for personal use only - asx · 2011. 2. 22. · yanzhou coal acquires felix resources proposed...

TRANSCRIPT

Road Show PresentationCascade Coal – A Company Making Transaction

23 February 2011

For

per

sona

l use

onl

y

Page 22

� Transaction Overview

White Energy’s Acquisition of Cascade Coal

� Strategic Rationale

Cascade Coal - A Company Making Transaction

� Combination Rationale

White Energy and Cascade Coal Combined

� Detailed Asset Overview

The Cascade Coal Assets

For

per

sona

l use

onl

y

Page 33

Why Cascade Coal ?

1Company-Making Transaction, Transforming White Energy into a Leading Mid-Tier Coal Company

2Rare Opportunity to Acquire a Large, Scarce, Export Quality, Open-Cut Coal Mining Asset in NSW

3Purchase Price of A$486m for 100% of the Equity in Cascade Coal is “Fair and Reasonable” and at the Lower End of IE Valuation Range of A$459m to A$587m

4Mt. Penny is Competitive with and Superior to Other Comparable Australian Thermal Coal Assets

5Mt. Penny Open-Cut 1 is Being Fast Tracked to Production in 2013, and is well positioned with Existing Rail Connection to Port of Newcastle

6Board/Management with Demonstrated Ability to Bring Coal Assets into Production – Moolarben, Ashton, Ulan and UnitedF

or p

erso

nal u

se o

nly

Page 44

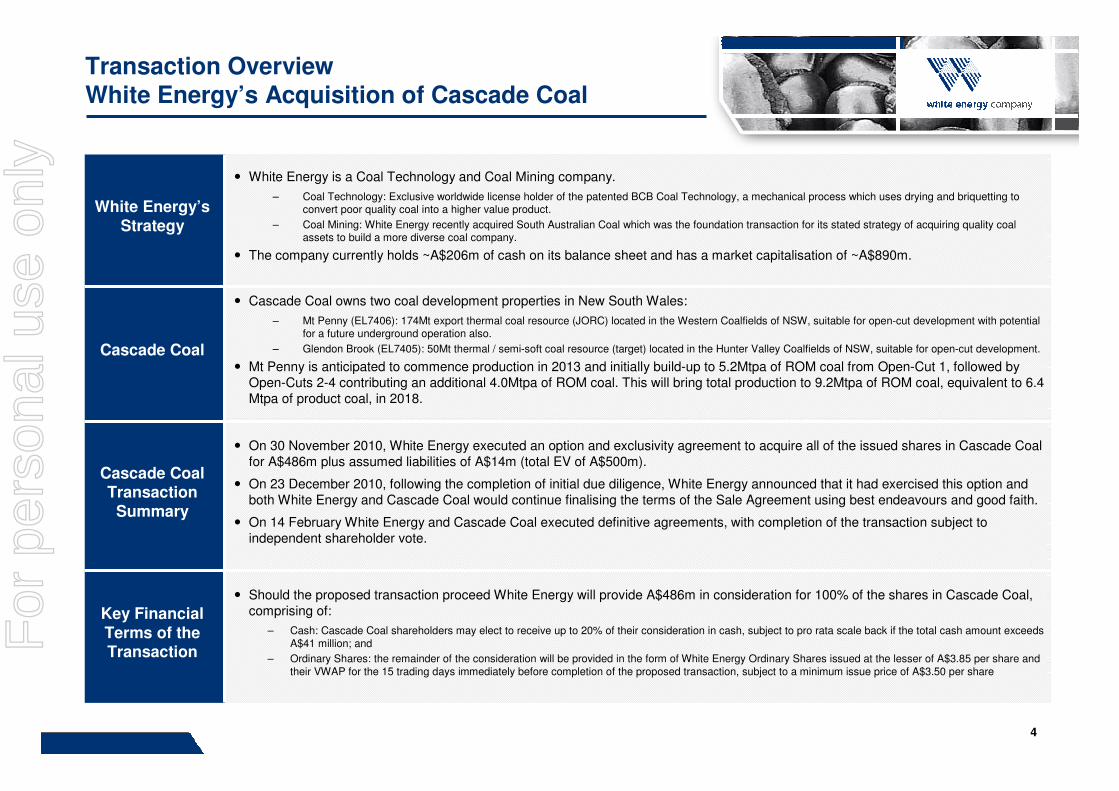

Transaction OverviewWhite Energy’s Acquisition of Cascade Coal

White Energy’s Strategy

� White Energy is a Coal Technology and Coal Mining company.

– Coal Technology: Exclusive worldwide license holder of the patented BCB Coal Technology, a mechanical process which uses drying and briquetting to convert poor quality coal into a higher value product.

– Coal Mining: White Energy recently acquired South Australian Coal which was the foundation transaction for its stated strategy of acquiring quality coal assets to build a more diverse coal company.

� The company currently holds ~A$206m of cash on its balance sheet and has a market capitalisation of ~A$890m.

Cascade Coal

� Cascade Coal owns two coal development properties in New South Wales:

– Mt Penny (EL7406): 174Mt export thermal coal resource (JORC) located in the Western Coalfields of NSW, suitable for open-cut development with potential for a future underground operation also.

– Glendon Brook (EL7405): 50Mt thermal / semi-soft coal resource (target) located in the Hunter Valley Coalfields of NSW, suitable for open-cut development.

� Mt Penny is anticipated to commence production in 2013 and initially build-up to 5.2Mtpa of ROM coal from Open-Cut 1, followed by Open-Cuts 2-4 contributing an additional 4.0Mtpa of ROM coal. This will bring total production to 9.2Mtpa of ROM coal, equivalent to 6.4 Mtpa of product coal, in 2018.

Cascade Coal Transaction

Summary

� On 30 November 2010, White Energy executed an option and exclusivity agreement to acquire all of the issued shares in Cascade Coal for A$486m plus assumed liabilities of A$14m (total EV of A$500m).

� On 23 December 2010, following the completion of initial due diligence, White Energy announced that it had exercised this option and both White Energy and Cascade Coal would continue finalising the terms of the Sale Agreement using best endeavours and good faith.

� On 14 February White Energy and Cascade Coal executed definitive agreements, with completion of the transaction subject to independent shareholder vote.

Key Financial Terms of the Transaction

� Should the proposed transaction proceed White Energy will provide A$486m in consideration for 100% of the shares in Cascade Coal, comprising of:

– Cash: Cascade Coal shareholders may elect to receive up to 20% of their consideration in cash, subject to pro rata scale back if the total cash amount exceeds A$41 million; and

– Ordinary Shares: the remainder of the consideration will be provided in the form of White Energy Ordinary Shares issued at the lesser of A$3.85 per share and their VWAP for the 15 trading days immediately before completion of the proposed transaction, subject to a minimum issue price of A$3.50 per share

For

per

sona

l use

onl

y

Page 55

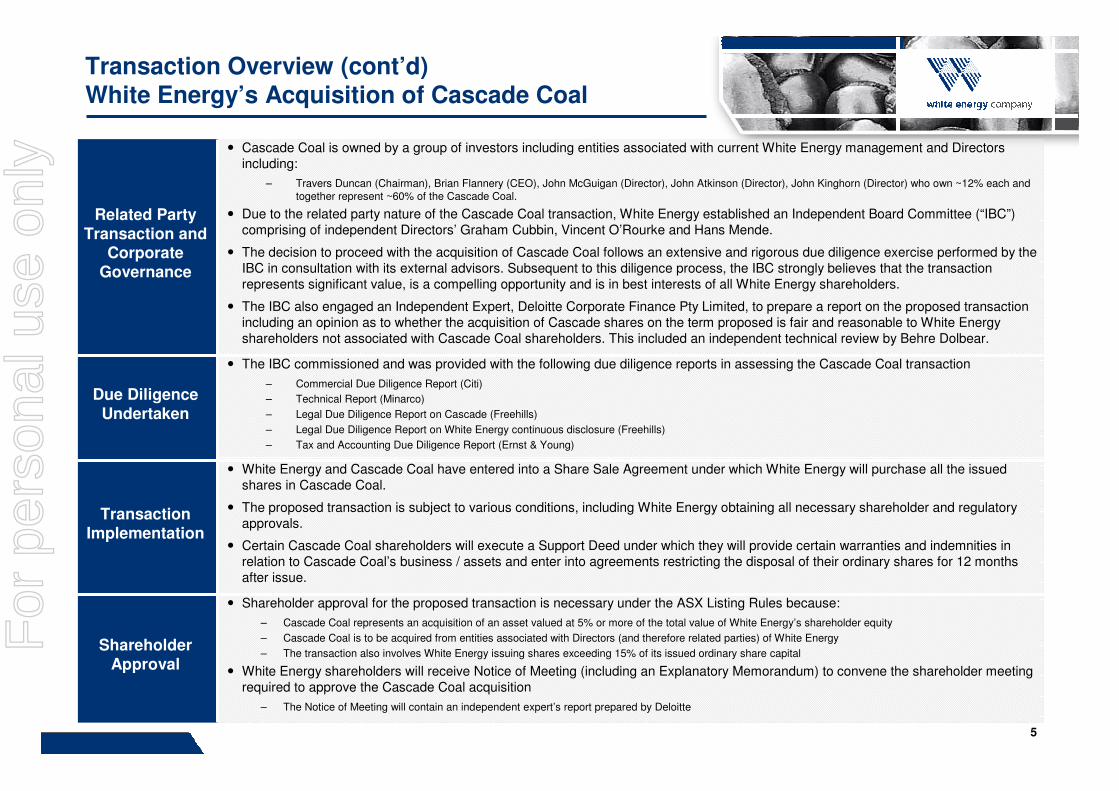

Transaction Overview (cont’d)White Energy’s Acquisition of Cascade Coal

Related Party Transaction and

Corporate Governance

� Cascade Coal is owned by a group of investors including entities associated with current White Energy management and Directors including:

– Travers Duncan (Chairman), Brian Flannery (CEO), John McGuigan (Director), John Atkinson (Director), John Kinghorn (Director) who own ~12% each and together represent ~60% of the Cascade Coal.

