for producer information only. not for use in sales situations income protection sales made easy...

TRANSCRIPT

For Producer Information Only. Not For Use In Sales Situations

INCOME PROTECTION SALES MADE EASY

Individual Disability Insurance

For Producer Information Only. Not For Use In Sales Situations

What you’ll learn today

1. Why you should sell Individual Disability Income (IDI) protection

2. How to simplify the conversation

3. Policy design options and approach techniques

4. Multiple needs of business owners and approach techniques

5. Sales pieces to share with clients

For Producer Information Only. Not For Use In Sales Situations

1 It’s a great door opener.

2Upon a disability, it helps clients pay daily living expenses and bills, including premiums on other insurance products they have with the producer.

3 It helps diversify your portfolio offering and provides attractive compensation.

4 It’s part of a producer’s due diligence.

5Solutions are available in sought-after markets (e.g., business owners and higher-income individuals)

Top Reasons to Sell IDI

For Producer Information Only. Not For Use In Sales Situations

Why people need income protection

4

1 in 4 of today’s 20-year olds will become disabled before retiring.1

The average long-term disability lasts 2.5 years2

50% of Americans would be in financial trouble in one month or less following a disability3

1Social Security Administration Fact Sheet, Feb. 201322010 Gen Re Disability Fact Book 3The Life and Health Foundation for Education (LIFE) survey, conducted by Kelton, April 2012

For Producer Information Only. Not For Use In Sales Situations

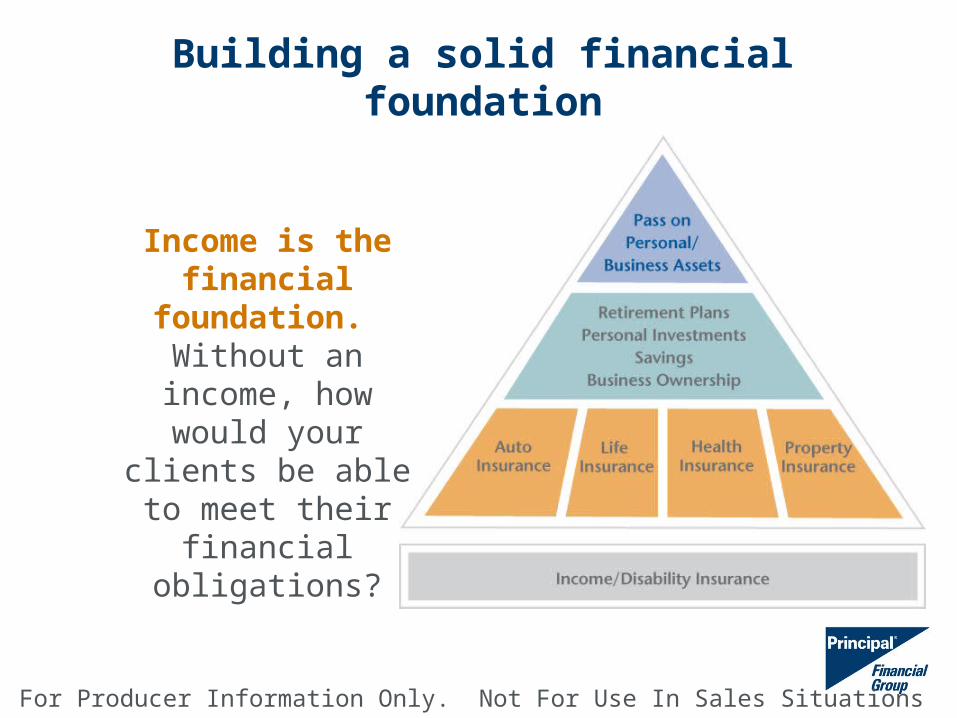

Building a solid financial foundation

Income is the financial foundation.

Without an income, how would your clients be able to meet their financial obligations?

For Producer Information Only. Not For Use In Sales Situations

Who is a likely prospect?

Almost everyone in the working population, but specifically those who:

• Are ages 30 to 50 (typically available to ages 18 to 60)

• Earning a minimum income of $40,000/year

• Are interested in protecting their most important asset – their ability to work and earn an income

• Have other risk and/or protection products with you

For Producer Information Only. Not For Use In Sales Situations

The Income Protection Conversation

• It’s up to you to talk about income protection.– If you don’t, someone else will.

