fnce 4040 derivatives chapter 4 - leeds-courses.colorado

TRANSCRIPT

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FNCE 4040– Derivatives

Chapter 4

Interest Rates

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Goals

• Discuss the types of rates needed for

Derivative Pricing

• Continuous Compounding

• Yield Curves

• Risk

• Forward Rate Agreements (FRA)

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Types of Rates

• For the purpose of this class there are three

types of interest rates that are relevant

– LIBOR

– Risk-free rates

– Interest Rates on collateral

• Important but out of scope rates include:

– Treasuries

– Overnight Interest Rate Swaps (OIS)

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

LIBOR

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

LIBOR

• London Interbank Offered Rate

– This is the rate of interest at which a bank is

prepared to borrow from another bank.

– It is compiled for a variety of maturities ranging

from Overnight to 1 year

– It exists on all 5 currencies – CHF, EUR, GBP,

JPY and USD

– It is compiled once a day ICE Benchmark

Administration (IBA)

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

LIBOR Process

• Once a day major banks submit the answer

to the following question

“At what rate could you borrow funds, were

you to do so by asking and then accepting

inter-bank offers in a reasonable market size

just prior to 11am London time?”

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Uses of LIBOR

• LIBOR rates are used for

– Interest Rate Futures • This is a futures contract whose price is derived by the interest

paid on 3-Month LIBOR

– Interest Rate Swaps • These are derivative instruments that “swap” LIBOR for fixed

interest rates generally for three or six month period. The maturity

of these tends to be 3 to 50 years

– Mortgages • Some Adjustable Rate Mortgages are linked to LIBOR rates

– Benchmark rate for short-term borrowing in the market.

– There has been a scandal surrounding LIBOR for the past

few years. If interested see the appendix.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

RISK FREE RATE

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

The Risk-Free Rate

• Derivatives pricing originally depended upon

a “risk-free” rate – The risk-free rate traditionally used by derivatives

practitioners was LIBOR

– Treasuries are an alternative but were

considered to be artificially low for a number of

reasons • Treasury bills and bonds must be purchased by financial

institutions to satisfy a variety of regulatory requirements.

Increases demand and decreases yield

• The amount of capital a bank has to have in order to support an

investment in treasury bills and bonds is lower

• Treasuries have a favorable tax treatment

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

The Risk-Free Rate

• In this course we will generally assume that

risk-free rates exist and they will be given to

you.

• We will assume that LIBOR is the risk-free

rate

• We will give you rates.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Collateral Based Discounting

• Derivatives pricing theory has moved to

Collateral Based Discounting – The yield curve relevant for discounting depends

on the collateral agreement

– Every derivatives contract might have a different

yield curve

• When we discuss pricing we will work through

at least one collateralized example

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

THE YIELD CURVE

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Yield Curve

• When pricing derivatives we will need a yield

curve.

• For our purposes a yield curve will consist of – Yields to specified maturities,

– A methodology for interpolating missing yields,

– A methodology for calculating forward rates

(rates that are for borrowing/lending starting in

the future)

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Theories of the Term Structure

• Liquidity Preference Theory: forward rates

higher than expected future zero rates

• Market Segmentation: short, medium and

long rates determined independently of each

other

• Expectations Theory: forward rates equal

expected future zero rates

– The Derivatives market uses this theory.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

CONTINUOUSLY

COMPOUNDED ZERO RATES

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Continuous Compounding

• The compounding frequency used for an

interest rate is the unit of measurement

• All else being equal, a more frequent

compounding frequency results in a higher

value of the investment at maturity

• In this class interest rates will be quoted as

continuously compounded zero rates

– Except when we are discussing a specific

instrument or market – for example LIBOR or

swap rates.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Continuous Compounding

• A zero rate (or spot rate), for maturity T is the rate of

interest earned on an investment that provides a

payoff only at time T

• Continuous compounding means that an investment

is instantaneously reinvested.

• In practical terms this means – $100 grows to $100 × 𝑒𝑅𝑐𝑇 when invested at a

continuously compounded rate 𝑅𝐶 to time 𝑇

– Conversely, $100 paid at time 𝑇 has a present value of

$100 × 𝑒−𝑅𝑐𝑇, when the continuously compounded

discount rate to time 𝑇 is 𝑅𝑐

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

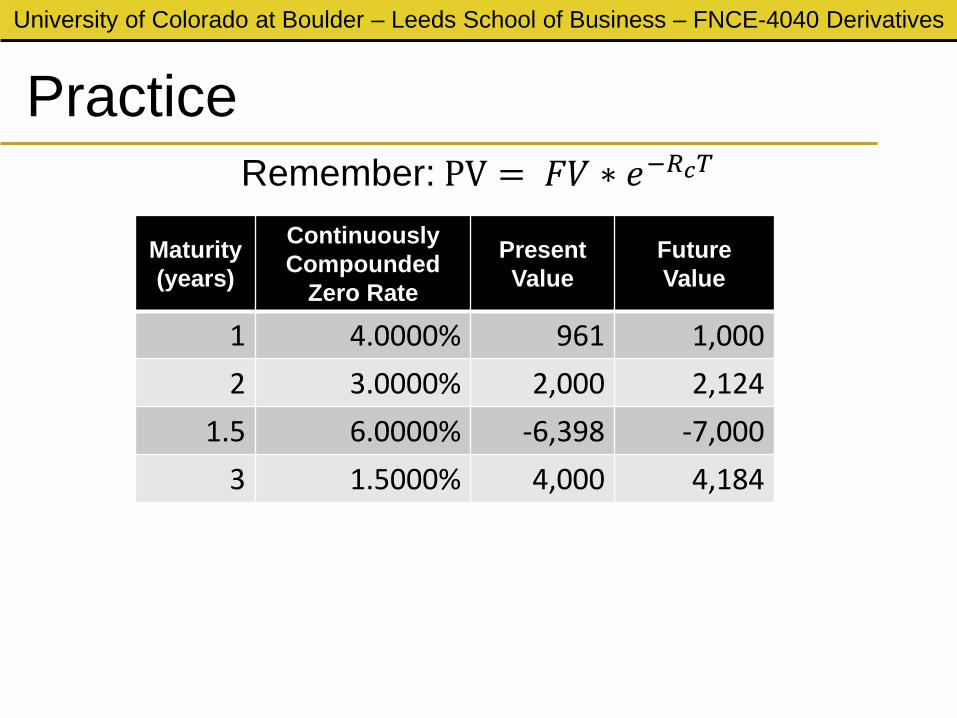

Practice

Maturity

(years)

