food beverage information project 2011 markets stream –global · some form of the “food to...

TRANSCRIPT

This information was prepared by Coriolis solely for the use of our client; it is not to be relied on by any third party without prior written consent.

Food & Beverage Information Project 2011Markets Stream – Global

Final ReportOctober 2011 – v1.21

www.foodandbeverage.govt.nz

Coriolis is a strategic management consulting andmarket research firm

We work with organisations to help them grow. For corporations, thatoften means developing strategies for revenue growth. Forgovernments, it means working on national economic development. Fornon‐profits, it means helping to grow their social impact.

We address all the problems that are involved in growth: strategy,marketing, pricing, innovation, new product development, new markets,organisation, leadership, economic competitiveness.

We bring to our clients specialised industry and functional expertise.We invest significant resources in building knowledge. We see it as ourmission to bring this knowledge to our clients and we publish much of itfor the benefit of others.

A hallmark of our work is rigorous, fact‐based analysis, grounded inproven methodologies. We rely on data because it provides clarity andaligns people.

However, we deliver results, not reports. To that end, we work side byside with our clients to create and implement practical solutions.

The Coriolis name

The coriolis force, named for French physicist Gaspard Coriolis (1792‐1843), may be seen on a large scale in the movement of winds andocean currents on the rotating earth. It dominates weather patterns,producing the counterclockwise flow observed around low‐pressurezones in the Northern Hemisphere and the clockwise flow around suchzones in the Southern Hemisphere. To us it means understanding thebig picture before you get into the details.

PO Box 90‐509, Victoria Street West, Auckland 1142, New ZealandTel: +64 9 623 1848 www.coriolisresearch.com

The objective of this report is to provide a factual source of high quality information on the current situation in the New Zealand Food and Beverage export markets for four audiences:

‐ Investors (domestic or international)‐ Industry participants (firms & individuals)‐ Government (across all roles and responsibilities)‐ Scientific researchers (academic, government & firm)

It creates a common set of facts and figures on the current situation in the industry.

It draws conclusions on potential industry strategic directionsand highlights opportunities for further investment and identifies how New Zealand can potentially triple exports by 2025

It forms a part of the wider Food & Beverage Information Project and will be updated annually.

PAGE 3

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

GLOSSARY OF TERMS

PAGE 5

This report uses the following acronyms and abbreviations

A$/AUD Australian dollar NA/ME/CA North Africa / Middle East / Central Asia

ABS Absolute change NZ New Zealand

ANZSIC AU/NZ Standard Industry Classification NZ$/NZD New Zealand dollar

AU Australia R&D Research and Development

Australasia Australia and New Zealand S Asia South Asia (Indian Subcontinent)

b Billion SE Asia South East Asia

CIF Cost, Insurance and Freight S.H./N.H. Southern/Northern Hemisphere

CAGR Compound Annual Growth Rate SS Africa Sub‐Saharan Africa

C/S America Central & South America (Latin America) T/O Turnover

CRI Crown Research Institute US/USA United States of America

CY Calendar year (ending Dec 21) US$/USD United States dollar

E Asia East Asia UK United Kingdom

EBITDA Earnings before interest, tax, depreciation and amortization

YE/YTD Year ending/Year to date

FOB Free on Board Sources

FY Financial year (of firm in question) AR Annual report

£/GBP British pounds Ce Coriolis estimate

HS Codes Harmonised System Codes for commodity classifications

Ci Coriolis interview

JV Joint venture K Kompass

m Million Ke Kompass estimate

n/a Not available/not applicable ws Website

METHODOLOGY & DATA SOURCES

PAGE 6 * Food and Agriculture Organisation of the United Nations

Data was from a variety of sources, and has a number of identified limitations

- This report uses a range of information sources, both qualitative and quantitative.

- The numbers in this report come from multiple sources. While we believe the data are directionally correct, we recognise the limitations in what information is available. - In many cases different data sources disagree (e.g.

Statistics New Zealand vs. FAO* vs. UN Comtrade). - Many data sources incorporate estimates of industry

experts. - As one example, in many cases, the value and/or volume

recorded as exported by one country does not match the amount recorded as being received as imports by the counterparty [for understood reasons].

- In addition, in some places, we have made our own clearly noted estimates.

- Coriolis has not been asked to independently verify or audit the information or material provided to it by or on behalf of the Client or any of the data sources used in the project.- The information contained in the report and any

commentary has been compiled from information and material supplied by third party sources and publicly available information which may (in part) be inaccurate or incomplete.

- Coriolis makes no representation, warranty or guarantee, whether express or implied, as to the quality, accuracy, reliability, currency or completeness of the information provided in the report.

- All trade data analysed in all sections of the F&B Information project are calculated and displayed in US$. This is done for a range of reasons:1. It is the currency most used in international trade2. It allows for cross country comparisons (e.g. vs. Denmark)3. It removes the impact of NZD exchange rate variability4. It is more comprehensible to non‐NZ audiences (e.g. foreign

investors)5. It is the currency in which the United Nations collects and

tabulates global trade data

- The opinions expressed in this report represent those of the industry participants interviewed and the authors. These do not necessarily represent those of Coriolis Limited or the New Zealand Government.

- If you have any questions about the methodology, sources or accuracy of any part of this report, please contact Tim Morris, the report’s lead author at Coriolis, on +64 9 623 1848

SPECIFIC UN COMTRADE DATA LIMITATIONS

- The data presented is accurate to its source, but not necessarily to New Zealand data

- The data analysed in this report is based on data provided by member governments to the United Nations.

- However, in the data the reported exports of one country regularly do not agree with the reported imports of another (in both volume and value).

- As the UN says: “Imports reported by one country do not coincide with exports reported by its trading partner. Differences are due to various factors including valuation (imports CIF, exports FOB), differences in inclusions/ exclusions of particular commodities, timing etc.”

- As a simple example, New Zealand paperwork submitted to New Zealand customs says New Zealand sent NZ$202,569,027 worth of dairy to Sri Lanka in 2010 but Sri Lanka (the receiving country) says it only received US$63,365,322 in 2010. There are a wide range of reasons why this could be the case.

- Q: Why don’t you just use NZ data?- If we use only New Zealand data, we can not calculate New Zealand's share of

Sri Lanka's imports. Using the UN data we can then assess how well New Zealand is performing, determine the competition and see how much growth is available.

- The interesting/useful information is not that we send US$420m to Singapore, but rather than this amounts to $84/person and this is only 5% of all their F&B imports. France sends twice as much as us. None of that is visible if we work with New Zealand export stats rather than country import stats.

- Our customs data only shows where the person filling out the export documentation states it is going and approximates its worth. As New Zealand does not charge duties on exports, value is more important on import documentation than export. Value is an estimate 2+ months prior to sale in market and is close but almost inevitably wrong.

- In addition where product ends up, can in many cases be a different from where the ship is going.

- Sending/receiving data is generally very accurate for some markets (e.g.

Australia, Japan), with some slight variance based on what is measured (FOB, CIF, etc.) and timing (product sent in December, arrives January)

- Aggregate global received volume is close enough to New Zealand’s sent volume. Disagreement is on where it went and how much it was worth.

- New Zealand data is not always correct. For example, New Zealand kiwifruit and avocado export data to Australia is incorrect. The Australian data is more accurate.

- As another example, New Zealand appears to send a lot to countries with ports, but little to landlocked countries. However, many countries not on a coast believe they receive product from New Zealand that New Zealand Customs do not know was sent.

- If New Zealand is doing very well in Central Asia it isn't necessarily going to show up in New Zealand export paperwork. Many of these countries receive four times as much from New Zealand as New Zealand Customs thinks is sent to them.

- For more details on the issue, the dataset methodology is available here:- http://unstats.un.org/unsd/trade/methodology%20IMTS.htm

- There is extensive discussion of the issue in the UN International Trade Statistics Knowledgebase:

- http://unstats.un.org/unsd/tradekb/Knowledgebase/

- If you have a country level concern the explanatory notes by country are here:- http://comtrade.un.org/db/mr/daExpNotebyRepYear.aspx

PAGE 7

The United Nations Comtrade database has specific important limitations around data

Structure of the New Zealand Food & Beverage Information Project(2011)

F&B INFORMATION PROJECTThe New Zealand Food & Beverage Information Project is designed to be the foundation of facts and figures on which a range of audiences can build

PAGE 8 Note: Every year two subsectors are completed in more detail. Seafood and Nutraceuticals in 2011

Dairy Sector

Meat Sector

ProduceSector

Seafood Sector

NutraceuticalsSector

Processed Foods Sector

Beverages Sector

Investor’s Guide

Global Markets

Overview

Sectors

Industry Snapshot

Markets High Potential Market Profiles

FirmsInvestors Government

Structure of the New Zealand Food & Beverage Information Project(2011)

MARKETS ANALYSISThis analysis of New Zealand global markets forms a part of the wider Food & Beverage Information Project

PAGE 9

FirmsInvestors Government

Dairy Sector

ProduceSector

Seafood Sector

NutraceuticalsSector

Processed Foods Sector

Beverages Sector

Investor’s GuideOverview

Sectors Meat Sector

Industry Snapshot

High Potential Market ProfilesMarkets Global Markets

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

OVERVIEW – THE PATH FORWARD

Situation- In the early days of its founding New Zealand was, conceptually

speaking, Britain’s farm. The country was the same size at the United Kingdom, but with a fraction of the population. The country produced staples of the English diet such as lamb, beef, butter, cheese and apples. These were produced in large quantities on a counter‐seasonal basis for shipment to the “home country” and other rich Western markets.

