for the six months ended 30 june 2017 - santam the santam business portfolio 4 market context 8...

TRANSCRIPT

REVIEWED INTERIM REPORT

FOR THE SIX MONTHSENDED 30 JUNE 2017

4 The Santam business portfolio

4 Market context

8 Financial results

46 Capital management

50 Group strategy and priorities

55 Reviewed interim report for Santam Ltd and its subsidiaries for the

six months ended 30 June 2017

TABLE OF CONTENTS

P R E S E N T A T I O N T O A N A L Y S T S S A N T A M L T D A N D I T S S U B S I D I A R I E SReviewed interim report for the six months ended 30 June 2017

2

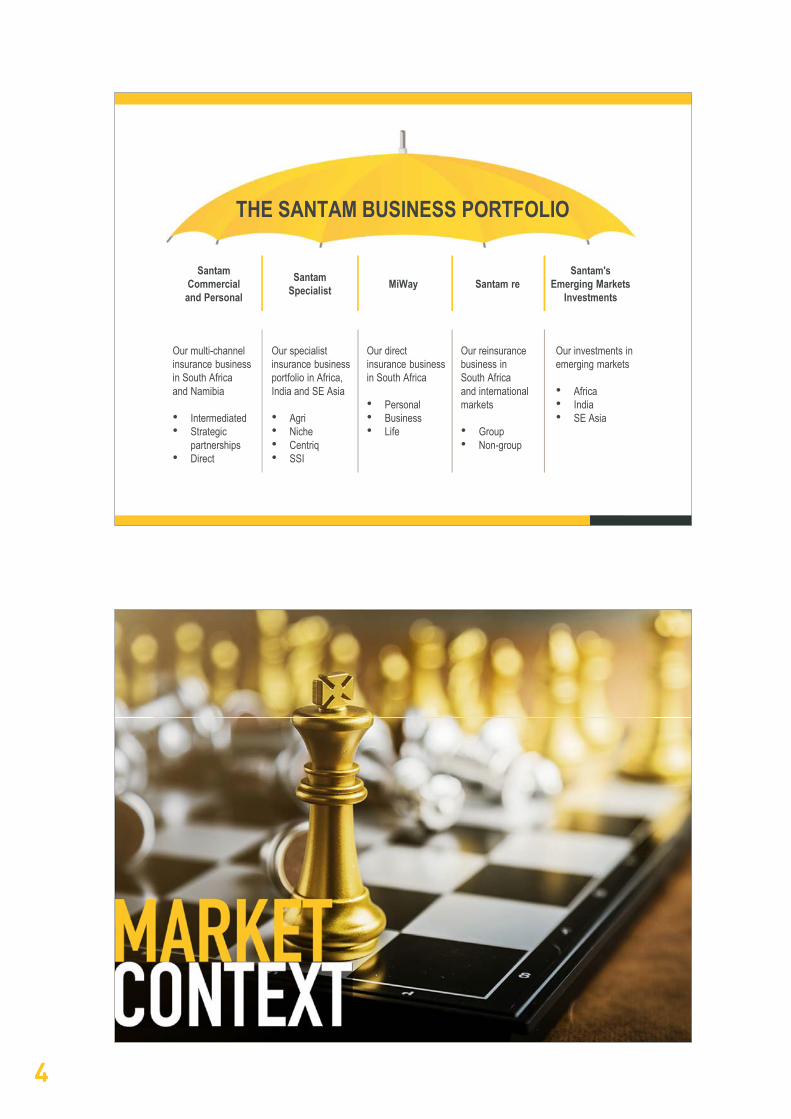

The Santam business portfolio

Market context

Financial results

Capital management

Group strategy and priorities

CONTENTS

CLICK TO EDIT MASTER

CLICK TO EDIT MASTER TITLE STYLE

PRESENTED BY LIZÉ LAMBRECHTS AND HENNIE NELFINANCIAL RESULTS FOR THE SIX MONTHS ENDED 30 JUNE 2017

3

4

Santam Commercial

and Personal

Santam Specialist MiWay

Santam Re

Our multi-channel insurance business in South Africa and Namibia

• Intermediated• Strategic

partnerships• Direct

Our specialist insurance business portfolio in Africa, India and SE Asia

• Agri• Niche• Centriq• SSI

Our direct insurance business in South Africa

• Personal • Business• Life

Our reinsurance business in South Africa and internationalmarkets

• Group• Non-group

Our investments in emerging markets

• Africa• India• SE Asia

Santam's Emerging Markets

InvestmentsSantam re

THE SANTAM BUSINESS PORTFOLIO

5

6

Source: Timetric

OPPORTUNITY FOR INSURANCE INVESTMENT:

EMERGING MARKETS2015-2020

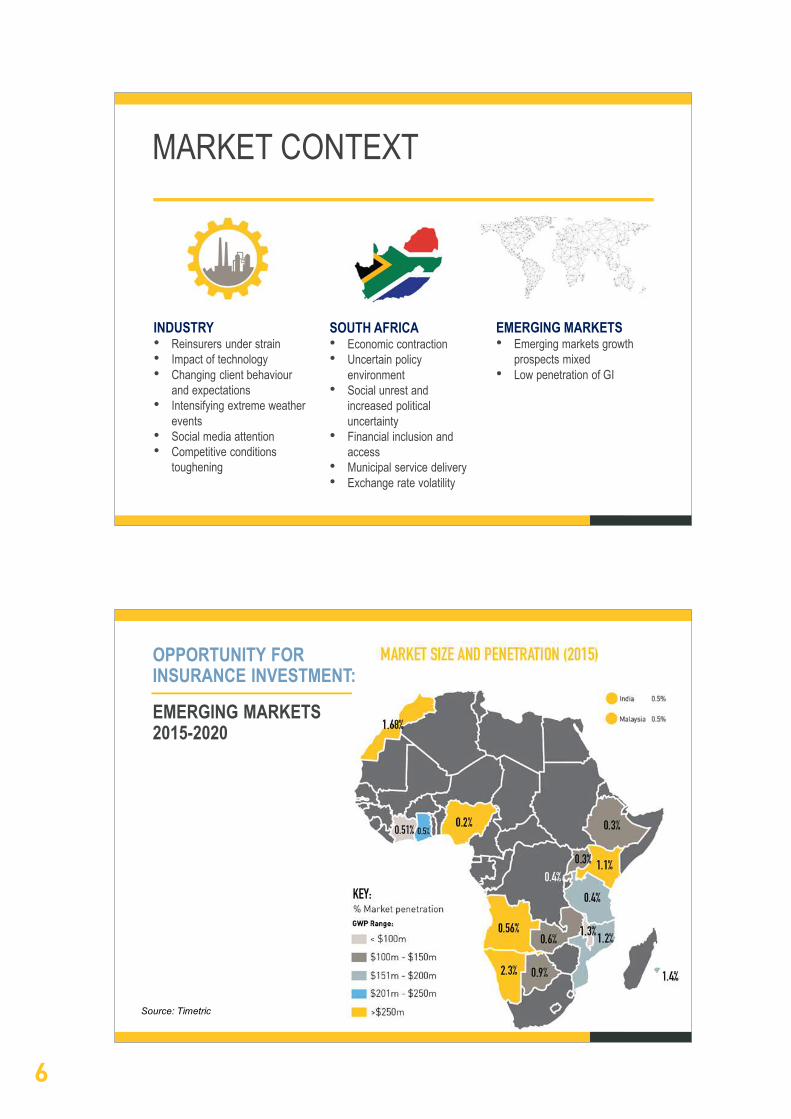

INDUSTRY• Reinsurers under strain• Impact of technology • Changing client behaviour

and expectations• Intensifying extreme weather

events• Social media attention• Competitive conditions

toughening

EMERGING MARKETS• Emerging markets growth

prospects mixed• Low penetration of GI

SOUTH AFRICA• Economic contraction• Uncertain policy

environment• Social unrest and

increased political uncertainty

• Financial inclusion and access

• Municipal service delivery• Exchange rate volatility

MARKET CONTEXT

7

8

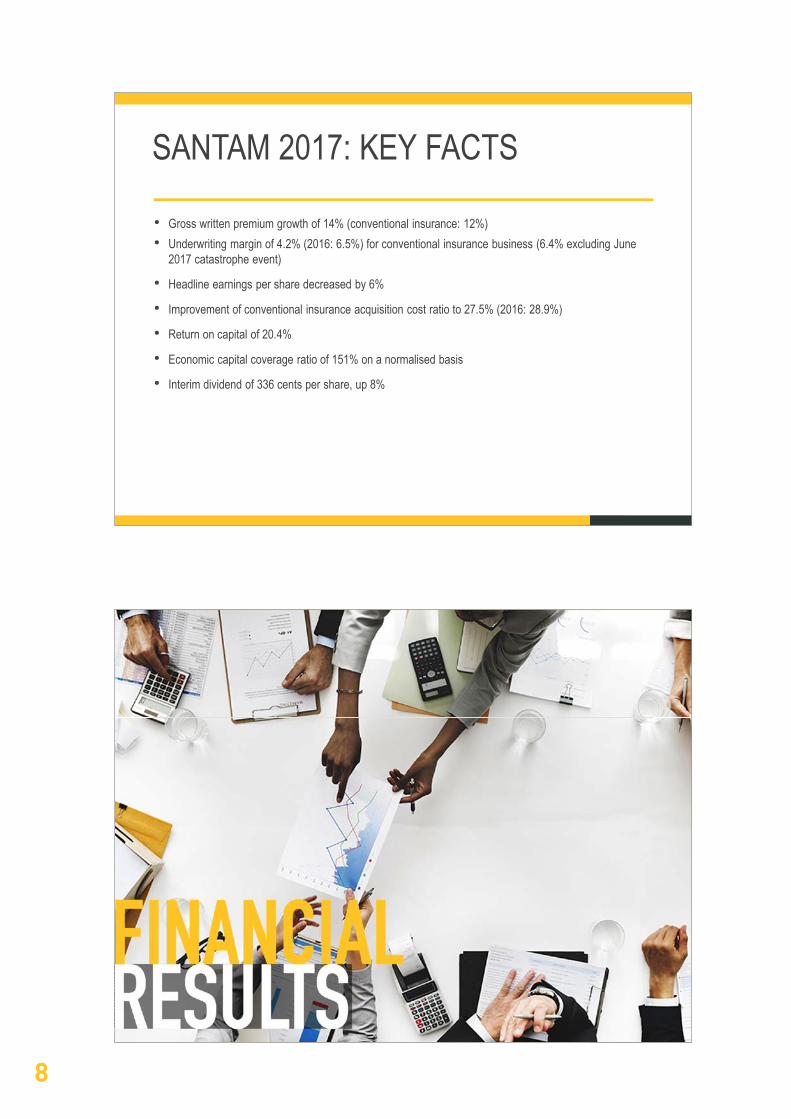

SANTAM 2017: KEY FACTS

• Gross written premium growth of 14% (conventional insurance: 12%)• Underwriting margin of 4.2% (2016: 6.5%) for conventional insurance business (6.4% excluding June

2017 catastrophe event)

• Headline earnings per share decreased by 6%

• Improvement of conventional insurance acquisition cost ratio to 27.5% (2016: 28.9%)

• Return on capital of 20.4%

• Economic capital coverage ratio of 151% on a normalised basis

• Interim dividend of 336 cents per share, up 8%

9

10

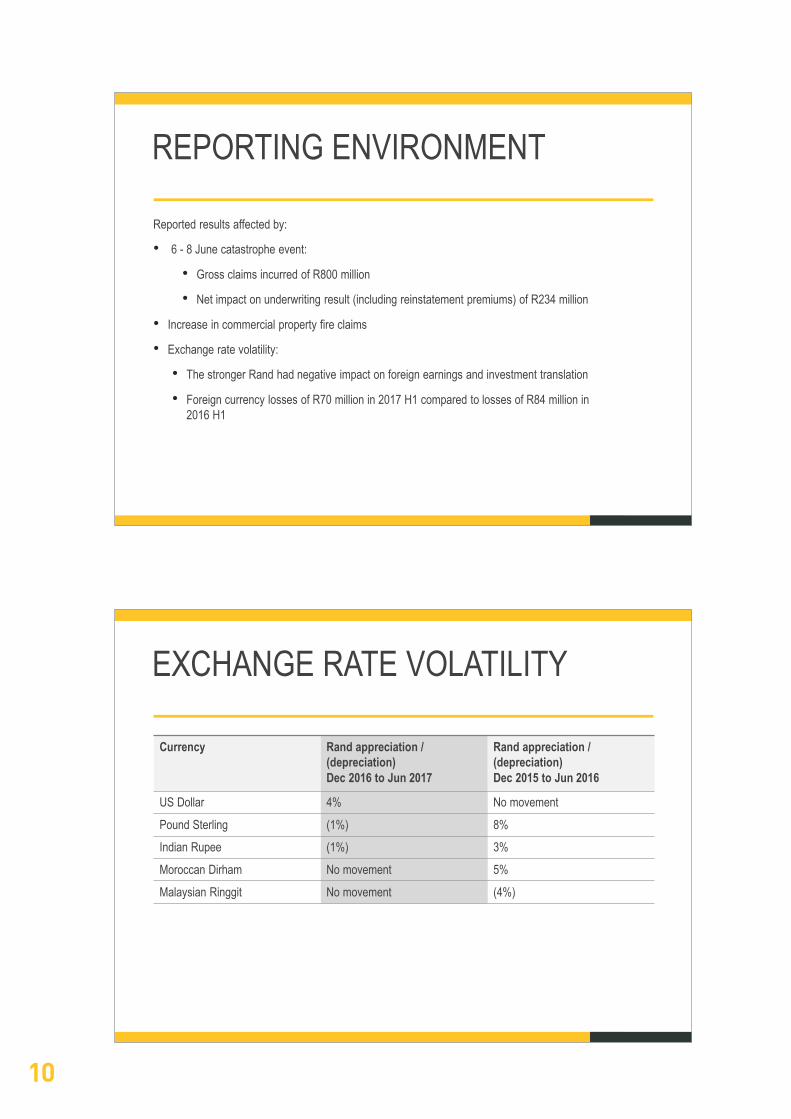

EXCHANGE RATE VOLATILITY

Currency Rand appreciation /(depreciation)Dec 2016 to Jun 2017

Rand appreciation / (depreciation) Dec 2015 to Jun 2016

US Dollar 4% No movement

Pound Sterling (1%) 8%

Indian Rupee (1%) 3%

Moroccan Dirham No movement 5%

Malaysian Ringgit No movement (4%)

REPORTING ENVIRONMENT

Reported results affected by:

• 6 - 8 June catastrophe event:

• Gross claims incurred of R800 million

• Net impact on underwriting result (including reinstatement premiums) of R234 million

• Increase in commercial property fire claims

• Exchange rate volatility:

• The stronger Rand had negative impact on foreign earnings and investment translation

• Foreign currency losses of R70 million in 2017 H1 compared to losses of R84 million in 2016 H1

11

12

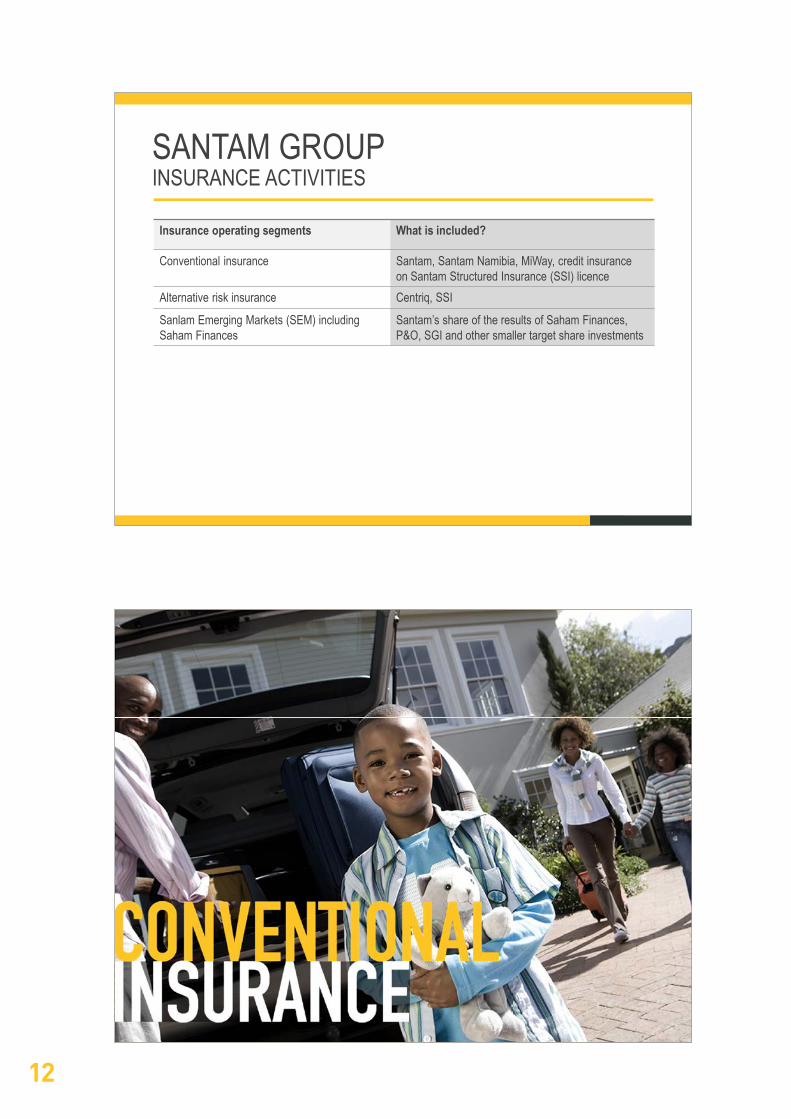

SANTAM GROUPINSURANCE ACTIVITIES

Insurance operating segments What is included?

Conventional insurance Santam, Santam Namibia, MiWay, credit insurance on Santam Structured Insurance (SSI) licence

Alternative risk insurance Centriq, SSI

Sanlam Emerging Markets (SEM) including Saham Finances

Santam’s share of the results of Saham Finances, P&O, SGI and other smaller target share investments

13

14

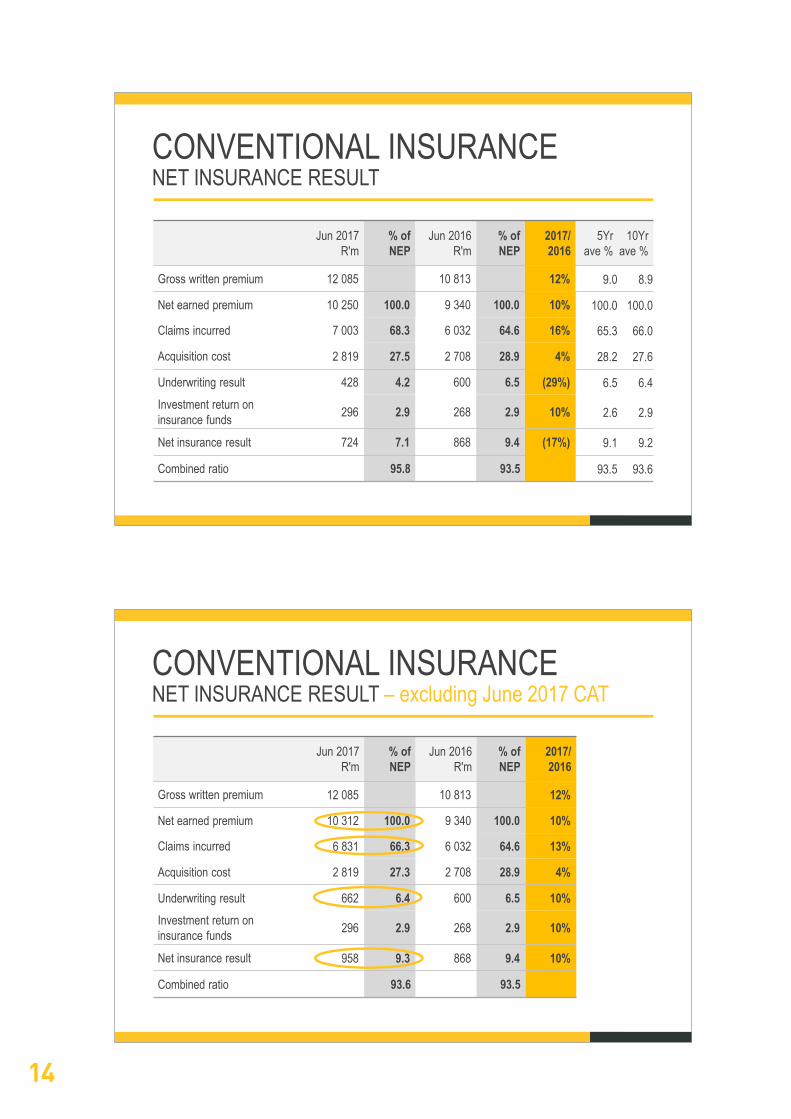

Jun 2017 R'm

% of NEP

Jun 2016 R'm

% of NEP

2017/2016

Gross written premium 12 085 10 813 12%

Net earned premium 10 312 100.0 9 340 100.0 10%

Claims incurred 6 831 66.3 6 032 64.6 13%

Acquisition cost 2 819 27.3 2 708 28.9 4%

Underwriting result 662 6.4 600 6.5 10%Investment return on insurance funds 296 2.9 268 2.9 10%

Net insurance result 958 9.3 868 9.4 10%

Combined ratio 93.6 93.5

CONVENTIONAL INSURANCE NET INSURANCE RESULT – excluding June 2017 CAT

Jun 2017 R'm

% of NEP

Jun 2016 R'm

% of NEP

2017/2016

5Yr ave %

10Yr ave %

Gross written premium 12 085 10 813 12% 9.0 8.9

Net earned premium 10 250 100.0 9 340 100.0 10% 100.0 100.0

Claims incurred 7 003 68.3 6 032 64.6 16% 65.3 66.0

Acquisition cost 2 819 27.5 2 708 28.9 4% 28.2 27.6

Underwriting result 428 4.2 600 6.5 (29%) 6.5 6.4Investment return on insurance funds 296 2.9 268 2.9 10% 2.6 2.9

