for personal use only - asx · diagnostic imaging in australia • diagnostic health services...

TRANSCRIPT

VICTORIA’S FASTEST GROWING DIAGNOSTIC IMAGING PROVIDER March 2012

1

For

per

sona

l use

onl

y

DISCLAIMER & IMPORTANT NOTICE

• This presentation does not constitute investment advice. Neither this presentation nor the information contained in it constitutes an offer, invitation, solicitation or recommendation in relation to the purchase or sale of shares in any jurisdiction.

• Shareholders should not rely on this presentation. This presentation does not take into account any person's particular investment objectives, financial resources or other relevant circumstances and the opinions and recommendations in this presentation are not intended to represent recommendations of particular investments to particular persons. All securities transactions involve risks, which include (among others) the risk of adverse or unanticipated market, financial or political developments.

• The information set out in this presentation does not purport to be all inclusive or to contain all the information which its recipients may require in order to make an informed assessment of Capitol Health. You should conduct your own investigations and perform your own analysis in order to satisfy yourself as to the accuracy and completeness of the information, statements and opinions contained in this presentation.

• To the fullest extent permitted by law, the Company does not make any representation or warranty, express or implied, as to the accuracy or completeness of any information, statements, opinions, estimates, forecasts or other representations contained in this presentation. No responsibility for any errors or omissions from this presentation arising out of negligence or otherwise is accepted.

• This presentation may include forward looking statements. Forward looking statements are only predictions and are subject to risks, uncertainties and assumptions which are outside the control of Capitol Health. These risks, uncertainties and assumptions include commodity prices, currency fluctuations, economic and financial market conditions in various countries and regions, environmental risks and legislative, fiscal or regulatory developments, political risks, project delay or advancement, approvals and cost estimates. Actual values, results or events may be materially different to those expressed or implied in this presentation. Given these uncertainties, readers are cautioned not to place reliance on forward looking statements.

• Any forward looking statements in this presentation speak only at the date of issue of this presentation. Subject to any continuing obligations under applicable law and the ASX Listing Rules, Capitol Health does not undertake any obligation to update or revise any information or any of the forward looking statements in this presentation or any changes in events, conditions or circumstances on which any such forward looking statement is based.

2

For

per

sona

l use

onl

y

ABOUT CAPITOL HEALTH

Second- largest network of

diagnostic imaging clinics in Victoria

Organic and acquisitive growth

strategy – IM Medical acquisition

35 diagnostic

imaging clinics

Full service offering – X rays

through to nuclear imaging

400k +

procedures conducted pa

Affordable billing revenue model

300+

employees and contractors

Listed on the ASX (stock code: CAJ)

Market Cap: A$15.2million

Only pure diagnostic imaging

company on the ASX

3

For

per

sona

l use

onl

y

INVESTMENT CASE

• Strong and growing state footprint • Highly focused strategy and ingrained

commercial culture • Dynamic and flexible management

style • Regulatory environment supports

growth strategy • Attractive offering for customers and

radiologists/partners • Defensive revenue base – healthcare

and majority bulk billing model • Highly scalable & low cost commercial

model • Consistently strong profitability • Significantly undervalued relative to

peers

Market Cap: A$15.2million

Share price: $0.05

(As of 9 March 2012)

Ordinary shares: 303.7m

(As of 9 March 2012)

Options: 25.3m

(Exp 30 April 2012)

Directors John Conidi, Managing Director Dominik Kucera, Executive Director &CFO Steven Sewell, Non-Executive Director Andrew Harrison, Non-Executive Director

4

For

per

sona

l use

onl

y

DIAGNOSTIC IMAGING IN AUSTRALIA

• Diagnostic health services provide information about diseases and other physical ailments

• Australian diagnostic imaging market was $2.3bn in 2011

• Market growth expected to average 4% p.a. over next five years

• Key growth drivers: – Population growth – Ageing population – Increasing focus on early detection and

illness prevention – Technological improvements in the

accuracy and capabilities of imaging techniques

5

For

per

sona

l use

onl

y

INCREASING SHARE OF VIC MARKET

• Growth strategy is both organic and acquisitive

• Recent acquisition of IM Medical’s diagnostic imaging business further increases Capitol’s share of the Victorian market