- There is the perception by many today that this is still the case. If you were to ask the average person on the street in New Zealand today where the country’s food exports go, you would still get some form of the “Food to Britain” narrative. Many smaller food and beverage manufacturers, in our experience, would also articulate something similar.

- Reality is very different. New Zealand is in the middle of a fundamental transition from feeding Westerners to feeding the Asia‐Pacific region. This transition is driving rapid change in the New Zealand food industry in what is being produced and where it is being sold. Key exports today include:- Milk powder for Asian dairy factories, used to produce

yoghurt and other dairy products- Frozen french fries, frozen hamburgers, and processed

cheese for fast food restaurants in South East Asia - Gold kiwifruit for Asian consumers

- Imagine an alternative reality where New Zealand was colonised not by England, but rather Japan or China. In this reality, New Zealand would produce very different foods and beverages. This is what the future potentially looks like.

Potential future strategic direction

- The export strategy of the typical New Zealand food and beverage firm thirty years ago was simple: go to the UK and sell to Sainsbury and Tesco.

- This report presents a very different export growth pathway for the New Zealand food & beverage exporter of today:1. Ensure you are the #1 or #2 in your category in NZ before

considering export2. Start in Australia: focus on winning “next door” and

creating a business 5x the size of NZ; consider strategic acquisitions to achieve this goal

3. Take the Pacific Islands seriously; in aggregate a large market where New Zealand has a good share

4. SE Asia is the next logical market to target; start in Singapore and expand to the other countries in the region

5. In East Asia, start in Hong Kong and Taiwan, then expand to the larger economies

This report measures and benchmarks New Zealand’s food & beverage export performance across key global regions and countries; it also paints a picture of the path forward

PAGE 11

New Zealand F&B trade value: exports vs. imports(US$b; 1965‐2010)

NZ F&B TRADE BALANCENew Zealand has a strong and growing trade surplus in food and beverage

PAGE 12 Note: does not exactly match other data due to use of SITC codes (rather than HT codes, which are not available back this far) for understood reasons; Source: UN Comtrade; Coriolis analysis

‐$5.0

$‐

$5.0

$10.0

$15.0

‐$5.0

$‐

$5.0

$10.0

$15.0

1965196619671968196919701971197219731974197519761977197819791980198119821983198419851986198719881989199019911992199319941995199619971998199920002001200220032004200520062007200820092010

Exports

Imports

Net tradebalance

New Zealand F&B import value(US$b; 2010)

NZ F&B IMPORTSNew Zealand imports a wide range of food and beverages; processed foods and beverages account for more than 55% of these imports

PAGE 13 Source: UN Comtrade database; Coriolis analysis

Dairy$113 4%

Meat$145 5%

Seafood$117 4%

Produce$308 11%

Grains$184 6%

Other$430 15%

Processed$1,184 42%

Beverages$360 13%

Total = US$2.8b$26 $113 $55

$145 $48

$117

$117

$308

$61

$184

$179

$430

$378

$1,184

$158

$360

2000 2010

Dairy

10 year New Zealand F&B import value(US$b; 2000 vs. 2010)

$2.8

$1.0

Meat

Seafood

Produce

Grains

Other

Processed

Beverages

16%10%

9%

10%

12%

9%

12%

9%

CAGR(00‐10)11%

Processed foods and beverages

55%

New Zealand export value by F&B total and by key segment(US$b; 2010)

F&B IMPORTANT TO TOTAL EXPORT VALUEFood and beverages (F&B) represent 54% of the total value of New Zealand’s exports

PAGE 14 Note: totals may not add due to rounding; Source: UN Comtrade database; Coriolis analysis

F&B$16.7 54%

Other$14.3 46% Dairy $7.8 47%

Meat $3.7 22%

Seafood $1.0 6%

Produce $1.3 8%

Grains $0.0 0%

Other $0.3 2%Processed $1.5

9%

Beverages $1.0 6%

Total = US$30.9b

Total = US$16.7b

New Zealand export value by F&B and non‐F&B(US$b; non‐inflation adjusted; 1965‐2010)

F&B GROWINGNew Zealand’s F&B exports have been growing

PAGE 15 1. CAGR = Compound Annual Growth Rate; Note: totals may not add due to rounding; Source: UN Comtrade database; Coriolis analysis

$0.5 $2.4

$5.6

$16.7

$0.4

$3.0

$7.9

$14.3

1965 1980 1995 2010

$30.9

$13.6

$5.5

$1.0

10.6%

13.7%

F&B

Allother

Rate of growth (CAGR1) in New Zealand export value by F&B and non‐F&B(CAGR; by 15 year periods; 1965‐2010)

65‐80

5.7%

6.7%

F&B

Allother

80‐95

7.5%

4.0%

F&B

Allother

95‐10

F&B

All other

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

Map of global regions used in our analysis(as used)

DEFINED GLOBAL REGIONSOur market analysis uses the following nine defined global regions

PAGE 17 Source: map (Wikipedia; free usage); Coriolis (colour and definitions)

Sub‐Saharan (SS) Africa

AustraliaPacific Islands

Central & South (C&S) America

NorthAmerica

East Asia

South East Asia

South Asia

Europe/Russia

North Africa/ Middle East/ Central Asia

(NA/ME/CA)

Aggregate annual F&B export value by key markets(US$b; %; 2010)

NZ F&B EXPORT VALUE BY REGIONNew Zealand exports F&B to a wide range of destinations; interestingly Asia is worth a third more than Europe, Russia and North America combined

PAGE 18 Note: totals may not add due to rounding; Source: UN Comtrade database; Coriolis analysis

Europe/Russia $2.8 17%

North America $2.0 12%

Australia/Pacific $2.1 13%

SE Asia $2.3 13%

East Asia $4.3 26%

South Asia $0.4 2%NA/ME/CA $1.6 9%

SS Africa $0.4 3%

C&S America $0.9 5%

Traditional Western markets~30%

Asianmarkets~40%

Total = $16.7b

North Africa/Middle EastCentral Asia

F&B export value by region over time(US$b; 2000 vs. 2010)

NZ F&B EXPORT VALUE BY REGION OVER TIMEGrowth is bring driven by Australia and Asia

PAGE 19 Note: totals may not add due to rounding; Source: UN Comtrade database; Coriolis analysis

$1.5 $2.8

$1.3

$2.0 $0.6

$2.1

$0.7

$2.3

$1.3

$4.3

$0.1

$0.4

$0.3

$1.6

$0.0

$0.4

$0.4

$0.9

2000 2010

Sub‐Saharan Africa

AustraliaPacific Islands

C&S America

NorthAmerica

East Asia

South East Asia

South Asia

Europe/Russia

25.7%

14.3%

9.3%

4.4%

12.3%

11.7%

17.8%

6.7%

16.6%

CAGR (00‐10)

10.4%$16.7

$6.2

+$0.4

+$1.6

+$0.5

+$0.7

+$2.9

+$1.5

+$0.3

+$1.3

+$1.2

Absolute (00‐10)

+$10.5

North Africa/Middle East/Central Asia

76%

53%

44%

34%25%

30% 29%23% 23%

17%

10%

27%

20%

23%

23%22%

15%21% 18%

12%

3%

4%

5%

7%

8%7%

9% 9%11%

13%

7%

5%

9%

6%

7%8%

8% 8% 8%

10%

0%

0%

4%

10%15% 6%

5% 6% 7%

10%

2%

3%

8% 9%6%

8%

10% 12% 11%14%

3%7% 11% 12%

16% 19%24% 22% 23% 26%

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010

NZ F&B EXPORT MARKETS

Total New Zealand F&B exports by region(US$m; non‐inflation adjusted; 1965‐2010)

New Zealand in the middle of a fundamental transition from feeding Westerners to feeding the Asia‐Pacific region

PAGE 20 Source: UN Comtrade database; Coriolis analysis

$540

45 yearchange in share

$692 $1,085 $2,429 $2,572 $4,037 $5,565 $6,200 $11,078 $16,676

Europe ‐59%

9%

Other

Australia/ Oceania

10%

E Asia

SE Asia

4%

22%

12%

N America 2%

North Africa/Middle EastCentral Asia

F&B export value growth matrix(2010)

NZ F&B EXPORT GROWTH MATRIXNew Zealand F&B exports have a range of opportunities for growth

PAGE 21 Source: UN Comtrade database; Coriolis analysis

10%

26%

24%

22%

18%

$2.8 $3.2$2.2 $2.4 $2.6$0.6 $0.8 $1.2 $1.4 $1.6

20%

$0.2 $0.4

C&S America

$0.0 $1.0 $2.0 $3.00%

Europe/Russia

North America

Australia/Pacific

SE AsiaEast Asia

South Asia

$1.8

SS Africa

28%

2%

4%

NA/ME/CA

8%

12%

14%

16%

6%

10 year value CAGR(00‐10)

10 year absolute value growth(US$b; 2010)

Size of bubble = export value (US$b; 2010)

Small but fast growing

Traditional markets but slow growing

Solid performers

!!!!