Net insurance result 724 7.1 868 9.4 (17%) 9.1 9.2

Combined ratio 95.8 93.5 93.5 93.6

CONVENTIONAL INSURANCE NET INSURANCE RESULT

15

16

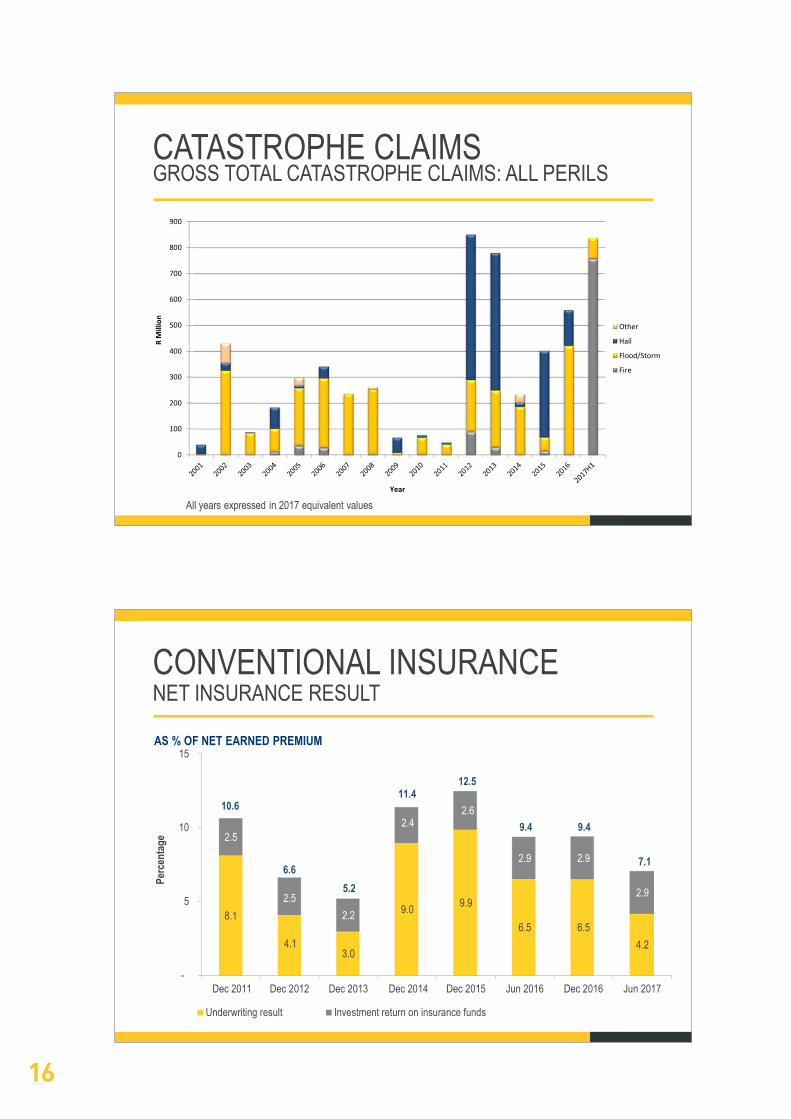

CONVENTIONAL INSURANCENET INSURANCE RESULT

AS % OF NET EARNED PREMIUM

8.1

4.13.0

9.0 9.9

6.5 6.54.2

2.5

2.52.2

2.42.6

2.9 2.9

2.9

-

5

10

15

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015 Jun 2016 Dec 2016 Jun 2017

Perc

enta

ge

Underwriting result Investment return on insurance funds

5.2

9.4

12.511.4

6.6

10.6

7.1

9.4

CATASTROPHE CLAIMSGROSS TOTAL CATASTROPHE CLAIMS: ALL PERILS

0

100

200

300

400

500

600

700

800

900

R M

illio

n

Year

Other

Hail

Flood/Storm

Fire

All years expressed in 2017 equivalent values

17

18

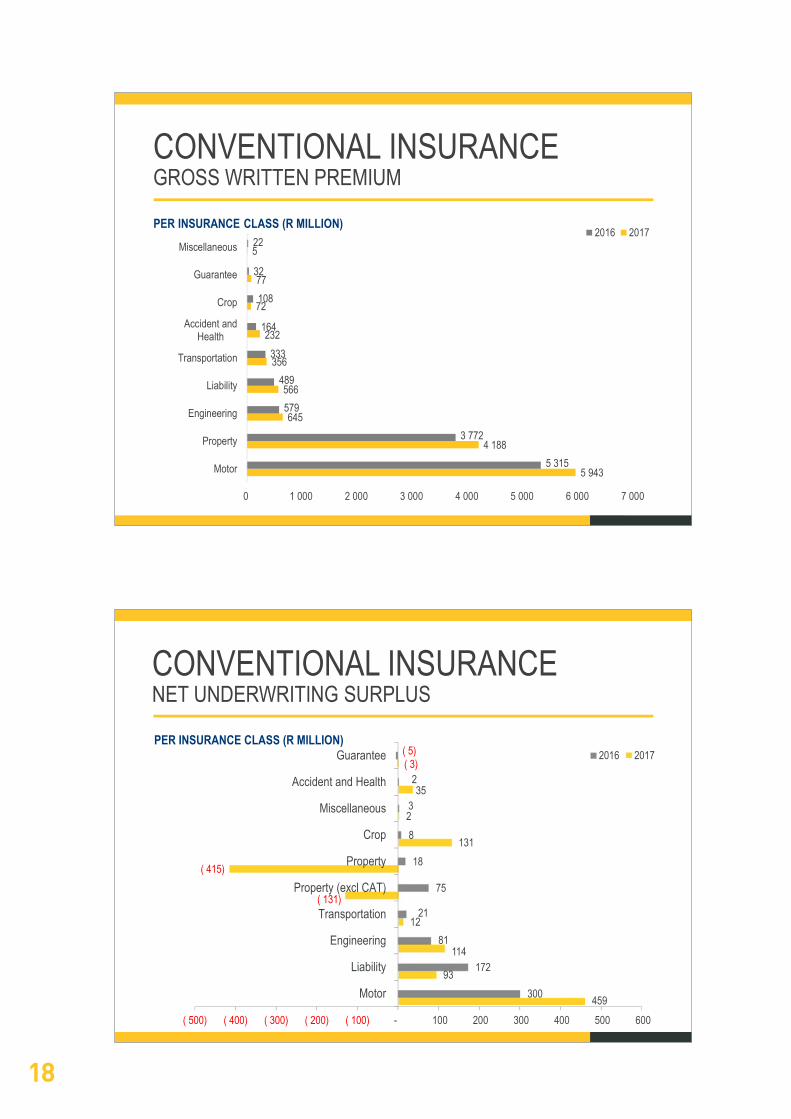

CONVENTIONAL INSURANCENET UNDERWRITING SURPLUS

PER INSURANCE CLASS (R MILLION)

459

93

114

12

( 131)

( 415)

131

2

35

( 3)

300

172

81

21

75

18

8

3

2

( 5)

( 500) ( 400) ( 300) ( 200) ( 100) - 100 200 300 400 500 600

Motor

Liability

Engineering

Transportation

Property (excl CAT)

Property

Crop

Miscellaneous

Accident and Health

Guarantee 2016 2017

PER INSURANCE CLASS (R MILLION)

CONVENTIONAL INSURANCEGROSS WRITTEN PREMIUM

5 943

4 188

645

566

356

232

72

77

5

5 315

3 772

579

489

333

164

108

32

22

0 1 000 2 000 3 000 4 000 5 000 6 000 7 000

Motor

Property

Engineering

Liability

Transportation

Accident andHealth

Crop

Guarantee

Miscellaneous2016 2017

19

20

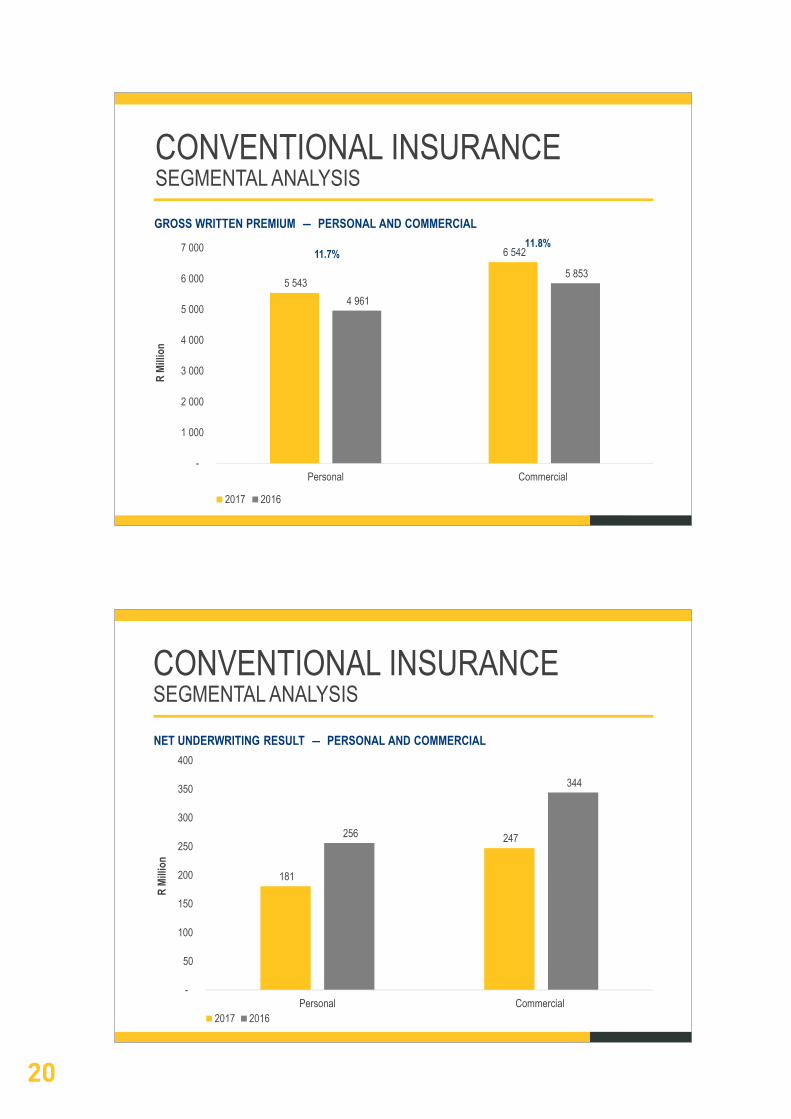

CONVENTIONAL INSURANCESEGMENTAL ANALYSIS

NET UNDERWRITING RESULT ― PERSONAL AND COMMERCIAL

181

247 256

344

-

50

100

150

200

250

300

350

400

Personal Commercial

R Mi

llion

2017 2016

CONVENTIONAL INSURANCESEGMENTAL ANALYSIS

GROSS WRITTEN PREMIUM ― PERSONAL AND COMMERCIAL

5 543

6 542

4 961

5 853

-

1 000

2 000

3 000

4 000

5 000

6 000

7 000

Personal Commercial

R Mi

llion

2017 2016

11.8%11.7%

21

22

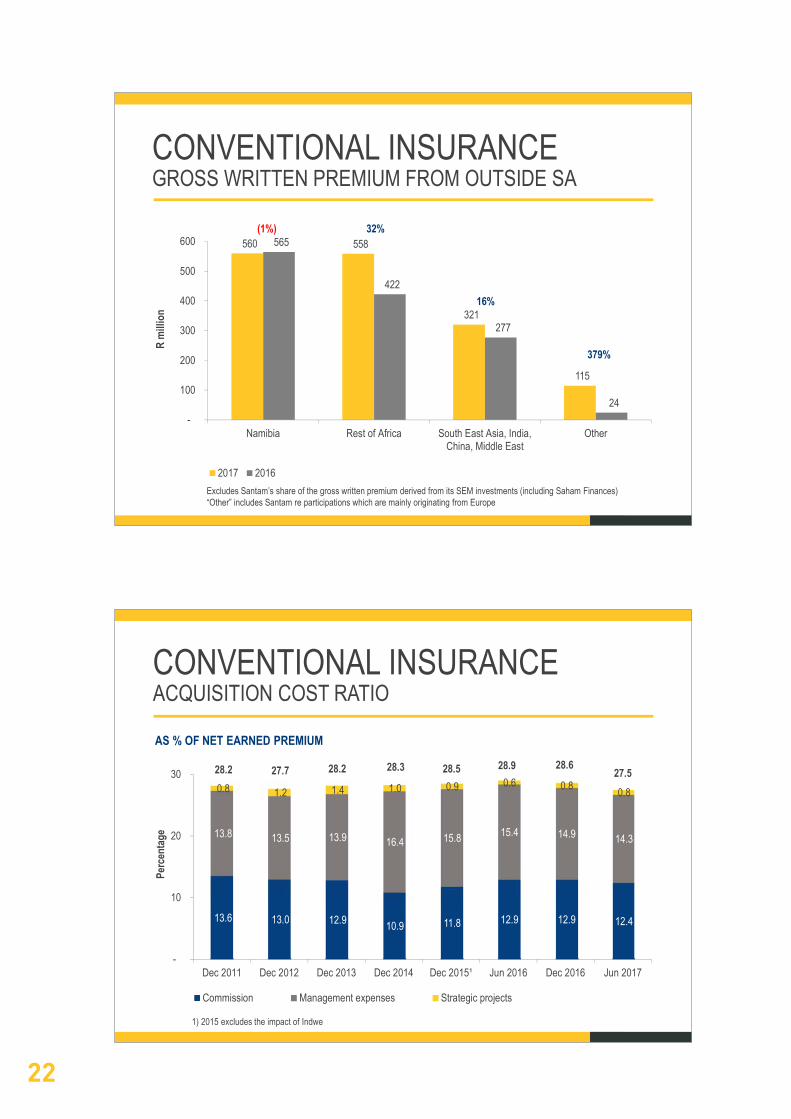

AS % OF NET EARNED PREMIUM

CONVENTIONAL INSURANCEACQUISITION COST RATIO

13.6 13.0 12.9 10.9 11.8 12.9 12.9 12.4

13.8 13.5 13.9 16.4 15.8 15.4 14.9 14.3

0.8 1.2 1.4 1.0 0.9 0.6 0.8 0.8

-

10

20

30

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015¹ Jun 2016 Dec 2016 Jun 2017

Perc

enta

ge

Commission Management expenses Strategic projects

28.2 27.7 28.2 28.3 28.5 27.528.628.9

1) 2015 excludes the impact of Indwe

CONVENTIONAL INSURANCEGROSS WRITTEN PREMIUM FROM OUTSIDE SA

Excludes Santam’s share of the gross written premium derived from its SEM investments (including Saham Finances)“Other” includes Santam re participations which are mainly originating from Europe

560 558

321

115

565

422

277

24 -

100

200

300

400

500

600

Namibia Rest of Africa South East Asia, India,China, Middle East

Other

R m

illion

2017 2016

(1%) 32%

16%

379%

23

24

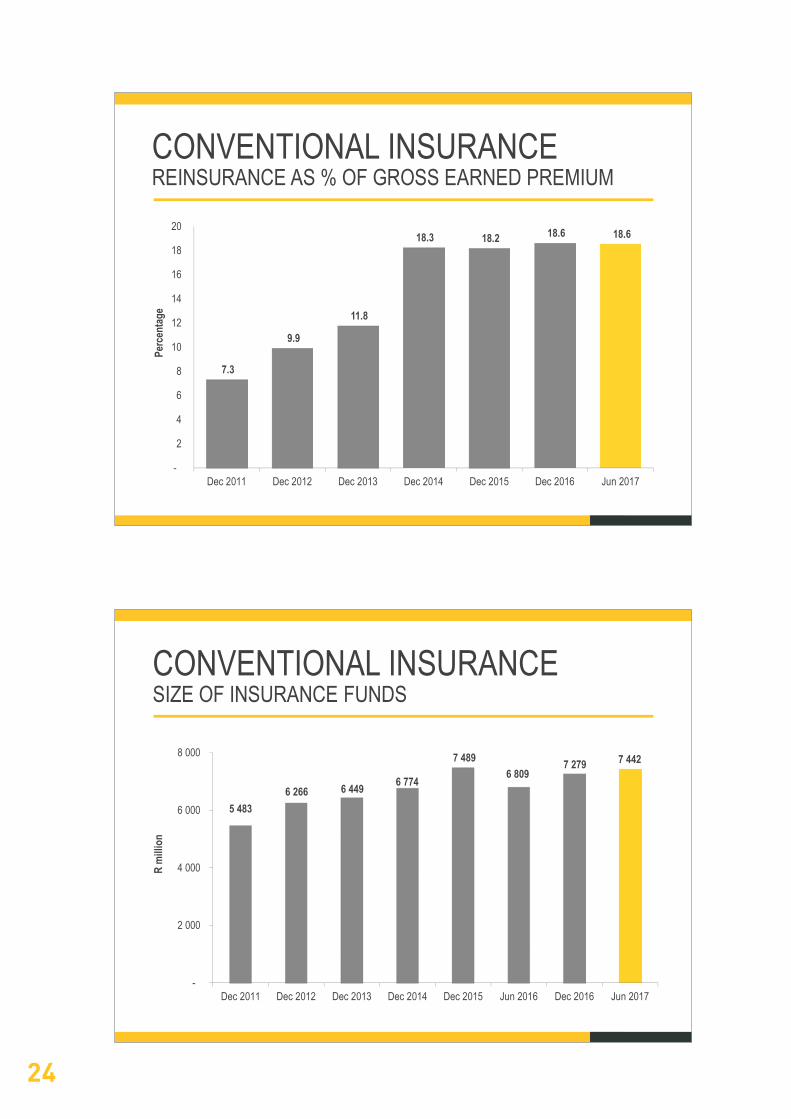

CONVENTIONAL INSURANCESIZE OF INSURANCE FUNDS

5 483 6 266 6 449 6 774

7 489 6 809

7 279 7 442

-

2 000

4 000

6 000

8 000

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015 Jun 2016 Dec 2016 Jun 2017

R m

illion

CONVENTIONAL INSURANCEREINSURANCE AS % OF GROSS EARNED PREMIUM

7.3

9.9

11.8

18.3 18.2 18.6 18.6

-

2

4

6

8

10

12

14

16

18

20

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015 Dec 2016 Jun 2017

Perc

enta

ge

25

26

CONVENTIONAL INSURANCEASSETS BACKING NET INSURANCE FUNDS

5 943 5 959 5 540

1 111 996 940

388 324 328

-

2 000

4 000

6 000

8 000

Jun 2017 Dec 2016 Jun 2016

R m

illion

Rand US Dollar Other currencies (mainly Namibian dollar)

7 442

6 8097 279

CURRENCY MIX

CONVENTIONAL INSURANCEINSURANCE FUNDS AS % OF GROSS EARNED PREMIUM

35.9 37.135.4

33.5 34.3

30.2 30.9 29.9

-

10

20

30

40

Dec 2011 Dec 2012 Dec 2013 Dec 2014 Dec 2015 Jun 2016 Dec 2016 Jun 2017

Perc

enta

ge

27

28

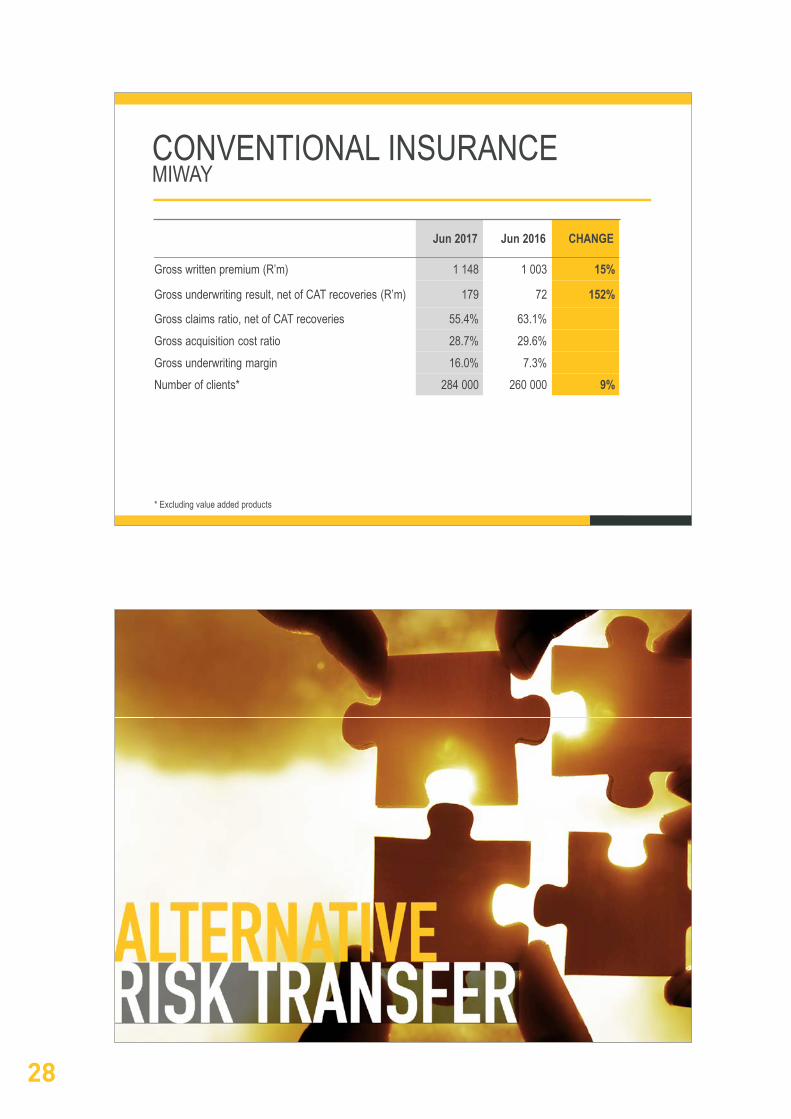

Jun 2017 Jun 2016 CHANGE

Gross written premium (R’m) 1 148 1 003 15%

Gross underwriting result, net of CAT recoveries (R’m) 179 72 152%

Gross claims ratio, net of CAT recoveries 55.4% 63.1%Gross acquisition cost ratio 28.7% 29.6%Gross underwriting margin 16.0% 7.3%Number of clients* 284 000 260 000 9%