� Due to the related party nature of the Cascade Coal transaction, White Energy established an Independent Board Committee (“IBC”) comprising of independent Directors’ Graham Cubbin, Vincent O’Rourke and Hans Mende.

� The decision to proceed with the acquisition of Cascade Coal follows an extensive and rigorous due diligence exercise performed by the IBC in consultation with its external advisors. Subsequent to this diligence process, the IBC strongly believes that the transaction represents significant value, is a compelling opportunity and is in best interests of all White Energy shareholders.

� The IBC also engaged an Independent Expert, Deloitte Corporate Finance Pty Limited, to prepare a report on the proposed transaction including an opinion as to whether the acquisition of Cascade shares on the term proposed is fair and reasonable to White Energyshareholders not associated with Cascade Coal shareholders. This included an independent technical review by Behre Dolbear.

Due Diligence Undertaken

� The IBC commissioned and was provided with the following due diligence reports in assessing the Cascade Coal transaction

– Commercial Due Diligence Report (Citi)

– Technical Report (Minarco)

– Legal Due Diligence Report on Cascade (Freehills)

– Legal Due Diligence Report on White Energy continuous disclosure (Freehills)

– Tax and Accounting Due Diligence Report (Ernst & Young)

Transaction Implementation

� White Energy and Cascade Coal have entered into a Share Sale Agreement under which White Energy will purchase all the issued shares in Cascade Coal.

� The proposed transaction is subject to various conditions, including White Energy obtaining all necessary shareholder and regulatory approvals.

� Certain Cascade Coal shareholders will execute a Support Deed under which they will provide certain warranties and indemnities in relation to Cascade Coal’s business / assets and enter into agreements restricting the disposal of their ordinary shares for 12 months after issue.

Shareholder Approval

� Shareholder approval for the proposed transaction is necessary under the ASX Listing Rules because:

– Cascade Coal represents an acquisition of an asset valued at 5% or more of the total value of White Energy’s shareholder equity

– Cascade Coal is to be acquired from entities associated with Directors (and therefore related parties) of White Energy

– The transaction also involves White Energy issuing shares exceeding 15% of its issued ordinary share capital

� White Energy shareholders will receive Notice of Meeting (including an Explanatory Memorandum) to convene the shareholder meeting required to approve the Cascade Coal acquisition

– The Notice of Meeting will contain an independent expert’s report prepared by Deloitte

For

per

sona

l use

onl

y

Page 66

Transaction StructureWhite Energy’s Acquisition of Cascade Coal

Mt. Penny Coal

Glendon Brook Coal

Coal Mining

Coal Technology

SA Coal

Coal Mining

Coal Technology

SA Coal

24%

60%

+

White Energy and Cascade Coal have common shareholders including the Chairman, CEO and 3 other Directors of White Energy. Currently this group hold ~24% of White Energy and ~60% of Cascade Coal, and will hold ~35% of White Energy should the transaction proceed.

Travers DuncanChairman: White Energy

Brian FlanneryCEO: White Energy

John McGuiganDirector: White Energy

John AtkinsonDirector: White Energy

John KinghornDirector: White Energy

For

per

sona

l use

onl

y

Page 77

Next Steps and Expected Timetable to Completion

Notice of Meeting and Explanatory Memorandum sent to

shareholders� Early March 2011

Time and date for determining eligibility to vote at the Meeting

� 7.00pm (Sydney Time) on Monday, 4 April 2011

Shareholder meeting to approve Cascade transaction

� 10.00am (Sydney Time) on Wednesday, 6 April 2011

Completion of Transaction (if approved by shareholder)

� April 2011

The Cascade Coal transaction is expected to complete in April 2011.

For

per

sona

l use

onl

y

Page 88

� Transaction Overview

White Energy’s Acquisition of Cascade Coal

� Strategic Rationale

Cascade Coal - A Company Making Transaction

� Combination Rationale

White Energy and Cascade Coal Combined

� Detailed Asset Overview

The Cascade Coal Assets

For

per

sona

l use

onl

y

Page 99

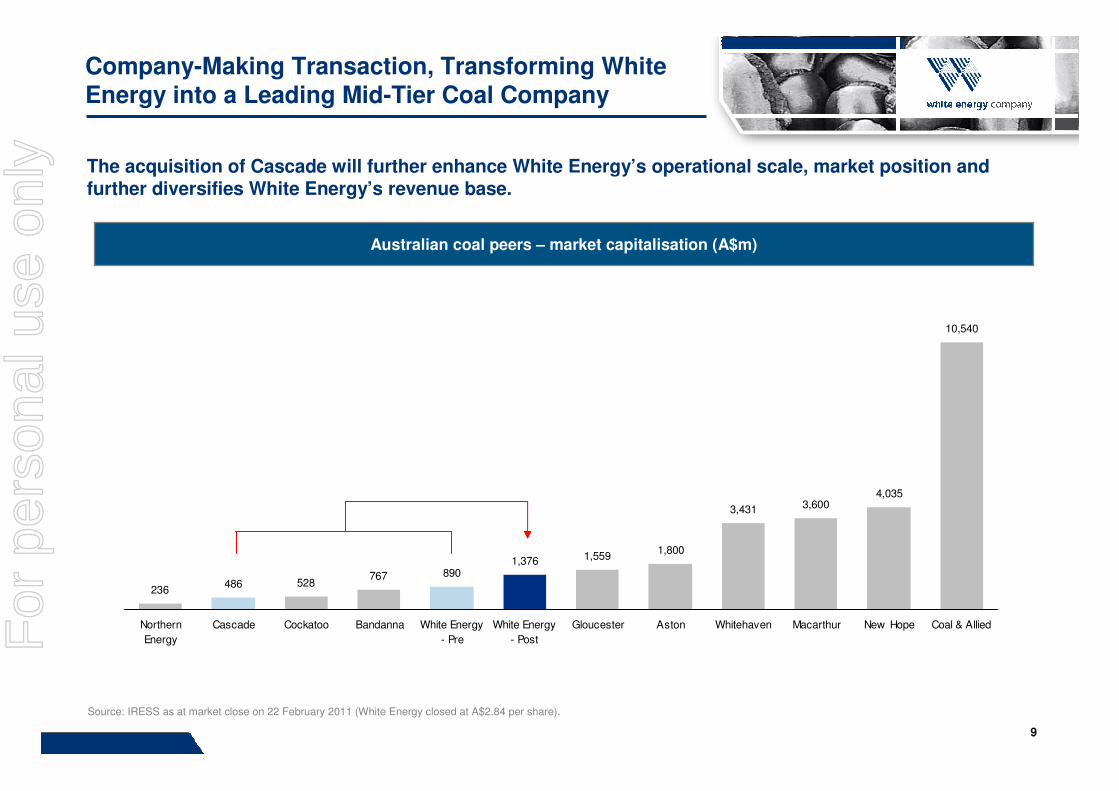

Australian coal peers – market capitalisation (A$m)

The acquisition of Cascade will further enhance White Energy’s operational scale, market position and further diversifies White Energy’s revenue base.

Company-Making Transaction, Transforming White Energy into a Leading Mid-Tier Coal Company

10,540

4,0353,6003,431

1,8001,5591,376

890767528486

236

Coal & AlliedNew HopeMacarthurWhitehavenAstonGloucesterWhite Energy

- Post

White Energy

- Pre

BandannaCockatooCascadeNorthern

Energy

Source: IRESS as at market close on 22 February 2011 (White Energy closed at A$2.84 per share).

For

per

sona

l use

onl

y

Page 1010

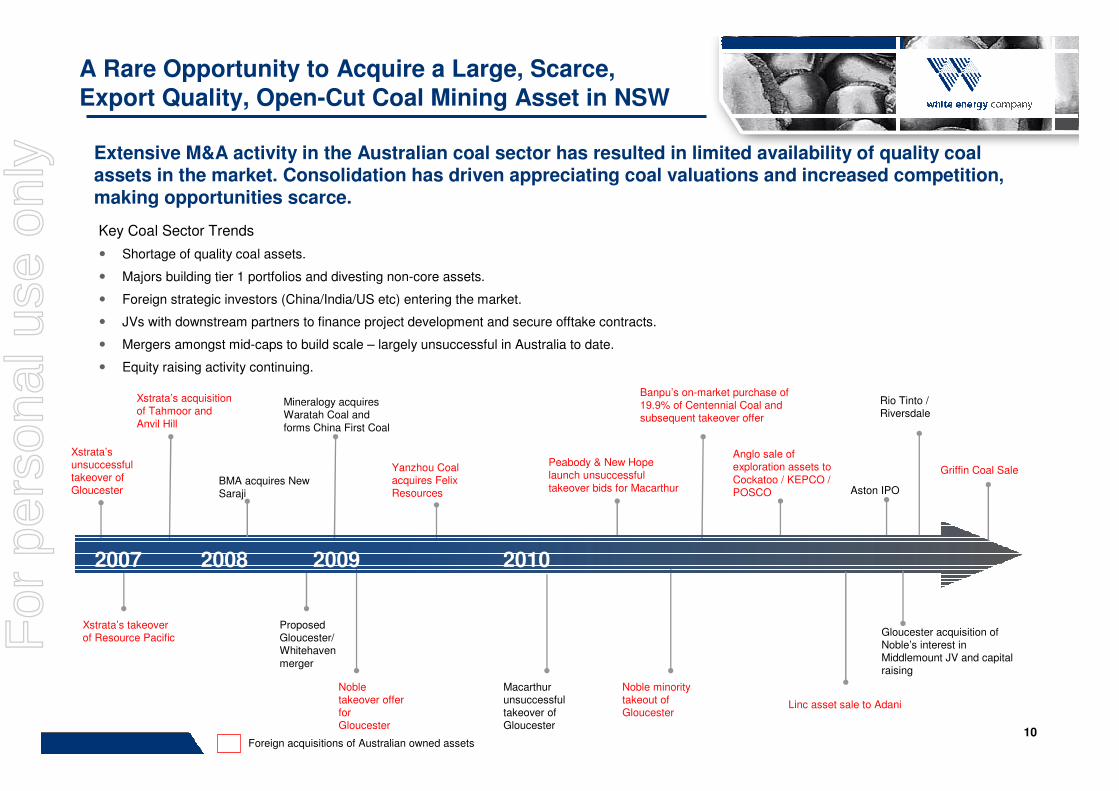

A Rare Opportunity to Acquire a Large, Scarce, Export Quality, Open-Cut Coal Mining Asset in NSW

Extensive M&A activity in the Australian coal sector has resulted in limited availability of quality coal assets in the market. Consolidation has driven appreciating coal valuations and increased competition, making opportunities scarce.

