fonterra annual results 2013 · global everyday nutrition brand portfolio crafted quality ......

TRANSCRIPT

© Fonterra Co-operative Group Ltd. 1 © Fonterra Co-operative Group Ltd.

© FONTERRA CO-OPERATIVE GROUP LIMITED

FONTERRA

ANNUAL RESULTS 2013

© Fonterra Co-operative Group Ltd. 2 © Fonterra Co-operative Group Ltd.

John Wilson – Chairman

© Fonterra Co-operative Group Ltd. 3 © Fonterra Co-operative Group Ltd.

Key highlights

FARMGATE MILK PRICE

$5.84kgMS

DIVIDEND

32 cps

EARNINGS PER SHARE

44 cps

DEBT TO DEBT PLUS EQUITY

39.6%

FINAL CASH PAYOUT

$6.16

NET PROFIT

$736m

© Fonterra Co-operative Group Ltd. 4 © Fonterra Co-operative Group Ltd.

Cash payout

(1) Cents per share

(2) $ per kgMS

(1)

6.10 7.60 6.08 5.84 8.30

0.27

0.30

0.32 0.32

0.32

6.37

7.90

6.40 6.16

8.62

2010 2011 2012 2013 2014F

Dividend Farmgate Milk Price (2) (1)

© Fonterra Co-operative Group Ltd. 5 © Fonterra Co-operative Group Ltd.

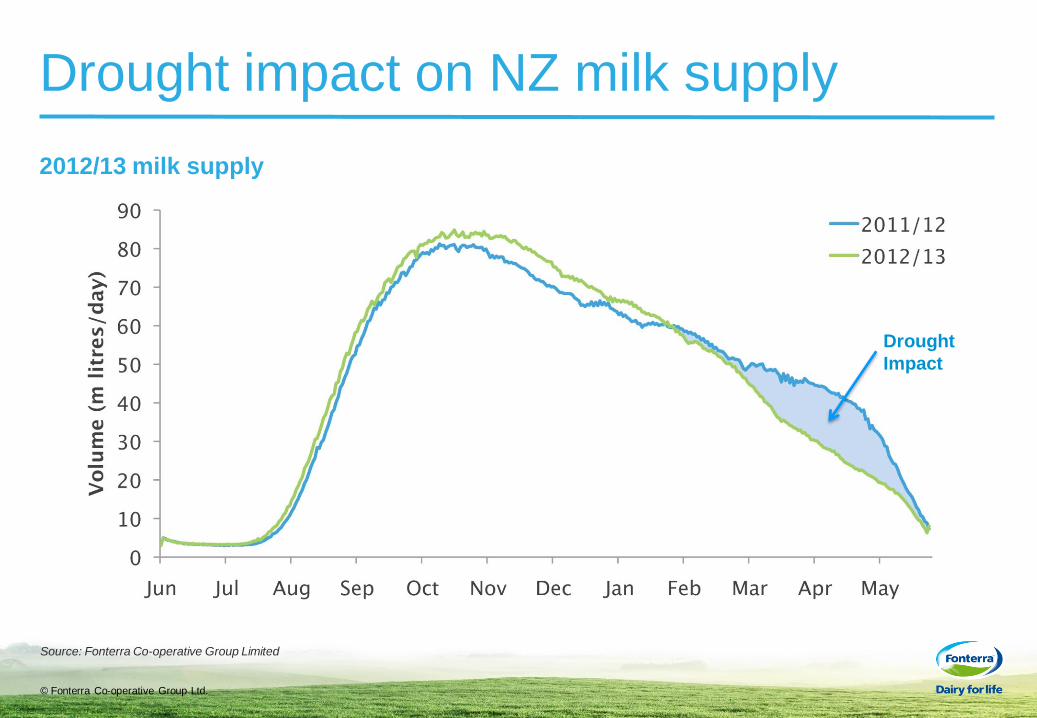

Drought impact on NZ milk supply

Source: Fonterra Co-operative Group Limited

2012/13 milk supply

Drought

Impact

© Fonterra Co-operative Group Ltd. 6 © Fonterra Co-operative Group Ltd.

Stronger Capital Structure

Nov 2012 Trading Among Farmers launched

Mar 2013 More flexible contracts for new

and growing, farmers

Apr 2013 1:40 Bonus Issue

May 2013 Second Supply Offer

No drought related capital outflows – confirming redemption risk has

been removed

© Fonterra Co-operative Group Ltd. 7 © Fonterra Co-operative Group Ltd.

Theo Spierings – CEO

© Fonterra Co-operative Group Ltd. 8 © Fonterra Co-operative Group Ltd.

Results highlights

Volume • Volume up in all segments, excluding ANZ

• Asia/Africa & Middle East - up 11%

• NZ Milk Products - up 1%

• Latin America - up 6%

• Australia/New Zealand - down 2% (excluding Norco)

Value • NPAT of $736m - up 18%

• Normalised EBIT - down 3%

• Normalised EPS of 471 cps

GROUP SALES VOLUME

4m MT

GROUP NORMALISED EBIT

$1BN

Note 1: Normalised EPS is calculated as net profit after tax attributed to equity holders of the Company, adjusted for normalisation adjustments, divided by the

weighted average number of Cooperative shares on issue. The normalisation adjustments are tax effected.