Continuously

Compounded

Zero Rate

Present

Value

Future

Value

1 4.0000% 961 1,000

2 3.0000% 2,000 2,124

1.5 6.0000% -6,398 -7,000

3 1.5000% 4,000 4,184

Remember: PV = 𝐹𝑉 ∗ 𝑒−𝑅𝑐𝑇

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

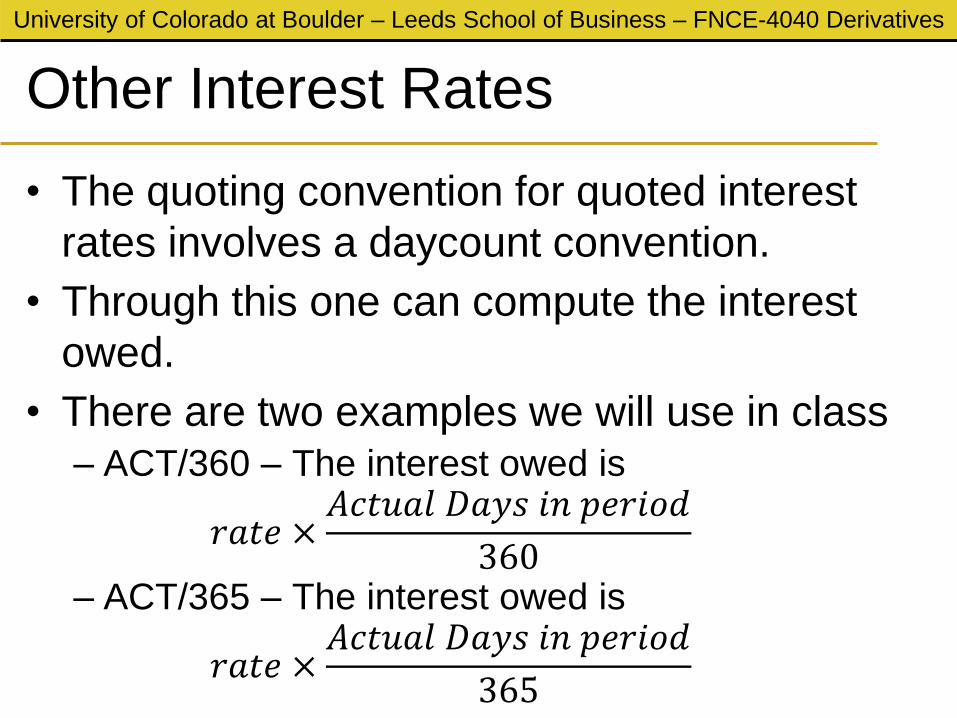

Other Interest Rates

• The quoting convention for quoted interest

rates involves a daycount convention.

• Through this one can compute the interest

owed.

• There are two examples we will use in class – ACT/360 – The interest owed is

𝑟𝑎𝑡𝑒 ×𝐴𝑐𝑡𝑢𝑎𝑙 𝐷𝑎𝑦𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑

360

– ACT/365 – The interest owed is

𝑟𝑎𝑡𝑒 ×𝐴𝑐𝑡𝑢𝑎𝑙 𝐷𝑎𝑦𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑

365

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

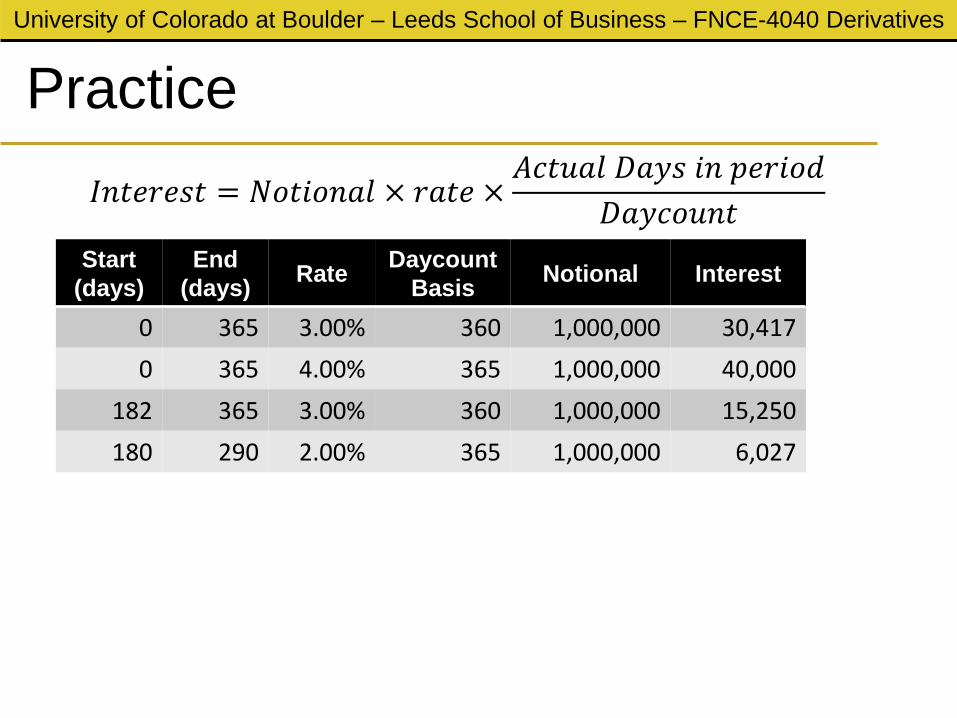

Start

(days)

