for a brighter future - cerro de pasco resources inc.€¦ · this presentation contains...

TRANSCRIPT

For A Brighter FutureCorporate Presentation - February 2020

This presentation contains "forward-looking statements" and "forward-looking information" (collectively, "forward-looking information") within the meaning of applicable Canadian securities legislation. All

information contained in this presentation, other than statements of current and historical fact, is forward-looking information. Often, but not always, forward-looking information can be identified by the use of

words such as "plans", "expects", "budget", "guidance", "scheduled", "estimates", "forecasts", "strategy", "target", "intends", "objective", "goal", "understands", "anticipates" and "believes" (and variations of these

or similar words) and statements that certain actions, events or results "may", "could", "would", "should", "might" "occur" or "be achieved" or "will be taken" (and variations of these or similar expressions). Forward-

looking information is also identifiable in statements of currently occurring matters which may continue in the future, such as "providing the Company with", "is currently", "allows/allowing for", "will advance" or

"continues to" or other statements that may be stated in the present tense with future implications. All of the forward-looking information in this presentation is qualified by this cautionary note. Forward-looking

information is based on, among other things, opinions, assumptions, estimates and analyses that, while considered reasonable by Cerro de Pasco Resources at the date the forward-looking information is

provided, inherently are subject to significant risks, uncertainties, contingencies and other factors that may cause actual results and events to be materially different from those expressed or implied by the forward-

looking information.

Forward-looking statements involve known and unknown risks, uncertainties, contingencies and other factors that may cause actual results and events to be materially different from those expressed or implied by

the forward-looking information. The risks, uncertainties, contingencies and other factors that may cause actual results to differ materially from those expressed or implied by the forward-looking information may

include, but are not limited to, risks generally associated with the mining industry, such as economic factors (including future commodity prices, currency fluctuations, energy prices and general cost escalation),

uncertainties related to the development and operation of Cerro de Pasco Resources projects, dependence on key personnel and employee and union relations, risks related to political or social unrest or change,

rights and title claims, operational risks and hazards, including unanticipated environmental, industrial and geological events and developments and the inability to insure against all risks, failure of plant,

equipment, processes, transportation and other infrastructure to operate as anticipated, compliance with government and environmental regulations, including permitting requirements and anti-bribery legislation,

volatile financial markets that may affect Cerro de Pasco Resources ability to obtain additional financing on acceptable terms, the failure to obtain required approvals or clearances from government authorities on

a timely basis, uncertainties related to the geology, continuity, grade and estimates of mineral reserves and resources, and the potential for variations in grade and recovery rates, uncertain costs of reclamation

activities, tax refunds, hedging transactions, as well as the risks discussed in Cerro de Pasco Resources listing statement dated July 26, 2018 and available on the Company’s profile on the CSE and SEDAR at

www.sedar.com. Should one or more risk, uncertainty, contingency or other factor materialize, or should any factor or assumption prove incorrect, actual results could vary materially from those expressed or

implied in the forward-looking information. Accordingly, the reader should not place undue reliance on forward-looking information. Ascendant does not assume any obligation to update or revise any forward-

looking information after the date of this presentation or to explain any material difference between subsequent actual events and any forward-looking information, except as required by applicable law.

The information concerning the Company’s mineral properties has been prepared in accordance with National Instrument 43-101 (“NI-43-101”) adopted by the Canadian Securities Administrators. In accordance

with NI-43-101, the terms “Mineral Reserves”, “Proven Mineral Reserve”, “Probable Mineral Reserve”, “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral

Resource” are defined in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Definition Standards for Mineral Resources and Mineral Reserves adopted by the CIM Council on May 10, 2014.

While the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are recognized and required by NI 43-101, the U.S. Securities Exchange

Commission (“SEC”) does not recognize them. The reader is cautioned that, except for that portion of mineral resources classified as mineral reserves, mineral resources do not have demonstrated economic

value. Inferred Mineral Resources have a high degree of uncertainty as to their existence and as to whether they can be economically or legally mined. It cannot be assumed that all or any part of any Inferred

Mineral Resource will ever be upgraded to a higher category. Therefore, the reader is cautioned not to assume that all or any part of an Inferred Mineral Resource exists, that it can be economically or legally

mined, or that it will ever be upgraded to a higher category. Likewise, you are cautioned not to assume that all or any part of a measured or Indicated Mineral Resource will ever be upgraded into Mineral

Reserves.

The Company has not completed any engineering study with respect to Volcan Operations and Quiulacocha and, consequently, there is no certainty that the stated projection in this presentation will be met or that

the Company’s operations at the Volcan and Quiulacocha Projects will be profitable.

This Presentation contains Future Oriented Production, Financial Information and Financial Outlooks (collectively, “PFOFI”) within the meaning of applicable Canadian securities laws. The PFOFI has been

prepared by management of Cerro de Pasco as at December 26, 2019 to demonstrate the potential benefits of the Transaction to shareholders. The PFOFI has been prepared based on a number of assumptions

that management of Cerro de Pasco believe are reasonable. However, because this information is highly subjective and subject to numerous risks, including the risks discussed under the heading “Cautionary

Note Regarding Forward-Looking Information", it should not be relied on as necessarily indicative of future results. Cerro de Pasco do not intend, and do not assume any obligation, to update this forward-looking

information except as otherwise required by applicable law.

Readers should be aware that the Company’s financial statements (and information derived therefrom) have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by

the International Accounting Standards Board and are subject to Canadian auditing and auditor independence standards. IFRS differs in some respects from United States generally accepted accounting

principles and thus the Company’s financial statements (and information derived there from) may not be comparable to those of United States companies .Unless otherwise indicated, all dollar values herein are in

US$ denomination.

2 | CSE:CDPR

Forward Looking Information

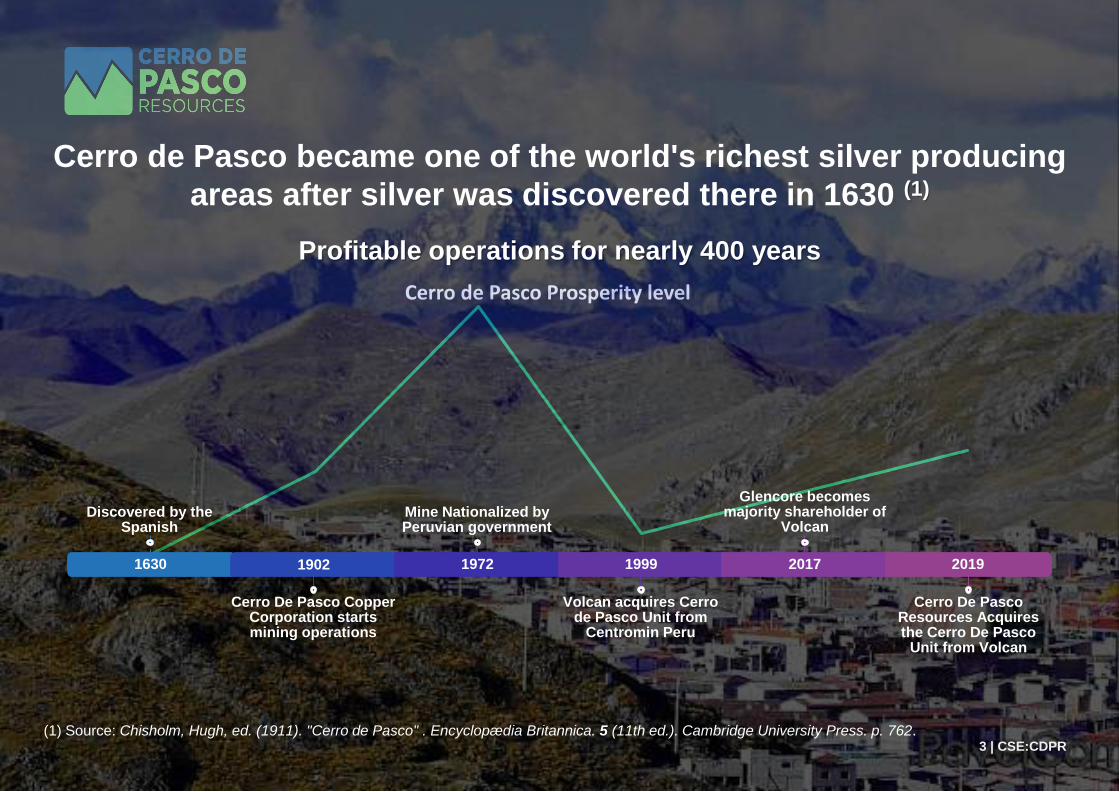

Cerro de Pasco Prosperity level

Cerro de Pasco became one of the world's richest silver producing

areas after silver was discovered there in 1630 (1)

Profitable operations for nearly 400 years

(1) Source: Chisholm, Hugh, ed. (1911). "Cerro de Pasco" . Encyclopædia Britannica. 5 (11th ed.). Cambridge University Press. p. 762.3 | CSE:CDPR