© Fonterra Co-operative Group Ltd. 9 © Fonterra Co-operative Group Ltd.

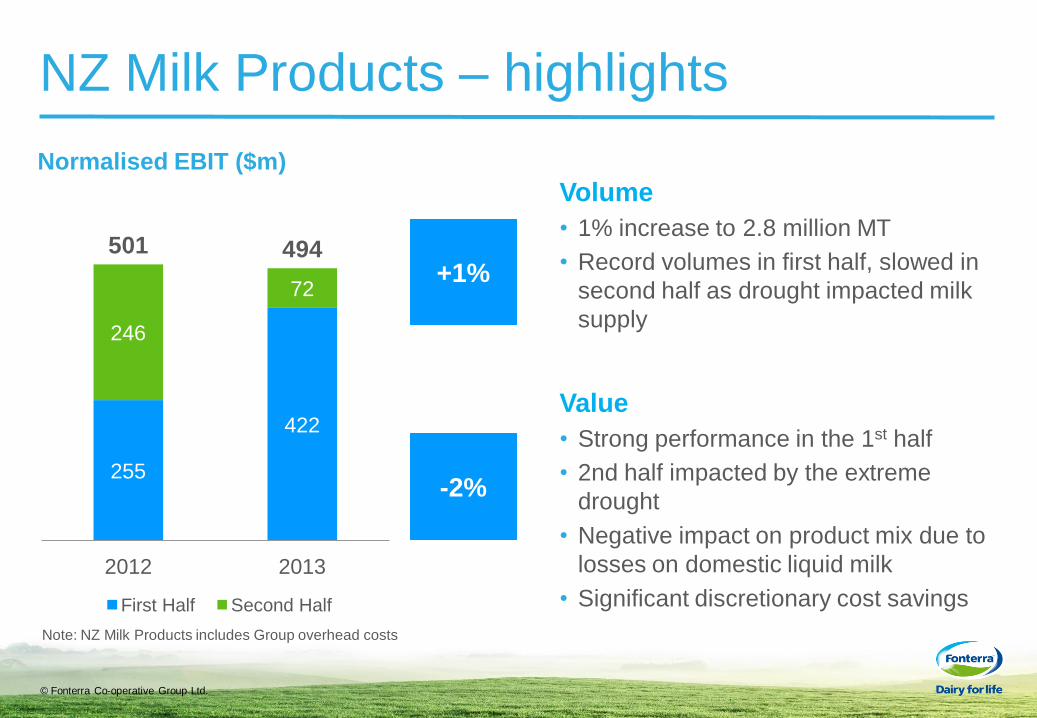

NZ Milk Products – highlights

-2%

+1%

Volume

• 1% increase to 2.8 million MT

• Record volumes in first half, slowed in

second half as drought impacted milk

supply

Value

• Strong performance in the 1st half

• 2nd half impacted by the extreme

drought

• Negative impact on product mix due to

losses on domestic liquid milk

• Significant discretionary cost savings

Normalised EBIT ($m)

255

422

246

72

501 494

2012 2013

First Half Second Half

Note: NZ Milk Products includes Group overhead costs

© Fonterra Co-operative Group Ltd. 10 © Fonterra Co-operative Group Ltd.

NZMP – key performance drivers

501

26

107

18 43

49

494

2012 Price Premiums

Product Mix

Quality Issues

Global Sourcing

Other/Cost Savings

2013

Normalised EBIT ($m)

© Fonterra Co-operative Group Ltd. 11 © Fonterra Co-operative Group Ltd.

Volatility in prices of powder and

non-powder products

-350

-300

-250

-200

-150

-100

-50

0

50

100

150

Aug-08 Feb-09 Aug-09 Feb-10 Aug-10 Feb-11 Aug-11 Feb-12 Aug-12 Feb-13 Aug-13

NZ Milk Products profit impact ($m)

© Fonterra Co-operative Group Ltd. 12 © Fonterra Co-operative Group Ltd.