CONVENTIONAL INSURANCEMIWAY

* Excluding value added products

29

30

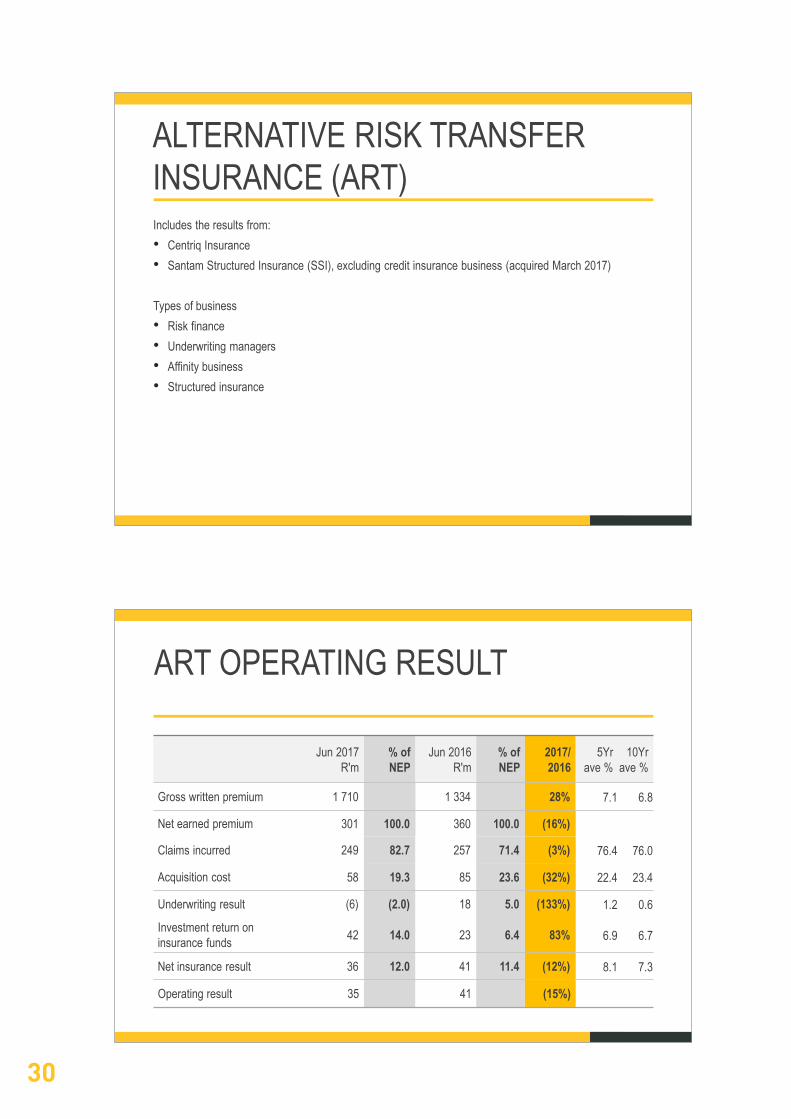

ART OPERATING RESULT

Jun 2017 R'm

% of NEP

Jun 2016 R'm

% of NEP

2017/2016

5Yr ave %

10Yr ave %

Gross written premium 1 710 1 334 28% 7.1 6.8

Net earned premium 301 100.0 360 100.0 (16%)

Claims incurred 249 82.7 257 71.4 (3%) 76.4 76.0

Acquisition cost 58 19.3 85 23.6 (32%) 22.4 23.4

Underwriting result (6) (2.0) 18 5.0 (133%) 1.2 0.6

Investment return on insurance funds 42 14.0 23 6.4 83% 6.9 6.7

Net insurance result 36 12.0 41 11.4 (12%) 8.1 7.3

Operating result 35 41 (15%)

ALTERNATIVE RISK TRANSFER INSURANCE (ART)Includes the results from:• Centriq Insurance• Santam Structured Insurance (SSI), excluding credit insurance business (acquired March 2017)

Types of business• Risk finance• Underwriting managers• Affinity business• Structured insurance

31

32

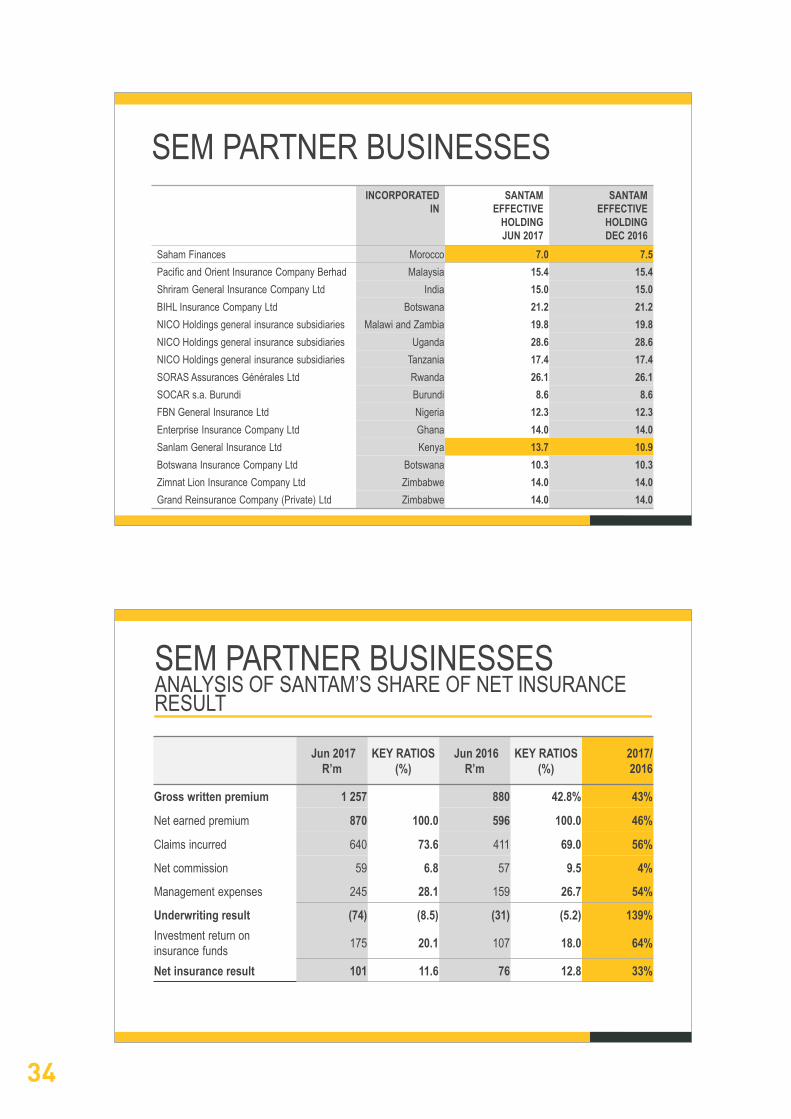

SEM PARTNER BUSINESSES

• Saham Finances • Effective interest of 7% held through SAN JV• Operates in 26 countries in Africa and the Middle East• Main insurance business:

• Morocco• Lebanon• Ivory Coast• Angola• Nigeria – Continental Re

• SEM Participation investments• SGI (India)• P&O (Malaysia)• 12 investments in African partner businesses

33

34

SEM PARTNER BUSINESSESANALYSIS OF SANTAM’S SHARE OF NET INSURANCE RESULT

Jun 2017R’m

KEY RATIOS (%)

Jun 2016R’m

KEY RATIOS(%)

2017/2016

Gross written premium 1 257 880 42.8% 43%

Net earned premium 870 100.0 596 100.0 46%

Claims incurred 640 73.6 411 69.0 56%

Net commission 59 6.8 57 9.5 4%

Management expenses 245 28.1 159 26.7 54%

Underwriting result (74) (8.5) (31) (5.2) 139%Investment return on insurance funds 175 20.1 107 18.0 64%

Net insurance result 101 11.6 76 12.8 33%

INCORPORATED IN

SANTAMEFFECTIVE

HOLDING JUN 2017

SANTAM EFFECTIVE

HOLDING DEC 2016

Saham Finances Morocco 7.0 7.5Pacific and Orient Insurance Company Berhad Malaysia 15.4 15.4 Shriram General Insurance Company Ltd India 15.0 15.0 BIHL Insurance Company Ltd Botswana 21.2 21.2 NICO Holdings general insurance subsidiaries Malawi and Zambia 19.8 19.8 NICO Holdings general insurance subsidiaries Uganda 28.6 28.6 NICO Holdings general insurance subsidiaries Tanzania 17.4 17.4 SORAS Assurances Générales Ltd Rwanda 26.1 26.1 SOCAR s.a. Burundi Burundi 8.6 8.6 FBN General Insurance Ltd Nigeria 12.3 12.3Enterprise Insurance Company Ltd Ghana 14.0 14.0 Sanlam General Insurance Ltd Kenya 13.7 10.9Botswana Insurance Company Ltd Botswana 10.3 10.3Zimnat Lion Insurance Company Ltd Zimbabwe 14.0 14.0Grand Reinsurance Company (Private) Ltd Zimbabwe 14.0 14.0

SEM PARTNER BUSINESSES

35

36

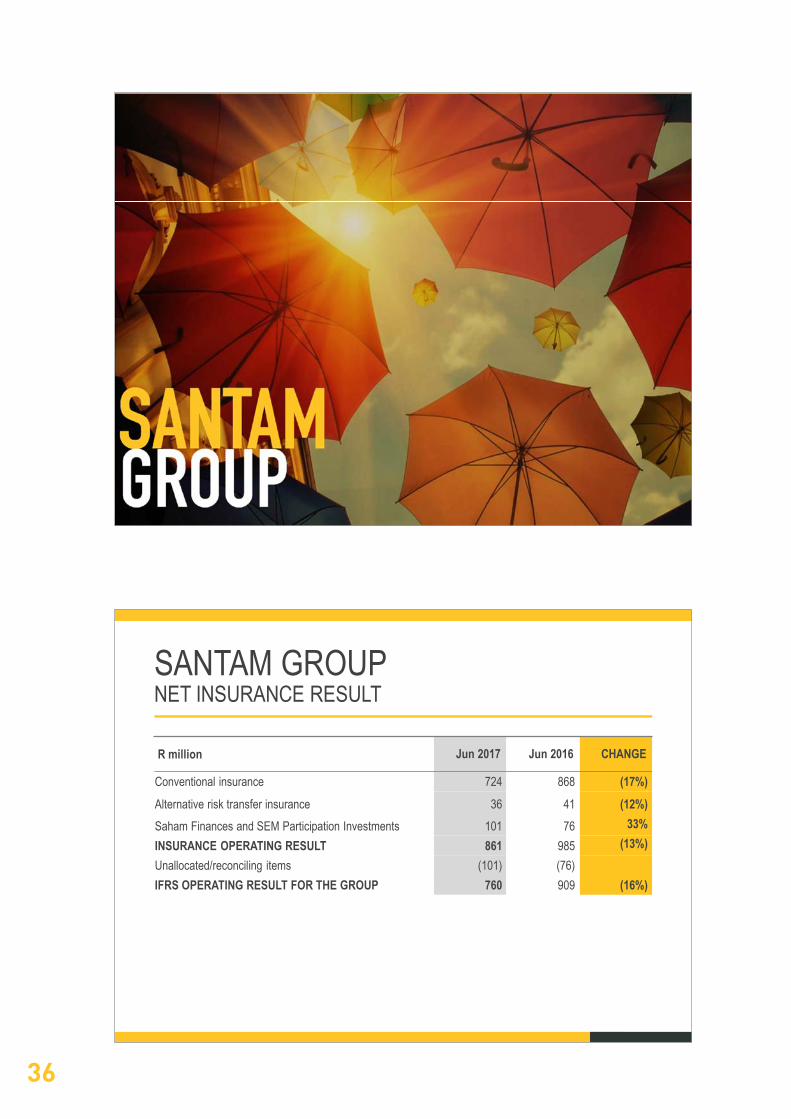

R million Jun 2017 Jun 2016 CHANGE

Conventional insurance 724 868 (17%)Alternative risk transfer insurance 36 41 (12%)Saham Finances and SEM Participation Investments 101 76 33%INSURANCE OPERATING RESULT 861 985 (13%)Unallocated/reconciling items (101) (76)IFRS OPERATING RESULT FOR THE GROUP 760 909 (16%)

SANTAM GROUPNET INSURANCE RESULT

37

38

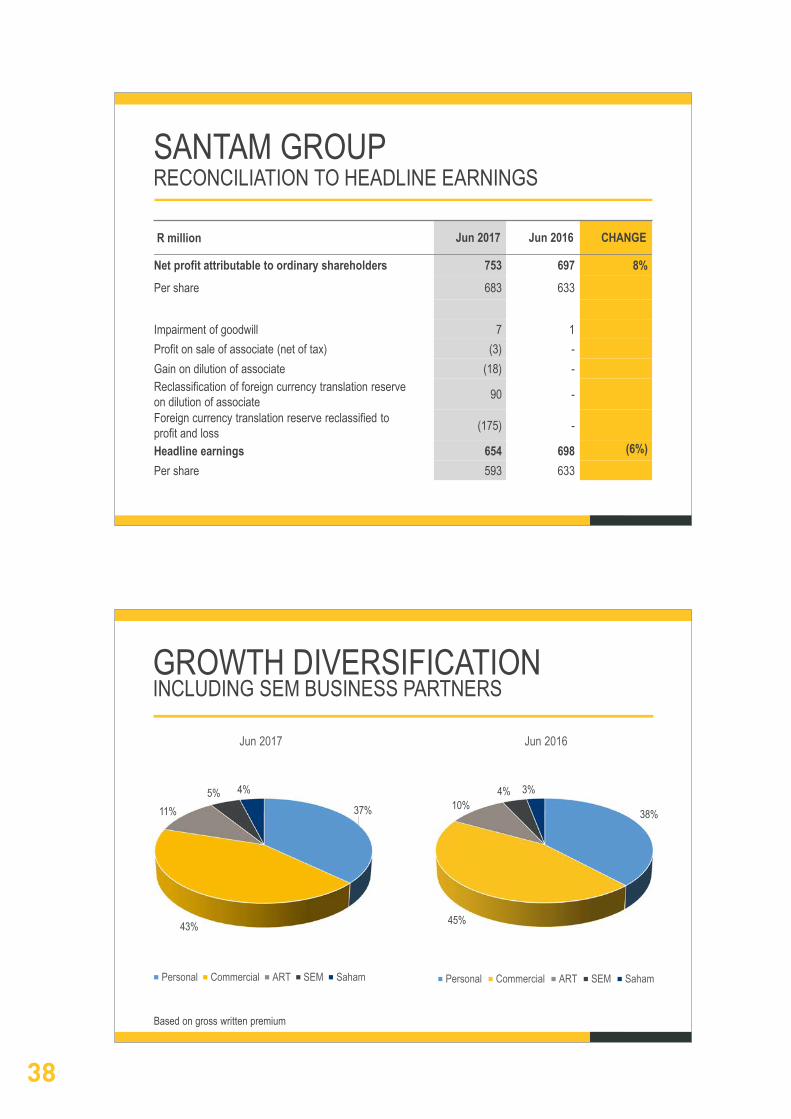

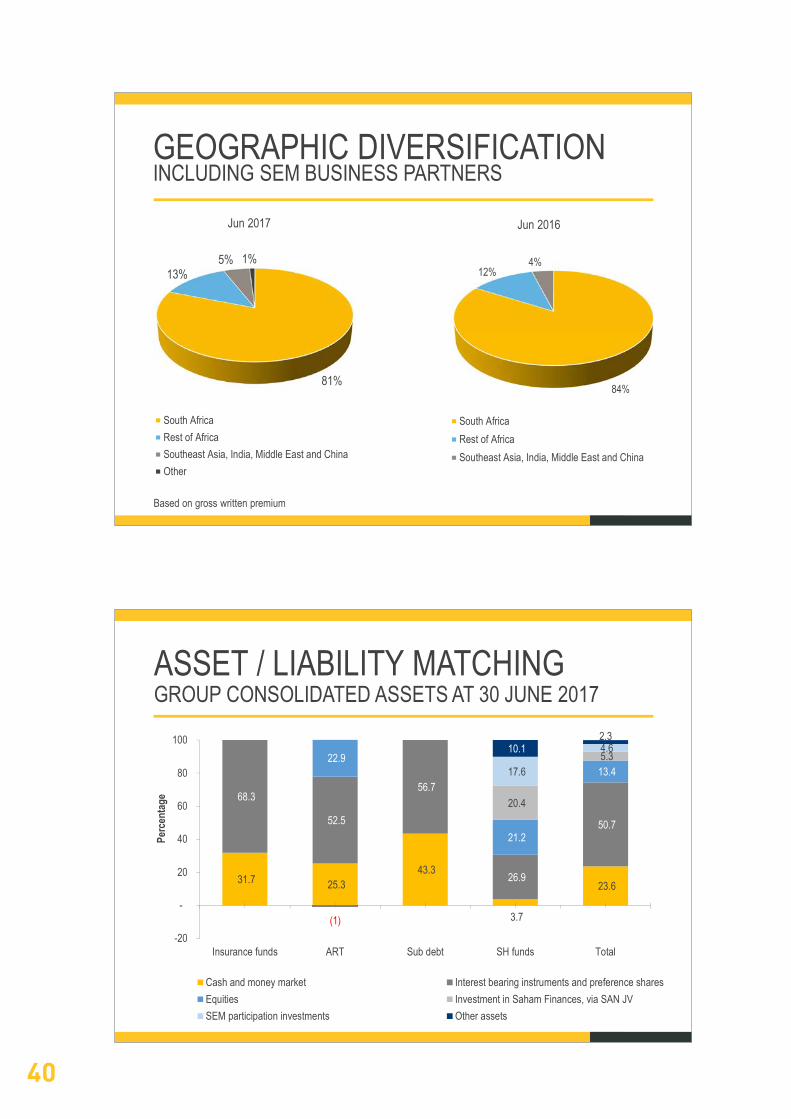

GROWTH DIVERSIFICATIONINCLUDING SEM BUSINESS PARTNERS

37%

43%

11%5% 4%

Jun 2017

Personal Commercial ART SEM Saham

38%

45%

10%4% 3%

Jun 2016

Personal Commercial ART SEM Saham

Based on gross written premium

R million Jun 2017 Jun 2016 CHANGE

Net profit attributable to ordinary shareholders 753 697 8%Per share 683 633

Impairment of goodwill 7 1Profit on sale of associate (net of tax) (3) -Gain on dilution of associate (18) -Reclassification of foreign currency translation reserveon dilution of associate 90 -

Foreign currency translation reserve reclassified toprofit and loss (175) -

Headline earnings 654 698 (6%)Per share 593 633

SANTAM GROUPRECONCILIATION TO HEADLINE EARNINGS

39

40

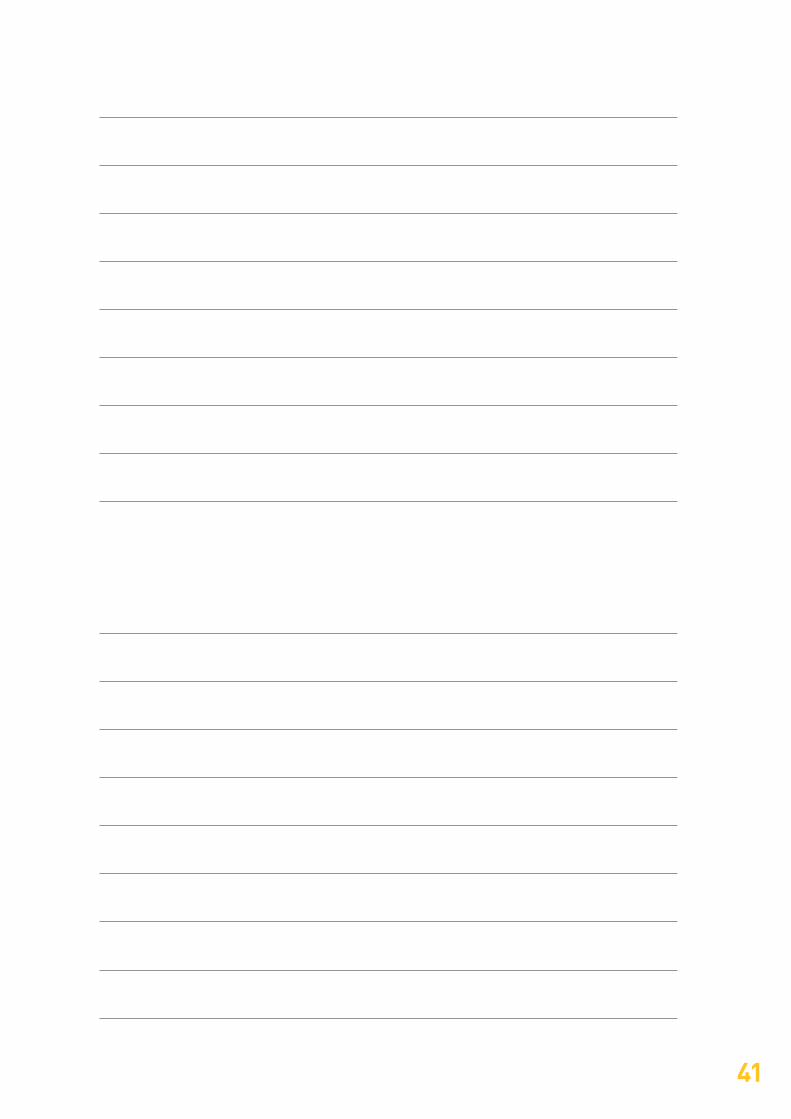

ASSET / LIABILITY MATCHINGGROUP CONSOLIDATED ASSETS AT 30 JUNE 2017

31.7 25.3 43.3

3.7

23.6

68.3

52.5

56.7

26.9

50.7

22.9

21.2

13.4

20.4

5.3 17.6

4.6

(1)

10.1 2.3

-20

-

20

40

60

80

100

Insurance funds ART Sub debt SH funds Total

Perc

enta

ge

Cash and money market Interest bearing instruments and preference sharesEquities Investment in Saham Finances, via SAN JVSEM participation investments Other assets

GEOGRAPHIC DIVERSIFICATIONINCLUDING SEM BUSINESS PARTNERS

81%

13%5% 1%

Jun 2017

South AfricaRest of AfricaSoutheast Asia, India, Middle East and ChinaOther

84%

12%4%

Jun 2016

South AfricaRest of AfricaSoutheast Asia, India, Middle East and China

Based on gross written premium

41

42

SHAREHOLDER FUNDSCURRENCY MIX1

39.1 41.8 50.9

9.0 12.9 8.4 20.4

17.5 17.6 6.4 6.4 6.5 17.6 16.4 12.0 7.6 5.0 4.6

-

20

40

60

80

100

Jun 2017 Dec 2016 Jun 2016

Perc

enta

ge

Rand US Dollar²Dirham (investment in Saham Finances, via SAN JV) Pound SterlingSEM (various currencies) Other currencies (mainly Namibian dollar)

1) Includes foreign denominated assets, as well as assets with foreign currency exposure2) Includes cash designated for the Saham Finances transaction (2017: Nil; 2016: USD 10 million)

SHAREHOLDER FUNDSASSET MIX

3.7 5.5 5.9

24.1 25.8 32.1

24.4 20.5 22.8

20.4 19.4 17.6

17.6 16.4 12

9.8 12.4 9.6

-

20

40

60

80

100

Jun 2017 Dec 2016 Jun 2016

Perc

enta

ge

Cash and money marketInterest-bearing instruments and preference sharesEquitiesInvestment in Saham Finances¹SEM participation investmentsOther assets

1) 2016 includes USD 10 million cash designated for the further subscription of shares in Saham Finances, via SAN JV

