foecke - how? strategies for greening the supply chain

TRANSCRIPT

How? Strategies to Green the Supply

Chain

A VERY (very) LARGE PENSION FUND SAYS

RETROFIT INDUSTRIAL ENERGY EFFICIENCY IS

THE BEST ASSET CLASS ON THE PLANET

WHY?

AN INVESTIGATION WITH THE ENVIRONMENTAL

DEFENSE FUND AND WAL-MART GLOBAL

SOURCING IN CHINA VISITING OVER 600

FACTORIES IN WAL-MART’S SUPPLY CHAIN

FOUND…

30-50% reductions in energy intensity in plastics fabrication

possible

Some factories doing more than

60%--on total energy

With throughput and quality improvements

Opportunities everywhere

• Wood fabrication

• Metal fabrication

• Painting and coating

• Complex systems manufacturing

• Compressed air

• Process heating--process cooling

ALL HAVE POTENTIAL FOR 30-40% REDUCTIONS

IN TOTAL ENERGY INTENSITY

Less than 2 years simple paybacks

JUST ON ENERGY

SAVINGS

4 big conclusions

Target-rich but data poor

Data

Target

The people with the answers have poor business models

Someone has to LOOK WRONG

NO ONE WANTS TO TAKE THE HIT

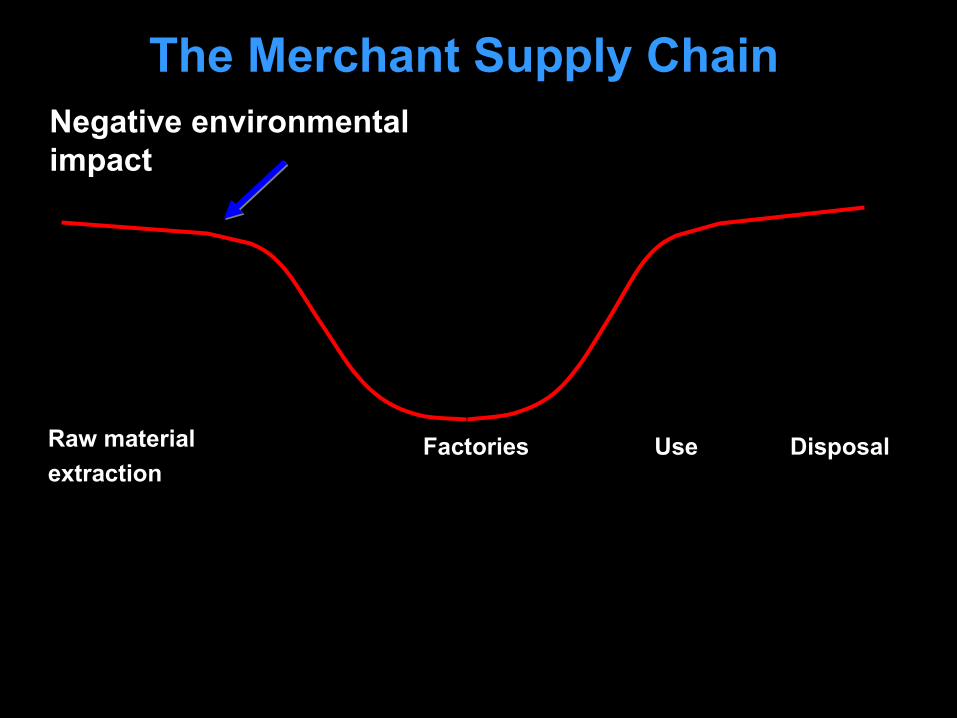

Raw material

extractionFactories Use Disposal

The Merchant Supply Chain

Product life cycle

Raw material

extractionFactories Use Disposal

Negative environmental impact

The Merchant Supply Chain

Raw material

extractionFactories Use Disposal

Negative environmental impact

Merchants’ ability toreduce impact

The Merchant Supply Chain

Where we need to go

Steps to a strategy

• More data– Meters– Process type and operation– State of play

• Better data– Self-reported just not good enough– Be bold; bring a list of proposed

alternatives tied to Best Practices

Steps to a strategy

• Are you a “manufacturing” customer?– Comfortable with process and design– Involved beyond cost, time and quality– If so, determine best practice and hold factories to

progress against that

• Or a “merchant” customer?– Focused on cost, time and quality– Limited insight into process and design– If so, make a clear link to environmental progress

against action plans and supplier acceptance

Steps to a strategy

• EE is not a core competency for factories– Usually less than 10% of controllable Cost of

Goods Sold– Avoid it because they’ve been burned or it seems

esoteric– Energy costs buried in overheadSO

• Who are your implementation partners?– EE technology providers: make it easy for them– Energy providers: help them aggregate– Consultants: use for process expertise and

oversight

Steps to a strategy

• Account for the uniqueness of each factory– Goals– Implementation arc– Presence of technical management