1630

Discovered by the Spanish

1902

Cerro De Pasco Copper Corporation starts mining operations

1972

Mine Nationalized by Peruvian government

1999

Volcan acquires Cerro de Pasco Unit from

Centromin Peru

2017

Glencore becomes majority shareholder of

Volcan

2019

Cerro De Pasco Resources Acquires the Cerro De Pasco

Unit from Volcan

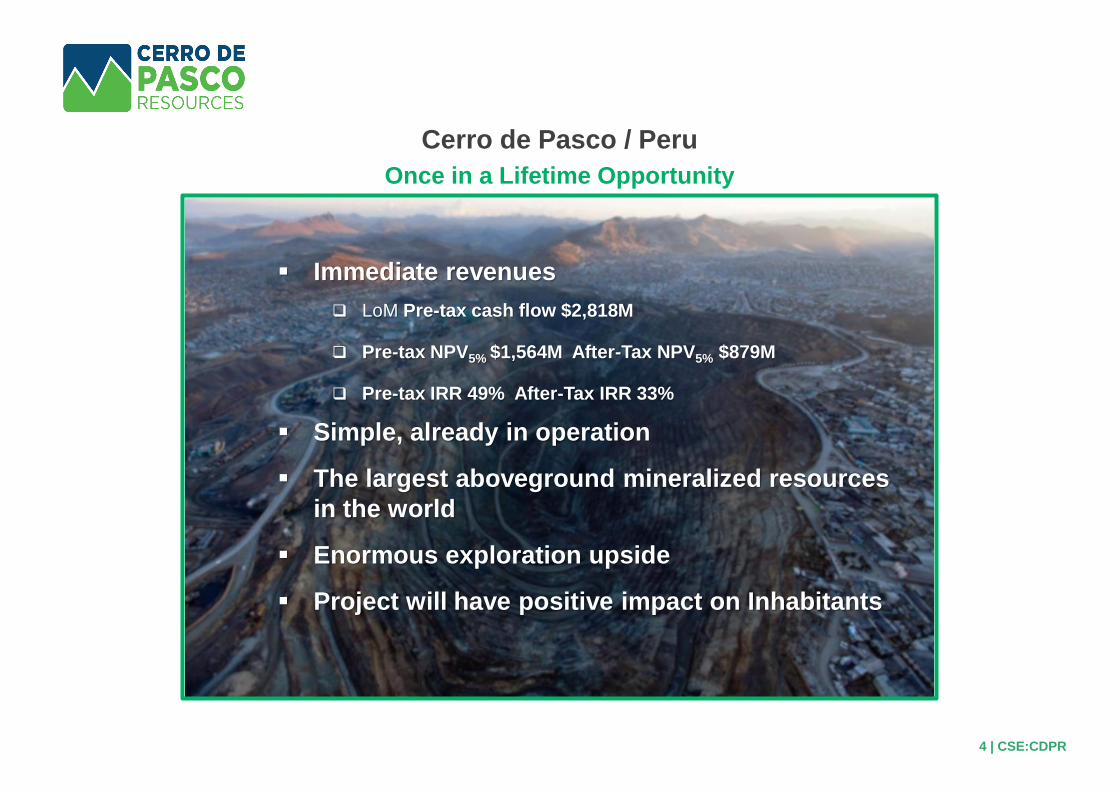

Cerro de Pasco / Peru

▪ Immediate revenues

❑ LoM Pre-tax cash flow $2,818M

❑ Pre-tax NPV5% $1,564M After-Tax NPV5% $879M

❑ Pre-tax IRR 49% After-Tax IRR 33%

▪ Simple, already in operation

▪ The largest aboveground mineralized resources

in the world

▪ Enormous exploration upside

▪ Project will have positive impact on Inhabitants

Once in a Lifetime Opportunity

4 | CSE:CDPR

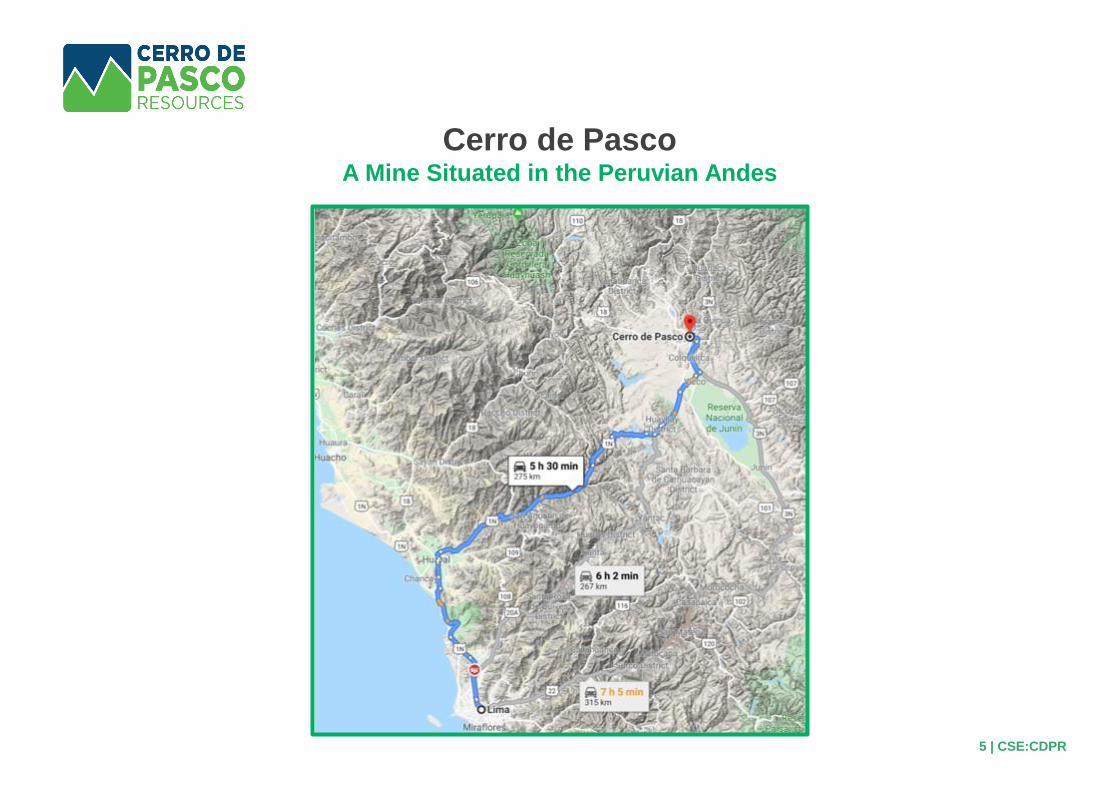

Cerro de PascoA Mine Situated in the Peruvian Andes

5 | CSE:CDPR

What We Own TodayThe “El Metalurgista” Mining Concession and Social License

6 | CSE:CDPR

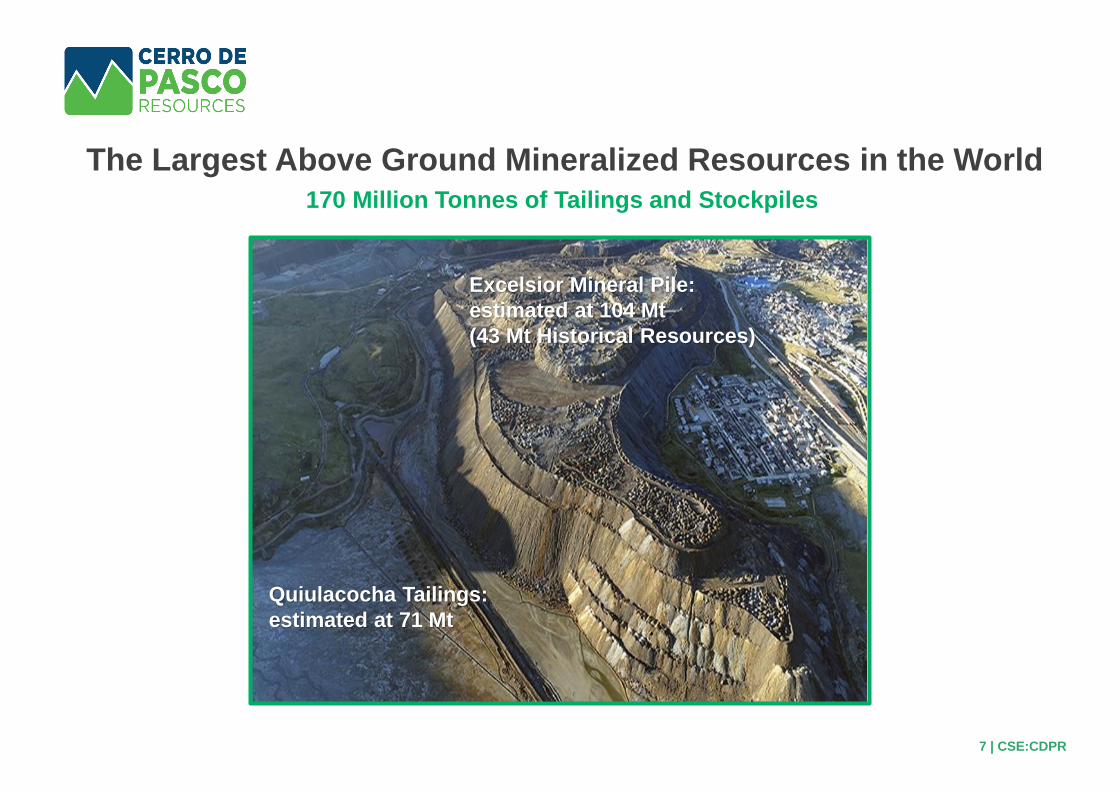

The Largest Above Ground Mineralized Resources in the World170 Million Tonnes of Tailings and Stockpiles