End

(days) Rate

Daycount

Basis Notional Interest

0 365 3.00% 360 1,000,000 30,417

0 365 4.00% 365 1,000,000 40,000

182 365 3.00% 360 1,000,000 15,250

180 290 2.00% 365 1,000,000 6,027

Practice

𝐼𝑛𝑡𝑒𝑟𝑒𝑠𝑡 = 𝑁𝑜𝑡𝑖𝑜𝑛𝑎𝑙 × 𝑟𝑎𝑡𝑒 ×𝐴𝑐𝑡𝑢𝑎𝑙 𝐷𝑎𝑦𝑠 𝑖𝑛 𝑝𝑒𝑟𝑖𝑜𝑑

𝐷𝑎𝑦𝑐𝑜𝑢𝑛𝑡

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Conversion

• We will often have rates given in a particular

form and have to convert to another.

• We can do this by computing the investment

return from the given rate and using this to

compute the unknown rate, or equating PVs:

𝑒𝑟𝑐𝑐∗𝑑𝑎𝑦𝑠/365 = 1 + 𝑟𝐴𝐶𝑇/360𝑑𝑎𝑦𝑠

360

𝑃𝑉 = 𝑒−𝑟𝑐𝑐∗𝑑𝑎𝑦𝑠/365 =1

1 + 𝑟𝐴𝐶𝑇/360𝑑𝑎𝑦𝑠360

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Practice

Start End ACT/360

Rate

ACT/365

Rate

C. comp.

Rate

0 365 3.00% 3.0417% 2.9963%

0 365 4.00% 4.0556% 3.9755%

182 365 3.00% 3.0417% 3.0187%

1 + 𝑟𝐴𝐶𝑇/360𝑑𝑎𝑦𝑠

360= 1 + 𝑟𝐴𝐶𝑇/365

𝑑𝑎𝑦𝑠

365= 𝑒𝑟𝑐𝑐∗𝑑𝑎𝑦𝑠/365

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

INTERPOLATION BETWEEN

RATES

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Interpolation

• When interpolating between rates we will

linearly interpolate continuously compounded

zero rates.

• The advantages of doing this are:

– It is easy to explain and implement

– It has great risk properties

• Sophisticated spline techniques are common

in the market.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Linear Interpolation

• If we know continuously compounded zero

rates 𝑧1 and 𝑧2 for two times 𝑡1 and 𝑡2 then

for time 𝑡 between 𝑡1 and 𝑡2 we define

𝑟 𝑡 = 𝑟1 +𝑟2 − 𝑟1𝑡2 − 𝑡1

𝑡 − 𝑡1

𝑡1 𝑡2

𝑟1

𝑟2

𝑡

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Practice

Time 1

years

Rate 1

cc zero

Time 2

years

Rate 2

cc zero

Maturity

years Rate

1 4.0000% 2 5.0000% 1.5 4.500%

1.5 2.0000% 2 1.5000% 1.8 1.700%

2 1.0000% 3 2.0000% 2.2 1.200%

𝑟 𝑡 = 𝑟1 +𝑟2 − 𝑟1𝑡2 − 𝑡1

𝑡 − 𝑡1

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FORWARD RATES

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Forward Rates

• The forward rate is the future zero rate

implied by today’s term structure of

interest rates

𝑒𝑓𝑛×(𝑇2−𝑇1)

𝑒𝑅2×𝑇2

𝑒𝑅1×𝑇1

𝑒𝑅1×𝑇1𝑒𝑓𝑛×(𝑇2−𝑇1) = 𝑒𝑅2×𝑇2

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Formula for Forward Rates

• Suppose that the zero rates for time periods

T1 and T2 are R1 and R2 with both rates

continuously compounded

• The forward rate for the period between times

T1 and T2 is

12

1122

TT

TRTR

• This formula is only approximately true when

rates are not expressed with continuous

compounding

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Practice

Time 1

years

Rate 1

cc zero

Time 2

years

Rate 2

cc zero

Forward Rate

between 𝒕𝟏 and 𝒕𝟐

1 4.0000% 2 5.0000% 6.0000%

1.5 2.0000% 2 1.7500% 1.0000%

2 1.0000% 3 2.0000% 4.0000%

𝐹1,2 =𝑅2𝑇2 − 𝑅1𝑇1𝑇2 − 𝑇1

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

RISK

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Industry Calc. of Rate Sensitivity: dv01

• Traders in practice use dv01: dollar value of

1bp increase in rates

• Shock interest rates by +1bp and compute

dollar change dv01

• Also compute bucketed dv01 – Shock interest rates by 1bp at various tenor

buckets

– Compute dollar impact of each individual shock

– You obtain a term structure of dv01s

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Example

• Consider an investment which pays

$1,000,000 in 1-years time. The one-year

continuously compounded zero rate is 3.00%.

• The present value of this investment is:

𝑃𝑉 = $1,000,000 ∙ 𝑒−0.03 = $970,446.53

• If interest rates increase by one basis-point

then the new PV will be:

𝑃𝑉 = $1,000,000 ∙ 𝑒−0.0301 = $970,348.49

• Thus the dv01 is -97.04 dollars.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Practice

Amount C.C.

Zero rate Maturity Original PV Bumped PV dv01

1,000,000 3.000% 1 $ 970,445.53 $ 970,348.49 $(97.04)

1,000,000 4.000% 1 $ 960,789.44 $ 960,693.37 $(96.07)

1,000,000 3.000% 2 $ 941,764.53 $ 941,576.20 $(188.33)

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FORWARD RATE AGREEMENT

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Forward Rate Agreement (FRA)

• A Forward Rate Agreement (FRA) is an OTC

agreement such that a certain interest rate

will apply to either borrowing or lending a

principal over a specified future period of

time.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Example

• For example a bank agrees to lend 1m USD

for 1 year starting in 1 year at an interest rate

of 3%. The rate is quoted with an ACT/360

daycount basis.