43

44

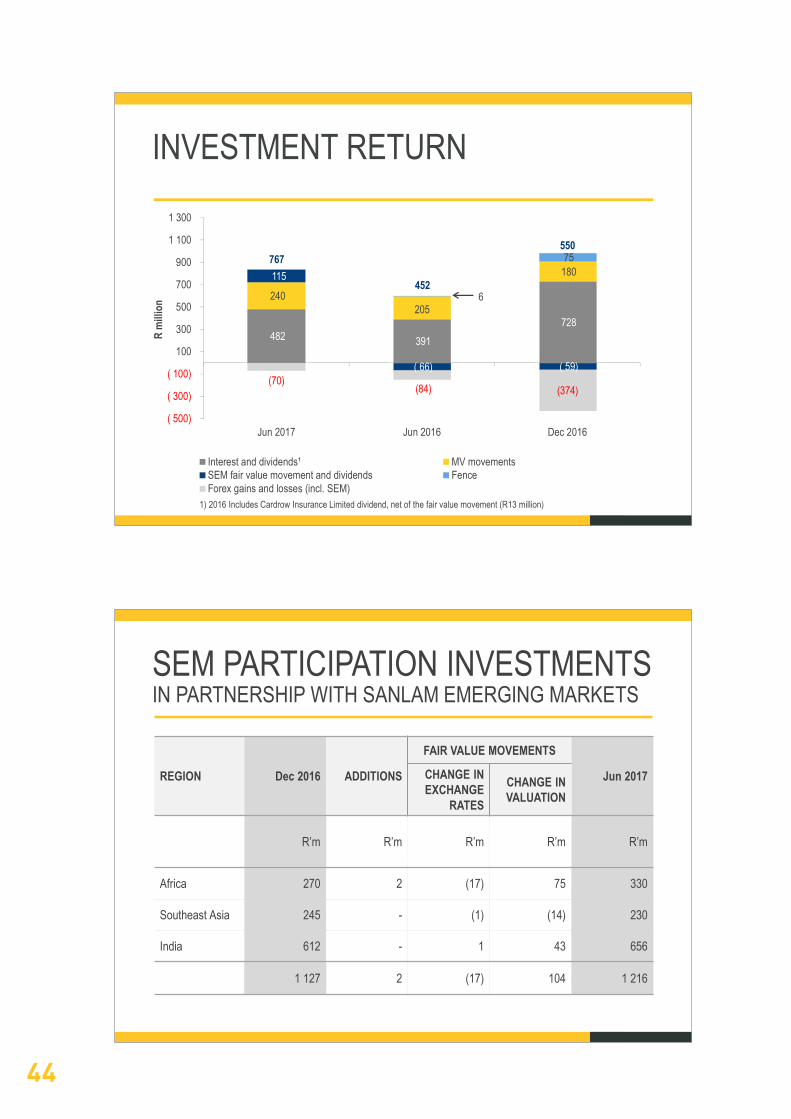

REGION Dec 2016 ADDITIONS

FAIR VALUE MOVEMENTS

Jun 2017CHANGE IN EXCHANGE

RATES

CHANGE IN VALUATION

R’m R’m R’m R’m R’m

Africa 270 2 (17) 75 330

Southeast Asia 245 - (1) (14) 230

India 612 - 1 43 656

1 127 2 (17) 104 1 216

SEM PARTICIPATION INVESTMENTSIN PARTNERSHIP WITH SANLAM EMERGING MARKETS

INVESTMENT RETURN

1) 2016 Includes Cardrow Insurance Limited dividend, net of the fair value movement (R13 million)

482 391 728

240 205

180 115

( 66) ( 59)

6

75

(70)(84) (374)

( 500)

( 300)

( 100)

100

300

500

700

900

1 100

1 300

Jun 2017 Jun 2016 Dec 2016

R m

illion

Interest and dividends¹ MV movementsSEM fair value movement and dividends FenceForex gains and losses (incl. SEM)

452

767550

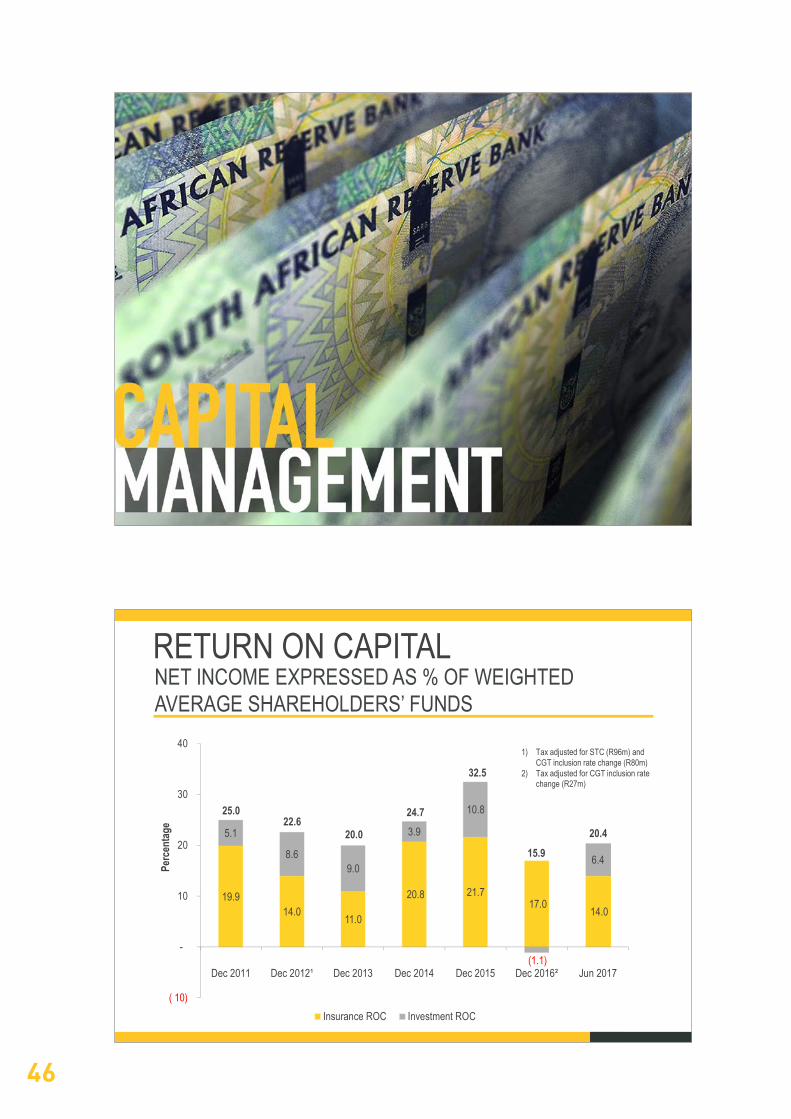

45

46

19.9 14.0 11.0

20.8 21.717.0 14.0

5.1

8.6 9.0

3.9

10.8

(1.1)

6.4

( 10)

-

10

20

30

40

Dec 2011 Dec 2012¹ Dec 2013 Dec 2014 Dec 2015 Dec 2016² Jun 2017

Perc

enta

ge

Insurance ROC Investment ROC

20.0

24.7

32.5

22.625.0

15.920.4

RETURN ON CAPITAL

1) Tax adjusted for STC (R96m) and CGT inclusion rate change (R80m)

2) Tax adjusted for CGT inclusion rate change (R27m)

NET INCOME EXPRESSED AS % OF WEIGHTED AVERAGE SHAREHOLDERS’ FUNDS

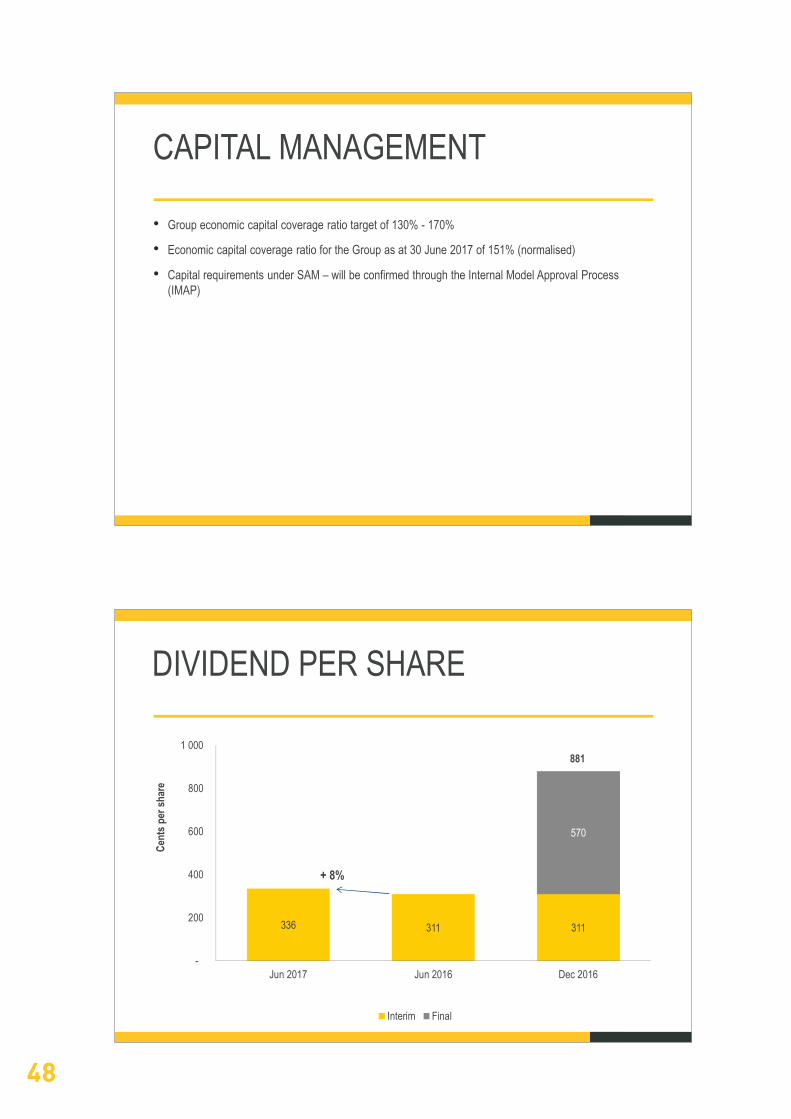

47

48

DIVIDEND PER SHARE

336 311 311

570

-

200

400

600

800

1 000

Jun 2017 Jun 2016 Dec 2016

Cent

s per

shar

e

Interim Final

+ 8%

881

CAPITAL MANAGEMENT

• Group economic capital coverage ratio target of 130% - 170%

• Economic capital coverage ratio for the Group as at 30 June 2017 of 151% (normalised)

• Capital requirements under SAM – will be confirmed through the Internal Model Approval Process (IMAP)

49

50

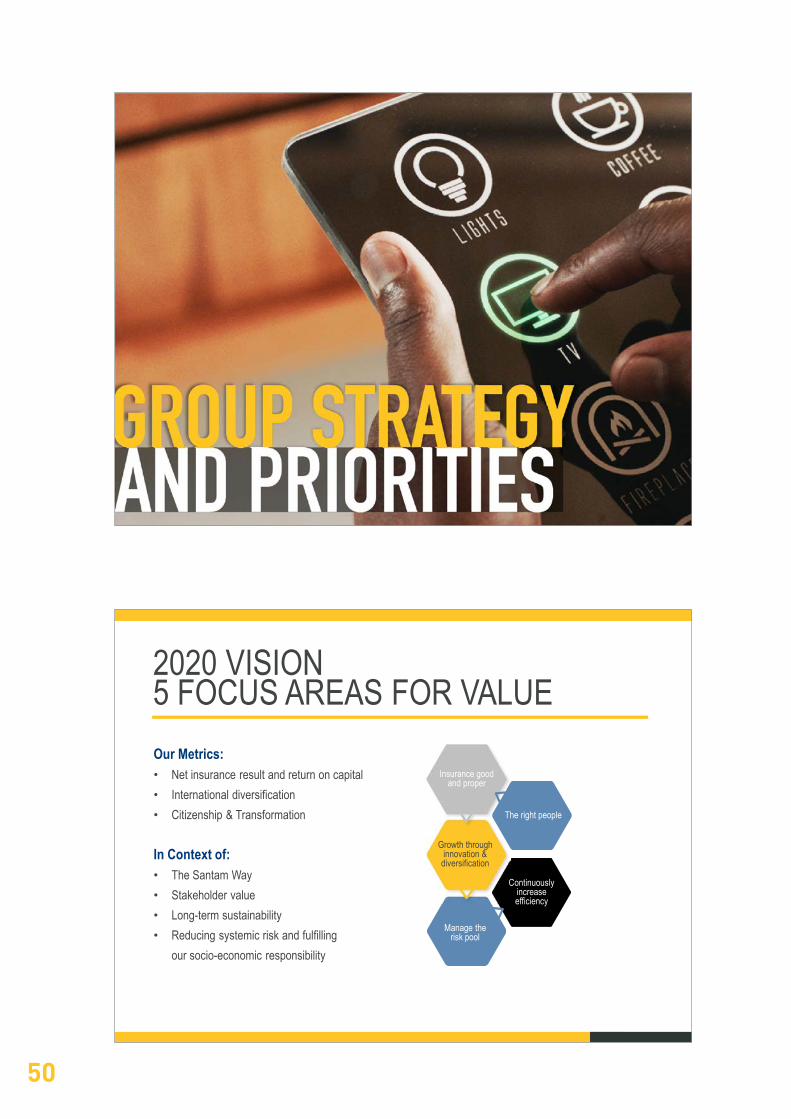

Our Metrics:• Net insurance result and return on capital• International diversification • Citizenship & Transformation

In Context of:• The Santam Way• Stakeholder value• Long-term sustainability• Reducing systemic risk and fulfilling

our socio-economic responsibility

2020 VISION5 FOCUS AREAS FOR VALUE

Growth through innovation &

diversification

Manage therisk pool

Continuouslyincreaseefficiency

The right people

Insurance good and proper

51

52

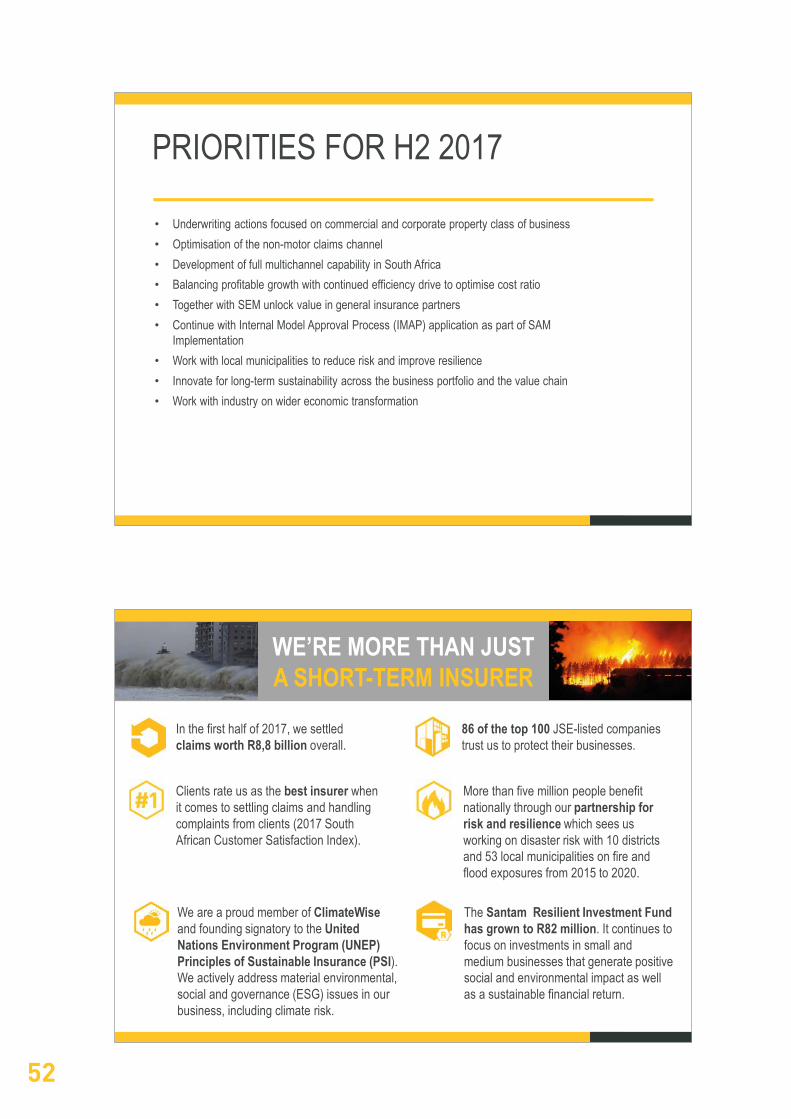

WE’RE MORE THAN JUST A SHORT-TERM INSURER

The Santam Resilient Investment Fund has grown to R82 million. It continues to focus on investments in small and medium businesses that generate positive social and environmental impact as well as a sustainable financial return.

We are a proud member of ClimateWiseand founding signatory to the United Nations Environment Program (UNEP) Principles of Sustainable Insurance (PSI). We actively address material environmental, social and governance (ESG) issues in our business, including climate risk.

Clients rate us as the best insurer when it comes to settling claims and handling complaints from clients (2017 South African Customer Satisfaction Index).

More than five million people benefit nationally through our partnership for risk and resilience which sees us working on disaster risk with 10 districts and 53 local municipalities on fire and flood exposures from 2015 to 2020.

In the first half of 2017, we settled claims worth R8,8 billion overall.

86 of the top 100 JSE-listed companies trust us to protect their businesses.

PRIORITIES FOR H2 2017

• Underwriting actions focused on commercial and corporate property class of business • Optimisation of the non-motor claims channel• Development of full multichannel capability in South Africa• Balancing profitable growth with continued efficiency drive to optimise cost ratio• Together with SEM unlock value in general insurance partners• Continue with Internal Model Approval Process (IMAP) application as part of SAM

Implementation• Work with local municipalities to reduce risk and improve resilience• Innovate for long-term sustainability across the business portfolio and the value chain• Work with industry on wider economic transformation

53

54

55

REVIEWED INTERIM REPORTFOR THE SIX MONTHSENDED 30 JUNE 2017

57 SALIENT FEATURES

58 FINANCIAL REVIEW

62 INDEPENDENT AUDITOR’S REVIEW REPORT

63 CONSOLIDATED STATEMENT OF FINANCIAL POSITION

64 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

65 CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

66 CONSOLIDATED STATEMENT OF CASH FLOWS

67 NOTES TO THE INTERIM FINANCIAL STATEMENTS

TABLE OF CONTENTS

57

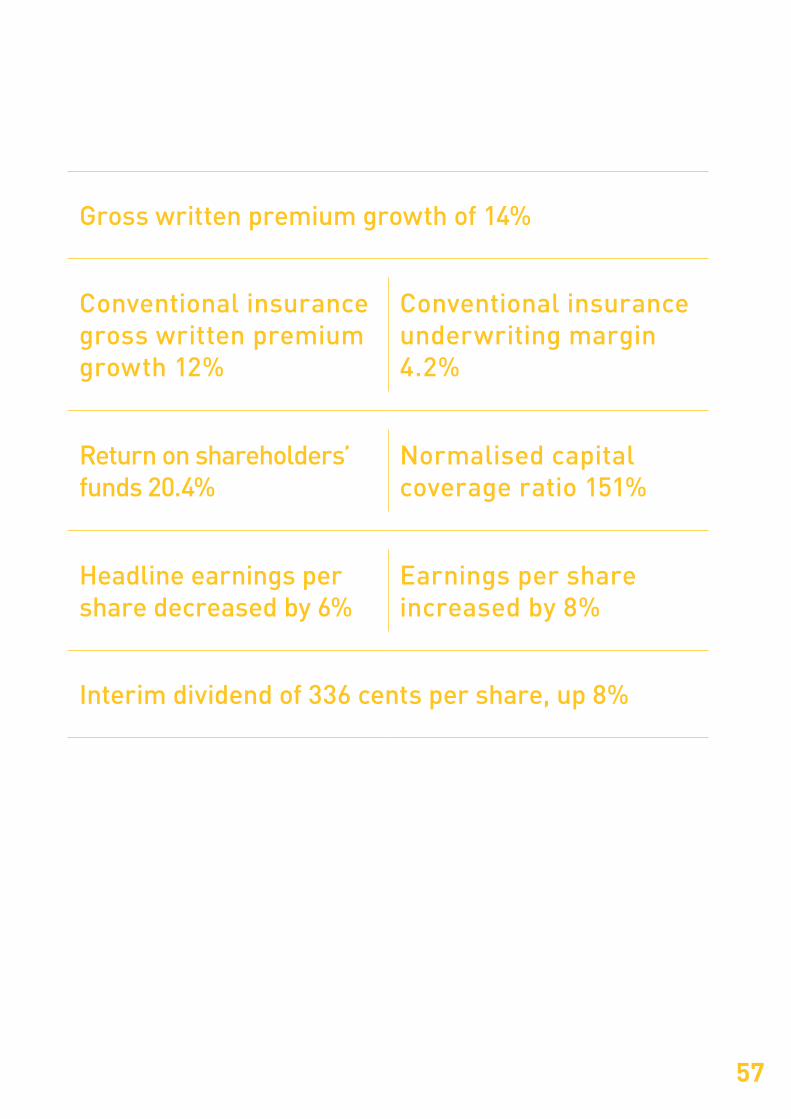

Gross written premium growth of 14%

Conventional insurance gross written premium growth 12%

Conventional insurance underwriting margin 4.2%

Return on shareholders’ funds 20.4%

Normalised capital coverage ratio 151%

Headline earnings per share decreased by 6%

Earnings per share increased by 8%

Interim dividend of 336 cents per share, up 8%

58

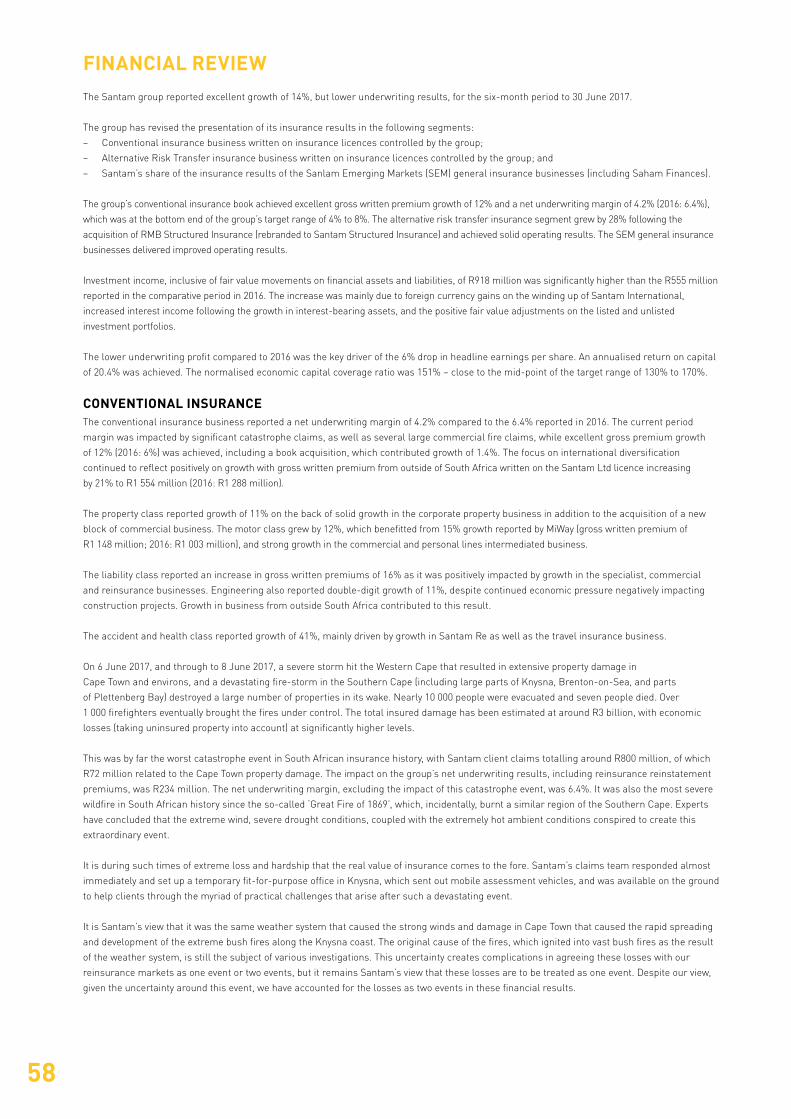

FINANCIAL REVIEWThe Santam group reported excellent growth of 14%, but lower underwriting results, for the six-month period to 30 June 2017.