• Market share growth expected to accelerate going forward

-10

-5

0

5

10

15

20

25

30

2009/10 2010/11

Primary Health (national) Sonic Healthcare (national) Capitol Health (Victoria)

Capitol’s revenue is growing at a faster rate than its competitors

% change in Diagnostic Imaging Revenue

6

For

per

sona

l use

onl

y

Acquisition of IM Medical’s diagnostic imaging business in exchange for the issue of CAJ ordinary shares

Five additional diagnostic imaging clinics in Melbourne

IM MEDICAL ACQUISITION

Benefits to Capitol Health

– Establishes Capitol Health’s position

as the second largest diagnostic

imaging clinic network in Victoria

– Newly acquired sites expected to add

~ 15% to FY 2012 operating revenue

– Shares issued to IM Medical will be

distributed to IM shareholders,

expanding the share register

7

For

per

sona

l use

onl

y

VISION AND STRATEGY

VISION:

to be the leading “community-based” diagnostic imaging provider in Victoria, delivering consistently strong shareholder returns

STRATEGY: 1. Provide superior offering to Patients, Radiologists and

Referrers 2. Clear business and geographical focus 3. Low cost delivery model supported by scalable IT

infrastructure backbone Underpinned by:

• Commercially focused team with a deep market understanding

• Dynamic and flexible management style

8

For

per

sona

l use

onl

y

CHANGES TO THE REGULATORY ENVIRONMENT

Changes to the 2011/12 Federal Health/Medicare Budget announced: • No changes to Medicare Rebates before

Nov 2013 at the earliest • Medicare benefits to be linked to the age

of equipment used • Government expects no change in pool of

funds to service Medicare benefits for Diagnostic Imaging

• Introduction of direct GP referrals for MRI • Full or partial licensing of all existing

unlicensed MRI’s in place, under installation or ordered as at budget time

9

For

per

sona

l use

onl

y

OPENS OPPORTUNITIES FOR CAPITOL

• Market consolidation to accelerate: – Capitol positioned as a natural consolidator with an

industry low cost structure – Proven track record of acquiring and integrating

diagnostic imaging businesses

• Radiologists without MRI capabilities likely to be shaken out of the market: – Capitol has significant MRI capabilities and is well

positioned to gain market share

• Medicare benefits to be linked to age of equipment – Significant recent investment by Capitol to upgrade

equipment – 5 MRI’s in place or on order – All machines licensed or eligible for licenses and

located in in commercial premises

• Capitol is an efficient operator with track record of strong profitability on bulk billing model

10

For

per

sona

l use

onl

y

POSES CHALLENGES FOR OTHERS

• Shift towards increased bulk billing expected: – Cost structure for competitors will

not support economic returns

• Providers without MRIs will suffer: – No additional MRIs will be issued

licenses – Rebate rates decreased for CT scans – Increase in referrals to MRI scans in

place of other technologies

Result = reduced industry supply / accelerated

consolidation

11

For

per

sona

l use

onl

y

ATTRACTIVE OFFERING

CUSTOMER PROPOSITION

Referring GPs

• Market leading information systems – lifetime information storage

• Quick and efficient reporting Patients • Low “bulk billing” pricing • Superior service & leading-edge equipment

RADIOLOGIST PROPOSITION

• Avoid ongoing earnings decline from regulatory reform

• Partner with CAJ, take advantage of our superior commercial model and significantly increase earnings

12

For

per

sona

l use

onl

y

DEFENSIVE REVENUE BASE

• Proven defensibility of healthcare spend

– Australian health sector as a whole grows faster than the Australian economy

• Current industry shift towards bulk billing

• Capitol Health protected by: – 98% bulk billing price offering

(regulations prohibit pricing below this level)

– Lowest cost operating position (competitors unable to compete on a bulk billing pricing model)