Xstrata’s unsuccessful takeover of Gloucester

Xstrata’s takeover of Resource Pacific

Xstrata’s acquisition of Tahmoor and Anvil Hill

Mineralogy acquires Waratah Coal and forms China First Coal

Yanzhou Coal acquires Felix Resources

Proposed Gloucester/ Whitehaven merger

Noble takeover offer for Gloucester

Macarthur unsuccessful takeover of Gloucester

BMA acquires New Saraji

Peabody & New Hope launch unsuccessful takeover bids for Macarthur

Noble minority takeout of Gloucester

Banpu’s on-market purchase of 19.9% of Centennial Coal and subsequent takeover offer

2007 2008 20102009

Anglo sale of exploration assets to Cockatoo / KEPCO / POSCO

Linc asset sale to Adani

Gloucester acquisition of Noble’s interest in Middlemount JV and capital raising

Aston IPO

Key Coal Sector Trends

� Shortage of quality coal assets.

� Majors building tier 1 portfolios and divesting non-core assets.

� Foreign strategic investors (China/India/US etc) entering the market.

� JVs with downstream partners to finance project development and secure offtake contracts.

� Mergers amongst mid-caps to build scale – largely unsuccessful in Australia to date.

� Equity raising activity continuing.

Foreign acquisitions of Australian owned assets

Rio Tinto / Riversdale

Griffin Coal Sale

For

per

sona

l use

onl

y

Page 1111

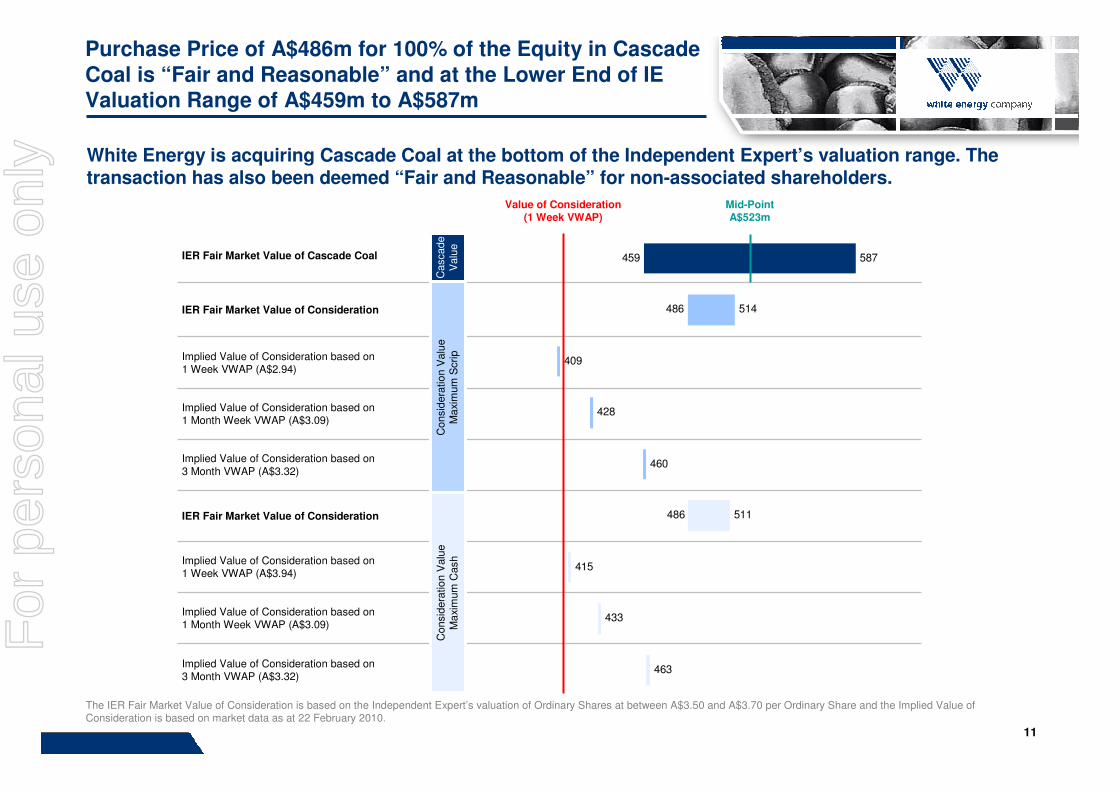

Purchase Price of A$486m for 100% of the Equity in Cascade Coal is “Fair and Reasonable” and at the Lower End of IE Valuation Range of A$459m to A$587m

White Energy is acquiring Cascade Coal at the bottom of the Independent Expert’s valuation range. The transaction has also been deemed “Fair and Reasonable” for non-associated shareholders.

The IER Fair Market Value of Consideration is based on the Independent Expert’s valuation of Ordinary Shares at between A$3.50 and A$3.70 per Ordinary Share and the Implied Value of Consideration is based on market data as at 22 February 2010.

IER Fair Market Value of Cascade Coal

IER Fair Market Value of Consideration

Implied Value of Consideration based on1 Week VWAP (A$2.94)

Implied Value of Consideration based on 1 Month Week VWAP (A$3.09)

Implied Value of Consideration based on 3 Month VWAP (A$3.32)

IER Fair Market Value of Consideration

Implied Value of Consideration based on 1 Week VWAP (A$3.94)

Implied Value of Consideration based on 1 Month Week VWAP (A$3.09)

Implied Value of Consideration based on 3 Month VWAP (A$3.32)

Consid

era

tio

n V

alu

eM

axi

mum

Scrip

Consid

era

tio

n V

alu

eM

axi

mum

Cash

Cascade

Valu

e

459

486

587

514

409

428

460

511

415

433

463

486

Mid-Point A$523m

Value of Consideration (1 Week VWAP)

For

per

sona

l use

onl

y

Page 1212

Mt. Penny is Competitively Positioned Within the Australian Export Thermal Coal Landscape

Mt Penny Open-Cut 1 is attractively positioned in the second quartile of Australian export thermal coal mines. This provides the project with flexibility in varying coal markets and allows it to significantly benefit in robust coal conditions.

0

40

80

120

160

200

0 20 40 60 80 100 120 140

201

0 F

OB

Cash C

osts

–in

c.

Roya

ltie

s &

Levi

es

(A$ p

er

sale

able

to

nn

e)

First Quartile Second Quartile Third Quartile Forth Quartile

Op

en

-Cu

t 1 (

Cascad

e)

Lo

M:

A$

56.0

/t

Op

en

-Cu

t 1 (

BD

A1)

Lo

M:

A$

60.4

/t

Note (1): Costs based on Behre Dolbear (BDA) FOB Cash Costs estimates, adjusted to include marketing, levies and royalties based on Deloitte assumptions for long-term coal prices and foreign exchange.

For

per

sona

l use

onl

y

Page 1313

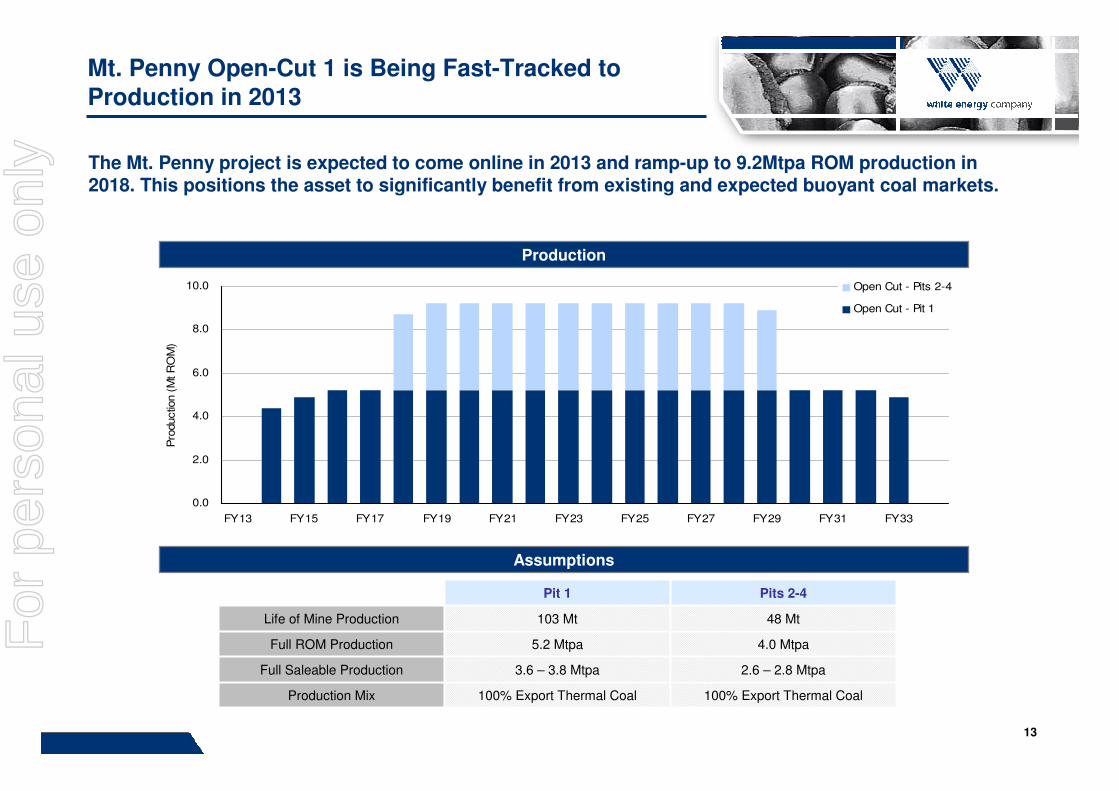

Pit 1 Pits 2-4

Life of Mine Production 103 Mt 48 Mt

Full ROM Production 5.2 Mtpa 4.0 Mtpa

Full Saleable Production 3.6 – 3.8 Mtpa 2.6 – 2.8 Mtpa

Production Mix 100% Export Thermal Coal 100% Export Thermal Coal

0.0

2.0

4.0

6.0

8.0

10.0

FY13 FY15 FY17 FY19 FY21 FY23 FY25 FY27 FY29 FY31 FY33

Pro

ductio

n (

Mt R

OM

) .