The group has revised the presentation of its insurance results in the following segments:

– Conventional insurance business written on insurance licences controlled by the group;

– Alternative Risk Transfer insurance business written on insurance licences controlled by the group; and

– Santam’s share of the insurance results of the Sanlam Emerging Markets (SEM) general insurance businesses (including Saham Finances).

The group’s conventional insurance book achieved excellent gross written premium growth of 12% and a net underwriting margin of 4.2% (2016: 6.4%),

which was at the bottom end of the group’s target range of 4% to 8%. The alternative risk transfer insurance segment grew by 28% following the

acquisition of RMB Structured Insurance (rebranded to Santam Structured Insurance) and achieved solid operating results. The SEM general insurance

businesses delivered improved operating results.

Investment income, inclusive of fair value movements on financial assets and liabilities, of R918 million was significantly higher than the R555 million

reported in the comparative period in 2016. The increase was mainly due to foreign currency gains on the winding up of Santam International,

increased interest income following the growth in interest-bearing assets, and the positive fair value adjustments on the listed and unlisted

investment portfolios.

The lower underwriting profit compared to 2016 was the key driver of the 6% drop in headline earnings per share. An annualised return on capital

of 20.4% was achieved. The normalised economic capital coverage ratio was 151% – close to the mid-point of the target range of 130% to 170%.

CONVENTIONAL INSURANCEThe conventional insurance business reported a net underwriting margin of 4.2% compared to the 6.4% reported in 2016. The current period

margin was impacted by significant catastrophe claims, as well as several large commercial fire claims, while excellent gross premium growth

of 12% (2016: 6%) was achieved, including a book acquisition, which contributed growth of 1.4%. The focus on international diversification

continued to reflect positively on growth with gross written premium from outside of South Africa written on the Santam Ltd licence increasing

by 21% to R1 554 million (2016: R1 288 million).

The property class reported growth of 11% on the back of solid growth in the corporate property business in addition to the acquisition of a new

block of commercial business. The motor class grew by 12%, which benefitted from 15% growth reported by MiWay (gross written premium of

R1 148 million; 2016: R1 003 million), and strong growth in the commercial and personal lines intermediated business.

The liability class reported an increase in gross written premiums of 16% as it was positively impacted by growth in the specialist, commercial

and reinsurance businesses. Engineering also reported double-digit growth of 11%, despite continued economic pressure negatively impacting

construction projects. Growth in business from outside South Africa contributed to this result.

The accident and health class reported growth of 41%, mainly driven by growth in Santam Re as well as the travel insurance business.

On 6 June 2017, and through to 8 June 2017, a severe storm hit the Western Cape that resulted in extensive property damage in

Cape Town and environs, and a devastating fire-storm in the Southern Cape (including large parts of Knysna, Brenton-on-Sea, and parts

of Plettenberg Bay) destroyed a large number of properties in its wake. Nearly 10 000 people were evacuated and seven people died. Over

1 000 firefighters eventually brought the fires under control. The total insured damage has been estimated at around R3 billion, with economic

losses (taking uninsured property into account) at significantly higher levels.

This was by far the worst catastrophe event in South African insurance history, with Santam client claims totalling around R800 million, of which

R72 million related to the Cape Town property damage. The impact on the group’s net underwriting results, including reinsurance reinstatement

premiums, was R234 million. The net underwriting margin, excluding the impact of this catastrophe event, was 6.4%. It was also the most severe

wildfire in South African history since the so-called ‘Great Fire of 1869’, which, incidentally, burnt a similar region of the Southern Cape. Experts

have concluded that the extreme wind, severe drought conditions, coupled with the extremely hot ambient conditions conspired to create this

extraordinary event.

It is during such times of extreme loss and hardship that the real value of insurance comes to the fore. Santam’s claims team responded almost

immediately and set up a temporary fit-for-purpose office in Knysna, which sent out mobile assessment vehicles, and was available on the ground

to help clients through the myriad of practical challenges that arise after such a devastating event.

It is Santam’s view that it was the same weather system that caused the strong winds and damage in Cape Town that caused the rapid spreading

and development of the extreme bush fires along the Knysna coast. The original cause of the fires, which ignited into vast bush fires as the result

of the weather system, is still the subject of various investigations. This uncertainty creates complications in agreeing these losses with our

reinsurance markets as one event or two events, but it remains Santam’s view that these losses are to be treated as one event. Despite our view,

given the uncertainty around this event, we have accounted for the losses as two events in these financial results.

59

In addition to the catastrophe events, the underwriting performance of the commercial and corporate property class came under pressure after

an increase in large property claims this year. During tough economic times claims often arise as maintenance and safety standards are

compromised, public service delivery falters, and fraud and arson, which are often difficult to prove, increase. While the drivers are not necessarily

the same, it is notable that Santam’s Property result also suffered when South Africa went through tough economic times from 2008 to 2009.

This challenge is receiving strategic focus by expanding capacity in the areas of risk management and surveying, implementing premium rate

increases, reducing exposure to certain types of risk, and increasing the level of risk sharing and risk management in collaboration

with clients.

The motor class reported strong underwriting performance in both the intermediated and direct distribution channels. MiWay reported excellent

results following an improvement in the claims ratio to 55.4% (2016: 63.1%) as it was positively impacted by disciplined underwriting. The business

contributed an underwriting profit of R179 million (2016: R72 million).

The engineering class of business achieved good underwriting results with limited claims activity during this period. The liability class was

impacted by a number of large claims, but maintained good underwriting results, although these were lower than the excellent results reported

in 2016. The crop insurance business achieved excellent results of R131 million (2016: R8 million), due to the low incidence of hail-related and

drought claims during this period.

Santam Re delivered satisfactory results on third-party business, despite the impact of the catastrophe events on the South African book of business.

The group entered into a new reinsurance arrangement to provide sideways cover against multiple catastrophe events, which replaced the previous

programme. In terms of the new arrangement, effective from May 2017, all catastrophe events that exceed R10 million (previously R50 million)

and capped at R100 million are aggregated under this agreement. A deductible aggregate of R300 million (previously R100 million) applies. The total

amount that can be claimed is R135 million (previously R100 million). There were no other significant changes to the group’s reinsurance programme.

The net acquisition cost ratio of 27.5% decreased from 28.9% in 2016. The management expense ratio decreased from 16% in 2016 to 15.1% in

2017, after being positively impacted by a continued focus on improved efficiencies, timing differences relating to marketing and IT spend as well

as lower incentive cost due to the reduced underwriting performance in 2017.

Strategic project costs, included as part of management expenses, amounted to 0.8% of net earned premium (2016: 0.6%). These costs mainly relate

to the continued development of a new core underwriting, administration and product management platform for the Santam intermediated business.

The project is progressing according to plan, with the majority of personal lines policies now being managed on the new platform. The migration

process for commercial business products is underway. Santam will maintain its focus on cost efficiencies to improve the management expense ratio

over the medium term.

The net commission ratio was 12.4% (2016: 12.9%), positively impacted by the growth in MiWay, where limited commission expenses are incurred,

as well as lower commission ratios on specialist business lines.

The investment return on insurance funds increased to R296 million (2016: R268 million), supported by higher average insurance funds for the

period, as well as the good investment performance of the investment portfolios backing the insurance funds.

ALTERNATIVE RISK TRANSFER INSURANCE (ART)Alternative risk transfer business consists of the risk finance, affinity, underwriting management and structuring businesses of Centriq Insurance

and the newly acquired Santam Structured Insurance. During March 2017, the Santam group acquired a shareholding of 100%, with an economic

interest of 90%, in RMB Structured Insurance (rebranded as Santam Structured Insurance) for R193 million in cash.

The ART business reported growth of 28% with gross written premium of R1 710 million (2016: R1 334 million). Centriq reported no gross written

premium growth due to refunds of risk finance premiums. This was set off by the acquisition of the Santam Structured Insurance book of business.

The ART business reported acceptable operating results before tax of R35 million (2016: R41 million).

SANLAM EMERGING MARKETS (SEM) GENERAL INSURANCE BUSINESSES (INCLUDING SAHAM FINANCES HELD THROUGH SAN JV)The emerging markets general insurance business portfolio includes investments in the Saham Finances Group in Morocco (with subsidiaries in

26 countries in Africa and the Middle East), Pacific & Orient Insurance Co. Bhd. (P&O) in Malaysia, Shriram General Insurance Company Ltd (SGI)

in India and a further 13 general insurance businesses throughout Africa, excluding South Africa and Namibia, which are held in conjunction

with SEM.

Santam’s share of the gross written premium of these businesses increased by 43% to R1 257 million (2016: R880 million) following the inclusion

of the Saham Finances results for the full six-month period (2016: four months), the additional investment in SGI during the second half of 2016,

and the good growth achieved across the businesses in the portfolio, with the exception of P&O. Saham Finances achieved growth in gross written

premium of 8% on a comparative basis.

FINANCIAL REVIEW

60

Santam’s share of the net insurance result of these businesses increased to R101 million compared to R76 million in 2016. The portfolio

of businesses achieved a net insurance margin of 11.6% compared to the 12.8% reported in 2016. The performance of Saham Finances and SGI

were in line with the business plans; however, P&O continues to experience negative growth in competitive market conditions while maintaining an

acceptable underwriting margin.

The Sanlam Group entered into an agreement in June 2017 to dispose of its various interests in the Enterprise Group in Ghana. In terms of the

co-investment arrangement with SEM, Santam, which has an economic interest of 14% in Enterprise Insurance Company (EIC), will also dispose

of its interest in Enterprise Insurance Company Ltd for R106 million.

Effective 10 May 2017, SEM and Santam, through SAN JV, acquired a further 16.6% interest in Saham Finances via a subscription for new

shares for US$351 million (R4.8 billion). Santam’s share of the purchase price, including transaction costs, was US$11 million (R152 million).

Santam’s ability to participate in the transaction was limited due to the size of the investment already held by Santam in SAN JV. The investment in

SAN JV comprised 20.4% of Santam’s shareholder funds at 30 June 2017 (December 2016: 17.5%) making it the largest strategic investment held

by Santam. Santam’s interest in SAN JV therefore diluted to 15% (previously 25%). The dilution of Santam’s interest in SAN JV did not affect any of

its existing shareholder rights.

INVESTMENT RESULTSListed equities achieved a return of 3.9% for the six months to June 2017, thereby outperforming the SWIX benchmark of 3.3%. The Santam

group’s interest exposure is managed in enhanced cash and active income portfolios. The interest portfolios comfortably exceeded their

STeFI-related benchmarks.

Positive fair value movements (excluding the impact of currency movements) of R104 million (2016: negative movement of R71 million) in Santam’s

interest in SEM’s general insurance businesses in Africa, India and Southeast Asia contributed to the improved investment performance.

Net earnings from associated companies of R54 million increased from the R45 million reported in 2016. SAN JV (Saham Finances) contributed

equity-accounted earnings of R26 million (2016: R29 million).

During June 2017, the company successfully issued additional unsecured subordinated debt to the value of R1 billion in anticipation of the

redemption of the R1 billion subordinated debt issued in 2007, which is callable in September 2017.

PROSPECTSTrading conditions remain very competitive in a low-growth economic environment. Real annual GDP contracted by 0.7% in the first quarter

following a contraction in the economy in the fourth quarter of 2016, which resulted in a technical recession. Inflation (average CPI) of 5.1% was

reported at the end of the second quarter. The repo rate was lowered by 25 basis points in July 2017 following the 75 basis points increase

in 2016. The decrease in the repo rate will marginally impact interest income for the group.

In April 2017, Standard & Poor’s (S&P) decreased Santam’s international counterparty credit and insurance financial strength rating from BBB to

BBB-, in line with their local currency sovereign rating on South Africa (BBB-, negative). On a national scale basis, Santam’s counterparty credit

rating remained unchanged at zaAAA following the recalibration of South Africa’s National scale ratings by S&P on 3 August 2017.

The group’s focus remains on growing profitably in South Africa and to increase its international diversification through the Santam Specialist

Business and Santam Re. International diversification is supported by close collaboration with the SEM general insurance businesses, which

utilises the extensive emerging markets footprint to source new business opportunities. Santam continues to focus strategically on supporting the

development of the SEM general insurance businesses by allocating appropriate technical resources. In South Africa, continued focus is placed on

the development of Santam’s full multichannel capability.

Santam will maintain its focus on cost efficiencies to improve the management expense ratio over the medium term. The investment market is

likely to remain uncertain. Continued high volatility is expected on interest-bearing instruments. The increased exposure to non-rand-denominated

business further increases foreign exchange volatility for the group.

The group economic capital requirement at 30 June 2017, based on the Santam internal model, amounted to R5.9 billion. The normalised

economic capital coverage ratio, assuming a sub-debt of R2 billion, was 151%, which was close to the mid-point of the target range

of 130% to 170%.

We remain committed to efficient capital management.

FINANCIAL REVIEW

61

FINANCIAL REVIEW

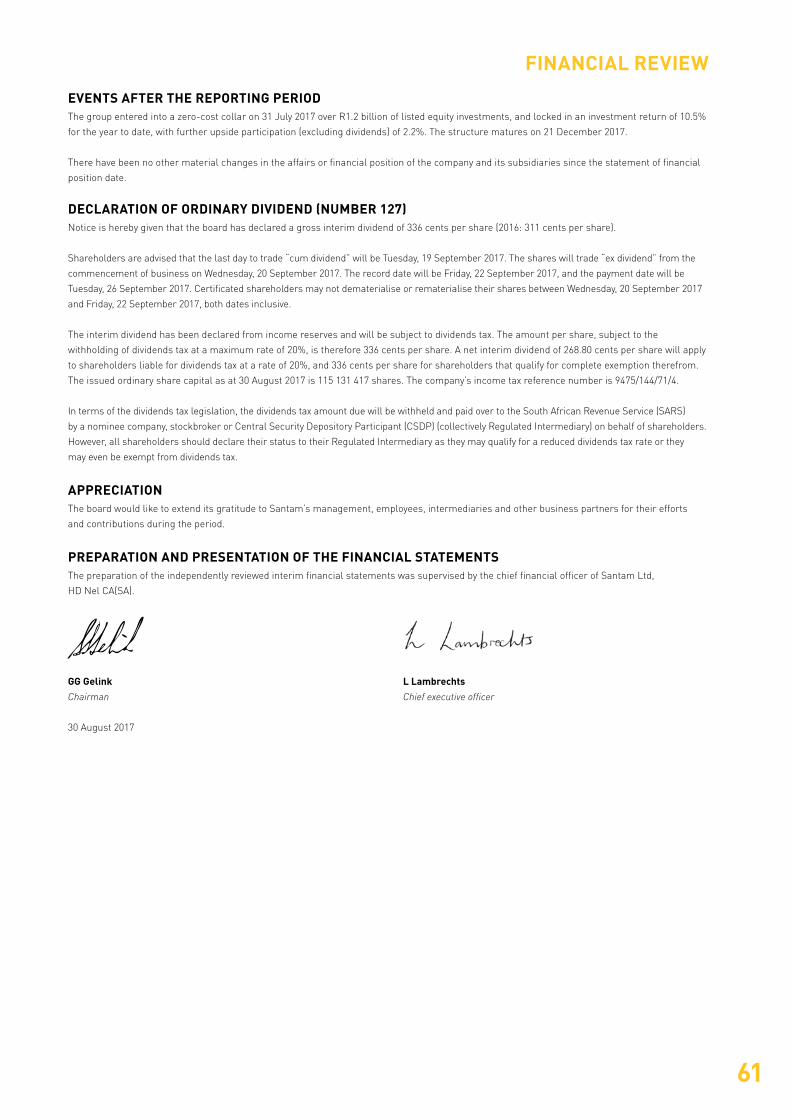

EVENTS AFTER THE REPORTING PERIODThe group entered into a zero-cost collar on 31 July 2017 over R1.2 billion of listed equity investments, and locked in an investment return of 10.5%

for the year to date, with further upside participation (excluding dividends) of 2.2%. The structure matures on 21 December 2017.

There have been no other material changes in the affairs or financial position of the company and its subsidiaries since the statement of financial

position date.

DECLARATION OF ORDINARY DIVIDEND (NUMBER 127)Notice is hereby given that the board has declared a gross interim dividend of 336 cents per share (2016: 311 cents per share).

Shareholders are advised that the last day to trade “cum dividend” will be Tuesday, 19 September 2017. The shares will trade “ex dividend” from the

commencement of business on Wednesday, 20 September 2017. The record date will be Friday, 22 September 2017, and the payment date will be

Tuesday, 26 September 2017. Certificated shareholders may not dematerialise or rematerialise their shares between Wednesday, 20 September 2017

and Friday, 22 September 2017, both dates inclusive.

The interim dividend has been declared from income reserves and will be subject to dividends tax. The amount per share, subject to the

withholding of dividends tax at a maximum rate of 20%, is therefore 336 cents per share. A net interim dividend of 268.80 cents per share will apply

to shareholders liable for dividends tax at a rate of 20%, and 336 cents per share for shareholders that qualify for complete exemption therefrom.

The issued ordinary share capital as at 30 August 2017 is 115 131 417 shares. The company’s income tax reference number is 9475/144/71/4.

In terms of the dividends tax legislation, the dividends tax amount due will be withheld and paid over to the South African Revenue Service (SARS)

by a nominee company, stockbroker or Central Security Depository Participant (CSDP) (collectively Regulated Intermediary) on behalf of shareholders.

However, all shareholders should declare their status to their Regulated Intermediary as they may qualify for a reduced dividends tax rate or they

may even be exempt from dividends tax.

APPRECIATIONThe board would like to extend its gratitude to Santam’s management, employees, intermediaries and other business partners for their efforts

and contributions during the period.

PREPARATION AND PRESENTATION OF THE FINANCIAL STATEMENTSThe preparation of the independently reviewed interim financial statements was supervised by the chief financial officer of Santam Ltd,

HD Nel CA(SA).

GG Gelink L LambrechtsChairman Chief executive officer

30 August 2017

62

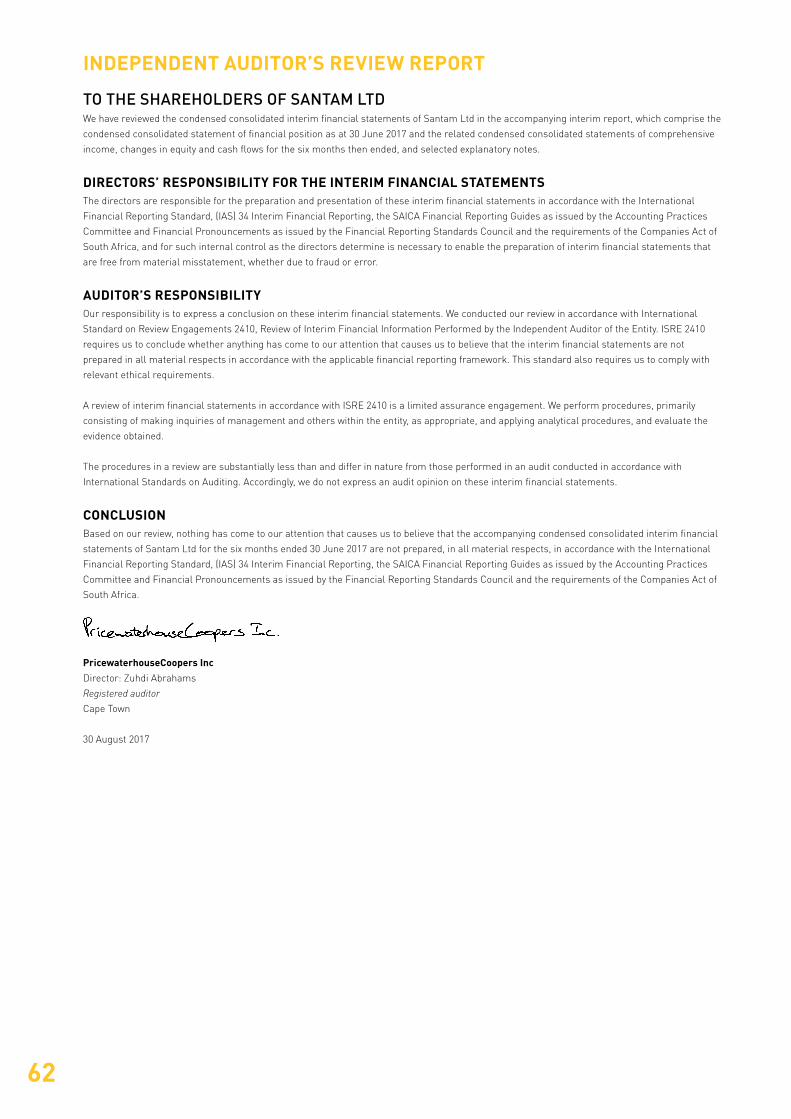

INDEPENDENT AUDITOR’S REVIEW REPORT

TO THE SHAREHOLDERS OF SANTAM LTDWe have reviewed the condensed consolidated interim financial statements of Santam Ltd in the accompanying interim report, which comprise the

condensed consolidated statement of financial position as at 30 June 2017 and the related condensed consolidated statements of comprehensive

income, changes in equity and cash flows for the six months then ended, and selected explanatory notes.