Excelsior Mineral Pile:

estimated at 104 Mt

(43 Mt Historical Resources)

Quiulacocha Tailings:

estimated at 71 Mt

7 | CSE:CDPR

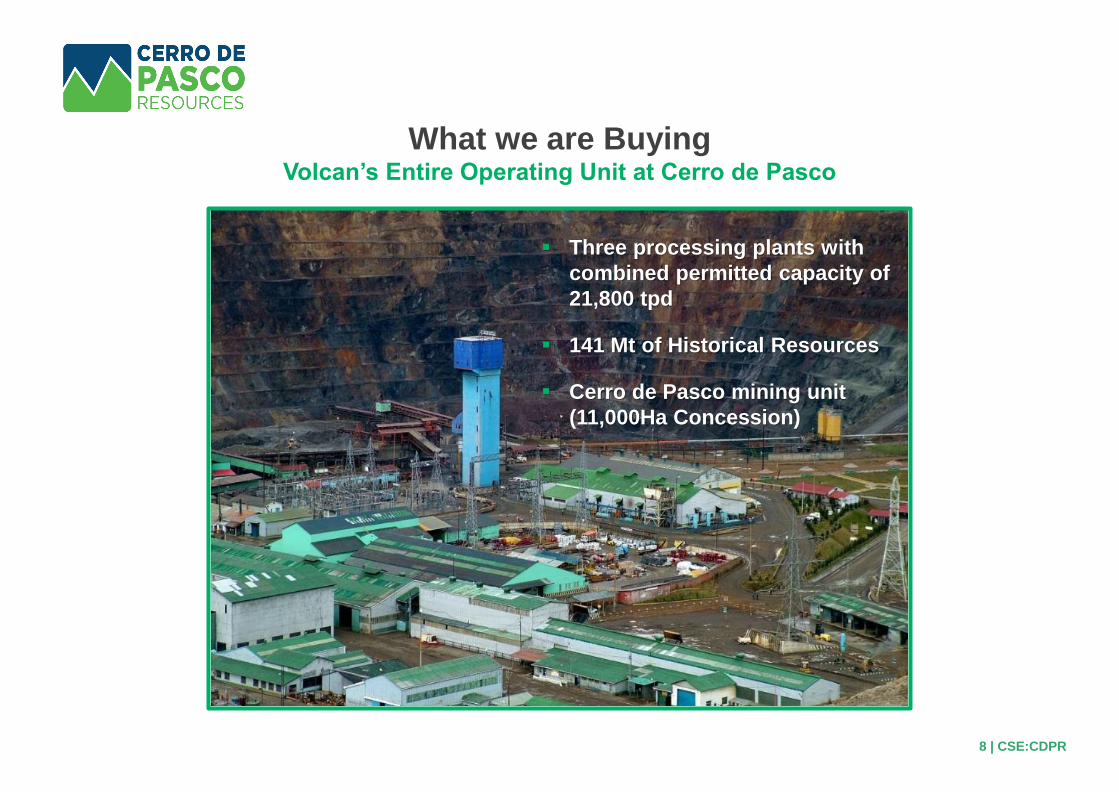

▪ Three processing plants with

combined permitted capacity of

21,800 tpd

▪ 141 Mt of Historical Resources

▪ Cerro de Pasco mining unit

(11,000Ha Concession)

What we are BuyingVolcan’s Entire Operating Unit at Cerro de Pasco

8 | CSE:CDPR

Sulphide Concentrators - Paragsha/San Expedito

Current Capacity: 7,000 tpd (from stockpiles)

Permitted Capacity: Paragsha – 17,500 tpd / San Expedito – 1,800 tpd

Replacement estimated value: USD240 M

2018 Production: Zn 11 Kt

Pb 4 Kt

Ag 0.4 million oz

2018 Revenues: USD 29 million

2019 Production: Zn 17 Kt

Pb 6 Kt

Ag 0.8 million oz

2019E Revenues: USD 53 million

(up 82%)

9 | CSE:CDPR

Oxide Plant

Replacement estimated value: USD 260 M

Current Capacity: 2,500 tpd

Oxide Leaching Plant Producing Doré Bars

2018 Production: Ag 3.4 million oz

Au 4,100 oz

2018 Revenues: USD 56 million

2019 Production: Ag 3.3 million oz

Au 16,300 oz

2019E Revenues: USD 78 million

(up 40%)

10 | CSE:CDPR

Ocroyoc Active Tailings Storage Facility (permitted)

Replacement estimated value: USD 40 M

11 | CSE:CDPR

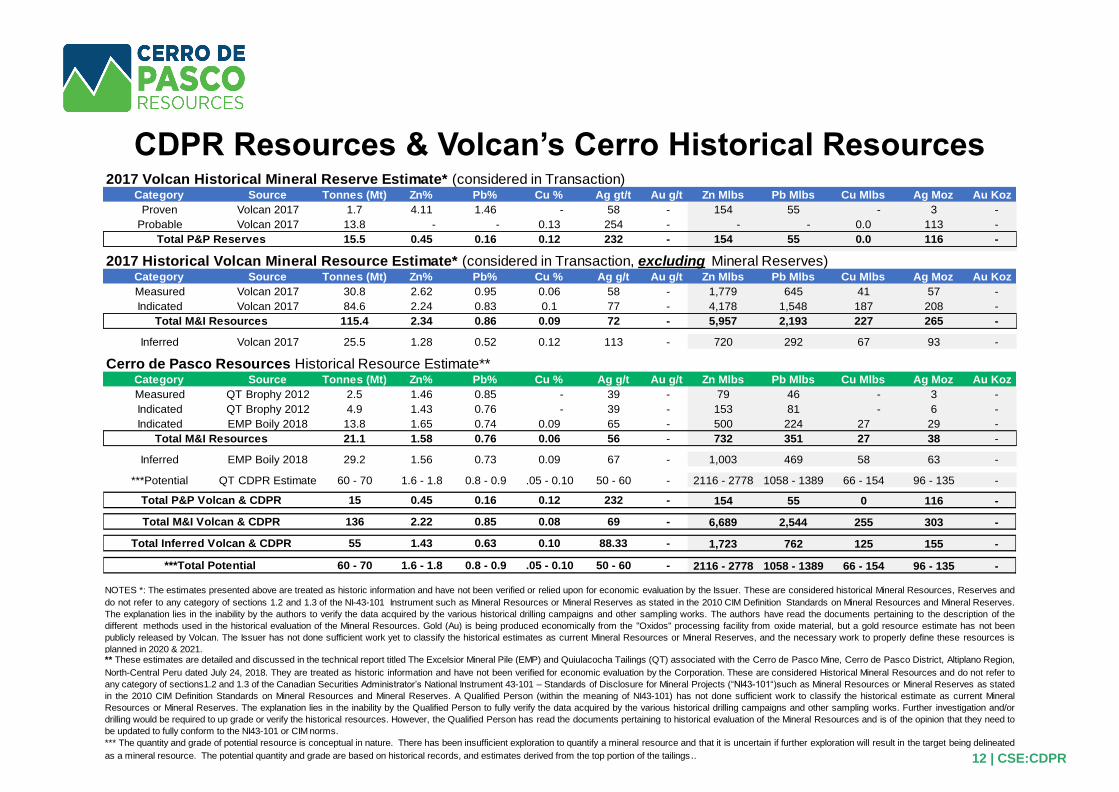

2017 Volcan Historical Mineral Reserve Estimate* (considered in Transaction)Category Source Tonnes (Mt) Zn% Pb% Cu % Ag gt/t Au g/t Zn Mlbs Pb Mlbs Cu Mlbs Ag Moz Au Koz

Proven Volcan 2017 1.7 4.11 1.46 - 58 - 154 55 - 3 -

Probable Volcan 2017 13.8 - - 0.13 254 - - - 0.0 113 -

15.5 0.45 0.16 0.12 232 - 154 55 0.0 116 -

2017 Historical Volcan Mineral Resource Estimate* (considered in Transaction, excluding Mineral Reserves)Category Source Tonnes (Mt) Zn% Pb% Cu % Ag g/t Au g/t Zn Mlbs Pb Mlbs Cu Mlbs Ag Moz Au Koz