Open Cut - Pits 2-4

Open Cut - Pit 1

Production

Assumptions

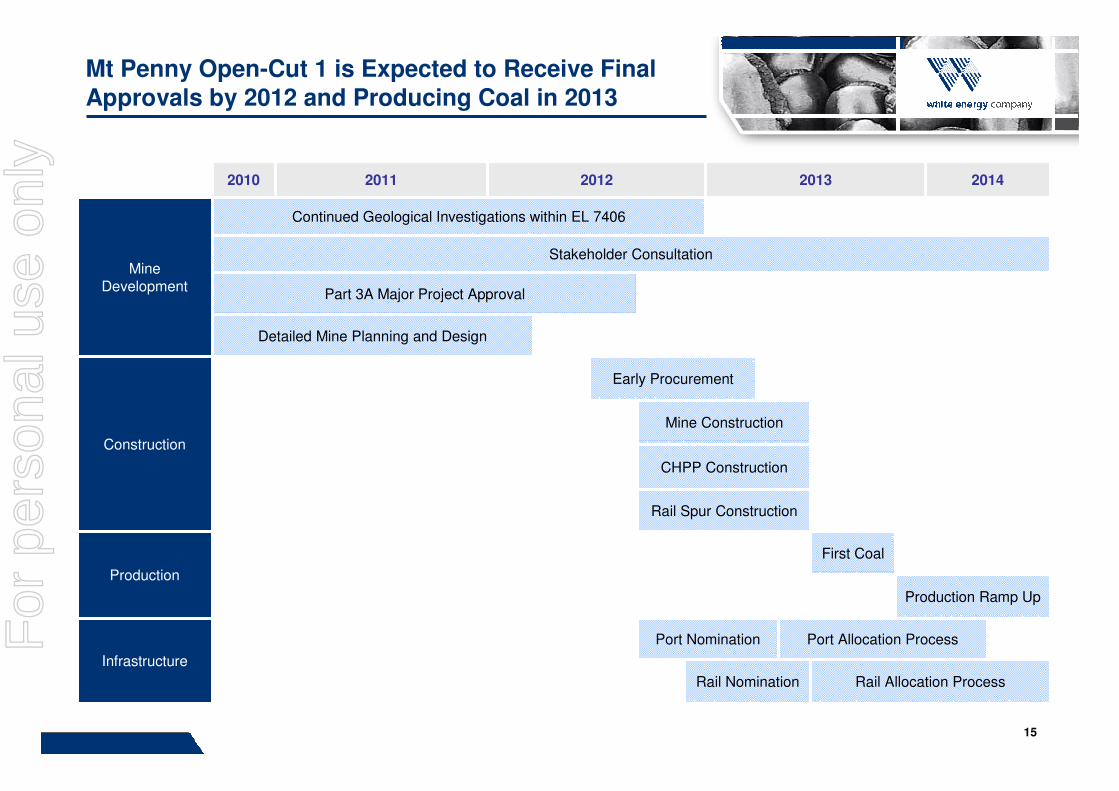

Mt. Penny Open-Cut 1 is Being Fast-Tracked to Production in 2013

The Mt. Penny project is expected to come online in 2013 and ramp-up to 9.2Mtpa ROM production in 2018. This positions the asset to significantly benefit from existing and expected buoyant coal markets.

For

per

sona

l use

onl

y

Page 1414

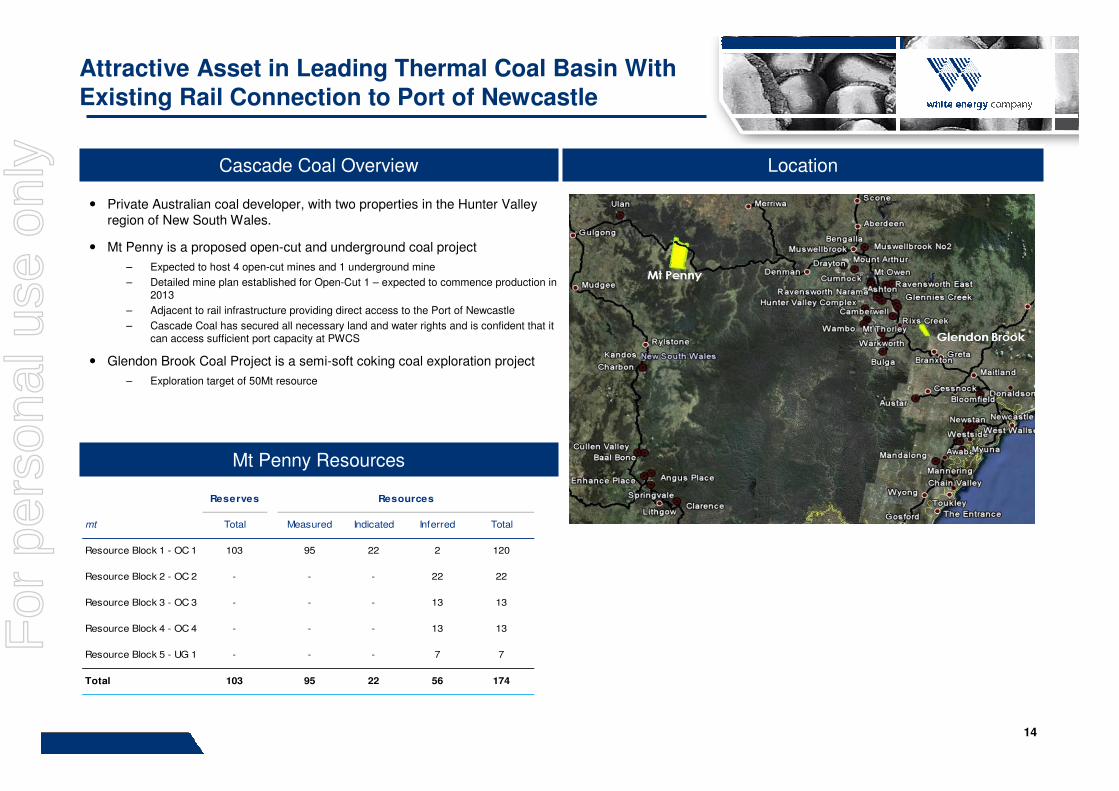

Attractive Asset in Leading Thermal Coal Basin With Existing Rail Connection to Port of Newcastle

Cascade Coal Overview Location

� Private Australian coal developer, with two properties in the Hunter Valley region of New South Wales.

� Mt Penny is a proposed open-cut and underground coal project

– Expected to host 4 open-cut mines and 1 underground mine

– Detailed mine plan established for Open-Cut 1 – expected to commence production in 2013

– Adjacent to rail infrastructure providing direct access to the Port of Newcastle

– Cascade Coal has secured all necessary land and water rights and is confident that it can access sufficient port capacity at PWCS

� Glendon Brook Coal Project is a semi-soft coking coal exploration project

– Exploration target of 50Mt resource

Mt Penny Resources

Reserves Resources

mt Total Measured Indicated Inferred Total

Resource Block 1 - OC 1 103 95 22 2 120

Resource Block 2 - OC 2 - - - 22 22

Resource Block 3 - OC 3 - - - 13 13

Resource Block 4 - OC 4 - - - 13 13

Resource Block 5 - UG 1 - - - 7 7

Total 103 95 22 56 174

For

per

sona

l use

onl

y

Page 1515

Mt Penny Open-Cut 1 is Expected to Receive Final Approvals by 2012 and Producing Coal in 2013