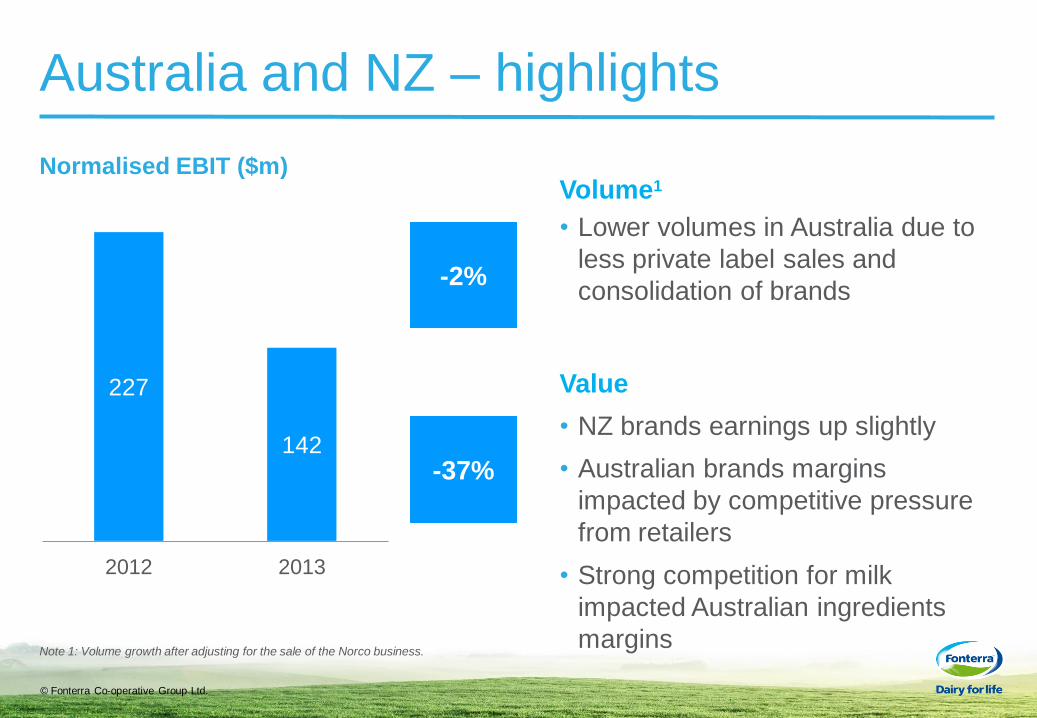

Australia and NZ – highlights

Volume1

• Lower volumes in Australia due to

less private label sales and

consolidation of brands

Value

• NZ brands earnings up slightly

• Australian brands margins

impacted by competitive pressure

from retailers

• Strong competition for milk

impacted Australian ingredients

margins

-37%

-2%

Note 1: Volume growth after adjusting for the sale of the Norco business.

Normalised EBIT ($m)

227

142

2012 2013

© Fonterra Co-operative Group Ltd. 13 © Fonterra Co-operative Group Ltd.

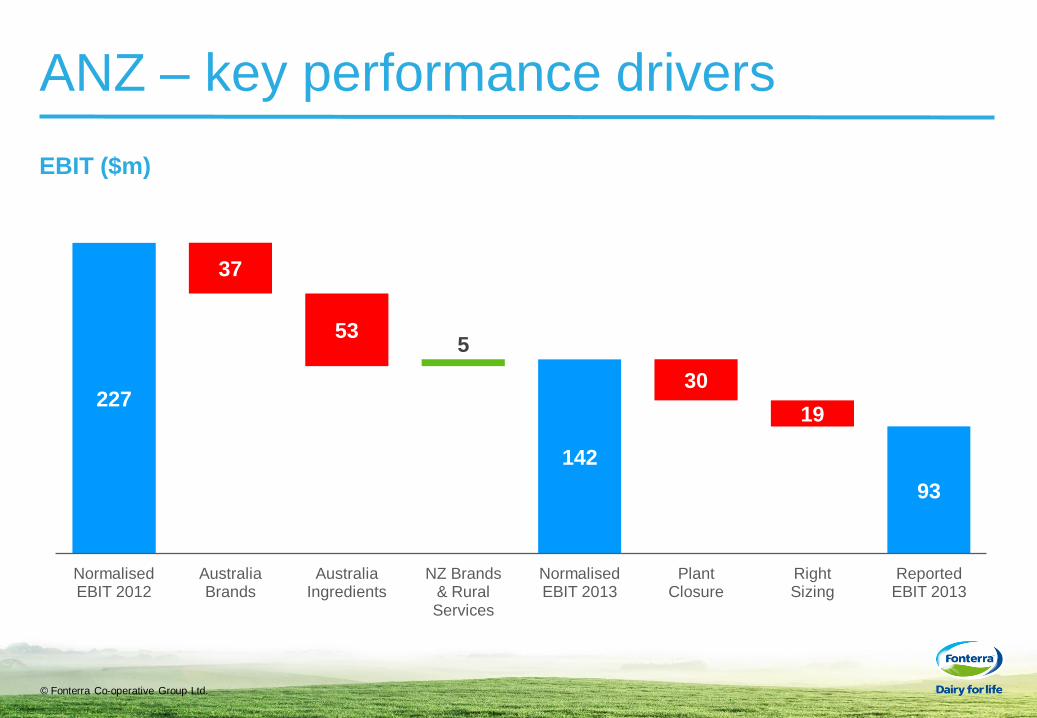

ANZ – key performance drivers

EBIT ($m)

227

37

53 5

142

30

19

93

Normalised EBIT 2012

Australia Brands

Australia Ingredients

NZ Brands & Rural Services

Normalised EBIT 2013

Plant Closure

Right Sizing

Reported EBIT 2013

© Fonterra Co-operative Group Ltd. 14 © Fonterra Co-operative Group Ltd.