Measured Volcan 2017 30.8 2.62 0.95 0.06 58 - 1,779 645 41 57 -

Indicated Volcan 2017 84.6 2.24 0.83 0.1 77 - 4,178 1,548 187 208 -

115.4 2.34 0.86 0.09 72 - 5,957 2,193 227 265 -

Inferred Volcan 2017 25.5 1.28 0.52 0.12 113 - 720 292 67 93 -

Cerro de Pasco Resources Historical Resource Estimate**Category Source Tonnes (Mt) Zn% Pb% Cu % Ag g/t Au g/t Zn Mlbs Pb Mlbs Cu Mlbs Ag Moz Au Koz

Measured QT Brophy 2012 2.5 1.46 0.85 - 39 - 79 46 - 3 -

Indicated QT Brophy 2012 4.9 1.43 0.76 - 39 - 153 81 - 6 -

Indicated EMP Boily 2018 13.8 1.65 0.74 0.09 65 - 500 224 27 29 -

21.1 1.58 0.76 0.06 56 - 732 351 27 38 -

Inferred EMP Boily 2018 29.2 1.56 0.73 0.09 67 - 1,003 469 58 63 -

***Potential QT CDPR Estimate 60 - 70 1.6 - 1.8 0.8 - 0.9 .05 - 0.10 50 - 60 - 2116 - 2778 1058 - 1389 66 - 154 96 - 135 -

15 0.45 0.16 0.12 232 - 154 55 0 116 -

136 2.22 0.85 0.08 69 - 6,689 2,544 255 303 -

55 1.43 0.63 0.10 88.33 - 1,723 762 125 155 -

60 - 70 1.6 - 1.8 0.8 - 0.9 .05 - 0.10 50 - 60 - 2116 - 2778 1058 - 1389 66 - 154 96 - 135 -

Total P&P Reserves

NOTES *: The estimates presented above are treated as historic information and have not been verified or relied upon for economic evaluation by the Issuer. These are considered historical Mineral Resources, Reserves and

do not refer to any category of sections 1.2 and 1.3 of the NI-43-101 Instrument such as Mineral Resources or Mineral Reserves as stated in the 2010 CIM Definition Standards on Mineral Resources and Mineral Reserves.

The explanation lies in the inability by the authors to verify the data acquired by the various historical drilling campaigns and other sampling works. The authors have read the documents pertaining to the description of the

different methods used in the historical evaluation of the Mineral Resources. Gold (Au) is being produced economically from the "Oxidos" processing facility from oxide material, but a gold resource estimate has not been

publicly released by Volcan. The Issuer has not done sufficient work yet to classify the historical estimates as current Mineral Resources or Mineral Reserves, and the necessary work to properly define these resources is

planned in 2020 & 2021. ** These estimates are detailed and discussed in the technical report titled The Excelsior Mineral Pile (EMP) and Quiulacocha Tailings (QT) associated with the Cerro de Pasco Mine, Cerro de Pasco District, Altiplano Region,

North-Central Peru dated July 24, 2018. They are treated as historic information and have not been verified for economic evaluation by the Corporation. These are considered Historical Mineral Resources and do not refer to

any category of sections1.2 and 1.3 of the Canadian Securities Administrator’s National Instrument 43-101 – Standards of Disclosure for Mineral Projects (“NI43-101“)such as Mineral Resources or Mineral Reserves as stated

in the 2010 CIM Definition Standards on Mineral Resources and Mineral Reserves. A Qualified Person (within the meaning of NI43-101) has not done sufficient work to classify the historical estimate as current Mineral

Resources or Mineral Reserves. The explanation lies in the inability by the Qualified Person to fully verify the data acquired by the various historical drilling campaigns and other sampling works. Further investigation and/or

drilling would be required to up grade or verify the historical resources. However, the Qualified Person has read the documents pertaining to historical evaluation of the Mineral Resources and is of the opinion that they need to

be updated to fully conform to the NI43-101 or CIM norms.

*** The quantity and grade of potential resource is conceptual in nature. There has been insufficient exploration to quantify a mineral resource and that it is uncertain if further exploration will result in the target being delineated

as a mineral resource. The potential quantity and grade are based on historical records, and estimates derived from the top portion of the tailings..

Total M&I Volcan & CDPR

Total M&I Resources

Total M&I Resources

Total P&P Volcan & CDPR

Total Inferred Volcan & CDPR

***Total Potential

CDPR Resources & Volcan’s Cerro Historical Resources

12 | CSE:CDPR

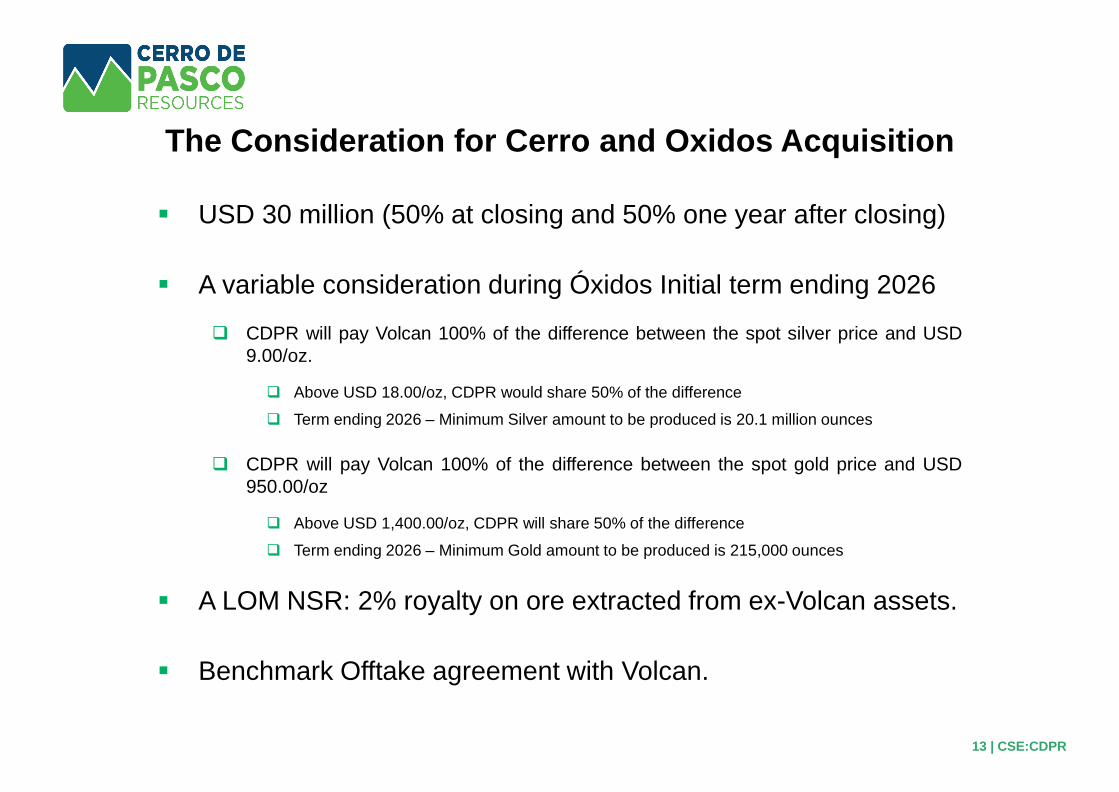

The Consideration for Cerro and Oxidos Acquisition

▪ USD 30 million (50% at closing and 50% one year after closing)

▪ A variable consideration during Óxidos Initial term ending 2026

❑ CDPR will pay Volcan 100% of the difference between the spot silver price and USD

9.00/oz.

❑ Above USD 18.00/oz, CDPR would share 50% of the difference

❑ Term ending 2026 – Minimum Silver amount to be produced is 20.1 million ounces

❑ CDPR will pay Volcan 100% of the difference between the spot gold price and USD

950.00/oz

❑ Above USD 1,400.00/oz, CDPR will share 50% of the difference

❑ Term ending 2026 – Minimum Gold amount to be produced is 215,000 ounces

▪ A LOM NSR: 2% royalty on ore extracted from ex-Volcan assets.

▪ Benchmark Offtake agreement with Volcan.

13 | CSE:CDPR

▪ CDPR has substantially larger above ground

inventories.

▪ Volcan has significant in-situ resources that would

require capital to develop.

▪ CDPR will generate substantially more capital to

develop the in-situ resources.

▪ Volcan is able to focus its efforts on its core assets

and still receives substantial profit through the

Oxidos variable consideration.

▪ Volcan and CDPR both see the grand vision for

Cerro de Pasco and agree that its large enough to

be its own dedicated entity.