Compensation potential

Producers who take a comprehensive approach with clients earn 30% more than those who do not.3

Marketpotential

67% of the private sector workforce has no long-term disability insurance.1

Nearly 50% of those who look into income protection, after being approached about it, buy some type of policy. 2

1 Social Security Administration, Fact Sheet, March 20112 LIMRA MarketFacts Quarterly, 2012.3 2010 Principal Life Insurance Company retail sales data

For Producer Information Only. Not For Use In Sales Situations

Approach techniques

I Can’t Afford It

• Premium coffee a day• Date night• Lunch every day• Smart phone

Why Do I Need It?• Illnesses, not accidents• Sharing a real story• Divide your income in half

I’d Never Use It• Life insurance • Auto insurance• Home insurance

www.principal.com/incomeprotection

For Producer Information Only. Not For Use In Sales Situations

Policy Design Options

Sell the premium – Typically 1% to 3% of gross income

Sell the product– Have the proposal ready and work off the proposal– Explain the elimination period and benefit period (and how they

can be used to customize the policy)– Policy pays in three ways

• Total Disability• Partial Disability• Catastrophic Disability

– Guaranteed benefits and premium– Ability to add riders to fit their specific needs – inflation protection,

ability to return to work part-time, etc.

For Producer Information Only. Not For Use In Sales Situations

$5,000/month benefit replaces 60% of $100,000 annual income

For 1.94% of annual income

For Producer Information Only. Not For Use In Sales Situations

PolicyComprehensive

CoverageModerate Coverage

Basic Coverage

Monthly Benefit $5,000 (maximum available)

$3,000 $1,200

Total Monthly Premium

Male $138.73 $83.24 $33.30

Female $207.86 $124.71 $49.89

Assumptions: Colorado resident, HH 750 policy, $100,000/annual income, 5A occupation class, Nonsmoker, age 35, 90 day Elimination Period, To Age 65 Benefit and Your Occupation Period, Residual Disability rider

Different coverage for different needs and budgets

For Producer Information Only. Not For Use In Sales Situations

• Quick and easy application process – Up to $4,000/month benefit for single-life

– Up to $6,000/month benefit for multi-life

• No routine medical requirements1

• No financial documentation required (If client earns under $150,000/year2)

• Underwriting decision within 48 hours (Once the application and TeleApp are completed and received)

1No blood, urine, exams, EKGs or APSs required unless a significant medical condition is reported by MIB, significant medical information is obtained from the TeleApp or other available information, or any other disability coverage has been issued or applied for on a nonmedical basis. Applications could be rated, ridered or declined based on all underwriting information available; this is not a guaranteed issue program. Urine/HIV test is required in Maine. Subject to Issue & Participation limits and minimum premium requirement. Combined Simplified DI and Simplified OE benefits cannot exceed $10,000/month.2Financial documentation required for certain occupations regardless of income.

Approach Technique #1Simplified Underwriting Program

Meet your clients’ income protection needs faster

For Producer Information Only. Not For Use In Sales Situations

Approach Technique #2Benefit Update rider

• Issue ages: 18 to 55• Available to all occupation classes • No cost rider — Provides benefit review opportunity every three

years without medical requirements1

• Two advance option triggers:– Losing group disability insurance– Having at least a 50% sustainable increase in income

• All definitions, discounts, provisions and current rates (at attained age) of the original policy apply

• No cap2 or age restrictions for benefit increases • To keep the BU rider inforce, the client must accept 50% of the

BU offer

1 – Advanced Options available every three-year period for Individual DI insurance 2 – Up to available Issue & Participation limits.

For Producer Information Only. Not For Use In Sales Situations

Approach Technique #2 continuedBenefit Update rider

Year Annual Income

Monthly Benefit Total

123

$90,000$95,000

$120,000

$4,750$4,940$5,750

45

6

$125,000$130,000

$160,000

$5,980$6,220

$7,350

789

$165,000$170,000

$195,00

$7,650$7,950$8,950

101112

$200,0000$205,000$250,00

$9,300$9,675$11,450

As your client’s income increases, so does the potential for BU increases – without evidence of medical insurability.

Example of how benefits can grow

For Producer Information Only. Not For Use In Sales Situations

Approach Technique #3Offer DI and DI Retirement Security together

Disability occurs

Begin receiving traditional DI insurance benefits

DI Retirement Security benefits paid to trust3

Begin receiving assets from trust

Elimination period satisfied

To Age 65

Funds diminish2

To Age 67

Trust assets are distributed as retirement income and continue until the funds are depleted.2

If you become disabled,1 monthly DI benefits are paid to you and the trust.

1 Assumes To Age 65 Benefit and Your Occupation periods. 2׀ Any remaining assets go to your estate if you die while receiving benefits. 3׀ DI Retirement Security is issued as a non-cancelable, guaranteed renewable, individual disability income insurance policy. It is not a pension or retirement program or a substitute for such a program. Retirement Security is not available for government employees, individuals with Group LTD coverage that includes a “retirement supplement” or anyone who is over insured based on Principal Life’s current Issue and Participation guidelines. It may not be available or the benefit amount may be reduced for certain occupations if there is existing DI coverage with lifetime benefits. Additional underwriting guidelines may apply. Invested based on risk tolerance.