Reshaping our Australian business

Tough environment

Retailers

Processors

Suppliers

Strong rivalry

Aggressive

competition for

milk supply

Intense retailer

pressure

1. Streamline brands portfolio

2. Grow everyday nutrition

3. Expand high-value nutritionals

4. Drive foodservice business

5. Reduce cost and complexity

Five key priorities

© Fonterra Co-operative Group Ltd. 15 © Fonterra Co-operative Group Ltd.

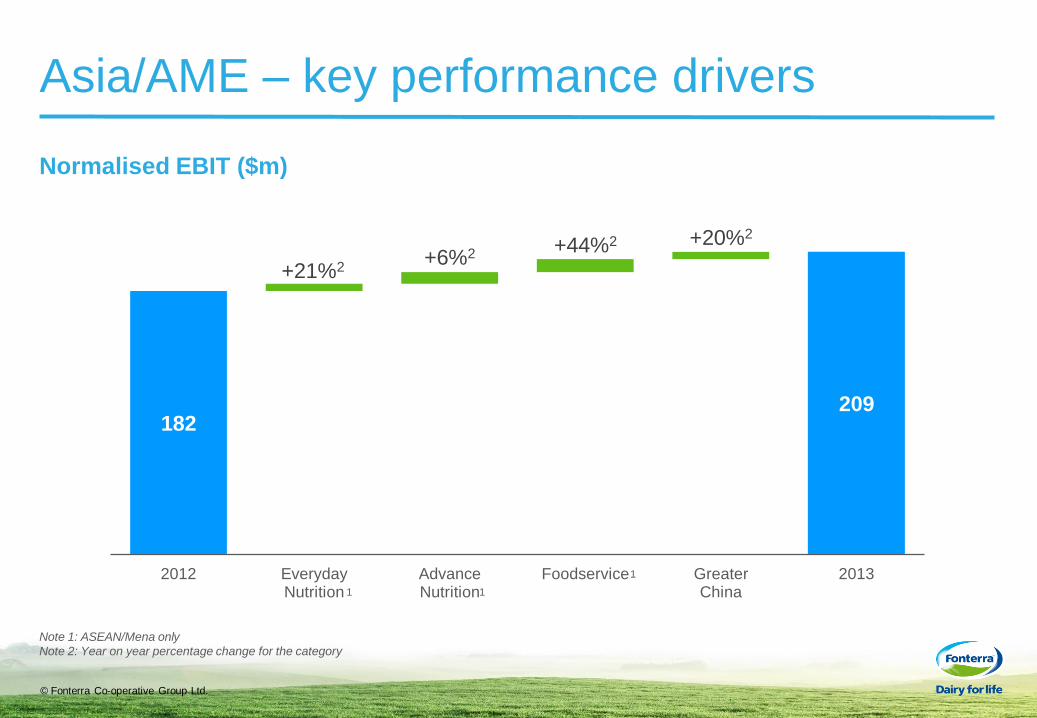

Asia/Africa/Middle East – highlights

Volume

• Growth driven by Greater China,

Indonesia, Malaysia and Vietnam

Value

• Asia/AME now our largest

consumer business

• Up 22% in ASEAN/MENA1

• Up 21% in Greater China1

+16%

+11%

Normalised EBIT ($m)

182 209

2012 2013

Note 1: Normalised EBIT measured by constant currency.

ASEAN/MENA means Fonterra’s business unit that operates in South East Asia, the Middle East and North Africa. There are some countries that fall within the

ASEAN/MENA business unit that are located outside these geographical regions such as Sri Lanka and Mauritius. It is part of the Asia/AME reportable segment.

© Fonterra Co-operative Group Ltd. 16 © Fonterra Co-operative Group Ltd.

Asia/AME – key performance drivers

Normalised EBIT ($m)

182

+21%2 +6%2 +44%2 +20%2

209

2012 Everyday Nutrition

Advance Nutrition

Foodservice Greater China

2013

Note 1: ASEAN/Mena only

Note 2: Year on year percentage change for the category

1 1

1

© Fonterra Co-operative Group Ltd. 17 © Fonterra Co-operative Group Ltd.