Why is Volcan Selling? – They See Synergies…

14 | CSE:CDPR

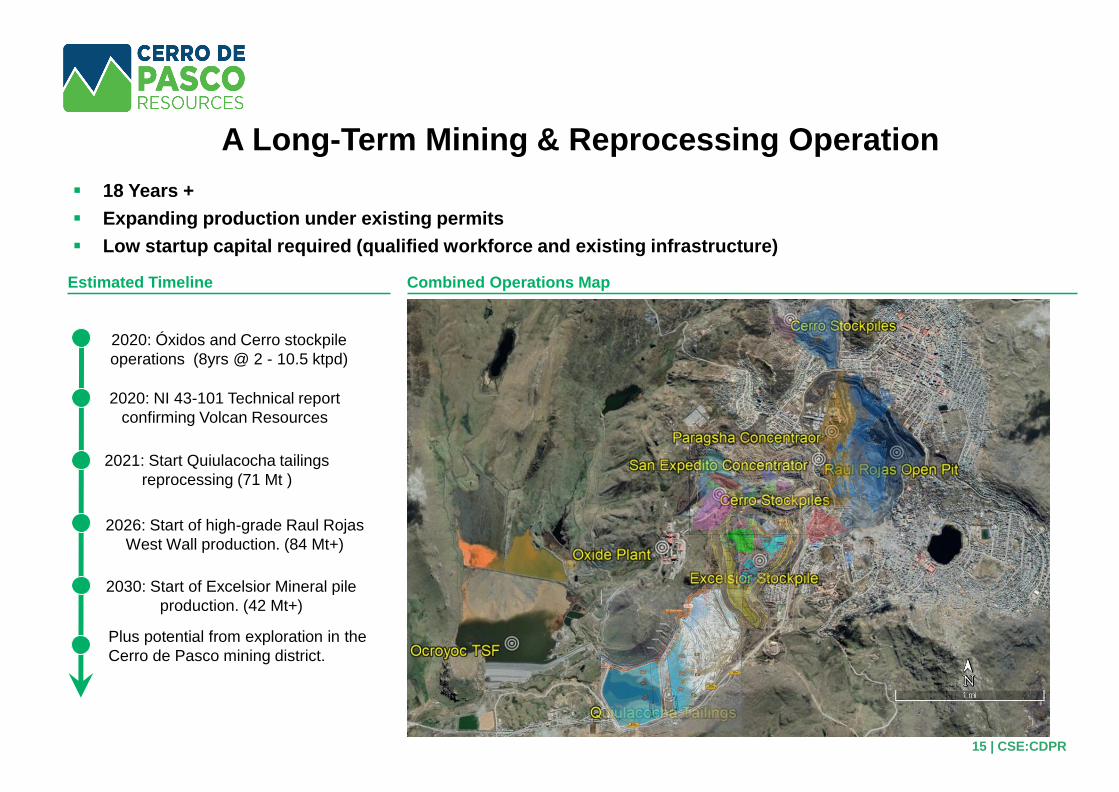

▪ 18 Years +

▪ Expanding production under existing permits

▪ Low startup capital required (qualified workforce and existing infrastructure)

2020: Óxidos and Cerro stockpile

operations (8yrs @ 2 - 10.5 ktpd)

2021: Start Quiulacocha tailings

reprocessing (71 Mt )

2026: Start of high-grade Raul Rojas

West Wall production. (84 Mt+)

2030: Start of Excelsior Mineral pile

production. (42 Mt+)

Plus potential from exploration in the

Cerro de Pasco mining district.

Combined Operations MapEstimated Timeline

2020: NI 43-101 Technical report

confirming Volcan Resources

A Long-Term Mining & Reprocessing Operation

15 | CSE:CDPR

West Wall + Exploration Upside

16 | CSE:CDPR

141 Mt of Historical Resources

A Rich Historical Mining Region with Outstanding Potential

▪ Multiple brownfield and greenfield targets exists

▪ Surface and underground drilling program for 2020 planned (10,000m)

▪ Geological mapping and sampling is planned for several areas of the project

17 | CSE:CDPR

Cerro de Paco mining unit (11,000Ha Concession)

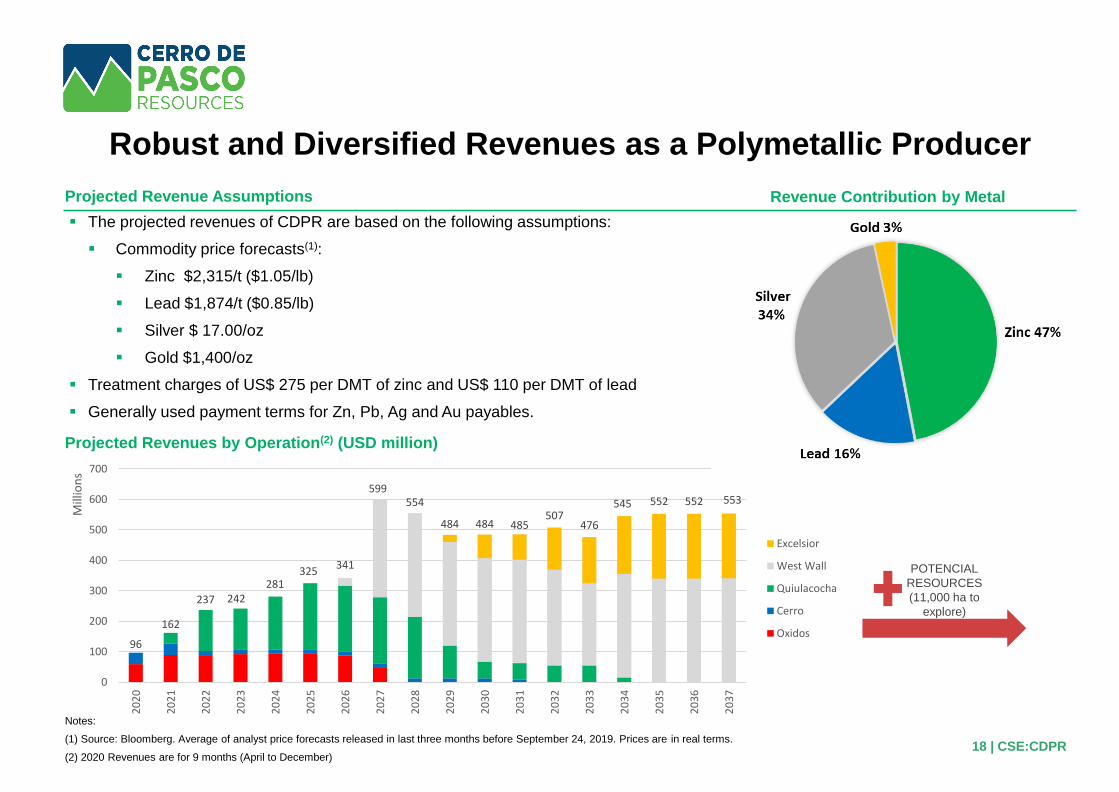

Projected Revenues by Operation(2) (USD million)

Projected Revenue Assumptions

▪ The projected revenues of CDPR are based on the following assumptions:

▪ Commodity price forecasts(1):

▪ Zinc $2,315/t ($1.05/lb)

▪ Lead $1,874/t ($0.85/lb)

▪ Silver $ 17.00/oz

▪ Gold $1,400/oz

▪ Treatment charges of US$ 275 per DMT of zinc and US$ 110 per DMT of lead

▪ Generally used payment terms for Zn, Pb, Ag and Au payables.

Notes:

(1) Source: Bloomberg. Average of analyst price forecasts released in last three months before September 24, 2019. Prices are in real terms.

(2) 2020 Revenues are for 9 months (April to December)

Robust and Diversified Revenues as a Polymetallic Producer

POTENCIAL

RESOURCES

(11,000 ha to

explore)

96

162

237 242281

325341

599554

484 484 485507

476

545 552 552 553

0

100

200

300

400

500

600

700

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

Mill

ion

s

Excelsior

West Wall

Quiulacocha

Cerro

Oxidos

Revenue Contribution by Metal

18 | CSE:CDPR

Projected EBITDA by Operation(2) (USD million)

Projected EBITDA Assumptions

▪ The projected EBITDA of CDPR are based on the following assumptions:

▪ Commodity price forecasts(1):

▪ Zinc $2,315/t ($1.05/lb)

▪ Lead $1,874/t ($0.85/lb)

▪ Silver $ 17.00/oz

▪ Gold $1,400/oz

▪ Treatment charges of US$ 275 per DMT of zinc and US$ 110 per DMT of lead

▪ Generally used payment terms for Zn, Pb, Ag and Au payables.

Notes: (1) Source: Bloomberg. Average of analyst price forecasts released in last three months before September 24, 2019. Prices are in real terms.

Significant, Robust & Diversified EBITDA as a Polymetallic Producer

POTENTIAL

RESOURCES

(11,000 ha to

explore)

19 | CSE:CDPR

1832

90 95

136

179 154

339 335

248236 239

278

240

305 314 314

367

28

0

50

100

150

200

250

300

350

400

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

Mill

ion

s

Excelsior

West Wall

Quiulacocha

Cerro

Oxidos

Chair Professor in Applied

Geochemistry at the Division of

Geosciences and Environmental

engineering Luleå University of

Technology, Sweden.

Clients include CODELCO, Anglo

American, BHP Billiton, Southern

Peru Copper Corporation, Mineria

Activa among others, as well

government agencies in Peru, Chile,

and Colombia.