2010 2011 2012 2013 2014

Mine Development

Continued Geological Investigations within EL 7406

Stakeholder Consultation

Part 3A Major Project Approval

Detailed Mine Planning and Design

Construction

Early Procurement

Mine Construction

CHPP Construction

Rail Spur Construction

Production

First Coal

Production Ramp Up

Infrastructure

Port Nomination Port Allocation Process

Rail Nomination Rail Allocation Process

For

per

sona

l use

onl

y

Page 1616

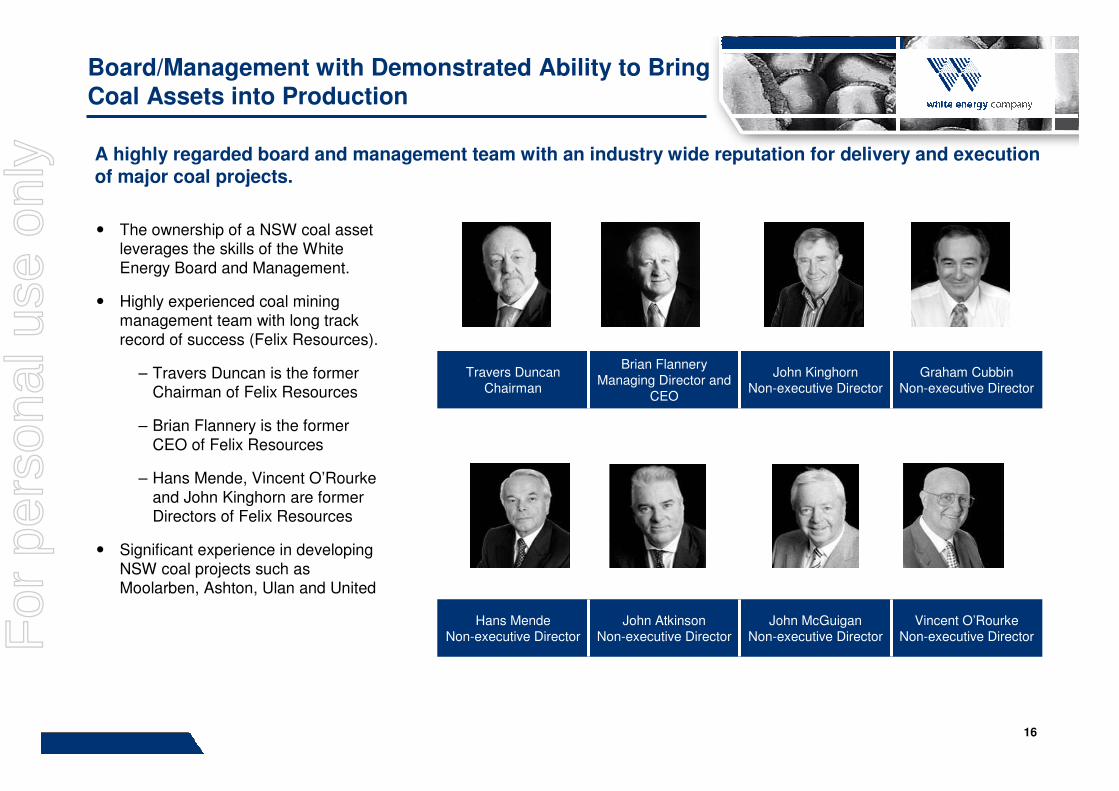

A highly regarded board and management team with an industry wide reputation for delivery and execution of major coal projects.

Board/Management with Demonstrated Ability to Bring Coal Assets into Production

Travers DuncanChairman

Brian FlanneryManaging Director and

CEO

John KinghornNon-executive Director

Graham CubbinNon-executive Director

Hans MendeNon-executive Director

John AtkinsonNon-executive Director

John McGuiganNon-executive Director

Vincent O’RourkeNon-executive Director

� The ownership of a NSW coal asset leverages the skills of the White Energy Board and Management.

� Highly experienced coal mining management team with long track record of success (Felix Resources).

– Travers Duncan is the former Chairman of Felix Resources

– Brian Flannery is the former CEO of Felix Resources

– Hans Mende, Vincent O’Rourke and John Kinghorn are former Directors of Felix Resources

� Significant experience in developing NSW coal projects such as Moolarben, Ashton, Ulan and United

For

per

sona

l use

onl

y

Page 1717

Why Cascade Coal ?

1Company-Making Transaction, Transforming White Energy into a Leading Mid-Tier Coal Company

2Rare Opportunity to Acquire a Large, Scarce, Export Quality, Open-Cut Coal Mining Asset in NSW

3Purchase Price of A$486m for 100% of the Equity in Cascade Coal is “Fair and Reasonable” and at the Lower End of IE Valuation Range of A$459m to A$587m

4Mt. Penny is Competitive with and Superior to Other Comparable Australian Thermal Coal Assets

5Mt. Penny Open-Cut 1 is Being Fast Tracked to Production in 2013, and is well positioned with Existing Rail Connection to Port of Newcastle

6Board/Management with Demonstrated Ability to Bring Coal Assets into Production – Moolarben, Ashton, Ulan and UnitedF

or p

erso

nal u

se o

nly

Page 1818

� Transaction Overview

White Energy’s Acquisition of Cascade Coal

� Strategic Rationale

Cascade Coal - A Company Making Transaction

� Combination Rationale

White Energy and Cascade Coal Combined

� Detailed Asset Overview

The Cascade Coal Assets

For

per

sona

l use

onl

y

Page 1919

The Continuing Evolution of White Energy

Upgrade Coal Fines

Other Related Coal Assets

Sub-bituminous Coal Assets

BCB Coal Upgrading

Technology

New Applicationseg. Coking

Coal

Acquisition of SACL provides development

options

Technology Offering

Conventional Coal Mining

Continue with joint venture business

model

Extend BCB technology into

new applications

The Cascade Coal acquisition represents the next step in the continuing evolution of White Energy into a diversified coal company.

Acquisition of Cascade Coal leverages

management skills and expertise

For

per

sona

l use

onl

y

Page 2020

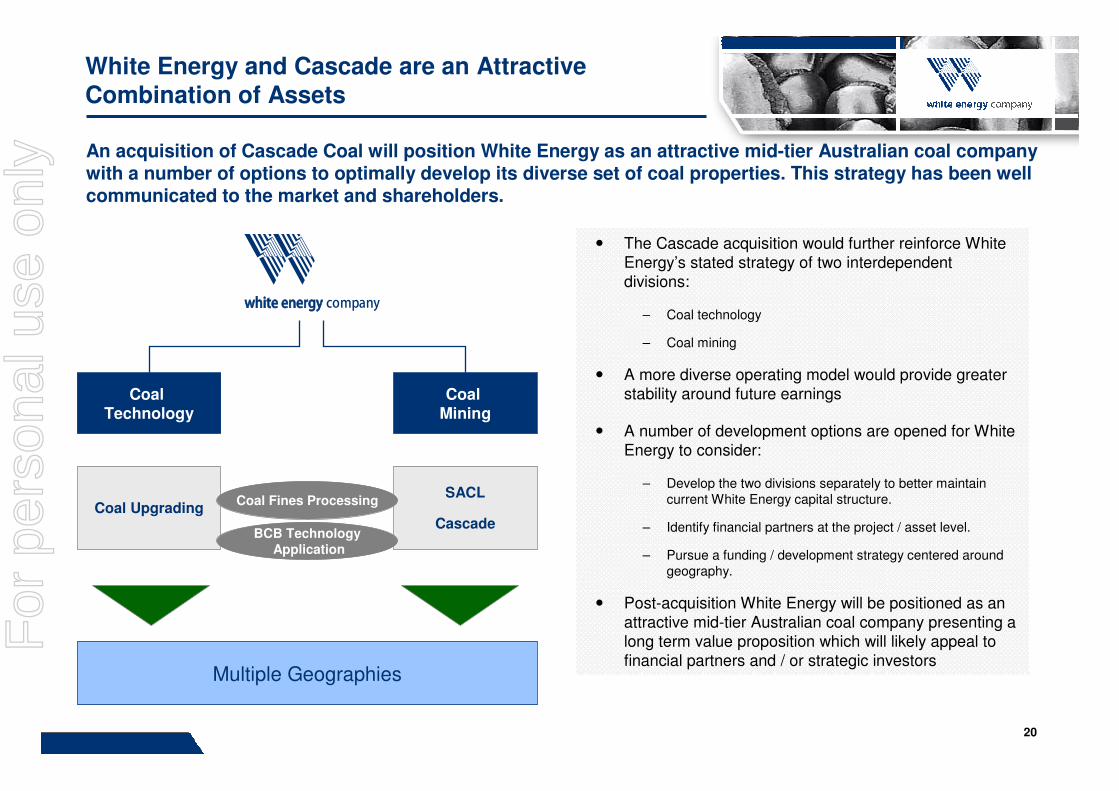

White Energy and Cascade are an Attractive Combination of Assets

� The Cascade acquisition would further reinforce White Energy’s stated strategy of two interdependent divisions:

– Coal technology

– Coal mining

� A more diverse operating model would provide greater stability around future earnings

� A number of development options are opened for White Energy to consider:

– Develop the two divisions separately to better maintain current White Energy capital structure.

– Identify financial partners at the project / asset level.

– Pursue a funding / development strategy centered around geography.

� Post-acquisition White Energy will be positioned as an attractive mid-tier Australian coal company presenting a long term value proposition which will likely appeal to financial partners and / or strategic investors

Coal Technology

Coal Mining

Multiple Geographies

Coal UpgradingSACL

Cascade

Coal Fines Processing

BCB TechnologyApplication

An acquisition of Cascade Coal will position White Energy as an attractive mid-tier Australian coal company with a number of options to optimally develop its diverse set of coal properties. This strategy has been well communicated to the market and shareholders.

For

per

sona

l use

onl

y

Page 2121

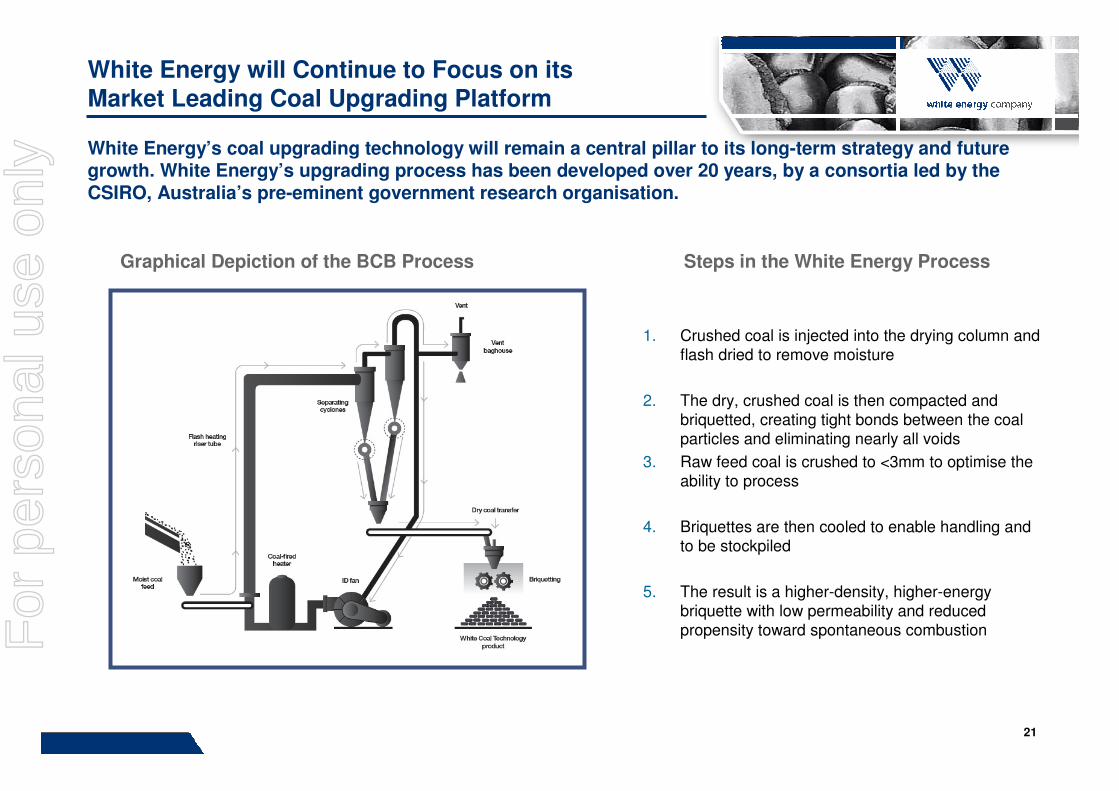

1. Crushed coal is injected into the drying column and flash dried to remove moisture

2. The dry, crushed coal is then compacted and briquetted, creating tight bonds between the coal particles and eliminating nearly all voids