13

For

per

sona

l use

onl

y

HIGHLY-SCALABLE & LOW COST COMMERCIAL MODEL

• Commercial model underpins growth strategy

• Highly-scalable : – Significant recent investment in IT systems

and high-technology equipment

– IT platform would facilitate significant clinic expansion

Result = margins and profits will expand significantly as the clinic network expands

• Low cost: – Ingrained commercial culture

– Ongoing margin growth

Result = radiologists driven to partner with CAJ to leverage model and increase earnings

14

For

per

sona

l use

onl

y

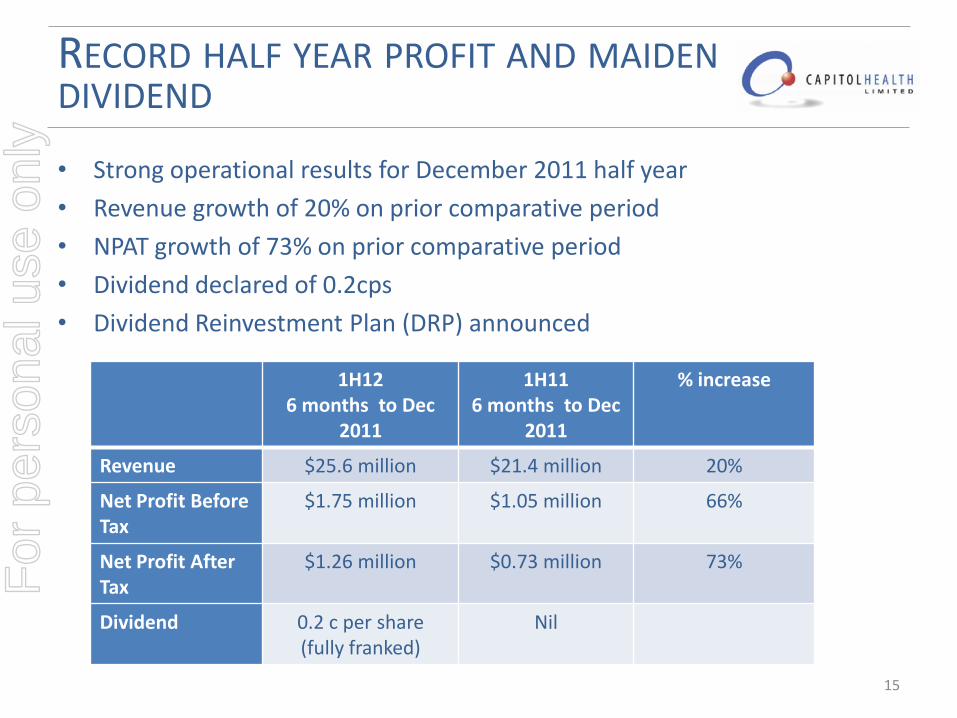

RECORD HALF YEAR PROFIT AND MAIDEN DIVIDEND

• Strong operational results for December 2011 half year

• Revenue growth of 20% on prior comparative period

• NPAT growth of 73% on prior comparative period

• Dividend declared of 0.2cps

• Dividend Reinvestment Plan (DRP) announced

1H12 6 months to Dec

2011

1H11 6 months to Dec

2011

% increase

Revenue $25.6 million $21.4 million 20%

Net Profit Before Tax

$1.75 million $1.05 million 66%

Net Profit After Tax

$1.26 million $0.73 million 73%

Dividend 0.2 c per share (fully franked)

