unconstrained forecast). Thiscase is empirically relevant for the period 1990–2005 withabnormally low log dividend–price ratios. Conversely,when logðD=PÞ is very high (bottom panel), the constraintsare less likely to bind, and so the three densities are moresimilar in shape, although once again the centers of thedistributions clearly differ.

For the T-bill rate (Fig. 6), similar mechanisms are atwork, although now with the opposite sign because theT-bill rate is always positive and the posterior estimates ofβ are centered on a negative value. This means that thelower constraints now bind when the T-bill rate is set atxþ2� SEðxÞ (bottom panel), once again leading to muchtighter distributions under the EP and SR constraints thanfor the unconstrained case. Empirically, this occurred inthe early 1980s, when the T-bill rate was particularly high.Finally, the model based on the default yield spread (Fig. 7)shows less of an asymmetry across the three conditioningscenarios regarding the shape and spread of the condi-tional posterior density estimates of the equity premium.

These figures imply that the economic constraintstighten the predictive density for the equity premium ina manner that depends asymmetrically on whether thepredictor variables take on large negative or positivevalues. Hence, how informative the bounds are, i.e., byhow much they shift and tighten the posterior density,depends on the value taken by the predictor variable, x.We illustrate this effect in Fig. 8 for the plots based on theT-bill rate.15 The top panel depicts the posterior mean ofthe equity premium distribution as a function of the T-billrate. The posterior mean declines linearly for theunconstrained model from a level near 1% per month forthe lowest values of the T-bill range to a level nearzero for the highest values.16 Under the SR- and EP-constrained models, the posterior mean is also reducedas the T-bill rate increases, but by far less than under theunconstrained model.

Turning to the uncertainty surrounding the predictedequity premium, the posterior variance of the equitypremium distribution (bottom panel) is large and risessharply under the unconstrained model as the T-bill ratemoves far away from its sample average. In contrast, whilethe posterior variance of the constrained equity premiumdistributions does rise when the T-bill rate takes on verysmall or very large values, it does so at a far slower rate.For example, for very high values of the T-bill rate, theposterior variance of the equity premium under theunconstrained model is close to four times higher thanunder the constrained models.

15 The plots for the log dividend–price ratio and default yield spreadare very similar and so are omitted.

16 Consistent with Fig. 6, the T-bill rate varies between x�2� SEðxÞand xþ2� SEðxÞ, with x and SEðxÞ denoting the full-sample average andstandard deviation of the T-bill rate, respectively.

k returns under economic constraints. Journal of Financial5i

Table 4Out-of-sample forecast performance (annual).

This table reports the out-of-sample R2 of unconstrained and constrained univariate prediction models for the annual excess return, rtþ1, measured relative to the prevailing mean model:

R2OoS ¼ 1�

∑t �1τ ¼ t �1ðrtþ1� r̂ tþ1jt Þ2

∑t �1τ ¼ t �1ðrtþ1�r tþ1jt Þ2

;

where r̂ tþ1jt is the mean of the predictive return distribution based on a regression of monthly excess returns on an intercept and a lagged predictor variable, xt: rtþ1 ¼ μþβxtþεtþ1. r tþ1jt is the forecast from the

prevailing mean model, which assumes that β¼ 0. The Campbell and Thompson (CT) truncation approach sets r̂ tþ1jt ¼maxð0; μ̂ tþ β̂ txt Þ, where μ̂t and β̂ t are the time t ordinary least squares estimates of μ and β.The equity premium (EP) constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and information set Dt , and the Sharpe ratio (SR [0,1]) constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; forτ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate using realized volatility. Panel A shows results for the full sample (1947–2010), while panels B and C report results for the subsamples 1947–1978 and1979–2010. Also reported are averages across all predictor variables. Bold figures highlight instances in which the constrained ROoS

2is higher than its unconstrained counterpart. We measure statistical significance

relative to the prevailing mean model using the Clark and West (2007) test statistic. nsignificance at 10% level; nnsignificance at 5% level; nnnsignificance at 1% level.

Panel A: full sample (1947–2010) Panel B: 1947–1978 Panel C: 1979–2010

Variable No CT EP SR [0,1] No CT EP SR [0,1] No CT EP SR [0,1]constraint truncation constraint constraint constraint truncation constraint constraint constraint truncation constraint constraint