• Make it easy for factories to “do the right thing”– Connect rather than direct– Connect environmental progress with

manufacturing excellence– Collaborate

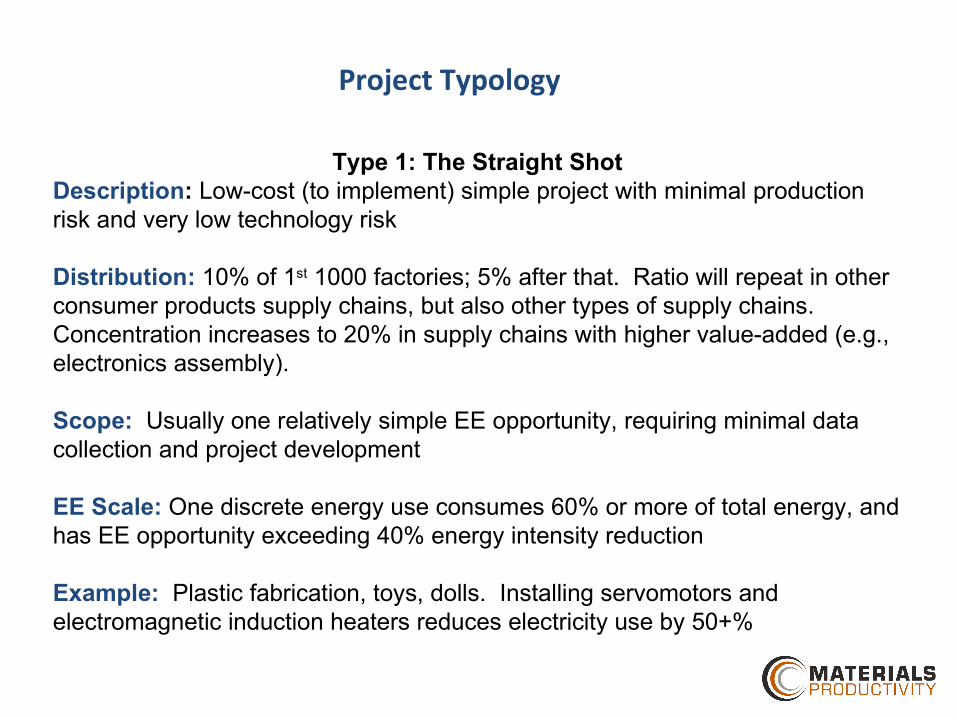

Project Typology

Type 1: The Straight ShotDescription: Low-cost (to implement) simple project with minimal production risk and very low technology risk

Distribution: 10% of 1st 1000 factories; 5% after that. Ratio will repeat in other consumer products supply chains, but also other types of supply chains. Concentration increases to 20% in supply chains with higher value-added (e.g., electronics assembly).

Scope: Usually one relatively simple EE opportunity, requiring minimal data collection and project development

EE Scale: One discrete energy use consumes 60% or more of total energy, and has EE opportunity exceeding 40% energy intensity reduction

Example: Plastic fabrication, toys, dolls. Installing servomotors and electromagnetic induction heaters reduces electricity use by 50+%