Nil

15

For

per

sona

l use

onl

y

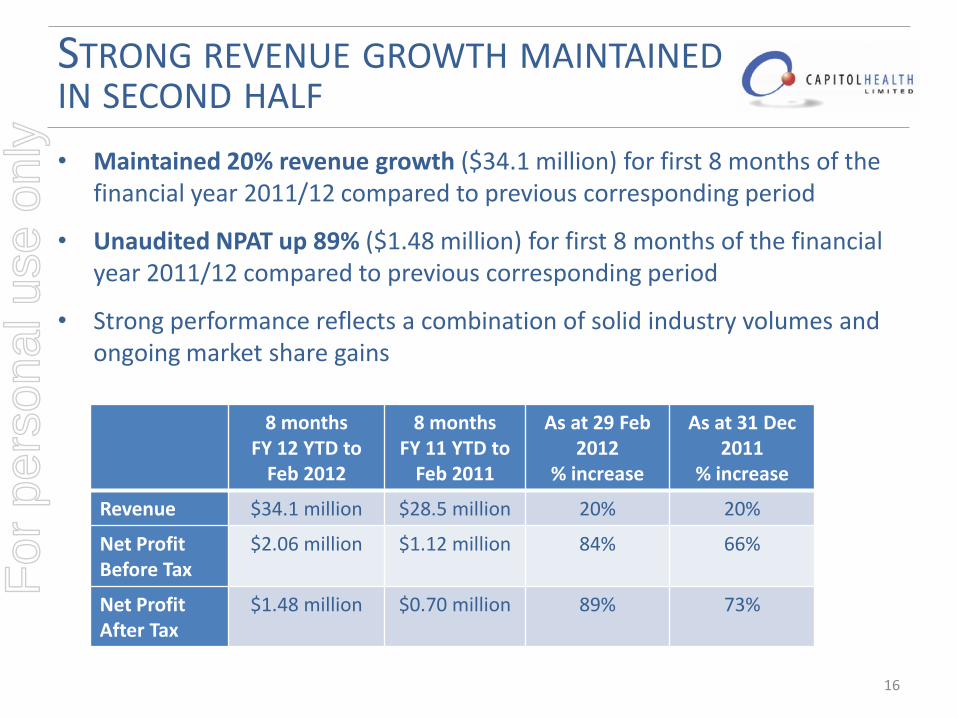

STRONG REVENUE GROWTH MAINTAINED IN SECOND HALF

• Maintained 20% revenue growth ($34.1 million) for first 8 months of the financial year 2011/12 compared to previous corresponding period

• Unaudited NPAT up 89% ($1.48 million) for first 8 months of the financial year 2011/12 compared to previous corresponding period

• Strong performance reflects a combination of solid industry volumes and ongoing market share gains

16

8 months FY 12 YTD to

Feb 2012

8 months FY 11 YTD to

Feb 2011

As at 29 Feb 2012

% increase

As at 31 Dec 2011

% increase

Revenue $34.1 million $28.5 million 20% 20%

Net Profit Before Tax

$2.06 million $1.12 million 84% 66%

Net Profit After Tax

$1.48 million $0.70 million 89% 73%

For

per

sona

l use

onl

y

0

0.2

0.4

0.6

0.8

1

1.2

1.4

0

5

10

15

20

25

30

35

40

45

50

2008 2009 2010 2011 2012

CONSISTENT PROFITABILITY GROWTH

Note: in 2009 a one-off non-cash goodwill impairment charge has been deducted to better reflect underlying profit

All in $m

119.6% 19.9%

28.8%

Annual Revenue Increase (%)

17

19.6% (1H)

1H NPAT

FY NPAT

DI Operations commenced

in 2008

For

per

sona

l use

onl

y

EXCITING YEAR AHEAD

• Consolidate acquisition of IM Medical’s clinics into Capitol Health network

• Strong ongoing organic growth

• Further growth through acquisitions expected

• Year to date results announced confirm growth trajectory of the Company

18

For

per

sona

l use

onl

y

INVESTMENT CASE

• Strong and growing state footprint

• Highly focused strategy and ingrained commercial culture

• Growth strategy is optimised for the Regulatory Environment

• Superior offering for Patients, Radiologists and Referrers

• Defensive revenue base – healthcare and bulk billing model

• Highly scalable & low cost commercial model

• Consistently strong profitability

• Significantly undervalued relative to peers

19

For

per

sona

l use

onl

y

CONTACT DETAILS

John Conidi, Managing Director Level 1

952 Mt Alexander Road Essendon VIC 3040

P: +61 (0) 3 9348 3333 F: +61 (0) 3 9370 0336

Email: [email protected]

www.capitolhealth.com.au

20

For

per

sona

l use

onl

y