20 | CSE:CDPR

Strategic Advisor - Bernhard Dold PhD

Environmental Engineering, Remediation

Specialist in:

Remediation, with focus on acid rock

drainage in mine waste and ore deposit

environments and its application for a

more sustainable mining operation.

21 | CSE:CDPR

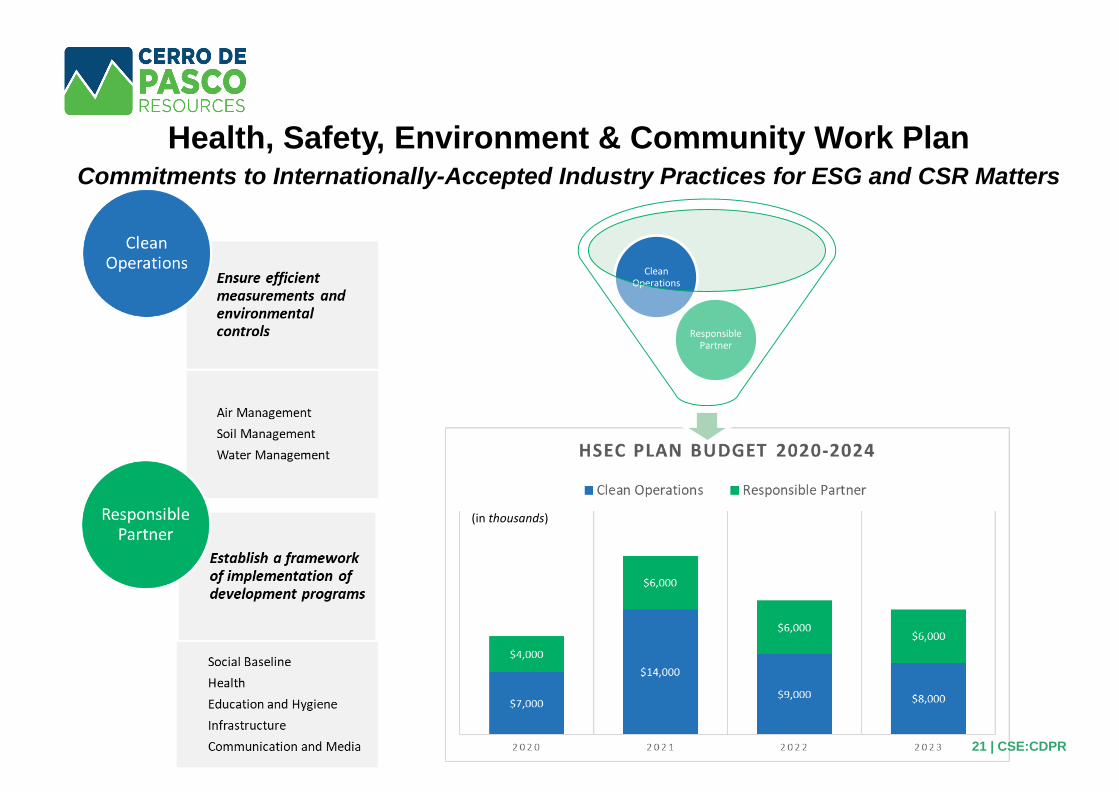

Responsible Partner

Clean Operations

Health, Safety, Environment & Community Work PlanCommitments to Internationally-Accepted Industry Practices for ESG and CSR Matters

(in thousands)

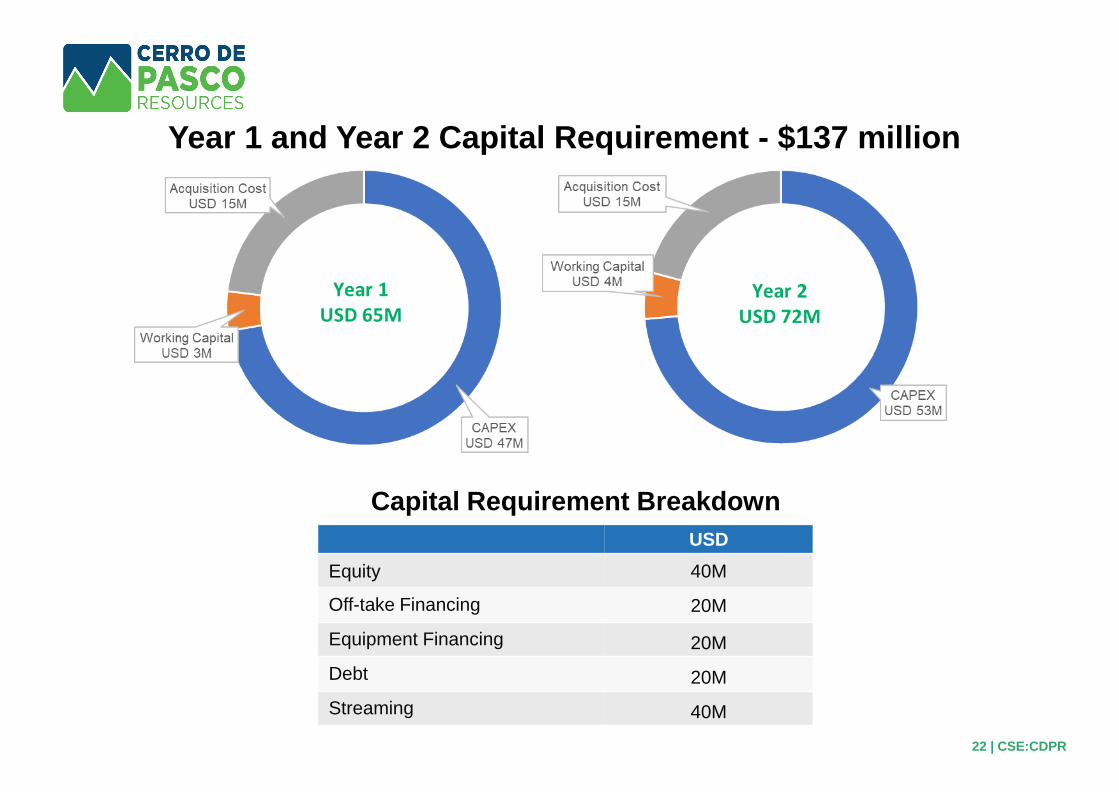

Year 1 and Year 2 Capital Requirement - $137 million

22 | CSE:CDPR

Capital Requirement Breakdown

USD

Equity 40M

Off-take Financing 20M

Equipment Financing 20M

Debt 20M

Streaming 40M

Cerro de Pasco Capital Structure

Listed on CSE – To seek listings on TSX and BVL

Number of Shares

Issued *253.2M

Warrants / Options 12.1M

Fully diluted 265.3M

Market capitalization ~$125M

Shares held by insiders 128.8M

Shares held in escrow * 176.3M

Release Dates

Percentage

Released

Number of Shares

Released

Insiders

Number of shares

Released

November 1, 2018 2% 3.5M 2.6M

February 1, 2019 5% 8.8M 6.4M

August 1, 2019 15% 26.5M 19.3M

February 1, 2020 15% 26.5M 19.3M

August 1, 2020 15% 26.5M 19.3M

February 1, 2021 15% 26.5M 19.3M

August 1, 2021 15% 26.5M 19.3M

February 1, 2022 the remaining

escrowed securities

31.5 M 23.3M

* On October 5, 2018, 176.3 M Shares were issued to the former securityholders of

Cerro de Pasco Resources pursuant to the Merger are held in Escrow:

23 | CSE:CDPR

Neil T. Ringdahl, President

Mr. Neil Ringdahl serves as the President of CDPR. Mr. Ringdahl is a South African mining engineer with 25

years of executive and operational experience in Latin America, Africa and Europe. Mr. Ringdahl has held

executive management positions in companies including Volcan Compañía Minera (2007/2009), Anglo

Platinum, Golden Star Resources, Korea Zinc Orvana, and is the COO of Ascendant Resources.

University of the Witwatersrand, BSc. Engineering Honours (Mining).

Manuel Rodriguez Mariátegui, Executive Director & Representative

Mr. Manuel Rodríguez Mariátegui is an executive with more than 30 years of management experience in the

mining sector. Mr. Rodriguez Mariategui is a Shareholder of Sociedad Minera Austria Duvaz, a company with

over 100 years of mining history and over 700 workers. Also acts as CEO of Minera Valor, and President of the

Investment and Risk Committee of Inversiones Don Lizandro.

Saint Mary's University in San Antonio Texas, Business Administration- International Business.

Executive Management

Steven Zadka, Executive Chairman

Mr. Steven Zadka serves as the Executive Chairman of Cerro de Pasco. Mr. Zadka is a metals and mining

investment banker with 15 years+ of transactional and executive management experience in Latin America,

USA and Canada. Mr. Zadka is a founding partner of CDPR

Bernard Baruch College in New York, BSc. in Finance and Real Estate development.