Year 1 Year 2

today

1𝑚 𝑈𝑆𝐷

1𝑚 𝑈𝑆𝐷

$1𝑚365

3603.00% = 30,416.67

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FRA Mechanics / Valuation – part 1

• From the lender’s viewpoint

• A loan of 𝑁 from 𝑇1 to 𝑇2 at an agreed rate 𝑅𝐾

• Let 𝐷 be the daycount fraction from 𝑇1 to 𝑇2

– For an FRA 𝐷 =𝐷𝑎𝑦𝑠 𝑇2 −𝐷𝑎𝑦𝑠(𝑇1)

360

𝑇1 𝑇2 today

Interest owed:

𝑁 × 𝑅𝐾 × 𝐷

𝑁

𝑁

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

𝑃𝑉 = −𝑁 ∙ 𝑒−𝑟1𝑇1 +𝑁 ∙ 1 + 𝑅𝐾 ∙ 𝐷 ∙ 𝑒−𝑟2𝑇2

FRA Mechanics / Valuation – part 1

• We can value the FRA given the continuously

compounded zero rates 𝑟1 and 𝑟2.

𝑇1 𝑇2 today

Interest owed:

𝑁 ∙ 𝑅𝐾 ∙ 𝐷

𝑁

𝑁

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

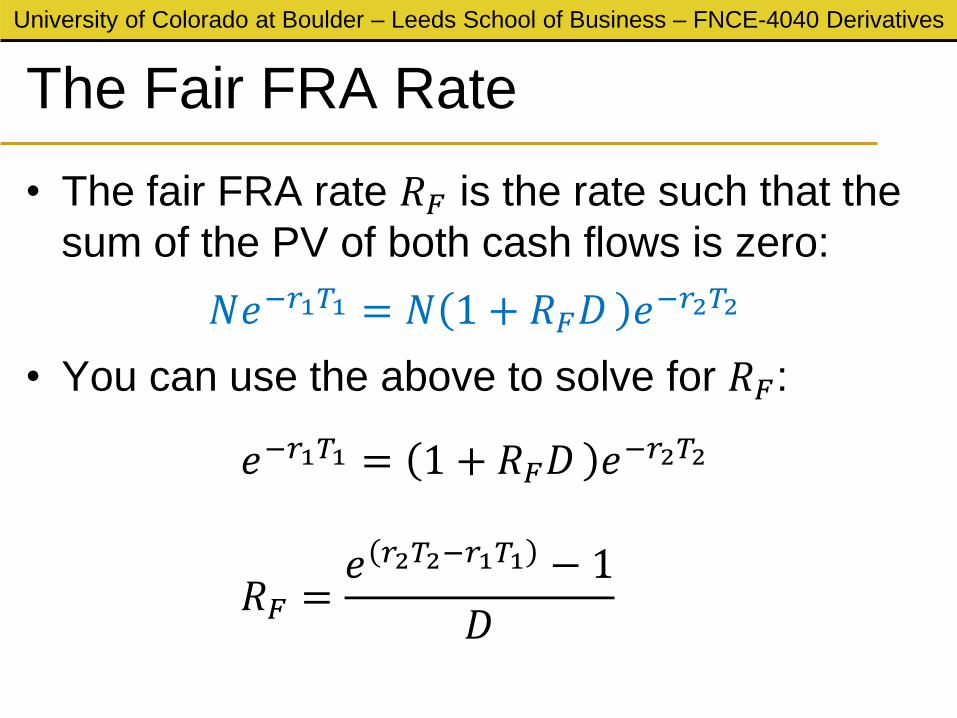

The Fair FRA Rate

• The fair FRA rate 𝑅𝐹 is the rate such that the

sum of the PV of both cash flows is zero:

𝑁𝑒−𝑟1𝑇1 = 𝑁 1 + 𝑅𝐹𝐷 𝑒−𝑟2𝑇2

• You can use the above to solve for 𝑅𝐹:

𝑒−𝑟1𝑇1 = 1 + 𝑅𝐹𝐷 𝑒−𝑟2𝑇2

𝑅𝐹 =𝑒 𝑟2𝑇2−𝑟1𝑇1 − 1

𝐷

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

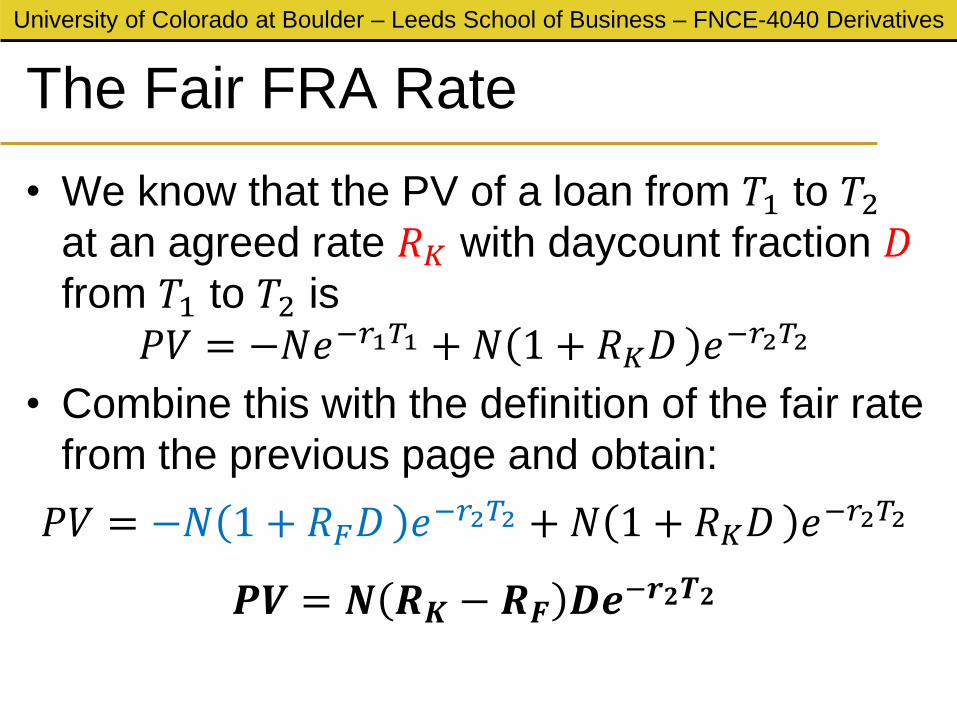

The Fair FRA Rate

• We know that the PV of a loan from 𝑇1 to 𝑇2

at an agreed rate 𝑅𝐾 with daycount fraction 𝐷

from 𝑇1 to 𝑇2 is

𝑃𝑉 = −𝑁𝑒−𝑟1𝑇1 +𝑁 1 + 𝑅𝐾𝐷 𝑒−𝑟2𝑇2

• Combine this with the definition of the fair rate

from the previous page and obtain:

𝑃𝑉 = −𝑁 1 + 𝑅𝐹𝐷 𝑒−𝑟2𝑇2 +𝑁 1 + 𝑅𝐾𝐷 𝑒

−𝑟2𝑇2

𝑷𝑽 = 𝑵 𝑹𝑲 − 𝑹𝑭 𝑫𝒆−𝒓𝟐𝑻𝟐

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Forward Rate Agreement (cont.)

• Equivalent to an agreement where interest at

a predetermined rate, RK is exchanged for

interest at the market rate

• Value an FRA by assuming that the forward

rate RF, is certain (has been discovered)

• So the value of an FRA is the PV of the

difference between:

– the interest that would be paid at rate RF and

– the interest that has to be paid at rate RK

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FRA Mechanics / Valuation – part 2 • A loan from 𝑇1 to 𝑇2

• From the lender’s viewpoint

𝑇1 𝑇2

Fair rate now for

period 𝑇1, 𝑇2 = 𝑅𝐾

today

Interest owed:

𝑁 × 𝑅𝐾 × 𝑇2 − 𝑇1

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Think of Mark-To-Market as the cost to offsetting

your position

FRA Mechanics / Valuation – part 2

Interest owed:

𝑁 × 𝑅𝐾 × 𝑇2 − 𝑇1

𝑒−𝑅2×𝑇2

𝑇1 𝑇2 today

Fair rate for period

𝑇1, 𝑇2 moves to 𝑹𝑭

Interest now prevailing:

𝑁 × 𝑹𝑭 × 𝑇2 − 𝑇1 Take the difference

and PV

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FRA example 1

• For example a bank agrees to lend 1m USD

for 1 year starting in 1 year at an interest rate

of 3%. The rate is quoted with an ACT/360

daycount basis.

• Assume that the interest rates are as follows:

Maturity

Continuously Compounded

Zero Rate

1 2.50%

2 2.60%

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

cc zero PV

2.50% -975,310

2.60% 978,205

FRA example 1 – Cashflows

Year 1 Year 2

today

1𝑚 𝑈𝑆𝐷

1𝑚 𝑈𝑆𝐷

$1𝑚365

3603.00% = 30,416.67

Maturity Cashflow

1 -1,000,000

2 1,030,417

𝑃𝑉 = 978,205 − 975,310 = 2,895

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FRA example 2

• For example a bank agrees to lend 1m USD

for 1 year starting in 1 year at the fair FRA

rate. The rate is quoted with an ACT/360

daycount basis. At what rate do they lend?

• Assume that the interest rates are as follows:

Maturity Continuously Compounded

Zero Rate

1 2.50%

2 2.60%

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

FRA - example 2

• The cont. comp. forward rate is

𝑓 =2.60% ∙ 2 − 2.50% ∙ 1

2 − 1= 2.70%

• We need to convert this to an ACT/360 rate

𝑒2.70%∙365 365 = 1 + 𝑟365

360

𝒓 = 𝟐. 𝟔𝟗𝟗𝟑%

Maturity Continuously Compounded

Zero Rate

1 2.50%

2 2.60%

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

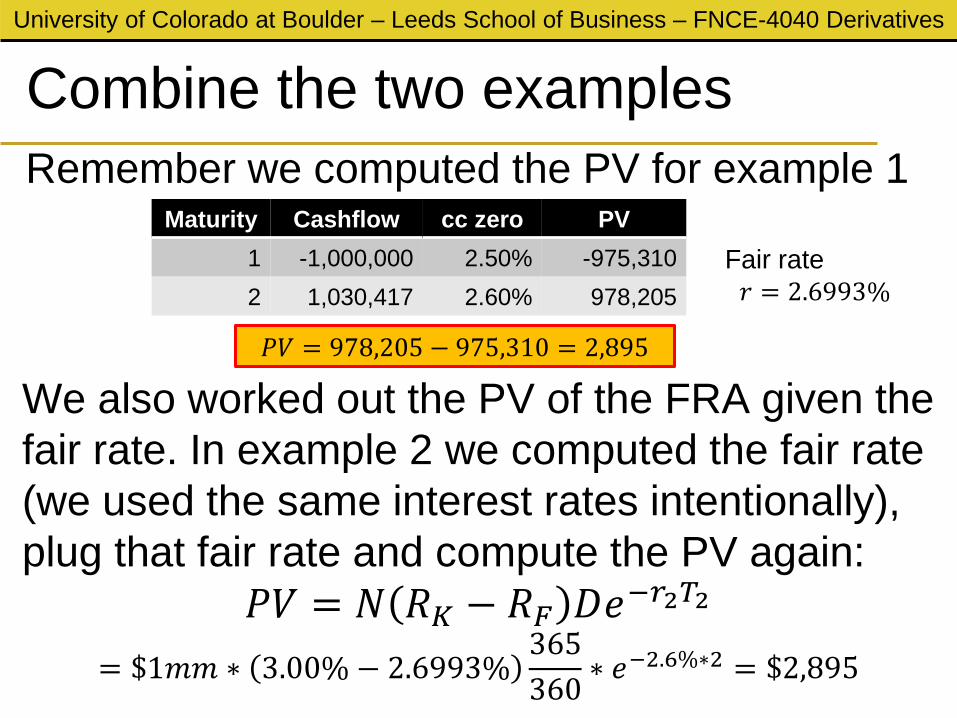

cc zero PV

2.50% -975,310

2.60% 978,205

Combine the two examples

Maturity Cashflow

1 -1,000,000

2 1,030,417

𝑃𝑉 = 978,205 − 975,310 = 2,895

Remember we computed the PV for example 1

We also worked out the PV of the FRA given the

fair rate. In example 2 we computed the fair rate

(we used the same interest rates intentionally),

plug that fair rate and compute the PV again:

𝑃𝑉 = 𝑁 𝑅𝐾 − 𝑅𝐹 𝐷𝑒−𝑟2𝑇2

= $1𝑚𝑚 ∗ 3.00% − 2.6993%365

360∗ 𝑒−2.6%∗2 = $2,895

Fair rate

𝑟 = 2.6993%

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

“Floating” FRA

• An FRA where one party agrees to pay the

other party whatever market interest rate will

prevail on a date 𝑇1 for the period 𝑇1, 𝑇2

• In other words: “I will pay you the fair interest

for the period 𝑇1, 𝑇2 that will be determined

at (some time 𝑇𝐾 between now and) time 𝑇1”

• What is the PV of this promise?

• Sounds like “I promise to give you what will

be fair at some point in the future”

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

RISK ON AN FRA

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

DV01

• Remember that the industry standard for

interest rate risk is the dv01 aka dollar value

of one basis point.

• Looking at the valuation formula

𝑃𝑉 = −𝑁𝑒−𝑟1𝑇1 +𝑁 1 + 𝑅𝐹𝐷 𝑒−𝑟2𝑇2

We can see that there are two interest rates

used in pricing an FRA: 𝑟1 and 𝑟2

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Heuristics

• Assume that 𝑅𝐹 is fixed – the contract has

already been entered.

• If we increase 𝑟1 by a basis point and leave 𝑟2

constant then the lender of money makes

money

• If we increase 𝑟2 by a basis point and leave 𝑟1

constant then the lender of money loses

money

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

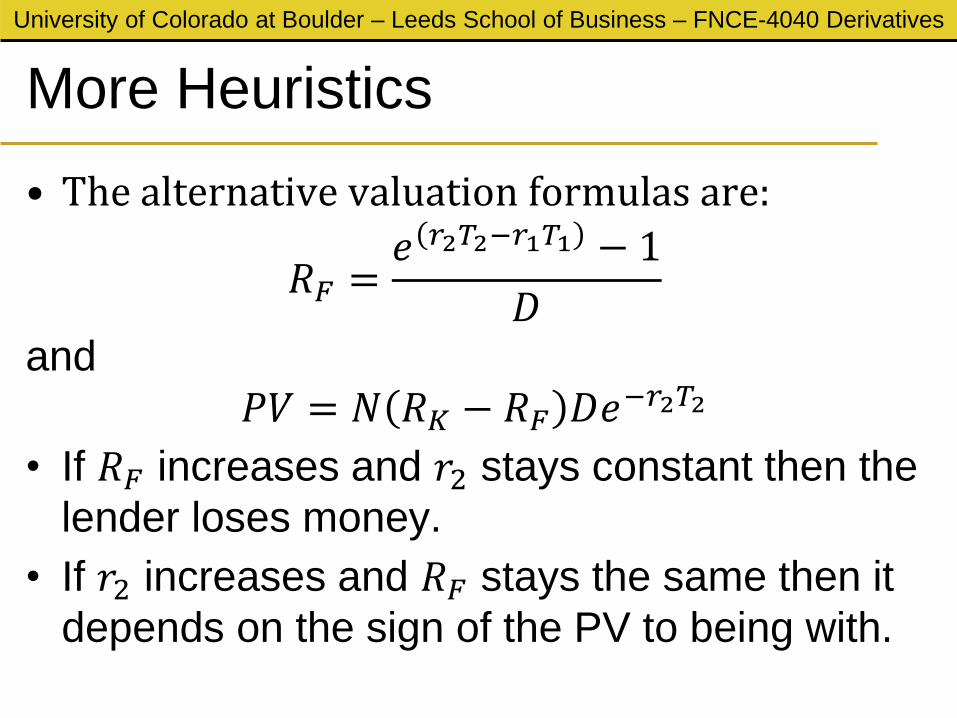

More Heuristics

• The alternative valuation formulas are:

𝑅𝐹 =𝑒 𝑟2𝑇2−𝑟1𝑇1 − 1

𝐷

and

𝑃𝑉 = 𝑁 𝑅𝐾 − 𝑅𝐹 𝐷𝑒−𝑟2𝑇2

• If 𝑅𝐹 increases and 𝑟2 stays constant then the

lender loses money.