Share of New Zealand export value by region by sector(% of US$; 2010)

SECTOR VALUE MIX BY REGIONExport value mix varies by market; developing markets dominated by dairy and meat; traditional US/EU markets more weighted to meat; Australia is the most balanced

PAGE 22 Note: totals may not add due to rounding; Source: UN Comtrade database; Coriolis analysis

24%

76%

34%

93%

76%

62%

90%

22%30%

10%

7%

15%

1%

20%

15%

8%

47%

48%

16%

5%

21%

1%

6%

0%

7%

10%

11%

5%

16%

2%2%

10%

1%

19%

6%

1%2%

4%

3%1% 1%

24%

5%9%

1% 1%1% 1% 3%

13%

1% 1% 3% 4% 3%

Australia/Pacific SE Asia East Asia South Asia NA/ME/CA SS Africa C&S America Europe/Russia North America

Processed foods

Seafood

Beverages

Meat

Grains

Produce

Other

Dairy

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

AUSTRALASIA/PACIFIC – RECOMMENDATIONS

Situation

- In aggregate Australia and the Pacific Islands are a large and attractive market for New Zealand food and beverage exporters- Close physically and culturally- Population of 32m (Australia 22m; P.I. 10m); same GDP as

India (aggregate nominal)- Mixture of highly developed markets and lower income

countries

- Region is effectively New Zealand’s home market

- New Zealand has excellent market share in the region- F&B import share typically 15‐30%- Higher in associated countries (e.g. Cook Islands)

- Significant trade agreements in place (e.g. CER1 with Australia 1983; Protocol on Investment in the New Zealand and Australia CER Agreement, 2011)

- New Zealand achieving strong value growth to Australia in particular (see “Moving to the Centre” report for details)

Potential market development strategy

- Start in Australia - Focus on winning “next door” rather than across a small

volume of exports across a wide range of countries- With Woolworths operating across both markets, New

Zealand supply is regularly being compared with Australian- New Zealand F&B exports are achieving excellent success

in Australia across a wide range of sectors and firms- Use own salesforce rather than outsource; consider

targeted acquisitions to build an in‐market presence

- Take Pacific Island market seriously- Do not operate under out dated assumptions or second

hand advice about levels of market development- In aggregate a large market where NZ F&B has strong share- French territories in particular are high income and have

modern global retailers (e.g. Carrefour; global #2)- Build a relationship with Carrefour and Casino;

leverage this into other markets - A small effort should produce strong results (as it is a low

priority for others)

- Consider a wider “island”‐focused strategy - New Zealand F&B exports are disproportionally successful

per capita in islands worldwide (e.g. Caribbean)

PAGE 24 1. CER Australia New Zealand Closer Economic Relations Trade Agreement; AANZFTA = ASEAN‐Australia‐New Zealand Free Trade Agreement

As a result of globalisation, Australia and the Pacific Islands are now New Zealand’s “home market”; they should be treated as such

Map of countries in Australasia/Pacific region(2010)

AUSTRALASIA/PACIFIC – REGIONAL OVERVIEWThe Australasian/Pacific Island region is now effectively New Zealand’s home market

PAGE 25 Source: Wikimedia Commons; Coriolis

New Zealand

Papua New Guinea

Australia

Aus/ Pacific, 0.5%

Other, 99.5%

Aus/ Pacific2%Other

98%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

Solomon Islands

Fiji

TongaNew

Caledonia

French Polynesia

Vanuatu

Tuvalu

MarshallIslands

Hawaii

Samoa

Tokelau

CookIslands

Kiribati

Fed State of MicronesiaPalau

The region has the same GDP

as India

AUSTRALASIA/PACIFIC – MARKET CHARACTERISTICS

Source: Coriolis

Australasian/Pacific Island markets have similar cuisine to NZ with common building blocks; markets also face a similar set of issues

Overview of key characteristics of the Australia / Pacific food & beverage market environment(2011)

Cuisine and culture Distribution Competitive environment

Food building blocks Market characteristics Key imported temperate foods and beverages

AU/NZ Pacific Islands AU/NZ Pacific Islands AU/NZ Pacific Islands

‐ Bread‐ Temperate fruit &

vegetables‐ Beef, chicken, pork‐ Processed foods‐ Local beer and wine;

imported spirits

‐ Tropical fruit‐ Tropical vegetables‐ Chicken, seafood‐ Sauces (e.g. fish sauce)‐ Beer and imported

wine and spirits

‐ Supermarket sector consolidated Expenditure on foodservice/food away larger than retail food (i.e. “spend more in restaurants than in supermarkets”)

‐ Retailers generally small and fragmentedby market

‐ Strong independent sector

‐ Many distributors have strong market power

‐ Inter‐regional trade‐ Premium spirits

(Brandy, Whisky, Gin)‐ Processed foods

‐ Grains‐ Meat‐ Temperate fruit and

vegetables‐ Processed foods‐ Imported foods for

tourists

Cultural & regulatory characteristics Supply chain issues Key suppliers of temperate foods and beverages

AU/NZ Pacific Islands AU/NZ Pacific Islands AU/NZ Pacific Islands

‐ Common regional food standards/regulations across AU/NZ

‐ Variable standards by market; many accept standards of others

‐ Some have EU standards

‐ Highly efficient modern supply chain

‐ Large number of small markets leading to high cost and inefficient distribution

‐ Some exceptions, particularly in French territories

‐ Inter‐regional‐ China‐ United States‐ Europe

‐ Australia‐ New Zealand‐ France‐ Other Europe‐ China

PAGE 26

Major regional groups with multi‐country operationsStrong operators in single market in region

Australia 823 super1,208 liquor561 petrol

742 super766 liquor619 conv174 dept

New Zealand 158 super48 conv

12 dept

French Polynesia

1 hyper2 super

1 super

Papua NewGuinea

New Caledonia

1 1 super

Fiji

Vanuatu 1 discount

Key chain food retail operators by outlet type* across Australia and select Pacific Island markets(2011)

AUSTRALASIA/PACIFIC – KEY SUPERMARKETS BY MARKETAustralasian and Pacific Island food retailing is still relatively fragmented outside AU/NZ

PAGE 27 *Supermarket, convenience, liquor, department, hypermarket; discount, Source: various company websites; various company annual reports; various published articles; Coriolis analysis

24 super 23 super

RB Patel

8 super

181 super/446 conv/94 liquor

21 super4 super 2 hyper 6 super1 hyper5 super

1,300+ super250 super 3 hyper

GDP/capita(US$/person; 2010 or latest available)

AUSTRALASIA/PACIFIC – KEY INDICATORSThe Australasian/Pacific region is made up of two large economies and a large number of small islands; while Australia is the key opportunity, the aggregate size of the Pacific Island market should not be ignored

PAGE 28 1. 1993 data (latest available); obviously greater today as it would be difficult for a country to import more F&B per capita than its GDP; Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$930 $110

$6.1 $2.8 $3.3 $0.2 $0.2 $0.2 $0.6 $0.5 $0.0 $0.0 $3.0 $0.6 $0.2 $0.3 $0.6 $0.2 $0.0 $0.7 $0.0 $8.2 $0.1

22.4 4.4

0.3 0.2 0.2 0.0 0.0 0.0 0.1 0.1 0.0 0.0 0.8 0.2 0.1 0.1 0.2 0.1 0.0 0.5 0.0

6.7 0.1

$41,531 $25,025 $23,106

$15,579 $13,253 $12,296 $9,160 $8,200 $7,280 $6,899 $6,673 $3,690 $3,590 $3,168 $2,608 $2,490 $2,308 $2,145 $1,494 $1,277 $1,250 $1,218 $1,163

AustraliaNew Zealand

French PolynesiaGuam

New CaledoniaWallis & Futuna

Cook IslandsPalau

Northern MarianaAmerican Samoa

NiueNauru

FijiSamoa

Marshall IslandsTonga

VanuatuFed. Micronesia

TuvaluSolomon Islands

TokelauPapua New Guinea

Kiribati

Population(people; m; 2010)

GDP(US$b; 2010)

$9,399 $2,840

$400 $66 $351 $11 $23 $11 $11 $22 $3 $6 $292 $75 $19 $46 $42 $28 $2 $55 $3 $486

$26

Total F&B Import value(US$m; 2010)

$420 $648

$1,515 $368

$1,411 $717 $1,154

$557 $126 $335

$2,220 $557 $344 $419 $308 $441

$173 $254 $225 $106

$1,945 $72 $265

F&B Import $/capita(US$/person; 2010)