Guy Goulet, Executive Director & CEO

Mr. Guy Goulet serves as CEO of CdPR with more than 30 years of experience in the mining sector. Mr. Goulet

has led numerous listed investments including a landmark lithium metal initiative and the largest water

treatment company in Canada. Over the course of his career, Mr. Goulet has raised over USD200 million in

equity capital.

École Polytechnique de Montréal, Geological Engineering.

24 | CSE:CDPR

Shane Whitty, VP Exploration & Technical Services

Mr. Shane Whitty is an experienced geology manager with 18 years of experience in Peru, Colombia and Ireland. Prior to join CdPR,

Mr. Whitty was the Mine Geologist of Volcan´s mining unit Cerro de Pasco, Geology Manager of the Soto Norte Project, Senior Project

Geologist of the Breca Group, Chief Technical Engineer of Ancash Limited Group and Production Geologist of ARCON International

Resources Ltd. Camborne School of Mines University of Exeter, B. Eng. (Hons) Industrial Geology.

Diederik Duvenage, VP Operations & Projects

Mr. Diederik Duvenage is a South African mining consultant with 28 years of mining experience in Latin America and Africa. Mr.

Duvenage has broad technical and project management background in both open pit and open cast mines. Mr. Duvenage has held

senior and executive management positions with both public and private companies including Volcan Companía, Anglo Coal, Anglo

Platinum, MineraTahoe Resources (Shahuindo Mine and Escobal Mina San Rafael), Stracon, ApogeeSilver, Ancash Mines and Golden

Star Resources.

Robert Boisjoli, CFO

Mr. Robert Boisjoli is a Fellow Chartered Professional Accountant with over 30 years of operational and advisory experience. Mr. Boisjoli

is the CEO of AKESOGEn, Inc., Chairman of Palos Management, managing director of Atwater Financial Group and partner at Robert

Boisjoli & Associates. Concordia University, B. Commerce, Graduate Diploma in Accountancy.

John Grewar, VP Processing Operations

Mr. John Grewar serves as VP Process Operations with 40 years experience in gold and base metal metallurgy in South Africa, Latin

America and Europe. Mr. Grewar has held senior and executive management positions with both public and private companies including

Anglo Vaal, Anglo Gold – Vaal Reefs and ERGO, Volcan Companía Minera, Korea Zinc, Apogee Silver, Orvana and Ascendant

Resources. Technicon Witwatersrand – Diploma in Extraction Metallurgy.

Edwin Mitchell, VP Safety, Health, Environment & Community

Mr. Edwin Mitchell has over 20 years of international experience in Environment, Health and Safety, Permitting, Community and

Stakeholder Relations. Mr. Mitchell worked previously for Southern Peaks Mining LP, Compañía Minera Condestable, and Compañía

Minera Quiruvilca in Peru and has operational and advisory experience with Walsh Peru, Ecology & Environment, Vector (Ausenco) the

United Nations Development Program (UNDP) in West Africa. BSc. Environmental Science (Professor Van Hall Institute); MA Public

Administration and Management Science (Catholic University Nijmegen - KUN), The Netherlands.

Executive Management (Cont’d)

25 | CSE:CDPR

Board of Directors John G. Booth, LLM, Independent Director

Mr. Booth has over 30 years of international experience in finance, law, ESG and corporate governance of natural resource

management. Mr. Booth has worked as a lawyer, banker, strategy consultant and fund manager with firms as Merrill Lynch,

ICAP, CEDEF and ABN AMRO, CIBC, World Bank, Climate Change Capital and Conservation Finance International. Mr. Booth

holds a BSc. in biology and environmental science, Canadian and US law degrees and a Master in International Finance, Tax

and Environmental Law and is a lecturer in ESG in the graduate business program at the University of London. Mr. Booth

serves on the Boards of four other publicly listed companies. Mr. Booth chair the Audit and Governance Committee.

David Shaw, Ph.D, Independent Director

Mr. Shaw has almost four decades of experience in the technical and financial sectors of the mining and oil and gas resource

industries. He has specialized in the investigation of the structural controls of mineral deposits, in the financial side he has

focused on financial and risk analysis of resource project investment. After graduating from Carleton University, Ottawa, with a

Ph.D. in Structural Geology, he was employed by Chevron Resources Canada as an in-house structural consultant in both the

mining and hydrocarbon divisions. He founded the Resource Research Department at Charlton Securities Ltd before assuming

the position as Senior Analyst at Yorkton Securities. Since the mid 1990’s he has worked as an independent consultant and

actual serves on the Boards of three other publicly listed resource companies. Mr. Shaw is a member of the Governance

Committee and assisted the whistle-blowing reporting.

Frank Hodgson, Independent Director

Mr. Hodgson is an investor with over 30 years´ experience in the Central London residential property market as a developer

where he dealt with sensitive environmental and social issues. Mr. Hodgson pioneered the “Swale Project”, a major scheme in

Kent with partners Bovis, Medway Port Authority, Bowater and UK Paper. Mr. Hodgson is a corporate investor via Small Private

Equity Companies, based in Mayfair, London. Mr. Hodgson is responsible of the whistle-blowing reporting and he is a member

of the Audit and Governance Committees.

Keith Brill, Independent Director

Mr. Brill is a management consultant with Gartner Inc., the world´s leading research and advisory company since 2016. Before

joining Gartner, Mr. Brill worked as a principal consultant for PA Consulting Group, a leading UK-based global consulting firm.

Mr. Brill holds a BSc. Summa Cum Laude major in Economics and Finance, minor in Spanish from the Moore School of

Business, University of South Carolina. Mr. Brill also holds an IMBA from Moore School of Business, University of South

Carolina. Mr. Brill is a member of the Audit Committee.

Note: Mr. Zadka, Mr. Goulet and Mr. Rodriguez Mariátegui are members of the board as executive directors.26 | CSE:CDPR

FOR A BRIGHTER FUTURE

203 – 22 Lafleur Av. N Av. Santo Toribio

Saint-Sauveur, Québec No. 115, Of. 702

J0R 1R0, CANADA San Isidro, Lima - PERÚ

+1.579.476.7000 +1.51 .712.3731 or 712.3729

APPENDIX

28 | CSE:CDPR

Expecting Improvement of Equity Value Post TransactionThe table below represents a peer group analysis of equity value based on in-situ resources. CDPR’s resource estimate in this table, are based on the figures foundon page 15 of this slide deck. This peer group analysis produces a Mean, Median and Mean (less outliers) per silver and silver equivalent ounce and based onrespective market capitalizations of each company. Using the Global Resources - AgEq Mean (less outliers), the comparison would suggest a CDPR share pricevalue at 32x the current level.

Silver Price (US$/ oz) $18.09

Gold Price (US$/ oz) $1,549.00 $13.52 $5.05

Zinc Price (US$/ lb) $1.05 $8.34 $3.61

Lead Price (US$/ lb) $0.87 $4.44 $1.96

Copper Price (US$/ lb) $2.77

per share M of shares US$ M # Ag AgEq(3) Ag AgEq(3) Ag AgEq(3) Ag AgEq(3) Ag AgEq(3) Ag AgEq(3) (%)

Alexco Resource Corp. AXU.TO CAD 2.85$ 118.7 260.2$ Yukon 5 30 41 $8.55 $6.28 84 126 $3.12 $2.07 108 162 $2.41 $1.61 67%

Americas Gold and Silver Corp. USA.TO CAD 4.01$ 82.6 254.8$ Mexico & Idaho 4 32 109 $7.92 $2.35 48 125 $5.33 $2.03 84 200 $3.03 $1.28 42%

Avino Silver & Gold Mines Ltd. ASM.TO CAD 0.84$ 76.0 49.1$ Mexico 2 - - 26 48 $1.87 $1.03 40 71 $1.23 $0.69 56%

Couer Mining Inc. CDE USD 7.70$ 240.5 1,852.0$ Global 5 171 438 $10.81 $4.23 229 453 $8.10 $4.09 364 825 $5.08 $2.25 44%

Endeavour Silver Corp. EDR.TO CAD 3.07$ 139.9 330.4$ Mexico 5 47 88 $7.03 $3.76 22 43 $14.81 $7.71 84 131 $3.95 $2.52 64%

First Majestic Silver Corp FR.TO CAD 15.52$ 204.8 2,444.6$ Mexico 7 103 171 $23.75 $14.30 150 260 $16.26 $9.41 262 472 $9.34 $5.17 55%

Fortuna Silver Mines Inc. FVI.TO CAD 5.24$ 160.3 646.0$ Latin America 3 46 216 $14.17 $2.99 6 34 $105.91 $18.85 39 75 $16.61 $8.60 52%

Great Panther Mining Ltd. GPR.TO CAD 0.74$ 311.4 177.2$ Mexico, Peru 3 - - 15 53 $11.52 $3.37 31 100 $5.76 $1.77 31%

Hecla Mining Company HL USD 3.35$ 495.5 1,660.1$ USA, Mexico 9 191 617 $8.69 $2.69 208 1,012 $7.97 $1.64 465 1,865 $3.57 $0.89 25%