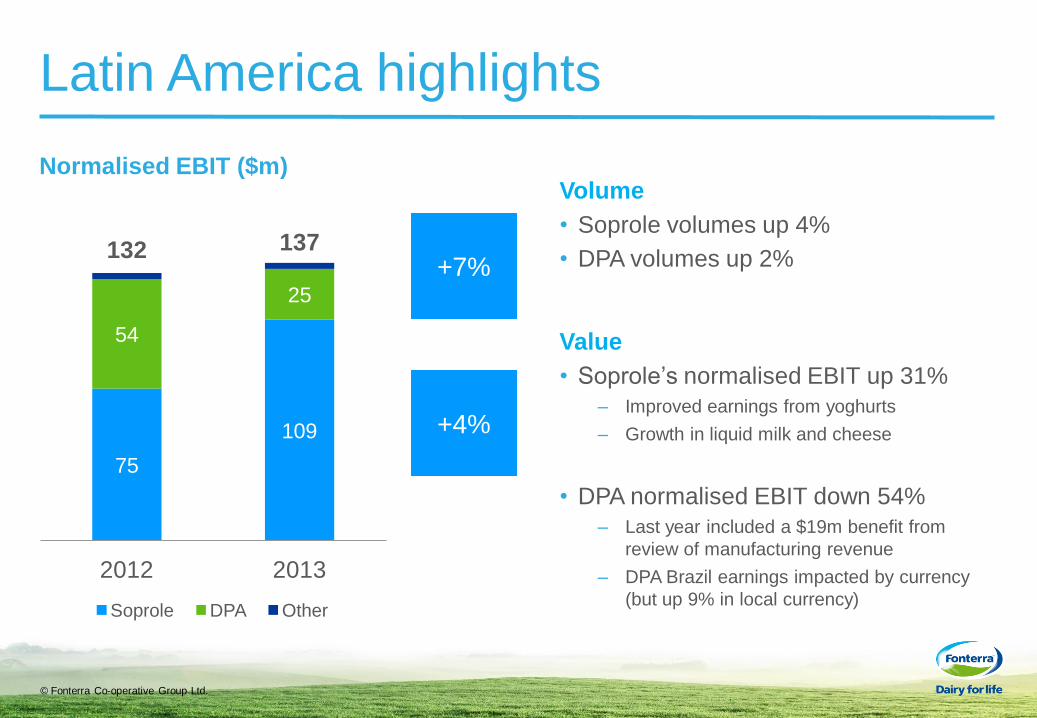

Latin America highlights

Volume

• Soprole volumes up 4%

• DPA volumes up 2%

Value

• Soprole’s normalised EBIT up 31%

– Improved earnings from yoghurts

– Growth in liquid milk and cheese

• DPA normalised EBIT down 54%

– Last year included a $19m benefit from

review of manufacturing revenue

– DPA Brazil earnings impacted by currency

(but up 9% in local currency)

+4%

+7%

Normalised EBIT ($m)

75

109

54

25

132 137

2012 2013

Soprole DPA Other

© Fonterra Co-operative Group Ltd. 18 © Fonterra Co-operative Group Ltd.

Latam – key performance drivers

Normalised EBIT ($m)

132

26 25 9

5

137

2012 Soprole DPA Southern Cone

Other 2013

© Fonterra Co-operative Group Ltd. 19 © Fonterra Co-operative Group Ltd.

Working Capital and Cash Flow

Note 1: excluding supplier payables

Working Capital Days1

Average working capital days improved by 8 days

to 98 days ($400m cash benefit)

105 106

98

2011 2012 2013

Operating & Investing Cash Flow

696

564

129

2011 2012 2013

688

Impact of advance rate change

© Fonterra Co-operative Group Ltd. 20 © Fonterra Co-operative Group Ltd.