3. Raw feed coal is crushed to <3mm to optimise the ability to process

4. Briquettes are then cooled to enable handling and to be stockpiled

5. The result is a higher-density, higher-energy briquette with low permeability and reduced propensity toward spontaneous combustion

Steps in the White Energy ProcessGraphical Depiction of the BCB Process

White Energy will Continue to Focus on its Market Leading Coal Upgrading Platform

White Energy’s coal upgrading technology will remain a central pillar to its long-term strategy and future growth. White Energy’s upgrading process has been developed over 20 years, by a consortia led by the CSIRO, Australia’s pre-eminent government research organisation.

For

per

sona

l use

onl

y

Page 2222

White Energy’s Facility in Tabang is the World’s First Commercial Scale Coal Upgrading Plant

� Kaltim Supacoal (KSC) is a joint venture between White Energy (51%) and Bayan (49%) established to operate coal upgrading plants in Tabang

– Bayan is one of the largest coal miners in Indonesia and owns several large sub-bituminous deposits in Tabang

� Tabang is located in East Kalimantan, Indonesia and is well positioned to key South East Asian and North Asian markets

� KSC has completed construction of an initial 1Mtpa coal upgrading module

– Plant has been commissioned and is currently ramping up to full capacity

– Work to address remaining technical issues at the Plant is underway

� KSC plans to significantly expand the capacity to 15 Mtpa

– Expansion will be prioritised over any other White Energy plants in Indonesia

White Energy’s industry leading plant in Tabang, Indonesia is now in production and has the capability to produce 1Mtpa of upgraded coal.

Joint Venture Structure

Coal Upgrading Technology

IndonesiaApprox. 4,400 Kcals/kg GAR Approx. 6,100 Kcals/kg GAR

PRB CoalApprox. 8,400 Btu/lb GAR Approx. 11,350 Btu/lb GAR

For

per

sona

l use

onl

y

Page 2323

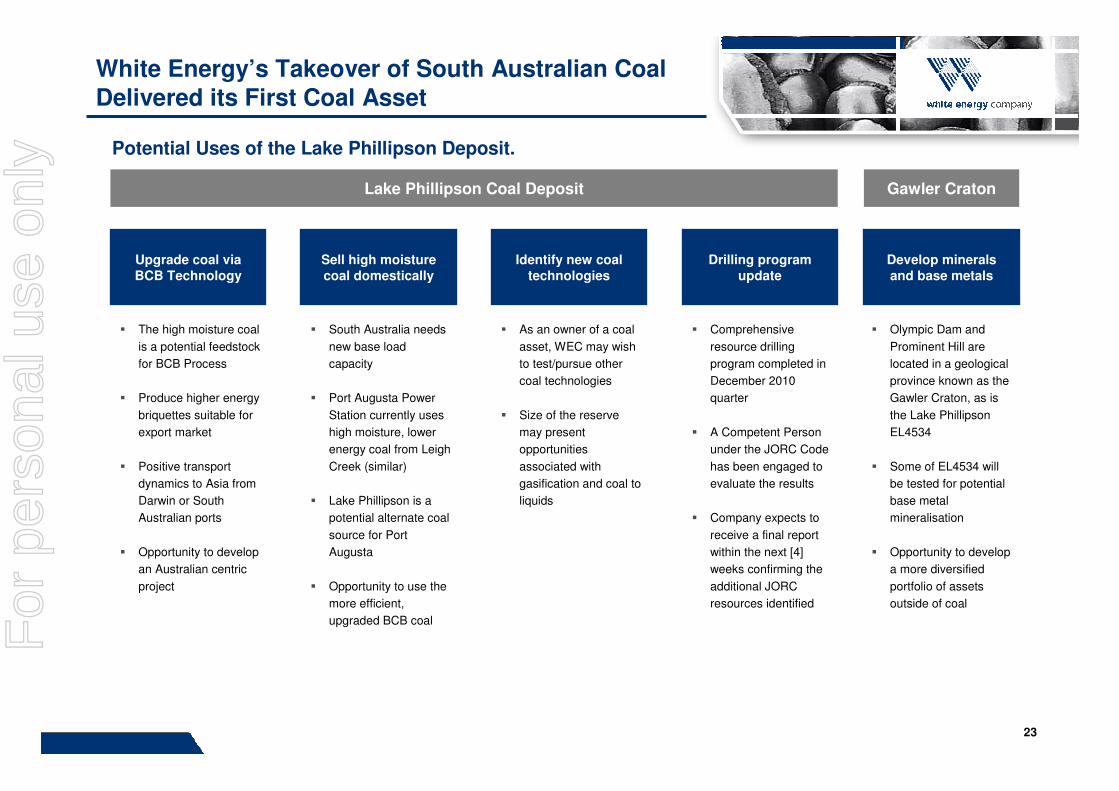

White Energy’s Takeover of South Australian Coal Delivered its First Coal Asset

Upgrade coal via BCB Technology

� The high moisture coal

is a potential feedstock

for BCB Process

� Produce higher energy

briquettes suitable for

export market

� Positive transport

dynamics to Asia from

Darwin or South

Australian ports

� Opportunity to develop

an Australian centric

project

Sell high moisture coal domestically

Identify new coal technologies

Develop minerals and base metals

� South Australia needs

new base load

capacity

� Port Augusta Power

Station currently uses

high moisture, lower

energy coal from Leigh

Creek (similar)

� Lake Phillipson is a

potential alternate coal

source for Port

Augusta

� Opportunity to use the

more efficient,

upgraded BCB coal

� As an owner of a coal

asset, WEC may wish

to test/pursue other

coal technologies

� Size of the reserve

may present

opportunities

associated with

gasification and coal to

liquids

� Olympic Dam and

Prominent Hill are

located in a geological

province known as the

Gawler Craton, as is

the Lake Phillipson

EL4534

� Some of EL4534 will

be tested for potential

base metal

mineralisation

� Opportunity to develop

a more diversified

portfolio of assets

outside of coal

Lake Phillipson Coal Deposit Gawler Craton

Drilling program update

� Comprehensive

resource drilling

program completed in

December 2010

quarter

� A Competent Person

under the JORC Code

has been engaged to

evaluate the results

� Company expects to

receive a final report

within the next [4]

weeks confirming the

additional JORC

resources identified

Potential Uses of the Lake Phillipson Deposit.

For

per

sona

l use

onl

y

Page 2424

� Transaction Overview

White Energy’s Acquisition of Cascade Coal

� Strategic Rationale

Cascade Coal - A Company Making Transaction

� Combination Rationale

White Energy and Cascade Coal Combined

� Detailed Asset Overview

The Cascade Coal Assets

For

per

sona

l use

onl

y

Page 2525

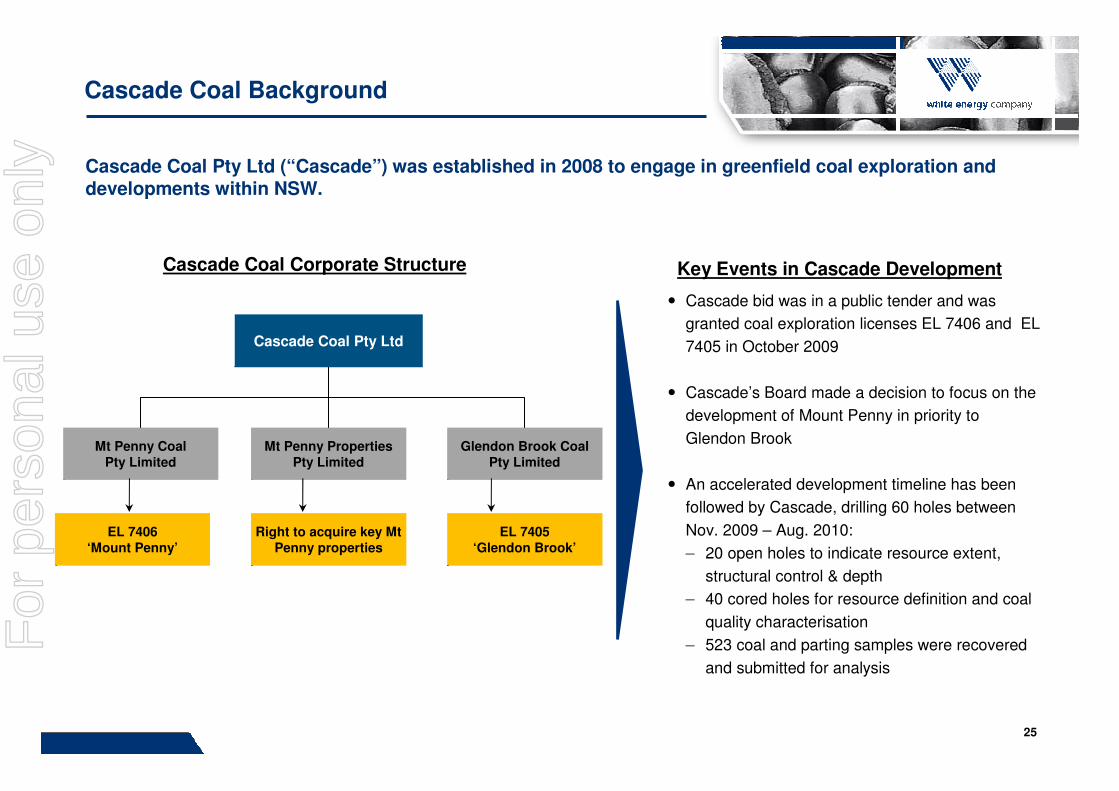

Cascade Coal Background

Cascade Coal Pty Ltd (“Cascade”) was established in 2008 to engage in greenfield coal exploration and developments within NSW.