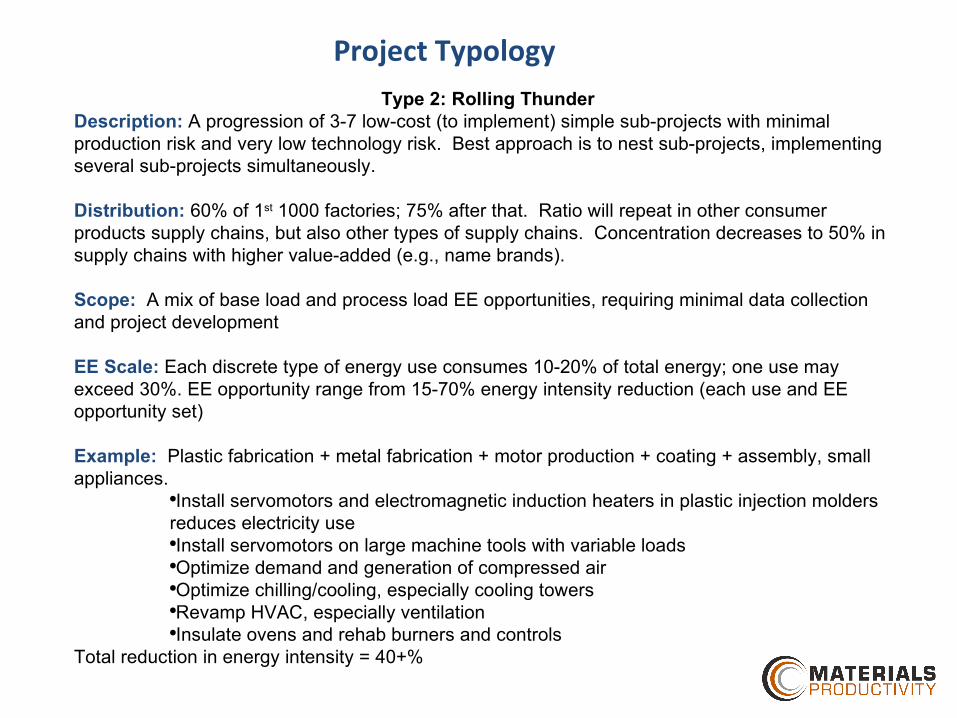

Project TypologyType 2: Rolling Thunder

Description: A progression of 3-7 low-cost (to implement) simple sub-projects with minimal production risk and very low technology risk. Best approach is to nest sub-projects, implementing several sub-projects simultaneously.

Distribution: 60% of 1st 1000 factories; 75% after that. Ratio will repeat in other consumer products supply chains, but also other types of supply chains. Concentration decreases to 50% in supply chains with higher value-added (e.g., name brands).

Scope: A mix of base load and process load EE opportunities, requiring minimal data collection and project development

EE Scale: Each discrete type of energy use consumes 10-20% of total energy; one use may exceed 30%. EE opportunity range from 15-70% energy intensity reduction (each use and EE opportunity set)

Example: Plastic fabrication + metal fabrication + motor production + coating + assembly, small appliances.

●Install servomotors and electromagnetic induction heaters in plastic injection molders reduces electricity use●Install servomotors on large machine tools with variable loads●Optimize demand and generation of compressed air●Optimize chilling/cooling, especially cooling towers●Revamp HVAC, especially ventilation●Insulate ovens and rehab burners and controls

Total reduction in energy intensity = 40+%

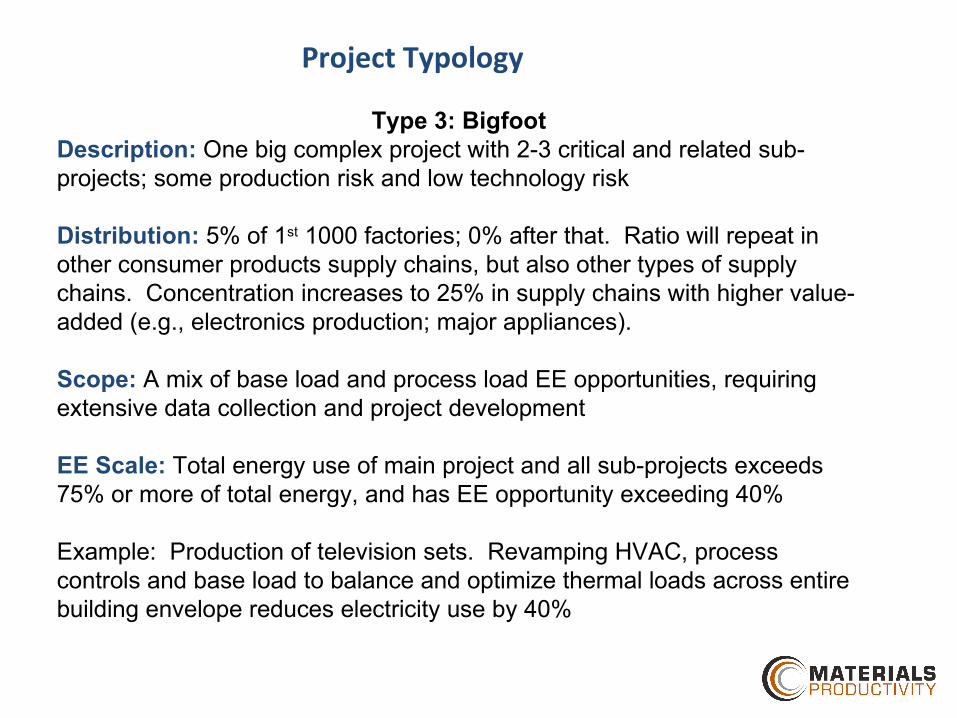

Project Typology

Type 3: BigfootDescription: One big complex project with 2-3 critical and related sub-projects; some production risk and low technology risk

Distribution: 5% of 1st 1000 factories; 0% after that. Ratio will repeat in other consumer products supply chains, but also other types of supply chains. Concentration increases to 25% in supply chains with higher value-added (e.g., electronics production; major appliances).

Scope: A mix of base load and process load EE opportunities, requiring extensive data collection and project development

EE Scale: Total energy use of main project and all sub-projects exceeds 75% or more of total energy, and has EE opportunity exceeding 40%

Example: Production of television sets. Revamping HVAC, process controls and base load to balance and optimize thermal loads across entire building envelope reduces electricity use by 40%

Project Typology

Type 4: Slow and SteadyDescription: A progression of 3-7 moderate-cost (to implement) sub-projects with minimal production risk and very low technology risk. Each project implementation complete before the next is opened. Requires a “portfolio” approach.