9.8m $28b $2b

In aggregate the Pacific Islands import US$2b worth of F&B

1

Dairy $1.1 7%

Meat $1.1 8%

Seafood $1.5 10%

Produce $1.1 8%

Grains $0.6 4%Other $1.7

12%

Processed $4.9 35%

Beverages $2.3 16%

Aggregate Australasia/Pacific total F&B import value from all source countries(US$b; 2010)

AUSTRALASIA/PACIFIC – TOTAL IMPORT VALUEAustralia is the largest market; regional trade is across a wide range of sectors, however processed foods and beverages account for 50%

PAGE 29 Source: UN Comtrade database; Coriolis analysis

Australia $9.4 66%

New Zealand $2.8 20%

Pacific Islands $2.0 14%

US$14.2b US$14.2b

By receiving country By product

NZ share of regional cross‐border exports/imports of F&B by sector(% of value; 2010)

AUSTRALASIA/PACIFIC – NZ PERFORMANCENew Zealand performs well in the region, in terms of share and sales across most sectors

PAGE 30 Note: Calculation is sum of exports to the region (or cross‐border/inter‐country trade); therefor New Zealand regional share excludes New Zealand sales to itself; likewise Australia share excludes Australia itself; Source: UN Comtrade database; Coriolis analysis

54%

18%

19%

23%

2%

4%

17%

21%

9%

10%

1%

8%

34%

8%

17%

9%

37%

72%

81%

69%

64%

88%

66%

70%

54%

18%

19%

23%

2%

4%

17%

21%

Dairy

Meat

Seafood

Produce

Grains

Other

Processed

Beverages

NZ Australia Other

$443

$152

$212

$191

$10

$46

$661

$369

Value of NZ F&B imports to region by sector(US$m; 2010)

Share of regional cross‐border F&B exports/imports by sector: NZ vs. AU vs. all other(% of value; 2010)

Value of F&B imports from NZ by country(US$m; 2010)

AUSTRALASIA/PACIFIC – NZ PERFORMANCENew Zealand performs very well across much of the region and is particularly strong in countries with an association with New Zealand (i.e. Niue and the Cook Islands)

PAGE 31 Note: Some countries not shown due to lack of data; all data should be treated as directional due to data quality issues; data is reporter‐received by country not sent by New Zealand; Source: UN Comtrade database; Coriolis analysis

$1,789

$78

$5

$50

$3

$21

$0

$3

$9

$2

$79

$19

$0

$14

$0

$6

$47

$0

Australia

French Polynesia

Guam

New Caledonia

Wallis & Futuna

Cook Islands

Palau

Northern Mariana

American Samoa

Niue

Fiji

Samoa

Marshall Islands

Tonga

Tuvalu

Solomon Islands

Papua New Guinea

Kiribati

$80

$297

$30

$200

$185

$1,058

$1

$31

$141

$1,385

$93

$108

$3

$131

$34

$12

$7

$3

NZ F&B imports per capita by country(US$/person; 2010)

NZ share of total F&B import value by country(%; 2010)

19%

20%

8%

14%

26%

92%

0%

25%

42%

62%

27%

26%

1%

30%

15%

12%

10%

1%

US$338m

In aggregate the Pacific Islands import US$2b

worth of F&B; how do we get more

share?

NewZealand

Australia USA Canada Europe SouthAmerica

China Japan Other EAsea

Beverages

Processed

Other

Grain

Produce

Seafood

Meat

Dairy

Aggregate export value to Australia/Pacific Islands by sector: NZ vs. select temperate countries or regions(US$b; 2010)

AUSTRALASIA/PACIFIC – IMPORT VALUE INTO REGION ACROSS PEERSNew Zealand already performs well into our closest neighbours; however opportunities remain to take further share from temperate peers

PAGE 32 Note: Some countries not shown due to lack of data; all data should be treated as directional due to data quality issues; Source: UN Comtrade database; Coriolis analysis

Comments/Notes

‐ To triple F&B exports to Australia and the Pacific looks hard; we should, however be able to ”eat Europe’s lunch”

‐ Peers in similar temperate zones (temperate peers) will send similar products to Australia and the Pacific Islands

Note

‐ Data is as reported by sender; does not sync with data as reported by receiver (for understood methodological reasons)

$2.1

$0.4

$1.4

$0.2 $0.2$0.1 $0.1

$0.7

$2.2

Only AU exports to Pacific Islands

High cost Europe sends more than us; why aren’t

we supplying this?

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

SE ASIA – RECOMMENDATIONS

Situation

- South East Asia is a highly attractive market for New Zealand food and beverage exporters- Next closest market after Australia- Population of 583m (more than all of Central and South

America) - Increasing wealth leading to increased demand for

imported food and beverages

- South East Asia is a natural trading partner for New Zealand- Tropical environment unable to efficiently produce many

temperate foodstuffs

- New Zealand has a relatively strong presence in the region- Awareness by some consumers of New Zealand as a quality

supplier- Long term (100 year+) supply of dairy and meat- Particularly into former co‐members of the British Empire

- Significant trade agreements in place or in development- AANZFTA1, 2010 (12 member) linkage in development- Malaysia NZ FTA, 2010- Thailand NZ, CEP, 2005- Singapore NZ CEP, 2001

Recommended market entry strategy

- Start in Singapore - High income country with rule‐of‐law that speaks English- Only 5m people so “do‐able” for New Zealand

manufacturing to scale‐up to supply without major capital expenditure

- Modern supermarket sector consolidated into 3 chains- Commit to the market; treat as a “region of New Zealand”;

put salespeople in the market; regularly call on retailers; run promotions

- Central location that is a natural regional base and distribution hub

- Already imports proportionally a lot of F&B from New Zealand

- Expand into Malaysia- Slightly larger population than Australia (28m people)- Already imports proportionally a lot of F&B from New

Zealand- Easily serviced from Singapore

- Expand into other key markets in the region- Thailand, Indonesia, the Philippines and Viet Nam

PAGE 34 1. AANZFTA = ASEAN‐Australia‐New Zealand Free Trade Agreement; CEP = Closer Economic Partnership; FTA = Free Trade Agreement

South East Asia is the next logical market for New Zealand food & beverage exporters with a strong presence in their home market (New Zealand, Australia and the Pacific Islands)

Map of countries in South East Asia/ASEAN(2010)

SE ASIA – REGIONAL OVERVIEWSouth East Asia is the closest regional market to New Zealand after Australasia; it represents almost 10% of world population and 3% of world GDP

PAGE 35 Note: East Timor is not currently part of ASEAN; Source: Wikimedia Commons; Coriolis

Myanmar

Indonesia

Vietnam

Philippines

Malaysia

Thailand

Laos

Cambodia

East Timor

Singapore

Brunei

SE Asia9%Other

91%

SE Asia3%

Other97%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

ASEAN Flag

All countries here are ASEAN members

SE ASIA – MARKET CHARACTERISTICS

Source: Coriolis

South East Asian markets have similar cuisine with common building blocks; markets also face a similar set of issues

Overview of key characteristics of the South East Asian food & beverage market environment(2011)

Cuisine and culture Distribution Competitive environment

Food building blocks Market characteristics Key imported temperate foods and beverages

‐ Rice‐ Tropical fruit (rambutan, durian, etc.)‐ Tropical/Asian vegetables‐ Chicken, seafood‐ Sauces (e.g. fish sauce)‐ Beer and local spirits

‐ Continuing strong presence of wet markets and fresh specialists

‐ Supermarket sector consolidated within markets but less so across markets

‐ Expenditure on foodservice/food away larger than retail food (i.e. “spend more in restaurants than in supermarkets”)

‐ European spirits (Brandy, Whisky, Gin)‐ Ingredient milk powder for local manufacturers to turn

into consumer dairy items (e.g. yoghurt drinks, infant formula)

‐ Apples‐ Beef

Cultural & regulatory characteristics Supply chain issues Key suppliers of temperate foods and beverages

‐ Religious limitations on protein consumption (Muslimpeoples don’t eat pork and require meat to be halal)

‐ Multiple languages across region leading to requirement for packaging by country

‐ No common regional food standards or regulations‐ Muslim restrictions on alcohol consumption‐ Various degrees of alcohol intolerance (ALDH2

deficiency) within population (particularly those of East Asian origin)

‐ Markets somewhat bi‐polar with world‐class, best practice retailers (e.g. Tesco) alongside wet markets

‐ Modern supply chains developing in higher income countries with spread of chain supermarket operators

‐ Sophistication of supply chain more variable elsewhere‐ Convoluted supply chain to support continuing

significant role of numerous wet markets selling fresh meat, seafood, fruit and vegetables

‐ Australia‐ China‐ United States‐ Europe‐ New Zealand

PAGE 36

Major regional groups with multi‐country operationsStrong operators in single market in region

Singapore 7 hyper105 super

2 hyper

Malaysia 123+17+2 hyper/super

25 hyper14 conv

32 stores 23 dept4 super

Thailand 663 stores 13 super 16 hyper89 super

Indonesia 120 super38 hyper125 conv

67 hyper16 super

Philippines

Vietnam 3 super 14 hyper

Brunei 1 hyper2 super

1 hyper

Key chain food retail operators by outlet type* across higher income South East Asia(2011)