• If 𝑟2 increases and 𝑅𝐹 stays the same then it

depends on the sign of the PV to being with.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

APPENDIX

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

DERIVING CONTINUOUSLY

COMPOUNDED RATES

Appendix

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Measuring Interest Rates

• The compounding frequency used for an

interest rate is the unit of measurement

• The difference between annual and quarterly

compounding comes that in the latter you

earn interest on interest throughout the year

• All else being equal, a more frequent

compounding frequency results in a higher

value of the investment at maturity

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Impact of Compounding

• When we compound 𝑚 times per year at rate

𝑅, A grows to A(1 + 𝑅/𝑚)𝑚 in one year

Compound. Freq. Value of $100 in 1year at 10%

Annual (m=1) 110.00

Semi-annual (m=2) 110.25

Quarterly (m=4) 110.38

Monthly (m=12) 110.47

Weekly (m=52) 110.51

Daily (m=365) 110.52

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Continuous Compounding

• Frequency of compounding matters

• At the limit of (compounding time)→0

the interest earned grows

exponentially

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

S

xTNxNT /* Let r=rate and

x=compounding time →

Nxrxrxr *1*1*1 Value End

timesN gcompoundin

NxrNexr *1ln

0x0x lim*1lim

How to derive Rc

Substitute

N=T/x

x

xrT

e

*1ln

0xlim

xdx

d

xrTdx

d

e

*1ln

0xlim

rT

rxr

T

ee

1

*1

1

0xlim

Looks like 0/0.

Use de l’Hôpital

Q.E.D.

Make x very

small. Then

use A=eln(A)

Checks: r=0 →End Value=1

T=0 →End Value=1

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Continuous Compounding

• So in the limit as we compound more and

more frequently, we obtain continuously

compounded interest rates

• $100 grows to $100 × 𝑒𝑅𝑐𝑇 when invested at

a continuously compounded rate R for time T

• Conversely, $100 paid at time T has a

PV=$100 × 𝑒−𝑅𝑐𝑇, when the continuously

compounded discount rate is 𝑅𝑐

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

US TREASURY MARKET

Appendix

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Treasury Rates

• Rates on instruments issued by a

government in its own currency

• The rate is different by country and reflects a

combination of credit and economic

considerations

• We will focus only on the US treasury market

Many interesting links, for example: Treasury

http://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/Historic-Yield-Data-Visualization.aspx

Bloomberg

http://www.bloomberg.com/markets/rates-bonds/government-bonds/us/

Stockcharts

http://stockcharts.com/freecharts/yieldcurve.html

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

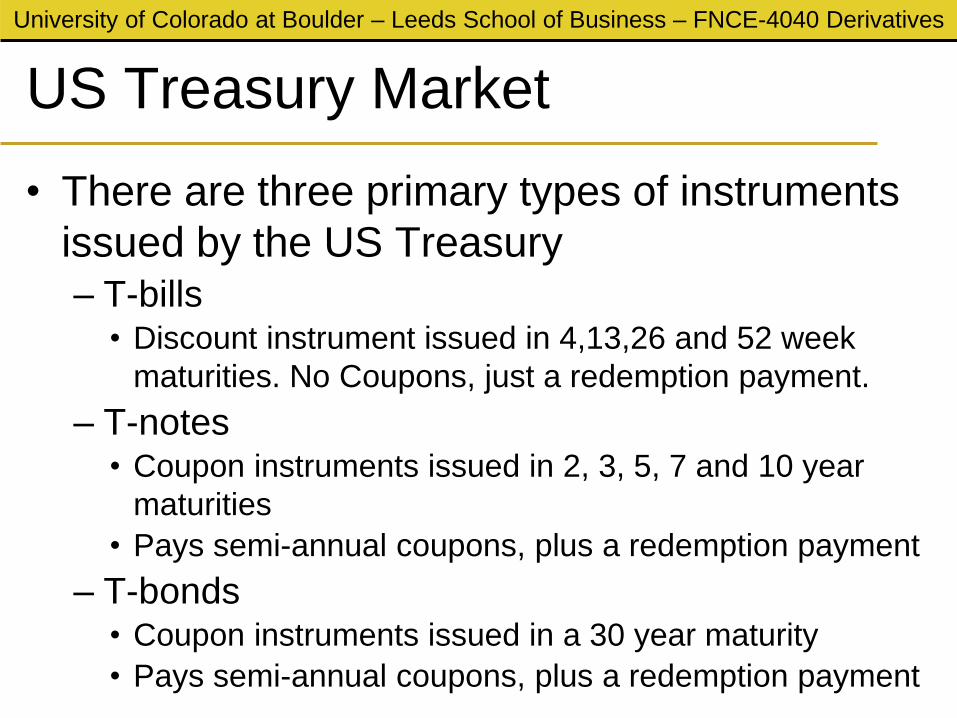

US Treasury Market

• There are three primary types of instruments

issued by the US Treasury – T-bills

• Discount instrument issued in 4,13,26 and 52 week

maturities. No Coupons, just a redemption payment.