DIRECTORS’ RESPONSIBILITY FOR THE INTERIM FINANCIAL STATEMENTSThe directors are responsible for the preparation and presentation of these interim financial statements in accordance with the International

Financial Reporting Standard, (IAS) 34 Interim Financial Reporting, the SAICA Financial Reporting Guides as issued by the Accounting Practices

Committee and Financial Pronouncements as issued by the Financial Reporting Standards Council and the requirements of the Companies Act of

South Africa, and for such internal control as the directors determine is necessary to enable the preparation of interim financial statements that

are free from material misstatement, whether due to fraud or error.

AUDITOR’S RESPONSIBILITYOur responsibility is to express a conclusion on these interim financial statements. We conducted our review in accordance with International

Standard on Review Engagements 2410, Review of Interim Financial Information Performed by the Independent Auditor of the Entity. ISRE 2410

requires us to conclude whether anything has come to our attention that causes us to believe that the interim financial statements are not

prepared in all material respects in accordance with the applicable financial reporting framework. This standard also requires us to comply with

relevant ethical requirements.

A review of interim financial statements in accordance with ISRE 2410 is a limited assurance engagement. We perform procedures, primarily

consisting of making inquiries of management and others within the entity, as appropriate, and applying analytical procedures, and evaluate the

evidence obtained.

The procedures in a review are substantially less than and differ in nature from those performed in an audit conducted in accordance with

International Standards on Auditing. Accordingly, we do not express an audit opinion on these interim financial statements.

CONCLUSIONBased on our review, nothing has come to our attention that causes us to believe that the accompanying condensed consolidated interim financial

statements of Santam Ltd for the six months ended 30 June 2017 are not prepared, in all material respects, in accordance with the International

Financial Reporting Standard, (IAS) 34 Interim Financial Reporting, the SAICA Financial Reporting Guides as issued by the Accounting Practices

Committee and Financial Pronouncements as issued by the Financial Reporting Standards Council and the requirements of the Companies Act of

South Africa.

PricewaterhouseCoopers IncDirector: Zuhdi Abrahams

Registered auditor

Cape Town

30 August 2017

63

Reviewed at Reviewed at Audited at

30 June 2017 30 June 2016 31 Dec 2016

Notes R million R million R million

ASSETSNon-current assets

Property and equipment 125 96 106

Intangible assets 860 837 885

Deferred income tax 63 124 105

Investment in associates and joint ventures 1 782 1 702 1 536

Financial assets at fair value through income

Equity securities 6 4 633 2 788 2 581

Debt securities 6 12 796 10 911 10 849

Reinsurance assets 7 279 164 140

Deposit with cell owner 141 231 163

Total non-current assets 20 679 16 853 16 365

Current assetsCell owners’ and policyholders’ interest 8 4 7

Financial assets at fair value through income

Equity securities 6 106 – –

Derivatives 6 6 6 1

Short-term money market instruments 6 2 665 1 981 1 361

Reinsurance assets 7 5 678 3 953 4 349

Deposit with cell owner 48 61 56

Deferred acquisition costs 425 410 469

Loans and receivables including insurance receivables 6 3 997 3 322 3 754

Income tax assets 33 17 19

Cash and cash equivalents 4 118 2 241 2 887

Non-current assets held for sale 8 – 125 8

Total current assets 17 084 12 120 12 911

Total assets 37 763 28 973 29 276

EQUITY AND LIABILITIESCapital and reserves attributable to the company’s equity holders

Share capital 103 103 103

Treasury shares (463) (460) (472)

Other reserves (113) 240 (41)

Distributable reserves 7 374 7 958 7 286

6 901 7 841 6 876

Non-controlling interest 475 461 469

Total equity 7 376 8 302 7 345

Non-current liabilitiesDeferred income tax 229 217 101

Financial liabilities at fair value through income

Debt securities 6 2 021 2 005 2 005

Derivatives 6 – 1 –

Cell owners’ and policyholders’ interest 1 206 1 060 1 153

Insurance liabilities 7 1 701 1 423 1 312

Reinsurance liability relating to cell owners 141 231 163

Total non-current liabilities 5 298 4 937 4 734

Current liabilitiesFinancial liabilities at fair value through income

Debt securities 6 1 047 48 48

Investment contracts 6 1 639 84 101

Derivatives 6 – 9 –Financial liabilities at amortised cost

Collateral guarantee contracts 6 134 104 123

Cell owners’ and policyholders’ interest 1 779 – –

Insurance liabilities 7 15 917 11 577 12 284

Reinsurance liability relating to cell owners 48 61 56

Deferred reinsurance acquisition revenue 214 183 273

Provisions for other liabilities and charges 98 83 71

Trade and other payables including insurance payables 6 4 132 3 407 4 093

Current income tax liabilities 81 178 148

Total current liabilities 25 089 15 734 17 197

Total liabilities 30 387 20 671 21 931

Total shareholders’ equity and liabilities 37 763 28 973 29 276

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

64

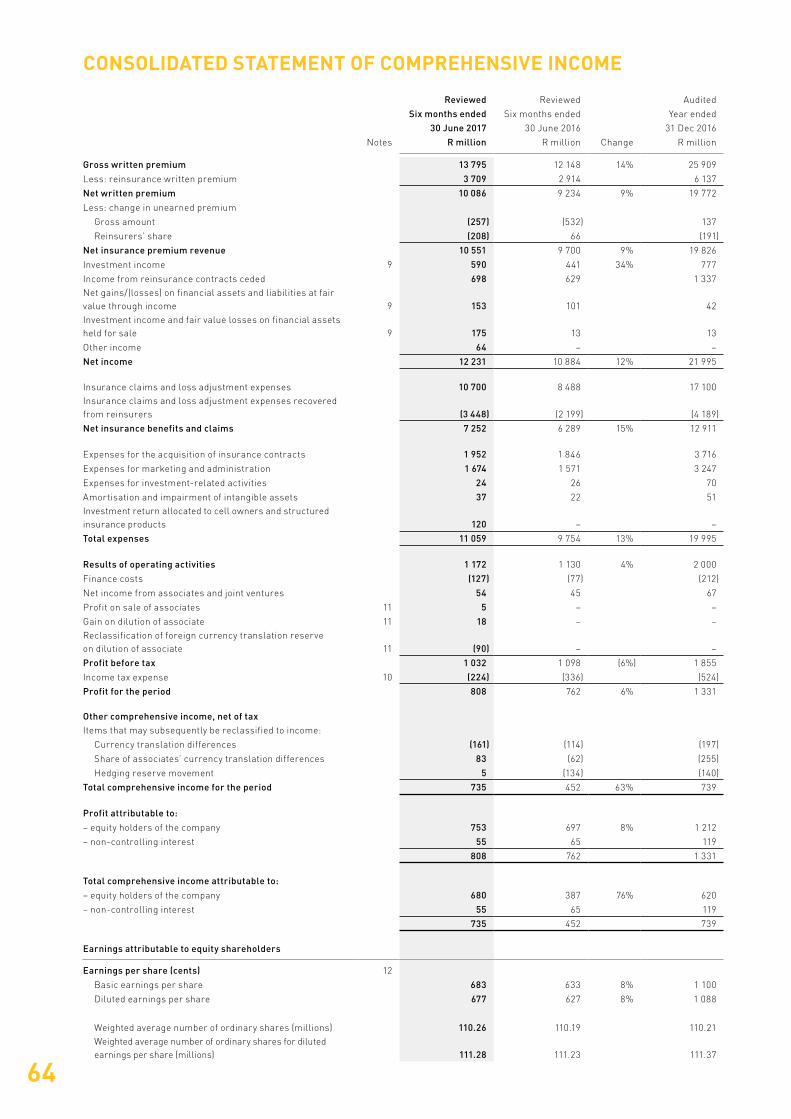

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

Reviewed Reviewed Audited

Six months ended Six months ended Year ended

30 June 2017 30 June 2016 31 Dec 2016

Notes R million R million Change R million

Gross written premium 13 795 12 148 14% 25 909

Less: reinsurance written premium 3 709 2 914 6 137

Net written premium 10 086 9 234 9% 19 772

Less: change in unearned premium

Gross amount (257) (532) 137

Reinsurers’ share (208) 66 (191)

Net insurance premium revenue 10 551 9 700 9% 19 826

Investment income 9 590 441 34% 777

Income from reinsurance contracts ceded 698 629 1 337 Net gains/(losses) on financial assets and liabilities at fair value through income 9 153 101 42 Investment income and fair value losses on financial assets held for sale 9 175 13 13

Other income 64 – –

Net income 12 231 10 884 12% 21 995

Insurance claims and loss adjustment expenses 10 700 8 488 17 100Insurance claims and loss adjustment expenses recovered from reinsurers (3 448) (2 199) (4 189)

Net insurance benefits and claims 7 252 6 289 15% 12 911

Expenses for the acquisition of insurance contracts 1 952 1 846 3 716

Expenses for marketing and administration 1 674 1 571 3 247

Expenses for investment-related activities 24 26 70

Amortisation and impairment of intangible assets 37 22 51Investment return allocated to cell owners and structured insurance products 120 – –

Total expenses 11 059 9 754 13% 19 995

Results of operating activities 1 172 1 130 4% 2 000

Finance costs (127) (77) (212)

Net income from associates and joint ventures 54 45 67

Profit on sale of associates 11 5 – –

Gain on dilution of associate 11 18 – –Reclassification of foreign currency translation reserve on dilution of associate 11 (90) – –

Profit before tax 1 032 1 098 (6%) 1 855

Income tax expense 10 (224) (336) (524)

Profit for the period 808 762 6% 1 331

Other comprehensive income, net of taxItems that may subsequently be reclassified to income:

Currency translation differences (161) (114) (197)

Share of associates’ currency translation differences 83 (62) (255)

Hedging reserve movement 5 (134) (140)

Total comprehensive income for the period 735 452 63% 739

Profit attributable to:– equity holders of the company 753 697 8% 1 212

– non-controlling interest 55 65 119

808 762 1 331

Total comprehensive income attributable to:– equity holders of the company 680 387 76% 620

– non-controlling interest 55 65 119

735 452 739

Earnings attributable to equity shareholders

Earnings per share (cents) 12

Basic earnings per share 683 633 8% 1 100

Diluted earnings per share 677 627 8% 1 088

Weighted average number of ordinary shares (millions) 110.26 110.19 110.21Weighted average number of ordinary shares for diluted earnings per share (millions) 111.28 111.23 111.37

65

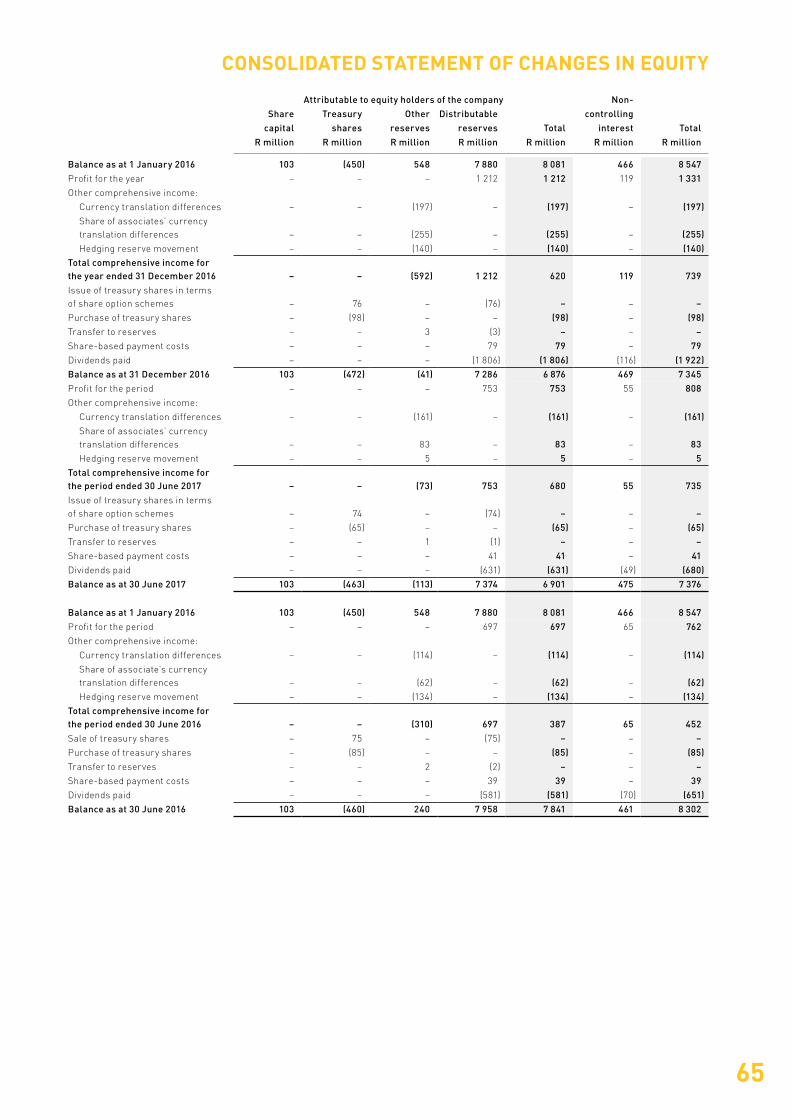

Attributable to equity holders of the company Non-Share Treasury Other Distributable controlling

capital shares reserves reserves Total interest TotalR million R million R million R million R million R million R million

Balance as at 1 January 2016 103 (450) 548 7 880 8 081 466 8 547 Profit for the year – – – 1 212 1 212 119 1 331 Other comprehensive income:

Currency translation differences – – (197) – (197) – (197)Share of associates’ currency translation differences – – (255) – (255) – (255)Hedging reserve movement – – (140) – (140) – (140)

Total comprehensive income for the year ended 31 December 2016 – – (592) 1 212 620 119 739 Issue of treasury shares in terms of share option schemes – 76 – (76) – – – Purchase of treasury shares – (98) – – (98) – (98)Transfer to reserves – – 3 (3) – – – Share-based payment costs – – – 79 79 – 79Dividends paid – – – (1 806) (1 806) (116) (1 922)Balance as at 31 December 2016 103 (472) (41) 7 286 6 876 469 7 345Profit for the period – – – 753 753 55 808Other comprehensive income:

Currency translation differences – – (161) – (161) – (161)Share of associates’ currency translation differences – – 83 – 83 – 83Hedging reserve movement – – 5 – 5 – 5

Total comprehensive income for the period ended 30 June 2017 – – (73) 753 680 55 735 Issue of treasury shares in terms of share option schemes – 74 – (74) – – – Purchase of treasury shares – (65) – – (65) – (65)Transfer to reserves – – 1 (1) – – – Share-based payment costs – – – 41 41 – 41Dividends paid – – – (631) (631) (49) (680)Balance as at 30 June 2017 103 (463) (113) 7 374 6 901 475 7 376

Balance as at 1 January 2016 103 (450) 548 7 880 8 081 466 8 547 Profit for the period – – – 697 697 65 762 Other comprehensive income:

Currency translation differences – – (114) – (114) – (114)Share of associate’s currency translation differences – – (62) – (62) – (62)Hedging reserve movement – – (134) – (134) – (134)

Total comprehensive income for the period ended 30 June 2016 – – (310) 697 387 65 452 Sale of treasury shares – 75 – (75) – – – Purchase of treasury shares – (85) – – (85) – (85)Transfer to reserves – – 2 (2) – – – Share-based payment costs – – – 39 39 – 39 Dividends paid – – – (581) (581) (70) (651)Balance as at 30 June 2016 103 (460) 240 7 958 7 841 461 8 302

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

66

CONSOLIDATED STATEMENT OF CASH FLOWS

Reviewed Reviewed Audited

Six months ended Six months ended Year ended

30 June 2017 30 June 2016 31 Dec 2016

Notes R million R million R million

Cash flows from operating activities

Cash generated from operations 1 637 844 2 171

Interest paid (94) (50) (161)

Income tax paid (210) (340) (681)

Net cash from operating activities 1 333 454 1 329

Cash flows from investing activities

Acquisition of financial assets (7 774) (9 505) (17 594)

Proceeds from sale of financial assets 6 799 8 538 17 764

Settlement of fence – – 75

Acquisition of business, net of cash acquired 11 852 – 70

Cash received through sale of subsidiaries 11 – 208 208

Purchases of equipment (20) (26) (60)

Purchases of intangible assets (12) (21) (50)

Proceeds from sale of equipment 1 1 2

Acquisition of associates and joint ventures 11 (152) (1 467) (1 467)

Capitalisation of associates 11 (14) – (10)

Proceeds from sale of associates 11 23 – –

Settlement of deferred conditional right relating to non-current assets held for sale – – 509

Cash proceeds from unwinding of non-current assets held for sale 8 – 394 –

Net cash used in investing activities (297) (1 878) (553)

Cash flows from financing activities

Purchase of treasury shares (65) (85) (98)

Proceeds from issue of unsecured subordinated callable notes 1 000 1 000 1 000

Increase in investment contract liabilities 5 7 31

Increase in collateral guarantee contracts 6 – 12

Dividends paid to company’s shareholders (631) (581) (1 806)

Dividends paid to non-controlling interest (49) (70) (116)

(Decrease)/increase in cell owners’ and policyholders’ interest (38) 120 (114)

Net cash from/(used in) financing activities 228 391 (1 091)

Net increase/(decrease) in cash and cash equivalents 1 264 (1 033) (315)

Cash and cash equivalents at the beginning of the period 2 887 3 349 3 349

Exchange losses on cash and cash equivalents (33) (75) (147)

Cash and cash equivalents at the end of the period 4 118 2 241 2 887

67

NOTES TO THE INTERIM FINANCIAL STATEMENTS

1. Basis of preparationThe condensed consolidated interim financial statements are prepared in accordance with International Financial Reporting Standards, IAS 34 – Interim Financial Reporting, the SAICA Financial Reporting Guides as issued by the Accounting Practices Committee and Financial Pronouncements as issued by the Financial Reporting Standards Council and the requirements of the Companies Act of South Africa.

2. Accounting policiesThe accounting policies applied in the preparation of the condensed consolidated interim financial statements are in terms of IFRS and are consistent with those accounting policies applied in the preparation of the previous consolidated annual financial statements, except for:

The following new IFRSs and/or IFRICs were effective for the first time from 1 January 2017: – Amendment to IAS 7 – Statement of Cash Flows – Amendment to IAS 12 – Income Taxes

There was no material impact on the condensed consolidated interim financial statements identified.

Of the standards that are not yet effective, management expects IFRS 9 and IFRS 17 to have an impact on the group. IFRS 9 addresses classification and measurement of financial assets and replaces the multiple classification and measurement models in IAS 39 with a single model that has only two classification categories: amortised cost and fair value. Based on management’s current assessment, the impact is not expected to be material.

IFRS 17 establishes the principles for the recognition, measurement, presentation and disclosure of insurance contracts within the scope of the standard. IFRS 17 was issued in May 2017 and applies to annual reporting periods beginning on or after 1 January 2021. Management is currently busy with a detailed assessment of the impact of this standard.

3. EstimatesThe preparation of condensed consolidated interim financial statements requires management to make judgements, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets and liabilities, income and expenses. Actual results may differ from these estimates.

In preparing these condensed consolidated interim financial statements, the significant judgements made by management in applying the group’s accounting policies and the key sources of estimation uncertainty are the same as those that applied to the consolidated annual financial statements for the year ended 31 December 2016.

4. Risk managementThe group’s activities expose it to a variety of financial risks: market risk (including price risk, interest rate risk, foreign currency risk and derivatives risk), credit risk and liquidity risk. Insurance activities expose the group to insurance risk (including pricing risk, reserving risk, accumulation risk and reinsurance risk). The group is also exposed to operational risk and legal risk.

The capital risk management philosophy is to maximise the return on shareholders’ capital within an appropriate risk framework.

The condensed consolidated interim financial statements do not include all risk management information and disclosure required in the annual financial statements and should be read in conjunction with the group’s annual financial statements as at 31 December 2016.

There have been no material changes in the risk management policies since 31 December 2016.

68

NOTES TO THE INTERIM FINANCIAL STATEMENTS

5. Segment informationOperating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker. The chief operating decision-maker, who is responsible for allocating resources and assessing performance of the operating segments, has been identified as the chief executive officer, supported by the group executive committee.

The group conducts mainly insurance and investment activities.

Insurance activities: The group has revised the presentation of its insurance results in the following segments:

– Conventional insurance business written on insurance licences controlled by the group. – Alternative risk transfer insurance business written on insurance licences controlled by the group. – Santam’s share of the insurance results of the Sanlam Emerging Markets general insurance businesses, including SAN JV (Saham Finances).

It is further analysed by insurance class. Operating segments are aggregated based on quantitative and/or qualitative significance. The performance of insurance activities is based on gross written premium as a measure of growth, with net underwriting result as measure of profitability.

As noted above, the presentation of insurance activities has been enhanced subsequent to the acquisition of SSI (refer to note 11). The comparative information has been restated to provide the information in the same enhanced format.

Investment activities:Investment activities are all investment-related activities undertaken by the group. Due to the nature of the activities conducted, investment activities are considered to be one operating segment. Investment activities are measured based on net investment income.

Growth is measured for strategic investments based on the gross written premium generated by the underlying businesses. The underwriting and investment return on insurance funds are provided for each of the underlying components included in the insurance segment for consideration by the chief operating decision-maker. With regard to the SEM and SAN JV (Saham Finances) insurance business, this information is considered to be a reallocation of fair value movements recognised on the SEM target shares as well as equity-accounted earnings on the investments in associates and joint ventures. It is also included as reconciling items in order to reconcile to the consolidated statement of comprehensive income. Overall profitability is measured based on net investment income and fair value movements from SEM target share investments and net income from associates and joint ventures.

Given the nature of the operations, there is no single external client that provides 10% or more of the group’s revenues.

The investment return on insurance funds is calculated based on the day-weighted effective return realised by the group on the assets held to cover the group’s net insurance working capital requirements.

Insurance business denominated in foreign currencies is covered by foreign denominated bank accounts and investment portfolios. Foreign exchange movements on underwriting activities are therefore offset against the foreign exchange movements recognised on the bank accounts and investment portfolios.

The Santam BEE transaction costs are unrelated to the core underwriting and investment performance of the group. Therefore, these costs are disclosed as unallocated activities.

Santam Ltd is domiciled in South Africa. Geographical analysis of the gross written premium and non-current assets and liabilities is based on the countries in which the business is underwritten or managed. Non-current assets comprise goodwill and intangible assets, property and equipment, investments in associates and joint ventures and SEM target shares (included in financial assets).