SE ASIA – KEY SUPERMARKETS BY MARKETSouth East Asian food retailing is a mixture of regional chains and strong local operators

PAGE 37 *Supermarket, convenience, liquor, department, hypermarket; discount, Source: various company websites; various company annual reports; various published articles; Coriolis analysis

GDP/capita(US$/person; 2010)

SE ASIA – KEY INDICATORSSouth East Asian countries range from very rich to very poor; the key opportunity for F&B exports is in the six major economies

PAGE 38 Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$15

$163

$207

$266

$515

$159

$92

$6

$11

$34

$1

0.4

5.0

28.3

63.5

234.2

94.0

85.8

6.3

13.4

50.5

1.1

$36,750

$32,701

$7,327

$4,194

$2,199

$1,688

$1,070

$905

$814

$679

$528

Brunei

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

Laos

Cambodia

Myanmar

East Timor

Population(people; m; 2010)

GDP(US$b; 2010)

$0.3

$9.1

$12.0

$7.3

$9.5

$6.1

$4.0

$0.2

$0.2

$0.0

Total F&B Import value(US$b; 2010)

$652

$1,826

$424

$114

$40

$65

$46

$‐

$13

$3

$14

F&B Import $/capita(US$; 2010)

N/A

Australia$9.4b

These six countries are the primary opportunity; 511m people, importing F&B worth $49b

Aggregate SE Asia total F&B import value from all source countries(US$b; 2010)

SE ASIA – TOTAL IMPORT VALUEThe six major markets account for 99% of F&B imports; F&B imports are spread across a range of sectors

PAGE 39 Source: UN Comtrade database; Coriolis analysis

Brunei $0.3 1%

Singapore $9.1 19%

Malaysia $12.0 25%

Thailand $7.3 15%

Indonesia $9.5 19%

Philippines $6.1 13%

Vietnam $4.0 8%Laos $0.0

0%

Cambodia $0.2 0%

Myanmar $0.2 0%

East Timor $0.0 0%

US$48.6b US$48.6b

By receiving country

Top 699%

Dairy $4.51 9% Meat $2.29 5%

Seafood $4.49 9%

Produce $4.24 9%

Grains $9.29 19%

Other $12.56 26%

Processed $8.03 17%

Beverages $3.13 6%

By product

e.g. palm oil, soy beans

(mostly inter‐regional)

Aggregate SE Asia total F&B import value from all source countries by mega‐region(US$b; 2010)

SE ASIA – IMPORT VALUE BY SOURCEOne third of F&B imports come from within the region, two thirds from outside the region

PAGE 40 Source: UN Comtrade database; Coriolis analysis

US$48.6b

SE Asia Inter‐Regional $15.5

32%

External $33.0 68%

By source By source by product

8%

4%

30%

21%

34%

51%

36%

17%

92%

96%

70%

79%

66%

49%

64%

83%

Dairy

Meat

Seafood

Produce

Grains

Other

Processed

Beverages

SE AsiaInter‐

Regional

External

Value of NZ F&B imports by country(US$b; 2010)

SE ASIA – NZ PERFORMANCENew Zealand performs very well in Singapore; Malaysia is strong and Thailand, Indonesia, the Philippines and Vietnam stand out as opportunities

PAGE 41 Source: UN Comtrade database; Coriolis analysis

$0.00

$0.42

$0.48

$0.34

$0.53

$0.38

$0.11

$‐

$0.002

$0.01

$0.000

Brunei

Singapore

Malaysia

Thailand

Indonesia

Philippines

Vietnam

Laos

Cambodia

Myanmar

East Timor

$6

$84

$17

$5

$2

$4

$1

$‐

$0

$0

$0

NZ F&B imports per capita by country(US$/person; 2010)

NZ share of total F&B import value by country(US$b; 2010)

1%

5%

4%

5%

6%

6%

3%

1%

0%

What is required to move these countries to

Australian levels of share (i.e. ~20%)

NZ share of regional F&B imports by sector(% of value; 2010)

SE ASIA – NZ PERFORMANCENew Zealand performs well in dairy and meat into SE Asia; processed foods also showing some success

PAGE 42 Source: UN Comtrade database; Coriolis analysis

36%

12%

1%

2%

0%

0%

2%

1%

Dairy

Meat

Seafood

Produce

Grains

Other

Processed

Beverages

$1.6

$0.3

$0.05

$0.1

$0

$0.02

$0.2

$0.03

Value of NZ F&B imports to region by sector(US$b; 2010)

Aggregate export value to South East Asia by sector: NZ vs. select temperate countries or regions(US$b; 2010)

SE ASIA – IMPORT VALUE INTO REGION ACROSS TEMPERATE PEERSTemperate country/region peer group suggest (1) there is more opportunity in dairy and (2) processed and beverages are opportunities

PAGE 43 Source: UN Comtrade database; Coriolis analysis

Comments/Notes

‐ To triple F&B exports to SE Asia New Zealand would need to export more than Europe to the region

‐ To grow NZ needs to either grow faster than the growth of the market or take sales from competitors

‐ Data here suggests there are further opportunities to take dairy sales from the US and Europe

‐ Data here suggests that there are further opportunities in processed foods and beverages; conceptually NZ should be able to take share from Europe and the US

Note

‐ While this analysis may look simple, the underlying dataset contained 103,807 data points

‐ Data is as reported by sender; does not sync with data as reported by receiver (for understood methodological reasons)

NewZealand

Australia USA Canada Europe S America China Japan Other EAsia

Beverages

Processed

Other

Grains

Produce

Seafood

Meat

Dairy

$2.3

$4.3

$4.9

$0.8

$6.2

$3.7

$4.3

$0.6

$1.2

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

EAST ASIA – RECOMMENDATIONS

Situation

- East Asia is a highly attractive market for New Zealand food and beverage exporters - Huge potential market (1.6b people)- Either sophisticated high wealth consumers or rapidly

becoming so, leading to increased demand for premium imported food and beverages

- A clear “once in a lifetime” opportunity to grow with China for the short‐medium term- Long run China will be a major competitor in F&B to New

Zealand (regions with similar climate but more scale and less cost)

- China should be self‐sufficient in dairy within a decade

- New Zealand has a relatively strong presence in the region- Strong position in dairy (38% of regional dairy imports)- Position in meat, produce and processed foods

- Significant trade agreements in place or in development- On‐going discussions with Japan- HK, China NZ CEP, 2011 (NZ China FTA, 2008)- Korea NZ FTA negotiations

- New Zealand currently poor at developing high status‐brands demanded by regions’ consumers

Recommended market entry strategy

- Start in Hong Kong (similar in many ways to Singapore)- High income country with rule‐of‐law that speaks English- Only 7m people so “do‐able” for New Zealand

manufacturing to scale‐up to supply without major capital expenditure

- Modern supermarket sector consolidated into 2 chains- Commit to the market; treat as a “region of New Zealand”;

put salespeople in the market; regularly call on retailers; run promotions

- Central location that is a natural regional base and distribution hub

- Already imports proportionally a lot of F&B from New Zealand

- Expand into Taiwan- Similar population to Australia (23m people)- Already imports proportionally a lot of F&B from New

Zealand- Can be ignored by others/competitors

- Expand into other key markets in the region- Japan, South Korea and China - Leave China to last; easy to do poorly, difficult to do well

PAGE 45 CEP = Closer Economic Partnership; FTA = Free Trade Agreement

East Asia is the current shining opportunity for New Zealand F&B exports

Map of countries in East Asia(2010)

EAST ASIA – REGIONAL OVERVIEWEast Asia represents 23% of world population and 20% of world GDP

PAGE 46 Source: Wikimedia Commons; Coriolis

Taiwan

East Asia23%

Other77%

East Asia20%

Other80%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

Japan

SouthKorea

NorthKorea

China

Mongolia

Hong KongMacao

EAST ASIA – MARKET CHARACTERISTICS

Source: Coriolis

While East Asia has three distinct major cultures (Chinese, Japanese and Korean), the markets have strong common characteristics

Overview of key characteristics of the East Asian food & beverage market environment(2011)

Cuisine and culture Distribution Competitive environment

Food building blocks Market characteristics Key imported temperate foods and beverages

‐ Rice and wheat (more in Northern regions)‐ Temperate and tropical fruit ‐ Asian vegetables‐ Pork, chicken, seafood, beef‐ Processed foods‐ Sauces (e.g. fish sauce)‐ Beer and local spirits

‐ Continuing strong presence of wet markets and fresh specialists

‐ Supermarket sector highly fragmented across most markets

‐ Expenditure on foodservice/food away larger than retail food (i.e. “spend more in restaurants than in supermarkets”)

‐ European spirits (Brandy, Whisky, Gin)‐ Ingredient milk powder for local manufacturers to turn

into consumer dairy items (e.g. yoghurt drinks, infant formula)