Cascade Coal Pty Ltd

Mt Penny Coal Pty Limited

Mt Penny Properties Pty Limited

Glendon Brook Coal Pty Limited

EL 7406‘Mount Penny’

Right to acquire key Mt Penny properties

EL 7405‘Glendon Brook’

Cascade Coal Corporate Structure Key Events in Cascade Development

� Cascade bid was in a public tender and was

granted coal exploration licenses EL 7406 and EL

7405 in October 2009

� Cascade’s Board made a decision to focus on the

development of Mount Penny in priority to

Glendon Brook

� An accelerated development timeline has been

followed by Cascade, drilling 60 holes between

Nov. 2009 – Aug. 2010:

– 20 open holes to indicate resource extent,

structural control & depth

– 40 cored holes for resource definition and coal

quality characterisation

– 523 coal and parting samples were recovered

and submitted for analysis

For

per

sona

l use

onl

y

Page 2626

Mount Penny – EL 7406

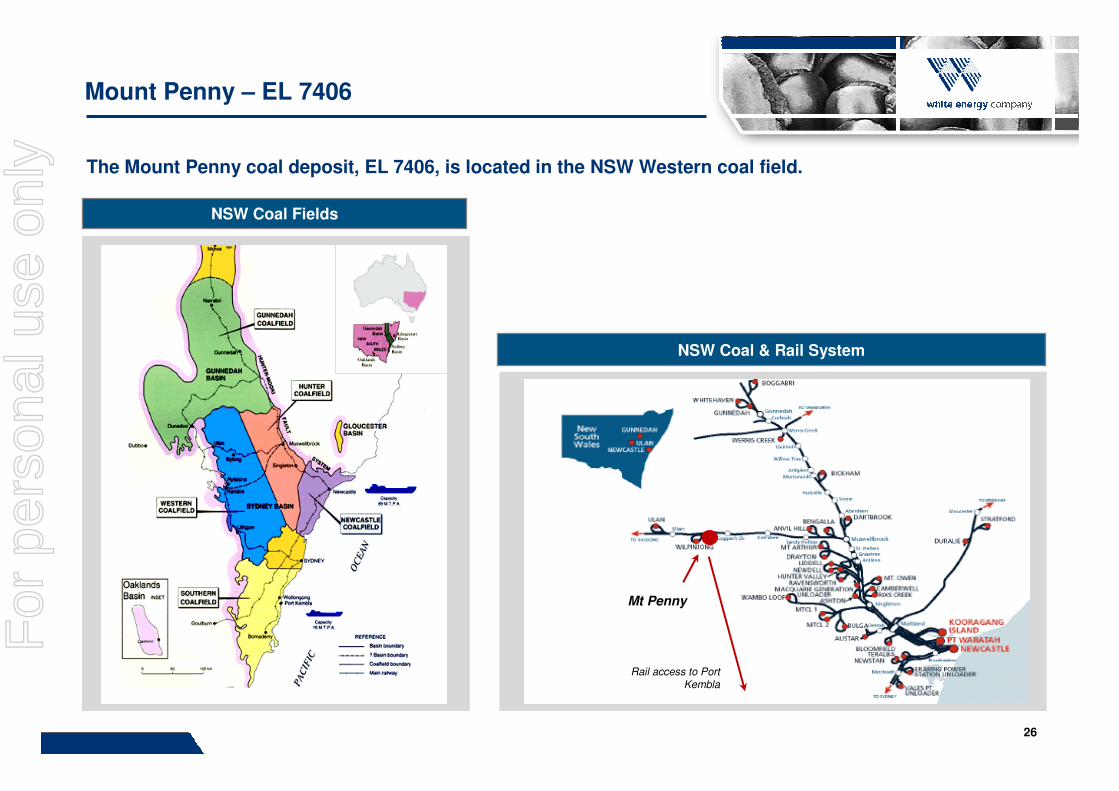

The Mount Penny coal deposit, EL 7406, is located in the NSW Western coal field.

NSW Coal Fields

NSW Coal & Rail System

Mt Penny

Rail access to Port Kembla

For

per

sona

l use

onl

y

Page 2727

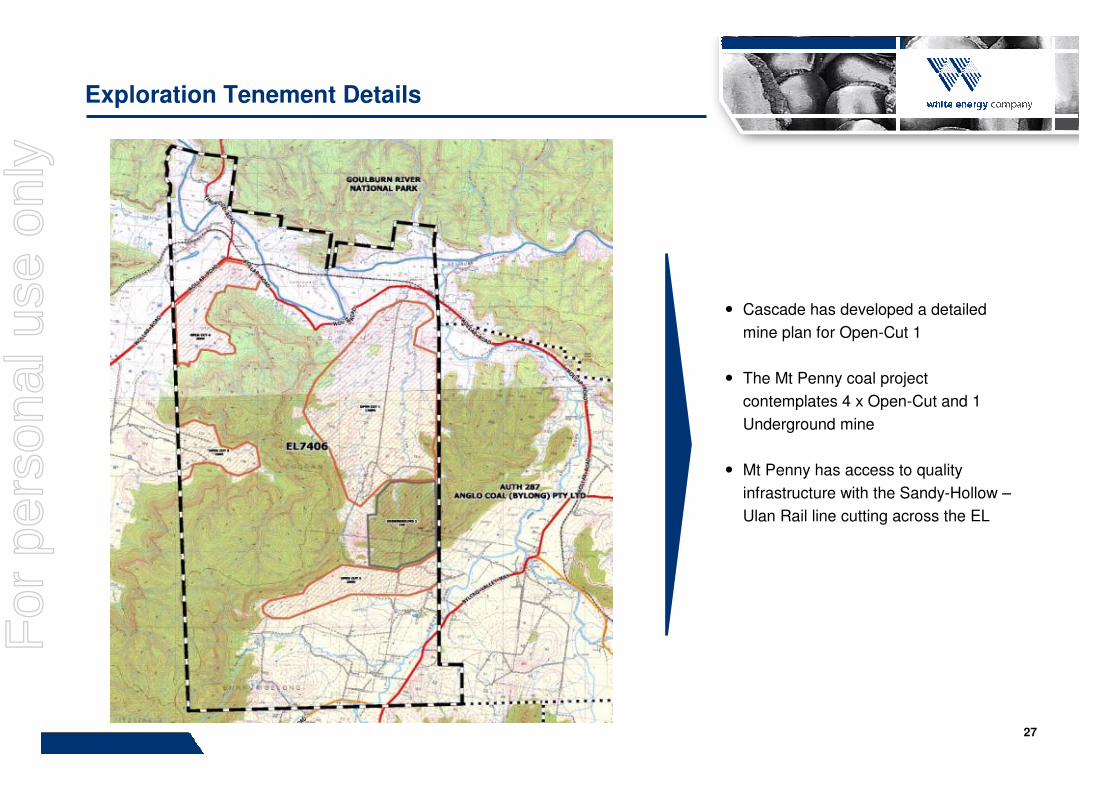

Exploration Tenement Details

� Cascade has developed a detailed

mine plan for Open-Cut 1

� The Mt Penny coal project

contemplates 4 x Open-Cut and 1

Underground mine

� Mt Penny has access to quality

infrastructure with the Sandy-Hollow –

Ulan Rail line cutting across the EL

For

per

sona

l use

onl

y

Page 2828

Exploration Tenement Details

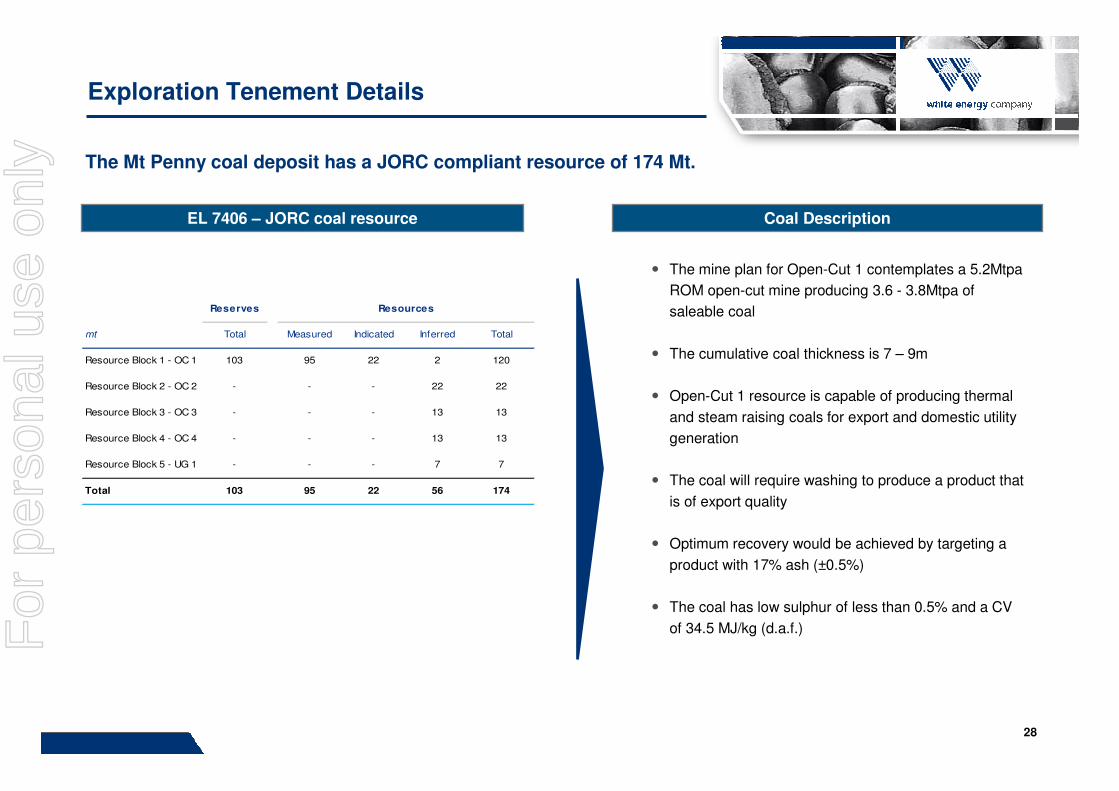

EL 7406 – JORC coal resource Coal Description

� The mine plan for Open-Cut 1 contemplates a 5.2Mtpa

ROM open-cut mine producing 3.6 - 3.8Mtpa of

saleable coal

� The cumulative coal thickness is 7 – 9m

� Open-Cut 1 resource is capable of producing thermal

and steam raising coals for export and domestic utility

generation

� The coal will require washing to produce a product that

is of export quality

� Optimum recovery would be achieved by targeting a

product with 17% ash (±0.5%)

� The coal has low sulphur of less than 0.5% and a CV

of 34.5 MJ/kg (d.a.f.)