69

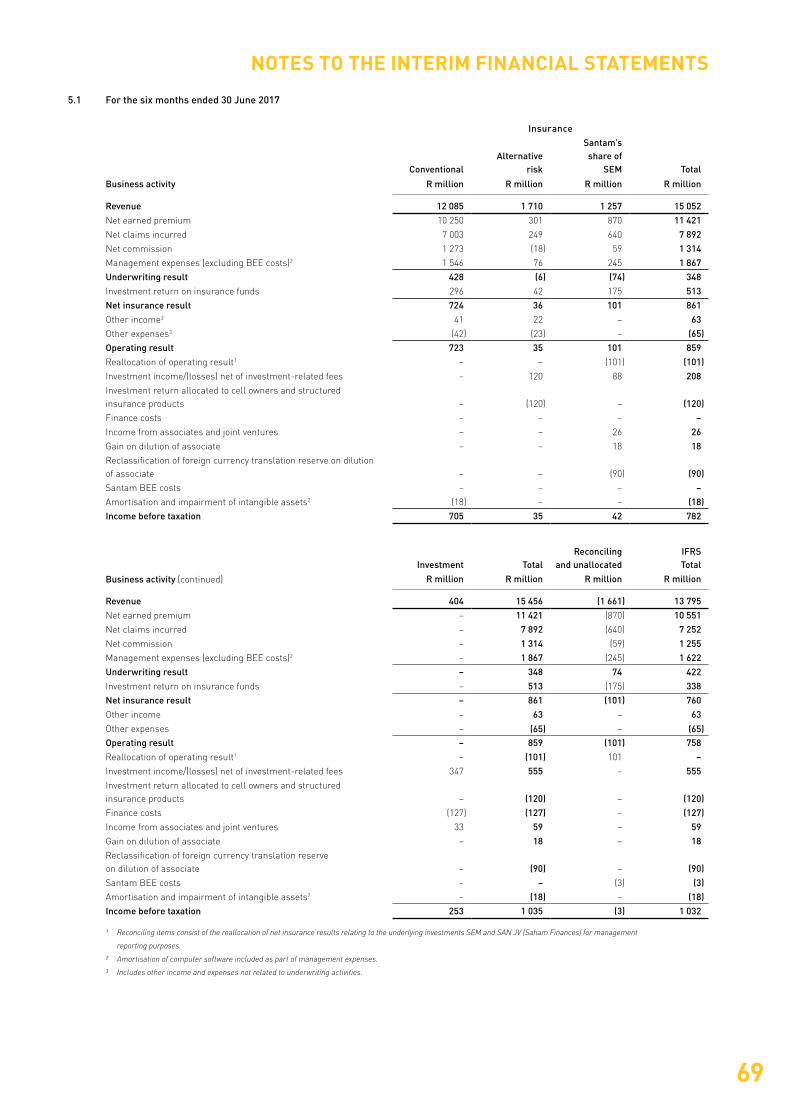

NOTES TO THE INTERIM FINANCIAL STATEMENTS

Business activity (continued)

Investment TotalReconciling

and unallocatedIFRSTotal

R million R million R million R million

Revenue 404 15 456 (1 661) 13 795 Net earned premium – 11 421 (870) 10 551 Net claims incurred – 7 892 (640) 7 252 Net commission – 1 314 (59) 1 255 Management expenses (excluding BEE costs)2 – 1 867 (245) 1 622Underwriting result – 348 74 422Investment return on insurance funds – 513 (175) 338Net insurance result – 861 (101) 760Other income – 63 – 63Other expenses – (65) – (65)Operating result – 859 (101) 758Reallocation of operating result1 – (101) 101 –Investment income/(losses) net of investment-related fees 347 555 – 555Investment return allocated to cell owners and structured insurance products – (120) – (120)Finance costs (127) (127) – (127)Income from associates and joint ventures 33 59 – 59Gain on dilution of associate – 18 – 18Reclassification of foreign currency translation reserve on dilution of associate – (90) – (90)Santam BEE costs – – (3) (3)Amortisation and impairment of intangible assets2 – (18) – (18)Income before taxation 253 1 035 (3) 1 032

1 Reconciling items consist of the reallocation of net insurance results relating to the underlying investments SEM and SAN JV (Saham Finances) for management

reporting purposes.

2 Amortisation of computer software included as part of management expenses.

3 Includes other income and expenses not related to underwriting activities.

5.1 For the six months ended 30 June 2017

Insurance

Business activity

ConventionalAlternative

risk

Santam’sshare of

SEM Total

R million R million R million R million

Revenue 12 085 1 710 1 257 15 052 Net earned premium 10 250 301 870 11 421 Net claims incurred 7 003 249 640 7 892 Net commission 1 273 (18) 59 1 314 Management expenses (excluding BEE costs)2 1 546 76 245 1 867Underwriting result 428 (6) (74) 348Investment return on insurance funds 296 42 175 513Net insurance result 724 36 101 861Other income3 41 22 – 63Other expenses3 (42) (23) – (65)Operating result 723 35 101 859Reallocation of operating result1 – – (101) (101)Investment income/(losses) net of investment-related fees – 120 88 208Investment return allocated to cell owners and structured insurance products – (120) – (120)Finance costs – – – – Income from associates and joint ventures – – 26 26Gain on dilution of associate – – 18 18Reclassification of foreign currency translation reserve on dilution of associate – – (90) (90)Santam BEE costs – – – – Amortisation and impairment of intangible assets2 (18) – – (18)Income before taxation 705 35 42 782

70

NOTES TO THE INTERIM FINANCIAL STATEMENTS

5. Segment information (continued)

5.1 For the six months ended 30 June 2017 (continued)

Gross written Underwriting premium result R million R million

Insurance activitiesThe group’s conventional insurance activities are spread over various classes of general insurance.

Accident and health 232 35

Crop 72 131

Engineering 645 114

Guarantee 77 (3)

Liability 566 93

Miscellaneous 5 2

Motor 5 944 459

Property 4 188 (415)

Transportation 356 12

Total 12 085 428

Comprising:Commercial insurance 6 542 247Personal insurance 5 543 181

Total 12 085 428

R million

Investment activitiesThe group’s return on investment-related activities can be analysed as follows:

Investment income 308

Net gains on financial assets and liabilities at fair value through income 63

Income from associates and joint ventures 33Investment-related revenue 404Expenses for investment-related activities (24)

Finance costs (127)Net total investment-related transactions 253

For detailed analysis of investment activities, refer to notes 6 and 9.

Santam's share of SEMThe group's return on Santam's share of SEM activities can be analysed as follows:

SEM

SAN JV (Saham

Finances) Total R million R million R million

Revenue 672 585 1 257

Net earned premium 434 436 870 Net claims incurred 359 281 640 Net commission 14 45 59 Management expenses (excluding BEE costs) 118 127 245 Underwriting result (57) (17) (74)Investment return on insurance funds 96 79 175 Net insurance result/operating result 39 62 101 Reallocation of operating result1 (39) (62) (101)Investment income net of investment-related fees 88 – 88 Income from associates and joint ventures – 26 26 Gain on dilution of associate – 18 18 Reclassification of foreign currency translation reserve on dilution of associate – (90) (90)Income/(loss) before taxation 88 (46) 42

1 Reconciling items consist of the reallocation of net insurance results relating to the underlying investments SEM and SAN JV (Saham Finances) for management

reporting purposes.

71

NOTES TO THE INTERIM FINANCIAL STATEMENTS

Business activity (continued)

Investment TotalReconciling

and unallocated Total

R million R million R million R million

Revenue 390 13 418 (1 270) 12 148

Net earned premium – 10 296 (596) 9 700

Net claims incurred – 6 700 (411) 6 289

Net commission – 1 274 (57) 1 217

Management expenses (excluding BEE costs)2 – 1 735 (159) 1 576

Underwriting result – 587 31 618

Investment return on insurance funds – 398 (107) 291

Net insurance result – 985 (76) 909

Other income – 60 – 16

Other expenses – (60) – (60)

Operating result – 985 (76) 909

Reallocation of operating result1 – (76) 76 –

Investment income/(losses) net of investment-related fees 348 337 – 337

Investment return allocated to cell owners and structured insurance products – (99) – (99)

Finance costs (77) (77) – (77)

Income from associates and joint ventures 16 45 – 45

Santam BEE costs – – (6) (6)

Amortisation and impairment of intangible assets2 – (11) – (11)

Income before taxation 287 1 104 (6) 1 098

1 Reconciling items consist of the reallocation of net insurance results relating to the underlying investments SEM and SAN JV (Saham Finances) for management

reporting purposes.

2 Amortisation of computer software included as part of management expenses.

3 Includes other income and expenses not related to underwriting activities.

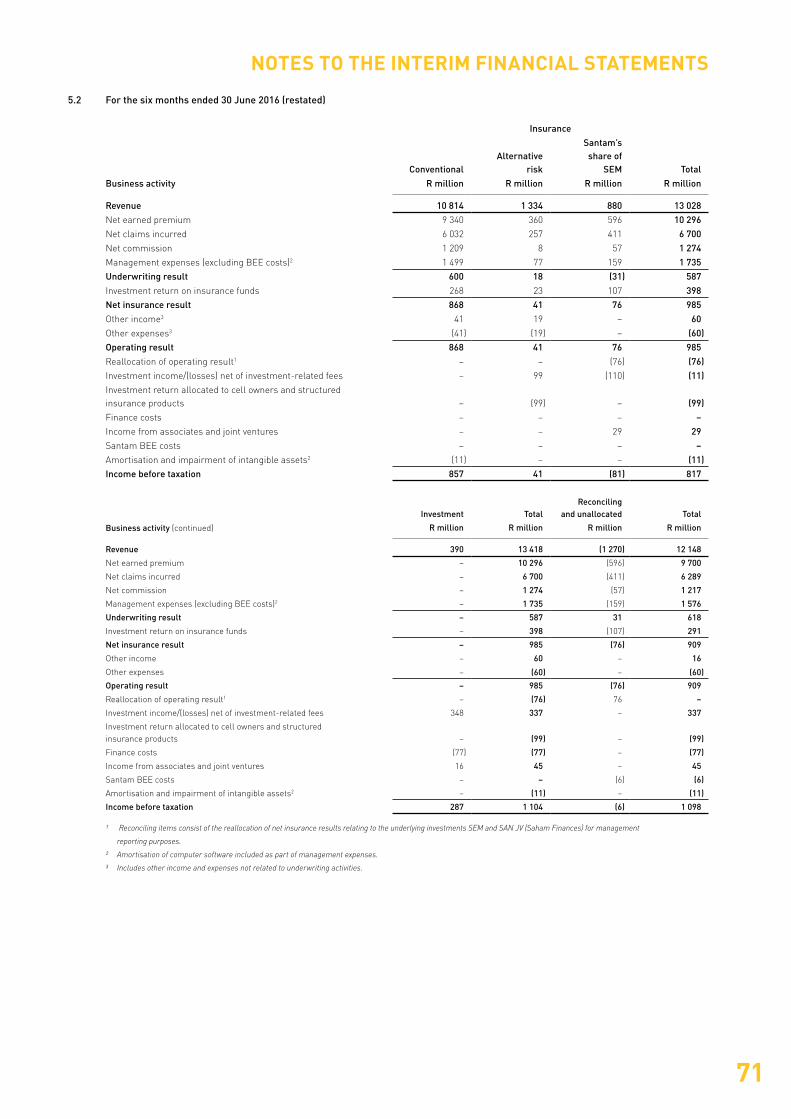

5.2 For the six months ended 30 June 2016 (restated)

Insurance

Business activityConventional

Alternativerisk

Santam’s share of

SEM TotalR million R million R million R million

Revenue 10 814 1 334 880 13 028 Net earned premium 9 340 360 596 10 296 Net claims incurred 6 032 257 411 6 700 Net commission 1 209 8 57 1 274 Management expenses (excluding BEE costs)2 1 499 77 159 1 735Underwriting result 600 18 (31) 587 Investment return on insurance funds 268 23 107 398Net insurance result 868 41 76 985Other income3 41 19 – 60Other expenses3 (41) (19) – (60)Operating result 868 41 76 985Reallocation of operating result1 – – (76) (76)Investment income/(losses) net of investment-related fees – 99 (110) (11) Investment return allocated to cell owners and structured insurance products – (99) – (99)Finance costs – – – – Income from associates and joint ventures – – 29 29Santam BEE costs – – – – Amortisation and impairment of intangible assets2 (11) – – (11)Income before taxation 857 41 (81) 817

72

NOTES TO THE INTERIM FINANCIAL STATEMENTS

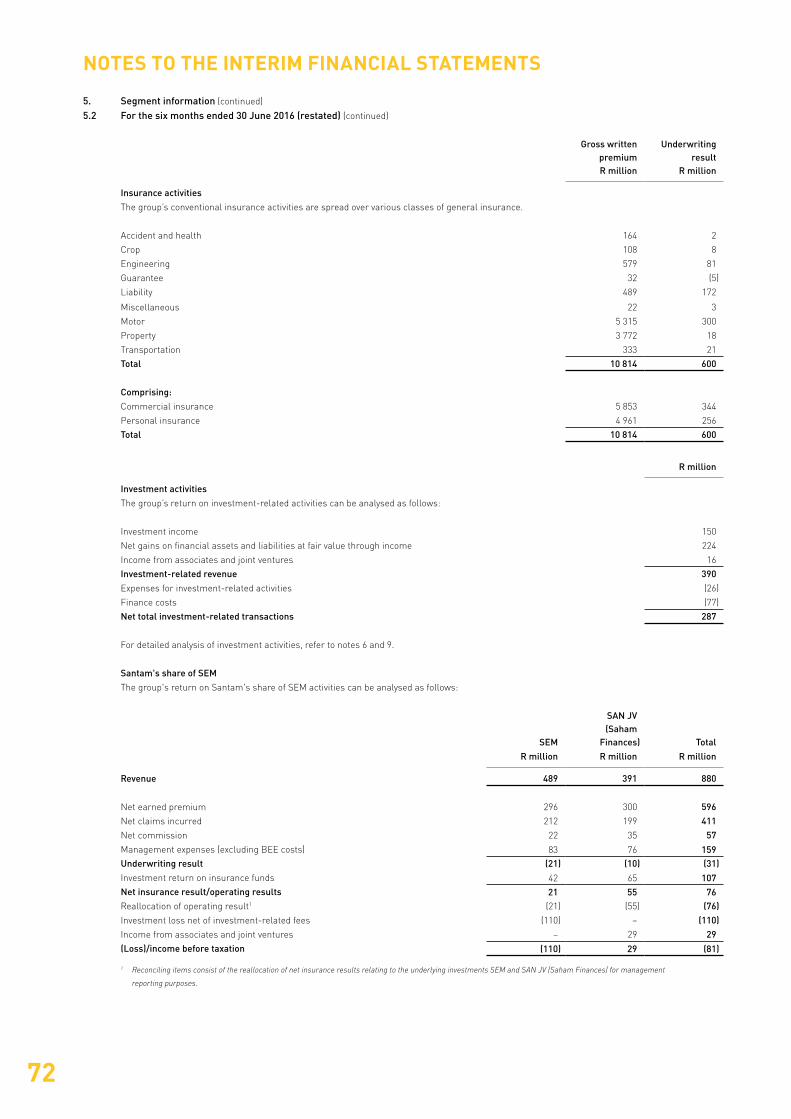

5. Segment information (continued)

5.2 For the six months ended 30 June 2016 (restated) (continued)

Gross writtenpremiumR million

Underwriting result

R million

Insurance activitiesThe group’s conventional insurance activities are spread over various classes of general insurance.

Accident and health 164 2

Crop 108 8

Engineering 579 81

Guarantee 32 (5)

Liability 489 172

Miscellaneous 22 3

Motor 5 315 300

Property 3 772 18

Transportation 333 21

Total 10 814 600

Comprising:Commercial insurance 5 853 344

Personal insurance 4 961 256

Total 10 814 600

R million

Investment activitiesThe group’s return on investment-related activities can be analysed as follows:

Investment income 150

Net gains on financial assets and liabilities at fair value through income 224

Income from associates and joint ventures 16

Investment-related revenue 390 Expenses for investment-related activities (26)

Finance costs (77)

Net total investment-related transactions 287

For detailed analysis of investment activities, refer to notes 6 and 9.

Santam's share of SEMThe group's return on Santam's share of SEM activities can be analysed as follows:

SEM

SAN JV (Saham

Finances) Total R million R million R million

Revenue 489 391 880

Net earned premium 296 300 596 Net claims incurred 212 199 411 Net commission 22 35 57 Management expenses (excluding BEE costs) 83 76 159 Underwriting result (21) (10) (31)Investment return on insurance funds 42 65 107Net insurance result/operating results 21 55 76Reallocation of operating result1 (21) (55) (76)Investment loss net of investment-related fees (110) – (110)Income from associates and joint ventures – 29 29 (Loss)/income before taxation (110) 29 (81)

1 Reconciling items consist of the reallocation of net insurance results relating to the underlying investments SEM and SAN JV (Saham Finances) for management

reporting purposes.

73

NOTES TO THE INTERIM FINANCIAL STATEMENTS

Business activity (continued)

Investment TotalReconciling

and unallocatedIFRSTotal

R million R million R million R million

Revenue 449 28 297 (2 388) 25 909 Net earned premium – 21 240 (1 414) 19 826 Net claims incurred – 13 893 (982) 12 911 Net commission – 2 500 (121) 2 379 Management expenses (excluding BEE costs)2 – 3 637 (369) 3 268 Underwriting result – 1 210 58 1 268 Investment return on insurance funds – 839 (220) 619 Net insurance result – 2 049 (162) 1 887 Other income – 127 – 127Other expenses – (126) – (126)Operating result – 2 050 (162) 1 888 Reallocation of operating result1 – (162) 162 – Investment income/(losses) net of investment-related fees 355 344 – 344 Investment return allocated to cell owners and structured insurance products – (202) – (202)Finance costs (212) (212) – (212)Income from associates including profit on sale 24 67 – 67 Santam BEE costs – – (9) (9)Amortisation and impairment of intangible assets2 – (21) – (21)Income before taxation 167 1 864 (9) 1 855

1 Reconciling items consist of the reallocation of net insurance results relating to the underlying investments SEM and SAN JV (Saham Finances) for management

reporting purposes.

2 Amortisation of computer software included as part of management expenses. Santam’s share of the costs to manage the SEM portfolio of R22 million has been included in

management expenses.

3 Includes other income and expenses not related to underwriting activities.

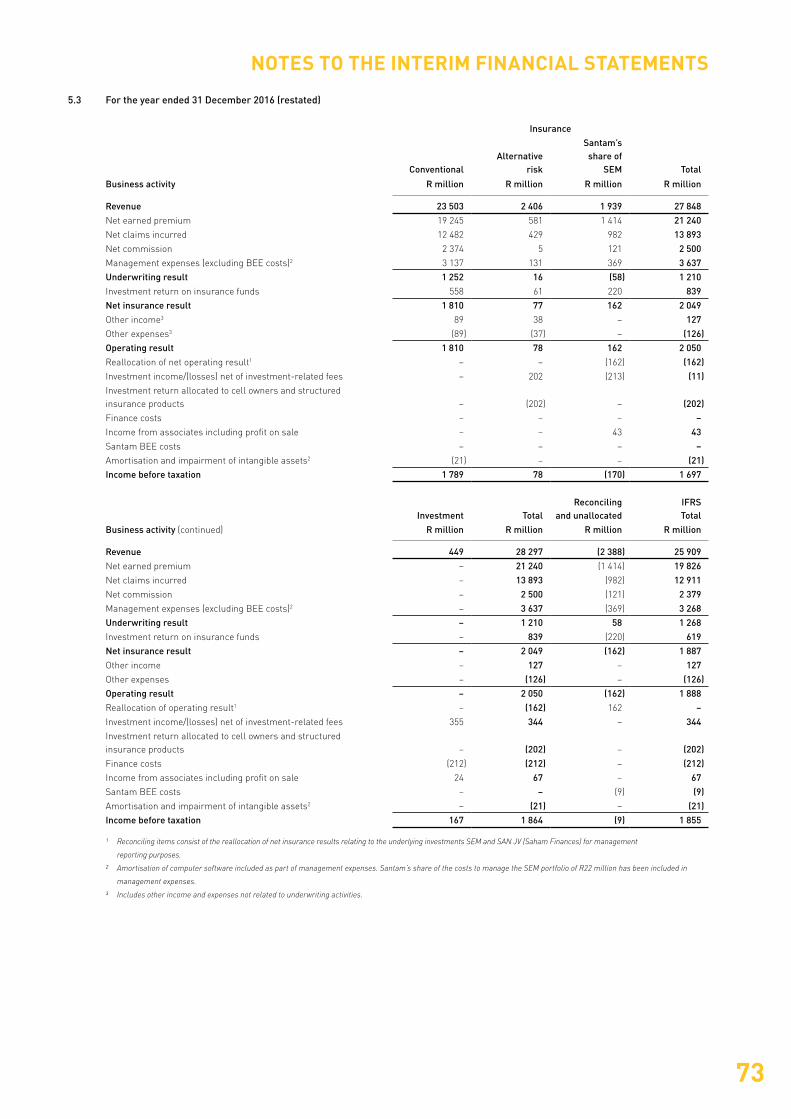

5.3 For the year ended 31 December 2016 (restated)

Insurance

Business activity

ConventionalAlternative

risk

Santam’s share of

SEM Total

R million R million R million R million

Revenue 23 503 2 406 1 939 27 848 Net earned premium 19 245 581 1 414 21 240 Net claims incurred 12 482 429 982 13 893 Net commission 2 374 5 121 2 500 Management expenses (excluding BEE costs)2 3 137 131 369 3 637 Underwriting result 1 252 16 (58) 1 210 Investment return on insurance funds 558 61 220 839Net insurance result 1 810 77 162 2 049 Other income3 89 38 – 127 Other expenses3 (89) (37) – (126)Operating result 1 810 78 162 2 050 Reallocation of net operating result1 – – (162) (162)Investment income/(losses) net of investment-related fees – 202 (213) (11)Investment return allocated to cell owners and structured insurance products – (202) – (202)Finance costs – – – – Income from associates including profit on sale – – 43 43Santam BEE costs – – – – Amortisation and impairment of intangible assets2 (21) – – (21)Income before taxation 1 789 78 (170) 1 697

74

NOTES TO THE INTERIM FINANCIAL STATEMENTS

5. Segment information (continued)

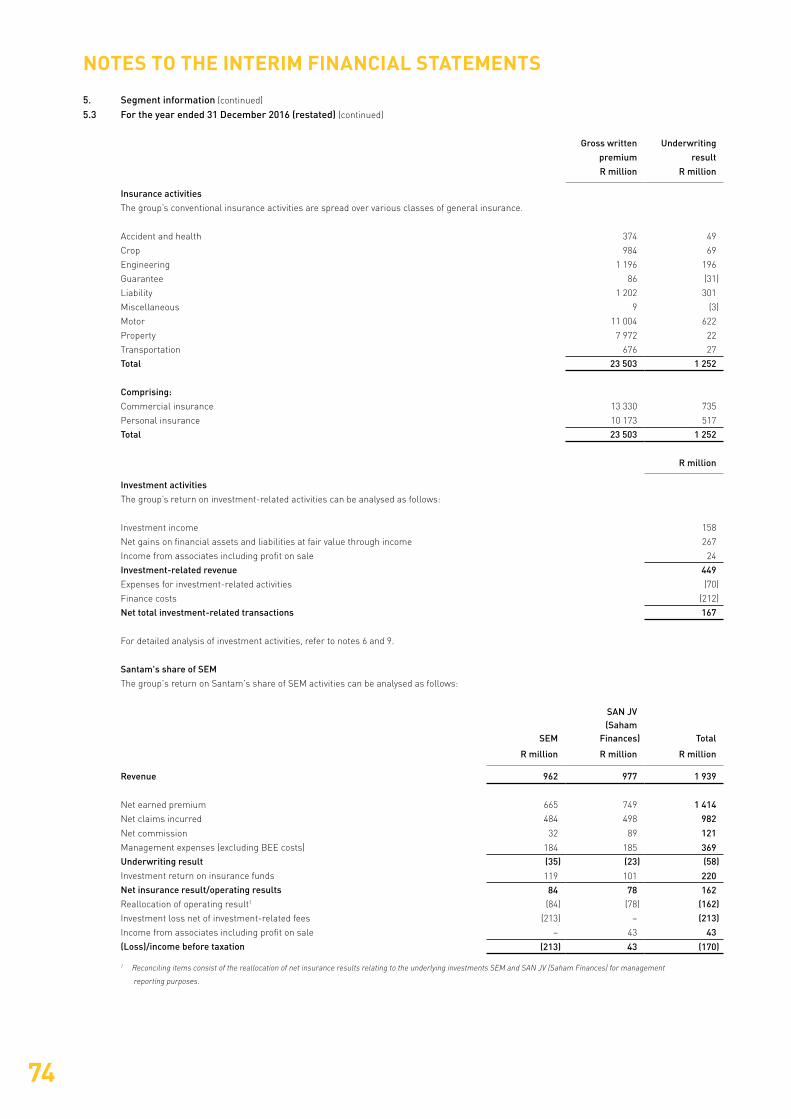

5.3 For the year ended 31 December 2016 (restated) (continued)

Gross written Underwriting premium result R million R million

Insurance activitiesThe group’s conventional insurance activities are spread over various classes of general insurance.