– T-notes • Coupon instruments issued in 2, 3, 5, 7 and 10 year

maturities

• Pays semi-annual coupons, plus a redemption payment

– T-bonds • Coupon instruments issued in a 30 year maturity

• Pays semi-annual coupons, plus a redemption payment

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

US Public Debt

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

US Public Debt

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

US Public Debt

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

US Public Debt

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

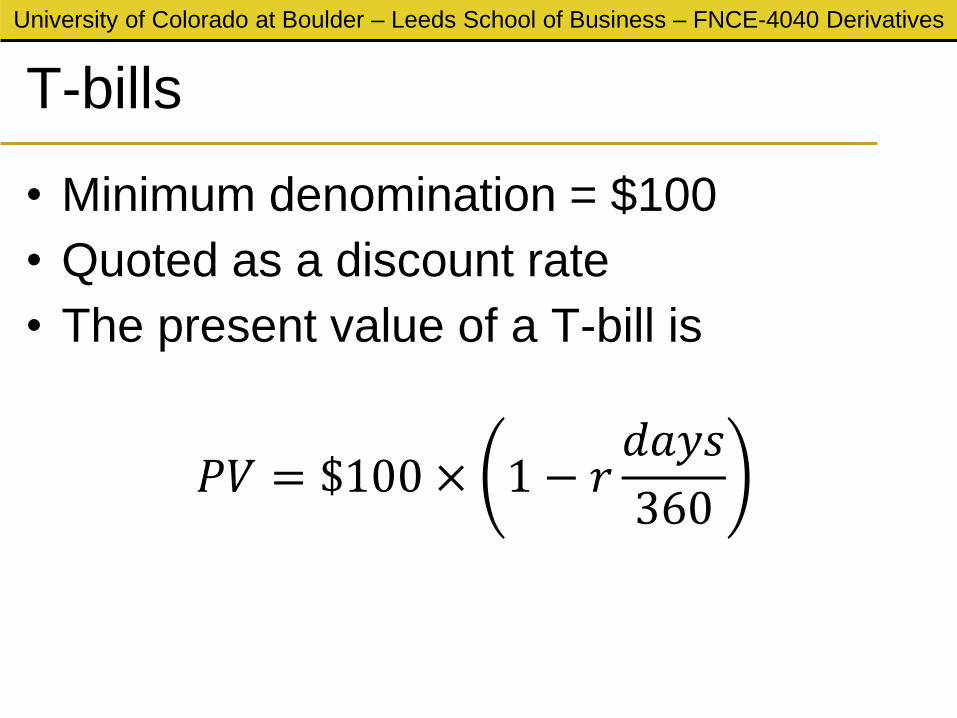

T-bills

• Minimum denomination = $100

• Quoted as a discount rate

• The present value of a T-bill is

𝑃𝑉 = $100 × 1 − 𝑟𝑑𝑎𝑦𝑠

360

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

T-notes and T-bonds

• The difference between notes and

bonds is simply the maturity

– Minimum denomination = $100.

– Pays interest every 6 months.

If the coupon rate is 𝑟 then the interest paid

is 𝑟 2 every 6 months.

– At maturity the notional of the note is paid

to the holder

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Treasury Strips

• Separate Trading of Registered Interest and

Principal of Securities

• STRIPS let investors hold and trade the

individual interest and principal components

of T-notes and T-bonds

• Popular because they let an investor receive

a known payment on a specific future date

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

Treasury Strips

• We will use STRIPs as our instrument of

choice when building a Treasury yield curve – It is quoted as a price. This simplifies the

mathematics

– Frequent maturities.

• These are not as liquid as the underlying

treasury so in practice would not choose to

use these.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

LIBOR SCANDAL

Appendix

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

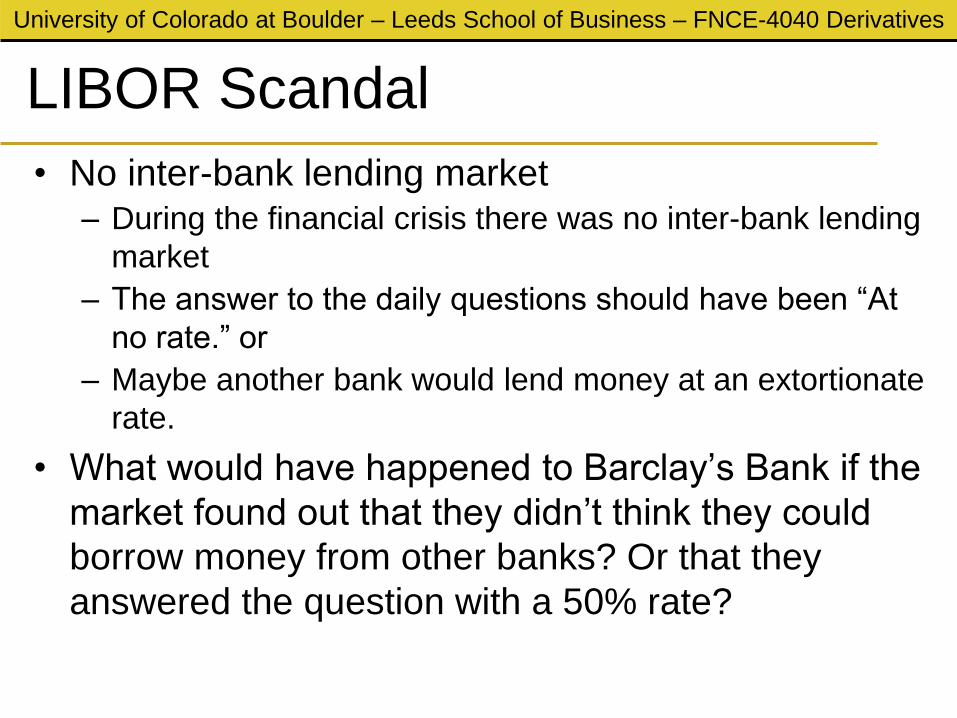

LIBOR Scandal

• No inter-bank lending market – During the financial crisis there was no inter-bank lending

market

– The answer to the daily questions should have been “At

no rate.” or

– Maybe another bank would lend money at an extortionate

rate.

• What would have happened to Barclay’s Bank if the

market found out that they didn’t think they could

borrow money from other banks? Or that they

answered the question with a 50% rate?

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

LIBOR Scandal

• Manipulation of fixings

– Imagine a 10m USD bet on 3-month USD

LIBOR. If LIBOR>=3.00% then receive 10m

USD. If LIBOR<3.00% then receive nothing.

– What happens if on the morning of the bet

LIBOR is trading at 2.98%? What can a trader

do to win the bet? • Pressure the person making the submission in his

bank to give a higher submission

• Speak to traders at other banks so that they will do

the same.

University of Colorado at Boulder – Leeds School of Business – FNCE-4040 Derivatives

LIBOR Scandal

• June 2012

– Barclay’s Bank paid fines of GBP290m for manipulation of the

rates

– Chairman and CEO resigns

• Dec 2012

– UBS is fined a total of USD1.5bn

• Feb 2013

– Royal Bank of Scotland expecting penalties of USD 612m

• Dec 2013

– 6 financial institutions in Europe fined by European Commission

70-260m EUR.

– UBS avoided fines of 2.5bn EUR by revealing the existence of

cartels.