‐ Counter‐seasonal temperate fruit‐ Beef

Cultural & regulatory characteristics Supply chain issues Key suppliers of temperate foods and beverages

‐ Key languages predominantly Mandarin, Cantonese, Japanese & Korean leading to requirement for packaging by country

‐ No common regional food standards or regulations‐ Various degrees of alcohol intolerance (ALDH2

deficiency) within population (particularly those of East Asian origin)

‐ Convoluted supply chains involving multiple levels of distributors across all markets

‐ Markets somewhat bi‐polar with world‐class, best practice retailers (e.g. Tesco) alongside wet markets

‐ Continuing significant role of numerous specialists and wet markets selling fresh meat, seafood, fruit and vegetables (particularly in China)

‐ Inter‐regional‐ Australia‐ United States‐ Europe‐ New Zealand

PAGE 47

Major regional groups with multi‐country operationsStrong operators in single market in region

Japan Exited 142 super 321 super 8 hyper

South Korea

Exited 305 hyper Exited 7 hyper

Taiwan 294 super 421 hyper2 super

Exited 24 hyper 6 hyper

Hong Kong 282 super964 conv338 HBC

Exited Exited

China 551 conv163 HBC

1,416 hyper

57 discount

88 hyper 322 hyper 114 hyper

Key chain food retail operators by outlet type* across select East Asian countries(2011)

EAST ASIA – KEY SUPERMARKETS BY MARKETEast Asian food retailing is highly competitive with strong local chains battling many of the largest retailers in the world

PAGE 48 *Supermarket, convenience, liquor, department, hypermarket; discount, Source: various company websites; various company annual reports; various published articles; Coriolis analysis

240 super

… many more

… many more

GDP/capita(US$/person; 2010)

EAST ASIA – KEY INDICATORSEast Asian countries range from very rich to very poor; the key opportunity for future F&B exports to the region is China

PAGE 49 Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$5,108

$22

$209

$810

$362

$4,814

$4

$28

127

1

7

50

23

1,339

3

24

$40,100

$40,022

$29,716

$16,268

$15,628

$3,596

$1,523

$1,172

Japan

Macao SAR

Hong KongSAR

South Korea

Taiwan

China

Mongolia

North Korea

Population(people; m; 2010)

GDP(US$b; 2010)

$59.3

$0.8

$17.2

$14.6

$9.4

$57.9

$0.2

$0.4

Total F&B Import value(US$b; 2010)

$466

$1,536

$2,447

$293

$407

$43

$82

$15

F&B Import $/capita(US$; 2010)

Australia$9.4b

In 2011 China moved into the #1 position in East Asia and #2 in the world after the USA

Dairy $5.3 3%

Meat $21.5 14%

Seafood $26.2 16%

Produce $13.3 8%

Grains $14.8 9%

Other $52.2 33%

Processed $17.3 11%

Beverages $9.1 6%

Aggregate East Asia total F&B import value from all source countries(US$b; 2010)

EAST ASIA – TOTAL IMPORT VALUEEast Asia imported US$160b worth of F&B in 2010 spread across the five key markets

PAGE 50 Source: UN Comtrade database; Coriolis analysis

Japan $59.3 37%

Macao SAR $0.8 1%

Hong Kong SAR $17.2 11%

South Korea $14.6 9%

Taiwan $9.4 6%China $57.9

36%

Mongolia $0.2 0%

North Korea $0.4 0%

US$160b US$160b

By receiving country

Top 699%

By product

e.g. palm oil, soy beans

NZ share of regional F&B imports by sector(% of value; 2010)

EAST ASIA – NZ PERFORMANCE BY SECTORNew Zealand performs well in dairy into East Asia; share is low otherwise with produce, meat and processed foods having limited presence

PAGE 51 Source: UN Comtrade database; Coriolis analysis

$2.0

$0.6

$0.4

$0.6

$0.0

$0.1

$0.5

$0.1

$3.3

$20.9

$25.9

$12.7

$14.8

$52.1

$16.9

$9.0

38%

3%

1%

4%

0%

0%

3%

1%

Dairy

Meat

Seafood

Produce

Grains

Other

Processed

Beverages

NZ Other

$2.0

$0.6

$0.4

$0.6

$0.0

$0.1

$0.5

$0.1

Value of NZ F&B imports to region by sector(US$b; 2010)

Value of total F&B imports to region by sector(US$b; 2010)

Value of NZ F&B imports by country(US$b; 2010)

EAST ASIA – NZ PERFORMANCE BY COUNTRYNew Zealand performs very well in Hong Kong; all other key countries appear to have opportunities for share growth

PAGE 52 Source: UN Comtrade database; Coriolis analysis

$1.2

$0.0

$0.3

$0.3

$0.5

$1.9

$0.0

$‐

Japan

Macao SAR

Hong KongSAR

South Korea

Taiwan

China

Mongolia

North Korea

$10

$18

$46

$6

$20

$1

$3

$‐

NZ F&B imports per capita by country(US$/person; 2010)

NZ share of total F&B import value by country(US$b; 2010)

2%

1%

2%

2%

5%

3%

4%

0%

What is required to move these countries to

Australian levels of share (i.e. ~20%)

NewZealand

Australia USA Canada Europe SouthAmerica

China Japan Other EastAsia

Beverages

Processed

Other

Grains

Produce

Seafood

Meat

Dairy

Aggregate export value to East Asia by sector: NZ vs. select temperate countries or regions(US$b; 2010)

EAST ASIA – IMPORT VALUE INTO REGION ACROSS PEERSWhile there are opportunities into temperate East Asia and growth is clearly possible, data suggests growth will come outside traditional raw ingredients

PAGE 53 Source: UN Comtrade database; Coriolis analysis

Comments/Notes

‐ Tripling F&B exports to East Asia would appear to be possible

‐ However, data suggests that a targeted approach is required

Note

‐ Data is as reported by sender; does not sync with data as reported by receiver (for understood methodological reasons)

$3.4

$6.2

$31.2

$6.9

$16.3

$25.8

$11.1

$1.5

$4.1

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

Map of countries in South Asia(2010)

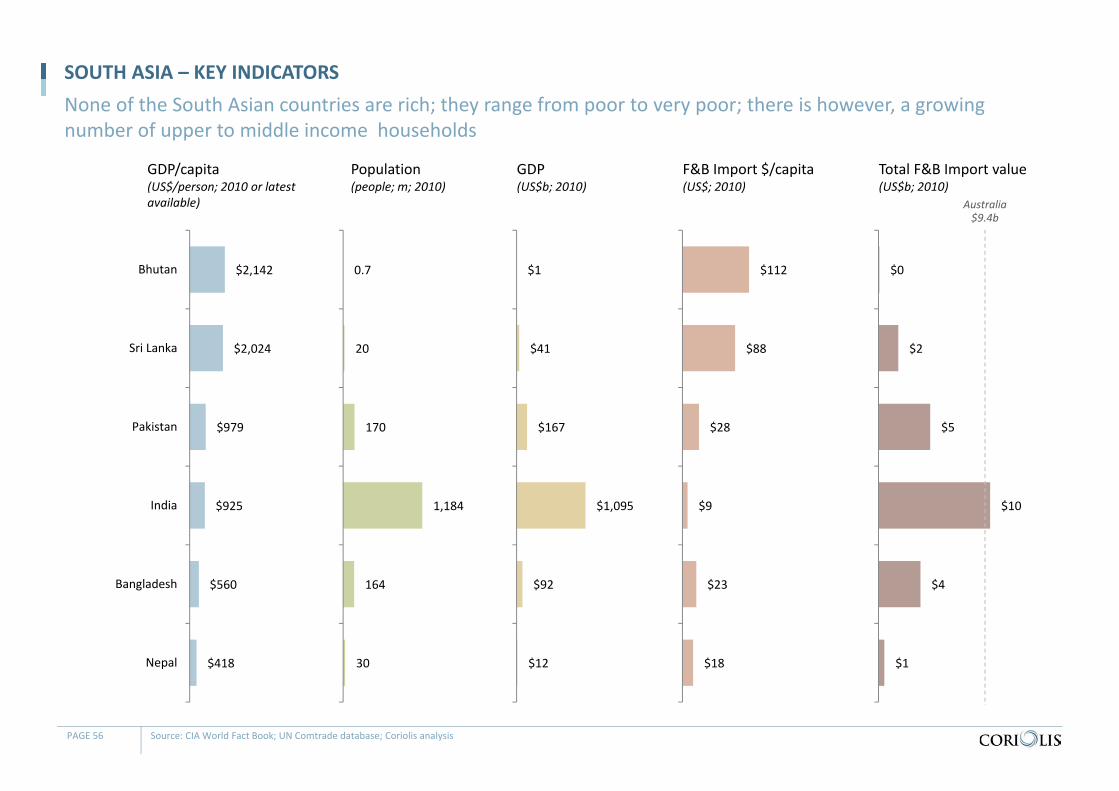

SOUTH ASIAN – REGIONAL OVERVIEWThe South Asian region, encompassing the Indian Subcontinent, represents 23% of the world population but only 2% of world GDP