Distribution: 25% of 1st 1000 factories. Unknown ratio will repeat in other consumer products supply chains, as well as other types of supply chains.

Scope: A mix of base load and process load EE opportunities, requiring minimal data collection and project development

EE Scale: Each discrete type of energy use consumes 10-20% of total energy; one use may exceed 30%. EE opportunity range from 15-70% energy intensity reduction (each use and EE opportunity set)

Example: Plastic fabrication + metal fabrication + motor production + coating + assembly, lighting. ●Install servomotors and electromagnetic induction heaters in plastic injection molders reduces electricity use●Install servomotors on large machine tools with variable loads●Optimize demand and generation of compressed air●Optimize chilling/cooling, especially cooling towers●Revamp HVAC, especially ventilation●Insulate ovens and rehab burners and controls

Total reduction in energy intensity = 50%

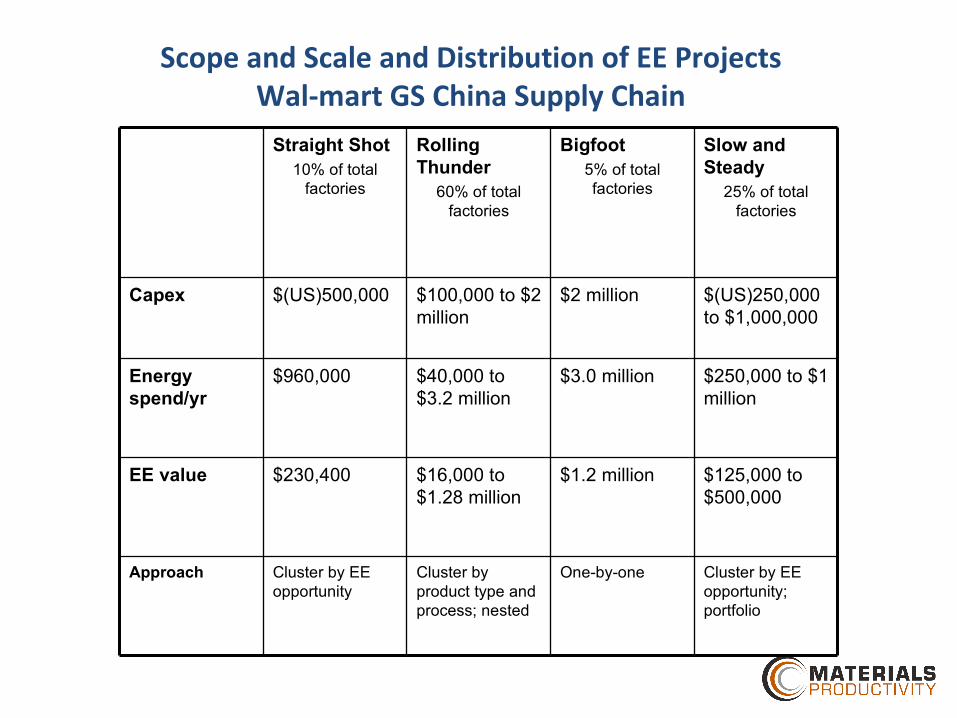

Straight Shot10% of total

factories

Rolling Thunder

60% of total factories

Bigfoot5% of total factories

Slow and Steady

25% of total factories

Capex $(US)500,000 $100,000 to $2 million

$2 million $(US)250,000 to $1,000,000

Energy spend/yr

$960,000 $40,000 to $3.2 million

$3.0 million $250,000 to $1 million

EE value $230,400 $16,000 to $1.28 million

$1.2 million $125,000 to $500,000

Approach Cluster by EE opportunity

Cluster by product type and process; nested

One-by-one Cluster by EE opportunity; portfolio

Scope and Scale and Distribution of EE ProjectsWal-mart GS China Supply Chain

Are you willing to…?

• Vouch for the credit quality of factories in your supply chain?

• Co-invest in EE projects?• Engage in collaborative projects to develop EE

alternatives by guaranteeing orders/prices?• Mandate metered data?• Work with the “muddled middle” after you scoop up

the “early adopters”?• Integrate EE (and overall environmental/social

progress) with sourcing and product design?

Things you need to know

• Audits do not really work very well• Many factories do not “own” their processes• You, as a “Big Customer”, may be the only

independent and neutral source of info for factories• After the first 20% of gains in reducing energy

intensity, EE pays off very slowly…unless the factory is horribly inefficient

• Finance (at the moment) seems to be a “Key to the [Implementation] Kingdom”

• Go to the Gemba; boots on the ground are critical