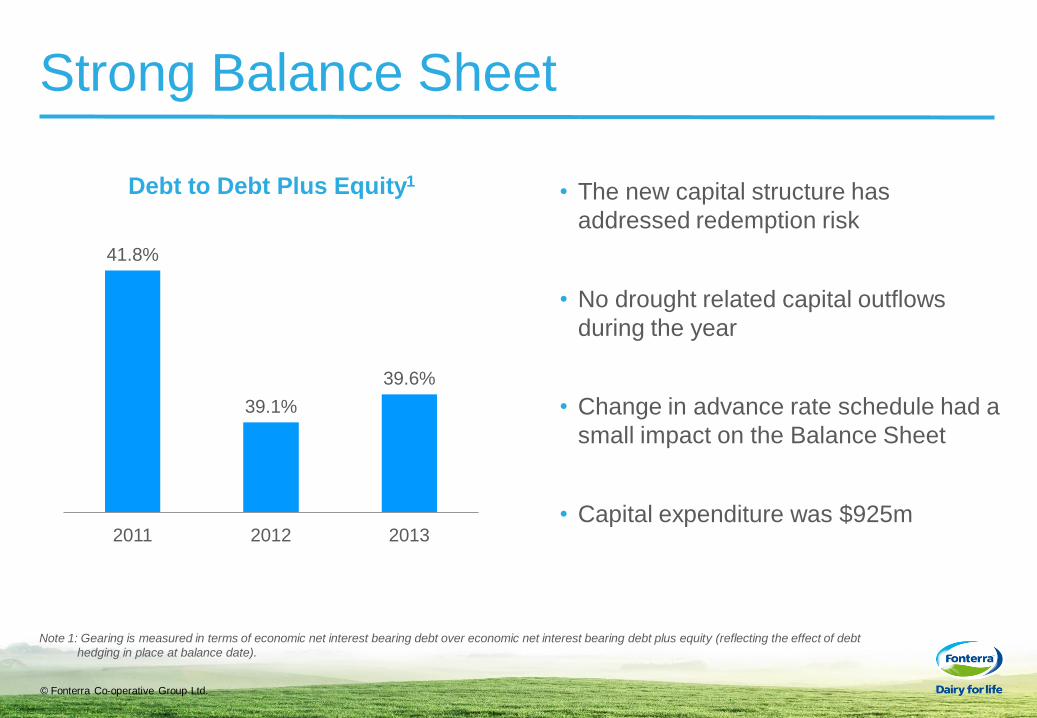

Strong Balance Sheet

Note 1: Gearing is measured in terms of economic net interest bearing debt over economic net interest bearing debt plus equity (reflecting the effect of debt

hedging in place at balance date).

Debt to Debt Plus Equity1

41.8%

39.1%

39.6%

2011 2012 2013

• The new capital structure has

addressed redemption risk

• No drought related capital outflows

during the year

• Change in advance rate schedule had a

small impact on the Balance Sheet

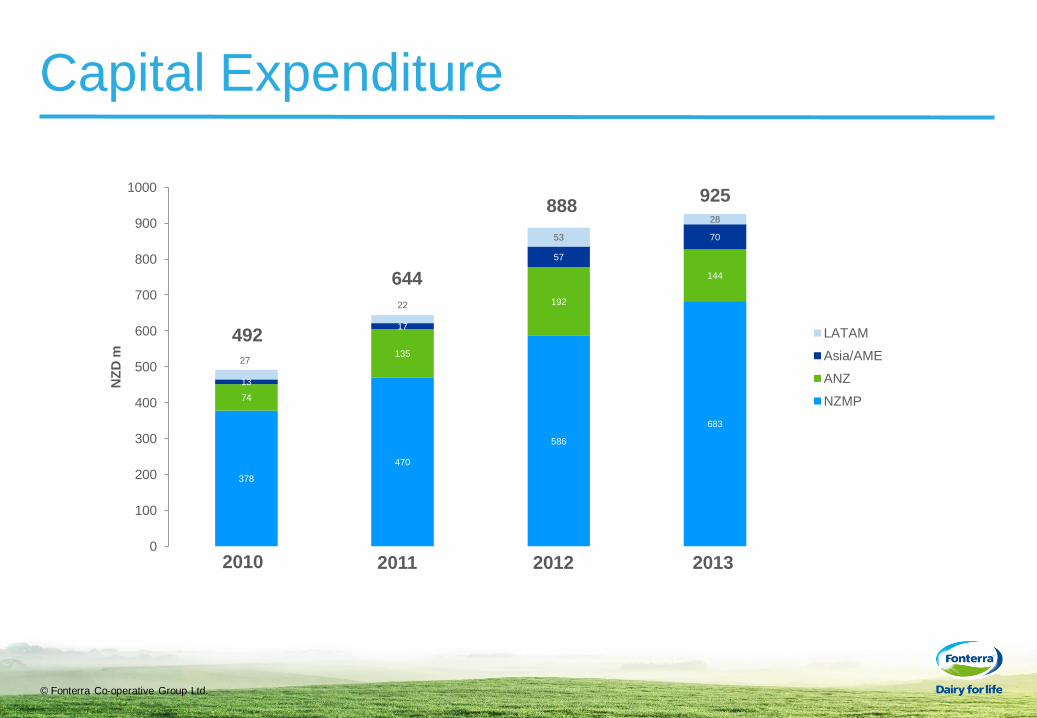

• Capital expenditure was $925m

© Fonterra Co-operative Group Ltd. 21 © Fonterra Co-operative Group Ltd.

Strategy Update & Outlook

© Fonterra Co-operative Group Ltd. 22 © Fonterra Co-operative Group Ltd.

Global trends driving demand for dairy

Continued

rise of

emerging

markets

Commodity

price

volatility

Nutrition for

the young

Nutrition for

the old

Sustainability

Disruption

© Fonterra Co-operative Group Ltd. 23 © Fonterra Co-operative Group Ltd.

Good progress on strategy STRATEGIC PATHS PROGRESS

Selectively

invest in milk pools

Alignment of

business and organisation

6

7

Develop selected leading

position in paediatrics &

maternal

Grow our

position in Anlene

Deliver on

foodservice potential

Build and grow beyond our

current consumer positions

Optimise NZ milk

1

2

3

4

5

EVERYDAY

NUTRITION

OUT-OF-HOME

ENABLERS

ADVANCED

NUTRITION

Darfield investment & Studholme acquisition

Optimise and drive value add products

Strong quality improvement and food safety focus

Reshape Australia brands

Launch of Anchor UHT in China

Asia and China roll-out tracking ahead of plan

$100m investment in UHT plant to remove supply

constraints

Growing Anlene in China and selected growth markets in

South East Asia

Pursue Anmum growth in China and Indonesia

Higher demand from emerging markets for paediatrics

third party manufacturing

Signed agreements to start second farming hub in China

Two farming hubs will produce 300m litres of milk

Support review completed in August

Australia rightsizing

Investing resources in China expansion

© Fonterra Co-operative Group Ltd. 24 © Fonterra Co-operative Group Ltd.