Hochschild Mining plc HOC.L GBP 1.75$ 510.6 1,169.9$ Latin America 4 46 106 $25.43 $11.04 178 1,035 $6.56 $1.13 331 1,387 $3.54 $0.84 24%

Pan American Silver Corp. PAAS.TO CAD 30.48$ 209.6 4,914.0$ Latin America 8 557 1,495 $8.82 $3.29 797 1,708 $6.17 $2.88 1,100 2,831 $4.47 $1.74 39%

SSR Mining Inc. SSRM.TO CAD 24.06$ 123.1 2,277.2$ Americas 7 39 374 $58.84 $6.10 629 1,279 $3.62 $1.78 691 1,468 $3.30 $1.55 47%

Cerro De Pasco Resources Inc. CDPR.CN CAD 0.500$ 253.3 97.4$ Peru 1 116 128 $0.84 $0.76 303 852 $0.32 $0.11 689 1,610 $0.14 $0.06 43%

$17.40 $5.70 $15.93 $4.67 $5.19 $2.41

12 $9.82 $3.99 $7.27 $2.47 $3.76 $1.67

62 $13.52 $5.05 $8.34 $3.61 $4.44 $1.96

Notes:

CAD 1.300135000

GBP 0.764575700

Date: 01/03/2020

Global Resources (4)

MC/oz

5. Silver Exposure = percentage of silver equivlent global resource that is silver (Ag/AgEq).

Sources: Quote Media, Market XLS, Company Reports, CDPR Estimates

2. Market Capitalization in US$ / 1 USD =

3. AgEq = silver equivalent on gross basis (no recovery factors) using current spot metal prices.

1. Priced in local currency.

4. Global resource (not a compliant measure ) include 43-101 compliant Measured, Indicated and Inferred resources.

Contained Silver

(Moz)

Silver

Exposure (5)

MEAN (US$/oz):

MEDIAN (US$/oz):

ADJUSTED MEAN - less outliers (US$/oz):

MC/oz MC/oz

Measured & Indicated (US$/oz)

Global Resources (4) (US$ / oz)

Measured & Indicated (US$/oz)

Global Resources (4) (US$ / oz)

Proven + Probable Reserves Measured & Indicated Resources

SummaryMC In Situ - Silver MC in Situ - Silver Equivalent (3)

# of companies (not including CDPR)

# of projects

Local

Currency

Price

(1)TickerCompany Name

Shares

O/S

Market

Cap. (2)

Project

Location(s) & (#)

Contained

Silver

Contained

Silver

Proven & Probable (US$/ oz)Proven & Probable (US$/ oz)

29 | CSE:CDPR

Expected Annual Average Payable Metal Production*

▪ 33.5 Moz/yr Silver equivalent metal

▪ Zinc 255 Mlbs/yr

▪ Lead 107 Mlbs/yr

▪ Silver 11 Moz/yr

▪ Gold 31 koz/yr**

▪ Figures exclude significant upside in exploration opportunities, pyrites, copper

and other metals production still to be fully determined

18 years+

*NOTE: Assumes metal prices of $1.05/lb Zn, $0.85/lb Pb, $17.00/oz Ag, $1,400/oz Au over LoM, Note that all financials

are subject to final negotiation of the offtake agreement & HSEC plan with Volcan, and possible adjustment to taxation.

**NOTE: Currently projected over the first 8 years only from oxides

30 | CSE:CDPR

4,4%

3,5%

2,2%

3,0%

1,2%

4,0%3,7%

2,3%

3,1%

2,2%

Peru Colombia Mexico Chile Brazil

Avg. 2009-2018

Avg. 2019P-2023P

2,8%

3,8% 4,1%

5,7% 5,9%

2,0%

3,1% 3,2% 2,9%

3,9%

Peru Colombia Mexico Chile Brazil

Avg. 2009-2018

Avg. 2019P-2023P

132 135

190

251

309

1 2 3 4 5

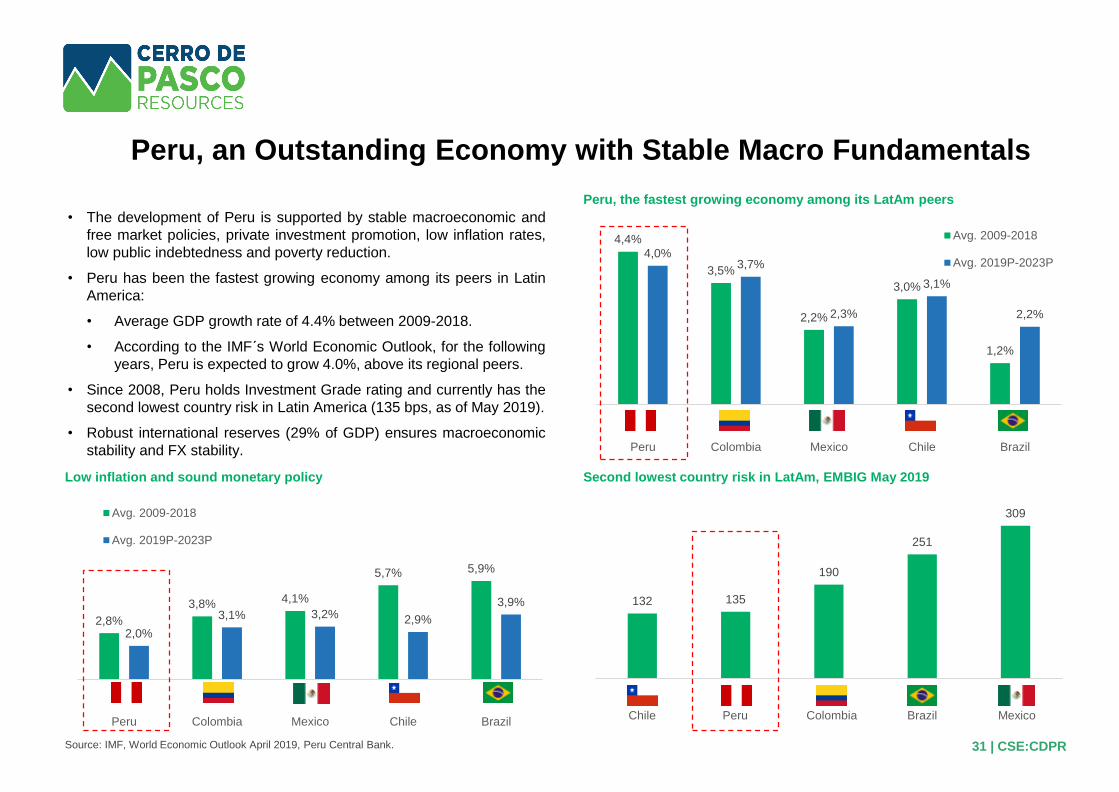

• The development of Peru is supported by stable macroeconomic and

free market policies, private investment promotion, low inflation rates,

low public indebtedness and poverty reduction.

• Peru has been the fastest growing economy among its peers in Latin

America:

• Average GDP growth rate of 4.4% between 2009-2018.

• According to the IMF´s World Economic Outlook, for the following

years, Peru is expected to grow 4.0%, above its regional peers.

• Since 2008, Peru holds Investment Grade rating and currently has the

second lowest country risk in Latin America (135 bps, as of May 2019).

• Robust international reserves (29% of GDP) ensures macroeconomic

stability and FX stability.

Source: IMF, World Economic Outlook April 2019, Peru Central Bank.

Peru, the fastest growing economy among its LatAm peers

Low inflation and sound monetary policy Second lowest country risk in LatAm, EMBIG May 2019

Peru, an Outstanding Economy with Stable Macro Fundamentals

PeruChile Colombia Brazil Mexico

31 | CSE:CDPR

6

2 2 2

3

4

Gold Copper Silver Zinc Lead Tin

92,9991,47

90,00

88,38

81,55

Source: Fraser Institute, Ministry of Energy and Mines (MEM).

Peru is a leading producer of several commodities

Peru, an attractive destination for investments ranks 14th out of 83

destinations for investment attractiveness Selected International companies with operations in Peru across commodities

Peru, a World Class Producer of Base & Precious Metals with a Friendly Investment Environment

Ba

se

Me

tals

Pre

cio

us

Me

tals

Peru

14th

……QuebecSaskatchewanWestern

AustraliaNevada

6th

2nd 2nd 2nd

3rd

4th

• Peru is a leading and established mining country: top producer of copper, silver,

zinc, lead, tin and gold.

• The Fraser Institute ranked Peru as 14th destination for investment in mining in

2018, improving 5 positions from 2017.

• Peru has a promotional investment framework for mining in place for several

decades, including:

• No discrimination between national and foreign investments.

• Access to stability agreements.

• The Mining Law provides for special incentives for mining investors depending

on project size (capacity and CAPEX).

• Growing trend in mineral reprocessing projects: Minera Shouxin (China) invested

USD 230 million in a 20ktpd tailings reprocessing project (Marcona mine, 2017)

and Minsur is investing USD 140 million in B2 tailings reprocessing project (San

Rafael mine, with estimated start in IVQ 2019).

32 | CSE:CDPR