The Mt Penny coal deposit has a JORC compliant resource of 174 Mt.

Reserves Resources

mt Total Measured Indicated Inferred Total

Resource Block 1 - OC 1 103 95 22 2 120

Resource Block 2 - OC 2 - - - 22 22

Resource Block 3 - OC 3 - - - 13 13

Resource Block 4 - OC 4 - - - 13 13

Resource Block 5 - UG 1 - - - 7 7

Total 103 95 22 56 174

For

per

sona

l use

onl

y

Page 2929

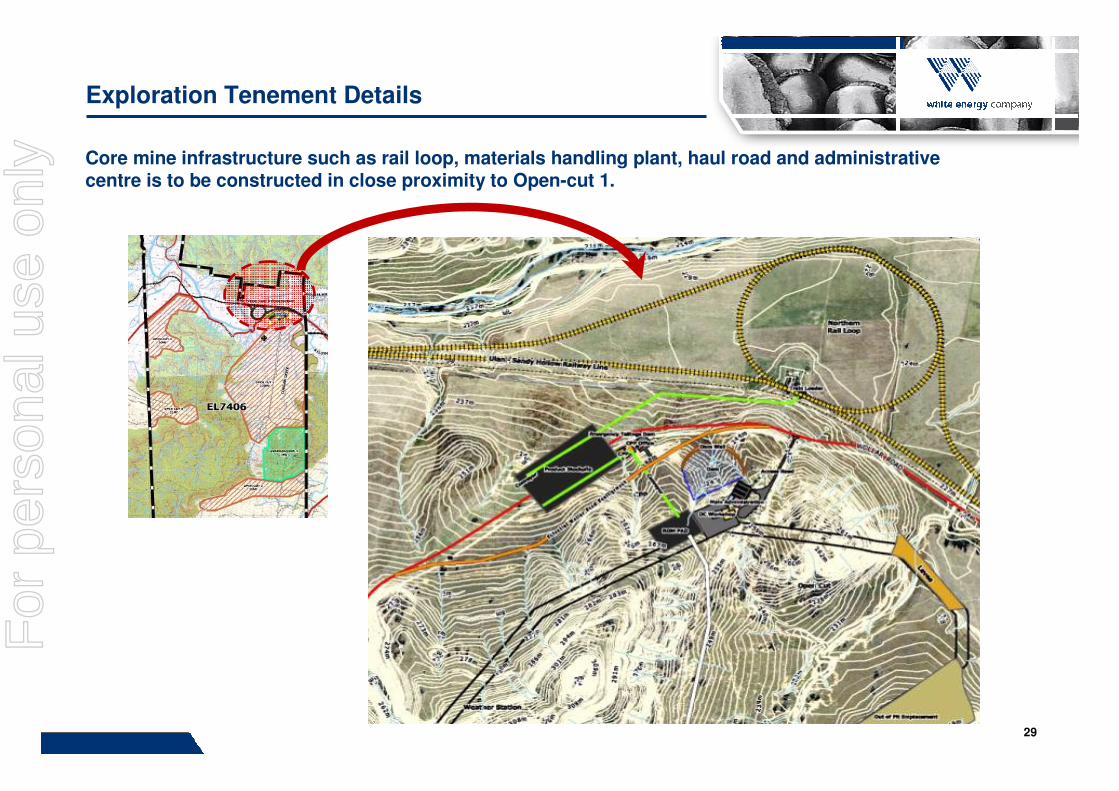

Exploration Tenement Details

Core mine infrastructure such as rail loop, materials handling plant, haul road and administrative centre is to be constructed in close proximity to Open-cut 1.

For

per

sona

l use

onl

y

Page 3030

Infrastructure and Utilities

Mt Penny is well positioned with respect to rail and utility infrastructure.

Rail Port Power Water

� Staged bi-directional

loop proposed –

enabling routing of trains

to Newcastle or Port

Kembla

� Sufficient excess rail

capacity to cater for Mt

Penny production

� Passing lanes to be

constructed to Wollar

and Bylong

� Port Waratah Coal

Service Terminal has

been identified as a

likely port for export

� Depending on rail

infrastructure Port

Kembla could emerge

as a viable export port

� Power requirements of

approximately 6.5 Mva

will be needed and can

be serviced from the

Bylong sub-station

� An application has been

submitted to Integral

Energy

� Water requirements for

Open-Cut 1 at 5.2 Mtpa

ROM operation is 1,500

mega liters

� Cascade believes it can

control Water Access

Licenses that provide

1,700 mega liters

� There may be an

opportunity to also

source water from site

run off

For

per

sona

l use

onl

y

Page 3131

Land Access and Encumbrances

Cascade Coal’s subsidiary Mt Penny Properties Pty Ltd has secured put and call options to purchase land located within Open-Cut 1 and over the relevant infrastructure areas

Controlled Land Native Title

� Based on searches of the register administrated by the

Native Title Tribunal completed on 30 September

2010, Mt Penny’s exploration license EL 7406 is not

covered by a native title claim

� Aboriginal Cultural Heritage surveys commenced

during October 2010 to ensure that it complies with

relevant guidelines

� Cascade has engaged relevant Aboriginal groups and

are following through with the relevant procedures

� Areas highlighted

in blue denotes

land controlled or

owned by

Mt Penny

Properties Pty

Limited

For

per

sona

l use

onl

y

Page 3232

Glendon Brook – Asset Snapshot

� Cascade was granted Glendon Brook in October 2009 for a

period of 5 years. Glendon Brook is located in the Hunter

Valley Coalfield approximately 12km east of Singleton and

immediately south of ML 1309 “Mitchell’s Flat” held by Xstrata

PLC.

� ML1309 expires in February 2014. The development consent

for the proposed rail access corridor which was also granted,

has allegedly expired, however Cascade is currently

investigating its options in this regard

� The coal is typical of the Vane group and a lower part of the

Burmawood formations, which are host to a number of coal

seams that are mined at Rixs Creek, Ashton, and Camberwell

mines.

� Cascade carried out exploration activity in September 2009

consisting of a fully cored hole in steep dipping zones. 13

samples ranging from 0.3 to 2.1m thick were intersected

For

per

sona

l use

onl

y

Page 3333

Except for the historical information contained herein, the matters discussed in this presentation contain forward-looking statements, including statements, containing the words “planned”, “expects”, “believes”, “strategy”, “opportunity”, “anticipates”, and similar words. Such forward-looking statements are subject to known and unknown risks, uncertainties, or other factors that may cause the company’s actual results to be materially different from historical results or any results expressed or implied by such forward-looking statements. We assume no obligation to update any forward-looking statements to reflect events or circumstances arising after the date hereof. In addition where comparisons are made between White Energy Company and other companies, we have made best efforts to properly interpret publicly made information by these companies but cannot be certain that such comparisons are completely accurate.

For more information visit www.whiteenergyco.com or contact:

Brian Flannery

Managing Director and CEO

White Energy Company Limited

+61 2 9959 0000

Forward looking statements

Ivan Maras

Chief Financial Officer

White Energy Company Limited

+61 2 9959 0000

For

per

sona

l use

onl

y

Page 3434

Competent Person Statement

Cascade Coal Pty Limited

The information in this presentation concerning the proposed acquisition of Cascade by White Energy, which relates to Coal

Reserves and Coal Resources at EL7406 and EL7405 is based on information compiled by Mr Michael Johnstone, who is a member of the Australasian Institute of Mining and Metallurgy. Mr Johnstone is the principal consultant of Minerva Geological Services PL.

Mr Michael Johnstone has 32 years of relevant mining and geological experience in coal. During this time he has either managed

exploration programs or contributed significantly to mining studies related to the estimation and assessment of coal resources, and in

the development of coal mining operations in Australia, India, Pakistan, Philippines and Vietnam. He was the project Geologist responsible for implementing the Ulan Stage 2 exploration program, and Exploration Manager for the Ashton and recently

commissioned Moolarben Development. He has sufficient experience which is relevant to the style of coal occurrence and type of

deposit under consideration and to the activity he is undertaking to qualify as a Competent Person as defined in the 2004 Edition of

the “Australasian Code for Reporting Mineral Resources and Ore Reserves”. Pursuant to the requirements of ASX Listing Rule 5.6,

Mr Johnstone consents to the inclusion in the announcement of the matters based on their information in the form and context, which it appears.

Michael Johnstone - February 2011

Member AIMMPrincipal Consultant

Minerva Geological Services Pty Ltd

For

per

sona

l use

onl

y

Maritime Trade TowersLevel 20, 201 Kent StreetSydney, NSW 2000Telephone: +61 2 9959 0000Facsimile: + 61 2 9959 0099Email: [email protected] ABN 62 071 527 083

For

per

sona

l use

onl

y