Adding value to our NZ milk pool

© Fonterra Co-operative Group Ltd. 25 © Fonterra Co-operative Group Ltd.

Everyday Nutrition

• Focus: Fewer, bigger brands

• Build from the core: butter and cheese

• Build more FMCG-oriented culture

Global Everyday Nutrition Brand Portfolio

Crafted Quality Natural Taste

Italian Culinary Taste

Enhancement Dairy Expert

Everyday Affordable & Accessible

Local Jewel Emerging Future

Global Power Brand

Global Power Brand Local Jewels

© Fonterra Co-operative Group Ltd. 26 © Fonterra Co-operative Group Ltd.

Foodservice

• Grow our leading positions in key target

markets

• Significant year-on-year growth

• Annual sales now over $1.3bn

• Continue to drive growth through:

– Greater investment in supply capacity

– Distinctive chef-led solution selling model

– Product/technology leadership

© Fonterra Co-operative Group Ltd. 27 © Fonterra Co-operative Group Ltd.

Advanced Nutrition

• Key focus to develop Anmum in selected markets

– Market leader in Malaysia

– Top 3 in Indonesia

– Build on Anmum’s success in Hong Kong and

extend further into China

• Continue to grow Anlene in high calcium category

• Expand Anlene in China and growth regions in

South East Asia

© Fonterra Co-operative Group Ltd. 28 © Fonterra Co-operative Group Ltd.

Strategy shifts portfolio to higher value add

ILLUSTRATIVE ONLY

© Fonterra Co-operative Group Ltd. 29 © Fonterra Co-operative Group Ltd.

Outlook

• 2014 Forecast Cash Payout of $8.62

– Forecast Farmgate Milk Price of $8.30

– Estimated dividend of 32 cps

• Headwinds for Fonterra

– Higher input costs make it harder to drive value growth in brands and foodservice in first half

– Negative impact on product mix margins as milk powder prices significantly outpace cheese and casein prices

– First half 2014 result will be significantly lower than first half 2013

– Prospects for second half look more positive for consumer businesses but remain uncertain for NZ Milk Products

• Estimated dividend of 32 cps unchanged

– Fonterra can draw on its Balance Sheet and Cash Flow strength to support estimated dividend, if required

• Confident in our Volume and Value strategy

– Difficult to predict when extreme price volatility on product mix will reverse, but expectations are that impact is likely to be short-term

– Future prospects for dairy and for Fonterra positive - our growth ambitions remain unchanged

© Fonterra Co-operative Group Ltd. 30 © Fonterra Co-operative Group Ltd.

Supplementary Information

© Fonterra Co-operative Group Ltd. 31 © Fonterra Co-operative Group Ltd.

Annual results summary

Million

Year ended

31 July 2013

Year ended

31 July 2012 Change

Total Sales Volume (million MT)

3.96

3.94

0%

Revenue

18,643

19,796

(6%)

Normalised EBIT (NZD million)

1,002

1,028

3%

Net Profit After Tax (NZD million)

736

624

18%

Earnings per share (cents)

44

41

7%

Dividends per share (cents)

32

32

0%

© Fonterra Co-operative Group Ltd. 32 © Fonterra Co-operative Group Ltd.

Normalisation adjustments

Million

Year ended

31 July 2013

Year ended

31 July

2012

Costs associated with planned closure of

Cororooke site (30) –

Costs associated with the Group’s Strategy Right-

sizing (38) –

Restructuring costs associated with the Group

Strategy Refresh – (30)

Other items 3 (3)

Impairment losses recorded in equity accounted

investees – (8)

Total normalised items (65) (41)

© Fonterra Co-operative Group Ltd. 33 © Fonterra Co-operative Group Ltd.

Reconciliation to Prospective Information

$ Million NZMP ANZ Asia/

AME

Latam Inter-

Segments

TOTAL

Prospective EBIT 517 201 223 125 (12) 1,054

Adjustments:

Changes in Org structure

17

12

(2)

6

1

-

Prospective EBIT –

adjusted

500 213 221 131 (11) 1,054

Prospective normalisation

adjustment

- 25 - - - 25

Prospective normalised

EBIT – adjusted

500 238 221 131 (11) 1,079

Actual EBIT 480 93 207 137 20 937

Actual normalisation

adjustments

14 49 2 - - 65

Actual normalised EBIT 494 142 209 137 20 1,002

© Fonterra Co-operative Group Ltd. 34 © Fonterra Co-operative Group Ltd.