Log dividend–price ratio 1.98%n 3.14%n 5.92%nnn 5.35%nnn 9.34%nn 9.34%nn 11.98%nnn 10.21%nnn �5.69% �3.33% �0.38% 0.30%Log dividend yield �8.54%n 3.30%nn 6.49%nn 4.29%nn �2.46%nn 13.01%nn 15.86%nnn 10.01%nnn �14.86% �6.81% �3.27% �1.66%Log earning–price ratio 1.66%n 5.55%nn 5.34%nn 4.84%nnn 10.99%nn 10.88%nn 8.87%nn 8.10%nnn �8.05% 0.00% 1.67% 1.45%Log smooth earning–price ratio �5.78%nn 2.84%nn 7.16%nnn 6.46%nnn 3.46%nn 7.89%nn 14.27%nnn 11.74%nnn �15.39% �2.41% �0.24% 0.98%Log dividend–payout ratio �4.00% �4.00% 2.01% 3.90%nnn �4.61% �4.61% 3.87% 7.59%nnn �3.37% �3.37% 0.08% 0.05%Book-to-market ratio �8.52% �4.19% 3.00%n 4.70%nn 2.46%n 2.25%n 6.27%n 8.57%nnn �19.96% �10.89% �0.41% 0.67%T-Bill rate �8.95% �2.67% 2.50%n 3.67%nn �4.81% �0.24% 6.18%nn 7.47%nnn �13.27% �5.19% �1.33% �0.28%Long-term yield �8.31% 1.13%n 2.27%n 4.12%nnn �3.86%n 7.28%nn 5.33%nn 7.89%nnn �12.94% �5.27% �0.91% 0.20%Long-term return �5.67%n �3.63%nn 3.24%nn 4.83%nnn 1.46%nn 5.44%nn 9.57%nn 8.64%nnn �13.08% �13.07% �3.34% 0.87%Term spread �5.39% �4.06% 2.40%n 3.80%nnn �8.25% �6.38% 5.47%nn 6.82%nnn �2.41% �1.64% �0.80% 0.66%Default yield spread �1.43% �1.43% 2.86%nn 3.33%nn �2.34% �2.34% 5.01%nn 5.94%nnn �0.49% �0.49% 0.62% 0.61%Default return spread �3.35% �3.00% 1.38% 3.42%nnn 4.67%nn 4.67%nn 4.42%n 6.49%nnn �11.70% �10.98% �1.78% 0.22%Stock variance �1.09% �1.09% 2.47%nn 3.31%nn �1.16% �1.16% 4.28%nn 5.67%nn �1.02% �1.02% 0.58% 0.85%Net equity expansion �16.23% �15.74% 0.07% 3.15%nnn �2.64% �1.64% 2.20% 6.63%nnn �30.37% �30.41% �2.15% �0.47%Inflation �6.29% �6.29% 0.80% 3.16%nnn �10.19% �10.19% 1.96% 6.09%nnn �2.24% �2.24% �0.40% 0.11%Percent equity issuing �4.40% �3.26% 1.66% 3.41%nnn 10.69%nn 8.94%nn 4.81%n 6.77%nnn �20.11% �15.97% �1.61% �0.08%

Average �5.27% �2.09% 3.10% 4.11% 0.17% 2.70% 6.90% 7.79% �10.93% �7.07% �0.85% 0.28%

Pleasecite

thisarticle

as:Petten

uzzo,D

.,etal.,Forecastin

gstock

returnsunder

econom

iccon

straints.Jou

rnalofFin

ancial

Econom

ics(2014),h

ttp://d

x.doi.org/10.1016/j.jfin

eco.2014.07.015i

D.Pettenuzzo

etal./

Journalof

FinancialEconom

ics](]]]])

]]]–]]]

18

Cum

ulat

ive

SS

E d

iffer

ence

Log dividend−price ratio

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005−0.01

0

0.01

0.02

Cum

ulat

ive

SS

E d

iffer

enceT−Bill rate

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005−0.01

0

0.01

0.02

Cum

ulat

ive

SS

E d

iffer

ence

Default yield spread

1940 1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 −0.01

0

0.01

0.02

Fig. 13. Forecast performance: cumulative sum of squared forecast error (SSE) differentials. This figure shows the sum of squared forecast errors of the prevailingmean model minus the sum of squared forecast errors of a forecast model with time-varying predictors. Each month we estimate the parameters of the forecastmodels recursively and generate one-step-ahead forecasts of excess returns which are in turn used to compute out-of-sample forecast errors. This procedure usesunivariate forecast models based on the log dividend–price ratio (top), the T-bill rate (middle), or the default yield spread (bottom) or a simple prevailing meanmodel which is our benchmark. We then plot the cumulative sum of squared forecast errors (SSEt) of the prevailing mean forecasts (SSEt

PM) relative to the univariate

forecasts, SSEPMt �SSEt . Values above zero indicate that a univariate forecast model generates better performance than the prevailing mean benchmark, whilenegative values suggest the opposite. The equity premium constrained model imposes that r̂ τþ1jt ¼

R ðμþβxτÞpðμ; βjDt Þ dμ dβ40; for τ¼ 1;…; t and informationset Dt , and the Sharpe ratio constraint imposes that 0r r̂ τþ1jt=σ̂ τþ1jtr1; for τ¼ 1;…; t, where σ̂ τþ1jt is the posterior volatility estimate from a stochasticvolatility model.

D. Pettenuzzo et al. / Journal of Financial Economics ] (]]]]) ]]]–]]] 19

3.3. Forecasts of equity premia