PAGE 55 Source: Wikimedia Commons; Coriolis

South Asia23%

Other77%

South Asia2%Other

98%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

India

Sri Lanka

Bangladesh

BhutanNepal

Pakistan

GDP/capita(US$/person; 2010 or latest available)

SOUTH ASIA – KEY INDICATORSNone of the South Asian countries are rich; they range from poor to very poor; there is however, a growing number of upper to middle income households

PAGE 56 Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$1

$41

$167

$1,095

$92

$12

0.7

20

170

1,184

164

30

$2,142

$2,024

$979

$925

$560

$418

Bhutan

Sri Lanka

Pakistan

India

Bangladesh

Nepal

Population(people; m; 2010)

GDP(US$b; 2010)

$0

$2

$5

$10

$4

$1

Total F&B Import value(US$b; 2010)

$112

$88

$28

$9

$23

$18

F&B Import $/capita(US$; 2010)

Australia$9.4b

Dairy $0.6 3%

Meat $0.0 0%Seafood $0.2 1%

Produce $4.7 22%

Grains $1.6 7%

Other $12.8 61%

Processed $0.8 4%

Beverages $0.4 2%

Aggregate South Asia total F&B import value from all source countries(US$b; 2010)

SOUTH ASIA – TOTAL IMPORT VALUEIn aggregate South Asia imported US$21b worth of F&B in 2010 (about +23% more than Hong Kong); most imports are food basics rather than value‐added premium/processed F&B

PAGE 57 Source: UN Comtrade database; Coriolis analysis

Bhutan $0 0%

Sri Lanka $2 9%

Pakistan $5 22%

India $10 48%Bangladesh $4 18%

Nepal $1 3%

US$21b US$21b

By receiving country By product

e.g. sugar, oils & fat

India imports about as

much F&B as Singapore

Value of NZ F&B imports by country(US$m; 2010)

SOUTH ASIA – NZ PERFORMANCE BY COUNTRYNew Zealand achieves a respectable F&B import share in Sri Lanka and has opportunities for improvement elsewhere

PAGE 58 Source: UN Comtrade database; Coriolis analysis

$‐

$64

$36

$47

$28

$2

Bhutan

Sri Lanka

Pakistan

India

Bangladesh

Nepal

$‐

$3.12

$0.21

$0.04

$0.17

$0.07

NZ F&B imports per capita by country(US$/person; 2010)

NZ share of total F&B import value by country(US$b; 2010)

0.0%

3.5%

0.8%

0.5%

0.7%

0.4%

The 6 countries here (1.4b people) import about as much F&B from NZ as Fiji, Samoa

and French Polynesia combined (1.3m people)

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

Map of countries in South East Asia/ASEAN(2010)

NA/ME/CA – REGIONAL OVERVIEWThe North Africa/Middle East/Central Asia region is a predominantly Muslim region at the intersection of Africa, Asia and Europe; it accounts for 7% of world population and 4% of world GDP

PAGE 60 Source: Wikimedia Commons; Coriolis

NA/ME/CA7%

Other93%

NA/ME/CA4%

Other96%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

Mongolia

Morocco

TajikistanArmenia

Azerbaijan

Algeria

WesternSahara

Jordan

LibyaEgypt

SaudiArabia

Yemen

Oman

IranAfghanistan

Iraq

Syria

Kazakhstan

KyrgyzstanUzbekistan

Turkmenistan

LebanonIsrael

Georgia

UAE

KuwaitBahrainQatar

GDP/capita(US$/person; 2010 or latest available)

NA/ME/CA – KEY INDICATORSThe NA/ME/CA region is made up of a wide range of countries

PAGE 61 Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$93 $229

$115 $216

$19 $52

$384 $61

$33 $107

$31 $43

$332 $135

$23 $91

$9 $11 $54

$188 $70

$30 $26 $5 $5 $13

1.7 4.6 3.0 7.6

0.8 2.8

26.2 6.4 4.2

16.2 5.1 9.0

75.1 35.4

6.3 31.9

3.2 4.4

22.5 78.7

31.5 27.8 24.3

5.5 7.0

29.1

$54,546 $49,706

$38,492 $28,373 $24,475 $18,397 $14,631 $9,441 $7,732 $6,606 $6,014 $4,725 $4,419 $3,805 $3,572 $2,849 $2,682 $2,475 $2,415 $2,388 $2,228 $1,091 $1,082 $854 $658 $457

QatarUnited Arab Emirates

KuwaitIsrael

BahrainOman

Saudi ArabiaLibya

LebanonKazakhstan

TurkmenistanAzerbaijan

IranAlgeriaJordan

MoroccoArmeniaGeorgia

SyriaEgyptIraq

UzbekistanYemen

KyrgyzstanTajikistan

Afghanistan

Population(people; m; 2010)

GDP(US$b; 2010)

$2 $5

$3 $4

$1 $2

$10 $2 $2 $2

$0.3 $1 $1

$6 $2

$4 $1 $1

$2 $9

$4 $1

$2 $1 $0.4 $1

Total F&B Import value(US$b; 2010)

$897 $1,167 $1,112

$513 $1,346

$695 $364 $303 $458

$133 $51 $109 $10 $169 $351

$119 $176 $185 $107 $118 $141

$22 $98 $92 $51 $21

F&B Import $/capita(US$; 2010)

1

Australia$9.4b

Dairy $6 9%

Meat $7 9%

Seafood $2 3%

Produce $7 10%

Grains $20 29%

Other $15 23%

Processed $9 13%

Beverages $3 4%

Aggregate NA/ME/CA total F&B import value from all source countries(US$b; 2010)

NA/ME/CA – TOTAL IMPORT VALUENorth Africa, the Middle East and Central Asia imported US$69b worth of F&B; the region requires significant imports of food “basics” (grains, sugar, oils & fats) due to it being (in general) quite dry

PAGE 62 Source: UN Comtrade database; Coriolis analysis

Qatar $2 2%

United Arab

Emirates $5 8%

Kuwait $3 5%

Israel $4 6%

Bahrain $1 2%

Oman $2 3%

Saudi Arabia $10 14%

Libya $2 3%

Lebanon $2 3%

Kazakhstan $2 3%

Turkmenistan $0.3 0%

Azerbaijan $1 1%

Iran $1 1%

Algeria $6 9%Jordan $2 3%

Morocco $4 6%

Armenia $1 1%

Georgia $1 1%

Syria $2 3%

Egypt $9 14%

Iraq $4 6%

Uzbekistan $1 1%

Yemen $2 3%

Kyrgyzstan $1 1%

Tajikistan $0.4 1%

Afghanistan $1 1%

US$69b US$69b

By receiving country By product

e.g. sugar, oils & fat

Value of NZ F&B imports by country(US$m; 2010)

NA/ME/CA – NZ PERFORMANCE BY COUNTRYNew Zealand performs well in a number of the richer countries, but there are opportunities across the region

PAGE 63 Source: UN Comtrade database; Coriolis analysis

$17 $7

$100 $2

$66 $29

$266 $15

$5 $0 $0 $18

$55 $188

$45 $67

$10 $8

$99 $132

$1 $5

$29 $0 $2 $0

QatarUnited Arab…

KuwaitIsrael

BahrainOman

Saudi ArabiaLibya

LebanonKazakhstan

TurkmenistanAzerbaijan

IranAlgeriaJordan

MoroccoArmeniaGeorgia

SyriaEgyptIraq

UzbekistanYemen

KyrgyzstanTajikistan

Afghanistan

$10 $1.42

$33 $0.28

$84 $10 $10

$2 $1.20 $0.02 $0.04 $2 $0.73 $5 $7

$2 $3 $2 $4 $2 $0.02 $0.18 $1 $0.05 $0.24 $0.00

NZ F&B imports per capita by country(US$/person; 2010)

NZ share of total F&B import value by country(US$b; 2010)

1%0%

3%0%

6%1%

3%1%

0%0%0%

2%8%

3%2%

2%2%

1%4%

1%0%

1%1%

0%0%

0%

What is required to move these countries to

Australian levels of share (i.e. ~20%)

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

Map of countries and regions in North America(2010)

NORTH AMERICA – REGIONAL OVERVIEWThe North American region, encompasses the United States (50 states) and Canada (13 provinces/territories), accounts for 5% of global population and 27% of global GDP

PAGE 65 Source: Wikimedia Commons; Coriolis

N. America

5%Other95%

N. America27%

Other73%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

Canada

UnitedStates

BritishColumbia Alberta

SaskatchewanManitoba

Ontario

Quebec

Newfoundland & Labrador

New BrunswickNova Scotia

Prince Edward I.