NZMP contribution margin

$million Year ended

31 July 2013

Year ended

31 July 2012

Sales Volume (000MT) 2,824 2,790

Gross Margin 1,251 1,285

Selling, marketing and distribution expenses (277) (269)

Contribution margin 974 1,016

Contribution margin per MT ($) 345 364

Growth (5%)

© Fonterra Co-operative Group Ltd. 35 © Fonterra Co-operative Group Ltd.

Whole milk powder and cheese prices

2,500

2,800

3,100

3,400

3,700

4,000

4,300

4,600

4,900

5,200

Aug-11 Oct-11 Dec-11 Feb-12 Apr-12 Jun-12 Aug-12 Oct-12 Dec-12 Feb-13 Apr-13 Jun-13 Jul-13

Weighted Average USD GDT Cheese Prices vs WMP Prices

Cheese

WMP H1 2013

H2 2013

© Fonterra Co-operative Group Ltd. 36 © Fonterra Co-operative Group Ltd.

NZ Milk Products Sales Volume by Product

1,031 1030

489 464

469 477

309 301

72 66

454 452

2013 2012

Whole Milk Powder Skim Milk Powder Cream Cheese Casein Other

2,790 MT

2,824 MT

© Fonterra Co-operative Group Ltd. 37 © Fonterra Co-operative Group Ltd.

Balance sheet strength

Credit

Rating

S&P A+

(stable outlook)

Fitch AA-

(stable outlook)

Weighted

Average

Term to

Maturity

As at 31 July

2013

(Drawn debt)

3.41 years

Strong Fundamentals Diversified Funding Sources

Offshore DCM

30%

NZ DCM

20%

Bank Facilities

50%

Strong Liquidity

Undrawn Facilities

$3,289m

82%

Drawn Facilities

$715m

18%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Bank Facilities - Total Limits

Debt Capital Markets

NZ

D m

illio

ns

Debt Maturity Profile (Year Ending July)

© Fonterra Co-operative Group Ltd. 38 © Fonterra Co-operative Group Ltd.

Capital Expenditure

378

470

586

683

74

135

192

144

13

17

57

70

27

22

53

28

0

100

200

300

400

500

600

700

800

900

1000

NZ

D m

LATAM

Asia/AME

ANZ

NZMP

2012 2013 2011 2010

925 888

644

492

© Fonterra Co-operative Group Ltd. 39 © Fonterra Co-operative Group Ltd.

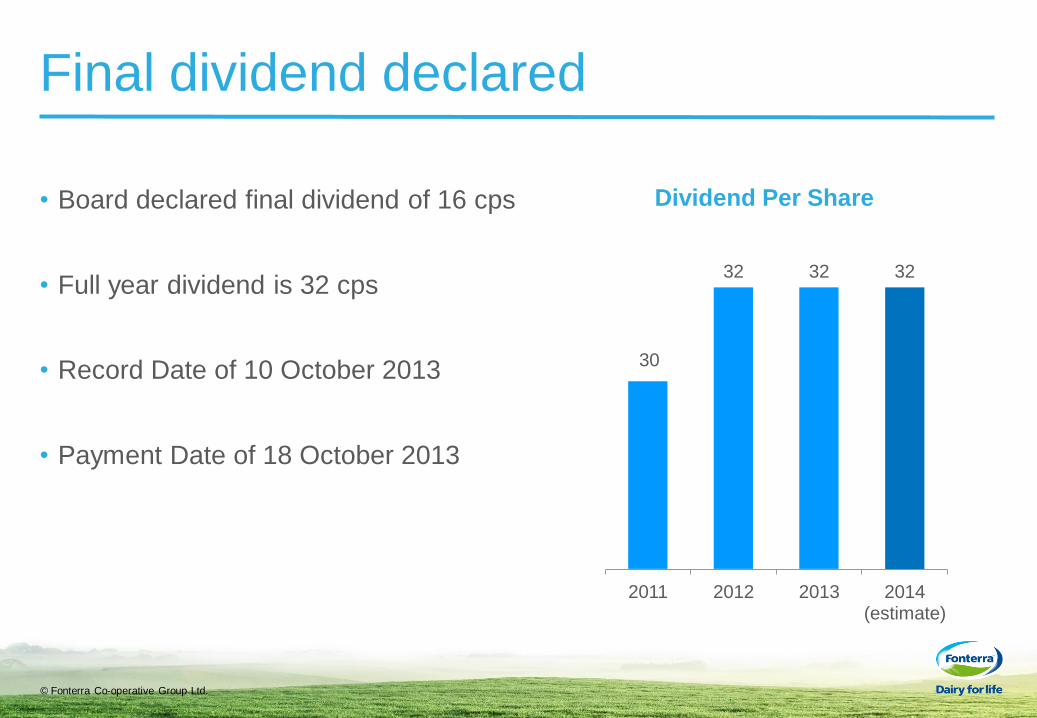

Final dividend declared

• Board declared final dividend of 16 cps

• Full year dividend is 32 cps

• Record Date of 10 October 2013

• Payment Date of 18 October 2013

30

32 32 32

2011 2012 2013 2014 (estimate)

Dividend Per Share