For Producer Information Only. Not For Use In Sales Situations

Multiple Needs of Business Owners

Solutions for Business Owners and Employee Benefit Needs

Business ProtectionOverhead Expense (OE)

Business Loan Protection (BLP) Rider1

Exit PlanningDisability Buy-Out (DBO)

For Producer Information Only. Not For Use In Sales Situations

Approach Technique #4More Disability Coverage, Less Cost

20% Multi-Life Discount

Assumptions: CO residents, non-smoker, 4A occupation classesDI: 90 day Elimination Period, To Age 65 Your Occupation and Benefit PeriodOE: 30 day Elimination Period, 12 month benefit factorKP: 180 day Elimination Period, lump sum benefit

For Producer Information Only. Not For Use In Sales Situations

• Informal Business Valuation– Provides the business owner with an

informal valuation of his/her business using five common valuation methods

– Conducted by team of CPAs and consultants

• Buy-Sell Agreement Review– Conducted to ensure Buy-Sell

agreement is effective and properly funded. Any gaps can mean sales opportunities for you.

– Conducted by team of Principal Life CPAs and attorneys

Approach Technique #5FREE Business Planning Services

For Producer Information Only. Not For Use In Sales Situations

Get Started Today

• Get to know the market

• See the tools available at www.principal.com/TargetBusinessOwners

• Meet with business owners; use the comprehensive disability fact finder

• Offer complementary business planning services

• Identify products and solutions

For Producer Information Only. Not For Use In Sales Situations

Sales Pieces to Share with Clients

• Principal Life has tools available to cover the top three objections:

“I won’t need it – I won’t get disabled”

“I can’t afford it” or “It’s not worth it.”

“I have other coverage so I’m protected”

For Producer Information Only. Not For Use In Sales Situations

Use? “I’ll Never Use It”

2 – The Principal Financial Well-Being Index, First Quarter 2013. | 3 – Data from model year introduction 2008 through July 2010, Highway Loss Data Institute. | 4 – Data from ISO, a Verisk Analytics Company. | 5 – Average premium for 2009, National Association of Insurance Commissioners. | 6 – Average premium among top Individual DI insurance carriers (Principal, MetLife, Standard, Guardian and Ameritas) for $1,000/month benefit, 45 year-old male, Colorado resident, non-smoker, $60,000 annual income, To age 65 benefit and Your Occupation periods, 90-day elimination period, non-cancelable. | 7 – $30,000 is the total payout of a $1,000/month benefit policy claim that pays for 2 ½ years, the average long-term disability claim length (2010 Gen Re Fact Book). | 8 – The policy offers the potential to pay ongoing monthly benefits until the end of the benefit period; To age 65 or 67 benefit period is the most common

For Producer Information Only. Not For Use In Sales Situations

Which option would you prefer?

PLAN A PLAN B

Annual salary$100,000

if working (before taxes)

Annual salary$98,600*

if working (before taxes)

$0Income while too sick or hurt to work

$60,000*Income while too sick or hurt to work from

your DI insurance policy (after taxes)

• If you become too sick or hurt to work tomorrow, what is your Plan B?

• Would you rely on co-workers to hold a fund-raiser for you?

• Plan ahead with income protection.

*100,000 less $1,400 in hypothetical annual disability income insurance premiums. Premiums and $5,000 monthly benefit amount depend on various factors. Your local representative can illustrate the exact amount you’re eligible for based on current underwriting guidelines. This a hypothetical example only.

For Producer Information Only. Not For Use In Sales Situations

Individual DI insurance can protect more of your

client’s income

Full paycheck. Healthy and working.

Group LTD benefits before taxes

Group LTD benefits after taxes

For the cost of 1 to 3 pennies…

Group coverage is a great start, but often not enough

For Producer Information Only. Not For Use In Sales Situations

The Cost of Doing Nothing

What’s more costly?• Purchasing an affordable DI policy today and

being protected in the event of the unexpected? • Incurring a disability and no longer having an

income?

• Consumers spend $4/day or $120/month on coffee.1

• For half that amount, about $56/month, they could protect their income2

1 –National Coffee Drinking Trends 2010, National Coffee Association – average cost for a brewed cup of coffee is $1.38 and consumers drink an average of 3.1 cups a day. | 2 - Male, Colorado resident, $60,000 annual income, $1,350 monthly benefit, To Age 65 Benefit Period and Your Occupation Period, non-smoker, Residual and Recovery Disability Benefit rider, 90-day elimination period, 4A occupation class.

For Producer Information Only. Not For Use In Sales Situations

Questions?

Insurance issued by Principal Life Insurance Company a member of thePrincipal Financial Group, Des Moines, IA 50392.

Disability insurance has exclusions and limitations. For costs and complete details of the coverage, contact your Principal Life Financial Representative.

DI 2298| 2778042009