Accident and health 374 49

Crop 984 69

Engineering 1 196 196

Guarantee 86 (31)

Liability 1 202 301

Miscellaneous 9 (3)

Motor 11 004 622

Property 7 972 22

Transportation 676 27

Total 23 503 1 252

Comprising:Commercial insurance 13 330 735

Personal insurance 10 173 517

Total 23 503 1 252

R million

Investment activitiesThe group’s return on investment-related activities can be analysed as follows:

Investment income 158

Net gains on financial assets and liabilities at fair value through income 267

Income from associates including profit on sale 24

Investment-related revenue 449Expenses for investment-related activities (70)

Finance costs (212)

Net total investment-related transactions 167

For detailed analysis of investment activities, refer to notes 6 and 9.

Santam's share of SEMThe group's return on Santam's share of SEM activities can be analysed as follows:

SEM

SAN JV (Saham

Finances) Total

R million R million R million

Revenue 962 977 1 939

Net earned premium 665 749 1 414 Net claims incurred 484 498 982

Net commission 32 89 121 Management expenses (excluding BEE costs) 184 185 369 Underwriting result (35) (23) (58)Investment return on insurance funds 119 101 220Net insurance result/operating results 84 78 162Reallocation of operating result1 (84) (78) (162)Investment loss net of investment-related fees (213) – (213)Income from associates including profit on sale – 43 43 (Loss)/income before taxation (213) 43 (170)

1 Reconciling items consist of the reallocation of net insurance results relating to the underlying investments SEM and SAN JV (Saham Finances) for management

reporting purposes.

75

NOTES TO THE INTERIM FINANCIAL STATEMENTS

Reviewed at Reviewed at Audited at

30 June 2017 30 June 2016 31 Dec 2016

R million R million R million

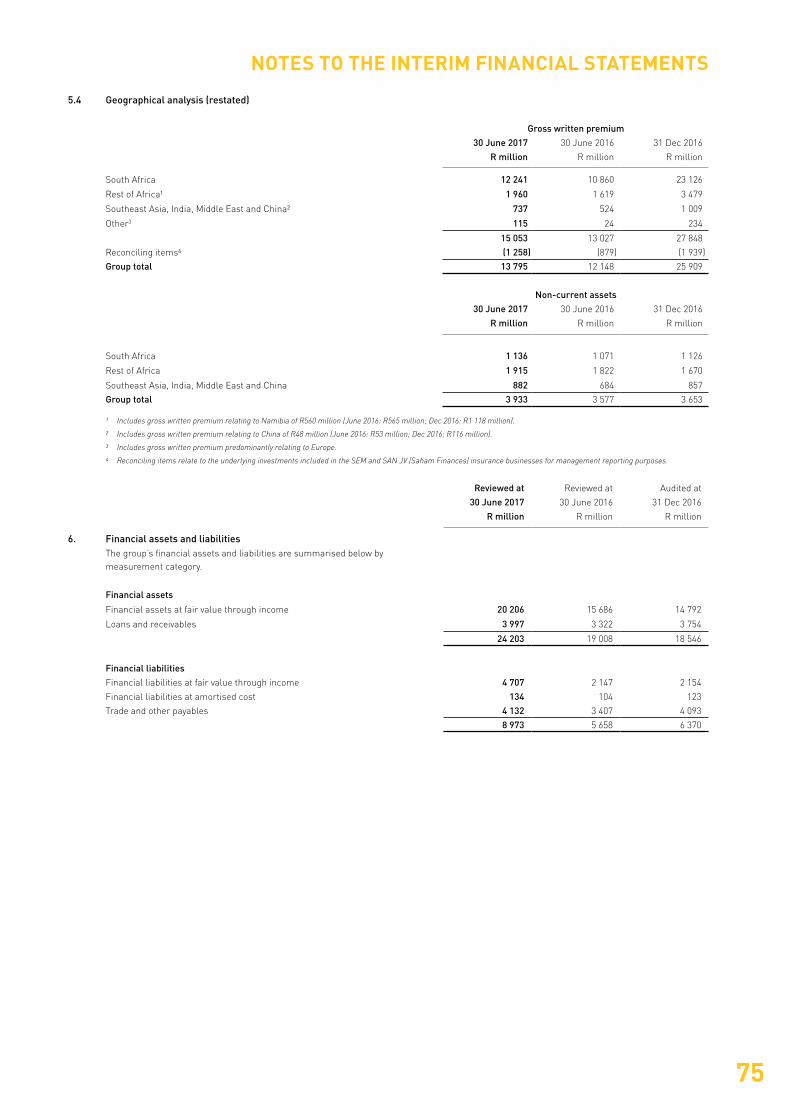

6. Financial assets and liabilitiesThe group’s financial assets and liabilities are summarised below by measurement category.

Financial assets

Financial assets at fair value through income 20 206 15 686 14 792

Loans and receivables 3 997 3 322 3 754

24 203 19 008 18 546

Financial liabilities Financial liabilities at fair value through income 4 707 2 147 2 154

Financial liabilities at amortised cost 134 104 123

Trade and other payables 4 132 3 407 4 093

8 973 5 658 6 370

5.4 Geographical analysis (restated)

Gross written premium 30 June 2017 30 June 2016 31 Dec 2016

R million R million R million

South Africa 12 241 10 860 23 126

Rest of Africa1 1 960 1 619 3 479

Southeast Asia, India, Middle East and China2 737 524 1 009

Other3 115 24 234

15 053 13 027 27 848

Reconciling items4 (1 258) (879) (1 939)

Group total 13 795 12 148 25 909

Non-current assets 30 June 2017 30 June 2016 31 Dec 2016

R million R million R million

South Africa 1 136 1 071 1 126

Rest of Africa 1 915 1 822 1 670

Southeast Asia, India, Middle East and China 882 684 857

Group total 3 933 3 577 3 653

1 Includes gross written premium relating to Namibia of R560 million (June 2016: R565 million; Dec 2016: R1 118 million).

2 Includes gross written premium relating to China of R48 million (June 2016: R53 million; Dec 2016: R116 million).

3 Includes gross written premium predominantly relating to Europe.

4 Reconciling items relate to the underlying investments included in the SEM and SAN JV (Saham Finances) insurance businesses for management reporting purposes.

76

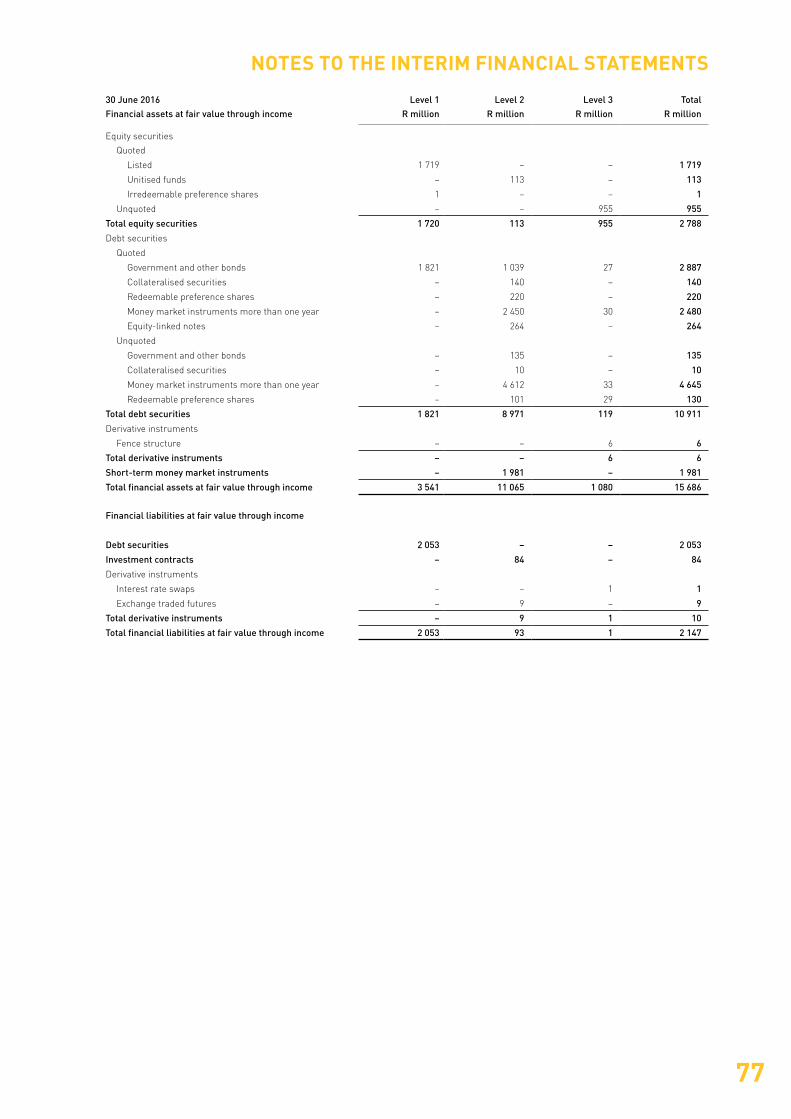

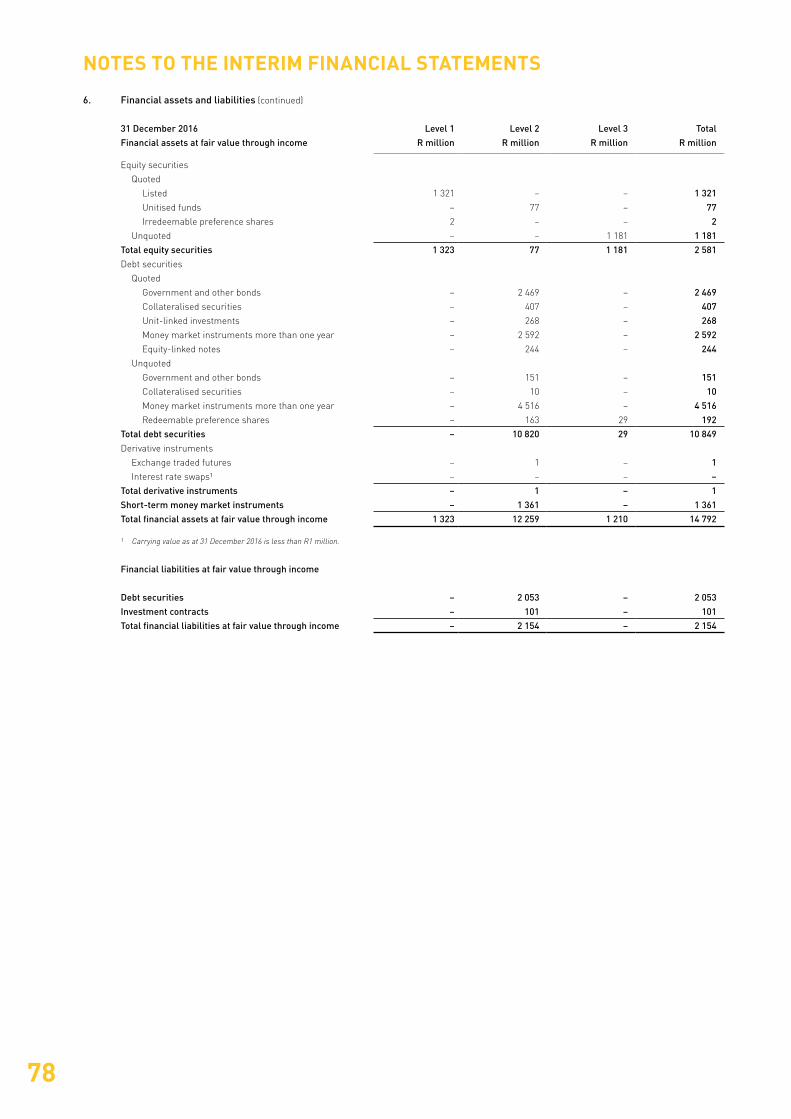

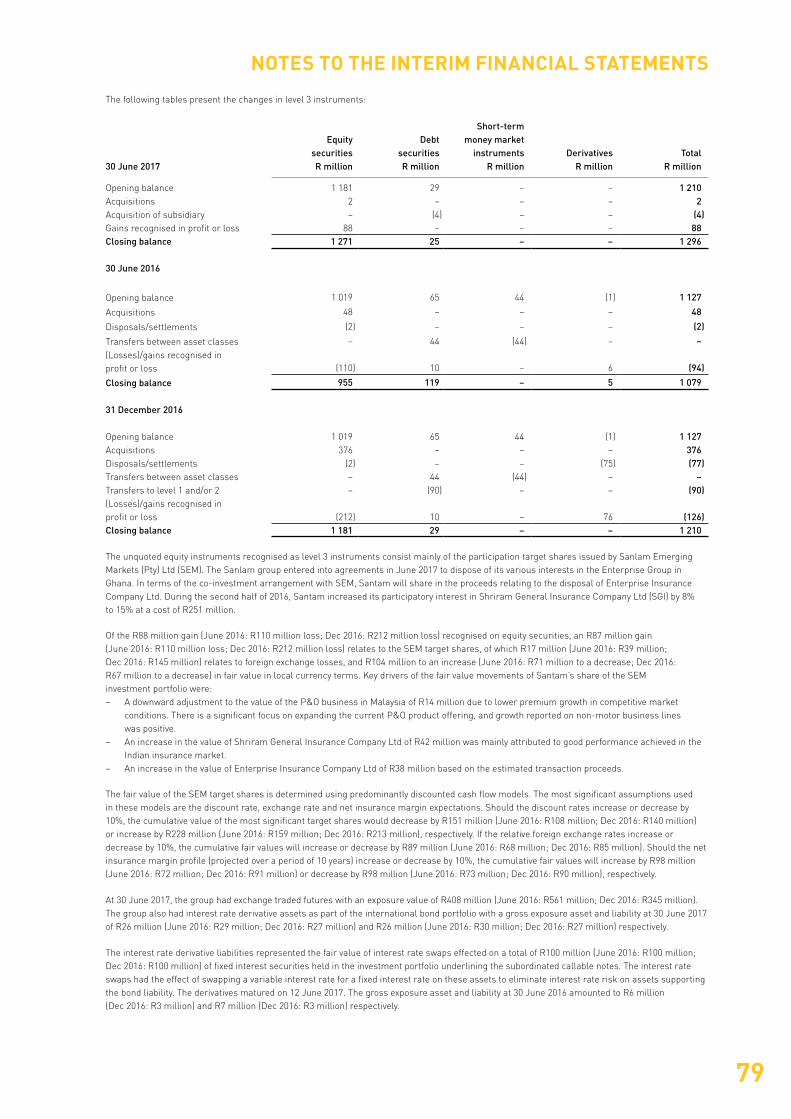

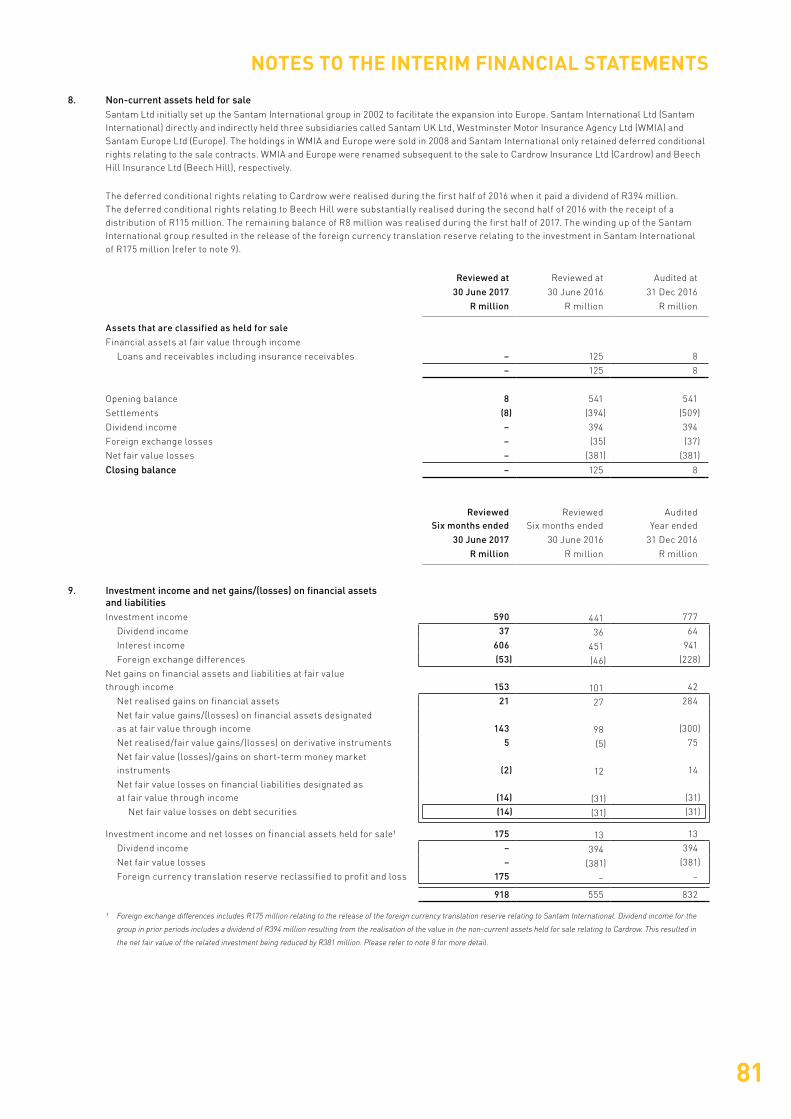

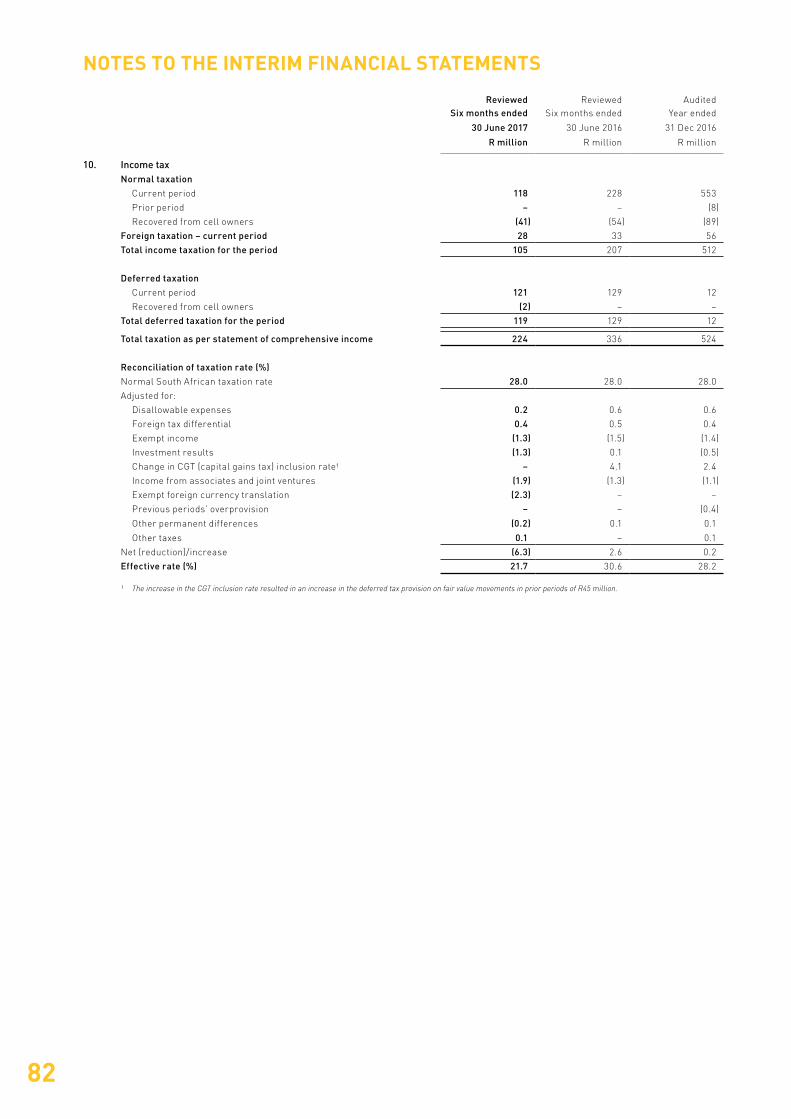

NOTES TO THE INTERIM FINANCIAL STATEMENTS

6. Financial assets and liabilities (continued)