Yukon

Alaska

NunavutNorthwest Territories

Washington

Oregon

California

Arizona

Texas

Florida

Nevada

Idaho

MontanaN. Dakota

S. DakotaWyoming

Utah Colorado

NewMexico

GeorgiaS. Carolina

N. Carolina

Virginia

Oklahoma

Kansas

Nebraska

MN

Louisiana

MS AL

TN

KYMO

AR

IO

IL

WIMI

IN OHPA

NY

WV MarylandDelawareNew Jersey

MaineMassachusettsNH

VT

CT RI

GDP/capita(US$/person; 2010)

NORTH AMERICA – KEY INDICATORSThe United States and Canada are both rich countries that import a lot of food and beverages (F&B)

PAGE 66 Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$46,582

$39,059

United States

Canada

Population(people; m; 2010)

GDP(US$b; 2010)

Total F&B Import value(US$b; 2009)

F&B Import $/capita(US$; 2009)

Australia$9.4b

309.8

34.2

$14,430

$1,335

$306

$804

$95

$27

Dairy $2.9 2%

Meat $7.5 6%

Seafood $17.5 14%

Produce $23.0 19%

Grains $4.0 3%

Other $20.8 17%

Processed $23.8 20%

Beverages $22.7 19%

Aggregate USA/Canada total F&B import value from all source countries(US$b; 2010)

NORTH AMERICA – TOTAL IMPORT VALUEIn aggregate North America imported US$122b worth of F&B in 2010; imports underperform in dairy and meat

PAGE 67 Source: UN Comtrade database; Coriolis analysis

United States 78%

Canada 22%

US$122b US$122b

By receiving country By product

Value of NZ F&B imports by country(US$m; 2010)

NORTH AMERICA – NZ PERFORMANCE BY COUNTRYNew Zealand is a relatively minor exporter to the United States and Canada

PAGE 68 Note: Some amount of the shipments to the Netherlands and Belgium (in particular) are for on shipment to the rest of Europe; unfortunately these are not effectively separable in the data; given what is here is the receiving countries report, there will therefore be some double counting; Source: UN Comtrade database; Coriolis analysis

NZ F&B imports per capita by country(US$/person; 2010)

NZ share of total F&B import value by country(US$b; 2010)

$1,817

$302

United States

Canada

$5.87

$8.83

1.9%

1.1%

NZ share of regional F&B imports by sector(% of value; 2010)

NORTH AMERICA – NZ PERFORMANCE BY SECTORNew Zealand performs well in dairy and meat into North America in terms of share; share is low otherwise

PAGE 69 Source: UN Comtrade database; Coriolis analysis

$0.5

$1.0

$0.2

$0.1

$0.0

$0.0

$0.1

$0.3

$2.5

$6.5

$17.3

$22.8

$4.0

$20.8

$23.7

$22.4

17%

13%

1%

1%

0%

0%

0%

1%

Dairy

Meat

Seafood

Produce

Grains

Other

Processed

Beverages

NZ Other

$0.5

$1.0

$0.2

$0.1

$0.0

$0.0

$0.1

$0.3

Value of NZ F&B imports to region by sector(US$b; 2010)

Value of total F&B imports to region by sector(US$b; 2010)

TABLE OF CONTENTS

Section Page

Contents 4

Glossary of terms 5

Methodology & data sources 6

F&B IP Overview 8

New Zealand F&B trade overview 10

New Zealand performance by region/market 16

a. High priority markets

1. Australia/Pacific Islands 23

2. South East Asia 33

3. East Asia 44

b. Secondary markets

1. South Asia 54

2. North Africa/Middle East/Central Asia 59

3. North America 64

4. Europe 70

c. Other markets 75

Map of countries in Europe(2010)

EUROPE – REGIONAL OVERVIEWThe European region (including Russia) accounts for 12% of global population and a third of global GDP

PAGE 71 Source: Wikimedia Commons; Coriolis

Europe/ Russia12%

Other88%

Europe/ Russia33%

Other67%

% of global population(people; 2010)

% of global gross domestic product(% US$; nominal; 2010)

Turkey

Belorussia

Portugal

Russia

Ukraine

Finland

PolandGermany

France

Spain

Iceland

IrelandU.K.

Italy

Sweden

Norway

Denmark

Estonia

Latvia

Lithuania

CzechSlovakia

Romania

Bulgaria

Greece

MoldovaSwiss Austria Hungary

Balkancountries

Netherlands

BelgiumLux

Slovenia

GDP/capita(US$/person; 2010 or latest available)

EUROPE – KEY INDICATORSEurope is made up of a wide range of countries ranging from very rich to poor

PAGE 72 Source: CIA World Fact Book; UN Comtrade database; Coriolis analysis

$47 $369 $484

$308 $227

$799 $242 $374 $462 $398

$2,666 $3,273

$12 $2,198 $2,090

$1,466 $338

$23 $50 $220

$8 $190 $88 $62 $18 $124 $423

$24 $36

$1,232 $608

$161 $4 $45 $49 $17 $9 $42 $12 $116 $11 $5

0.5 4.9 7.8 5.5 4.5

16.6 5.4 8.4 10.8 9.4

65.4 81.8

0.3 62.0 60.3

47.0 11.3

0.8 2.1 10.6

0.4 10.5 5.4 4.4 1.3 10.0

38.2 2.2 3.3

141.9 72.6

21.5 0.6 7.6 9.5 3.8 2.0 9.9

3.2 45.9

4.4 3.6

$92,611 $75,420

$62,200 $55,647

$50,860 $48,121 $45,168 $44,716 $42,623 $42,462 $40,735 $40,033 $37,056 $35,428 $34,637 $31,224 $29,922 $28,958

$24,037 $20,664 $18,528 $18,045 $16,277 $13,916 $13,470 $12,403 $11,083 $10,805 $10,801 $8,681 $8,385 $7,486 $7,122 $5,910 $5,177 $4,502 $4,308 $4,304 $3,671 $2,522 $2,475 $1,495

LuxembourgNorway

SwitzerlandDenmarkIreland

NetherlandsFinlandAustriaBelgiumSwedenFrance

GermanyIceland

United KingdomItalySpain

GreeceCyprus

SloveniaPortugal

MaltaCzech Republic

SlovakiaCroatiaEstoniaHungaryPolandLatvia

LithuaniaRussiaTurkey

RomaniaMontenegro

BulgariaBelarus

Bosnia HerzegovinaMacedonia

SerbiaAlbaniaUkraineGeorgiaMoldova

Population(people; m; 2010)

GDP(US$b; 2010)

$2 $6 $9 $10

$7 $38

$4 $10

$31 $12

$46 $74

$0 $50

$37 $29

$8 $1 $2

$9 $1

$6 $4 $2 $1 $4

$11 $1 $2

$25 $5 $4

$0 $2 $2 $1 $1 $1 $1 $4

$1 $‐

Total F&B Import value(US$b; 2009)

$3,954 $1,141 $1,179

$1,755 $1,504

$2,292 $829 $1,167

$2,818 $1,233

$706 $900 $1,232

$800 $614 $613 $675

$1,296 $896 $869

$1,406 $589 $673

$416 $1,048

$365 $276 $660 $708

$179 $73 $203

$793 $272 $206 $368 $310 $90 $202 $92 $152 $‐

F&B Import $/capita(US$; 2009)

Australia$9.4b

Dairy $35 8%

Meat $59 13%

Seafood $43 9%

Produce $73 16%

Grains $25 5%

Other $81 17%

Processed $96 21%

Beverages $51 11%

Aggregate European total F&B import value from all source countries(US$b; 2009)

EUROPE – TOTAL IMPORT VALUEIn aggregate Europe imported US$463b worth of F&B in 2009; imports were spread across all sectors

PAGE 73 Source: UN Comtrade database; Coriolis analysis

Luxembourg 0%

Norway 1%

Switzerland 2%

Denmark 2%

Ireland 1%

Netherlands 8%

Finland 1%Austria 2%

Belgium 7%

Sweden 2%

France 10%

Germany 16%

Iceland 0%

United Kingdom 11%

Italy 8%Spain 6%

Greece 2%Cyprus 0%

Slovenia 0%Portugal 2%

Malta 0%

Czech Republic 1%

Slovakia 1%

Croatia 0%Estonia 0%

Hungary 1%Poland 2%

Latvia 0%

Lithuania 1%

Russia 5%

Turkey 1%

Romania 1%

Montenegro 0%

Bulgaria 0%

Belarus 0%

Bosnia Herzegovina 0%Macedonia 0%

Serbia 0% Albania 0%Ukraine 1%

Georgia 0%

US$463b US$463b

By receiving country By product

e.g. coffee, cocoa, sugar, oils & fat

Value of NZ F&B imports by country(US$m; 2009)

EUROPE – NZ PERFORMANCE BY COUNTRYNew Zealand is a relatively minor player in European F&B imports

PAGE 74 Note: Some amount of the shipments to the Netherlands and Belgium (in particular) are for on shipment to the rest of Europe; unfortunately these are not effectively separable in the data; given what is here is the receiving countries report, there will therefore be some double counting; Source: UN Comtrade database; Coriolis analysis

$0 $18

$67 $69

$27 $320

$21 $31

$401 $39

$333 $549

$1 $905

$86 $138

$40 $14 $1 $19 $5 $3 $1 $4 $1 $0 $8 $0 $0

$109 $5 $0 $0 $2 $3 $1 $0 $1 $1 $5 $6